U.S. Financial Accounts: Uses and Improvements

|

|

|

- Lauren Randall

- 8 years ago

- Views:

Transcription

1 U.S. Financial Accounts: Susan Hume McIntosh Group Manager, Financial Accounts Projects Board of Governors of the Federal Reserve System Financial Information Forum of Latin American and Caribbean Central Banks Mexico City, Mexico

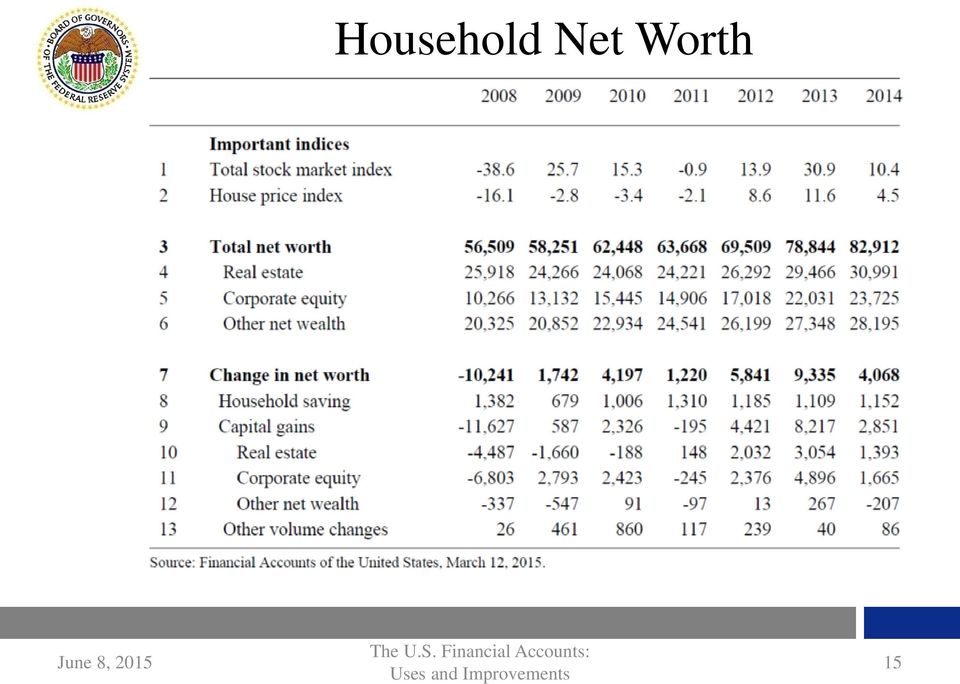

2 Household Net Worth Americans Are Richer and Behaving Responsibly for Once They owe less on their mortgages, and their bank accounts are flush with cash. In the last year, unemployment dropped, stocks reached record highs, and gas prices plunged. Americans got richer, so what did we do to celebrate? We paid down our mortgages. As the net worth of U.S. households rose 5.2 percent last year, to $82.9 trillion, new Federal Reserve data show the value of outstanding mortgages fell slightly in the same period. Homeowners now own 54.5 percent of their real estate, up from less than 40 percent three years earlier. Meanwhile, most other kinds of debt are up only slightly. The Fed s measure of consumer credit rose $218.4 billion last year, to $3.3 trillion. The strongest growth in debt is confined to two areas student loans and auto loans which accounted for more than 80 percent of the rise. Bloomberg Business, March 12,

3 Discussion Outline History and scope Integrated macroeconomic accounts Uses of the Financial Accounts 1. Household balance sheet 2. Debt growth 3. Nonbank financial institutions Recent improvements 1. Pension entitlements 2. Mortgage charge-offs 3. Consumer credit detail Enhanced Financial Accounts 3

4 History of FA Tables first published Annual flow statistics: 1955 Quarterly flow statistics: 1959 (Unadj.); 1962 (SA) Outstandings (levels) tables: early 1960s (A); early 1990s (Q) Balance sheets, reconciliation tables, and supplemental tables Integrated Macroeconomic Accounts: 2004 Availability Annual data: Quarterly data: 1952:Q4-2014:Q4 Integrated accounts: (A), 1960:Q1-2014:Q4 (Q) Z.1 published about 10 weeks following the end of a quarter 4 4

, 1960:Q1-2014:Q4 (Q) Z.")

5 History of Integrated Accounts in U.S. Joint between the Bureau of Economic Analysis (BEA) and the Federal Reserve Board (FRB) Based on SNA format; consistent with SNA2008 First version released at NBER Conference April 2004 (annual data ) Annual data for and quarterly data for 1960q1-2014q4 Tables at Data at Documentation (FOF Guide) at Articles 1. Cagetti, Marco, Elizabeth Ball Holmquist, Lisa Lynn, Susan Hume McIntosh, and David Wasshausen (2012). "The Integrated Macroeconomic Accounts of the United States," Finance and Economics Discussion Series Board of Governors of the Federal Reserve System (U.S.). 2. Teplin, Albert, Charles Mead, Brent Moulton, Rochelle Antoniewicz, Susan McIntosh, Michael Palumbo, and Genevieve Solomon (2005). "Integrated Macroeconomic Accounts for the United States: Draft SNA-USA," BEA Papers Bureau of Economic Analysis. 5

at http://www.federalreserve.gov/apps/fof Articles 1. Cagetti, Marco, Elizabeth Ball Holmquist, Lisa Lynn, Susan Hume McIntosh, and David Wasshausen (2012).")

6 Sequence of Accounts 6

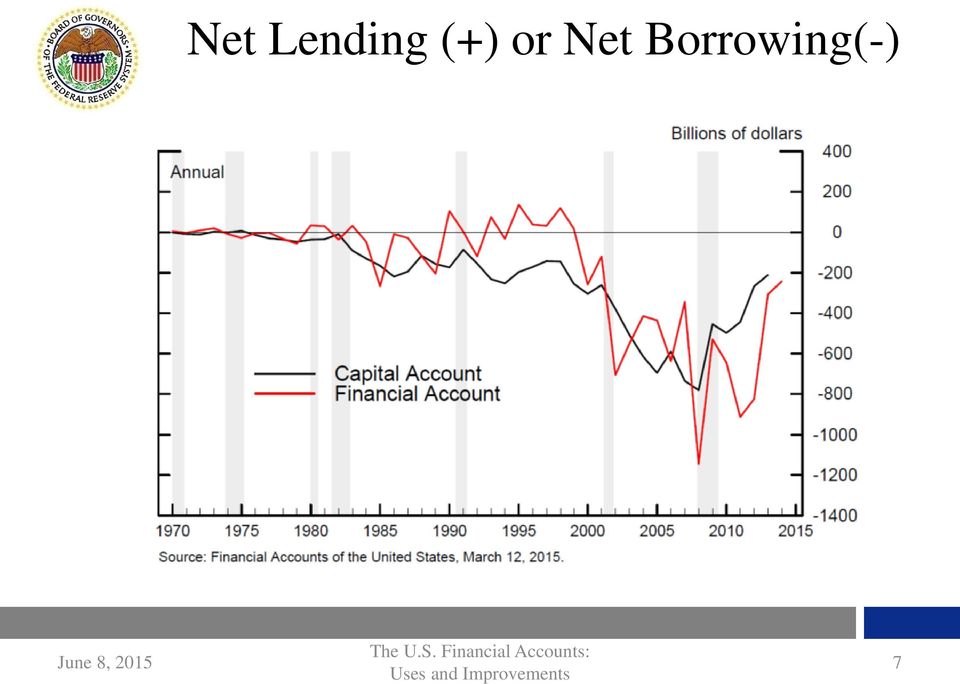

7 Net Lending (+) or Net Borrowing(-) 7

8 Net Lending (+) or Net Borrowing(-): June

9 Net Lending(+) or Net Borrowing(-), by Households and Nonprofits 9

10 Net Lending(+) or Net Borrowing(-), by Financial Corporations 10

11 Project to Develop Financial Business Subsectors 22 financial subsectors in the Financial Accounts; balance sheet, transactions, revaluations, and OCVA (institution-based) Sectoral problems aligning with the current and capital accounts from BEA (industry-based) BEA has developed 5 subsectors with annual data beginning in 2001; NAICS was used throughout this period. Still in research stage. Hope to publish by end of year Will present at BEA Advisory meeting on May 8,

12 BEA Financial Subsectors Depository institutions: U.S.-chartered, foreign banking offices in U.S., and credit unions; we also include banks in U.S.-affiliated areas in FAs Insurance companies: property-casualty insurance companies and life insurance companies Pension funds: private, federal government, and state and local government plans Federal Reserve banks: similar to Monetary Authority sector in FAs; does not include Federal Reserve Board Remaining non-depository institutions 12

13 Uses of the Financial Accounts Measure the acquisition of physical and financial assets throughout the U.S. economy Track the sources of funds used to acquire the assets Record the net volume of transactions in financial instruments Provide a means of analyzing the development of instruments and the behavior of sectors over business cycles Record the role of financial intermediaries in transferring funds between sectors Only source to provide household sector balance sheet quarterly 13

14 Projection Household net worth important to forecast of consumption component of GDP; life-cycle theory of consumption Forecast based on expected movements in real estate, equity markets, and the personal savings rate Simplified framework rather than trying to forecast a condensed version of the entire Financial Accounts 14

15 Household Net Worth 15

16 Household Net Worth Relative to Disposable Personal Income 16

17 Corporate and Home Equity Relative to Disposable Personal Income 17

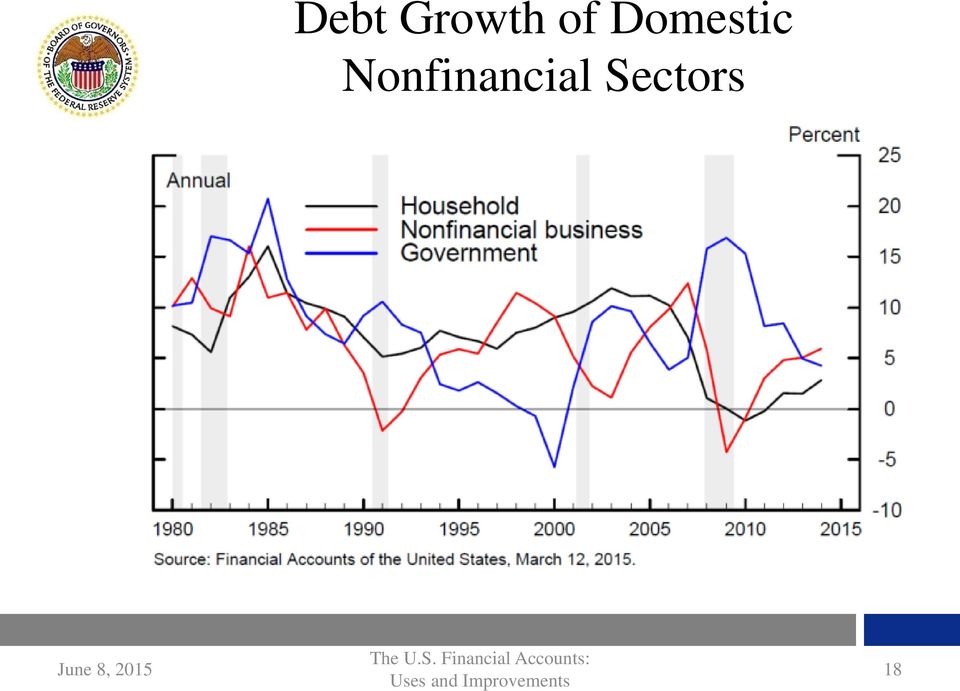

18 Debt Growth of Domestic Nonfinancial Sectors 18

19 Household Liabilities Relative to Disposable Personal Income 19

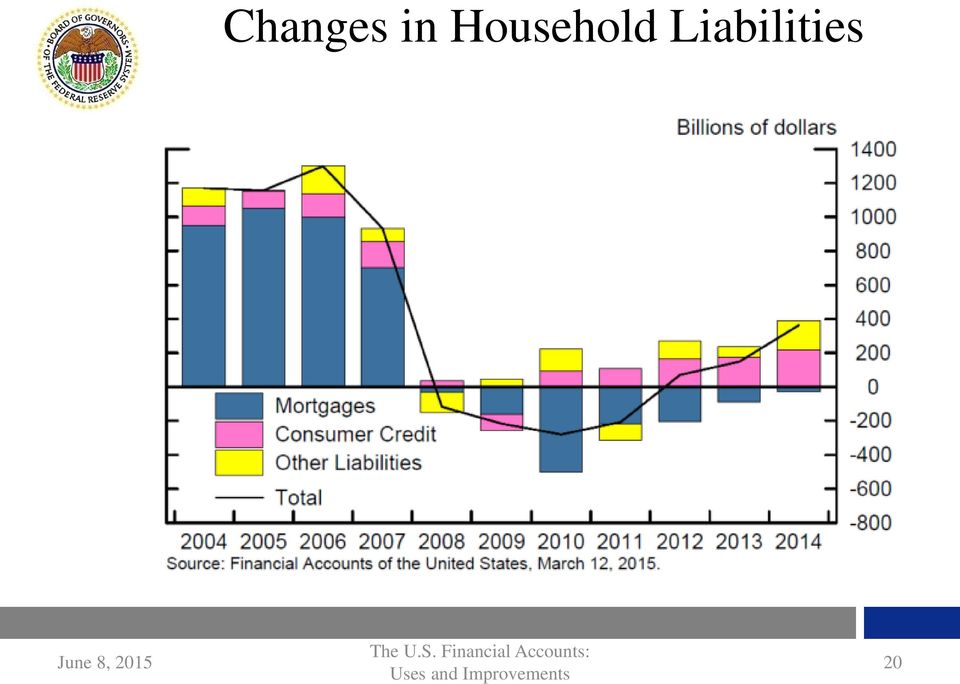

20 Changes in Household Liabilities 20

21 Consumer Credit 21

22 Nonbank Financial Sector Vice chairman Stanley Fischer speech on 3/27/2015 on The Importance of the Nonbank Financial Sector at a conference with the Bundesbank and German Ministry of Finance, Frankfurt 1980 nonbanks 40% of domestic financial sectors; late 1990s nonbanks were 2/3 of the total; percentage remained stable Reforms: Financial Stability Oversight council (FSOC), SEC new rules for money market mutual funds, securitizers must retain at least 5% of the credit risk of assets FSOC designated 4 U.S. nonbank financial institutions as systemically important; subject to consolidated supervision by the FRB Data issues: hedge funds, derivative market, limited information on leverage and maturity transformation 22

23 Recent Improvements Online Guide: release highlights, FEDS notes, international data submissions Reorganization of tables, more supplemental tables and memo items Close gaps with international standards Continued collaboration with other statistical agencies Splitting flow into transaction, revaluation, and other volume changes. Pension funds on an accrual basis 23

24 Economic Flows Transactions Level t-1 Revaluations Level t OCVAs 24

25 Changes in Household and Nonprofit Net Worth 25

26 Home Mortgage Charge-offs Home mortgage debt declined $1.3 trillion since the 2008 peak, with 75% of decline due to charge-offs Previous treatment: Charge-offs a negative component of aggregate mortgage borrowing (transaction) New treatment: Charge-offs excluded from aggregate borrowing; now included in other changes in volume Increases reported mortgage debt transactions Reduces personal saving Mortgage debt outstanding and household net worth unchanged 26

27 Change in Residential Mortgage Debt 27

28 Household Retirement Assets 28

29 Pension Entitlements of the Household Sector 29

30 Claims of Pension Funds on Sponsors 30

31 Enhanced Financial Accounts Maintain basic framework More detail, dimensionality, and scope Additional detail on financial instruments Information on holdings and activities currently not well described Higher frequency data, supplementary data, and data for lower levels of aggregation Improved data dissemination and communication FEDS Note: Enhanced Financial Accounts, by Josh Gallin and Paul Smith, August 1,

32 Additional Detail on Financial Instruments Treasury securities split into bills and other Corporate bonds split into structured products and other; also holdings by domestic and foreign Split federal funds from repurchase agreements Detail on consumer credit Credit-risk ratings of fixed-income securities Social security table Different measures of government debt 529 educational plans 32

33 Holdings and Activities Currently Not Well Described Securities lending and the investment of cash collateral pools Hedge funds and other private funds Nonprofit organizations Holding companies other than those that own a depository institution Derivatives credit default and interest-rate swaps Employee stock options Net national wealth table 33

34 Data at Higher Frequencies and Lower Levels of Aggregation Monthly money-market mutual fund data Weekly commercial paper data Mutual fund data by type of fund Nonfinancial corporate business sector by industry Rest of world borrowing and lending by region Distributional work using the Survey of Consumer Finances 34

35 Improved Data Dissemination and Communication Online Guide Release highlights FEDS notes International data submissions with SDMX New website being developed Enhanced data download capabilities Possible conference in 2016 with users on the EFA 35

36

The Integrated Macroeconomic Accounts of the United States

The Integrated Macroeconomic Accounts of the United States McIntosh, Susan Hume Board of Governors of the Federal Reserve System, Research and Statistics 20 th and Constitution Ave., N.W. Washington, D.C.

The Integrated Macroeconomic Accounts of the United States McIntosh, Susan Hume Board of Governors of the Federal Reserve System, Research and Statistics 20 th and Constitution Ave., N.W. Washington, D.C.

The Integrated Macroeconomic Accounts of the United States

The Integrated Macroeconomic Accounts of the United States Marco Cagetti, Elizabeth Ball Holmquist, Lisa Lynn, Susan Hume McIntosh, and David Wasshausen 1 The integrated macroeconomic accounts (IMAs),

The Integrated Macroeconomic Accounts of the United States Marco Cagetti, Elizabeth Ball Holmquist, Lisa Lynn, Susan Hume McIntosh, and David Wasshausen 1 The integrated macroeconomic accounts (IMAs),

Flow of Funds - Overview of Japan, US, and the Euro area -

Flow of Funds - Overview of, US, and the - September 30, 201 Research and Statistics Department Bank of *In this paper, major sectors are compared either among, the, and the or between and the. Ⅰ. Overview:,

Flow of Funds - Overview of, US, and the - September 30, 201 Research and Statistics Department Bank of *In this paper, major sectors are compared either among, the, and the or between and the. Ⅰ. Overview:,

Flow of Funds Accounts of the United States

June 5, 2008 Flow of Funds Accounts of the United States Annual Flows and Outstandings 2005-2007 Board of Governors of the Federal Reserve System, Washington D.C. 20551 Table of Contents Flows Levels Title

June 5, 2008 Flow of Funds Accounts of the United States Annual Flows and Outstandings 2005-2007 Board of Governors of the Federal Reserve System, Washington D.C. 20551 Table of Contents Flows Levels Title

Flow of Funds Data Dictionary

Flow of Funds Data Dictionary October 2003 This version of documentation is preliminary and does not necessarily represent the current Global Insight (formerly DRI WEFA) database. The availability of specific

Flow of Funds Data Dictionary October 2003 This version of documentation is preliminary and does not necessarily represent the current Global Insight (formerly DRI WEFA) database. The availability of specific

BEA BRIEFING A Guide to the Integrated Macroeconomic Accounts

12 April 213 BEA BRIEFING A Guide to the Integrated Macroeconomic Accounts By Takashi Yamashita T The author is grateful to Marco Cagetti, Elizabeth Holmquist, Robert Kornfeld, Lisa Lynn, Susan Hume McIntosh,

12 April 213 BEA BRIEFING A Guide to the Integrated Macroeconomic Accounts By Takashi Yamashita T The author is grateful to Marco Cagetti, Elizabeth Holmquist, Robert Kornfeld, Lisa Lynn, Susan Hume McIntosh,

Financial Stability Oversight Council. Staff Guidance. Methodologies Relating to Stage 1 Thresholds. June 8, 2015

Financial Stability Oversight Council Staff Guidance Methodologies Relating to Stage 1 Thresholds June 8, 2015 Stage 1 Overview Section 113 of the Dodd-Frank Wall Street Reform and Consumer Protection

Financial Stability Oversight Council Staff Guidance Methodologies Relating to Stage 1 Thresholds June 8, 2015 Stage 1 Overview Section 113 of the Dodd-Frank Wall Street Reform and Consumer Protection

The U.S. Flow of Funds Accounts and Their Uses

The U.S. Flow of Funds Accounts and Their Uses Albert M. Teplin, of the Board's Division of Research and Statistics, prepared this article. Andrew M. Tyler assisted with the data. Each day, a wealth of

The U.S. Flow of Funds Accounts and Their Uses Albert M. Teplin, of the Board's Division of Research and Statistics, prepared this article. Andrew M. Tyler assisted with the data. Each day, a wealth of

Chapter 17. Financial Management and Institutions

Chapter 17 Financial Management and Institutions 1 2 3 4 Identify the functions performed by a firm s financial managers. Describe the characteristics and functions of money. Identify the various measures

Chapter 17 Financial Management and Institutions 1 2 3 4 Identify the functions performed by a firm s financial managers. Describe the characteristics and functions of money. Identify the various measures

How Property/Casualty Insurance Companies Invest Premium Dollars

How Property/Casualty Insurance Companies Invest Premium Dollars OVERVIEW Every day, property/casualty insurers enable our economy to function by helping individuals and businesses address the various

How Property/Casualty Insurance Companies Invest Premium Dollars OVERVIEW Every day, property/casualty insurers enable our economy to function by helping individuals and businesses address the various

MONETARY AND FINANCIAL STATISTICS MANUAL. Index

MONETARY AND FINANCIAL STATISTICS MANUAL Index Numbers in references refer to paragraphs Accounting rules, 182 Accrual accounting, 227-239 Accumulation accounts, 406-407, 413, 417, 421-423, 426-437 Administered

MONETARY AND FINANCIAL STATISTICS MANUAL Index Numbers in references refer to paragraphs Accounting rules, 182 Accrual accounting, 227-239 Accumulation accounts, 406-407, 413, 417, 421-423, 426-437 Administered

Guidelines For Compiling Sectoral Accounts

Guidelines For Compiling Sectoral Accounts Venkat Josyula Developing and Improving Sectoral Financial Accounts Algiers, January 20-21, 2016 The views expressed herein are those of the author and should

Guidelines For Compiling Sectoral Accounts Venkat Josyula Developing and Improving Sectoral Financial Accounts Algiers, January 20-21, 2016 The views expressed herein are those of the author and should

Z.1: Financial Accounts of the United States All Table Descriptions

Z.1: Financial Accounts of the United States All Table Descriptions June 9, 2016 Data Tables Summaries Title Tables Page Flow of Funds Matrix Flows 4 Flow of Funds Matrix Assets and Liabilities 4 Debt

Z.1: Financial Accounts of the United States All Table Descriptions June 9, 2016 Data Tables Summaries Title Tables Page Flow of Funds Matrix Flows 4 Flow of Funds Matrix Assets and Liabilities 4 Debt

Public Sector Debt - Instructions

Public Sector Debt - Instructions Under the auspices of the Task Force on Finance Statistics 1 the World Bank has developed a new database to disseminate quarterly data on government, and more broadly,

Public Sector Debt - Instructions Under the auspices of the Task Force on Finance Statistics 1 the World Bank has developed a new database to disseminate quarterly data on government, and more broadly,

Comments on Quarterly Financial Accounts for 1Q 2009

Comments on Quarterly Financial Accounts for 1Q 29 1 The ESA95 system distinguishes the following institutional sectors and sub-sectors: Non-financial corporations S.11 Financial corporations S.12 The

Comments on Quarterly Financial Accounts for 1Q 29 1 The ESA95 system distinguishes the following institutional sectors and sub-sectors: Non-financial corporations S.11 Financial corporations S.12 The

Broker-Dealer Finance and Financial Stability

EMBARGOED UNTIL WEDNESDAY, AUGUST 13, 2014 AT 9:20 A.M. EASTERN TIME OR UPON DELIVERY Broker-Dealer Finance and Financial Stability Eric S. Rosengren President & CEO Federal Reserve Bank of Boston August

EMBARGOED UNTIL WEDNESDAY, AUGUST 13, 2014 AT 9:20 A.M. EASTERN TIME OR UPON DELIVERY Broker-Dealer Finance and Financial Stability Eric S. Rosengren President & CEO Federal Reserve Bank of Boston August

Guide to Japan s Flow of Funds Accounts

Guide to Japan s Flow of Funds Accounts Research and Statistics Department Bank of Japan Introduction The Bank of Japan has been compiling the Flow of Funds Accounts Statistics (the FFA) since 1958, covering

Guide to Japan s Flow of Funds Accounts Research and Statistics Department Bank of Japan Introduction The Bank of Japan has been compiling the Flow of Funds Accounts Statistics (the FFA) since 1958, covering

Guidelines for Preparing an Error-Free Call Report: FFIEC 002 Common Reporting Errors

Guidelines for Preparing an Error-Free Call Report: FFIEC 002 Federal Reserve Bank of New York Updated by: Susan Jessop December, 2002 Guidelines for Preparing an Error-Free Call Report (For FFIEC 002

Guidelines for Preparing an Error-Free Call Report: FFIEC 002 Federal Reserve Bank of New York Updated by: Susan Jessop December, 2002 Guidelines for Preparing an Error-Free Call Report (For FFIEC 002

How do you Complete the Picture of Credit Intermediation? Production and Consumption of Shadow Banking Services in the United States

How do you Complete the Picture of Credit Intermediation? Production and Consumption of Shadow Banking Services in the United States By Carol Corrado, Kyle Hood, and Marshall Reinsdorf Draft: July 11,

How do you Complete the Picture of Credit Intermediation? Production and Consumption of Shadow Banking Services in the United States By Carol Corrado, Kyle Hood, and Marshall Reinsdorf Draft: July 11,

Sixteenth Meeting of the IMF Committee on Balance of Payments Statistics Washington D.C., December 1 5, 2003

BOPCOM-03/23 Sixteenth Meeting of the IMF Committee on Balance of Payments Statistics Washington D.C., December 1 5, 2003 The Statistical Treatment of Unit Trusts Prepared by the South African Reserve

BOPCOM-03/23 Sixteenth Meeting of the IMF Committee on Balance of Payments Statistics Washington D.C., December 1 5, 2003 The Statistical Treatment of Unit Trusts Prepared by the South African Reserve

Supporting Statement for the Domestic Finance Company Report of Consolidated Assets and Liabilities (FR 2248; OMB No. 7100-0005)

") Supporting Statement for the Domestic Finance Company Report of Consolidated Assets and Liabilities (FR 2248; OMB No. 7100-0005) Summary The Board of Governors of the Federal Reserve System, under delegated

Supporting Statement for the Domestic Finance Company Report of Consolidated Assets and Liabilities (FR 2248; OMB No. 7100-0005) Summary The Board of Governors of the Federal Reserve System, under delegated

The New Architecture of U.S. National Accounts

Designing a New Architecture for the U.S. National Accounts By DALE W. JORGENSON The key elements of a new architecture for the U.S. national accounts have been developed in a prototype system constructed

Designing a New Architecture for the U.S. National Accounts By DALE W. JORGENSON The key elements of a new architecture for the U.S. national accounts have been developed in a prototype system constructed

Employment declined dramatically Nonfarm payroll employment (index=100 at peak of business cycle)

") Employment declined dramatically Nonfarm payroll employment (index=1 at peak of business cycle) 27 1981 1973 199 21 198 Index 14 13 12 11 1 99 98 97 96 95 94-5 5 1 15 2 25 3 35 4 Months since peak of business

Employment declined dramatically Nonfarm payroll employment (index=1 at peak of business cycle) 27 1981 1973 199 21 198 Index 14 13 12 11 1 99 98 97 96 95 94-5 5 1 15 2 25 3 35 4 Months since peak of business

Special Purpose Entities (SPEs) and the. Securitization Markets

and the. Securitization Markets") Special Purpose Entities (SPEs) and the Securitization Markets Prepared by: The Bond Market Association International Swaps & Derivatives Association Securities Industry Association February 1, 2002 Special

Special Purpose Entities (SPEs) and the Securitization Markets Prepared by: The Bond Market Association International Swaps & Derivatives Association Securities Industry Association February 1, 2002 Special

Athens University of Economics and Business

Athens University of Economics and Business MSc in International Shipping, Finance and Management Corporate Finance George Leledakis An Overview of Corporate Financing Topics Covered Corporate Structure

Athens University of Economics and Business MSc in International Shipping, Finance and Management Corporate Finance George Leledakis An Overview of Corporate Financing Topics Covered Corporate Structure

Measuring Credit 1. Introduction. What Is Credit?

Measuring Credit 1 Introduction Central banks put significant emphasis on credit aggregates for understanding financial conditions in the economy. Measuring credit outstanding, however, is not straightforward,

Measuring Credit 1 Introduction Central banks put significant emphasis on credit aggregates for understanding financial conditions in the economy. Measuring credit outstanding, however, is not straightforward,

QUARTERLY FINANCIAL ACCOUNTS NORGES BANK I. INTRODUCTION

QUARTERLY FINANCIAL ACCOUNTS NORGES BANK I. INTRODUCTION Statistics Norway published the first set of annual financial balance sheets in 1957. The accounts recorded the stocks of financial assets and liabilities

QUARTERLY FINANCIAL ACCOUNTS NORGES BANK I. INTRODUCTION Statistics Norway published the first set of annual financial balance sheets in 1957. The accounts recorded the stocks of financial assets and liabilities

Public Finance and Banking

9 Public Finance and Banking A General Government Deficit (GG Deficit) of 12,460 million or 7.6% of GDP was recorded in 2012, significantly lower than the 2011 GG Deficit of 21,267 million or 13.1% of

9 Public Finance and Banking A General Government Deficit (GG Deficit) of 12,460 million or 7.6% of GDP was recorded in 2012, significantly lower than the 2011 GG Deficit of 21,267 million or 13.1% of

How To Divide Life Insurance Assets Into Two Accounts

2ASSETS Assets held by life insurers back the companies life, annuity, and health liabilities. Accumulating these assets via the collection of premiums from policyholders and earnings on investments provides

2ASSETS Assets held by life insurers back the companies life, annuity, and health liabilities. Accumulating these assets via the collection of premiums from policyholders and earnings on investments provides

Assessing the Risks of Mortgage REITs. By Sabrina R. Pellerin, David A. Price, Steven J. Sabol, and John R. Walter

Economic Brief November 2013, EB13-11 Assessing the Risks of Mortgage REITs By Sabrina R. Pellerin, David A. Price, Steven J. Sabol, and John R. Walter Regulators have expressed concern about the growth

Economic Brief November 2013, EB13-11 Assessing the Risks of Mortgage REITs By Sabrina R. Pellerin, David A. Price, Steven J. Sabol, and John R. Walter Regulators have expressed concern about the growth

Development of mortgage lending in Russia

Development of mortgage lending in Russia Development of Russian mortgage market: 2007-2012 Mortgage origination, bln. (RUB/$) Mortgage share of residential market turnover 1000 900 800 700 600 500 400

Development of mortgage lending in Russia Development of Russian mortgage market: 2007-2012 Mortgage origination, bln. (RUB/$) Mortgage share of residential market turnover 1000 900 800 700 600 500 400

Producer Price Indexes for Financial Services

Producer Price Indexes for Financial Services Andrew Baer Services Section Chief Producer Price Index Program U.S. Bureau of Labor Statistics December 2014 Overview Investment Banking and Securities Dealing

Producer Price Indexes for Financial Services Andrew Baer Services Section Chief Producer Price Index Program U.S. Bureau of Labor Statistics December 2014 Overview Investment Banking and Securities Dealing

I. Introduction. II. Financial Markets (Direct Finance) A. How the Financial Market Works. B. The Debt Market (Bond Market)

A. How the Financial Market Works. B. The Debt Market (Bond Market)") University of California, Merced EC 121-Money and Banking Chapter 2 Lecture otes Professor Jason Lee I. Introduction In economics, investment is defined as an increase in the capital stock. This is important

University of California, Merced EC 121-Money and Banking Chapter 2 Lecture otes Professor Jason Lee I. Introduction In economics, investment is defined as an increase in the capital stock. This is important

Bank of Ireland US Branch Resolution Plan. Public Version. December 2013. BOI Group Classification: Green - Public

Bank of Ireland US Branch Resolution Plan Public Version December 2013 BOI Group Classification: Green - Public Table of Contents 1. Introduction... 2 2. Name of material entities... 2 3. Core operations

Bank of Ireland US Branch Resolution Plan Public Version December 2013 BOI Group Classification: Green - Public Table of Contents 1. Introduction... 2 2. Name of material entities... 2 3. Core operations

Bank Liabilities Survey. Survey results 2013 Q3

Bank Liabilities Survey Survey results 13 Q3 Bank Liabilities Survey 13 Q3 Developments in banks balance sheets are of key interest to the Bank of England in its assessment of economic conditions. Changes

Bank Liabilities Survey Survey results 13 Q3 Bank Liabilities Survey 13 Q3 Developments in banks balance sheets are of key interest to the Bank of England in its assessment of economic conditions. Changes

Guide to Reformatted Quarterly Financial Data Supplement

Guide to Reformatted Quarterly Financial Data Supplement This guide to the reformatted quarterly financial data supplement is intended to highlight the key changes to the supplement and is not a comprehensive

Guide to Reformatted Quarterly Financial Data Supplement This guide to the reformatted quarterly financial data supplement is intended to highlight the key changes to the supplement and is not a comprehensive

Key monetary statistics September 2014

Key monetary statistics September 2014 On a monthly basis, the monetary aggregate M3 increased by 0.6 percent to 1,059 billion dirhams. This change is mainly due to the 1.4 percent increase in bank lending

Key monetary statistics September 2014 On a monthly basis, the monetary aggregate M3 increased by 0.6 percent to 1,059 billion dirhams. This change is mainly due to the 1.4 percent increase in bank lending

Credit Conditions Survey. Survey results 2014 Q4

Credit Conditions Survey Survey results 14 Q4 Credit Conditions Survey 14 Q4 As part of its mission to maintain monetary stability and financial stability, the Bank needs to understand trends and developments

Credit Conditions Survey Survey results 14 Q4 Credit Conditions Survey 14 Q4 As part of its mission to maintain monetary stability and financial stability, the Bank needs to understand trends and developments

CITI REPORTS FIRST QUARTER INCOME OF $5.01 BILLION, EPS OF $1.01 RECORD REVENUES OF $25.5 BILLION, UP 15% INTERNATIONAL REVENUES UP 18%

CITI REPORTS FIRST QUARTER INCOME OF $5.01 BILLION, EPS OF $1.01 RECORD REVENUES OF $25.5 BILLION, UP 15% INTERNATIONAL REVENUES UP 18% RECORD REVENUES AND NET INCOME IN MARKETS & BANKING AND WEALTH MANAGEMENT

CITI REPORTS FIRST QUARTER INCOME OF $5.01 BILLION, EPS OF $1.01 RECORD REVENUES OF $25.5 BILLION, UP 15% INTERNATIONAL REVENUES UP 18% RECORD REVENUES AND NET INCOME IN MARKETS & BANKING AND WEALTH MANAGEMENT

Methodological notes on monetary statistics of depository institutions

Methodology Pursuant to the new Decision on Minimum Standards for Credit Risk Management in Banks 1 the following new decisions were passed: Decision on Chart of Accounts for Banks 2 and the Decision on

Methodology Pursuant to the new Decision on Minimum Standards for Credit Risk Management in Banks 1 the following new decisions were passed: Decision on Chart of Accounts for Banks 2 and the Decision on

Lecture 4: The Aftermath of the Crisis

Lecture 4: The Aftermath of the Crisis 2 The Fed s Efforts to Restore Financial Stability A financial panic in fall 2008 threatened the stability of the global financial system. In its lender-of-last-resort

Lecture 4: The Aftermath of the Crisis 2 The Fed s Efforts to Restore Financial Stability A financial panic in fall 2008 threatened the stability of the global financial system. In its lender-of-last-resort

1 Regional Bank Regional banks specialize in consumer and commercial products within one region of a country, such as a state or within a group of states. A regional bank is smaller than a bank that operates

1 Regional Bank Regional banks specialize in consumer and commercial products within one region of a country, such as a state or within a group of states. A regional bank is smaller than a bank that operates

The Effects of Funding Costs and Risk on Banks Lending Rates

The Effects of Funding Costs and Risk on Banks Lending Rates Daniel Fabbro and Mark Hack* After falling for over a decade, the major banks net interest margins appear to have stabilised in a relatively

The Effects of Funding Costs and Risk on Banks Lending Rates Daniel Fabbro and Mark Hack* After falling for over a decade, the major banks net interest margins appear to have stabilised in a relatively

General guidelines for the completion of the bank lending survey questionnaire

General guidelines for the completion of the bank lending survey questionnaire This document includes the general guidelines for the completion of the questionnaire and the terminology used in the survey.

General guidelines for the completion of the bank lending survey questionnaire This document includes the general guidelines for the completion of the questionnaire and the terminology used in the survey.

What s on a bank s balance sheet?

The Capital Markets Initiative January 2014 TO: Interested Parties FROM: David Hollingsworth and Lauren Oppenheimer RE: Capital Requirements and Bank Balance Sheets: Reviewing the Basics What s on a bank

The Capital Markets Initiative January 2014 TO: Interested Parties FROM: David Hollingsworth and Lauren Oppenheimer RE: Capital Requirements and Bank Balance Sheets: Reviewing the Basics What s on a bank

Table 1 Reconciliation of FFA and SCF Definitions of Financial Assets

Table 1 Reconciliation of FFA and Definitions of Financial Assets Asset category FFA Checkable deposits Time & savings deposits Money market mutual funds Government securities Municipal securities Corporate

Table 1 Reconciliation of FFA and Definitions of Financial Assets Asset category FFA Checkable deposits Time & savings deposits Money market mutual funds Government securities Municipal securities Corporate

T he restrictions of Sections 23A and Regulation W

BNA s Banking Report Reproduced with permission from BNA s Banking Report, 100 BBR 109, 1/15/13, 01/15/2013. Copyright 2013 by The Bureau of National Affairs, Inc. (800-372-1033) http://www.bna.com REGULATION

BNA s Banking Report Reproduced with permission from BNA s Banking Report, 100 BBR 109, 1/15/13, 01/15/2013. Copyright 2013 by The Bureau of National Affairs, Inc. (800-372-1033) http://www.bna.com REGULATION

Data on the balance sheet positions of households and financial and non-financial corporations in Slovenia

Data on the balance sheet positions of households and financial and non-financial corporations in Slovenia Nina Bostner 1. Introduction Financial accounts statistics represent an important analytic tool

Data on the balance sheet positions of households and financial and non-financial corporations in Slovenia Nina Bostner 1. Introduction Financial accounts statistics represent an important analytic tool

Central Bank Survey. General Provisions

Summary Methodology Central Bank Survey, Credit Institutions Survey, Banking System Survey, Other Financial Institutions Survey, Financial Sector Survey Central Bank Survey, Credit Institutions Survey,

Summary Methodology Central Bank Survey, Credit Institutions Survey, Banking System Survey, Other Financial Institutions Survey, Financial Sector Survey Central Bank Survey, Credit Institutions Survey,

Wealth Management Solutions

Wealth Management Solutions Delray Financial Group LLC is an independent regional boutique wealth management firm whose sole business is to serve its clients. With over 25 years of personalized, professional

Wealth Management Solutions Delray Financial Group LLC is an independent regional boutique wealth management firm whose sole business is to serve its clients. With over 25 years of personalized, professional

Statistics Netherlands. Macroeconomic Imbalances Factsheet

Macroeconomic Imbalances Factsheet Introduction Since the outbreak of the credit crunch crisis in 2008, and the subsequent European debt crisis, it has become clear that there are large macroeconomic imbalances

Macroeconomic Imbalances Factsheet Introduction Since the outbreak of the credit crunch crisis in 2008, and the subsequent European debt crisis, it has become clear that there are large macroeconomic imbalances

TABLE 1: SCOPE OF APPLICATION Capital Deficiencies (Table 1, (e))

)") Particulars 4. Subsidiary n TABLE 1: SCOPE OF APPLICATION Capital Deficiencies (Table 1, (e)) The aggregate amount of capital deficiencies in subsidiaries not included in the consolidation i.e. that are

Particulars 4. Subsidiary n TABLE 1: SCOPE OF APPLICATION Capital Deficiencies (Table 1, (e)) The aggregate amount of capital deficiencies in subsidiaries not included in the consolidation i.e. that are

Classification and Presentation of Data on Claims and Liabilities

CNB BULLETIN NOTES ON METHODOLOGY 1 Classification and Presentation of Data on Claims and Liabilities The Croatian National Bank has begun to implement the ESA 2010 standard in its statistics, which also

CNB BULLETIN NOTES ON METHODOLOGY 1 Classification and Presentation of Data on Claims and Liabilities The Croatian National Bank has begun to implement the ESA 2010 standard in its statistics, which also

Macroeconomics, 8e (Parkin) Testbank 1

Testbank 1") Macroeconomics, 8e (Parkin) Testbank 1 Chapter 9 Money, the Price Level, and Inflation 9.1 What is Money? 1) The functions of money are A) medium of exchange and the ability to buy goods and services.

Macroeconomics, 8e (Parkin) Testbank 1 Chapter 9 Money, the Price Level, and Inflation 9.1 What is Money? 1) The functions of money are A) medium of exchange and the ability to buy goods and services.

Currency: The paper money and coins owned by people and business firms

WHAT IS MONEY? Things acceptable as a means of payment 2 TYPES OF MONEY 1. COMMODITY MONIES: 2. FIAT MONIES (TOKEN MONIES): DECREED BY THE GOV T AS LEGAL TENDER. The gov t promises the public that will

WHAT IS MONEY? Things acceptable as a means of payment 2 TYPES OF MONEY 1. COMMODITY MONIES: 2. FIAT MONIES (TOKEN MONIES): DECREED BY THE GOV T AS LEGAL TENDER. The gov t promises the public that will

The Federal Reserve System. The Structure of the Fed. The Fed s Goals and Targets. Economics 202 Principles Of Macroeconomics

Economics 202 Principles Of Macroeconomics Professor Yamin Ahmad The Federal Reserve System The Federal Reserve System, or the Fed, is the central bank of the United States. Supplemental Notes to Monetary

Economics 202 Principles Of Macroeconomics Professor Yamin Ahmad The Federal Reserve System The Federal Reserve System, or the Fed, is the central bank of the United States. Supplemental Notes to Monetary

nstitutional (economic) units, industries and sectors are the main components of economy.

units, industries and sectors are the main components of economy.") 2. Sectors of Economy I nstitutional (economic) units, industries and sectors are the main components of economy. The economy is divided into domestic economy and the rest of the world. The domestic economy

2. Sectors of Economy I nstitutional (economic) units, industries and sectors are the main components of economy. The economy is divided into domestic economy and the rest of the world. The domestic economy

McQueen Financial Advisors

Fall Leadership Development Conference Interest Rate Risk and Industry Trends Jim Craven McQueen Financial Advisors SEC Registered Investment Advisor $4 Billion + under management Municipal & Corporate

Fall Leadership Development Conference Interest Rate Risk and Industry Trends Jim Craven McQueen Financial Advisors SEC Registered Investment Advisor $4 Billion + under management Municipal & Corporate

Financial-Institutions Management. Solutions 6

Solutions 6 Chapter 25: Loan Sales 2. A bank has made a three-year $10 million loan that pays annual interest of 8 percent. The principal is due at the end of the third year. a. The bank is willing to

Solutions 6 Chapter 25: Loan Sales 2. A bank has made a three-year $10 million loan that pays annual interest of 8 percent. The principal is due at the end of the third year. a. The bank is willing to

CREDIT UNION TRENDS REPORT

CREDIT UNION TRENDS REPORT CUNA Mutual Group Economics June 2 (April 2 data) Highlights During April, credit unions picked up 3, new memberships, credit union loan balances grew at an annualized 1.7% pace,

CREDIT UNION TRENDS REPORT CUNA Mutual Group Economics June 2 (April 2 data) Highlights During April, credit unions picked up 3, new memberships, credit union loan balances grew at an annualized 1.7% pace,

HARD TIMES A Macroeconomic Analysis Presented To: The Financial Advisor Symposium

HARD TIMES A Macroeconomic Analysis Presented To: The Financial Advisor Symposium April 16, 2008 1250 S. Capital of Texas Highway Building 3, Suite 600 Austin, Texas 78746-6443 512-327-7200 Fax 512-327-8646

HARD TIMES A Macroeconomic Analysis Presented To: The Financial Advisor Symposium April 16, 2008 1250 S. Capital of Texas Highway Building 3, Suite 600 Austin, Texas 78746-6443 512-327-7200 Fax 512-327-8646

Banks Funding Costs and Lending Rates

Cameron Deans and Chris Stewart* Over the past year, lending rates and funding costs have both fallen in absolute terms but have risen relative to the cash rate. The rise in funding costs, relative to

Cameron Deans and Chris Stewart* Over the past year, lending rates and funding costs have both fallen in absolute terms but have risen relative to the cash rate. The rise in funding costs, relative to

5. Principles of Compilation of Monetary Statistics for Armenia

5. Principles of Compilation of Monetary Statistics for Armenia T he framework for the monetary statistics involves analytical presentation of balance sheets of financial sector s depository and nondepository

5. Principles of Compilation of Monetary Statistics for Armenia T he framework for the monetary statistics involves analytical presentation of balance sheets of financial sector s depository and nondepository

FY2008 First Quarter Consolidated Financial Results:

FY2008 First Quarter Consolidated Financial Results: For the Three Months Ended June 30, 2007 July 30, 2007 Company name Stock exchange listing Representative URL Contact person : Isuzu Motors Limited

FY2008 First Quarter Consolidated Financial Results: For the Three Months Ended June 30, 2007 July 30, 2007 Company name Stock exchange listing Representative URL Contact person : Isuzu Motors Limited

HSBC BANK CANADA FIRST QUARTER 2014 RESULTS

7 May 2014 HSBC BANK CANADA FIRST QUARTER 2014 RESULTS Profit before income tax expense for the quarter ended 2014 was C$233m, a decrease of 13.4% compared with the same period in and broadly unchanged

7 May 2014 HSBC BANK CANADA FIRST QUARTER 2014 RESULTS Profit before income tax expense for the quarter ended 2014 was C$233m, a decrease of 13.4% compared with the same period in and broadly unchanged

Financial Overview INCOME STATEMENT ANALYSIS

In the first half of 2006, China s economy experienced steady and swift growth as evidenced by a 10.9% surge in GDP. In order to prevent the economy from getting overheated and to curb excess credit extension,

In the first half of 2006, China s economy experienced steady and swift growth as evidenced by a 10.9% surge in GDP. In order to prevent the economy from getting overheated and to curb excess credit extension,

American International Group, Inc. Financial Supplement Fourth Quarter 2005

Financial Supplement Fourth Quarter 2005 This report should be read in conjunction with AIG's Annual Report on Form 10-K for the year ended December 31, 2005 filed with the Securities and Exchange Commission.

Financial Supplement Fourth Quarter 2005 This report should be read in conjunction with AIG's Annual Report on Form 10-K for the year ended December 31, 2005 filed with the Securities and Exchange Commission.

CHAPTER 5. STOCKS, FLOWS, AND ACCOUNTING RULES

CHAPTER 5. STOCKS, FLOWS, AND ACCOUNTING RULES Contents Page I. Introduction...2 II. Stocks Positions and Flows...2 A. Adding-up Identities...3 B. Flows...4 III. Accounting Rules...27 A. Time of Recording...27

CHAPTER 5. STOCKS, FLOWS, AND ACCOUNTING RULES Contents Page I. Introduction...2 II. Stocks Positions and Flows...2 A. Adding-up Identities...3 B. Flows...4 III. Accounting Rules...27 A. Time of Recording...27

FR Y-9C and FR Y-9LP Reports. Updated: 01/01/2014

FR Y-9C and FR Y-9LP Reports Updated: 01/01/2014 Agenda Introduction Report Processing Cycle Reporting Requirements Definitions Tiered Holding Company Overview and Schedules of the FR Y-9C Overview and

FR Y-9C and FR Y-9LP Reports Updated: 01/01/2014 Agenda Introduction Report Processing Cycle Reporting Requirements Definitions Tiered Holding Company Overview and Schedules of the FR Y-9C Overview and

FHLBanks: The Basics. For more information, visit www.fhlbanks.com.

FHLBanks: The Basics For more information, visit www.fhlbanks.com. The Federal Home Loan Banks (FHLBanks) are 11 private, wholesale banks regionally based throughout the U.S. They are cooperatively owned

FHLBanks: The Basics For more information, visit www.fhlbanks.com. The Federal Home Loan Banks (FHLBanks) are 11 private, wholesale banks regionally based throughout the U.S. They are cooperatively owned

1-3Q of FY2014 87.43 78.77 1-3Q of FY2013 74.47 51.74

January 30, 2015 Resona Holdings, Inc. Consolidated Financial Results for the Third Quarter of Fiscal Year 2014 (Nine months ended December 31, 2014/Unaudited) Code number: 8308 Stock

January 30, 2015 Resona Holdings, Inc. Consolidated Financial Results for the Third Quarter of Fiscal Year 2014 (Nine months ended December 31, 2014/Unaudited) Code number: 8308 Stock

4. The minimum amount of owners' equity in a bank mandated by regulators is called a requirement. A) reserve B) margin C) liquidity D) capital

reserve B) margin C) liquidity D) capital") Chapter 4 - Sample Questions 1. Quantitative easing is most closely akin to: A) discount lending. B) open-market operations. C) fractional-reserve banking. D) capital requirements. 2. Money market mutual

Chapter 4 - Sample Questions 1. Quantitative easing is most closely akin to: A) discount lending. B) open-market operations. C) fractional-reserve banking. D) capital requirements. 2. Money market mutual

READING 1. The Money Market. Timothy Q. Cook and Robert K. LaRoche

READING 1 The Money Market Timothy Q. Cook and Robert K. LaRoche The major purpose of financial markets is to transfer funds from lenders to borrowers. Financial market participants commonly distinguish

READING 1 The Money Market Timothy Q. Cook and Robert K. LaRoche The major purpose of financial markets is to transfer funds from lenders to borrowers. Financial market participants commonly distinguish

The Architecture of the System of National Accounts: A three-way international Comparison Canada, Australia and the United Kingdom

The Architecture of the System of National Accounts: A three-way international Comparison Canada, Australia and the United Kingdom Karen Wilson Director General System of National Accounts Branch Statistics

The Architecture of the System of National Accounts: A three-way international Comparison Canada, Australia and the United Kingdom Karen Wilson Director General System of National Accounts Branch Statistics

Lecture Notes on MONEY, BANKING, AND FINANCIAL MARKETS. Peter N. Ireland Department of Economics Boston College. irelandp@bc.edu

Lecture Notes on MONEY, BANKING, AND FINANCIAL MARKETS Peter N. Ireland Department of Economics Boston College irelandp@bc.edu http://www2.bc.edu/~irelandp/ec261.html Chapter 2: An Overview of the Financial

Lecture Notes on MONEY, BANKING, AND FINANCIAL MARKETS Peter N. Ireland Department of Economics Boston College irelandp@bc.edu http://www2.bc.edu/~irelandp/ec261.html Chapter 2: An Overview of the Financial

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-Q

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-Q È QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the quarterly period ended

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-Q È QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the quarterly period ended

Is U.S. Household Savings Rate Dangerously Low?

GLOBAL COMMENTARY July 22, 28 David Malpass 212-876-44 dmalpass@encimaglobal.com Is U.S. Household Savings Rate Dangerously Low? The front page of Sunday s New York Times highlighted the heavy household

GLOBAL COMMENTARY July 22, 28 David Malpass 212-876-44 dmalpass@encimaglobal.com Is U.S. Household Savings Rate Dangerously Low? The front page of Sunday s New York Times highlighted the heavy household

C. Reporting requirements for the consolidated banking statistics

C. Reporting requirements for the consolidated banking statistics C.1. General The consolidated banking statistics (CBS) capture the consolidated positions of banks worldwide offices, including the positions

C. Reporting requirements for the consolidated banking statistics C.1. General The consolidated banking statistics (CBS) capture the consolidated positions of banks worldwide offices, including the positions

Real Effects of Inflation through the Redistribution of Nominal Wealth: Technical Appendix

Real Effects of Inflation through the Redistribution of Nominal Wealth: Technical Appendix Matthias Doepke UCLA, FRB Minneapolis, and CEPR Martin Schneider NYU October 2004 Juan Pablo Medina provided excellent

Real Effects of Inflation through the Redistribution of Nominal Wealth: Technical Appendix Matthias Doepke UCLA, FRB Minneapolis, and CEPR Martin Schneider NYU October 2004 Juan Pablo Medina provided excellent

Comparison of micro and macro frameworks

OECD Framework for Statistics on the Distribution of Household Income, Consumption and Wealth OECD 2013 Comparison of micro and macro frameworks The main framework developed for analysis of income at the

OECD Framework for Statistics on the Distribution of Household Income, Consumption and Wealth OECD 2013 Comparison of micro and macro frameworks The main framework developed for analysis of income at the

CONTACTS: PRESS RELATIONS BETSY CASTENIR (212) 339-3424 INVESTOR RELATIONS ROBERT TUCKER (212) 339-0861 FSA HOLDINGS FIRST QUARTER 2004 RESULTS

339-3424 INVESTOR RELATIONS ROBERT TUCKER (212) 339-0861 FSA HOLDINGS FIRST QUARTER 2004 RESULTS") FOR IMMEDIATE RELEASE CONTACTS: PRESS RELATIONS BETSY CASTENIR (212) 339-3424 INVESTOR RELATIONS ROBERT TUCKER (212) 339-0861 FSA HOLDINGS FIRST QUARTER 2004 RESULTS NET INCOME $84 Million in Q1 04 (+28%

FOR IMMEDIATE RELEASE CONTACTS: PRESS RELATIONS BETSY CASTENIR (212) 339-3424 INVESTOR RELATIONS ROBERT TUCKER (212) 339-0861 FSA HOLDINGS FIRST QUARTER 2004 RESULTS NET INCOME $84 Million in Q1 04 (+28%

(April 1, 2015 June 30, 2015)

") Financial Results Summary of Consolidated Financial Results For the Three-month Period Ended June 30, 2015 (IFRS basis) (April 1, 2015 June 30, 2015) *This document is an English translation of materials

Financial Results Summary of Consolidated Financial Results For the Three-month Period Ended June 30, 2015 (IFRS basis) (April 1, 2015 June 30, 2015) *This document is an English translation of materials

Tables. Standard symbols:. Category not applicable.. Data not available... Data not yet available Nil 0 Less than half the 0.0 final digit shown

Tables 1. Norges Bank. Balance sheet. In millions of NOK 2. Norges Bank. Investments for Government Pension Fund - Global. In millions of NOK 3. Banks. Balance sheet. In millions of NOK 4. Banks. Loans

Tables 1. Norges Bank. Balance sheet. In millions of NOK 2. Norges Bank. Investments for Government Pension Fund - Global. In millions of NOK 3. Banks. Balance sheet. In millions of NOK 4. Banks. Loans

Development of consumer credit in China

Development of consumer credit in China Shen Bingxi and Yan Lijuan 1 Summary Consumer credit particularly personal consumer loans such as home mortgages and loans financing purchases of automobiles and

Development of consumer credit in China Shen Bingxi and Yan Lijuan 1 Summary Consumer credit particularly personal consumer loans such as home mortgages and loans financing purchases of automobiles and

Outstanding Loans Received From Abroad by Private Sector. Definitions and Explanations. Statistics Department Balance of Payments Division

Outstanding Loans Received From Abroad by Private Sector Definitions and Explanations Statistics Department Balance of Payments Division Contents I- Definitions... 3 II- Compilation Of The External Debt

Outstanding Loans Received From Abroad by Private Sector Definitions and Explanations Statistics Department Balance of Payments Division Contents I- Definitions... 3 II- Compilation Of The External Debt

Liquidity Constraints in the U.S. Housing Market

Liquidity Constraints in the U.S. Housing Market Denis Gorea Virgiliu Midrigan May 215 Contents A Income Process 2 B Moments 4 C Mortgage duration 5 D Cash-out refinancing 5 E Housing turnover 6 F House

Liquidity Constraints in the U.S. Housing Market Denis Gorea Virgiliu Midrigan May 215 Contents A Income Process 2 B Moments 4 C Mortgage duration 5 D Cash-out refinancing 5 E Housing turnover 6 F House

HMBS Overview. Ginnie Mae s Program to Securitize Government Insured Home Equity Conversion Mortgages

HMBS Overview Ginnie Mae s Program to Securitize Government Insured Home Equity Conversion Mortgages Table of Contents Tab A: Program Overview Tab B: Home Equity Conversion Mortgage (HECM) Trends Tab C:

HMBS Overview Ginnie Mae s Program to Securitize Government Insured Home Equity Conversion Mortgages Table of Contents Tab A: Program Overview Tab B: Home Equity Conversion Mortgage (HECM) Trends Tab C:

Monetary and Financial Trends First Quarter 2011. Table of Contents

Financial Stability Directorate Monetary and Financial Trends First Quarter 2011 Table of Contents Highlights... 1 1. Monetary Aggregates... 3 2. Credit Developments... 4 3. Interest Rates... 7 4. Domestic

Financial Stability Directorate Monetary and Financial Trends First Quarter 2011 Table of Contents Highlights... 1 1. Monetary Aggregates... 3 2. Credit Developments... 4 3. Interest Rates... 7 4. Domestic

2013 Estimate. Liz Marshall, Sabrina Pellerin, Federal Reserve Bank of Richmond Richmond, VA 23261. Published May 2015 Revised February 2016

2013 Estimate Liz Marshall, Sabrina Pellerin, and John Walter Federal Reserve Bank of Richmond Richmond, VA 23261 Published May 2015 Revised February 2016 This document can be downloaded without charge

2013 Estimate Liz Marshall, Sabrina Pellerin, and John Walter Federal Reserve Bank of Richmond Richmond, VA 23261 Published May 2015 Revised February 2016 This document can be downloaded without charge

Opening Doors For Muslim Families In America

Fe r d de i M a c We Open Doors Opening Doors For Muslim Families In America Saber Salam Vice President, Freddie Mac April 2002 Introduction The dream of homeownership is at the core of American society.

Fe r d de i M a c We Open Doors Opening Doors For Muslim Families In America Saber Salam Vice President, Freddie Mac April 2002 Introduction The dream of homeownership is at the core of American society.

CITIGROUP REPORTS FOURTH QUARTER 2011 NET INCOME OF $1.2 BILLION OR $0.38 PER SHARE 1, COMPARED TO $1.3 BILLION OR $0.43 IN FOURTH QUARTER 2010

On February 9, 2012, Citi announced an adjustment to its fourth quarter and full year 2011 financial results to reflect an additional $209 million of after-tax ($275 million pre-tax) charges to increase

On February 9, 2012, Citi announced an adjustment to its fourth quarter and full year 2011 financial results to reflect an additional $209 million of after-tax ($275 million pre-tax) charges to increase

Your Assets are Safeguarded. at Morgan Stanley

Your Assets are Safeguarded at Morgan Stanley Our valued wealth management clients have entrusted a total of more than $1.8 trillion in assets with Morgan Stanley as of September 30, 2013, making us one

Your Assets are Safeguarded at Morgan Stanley Our valued wealth management clients have entrusted a total of more than $1.8 trillion in assets with Morgan Stanley as of September 30, 2013, making us one

State Bank Financial Corporation Reports Fourth Quarter and Full Year 2015 Financial Results

Investor Relations Contact: Jeremy Lucas 404.239.8626 / jeremy.lucas@statebt.com Fourth Quarter 2015 Highlights State Bank Financial Corporation Reports Fourth Quarter and Full Year 2015 Financial Results

Investor Relations Contact: Jeremy Lucas 404.239.8626 / jeremy.lucas@statebt.com Fourth Quarter 2015 Highlights State Bank Financial Corporation Reports Fourth Quarter and Full Year 2015 Financial Results

- 168 - Chapter Seven. Specification of Financial Soundness Indicators for Other Sectors

- 168 - Chapter Seven Specification of Financial Soundness Indicators for Other Sectors Introduction 7.1 Drawing on the definitions and concepts set out in Part I of the Guide, this chapter explains how

- 168 - Chapter Seven Specification of Financial Soundness Indicators for Other Sectors Introduction 7.1 Drawing on the definitions and concepts set out in Part I of the Guide, this chapter explains how

Frankfurt am Main 27 April 2010. Deutsche Bank reports first quarter 2010 net income of EUR 1.8 billion

Release Frankfurt am Main 27 April 2010 Deutsche Bank reports first quarter 2010 net income of EUR 1.8 billion Net revenues of EUR 9.0 billion, up 24% Second best quarterly income before income taxes of

Release Frankfurt am Main 27 April 2010 Deutsche Bank reports first quarter 2010 net income of EUR 1.8 billion Net revenues of EUR 9.0 billion, up 24% Second best quarterly income before income taxes of

Bank Regulators Data Show Continued Increase in Adversely Classified Syndicated Bank Loans in 2001

Joint Release Board of Governors of the Federal Reserve System Federal Deposit Insurance Corporation Office of the Comptroller of the Currency For Immediate Release October 5, 2001 NR 2001-87 Bank Regulators

Joint Release Board of Governors of the Federal Reserve System Federal Deposit Insurance Corporation Office of the Comptroller of the Currency For Immediate Release October 5, 2001 NR 2001-87 Bank Regulators

Chapter 2. Practice Problems. MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

Chapter 2 Practice Problems MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) Assume that you borrow $2000 at 10% annual interest to finance a new

Chapter 2 Practice Problems MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) Assume that you borrow $2000 at 10% annual interest to finance a new

VIA ELECTRONIC TRANSMISSION. www.regulations.gov. June 12, 2013.

Nationwide. Mark R. Thresher. Executive Vice President. Chief Financial Officer. Nationwide Insurance. VIA ELECTRONIC TRANSMISSION. www.regulations.gov June 12, 2013. Robert dev. Frierson, Secretary. Board

Nationwide. Mark R. Thresher. Executive Vice President. Chief Financial Officer. Nationwide Insurance. VIA ELECTRONIC TRANSMISSION. www.regulations.gov June 12, 2013. Robert dev. Frierson, Secretary. Board

MORGAN STANLEY Financial Supplement - 4Q 2015 Table of Contents

Page # MORGAN STANLEY Financial Supplement - 4Q 2015 Table of Contents 1. Quarterly Consolidated Financial Summary 2. Quarterly Consolidated Income Statement Information 3. Quarterly Consolidated Financial

Page # MORGAN STANLEY Financial Supplement - 4Q 2015 Table of Contents 1. Quarterly Consolidated Financial Summary 2. Quarterly Consolidated Income Statement Information 3. Quarterly Consolidated Financial