Exchanges go live: Early trends in exchange dynamics

|

|

|

- Basil Aron Gilbert

- 8 years ago

- Views:

Transcription

1 Exchanges go live: Early trends in exchange dynamics After three and a half years of forecasting, data is now emerging from the individual exchanges that can inform the likely impact of the Affordable Care Act. 1 The McKinsey Center for U.S. Health System Reform has developed a database covering more than 21,000 unique qualified health plans filed on the public exchanges in all 501 rating areas in the 50 states and District of Columbia. This Intelligence Brief describes five trends emerging from the first few weeks of exchange data: The competitive landscape in the individual market has changed considerably, given the number of new entrants These new entrants are pricing competitively, but are not usually price leaders Premium levels vary considerably, both within and across markets Zero-net-premium products are widely available Managed-care-like designs are re-emerging, particularly among the new entrants We based our analysis of each of these trends on data accessed directly from the public exchanges as of October 15 th, The situation remains dynamic, however, as there have been widely acknowledged challenges with the exchanges. Data releases are being refreshed regularly as the public exchanges resolve technical issues, and all analyses are contingent upon the accuracy of the information released. Accordingly, the trends described in this Intelligence Brief should be considered as directional indicators of how the public exchanges are likely unfolding, and not as conclusive proof of industry changes. Nonetheless, the trends can begin to inform both near-term and longer-term strategic actions. 1 This analysis focuses on individual-exchange products, because they are the only plans that enable income-eligible consumers to receive the federal premium and cost-sharing subsidies. Complete off-exchange filings may not be available in every state until the end of 2013, and thus they have not been included in the analysis. 2 All data was obtained directly from the public exchanges over the first two weeks of October, by shopping directly on all exchanges as well as through datasets released by the federal exchange.

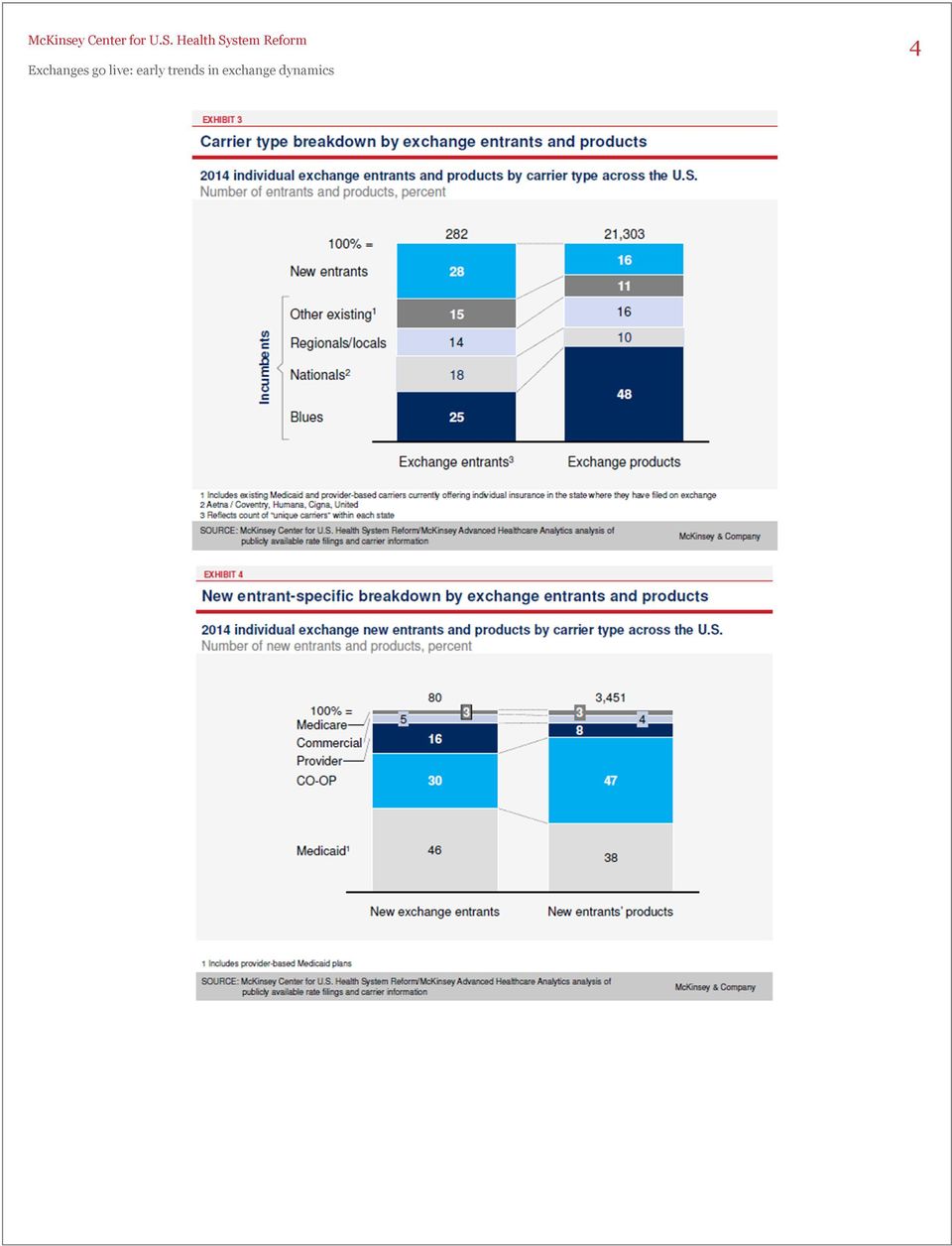

2 2 The competitive landscape in the individual market has changed considerably, given the number of new entrants The competitor composition of the individual market has changed. Two-thirds of the unique payors 3 offering individual plans in 2012 have filed on the public exchanges in the same states. Yet 80 new entrants (defined as carriers participating in the individual market for the first time in a given state) have filed on those same exchanges (Exhibit 1). The intensity of post-reform competition varies greatly across the country. The number of carriers in any state offering products on the public exchanges is as low as 1 and as high as 17 (Exhibit 2). Similar variability exists among the rating areas within a state; the number of carriers in individual rating areas ranges from 1 to Our calculations are based on the number of carriers that offer plans in each state. As a result, a national carrier that offered plans in 12 states in 2012 would be counted as 12 unique payors in that year. In addition, a carrier that offers 2014 exchange plans in 4 rating areas in a state is counted as a single entrant in that state.

.")

3 3 Nationwide, new entrants represent 28 percent of all carriers on the exchanges and 16 percent of all products offered. The new entrants include a range of organizations, as shown in Exhibits 3-4. Medicaid carriers (organizations previously providing plans to Medicaid enrollees and now offering commercial coverage on the exchanges) are the most common type of new entrant. However, consumer-operated and oriented plans (CO-OPs) are offering the most products of all new entrants in the market. Among the incumbent payors, Blue Cross Blue Shield plans are the most active on the exchanges. They comprise 25 percent of all exchange participants and offer products in all but three states and all but five percent of the rating areas. National insurers 4 (i.e., Aetna/Coventry, Humana, Cigna, UnitedHealth) comprise 18 percent of all participants. They offer plans in 28 states and 38 percent of the rating areas. The different approaches taken by the Blues versus the national carriers are reflected in the number of products they are offering. Blues plans account for almost half of all exchange products, while national carriers account for less than 10 percent of all products. 4 The term national insurers refers to all commercial health insurers that have a presence in more than four states and have filed on the exchanges. Anthem, HCSC, and Regence are excluded because they are classified as Blues plans.

4 4

5 5 New entrants are pricing competitively, but are not usually price leaders Across the country, about half the new entrants plans are priced below the median in their respective markets. 5 Furthermore, 31 percent of the new entrants plans are within 10 percent of the lowest-price plan (the price range our research suggests most consumers are willing to consider 6 ). The new entrants rates are consistent with incumbents rates, with 47 percent of incumbents plans priced below the median and 33 percent within 10 percent of the lowest-price plan (Exhibit 5). However, incumbents are more likely to be price leaders. Even in rating areas where new entrants are present, incumbents are offering 66 percent of the lowest-price products in each metal tier. Across markets, Blues plans are the most common price leaders, offering 42 percent of all lowest-price products across the U.S. While national insurers are competing in fewer markets (38 percent of rating areas covering slightly more than half of non-elderly uninsured 7 ), they are more competitive in those states, offering the lowest-price product 56 percent of the time. Among new entrants, CO-OPs have emerged as price leaders, offering 37 percent of lowest-price products in the 22 states where CO-OPs are present. 5 This percentage is lower than the 66 percent we reported in our September Intelligence Brief, as the September estimate was based on available data of plans filed in only eight states. 6 In our exchange simulations, we observed the lowest priced products and products priced within 10-15% of the lowestprice product netting a considerable share of lives, especially in lower metal tiers. However, strong brands were still able to offset the price advantage and retain strong share in many geographies. 7 Non-elderly uninsured defined as those over 100 percent FPL in non-medicaid expansion states and over 138 percent FPL in Medicaid expansion states.

6 6 Although these pricing trends are relevant at a cross-market level, plan pricing varies significantly across rating areas, as we discuss below. In one-fourth of the largest cities with new entrants, a majority of the new entrants products 100 percent in Los Angeles, 86 percent in Milwaukee, and 67 percent in Indianapolis, for example are priced within 10 percent of the lowest-price product. Premium levels vary considerably, both within and across markets In most rating areas, large variations in pricing are present within and across metal tiers. Close to half of all non-elderly uninsured individuals 7 are offered premiums in their rating areas that vary by over 50 percent within a single tier across bronze, silver, and gold, and close to one-fifth of uninsured are seeing this type of variation in platinum (Exhibit 6). There may be several potential factors contributing to these pricing differences within a given rating area, including degree of network narrowing, different costs of care, and different assumptions about risk pool (i.e., morbidity of expected membership and impact of risk adjustors/re-insurance). Of these, narrow networks likely represent the largest sustainable price-lowering action carriers are taking in There appears to be some correlation between pricing and metal tier. In almost all rating areas, the lowest-price product in one tier is less expensive than the lowest-price product in the tier above it. However, there is often considerable overlap within single rating areas in the range of prices offered in each tier and across tiers. As a result, a 40-year-old single person can buy a bronze, silver, or gold plan for the same price in 43 percent of rating areas. Similarly, in 20 percent of the rating areas offering a platinum product, a 40-year-old can purchase a bronze, silver, gold, or platinum plan at the same price. In Phoenix,

7 7 Arizona, for example, a 40-year-old who is willing to spend $249 per month could find at least one product at that price in each metal tier. The variation in pricing across rating areas is also considerable. Among bronze plans, for example, the least-expensive product for a 40-year-old single person is $115 per month in Minnesota but $403 in Colorado (this Colorado product actually costs more than the leastexpensive platinum plans in almost 80 percent of the rating areas offering platinum products). Although underlying differences in the cost of care across markets may explain part of the variation in premium levels across markets, they unlikely explain all of it. Considerably more data and a full multivariate analysis will be required to isolate the specific independent variables affecting the pricing dispersion across markets. 8 Zero-net-premium products are widely available Across the U.S., 6 to 7 million people may be eligible for a zero-net-premium bronze plan and ~1 million may be eligible for a zero-net-premium silver plan. This estimate includes uninsured as well as currently individually insured, with uninsured comprising the majority (~85 percent) (Exhibit 7). In a zero-net-premium plan, the federal premium subsidy covers the entire premium (many people still face co-payments for services delivered). The subsidy amount is calculated as the difference in the price of the second-lowest silver plan in that rating area and the maximum premium the person is expected to pay. This maximum is a function of the person s income and family size. Persons with income up to 400 percent of the federal poverty level are eligible for a subsidy. 8 McKinsey Reform Center plans to conduct and publish this multivariate analysis later this year.

.")

8 8 To illustrate, consider a 42 year old single female living in Jackson, Mississippi earning $23,000 a year (200 percent of the federal poverty level). For her income level, the maximum premium she is expected to pay is 6.3 percent of her income, or $121 a month. Because the second-lowest silver plan available in her rating area is $425, the federal premium subsidy for her is $304. If she chooses to buy the lowest-price bronze product (priced at $236), the net premium for her is zero because it is priced below her subsidy. While the premium increases directly with a person s age, higher premium products increase at a greater rate as age increases (Exhibit 8). 9 Accordingly, older people are eligible for larger subsidies than are younger people, increasing the likelihood that they can obtain a zero-net-premium product. Similarly, people with lower incomes are more likely to be eligible for zero-net-premium products, because subsidy levels increase as income decreases. The number of zero-net-premium products a person has available to them depends on his/her subsidy amount, the number of plans priced below the second-lowest silver plan in his/her rating area, and the differences in price among those plans. The greater the price differential between the second-lowest silver plan and either the lowest silver or lowest bronze plan, the more likely it is that the person can find one or more zero-net-premium products. Because premium levels vary widely across rating areas, the availability of zeronet-premium products also varies widely. For example, our research suggests that about 40 9 As age increases, higher priced products increase at the same rate as lower priced products, according to the HHS standard age curve for 2014 individual market premiums (except in NY and VT). However, while the rate of increase is the same, the absolute dollar difference is different, resulting in higher subsidies for higher-priced products, since subsidies are calculated by a flat dollar amount regardless of age.

, the net premium for her is zero because it is priced below her subsidy.")

9 9 percent of the non-elderly uninsured 7 in Missouri are eligible for zero-net-premium bronze plans, compared to only 2 percent of the uninsured in New Jersey. It is not yet known how many of those eligible for zero-net-premium bronze plans will opt to buy a bronze plan rather than a silver plan, especially since almost all of these individuals would be eligible for a cost-sharing subsidy 10 if they bought a silver plan. 11 At present, zero-net-premium silver plans are available to ~1 million individuals, where eligible individuals can obtain a plan requiring no premiums yet containing cost-sharing subsidies, resulting in limited out-of-pocket costs. Managed-care-like designs are re-emerging, particularly among the new entrants A more diverse set of benefit designs is emerging. Close to 60 percent of all exchange products incorporate managed-care-like benefit designs, in the form of either health maintenance organizations (HMOs) or exclusive provider organizations (EPOs). New entrants offer these products more often than incumbents, with 67 percent of new entrants plans HMOs or EPOs, compared with 57 percent of incumbents plans (Exhibit 9). Of new entrants, Medicaid entrants almost exclusively offer managed-care-like plans, with close to 90 percent of products structured as HMOs. CO-OPs and provider-based entrants are each offering ~50 percent HMOs or EPOs. 10 Cost-sharing subsidies offset an individual s total out-of-pocket spending incurred when using health services (outside of their monthly premiums), including co-payments, co-insurance, and deductibles. 11 Individuals earning up to $28,725 a year (250 percent of the federal poverty level) are eligible for cost-sharing subsidies, but only if they buy a silver plan.

10 10 Managed-care-like features are widely believed to be a way to hold down costs and thus permit payors to offer lower premiums. Our analysis of exchange plan benefit designs shows some correlation with premium levels: HMO and EPO plans represent 69 percent of all lowest-price products in markets where offered. In addition, of all product offerings within each benefit design type, HMO and EPO plans have 34 percent of products priced within 10 percent of the lowest-price plan, compared with 31 percent of all PPO and POS plans. This latter trend reveals that beyond the more traditional managed-care-like benefit designs, even less restrictive designs are beginning to impose some restrictions as a way to keep premiums low. Analysis of more data about the provider networks affiliated with each exchange offering and benefit design type will reveal further trends regarding how payors have utilized network design to achieve lower rates. The actuarial assumptions behind insurers 2014 exchange filings are beginning to show the degree to which network has been used as a cost-reduction lever. For example, in one rating area, some payors optimized their networks to reduce premiums by as much as 24 percent (Exhibit 10). We need to obtain a deeper understanding of the trade-offs consumers face such as how they choose among managed-care-like features, network breadth, and price, and how willing they are to make trade-offs among these features. 12 Although more restrictive features appear to be a way to meet consumer demand for low price points, it is yet unclear how consumers will actually respond to these features over the long term. 12 McKinsey Reform Center plans to conduct and publish an analysis of exchange network trends in November.

11 11 The early trends presented in this Intelligence Brief provide an emerging view of the competitive landscape unfolding on the public exchanges across the United States. However, these trends are directional indicators only. Given the dynamic nature of the exchanges and the data emerging from them, we need to conduct additional analysis to better understand the extent to which competitive dynamics are changing. The Reform Center is continuing to analyze all product offerings across the country to develop a comprehensive perspective on exchange dynamics; we will release additional results publicly in the form of white papers over the coming months. Ananya Banerjee, Erica Coe, and Jim Oatman

12 12 Appendix Additional background on the underlying research The analysis supporting this Intelligence Brief is informed by a new McKinsey Health Systems and Services Practice asset that has been developed jointly by the Center for U.S. Health System Reform and McKinsey Advance Healthcare Analytics (MAHA). Instead of estimates and projections, this tool offers a real-time view of what has actually been filed on the exchanges over 21,000 qualified health plans for plan year The Reform Center/MAHA tool can compare individual and small-group rate filings, pre- to post-aca trends, pricing across plan types and actuarial value tiers by consumer characteristics, predictions of market share based on filings and consumer-predicted dynamics, and more. Specific analyses are available upon request from the Reform Center/MAHA team; we look forward to helping our clients achieve success in the post-aca market through the use of data-driven analysis on specific market trends. Please contact reformcenter@mckinsey.com with any inquiries. To access the Reform Center s September Intelligence Brief, Emerging exchange dynamics: Temporary turbulence or sustainable market disruption?, go to: Glossary of health care terms Consumer-operated and oriented plan (CO-OP) a new entrant that is a recipient of federal CO-OP grant funding and is not a prior commercial carrier EPO an exclusive provider organization is a plan model that is similar to an HMO. It provides no coverage for any services delivered by out-of-network providers or facilities except in emergency or urgent care situations; however, it generally does not require members to use a primary care physician for in-network referrals Existing entrant also referred to as incumbent, an insurance carrier that offered individual insurance in the respective state s individual market for plan year 2013, based on 2012 SNL data Gatekeeper an approach that limits access to healthcare services in some way (e.g., by requiring referrals through a primary care provider) HMO a health maintenance organization is a plan model centered around a primary care physician who acts as gatekeeper to other services and referrals; it provides no coverage for out-of-network services except in emergency or urgent-care situations Medicaid new entrant a new entrant that offered only Medicaid insurance in the past PMPM per member per month PPO a preferred provider organization is a plan model that allows members to see doctors and get services that are not part of a network, but out-of-network services require a higher copayment

13 13 POS a point-of-service plan is hybrid of an HMO model and a PPO model; it is an openaccess plan model that assigns members a primary care physician and provides partial coverage for out-of-network services Provider entrant a new entrant that operates as a provider/health system today October 2013 Copyright 2013 McKinsey & Company CONFIDENTIAL AND PROPRIETARY Any use of this material without specific permission of McKinsey & Company is strictly prohibited.

Hospital networks: Configurations on the exchanges and their impact on premiums

Hospital networks: Configurations on the exchanges and their impact on premiums The configuration of hospital networks is changing on the new public health exchanges and, in many cases, having a direct

Hospital networks: Configurations on the exchanges and their impact on premiums The configuration of hospital networks is changing on the new public health exchanges and, in many cases, having a direct

Hospital networks: Evolution of the configurations on the 2015 exchanges

Hospital networks: Evolution of the configurations on the 2015 exchanges Now that the 2015 open enrollment period (OEP) has ended, we have updated our network database to include all networks offered on

Hospital networks: Evolution of the configurations on the 2015 exchanges Now that the 2015 open enrollment period (OEP) has ended, we have updated our network database to include all networks offered on

Emerging exchange dynamics: Temporary turbulence or sustainable market disruption?

Emerging exchange dynamics: Temporary turbulence or sustainable market disruption? INTRODUCTION Health insurance carriers in every state have now filed their proposed product offerings for the public exchanges

Emerging exchange dynamics: Temporary turbulence or sustainable market disruption? INTRODUCTION Health insurance carriers in every state have now filed their proposed product offerings for the public exchanges

Competition and choice are increasing

Intelligence Brief 2015 OEP: Emerging trends in the individual exchanges The 2015 open enrollment period (OEP) begins in about seven weeks. To develop a preliminary understanding of how it is likely to

Intelligence Brief 2015 OEP: Emerging trends in the individual exchanges The 2015 open enrollment period (OEP) begins in about seven weeks. To develop a preliminary understanding of how it is likely to

Understanding Private Health Insurance Plan Choices and Provider Networks

Understanding Private Health Insurance Plan Choices and Provider Networks Definitions Deductible Out-of-Pocket-Maximum Embedded Deductible Aggregate Deductible Networks PPO EPO HMO POS - HDHP HSA Catastrophic

Understanding Private Health Insurance Plan Choices and Provider Networks Definitions Deductible Out-of-Pocket-Maximum Embedded Deductible Aggregate Deductible Networks PPO EPO HMO POS - HDHP HSA Catastrophic

Health Insurance for PLTS Students. KAREN MARRINER, MBA Licensed Insurance Agent KM Consulting

Health Insurance for PLTS Students KAREN MARRINER, MBA Licensed Insurance Agent KM Consulting True or False? Individuals can be charged more for their health insurance for having medical conditions. All

Health Insurance for PLTS Students KAREN MARRINER, MBA Licensed Insurance Agent KM Consulting True or False? Individuals can be charged more for their health insurance for having medical conditions. All

Insights AdvocateCare Health Insurance Exchanges

Insights AdvocateCare Physician Edition April 16, 2013 Executive Summary (HIX, also called Health Insurance Marketplace) a key provision of The Patient Protection and Affordable Care Act (ACA, Affordable

Insights AdvocateCare Physician Edition April 16, 2013 Executive Summary (HIX, also called Health Insurance Marketplace) a key provision of The Patient Protection and Affordable Care Act (ACA, Affordable

List of Insurance Terms and Definitions for Uniform Translation

Term actuarial value Affordable Care Act allowed charge Definition The percentage of total average costs for covered benefits that a plan will cover. For example, if a plan has an actuarial value of 70%,

Term actuarial value Affordable Care Act allowed charge Definition The percentage of total average costs for covered benefits that a plan will cover. For example, if a plan has an actuarial value of 70%,

Connecticut Health Insurance Exchange. June 2012 [SHOP BRIEFING] An overview of the Small Business Health Options Program (SHOP) Exchange

![Connecticut Health Insurance Exchange. June 2012 [SHOP BRIEFING] An overview of the Small Business Health Options Program (SHOP) Exchange](/thumbs/32/15645614.jpg "Connecticut Health Insurance Exchange. June 2012 [SHOP BRIEFING] An overview of the Small Business Health Options Program (SHOP) Exchange") Connecticut Health Insurance Exchange June 2012 [SHOP BRIEFING] An overview of the Small Business Health Options Program (SHOP) Exchange Overview The federal health care reform law directs states to set

Connecticut Health Insurance Exchange June 2012 [SHOP BRIEFING] An overview of the Small Business Health Options Program (SHOP) Exchange Overview The federal health care reform law directs states to set

Choosing the Best Plan for You: A Tool for Purchasing Coverage in the Health Insurance Exchange

Choosing the Best Plan for You: A Tool for Purchasing Coverage in the Health Insurance Exchange The Affordable Care Act (ACA) makes health insurance available to nearly all Americans and the law requires

Choosing the Best Plan for You: A Tool for Purchasing Coverage in the Health Insurance Exchange The Affordable Care Act (ACA) makes health insurance available to nearly all Americans and the law requires

Exchange 101. August 2013

Exchange 101 August 2013 455430 27517 Penalties for individuals 2017 and beyond: Annual adjustments 2016: Greater of $695 or 2.5% of taxable income 2015: Greater of $325 or 2% of taxable income 2014: Greater

Exchange 101 August 2013 455430 27517 Penalties for individuals 2017 and beyond: Annual adjustments 2016: Greater of $695 or 2.5% of taxable income 2015: Greater of $325 or 2% of taxable income 2014: Greater

The Health Benefit Exchange and the Commercial Insurance Market

The Health Benefit Exchange and the Commercial Insurance Market Overview The federal health care reform law directs states to set up health insurance marketplaces, called Health Benefit Exchanges, that

The Health Benefit Exchange and the Commercial Insurance Market Overview The federal health care reform law directs states to set up health insurance marketplaces, called Health Benefit Exchanges, that

Insurance Exchanges: New Market Opportunities & Threats to Access. February 2014 avalerehealth.net

Insurance Exchanges: New Market Opportunities & Threats to Access February 2014 avalerehealth.net Despite Slow Initial Enrollment, Exchange Participation Is Accelerating Most Sign-Ups Expected Close to

Insurance Exchanges: New Market Opportunities & Threats to Access February 2014 avalerehealth.net Despite Slow Initial Enrollment, Exchange Participation Is Accelerating Most Sign-Ups Expected Close to

ACA Premium Impact Variability of Individual Market Premium Rate Changes Robert M. Damler, FSA, MAAA Paul R. Houchens, FSA, MAAA

ACA Premium Impact Variability of Individual Market Premium Rate Changes Robert M. Damler, FSA, MAAA Paul R. Houchens, FSA, MAAA BACKGROUND The Patient Protection and Affordable Care Act (ACA) introduces

ACA Premium Impact Variability of Individual Market Premium Rate Changes Robert M. Damler, FSA, MAAA Paul R. Houchens, FSA, MAAA BACKGROUND The Patient Protection and Affordable Care Act (ACA) introduces

Amy Burke, Arpit Misra, and Steven Sheingold June 18, 2014

ASPE RESEARCH BRIEF PREMIUM AFFORDABILITY, COMPETITION, AND CHOICE IN THE HEALTH INSURANCE MARKETPLACE, 2014 Amy Burke, Arpit Misra, and Steven Sheingold June 18, 2014 A central feature of the Affordable

ASPE RESEARCH BRIEF PREMIUM AFFORDABILITY, COMPETITION, AND CHOICE IN THE HEALTH INSURANCE MARKETPLACE, 2014 Amy Burke, Arpit Misra, and Steven Sheingold June 18, 2014 A central feature of the Affordable

Cost-sharing Charges in Marketplace Health Insurance Plans - Part II

September 2013 Cost-sharing Charges in Marketplace Health Insurance Plans - Part II Starting in January 2014, new health insurance marketplaces (also called exchanges) will provide a way for people to

September 2013 Cost-sharing Charges in Marketplace Health Insurance Plans - Part II Starting in January 2014, new health insurance marketplaces (also called exchanges) will provide a way for people to

How To Determine The Impact Of The Health Care Law On Insurance In Indiana

ACA Impact on Premium Rates in the Individual and Small Group Markets Paul R. Houchens, FSA, MAAA BACKGROUND The Patient Protection and Affordable Care Act (ACA) introduces significant changes in covered

ACA Impact on Premium Rates in the Individual and Small Group Markets Paul R. Houchens, FSA, MAAA BACKGROUND The Patient Protection and Affordable Care Act (ACA) introduces significant changes in covered

How To Get A Dental Plan On The Marketplace

2014 Delaware Qualified Health Plans Individual Market Overview October 8, 2013 www.pcghealth.com Topics Overview of QHPs in the Individual Market QHP Issuers Plan Summary Premium Rates and Cost-Sharing

2014 Delaware Qualified Health Plans Individual Market Overview October 8, 2013 www.pcghealth.com Topics Overview of QHPs in the Individual Market QHP Issuers Plan Summary Premium Rates and Cost-Sharing

Issue Brief: The Health Benefit Exchange and the Small Employer Market

Issue Brief: The Health Benefit Exchange and the Small Employer Market Overview The federal health care reform law directs states to set up health insurance marketplaces, called Health Benefit Exchanges,

Issue Brief: The Health Benefit Exchange and the Small Employer Market Overview The federal health care reform law directs states to set up health insurance marketplaces, called Health Benefit Exchanges,

WASHINGTON QUALIFIED HEALTH PLAN SELECTION: CONSIDERATIONS FOR CONSUMERS

WASHINGTON QUALIFIED HEALTH PLAN SELECTION: CONSIDERATIONS FOR CONSUMERS December 2013 Support for this resource provided through a grant from the Robert Wood Johnson Foundation s State Health Reform Assistance

WASHINGTON QUALIFIED HEALTH PLAN SELECTION: CONSIDERATIONS FOR CONSUMERS December 2013 Support for this resource provided through a grant from the Robert Wood Johnson Foundation s State Health Reform Assistance

Exchanges three years in: Market variations and factors affecting performance

Intelligence Brief Exchanges three years in: Market variations and factors affecting performance The third open enrollment period (OEP) for the public exchanges concluded in January. Many carriers both

Intelligence Brief Exchanges three years in: Market variations and factors affecting performance The third open enrollment period (OEP) for the public exchanges concluded in January. Many carriers both

New Hampshire Health Insurance Market Analysis

New Hampshire Health Insurance Market Analysis REPORT PREPARED FOR NEW HAMPSHIRE INSURANCE DEPARTMENT BY JULIA LERCHE, FSA, MAAA, MSPH CHIA YI CHIN BRITTNEY PHILLIPS AUGUST 18, 2014 TABLE OF CONTENTS 1.

New Hampshire Health Insurance Market Analysis REPORT PREPARED FOR NEW HAMPSHIRE INSURANCE DEPARTMENT BY JULIA LERCHE, FSA, MAAA, MSPH CHIA YI CHIN BRITTNEY PHILLIPS AUGUST 18, 2014 TABLE OF CONTENTS 1.

How to Apply for Health Insurance in the Age of Obamacare

Share this book on 2015 Edition How to Apply for Health Insurance in the Age of Obamacare Your guide to finding, comparing and enrolling in a plan that s right for you By Jeff Smedsrud Chief Executive

Share this book on 2015 Edition How to Apply for Health Insurance in the Age of Obamacare Your guide to finding, comparing and enrolling in a plan that s right for you By Jeff Smedsrud Chief Executive

As of January 1, 2014, most individuals must have some form of health coverage, or pay a penalty to the federal government.

Consumer Alert Health Insurance for 2014: What You Need to Know Before You Enroll (Individuals) As of January 1, 2014, most individuals must have some form of health coverage, or pay a penalty to the federal

Consumer Alert Health Insurance for 2014: What You Need to Know Before You Enroll (Individuals) As of January 1, 2014, most individuals must have some form of health coverage, or pay a penalty to the federal

Health Insurance Shopper s Guide 3 steps to choosing the right health plan for you and your family.

Health Insurance Shopper s Guide 3 steps to choosing the right health plan for you and your family. Ready to get started? We re here for you online, on the phone or in person. Visit for a quick and free

Health Insurance Shopper s Guide 3 steps to choosing the right health plan for you and your family. Ready to get started? We re here for you online, on the phone or in person. Visit for a quick and free

Ohio Health Insurance Exchanges. Information contained within the this presentation is subject to change.

Ohio Health Insurance Exchanges Information contained within the this presentation is subject to change. Affordable Care Act (ACA) Comprehensive health care reform law enacted in March 2010 in two parts:

Ohio Health Insurance Exchanges Information contained within the this presentation is subject to change. Affordable Care Act (ACA) Comprehensive health care reform law enacted in March 2010 in two parts:

Nevada Health Insurance Market Study

Nevada Health Insurance Market Study Prepared for the State of Nevada March 2012 Gorman Actuarial, LLC 210 Robert Road Marlborough, MA 01752 Bela Gorman, FSA, MAAA Don Gorman Jenn Smagula, FSA, MAAA Gorman

Nevada Health Insurance Market Study Prepared for the State of Nevada March 2012 Gorman Actuarial, LLC 210 Robert Road Marlborough, MA 01752 Bela Gorman, FSA, MAAA Don Gorman Jenn Smagula, FSA, MAAA Gorman

HEALTH CARE REFORM CHECKLIST

HEALTH CARE REFORM CHECKLIST As a small employer, you need to be aware of the new regulations tied to the Affordable Care Act. Refer to this checklist to ensure you understand each one and that you re

HEALTH CARE REFORM CHECKLIST As a small employer, you need to be aware of the new regulations tied to the Affordable Care Act. Refer to this checklist to ensure you understand each one and that you re

Health insurance Marketplace. What to expect in 2014

Health insurance Marketplace What to expect in 2014 Overview The Affordable Care Act (ACA) includes several provisions geared to extend greater access to health insurance benefits to more people. Beginning

Health insurance Marketplace What to expect in 2014 Overview The Affordable Care Act (ACA) includes several provisions geared to extend greater access to health insurance benefits to more people. Beginning

C A LIFORNIA HEALTHCARE FOUNDATION. s n a p s h o t California s Individual and Small Group Markets on the Eve of Reform

C A LIFORNIA HEALTHCARE FOUNDATION s n a p s h o t California s Individual and Small Group Markets on the Eve of Reform 2011 Introduction California s individual and small group health insurance markets

C A LIFORNIA HEALTHCARE FOUNDATION s n a p s h o t California s Individual and Small Group Markets on the Eve of Reform 2011 Introduction California s individual and small group health insurance markets

The Evolving Affordable Care Act Marketplaces

THE HEALTH OF AMERICA R E P O R T THE HEALTH OF AMERICA THE HEALTH OF AMERICA REPORT BLUE CROSS BLUE SHIELD THE HEALTH OF AMERICA REPORT The Evolving Affordable Care Act Marketplaces The 2015 to 2016 Transition

THE HEALTH OF AMERICA R E P O R T THE HEALTH OF AMERICA THE HEALTH OF AMERICA REPORT BLUE CROSS BLUE SHIELD THE HEALTH OF AMERICA REPORT The Evolving Affordable Care Act Marketplaces The 2015 to 2016 Transition

Setting and Valuing Health Insurance Benefits

Chris L. Peterson Specialist in Health Care Financing April 6, 2009 Congressional Research Service CRS Report for Congress Prepared for Members and Committees of Congress 7-5700 www.crs.gov R40491 Contents

Chris L. Peterson Specialist in Health Care Financing April 6, 2009 Congressional Research Service CRS Report for Congress Prepared for Members and Committees of Congress 7-5700 www.crs.gov R40491 Contents

Health plans for individuals and families

2015 Health Plan Information Health plans for individuals and families + Choosing the right plan for you + Subsidy eligibility information + Plan comparison charts + Terms and definitions + How to enroll

2015 Health Plan Information Health plans for individuals and families + Choosing the right plan for you + Subsidy eligibility information + Plan comparison charts + Terms and definitions + How to enroll

How To Rate A City For A Single At 250 Percent Of Poverty

September 2013 An Early Look at Premiums and Insurer Participation in Health Insurance Marketplaces, 2014 Cynthia Cox, Gary Claxton, Larry Levitt, Hana Khosla Under the Affordable Care Act (ACA), individuals

September 2013 An Early Look at Premiums and Insurer Participation in Health Insurance Marketplaces, 2014 Cynthia Cox, Gary Claxton, Larry Levitt, Hana Khosla Under the Affordable Care Act (ACA), individuals

Healthy Business Chat 07/10/2014

Healthy Business Chat 07/10/2014 1 What Is An Insurance Exchange? An Insurance Exchange is an organized marketplace for insurance plans to compete and offer services efficiently in the small group and

Healthy Business Chat 07/10/2014 1 What Is An Insurance Exchange? An Insurance Exchange is an organized marketplace for insurance plans to compete and offer services efficiently in the small group and

The Impact of the ACA on Maine s Health Insurance Markets

The Impact of the ACA on Maine s Health Insurance Markets Prepared for the Maine Bureau of Insurance May 31, 2011 Gorman Actuarial, LLC 210 Robert Road Marlborough, MA 01752 Jennifer Smagula, FSA, MAAA

The Impact of the ACA on Maine s Health Insurance Markets Prepared for the Maine Bureau of Insurance May 31, 2011 Gorman Actuarial, LLC 210 Robert Road Marlborough, MA 01752 Jennifer Smagula, FSA, MAAA

Small Group Plan Options HMO

HMO Platinum Plans These plans will cover about 90% of your service and you are responsible for the other 10% Benefits Platinum Platinum Platinum 25 / 50 / 500 HMO 20 / 40 / 1000 HMO 20 / 40 HMO Deductible

HMO Platinum Plans These plans will cover about 90% of your service and you are responsible for the other 10% Benefits Platinum Platinum Platinum 25 / 50 / 500 HMO 20 / 40 / 1000 HMO 20 / 40 HMO Deductible

Countdown to 2014: HEALTH CARE REFORM WHAT YOU NEED TO KNOW

Countdown to 2014: HEALTH CARE REFORM WHAT YOU NEED TO KNOW Coordinated by: -The Affordable Care Act- -Employer Notification- Monday, September 9, 2013 Registration 8:15 a.m. 8:45 a.m. Welcome 8:45 a.m.

Countdown to 2014: HEALTH CARE REFORM WHAT YOU NEED TO KNOW Coordinated by: -The Affordable Care Act- -Employer Notification- Monday, September 9, 2013 Registration 8:15 a.m. 8:45 a.m. Welcome 8:45 a.m.

INDIVIDUAL HEALTH INSURANCE In Maine

A Consumer s Guide To... INDIVIDUAL HEALTH INSURANCE In Maine Published by: The Maine Bureau of Insurance September 2015 Paul R. LePage Governor Eric A. Cioppa Superintendent Basics of Individual Health

A Consumer s Guide To... INDIVIDUAL HEALTH INSURANCE In Maine Published by: The Maine Bureau of Insurance September 2015 Paul R. LePage Governor Eric A. Cioppa Superintendent Basics of Individual Health

GBS Benefits, Inc. Health Care Reform. The Individual Mandate, Exchanges, and Medicaid Expansion

GBS Benefits, Inc. Health Care Reform August 2013 The Individual Mandate, Exchanges, and Medicaid Expansion As of January 1, 2014, the Affordable Care Act (ACA) requires most U.S. citizens and lawful residents

GBS Benefits, Inc. Health Care Reform August 2013 The Individual Mandate, Exchanges, and Medicaid Expansion As of January 1, 2014, the Affordable Care Act (ACA) requires most U.S. citizens and lawful residents

Health Reform Employer Impact Analysis. Sample Employer. Prepared for. Date

Health Reform Employer Impact Analysis Prepared for Sample Employer Date 2 Health Reform Employer Impact Analysis Overview Beginning in 2014, an applicable large employer becomes subject to what are referred

Health Reform Employer Impact Analysis Prepared for Sample Employer Date 2 Health Reform Employer Impact Analysis Overview Beginning in 2014, an applicable large employer becomes subject to what are referred

Health Insurance Buyers Guide. What You Need to Know to Get Started

Health Insurance Buyers Guide What You Need to Know to Get Started Time to Enroll The Affordable Care Act has changed the way that many people get health insurance. You may have more options and more ways

Health Insurance Buyers Guide What You Need to Know to Get Started Time to Enroll The Affordable Care Act has changed the way that many people get health insurance. You may have more options and more ways

Health plans for individuals and families

2015 Health Plan Information Health plans for individuals and families + Choosing the right plan for you + Subsidy eligibility information + Plan comparison charts + Terms and definitions + How to enroll

2015 Health Plan Information Health plans for individuals and families + Choosing the right plan for you + Subsidy eligibility information + Plan comparison charts + Terms and definitions + How to enroll

INDIVIDUAL HEALTH INSURANCE GUIDE. Introduction. What is the Health Insurance Marketplace?

INDIVIDUAL HEALTH INSURANCE GUIDE Introduction On November 15th, 2014, the second annual Open Enrollment Period for Individual Health Insurance begins. The Affordable Care Act (ACA) requires all US citizens

INDIVIDUAL HEALTH INSURANCE GUIDE Introduction On November 15th, 2014, the second annual Open Enrollment Period for Individual Health Insurance begins. The Affordable Care Act (ACA) requires all US citizens

DRAFT. Final Report. Wisconsin Department of Health Services Division of Health Care Access and Accountability

Final Report Wisconsin Department of Health Services Division of Health Care Access and Accountability Wisconsin s Small Group Insurance Market March 2009 Table of Contents 1 INTRODUCTION... 3 2 EMPLOYER-BASED

Final Report Wisconsin Department of Health Services Division of Health Care Access and Accountability Wisconsin s Small Group Insurance Market March 2009 Table of Contents 1 INTRODUCTION... 3 2 EMPLOYER-BASED

A Consumer Guide to Understanding Health Plan Networks

A Consumer Guide to Understanding Health Plan Networks Table of Contents steps you can take to understand your health plan s provider network pg 4 What a provider network is pg 8 Many people are now shopping

A Consumer Guide to Understanding Health Plan Networks Table of Contents steps you can take to understand your health plan s provider network pg 4 What a provider network is pg 8 Many people are now shopping

Massachusetts Health Connector logo. The Health Connector: Massachusetts New and Improved Health Insurance Marketplace

Massachusetts Health Connector logo The Health Connector: Massachusetts New and Improved Health Insurance Marketplace Massachusetts: The model for national health care reform 1 Massachusetts led the nation

Massachusetts Health Connector logo The Health Connector: Massachusetts New and Improved Health Insurance Marketplace Massachusetts: The model for national health care reform 1 Massachusetts led the nation

Small Group Health Insurance in 2008

Small Group Health Insurance in 2008 March 2009 A Comprehensive Survey of Premiums, Product Choices, and Benefits CONTENTS Summary...2 I. Introduction: The Small Group Market in Context...4 II. Premiums

Small Group Health Insurance in 2008 March 2009 A Comprehensive Survey of Premiums, Product Choices, and Benefits CONTENTS Summary...2 I. Introduction: The Small Group Market in Context...4 II. Premiums

Certification of Comparability of Pediatric Coverage Offered by Qualified Health Plans November 25, 2015

DEPARTMENT OF HEALTH AND HUMAN SERVICES Centers for Medicare & Medicaid Services 7500 Security Boulevard, Mail Stop S2-26-12 Baltimore, MD 21244-1850 Certification of Comparability of Pediatric Coverage

DEPARTMENT OF HEALTH AND HUMAN SERVICES Centers for Medicare & Medicaid Services 7500 Security Boulevard, Mail Stop S2-26-12 Baltimore, MD 21244-1850 Certification of Comparability of Pediatric Coverage

HEALTH CARE REFORM DOCUMENT FROM THE WEBSITE OF BLUE CROSS BLUE SHIELD OF NORTH DAKOTA

HEALTH CARE REFORM DOCUMENT FROM THE WEBSITE OF BLUE CROSS BLUE SHIELD OF NORTH DAKOTA Frequently Asked Questions I ve heard the federal government launched a new website called Healthcare.gov. How can

HEALTH CARE REFORM DOCUMENT FROM THE WEBSITE OF BLUE CROSS BLUE SHIELD OF NORTH DAKOTA Frequently Asked Questions I ve heard the federal government launched a new website called Healthcare.gov. How can

WASBO Federal Health Care Reform Patient Protection and Affordable Care Act

WASBO Federal Health Care Reform Patient Protection and Affordable Care Act What and Employer Needs to Know for 2015 & 2016 May 15, 2015 David A. Grunke Sr. Director, Sales Operations WPS Health Insurance

WASBO Federal Health Care Reform Patient Protection and Affordable Care Act What and Employer Needs to Know for 2015 & 2016 May 15, 2015 David A. Grunke Sr. Director, Sales Operations WPS Health Insurance

2016 HIV Pre-Exposure Prophylaxis (PrEP) Health Insurance Assessment

Health Insurance Assessment") 2016 HIV Pre-Exposure Prophylaxis (PrEP) Health Insurance Assessment December 2015 Report produced by: Cesar Egurrola Clinical Coordinator Petersen Clinics Shannon Smith Director, Special Projects Department

2016 HIV Pre-Exposure Prophylaxis (PrEP) Health Insurance Assessment December 2015 Report produced by: Cesar Egurrola Clinical Coordinator Petersen Clinics Shannon Smith Director, Special Projects Department

Health Insurance Premium Credits in the Patient Protection and Affordable Care Act (PPACA)

") Health Insurance Premium Credits in the Patient Protection and Affordable Care Act (PPACA) Chris L. Peterson Specialist in Health Care Financing Thomas Gabe Specialist in Social Policy April 28, 2010 Congressional

Health Insurance Premium Credits in the Patient Protection and Affordable Care Act (PPACA) Chris L. Peterson Specialist in Health Care Financing Thomas Gabe Specialist in Social Policy April 28, 2010 Congressional

2. EXECUTIVE SUMMARY. Assist with the first year of planning for design and implementation of a federally mandated American health benefits exchange

2. EXECUTIVE SUMMARY The Patient Protection and Affordable Care Act of 2010 and the Health Care and Education Reconciliation Act of 2010, collectively referred to as the Affordable Care Act (ACA), introduces

2. EXECUTIVE SUMMARY The Patient Protection and Affordable Care Act of 2010 and the Health Care and Education Reconciliation Act of 2010, collectively referred to as the Affordable Care Act (ACA), introduces

Health Insurance Premium Credits Under PPACA (P.L. 111-148)

") Health Insurance Premium Credits Under PPACA (P.L. 111-148) Chris L. Peterson Specialist in Health Care Financing Thomas Gabe Specialist in Social Policy April 6, 2010 Congressional Research Service CRS

Health Insurance Premium Credits Under PPACA (P.L. 111-148) Chris L. Peterson Specialist in Health Care Financing Thomas Gabe Specialist in Social Policy April 6, 2010 Congressional Research Service CRS

Realizing Health Reform s Potential

Realizing Health Reform s Potential JUNE 2016 Promoting Value for Consumers: Comparing Individual Health Insurance Markets Inside and Outside the ACA s Exchanges The mission of The Commonwealth Fund is

Realizing Health Reform s Potential JUNE 2016 Promoting Value for Consumers: Comparing Individual Health Insurance Markets Inside and Outside the ACA s Exchanges The mission of The Commonwealth Fund is

Let us help you choose the health insurance plan that fits you best

Let us help you choose the health insurance plan that fits you best Call 855-381-1212, visit bcbstx.com or contact an independent Blue Cross and Blue Shield of Texas agent to get a quote today. Life is

Let us help you choose the health insurance plan that fits you best Call 855-381-1212, visit bcbstx.com or contact an independent Blue Cross and Blue Shield of Texas agent to get a quote today. Life is

How To Compare Health Insurance Plans

The three most important questions you need to ask Health care can be very expensive. Having a baby costs about $30,000, and so does the average three-day hospital stay. Health insurance is a way to reduce

The three most important questions you need to ask Health care can be very expensive. Having a baby costs about $30,000, and so does the average three-day hospital stay. Health insurance is a way to reduce

Health Insurance. Where should you SHOP for your health insurance coverage? Decision-Making Guide presented by Bob Hopper Insurance Services

Health Insurance Where should you SHOP for your health insurance coverage? Decision-Making Guide presented by Bob Hopper Insurance Services We ll help you locate the health plan that offers the best value

Health Insurance Where should you SHOP for your health insurance coverage? Decision-Making Guide presented by Bob Hopper Insurance Services We ll help you locate the health plan that offers the best value

Analysis of National Sales Data of Individual and Family Health Insurance

Analysis of National Sales Data of Individual and Family Health Insurance Implications for Policymakers and the Effectiveness of Health Insurance Tax Credits Vip Patel, Chairman ehealthinsurance June 2001

Analysis of National Sales Data of Individual and Family Health Insurance Implications for Policymakers and the Effectiveness of Health Insurance Tax Credits Vip Patel, Chairman ehealthinsurance June 2001

PRIVATE HEALTH INSURANCE. Early Evidence Finds Premium Tax Credit Likely Contributed to Expanded Coverage, but Some Lack Access to Affordable Plans

United States Government Accountability Office Report to Congressional Committees March 2015 PRIVATE HEALTH INSURANCE Early Evidence Finds Premium Tax Credit Likely Contributed to Expanded Coverage, but

United States Government Accountability Office Report to Congressional Committees March 2015 PRIVATE HEALTH INSURANCE Early Evidence Finds Premium Tax Credit Likely Contributed to Expanded Coverage, but

Comments on the Health Net Life Insurance Company Proposal to Submit New Plans, Effective 1 January, 2014. State Tracking Number: HAO 2013 0108

July, 2013 Comments on the Health Net Life Insurance Company Proposal to Submit New Plans, Effective 1 January, 2014. State Tracking Number: HAO 2013 0108 Health Insurance Rate Watch A Project of CALPIRG

July, 2013 Comments on the Health Net Life Insurance Company Proposal to Submit New Plans, Effective 1 January, 2014. State Tracking Number: HAO 2013 0108 Health Insurance Rate Watch A Project of CALPIRG

Prepared for State of Minnesota. February 2013

The Impact of the ACA and Exchange on Minnesota: Updated Estimates Prepared for State of Minnesota February 2013 Dr. Jonathan Gruber MIT Department of Economics 50 Memorial Drive Cambridge, MA 02142 Gorman

The Impact of the ACA and Exchange on Minnesota: Updated Estimates Prepared for State of Minnesota February 2013 Dr. Jonathan Gruber MIT Department of Economics 50 Memorial Drive Cambridge, MA 02142 Gorman

Briefing Paper Individual Health Insurance Markets Grow and Are Transformed: Results for Four States Allan Baumgarten, 2014

Briefing Paper Individual Health Insurance s Grow and Are Transformed: Results for Four States As implementation of the Affordable Care Act (ACA) continues, the market for individual health insurance has

Briefing Paper Individual Health Insurance s Grow and Are Transformed: Results for Four States As implementation of the Affordable Care Act (ACA) continues, the market for individual health insurance has

Exchanges and the ACA What You Need to Know for 2014

Exchanges and the ACA What You Need to Know for 2014 How the Affordable Care Act affects the Individual Health Insurance Market This presentation is for informational purposes only and does not constitute

Exchanges and the ACA What You Need to Know for 2014 How the Affordable Care Act affects the Individual Health Insurance Market This presentation is for informational purposes only and does not constitute

Health Care Reform Update

Small Businesses No Financial Requirements for Small Businesses: The ACA imposes no financial requirements for small businesses to contribute to their employees health insurance. However, beginning in

Small Businesses No Financial Requirements for Small Businesses: The ACA imposes no financial requirements for small businesses to contribute to their employees health insurance. However, beginning in

Patient Protection and Affordable Care Act (H.R. 3590)

") on Health Reform Passing comprehensive health care reform has been a priority of the President and Congress. The U.S. House of Representatives passed the Affordable Health Care for America Act on November

on Health Reform Passing comprehensive health care reform has been a priority of the President and Congress. The U.S. House of Representatives passed the Affordable Health Care for America Act on November

ISSUE BRIEF. Health Insurance Marketplace Premiums for 2014

ASPE ISSUE BRIEF Health Insurance Marketplace Premiums for 2014 On October 1, 2013, a Health Insurance Marketplace will open in each state, providing a new, simplified way to compare individual market

ASPE ISSUE BRIEF Health Insurance Marketplace Premiums for 2014 On October 1, 2013, a Health Insurance Marketplace will open in each state, providing a new, simplified way to compare individual market

Health Care Law & You

Health Care Law & You How to get the most out of your health care dollars 2014 Independence Blue Cross Independence Blue Cross is an independent licensee of the Blue Cross and Blue Shield Association.

Health Care Law & You How to get the most out of your health care dollars 2014 Independence Blue Cross Independence Blue Cross is an independent licensee of the Blue Cross and Blue Shield Association.

Q. My company already offers employee health coverage, how does the law impact me?

Frequently Asked Questions Q. Will my business be required to provide employee health insurance under the health care law? A. The law does not mandate employers provide employees health care coverage.

Frequently Asked Questions Q. Will my business be required to provide employee health insurance under the health care law? A. The law does not mandate employers provide employees health care coverage.

WELCOME TO A NEW ERA IN HEALTH CARE COVERAGE FOR TENNESSEE.

WELCOME TO A NEW ERA IN HEALTH CARE COVERAGE FOR TENNESSEE. Quality Health Plans for Individuals and Families in Tennessee. TABLE OF CONTENTS INTRODUCTION...1 Who are we?... 1 What is a CO-OP?...1 Our

WELCOME TO A NEW ERA IN HEALTH CARE COVERAGE FOR TENNESSEE. Quality Health Plans for Individuals and Families in Tennessee. TABLE OF CONTENTS INTRODUCTION...1 Who are we?... 1 What is a CO-OP?...1 Our

Assessing the 2015 MA Star ratings

Intelligence Brief On October 10, 2014, CMS released the Medicare Advantage (MA) Star ratings for 2015. We analyzed CMS s data covering 691 MA plan contracts across the 50 states to determine which types

Intelligence Brief On October 10, 2014, CMS released the Medicare Advantage (MA) Star ratings for 2015. We analyzed CMS s data covering 691 MA plan contracts across the 50 states to determine which types

The Large Business Guide to Health Care Law

The Large Business Guide to Health Care Law How the new changes in health care law will affect you and your employees Table of contents Introduction 3 Part I: A general overview of the health care law

The Large Business Guide to Health Care Law How the new changes in health care law will affect you and your employees Table of contents Introduction 3 Part I: A general overview of the health care law

your guide to health INSURANCE reform

CURRENT LOGO your guide to health INSURANCE reform for This guide explains how Health Reform will affect Individual and Family health plans, helps you understand different types of health insurance and

CURRENT LOGO your guide to health INSURANCE reform for This guide explains how Health Reform will affect Individual and Family health plans, helps you understand different types of health insurance and

REGULATORY UPDATE Vol. 1 No. 18

REGULATORY UPDATE Vol. 1 No. 18 FAQs on Exchanges August 7, 2013 IN THIS ISSUE FAQs on Exchanges Employer Mandate Delay Transitional Guidance Issued Individual Mandate Final Rules Issued Possible Exchange

REGULATORY UPDATE Vol. 1 No. 18 FAQs on Exchanges August 7, 2013 IN THIS ISSUE FAQs on Exchanges Employer Mandate Delay Transitional Guidance Issued Individual Mandate Final Rules Issued Possible Exchange

The Implications of a Finding for the Plaintiffs in House v. Burwell

H E A L T H P O L I C Y C E N T E R The Implications of a Finding for the Plaintiffs in House v. Burwell $47 Billion More in Federal Spending over 10 years and Smaller Marketplaces Linda J. Blumberg and

H E A L T H P O L I C Y C E N T E R The Implications of a Finding for the Plaintiffs in House v. Burwell $47 Billion More in Federal Spending over 10 years and Smaller Marketplaces Linda J. Blumberg and

How To Calculate Health Insurance Premiums In The American Health Insurance Exchange

Health Insurance Premium Credits in the Patient Protection and Affordable Care Act (ACA) Bernadette Fernandez Specialist in Health Care Financing Thomas Gabe Specialist in Social Policy December 30, 2011

Health Insurance Premium Credits in the Patient Protection and Affordable Care Act (ACA) Bernadette Fernandez Specialist in Health Care Financing Thomas Gabe Specialist in Social Policy December 30, 2011

SISC HEALTH BENEFITS 101. South Orange County Community College District August 11, 2015

1 SISC HEALTH BENEFITS 101 South Orange County Community College District August 11, 2015 2 SISC Schools Helping Schools Established in 1979, Self-Insured Schools of California (SISC) operates as a public

1 SISC HEALTH BENEFITS 101 South Orange County Community College District August 11, 2015 2 SISC Schools Helping Schools Established in 1979, Self-Insured Schools of California (SISC) operates as a public

EXPLORING NEW YORK S SHOP MARKETPLACE. An Overview for Small Groups

EXPLORING NEW YORK S SHOP MARKETPLACE An Overview for Small Groups TABLE OF CONTENTS Why SHOP... 1 Who Can Enroll...2 How to Enroll...3 Choosing Plans...4 Our SHOP Offerings...5 SHOP Plan Comparison...6-7

EXPLORING NEW YORK S SHOP MARKETPLACE An Overview for Small Groups TABLE OF CONTENTS Why SHOP... 1 Who Can Enroll...2 How to Enroll...3 Choosing Plans...4 Our SHOP Offerings...5 SHOP Plan Comparison...6-7

kynect Overview and Update Executive Director

kynect Overview and Update Carrie Banahan Executive Director March 27, 2014 What is kynect? An organized marketplace for individuals and employees of small businesses to shop for health insurance offered

kynect Overview and Update Carrie Banahan Executive Director March 27, 2014 What is kynect? An organized marketplace for individuals and employees of small businesses to shop for health insurance offered

Health Insurance Marketplace. vhealth insurance exchanges. What to expect in 2014. What to expect in 2014

vhealth insurance exchanges Health Insurance Marketplace What to expect in 2014 What to expect in 2014 The basics of exchanges As part of the Affordable Care Act (ACA or health care reform law), starting

vhealth insurance exchanges Health Insurance Marketplace What to expect in 2014 What to expect in 2014 The basics of exchanges As part of the Affordable Care Act (ACA or health care reform law), starting

How ACA is Changing Employer Health Benefits and the Marketplace Presented by:

North Carolina State Health Plan How ACA is Changing Employer Health Benefits and the Marketplace Presented by: J. Richard Johnson Senior Vice President, Public Sector Health Practice Leader rjohnson@segalco.com

North Carolina State Health Plan How ACA is Changing Employer Health Benefits and the Marketplace Presented by: J. Richard Johnson Senior Vice President, Public Sector Health Practice Leader rjohnson@segalco.com

Shopping for a health care plan can be confusing. Let us help.

We re here to help Shopping for a health care plan can be confusing. Let us help. Thank you for trusting Anthem Blue Cross and Blue Shield for your health coverage. We re here to protect you from the high

We re here to help Shopping for a health care plan can be confusing. Let us help. Thank you for trusting Anthem Blue Cross and Blue Shield for your health coverage. We re here to protect you from the high

EXPLORING NEW YORK S SHOP MARKETPLACE 2016 Overview for Small Groups

EXPLORING NEW YORK S SHOP MARKETPLACE 2016 Overview for Small Groups TABLE OF CONTENTS Why SHOP... 1 Who Can Enroll...2 How to Enroll...3 Choosing Plans...4 Our SHOP Offerings...5 SHOP Plan Comparison...6-7

EXPLORING NEW YORK S SHOP MARKETPLACE 2016 Overview for Small Groups TABLE OF CONTENTS Why SHOP... 1 Who Can Enroll...2 How to Enroll...3 Choosing Plans...4 Our SHOP Offerings...5 SHOP Plan Comparison...6-7

The Small Business Guide to Health Care Law

The Small Business Guide to Health Care Law How new changes in health care law will affect you and your employees Table of Contents Introduction 3 Part I: A General Overview of Health Care Law 4 The Affects

The Small Business Guide to Health Care Law How new changes in health care law will affect you and your employees Table of Contents Introduction 3 Part I: A General Overview of Health Care Law 4 The Affects

Your Guide to Health Insurance Learn how to choose the best health plan

Your Guide to Health Insurance Learn how to choose the best health plan Subsidy Welcome Thank you for considering AmeriHealth New Jersey as your health insurer. We know the importance of having quality

Your Guide to Health Insurance Learn how to choose the best health plan Subsidy Welcome Thank you for considering AmeriHealth New Jersey as your health insurer. We know the importance of having quality

STATE CONSIDERATIONS ON ADOPTING HEALTH REFORM S BASIC HEALTH OPTION Federal Guidance Needed for States to Fully Assess Option by January Angeles

820 First Street NE, Suite 510 Washington, DC 20002 Tel: 202-408-1080 Fax: 202-408-1056 center@cbpp.org www.cbpp.org March 13, 2012 STATE CONSIDERATIONS ON ADOPTING HEALTH REFORM S BASIC HEALTH OPTION

820 First Street NE, Suite 510 Washington, DC 20002 Tel: 202-408-1080 Fax: 202-408-1056 center@cbpp.org www.cbpp.org March 13, 2012 STATE CONSIDERATIONS ON ADOPTING HEALTH REFORM S BASIC HEALTH OPTION

New provider networks will support health plans sold on and off the Health Insurance Marketplace

Health Insurance Exchange October 2013 New provider networks will support health plans sold on and off the Health Insurance Marketplace Anthem Blue Cross and Blue Shield and our subsidiary HMO Nevada (Anthem)

Health Insurance Exchange October 2013 New provider networks will support health plans sold on and off the Health Insurance Marketplace Anthem Blue Cross and Blue Shield and our subsidiary HMO Nevada (Anthem)

ISSUE BRIEF. A Little Knowledge Is a Risky Thing: Wide Gap in What People Think They Know About Health Insurance and What They Actually Know

October 214 Amended A Little Knowledge Is a Risky Thing: Wide Gap in What People Think They Know About Health and What They Actually Know BY KATHRYN A. PAEZ AND CORETTA J. MALLERY Under the 2 Affordable

October 214 Amended A Little Knowledge Is a Risky Thing: Wide Gap in What People Think They Know About Health and What They Actually Know BY KATHRYN A. PAEZ AND CORETTA J. MALLERY Under the 2 Affordable

Covered California: Competition in the Health Insurance Market?

Covered California: Competition in the Health Insurance Market? Richard M. Scheffler, Ph.D. Distinguished Professor of Health Economics & Public Policy Director, Nicholas C. Petris Center University of

Covered California: Competition in the Health Insurance Market? Richard M. Scheffler, Ph.D. Distinguished Professor of Health Economics & Public Policy Director, Nicholas C. Petris Center University of

Premium Tax Credits: Answers to Frequently Asked Questions

Updated July 2013 Premium Tax Credits: Answers to Frequently Asked Questions Beginning in 2014, millions of Americans will become eligible for a new premium tax credit that will help them pay for health

Updated July 2013 Premium Tax Credits: Answers to Frequently Asked Questions Beginning in 2014, millions of Americans will become eligible for a new premium tax credit that will help them pay for health

Solutions for Today Flexibility for Tomorrow.

Solutions for Today Flexibility for Tomorrow. Medicare Products and Services For More Information call our Senior Care Specialist, Raun Lynch at 856.380.5079 Or visit us on the web at www.cbdi-inc.com

Solutions for Today Flexibility for Tomorrow. Medicare Products and Services For More Information call our Senior Care Specialist, Raun Lynch at 856.380.5079 Or visit us on the web at www.cbdi-inc.com

Prepared for Minnesota Department of Commerce. April, 2012

The Impact of the ACA and Exchange on Minnesota Prepared for Minnesota Department of Commerce April, 2012 Dr. Jonathan Gruber MIT Department of Economics 50 Memorial Drive Cambridge, MA 02142 Gorman Actuarial,

The Impact of the ACA and Exchange on Minnesota Prepared for Minnesota Department of Commerce April, 2012 Dr. Jonathan Gruber MIT Department of Economics 50 Memorial Drive Cambridge, MA 02142 Gorman Actuarial,

SOMETHING OLD, SOMETHING NEW: TEXAS TWO HIGH-RISK POOLS

July 19, 2010 Contact: Stacey Pogue, pogue@cppp.org SOMETHING OLD, SOMETHING NEW: TEXAS TWO HIGH-RISK POOLS Thanks to national health reform, Texas now has two separate high-risk pools that offer health

July 19, 2010 Contact: Stacey Pogue, pogue@cppp.org SOMETHING OLD, SOMETHING NEW: TEXAS TWO HIGH-RISK POOLS Thanks to national health reform, Texas now has two separate high-risk pools that offer health

Your guide to finding the best health insurance plan.

LIFE HAS OPPORTUNITIES Your guide to finding the best health insurance plan. Start saving today with the help of Excellus BlueCross BlueShield. National strength. Local focus. Individual care. SM Contents

LIFE HAS OPPORTUNITIES Your guide to finding the best health insurance plan. Start saving today with the help of Excellus BlueCross BlueShield. National strength. Local focus. Individual care. SM Contents

Non-Group Health Insurance: Many Insured Americans with High Out-of-Pocket Costs Forgo Needed Health Care

Affordable Care Act Non-Group Health Insurance: Many Insured Americans with High Out-of-Pocket Costs Forgo Needed Health Care SPECIAL REPORT / MAY 2015 WWW.FAMILIESUSA.ORG Executive Summary Since its passage

Affordable Care Act Non-Group Health Insurance: Many Insured Americans with High Out-of-Pocket Costs Forgo Needed Health Care SPECIAL REPORT / MAY 2015 WWW.FAMILIESUSA.ORG Executive Summary Since its passage

The Impact of the ACA on Wisconsin's Health Insurance Market

The Impact of the ACA on Wisconsin's Health Insurance Market Prepared for the Wisconsin Department of Health Services July 18, 2011 Gorman Actuarial, LLC 210 Robert Road Marlborough, MA 01752 Jennifer

The Impact of the ACA on Wisconsin's Health Insurance Market Prepared for the Wisconsin Department of Health Services July 18, 2011 Gorman Actuarial, LLC 210 Robert Road Marlborough, MA 01752 Jennifer

Federal exchange auto-enrollment: Emerging data and new proposals

Federal exchange auto-enrollment: Emerging data and new proposals Jason A. Clarkson, FSA, MAAA William A. Gibula, ASA, MAAA Paul R. Houchens, FSA, MAAA EXECUTIVE SUMMARY The U.S. Department of Health and

Federal exchange auto-enrollment: Emerging data and new proposals Jason A. Clarkson, FSA, MAAA William A. Gibula, ASA, MAAA Paul R. Houchens, FSA, MAAA EXECUTIVE SUMMARY The U.S. Department of Health and

Let us help you choose the health insurance plan that fits you best

Let us help you choose the health insurance plan that fits you best Call 855-381-1212, visit bcbstx.com or contact an independent Blue Cross and Blue Shield of Texas agent to get a quote today. Life Is

Let us help you choose the health insurance plan that fits you best Call 855-381-1212, visit bcbstx.com or contact an independent Blue Cross and Blue Shield of Texas agent to get a quote today. Life Is

STATE OF CONNECTICUT

STATE OF CONNECTICUT INSURANCE DEPARTMENT Aetna Life Insurance Company Individual Off-Exchange 2016 Rate Filing Finding of Facts 1. The purpose of this filing is to provide details of the premium rate

STATE OF CONNECTICUT INSURANCE DEPARTMENT Aetna Life Insurance Company Individual Off-Exchange 2016 Rate Filing Finding of Facts 1. The purpose of this filing is to provide details of the premium rate