Credit Card Surcharge Rules & Fee Reductions. September 17, 2014 Matt Fluegge Vantiv

|

|

|

- Cory Norris

- 10 years ago

- Views:

Transcription

1 Credit Card Surcharge Rules & Fee Reductions September 17, 2014 Matt Fluegge Vantiv

2 B2B Trends Surcharging Rules Reducing Fees Impact New Interchange Rates 10/18/14

3 EFT s: Electronic Funds Transfer types EDI (Electronic Data Interchange) WIRE Transfers ACH (Automated Clearing House) Credit Cards Debit Cards

Credit")

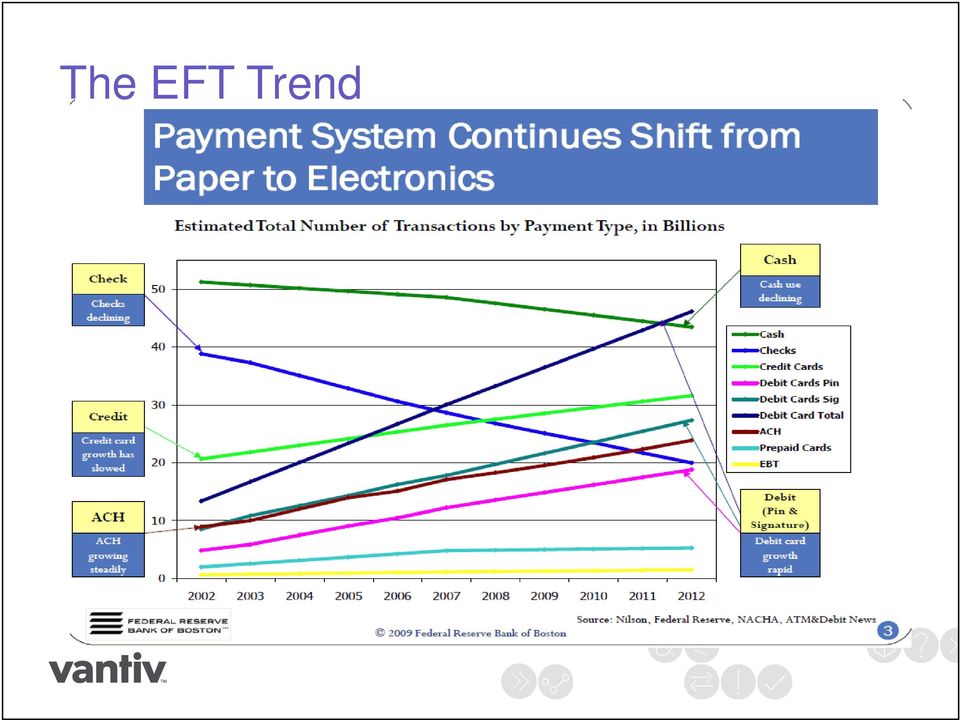

4 The EFT Trend

5 US Market Today* 511 million credit cards 31% of the global total 572 million debit cards 32% of the global total 16 million payment terminals 11 million integrated 5 million stand alone Wedge readers unaccounted for Utilized by many industries * Data is only based on information provided by Vantiv s partners and does not include all international payment systems. 5

6 US Market Today* 16 Independent PIN Debit Networks 37% of total US debit volume Routed 19 Billion of US PIN transactions in 2012 Federal regulations ensure merchant least cost routing option for PIN debit transactions 9 Acquirers Represent 70% of Processing Volume Independent Sales Organizations (ISOs) Primary business interface of small merchants 500+ Independent Software Vendors (ISVs) Primary processing interface to mid-tier merchants *Data is only based on information provided by Vantiv s partners and does not include all international payment systems. 6

7 Card Growth* Credit, debit, and prepaid general purpose consumer and commercial payment cards issued in the United States generated $4.530 trillion in purchases of goods and services in 2013, and increase of 7.8% from Source: The Nielson Report *Source: By What's Next In Payments, 8:00 AM EDT May 29th,

8 B2B Growth Statistics In 2008, $665 billion worth of goods and services were purchased using commercial card products Getting Down to Business: Commercial Cards in B2B Payments, 2011 From 2003 to 2008, spending on corporate cards grew 192%* In 2012, 37% of small businesses used credit cards to meet capital needs National Small Business Association Small Business Access to Capital Survey, 2012 *Source: Blakeley and Blakeley 8

9 Commercial Card Growth Business/Commercial Card usage is increasing at a rate of 14% year over year Federal Reserve Payments Study Packaged Facts forecasts global Commercial Card purchase volume to grow by 13% in 2014 and in 2015, rising from $1.4 trillion to $1.79 trillion. David Morris, Packaged Facts, 04/02/2014* Annual Purchasing Card spending is expected to increase to $290 billion by 2016 with an expected 8% to 10% compound annual growth rate (CAGR). RPMG Research Corporation* The number of companies using virtual purchasing cards in 2014 is expected to increase 21 percent, as compared to 2012.* *Source: By pymnts@pymnts, What's Next In Payments, 8:00 AM EDT May 29th,

10 B2B Payments B2B Payments Check ACH Card Wire & Other 5% 7% 28% 60% Approximate payment types within the B2B Industries 10

11 Emerging B2B category performance Year-over-year credit card growth in emerging verticals and categories up 34% through June Source: MC clearing data for commercial credit products. YTD June 2014 over YTD June 2013.

12 Substantial Growth Vantiv Card Networks Merchants 12

13 SURCHARGING: NETWORK RULES

14 What is a Surcharge? A surcharge is an additional fee that a merchant adds on to a transaction when a customer uses a credit card for payment. 14

15 Changes to No Surcharging Operating Rules Effective January 27, 2013, U.S. merchants will have the option of adding a surcharge to Visa and MasterCard credit card transactions. Merchants who surcharge credit card transactions will be subject to the following requirements: 15

16 New Surcharging Operating Rules continued Visa and MasterCard will permit surcharging of credit card transactions only. The settlement does NOT change current restrictions on the surcharging of debit transactions (signature or PIN). Merchants will be able to surcharge credit card transactions at the brand level or product level. Brand Level = Merchant charges same % on all Visa and/or MC credit cards Product Level = Merchant charges a % on particular types, such as Rewards Cards, Signature, World Cards, etc. 16

17 New Surcharging Operating Rules continued Merchants are only allowed to assess a surcharge that does not exceed their effective rate for the applicable credit card surcharged. Merchants can surcharge up to their cost, capped at 4%. 17

18 New Surcharging Operating Rules continued Calculating the effective rate/surcharge amount: The average effective Interchange Reimbursement Fee rate plus the average of all fees imposed by Visa on the Acquirer or Merchant, expressed as a percentage of the Transaction amount, applicable to Visa Credit Card Transactions at the Merchant for the preceding one or twelve months, at the option of the Merchant Merchants that elect to surcharge must provide advance written notice to Visa, MasterCard, Discover, and the merchant acquirer 30 days prior to surcharging. 18

19 New Surcharging Operating Rules continued Merchants will be required to disclose their surcharge policy at the point of store entry... We impose a surcharge on credit cards that is not greater than our cost of acceptance and the point of sale prior to the purchase transaction being completed. We impose a surcharge of % on the transaction amount on Visa and MC payments. We do not surcharge Visa & MC debit cards. 19

20 New Surcharging Operating Rules continued The Transaction Receipt must show the Surcharge amount separately on the front of the receipt in the same type font and size as the other items, after the subtotal (allowing for any discounts) and before the final Transaction amount. The Surcharge amount must not be identified as a Visa-imposed surcharge. If a refund/credit is issued, merchant must refund the surcharge as well. 20

21 New Surcharging Operating Rules continued Can merchants pick and choose how they will surcharge based on: Size of transaction No The customer/cardholder No Maybe Products being sold... MasterCard says: A merchant with multiple business units/divisions may opt to impose a surcharge on credit transactions at all, some, or none of its business units/divisions. 21

22 Violating the Operating Rules Currently, all complaints are coming from the cardholder, but Visa has secret shoppers out there. Cardholder may initiate a MC chargeback / Visa compliance case to recover an invalid surcharge. MC = standard chargeback fees Visa = fee of $2 up to $600 If the merchant fails to become compliant after notification: MC = up to $25,000/month Visa = up to $5,000/month Both can increase the fines until merchant is compliant 22

23 New Surcharging Operating Rules continued Several states laws currently prohibit or restrict surcharging. Please consult your legal counsel for review of state laws and how they may impact your ability to surcharge. Currently, there are 11 states: California, Colorado, Connecticut Florida, Kansas, Maine, Massachusetts New York, Oklahoma, Texas, and Utah 23

24 24

25 Convenience Fees vs. Surcharges The Convenience Fee Rules listed below are based on Visa s rules, as they are the strictest. Other rules apply if accepting only MC/ and AMEX CONVENIENCE FEES Allowed only on CNP transactions Through an alternative channel from merchant s normal payment channel Fee is a flat or fixed amount Applicable to all forms of payment Disclosed prior to the completion of the transaction and the cardholder is given the opportunity to cancel. Included as part of the total sale. Allowed on credit and signature debit. Special programs for government and higher education SURCHARGES Allowed on CNP and CP transactions. Fee is a percentage of the sale Applies only to credit cards, not debit Competing brands should be surcharged, if contract allows. Disclosure surcharge policy Merchant must provide prior notice before implementation. Be mindful of state laws. *Surcharges & convenience fees cannot be applied on the same payment. 25

26 Whether you choose to impose a surcharge or not, merchants are looking to reduce the cost of card acceptance. How can this be done?

27 Payment System Roles & Responsibilities Three key entities manage the payment system: Issuers: Issue cards Assume buyer s credit risk Generate reports Provide customer service Networks: Provide systems/operations Develop products Provide risk management Offer advertising and promotions Set standards and rules Acquirers: Sign up merchants Underwrite merchant risk Provide processing Handle authorization Manage Capture/Settlement Generate reports Provider customer service 27

28 Fee Breakdown Interchange Network Assessments & Other Fees Processing Fee 28

29 Interchange Management What is the Interchange Fee? The largest cost component of a merchant transaction Collected by Acquirer from the merchant for every Visa, MasterCard, and Discover transaction. Passed through Visa, MasterCard, and Discover to the card Issuer. NOTE: Does not include other network pass-through fees such as those for Dues & Assessments, Network Access & Brand Usage, Acquirer Processing, Network Settlement / Base II, Risk, etc. 29

30 Fee Breakdown $500 Visa B2B Transaction $ $1.25 $ $ $0.001 $0.04 Interchange (2.10% + $0.10) Visa Base II Fee Tran Fee Comm/Gateway Fee Visa Acq. Proc. Fee Visa Assessment Total Cost = $12.46 $10.60 Visa Risk Fee Interchange represents 85% of the cost of this transaction. *Based on Average Ticket currently qualifying for the Visa Commercial B2B (Business, Corp) rate effective April 2012

31 Interchange Management Fees are influenced by 3 key considerations Market Segment Processing Technology Products B2B Travel & Entertainment Fuel Grocery Other Retail Recurring Payments ecommerce Restaurants Emerging Market Card Terminal POS Software Systems Virtual Terminal Automated Fuel Dispenser (AFD ) Key Entry Emerging Technology Consumer Cards Credit Debit Rewards World Signature Commercial Cards Purchasing Business Corporate Fleet 31

32 Visa Business Card Not Present Transaction With AVS (Address Verification) 2.10% + $0.10 Without AVS and Level II data 2.95% + $ % Downgrade 32

33 Interchange Management Incentive Interchange Programs Commercial Cards Level II / III Commercial Cards Large Ticket Savings Opportunity: Decreased expense Increased profit 33

34 Commercial Card Data Levels Level 1: Card number, expiration date, location information, Tax ID, AVS Level 2: Customer Code Sales Tax Indicator Sales Tax Amount Tax exempt transactions cannot qualify for Level 2, but they can qualify for Level 3 Level 3: Line Item Detail invoice data such as quantity, description, dollar amount The greater amount of data provided, the lower the interchange rate. 34

35 Interchange Rate Examples Visa Purchasing Card: Purchasing Standard (no AVS): 2.95% + $0.10 Purchasing Electronic (minimal data): 2.75% + $0.10 Purchasing B2B Rate (tax exempt): 2.40% + $0.10 Purchasing Level II Rate (taxable): 2.05% + $0.10 Purchasing Level III Rate: 1.95% + $0.10 Purchasing Large Ticket Rate: 1.45% + $35.00 MasterCard Business Card: Business Standard (missing data): 2.95% + $0.10 Business Data Rate I (Level I): 2.65% + $0.10 Business Data Rate II (Level II, taxable): 2.00% + $0.10 Business Data Rate III (Level III): 1.75% + $0.10 Business Large Ticket Rate: 1.20% + $

36 Sample Transaction Costs: Interchange Expense Visa Purchasing Card: $500 transaction Purchasing Electronic (minimal data): $13.85 Purchasing B2B (tax exempt, w/out Level 3): $12.10 Purchasing Level II Rate (taxable): $10.10 Purchasing Level III Rate: $ % reduction in cost by processing Level III data versus minimal data. MasterCard Business Card: $500 transaction Business Data Rate I (Level I): $13.35 Business Data Rate II (Level II, taxable): $10.10 Business Data Rate III (Level III): $ % reduction in cost by processing Level III data versus Level I 36

37 Large Ticket Interchange Expense Visa Purchasing Card: $50,000 transaction Purchasing Electronic (minimal data): $1, Purchasing B2B Rate (tax exempt): $1, Purchasing Level II Rate: $1, Purchasing Large Ticket Rate: $ % reduction in cost by processing Level III data versus minimal data. MasterCard Business Card: $50,000 transaction Business Data Rate I (Level I): $1, Business Data Rate II (Level II): $1, Business Large Ticket: $ % reduction in cost by processing Level III versus Level I data 37

38 Large Ticket Example MasterCard Business L4 Card: $39, transaction Data Rate I (tax-exempt) 2.96% + $0.10 $1, Data Rate II (taxable) 2.31% + $0.10 $ Large Ticket (level III) 1.51% + $40.00 $ % reduction in cost by processing Level III versus Level I data $ Savings 38

39 B2B COMPANY PROCESSING FEE SUMMARY Current NACM Program Savings Account 1 - Sept. $87, $61, $25, Account 1 - Oct. $63, $45, $18, Account 2 - Sept. $3, $2, $ Account 2 - Oct. $2, $2, $ Account 3 - Sept. $3, $1, $2, Account 3 - Oct. $6, $2, $4, TOTALS $167, $116, $51, * EFFECTIVE RATE 3.14% 2.17% $5,347, Effective rate = fees divided by Visa/MC/Discover Sales Visa/MC/Disc Sales AVG. MONTHLY SAVINGS $25, % TOTAL ANNUAL SAVINGS $310, SAVE 39

40 Level 3 Impact Without Level 3 Data on tax exempt payments, merchants are paying 0.15% to 0.90% more than they could be on every applicable commercial card transaction. 40

41 Changes to Commercial Card Interchange Interchange Fee Program Every card type/category is increasing by 0.00% to 0.45%, Except Level III qualified cards Visa Corporate Current Visa Purchasing Effective October 18, 2014 Visa Corporate and Visa Purchasing Commercial Electronic 2.75% + $ % + $ % + $0.10 Commercial Non-Travel Level III 1.95% + $ % + $ % + $0.10 Commercial Travel Service 2.55% +$ % + $ % + $0.10 Commercial Business-to Business 2.10% + $ % + $ % + $0.10 Commercial Retail 2.10% + $ % + $ % + $0.10 Commercial Card-Not Present 2.20% + $ % + $ % + $0.10 Commercial Electronic with Data 2.75% + $ % + $ % + $

42 FREE SAVINGS ANALYSIS & QUESTIONS Interested in a FREE interchange qualification analysis for attending today s presentation? or fax a copy of your company s recent monthly merchant services statement(s) to: Matt Fluegge [email protected] (fax) (phone) THANK YOU!! 42

Updates on Credit Card Surcharging and Acceptance. Matt Fluegge, Ron Clifford, Scott Blakeley, Brad Boe June 14, 2016 9:00 am Session Number 25042

Updates on Credit Card Surcharging and Acceptance Matt Fluegge, Ron Clifford, Scott Blakeley, Brad Boe June 14, 2016 9:00 am Session Number 25042 Updates on Credit Card Surcharging and Acceptance June

Updates on Credit Card Surcharging and Acceptance Matt Fluegge, Ron Clifford, Scott Blakeley, Brad Boe June 14, 2016 9:00 am Session Number 25042 Updates on Credit Card Surcharging and Acceptance June

ELECTRONIC PAYMENT PROCESSING NEW TOOLS AND TECHNOLOGY

ELECTRONIC PAYMENT PROCESSING NEW TOOLS AND TECHNOLOGY Matt Fluegge Dean Middleton Dan Sollis National Acct. Executive President, UTA Executive VP TODAY, YOU WILL LEARN ABOUT: ACH GATEWAY CREDIT CARD GATEWAY

ELECTRONIC PAYMENT PROCESSING NEW TOOLS AND TECHNOLOGY Matt Fluegge Dean Middleton Dan Sollis National Acct. Executive President, UTA Executive VP TODAY, YOU WILL LEARN ABOUT: ACH GATEWAY CREDIT CARD GATEWAY

U.S. Merchant Class Settlement MasterCard Frequently Asked Questions Merchant

U.S. Merchant Class Settlement MasterCard Frequently Asked Questions Merchant Surcharge Q. What is a surcharge? A. A surcharge is an additional fee that a merchant adds on a transaction when a consumer

U.S. Merchant Class Settlement MasterCard Frequently Asked Questions Merchant Surcharge Q. What is a surcharge? A. A surcharge is an additional fee that a merchant adds on a transaction when a consumer

How to Talk to Vendors about Accepting Card Payments

How to Talk to Vendors about Accepting Card Payments Presented by: David Nakagawa Maureen Sudbay Kristen Bolden Visa Overview 14,600 Financial institution clients 1 2.2 billion Visa cards (as of June 30,

How to Talk to Vendors about Accepting Card Payments Presented by: David Nakagawa Maureen Sudbay Kristen Bolden Visa Overview 14,600 Financial institution clients 1 2.2 billion Visa cards (as of June 30,

Merchant Services Tool Kit TEXPO 2013

Merchant Services Tool Kit TEXPO 2013 Surcharges Visa Information Website Site Preview and PDF s: www.visa.com/merchantsurcharging Materials Notification of Intent to Surcharge Merchants who choose to

Merchant Services Tool Kit TEXPO 2013 Surcharges Visa Information Website Site Preview and PDF s: www.visa.com/merchantsurcharging Materials Notification of Intent to Surcharge Merchants who choose to

A Glossary of Key Terms for the Vendor to Surcharge to Make Card Payments a Price Competitive Payment Channel By: Scott Blakeley, Esq.

A Glossary of Key Terms for the Vendor to Surcharge to Make Card Payments a Price Competitive Payment Channel By: Scott Blakeley, Esq. & Brad Boe Abstract Customers have payment channel choices, whether

A Glossary of Key Terms for the Vendor to Surcharge to Make Card Payments a Price Competitive Payment Channel By: Scott Blakeley, Esq. & Brad Boe Abstract Customers have payment channel choices, whether

Interchange Optimization: Are you getting the best rate?

2012 Interchange Optimization: Are you getting the best rate? Northpark Town Center 1200 Abernathy Road, Suite 1700 Atlanta, Georgia 30328 (800) 846-1305 www.optimizedpmts.com There are many costs associated

2012 Interchange Optimization: Are you getting the best rate? Northpark Town Center 1200 Abernathy Road, Suite 1700 Atlanta, Georgia 30328 (800) 846-1305 www.optimizedpmts.com There are many costs associated

Guidelines for Accepting Credit Cards as a Form of Payment for Education, Registration and Other Fees

Guidelines for Accepting Credit Cards as a Form of Payment for Education, Registration and Other Fees Background Over the past few years, the use of credit cards as a payment option for purchasing goods

Guidelines for Accepting Credit Cards as a Form of Payment for Education, Registration and Other Fees Background Over the past few years, the use of credit cards as a payment option for purchasing goods

Visa Infinite Infinite Platinum

INTERCHANGE RATES The following is a summary of interchange rates of Visa Canada, MasterCard Canada, Discover Financial Service and Interac Direct Payment. For more information please visit: http://www.visa.ca/en/aboutcan/mediacentre/interchange/index.jsp

INTERCHANGE RATES The following is a summary of interchange rates of Visa Canada, MasterCard Canada, Discover Financial Service and Interac Direct Payment. For more information please visit: http://www.visa.ca/en/aboutcan/mediacentre/interchange/index.jsp

Payment Processing Guidance. 2013 Edition

PAYMAXX PRO, LLC Payment Processing Guidance 2013 Edition This document provides thought leadership on payment processing to new or existing merchants who accept credit/debit card or ACH payments. This

PAYMAXX PRO, LLC Payment Processing Guidance 2013 Edition This document provides thought leadership on payment processing to new or existing merchants who accept credit/debit card or ACH payments. This

Credit Card Convenience Fee and Surcharge Rules North Carolina Office of the State Controller Revised May 23, 2011

Credit Card Convenience Fee and Surcharge Rules North Carolina Office of the State Controller Revised May 23, 2011 Card Brand Rules Complexity and Interpretation Government agencies functioning as merchants

Credit Card Convenience Fee and Surcharge Rules North Carolina Office of the State Controller Revised May 23, 2011 Card Brand Rules Complexity and Interpretation Government agencies functioning as merchants

Dates VISA MasterCard Discover American Express. support EMV. International ATM liability shift 2

Network Updates Summer 2013 We are committed to working closely with you on achieving your business goals. As a part of this commitment, we carefully monitor Network changes and summarize them for your

Network Updates Summer 2013 We are committed to working closely with you on achieving your business goals. As a part of this commitment, we carefully monitor Network changes and summarize them for your

Visa Canada Interchange Reimbursement Fees

Visa Canada The following tables set forth the interchange reimbursement fees applied on Visa financial transactions completed in Canada. 1 Visa uses interchange reimbursement fees as transfer fees between

Visa Canada The following tables set forth the interchange reimbursement fees applied on Visa financial transactions completed in Canada. 1 Visa uses interchange reimbursement fees as transfer fees between

Payment Methods. The cost of doing business. Michelle Powell - BASYS Processing, Inc.

Payment Methods The cost of doing business Michelle Powell - BASYS Processing, Inc. You ve got to spend money, to make money Major Industry Topics Industry Process Flow PCI DSS Compliance Risks of Non-Compliance

Payment Methods The cost of doing business Michelle Powell - BASYS Processing, Inc. You ve got to spend money, to make money Major Industry Topics Industry Process Flow PCI DSS Compliance Risks of Non-Compliance

Understanding Your Merchant Fees Presented by:

Understanding Your Merchant Fees Presented by: Melinda Speer Terry Endres VP Strategic Sales Executive SVP Treasury Management Officer Health, Institutions, & Government Government Treasury Services Chicago,

Understanding Your Merchant Fees Presented by: Melinda Speer Terry Endres VP Strategic Sales Executive SVP Treasury Management Officer Health, Institutions, & Government Government Treasury Services Chicago,

What is Interchange. How Complex is Interchange?

What is Interchange The foundation of the entire Bankcard Processing industry s cost structure. Interchange is the wholesale price, charged by Card Issuing Bank, for Authorization and Settlement of a credit

What is Interchange The foundation of the entire Bankcard Processing industry s cost structure. Interchange is the wholesale price, charged by Card Issuing Bank, for Authorization and Settlement of a credit

Visa U.S.A. Interchange Reimbursement Fees

Visa U.S.A. The following tables set forth the interchange reimbursement fees applied on Visa financial transactions completed within the 50 United States and the District of Columbia. Visa uses interchange

Visa U.S.A. The following tables set forth the interchange reimbursement fees applied on Visa financial transactions completed within the 50 United States and the District of Columbia. Visa uses interchange

How Do I Understand Credit Card Processing Fees?

How Do I Understand Credit Card Processing Fees? Credit card processing rates and fees are often misunderstood and confusing, so we are committed to helping you understand the various costs associated

How Do I Understand Credit Card Processing Fees? Credit card processing rates and fees are often misunderstood and confusing, so we are committed to helping you understand the various costs associated

Acceptance to Minimize Fraud

Best Practices for Credit Card Acceptance to Minimize Fraud By implementing best practices in credit card processing, you decrease the likelihood of fraudulent transactions and chargebacks. In general,

Best Practices for Credit Card Acceptance to Minimize Fraud By implementing best practices in credit card processing, you decrease the likelihood of fraudulent transactions and chargebacks. In general,

Managing A Convenience Fee Program

Managing A Convenience Fee Program Michael Volk Vice President, Commercial Product Manager U.S. Bank Jeremy Krahl Regional Sales Manager Elavon Information Services NACHA Payments 2008 May 21, 2008 Agenda

Managing A Convenience Fee Program Michael Volk Vice President, Commercial Product Manager U.S. Bank Jeremy Krahl Regional Sales Manager Elavon Information Services NACHA Payments 2008 May 21, 2008 Agenda

Merchant Processing Application and Agreement Form (MPA) Agent Training First Data Learning Organization

Agent Training First Data Learning Organization") Merchant Processing Application and Agreement Form (MPA) Agent Training First Data Learning Organization Copyright 2010, First Data Corporation. All Rights Reserved. Developer: 26/CD Rev: 5/17/2010 Objectives

Merchant Processing Application and Agreement Form (MPA) Agent Training First Data Learning Organization Copyright 2010, First Data Corporation. All Rights Reserved. Developer: 26/CD Rev: 5/17/2010 Objectives

PayLeap Guide. One Stop

PayLeap Guide One Stop PayLeap does it all. Take payments in person? Check. Payments over the phone or by mail? Check. Payments from mobile devices? Of course. Online payments? No problem. In addition

PayLeap Guide One Stop PayLeap does it all. Take payments in person? Check. Payments over the phone or by mail? Check. Payments from mobile devices? Of course. Online payments? No problem. In addition

TABLE OF CONTENTS. A Merchant Service by Any Other Name. AAmonte, Inc. is a registered ISO of Wells Fargo Bank, N.A., Walnut Creek, CA.

TABLE OF CONTENTS Beware of Merchant Services Pg.1 Managing Payment Processing Costs Pg.2 Credit Card Surcharges Pg.3 Stopping Fraud Pg.4 Dishonest Merchant Services Pg.4 Credit Card Decliines Pg.5 Knowing

TABLE OF CONTENTS Beware of Merchant Services Pg.1 Managing Payment Processing Costs Pg.2 Credit Card Surcharges Pg.3 Stopping Fraud Pg.4 Dishonest Merchant Services Pg.4 Credit Card Decliines Pg.5 Knowing

Visa Debit processing. For ecommerce and telephone order merchants

Visa Debit processing For ecommerce and telephone order merchants Table of contents About this guide 3 General procedures 3 Authorization best practices 3 Status check transactions 4 Authorization reversals

Visa Debit processing For ecommerce and telephone order merchants Table of contents About this guide 3 General procedures 3 Authorization best practices 3 Status check transactions 4 Authorization reversals

Visa USA Interchange Reimbursement Fees

Visa USA Interchange Reimbursement Fees Visa Supplemental Requirements 18 April 2015 Visa Public ii Visa Public 16 April 2015 Introduction to the Introduction to the The following tables set forth the

Visa USA Interchange Reimbursement Fees Visa Supplemental Requirements 18 April 2015 Visa Public ii Visa Public 16 April 2015 Introduction to the Introduction to the The following tables set forth the

How To Get A Visa Check Card

Visa U.S.A. The following tables set forth the interchange reimbursement fees applied on Visa financial transactions completed within the 50 United States and the District of Columbia. Visa uses interchange

Visa U.S.A. The following tables set forth the interchange reimbursement fees applied on Visa financial transactions completed within the 50 United States and the District of Columbia. Visa uses interchange

GLOSSARY OF MOST COMMONLY USED TERMS IN THE MERCHANT SERVICES INDUSTRY

GLOSSARY OF MOST COMMONLY USED TERMS IN THE MERCHANT SERVICES INDUSTRY Acquiring Bank The bank or financial institution that accepts credit and/or debit card payments for products or services on behalf

GLOSSARY OF MOST COMMONLY USED TERMS IN THE MERCHANT SERVICES INDUSTRY Acquiring Bank The bank or financial institution that accepts credit and/or debit card payments for products or services on behalf

Discover Interchange Fees

Discover Assessment Fees: 0.11% PSL Retail (Cardswipe Best Rate) Discover Interchange Fees Rate Per Item Core (Best Rate) 1.56% $0.10 Debit 1.10% $0.16 Prepaid 1.10% $0.16 Rewards 1.71% $0.10 Premium 1.71%

Discover Assessment Fees: 0.11% PSL Retail (Cardswipe Best Rate) Discover Interchange Fees Rate Per Item Core (Best Rate) 1.56% $0.10 Debit 1.10% $0.16 Prepaid 1.10% $0.16 Rewards 1.71% $0.10 Premium 1.71%

Glossary ACH Acquirer Assessments: AVS Authorization Back End: Backbilling Basis Point Batch

Glossary ACH: Automated Clearing House; an electronic payment network most commonly associated with payroll direct deposit, recurring payments, and is the network most commonly used to settle merchant

Glossary ACH: Automated Clearing House; an electronic payment network most commonly associated with payroll direct deposit, recurring payments, and is the network most commonly used to settle merchant

The Merchant s Guide To Achieving Better Interchange Rates

The Merchant s Guide To Achieving Better Interchange Rates Wells Fargo Merchant Services 2007 Wells Fargo Merchant Services, L.L.C. All rights reserved. 04/07 Table of Contents Manage Your Card Payment

The Merchant s Guide To Achieving Better Interchange Rates Wells Fargo Merchant Services 2007 Wells Fargo Merchant Services, L.L.C. All rights reserved. 04/07 Table of Contents Manage Your Card Payment

Your Merchant Statement Guide

Your Merchant Statement Guide HOW TO READ YOUR STATEMENT 1. Billing Address The address given at the time of set-up. 2. Merchant Billing Detail Information identifying you and your relationship with Elavon.

Your Merchant Statement Guide HOW TO READ YOUR STATEMENT 1. Billing Address The address given at the time of set-up. 2. Merchant Billing Detail Information identifying you and your relationship with Elavon.

Credit/Debit Card Processing Requirements and Best Practices. Adele Honeyman Oregon State Treasury Training Specialist

Credit/Debit Card Processing Requirements and Best Practices Adele Honeyman Oregon State Treasury Training Specialist 1 What? What do I need to know about excepting credit cards? Who s involved, how it

Credit/Debit Card Processing Requirements and Best Practices Adele Honeyman Oregon State Treasury Training Specialist 1 What? What do I need to know about excepting credit cards? Who s involved, how it

Online Payment Processing Definitions From Credit Research Foundation (http://www.crfonline.org/)

") Online Payment Processing Definitions From Credit Research Foundation (http://www.crfonline.org/) The following glossary represents definitions for commonly-used terms in online payment processing. Address

Online Payment Processing Definitions From Credit Research Foundation (http://www.crfonline.org/) The following glossary represents definitions for commonly-used terms in online payment processing. Address

and Agreement Form ( MPA )

") Merchant Processing Application and Agreement Form ( MPA ) Revised December 2011 1 General Binding Contract Information Item Merchant Processing Application and Agreement ( MPA ) Action This is a legal

Merchant Processing Application and Agreement Form ( MPA ) Revised December 2011 1 General Binding Contract Information Item Merchant Processing Application and Agreement ( MPA ) Action This is a legal

How To Choose A Payment Processor In Australia

PAYMENT PROCESSING Do you truly understand? A Payment Processing Primer For a business owner, payment processing is one of those aspects of the business that you shouldn t have to worry about. It s not

PAYMENT PROCESSING Do you truly understand? A Payment Processing Primer For a business owner, payment processing is one of those aspects of the business that you shouldn t have to worry about. It s not

Merchant Account Glossary of Terms

Merchant Account Glossary of Terms From offshore merchant accounts to the truth behind free merchant accounts, get answers to some of the most common and frequently asked questions. If you cannot find

Merchant Account Glossary of Terms From offshore merchant accounts to the truth behind free merchant accounts, get answers to some of the most common and frequently asked questions. If you cannot find

Card Acceptance Best Practices to Manage Rates and Minimize Risk

Card Acceptance Best Practices to Manage Rates and Minimize Risk Kim Jackson VP, Transfund Merchant Services April 23, 2014 BOK Financial is registered with the National Association of State Boards of

Card Acceptance Best Practices to Manage Rates and Minimize Risk Kim Jackson VP, Transfund Merchant Services April 23, 2014 BOK Financial is registered with the National Association of State Boards of

MERCHANT ACCOUNT INSTRUCTIONS

MERCHANT ACCOUNT INSTRUCTIONS Please open this applica;on using Adobe Reader so all fields read correctly Now that you re ready to get your account setup, please have all your personal, business and banking

MERCHANT ACCOUNT INSTRUCTIONS Please open this applica;on using Adobe Reader so all fields read correctly Now that you re ready to get your account setup, please have all your personal, business and banking

VISA INTERCHANGE APRIL 2015 CPS Retail Credit 1.51% $0.10 Chip Full Data 1.10% CPS Retail Debit 0.80% $0.15 Chip Full Data-Visa Electron 1.10% U.S.

VISA INTERCHANGE APRIL 2015 CPS Retail Credit 1.51% $0.10 Chip Full Data 1.10% CPS Retail Debit 0.80% $0.15 Chip Full Data-Visa Electron 1.10% U.S. Regulated 0.05% $0.22 Chip Full Data with PIN 1.10% CPS/Retail

VISA INTERCHANGE APRIL 2015 CPS Retail Credit 1.51% $0.10 Chip Full Data 1.10% CPS Retail Debit 0.80% $0.15 Chip Full Data-Visa Electron 1.10% U.S. Regulated 0.05% $0.22 Chip Full Data with PIN 1.10% CPS/Retail

WVU FOUNDATION & UNIVERSITY PURCHASING CARD PROGRAM POLICIES & PROCEDURES. Updated October 2012

WVU FOUNDATION & UNIVERSITY PURCHASING CARD PROGRAM POLICIES & PROCEDURES Updated October 2012 Introduction This document contains the guidelines applicable to the WVU Foundation, Inc. Purchasing Card

WVU FOUNDATION & UNIVERSITY PURCHASING CARD PROGRAM POLICIES & PROCEDURES Updated October 2012 Introduction This document contains the guidelines applicable to the WVU Foundation, Inc. Purchasing Card

ACCESS FEES NETWORK FEES. $710.00 x 2.25%= $15.98. 7 Transactions x $0.10= $0.70 $15.98 + $0.70= $16.68

Glossary of Credit Card Fees INTERCHANGE FEES Set by the payment networks such as Visa and MasterCard and are paid to the bank that issued the credit card. The fee is based on card type. Each card type

Glossary of Credit Card Fees INTERCHANGE FEES Set by the payment networks such as Visa and MasterCard and are paid to the bank that issued the credit card. The fee is based on card type. Each card type

The Comprehensive, Yet Concise Guide to Credit Card Processing

The Comprehensive, Yet Concise Guide to Credit Card Processing Written by David Rodwell CreditCardProcessing.net Terms of Use This ebook was created to provide educational information regarding payment

The Comprehensive, Yet Concise Guide to Credit Card Processing Written by David Rodwell CreditCardProcessing.net Terms of Use This ebook was created to provide educational information regarding payment

Credit vs. Debit: The Network Perspective

July 25, 2010 Credit vs. Debit: The Network Perspective Richard Santoro, Vice President, Government Affairs MasterCard Worldwide 1 Overview Origins of Payment Cards Four-Party Payment System Model Anatomy

July 25, 2010 Credit vs. Debit: The Network Perspective Richard Santoro, Vice President, Government Affairs MasterCard Worldwide 1 Overview Origins of Payment Cards Four-Party Payment System Model Anatomy

Adjustment A debit or credit to a cardholder or merchant account to correct a transaction error

Glossary of Terms A ABA Routing Number This 9-digit number is assigned by the American Banker s Association and is used to identify individual banks. When performing an ACH transfer from one bank account

Glossary of Terms A ABA Routing Number This 9-digit number is assigned by the American Banker s Association and is used to identify individual banks. When performing an ACH transfer from one bank account

Clark Brands Payment Methods Manual. First Data Locations

Clark Brands Payment Methods Manual First Data Locations Table of Contents Introduction... 3 Valid Card Types... 3 Authorization Numbers, Merchant ID Numbers and Request for Copy Fax Numbers... 4 Other

Clark Brands Payment Methods Manual First Data Locations Table of Contents Introduction... 3 Valid Card Types... 3 Authorization Numbers, Merchant ID Numbers and Request for Copy Fax Numbers... 4 Other

CREDIT CARD PROCESSING GLOSSARY OF TERMS

CREDIT CARD PROCESSING GLOSSARY OF TERMS 3DES A highly secure encryption system that encrypts data 3 times, using 3 64-bit keys, for an overall encryption key length of 192 bits. Also called triple DES.

CREDIT CARD PROCESSING GLOSSARY OF TERMS 3DES A highly secure encryption system that encrypts data 3 times, using 3 64-bit keys, for an overall encryption key length of 192 bits. Also called triple DES.

Request for Proposals

Will County Treasurer Request for Proposals Merchant Services, ACH, and Online Bill Payment Brian S. McDaniel 3/5/2014 Introduction General Rules The Will County Treasurer will consider proposals from

Will County Treasurer Request for Proposals Merchant Services, ACH, and Online Bill Payment Brian S. McDaniel 3/5/2014 Introduction General Rules The Will County Treasurer will consider proposals from

Answers for Merchant Service RFP Questions

Answers for Merchant Service RFP Questions The Will County Treasurer s Office has received several questions concerning our RFP for Merchant Services and Credit Card Processing. Here are our replies. We

Answers for Merchant Service RFP Questions The Will County Treasurer s Office has received several questions concerning our RFP for Merchant Services and Credit Card Processing. Here are our replies. We

Omaha Monthend Statements Review

Omaha Monthend Statements Review First Data Learning Organization Copyright 2010, First Data Corporation. All Rights Reserved. Developer: 26 Rev: 01/12/2010 V:1.0 Objectives The FDR System generates and

Omaha Monthend Statements Review First Data Learning Organization Copyright 2010, First Data Corporation. All Rights Reserved. Developer: 26 Rev: 01/12/2010 V:1.0 Objectives The FDR System generates and

Contact Name: City, State, Zip: Owner/Officer/Principal Name: Title: DOB: Close Date Existing MID: % Imprint (Manually Keyed) No Refund

No Refund") MERCHANT APPLICATION 314 S. 200 W. Farmington, UT 84025 Phone: 801-298-1212 Fax: 801-951-8210 Please carefully complete the enclosed Application and read the attached Terms and Conditions and other additional

MERCHANT APPLICATION 314 S. 200 W. Farmington, UT 84025 Phone: 801-298-1212 Fax: 801-951-8210 Please carefully complete the enclosed Application and read the attached Terms and Conditions and other additional

Merchant Card Processing Best Practices

Merchant Card Processing Best Practices Background: The major credit card companies (VISA, MasterCard, Discover, and American Express) have published a uniform set of data security standards that ALL merchants

Merchant Card Processing Best Practices Background: The major credit card companies (VISA, MasterCard, Discover, and American Express) have published a uniform set of data security standards that ALL merchants

Cost-management strategies. Your guide to accepting card payments cost-effectively

Cost-management strategies Your guide to accepting card payments cost-effectively Table of Contents Guidance from Wells Fargo Merchant Services...3 The secret to better interchange rates...4 Why interchange

Cost-management strategies Your guide to accepting card payments cost-effectively Table of Contents Guidance from Wells Fargo Merchant Services...3 The secret to better interchange rates...4 Why interchange

Appendix. Data Tables

Appendix Data Tables Index of Tables Part 1: In-Store Payment Preferences...167 1.1 What payment products do you have?...167 1.2 How often do you use the following payment methods for purchases in stores?...167

Appendix Data Tables Index of Tables Part 1: In-Store Payment Preferences...167 1.1 What payment products do you have?...167 1.2 How often do you use the following payment methods for purchases in stores?...167

How to Read Your Monthly Statement (Card, ACH and Excel Spreadhseet)

") How to Read Your Monthly Statement (Card, ACH and Excel Spreadhseet) Your Monthly Card Statement is broken out into 3 parts. Each section will be explained in greater detail in the few pages. The first

How to Read Your Monthly Statement (Card, ACH and Excel Spreadhseet) Your Monthly Card Statement is broken out into 3 parts. Each section will be explained in greater detail in the few pages. The first

SUBMITTER MERCHANT AGREEMENT PAYMENT PROCESSING INSTRUCTIONS AND GUIDELINES

SUBMITTER MERCHANT AGREEMENT PAYMENT PROCESSING INSTRUCTIONS AND GUIDELINES Paymentech, L.P. ( Paymentech or we, us or our and the like) and ( ) are excited about the opportunity to provide you with state-of-the-art

SUBMITTER MERCHANT AGREEMENT PAYMENT PROCESSING INSTRUCTIONS AND GUIDELINES Paymentech, L.P. ( Paymentech or we, us or our and the like) and ( ) are excited about the opportunity to provide you with state-of-the-art

Table of Contents The Market for Merchant Services... 1 The Basics of Payment Processing... 2 Authorization Settlement Funding... 2 Authorization...

Table of Contents The Market for Merchant Services... 1 The Basics of Payment Processing... 2 Authorization Settlement Funding... 2 Authorization... 2 Settlement... 2 Funding... 2 Credit Card Processing

Table of Contents The Market for Merchant Services... 1 The Basics of Payment Processing... 2 Authorization Settlement Funding... 2 Authorization... 2 Settlement... 2 Funding... 2 Credit Card Processing

Redwood Merchant Services. Merchant Processing Terminology

ACH - Automated Clearing House for member banks to process electronic payments or withdrawals. (Credits or debits to a bank account) through the Federal Reserve Bank. Acquiring Bank - Licensed Visa/MasterCard

ACH - Automated Clearing House for member banks to process electronic payments or withdrawals. (Credits or debits to a bank account) through the Federal Reserve Bank. Acquiring Bank - Licensed Visa/MasterCard

The Science of Credit Card Processing

The Science of Credit Card Processing Page 1 Credit Card Processing How does credit card processing work? You may receive credit card payments from customers from a variety of sources. You may swipe their

The Science of Credit Card Processing Page 1 Credit Card Processing How does credit card processing work? You may receive credit card payments from customers from a variety of sources. You may swipe their

EMV in Hotels Observations and Considerations

EMV in Hotels Observations and Considerations Just in: EMV in the Mail Customer Education: Credit Card companies have already started customer training for the new smart cards. 1 Questions to be Answered

EMV in Hotels Observations and Considerations Just in: EMV in the Mail Customer Education: Credit Card companies have already started customer training for the new smart cards. 1 Questions to be Answered

Using Prepaid Cards for Claims (and other) Payments

Payments") Using Prepaid Cards for Claims (and other) Payments American Association of State Compensation Insurance Funds Super Conference Presentation October 2 October 5, 2012 Rick Pileggi Senior Vice President

Using Prepaid Cards for Claims (and other) Payments American Association of State Compensation Insurance Funds Super Conference Presentation October 2 October 5, 2012 Rick Pileggi Senior Vice President

Table of Contents. Overview. What is payment processing? Who s Who. Types of Payment Solutions. Online Transactions. Interchange Process

Overview Credit Card Processing 101 is your go-to handbook for navigating the payments industry. This document provides a quick and thorough understanding on how businesses accept electronic payments,

Overview Credit Card Processing 101 is your go-to handbook for navigating the payments industry. This document provides a quick and thorough understanding on how businesses accept electronic payments,

UNDERSTANDING MERCHANT PRICING

UNDERSTANDING MERCHANT PRICING 0 CONTENTS Definitions.. 1 Pricing Structures. 2 Tiered Pricing 3 Flat Rate Pricing 4 Cost Plus Pricing...5 Additional Resources 6 Visa Interchange Fees Table 7 MasterCard

UNDERSTANDING MERCHANT PRICING 0 CONTENTS Definitions.. 1 Pricing Structures. 2 Tiered Pricing 3 Flat Rate Pricing 4 Cost Plus Pricing...5 Additional Resources 6 Visa Interchange Fees Table 7 MasterCard

All Things Payments & EMV. www.thestrawgroup.com / www.paymentspulse.com

All Things Payments & EMV www.thestrawgroup.com / www.paymentspulse.com Section 1: Payments Primer History and major payments milestones Merchants having the ability to accept card brands is the foundation

All Things Payments & EMV www.thestrawgroup.com / www.paymentspulse.com Section 1: Payments Primer History and major payments milestones Merchants having the ability to accept card brands is the foundation

The following information was prepared to assist you in understanding potential Electronic Value Transfer terminology.

ELECTRONIC VALUE TRANSFER CONTRACT (EVT) GLOSSARY OF TERMS The following information was prepared to assist you in understanding potential terminology. Term Description ACH Automated Clearing House is

ELECTRONIC VALUE TRANSFER CONTRACT (EVT) GLOSSARY OF TERMS The following information was prepared to assist you in understanding potential terminology. Term Description ACH Automated Clearing House is

Interchange Qualification Matrix

Interchange Qualification Matrix Includes: Visa and MasterCard Interchange Programs PIN Debit Interchange and Switch Fees VISA AND MASTERCARD PREFACE A significant amount of the fees that we charge to

Interchange Qualification Matrix Includes: Visa and MasterCard Interchange Programs PIN Debit Interchange and Switch Fees VISA AND MASTERCARD PREFACE A significant amount of the fees that we charge to

Accepting Credit Cards 101

1 Accepting Credit Cards 101 Payment Cards: A Brief History and the Invention of. The Key Players: The Associations, Member Banks, Processors, Service Providers, Agents, Cardholders, and Merchants : Card

1 Accepting Credit Cards 101 Payment Cards: A Brief History and the Invention of. The Key Players: The Associations, Member Banks, Processors, Service Providers, Agents, Cardholders, and Merchants : Card

An Education in Merchant Processing

An Education in Merchant Processing Presented by: Michael Mintz COO - AMG Payment Solutions Today s Agenda Introduction and Background Important Industry Terms The Electronic Payment Process Interchange

An Education in Merchant Processing Presented by: Michael Mintz COO - AMG Payment Solutions Today s Agenda Introduction and Background Important Industry Terms The Electronic Payment Process Interchange

ACQUIRER OR ACQUIRING BANK A financial institution (often a bank) where a merchant has an account to process transactions and card payments

where a merchant has an account to process transactions and card payments") A TO Z JARGON BUSTER A ACQUIRER OR ACQUIRING BANK A financial institution (often a bank) where a merchant has an account to process transactions and card payments ATM Automated Teller Machine. Unattended,

A TO Z JARGON BUSTER A ACQUIRER OR ACQUIRING BANK A financial institution (often a bank) where a merchant has an account to process transactions and card payments ATM Automated Teller Machine. Unattended,

ACQUIRER PASS THROUGH FEES

ACQUIRER PASS THROUGH FEES BASED ON VOLUME BASED ON NUMBER OF TRANSACTIONS ASSESSMENTS (V/MC/DISC) VISA SETTLEMENT NETWORK ACCESS FEE VISA INTERNATIONAL ASSESSMENT FEE VISA INTERNATIONAL ACQUIRER FEE MASTERCARD

ACQUIRER PASS THROUGH FEES BASED ON VOLUME BASED ON NUMBER OF TRANSACTIONS ASSESSMENTS (V/MC/DISC) VISA SETTLEMENT NETWORK ACCESS FEE VISA INTERNATIONAL ASSESSMENT FEE VISA INTERNATIONAL ACQUIRER FEE MASTERCARD

Ti ps. Merchant. for Credit Card Transactions. Processing Tips CARD ONE INTERNATIONAL INC

Merchant Processing Tips Ti ps for Credit Card Transactions CARD ONE INTERNATIONAL INC Card One International Inc - Merchant Processing Tips for Card Transactions Page 1 of 11 Merchant Processing Tips

Merchant Processing Tips Ti ps for Credit Card Transactions CARD ONE INTERNATIONAL INC Card One International Inc - Merchant Processing Tips for Card Transactions Page 1 of 11 Merchant Processing Tips

Electronic Value Transfer Administrator Form EVTA-2, Key Merchant Services (KMS) Work Order Contract PS65792

Work Order Contract PS65792") Authorized User Code Date Requisition No. Comptroller's ID No.: Commodity Group No.: 79008 Work Order No. Authorized User & Federal Identification #: Contractor: Key Merchant Services, LLC Two Concourse

Authorized User Code Date Requisition No. Comptroller's ID No.: Commodity Group No.: 79008 Work Order No. Authorized User & Federal Identification #: Contractor: Key Merchant Services, LLC Two Concourse

Town of Fairview, Texas Request for Proposal Merchant Card Services

Town of Fairview, Texas Request for Proposal Merchant Card Services SECTION I REQUEST FOR PROPOSAL INFORMATION A. Introduction and Background The Town of Fairview (the Town) is requesting proposals from

Town of Fairview, Texas Request for Proposal Merchant Card Services SECTION I REQUEST FOR PROPOSAL INFORMATION A. Introduction and Background The Town of Fairview (the Town) is requesting proposals from

EDUCATION - TERMS 101

EDUCATION - TERMS 101 ACH (Automated Clearing House): A processing organization networked with others to exchange (clear and settle) electronic debit/credit transactions (no physical checks). ABA Routing

EDUCATION - TERMS 101 ACH (Automated Clearing House): A processing organization networked with others to exchange (clear and settle) electronic debit/credit transactions (no physical checks). ABA Routing

Credit Card Processing 101

Credit Card Processing 101 Customers have come to expect credit cards as a payment option. With ATM fees continuing to rise, some consumers may even exclusively choose to take their purchasing power to

Credit Card Processing 101 Customers have come to expect credit cards as a payment option. With ATM fees continuing to rise, some consumers may even exclusively choose to take their purchasing power to

Interchange Plus Pricing. Bringing Transparency to Credit Card Processing Fees

Interchange Plus Pricing Bringing Transparency to Credit Card Processing Fees Industry Whitepaper by Marlon Harris, emerchant Inc. Most credit card processors simplify the complexity of interchange by

Interchange Plus Pricing Bringing Transparency to Credit Card Processing Fees Industry Whitepaper by Marlon Harris, emerchant Inc. Most credit card processors simplify the complexity of interchange by

State Gift Card Consumer Protection Laws*

State Gift Card Consumer Protection Laws* The following is a summary of state gift card laws. The Credit CARD Act of 2009 may provide additional gift card protections. The money on store-issued gift cards,

State Gift Card Consumer Protection Laws* The following is a summary of state gift card laws. The Credit CARD Act of 2009 may provide additional gift card protections. The money on store-issued gift cards,

An access number, dialed by a modem, that lets a computer communicate with an Internet Service Provider (ISP) or some other service provider.

or some other service provider.") TERM DEFINITION Access Number Account Number Acquirer Acquiring Bank Acquiring Processor Address Verification Service (AVS) Association Authorization Authorization Center Authorization Fee Automated Clearing

TERM DEFINITION Access Number Account Number Acquirer Acquiring Bank Acquiring Processor Address Verification Service (AVS) Association Authorization Authorization Center Authorization Fee Automated Clearing

Exhibit K Official Payments Corporation Convenience Fee Services

This Exhibit K is between You ( Authorized User ) and Official Payments Corporation ( OPC ) and is made a part of and is subject to the terms and conditions of the Master Services Agreement ( Agreement

This Exhibit K is between You ( Authorized User ) and Official Payments Corporation ( OPC ) and is made a part of and is subject to the terms and conditions of the Master Services Agreement ( Agreement

2015 Interchange Qualification Guide

2015 Interchange Qualification Guide QUALIFICATION CATEGORY DEFINITIONS Transactions that meet all of the requirements for the merchant s industry. Merchants will pay the lowest or best discount rate for

2015 Interchange Qualification Guide QUALIFICATION CATEGORY DEFINITIONS Transactions that meet all of the requirements for the merchant s industry. Merchants will pay the lowest or best discount rate for

Rules for Visa Merchants. Card Acceptance and Chargeback Management Guidelines

Rules for Visa Merchants Card Acceptance and Chargeback Management Guidelines Rules for Visa Merchants Card Acceptance and Chargeback Management Guidelines Table of Contents Introduction..............................................................

Rules for Visa Merchants Card Acceptance and Chargeback Management Guidelines Rules for Visa Merchants Card Acceptance and Chargeback Management Guidelines Table of Contents Introduction..............................................................

Funded to Your Bank $23,736.93

THIS IS A SAMPLE STATEMENT YOUR CARD PROCESSING STATEMENT 099382/000001/187698/0001/23882/0000/144030 000 01 000000 Page 1 of 8 THIS IS NOT A BILL This is the overall summary of the account activity for

THIS IS A SAMPLE STATEMENT YOUR CARD PROCESSING STATEMENT 099382/000001/187698/0001/23882/0000/144030 000 01 000000 Page 1 of 8 THIS IS NOT A BILL This is the overall summary of the account activity for

Recurring Payments Best Practices Guide

Recurring Payments Best Practices Guide Table of Contents DEFINITIONS... 3 RECURRING TRANSACTION... 3 INSTALLMENT TRANSACTIONS... 3 RECURRING PAYMENT INDICATOR... 4 CARDHOLDER BENEFITS & BEST PRACTICES...

Recurring Payments Best Practices Guide Table of Contents DEFINITIONS... 3 RECURRING TRANSACTION... 3 INSTALLMENT TRANSACTIONS... 3 RECURRING PAYMENT INDICATOR... 4 CARDHOLDER BENEFITS & BEST PRACTICES...

VISA CLASSIC CONSUMER CREDIT CARD AGREEMENT

VISA CLASSIC CONSUMER CREDIT CARD AGREEMENT In this Agreement, Agreement means this Consumer Credit Card Agreement. Disclosure means the Credit Card Account Opening Disclosure. The Account Opening Disclosure

VISA CLASSIC CONSUMER CREDIT CARD AGREEMENT In this Agreement, Agreement means this Consumer Credit Card Agreement. Disclosure means the Credit Card Account Opening Disclosure. The Account Opening Disclosure

Questions and Answers PCI Compliance (Updated May 23, 2014)

") Questions and Answers PCI Compliance (Updated ) The Alberta government is working toward PCI compliance, an industry standard created by the credit card industry to improve cardholder data security. The

Questions and Answers PCI Compliance (Updated ) The Alberta government is working toward PCI compliance, an industry standard created by the credit card industry to improve cardholder data security. The

Public authorities have recently intervened in the U.S. payment

The New Debit Card Regulations: Effects on Merchants, Consumers, and Payments System Efficiency By Fumiko Hayashi Public authorities have recently intervened in the U.S. payment card industry to address

The New Debit Card Regulations: Effects on Merchants, Consumers, and Payments System Efficiency By Fumiko Hayashi Public authorities have recently intervened in the U.S. payment card industry to address

Payment Network Fees. Statement Descriptor. Visa. Fee Definition. Visa US Acquirer Service Fee (Assessments) Visa Assessment Fee

Visa Assessment Fee") Visa Visa US Acquirer Service (Assessments) Visa Assessment 0.13% The Visa US Acquirer Service will be assessed to all Visa sale transactions. Visa International Service International Service - ISA The

Visa Visa US Acquirer Service (Assessments) Visa Assessment 0.13% The Visa US Acquirer Service will be assessed to all Visa sale transactions. Visa International Service International Service - ISA The

Chargeback Reason Code List - U.S.

AL Airline Transaction Dispute AP Automatic Payment AW Altered Amount CA Cash Advance Dispute CD Credit Posted as Card Sale CR Cancelled Reservation This chargeback occurs because of a dispute on an Airline

AL Airline Transaction Dispute AP Automatic Payment AW Altered Amount CA Cash Advance Dispute CD Credit Posted as Card Sale CR Cancelled Reservation This chargeback occurs because of a dispute on an Airline

Why Savings from Private Label ACH Debit Programs May Not Always Add Up.

Commissioned by MasterCard. Why Savings from Private Label ACH Debit Programs May Not Always Add Up. A detailed cost comparison between ACH-based store loyalty programs and network debit cards. Edgar,

Commissioned by MasterCard. Why Savings from Private Label ACH Debit Programs May Not Always Add Up. A detailed cost comparison between ACH-based store loyalty programs and network debit cards. Edgar,

Choosing the Right Merchant Account Provider. 5 Essential Factors Every Business Owner Must Understand Before Choosing a Payment Processing Provider

Choosing the Right Merchant Account Provider 5 Essential Factors Every Business Owner Must Understand Before Choosing a Payment Processing Provider 5 Essential Factors Starting to accept credit cards at

Choosing the Right Merchant Account Provider 5 Essential Factors Every Business Owner Must Understand Before Choosing a Payment Processing Provider 5 Essential Factors Starting to accept credit cards at

INTERCHANGE RATE SCHEDULE (Effective April, 2014)

") This Interchange Rate Schedule contains a summary of the primary qualification criteria established by Visa, MasterCard, and Discover Network (sometimes referred to as Discover) for most interchange programs

This Interchange Rate Schedule contains a summary of the primary qualification criteria established by Visa, MasterCard, and Discover Network (sometimes referred to as Discover) for most interchange programs

Visa Interchange Programs and Rate Schedule (Effective January, 2015)

") CPS / Retail Credit 1.51% $0.10 CPS / Retail Debit 0.80% $0.15 CPS / Retail Prepaid 1.15% $0.15 This Interchange Programs and Rate Schedule contains a summary of the primary qualification criteria established

CPS / Retail Credit 1.51% $0.10 CPS / Retail Debit 0.80% $0.15 CPS / Retail Prepaid 1.15% $0.15 This Interchange Programs and Rate Schedule contains a summary of the primary qualification criteria established

Chargebacks: Another Payment Card Acceptance Cost for Merchants

Chargebacks: Another Payment Card Acceptance Cost for Merchants Fumiko Hayashi, Zach Markiewicz, and Richard J. Sullivan January 216 RWP 16-1 http://dx.doi.org/1.18651/rwp216-1 Chargebacks: Another Payment

Chargebacks: Another Payment Card Acceptance Cost for Merchants Fumiko Hayashi, Zach Markiewicz, and Richard J. Sullivan January 216 RWP 16-1 http://dx.doi.org/1.18651/rwp216-1 Chargebacks: Another Payment

EMV FAQs. Contact us at: [email protected]. Visit us online: VancoPayments.com

EMV FAQs Contact us at: [email protected] Visit us online: VancoPayments.com What are the benefits of EMV cards to merchants and consumers? What is EMV? The acronym EMV stands for an organization formed

EMV FAQs Contact us at: [email protected] Visit us online: VancoPayments.com What are the benefits of EMV cards to merchants and consumers? What is EMV? The acronym EMV stands for an organization formed