Changing Discount Rates for Determining Lump Sums An Analysis by the Pension Committee of the American Academy of Actuaries

|

|

|

- Darren Bernard Mills

- 8 years ago

- Views:

Transcription

1 Changing Discount Rates for Determining Lump Sums An Analysis by the Pension Committee of the American Academy of Actuaries Donald J. Segal, FSA, MAAA, Chair Ron Gebhardtsbauer, FSA, MAAA, Senior Pension Fellow June 17, 2003

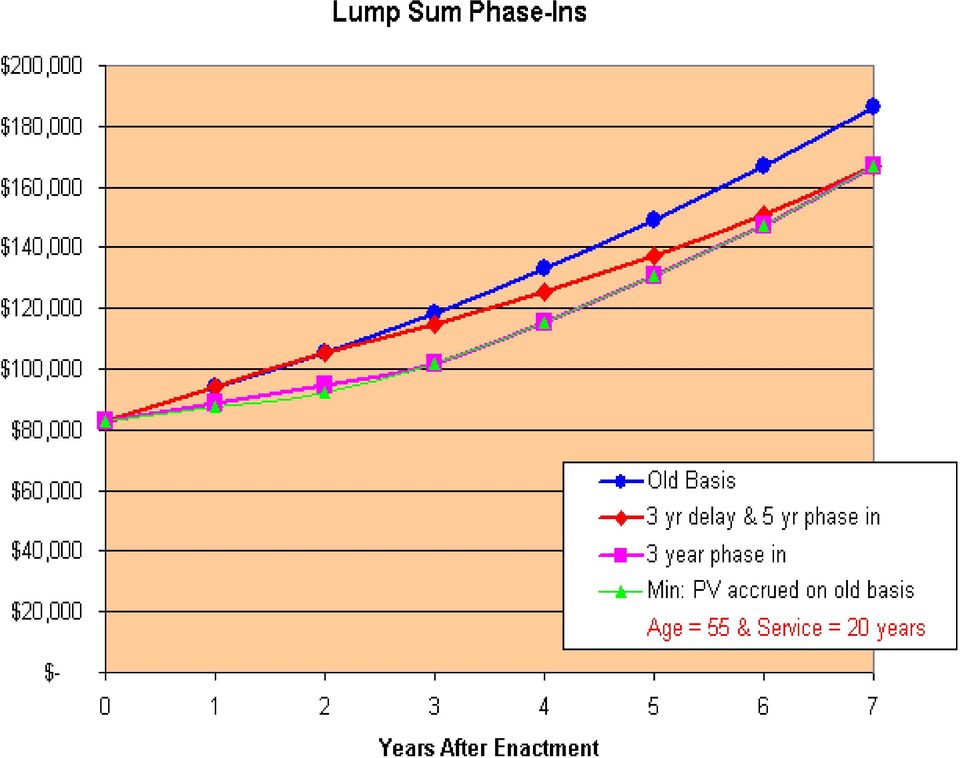

2 Changing Discount Rates for Determining Lump Sums The minimum lump sum payable from a pension plan has increased dramatically due to the unusually low 30-year Treasury rates of the past few years. This has made pension plans that have lump sum provisions much more expensive than the plan sponsor ever intended. Proposals to increase the lump sum interest rate could reduce lump sums unless they provide a transition period. This paper discusses the reasons why a change is needed and provides information on possible transition rules. The attached charts show that a 3-year or 5-year transition to the new interest rate will keep lump sums from decreasing, whether the employee is young or approaching retirement. History: In the early 1980s, interest rates were above 10 percent and lump sums became quite small. In the Retirement Equity Act of 1984, Congress mandated that the minimum lump sum be based on Pension Benefit Guaranty Corporation (PBGC) discount factors (which at that time were 10 percent for benefits payable immediately). By 1993, PBGC s interest factors were all under 5 percent, and for various reasons PBGC changed its method for setting its discount factors. Their rate for retired employees increased by about 150 basis points, which would have reduced lump sums by 10 percent or more. For this reason (and others), PBGC asked Congress to stop using this rate for determining lump sums. For reasons of simplicity, PBGC suggested that Congress choose just one rate (regardless of whether the lump sum was larger or smaller than $25,000 and whether payments were payable immediately or after a long deferral period). In the Retirement Protection Act of 1994, Congress chose the 30-year Treasury rate, which at the time was larger than the old PBGC discount factor by over 150 basis points, and slightly larger than the new PBGC discount factor. In 1998, however, the 30-year Treasury rate fell below the new PBGC discount factor. It has made lump sums larger than if the PBGC factors were used and thus, larger than the cost of the pensions using insurance company pricing (which is what the PBGC factors are based on). Several reasons have been suggested for the unusually low Treasury rates. In 1998, for the first time in over 30 years, projections from the Congressional Budget Office (CBO) suggested that the US would pay off its public debt in 8 years. In 2001, Treasury announced that they would no longer issue 30-year Treasuries. Meanwhile, due to falling stock markets, investors have sought Treasury bonds in greater numbers. The law of supply and demand suggests that with reduced supply (and continued demand), prices will go up. Treasury bond prices did go up and their interest rates dropped. In fact, they dropped faster than corporate bond rates. Today the 30-year Treasury rate is under 4.4 percent - the lowest in almost 50 years. Problems with Using the Low 30-year Treasury Rate: As discussed in our testimony before House Ways & Means on April 30, 2003, 1 there are several concerns caused by using the unusually low 30-year Treasury rate. For example: Spousal benefits The use of Treasury rates for determining lump sums makes the lump sum amount so large that it discourages employees from taking the 1 Challenges Facing Pension Plans at 2

3 plan s automatic joint and survivor annuity. This conflicts with the original intent of ERISA to encourage pensions for surviving spouses. Public policy Taking lump sums may be viewed negatively from a public policy perspective because more retirees will spend down their lump sum too quickly and end up relying on government assistance (Supplemental Security Income and Medicaid). Plans funding levels The payment of a lump sum from an underfunded plan decreases the funding ratio, particularly if the lump sum is subsidized by the unusually low Treasury rate. In addition, plans will tend to be less well funded, because Notice prohibits the subsidy from being included in the current liability calculation. This is not only a concern for participants 2 but also for the PBGC. Increased costs beyond amounts intended Plan sponsors have to contribute more funds to the plan because the low Treasury rate made lump sums larger (not because the employer decided to increase lump sums). Thus, the plan is more expensive than the employer originally intended. Obstruction of collective bargaining process Due to the expense of paying larger lump sums, plan sponsors are less able to make plan improvements suggested by workers at the next bargaining period. Thus, requiring the Treasury rate supplants the collective bargaining process and discriminates against participants that don t take lump sums. If employees were permitted to decide where the funds should go, labor organization staff have stated that employees would probably bargain to use the funds to improve the benefit formula for all workers, as opposed to those who just take lump sums. Transition Rules: Changing to a higher interest rate can reduce a worker s lump sum, so a transition rule may be helpful. For example, some organizations suggest gradually changing to a composite corporate bond rate over three years. This 3-year phase-in could limit the increase in the interest rate to about 34 basis points per year. 3 We note that Treasury rates have increased in the past. In 1996 and 1999, the rate went up 150 basis points, so this would not be the first time participants have experienced an increase in lump sum interest rates. In the legislation introduced by Reps. Portman and Cardin, the transition is delayed 3 years and then phased in over 5 years. The delay protects nearterm retirees from any change in the lump sum amount. Furthermore, with a 3 or 5-year transition, a worker s lump sum will not go down. It will grow because each year workers get additional service and pay increases, and their age gets one year closer to their normal retirement date (NRD). 4 In fact, our calculations show that transition rules would keep lump sums from decreasing even if the worker does not receive a pay increase or their service is greater than the plan maximum. Lump sums can go down, however, for younger employees who had quit employment in the past but had not taken 2 For example, retirees of Polaroid are suing their former employer for paying the mandated, subsidized lump sums to recent retirees, because they are defunding the plan. This means the retirees will have their benefits cut down to the guaranteed benefit by PBGC. 3 Unless all interest rates rise dramatically in the next three years. 4 Each year, participants get one year closer to their normal retirement date (NRD), which means their lump sum increases by one year s interest rate (unless they are already beyond their NRD, in which case the lump sum can decrease but this already happens without changing interest rates). 3

4 their lump sum. Thus, we would recommend that employers notify them of the change and allow them to cash out before the change takes effect. The attached calculations and graphs show the effects of three different transition rules (the Erisa Industry s 3-year phase-in, Portman-Cardin s delayed 5-year phase-in, and the current anti-cutback rule) on the lump sum amount. We have assumed that interest rates will remain where they are today. If interest rates go up or down, it will push all of the lump sum amounts proportionately. The graphs confirm that lump sum amounts will always increase during the transition to the new interest rate, even if the worker s service exceeds the plan maximum, or if the worker does not receive a pay increase. The calculations also assume that the new rate is a composite corporate bond rate equal to the average of the High-Quality Long-Term bond indices of Merrill Lynch, Salomon, Moody s, and Lehman. This rate is now about 100 basis points higher than the 30-year Treasury rate. 5 Maximum Lump Sums: In addition, we suggest Congress simplify the very complex calculations caused by 415(b)(2)(E) for maximum lump sums. One simple alternative suggested by the American Society of Pension Actuaries (ASPA) would be to use just one interest rate. Our paper, Alternatives to the 30-Year Treasury Rate, suggested that it could be somewhere in the 5 percent to 8 percent range. The Academy has also suggested to the Treasury Department in the past that the rules could be greatly simplified by deleting the words or the rate specified in the plan in 415(b)(2)(E), so that the maximum lump sum would be the same in all plans (and the discount rate used above and below the NRA would be the same). 5 In July of 1994 this composite rate was about 67 basis points higher than the Treasury rate. In May of 2000, it was over 200 basis points higher, because high-quality corporate bond rates did not fall as fast as Treasury rates. 4

5 Lump Sum Phase-Ins $35,000 $30,000 $25,000 $20,000 $15,000 $10,000 $5,000 $- Old Basis 3 yr delay & 5 yr phase in 3 year phase in Min: PV accrued on old basis Age = 35 & Service = 5 years Years After Enactment 5

6 6

Retirement Plan Participants and/or Beneficiaries. Harvard Human Resources, Benefits. Annual Funding Notice Harvard University Retirement Plan

Richard A. and Susan F. Smith Campus Center 1350 Massachusetts Avenue Cambridge, MA 02138 TO: FROM: SUBJECT: Retirement Plan Participants and/or Beneficiaries Harvard Human Resources, Benefits Annual Funding

Richard A. and Susan F. Smith Campus Center 1350 Massachusetts Avenue Cambridge, MA 02138 TO: FROM: SUBJECT: Retirement Plan Participants and/or Beneficiaries Harvard Human Resources, Benefits Annual Funding

ANNUAL FUNDING NOTICE For THE UNIVERSITY OF CHICAGO PENSION PLAN FOR STAFF EMPLOYEES. Introduction

ANNUAL FUNDING NOTICE For THE UNIVERSITY OF CHICAGO PENSION PLAN FOR STAFF EMPLOYEES Introduction This notice includes important information about the funding status of your single employer pension plan

ANNUAL FUNDING NOTICE For THE UNIVERSITY OF CHICAGO PENSION PLAN FOR STAFF EMPLOYEES Introduction This notice includes important information about the funding status of your single employer pension plan

Domestic Relations. Journal of Ohio

Domestic Relations Stanley Morganstern, Esq. Editor-in-Chief Journal of Ohio Laurel G. Streim Esq. Associate Editor July / August 2006 Volume 18 Issue 4 IN THIS ISSUE: Valuing Pension Benefits in Divorce

Domestic Relations Stanley Morganstern, Esq. Editor-in-Chief Journal of Ohio Laurel G. Streim Esq. Associate Editor July / August 2006 Volume 18 Issue 4 IN THIS ISSUE: Valuing Pension Benefits in Divorce

Pension Protection Act of 2006 Changes Affect Single-Employer Defined Benefit Plans in 2008

Important Information Legislation June 2007 Pension Protection Act of 2006 Changes Affect Single-Employer Defined Benefit Plans in 2008 This is one of a series of Pension Analyst publications providing

Important Information Legislation June 2007 Pension Protection Act of 2006 Changes Affect Single-Employer Defined Benefit Plans in 2008 This is one of a series of Pension Analyst publications providing

Pension Protection Act of 2006 Makes Significant Changes to Single Employer Defined Benefit Plans

Important Information Legislation November 2006 Pension Protection Act of 2006 Makes Significant Changes to Single Employer Defined Benefit Plans This is one of a series of Pension Analyst publications

Important Information Legislation November 2006 Pension Protection Act of 2006 Makes Significant Changes to Single Employer Defined Benefit Plans This is one of a series of Pension Analyst publications

CRS Report for Congress

December 3, 2007 CRS Report for Congress Lump-Sum Distributions under the Pension Protection Act Summary Patrick Purcell Specialist in Income Security Domestic Social Policy Division The Pension Protection

December 3, 2007 CRS Report for Congress Lump-Sum Distributions under the Pension Protection Act Summary Patrick Purcell Specialist in Income Security Domestic Social Policy Division The Pension Protection

Executive Summary. Introduction

2013 ERISA Advisory Council Private Sector Pension De-risking and Participant Protections Testimony of John G. Ferreira Partner, Morgan, Lewis & Bockius LLP 1 Executive Summary In my view, there is no

2013 ERISA Advisory Council Private Sector Pension De-risking and Participant Protections Testimony of John G. Ferreira Partner, Morgan, Lewis & Bockius LLP 1 Executive Summary In my view, there is no

MAP-21 SUPPLEMENT TO ANNUAL FUNDING NOTICE

MAP-21 SUPPLEMENT TO ANNUAL FUNDING NOTICE OF THE ACADEMY OF NATURAL SCIENCES OF PHILADELPHIA PENSION PLAN FOR PLAN YEAR BEGINNING JANUARY 1, 2013 AND ENDING DECEMBER 31, 2013 ( Plan Year ) This is a temporary

MAP-21 SUPPLEMENT TO ANNUAL FUNDING NOTICE OF THE ACADEMY OF NATURAL SCIENCES OF PHILADELPHIA PENSION PLAN FOR PLAN YEAR BEGINNING JANUARY 1, 2013 AND ENDING DECEMBER 31, 2013 ( Plan Year ) This is a temporary

April 29, 2016. Dear Colleague,

Loral R. Blinde Vice President People & Employee Services April 29, 2016 Dear Colleague, I am pleased to share the enclosed Annual Funding Notice, which details information about your pension plan, the

Loral R. Blinde Vice President People & Employee Services April 29, 2016 Dear Colleague, I am pleased to share the enclosed Annual Funding Notice, which details information about your pension plan, the

PRESENT LAW AND BACKGROUND RELATING TO EMPLOYER-SPONSORED DEFINED BENEFIT PENSION PLANS AND THE PENSION BENEFIT GUARANTY CORPORATION ( PBGC )

") PRESENT LAW AND BACKGROUND RELATING TO EMPLOYER-SPONSORED DEFINED BENEFIT PENSION PLANS AND THE PENSION BENEFIT GUARANTY CORPORATION ( PBGC ) Scheduled for a Public Hearing Before the SENATE COMMITTEE

PRESENT LAW AND BACKGROUND RELATING TO EMPLOYER-SPONSORED DEFINED BENEFIT PENSION PLANS AND THE PENSION BENEFIT GUARANTY CORPORATION ( PBGC ) Scheduled for a Public Hearing Before the SENATE COMMITTEE

SUPPLEMENT TO ANNUAL FUNDING NOTICE OF MAYO PENSION PLAN FOR PLAN YEAR BEGINNING JANUARY 1, 2015 AND ENDING DECEMBER 31, 2015 ( Plan Year )

") SUPPLEMENT TO ANNUAL FUNDING NOTICE OF MAYO PENSION PLAN FOR PLAN YEAR BEGINNING JANUARY 1, 2015 AND ENDING DECEMBER 31, 2015 ( Plan Year ) This is a temporary supplement to your annual funding notice.

SUPPLEMENT TO ANNUAL FUNDING NOTICE OF MAYO PENSION PLAN FOR PLAN YEAR BEGINNING JANUARY 1, 2015 AND ENDING DECEMBER 31, 2015 ( Plan Year ) This is a temporary supplement to your annual funding notice.

Notice to Participants in the Visa Retirement Plan

Notice to Participants in the Visa Retirement Plan In August, Visa announced that the Visa International and Visa USA Boards recently endorsed a new retirement plan formula that replaces the current benefit

Notice to Participants in the Visa Retirement Plan In August, Visa announced that the Visa International and Visa USA Boards recently endorsed a new retirement plan formula that replaces the current benefit

Benefit Reductions in the Central States Multiemployer DB Pension Plan: Frequently Asked Questions

Benefit Reductions in the Central States Multiemployer DB Pension Plan: Frequently Asked Questions John J. Topoleski Analyst in Income Security Gary Sidor Technical Information Specialist January 28, 2016

Benefit Reductions in the Central States Multiemployer DB Pension Plan: Frequently Asked Questions John J. Topoleski Analyst in Income Security Gary Sidor Technical Information Specialist January 28, 2016

Lump-Sum Pension Payments: 2008 and Beyond

BENEFITS INFORMATION BULLETIN Milliman Employee Benefits December 14, 2007 BIB 07-01 Effective for plan years beginning in 2008, ERISA-covered defined benefit retirement plans that offer participants lump-sum

BENEFITS INFORMATION BULLETIN Milliman Employee Benefits December 14, 2007 BIB 07-01 Effective for plan years beginning in 2008, ERISA-covered defined benefit retirement plans that offer participants lump-sum

ANNUAL FUNDING NOTICE For The Johns Hopkins University Support Staff Pension Plan. Introduction

Human Resources Benefits Service Center Johns Hopkins at Eastern 1101 E. 33 rd Street, Suite D100 Baltimore, MD 21218-2696 410-516-2000 / Fax 443-997-5820 ANNUAL FUNDING NOTICE For The Johns Hopkins University

Human Resources Benefits Service Center Johns Hopkins at Eastern 1101 E. 33 rd Street, Suite D100 Baltimore, MD 21218-2696 410-516-2000 / Fax 443-997-5820 ANNUAL FUNDING NOTICE For The Johns Hopkins University

Subcommittee on Employer-Employee Relations Committee on Education and the Workforce U.S. House of Representatives 2175 Rayburn House Office Building

Subcommittee on Employer-Employee Relations Committee on Education and the Workforce U.S. House of Representatives 2175 Rayburn House Office Building Hearing on: Examining Long-Term Solutions to Reform

Subcommittee on Employer-Employee Relations Committee on Education and the Workforce U.S. House of Representatives 2175 Rayburn House Office Building Hearing on: Examining Long-Term Solutions to Reform

Preventing Disastrous DB Distributions Sunday, April 28, 2013

Preventing Disastrous DB Distributions Sunday, April 28, 2013 David B. Farber, ASA, COPA, EA, MSPA Defined Benefit Distributions Participant must elect form of benefit prior to payment from plan Types

Preventing Disastrous DB Distributions Sunday, April 28, 2013 David B. Farber, ASA, COPA, EA, MSPA Defined Benefit Distributions Participant must elect form of benefit prior to payment from plan Types

Basics of Corporate Pension Plan Funding

Basics of Corporate Pension Plan Funding A White Paper by Manning & Napier www.manning-napier.com Unless otherwise noted, all figures are based in USD. 1 Introduction In general, a pension plan is a promise

Basics of Corporate Pension Plan Funding A White Paper by Manning & Napier www.manning-napier.com Unless otherwise noted, all figures are based in USD. 1 Introduction In general, a pension plan is a promise

Actuarial Speak 101 Terms and Definitions

Actuarial Speak 101 Terms and Definitions Introduction and Caveat: It is intended that all definitions and explanations are accurate. However, for purposes of understanding and clarity of key points, the

Actuarial Speak 101 Terms and Definitions Introduction and Caveat: It is intended that all definitions and explanations are accurate. However, for purposes of understanding and clarity of key points, the

April 2015. Dear Consolidated Edison Retirement Plan Participant:

Consolidated Edison Company of New York, Inc. 4 Irving Place New York NY 10003-0987 April 2015 Dear Consolidated Edison Retirement Plan Participant: The Consolidated Edison Retirement Plan is subject to

Consolidated Edison Company of New York, Inc. 4 Irving Place New York NY 10003-0987 April 2015 Dear Consolidated Edison Retirement Plan Participant: The Consolidated Edison Retirement Plan is subject to

96.30% 82.88% 93.20% 81.98% 97.73% 85.79% $252,254 $1,357,845 $490,361 $1,477,463 $167,281 $1,193,625 $0 $0 $0 $0 $0 $0 INFORMATION TABLE

SUPPLEMENT TO ANNUAL FUNDING NOTICE OF COLUMBIA UNIVERSITY RETIREMENT PLAN FOR SUPPORTING STAFF ( PLAN ) FOR PLAN YEAR BEGINNING JULY 1, 2014 AND ENDING JUNE 30, 2015 This is a temporary supplement to

SUPPLEMENT TO ANNUAL FUNDING NOTICE OF COLUMBIA UNIVERSITY RETIREMENT PLAN FOR SUPPORTING STAFF ( PLAN ) FOR PLAN YEAR BEGINNING JULY 1, 2014 AND ENDING JUNE 30, 2015 This is a temporary supplement to

Freezing Defined Benefit Plans

View the online version at http://us.practicallaw.com/6-502-3611 Freezing Defined Benefit Plans DAVID N. LEVINE AND LARS C. GOLUMBIC, GROOM LAW GROUP, CHARTERED This Practice Note provides a basic overview

View the online version at http://us.practicallaw.com/6-502-3611 Freezing Defined Benefit Plans DAVID N. LEVINE AND LARS C. GOLUMBIC, GROOM LAW GROUP, CHARTERED This Practice Note provides a basic overview

IRS Issues Proposed Regulations and New Guidance Regarding Lifetime Income Payments Under Retirement Plans

IRS Issues Proposed Regulations and New Guidance Regarding Lifetime Income Payments Under Retirement Plans The Treasury and IRS released proposed regulations and guidance that would make it easier for

IRS Issues Proposed Regulations and New Guidance Regarding Lifetime Income Payments Under Retirement Plans The Treasury and IRS released proposed regulations and guidance that would make it easier for

Actuarial Speak 101 Terms and Definitions

Actuarial Speak 101 Terms and Definitions Introduction and Caveat: It is intended that all definitions and explanations are accurate. However, for purposes of understanding and clarity of key points, the

Actuarial Speak 101 Terms and Definitions Introduction and Caveat: It is intended that all definitions and explanations are accurate. However, for purposes of understanding and clarity of key points, the

""" PBGC Pension Benefit Guaranty Corporation Protecting America's Pensions 1200 K Street, N.W., Washington, D.C. 20005-4026

""" PBGC Pension Benefit Guaranty Corporation Protecting America's Pensions 1200 K Street, N.W., Washington, D.C. 20005-4026 August 29, 2014 I' Re: Appeal 2013-11111; Case~ (the or the "Plan") Dear-: T~oard

""" PBGC Pension Benefit Guaranty Corporation Protecting America's Pensions 1200 K Street, N.W., Washington, D.C. 20005-4026 August 29, 2014 I' Re: Appeal 2013-11111; Case~ (the or the "Plan") Dear-: T~oard

Title IV Treatment of Rollovers from Defined Contribution Plans to Defined Benefit Plans

[Billing Code 7709-02-P] PENSION BENEFIT GUARANTY CORPORATION 29 CFR Parts 4001, 4022, and 4044 RIN 1212-AB23 Title IV Treatment of Rollovers from Defined Contribution Plans to Defined Benefit Plans AGENCY:

[Billing Code 7709-02-P] PENSION BENEFIT GUARANTY CORPORATION 29 CFR Parts 4001, 4022, and 4044 RIN 1212-AB23 Title IV Treatment of Rollovers from Defined Contribution Plans to Defined Benefit Plans AGENCY:

The Impact of Pension Reform Proposals on Claims Against the Pension Insurance Program, Losses to Participants, and Contributions

The Impact of Pension Reform Proposals on Claims Against the Pension Insurance Program, Losses to Participants, and Contributions Pension Benefit Guaranty Corporation October 26, 2005 Contents Introduction

The Impact of Pension Reform Proposals on Claims Against the Pension Insurance Program, Losses to Participants, and Contributions Pension Benefit Guaranty Corporation October 26, 2005 Contents Introduction

Annual Funding Notice For TOTAL Finance USA, Inc. Cash Balance Pension Plan

Annual Funding Notice For TOTAL Finance USA, Inc. Cash Balance Pension Plan Introduction This notice includes important information about the funding status of your pension plan ( the Plan ) and general

Annual Funding Notice For TOTAL Finance USA, Inc. Cash Balance Pension Plan Introduction This notice includes important information about the funding status of your pension plan ( the Plan ) and general

The following questions were about a general understanding of FTAP and why it is important.

Employee meetings were held on May 17, 2012 and May 21, 2012 to discuss employee questions relating to the Retirement Plan of Marathon Oil Company ( Retirement Plan ) Funding Target Attainment Percentage

Employee meetings were held on May 17, 2012 and May 21, 2012 to discuss employee questions relating to the Retirement Plan of Marathon Oil Company ( Retirement Plan ) Funding Target Attainment Percentage

2014 ANNUAL FUNDING NOTICE FOR CENTRAL STATES, SOUTHEAST AND SOUTHWEST AREAS PENSION PLAN

2014 ANNUAL FUNDING NOTICE FOR CENTRAL STATES, SOUTHEAST AND SOUTHWEST AREAS PENSION PLAN Introduction This notice includes important information about the funding status of your multiemployer pension

2014 ANNUAL FUNDING NOTICE FOR CENTRAL STATES, SOUTHEAST AND SOUTHWEST AREAS PENSION PLAN Introduction This notice includes important information about the funding status of your multiemployer pension

The 2004 Report of the Social Security Trustees: Social Security Shortfalls, Social Security Reform and Higher Education

POLICY BRIEF Visit us at: www.tiaa-crefinstitute.org. September 2004 The 2004 Report of the Social Security Trustees: Social Security Shortfalls, Social Security Reform and Higher Education The 2004 Social

POLICY BRIEF Visit us at: www.tiaa-crefinstitute.org. September 2004 The 2004 Report of the Social Security Trustees: Social Security Shortfalls, Social Security Reform and Higher Education The 2004 Social

NYS Teamsters Conference Pension & Retirement Fund

NYS Teamsters Conference Pension & Retirement Fund 1. Pension Protection Act of 2006 ( PPA ) pages 2-18 2. Rehabilitation Plan Schedules pages 20-39 3. Employer Surcharges pages 41-45 4. Questions Pension

NYS Teamsters Conference Pension & Retirement Fund 1. Pension Protection Act of 2006 ( PPA ) pages 2-18 2. Rehabilitation Plan Schedules pages 20-39 3. Employer Surcharges pages 41-45 4. Questions Pension

Defined Benefit Retirement Plan. Summary Plan Description

Defined Benefit Retirement Plan Summary Plan Description This booklet is not the Plan document, but only a summary of its main provisions and not every limitation or detail of the Plan is included. Every

Defined Benefit Retirement Plan Summary Plan Description This booklet is not the Plan document, but only a summary of its main provisions and not every limitation or detail of the Plan is included. Every

WHAT CAN WE LEARN FROM SIX COMMON ANNUITY PURCHASE MISCONCEPTIONS?

THOUGHTCAPITAL OCTOBER 2014 PENSION RISK MANAGEMENT: WHAT CAN WE LEARN FROM SIX COMMON ANNUITY PURCHASE MISCONCEPTIONS? For decades, an annuity purchase has offered a safe and effective way for DB plan

THOUGHTCAPITAL OCTOBER 2014 PENSION RISK MANAGEMENT: WHAT CAN WE LEARN FROM SIX COMMON ANNUITY PURCHASE MISCONCEPTIONS? For decades, an annuity purchase has offered a safe and effective way for DB plan

Pension plan terminations: Minimizing cost and risk

Pension plan terminations: Minimizing cost and risk Vanguard commentary May 2011 It is well understood and accepted these days that the nature of a pension plan s liability affects its investment strategy

Pension plan terminations: Minimizing cost and risk Vanguard commentary May 2011 It is well understood and accepted these days that the nature of a pension plan s liability affects its investment strategy

GAO STATE AND LOCAL GOVERNMENT RETIREE BENEFITS. Current Funded Status of Pension and Health Benefits. Report to the Committee on Finance, U.S.

GAO United States Government Accountability Office Report to the Committee on Finance, U.S. Senate January 2008 STATE AND LOCAL GOVERNMENT RETIREE BENEFITS Current Funded Status of Pension and Health Benefits

GAO United States Government Accountability Office Report to the Committee on Finance, U.S. Senate January 2008 STATE AND LOCAL GOVERNMENT RETIREE BENEFITS Current Funded Status of Pension and Health Benefits

Annual Funding Notice for Retirement Plan for Staff Employees

Annual Funding Notice for Retirement Plan for Staff Employees Introduction This notice includes important funding information about your pension plan ( the Plan ). This notice also provides a summary of

Annual Funding Notice for Retirement Plan for Staff Employees Introduction This notice includes important funding information about your pension plan ( the Plan ). This notice also provides a summary of

De-risking Alternatives for Plan Sponsors Compliance Requirements. April 16, 2015 Presented by: Michael Falk, Erin Kartheiser, and Steve Flores

De-risking Alternatives for Plan Sponsors Compliance Requirements April 16, 2015 Presented by: Michael Falk, Erin Kartheiser, and Steve Flores Today s elunch Presenters Michael Falk Partner, Employee Benefits

De-risking Alternatives for Plan Sponsors Compliance Requirements April 16, 2015 Presented by: Michael Falk, Erin Kartheiser, and Steve Flores Today s elunch Presenters Michael Falk Partner, Employee Benefits

PLAN SPONSOR BASICS: CASH BALANCE PLANS. Presenters: John Ferreira and Jared Rogers March 31, 2015. 2015 Morgan, Lewis & Bockius LLP

PLAN SPONSOR BASICS: CASH BALANCE PLANS Presenters: John Ferreira and Jared Rogers March 31, 2015 2015 Morgan, Lewis & Bockius LLP Overview of Today s Training Introduction to Cash Balance Plans Brief

PLAN SPONSOR BASICS: CASH BALANCE PLANS Presenters: John Ferreira and Jared Rogers March 31, 2015 2015 Morgan, Lewis & Bockius LLP Overview of Today s Training Introduction to Cash Balance Plans Brief

Overview of Hybrid Plans (Cash Balance and Pension Equity Plans)

") Overview of Hybrid Plans (Cash Balance and Pension Equity Plans) By: Al Reich Reviewers: Steve Klubock, Anita Bower, and Bill Anderson Overview INTERNAL REVENUE SERVICE TAX EXEMPT AND GOVERNMENT ENTITIES

Overview of Hybrid Plans (Cash Balance and Pension Equity Plans) By: Al Reich Reviewers: Steve Klubock, Anita Bower, and Bill Anderson Overview INTERNAL REVENUE SERVICE TAX EXEMPT AND GOVERNMENT ENTITIES

IRS Publishes Final Rules for Required Payments From Defined Benefit Plans

IMPORTANT INFORMATION Distributions and Withdrawals November 2005 IRS Publishes Final Rules for Required Payments From Defined Benefit Plans WHO'S AFFECTED These rules apply to sponsors of and participants

IMPORTANT INFORMATION Distributions and Withdrawals November 2005 IRS Publishes Final Rules for Required Payments From Defined Benefit Plans WHO'S AFFECTED These rules apply to sponsors of and participants

Christian Brothers Employee Retirement Plan

7.1.2014.SummaryPlanDescription.001018 Christian Brothers Employee Retirement Plan July 1, 2014 Christian Brothers Retirement Planning Services 1205 Windham Parkway, Romeoville, IL 60446-1679 800.807.0700

7.1.2014.SummaryPlanDescription.001018 Christian Brothers Employee Retirement Plan July 1, 2014 Christian Brothers Retirement Planning Services 1205 Windham Parkway, Romeoville, IL 60446-1679 800.807.0700

Earning Cash Balance Pay Credits

You Have a Choice New Cash Balance Pension You Have a Choice The important thing to understand is this: If you were hired through December 31, 2012 you don t have to change to the new cash balance pension

You Have a Choice New Cash Balance Pension You Have a Choice The important thing to understand is this: If you were hired through December 31, 2012 you don t have to change to the new cash balance pension

Pension. Presented by Frank Minter & Al Duscher

Pension Presented by Frank Minter & Al Duscher DRIVING INTO THE FUTURE AND LOOKING IN THE REARVIEW MIRROR HELPFUL TO UNDERSTAND THE HISTORY OF HOW WE GOT TO WHERE WE ARE NOW WHAT HAS CHANGED? WHY IS ALU

Pension Presented by Frank Minter & Al Duscher DRIVING INTO THE FUTURE AND LOOKING IN THE REARVIEW MIRROR HELPFUL TO UNDERSTAND THE HISTORY OF HOW WE GOT TO WHERE WE ARE NOW WHAT HAS CHANGED? WHY IS ALU

U.S. DEPARTMENT OF LABOR. Office of Inspector General. PWBA Needs to Improve Oversight of Cash Balance Plan Lump Sum Distributions

U.S. DEPARTMENT OF LABOR Office of Inspector General PWBA Needs to Improve Oversight of Cash Balance Plan Lump Sum Distributions U.S. Department of Labor Office of Inspector General Report No. 09-02-001-12-121

U.S. DEPARTMENT OF LABOR Office of Inspector General PWBA Needs to Improve Oversight of Cash Balance Plan Lump Sum Distributions U.S. Department of Labor Office of Inspector General Report No. 09-02-001-12-121

Scheduled for a Public Hearing Before the SUBCOMMITTEE ON SELECT REVENUE MEASURES of the HOUSE COMMITTEE ON WAYS AND MEANS on June 28, 2005

PRESENT LAW AND BACKGROUND RELATING TO MULTIEMPLOYER DEFINED BENEFIT PENSION PLANS AND RELATED PROVISIONS OF H.R. 2830, THE PENSION PROTECTION ACT OF 2005 Scheduled for a Public Hearing Before the SUBCOMMITTEE

PRESENT LAW AND BACKGROUND RELATING TO MULTIEMPLOYER DEFINED BENEFIT PENSION PLANS AND RELATED PROVISIONS OF H.R. 2830, THE PENSION PROTECTION ACT OF 2005 Scheduled for a Public Hearing Before the SUBCOMMITTEE

LDI for DB plans with lump sum benefit payment options

PRACTICE NOTE LDI for DB plans with lump sum benefit payment options Justin Owens, FSA, CFA, EA, Senior Asset Allocation Strategist Valerie Dion, CFA, FSA, Senior Consultant ISSUE: How does a lump sum

PRACTICE NOTE LDI for DB plans with lump sum benefit payment options Justin Owens, FSA, CFA, EA, Senior Asset Allocation Strategist Valerie Dion, CFA, FSA, Senior Consultant ISSUE: How does a lump sum

Glossary of Qualified

Glossary of Qualified Retirement Plan Terms 401(k) Plan: A qualified profit sharing or stock bonus plan under which plan participants have an option to put money into the plan or receive the same amount

Glossary of Qualified Retirement Plan Terms 401(k) Plan: A qualified profit sharing or stock bonus plan under which plan participants have an option to put money into the plan or receive the same amount

An Actuarial Perspective on Pension Plan Funding

An Actuarial Perspective on Pension Plan Funding Donald J. Segal September 2013 PRC WP2013-13 Pension Research Council Working Paper Pension Research Council The Wharton School, University of Pennsylvania

An Actuarial Perspective on Pension Plan Funding Donald J. Segal September 2013 PRC WP2013-13 Pension Research Council Working Paper Pension Research Council The Wharton School, University of Pennsylvania

How To Understand Retirement Plans

Retirement, Health, and Life Insurance Part Two Chapter Four Employer-Sponsored Retirement Plans Chapter Outline Defining Retirement Plans Origins of Employer-Sponsored Retirement Benefits Trends in Retirement

Retirement, Health, and Life Insurance Part Two Chapter Four Employer-Sponsored Retirement Plans Chapter Outline Defining Retirement Plans Origins of Employer-Sponsored Retirement Benefits Trends in Retirement

Legal Alert: Pension Protection Act of 2006 Changes Affecting Defined Contribution Plans

Legal Alert: Pension Protection Act of 2006 Changes Affecting Defined Contribution Plans August 16, 2006 A little more than half of the 907 pages of the Pension Protection Act of 2006 deal with pension

Legal Alert: Pension Protection Act of 2006 Changes Affecting Defined Contribution Plans August 16, 2006 A little more than half of the 907 pages of the Pension Protection Act of 2006 deal with pension

Hughes Hubbard & Reed LLP

Hughes Hubbard & Reed LLP EMPLOYEE BENEFITS ADVISORY May 2001 Required GUST Amendments for Qualified Retirement Plans The deadline for adopting GUST amendments to qualified retirement plans and submitting

Hughes Hubbard & Reed LLP EMPLOYEE BENEFITS ADVISORY May 2001 Required GUST Amendments for Qualified Retirement Plans The deadline for adopting GUST amendments to qualified retirement plans and submitting

CRS Report for Congress Received through the CRS Web

Order Code RS21115 Updated March 11, 2002 CRS Report for Congress Received through the CRS Web The Enron Bankruptcy and Employer Stock in Retirement Plans Summary Patrick J. Purcell Specialist in Social

Order Code RS21115 Updated March 11, 2002 CRS Report for Congress Received through the CRS Web The Enron Bankruptcy and Employer Stock in Retirement Plans Summary Patrick J. Purcell Specialist in Social

CRS Report for Congress

Order Code RL30631 CRS Report for Congress Received through the CRS Web Retirement Benefits for Members of Congress Updated January 21, 2005 Patrick J. Purcell Specialist in Social Legislation Domestic

Order Code RL30631 CRS Report for Congress Received through the CRS Web Retirement Benefits for Members of Congress Updated January 21, 2005 Patrick J. Purcell Specialist in Social Legislation Domestic

QDRO APPROVAL GUIDELINES AND PROCEDURES

QDRO APPROVAL GUIDELINES AND PROCEDURES Retirement Plan of Marathon Oil Company Effective date of this document: January 1, 2012 FOR ASSISTANCE CREATING A QDRO, GO TO: ****** QDRO.FIDELITY.COM *******

QDRO APPROVAL GUIDELINES AND PROCEDURES Retirement Plan of Marathon Oil Company Effective date of this document: January 1, 2012 FOR ASSISTANCE CREATING A QDRO, GO TO: ****** QDRO.FIDELITY.COM *******

Kimberly-Clark Corporation U.S. Pension Plan

Kimberly-Clark Corporation U.S. Pension Plan April 2013 Dear Plan Participant: Here is your Annual Funding Notice for the Kimberly-Clark Corporation U.S. Pension Plan as of December 31, 2012. Also, instructions

Kimberly-Clark Corporation U.S. Pension Plan April 2013 Dear Plan Participant: Here is your Annual Funding Notice for the Kimberly-Clark Corporation U.S. Pension Plan as of December 31, 2012. Also, instructions

Personal Retirement Account Plan Summary Plan Description

Personal Retirement Account Plan Summary Plan Description Table of Contents Who Is Eligible...1 When You Participate...1 When You Are Vested...1 Break in Service...1 Maternity/Paternity Absence...1 Your

Personal Retirement Account Plan Summary Plan Description Table of Contents Who Is Eligible...1 When You Participate...1 When You Are Vested...1 Break in Service...1 Maternity/Paternity Absence...1 Your

The GPO predominantly penalizes women educators in California, while the WEP penalizes many individuals who switch careers into public service.

Chair Pomeroy and Members, Social Security has met the social insurance promise to ensure workers will not have to live in old age poverty. This promise needs to be guaranteed for current and future workers.

Chair Pomeroy and Members, Social Security has met the social insurance promise to ensure workers will not have to live in old age poverty. This promise needs to be guaranteed for current and future workers.

Recent Trends In Pension Buyouts And Lump Sum Offers

Portfolio Media. Inc. 860 Broadway, 6th Floor New York, NY 10003 www.law360.com Phone: +1 646 783 7100 Fax: +1 646 783 7161 customerservice@law360.com Recent Trends In Pension Buyouts And Lump Sum Offers

Portfolio Media. Inc. 860 Broadway, 6th Floor New York, NY 10003 www.law360.com Phone: +1 646 783 7100 Fax: +1 646 783 7161 customerservice@law360.com Recent Trends In Pension Buyouts And Lump Sum Offers

37390 Federal Register / Vol. 73, No. 127 / Tuesday, July 1, 2008 / Proposed Rules

37390 Federal Register / Vol. 73, No. 127 / Tuesday, July 1, 2008 / Proposed Rules Drafting Information The principal author of these regulations is Matthew P. Howard of the Office of the Associate Chief

37390 Federal Register / Vol. 73, No. 127 / Tuesday, July 1, 2008 / Proposed Rules Drafting Information The principal author of these regulations is Matthew P. Howard of the Office of the Associate Chief

BORGWARNER INC. RETIREMENT PLAN - CASH BALANCE COMPONENT SUMMARY PLAN DESCRIPTION

BORGWARNER INC. RETIREMENT PLAN - CASH BALANCE COMPONENT SUMMARY PLAN DESCRIPTION 2008 TABLE OF CONTENTS Page INTRODUCTION... 1 ELIGIBILITY TO PARTICIPATE... 2 Who is eligible to participate in the Plan?...

BORGWARNER INC. RETIREMENT PLAN - CASH BALANCE COMPONENT SUMMARY PLAN DESCRIPTION 2008 TABLE OF CONTENTS Page INTRODUCTION... 1 ELIGIBILITY TO PARTICIPATE... 2 Who is eligible to participate in the Plan?...

The Commuted Value Option at GM

The Commuted Value Option at GM In the September 2012 Detroit 3 negotiations, the CAW agreed to the Ford and GM request on commuted value (CV) options. After December 31, 2012, CAW members retiring with

The Commuted Value Option at GM In the September 2012 Detroit 3 negotiations, the CAW agreed to the Ford and GM request on commuted value (CV) options. After December 31, 2012, CAW members retiring with

Fundamentals of Current Pension Funding and Accounting For Private Sector Pension Plans

Fundamentals of Current Pension Funding and Accounting For Private Sector Pension Plans An Analysis by the Pension Committee of the American Academy of Actuaries July 2004 The American Academy of Actuaries

Fundamentals of Current Pension Funding and Accounting For Private Sector Pension Plans An Analysis by the Pension Committee of the American Academy of Actuaries July 2004 The American Academy of Actuaries

In recent years, plan sponsors have been focusing

November 2012 By Elizabeth Thomas Dold and David N. Levine A Look at Retiree Cashouts as the New De-Risking Strategy Elizabeth Thomas Dold and David N. Levine are Principals at Groom Law Group, Chartered

November 2012 By Elizabeth Thomas Dold and David N. Levine A Look at Retiree Cashouts as the New De-Risking Strategy Elizabeth Thomas Dold and David N. Levine are Principals at Groom Law Group, Chartered

Alcatel-Lucent Retirement Income Plan

Alcatel-Lucent Retirement Income Plan Alcatel USA, Inc. Retirement Plan for Production Employees Provisions of the Alcatel USA, Inc. Consolidated Retirement Plan Summary Plan Description June 1, 2013 DISCLAIMER

Alcatel-Lucent Retirement Income Plan Alcatel USA, Inc. Retirement Plan for Production Employees Provisions of the Alcatel USA, Inc. Consolidated Retirement Plan Summary Plan Description June 1, 2013 DISCLAIMER

COUNTY EMPLOYEES' ANNUITY AND BENEFIT FUND OF COOK COUNTY ACTUARIAL VALUATION AS OF DECEMBER 31,2011

COUNTY EMPLOYEES' ANNUITY AND BENEFIT FUND OF COOK COUNTY ACTUARIAL VALUATION AS OF DECEMBER 31,2011 GOLDSTEIN & ASSOCIATES Actuaries and Consultants 29 SOUTH LaSALLE STREET CHICAGO, ILLINOIS 60603 PHONE

COUNTY EMPLOYEES' ANNUITY AND BENEFIT FUND OF COOK COUNTY ACTUARIAL VALUATION AS OF DECEMBER 31,2011 GOLDSTEIN & ASSOCIATES Actuaries and Consultants 29 SOUTH LaSALLE STREET CHICAGO, ILLINOIS 60603 PHONE

RETIREMENT PLAN STRATEGIES

0213702 For Plan Sponsor and Advisor Use - Public Use Permitted. RETIREMENT PLAN STRATEGIES De-risking pensions emerging opportunity through lump sum cash-outs under the Pension Protection Act of 2006

0213702 For Plan Sponsor and Advisor Use - Public Use Permitted. RETIREMENT PLAN STRATEGIES De-risking pensions emerging opportunity through lump sum cash-outs under the Pension Protection Act of 2006

For a complete list of EBSA publications, call toll-free: 1-866-444-EBSA (3272) This material will be made available in alternate format upon request:

This material will be made available in alternate format upon request:") This publication has been developed by the U.S. Department of Labor, Employee Benefits Security Administration. It is available on the Internet at: www.dol.gov/ebsa For a complete list of EBSA publications,

This publication has been developed by the U.S. Department of Labor, Employee Benefits Security Administration. It is available on the Internet at: www.dol.gov/ebsa For a complete list of EBSA publications,

DOL Provides Guidance on Qualified Domestic Relations Orders

Important Information Plan Administration and Operation September 1997* DOL Provides Guidance on Qualified Domestic Relations Orders WHO'S AFFECTED Qualified Domestic Relations Order rules apply to all

Important Information Plan Administration and Operation September 1997* DOL Provides Guidance on Qualified Domestic Relations Orders WHO'S AFFECTED Qualified Domestic Relations Order rules apply to all

Multiple annuity starting dates.

August 11, 2005 Ms. Linda S. F. Marshall Office of the Division Counsel/Associate Chief Counsel CC:PA:LPD:PR (REG-130241-04) Room 5203 Internal Revenue Service POB 7604 Ben Franklin Station Washington,

August 11, 2005 Ms. Linda S. F. Marshall Office of the Division Counsel/Associate Chief Counsel CC:PA:LPD:PR (REG-130241-04) Room 5203 Internal Revenue Service POB 7604 Ben Franklin Station Washington,

Benefits Handbook Date September 1, 2015. Marsh & McLennan Companies Retirement Plan

Date September 1, 2015 Marsh & McLennan Companies Retirement Plan Marsh & McLennan Companies Marsh & McLennan Companies Retirement Plan The (also referred to as the Plan ) is the central part of the Company

Date September 1, 2015 Marsh & McLennan Companies Retirement Plan Marsh & McLennan Companies Marsh & McLennan Companies Retirement Plan The (also referred to as the Plan ) is the central part of the Company

Evaluating Retiree Cash-out Windows

Evaluating Retiree Cash-out Windows Recent IRS Private Letter Rulings confirm that qualified pension plans that are not terminating can offer participants who are currently receiving annuity payments a

Evaluating Retiree Cash-out Windows Recent IRS Private Letter Rulings confirm that qualified pension plans that are not terminating can offer participants who are currently receiving annuity payments a

Lump Sum Payments for Terminated Vested Participants. 2012 Retirement Webinar Series March 8, 2012

Lump Sum Payments for Terminated Vested Participants 2012 Retirement Webinar Series March 8, 2012 Lump Sum Payments for Terminated Vested Participants Today s Participants Joe McDonald Aon Hewitt Byron

Lump Sum Payments for Terminated Vested Participants 2012 Retirement Webinar Series March 8, 2012 Lump Sum Payments for Terminated Vested Participants Today s Participants Joe McDonald Aon Hewitt Byron

Variable Annuity Pension Plans: A Balanced Approach to Retirement Risk

Variable Annuity Pension Plans: A Balanced Approach to Retirement Kelly Coffing, EA, FSA, MAAA Principal and Consulting Actuary Milliman, Seattle, Washington Grant Camp, EA, FSA, MAAA, Consulting Actuary

Variable Annuity Pension Plans: A Balanced Approach to Retirement Kelly Coffing, EA, FSA, MAAA Principal and Consulting Actuary Milliman, Seattle, Washington Grant Camp, EA, FSA, MAAA, Consulting Actuary

Annuities The Key to a

Annuities The Key to a Secure Retirement 1 Saving for retirement is crucial, and making sure those resources last throughout your lifetime is just as important. Annuities do both helping you save, then

Annuities The Key to a Secure Retirement 1 Saving for retirement is crucial, and making sure those resources last throughout your lifetime is just as important. Annuities do both helping you save, then

IRS Issues Minimum Required Contribution Rules For Defined Benefit Plans

Important Information Plan Administration and Operation July 2008 IRS Issues Minimum Required Contribution Rules For Defined Benefit Plans WHO'S AFFECTED These developments affect sponsors of qualified

Important Information Plan Administration and Operation July 2008 IRS Issues Minimum Required Contribution Rules For Defined Benefit Plans WHO'S AFFECTED These developments affect sponsors of qualified

Raising the Retirement Age for Social Security

A October 2002 I SSUE B RIEF A MERICAN A CADEMY of A CTUARIES Raising the Retirement Age for Social Security When the Social Security program began paying monthly benefits in 1940, workers could receive

A October 2002 I SSUE B RIEF A MERICAN A CADEMY of A CTUARIES Raising the Retirement Age for Social Security When the Social Security program began paying monthly benefits in 1940, workers could receive

Will They Take the Money and Run?

Will They Take the Money and Run? A Perspective on Pension Lump Sum Cash-Outs November 2012 Lockton Retirement Services The tide is changing in favor of personal financial conservatism. Gone are the days

Will They Take the Money and Run? A Perspective on Pension Lump Sum Cash-Outs November 2012 Lockton Retirement Services The tide is changing in favor of personal financial conservatism. Gone are the days

Piecing Together Retirement

Piecing Together Retirement Peace of Mind Financial Planning Provides the Framework Retirement planning is much like planning a trip. You should begin financial planning for retirement well ahead of the

Piecing Together Retirement Peace of Mind Financial Planning Provides the Framework Retirement planning is much like planning a trip. You should begin financial planning for retirement well ahead of the

SOA 2010 Annual Meeting & Exhibit Oct. 17-20, 2010. Session 118 PD, Statutory Hybrid Plans. Moderator: Ellen L. Kleinstuber, ASA, EA, FCA, MAAA, MSPA

SOA 2010 Annual Meeting & Exhibit Oct. 17-20, 2010 Session 118 PD, Statutory Hybrid Plans Moderator: Ellen L. Kleinstuber, ASA, EA, FCA, MAAA, MSPA Presenters: David R. Godofsky, FSA, EA, FCA, MAAA Sarah

SOA 2010 Annual Meeting & Exhibit Oct. 17-20, 2010 Session 118 PD, Statutory Hybrid Plans Moderator: Ellen L. Kleinstuber, ASA, EA, FCA, MAAA, MSPA Presenters: David R. Godofsky, FSA, EA, FCA, MAAA Sarah

TABLE OF CONTENTS. Introduction... 1. Membership... 1. Defined Benefit Portion of the Hybrid... 2. Retirement Benefits for Public Safety Officer...

TABLE OF CONTENTS Introduction... 1 Membership... 1 Defined Benefit Portion of the Hybrid... 2 Retirement Benefits... 4 Retirement Benefits for Public Safety Officer... 5 Cost-of-Living Adjustments after

TABLE OF CONTENTS Introduction... 1 Membership... 1 Defined Benefit Portion of the Hybrid... 2 Retirement Benefits... 4 Retirement Benefits for Public Safety Officer... 5 Cost-of-Living Adjustments after

April 24, 2008. Honorable George Miller Chairman Committee on Education and Labor U.S. House of Representatives Washington, DC 20515

CONGRESSIONAL BUDGET OFFICE U.S. Congress Washington, DC 20515 Peter R. Orszag, Director April 24, 2008 Honorable George Miller Chairman Committee on Education and Labor U.S. House of Representatives Washington,

CONGRESSIONAL BUDGET OFFICE U.S. Congress Washington, DC 20515 Peter R. Orszag, Director April 24, 2008 Honorable George Miller Chairman Committee on Education and Labor U.S. House of Representatives Washington,

PRIVATE PENSIONS. Participants Need Better Information When Offered Lump Sums That Replace Their Lifetime Benefits

United States Government Accountability Office Report to the Ranking Member, Committee on Ways and Means, House of Representatives January 2015 PRIVATE PENSIONS Participants Need Better Information When

United States Government Accountability Office Report to the Ranking Member, Committee on Ways and Means, House of Representatives January 2015 PRIVATE PENSIONS Participants Need Better Information When

Senator Tom Harkin chaired the U.S. Senate

Variable Annuity Pension Plans an Emerging Retirement Plan Design Variable annuity pension plans (VAPPs) are not new but may deserve a second look by plan sponsors seeking a more secure retirement plan

Variable Annuity Pension Plans an Emerging Retirement Plan Design Variable annuity pension plans (VAPPs) are not new but may deserve a second look by plan sponsors seeking a more secure retirement plan

Alert. Client PROSKAUER ROSE SM. Employee Benefits Provisions Under the Economic Growth And Tax Relief Reconciliation Act of 2001

PROSKAUER ROSE SM Client Alert Employee Benefits Provisions Under the Economic Growth And Tax Relief Reconciliation Act of 2001 On June 7, 2001, President Bush signed into law The Economic Growth and Tax

PROSKAUER ROSE SM Client Alert Employee Benefits Provisions Under the Economic Growth And Tax Relief Reconciliation Act of 2001 On June 7, 2001, President Bush signed into law The Economic Growth and Tax

The Pension Protection Act of 2006

Raymond James John Dulay Financial Advisor 550 W. Washington Blvd. Suite 1050 Chicago, IL 60661 312-869-3889 888-711-4301 John.Dulay@raymondjames.com www.truenorthretirementpartners.com The Pension Protection

Raymond James John Dulay Financial Advisor 550 W. Washington Blvd. Suite 1050 Chicago, IL 60661 312-869-3889 888-711-4301 John.Dulay@raymondjames.com www.truenorthretirementpartners.com The Pension Protection

NYU Staff Pension Plan. Summary Plan Description

NYU Staff Pension Plan Summary Plan Description Office & Clerical Staff Laboratory & Technical Staff Non-Union Service Staff Sergeant Guards Security Officers This booklet summarizes the provisions contained

NYU Staff Pension Plan Summary Plan Description Office & Clerical Staff Laboratory & Technical Staff Non-Union Service Staff Sergeant Guards Security Officers This booklet summarizes the provisions contained

Nonqualified Deferred Compensation Plans Why Administration Matters

Nonqualified Deferred Compensation Plans Why Administration Matters By: Howard D. Stern, FSA Vice President & Actuary The Pangburn Company HOWARD D. STERN, FSA is Vice President and Actuary with the Pangburn

Nonqualified Deferred Compensation Plans Why Administration Matters By: Howard D. Stern, FSA Vice President & Actuary The Pangburn Company HOWARD D. STERN, FSA is Vice President and Actuary with the Pangburn

Ameren Retirement Plan Union Cash Balance Supplement

A Plan Designed to Provide Security for Employees of Ameren Retirement Plan Union Cash Balance Supplement Benefits for Certain Contract Employees Amended and Restated January 1, 2012 The following is a

A Plan Designed to Provide Security for Employees of Ameren Retirement Plan Union Cash Balance Supplement Benefits for Certain Contract Employees Amended and Restated January 1, 2012 The following is a

Lump Sums under the Pension Protection Act of 2006

Lump Sums under the Pension Protection Act of 2006 November 15, 2006 An article in the October 25th Wall Street Journal article entitled Changes in Defined-Benefit Plans Affect Many Highly-Paid Workers;

Lump Sums under the Pension Protection Act of 2006 November 15, 2006 An article in the October 25th Wall Street Journal article entitled Changes in Defined-Benefit Plans Affect Many Highly-Paid Workers;

SOA 2011 Annual Meeting & Exhibit Oct. 16-19, 2011. Session 118 OF, Plan Termination Seminar: Session 4 Getting It Done

SOA 2011 Annual Meeting & Exhibit Oct. 16-19, 2011 Session 118 OF, Plan Termination Seminar: Session 4 Getting It Done Moderator: Brian C. Donohue, FSA, EA, FCA, MAAA Presenters: Karen Ambrose Monica L.

SOA 2011 Annual Meeting & Exhibit Oct. 16-19, 2011 Session 118 OF, Plan Termination Seminar: Session 4 Getting It Done Moderator: Brian C. Donohue, FSA, EA, FCA, MAAA Presenters: Karen Ambrose Monica L.

MEMORANDUM. ERISA s Structure

1920 N Street NW Suite 400 Washington, DC 20036-1659 T 202.833.6400 www.segalco.com MEMORANDUM To: From: Hank Kim, Executive Director and Counsel, NCPERS Sarah Mysiewicz Gill, Senior Legal Representative,

1920 N Street NW Suite 400 Washington, DC 20036-1659 T 202.833.6400 www.segalco.com MEMORANDUM To: From: Hank Kim, Executive Director and Counsel, NCPERS Sarah Mysiewicz Gill, Senior Legal Representative,

Employee Benefits Report

Employee Benefits Report 777 Zeckendorf Blvd. Garden City, NY 11530 (516) 745-7500 Life Benefits June 2011 Volume 9 Number 6 How Do Your Life Benefits Measure Up? In December 2010, the U.S. Bureau of Labor

Employee Benefits Report 777 Zeckendorf Blvd. Garden City, NY 11530 (516) 745-7500 Life Benefits June 2011 Volume 9 Number 6 How Do Your Life Benefits Measure Up? In December 2010, the U.S. Bureau of Labor

Making Retirement Work

Making Retirement Work Francis J. Sennott March 12, 2013 ROPES & GRAY LLP Agenda Planning for Retirement Saving for retirement Qualified retirement plans Other personal savings Investment planning Social

Making Retirement Work Francis J. Sennott March 12, 2013 ROPES & GRAY LLP Agenda Planning for Retirement Saving for retirement Qualified retirement plans Other personal savings Investment planning Social

PLEASE PRINT CLEARLY IN BLUE/BLACK INK

PLEASE PRINT CLEARLY IN BLUE/BLACK INK PENSION OPTION AND BENEFICIARY FORM PENSION OPTION AND BENEFICIARY FORM FORMER 144 HOSPITAL DIVISION BASIC DEFERRED PENSION FORMER 144 HOSPITAL DIVISION BASIC DEFERRED

PLEASE PRINT CLEARLY IN BLUE/BLACK INK PENSION OPTION AND BENEFICIARY FORM PENSION OPTION AND BENEFICIARY FORM FORMER 144 HOSPITAL DIVISION BASIC DEFERRED PENSION FORMER 144 HOSPITAL DIVISION BASIC DEFERRED

EXPLANATORY NOTES FOR TWO PLANS ARE BETTER THAN ONE

EXPLANATORY NOTES FOR TWO PLANS ARE BETTER THAN ONE Page 1 Page 2 As with most partnerships in life, there are match s of strengths with weaknesses. This is the case with adding on a Cash Balance Plan

EXPLANATORY NOTES FOR TWO PLANS ARE BETTER THAN ONE Page 1 Page 2 As with most partnerships in life, there are match s of strengths with weaknesses. This is the case with adding on a Cash Balance Plan

IRS Issues Proposed Regulations on the Conditions Under Which a Plan Amendment May Reduce or Eliminate Protected Benefits

A R T I C L E IRS Issues Proposed Regulations on the Conditions Under Which a Plan Amendment May Reduce or Eliminate Protected Benefits B Y M ELANIE N. ASKA K NOX On March 22, 2004, Treasury and IRS issued

A R T I C L E IRS Issues Proposed Regulations on the Conditions Under Which a Plan Amendment May Reduce or Eliminate Protected Benefits B Y M ELANIE N. ASKA K NOX On March 22, 2004, Treasury and IRS issued

The Water and Power Employees Retirement Disability and Death Benefit Insurance Plan

The Water and Power Employees Retirement Disability and Death Benefit Insurance Plan Review of the Death Benefit Fund as of July 1, 2014 Family Death Benefit Allowance Fund Supplemental Family Death Benefit

The Water and Power Employees Retirement Disability and Death Benefit Insurance Plan Review of the Death Benefit Fund as of July 1, 2014 Family Death Benefit Allowance Fund Supplemental Family Death Benefit

THE SUPER 401K PLAN & THE SUPER 401K PLAN WITH THE PRIME OPTION

THE SUPER 401K PLAN & THE SUPER 401K PLAN WITH THE PRIME OPTION INTRODUCING THE TAX RESERVE A TAX FREE RETIREMENT INCOME/LIFE INSURANCE BENEFIT FULLY FUNDED BY TAX DEFERRALS MAXIMUM TAX DEDUCTIBLE CONTRIBUTIONS

THE SUPER 401K PLAN & THE SUPER 401K PLAN WITH THE PRIME OPTION INTRODUCING THE TAX RESERVE A TAX FREE RETIREMENT INCOME/LIFE INSURANCE BENEFIT FULLY FUNDED BY TAX DEFERRALS MAXIMUM TAX DEDUCTIBLE CONTRIBUTIONS

Your Legacy Pension Benefit

Important Changes to Your Legacy Pension Benefit What s Inside What s Changing and What s Staying the Same... Page 2 Why Are We Making These Changes?... Page 2 A Closer Look at Calculating Final Average

Important Changes to Your Legacy Pension Benefit What s Inside What s Changing and What s Staying the Same... Page 2 Why Are We Making These Changes?... Page 2 A Closer Look at Calculating Final Average