How To Compare The Difference Between A Credit Card And Octopus Mobile Payment In Hong Kong

|

|

|

- Gervais Bates

- 3 years ago

- Views:

Transcription

1 Dr Ludwig Chang, FDS Comparison of Consumers behavioral intention towards Credit Card Mobile Payment and Octopus Mobile Payment in Hong Kong BY Lo Ka Foon Information Systems and e-business Management Concentration An Honours Degree Project Submitted to the School of Business in Partial Fulfillment of the Graduation Requirement for the Degree of Bachelor of Business Administration (Honours) Hong Kong Baptist University Hong Kong April 2014

Hong Kong Baptist University Hong")

2 Acknowledgement I would like to take this opportunity to express my sincerely thankfulness and indebtedness to my supervisor, Dr. Ludwig Chang M. K., for his supervision and guidance. Dr. Chang is always willing to share his precious opinions and insights to me during meetings. His profession in conducting research and valuable advises have provided me with a clear direction of how to perform a research and broadened my horizons. It would be impossible for me to finish this meaningful research without the supports from Dr. Chang. Nevertheless, I would like to thank all of the people who have helped me to finish this research, especially the Professors in HKBU. The knowledge they shared with me has equipped me with the ability in performing the study. Without the participation of the respondents, I cannot gain data to investigate the hypotheses too.

3 Abstract With recent growth of technology, mobile payment has become increasingly popular in our daily lives. Users can pay for goods and services with their mobile devices. In Hong Kong, the most recent mobile payment methods via Near Field Communication (NFC) technology are Credit Card Mobile Payment provided by banks and Octopus Mobile Payment provided by Octopus Card Limited (OCL). Previous researches have investigated the relationships between different variables and Behavioral Intention with Technology Acceptance Model (TAM) in different countries. This study tests a model of acceptance of mobile payment based on Unified Technology Acceptance and Use of Technology (UTAUT) model in Hong Kong. The research model contains 8 factors that may affect consumers behavioral intention, including Performance Expectancy, Effort Expectancy, Social Influence, Facilitating Conditions, Trialability, Communicability, Perceived Risk and Personal Innovativeness in the Domain of Information Technology. Behavioral Intentions of Credit Card mobile payment and Octopus mobile payment will be analyzed separately. Comparison was made based on the factors influencing these two different mobile payment methods. The results indicated that different factors have different effect on different mobile payment methods. The Behavioral Intention of each mobile payment methods is affected by four variables. This report will discuss and attempt to explain why some factors are significant or insignificant for each mobile payment methods. Some implications will be provided for banks and Octopus Card Limited too.

model in Hong Kong.")

4 Table of Contents 1 Introduction Background Research Objective Literature review Technology acceptance theories The Buyer Decision Process for new Product Individual Differences in Innovativeness Product Characteristics Relative advantage Compatibility Complexity Divisibility Communicability Perceived Risk Studies on Mobile Payment Adoption Research model and hypotheses Behavioral Intention Trialability Communicability Performance Expectancy Effort Expectancy Social Influence Facilitating Conditions Perceived Risk Personal Innovativeness in the Domain of Information Technology... 18

5 4 Research Methodology Construct measurement Design of questionnaire Data collection procedure Survey Response Data Analysis and Result Reliability Test Correlation Analysis Hypothesis Testing Factors affecting Behavioral Intention (BI) Credit Card Mobile Payment Octopus Mobile Payment Factors affecting Performance Expectancy (PE) Credit Card Mobile Payment Octopus Mobile Payment Factors affecting Effort Expectancy (EE) Credit Card Mobile Payment Octopus Mobile Payment Comparison of Mobile Payment Methods Structural models and Summaries of the results Discussion and Implications Facilitating Conditions and Trialability Performance Expectancy and Perceived Risk Communicability and Personal Innovativeness in the Domain of Information Technology Effort Expectancy and Social Influence Moderating effects of PIIT Limitation Conclusion... 38

6 9 References Appendix 1: Survey Items Appendix 2: Questionnaire (English Version) Appendix 3: Questionnaire (Chinese Version) Appendix 4: Demographic profile of respondents Appendix 5: Descriptive Statistics for Factors Appendix 6: Results of reliability test Appendix 7: Correlation of Constructs for Credit Card Mobile Payment Appendix 8: Correlation of Constructs for Octopus Mobile Payment Appendix 9: UTAUT Model Appendix 10: Adopter Group... 57

7 1 Introduction 1.1 Background Due to the development of Near Field Communication (NFC) which is a contactless communication that allows users to send data over a NFC compatible device, mobile payment can be used to perform different types of transactions. Mobile payment is a method that consumers make use of their mobile phones to make payments for goods or services (HSBC, n.d.). There are various types of mobile payments, such as direct mobile billing and contactless NFC (Wikipedia, 2013). According to Amoroso and Magnier-Watanabe (2012), it is any payment that initiates, authorizes and confirms a commercial transaction through a mobile device. Mobile payment is defined as using a mobile phone for contactless payment in some merchants through a specific device provided by Visa, MasterCard and Octopus Card Limited (OCL) in this paper. Banks such as The Hongkong and Shanghai Banking Corporation (HSBC) started to provide mobile payment (NearFieldCommunication.org, n.d., HSBC, n.d.; Hang Seng Bank, n.d.). Users can make credit card payment via their mobile phones with NFC. Banks make use of NFC to provide mobile payment by using Visa paywave and MasterCard PayPass (Visa, n.d.; Master Card, n.d.). Customers can use them to make payment through tapping mobile phone on a reader after installing a specific application on the mobile phone. Similar application can be found in Mobile Suica which allows i-mode phones to be used as normal train tickets (Amoroso et al, 2012). Suica card is a contactless smart card for fares payment on JR East railway network, similar to the usage and function of Octopus card in Hong Kong. In 2006, East Japan 1

.")

8 Railway Company (JR East) issued mobile Suica and it got 1.5 million subscribers after 3 years. Users just need to hold the mobile phone near the sensor to pay for any transaction. (Wireless Watch Japan, 2005; East Japan Railway Company, 2005). In Hong Kong, Octopus Card Limited (OCL) also spotted the opportunity in mobile payment. Recently, it introduced a new service Octopus Mobile Payment Service to compete with the mobile payment provided by banks which use NFC to transmit payment information (Yahoo!, 2013; Octopus, 2013). Once consumers adopted Octopus Mobile SIM (OMS), they can make payment by just tapping their smartphone, similar to the use of octopus. 1.2 Research Objective As increasing number of merchants start accepting mobile payment via credit cards or octopus cards and more devices can support mobile payment, Hong Kong market seems to be ready to adopt NFC mobile payment services and there is no doubt that mobile commerce will become the future trend (Ho, 2012). However, a report from MasterCard (2012) pointed out that although it is easy for companies in Hong Kong to adapt new technologies and consumers are experienced at using contactless payments because of Octopus card, consumers in Hong Kong are less familiar and less willing to use Mobile Payment. For Hong Kong, it is just in an initial stage of mobile payment adoption (Au et al., 2008). Although banks have introduced mobile payment for more than one year, not many people are using or willing to use this technology. There can be a number of reasons influencing their intention. 2

, they can make payment by just tapping their smartphone, similar to the use of octopus. 1.")

9 One of the reasons that deter Hong Kong citizens from adopting mobile payment may be the restrictions. Although mobile payment provides a lot of convenience for consumers, many restrictions and processes need to be taken before they can really use the mobile payment. For example, Hang Seng Mobile Payment (Application from Hang Seng Bank to provide mobile payment) only allows Hang Seng MasterCard Credit Card Principal Card holders and PCCW-HKT mobile network customers to use this service (Hang Seng Bank, n.d.). Even for existing PCCW-HKT customers, they have to exchange for the NFC SIM Card and it is not applicable for prepaid card, 2G mobile plan or designated mobile plan. It may decrease their intention to use this service as they expect they have to put much effort to adopt the new technology. People may also believe that it is risky to use mobile payment. In 2010, OCL had been discovered that it had sold Octopus card holders personal information to third parties since 2006 (Lui & Mao, 2010). After this scandal, card holders may be more concerned about the privacy and security problems of Octopus. People may become less willing to use mobile payment because they are afraid that more personal data will be discovered and misused by the OCL as well as banks. Moreover, since Octopus Card service is well developed, customers may find that the functions of credit card mobile payment and octopus mobile payment are very similar with the traditional octopus. Therefore, they may take the view that it is not necessary for them to use this service. They can perform transaction easily using octopus card without adopting mobile payment. 3

.")

10 Many factors can influence customers intention to use mobile payment, for example, availability, reliability and acceptance (Amoroso et al., 2012). This paper has two main purposes. First, this paper aims at identifying the variables that would influence consumers intention to adopt mobile payment. Therefore, we can understand that how mobile payment launchers can improve the service to enhance its usage. Second, factors affecting customers intention will be compared between credit card mobile payment and Octopus mobile payment. When customers choose to use mobile payment, the factors affecting consumers intention to adopt credit card mobile payment may be different from the factors influencing consumers intention to adopt Octopus mobile payment. This paper will also study the differences. 4

11 2 Literature review In this section, literature review and theoretical background about technology acceptance theories, buyer decision processes for a new product, perceived risk and mobile payment will be discussed. 2.1 Technology acceptance theories Several models have been built to elaborate the intention or acceptance for a user to adopt a new technology. Technology acceptance model (TAM) is one of the most popular models among technology acceptance theories. Technology acceptance model is a research model that commonly used in explaining the IT adoption behavior of users. TAM has two belief variables which are perceived usefulness and perceived ease of use (Kim et al., 2009). They will directly and indirectly influence an individual s intention to adopt the technology. Perceived usefulness is the extent that an individual takes the view that using that technology will improve the performance of his or her job while perceived ease of use is the extent that an individual takes the view that he or she will find no difficulty in using that technology. TAM2 has extended the origianl TAM, which included more variables (Venkatesh et al., 2000). The antecedents of perceived usefulness include subjective norm, image, job relevance and output quality while voluntariness and experience are the new moderators. TAM3 is the latest TAM which added two main aspects: four anchors which included computer self-efficacy, perceptions of external control, computer anxiety and computer playfulness as well as two adjustments which are objective usability and perceived enjoyment (Venkatesh et al., 2008). 5

12 Since TAM mainly emphasizes on perceived usefulness and perceived ease of use, and includes too many constructs that may not affect consumers intention to adopt mobile payment directly or indirectly, in this paper, a model combined different models, unified theory of acceptance and use of technology (UTAUT), will be used as UTAUT provides the manner in a more complete and realistic than TAM (Rosen, 2005). In UTAUT model which has been shown in Appendix 9, there are four direct determinants and key moderators (Venkatesh et al., 2003). The four constructs affecting consumers acceptance and usage behavior are performance expectancy, effort expectancy, social influence and facilitating conditions. The moderators in UTAUT are gender, age, voluntariness and experience. Performance expectancy is an extent that an individual takes the view that he or she can gain in job performance by using the new system. Effort expectancy is an extent that a person takes the view that the new system is not difficult for him or her to use. For social influence, it is an extent that a person takes the view that others think the new system should be used. Facilitating conditions represent an extent that a person takes the view that there is enough support to use the new system. When comparing to TAM, some constructs are considered as the same as the constructs in UTAUT, Perceived usefulness and perceived ease of use in TAM are the same as performance expectancy and effort expectancy respectively (Kim et al., 2010). 2.2 The Buyer Decision Process for new Product According to Kotler and Armstrong (2010), adoption process is the process a person goes through the first learning about a new product to final adoption where this product can be a good, service, or idea that is new from the 6

13 perspective of the potential customers. There are five stages in the adoption process including awareness, interest, evaluation, trial and adoption. Some consumers go through these stages quickly while others go through slowly. It depends on individual differences in innovativeness and product characteristics Individual Differences in Innovativeness Depending on the readiness for consumers to try the new product, there are five adopter groups including innovators, early adopters, early majority, late majority and laggards as shown in the Appendix 10. It depends on the time between an innovation is introduced and a customer use it. Since credit card mobile payment and Octopus mobile payment are new technology in Hong Kong and only small numbers of people adopt this technology according to MasterCard s report (MasterCard, 2012), they cannot be separated from the above adopter groups. In this paper, analysis will be done based on participants characteristics in innovativeness instead of separating them into several adopter groups. To evaluate the level of consumers willingness to attempt new information technology, PIIT, which refers to Personal Innovativeness in the Domain of Information Technology, has been introduced in 1998 (Agarwal et al., 1998). As PIIT is considered to be the willingness of a consumer to experiment innovation, marketers can target on the consumers with higher innovativeness first to gain early sales and word of mouth (Rosen, 2005). In a recent study, innovative consumers have four main characteristics, 7

14 including a consumer s willingness to make changes in things and concepts, a consumer s capability to affect other people to adopt innovative things and concepts, a consumer is supportive in tackling problems and deciding decisions in a social system or an organization, and the rate and time of adoption of the aforementioned changes in a functional relationship (Ho et al., 2011). Therefore, we can expect that consumers with higher PIIT will have higher intention to adopt mobile payment and may be affected differently by the antecedents Product Characteristics Rogers (2010) introduced five product characteristics that can affect the adoption s rate of a new product, including relative advantage, compatibility, complexity, divisibility and communicability. Since some of them are nearly the same as the constructs in UTAUT model, the characteristics and constructs in UTAUT with similar meaning will be represented by constructs in UTAUT Relative advantage In Innovation Diffusion Theory (IDT), relative advantage is the extent that a consumer perceives that an innovation is better than its precursor (Moore et al., 1991). It emphasizes on the perception of consumers rather than the objective advantage of the innovation. It can be evaluated by several factors, such as convenience and economic gains (Ho et al., 2011). It refers to consumers perception rather than objective advantage 8

introduced five product characteristics that can affect the adoption s rate of a new product, including relative advantage, compatibility, complexity,")

15 of the innovation. Since it is a construct in IDT and it was combined with other constructs to become a root construct of Performance Expectancy in UTAUT, we will treat relative advantage as performance expectancy in this paper (Venkatesh et al., 2003) Compatibility Since compatibility, which represents the extent that an individual perceives that an innovation is constant with their existing values, experiences of potential and desires in IDT, is also combined with constructs from different theories or models to be the root construct of Facilitating Conditions, it will be preserved as facilitating conditions in this paper (Moore et al., 1991; Venkatesh et al., 2003) Complexity Complexity is the extent that a consumer perceives that a new technology is relatively difficult for them to understand and use (Thompson et al., 1991). According to Venkatesh et al. (2003), complexity is one of the root constructs for Effort Expectancy in UTAUT. Therefore, complexity will be treated as effort expectancy in this paper Divisibility Divisibility is the extent that an innovation may be experimented on a limited basis (Kotler et al., 2010). A new product that can be tried will increase the adoption because the uncertainty will be decreased during experiment. 9

. 2.")

16 Communicability Communicability is the extent that extent when consumers use the new product, the result can be observed or described to others (Kotler et al., 2010). If a consumer perceives that the results of using a new product are easy to observe, he or she will become more likely to use it. 2.3 Perceived Risk The level of perceived risk will affect the decision of customers (Lu et al., 2005). According to Swilley (2010), perceived risk in mobile payment is the loss of data because of credit card fraud. It can also be considered as the expectations of negative consequences or attitudes toward providing information to the seller via mobile device (Amoroso et al., 2012). Risk can be divided into several categories, including physical risk (PHR), functional risk (FUR), social risk (SOR), time-loss risk (TLR), Financial risk (FIR), Opportunity cost risk (OCR) and information risk (INR) (Lu et al., 2005). Each of them refers to different uncertainties that consumers may face. Since not all risks are appropriate or relevant to mobile payment, perceived risk in this paper will be defined as the loss of data and misuse of data. Potential credit card and octopus mobile payment users may be afraid of the possibilities that their information will be stolen or misused for transactions or other purpose without their permission after they installed or used credit card mobile payment. 10

, perceived risk in mobile payment is the loss of data because of credit card fraud.")

17 2.4 Studies on Mobile Payment Adoption Mobile payment is a specific form of electronic manner to handle payment (Schierz et al, 2010). In the past few decades, a number of studies about mobile payment have been done to discuss the factors that are significant in affecting consumers perspectives towards mobile payment. In a multi-country study which applied Actor Network Theory (ANT) for identifying factors that affect mobile payment adoption, it has found that the constructs that can influence mobile payment adoption are the degree of synergy between the macro-actors in that country, how consumers associate values to it, the relationship between the primary point of contact and the consumers, how correctly the micro-environment of a micro-actor is identified, market conditions, and the presence of catalysts (Warren et al, 2008). It has also pointed out that different patterns of mobile payment adoption will be different for different countries. For customer loyalty in mobile payment, a study in Iran has found that security, customer satisfaction, perceived risk, perceived usefulness, perceived ease of use, customization and responsiveness are the most essential factors (Sanayei et al, 2011). A study about mobile suica which is similar to mobile Octopus has proposed a comprehensive model to illuminates variables that would affect mobile payment adoption, including perceived usefulness, attitude, facilitating conditions, perceived value, perceived security and privacy, social influence, trust, perceived risk, and attractiveness (Amoroso et al, 2012). 11

18 Studies have also proved that perceived cost, perceived risk, trust, relative advantage, image, perceived compatibility, perceived security, perceived usefulness, perceived ease of use, individual mobility, subjective norm, availability, confidentiality, privacy, processing integrity will also have positive or negative impacts on consumers adoption or behavioral intention or attitude of mobile payment (Lu et al, 2011; Schierz et al, 2010; Kim et al, 2010; Meharia, 2012). Various perspectives or theories can be used to explain behavioral intention and adoption of mobile payment and all of them have developed a better understanding of mobile payment for us. Most of the studies focused on the effect of and what would affect perceived usefulness and perceived ease of use on mobile payment adoption from TAM. Since limited studies are established based on UTAUT model or discussed the situation in Hong Kong, this paper will further studies mobile payment in Hong Kong using UTAUT model. 12

19 3 Research model and hypotheses In order to identify the factors that will affect consumers behavioral intention to use mobile payment, the following hypotheses have been developed and the comparison of credit card mobile payment and octopus mobile payment will be discussed in the later parts. The research model to be studied is shown in Figure 1, which is mainly developed based on UTAUT model with some additional factors. The research model includes four constructs from UTAUT, two constructs from IDT, perceived risk, and individual differences in innovativeness as moderators. Figure 1 Research Model 3.1 Behavioral Intention Behavioral Intention is the likelihood that consumer will use an innovation (Venkatesh et al., 2003). With higher behavioral intention, a consumer will 13

20 become more likely to use a new technology. There are several antecedents that may affect an individual s behavioral intention. 3.2 Trialability Trialability has the same meaning as divisibility which is the extent that a person can experiment and try the innovation (Roger, 2010). Roger (2010) stated that trialability will affect consumers intention to use goods. Also, a positive relationship between trialability and adoption intention has been found. It can strengthen the intention to adopt a new product and eliminate the insecurity about an innovation (Ho et al., 2011). Since consumers have to register or fulfill particular requirements before they use credit card mobile payment or octopus mobile payment, it will be difficult to let consumers try before they adopt and they will, therefore, have lesser intention to adopt mobile payment. H1. Triablability will have a positive effect on Behavioral intention. 3.3 Communicability Communicability is one of the antecedents of result demonstrability. It was found to have a positive relationship to behavioral intention (Wahid, 2010). In TAM2 model and TAM3 model, result demonstrability shows a positive effect on perceived usefulness which is defined as performance expectancy in this study (Venkatesh et al., 2008). Result demonstrability is the degree that an individual takes the view that the outcomes are tangible, observable and communicable for using the system (Moore et al., 1991). It was also found to have a positive relationship with perceived ease of use which is same as effort expectancy (Kacmar et al., 2009). Since communicability is the antecedent of result 14

.")

21 demonstrability, communicability will, therefore, be treated to have the same effect as result demonstrability in this paper. If customers believe that mobile payment is communicable, their performance expectancy, effort expectancy and behavioral intention will increase. H2a. Communicability will have a positive effect on performance expectancy. H2b. Communicability will have a positive effect on effort expectancy. H2c. Communicability will have a positive effect on behavioral intention. 3.4 Performance Expectancy Performance Expectancy and perceived usefulness in UTAUT and TAM are the most powerful methods to illuminate behavioral intention to adopt a new system (Park et al., 2007). Perceived usefulness was found to have strong effect on consumers attitude to use mobile payment system (Meharia, 2012). If consumers find that adopting credit card or octopus mobile payment can help them to perform their jobs better, their intentions to use these kinds of mobile payment methods will increase. H3. Performance Expectancy will have a positive effect on behavioral intention. 3.5 Effort Expectancy Effort expectancy has been found to affect behavioral intention positively in several studies (Park et al., 2007; Im et al., 2011). Meharia (2012) has also found that perceived ease of use will affect consumers attitude towards adopting mobile 15

22 payment. The willingness of consumers to use credit card or octopus mobile payment will increase if they think that the system is easy for them to use. H4. Effort expectancy will have a positive effect on behavioral intention. 3.6 Social Influence Social influence has a direct effect on behavioral intention under mandatory settings and inexperienced system environments even consumers do not have the intention to perform a behavior originally if they think others consider that they have to use it or being motivated by some referents (Venkatesh et al., 2000; Park et al., 2007). It was found that attitude on using mobile technologies was affected by social influence (Park et al., 2007). However, mobile payment methods are newly offered in Hong Kong. There may be little referents since not many people are familiar with the technology. Moreover, consumers can choose to use these methods or not. Thus, social influence may not have great impact in behavioral intention yet. H5. Social Influence will have a positive effect on behavioral intention. 3.7 Facilitating Conditions In UTAUT, facilitating conditions are the antecedents of Use Behavior instead of affecting behavioral intention directly (Venkatesh et al., 2003). Although facilitating conditions were not significant in elaborating behavioral intention in UTAUT, it was found to slightly affect the behavioral intention of mobile technologies in early adoption stage (Park et al., 2007). As Hong Kong does not have many merchants to support the use of credit card mobile payment yet while 16

23 octopus mobile payment can be used widely once you adopted it because of the existing octopus system, the relationship between facilitating conditions and behavioral intention may be stronger for credit card mobile payment. H6. Facilitating Conditions will have a positive effect on behavioral intention. 3.8 Perceived Risk Cunningham (1967) defined risk as the uncertainty and adverse consequences a consumer feels or perceives when he or she is buying a product. Perceived risk will play a significant role in affecting the perceived usefulness and perceived ease of use but it will not affect the behavioral intention directly (Lu et al., 2005). The lower the level of perceived risk is, the higher the adoption behavior, perceived ease of use and perceived usefulness will be (Wafa, 2009). Consumers perception of risk using mobile payment systems will diminish their intention to adopt these systems (Lu et al., 2011). As the risk is very high if users lose their phones or their information is stolen by others, the perceived risk for customers may have a great impact on the behavioral intention. H7a. Perceived risk will have a negative effect on performance expectancy. H7b. Perceived risk will have a negative effect on effort expectancy. H7c. Perceived risk will have a negative effect on behavioral intention. 17

24 3.9 Personal Innovativeness in the Domain of Information Technology Based on different consumers innovativeness, they may have different reaction towards a new technology. The higher level of Personal Innovativeness in the Domain of Information Technology (PIIT) is, the higher opportunity that a person will have a behavioral intention and adopt the new technology earlier than others with lower level of PIIT since they are more willing to try new things (Agarwal et al., 1998). Innovativeness of consumer affects behavioral intention significantly and positively (Ho et al., 2011). Innovativeness has been found to affect the use of m-services positively and innovative consumers will be more willing to try new m-services (Mort et al., 2007). Apart from being an essential predictor of behavioral intentions, Rosen (2005) also found that PIIT can moderate the effect of usefulness and ease of use on intention. PIIT can work as the moderators among three UTAUT constructs and behavioral intention, including relative advantage, ease of use and compatibility (Agarwal et al., 1998). As innovative individuals appear to be more curious and active in seeking information, they will find more information about a new technology to understand it before they adopt and think the innovation is more useful and easier to use than less innovative consumers (Kim et al., 2012). This contributes to a moderating effect between performance expectancy and effort expectancy with behavioral intention. Moreover, the relationship will be moderated because innovative consumers have higher willingness to make changes and they are more capable to deal with uncertainty (Ho et al., 2011; Agarwal et al., 1998). Their abilities to cope with difficulties make them believe that they do not need to pay much effort to adopt mobile payment. Thus, more innovativeness people will be affected less by the complexity of the new technology. 18

25 H8a. PIIT will have a positive effect on behavioral intention. H8b. PIIT will moderate the relationship between performance expectancy and behavioral intention. H8c. PIIT will moderate the relationship between effort expectancy and behavioral intention. According to past researches, fourteen hypotheses have been developed to show the proposed relationships between different variables. To examine whether the hypotheses are tenable, data will be needed to prove that the relationships exist. A research has been established to collect the data. 19

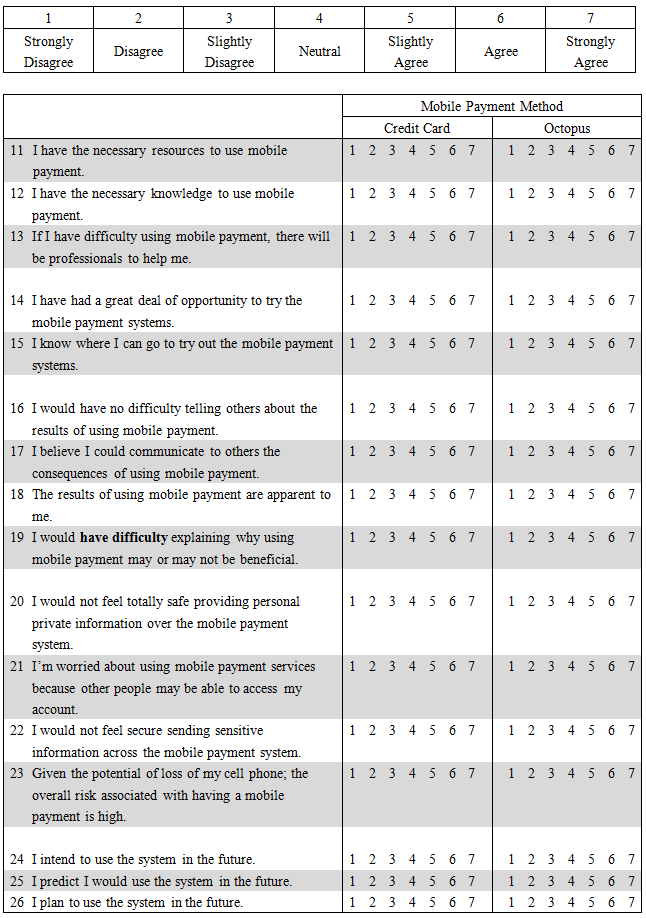

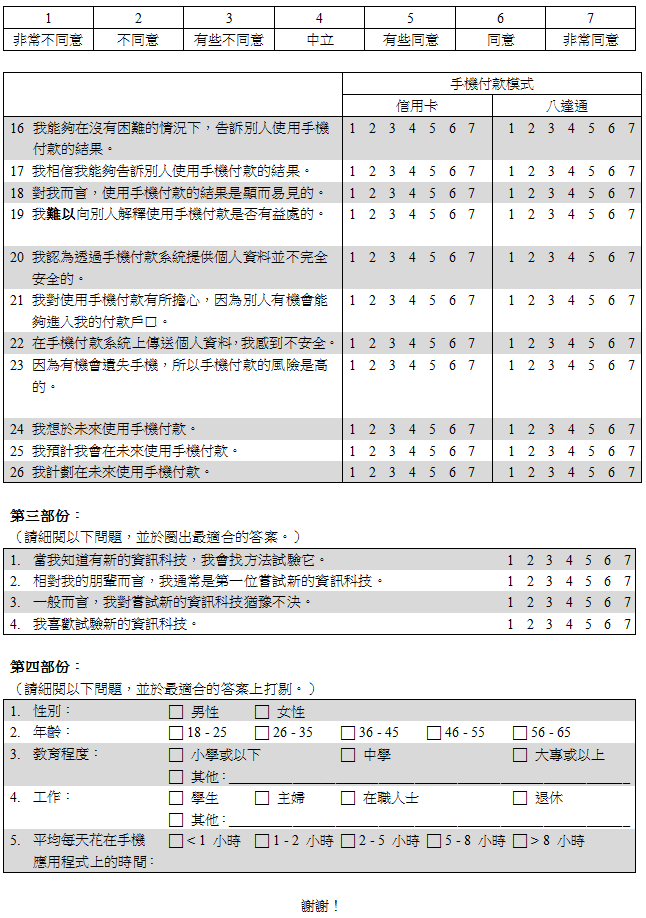

26 4 Research Methodology 4.1 Construct measurement To investigate consumer s intention to use mobile payment and compare the difference between credit card and octopus mobile payment, data collection had be done based on a structured questionnaire with multi-item measures to ensure the validity of each instrument. The research model in this study includes 9 constructs; their measurements were adapted from previous studies and revised to fit the study. A seven-point Likert scale from strongly disagree to strongly agree was used in the questionnaire to measure the constructs. In order to ensure all participants know what mobile payment is, participants were given the definition of mobile payment at the beginning of the questionnaire. The survey items can be found in the Appendix Design of questionnaire The questionnaire contains four main parts. The first part is a screening question to make sure that participants are smartphone users. Non smartphone users were not required to continue the questionnaire. The second part which measures participants perception of mobile payment includes eight constructs divisibility, communicability, performance expectancy, effort expectancy, social influence, facilitating conditions, perceived risk and behavioral intention. This part has been divided into two sections, credit card mobile payment and octopus mobile payment, to evaluate participates perception of two different mobile payment methods. The third part evaluates participants personal innovativeness in the domain of information technology. The forth part emphasizes on the demographic data of participants, such as age and gender. The design of the questionnaire can be found in Appendix 2 and Appendix 3. 20

27 4.3 Data collection procedure In this study, data was collected via two methods online and offline. Qualtrics.com was used for developing the survey online and online survey was conducted online via social networking Facebook, where participates were invited to conduct the web-based research. Questionnaires were also distributed in hardcopy. Both English and Chinese version questionnaires have been developed to ensure participants can fully understand all questions. English version questionnaires were distributed online using Qualtrics.com while Chinese version questionnaires were distributed offline. The target of this study focused on smartphone users who aged between years old. 4.4 Survey Response During 3 rd of March to 23 rd of March, 218 questionnaires have been distributed online and offline. 205 valid responses out of 218 questionnaires were collected and utilized for data analysis. The remaining questionnaires have been considered to be invalid because of incompleteness of the questionnaires or invalid responses. Among these 205 usable questionnaires, there are 97 male respondents and 108 female respondents. The main age group of the respondents is years old and around half of the respondents are student. Demographic profile of the respondents is shown in the Appendix 4. 21

28 5 Data Analysis and Result To understand which variables will affect the behavioral intention of adopting mobile payment and the difference between credit card mobile payment and octopus mobile payment, statistical analysis will be examined in the following part. Since the study contains two different mobile payment methods, two different analyses will be executed separately with the aid of Statistical Package for the Social Sciences (SPSS) to test the model. 5.1 Reliability Test In order to test the reliability of the data, reliability analysis was performed by using Cronbach s Alpha. The scale will be considered to be consistent if Cronbach s Alpha is larger than 0.7. The results of reliability test can be found in Appendix 6. Most of the scales are reliable and consistent with the Cronbach s Alpha larger than 0.7. FC3 and PIIT3 for both payment methods were deleted as the Cronbach s Alpha of their corresponding construct is lower than 0.7 and deleting them brought the values higher than 0.7. CO4 for both payment methods will also be deleted as the reliability for Communicability will be significantly increased if it is deleted. The adjusted results of reliability test and the descriptive statistics of factors are shown in the Appendix Correlation Analysis Pearson s correlation analysis has been performed to investigate the relationships between two variables with a range from 1 (positive relationship) to -1 (negative relationship). If the value is closer to 1 or -1, it indicates a stronger relationship between two variables. The results have been shown in the Appendix 7 and Appendix 8. 22

29 5.3 Hypothesis Testing Linear regression was performed to find the relationships between independent variables and dependent variables. R Square represents the strength of association between dependent variables and independent variables. Since the hypotheses are one-tailed test, the relationships will be considered as significant if the p-value (sig.) printout from SPSS is lower than 0.1, which is equivalent to set the Alpha value to Hence, the below p-value will be divided by Factors affecting Behavioral Intention (BI) Behavioral Intention is a dependent variable that is affected by both independent variables and moderators. The independent variables affecting Behavioral Intention is Performance Expectancy, Effort Expectancy, Social Influence, Facilitating Conditions, Trialability, Communicability, Perceived Risk and Personal Innovativeness in the Domain of Information Technology (PIIT). PIIT also acts as a moderator of Performance Expectancy and Effort Expectancy between Behavioral Intention Credit Card Mobile Payment The hypothesis testing result of Behavioral Intention is shown in table 7. The R Square is 0.583, which means 58.3% of variance in Behavioral Intention can be explained by its independent variables. As the p-value for Performance Expectancy, Facilitating Conditions, Trialability and Perceived Risk are smaller than 0.05, these independent variables are positively related to Behavioral Intention. However, no significant effect can be found between Behavioral and other independent variables. Moderators do not have significant effect too. Therefore, only H1, H3, 23

30 H6 and H7c are supported and H2b, H4, H5, H8a, H8b and H8c are not supported by the findings for Credit Card Mobile Payment. Table 1 Hypothesis Testing of BI (Credit Card Mobile Payment) Behavioral Intention (R Square: 0.583) Model B Std. Error Beta T Sig. (p-value) (Constant) PE * EE SI FC * TR * CO PR * PIIT Interaction of Performance Expectancy and PIIT Interaction of Effort Expectancy and PIIT Octopus Mobile Payment The hypothesis testing result of Behavioral Intention is shown in table 8. The R Square is 0.660, which means 66.0% of variance in Behavioral Intention can be explained by its independent variables. As the p-value for Facilitating Conditions, Trialability, Communicability and PIIT are smaller than 0.05, these independent variables are positively related to Behavioral Intention. However, no significant effect can be found between Behavioral and other independent variables. Moderators do not 24

31 have significant effect too. Therefore, only H1, H2c, H6 and H8a are supported and H3, H4, H5, H7c, H8b and H8c are not supported by the findings for Octopus Mobile Payment. Table 2 Hypothesis Testing of BI (Octopus Mobile Payment) Behavioral Intention (R Square: 0.660) Model B Std. Error Beta T Sig. (p-value) (Constant) PE EE SI FC * TR * CO * PR PIIT * Interaction of Performance Expectancy and PIIT Interaction of Effort Expectancy and PIIT Factors affecting Performance Expectancy (PE) Performance Expectancy is a dependent variable that is determined by Communicability and Perceived Risk Credit Card Mobile Payment The hypothesis testing result of Performance Expectancy is shown in table 3. The R Square is 0.307, which means 30.7% of variance in 25

32 Performance Expectancy can be explained by Communicability and Perceived Risk. Both Communicability and Perceived Risk are positively related to Performance Expectancy as their p-values are Therefore, H2a and H7a for Credit Card Mobile Payment are supported. Table 3 Hypothesis Testing of PE (Credit Card Mobile Payment) Performance Expectancy (R Square: 0.307) Model B Std. Error Beta T Sig. (p-value) (Constant) CO * PR * Octopus Mobile Payment The hypothesis testing result of Performance Expectancy is shown in table 4. The R Square is 0.373, which means 37.3% of variance in Performance Expectancy can be explained by Communicability and Perceived Risk. With p-value = 0.000, Communicability is positively related to Performance Expectancy. However, no significant effect can be found between Perceived Risk and Performance Expectancy. Therefore, H2a is supported and H7a is not supported by the findings. Table 4 Hypothesis Testing of PE (Octopus Mobile Payment) Performance Expectancy (R Square: 0.373) Model B Std. Error Beta T Sig. (p-value) (Constant) CO * PR

33 5.3.3 Factors affecting Effort Expectancy (EE) Effort Expectancy is a dependent variable that is determined by Communicability and Perceived Risk Credit Card Mobile Payment The hypothesis testing result of Effort Expectancy is shown in table 5. The R Square is 0.426, which means 42.6% of variance in Effort Expectancy can be explained by Communicability and Perceived Risk. As the p-value for Communicability and Perceived Risk are and respectively, both of them are positively related to Effort Expectancy. Therefore, H2b and H7b for Credit Card Mobile Payment are supported by the findings. Table 5 Hypothesis Testing of EE (Credit Card Mobile Payment) Effort Expectancy (R Square: 0.426) Model B Std. Error Beta T Sig. (p-value) (Constant) CO * PR * Octopus Mobile Payment The hypothesis testing result of Effort Expectancy is shown in table 6. The R Square is 0.619, which means 61.9% of variance in Effort Expectancy can be explained by Communicability and Perceived Risk. As the p-value for Communicability and Perceived Risk are and respectively, both of them are positively related to Effort 27

34 Expectancy. Therefore, H2b and H7b are supported by the findings for Octopus Card Mobile Payment. Table 6 Hypothesis Testing of EE (Octopus Mobile Payment) Effort Expectancy (R Square: 0.619) Model B Std. Error Beta T Sig. (p-value) (Constant) CO * PR * 5.4 Comparison of Mobile Payment Methods The last thing to be performed is the comparison of the two different mobile payment methods. Unstandardized Coefficients (B) was compared to see which variables have a greater impact for credit card mobile payment and octopus mobile payment. After compared the unstandardized coefficients (B) in table 1 and table 2 in section 5.3.1, Performance Expectancy, Effort Expectancy, Trialability and Perceived Risk have been found to have a great influence for credit card mobile payment. Facilitating conditions, Communicability and Personal Innovativeness in the Domain of Information Technology have a higher impact on Octopus mobile payment. Social Influence has the same level of impact for both mobile payment methods as their unstandardized coefficients (B) are the same. 5.5 Structural models and Summaries of the results The structural models and summaries of the hypotheses testing results are shown in the below tables and graphs. Summary of hypotheses testing results can be found in table 7. It has shown that 8 out of 14 hypotheses can be supported for 28

35 Credit Card Mobile Payment and 7 out of 14 hypotheses can be supported for Octopus Mobile Payment. No moderating effect can be found by the results. Figure 2 has shown the structural models of Credit Card Mobile Payment and Octopus Mobile Payment. Table 7 Summary of Hypotheses testing results Hypotheses testing results Path Credit Card Octopus Card H1 Triablability Behavioral Intention H2a Communicability Performance Expectancy H2b Communicability Effort Expectancy H2c Communicability Behavioral Intention H3 Performance Expectancy Behavioral Intention H4 Effort expectancy Behavioral Intention H5 Social Influence Behavioral Intention H6 Facilitating Conditions Behavioral Intention H7a Perceived risk Performance Expectancy H7b Perceived risk Effort expectancy H7b Perceived risk Behavioral Intention H8a PIIT Behavioral Intention H8b Moderator PIIT will affect (Performance expectancy Behavioral Intention) H8c Moderator PIIT will affect (Effort expectancy Behavioral Intention) 29

36 Figure 2 Structural Model 30

37 6 Discussion and Implications This research aims at studying the factors that would affect consumers behavioral intention in using credit card mobile payment and octopus mobile payment, and further investigating the difference of the factors between two mobile payment methods. Nevertheless, the results have shown that not all hypotheses are supported by the data collected. In this part, different factors that influence behavioral intention will be discussed and some implications for credit card mobile payment and octopus mobile payment will be provided. 6.1 Facilitating Conditions and Trialability For both mobile payment methods, Facilitating Conditions and Trialability are significant predictors for Behavioral Intention. Consumers still are not aware of or familiar with mobile payment in Hong Kong. Many of them do not even know what mobile payment is or how mobile payment can benefit their daily lives. As mobile payment is a new thing for consumer, it would be essential for them to have a better understanding about how to use it and where they can try it, no matter for which mobile payment methods. The more information they know about mobile payment, the higher intention for them to use mobile payment. If they do not have enough resources or knowledge to get a trial on mobile payment, they would have no interest in using it. Therefore, it would be important for banks and Octopus Card Limited to have more promotion about this new technology. It would attract more people to use mobile payment if they have a better knowledge about mobile payment and recognize the advantages of using mobile payment. There are many prerequisites for people to adopt mobile payment, such as the model of the mobile phone and 31

38 mobile service provider. It is necessary to minimize the prerequisites of adopting mobile payment too as people who have intention to use mobile payment may be hindered from adopting it because of the prerequisites. When people find that it is difficult for them to try it, their intention of using mobile payment may be decreased. 6.2 Performance Expectancy and Perceived Risk According to the results, Performance Expectancy and Perceived Risk are significant predictors for Behavioral Intention for credit card mobile payment, but not for octopus mobile payment. For Performance Expectancy, it is important for the intention of using credit card mobile payment but not octopus mobile payment because credit card mobile payment is quite different from traditional credit card in term of their usages and results. Whether credit card mobile payment is useful or performs better than tradition credit card will be important for customers in determining whether they want to adopt it. By contrast, the usage of using octopus mobile payment is nearly same as octopus card. People are relatively familiar with what octopus card can perform already and expect that octopus mobile payment will bring them similar advantages. Hence, Performance Expectancy does not affect their behavioral intention of octopus mobile payment that much. For Perceived Risk, the outcome is like Effort Expectancy. It is a significant predictor of Behavioral Intention to credit card mobile payment because credit card contains more private information about the users and the potential loss is higher in light of the bank account information. Due to these reasons, Perceived 32

39 Risk would have a significant impact on whether they want to adopt credit card mobile payment. As people may consider that the risks of using octopus mobile payment are the same as using octopus card and there is lesser information contained in octopus card, it does not have a significant effect on octopus card. Perceived Risk is found to have significant relationship with Effort Expectancy for both mobile payment methods and Performance Expectancy for credit card mobile payment too. It has a significant relationship between Perceived Risk and Effort Expectancy because they may think they have to spend more time on controlling the mobile payment system if there is a higher risk. Perceived Risk is a significant predictor of Performance Expectancy for credit card mobile payment because the risks of adopting this mobile payment method are high. Since much sensitive information may lose or be explored, Perceived Risk will affect whether people think it is useful. However, for octopus mobile payment, Perceived Risk does not have a significant relationship with Performance Expectancy because the risks of adopting octopus mobile payment are relatively low. It does not affect Performance Expectancy very much. As a result, banks may need to emphasize on promoting the benefits of adopting credit card mobile payment and improve the security. By providing more information about credit card mobile payment, people may find it is beneficial for them to pay through mobile phones and become more willing to adopt credit card mobile payment. Banks can also enhance their intention of adopting mobile payment by improving the security level of the application or promoting the security protection of the system. 33

40 6.3 Communicability and Personal Innovativeness in the Domain of Information Technology Communicability and Personal Innovativeness in the Domain of Information Technology are significant predictors for octopus mobile payment. However, there is no significant effect for credit card mobile payment. For Communicability, it is a significant predictor of Behavioral Intention of adopting octopus card mobile payment but not credit card mobile payment. As mentioned before, octopus mobile payment is quite similar with traditional octopus card. Since customers would believe that the outcome of using octopus mobile payment is similar too, they may expect the outcome of using it will be as observable and communicable as traditional octopus card. However, not many merchants support credit card mobile payment at this stage and people will have fewer chances to adopt it. They may not have much expectation about the communicability of credit card mobile payment. Therefore, whether the results are apparent may not be that important for them and Communicability of credit card mobile payment does not affect the Behavioral Intention a lot. For Personal Innovativeness in the Domain of Information Technology (PIIT), the outcome is the same with Communicability. It is a significant predictor of Behavioral Intention to octopus card mobile payment because octopus mobile payment is the latest mobile payment method using NFC function in Hong Kong. Customers with higher level of PIIT who are fond of trying innovation will have higher intention of using octopus mobile payment. Nonetheless, credit card mobile payment has been launched for a few years and it is not that up-to-date when compared to octopus mobile payment. It would have lesser effect on 34

41 Behavioral Intention. Communicability is also a significant predictor for Performance Expectancy and Effort Expectancy in both mobile payment methods. If people are able to explain the results of using mobile payment, they will think mobile payment is useful and easy to use. People tend to feel something is good when they can share the benefits of using it with others. It is suggested that Octopus Card Limited should show the results of adopting octopus mobile payment and explain the difference between octopus mobile payment and octopus card to its potential customers. People can, therefore, understand or tell others the results as well as the difference, and become more willing to adopt octopus mobile payment. 6.4 Effort Expectancy and Social Influence Effort Expectancy and Social Influence have no significant relationship with Behavioral Intention in this study. As not many people have a clear idea about mobile payment, they may not know the effort they have to spend on using mobile payment. Several studies also found that there is no significant relationship between Effort Expectancy and Behavioral Intention (Akturan & Tezcan, 2012; Lewis et al, 2003; Szajna, 1996). Effort Expectancy will have less impact on their intention of adopting mobile payment with low level of experience of mobile payment. Since not many people will tell other or be told to use mobile payment under this situation and some of them may not know whether others think they should use mobile payment, Social Influence does not have much influence on Behavioral Intention too. 35

42 Since Effort Expectancy and Social Influence are not significant predictors, banks and Octopus Card Limited should spend more resources on other factors that have significant influence on Behavioral Intention, especially the Facilitating Conditions and Trialability. They should provide more opportunities for customers to try the mobile payment system and provide more supports for those who intend to adopt mobile payment rather than just emphasizing on the easiness of using mobile payment. 6.5 Moderating effects of PIIT No moderating effect can be found to have significant relationship in this model. PIIT is not an effective moderator between Performance Expectancy and Behavioral Intention or between Effort Expectancy and Behavioral Intention. People who are more innovative may not have much idea about mobile payment too. Normally, they think an innovation is more useful and easier to use because they are eager to do research and get more information about a new product. Since the knowledge they have may be the same with less innovative people, they may have similar perception about this technology with people who are less innovative. Therefore, they would not find mobile payment is more useful or easier to use than others. 36

43 7 Limitation Although this study provides some useful insights about mobile payment, there are still some limitations in this study. The samples collected are not representative enough because of two reasons. First, the sample size of this study is relatively small to represent the entire population in Hong Kong. In order to gain a result that is more precise and representative, the research base can be enlarged in future study. Second, the age group and occupation group are too concentrated. Most of the respondents are students and aged between 18 and 25. As it could affect the results of the study, different groups of people should be interviewed to reflect their preferences in the future research. Moreover, only two mobile payment methods have been chosen to investigate in this study. Indeed, many different mobile payment methods have been developed to provide payment services with mobile devices. For example, TaoBao has recently enabled users to pay for their purchases through mobile devices with their Octopus Card. In future study, more mobile payment methods can be considered. 37

44 8 Conclusion To conclude, this study mainly emphasizes on evaluating the effect of different factors and comparing credit card mobile payment with octopus mobile payment. The findings of this study show that Facilitating Conditions and Trialability are significant factors of Behavioral Intention for both mobile payment methods. For Effort Expectancy and Perceived Risk, they are significant factors of Behavioral Intention for credit card mobile payment only. For Communicability and Personal Innovativeness in the Domain of Information Technology, they are significant factors of Behavioral Intention for octopus mobile payment only. There is no significant effect between Performance Expectancy and Behavioral Intention or Social Influence and Behavioral Intention as well as the moderator. With the insights provided in this study, banks and Octopus Card Limited can increase consumers intention to adopt mobile payment based on the results. The most crucial step they should take is to increase the promotion of mobile payment and expand consumers understanding about mobile payment. 38

45 9 References Agarwal, R., and Prasad, J. "A Conceptual and Operational Definition of Personal Innovativeness in the Domain of Information Technology," Information Systems Research (9:2) 1998, pp Akturan, U., & Tezcan, N. (2012). Mobile banking adoption of the youth market. Marketing Intelligence & Planning, 30(4), Al-Jabri, I. M., & Sohail, M. S. (2012). Mobile Banking Adoption: Application Of Diffusion Of Innovation Theory. Journal of Electronic Commerce Research,13(4), Amoroso, D. L., & Magnier-Watanabe, R. (2012). Building a research model for mobile wallet consumer adoption: The case of mobile suica in japan. Journal of Theoretical and Applied Electronic Commerce Research, 7(1), DOI: /S Au, Y. A., & Zafar, H. (2008). A multi-country assessment of mobile payment adoption. UTSA, College of Business. East Japan Railway Company. Mobile Suica Service to Start Saturday, January 28, 2006!. Retrieved November 2, 2013 from Hang Seng Bank. (n.d.). Hang Seng Mobile Payment Service. Retrieved October 14, 2013 from Ho, A. (2012). Is Hong Kong ready to go mobile?. Hong Kong Business. Retrieved November 16, 2013 from -mobile Ho, C. H., & Wu, W. (2011). Role of Innovativeness of Consumer in Relationship between Perceived Attributes of New Products and Intention to Adopt. International Journal of Electronic BusinessManagement, 9(3), 258. HSBC. (n.d.). Mobile Payments. Retrieved October 14, 2013 from 39

46 Im, I., Hong, S., & Kang, M. S. (2011). An international comparison of technology adoption: Testing the UTAUT model. Information & Management,48(1), 1-8. Kacmar, C. J., Fiorito, S. S., & Carey, J. M. (2009). The influence of attitude on the acceptance and use of information systems. Information Resources Management Journal (IRMJ), 22(2), Kim, C., Mirusmonov, M., & Lee, I. (2010). An empirical examination of factors influencing the intention to use mobile payment. Computers in Human Behavior, 26(3), DOI: /j.chb Kotler, P. J., & Armstrong, G. M. (2010). Principles of marketing. (pp ). Pearson Education. Lewis, W., Agarwal, R., & Sambamurthy, V. (2003). Sources of influence on beliefs about information technology use: an empirical study of knowledge workers. Mis Quarterly, Lu, H. P., Hsu, C. L., & Hsu, H. Y. (2005). An empirical study of the effect of perceived risk upon intention to use online applications. Information Management & Computer Security, 13(2), Lu, Y., Yang, S., Chau, P. Y., & Cao, Y. (2011). Dynamics between the trust transfer process and intention to use mobile payment services: A cross-environment perspective. Information & Management, 48(8), Lui, M. & Mao, D. (2012). MTR s Octopus sold personal data about 1.97 million users, RTHK Reports. Bloomberg.com. Retrieved November 16, 2013 from -in-hong-kong-for-5-6-million-rthk-says.html Master Card. (2012). Mobile readiness in Hong Kong. Retrieved November 2, 2013, from Master Card. (n.d.). Retrieved November 2, 2013 from 40

47 Meharia, P. (2012). Assurance on the reliability of mobile payment system and its effects on its use: an empirical examination. Journal of Accounting and Management Information Systems, 11(1), Moore, G. C. & Benhasat, I. (1991). Development of an Instrument to Measure the Perceptions of Adopting an Information Technology Innovation. Information System Research. 2(3), Mort, G., & Drennan, J. (2007). Mobile communications: a study of factors influencing consumer use of m-services. Journal of Advertising Research, 47(3), NearFieldCommunication.org. (n.d.). Retrieved October 14, 2013 from Octopus. (2013). Hong Kong's First Octopus Mobile Payment Service Introduced. Retrieved November 2, 2013 from Park, J., Yang, S., & Lehto, X. (2007). Adoption of mobile technologies for Chinese consumers. Journal of Electronic Commerce Research, 8(3), Rogers, E. M. (2010). Diffusion of innovations (4th ed.). Simon and Schuster. Rosen, P. A. (2005). The effect of personal innovativeness on technology acceptance and use (Doctoral dissertation, Oklahoma State University). Sanayei, A., Ranjbarian, B., Shaemi, A., & Ansari, A. (2011). Determinants of Customer Loyalty Using Mobile Payment Services in Iran. IJCRB, 3(6), 22. Schierz, P. G., Schilke, O., & Wirtz, B. W. (2010). Understanding consumer acceptance of mobile payment services: An empirical analysis. Electronic Commerce Research and Applications, 9(3), Swilley, E. (2010). Technology rejection: the case of the wallet phone. Journal of Consumer Marketing, 27(4),

48 Szajna, B. (1996). Empirical evaluation of the revised technology acceptance model. Management science, 42(1), Thompson, R. L., Higgins, C. A., & Howell, J. M. (1991). Personal computing: toward a conceptual model of utilization. MIS quarterly, Venkatesh, V., & Bala, H. (2008). Technology acceptance model 3 and a research agenda on interventions. Decision sciences, 39(2), Venkatesh, V., & Davis, F. D. (2000). A theoretical extension of the technology acceptance model: four longitudinal field studies. Management science, 46(2), Venkatesh, V., Morris, M.G., Davis, G. B., & Davis, F. D. (2003). User acceptance of Information Technology: Toward a unified view. MIS Quarterly, 27(3), Visa Developers. (n.d.). Visa paywave for Mobile. Retrieved November 2, 2013 from Visa. (n.d.). Retrieved November 2, 2013 from Wafa, S. A. (2009). The Effect of Perceived Risk on the Intention to Use E-commerce: The Case of Algeria. Journal of Internet Banking and Commerce,14(1). Wahid, F. (2010). Examining adoption of e-procurement in public sector using the perceived characteristics of innovating: Indonesian perspective. In Next Generation Society. Technological and Legal Issues (pp ). Springer Berlin Heidelberg. Warren, Y., & Zafar, H. (2008). A Multi-Country Assessment of Mobile Payment Adoption (No. 0055). College of Business, University of Texas at San Antonio. Wikipedia. (2013). Mobile payment. Retrieved November 2, 2013, from 42

49 Wireless Watch Japan. (2005). Japan Rail, DoCoMo State Mobile Suica Plans. Retrieved November 2, 2013 from Yahoo!. (2013). 八 達 通 推 手 機 版 保 江 山. Retrieved October 14, 2013 from %E6%8E%A8%E6%89%8B%E6%A9%9F%E7%89%88%E4%BF%9D%E6% B1%9F%E5%B1%B html Zhou, T., Lu, Y., & Wang, B. (2010). Integrating TTF and UTAUT to explain mobile banking user adoption. Computers in Human Behavior, 26(4),

50 Appendix 1: Survey Items 44

51 45

52 Notes: Reverse Scaled Item 46

53 Appendix 2: Questionnaire (English Version) 47

54 48

55 49

56 Appendix 3: Questionnaire (Chinese Version) 50

57 51

CHAPTER 5: CONSUMERS ATTITUDE TOWARDS ONLINE MARKETING OF INDIAN RAILWAYS

CHAPTER 5: CONSUMERS ATTITUDE TOWARDS ONLINE MARKETING OF INDIAN RAILWAYS 5.1 Introduction This chapter presents the findings of research objectives dealing, with consumers attitude towards online marketing

CHAPTER 5: CONSUMERS ATTITUDE TOWARDS ONLINE MARKETING OF INDIAN RAILWAYS 5.1 Introduction This chapter presents the findings of research objectives dealing, with consumers attitude towards online marketing

Mobile Stock Trading (MST) and its Social Impact: A Case Study in Hong Kong

and its Social Impact: A Case Study in Hong Kong") Mobile Stock Trading (MST) and its Social Impact: A Case Study in Hong Kong K. M. Sam 1, C. R. Chatwin 2, I. C. Ma 3 1 Department of Accounting and Information Management, University of Macau, Macau, China

Mobile Stock Trading (MST) and its Social Impact: A Case Study in Hong Kong K. M. Sam 1, C. R. Chatwin 2, I. C. Ma 3 1 Department of Accounting and Information Management, University of Macau, Macau, China

An Application of the UTAUT Model for Understanding Student Perceptions Using Course Management Software

An Application of the UTAUT Model for Understanding Student Perceptions Using Course Management Software Jack T. Marchewka Chang Liu Operations Management and Information Systems Department Northern Illinois

An Application of the UTAUT Model for Understanding Student Perceptions Using Course Management Software Jack T. Marchewka Chang Liu Operations Management and Information Systems Department Northern Illinois

ANALYSIS OF USER ACCEPTANCE OF A NETWORK MONITORING SYSTEM WITH A FOCUS ON ICT TEACHERS

ANALYSIS OF USER ACCEPTANCE OF A NETWORK MONITORING SYSTEM WITH A FOCUS ON ICT TEACHERS Siti Rahayu Abdul Aziz 1, Mohamad Ibrahim 2, and Suhaimi Sauti 3 1 Universiti Teknologi MARA, Malaysia, rahayu@fskm.uitm.edu.my

ANALYSIS OF USER ACCEPTANCE OF A NETWORK MONITORING SYSTEM WITH A FOCUS ON ICT TEACHERS Siti Rahayu Abdul Aziz 1, Mohamad Ibrahim 2, and Suhaimi Sauti 3 1 Universiti Teknologi MARA, Malaysia, rahayu@fskm.uitm.edu.my

Task-Technology Fit and Adoption Behaviors of Mobile Business Systems

International DSI / Asia and Pacific DSI 2007 Full Paper (July, 2007) Task-Technology Fit and Adoption Behaviors of Mobile Business Systems Ching-Chang Lee *, Kuo-Wei Su, Cheng-Ta Lu, Xin-Xin Yu National

International DSI / Asia and Pacific DSI 2007 Full Paper (July, 2007) Task-Technology Fit and Adoption Behaviors of Mobile Business Systems Ching-Chang Lee *, Kuo-Wei Su, Cheng-Ta Lu, Xin-Xin Yu National

EXAMINING HEALTHCARE PROFESSIONALS ACCEPTANCE OF ELECTRONIC MEDICAL RECORDS USING UTAUT

EXAMINING HEALTHCARE PROFESSIONALS ACCEPTANCE OF ELECTRONIC MEDICAL RECORDS USING UTAUT Matthew J. Wills, Dakota State University Omar F. El-Gayar, Dakota State University Dorine Bennett, Dakota State

EXAMINING HEALTHCARE PROFESSIONALS ACCEPTANCE OF ELECTRONIC MEDICAL RECORDS USING UTAUT Matthew J. Wills, Dakota State University Omar F. El-Gayar, Dakota State University Dorine Bennett, Dakota State

A COMPARISON ANALYSIS ON THE INTENTION TO CONTINUED USE OF A LIFELONG LEARNING WEBSITE

International Journal of Electronic Business Management, Vol. 10, No. 3, pp. 213-223 (2012) 213 A COMPARISON ANALYSIS ON THE INTENTION TO CONTINUED USE OF A LIFELONG LEARNING WEBSITE Hsiu-Li Liao * and

International Journal of Electronic Business Management, Vol. 10, No. 3, pp. 213-223 (2012) 213 A COMPARISON ANALYSIS ON THE INTENTION TO CONTINUED USE OF A LIFELONG LEARNING WEBSITE Hsiu-Li Liao * and

The Diffusion of E-Learning Innovations in an Australian Secondary College: Strategies and Tactics for Educational Leaders

The Diffusion of E-Learning Innovations in an Australian Secondary College: Strategies and Tactics for Educational Leaders Sam Jebeile Division of Economic and Financial Studies Macquarie University Australia

The Diffusion of E-Learning Innovations in an Australian Secondary College: Strategies and Tactics for Educational Leaders Sam Jebeile Division of Economic and Financial Studies Macquarie University Australia

Older-Users Acceptance of Smartcard Payment Systems: An Investigation of an Old-street Venders

Older-Users Acceptance of Smartcard Payment Systems: An Investigation of an Old-street Venders 1 Sheng-Chin Yu, 2 Fong-Ling Fu, 3 Chia-jen Ting, 4 Hsing-Chuan Lu 1, Assoc Prof. of TungNan University, scyu@mail.tnu.edu.tw

Older-Users Acceptance of Smartcard Payment Systems: An Investigation of an Old-street Venders 1 Sheng-Chin Yu, 2 Fong-Ling Fu, 3 Chia-jen Ting, 4 Hsing-Chuan Lu 1, Assoc Prof. of TungNan University, scyu@mail.tnu.edu.tw

Barriers & Incentives to Obtaining a Bachelor of Science Degree in Nursing

Southern Adventist Univeristy KnowledgeExchange@Southern Graduate Research Projects Nursing 4-2011 Barriers & Incentives to Obtaining a Bachelor of Science Degree in Nursing Tiffany Boring Brianna Burnette

Southern Adventist Univeristy KnowledgeExchange@Southern Graduate Research Projects Nursing 4-2011 Barriers & Incentives to Obtaining a Bachelor of Science Degree in Nursing Tiffany Boring Brianna Burnette

MAGNT Research Report (ISSN. 1444-8939) Vol.2 (Special Issue) PP: 213-220

Vol.2 (Special Issue) PP: 213-220") Studying the Factors Influencing the Relational Behaviors of Sales Department Staff (Case Study: The Companies Distributing Medicine, Food and Hygienic and Cosmetic Products in Arak City) Aram Haghdin

Studying the Factors Influencing the Relational Behaviors of Sales Department Staff (Case Study: The Companies Distributing Medicine, Food and Hygienic and Cosmetic Products in Arak City) Aram Haghdin

Asian Research Journal of Business Management

Asian Research Journal of Business Management FACTORS INFLUENCING ONLINE TRADING ADOPTION: A STUDY ON INVESTORS ATTITUDE IN GREATER VISAKHAPATNAM CITY Dr. Krishna Mohan Vaddadi 1 & Merugu Pratima 2 * 1

Asian Research Journal of Business Management FACTORS INFLUENCING ONLINE TRADING ADOPTION: A STUDY ON INVESTORS ATTITUDE IN GREATER VISAKHAPATNAM CITY Dr. Krishna Mohan Vaddadi 1 & Merugu Pratima 2 * 1

Evaluating the Factors Affecting on Intension to Use of E-Recruitment

American Journal of Information Science and Computer Engineering Vol., No. 5, 205, pp. 324-33 http://www.aiscience.org/journal/ajisce Evaluating the Factors Affecting on Intension to Use of E-Recruitment

American Journal of Information Science and Computer Engineering Vol., No. 5, 205, pp. 324-33 http://www.aiscience.org/journal/ajisce Evaluating the Factors Affecting on Intension to Use of E-Recruitment

Technology Complexity, Personal Innovativeness And Intention To Use Wireless Internet Using Mobile Devices In Malaysia

International Review of Business Research Papers Vol.4 No.5. October-November 2008. PP.1-10 Technology Complexity, Personal Innovativeness And Intention To Use Wireless Internet Using Mobile Devices In

International Review of Business Research Papers Vol.4 No.5. October-November 2008. PP.1-10 Technology Complexity, Personal Innovativeness And Intention To Use Wireless Internet Using Mobile Devices In

The Online Banking Usage in Indonesia: An Empirical Study

DOI: 10.7763/IPEDR. 2012. V54. 19 The Online Banking Usage in Indonesia: An Empirical Study Sulistyo Budi Utomo 1 + 1 Indonesia School of Economics (STIESIA) Surabaya Abstract. Many Indonesian banks have

DOI: 10.7763/IPEDR. 2012. V54. 19 The Online Banking Usage in Indonesia: An Empirical Study Sulistyo Budi Utomo 1 + 1 Indonesia School of Economics (STIESIA) Surabaya Abstract. Many Indonesian banks have

Issues in Information Systems Volume 16, Issue I, pp. 163-169, 2015

A Task Technology Fit Model on e-learning Linwu Gu, Indiana University of Pennsylvania, lgu@iup.edu Jianfeng Wang, Indiana University of Pennsylvania, jwang@iup.edu ABSTRACT In this research, we propose

A Task Technology Fit Model on e-learning Linwu Gu, Indiana University of Pennsylvania, lgu@iup.edu Jianfeng Wang, Indiana University of Pennsylvania, jwang@iup.edu ABSTRACT In this research, we propose

Employees technology acceptance of ERP systems in a Bulgarian car dealer company

Employees technology acceptance of ERP systems in a Bulgarian car dealer company Vladislav Damaskinov 1, Panayiotis H. Ketikidis 2, Adrian Solomon 3 1 The University of Sheffield International Faculty,

Employees technology acceptance of ERP systems in a Bulgarian car dealer company Vladislav Damaskinov 1, Panayiotis H. Ketikidis 2, Adrian Solomon 3 1 The University of Sheffield International Faculty,

An Empirical Study on the Influence of Perceived Credibility of Online Consumer Reviews

An Empirical Study on the Influence of Perceived Credibility of Online Consumer Reviews GUO Guoqing 1, CHEN Kai 2, HE Fei 3 1. School of Business, Renmin University of China, 100872 2. School of Economics

An Empirical Study on the Influence of Perceived Credibility of Online Consumer Reviews GUO Guoqing 1, CHEN Kai 2, HE Fei 3 1. School of Business, Renmin University of China, 100872 2. School of Economics

COMPARISONS OF CUSTOMER LOYALTY: PUBLIC & PRIVATE INSURANCE COMPANIES.

277 CHAPTER VI COMPARISONS OF CUSTOMER LOYALTY: PUBLIC & PRIVATE INSURANCE COMPANIES. This chapter contains a full discussion of customer loyalty comparisons between private and public insurance companies

277 CHAPTER VI COMPARISONS OF CUSTOMER LOYALTY: PUBLIC & PRIVATE INSURANCE COMPANIES. This chapter contains a full discussion of customer loyalty comparisons between private and public insurance companies

EFFECT OF ENVIRONMENTAL CONCERN & SOCIAL NORMS ON ENVIRONMENTAL FRIENDLY BEHAVIORAL INTENTIONS

169 EFFECT OF ENVIRONMENTAL CONCERN & SOCIAL NORMS ON ENVIRONMENTAL FRIENDLY BEHAVIORAL INTENTIONS Joshi Pradeep Assistant Professor, Quantum School of Business, Roorkee, Uttarakhand, India joshipradeep_2004@yahoo.com

169 EFFECT OF ENVIRONMENTAL CONCERN & SOCIAL NORMS ON ENVIRONMENTAL FRIENDLY BEHAVIORAL INTENTIONS Joshi Pradeep Assistant Professor, Quantum School of Business, Roorkee, Uttarakhand, India joshipradeep_2004@yahoo.com

ConsumerBehaviouralIntentionstowardInternetMarketing

Global Journal of Science Frontier Research: Interdiciplinary Volume 15 Issue 1 Version 1.0 Year 2015 Type : Double Blind Peer Reviewed International Research Journal Publisher: Global Journals Inc. (USA

Global Journal of Science Frontier Research: Interdiciplinary Volume 15 Issue 1 Version 1.0 Year 2015 Type : Double Blind Peer Reviewed International Research Journal Publisher: Global Journals Inc. (USA

User Behavior Research of Information Security Technology Based on TAM

, pp.203-210 http://dx.doi.org/10.14257/ijsia.2014.8.2.21 User Behavior Research of Information Security Technology Based on TAM Wang Cheng 1 and Wang Shi-bo 1 1 School of Economics and Management of Qiqihar

, pp.203-210 http://dx.doi.org/10.14257/ijsia.2014.8.2.21 User Behavior Research of Information Security Technology Based on TAM Wang Cheng 1 and Wang Shi-bo 1 1 School of Economics and Management of Qiqihar

Students Acceptance on Document Sharing through Online Storage System

Students Acceptance on Document Sharing through Online Storage System Wan Hussain Wan Ishak, Fadhilah Mat Yamin, Amlus Ibrahim Universiti Utara Malaysia, Sintok, Kedah, Malaysia Email: hussain@uum.edu.my

Students Acceptance on Document Sharing through Online Storage System Wan Hussain Wan Ishak, Fadhilah Mat Yamin, Amlus Ibrahim Universiti Utara Malaysia, Sintok, Kedah, Malaysia Email: hussain@uum.edu.my

How to Get More Value from Your Survey Data

Technical report How to Get More Value from Your Survey Data Discover four advanced analysis techniques that make survey research more effective Table of contents Introduction..............................................................2

Technical report How to Get More Value from Your Survey Data Discover four advanced analysis techniques that make survey research more effective Table of contents Introduction..............................................................2

Customers Acceptance of Online Shopping In Saudi Arabia

Customers Acceptance of Online Shopping In Saudi Arabia Sulaiman A. Al-Hudhaif, Ph.D. Saleh Saad Alqahtani, Ph.D. College of Business Administration King Saud University Introduction: Good news for e-

Customers Acceptance of Online Shopping In Saudi Arabia Sulaiman A. Al-Hudhaif, Ph.D. Saleh Saad Alqahtani, Ph.D. College of Business Administration King Saud University Introduction: Good news for e-

SCIENCE ROAD JOURNAL

SCIENCE ROAD Journal SCIENCE ROAD JOURNAL Year: 2015 Volume: 03 Issue: 03 Pages: 278-285 Analyzing the impact of knowledge management on the success of customer communications with intermediary role of

SCIENCE ROAD Journal SCIENCE ROAD JOURNAL Year: 2015 Volume: 03 Issue: 03 Pages: 278-285 Analyzing the impact of knowledge management on the success of customer communications with intermediary role of

Electronic Ticketing in Airline Industries among Malaysians: the Determinants

Electronic Ticketing in Airline Industries among ns: the Determinants Tee Poh Kiong Faculty of Business and Management Behrooz Gharleghi Benjamin Chan Yin-Fah Faculty of Business and Management Centre

Electronic Ticketing in Airline Industries among ns: the Determinants Tee Poh Kiong Faculty of Business and Management Behrooz Gharleghi Benjamin Chan Yin-Fah Faculty of Business and Management Centre

The impact of relationship marketing on customer loyalty enhancement (Case study: Kerman Iran insurance company)

") Marketing and Branding Research 3(2016) 41-49 MARKETING AND BRANDING RESEARCH WWW.AIMIJOURNAL.COM INDUSTRIAL MANAGEMENT INSTITUTE The impact of relationship marketing on customer loyalty enhancement (Case

Marketing and Branding Research 3(2016) 41-49 MARKETING AND BRANDING RESEARCH WWW.AIMIJOURNAL.COM INDUSTRIAL MANAGEMENT INSTITUTE The impact of relationship marketing on customer loyalty enhancement (Case

INVESTIGATION OF EFFECTIVE FACTORS IN USING MOBILE ADVERTISING IN ANDIMESHK. Abstract

INVESTIGATION OF EFFECTIVE FACTORS IN USING MOBILE ADVERTISING IN ANDIMESHK Mohammad Ali Enayati Shiraz 1, Elham Ramezani 2 1-2 Department of Industrial Management, Islamic Azad University, Andimeshk Branch,

INVESTIGATION OF EFFECTIVE FACTORS IN USING MOBILE ADVERTISING IN ANDIMESHK Mohammad Ali Enayati Shiraz 1, Elham Ramezani 2 1-2 Department of Industrial Management, Islamic Azad University, Andimeshk Branch,

PREDICTING ACCEPTANCE OF ELECTRONIC MEDICAL RECORDS: WHAT FACTORS MATTER MOST?

PREDICTING ACCEPTANCE OF ELECTRONIC MEDICAL RECORDS: WHAT FACTORS MATTER MOST? Shanan G. Gibson & Elaine D. Seeman College of Business, East Carolina University gibsons@ecu.edu; seemane@ecu.edu ABSTRACT

PREDICTING ACCEPTANCE OF ELECTRONIC MEDICAL RECORDS: WHAT FACTORS MATTER MOST? Shanan G. Gibson & Elaine D. Seeman College of Business, East Carolina University gibsons@ecu.edu; seemane@ecu.edu ABSTRACT

Potentiality of Online Sales and Customer Relationships

Potentiality of Online Sales and Customer Relationships P. Raja, R. Arasu, and Mujeebur Salahudeen Abstract Today Internet is not only a networking media, but also as a means of transaction for consumers

Potentiality of Online Sales and Customer Relationships P. Raja, R. Arasu, and Mujeebur Salahudeen Abstract Today Internet is not only a networking media, but also as a means of transaction for consumers

Jurnal Teknologi CONTINUOUS USE OF ONLINE STORAGE SYSTEM FOR DOCUMENT SHARING. Full Paper. Fadhilah Mat Yamin a*, Wan Hussain Wan Ishak b

Jurnal Teknologi CONTINUOUS USE OF ONLINE STORAGE SYSTEM FOR DOCUMENT SHARING Fadhilah Mat Yamin a*, Wan Hussain Wan Ishak b a School of Technology Management & Logistics, College of Business, Universiti

Jurnal Teknologi CONTINUOUS USE OF ONLINE STORAGE SYSTEM FOR DOCUMENT SHARING Fadhilah Mat Yamin a*, Wan Hussain Wan Ishak b a School of Technology Management & Logistics, College of Business, Universiti

Decision Support Systems

Decision Support Systems 51 (2011) 587 596 Contents lists available at ScienceDirect Decision Support Systems journal homepage: www.elsevier.com/locate/dss The adoption of mobile healthcare by hospital's

Decision Support Systems 51 (2011) 587 596 Contents lists available at ScienceDirect Decision Support Systems journal homepage: www.elsevier.com/locate/dss The adoption of mobile healthcare by hospital's