The interplay of physical and financial layers in today's oil markets

|

|

|

- Philomena Cunningham

- 8 years ago

- Views:

Transcription

1 Master of Advanced Studies in International Oil and Gas Leadership The interplay of physical and financial layers in today's oil markets Giacomo Luciani IEA Energy Training Week Paris, April 5, 2013

2 The Market for Brent Brent is a field in the UK North Sea. The market consists of: A spot market; A physical forward market; A futures market based at the International Petroleum Exchange (IPE) in London

3 The spot market, or dated Brent Dated Brent refers to the sale of a specific cargo that is either available in a specific loading slot or that is already loaded and in transit to some destination. Main characteristics: Transactions are bilateral, Over the counter (OTC), For variable quantities.

,")

4 The forward market, or 21-day Brent The 21-day cargo is a standard parcel (600,000 barrels) that will be made available by the seller to the buyer on an unspecified day of the relevant month (buyer must be notified of loading date at least 21 days in advance. The clearing involves book-outs or seller s nominations, which can take place on any day in the period starting 21 days before the beginning of the relevant month. As dated Brent, 21-day Brent is bilateral and OTC but it is standardized.

5 Price Reporting Agencies (PRAs) If transactions are bilateral and OTC, prices are not easily visible Price Reporting Agencies are private providers who survey the market for prices Two main PRAs for oil: Platt s and Argus Different methodologies: Platt s window Are PRAs neutral or do they influence the market? Should they be regulated? (issue being discussed by the G20)

6 The futures market The futures market was launched by the International Petroleum Exchange (IPE today International Commodity Exchange - ICE) in contract = 1000 barrels Contract based on cash settlement and not on physical delivery If a contract is allowed to expire the settlement price is the Brent index Central exchange and clearing house rather than bilateral trades Several months (indeed, years) traded

7 Options Launched by the IPE in 1989 A call option gives the holder the right to buy the underlying futures contract, and a put option the right to sell. Call and put options may be combined to design complex risk management strategies.

8 What are options for? Any buyer or seller on the petroleum market faces a price risk. Options and futures allow parties facing a structural risk to limit that risk, selling it to speculators (or insurers ).

9 Hedging A producer can sell futures or buy put options to ensure a minimum level of prices. A large consumer can buy futures or a call option to ensure against very high prices Major companies are on both sides of the market and may be doing both things at the same time.

10 Why so many Paper Barrels? Most participants in the futures market are there to manage their risk, not to acquire Brent crude. Buying and selling Brent futures and options is an effective strategy because other crude prices follow Brent movements.

11 The Structure of the Oil Market At the center, we find the market for Brent and WTI, which influence each other Brent and WTI trade few physical and lots of paper barrels Paper and wet barrels influence each other, but paper barrels are more important Smaller markets, such as ANS and Dubai, are influenced by Brent and WTI

12

13

14 The Influence of Brent Consilience Energy Advisory Group Ltd Physical = 83.6 million b/d in Estimated that 2/3 priced by reference to Brent = 20 billion/year. The ICE futures contract for Brent alone traded >130 billion bbls in 2011 OTC forwards- volume unknown but likely to be more than futures PSC- cost recovery, profit share Tax Gas contracts? Can t be less than 200 billion bbls per year, even on conservative estimates 14 COPYRIGHT CEAG LTD

15 Feature of Physical Benchmarks: Financial Layers and the Spot Price Many financial layers (paper markets) emerged around physical benchmarks Financial layers highly interlinked with benchmarks through process of arbitrage and development of products that link layers together Idea that one can isolate physical from financial layers in current oil pricing system is simplistic Information derived from financial layers plays an important role in identifying the price level of the benchmark Brent market: Price of Dated Brent assessed using information from many layers including CFDs, forward markets, EFPs and futures markets WTI complex: prices of the various physical benchmarks strongly interlinked with the futures markets Price of Dubai often derived using information from the very active OTC Dubai/Brent swaps market and the inter-dubai swap market

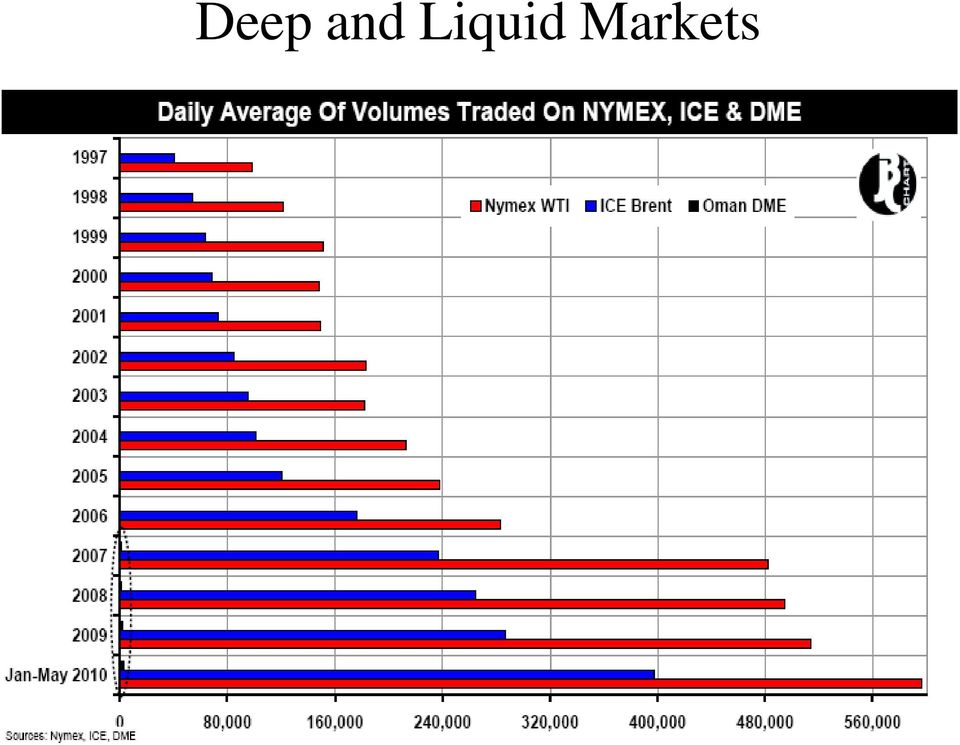

16 Deep and Liquid Markets

17 The Inter-linkages Between Financial and Physical Layers Inter-Dubai Swap Market Dubai Price Forward Dubai Contract For Differences (CFDs) Exchange for Physicals (EFPs) Dated Brent Forward Brent Brent Futures Market Dubai/Brent Exchange for Physicals (EFPs)

18 DATED EFP FORWARD CFD FUTURES (several years traded) WTI Dubai BRENT OIL Oil Products LPG Naphtha Gasoline Diesel Fuel oil Several traded hubs Pipeline LNG GAS COAL POWER CARBON

19 Other Crudes All other major crudes are priced on the basis of formulas which tie them to Brent or WTI The producing countries oppose the free trading of their crudes, and restrict destination and secondary trading Formulas are modified from time to time, but the essence remains

20 Example: Saudi Arabia s Prices for 04/13 Source: Middle East Economic Survey 15 March 2013

21 Why oil producing countries like reference pricing? Accepting pricing out of a marker implies that producers are giving up on an important role They should naturally be price makers, instead are price takers Why? First and foremost because in the past they failed in the management of posted prices.

22 Why there is no Arabian Light market? Setting up a market for a major crude, such as e.g. Arabian Light, is not easy because there is just one seller The seller does not want the responsibility of making prices, because he is afraid of international political pressure or domestic dissension.

23 How is the Market Cleared? Brent/WTI are not the marginal crudes that balance demand and supply. Yet, it is Brent/WTI that make the price. The implication is that demand and supply are not necessarily balanced: OPEC and other operators manage supply and/or stocks, given the price.

24 Features of Benchmarks: Physical Liquidity of Benchmarks Markets with relatively low physical liquidity set the price for markets with much higher volume of production Low physical liquidity and squeezes As markets become thinner and thinner, squeezes and distortions become more widespread Prices and spreads become less informative and more volatile Nature of these benchmarks tends to evolve over time but not without problems Widen the benchmark for assessment purposes Assessment of traditional Brent benchmark now includes North Sea streams Forties, Oseberg and Ekofisk (BFOE) Dubai price includes Oman and Upper Zakum Short-term solutions of adding additional streams successful in alleviating problem of squeezes but should not distract observers from raising key questions What are necessary conditions for the emergence of successful benchmarks in the most liquid market in terms of production? Would a shift to price assessment in markets with high physical liquidity improve the price discovery process?

25 The Feedback Issue Given this market structure, operators that have no interest in Brent crude trade in Brent futures and options, to manage their risk In this way, a certain feedback is obtained between the global physical oil market and Brent However, such feedback is limited and partial The feedback would be greater if all operators hedged systematically; in that case, an excess of demand would raise the price of calls, financial intermediaries would lower the price of puts, producers would be incentivated

26 Perception of Limited Feedbacks Uncertainty about existence of and timing of feedbacks from prices to oil supply and demand increased markedly during boom Perception of strong feedbacks replaced by perception of limited feedbacks Key feedbacks that were perceived to be absent Oil demand response to oil prices High oil prices would trigger a rise in global inflation rates and a subsequent recession, tempering growth in the demand for oil High oil prices would induce strong growth in non-opec supply OPEC would increase its oil supply to prevent oil prices from rising to high levels or try to put a cap on the oil price

27 The Forward Curve At any point in time, we have several prices for the same marker for different maturity future contracts. If prices for subsequent months are lower than the closest-month price the market is said to be in backwardation If prices for subsequent months are higher than the closest-month price the market is said to be in contango

28 Source: Royal Bank of Scotland March 28, 2013 Brent Forward Curve

29 Parallel shift in the Futures Curve

30 Meaning of contango A contango occurs when the market expects future prices to be higher than today s Normally, a contango occurs when prompt prices are low, backwardation when they are high Backwardation is the normal state of a market because holding stocks has a physical and financial cost (interest rate)

31 What is the impact of backwardation/contango? Contango encourages the buildup of physical stocks (you earn money by buying spot and selling futures, while holding the commodity) Backwardation encourages financial commodity investors (you make money by buying futures and waiting for futures to converge to spot prices)

ICE Middle East Sour Crude Oil Futures Contract: FAQ

ICE Middle East Sour Crude Oil Futures Contract: FAQ 1. Why are we launching a sour crude contract? To provide a hedging tool to accommodate risk management needs in the global market for sour crude oil.

ICE Middle East Sour Crude Oil Futures Contract: FAQ 1. Why are we launching a sour crude contract? To provide a hedging tool to accommodate risk management needs in the global market for sour crude oil.

The Crude Oil Pricing System: Features & Prospects

The Crude Oil Pricing System: Features & Prospects Dr Bassam Fattouh Oxford Institute for Energy Studies 29 March 2011 Presented at the Surrey Energy Economics Centre Speculation Versus Fundamentals Debate

The Crude Oil Pricing System: Features & Prospects Dr Bassam Fattouh Oxford Institute for Energy Studies 29 March 2011 Presented at the Surrey Energy Economics Centre Speculation Versus Fundamentals Debate

The Dubai Benchmark and Its Role in the International Oil Pricing System

Oxford Energy Comment March 2012 The Dubai Benchmark and Its Role in the International Oil Pricing System By Bassam Fattouh INTRODUCTION Dubai became the main price marker for the Gulf region by default

Oxford Energy Comment March 2012 The Dubai Benchmark and Its Role in the International Oil Pricing System By Bassam Fattouh INTRODUCTION Dubai became the main price marker for the Gulf region by default

Topic 9: Energy Pricing and Trading in Financial Markets. () Global Energy Issues, Industries and Markets 1 / 41

Global Energy Issues, Industries and Markets 1 / 41") Topic 9: Energy Pricing and Trading in Financial Markets () Global Energy Issues, Industries and Markets 1 / 41 Introduction Energy prices determined in many ways E.g. long term contracts for natural gas

Topic 9: Energy Pricing and Trading in Financial Markets () Global Energy Issues, Industries and Markets 1 / 41 Introduction Energy prices determined in many ways E.g. long term contracts for natural gas

Contents. Introduction Course Overview Program Outline Who Should Attend? Course Leaders Background Contact & Booking Information.

Energy Markets & Pricing UNIST 2014 Contents Introduction Course Overview Program Outline Who Should Attend? Course Leaders Background Contact & Booking Information Slide 2 Introduction Energy Markets

Energy Markets & Pricing UNIST 2014 Contents Introduction Course Overview Program Outline Who Should Attend? Course Leaders Background Contact & Booking Information Slide 2 Introduction Energy Markets

INTRODUCTION. Production / Extraction of Oil. Distribution & Sale to refined products to end users

CRUDE OIL INTRODUCTION Crude oil holds prominence as input to the global growth engine since it is the most important source of energy accounting for more than two fifth of the global energy consumption.

CRUDE OIL INTRODUCTION Crude oil holds prominence as input to the global growth engine since it is the most important source of energy accounting for more than two fifth of the global energy consumption.

How To Price Oil

B A C K G R O U N D E R OIL The Structure of Global Oil Markets June 2010 BACKGROUNDER: The Structure of Global Oil Markets WHAT ARE THE VARIOUS OIL TRADING STRUCTURES? Total world production of crude

B A C K G R O U N D E R OIL The Structure of Global Oil Markets June 2010 BACKGROUNDER: The Structure of Global Oil Markets WHAT ARE THE VARIOUS OIL TRADING STRUCTURES? Total world production of crude

Platts Forward Curve-Oil

[OIL ] METHODOLOGY AND SPECIFICATIONS GUIDE Platts Forward Curve-Oil (Latest Update: ) OIL Derivatives methodology guide 2 Market Methodology 2 GENERAL ASSESSMENT PRINCIPLES 2 Disclosure 2 ASIA PACIFIC

[OIL ] METHODOLOGY AND SPECIFICATIONS GUIDE Platts Forward Curve-Oil (Latest Update: ) OIL Derivatives methodology guide 2 Market Methodology 2 GENERAL ASSESSMENT PRINCIPLES 2 Disclosure 2 ASIA PACIFIC

Oil Markets in Transition and the Dubai Crude Oil Benchmark

October 2014 Oil Markets in Transition and the Dubai Crude Oil Benchmark OXFORD ENERGY COMMENT Adi Imsirovic GM, Clearsource Commodity Services Ltd 1. Introduction Dubai crude oil has been the main Asian

October 2014 Oil Markets in Transition and the Dubai Crude Oil Benchmark OXFORD ENERGY COMMENT Adi Imsirovic GM, Clearsource Commodity Services Ltd 1. Introduction Dubai crude oil has been the main Asian

5th Annual Oil Trader Academy

5th Annual Oil Trader Academy ICE Futures Europe, London July-August 2015 ICE Education and IBH have combined their expertise to provide an innovative and practical programme covering all aspects of the

5th Annual Oil Trader Academy ICE Futures Europe, London July-August 2015 ICE Education and IBH have combined their expertise to provide an innovative and practical programme covering all aspects of the

The Energy Markets Peter C. Fusaro 1. Introduction This chapter introduces the energy markets from a risk management perspective.

The Energy Markets Peter C. Fusaro 1 Introduction This chapter introduces the energy markets from a risk management perspective. Energy trading began in 1978 with the first oil futures contract on the

The Energy Markets Peter C. Fusaro 1 Introduction This chapter introduces the energy markets from a risk management perspective. Energy trading began in 1978 with the first oil futures contract on the

response to the immense volatility that resulted from the oil price

IntercontinentalExchange (ICE ) became a center for global petroleum risk management and trading with its acquisition of the International Petroleum Exchange (IPE ) in June 2001, which is today known as

IntercontinentalExchange (ICE ) became a center for global petroleum risk management and trading with its acquisition of the International Petroleum Exchange (IPE ) in June 2001, which is today known as

The Pricing of Crude Oil

Stephanie Dunn and James Holloway* Arguably no commodity is more important for the modern economy than oil. This is true in terms of both production and financial market activity. Yet its pricing is relatively

Stephanie Dunn and James Holloway* Arguably no commodity is more important for the modern economy than oil. This is true in terms of both production and financial market activity. Yet its pricing is relatively

GUIDANCE ICE Futures Europe EFP, EFS, Soft Commodity EFRP and Basis Trade Policy

GUIDANCE ICE Futures Europe EFP, EFS, Soft Commodity EFRP and Basis Trade Policy September 2014 Copyright Intercontinental Exchange, Inc. 2014. All Rights Reserved. ICE Futures Europe Guidance on the Exchange

GUIDANCE ICE Futures Europe EFP, EFS, Soft Commodity EFRP and Basis Trade Policy September 2014 Copyright Intercontinental Exchange, Inc. 2014. All Rights Reserved. ICE Futures Europe Guidance on the Exchange

Joint IEA-IEF-OPEC Report on the 4th Workshop. Interactions between Physical and Financial Energy Markets. 31 March 2014.

Joint IEA-IEF-OPEC Report on the 4th Workshop Interactions between Physical and Financial Energy Markets 31 March 2014 Vienna, Austria 1 Executive Summary The Fourth IEA-IEF-OPEC Workshop on the Interactions

Joint IEA-IEF-OPEC Report on the 4th Workshop Interactions between Physical and Financial Energy Markets 31 March 2014 Vienna, Austria 1 Executive Summary The Fourth IEA-IEF-OPEC Workshop on the Interactions

Platts Oil Benchmarks & Price Assessment Methodology. October 4, 2012 - London

Platts Oil Benchmarks & Price Assessment Methodology October 4, 2012 - London Agenda Introduction and the role of benchmarks Platts price discovery process Global commodity markets outlook Platts MOC liquidity:

Platts Oil Benchmarks & Price Assessment Methodology October 4, 2012 - London Agenda Introduction and the role of benchmarks Platts price discovery process Global commodity markets outlook Platts MOC liquidity:

TRADING PLACES inside the oil futures market. Karen Matusic

TRADING PLACES inside the oil futures market Karen Matusic Nymex Facts Biggest commodities futures market Volumes account for more than 10 times world oil production Started as a milk and butter exchange

TRADING PLACES inside the oil futures market Karen Matusic Nymex Facts Biggest commodities futures market Volumes account for more than 10 times world oil production Started as a milk and butter exchange

the International Petroleum Exchange (IPE) in June 2001, which is response to the immense volatility that resulted from the oil price

in June 2001, which is response to the immense volatility that resulted from the oil price") ICE CRUDE OIL IntercontinentalExchange (ICE ) b e c a m e a c e n t e r f o r g l o b a l petroleum risk management and trading with its acquisition of the International Petroleum Exchange (IPE) in June

ICE CRUDE OIL IntercontinentalExchange (ICE ) b e c a m e a c e n t e r f o r g l o b a l petroleum risk management and trading with its acquisition of the International Petroleum Exchange (IPE) in June

Crude Oil Trading and

Exercises & Interactive Trading Simulation included! Crude Oil Trading and Price Risk Management Maximize Trading Profits and Manage Risk Effectively in a Volatile Market 18th 22nd May 2015, Kuala Lumpur,

Exercises & Interactive Trading Simulation included! Crude Oil Trading and Price Risk Management Maximize Trading Profits and Manage Risk Effectively in a Volatile Market 18th 22nd May 2015, Kuala Lumpur,

Argus response to consultation questions

Argus response to consultation questions Argus has decided to limit its response to those questions it considers most directly relevant to its business and the markets for which is provides post-trade

Argus response to consultation questions Argus has decided to limit its response to those questions it considers most directly relevant to its business and the markets for which is provides post-trade

The price of West Texas Intermediate crude oil on the New York Mercantile Exchange reached $39.99 on February 27, 2003.

29 III. THE PRICING OF CRUDE OIL Leon Hess, whose oil company made more than $200 million by trading oil futures during the Persian Gulf crisis... said he longs for the days when oil company barons could

29 III. THE PRICING OF CRUDE OIL Leon Hess, whose oil company made more than $200 million by trading oil futures during the Persian Gulf crisis... said he longs for the days when oil company barons could

Oil and Gas Prices. Oil and Gas Investor Summit London 17th-18th June 2014

Oil and Gas Prices Oil and Gas Investor Summit London 17th-18th June 2014 Oil Price Drowning in oil Economist, March 1999 $10 oil might actually be too optimistic. We may be heading for $5. Crude touches

Oil and Gas Prices Oil and Gas Investor Summit London 17th-18th June 2014 Oil Price Drowning in oil Economist, March 1999 $10 oil might actually be too optimistic. We may be heading for $5. Crude touches

Glossary of Energy Terms

Glossary of Energy Terms A API gravity A measure of the weight of hydrocarbons according to a scale established by the American Petroleum Institute. Crude oils with higher values are lighter and tend to

Glossary of Energy Terms A API gravity A measure of the weight of hydrocarbons according to a scale established by the American Petroleum Institute. Crude oils with higher values are lighter and tend to

SECTION TTT PART II C: DIFFERENTIALS CRUDE OIL AND REFINED PRODUCTS PART II: SPECIFIC STANDARD TERMS FOR SWAP FUTURES CONTRACTS:

SECTION TTT PART II C: DIFFERENTIALS CRUDE OIL AND REFINED TTT PART II: SPECIFIC STANDARD TERMS FOR SWAP FUTURES CONTRACTS: C. DIFFERENTIALS - CRUDE OIL AND REFINED 25. Monthly CFD - Monthly Brent CFD

SECTION TTT PART II C: DIFFERENTIALS CRUDE OIL AND REFINED TTT PART II: SPECIFIC STANDARD TERMS FOR SWAP FUTURES CONTRACTS: C. DIFFERENTIALS - CRUDE OIL AND REFINED 25. Monthly CFD - Monthly Brent CFD

or enters into a Futures contract (either on the IPE or the NYMEX) with delivery date September and pay every day up to maturity the margin

with delivery date September and pay every day up to maturity the margin") Cash-Futures arbitrage processes Cash futures arbitrage consisting in taking position between the cash and the futures markets to make an arbitrage. An arbitrage is a trade that gives in the future some

Cash-Futures arbitrage processes Cash futures arbitrage consisting in taking position between the cash and the futures markets to make an arbitrage. An arbitrage is a trade that gives in the future some

3/11/2015. Crude Oil Price Risk Management. Crude Oil Price Risk Management. Crude Oil Price Risk Management. Outline

1 Phoenix Energy Marketing Consultants Inc. 2 Outline What is crude oil price risk management? Why manage crude oil price risk? How do companies manage crude oil price risk? What types of deals do companies

1 Phoenix Energy Marketing Consultants Inc. 2 Outline What is crude oil price risk management? Why manage crude oil price risk? How do companies manage crude oil price risk? What types of deals do companies

Short-Term Energy Outlook Market Prices and Uncertainty Report

February 2016 Short-Term Energy Outlook Market Prices and Uncertainty Report Crude Oil Prices: The North Sea Brent front month futures price settled at $34.46/b on February 4 $2.76 per barrel (b) below

February 2016 Short-Term Energy Outlook Market Prices and Uncertainty Report Crude Oil Prices: The North Sea Brent front month futures price settled at $34.46/b on February 4 $2.76 per barrel (b) below

OIL MARKETS AND THEIR ANALYSIS IEA ENERGY TRAINING WEEK PARIS, APRIL 2013

OIL MARKETS AND THEIR ANALYSIS IEA ENERGY TRAINING WEEK PARIS, APRIL 2013 A (VERY) BRIEF OVERVIEW OF THE OIL INDUSTRY End consumers buy refined products (eg gasoline / diesel) Refineries buy crude oil

OIL MARKETS AND THEIR ANALYSIS IEA ENERGY TRAINING WEEK PARIS, APRIL 2013 A (VERY) BRIEF OVERVIEW OF THE OIL INDUSTRY End consumers buy refined products (eg gasoline / diesel) Refineries buy crude oil

An Anatomy of the Crude Oil Pricing System

An Anatomy of the Crude Oil Pricing System Bassam Fattouh 1 WPM 40 January 2011 1 Bassam Fattouh is the Director of the Oil and Middle East Programme at the Oxford Institute for Energy Studies; Research

An Anatomy of the Crude Oil Pricing System Bassam Fattouh 1 WPM 40 January 2011 1 Bassam Fattouh is the Director of the Oil and Middle East Programme at the Oxford Institute for Energy Studies; Research

OPEC s One-Way Option: Investors and the Price of Crude Oil. Philip K. Verleger, Jr. PKVerleger LLC

OPEC s One-Way Option: Investors and the Price of Crude Oil Philip K. Verleger, Jr. PKVerleger LLC Theme After ten years, commodities have finally become a suitable investment class for pension funds.

OPEC s One-Way Option: Investors and the Price of Crude Oil Philip K. Verleger, Jr. PKVerleger LLC Theme After ten years, commodities have finally become a suitable investment class for pension funds.

Oil Price Reporting Agencies. Report by. IEA, IEF, OPEC and IOSCO to G20 Finance Ministers, October 2011

Oil Price Reporting Agencies Report by IEA, IEF, OPEC and IOSCO to G20 Finance Ministers, October 2011 This Joint Report and the annexed report prepared by the consultants do not necessarily express the

Oil Price Reporting Agencies Report by IEA, IEF, OPEC and IOSCO to G20 Finance Ministers, October 2011 This Joint Report and the annexed report prepared by the consultants do not necessarily express the

Introduction to Equity Derivatives on Nasdaq Dubai NOT TO BE DISTRIUTED TO THIRD PARTIES WITHOUT NASDAQ DUBAI S WRITTEN CONSENT

Introduction to Equity Derivatives on Nasdaq Dubai NOT TO BE DISTRIUTED TO THIRD PARTIES WITHOUT NASDAQ DUBAI S WRITTEN CONSENT CONTENTS An Exchange with Credentials (Page 3) Introduction to Derivatives»

Introduction to Equity Derivatives on Nasdaq Dubai NOT TO BE DISTRIUTED TO THIRD PARTIES WITHOUT NASDAQ DUBAI S WRITTEN CONSENT CONTENTS An Exchange with Credentials (Page 3) Introduction to Derivatives»

Energy Risk Professional (ERP ) Examination. Practice Quiz 3: Financial Products

Examination. Practice Quiz 3: Financial Products") Energy Risk Professional (ERP ) Examination Practice Quiz 3: Financial Products TABLE OF CONTENTS Introduction...............................................................1 ERP Practice Quiz 3 Candidate

Energy Risk Professional (ERP ) Examination Practice Quiz 3: Financial Products TABLE OF CONTENTS Introduction...............................................................1 ERP Practice Quiz 3 Candidate

A Survey on Pricing of Asian Marker Crude Oil and Formation of Appropriate Market Prices 1

A Survey on Pricing of Asian Marker Crude Oil and Formation of Appropriate Market Prices 1 Yasuhiko Nagata, Senior Economist, Oil and Gas Strategy Group, Strategy and Industry Research Unit Sanae Kurita,

A Survey on Pricing of Asian Marker Crude Oil and Formation of Appropriate Market Prices 1 Yasuhiko Nagata, Senior Economist, Oil and Gas Strategy Group, Strategy and Industry Research Unit Sanae Kurita,

A Model for the Russian Energy Trading Market: An Assessment of the American Exchange Trading Experience

Alexander Gudkov A Model for the Russian Energy Trading Market: An Assessment of the American Exchange Trading Experience Introduction Alexander Gudkov*, Chief Executive Officer of Non-Commercial Partnership

Alexander Gudkov A Model for the Russian Energy Trading Market: An Assessment of the American Exchange Trading Experience Introduction Alexander Gudkov*, Chief Executive Officer of Non-Commercial Partnership

International Oil Pricing Mechanism and Analysis on Oil Price Fluctuation Reasons

International Oil Pricing Mechanism and Analysis on Oil Price Fluctuation Reasons By Mr. Wang Nengquan, Chief Economist Sinochem International Oil Company, Sinochem Corporation Hyatt Regency,Hangzhou,

International Oil Pricing Mechanism and Analysis on Oil Price Fluctuation Reasons By Mr. Wang Nengquan, Chief Economist Sinochem International Oil Company, Sinochem Corporation Hyatt Regency,Hangzhou,

Industry Informational Report. Exchange for Physicals (EFP)

") Industry Informational Report Exchange for Physicals (EFP) Background information on transaction structure, industry practice and applications prepared by RISK LIMITED CORPORATION All information contained

Industry Informational Report Exchange for Physicals (EFP) Background information on transaction structure, industry practice and applications prepared by RISK LIMITED CORPORATION All information contained

Crude Oil: What every investor needs to know By Andy Hecht

Crude Oil: What every investor needs to know By Andy Hecht Crude oil is considered by many to be the most important commodity market in the world. The value of crude oil affects almost every individual

Crude Oil: What every investor needs to know By Andy Hecht Crude oil is considered by many to be the most important commodity market in the world. The value of crude oil affects almost every individual

Manual for SOA Exam FM/CAS Exam 2.

Manual for SOA Exam FM/CAS Exam 2. Chapter 7. Derivative markets. c 2009. Miguel A. Arcones. All rights reserved. Extract from: Arcones Manual for the SOA Exam FM/CAS Exam 2, Financial Mathematics. Fall

Manual for SOA Exam FM/CAS Exam 2. Chapter 7. Derivative markets. c 2009. Miguel A. Arcones. All rights reserved. Extract from: Arcones Manual for the SOA Exam FM/CAS Exam 2, Financial Mathematics. Fall

(c) 2006-2014 Gary R. Evans. May be used for non-profit educational purposes only without permission of the author.

2006-2014 Gary R. Evans. May be used for non-profit educational purposes only without permission of the author.") The futures markets Introduction and Mechanics, using Natural Gas as the example (c) 2006-2014 Gary R. Evans. May be used for non-profit educational purposes only without permission of the author. Forward

The futures markets Introduction and Mechanics, using Natural Gas as the example (c) 2006-2014 Gary R. Evans. May be used for non-profit educational purposes only without permission of the author. Forward

Introduction to Futures Contracts

Introduction to Futures Contracts September 2010 PREPARED BY Eric Przybylinski Research Analyst Gregory J. Leonberger, FSA Director of Research Abstract Futures contracts are widely utilized throughout

Introduction to Futures Contracts September 2010 PREPARED BY Eric Przybylinski Research Analyst Gregory J. Leonberger, FSA Director of Research Abstract Futures contracts are widely utilized throughout

CALIFORNIA STATE TEACHERS RETIREMENT SYSTEM COMMODITY PORTFOLIO POLICY

CALIFORNIA STATE TEACHERS RETIREMENT SYSTEM COMMODITY PORTFOLIO POLICY INVESTMENT BRANCH NOVEMBER 2010 P. Commodity Portfolio Policy INTRODUCTION In accordance with the Investment Policy and Management

CALIFORNIA STATE TEACHERS RETIREMENT SYSTEM COMMODITY PORTFOLIO POLICY INVESTMENT BRANCH NOVEMBER 2010 P. Commodity Portfolio Policy INTRODUCTION In accordance with the Investment Policy and Management

Oil Trading. Simon Basey / November 28, 2013

Oil Trading Simon Basey / November 28, 2013 What does IST do? Markets BP s equity crude oil, NGLs and natural gas Offers risk management products to third parties Imports crude oil and other feedstocks

Oil Trading Simon Basey / November 28, 2013 What does IST do? Markets BP s equity crude oil, NGLs and natural gas Offers risk management products to third parties Imports crude oil and other feedstocks

Commodities Awareness Programme. Asia. Maycroft

Commodities Awareness Programme Asia Maycroft Training objectives The target audience for this training are the marketing or sales people of the bank. These people have direct contact with (potential)

Commodities Awareness Programme Asia Maycroft Training objectives The target audience for this training are the marketing or sales people of the bank. These people have direct contact with (potential)

(c) 2006-2014 Gary R. Evans. May be used for non-profit educational purposes only without permission of the author.

2006-2014 Gary R. Evans. May be used for non-profit educational purposes only without permission of the author.") The futures markets Introduction and Mechanics (c) 2006-2014 Gary R. Evans. May be used for non-profit educational purposes only without permission of the author. Forward contracts... Forward contracts

The futures markets Introduction and Mechanics (c) 2006-2014 Gary R. Evans. May be used for non-profit educational purposes only without permission of the author. Forward contracts... Forward contracts

The forward market for oil

By Patrick Campbell of the Bank s Foreign Exchange Division, Bjorn-Erik Orskaug of the Bank s International Finance Division and Richard Williams of the Bank s International Economic Analysis Division.

By Patrick Campbell of the Bank s Foreign Exchange Division, Bjorn-Erik Orskaug of the Bank s International Finance Division and Richard Williams of the Bank s International Economic Analysis Division.

Box 6 International Oil Prices: 2002-03

Annual Report 2002-03 International Oil Prices: 2002-03 Box 6 International Oil Prices: 2002-03 Notwithstanding the state of the world economy, characterised by sluggish growth in 2002, the world crude

Annual Report 2002-03 International Oil Prices: 2002-03 Box 6 International Oil Prices: 2002-03 Notwithstanding the state of the world economy, characterised by sluggish growth in 2002, the world crude

What drives crude oil prices?

What drives crude oil prices? An analysis of 7 factors that influence oil markets, with chart data updated monthly and quarterly Washington, DC U.S. Energy Information Administration Independent Statistics

What drives crude oil prices? An analysis of 7 factors that influence oil markets, with chart data updated monthly and quarterly Washington, DC U.S. Energy Information Administration Independent Statistics

Contract pricing disputes

Ted Greeno Caroline Kehoe Herbert Smith LLP 1. Introduction Contract pricing disputes in the energy industries typically arise in the context of long-term contracts under which an initial price agreed

Ted Greeno Caroline Kehoe Herbert Smith LLP 1. Introduction Contract pricing disputes in the energy industries typically arise in the context of long-term contracts under which an initial price agreed

Forward and Futures Markets. Class Objectives. Class Objectives

Forward and Futures Markets Peter Ritchken Kenneth Walter Haber Professor of Finance Case Western Reserve University Cleveland, Ohio, 44106 Peter Ritchken Forwards and Futures 1 Class Objectives Buying

Forward and Futures Markets Peter Ritchken Kenneth Walter Haber Professor of Finance Case Western Reserve University Cleveland, Ohio, 44106 Peter Ritchken Forwards and Futures 1 Class Objectives Buying

2015 Oil Outlook. january 21, 2015

MainStay Investments is pleased to provide the following investment insights from Epoch Investment Partners, Inc., a premier institutional manager and subadvisor to a number of MainStay Investments products.

MainStay Investments is pleased to provide the following investment insights from Epoch Investment Partners, Inc., a premier institutional manager and subadvisor to a number of MainStay Investments products.

Mechanics of the Futures Market. Andrew Wilkinson

Mechanics of the Futures Market Andrew Wilkinson Risk Disclosure Options and Futures are not suitable for all investors. The amount you may lose may be greater than your initial investment. Before trading

Mechanics of the Futures Market Andrew Wilkinson Risk Disclosure Options and Futures are not suitable for all investors. The amount you may lose may be greater than your initial investment. Before trading

Comments on Energy Markets

Comments on Energy Markets Philip K. Verleger, Jr. Volume I, No. 1 May 16, 27 Impacts of Passive Commodity Investors on Energy Markets and Energy Prices Wall Street has made commodities a new asset class.

Comments on Energy Markets Philip K. Verleger, Jr. Volume I, No. 1 May 16, 27 Impacts of Passive Commodity Investors on Energy Markets and Energy Prices Wall Street has made commodities a new asset class.

Manual for SOA Exam FM/CAS Exam 2.

Manual for SOA Exam FM/CAS Exam 2. Chapter 7. Derivatives markets. c 2009. Miguel A. Arcones. All rights reserved. Extract from: Arcones Manual for the SOA Exam FM/CAS Exam 2, Financial Mathematics. Fall

Manual for SOA Exam FM/CAS Exam 2. Chapter 7. Derivatives markets. c 2009. Miguel A. Arcones. All rights reserved. Extract from: Arcones Manual for the SOA Exam FM/CAS Exam 2, Financial Mathematics. Fall

Futures Contract Introduction

Futures Contract Introduction 1 The first futures exchange market was the Dojima Rice exchange in Japan in the 1730s, to meet the needs of samurai who being paid in rice and after a series of bad harvests

Futures Contract Introduction 1 The first futures exchange market was the Dojima Rice exchange in Japan in the 1730s, to meet the needs of samurai who being paid in rice and after a series of bad harvests

DME Oman Contracts - The Year in Review 2009

DME 2009 - The Year in Review 2009 was a positive year for the DME characterised by four significant developments. Firstly, liquidity has increased with trading volumes achieving a 69% year-on-year increase

DME 2009 - The Year in Review 2009 was a positive year for the DME characterised by four significant developments. Firstly, liquidity has increased with trading volumes achieving a 69% year-on-year increase

Return to Risk Limited website: www.risklimited.com. Overview of Options An Introduction

Return to Risk Limited website: www.risklimited.com Overview of Options An Introduction Options Definition The right, but not the obligation, to enter into a transaction [buy or sell] at a pre-agreed price,

Return to Risk Limited website: www.risklimited.com Overview of Options An Introduction Options Definition The right, but not the obligation, to enter into a transaction [buy or sell] at a pre-agreed price,

To What Extent is a Liquid LNG Hub in the Middle East Feasible?

96 WAGBARA: IS A LIQUID LNG HUB IN THE MIDDLE EAST FEASIBLE?: [2008] I.E.L.R. To What Extent is a Liquid LNG Hub in the Middle East Feasible? OBINDAH WAGBARA * Centre for Energy, Petroleum and Mineral

96 WAGBARA: IS A LIQUID LNG HUB IN THE MIDDLE EAST FEASIBLE?: [2008] I.E.L.R. To What Extent is a Liquid LNG Hub in the Middle East Feasible? OBINDAH WAGBARA * Centre for Energy, Petroleum and Mineral

THE ROLE OF WTI AS A CRUDE OIL BENCHMARK

THE ROLE OF WTI AS A CRUDE OIL BENCHMARK Prepared for: CME GROUP. Buenos Aires Calgary Dubai Houston London Los Angeles Moscow Singapore January 2010 K. D. Miller M. T. Chevalier J. Leavens CME Group

THE ROLE OF WTI AS A CRUDE OIL BENCHMARK Prepared for: CME GROUP. Buenos Aires Calgary Dubai Houston London Los Angeles Moscow Singapore January 2010 K. D. Miller M. T. Chevalier J. Leavens CME Group

Dated Brent: The pricing Benchmark for Asia-pacific Sweet crude Oil

MARKET ISSUES: OIL Dated Brent: The pricing Benchmark for Asia-pacific Sweet crude Oil May 2011 Foreword by Jorge Montepeque, Global Editorial Director of Market Reporting MARKET ISSUES: OIL Platts Dated

MARKET ISSUES: OIL Dated Brent: The pricing Benchmark for Asia-pacific Sweet crude Oil May 2011 Foreword by Jorge Montepeque, Global Editorial Director of Market Reporting MARKET ISSUES: OIL Platts Dated

Fundamentals of Futures and Options (a summary)

") Fundamentals of Futures and Options (a summary) Roger G. Clarke, Harindra de Silva, CFA, and Steven Thorley, CFA Published 2013 by the Research Foundation of CFA Institute Summary prepared by Roger G.

Fundamentals of Futures and Options (a summary) Roger G. Clarke, Harindra de Silva, CFA, and Steven Thorley, CFA Published 2013 by the Research Foundation of CFA Institute Summary prepared by Roger G.

Commodities and trade

Commodities and trade Crude oil Stig-Inge Gustafsson stig-inge.gustafsson@liu.se IEI-Energy Systems Commodities and trade p. 1/72 Important Hard facts about trading are not easily found. Your professor

Commodities and trade Crude oil Stig-Inge Gustafsson stig-inge.gustafsson@liu.se IEI-Energy Systems Commodities and trade p. 1/72 Important Hard facts about trading are not easily found. Your professor

How To Understand The Impact Of Price Risk On Commodity Trading

Global Commodities Forum Palais des Nations, Geneva 23-24 January 2012 Price risks & Volatility: Impact on Commodity Trading Companies By Mr. Samir Zreikat, Director, Dealigents Sàrl, Geneva "The views

Global Commodities Forum Palais des Nations, Geneva 23-24 January 2012 Price risks & Volatility: Impact on Commodity Trading Companies By Mr. Samir Zreikat, Director, Dealigents Sàrl, Geneva "The views

9 Hedging the Risk of an Energy Futures Portfolio UNCORRECTED PROOFS. Carol Alexander 9.1 MAPPING PORTFOLIOS TO CONSTANT MATURITY FUTURES 12 T 1)

") Helyette Geman c0.tex V - 0//0 :00 P.M. Page Hedging the Risk of an Energy Futures Portfolio Carol Alexander This chapter considers a hedging problem for a trader in futures on crude oil, heating oil and

Helyette Geman c0.tex V - 0//0 :00 P.M. Page Hedging the Risk of an Energy Futures Portfolio Carol Alexander This chapter considers a hedging problem for a trader in futures on crude oil, heating oil and

Room XXVI Palais des Nations Geneva, Switzerland. Oil Market Outlook. Eissa B. Alzerma Oil Price Analyst Petroleum Studies Department, OPEC

UNCTAD Multi-Year Expert Meeting on Commodities and Development 2013 Recent developments and new challenges in commodity markets, and policy options for commodity-based inclusive growth and sustainable

UNCTAD Multi-Year Expert Meeting on Commodities and Development 2013 Recent developments and new challenges in commodity markets, and policy options for commodity-based inclusive growth and sustainable

Rush hour in Kolkata (formerly Calcutta), India. Between 1990 and 2000, the number of motor vehicles per capita more than doubled in four

, India. Between 1990 and 2000, the number of motor vehicles per capita more than doubled in four") Rush hour in Kolkata (formerly Calcutta), India. Between 1990 and 2000, the number of motor vehicles per capita more than doubled in four Asia-Pacific nations: South Korea, the Philippines, India, and

Rush hour in Kolkata (formerly Calcutta), India. Between 1990 and 2000, the number of motor vehicles per capita more than doubled in four Asia-Pacific nations: South Korea, the Philippines, India, and

EI Data Service useful information: DSI01a A glossary of selected oil trading terms A B C D E F G H I J K L M N O P R S T U V W

EI Data Service useful information: DSI01a A glossary of selected oil trading terms A B C D E F G H I J K L M N O P R S T U V W 21 Day BFOE market: A forward market, trading in physical cargoes of 600,000

EI Data Service useful information: DSI01a A glossary of selected oil trading terms A B C D E F G H I J K L M N O P R S T U V W 21 Day BFOE market: A forward market, trading in physical cargoes of 600,000

Proxy Hedging of Commodities

Proxy Hedging of Commodities Hedging Gasoil Commitments in Related Futures Markets Master s Thesis in Advanced Economics and Finance 1 by Cecilie Viken and Marianne Solem Thorsrud November 16, 2013 Supervisors

Proxy Hedging of Commodities Hedging Gasoil Commitments in Related Futures Markets Master s Thesis in Advanced Economics and Finance 1 by Cecilie Viken and Marianne Solem Thorsrud November 16, 2013 Supervisors

Workshop Agenda Certified Commodities Analyst OBJECTIVE KEY AREAS FOCUS WHO SHOULD ATTEND. About your trainer UNIQUE MARKETS SPOT COMPLEX

markets are one of the more diverse markets in the capital markets arena and feature in investment portfolios in an increasing manner although traditionally they are traded in physicals taking in the whole

markets are one of the more diverse markets in the capital markets arena and feature in investment portfolios in an increasing manner although traditionally they are traded in physicals taking in the whole

Recent Oil-Market Developments: Causes and Implications

Recent Oil-Market Developments: Causes and Implications Statement of Professor Robert J. Weiner Professor of International Business, Public Policy & Public Administration, and International Affairs, George

Recent Oil-Market Developments: Causes and Implications Statement of Professor Robert J. Weiner Professor of International Business, Public Policy & Public Administration, and International Affairs, George

IntercontinentalExchange. Credit Suisse Financial Services Forum February 7, 2008

IntercontinentalExchange Credit Suisse Financial Services Forum February 7, 2008 Forward-Looking Statements Forward-Looking Statements This presentation may contain forward-looking statements made pursuant

IntercontinentalExchange Credit Suisse Financial Services Forum February 7, 2008 Forward-Looking Statements Forward-Looking Statements This presentation may contain forward-looking statements made pursuant

IPE GAS OIL FUTURES CONTRACT SPECIFICIATIONS

IPE GAS OIL FUTURES CONTRACT SPECIFICIATIONS BACKGROUND The IPE Gas Oil futures contract is designed to provide users with an effective hedging instrument and trading opportunities. Its underlying physical

IPE GAS OIL FUTURES CONTRACT SPECIFICIATIONS BACKGROUND The IPE Gas Oil futures contract is designed to provide users with an effective hedging instrument and trading opportunities. Its underlying physical

Energy Value Chains. What is a Value Chain?

Energy s Overview of Fundamentals Center for Energy Economics, UT-Austin. No reproduction, distribution or attribution without permission. 1 What is a? The process of linking specific functions from input

Energy s Overview of Fundamentals Center for Energy Economics, UT-Austin. No reproduction, distribution or attribution without permission. 1 What is a? The process of linking specific functions from input

Control over oil markets, once the province of the major

How B Y P HILIP K. VERLEGER, JR. Wall Street Controls Oil And how OPEC will be the fall guy for $90 oil. THE MAGAZINE OF INTERNATIONAL ECONOMIC POLICY 888 16th Street, N.W. Suite 740 Washington, D.C. 006

How B Y P HILIP K. VERLEGER, JR. Wall Street Controls Oil And how OPEC will be the fall guy for $90 oil. THE MAGAZINE OF INTERNATIONAL ECONOMIC POLICY 888 16th Street, N.W. Suite 740 Washington, D.C. 006

General Forex Glossary

General Forex Glossary A ADR American Depository Receipt Arbitrage The simultaneous buying and selling of a security at two different prices in two different markets, with the aim of creating profits without

General Forex Glossary A ADR American Depository Receipt Arbitrage The simultaneous buying and selling of a security at two different prices in two different markets, with the aim of creating profits without

ECF Case. information about prices, the North Sea Brent Crude Oil market, the European Commission

Case 1:13-cv-07089-ALC-SN Document 1 Filed 10/04/13 Page 1 of 85 UNITED STATES DISTRICT COURT SOUTHERN DISTRICT OF NEW YORK KEVIN McDONNELL, ANTHONY INSINGA, ROBERT MICHIELS and JOHN DEVIVO, on behalf

Case 1:13-cv-07089-ALC-SN Document 1 Filed 10/04/13 Page 1 of 85 UNITED STATES DISTRICT COURT SOUTHERN DISTRICT OF NEW YORK KEVIN McDONNELL, ANTHONY INSINGA, ROBERT MICHIELS and JOHN DEVIVO, on behalf

Chapter 10 Forwards and Futures

Chapter 10 Forwards and Futures Road Map Part A Introduction to finance. Part B Valuation of assets, given discount rates. Part C Determination of risk-adjusted discount rate. Part D Introduction to derivatives.

Chapter 10 Forwards and Futures Road Map Part A Introduction to finance. Part B Valuation of assets, given discount rates. Part C Determination of risk-adjusted discount rate. Part D Introduction to derivatives.

Commodities Lifecycle Events White Paper

Commodities Lifecycle Events White Paper Section I: Introduction... 2 Section II: Summary of Commodities Lifecycle Events... 2 Section III: Current State of Lifecycle Event Processing... 7 Section IV:

Commodities Lifecycle Events White Paper Section I: Introduction... 2 Section II: Summary of Commodities Lifecycle Events... 2 Section III: Current State of Lifecycle Event Processing... 7 Section IV:

The current decoupling of oil and gas prices, where prices of the two commodities move in different directions, negatively affects Gazprom s export

The current decoupling of oil and gas prices, where prices of the two commodities move in different directions, negatively affects Gazprom s export sales by driving up oil-indexed gas prices and leading

The current decoupling of oil and gas prices, where prices of the two commodities move in different directions, negatively affects Gazprom s export sales by driving up oil-indexed gas prices and leading

Whither Oil Prices and Volatility?

OIL PRICE VOLATILITY What Do We Know? Robert J. Weiner Professor of International Business, Public Policy & Public Administration, and International Affairs, George Washington University Membre Associé,,

OIL PRICE VOLATILITY What Do We Know? Robert J. Weiner Professor of International Business, Public Policy & Public Administration, and International Affairs, George Washington University Membre Associé,,

PRICE PATTERN IN FUTURES MARKET

PRICE PATTERN IN FUTURES MARKET Objective This part explains the concept of Basis which is the price difference between an underlying asset and its future. How basis can be used for effectively hedging

PRICE PATTERN IN FUTURES MARKET Objective This part explains the concept of Basis which is the price difference between an underlying asset and its future. How basis can be used for effectively hedging

Best ETF Trading Practices

Presented by QQQ TM Also inside: 2 Why best trading practices matter 3 The value of a pretrade analysis 4 Evaluating ETFs for trading efficiency 5 Mechanics of ETF trades 5 Relationships between ETF trading

Presented by QQQ TM Also inside: 2 Why best trading practices matter 3 The value of a pretrade analysis 4 Evaluating ETFs for trading efficiency 5 Mechanics of ETF trades 5 Relationships between ETF trading

Risk Disclosure Statement for CFDs on Securities, Indices and Futures

Risk Disclosure on Securities, Indices and Futures RISK DISCLOSURE STATEMENT FOR CFDS ON SECURITIES, INDICES AND FUTURES This disclosure statement discusses the characteristics and risks of contracts for

Risk Disclosure on Securities, Indices and Futures RISK DISCLOSURE STATEMENT FOR CFDS ON SECURITIES, INDICES AND FUTURES This disclosure statement discusses the characteristics and risks of contracts for

offering a comprehensive range of investment products and services.

Linear Investments is a global investment manager offering comprehensive range of Investments is aaglobal investment manager investment products and services Linear offering a comprehensive range of investment

Linear Investments is a global investment manager offering comprehensive range of Investments is aaglobal investment manager investment products and services Linear offering a comprehensive range of investment

How Do Energy Suppliers Make Money? Copyright 2015. Solomon Energy. All Rights Reserved.

Bills for electricity and natural gas can be a very high proportion of a company and household budget. Accordingly, the way in which commodity prices are set is of material importance to most consumers.

Bills for electricity and natural gas can be a very high proportion of a company and household budget. Accordingly, the way in which commodity prices are set is of material importance to most consumers.

THE GLOBAL SOURCE FOR COMMODITIES KOCH SUPPLY & TRADING

THE GLOBAL SOURCE FOR COMMODITIES KOCH SUPPLY & TRADING KOCH SUPPLY & TRADING: CAPABILITIES Refined Products Crude Oil Global crude oil markers (WTI, Brent, Dubai) and grades of oil priced off these markers

THE GLOBAL SOURCE FOR COMMODITIES KOCH SUPPLY & TRADING KOCH SUPPLY & TRADING: CAPABILITIES Refined Products Crude Oil Global crude oil markers (WTI, Brent, Dubai) and grades of oil priced off these markers

Price formation in liberalised gas markets. Patrick Heren Heren Energy Ltd

Price formation in liberalised gas markets Patrick Heren Heren Energy Ltd Brief advertisement Publishers of daily gas and power market reports, the Heren Index and European Gas Markets newsletter. Independent

Price formation in liberalised gas markets Patrick Heren Heren Energy Ltd Brief advertisement Publishers of daily gas and power market reports, the Heren Index and European Gas Markets newsletter. Independent

Trading in Treasury Bond Futures Contracts and Bonds in Australia

Trading in Treasury Bond Futures Contracts and Bonds in Australia Belinda Cheung* Treasury bond futures are a key financial product in Australia, with turnover in Treasury bond futures contracts significantly

Trading in Treasury Bond Futures Contracts and Bonds in Australia Belinda Cheung* Treasury bond futures are a key financial product in Australia, with turnover in Treasury bond futures contracts significantly

CFD Trading Guide Instrument Information Section 2 May 2010

CFD Trading Guide Instrument Information Section 2 May 2010 Contents 1 Financing and Margin...1 2 Shares...2 2.1 Trading Hours... 2 2.1.1 Normal Trading Hours...2 2.1.2 Extended Trading Hours...2 2.2 Placing

CFD Trading Guide Instrument Information Section 2 May 2010 Contents 1 Financing and Margin...1 2 Shares...2 2.1 Trading Hours... 2 2.1.1 Normal Trading Hours...2 2.1.2 Extended Trading Hours...2 2.2 Placing

IPE Natural Gas futures Contract October 13, 2005

IPE Natural Gas futures Contract October 13, 2005 Copyright Intercontinental Exchange, Inc. 2005. All Rights Reserved. IPE Natural Gas futures Contract Background The IPE Natural Gas futures contract enables

IPE Natural Gas futures Contract October 13, 2005 Copyright Intercontinental Exchange, Inc. 2005. All Rights Reserved. IPE Natural Gas futures Contract Background The IPE Natural Gas futures contract enables

Options Strategy for Professional Clients

Options Strategy for Professional Clients Optimise is an options strategy which uses market volatility selling FTSE100 cash settled options contracts. Premium is taken from the market on options that are

Options Strategy for Professional Clients Optimise is an options strategy which uses market volatility selling FTSE100 cash settled options contracts. Premium is taken from the market on options that are

Contracts for Difference (CFDs)

") Contract for Difference (CFDs) and FCA Disclosure Requirements What are Contract for Difference (CFDs) CFDs (also known as Synthetic Equity Swaps (SES)) are Over the Counter (OTC) transactions which allow

Contract for Difference (CFDs) and FCA Disclosure Requirements What are Contract for Difference (CFDs) CFDs (also known as Synthetic Equity Swaps (SES)) are Over the Counter (OTC) transactions which allow

Risks of Investments explained

Risks of Investments explained Member of the London Stock Exchange .Introduction Killik & Co is committed to developing a clear and shared understanding of risk with its clients. The categories of risk

Risks of Investments explained Member of the London Stock Exchange .Introduction Killik & Co is committed to developing a clear and shared understanding of risk with its clients. The categories of risk

CommSeC CFDS: IntroDuCtIon to CommoDItIeS

CommSec CFDs: Introduction to Commodities We re here to help To find out more, call us on 1300 307 853, from 8am Monday to 6am Saturday, email us at cfds@commsec.com.au or visit our website at commsec.com.au.

CommSec CFDs: Introduction to Commodities We re here to help To find out more, call us on 1300 307 853, from 8am Monday to 6am Saturday, email us at cfds@commsec.com.au or visit our website at commsec.com.au.

ORDER EXECUTION POLICY

ORDER EXECUTION POLICY General provisions 1. Forex Rally will take all reasonable steps and measures in order to obtain the best quality of service for its Clients. 2. The herein Order Execution Policy

ORDER EXECUTION POLICY General provisions 1. Forex Rally will take all reasonable steps and measures in order to obtain the best quality of service for its Clients. 2. The herein Order Execution Policy

Obligatory transactions on a specified date at a predetermined price

Obligatory transactions on a specified date at a predetermined price DERIVATIVE MARKET Bond Derivatives Bond Futures www.jse.co.za Johannesburg Stock Exchange A bond future is a contractual obligation

Obligatory transactions on a specified date at a predetermined price DERIVATIVE MARKET Bond Derivatives Bond Futures www.jse.co.za Johannesburg Stock Exchange A bond future is a contractual obligation

Program for Energy Trading, Derivatives and Risk Management by Kyos Energy Consulting, dr Cyriel de Jong Case studies

Program for Energy Trading, Derivatives and Risk Management by Kyos Energy Consulting, dr Cyriel de Jong Case studies We use cases throughout its course in various forms. The cases support the application

Program for Energy Trading, Derivatives and Risk Management by Kyos Energy Consulting, dr Cyriel de Jong Case studies We use cases throughout its course in various forms. The cases support the application

Trading and Shipping

Trading and Shipping Trading and Shipping TRT / OMT TRT / MTP Oil Markets and Trading 3 Days To provide a better understanding of the structure of the markets, the uses and the impacts of physical and

Trading and Shipping Trading and Shipping TRT / OMT TRT / MTP Oil Markets and Trading 3 Days To provide a better understanding of the structure of the markets, the uses and the impacts of physical and