Utilizing a Collection Agency

|

|

|

- Evan Rich

- 8 years ago

- Views:

Transcription

1 Utilizing a Collection Agency Donna Fraczek Court Administrator 71-B B District Court You may be surprised at the amount of outstanding debt owed the court! Is the collection of old debt so overwhelming that you just ignore it? Does the amount past due warrant the time you and your staff have to spend to collect it? 1

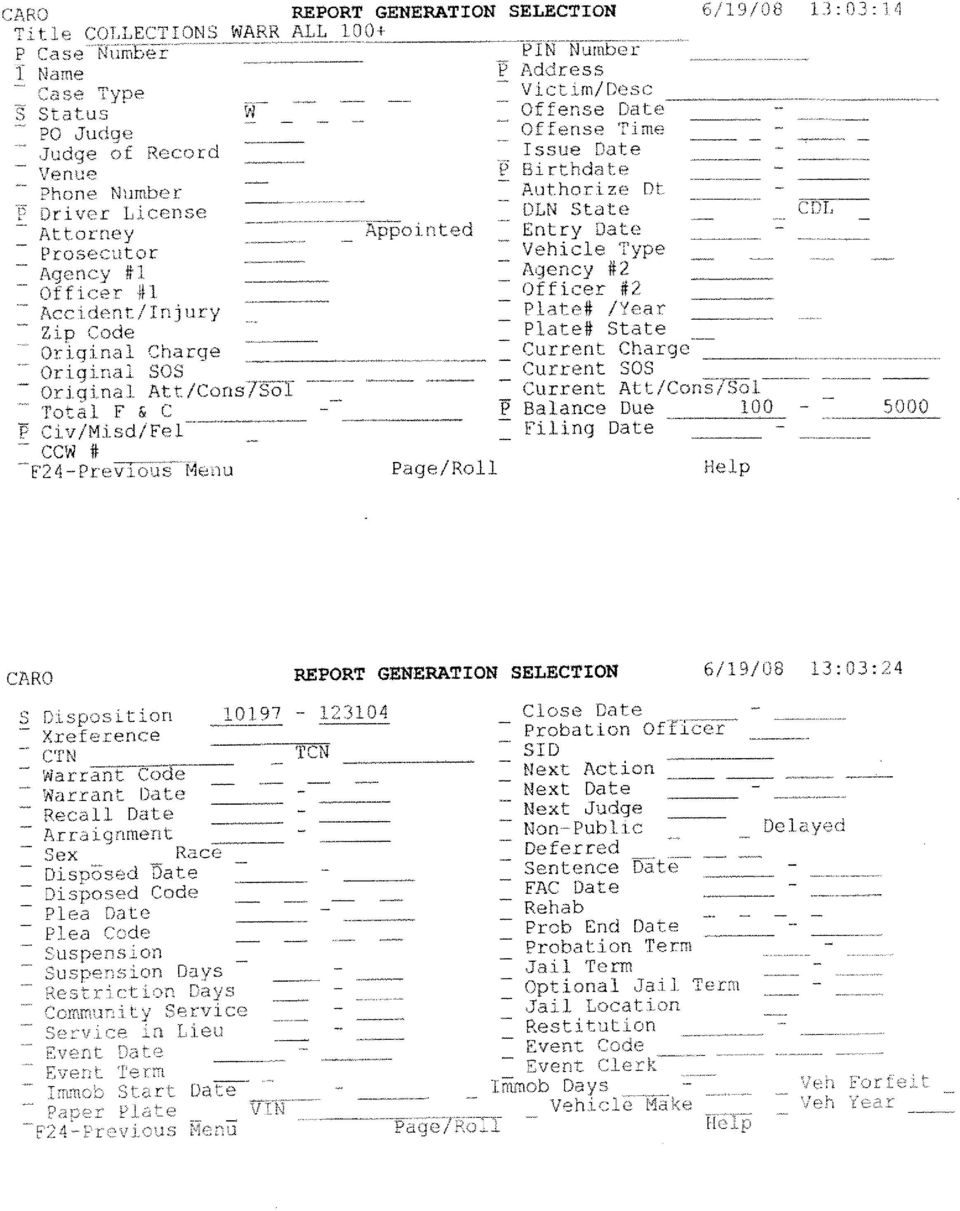

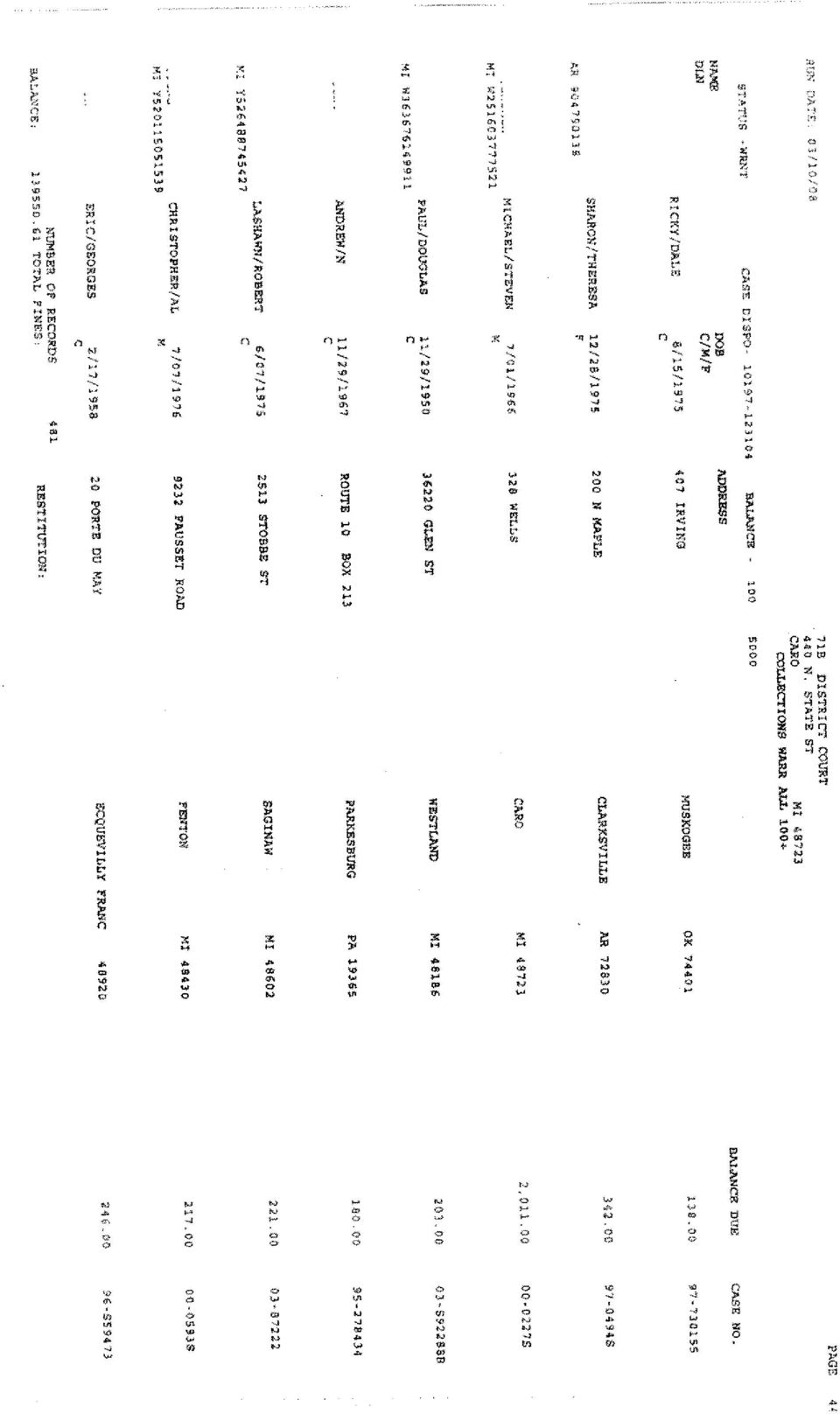

2 Cases over three years old are the most difficult to collect. Are you EVER going to collect it in-house or just wait for them to get picked up on warrants? Do your local police agencies pursue old warrants that have been issued for failing to pay fines and costs? Many times staffing does not allow for a full-time collections program. Even if you have a collections staff, do you want them to spend their time and resources to collect old debt? What have you got to lose? Considerations Where Do I Start? Use a report generator to determine the following: Old uncollectible cases In warrant status Late fees already attached No restitution owing Number of cases and total amount owing 2

3 Choosing a Collection Agency Licensed by Department of Labor & Economic Growth michigan.gov/dleg Being a member of a Michigan association and a national association is desirable. The associations should require they: Abide by a code of ethics. Are familiar with Fair Debt Collection Practices Act and Michigan Collection Practices Act. Examples: Insured/Bonded Choosing a Collection Agency, cont. Location of Agency Local Agencies May know defendant and/or family. May have had past or present contact with defendant if they collect for other local businesses. May be collecting for other county departments such as the sheriff s dept. and/or other courts. 3

4 Choosing a Collection Agency, cont. What methods of collection are used? Credit Report Skip Trace For those with no current addresses or telephone numbers. For online search techniques, networking, and special directories. Make sure they have a good skip trace method. Test them. Starting only with your name, see how long it takes them to develop your name, address, and telephone number. Give them each a couple of old cases and see how long it takes to get beneficial information that aids in the collection process. s. Choosing a Collection Agency, cont. Do they follow set practices that are nonthreatening,, professional, and respectful? Letters Ask to see samples of letters they send. Telephone contact Continued contact once located If possible, it is beneficial to go to their office and observe their practices. 4

5 Choosing a Collection Agency, cont. Have them provide you with a list of references Check those references and ask about the time it took for collection. Ask those references if they are satisfied with the agency s collections efforts. Choosing a Collection Agency, cont. Will they provide you with monthly reports with a complete accounting of amounts paid? They will need to send to you the entire amount they collected, and you will then have your funding unit send them a check for their commission. Communication needs to be immediate between the agency and court staff, AND court staff and the agency. Recall of warrants needs to be timely. 5

6 Cost Get estimates from several different collection agencies. Don t be afraid to negotiate. Percent (range from 15-50%) 50%) of amount collected. Will they charge you for a defendant who is picked up and serves time in lieu of fines/costs? Get Your Funding Unit on Board Show them the amount of outstanding debt that you are attempting to collect. They need to know that this potential revenue has been determined uncollectible due to staffing issues, jail overcrowding, or whatever your court s individual circumstances are. 6

7 Funding Unit, cont. Show them the potential revenue that can be collected compared to the cost of a collection agency. It may be easier to have one or two commissioners or the county administrator educated about your plan prior to presenting it to the entire board. Keep them informed of the progress. The Contract: What to Include Minimum balances to be turned over Agency must be licensed Must comply with: The law. Michigan Collection Practices Act. Fair Debt Collection Practices Act. 7

8 The Contract: What to Include, cont. Confidentiality requirements. Deposit requirements of moneys collected by the agency. Reports required by the court. Court s requirement for remittance of money collected by the agency. Amount of agency fee and how it will be paid. The Contract: What to Include, cont. Details on how agency will notify court when debt is paid, etc. Details on how court will notify agency when debt is paid to court. Do you have to pay if defendant received jail time in lieu of outstanding debt, etc.? Will partial payment be accepted yes or no? 8

9 Communication! Communication! Communication! Continued communication with your collection agency is important. Staff contact person needs to be assigned. Review status at least twice a year with an in- person meeting with the agency owner or manager. Keep your funding unit informed of your progress. 9

10 BILLING DATE TOTAL COLLECTED COMMISSION PD. TO UNITED COLLECTIONS TOTAL REVENUE AFTER COMMISSION 9/1/2007 $1, $ $ /1/2007 $1, $ $ /1/2007 $2, $ $1, /1/2007 $1, $ $1, /1/2008 $ $ $ /1/2008 $1, $ $1, /1/2008 $1, $ $ /1/2008 $ $ $ /2/2008 $1, $ $ /1/2008 $ $ $ $13, $4, $8, One group of files was sent to the collection agency on 7/3/2007. The files that were sent were cases that had warrants issued between 1997 and The total amount owed on the files sent was $134,

11

12

13

14 The Fair Debt Collection Practices Act can be found at:

15 REGULATION OF COLLECTION PRACTICES Act 70 of 1981 AN ACT to regulate the collection practices of certain persons; to provide for the powers and duties of certain state agencies; and to provide penalties and civil fines. History: 1981, Act 70, Imd. Eff. June 29, The People of the State of Michigan enact: Definitions. Sec. 1. As used in this act: (a) Claim or debt means an obligation or alleged obligation for the payment of money or thing of value arising out of an expressed or implied agreement or contract for a purchase made primarily for personal, family, or household purposes. (b) Collection agency means a person directly or indirectly engaged in soliciting a claim for collection or collecting or attempting to collect a claim owed or due or asserted to be owed or due another, or repossessing or attempting to repossess a thing of value owed or due or asserted to be owed or due another person, arising out of an expressed or implied agreement. Collection agency includes a person representing himself or herself as a collection or repossession agency or a person performing the activities of a collection agency, on behalf of another, which activities are regulated by Act No. 299 of the Public Acts of 1980, as amended, being sections to of the Michigan Compiled Laws. Collection agency includes a person who furnishes or attempts to furnish a form or a written demand service represented to be a collection or repossession technique, device, or system to be used t o collect or repossess claims, if the form contains the name of a person other than the creditor in a manner indicating that a request or demand for payment is being made by a person other than the creditor even though the form directs the debtor to make payment directly to the creditor rather than to the other person whose name appears on the form. Collection agency includes a person who uses a fictitious name or the name of another in the collection or repossession of claims to convey to the debtor that a third person is collecting or repossessing or has been employed to collect or repossess the claim. (c) Communicate means the conveying of information regarding a debt directly or indirectly to a person through any medium. (d) Consumer or debtor means a natural person obligated or allegedly obligated to pay a debt. (e) Creditor or principal means a person who offers or extends credit creating a debt or a person to whom a debt is owed or due or asserted to be owed or due. Creditor or principal does not include a person who receives an assignment or transfer or a debt solely for the purpose of facilitating collection of the debt for the assignor or transferor. In those instances, the assignor or transferor of the debt shall continue to be considered the creditor or the principal for purposes of this act. (f) Person means an individual, sole proprietorship, partnership, association, or corporation. (g) Regulated person means a person whose collection activities are confined and are directly related to the operation of a business other than that of a collection agency including the following: (i) A regular employee when collecting accounts for 1 employer if the collection efforts are carried on in the name of the employer. (ii) A state or federally chartered bank when collecting its own claim. (iii) A trust company when collecting its own claim. (iv) A state or federally chartered savings and loan association when collecting its own claim. (v) A state or federally chartered credit union when collecting its own claim. (vi) A licensee under Act No. 21 of the Public Acts of 1939, as amended, being sections to of the Michigan Compiled Laws. (vii) A business licensed by the state under a regulatory act by which collection activity is regulated. (viii) An abstract company doing an escrow business. (ix) A licensed real estate broker or salesperson if the claim being handled by the broker or salesperson is related to or in connection with the broker or salesperson's real estate business. (x) A public officer or a person acting under court order. (xi) An attorney handling claims and collections on behalf of a client and in the attorney's own name. History: 1981, Act 70, Imd. Eff. June 29, Prohibited acts. Rendered Thursday, June 19, 2008 Page 1 Michigan Compiled Laws Complete Through PA 162 of 2008 Legislative Council, State of Michigan Courtesy of

16 Sec. 2. A regulated person shall not commit 1 or more of the following acts: (a) Communicating with a debtor in a misleading or deceptive manner, such as using the stationery of an attorney or credit bureau unless the regulated person is an attorney or is a credit bureau and it is disclosed that it is the collection department of the credit bureau. (b) Using forms or instruments which simulate the appearance of judicial process. (c) Using seals or printed forms of a government agency or instrumentality. (d) Using forms that may otherwise induce the belief that they have judicial or official sanction. (e) Making an inaccurate, misleading, untrue, or deceptive statement or claim in a communication to collect a debt or concealing or not revealing the purpose of a communication when it is made in connection with collecting a debt. (f) Misrepresenting in a communication with a debtor 1 or more of the following: (i) The legal status of a legal action being taken or threatened. (ii) The legal rights of the creditor or debtor. (iii) That the nonpayment of a debt will result in the debtor's arrest or imprisonment, or the seizure, garnishment, attachment, or sale of the debtor's property. (iv) That accounts have been turned over to innocent purchasers for value. (g) Communicating with a debtor without accurately disclosing the caller's identity or cause expenses to the debtor for a long distance telephone call, telegram, or other charge. (h) Communicating with a debtor, except through billing procedure when the debtor is actively represented by an attorney, the attorney's name and address are known, and the attorney has been contacted in writing by the credit grantor or the credit grantor's representative or agent, unless the attorney representing the debtor fails to answer written communication or fails to discuss the claim on its merits within 30 days after receipt of the written communication. (i) Communicating information relating to a debtor's indebtedness to an employer or an employer's agent unless the communication is specifically authorized in writing by t he debtor subsequent to the forwarding of the claim for collection, the communication is in response to an inquiry initiated by the debtor's employer or the employer's agent, or the communication is for the purpose of acquiring location information about the debtor. (j) Using or employing, in connection with collection of a claim, a person acting as a peace or law enforcement officer or any other officer authorized to serve legal papers. (k) Using or threatening to use physical violence in connection with collection of a claim. (l) Publishing, causing to be published, or threatening to publish lists of debtors, except for credit reporting purposes, when in response to a specific inquiry from a prospective credit grantor about a debtor. (m) Using a shame card, shame automobile, or otherwise bring to public notice that the consumer is a debtor, except with respect to a legal proceeding which is instituted. (n) Using a harassing, oppressive, or abusive method to collect a debt, including causing a telephone to ring or engaging a person in telephone conversation repeatedly, continuously, or at unusual times or places which are known to be inconvenient to the debtor. All communications shall be made from 8 a.m. to 9 p.m. unless the debtor expressly agrees in writing to communications at another time. All telephone communications made from 9 p.m. to 8 a.m. shall be presumed to be made at an inconvenient time in the absence of facts to the contrary. (o) Using profane or obscene language. (p) Using a method contrary to a postal law or regulation to collect an account. (q) Failing to implement a procedure designed to prevent a violation by an employee. (r) Communicating with a consumer regarding a debt by post card. (s) Employing a person required to be licensed under article 9 of Act No. 299 of the Public Acts of 1980, being sections to of the Michigan Compiled Laws, to collect a claim unless that person is licensed under article 9 of Act No. 299 of the Public Acts of History: 1981, Act 70, Imd. Eff. June 29, Cease and desist order; hearing; failure to comply with order; action in circuit court; fine. Sec. 3. (1) The attorney general may order a regulated person to cease and desist from violating this act. (2) A regulated person ordered to cease and desist is entitled to a hearing before the appropriate officer as determined by the attorney general if he or she files a written request within 30 days after the effective date of the order. (3) If a regulated person fails to comply with a cease and desist order issued pursuant to this act, the attorney general may commence an action in the circuit court for Ingham county or in a circuit court for a Rendered Thursday, June 19, 2008 Page 2 Michigan Compiled Laws Complete Through PA 162 of 2008 Legislative Council, State of Michigan Courtesy of

Using forms or instruments which simulate the appearance of judicial process. (c) Using seals or printed forms of a government agency or instrumentality.")

17 county where the person is doing business, to enjoin violations of the cease and desist order or to seek enforcement of a previously issued order. The court may impose a fine or not more than $ for each violation of the cease and desist order. History: 1981, Act 70, Imd. Eff. June 29, Action to restrain act or practice; injunction and other equitable orders or judgments. Sec. 4. The attorney general may bring an action to restrain, by temporary or permanent injunction, an act or practice in violation of this act. The action may be brought in the circuit court for the county where the defendant resides or conducts business. The court may issue a temporary or permanent injunction and make other equitable orders or judgments, including restitution to consumers. History: 1981, Act 70, Imd. Eff. June 29, Assurance of discontinuance; contents; filing; record; opening closed matter for further proceedings. Sec. 5. When the attorney general has authority to institute an action pursuant to section 4, the attorney general may accept an assurance of discontinuance of any method, act, or practice from the person alleged to be engaged in or to have been engaged in a violation. The assurance may include the stipulation for the voluntary payment, by the person, of the costs of investigation, an amount for restitution to aggrieved persons, or both. An assurance of discontinuance shall be in writing and filed with the circuit court. The clerk of the court shall maintain a record of the filings. A matter closed pursuant to this section may be opened by the attorney general for further proceedings. History: 1981, Act 70, Imd. Eff. June 29, Wilful violation of act or engaging in recurring course of wilful conduct in violation of act; penalties. Sec. 6. (1) In an action brought under this act, if the court finds that a regulated person has wilfully violated this act, the attorney general, upon petition to the court, may recover, on behalf of the state, a civil fine not exceeding $ per violation. (2) A regulated person engaging in a recurring course of wilful conduct in violation of this act shall be fined not more than $5, for the first offense, and not more than $10,000.00, or imprisoned for not more than 1 year, or both, for a second or subsequent offense. History: 1981, Act 70, Imd. Eff. June 29, Action for damages or equitable relief; amount of recovery; civil fine; attorney's fees and court costs. Sec. 7. (1) A person who suffers injury, loss, or damage, or from whom money was collected by the use of a method, act, or practice in violation of this act may bring an action for damages or other equitable relief. (2) In an action brought pursuant to subsection (1), if the court finds for the petitioner, recovery shall be in the amount of actual damages or $50.00, whichever is greater. If the court finds that the method, act, or practice was a wilful violation, the court may assess a civil fine of not less than 3 times the actual damages, or $150.00, whichever is greater, and shall award reasonable attorney's fees and court costs incurred in connection with the action. History: 1981, Act 70, Imd. Eff. June 29, Communications with person other than debtor for purpose of acquiring location information; required statements. Sec. 8. (1) A regulated person communicating with any person other than the debtor, for the purpose of acquiring location information about the debtor, shall state all of the following: (a) The name of the individual seeking the location information. (b) Whether the purpose of the communication is for confirmation or correction of location information about the debtor. (2) For purposes of this act, location information shall consist only of a debtor's place of abode and place of employment and the telephone number at each place. History: 1981, Act 70, Imd. Eff. June 29, Rendered Thursday, June 19, 2008 Page 3 Michigan Compiled Laws Complete Through PA 162 of 2008 Legislative Council, State of Michigan Courtesy of

18

19

20

21

22

The Rosenthal Fair Debt Collection Practices Act California Civil Code 1788 et seq.

The Rosenthal Fair Debt Collection Practices Act California Civil Code 1788 et seq. 1788. This title may be cited as the Rosenthal Fair Debt Collection Practices Act. 1788.1 (a) The Legislature makes the

The Rosenthal Fair Debt Collection Practices Act California Civil Code 1788 et seq. 1788. This title may be cited as the Rosenthal Fair Debt Collection Practices Act. 1788.1 (a) The Legislature makes the

Consumer Collection Agencies

Sec. 36a-809 page 1 (12-08) TABLE OF CONTENTS Consumer Collection Agencies Repealed.......................... 36a-809-1 36a-809-5 Definitions................................ 36a-809-6 Books and records...........................

Sec. 36a-809 page 1 (12-08) TABLE OF CONTENTS Consumer Collection Agencies Repealed.......................... 36a-809-1 36a-809-5 Definitions................................ 36a-809-6 Books and records...........................

Fair Debt Collection Practices Act

Background The Fair Debt Collection Practices Act (FDCPA) (15 USC 1692 et seq.), which became effective in March 1978, was designed to eliminate abusive, deceptive, and unfair debt collection practices.

Background The Fair Debt Collection Practices Act (FDCPA) (15 USC 1692 et seq.), which became effective in March 1978, was designed to eliminate abusive, deceptive, and unfair debt collection practices.

VII 3.1. VII. Unfair and Deceptive Practices FDCPA. Fair Debt Collection Practices Act. Introduction. Communications Connected with Debt Collection

Fair Debt Collection Practices Act Introduction The Fair Debt Collection Practices Act (FDCPA), effective in 1978, was designed to eliminate abusive, deceptive, and unfair debt collection practices. The

Fair Debt Collection Practices Act Introduction The Fair Debt Collection Practices Act (FDCPA), effective in 1978, was designed to eliminate abusive, deceptive, and unfair debt collection practices. The

CHAPTER 13-04-02 COLLECTION AGENCIES

CHAPTER 13-04-02 COLLECTION AGENCIES Section 13-04-02-01 De nitions 13-04-02-02 Prohibited Advertising and Communications 13-04-02-03 Debt Collectors - Approval 13-04-02-04 Prohibited Practices 13-04-02-05

CHAPTER 13-04-02 COLLECTION AGENCIES Section 13-04-02-01 De nitions 13-04-02-02 Prohibited Advertising and Communications 13-04-02-03 Debt Collectors - Approval 13-04-02-04 Prohibited Practices 13-04-02-05

IX. FLORIDA CONSUMER COLLECTION PRACTICES ACT

IX. FLORIDA CONSUMER COLLECTION PRACTICES ACT Sec. 559.55 Definitions. 559.551 Short title. PART IV - CONSUMER COLLECTION PRACTICES (FCCPA) 559.552 Relationship of state and federal law. 559.553 Registration

IX. FLORIDA CONSUMER COLLECTION PRACTICES ACT Sec. 559.55 Definitions. 559.551 Short title. PART IV - CONSUMER COLLECTION PRACTICES (FCCPA) 559.552 Relationship of state and federal law. 559.553 Registration

Fair Debt Collection Practices Act 1

Fair Debt Collection Practices Act 1 The Fair Debt Collection Practices Act (FDCPA)(15 U.S.C. 1692 et seq.), which became effective March 20, 1978, was designed to eliminate abusive, deceptive, and unfair

Fair Debt Collection Practices Act 1 The Fair Debt Collection Practices Act (FDCPA)(15 U.S.C. 1692 et seq.), which became effective March 20, 1978, was designed to eliminate abusive, deceptive, and unfair

Chapter 21 Credit Services Organizations Act

Chapter 21 Credit Services Organizations Act 13-21-1 Short title. This chapter is known as the "Credit Services Organizations Act." Enacted by Chapter 29, 1985 General Session 13-21-2 Definitions -- Exemptions.

Chapter 21 Credit Services Organizations Act 13-21-1 Short title. This chapter is known as the "Credit Services Organizations Act." Enacted by Chapter 29, 1985 General Session 13-21-2 Definitions -- Exemptions.

DEBT COLLECTION LAW. DISTRICT OF COLUMBIA OFFICIAL CODE Copyright 2014 by the District of Columbia

DEBT COLLECTION LAW DISTRICT OF COLUMBIA OFFICIAL CODE Copyright 2014 by the District of Columbia Current through December 13, 2013 and through D.C. Act 20-210 (except D.C. Acts 20-130, 20-157, and 20-204)

DEBT COLLECTION LAW DISTRICT OF COLUMBIA OFFICIAL CODE Copyright 2014 by the District of Columbia Current through December 13, 2013 and through D.C. Act 20-210 (except D.C. Acts 20-130, 20-157, and 20-204)

DEBT COLLECTION LAW. (1A) creditor means a claimant or other person holding a claim;

creditor means a claimant or other person holding a claim;") DEBT COLLECTION LAW DC Code 28-3814 District of Columbia Official Code 2001 Edition Division V. Local Business Affairs Title 28. Commercial Instruments and Transactions. Subtitle II. Other Commercial Transactions.

DEBT COLLECTION LAW DC Code 28-3814 District of Columbia Official Code 2001 Edition Division V. Local Business Affairs Title 28. Commercial Instruments and Transactions. Subtitle II. Other Commercial Transactions.

OFFICE OF ATTORNEY GENERAL, STATE OF FLORIDA, DEPARTMENT OF LEGAL AFFAIRS,

IN THE CIRCUIT COURT OF THE FOURTH JUDICIAL CIRCUIT IN AND FOR DUVAL COUNTY, FLORIDA OFFICE OF ATTORNEY GENERAL, STATE OF FLORIDA, DEPARTMENT OF LEGAL AFFAIRS, Case No.: v. Plaintiff, BASS PRELITIGATION

IN THE CIRCUIT COURT OF THE FOURTH JUDICIAL CIRCUIT IN AND FOR DUVAL COUNTY, FLORIDA OFFICE OF ATTORNEY GENERAL, STATE OF FLORIDA, DEPARTMENT OF LEGAL AFFAIRS, Case No.: v. Plaintiff, BASS PRELITIGATION

STATE OF MICHIGAN DEPARTMENT OF LICENSING & REGULATORY AFFAIRS OFFICE OF FINANCIAL AND INSURANCE REGULATION

STATE OF MICHIGAN DEPARTMENT OF LICENSING & REGULATORY AFFAIRS OFFICE OF FINANCIAL AND INSURANCE REGULATION Before the Commissioner of the Office of Financial and Insurance Regulation In the matter of:

STATE OF MICHIGAN DEPARTMENT OF LICENSING & REGULATORY AFFAIRS OFFICE OF FINANCIAL AND INSURANCE REGULATION Before the Commissioner of the Office of Financial and Insurance Regulation In the matter of:

Nebraska Loan Broker Act Chapter 45, Article 1, Section f 45-189 to 45-193

45-189 Loan brokers; legislative findings. The Legislature finds that: Nebraska Loan Broker Act Chapter 45, Article 1, Section f 45-189 to 45-193 (1) Many professional groups are presently licensed or

45-189 Loan brokers; legislative findings. The Legislature finds that: Nebraska Loan Broker Act Chapter 45, Article 1, Section f 45-189 to 45-193 (1) Many professional groups are presently licensed or

Be it enacted by the People of the State of Illinois,

AN ACT concerning government. Be it enacted by the People of the State of Illinois, represented in the General Assembly: Section 5. The Collection Agency Act is amended by changing Sections 2, 9.1, 9.2,

AN ACT concerning government. Be it enacted by the People of the State of Illinois, represented in the General Assembly: Section 5. The Collection Agency Act is amended by changing Sections 2, 9.1, 9.2,

SB 588. Employment: nonpayment of wages: Labor Commissioner: judgment enforcement.

SB 588. Employment: nonpayment of wages: Labor Commissioner: judgment enforcement. (1) The Enforcement of Judgments Law provides for the enforcement of money judgments and other civil judgments. Under

SB 588. Employment: nonpayment of wages: Labor Commissioner: judgment enforcement. (1) The Enforcement of Judgments Law provides for the enforcement of money judgments and other civil judgments. Under

UNITED STATES DISTRICT COURT MIDDLE DISTRICT OF FLORIDA, TAMPA DIVISION

UNITED STATES DISTRICT COURT MIDDLE DISTRICT OF FLORIDA, TAMPA DIVISION Consumer Financial Protection Bureau and Office of the Attorney General, State of Florida, Department of Legal Affairs, Case No.

UNITED STATES DISTRICT COURT MIDDLE DISTRICT OF FLORIDA, TAMPA DIVISION Consumer Financial Protection Bureau and Office of the Attorney General, State of Florida, Department of Legal Affairs, Case No.

CAUSE NO. PLAINTIFF S ORIGINAL PETITION. Greg Abbott, and complains of OLD UNITED LIFE INSURANCE COMPANY ( Defendant ), and I.

, and I.") CAUSE NO. STATE OF TEXAS, Plaintiff, v. OLD UNITED LIFE INSURANCE COMPANY, Defendant. IN THE DISTRICT COURT OF TRAVIS COUNTY, TEXAS JUDICIAL DISTRICT PLAINTIFF S ORIGINAL PETITION TO THE HONORABLE JUDGE

CAUSE NO. STATE OF TEXAS, Plaintiff, v. OLD UNITED LIFE INSURANCE COMPANY, Defendant. IN THE DISTRICT COURT OF TRAVIS COUNTY, TEXAS JUDICIAL DISTRICT PLAINTIFF S ORIGINAL PETITION TO THE HONORABLE JUDGE

CALIFORNIA FAIR DEBT COLLECTION PRACTICES ACT Updated 1 January 2012

I. BACKGROUND CALIFORNIA FAIR DEBT COLLECTION PRACTICES ACT Updated 1 January 2012 A. Contents: This memorandum summarizes California's Fair Debt Collection Practices Act, California Civil Code (the "CCC")

I. BACKGROUND CALIFORNIA FAIR DEBT COLLECTION PRACTICES ACT Updated 1 January 2012 A. Contents: This memorandum summarizes California's Fair Debt Collection Practices Act, California Civil Code (the "CCC")

AN ACT RELATING TO LABOR AND EMPLOYMENT; AMENDING THE MINIMUM WAGE ACT TO CREATE A PREFERENCE FOR CIVIL ACTIONS AND APPEALS

AN ACT RELATING TO LABOR AND EMPLOYMENT; AMENDING THE MINIMUM WAGE ACT TO CREATE A PREFERENCE FOR CIVIL ACTIONS AND APPEALS BROUGHT TO COLLECT UNPAID OR UNDERPAID WAGES TO BE HEARD BY THE COURT TO THE

AN ACT RELATING TO LABOR AND EMPLOYMENT; AMENDING THE MINIMUM WAGE ACT TO CREATE A PREFERENCE FOR CIVIL ACTIONS AND APPEALS BROUGHT TO COLLECT UNPAID OR UNDERPAID WAGES TO BE HEARD BY THE COURT TO THE

13-25a-101. Title. This chapter is known as the "Telephone and Facsimile Solicitation Act."

13-25a-101. Title. This chapter is known as the "Telephone and Facsimile Solicitation Act." Enacted by Chapter 26, 1996 General Session 13-25a-102. Definitions. As used in this chapter: (1) "Advertisement"

13-25a-101. Title. This chapter is known as the "Telephone and Facsimile Solicitation Act." Enacted by Chapter 26, 1996 General Session 13-25a-102. Definitions. As used in this chapter: (1) "Advertisement"

Debt Adjusting Companies and Credit Services Businesses: Tennessee s Requirements

Debt Adjusting Companies and Credit Services Businesses: Tennessee s Requirements Tennessee law has separate provisions relative to debt adjusting companies and credit services businesses (see the definitions

Debt Adjusting Companies and Credit Services Businesses: Tennessee s Requirements Tennessee law has separate provisions relative to debt adjusting companies and credit services businesses (see the definitions

940 CMR: OFFICE OF THE ATTORNEY GENERAL

940 CMR 7.00: DEBT COLLECTION REGULATIONS Section 7.01: Purpose of Regulation 7.02: Scope 7.03: Definitions 7.04: Contact with Debtors 7.05: Contact with Persons Residing in the Household of a Debtor 7.06:

940 CMR 7.00: DEBT COLLECTION REGULATIONS Section 7.01: Purpose of Regulation 7.02: Scope 7.03: Definitions 7.04: Contact with Debtors 7.05: Contact with Persons Residing in the Household of a Debtor 7.06:

TITLE 81. BANKS AND FINANCIAL INSTITUTIONS CHAPTER 22. MISSISSIPPI DEBT MANAGEMENT SERVICES ACT [REPEALED EFFECTIVE JULY 1, 2013]

![TITLE 81. BANKS AND FINANCIAL INSTITUTIONS CHAPTER 22. MISSISSIPPI DEBT MANAGEMENT SERVICES ACT [REPEALED EFFECTIVE JULY 1, 2013]](/thumbs/32/15491712.jpg "TITLE 81. BANKS AND FINANCIAL INSTITUTIONS CHAPTER 22. MISSISSIPPI DEBT MANAGEMENT SERVICES ACT [REPEALED EFFECTIVE JULY 1, 2013]") TITLE 81. BANKS AND FINANCIAL INSTITUTIONS CHAPTER 22. MISSISSIPPI DEBT MANAGEMENT SERVICES ACT [REPEALED EFFECTIVE JULY 1, 2013] Section 81-22-1. Short title [Repealed effective July 1, 2013] 81-22-3.

TITLE 81. BANKS AND FINANCIAL INSTITUTIONS CHAPTER 22. MISSISSIPPI DEBT MANAGEMENT SERVICES ACT [REPEALED EFFECTIVE JULY 1, 2013] Section 81-22-1. Short title [Repealed effective July 1, 2013] 81-22-3.

Credit Services Organization Act 24 O.S. 131 148

Credit Services Organization Act 24 O.S. 131 148 Chapter 8 Credit Services Organization Act Section 131 Short Title This act shall be known and may be cited as the "Credit Services Organization Act". Added

Credit Services Organization Act 24 O.S. 131 148 Chapter 8 Credit Services Organization Act Section 131 Short Title This act shall be known and may be cited as the "Credit Services Organization Act". Added

UNOFFICIAL COPY OF SENATE BILL 660. ENROLLED BILL -- Finance/Economic Matters -- Read and Examined by Proofreaders:

I1 UNOFFICIAL COPY OF SENATE BILL 660 ENROLLED BILL -- Finance/Economic Matters -- (5lr2457) Introduced by Senator Astle Senators Astle and Exum Read and Examined by Proofreaders: Proofreader. Proofreader.

I1 UNOFFICIAL COPY OF SENATE BILL 660 ENROLLED BILL -- Finance/Economic Matters -- (5lr2457) Introduced by Senator Astle Senators Astle and Exum Read and Examined by Proofreaders: Proofreader. Proofreader.

Assembly Bill No. 344 CHAPTER 733

Assembly Bill No. 344 CHAPTER 733 An act to amend Sections 4970, 4973, 4974, 4975, 4977, 4978, 4978.6, 4979, and 4979.7 of the Financial Code, as added by Assembly Bill 489 of the 2001-02 Regular Session,

Assembly Bill No. 344 CHAPTER 733 An act to amend Sections 4970, 4973, 4974, 4975, 4977, 4978, 4978.6, 4979, and 4979.7 of the Financial Code, as added by Assembly Bill 489 of the 2001-02 Regular Session,

Chapter 213. Enforcement of Texas Unemployment Compensation Act... 2 Subchapter A. General Enforcement Provisions... 2 Sec. 213.001.

Chapter 213. Enforcement of Texas Unemployment Compensation Act... 2 Subchapter A. General Enforcement Provisions... 2 Sec. 213.001. Representation in Court... 2 Sec. 213.002. Prosecution of Criminal Actions...

Chapter 213. Enforcement of Texas Unemployment Compensation Act... 2 Subchapter A. General Enforcement Provisions... 2 Sec. 213.001. Representation in Court... 2 Sec. 213.002. Prosecution of Criminal Actions...

Texas Security Freeze Law

Texas Security Freeze Law BUSINESS & COMMERCE CODE CHAPTER 20. REGULATION OF CONSUMER CREDIT REPORTING AGENCIES 20.01. DEFINITIONS. In this chapter: (1) "Adverse action" includes: (A) the denial of, increase

Texas Security Freeze Law BUSINESS & COMMERCE CODE CHAPTER 20. REGULATION OF CONSUMER CREDIT REPORTING AGENCIES 20.01. DEFINITIONS. In this chapter: (1) "Adverse action" includes: (A) the denial of, increase

STATE OF NEW JERSEY. SENATE, No. 1988. 213th LEGISLATURE. Sponsored by: Senator JEFF VAN DREW District 1 (Cape May, Atlantic and Cumberland)

") SENATE, No. STATE OF NEW JERSEY th LEGISLATURE INTRODUCED JUNE, 00 Sponsored by: Senator JEFF VAN DREW District (Cape May, Atlantic and Cumberland) SYNOPSIS "New Jersey Fair Debt Collection Practices Act."

SENATE, No. STATE OF NEW JERSEY th LEGISLATURE INTRODUCED JUNE, 00 Sponsored by: Senator JEFF VAN DREW District (Cape May, Atlantic and Cumberland) SYNOPSIS "New Jersey Fair Debt Collection Practices Act."

CONSUMER MORTGAGE PROTECTION ACT Act 660 of 2002. The People of the State of Michigan enact:

CONSUMER MORTGAGE PROTECTION ACT Act 660 of 2002 AN ACT to prohibit certain lending practices; to require disclosure of certain information for home loans; to prescribe certain duties and obligations of

CONSUMER MORTGAGE PROTECTION ACT Act 660 of 2002 AN ACT to prohibit certain lending practices; to require disclosure of certain information for home loans; to prescribe certain duties and obligations of

INSTRUCTIONS FOR COMPLETING OFFICIAL FORM 1, VOLUNTARY PETITION I. INTRODUCTION

INSTRUCTIONS FOR COMPLETING OFFICIAL FORM 1, VOLUNTARY PETITION I. INTRODUCTION This form, known as a "voluntary petition," must be used by a debtor to begin a bankruptcy case. Filing this petition is

INSTRUCTIONS FOR COMPLETING OFFICIAL FORM 1, VOLUNTARY PETITION I. INTRODUCTION This form, known as a "voluntary petition," must be used by a debtor to begin a bankruptcy case. Filing this petition is

Chapter 24 Title Lending Registration Act. Part 1 General Provisions

Chapter 24 Title Lending Registration Act Part 1 General Provisions 7-24-101 Title. This chapter is known as the "Title Lending Registration Act." 7-24-102 Definitions. As used in this chapter: (1) "Nationwide

Chapter 24 Title Lending Registration Act Part 1 General Provisions 7-24-101 Title. This chapter is known as the "Title Lending Registration Act." 7-24-102 Definitions. As used in this chapter: (1) "Nationwide

GENERAL ASSEMBLY OF NORTH CAROLINA SESSION 1991 H 1 HOUSE BILL 22

GENERAL ASSEMBLY OF NORTH CAROLINA SESSION H HOUSE BILL Short Title: Regulate Reverse Mortgages. (Public) Sponsors: Representatives Brubaker, Easterling, Hasty, Ligon, Lineberry, Privette, and Woodard.

GENERAL ASSEMBLY OF NORTH CAROLINA SESSION H HOUSE BILL Short Title: Regulate Reverse Mortgages. (Public) Sponsors: Representatives Brubaker, Easterling, Hasty, Ligon, Lineberry, Privette, and Woodard.

TEXAS UNFAIR CLAIMS STATUTES AND REGULATIONS

TEXAS UNFAIR CLAIMS STATUTES AND REGULATIONS 541.060. UNFAIR SETTLEMENT PRACTICES. (a) It is an unfair method of competition or an unfair or deceptive act or practice in the business of insurance to engage

TEXAS UNFAIR CLAIMS STATUTES AND REGULATIONS 541.060. UNFAIR SETTLEMENT PRACTICES. (a) It is an unfair method of competition or an unfair or deceptive act or practice in the business of insurance to engage

HOUSE COMMITTEE ON APPROPRIATIONS FISCAL NOTE. SENATE BILL NO. 622 PRINTERS NO. 2222 PRIME SPONSOR: Ward

HOUSE COMMITTEE ON APPROPRIATIONS FISCAL NOTE SENATE BILL NO. 622 PRINTERS NO. 2222 PRIME SPONSOR: Ward COST / (SAVINGS) FUND FY 2013/14 FY 2014/15 Banking Fund $0 See Fiscal Impact SUMMARY: Creates a

HOUSE COMMITTEE ON APPROPRIATIONS FISCAL NOTE SENATE BILL NO. 622 PRINTERS NO. 2222 PRIME SPONSOR: Ward COST / (SAVINGS) FUND FY 2013/14 FY 2014/15 Banking Fund $0 See Fiscal Impact SUMMARY: Creates a

ILLINOIS CREDIT REPAIR LAWS

ILLINOIS CREDIT REPAIR LAWS This page contains information about starting a credit repair business in Illinois as well as legal information and Credit Repair laws for the State of Illinois. IL ST Ch. 815,

ILLINOIS CREDIT REPAIR LAWS This page contains information about starting a credit repair business in Illinois as well as legal information and Credit Repair laws for the State of Illinois. IL ST Ch. 815,

Dealing with Debt Collectors. collection activity has certainly increased tremendously with the downturn of the

Dealing with Debt Collectors The debt collection industry has grown immensely in the United States, and debt collection activity has certainly increased tremendously with the downturn of the American economy.

Dealing with Debt Collectors The debt collection industry has grown immensely in the United States, and debt collection activity has certainly increased tremendously with the downturn of the American economy.

Michie's Legal Resources. This part shall be known and may be cited as the Tennessee Identity Theft Deterrence Act of 1999. [Acts 1999, ch. 201, 2.

http://www.michie.com/tennessee/lpext.dll/tncode/12ebe/13cdb/1402c/1402e?f=templates&... Page 1 of 1 47-18-2101. Short title. This part shall be known and may be cited as the Tennessee Identity Theft Deterrence

http://www.michie.com/tennessee/lpext.dll/tncode/12ebe/13cdb/1402c/1402e?f=templates&... Page 1 of 1 47-18-2101. Short title. This part shall be known and may be cited as the Tennessee Identity Theft Deterrence

DEBT MANAGEMENT ACT Act 148 of 1975. The People of the State of Michigan enact:

DEBT MANAGEMENT ACT Act 148 of 1975 AN ACT to regulate the business of debt management; to require licenses and establish license fees; to prescribe the powers and duties of certain state agencies and

DEBT MANAGEMENT ACT Act 148 of 1975 AN ACT to regulate the business of debt management; to require licenses and establish license fees; to prescribe the powers and duties of certain state agencies and

AMENDED ADMINISTRATIVE ORDER GOVERNING A COLLECTIONS COURT PROGRAM IN ORANGE COUNTY

ADMINISTRATIVE ORDER NO. 07-99-26-5 IN THE CIRCUIT COURT OF THE NINTH JUDICIAL CIRCUIT, IN AND FOR ORANGE COUNTY, FLORIDA AMENDED ADMINISTRATIVE ORDER GOVERNING A COLLECTIONS COURT PROGRAM IN ORANGE COUNTY

ADMINISTRATIVE ORDER NO. 07-99-26-5 IN THE CIRCUIT COURT OF THE NINTH JUDICIAL CIRCUIT, IN AND FOR ORANGE COUNTY, FLORIDA AMENDED ADMINISTRATIVE ORDER GOVERNING A COLLECTIONS COURT PROGRAM IN ORANGE COUNTY

TOO MANY DEBTS? HOW TO DEAL WITH YOUR DEBTS AND STOP DEBT COLLECTORS FROM HARASSING YOU

LEGAL AID CONSUMER FACT SHEET # 1 TOO MANY DEBTS? HOW TO DEAL WITH YOUR DEBTS AND STOP DEBT COLLECTORS FROM HARASSING YOU Important Note: The following fact sheet is not intended to substitute for legal

LEGAL AID CONSUMER FACT SHEET # 1 TOO MANY DEBTS? HOW TO DEAL WITH YOUR DEBTS AND STOP DEBT COLLECTORS FROM HARASSING YOU Important Note: The following fact sheet is not intended to substitute for legal

GENERAL ASSEMBLY OF NORTH CAROLINA 1991 SESSION CHAPTER 546 HOUSE BILL 22

GENERAL ASSEMBLY OF NORTH CAROLINA 1991 SESSION CHAPTER 546 HOUSE BILL 22 AN ACT TO REGULATE REVERSE MORTGAGES. The General Assembly of North Carolina enacts: Section 1. Chapter 53 of the General Statutes

GENERAL ASSEMBLY OF NORTH CAROLINA 1991 SESSION CHAPTER 546 HOUSE BILL 22 AN ACT TO REGULATE REVERSE MORTGAGES. The General Assembly of North Carolina enacts: Section 1. Chapter 53 of the General Statutes

COLLECTION AND DEBT REPAYMENT PRACTICES REGULATION

Province of Alberta FAIR TRADING ACT COLLECTION AND DEBT REPAYMENT PRACTICES REGULATION Alberta Regulation 194/1999 With amendments up to and including Alberta Regulation 57/2014 Office Consolidation Published

Province of Alberta FAIR TRADING ACT COLLECTION AND DEBT REPAYMENT PRACTICES REGULATION Alberta Regulation 194/1999 With amendments up to and including Alberta Regulation 57/2014 Office Consolidation Published

GENERAL ASSEMBLY OF NORTH CAROLINA SESSION 2007 S 1 SENATE BILL 1198

GENERAL ASSEMBLY OF NORTH CAROLINA SESSION 0 S SENATE BILL Short Title: Regulate Debt Settlement. Sponsors: Senators Clodfelter; and Berger of Rockingham. Referred to: Commerce, Small Business and Entrepreneurship.

GENERAL ASSEMBLY OF NORTH CAROLINA SESSION 0 S SENATE BILL Short Title: Regulate Debt Settlement. Sponsors: Senators Clodfelter; and Berger of Rockingham. Referred to: Commerce, Small Business and Entrepreneurship.

COLORADO CREDIT SERVICES ORGANIZATION ACT. Table of Contents COLORADO CREDIT SERVICES ORGANIZATION ACT... 1

COLORADO CREDIT SERVICES ORGANIZATION ACT Table of Contents COLORADO CREDIT SERVICES ORGANIZATION ACT... 1 12-14.5-101. Short title.... 1 12-14.5-102. Legislative declaration.... 1 12-14.5-103. Definitions...

COLORADO CREDIT SERVICES ORGANIZATION ACT Table of Contents COLORADO CREDIT SERVICES ORGANIZATION ACT... 1 12-14.5-101. Short title.... 1 12-14.5-102. Legislative declaration.... 1 12-14.5-103. Definitions...

11 LC 14 0449ER A BILL TO BE ENTITLED AN ACT

House Bill 338 By: Representative Bryant of the 160 th A BILL TO BE ENTITLED AN ACT 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 To amend Title 44 of the Official Code of Georgia Annotated, relating to property,

House Bill 338 By: Representative Bryant of the 160 th A BILL TO BE ENTITLED AN ACT 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 To amend Title 44 of the Official Code of Georgia Annotated, relating to property,

The Mortgage Brokerages and Mortgage Administrators Act

MORTGAGE BROKERAGES AND 1 The Mortgage Brokerages and Mortgage Administrators Act being Chapter M-20.1* of The Statutes of Saskatchewan, 2007 (effective October 1, 2010), as amended by the Statutes of

MORTGAGE BROKERAGES AND 1 The Mortgage Brokerages and Mortgage Administrators Act being Chapter M-20.1* of The Statutes of Saskatchewan, 2007 (effective October 1, 2010), as amended by the Statutes of

CHAPTER 493. REGULATORY LOANS. REGULATORY LOAN ACT Act 21 of 1939. The People of the State of Michigan enact:

CHAPTER 493. REGULATORY LOANS REGULATORY LOAN ACT Act 21 of 1939 AN ACT to define and regulate the business of making regulatory loans; to permit the licensing of persons engaged in that business; to provide

CHAPTER 493. REGULATORY LOANS REGULATORY LOAN ACT Act 21 of 1939 AN ACT to define and regulate the business of making regulatory loans; to permit the licensing of persons engaged in that business; to provide

Title 9-A: MAINE CONSUMER CREDIT CODE

Title 9-A: MAINE CONSUMER CREDIT CODE Article 10: LOAN BROKERS Table of Contents Part 1. GENERAL PROVISIONS... 3 Section 10-101. SHORT TITLE... 3 Section 10-102. DEFINITIONS... 3 Part 2. REGISTRATION AND

Title 9-A: MAINE CONSUMER CREDIT CODE Article 10: LOAN BROKERS Table of Contents Part 1. GENERAL PROVISIONS... 3 Section 10-101. SHORT TITLE... 3 Section 10-102. DEFINITIONS... 3 Part 2. REGISTRATION AND

Debt Collection From the Debtor s Perspective. A Few Facts About the Debt Burden of American Households. Debt Facts 8/14/2013

Debt Collection From the Debtor s Perspective Linda Cook Senior Staff Attorney Ohio Poverty Law Center lcook@ohiopovertylaw.org 2013 Ohio Poverty Law Center A Few Facts About the Debt Burden of American

Debt Collection From the Debtor s Perspective Linda Cook Senior Staff Attorney Ohio Poverty Law Center lcook@ohiopovertylaw.org 2013 Ohio Poverty Law Center A Few Facts About the Debt Burden of American

VOLUNTARY PETITION I. APPLICABLE LAW AND RULES

Instructions, Form B1 11.21.12 VOLUNTARY PETITION This form, known as a voluntary petition must be used by a debtor to begin a bankruptcy case. Filing this petition is how an individual or other entity

Instructions, Form B1 11.21.12 VOLUNTARY PETITION This form, known as a voluntary petition must be used by a debtor to begin a bankruptcy case. Filing this petition is how an individual or other entity

OCCUPATIONS CODE TITLE 8. REGULATION OF ENVIRONMENTAL AND INDUSTRIAL TRADES CHAPTER 1303. RESIDENTIAL SERVICE COMPANIES. As Revised and in Effect on

OCCUPATIONS CODE TITLE 8. REGULATION OF ENVIRONMENTAL AND INDUSTRIAL TRADES CHAPTER 1303. RESIDENTIAL SERVICE COMPANIES As Revised and in Effect on September 1, 2009 Texas Real Estate Commission P.O. Box

OCCUPATIONS CODE TITLE 8. REGULATION OF ENVIRONMENTAL AND INDUSTRIAL TRADES CHAPTER 1303. RESIDENTIAL SERVICE COMPANIES As Revised and in Effect on September 1, 2009 Texas Real Estate Commission P.O. Box

CONSUMER LOAN BROKER ACT. 81-19-11. Investigation of applicant; issuance or denial of license; time limit for acting on applications.

CONSUMER LOAN BROKER ACT Section 81-19-1. Short title. 81-19-3. Definitions. 81-19-5. License requirement; penalty for violation. 81-19-7. Exclusions from chapter coverage. 81-19-9. License application;

CONSUMER LOAN BROKER ACT Section 81-19-1. Short title. 81-19-3. Definitions. 81-19-5. License requirement; penalty for violation. 81-19-7. Exclusions from chapter coverage. 81-19-9. License application;

SENATE FILE NO. SF0013. Sponsored by: Joint Minerals, Business and Economic Development Interim Committee A BILL. for

00 STATE OF WYOMING 0LSO-00 SENATE FILE NO. SF00 Residential Mortgage Practices Act. Sponsored by: Joint Minerals, Business and Economic Development Interim Committee A BILL for AN ACT relating to trade

00 STATE OF WYOMING 0LSO-00 SENATE FILE NO. SF00 Residential Mortgage Practices Act. Sponsored by: Joint Minerals, Business and Economic Development Interim Committee A BILL for AN ACT relating to trade

Credit Repair Organizations Act

Credit Repair Organizations Act Title IV of the Consumer Credit Protection Act (Public Law 90-321, 82 Stat. 164) is amended to read as follows: TITLE IV--CREDIT REPAIR ORGANIZATIONS'' Sec. 401. Short title.

Credit Repair Organizations Act Title IV of the Consumer Credit Protection Act (Public Law 90-321, 82 Stat. 164) is amended to read as follows: TITLE IV--CREDIT REPAIR ORGANIZATIONS'' Sec. 401. Short title.

PHILADELPHIA BOARD OF ETHICS REGULATION NO. 1 CAMPAIGN FINANCE. Table of Contents

PHILADELPHIA BOARD OF ETHICS REGULATION NO. 1 CAMPAIGN FINANCE Table of Contents Subpart A. Scope; Definitions Subpart B. Contribution Limits Subpart C. Excess Pre-Candidacy Contributions; Excess Post-Candidacy

PHILADELPHIA BOARD OF ETHICS REGULATION NO. 1 CAMPAIGN FINANCE Table of Contents Subpart A. Scope; Definitions Subpart B. Contribution Limits Subpart C. Excess Pre-Candidacy Contributions; Excess Post-Candidacy

CHAPTER 2--CREDIT REPAIR ORGANIZATIONS SEC. 2451. REGULATION OF CREDIT REPAIR ORGANIZATIONS.

CODES COMPLAINTS EMPLOYEE CERTIFICATION FEDERAL LAWS NACSO GUIDELINES LOG OUT CHAPTER 2--CREDIT REPAIR ORGANIZATIONS SEC. 2451. REGULATION OF CREDIT REPAIR ORGANIZATIONS. Title IV of the Consumer Credit

CODES COMPLAINTS EMPLOYEE CERTIFICATION FEDERAL LAWS NACSO GUIDELINES LOG OUT CHAPTER 2--CREDIT REPAIR ORGANIZATIONS SEC. 2451. REGULATION OF CREDIT REPAIR ORGANIZATIONS. Title IV of the Consumer Credit

MORTGAGE LOAN ORIGINATOR LICENSING ACT Act 75 of 2009. The People of the State of Michigan enact:

MORTGAGE LOAN ORIGINATOR LICENSING ACT Act 75 of 2009 AN ACT to provide for the licensing of mortgage loan originators; to regulate the business practices of mortgage loan originators; to establish certain

MORTGAGE LOAN ORIGINATOR LICENSING ACT Act 75 of 2009 AN ACT to provide for the licensing of mortgage loan originators; to regulate the business practices of mortgage loan originators; to establish certain

Senate. File No. 757. Approved by the Legislative Commissioner May 3, 2014

Senate General Assembly File No. 757 February Session, 2014 (Reprint of File No. 191) Substitute Senate Bill No. 209 As Amended by Senate Amendment Schedule "A" and House Amendment Schedule "A" Approved

Senate General Assembly File No. 757 February Session, 2014 (Reprint of File No. 191) Substitute Senate Bill No. 209 As Amended by Senate Amendment Schedule "A" and House Amendment Schedule "A" Approved

CREDIT INSURANCE ACT Act 173 of 1958. The People of the State of Michigan enact:

CREDIT INSURANCE ACT Act 173 of 1958 AN ACT to provide for the regulation of credit life insurance and credit accident and health insurance; to define the powers and duties of the state commissioner of

CREDIT INSURANCE ACT Act 173 of 1958 AN ACT to provide for the regulation of credit life insurance and credit accident and health insurance; to define the powers and duties of the state commissioner of

Regular Session, 2008. ACT No. 858. To amend and reenact R.S. 9:3573.1, 3573.2(A), 3573.3(1), (8), (9) and (10), 3573.4,

, 3573.3(1), (8), (9) and (10), 3573.4,") Regular Session, 0 SENATE BILL NO. ACT No. BY SENATOR MARIONNEAUX 0 AN ACT To amend and reenact R.S. :.,.(A),.(), (), () and (0),.,.(A)(),.0(C),.(B) and (C),.(B) and (C), and., and to repeal R.S. :.(),.,

Regular Session, 0 SENATE BILL NO. ACT No. BY SENATOR MARIONNEAUX 0 AN ACT To amend and reenact R.S. :.,.(A),.(), (), () and (0),.,.(A)(),.0(C),.(B) and (C),.(B) and (C), and., and to repeal R.S. :.(),.,

COLORADO FAIR DEBT COLLECTION PRACTICES ACT COLORADO CHILD SUPPORT COLLECTION CONSUMER PROTECTION ACT RELATED LAWS AND RULES. (Effective July 1, 2011)

") COLORADO FAIR DEBT COLLECTION PRACTICES ACT COLORADO CHILD SUPPORT COLLECTION CONSUMER PROTECTION ACT RELATED LAWS AND RULES (Effective July 1, 2011) Table of Contents ARTICLE 14 COLORADO FAIR DEBT COLLECTION

COLORADO FAIR DEBT COLLECTION PRACTICES ACT COLORADO CHILD SUPPORT COLLECTION CONSUMER PROTECTION ACT RELATED LAWS AND RULES (Effective July 1, 2011) Table of Contents ARTICLE 14 COLORADO FAIR DEBT COLLECTION

NC General Statutes - Chapter 75 Article 4 1

Article 4. Telephone Solicitations. 75-100. Findings. The General Assembly finds all of the following: (1) The use of the telephone to market goods and services to the home is now pervasive due to the

Article 4. Telephone Solicitations. 75-100. Findings. The General Assembly finds all of the following: (1) The use of the telephone to market goods and services to the home is now pervasive due to the

UNDERSTANDING THE COLLECTION PROCESS FOR COMMUNITY ASSOCIATIONS

UNDERSTANDING THE COLLECTION PROCESS FOR COMMUNITY ASSOCIATIONS 1. PRE-LITIGATION BY: MULCAHY LAW FIRM, P.C. Almost every community association has problems in collecting unpaid assessments. Most associations

UNDERSTANDING THE COLLECTION PROCESS FOR COMMUNITY ASSOCIATIONS 1. PRE-LITIGATION BY: MULCAHY LAW FIRM, P.C. Almost every community association has problems in collecting unpaid assessments. Most associations

NEW YORK STATE DEPARTMENT OF FINANCIAL SERVICES 23 NYCRR 1 DEBT COLLECTION BY THIRD-PARTY DEBT COLLECTORS AND DEBT BUYERS

NEW YORK STATE DEPARTMENT OF FINANCIAL SERVICES 23 NYCRR 1 DEBT COLLECTION BY THIRD-PARTY DEBT COLLECTORS AND DEBT BUYERS I, Benjamin M. Lawsky, Superintendent of Financial Services, pursuant to the authority

NEW YORK STATE DEPARTMENT OF FINANCIAL SERVICES 23 NYCRR 1 DEBT COLLECTION BY THIRD-PARTY DEBT COLLECTORS AND DEBT BUYERS I, Benjamin M. Lawsky, Superintendent of Financial Services, pursuant to the authority

Debt Collection. Federal Trade Commission consumer.ftc.gov

Debt Collection Federal Trade Commission consumer.ftc.gov If you re behind in paying your bills, or a creditor s records mistakenly make it appear that you are, a debt collector may be contacting you.

Debt Collection Federal Trade Commission consumer.ftc.gov If you re behind in paying your bills, or a creditor s records mistakenly make it appear that you are, a debt collector may be contacting you.

CHAPTER 49. PROSECUTING ATTORNEYS. CRIMINAL PROCEEDINGS IN SUPREME COURT Act 72 of 1887. The People of the State of Michigan enact:

CHAPTER 49. PROSECUTING ATTORNEYS CRIMINAL PROCEEDINGS IN SUPREME COURT Act 72 of 1887 AN ACT to require prosecuting attorneys to appear and conduct criminal proceedings in the supreme court in certain

CHAPTER 49. PROSECUTING ATTORNEYS CRIMINAL PROCEEDINGS IN SUPREME COURT Act 72 of 1887 AN ACT to require prosecuting attorneys to appear and conduct criminal proceedings in the supreme court in certain

SUPREME COURT OF PENNSYLVANIA DOMESTIC RELATIONS PROCEDURAL RULES COMMITTEE RECOMMENDATION 140

SUPREME COURT OF PENNSYLVANIA DOMESTIC RELATIONS PROCEDURAL RULES COMMITTEE RECOMMENDATION 140 CHAPTER 1950. ACTIONS PURSUANT TO THE PROTECTION OF VICTIMS OF SEXUAL VIOLENCE OR INTIMIDATION ACT Rule 1951.

SUPREME COURT OF PENNSYLVANIA DOMESTIC RELATIONS PROCEDURAL RULES COMMITTEE RECOMMENDATION 140 CHAPTER 1950. ACTIONS PURSUANT TO THE PROTECTION OF VICTIMS OF SEXUAL VIOLENCE OR INTIMIDATION ACT Rule 1951.

LOUISIANA REVISED STATUTES TITLE 9. CIVIL CODE BOOK III OF THE DIFFERENT MODES OF ACQUIRING THE OWNERSHIP OF THINGS CODE TITLE VII SALE

2941. "Bond for deed" defined LOUISIANA REVISED STATUTES TITLE 9. CIVIL CODE BOOK III OF THE DIFFERENT MODES OF ACQUIRING THE OWNERSHIP OF THINGS CODE TITLE VII SALE CHAPTER 2. Conventional Sales PART

2941. "Bond for deed" defined LOUISIANA REVISED STATUTES TITLE 9. CIVIL CODE BOOK III OF THE DIFFERENT MODES OF ACQUIRING THE OWNERSHIP OF THINGS CODE TITLE VII SALE CHAPTER 2. Conventional Sales PART

House Proposal of Amendment S. 7 An act relating to social networking privacy protection. The House proposes to the Senate to amend the bill by

House Proposal of Amendment S. 7 An act relating to social networking privacy protection. The House proposes to the Senate to amend the bill by striking all after the enacting clause and inserting in lieu

House Proposal of Amendment S. 7 An act relating to social networking privacy protection. The House proposes to the Senate to amend the bill by striking all after the enacting clause and inserting in lieu

Chapter 339. (House Bill 392) Commercial Law Debt Settlement Services Study

Commercial Law Debt Settlement Services Study") Chapter 339 (House Bill 392) AN ACT concerning Commercial Law Debt Settlement Services Study FOR the purpose of prohibiting a person from offering, providing, or attempting to provide debt settlement services

Chapter 339 (House Bill 392) AN ACT concerning Commercial Law Debt Settlement Services Study FOR the purpose of prohibiting a person from offering, providing, or attempting to provide debt settlement services

CHAPTER 80G BULLION COIN DEALERS

1 MINNESOTA STATUTES 2015 80G.01 CHAPTER 80G BULLION COIN DEALERS 80G.01 DEFINITIONS. 80G.02 REGISTRATION. 80G.03 REGISTRATION DENIAL, NONRENEWAL, REVOCATION, AND SUSPENSION. 80G.04 CRIMINAL CONVICTIONS.

1 MINNESOTA STATUTES 2015 80G.01 CHAPTER 80G BULLION COIN DEALERS 80G.01 DEFINITIONS. 80G.02 REGISTRATION. 80G.03 REGISTRATION DENIAL, NONRENEWAL, REVOCATION, AND SUSPENSION. 80G.04 CRIMINAL CONVICTIONS.

METHODIST HEALTH SYSTEM ADMINISTRATIVE TITLE: DETECTING FRAUD AND ABUSE AND AN OVERVIEW OF THE FEDERAL AND STATE FALSE CLAIMS ACTS

METHODIST HEALTH SYSTEM ADMINISTRATIVE Formulated: 6/19/07 Reviewed: Revised: Effective: 10/30/07 TITLE: DETECTING FRAUD AND ABUSE AND AN OVERVIEW OF THE FEDERAL AND STATE FALSE CLAIMS ACTS PURPOSE: Methodist

METHODIST HEALTH SYSTEM ADMINISTRATIVE Formulated: 6/19/07 Reviewed: Revised: Effective: 10/30/07 TITLE: DETECTING FRAUD AND ABUSE AND AN OVERVIEW OF THE FEDERAL AND STATE FALSE CLAIMS ACTS PURPOSE: Methodist

SUMMARY OF THE FAIR DEBT COLLECTION PRACTICES STATUTES

STATE OF CALIFORNIA STATE AND CONSUMER SERVICES AGENCY ARNOLD SCHWARZENEGGER, Governor CALIFORNIA DEPARTMENT OF CONSUMER AFFAIRS DIVISION OF LEGAL AFFAIRS 1625 NORTH MARKET BLVD. SACRAMENTO, CA 95834 Legal

STATE OF CALIFORNIA STATE AND CONSUMER SERVICES AGENCY ARNOLD SCHWARZENEGGER, Governor CALIFORNIA DEPARTMENT OF CONSUMER AFFAIRS DIVISION OF LEGAL AFFAIRS 1625 NORTH MARKET BLVD. SACRAMENTO, CA 95834 Legal

3. "Consumer reporting agency" has the meaning ascribed to it in 15 U.S.C. Sec. 1681a(f).

.") Combo security freeze bill with consensus areas. Where no consensus: AG language in left column, CDIA language in right column. In some cases, differences on specific points are identified in text of bill.

Combo security freeze bill with consensus areas. Where no consensus: AG language in left column, CDIA language in right column. In some cases, differences on specific points are identified in text of bill.

IC 28-1-29 Chapter 29. Debt Management Companies

IC 28-1-29 Chapter 29. Debt Management Companies IC 28-1-29-0.5 Inapplicability; attorneys; depository financial institutions; third-party bill paying services Sec. 0.5. (a) This chapter does not apply

IC 28-1-29 Chapter 29. Debt Management Companies IC 28-1-29-0.5 Inapplicability; attorneys; depository financial institutions; third-party bill paying services Sec. 0.5. (a) This chapter does not apply

Mortgage Loan Company Act

Mortgage Loan Company Act CHAPTER 58 ARTICLE 21 Mortgage Loan Companies and Loan Brokers Section: 58-21-1 Short title. 58-21-2 Definitions. 58-21-3 License required; qualified manager. 58-21-4 Application

Mortgage Loan Company Act CHAPTER 58 ARTICLE 21 Mortgage Loan Companies and Loan Brokers Section: 58-21-1 Short title. 58-21-2 Definitions. 58-21-3 License required; qualified manager. 58-21-4 Application

CHARITABLE ORGANIZATIONS AND SOLICITATIONS ACT Act 169 of 1975. The People of the State of Michigan enact:

CHARITABLE ORGANIZATIONS AND SOLICITATIONS ACT Act 169 of 1975 AN ACT to regulate charitable organizations, professional fund raisers and other persons soliciting or collecting contributions on behalf

CHARITABLE ORGANIZATIONS AND SOLICITATIONS ACT Act 169 of 1975 AN ACT to regulate charitable organizations, professional fund raisers and other persons soliciting or collecting contributions on behalf

State of New Hampshire Banking Department ) ) ) ) ) Cease and Desist Order Department, ) ) ) ) ) ) ) ) ) ) ) Case No.: 08-228 NOTICE OF ORDER

) ) ) ) Cease and Desist Order Department, ) ) ) ) ) ) ) ) ) ) ) Case No.: 08-228 NOTICE OF ORDER") 1 State of New Hampshire Banking Department Case No.: 0- In re the Matter of: State of New Hampshire Banking Cease and Desist Order Department, Petitioner, and Magnum Cash Advance (d/b/a International

1 State of New Hampshire Banking Department Case No.: 0- In re the Matter of: State of New Hampshire Banking Cease and Desist Order Department, Petitioner, and Magnum Cash Advance (d/b/a International

SENATE STAFF ANALYSIS AND ECONOMIC IMPACT STATEMENT

SENATE STAFF ANALYSIS AND ECONOMIC IMPACT STATEMENT (This document is based on the provisions contained in the legislation as of the latest date listed below.) BILL: SB 2240 SPONSOR: SUBJECT: Senator Garcia

SENATE STAFF ANALYSIS AND ECONOMIC IMPACT STATEMENT (This document is based on the provisions contained in the legislation as of the latest date listed below.) BILL: SB 2240 SPONSOR: SUBJECT: Senator Garcia

Chapter 307. (Senate Bill 585) Commercial Law Patent Infringement Assertions Made in Bad Faith

Commercial Law Patent Infringement Assertions Made in Bad Faith") Chapter 307 (Senate Bill 585) AN ACT concerning Commercial Law Patent Infringement Assertions Made in Bad Faith FOR the purpose of prohibiting a person from making certain assertions of patent infringement

Chapter 307 (Senate Bill 585) AN ACT concerning Commercial Law Patent Infringement Assertions Made in Bad Faith FOR the purpose of prohibiting a person from making certain assertions of patent infringement

Compliance Plan False Claims Act & Whistleblower Provisions Purpose/Policy/Procedures

CATHOLIC CHARITIES OF THE ROMAN CATHOLIC DIOCESE OF SYRACUSE, NY and TOOMEY RESIDENTIAL AND COMMUNITY SERVICES Compliance Plan False Claims Act & Whistleblower Provisions Purpose/Policy/Procedures Purpose:

CATHOLIC CHARITIES OF THE ROMAN CATHOLIC DIOCESE OF SYRACUSE, NY and TOOMEY RESIDENTIAL AND COMMUNITY SERVICES Compliance Plan False Claims Act & Whistleblower Provisions Purpose/Policy/Procedures Purpose:

History: Add. 1971, Act 19, Imd. Eff. May 5, 1971; Am. 1976, Act 89, Imd. Eff. Apr. 17, 1976.

MOTOR VEHICLE ACCIDENT CLAIMS ACT Act 198 of 1965 AN ACT providing for the establishment, maintenance and administration of a motor vehicle accident claims fund for the payment of damages for injury to

MOTOR VEHICLE ACCIDENT CLAIMS ACT Act 198 of 1965 AN ACT providing for the establishment, maintenance and administration of a motor vehicle accident claims fund for the payment of damages for injury to

Title IV of the Consumer Credit Protection Act (Public Law 90-321, 82 Stat. 164) is amended to read as follows:

is amended to read as follows:") The Credit Repair Organizations Act CHAPTER 2--CREDIT REPAIR ORGANIZATIONS(1) SEC. 2451. REGULATION OF CREDIT REPAIR ORGANIZATIONS. Title IV of the Consumer Credit Protection Act (Public Law 90-321, 82

The Credit Repair Organizations Act CHAPTER 2--CREDIT REPAIR ORGANIZATIONS(1) SEC. 2451. REGULATION OF CREDIT REPAIR ORGANIZATIONS. Title IV of the Consumer Credit Protection Act (Public Law 90-321, 82

63rd Legislature AN ACT GENERALLY REVISING THE MONTANA DEFERRED DEPOSIT LOAN ACT; EXTENDING THE TIME

63rd Legislature HB0116 AN ACT GENERALLY REVISING THE MONTANA DEFERRED DEPOSIT LOAN ACT; EXTENDING THE TIME TO REQUEST A HEARING; ADDING PENALTIES INCLUDING FORFEITURE OF LOAN PRINCIPAL FOR LOANS MADE

63rd Legislature HB0116 AN ACT GENERALLY REVISING THE MONTANA DEFERRED DEPOSIT LOAN ACT; EXTENDING THE TIME TO REQUEST A HEARING; ADDING PENALTIES INCLUDING FORFEITURE OF LOAN PRINCIPAL FOR LOANS MADE

(c) Providing advice or assistance to a buyer with regard to either subdivision (a) or (b) of this paragraph.

Providing advice or assistance to a buyer with regard to either subdivision (a) or (b) of this paragraph.") ARIZONA CREDIT REPAIR LAWS Arizona Credit Repair Organizations Act Title 44. Trade and Commerce Chapter 11. Regulations Concerning Particular Businesses Article 7. Credit Services 44-1701. Definitions

ARIZONA CREDIT REPAIR LAWS Arizona Credit Repair Organizations Act Title 44. Trade and Commerce Chapter 11. Regulations Concerning Particular Businesses Article 7. Credit Services 44-1701. Definitions

The Trust and Loan Corporations Act, 1997

1 The Trust and Loan Corporations Act, 1997 being Chapter T-22.2* of the Statutes of Saskatchewan, 1997 (effective September 1, 1999, clause 44(a), and section 57 not yet proclaimed) as amended by the

1 The Trust and Loan Corporations Act, 1997 being Chapter T-22.2* of the Statutes of Saskatchewan, 1997 (effective September 1, 1999, clause 44(a), and section 57 not yet proclaimed) as amended by the

In the United States District Court for the Northern District of Georgia Atlanta Division

Case 1:14-cv-02211-AT Document 61-1 Filed 12/28/15 Page 1 of 20 In the United States District Court for the Northern District of Georgia Atlanta Division Consumer Financial Protection Bureau, Plaintiff,

Case 1:14-cv-02211-AT Document 61-1 Filed 12/28/15 Page 1 of 20 In the United States District Court for the Northern District of Georgia Atlanta Division Consumer Financial Protection Bureau, Plaintiff,

ASSEMBLY BILL No. 597

AMENDED IN ASSEMBLY APRIL 14, 2015 california legislature 2015 16 regular session ASSEMBLY BILL No. 597 Introduced by Assembly Member Cooley February 24, 2015 An act to amend Sections 36 and 877 of, and

AMENDED IN ASSEMBLY APRIL 14, 2015 california legislature 2015 16 regular session ASSEMBLY BILL No. 597 Introduced by Assembly Member Cooley February 24, 2015 An act to amend Sections 36 and 877 of, and

MICHIGAN S LEMON L AW: HOW TO AVOID GETTING STUCK WITH A LEMON CONSUMER PROTECTION DIVISION DEPARTMENT OF THE ATTORNEY GENERAL

CONSUMER PROTECTION DIVISION DEPARTMENT OF THE ATTORNEY GENERAL MICHIGAN S LEMON L AW: HOW TO AVOID GETTING STUCK WITH A LEMON JENNIFER M. GRANHOLM ATTORNEY GENERAL JENNIFER M. GRANHOLM ATTORNEY GENERAL

CONSUMER PROTECTION DIVISION DEPARTMENT OF THE ATTORNEY GENERAL MICHIGAN S LEMON L AW: HOW TO AVOID GETTING STUCK WITH A LEMON JENNIFER M. GRANHOLM ATTORNEY GENERAL JENNIFER M. GRANHOLM ATTORNEY GENERAL

CREDIT REPAIR ORGANIZATIONS ACT 15 U.S.C. 1679 et. seq.

CREDIT REPAIR ORGANIZATIONS ACT 15 U.S.C. 1679 et. seq. Please note that the information contained herein should not be construed as legal advice and is intended for informational purposes only. In addition,

CREDIT REPAIR ORGANIZATIONS ACT 15 U.S.C. 1679 et. seq. Please note that the information contained herein should not be construed as legal advice and is intended for informational purposes only. In addition,

ORDERED, ADJUDGED AND DECREED,

STEPHEN CALKINS General Counsel CAROLE A. PAYNTER (CP 4091) Federal Trade Commission 150 William Street, 13th floor New York, New York 10038 (212) 264-1225 Attorneys for Plaintiff UNITED STATES DISTRICT

STEPHEN CALKINS General Counsel CAROLE A. PAYNTER (CP 4091) Federal Trade Commission 150 William Street, 13th floor New York, New York 10038 (212) 264-1225 Attorneys for Plaintiff UNITED STATES DISTRICT

Enrolled Copy S.B. 54

1 CREDIT MONITORING FOR MINORS 2 2015 GENERAL SESSION 3 STATE OF UTAH 4 Chief Sponsor: Aaron Osmond 5 House Sponsor: Rich Cunningham 6 7 LONG TITLE 8 General Description: 9 This bill modifies and enacts

1 CREDIT MONITORING FOR MINORS 2 2015 GENERAL SESSION 3 STATE OF UTAH 4 Chief Sponsor: Aaron Osmond 5 House Sponsor: Rich Cunningham 6 7 LONG TITLE 8 General Description: 9 This bill modifies and enacts

The Trunkett Law Firm 2271 McGregor Blvd., Suite 300 Fort Myers, FL 33901 (239) 790-4529 www.trunkettlaw.com

790-4529 www.trunkettlaw.com") Credit Card Case Intake Form Date: Name: Address: Cell Phone: Home Phone: Work Phone: Email: **Email is the preferred method of communication by the Trunkett Law Firm. All documents and correspondence

Credit Card Case Intake Form Date: Name: Address: Cell Phone: Home Phone: Work Phone: Email: **Email is the preferred method of communication by the Trunkett Law Firm. All documents and correspondence

2. "Consumer" means an individual. (same as 15 U.S.C. 1681a(c))

)") Combo security freeze bill with consensus areas. Where no consensus: AG language in left column, CDIA language in right column. In some cases, differences on specific points are identified in text of bill.

Combo security freeze bill with consensus areas. Where no consensus: AG language in left column, CDIA language in right column. In some cases, differences on specific points are identified in text of bill.

TITLE 34. LABOR AND WORKERS' COMPENSATION CHAPTER 19. CONSCIENTIOUS EMPLOYEE PROTECTION ACT. N.J. Stat. 34:19-1 (2007)

") TITLE 34. LABOR AND WORKERS' COMPENSATION CHAPTER 19. CONSCIENTIOUS EMPLOYEE PROTECTION ACT N.J. Stat. 34:19-1 (2007) 34:19-1. Short title This act shall be known and may [be] cited as the "Conscientious

TITLE 34. LABOR AND WORKERS' COMPENSATION CHAPTER 19. CONSCIENTIOUS EMPLOYEE PROTECTION ACT N.J. Stat. 34:19-1 (2007) 34:19-1. Short title This act shall be known and may [be] cited as the "Conscientious

NC General Statutes - Chapter 53 Article 21 1

Article 21. Reverse Mortgages. 53-255. Title. This Article shall be known and may be cited as the Reverse Mortgage Act. (1991, c. 546, s. 1; 1995, c. 115, s. 1.) 53-256. Purpose. It is the intent of the

Article 21. Reverse Mortgages. 53-255. Title. This Article shall be known and may be cited as the Reverse Mortgage Act. (1991, c. 546, s. 1; 1995, c. 115, s. 1.) 53-256. Purpose. It is the intent of the

Policies and Procedures: WVUPC Policy Pursuant to the Requirements of the Deficit Reduction Act of 2005

POLICY/PROCEDURE NO.: B-17 Effective date: Jan. 1, 2007 Date(s) of review/revision: Nov. 1, 2015 Policies and Procedures: WVUPC Policy Pursuant to the Requirements of the Deficit Reduction Act of 2005

POLICY/PROCEDURE NO.: B-17 Effective date: Jan. 1, 2007 Date(s) of review/revision: Nov. 1, 2015 Policies and Procedures: WVUPC Policy Pursuant to the Requirements of the Deficit Reduction Act of 2005

How To Prevent A Telephone Solicitation In North Dakota

CHAPTER 51-28 TELEPHONE SOLICITATIONS 51-28-01. Definitions. In this chapter, unless the context or subject matter otherwise requires, the terms shall have the meanings as follows: 1. "Automatic dialing-announcing

CHAPTER 51-28 TELEPHONE SOLICITATIONS 51-28-01. Definitions. In this chapter, unless the context or subject matter otherwise requires, the terms shall have the meanings as follows: 1. "Automatic dialing-announcing

LIQUIDATION UNDER CHAPTER 7

LIQUIDATION UNDER CHAPTER 7 1. WHAT IS CHAPTER 7 AND HOW DOES IT WORK? Chapter 7 is that part (or chapter) of the Bankruptcy Code that deals with liquidation. The Bankruptcy Code is that part of the federal

LIQUIDATION UNDER CHAPTER 7 1. WHAT IS CHAPTER 7 AND HOW DOES IT WORK? Chapter 7 is that part (or chapter) of the Bankruptcy Code that deals with liquidation. The Bankruptcy Code is that part of the federal