Appendix B IMPLEMENTATION GUIDANCE

|

|

|

- Cecilia Hicks

- 10 years ago

- Views:

Transcription

1 Appendix B IMPLEMENTATION GUIDANCE CONTENTS Paragraph Numbers Introduction...B1 Fair Value Measurement Objective and Its Application... B2 B12 Fair Value of Instruments Granted under a Share-Based Payment Arrangement... B4 B6 Valuation Techniques... B7 B12 Valuation Techniques for Share Options... B9 B12 Selecting Assumptions for Use in an Option-Pricing Model... B13 B30 Consistent Use of Valuation Techniques and Methods for Selecting Assumptions... B17 B19 Expected Term of Employee Share Options... B20 B23 Expected Volatility... B24 B26 Expected Dividends... B27 B28 Other Considerations... B29 B30 Market, Performance, and Service Conditions... B31 B36 Market, Performance, and Service Conditions That Affect Vesting and Exercisability... B31 B33 Market, Performance, and Service Conditions That Affect Factors Other Than Vesting and Exercisability... B34 B36 Estimating the Requisite Service Period of Awards with Market, Performance, and Service Conditions... B37 B49 Explicit, Implicit, Derived, and Requisite Service Periods... B38 B41 Share-Based Payment Arrangement with a Performance Condition and Multiple Service Periods... B42 B44 Share-Based Payment Arrangement with a Service Condition and Multiple Service Periods... B45 B46 Share-Based Payment Arrangement with Market and Service Conditions and Multiple Service Periods... B47 B49 Illustrative Computations and Other Guidance... B50 B190 Illustration 1 Definition of Employee... B50 B51 Illustration 2 Service Inception Date and Grant Date... B52 B56 Illustration 3 Determining the Grant Date... B57 B58 Illustration 4 Accounting for Share Options with Service Conditions... B59 B75 Share Options with Cliff Vesting... B64 B69 Income Taxes...B67 Cash Flows from Income Taxes... B68 B69 Share Options with Graded Vesting... B70 B75 38

2 Paragraph Numbers Illustration 5 Share Option with Performance Condition... B76 B81 Illustration 5(a) Share Option Award under Which the Number of Options to Be Earned Varies... B76 B79 Illustration 5(b) Share Option Award under Which the Exercise Price Varies... B80 B81 Illustration 6 Other Performance Conditions... B82 B84 Illustration 7 Share Option with a Market Condition (Indexed Exercise Price)... B85 B91 Illustration 8 Stock Unit with Performance and Market Conditions... B92 B95 Illustration 9 Share Option with Exercise Price That Increases by a Fixed Amount or a Fixed Percentage... B96 B97 Illustration 10 Share-Based Payment Award Granted by a Nonpublic Entity That Is Not an SEC Registrant and Elects the Intrinsic Value Method... B98 B107 Illustration 10(a) Share Award... B99 B101 Income Taxes... B100 B101 Illustration 10(b) Share Option Award... B102 B107 Illustration 11 Share-Based Liability (Cash-Settled Share Appreciation Rights)... B108 B114 Income Taxes... B113 B114 Illustration 12 Modifications and Settlements... B115 B121 Illustration 12(a) Modification of Vested Share Options... B115 B116 Illustration 12(b) Share Settlement of Vested Share Options...B117 Illustration 12(c) Modification of Nonvested Share Options... B118 B120 Illustration 12(d) Cash Settlement of Nonvested Share Options...B121 Illustration 13 Modifications of Awards with Performance and Service Vesting Conditions... B122 B131 Illustration 13(a) Type I (Probable-to-Probable) Modification... B124 B125 Illustration 13(b) Type II (Probable-to-Improbable) Modification... B126 B127 Illustration 13(c) Type III (Improbable-to-Probable) Modification... B128 B129 Illustration 13(d) Type IV (Improbable-to-Improbable) Modification... B130 B131 Illustration 14 Modifications That Change an Award s Classification... B132 B153 Illustration 14(a) Equity-to-Liability Modification (Share-Settled Share Options to Cash-Settled Share Options)... B133 B141 Income Taxes... B139 B141 39

3 Paragraph Numbers Illustration 14(b) Equity-to-Equity Modification (Share Options to Shares)...B142 Illustration 14(c) Liability-to-Equity Modification (Cash-Settled to Share-Settled SARs)... B143 B148 Illustration 14(d) Liability-to-Liability Modification (Cash SARs to Cash SARs)... B149 B152 Illustration 14(e) Equity-to-Liability Modification (Share Options to Fixed Cash Payment)...B153 Illustration 15 Share Award with a Clawback Feature...B154 Illustration 16 Tandem Plan Share Options or Cash SARs... B155 B158 Illustration 17 Tandem Plan Phantom Shares or Share Options... B159 B167 Illustration 18 Look-Back Share Options... B168 B176 Illustration 19 Employee Share Purchase Plans... B177 B179 Illustration 20 Book Value Share Purchase Plans (Nonpublic Enterprises Only)... B180 B182 Illustration 21 Voluntary (or Involuntary) Change to Fair-Value-Based Method (Nonpublic Enterprises Only)...B183 Illustration 22 When Certain Instruments Become Subject to Statement B184 Illustration 23 Transition Using the Modified Prospective Method... B185 B190 Minimum Disclosure Requirements and Illustrative Disclosures... B191 B193 Supplemental Disclosures...B193 40

.")

4 Appendix B IMPLEMENTATION GUIDANCE INTRODUCTION B1. This appendix, which is an integral part of this Statement, 1 provides implementation guidance (a) that illustrates the fair-value-based method of accounting for share-based compensation arrangements with employees and (b) that elaborates on certain other aspects of this Statement. The illustrations are designed to provide guidance on, and emphasize considerations that should be taken into account in, applying this Statement. Using this guidance to apply this Statement in actual situations will require the exercise of judgment. FAIR VALUE MEASUREMENT OBJECTIVE AND ITS APPLICATION B2. The measurement objective for equity instruments granted to employees is to estimate the fair value of the equity instruments to which employees become entitled when they have rendered the requisite service and satisfied any other conditions necessary to earn the right to benefit from the instruments. That estimate is based on the share price (and other pertinent factors, including those enumerated in paragraph 19 of this Statement) at the grant date and is not remeasured in subsequent periods under the modified grant-date method. Restrictions (refer to Appendix E) that continue in effect after employees have earned the right to benefit from their equity instruments affect the value of the instruments issued at the vesting date and, therefore, are reflected in estimating the instruments fair value at the grant date. 2 The estimated fair value of an equity instrument on the date it is granted should not reflect the effects of vesting conditions or other restrictions that apply only during the vesting period. 3 Those effects are reflected by recognizing compensation cost only for awards that actually vest because the requisite service is provided. Reload features and contingent features that require an employee to transfer equity shares earned or realized gains from the sale of equity instruments earned as a result of share-based payment arrangements to the issuing enterprise for consideration that is less than fair value on the date of transfer (including 1 The phrase this Statement refers to Statement 123 as revised by Statement 15X (that is, this proposed Statement). 2 For example, if restricted shares (refer to Appendix E) are granted to an employee, the post-vesting restriction shall be reflected in estimating the grant-date fair value of the shares, but only to the extent that the post-vesting restriction would affect the amount at which the shares being valued would be exchanged (paragraph B4). For instance, if the shares are traded in an active market, post-vesting restrictions may have little, if any, effect on the amount at which the shares being valued would be exchanged. 3 Performance and service conditions (refer to Appendix E) are vesting conditions for purposes of this Statement. However, market conditions (refer to Appendix E) are not vesting conditions for purposes of this Statement; rather, market conditions may affect exercisability of an award. Consequently, market conditions are included in the estimate of the grant-date fair value of awards. 41

5 no consideration), such as a clawback feature, 4 shall not be considered in estimating the fair value of an equity instrument on the date it is granted. Those features are accounted for if and when a reload grant or contingent event occurs. B3. The fair value measurement objective for liabilities incurred under share-based payment arrangements with employees is the same as for equity instruments. However, awards classified as liabilities are subsequently remeasured to their fair values (or a pro rata portion thereof until the requisite service has been rendered) at the end of each reporting period until the liability is settled. Fair Value of Instruments Granted under a Share-Based Payment Arrangement B4. Fair value is defined in FASB Concepts Statement No. 7, Using Cash Flow Information and Present Value in Accounting Measurements, as follows: The amount at which that asset (or liability) could be bought (or incurred) or sold (or settled) in a current transaction between willing parties, that is, other than in a forced or liquidation sale. [Glossary of Terms of Concepts Statement 7] That definition refers explicitly only to assets and liabilities, but the concept of value in a current exchange embodied in it applies equally to the equity instruments subject to this Statement. Observable market prices of identical or similar equity or liability instruments in active markets are the best evidence of fair value and, if available, are to be used as the basis for the measurement of equity and liability instruments awarded as part of share-based payment arrangements with employees. For example, awards to employees of a public entity of shares of its common stock, subject only to a service or performance condition for vesting, that are awards of nonvested shares, are to be measured based on the market price of otherwise identical (that is, identical except for the vesting condition) common stock traded in the marketplace. B5. If observable market prices of identical or similar equity or liability instruments of the entity are not available, the fair value of equity and liability instruments awarded to employees shall be estimated by using a valuation technique that (a) is applied in a manner consistent with the fair value measurement objective and the other requirements of this Statement, (b) is based on established principles of financial economic theory and generally accepted by experts in that field (paragraph B9), and (c) reflects any and all substantive characteristics of the instrument (except for those characteristics explicitly excluded, such as vesting conditions and reload features). That is, the fair value estimate for equity and liability instruments granted as part of a share-based payment arrangement shall be determined by applying a valuation technique that would be used in valuing instruments with the same characteristics (except for those explicitly excluded by this 4 A clawback feature can take various forms but often functions as a noncompete mechanism: for example, an employee that terminates the employment relationship and begins to work for a competitor is required to transfer to the issuing enterprise (former employer) shares granted and earned under a share-based payment arrangement. 42

at the end of each reporting")

6 Statement) to form the basis for an amount at which the instruments being valued would be exchanged (paragraph B6). B6. In estimating the fair value of employee share options at the grant date, the determination of the amount at which the instruments being valued would be exchanged would factor in expectations of the probability that the options would vest (that is, that the service or performance vesting conditions would be satisfied). However, as noted in paragraph B2, the measurement objective in this Statement is to estimate the fair value at the grant date of the equity instruments to which employees will become entitled when the service or performance conditions for vesting have been satisfied (that is, when the requisite service has been rendered). Therefore, the estimated fair value of the equity instruments at grant date does not take into account the effect on fair value of vesting conditions and other restrictions prior to vesting (as well as other items explicitly excluded). The effect of the vesting conditions and other restrictions prior to vesting are considered by the modified grant-date method by recognizing compensation cost only for instruments that vest (in other words, instruments for which the requisite service is rendered). Valuation Techniques B7. In applying a valuation technique, inputs and assumptions should be those that would be used or made in accordance with paragraph B5. That is, the estimates and assumptions should reflect information that is (or would be) available to form the basis for an amount at which the instruments being valued would be exchanged. In estimating fair value, the assumptions made should not represent the biases of a particular party. Some of those assumptions will be based on or determined directly from external data. Other assumptions will be derived from the entity s own historical experience with sharebased payment arrangements. 5 B8. The fair value of any equity or liability instrument depends on the specific characteristics of that instrument. Paragraph 19 of this Statement enumerates a list of substantive characteristics of equity instruments with option (or option-like) features that shall be considered in estimating their fair value. However, a share-based payment arrangement could contain other features that should be included in a fair value estimate (such as a market condition). Judgment will be required to determine both what features should be included and, as described in paragraphs B9 B12, how to incorporate those features in the valuation technique used. Valuation Techniques for Share Options B9. Several valuation techniques, including a lattice model (an example of which is a binomial model) and a closed-form model (an example of which is the Black-Scholes- 5 This guidance is not intended to preclude use of an entity s own data about employee option exercises in developing the fair value estimate. Forming the basis for an amount at which instruments being valued would be exchanged would require data about expected option exercises, and such data generally could be obtained only from the entity. 43

7 Merton formula) meet the criteria required by this Statement for estimating the fair values of employee share options and similar instruments. Those valuation techniques or models, sometimes referred to as option-pricing models, are based on well-established financial economic theory. Those models are used by valuation professionals, dealers of derivative instruments, and other experts to estimate the fair values of options and similar instruments related to equity securities, currencies, interest rates, and commodities. Those models are used to establish trade prices for derivative instruments, to establish fair market values for U.S. tax purposes, and to establish values in adjudications. Both a lattice model and a closed-form model can be adjusted to account for the characteristics of share options and similar instruments granted to employees. B10. This Statement requires the use of a valuation technique or model that meets the requirements in paragraph B5 to estimate the fair values of employee share options and similar instruments. The selection of a valuation model will depend on the substantive characteristics of each arrangement and the availability of data necessary to use the model. A valuation model that is more fully able to capture and better reflects those characteristics is preferable and should be used if it is practicable to do so. For example, the Black-Scholes-Merton formula, a closed-form model, assumes that option exercises occur at the end of an option s contractual term, and that volatility, dividends, and riskfree interest rates are constant over the option s term. If used to estimate the fair value of employee share options and similar instruments, the Black-Scholes-Merton formula must be adjusted to take account of certain characteristics of employee share options and similar instruments that are not consistent with the assumptions of the model (for example, exercise prior to the end of the option s contractual term and changing volatility and dividends). Because of the nature of the formula, those adjustments take the form of weighted-average assumptions about those characteristics. In contrast, a lattice model can be designed to incorporate certain characteristics of employee share options and similar instruments; it can accommodate changes in dividends and volatility over the option s contractual term, estimates of expected option exercise patterns during the option s contractual term, and blackout periods. 6 A lattice model, therefore, is more fully able to capture and better reflects the characteristics of a particular employee share option or similar instrument in the estimate of fair value. 7 B11. Although a lattice model may be preferable because of its ability to more fully capture and better reflect the characteristics of a particular employee share option or similar instrument in the estimate of fair value, it may not be practicable to use such a 6 A blackout period is a period of time during which an employee is contractually or legally prohibited from exercising a share option granted under a share-based payment arrangement. 7 Valuation techniques used for employee share options and similar instruments estimate the fair value of those instruments at a single point in time (for example, at the grant date) that is independent of all other points in time. The estimated fair value of those instruments will change over time as factors used in estimating their fair value change, for instance, as share prices fluctuate, risk-free interest rates change, or dividend streams are modified. That change in the estimated fair value of those instruments is a normal economic process to which any valuable resource is subject. The estimated fair value of those instruments at a single point in time is neither a prediction nor a forecast of what the estimated fair value of those instruments may be in the future or was in the past. 44

8 model. For example, an enterprise may lack the historical data on employee exercise patterns that could be used within a lattice model in estimating expected option exercises over the option s contractual term. For instance, a nonpublic enterprise that elects to account for employee share options using the fair-value-based method or a newly public company may not have a significant history of share option exercise; consequently, such entities may conclude that it is not practicable to use a lattice model and that a closedform model would provide a reasonable estimate of fair value. Entities that do not have reasonable access to the data required by a lattice model may conclude that a closed-form model provides a reasonable estimate of fair value; those entities subsequently may obtain reasonable access to the data and decide to use a lattice model. Further, entities for which compensation cost is not a significant element of the financial statements may conclude that a closed-form model produces estimates of fair value that are not materially different from those produced by a lattice model and that this pattern can reasonably be assumed to persist. Those entities may conclude that a closed-form model provides reasonable estimates of fair value. 8 B12. Public entities for which compensation cost from share option arrangements is a significant element of the financial statements may conclude, when inputs are available, that a lattice model would provide a better estimate of fair value because of its ability to more fully capture and better reflect the characteristics of a particular employee share option or similar instrument in the estimate of fair value. SELECTING ASSUMPTIONS FOR USE IN AN OPTION-PRICING MODEL B13. If an observable market price is not available for an option with the same or similar terms and conditions, this Statement requires an entity to estimate the fair value of an employee share option or similar instrument using a valuation model that meets the requirements in paragraph B5 and takes into account, at a minimum: a. The exercise price of the option b. The expected term 9 of the option, taking into account both the contractual term of the option and the effects of employees expected exercise and post-vesting employment termination behavior (refer to paragraph B20 for an explanation of the expected term in the context of a lattice model) c. The current price of the underlying share d. The expected volatility of the price of the underlying share 8 Even if an entity concludes that a closed-form model provides a reasonable estimate of fair value, that entity should perform a rigorous analysis of the employee share option or similar instrument s expected term in estimating that input for use in the model. 9 The fair value of a transferable share option is based on its contractual term because rarely is it economically advantageous to exercise, rather than sell, a transferable share option before the end of its contractual term. Employee share options generally differ from transferable (or traded) share options in that employees cannot sell their share options they can only exercise them. To reflect the effect of employees inability to sell their vested options, this Statement requires that the fair value of an employee share option be based on its expected term rather than its contractual term. 45

9 e. The expected dividends on the underlying share (except as provided in paragraphs 32 and 33 of this Statement) f. The risk-free interest rate(s) for the expected term of the option. 10 A U.S. entity issuing an option on its own shares must use as the risk-free interest rates the implied yields from the U.S. Treasury zero-coupon yield curve over the expected term of the option if the entity is using a lattice model incorporating the option s contractual term. If the entity is using a closed-form model, the risk-free interest rate is the implied yield currently available on U.S. Treasury zero-coupon issues with a remaining term equal to the expected term used as the input to the model. For entities based in jurisdictions outside the United States, the risk-free interest rate is the implied yield currently available on zero-coupon government issues denominated in the currency of the market in which the share (or underlying share), which is the basis for the instrument awarded, primarily trades. It may be necessary to use an appropriate substitute if no such government issues exist or circumstances indicate that the implied yield on zero-coupon government issues is not representative of the risk-free interest rate (for example, in high-inflation economies). Guidance on selecting the other assumptions listed above is provided in the following paragraphs. B14. There is likely to be a range of reasonable estimates for expected volatility, dividends, and option term. If no amount within the range is more or less likely than any other amount, an average of the range (its expected value) should be used. In using a lattice model, the expected values used are to be determined for a particular node (or multiple nodes during a particular time period) of the lattice and not over multiple periods, unless such application is supportable given the characteristics of the instrument being valued. 11 B15. Expectations about the future generally are based on past experience, modified to reflect ways in which currently available information indicates that the future is reasonably expected to differ from the past. In many circumstances, the available information may indicate that unadjusted historical experience is a relatively poor predictor of future experience. For example, an entity with two distinctly different lines of business of approximately equal size may dispose of the one that was significantly less volatile and generated more cash than the other. In that situation, volatility, dividends, and perhaps employees exercise and post-vesting termination behavior from the predisposition (or disposition) period may not be the best information on which to base reasonable expectations for the future. B16. In other circumstances, historical information may not be available. For example, an entity whose common stock has only recently become publicly traded may have little, 10 The term expected in items (b), (d), (e), and (f) relates to assumptions about the respective factor that is used as an input in a valuation model. 11 The term supportable is used in its general sense: capable of being maintained, confirmed, or made good; defensible (The Compact Oxford English Dictionary, 2 nd edition, 1998). Application is supportable if it is based on reasonable arguments, given a rigorous analysis that takes into account the relevant facts and circumstances. 46

10 if any, historical data on the volatility of its own shares. That entity might base expectations about future volatility on the average volatilities of similar entities for an appropriate period following their going public. A nonpublic entity that elects to use the fair-value-based method of accounting will need to exercise judgment in selecting a method to estimate expected volatility and might do so by basing its volatility expectations on the average volatilities of otherwise similar public entities. 12 Consistent Use of Valuation Techniques and Methods for Selecting Assumptions B17. Data and assumptions used to estimate the fair value of equity and liability instruments granted to employees should be determined in a consistent manner from period to period. For example, for grants made before the market closes, an entity might use either the closing share price or the average of that day s share price as the current share price on the grant date, but whichever method is selected, it should be used consistently. The valuation technique an entity selects to estimate fair value also should be used consistently and should not be changed unless a different valuation technique is expected to produce a better estimate of fair value. B18. For employee share options and similar instruments, a lattice model is preferable to a closed-form model and, therefore, is preferable for justifying a change in accounting principle. Once an entity changes its valuation technique for employee share options and similar instruments to a lattice model, it may not change to a less preferable valuation technique. 13 A change in valuation technique is a change in accounting estimate or a change in accounting estimate inseparable from a change in accounting principle, depending on the facts and circumstances, for purposes of applying APB Opinion No. 20, Accounting Changes. For example, if an entity changes its valuation technique from a closed-form model to a lattice model because it has accumulated data to support an estimate of expected option exercise over the contractual term of the option, that change is a change in accounting estimate because that change is based on new information that provides better insight and improved judgment. B19. Not all of the general guidance on selecting assumptions provided in paragraphs B2 B18 is repeated in the following discussion of factors to be considered in selecting specific assumptions. However, the general guidance is intended to apply to each individual assumption. An entity should not estimate share option fair values based on historical average share option lives, historical share price volatility, or historical dividends (whether stated as a yield or a dollar amount) without considering the extent to which future experience is reasonably expected to differ from historical experience. 12 This paragraph is in no way intended to suggest that historical volatility is the only indicator of expected volatility. Expected volatility is an expectation of volatility over the expected term of an employee share option or similar instrument; paragraphs B24 and B25 provide further guidance on estimating expected volatility. 13 However, if subsequent to that change an entity grants a different type of share-based payment award (for instance, a share option with a three-month contractual term that is exercisable only at the end of its term) it may decide that a closed-form model provides a reasonable estimate of fair value, given the characteristics of the instrument being valued. 47

11 Expected Term of Employee Share Options B20. Expected term is an input to a closed-form model. However, if an entity uses a lattice model that has been modified to take into account an option s contractual term and employees expected exercise and post-vesting employment termination behavior, the expected term is estimated based on the resulting output of the lattice. 14 For example, an entity s experience might indicate that option holders tend to exercise those options when the share price reaches 200 percent of the exercise price. If so, that entity might use a lattice model that assumes exercise of the option at each node along each share price path in a lattice at which the early exercise expectation is met, provided that the option is vested and exercisable at that point. Moreover, such a model would assume exercise at the end of the contractual term on price paths along which the exercise expectation is not met but the options are in-the-money 15 at the end of the contractual term. That method recognizes that employees exercise behavior is correlated with the price of the underlying share. Employees expected post-vesting employment termination behavior also would be factored in. Expected term then could be estimated based on the output of the resulting lattice. 16 B21. Other factors that may affect expectations about employees exercise and postvesting employment termination behavior include the following: a. The vesting period of the award. An option s expected term must at least include the vesting period. b. Employees past exercise and post-vesting employment termination behavior for similar grants. c. Expected volatility of the price of the underlying share. d. Blackout periods and other coexisting arrangements such as agreements that allow for exercise to automatically occur during blackout periods if certain conditions are satisfied. B22. If sufficient information about employees expected exercise and post-vesting employment termination behavior is available, a method like the one described in paragraph B20 would produce a better estimate of the fair value of an employee share option because that method reflects more information about the instrument being valued (paragraph B10). However, if sufficient information about exercise and post-vesting employment termination behavior is not available, expected term would be estimated in 14 In some share option arrangements, an option holder may exercise an option prior to vesting (usually to obtain a favorable tax treatment); however, such arrangements generally require that any shares received upon exercise be returned to the entity (with or without a return of the exercise price to the holder) if the vesting conditions are not ultimately satisfied. Such an exercise is not substantive for accounting purposes. 15 The terms at-the-money, in-the-money, and out-of-the-money are used to describe share options whose exercise price is equal to, less than, or greater than the market price of the underlying share, respectively. 16 An example of an acceptable method, for purposes of financial statement disclosures, of estimating the expected term based on the results of a lattice model is to use the lattice model s estimated fair value of a share option as an input to a closed-form model, and then to solve the closed-form model for the expected term. 48

12 some other manner. That estimate would take into account whatever relevant and supportable information is available, including industry averages and other pertinent evidence, such as published academic research. B23. Option value is not a linear function of option term; value increases at a decreasing rate as the term lengthens. For example, a two-year option is worth less than twice as much as a one-year option, other things being equal. Accordingly, estimating the fair value of an option based on a single expected term that effectively averages the widely differing exercise and post-vesting employment termination behaviors of identifiable groups of employees will potentially misstate the value of the entire award. Aggregating individual awards into relatively homogenous groups with respect to exercise and postvesting employment termination behaviors, and estimating the fair value of the options granted to each group separately reduces such potential misstatement; that aggregation of individual awards should be performed regardless of whether the lattice or closed-form model is used to estimate the fair value. For example, the experience of an employer that grants options broadly to all levels of employees might indicate that hourly employees tend to exercise for a smaller percentage gain than do more highly compensated employees. In addition, employees who are encouraged or required to hold a minimum amount of their employer s equity instruments, including options, might exercise options, on average, at higher share prices (or later) than employees not subject to that provision. Expected Volatility B24. Volatility is a measure of the amount by which a financial variable such as a price has fluctuated (historical volatility) or is expected to fluctuate (expected volatility) during a period. The concept of volatility is defined more fully in Appendix E. This Statement does not specify a particular method of estimating expected volatility; rather, paragraph B25 provides a list of factors that might be considered in estimating expected volatility. An entity s estimate of expected volatility should be reasonable and supportable. B25. Factors to consider in estimating expected volatility include: a. The term structure of the volatility of the share price over the most recent period that is generally commensurate with (1) the contractual term of the option if a lattice model is being used to estimate fair value or (2) the expected term of the option if a closed-form model is being used. b. The implied volatility of the share price determined from the market prices of traded options. Additionally, the term structure of the implied volatility of the share price over the most recent period that is generally commensurate with (1) the contractual term of the option if a lattice model is being used to estimate fair value or (2) the expected term of the option if a closed-form model is being used. c. For public companies, the length of time an entity s shares have been publicly traded. If that period is shorter than the expected term of the option, the term structure of volatility for the longest period for which trading activity is available should be more relevant. A newly public entity also might consider the volatility of 49

13 similar entities. 17 A nonpublic entity that elects the fair-value-based method might base its expected volatility on the volatilities of entities that are similar except for having publicly traded securities. d. The mean-reverting 18 tendency of volatilities. For example, in computing historical volatility, an entity might disregard an identifiable period of time in which its share price was extraordinarily volatile because of a failed takeover bid or a major restructuring. Statistical models have been developed that take into account the mean-reverting tendency of volatilities. e. Appropriate and regular intervals for price observations. If an entity considers historical volatility or implied volatility in estimating expected volatility, it should use the intervals that are appropriate based on the facts and circumstances and provide the basis for a reasonable fair value estimate. For example, a publicly traded entity might use daily price observations, while a nonpublic entity with shares that occasionally change hands at negotiated prices might use monthly price observations. f. Corporate structure. An entity s corporate structure may affect expected volatility. For instance, an entity with two distinctly different lines of business of approximately equal size may dispose of the one that was significantly less volatile and generated more cash than the other. In that situation, an entity would consider the effect of that disposition in its estimate of expected volatility. An entity that uses historical share price volatility as its estimate of expected volatility without considering the extent to which future experience is reasonably expected to differ from historical experience (and the other factors cited in this paragraph) would not comply with the requirements of this Statement. B26. Lattice models can incorporate a term structure of volatilities; that is, a range of expected volatilities can be incorporated into the lattice over an option s contractual term. That capability is one of the advantages of a lattice model as explained in paragraph B10. Determining how a range of expected volatilities can be incorporated into a lattice model to provide a reasonable fair value estimate is a matter of judgment and should be based on a careful consideration of the factors identified in paragraph B25. Expected Dividends B27. Option-pricing models generally call for expected dividend yield as an input. However, the models may be modified to use an expected dividend amount rather than a yield. An entity may use either its expected yield or its expected payments. If the latter is chosen, the entity s historical pattern of increases in dividends should be considered. For example, if an entity s policy generally has been to increase dividends by approximately 3 percent per year, its estimated share option value should not be based on a fixed dividend amount throughout the share option s expected term. 17 In evaluating similarity, an entity would likely consider factors such as industry, stage of life cycle, and financial leverage. 18 Mean reversion refers to the tendency of a financial variable, such as volatility, to revert to some long-run average level. 50

14 B28. Generally, the assumption about expected dividends should be based on publicly available information (paragraph B7). As with other inputs to an option-pricing model, an entity should use the expected dividends that would likely be reflected in an amount at which the option would be exchanged (paragraph B5). Other Considerations B29. An entity may need to consider the effect of its credit risk on the estimated fair value of awards that contain cash settlement features (liability instruments) because cash payoffs from the awards are not independent of the entity s risk of default. Any creditrisk adjustment to the estimated fair value of awards with cash payoffs that increase with increases in the price of the underlying share is expected to be de minimis because increases in an entity s share price generally are positively associated with its ability to liquidate its liabilities. However, a credit-risk adjustment to the estimated fair value of awards with cash payoffs that increase with decreases in the price of the entity s shares may be necessary because decreases in an entity s share price generally are negatively associated with an entity s ability to liquidate its liabilities. B30. Contingent features that might cause a loss to the employee of equity shares earned or realized gains from the sale of equity instruments earned as a result of share-based payment arrangements, such as a clawback feature (paragraph B2, footnote 4), are not accounted for in the estimated fair value of an equity instrument on the date it is granted. Those features are accounted for if and when the loss to the employee occurs. For instance, a share-based payment may stipulate that vested equity shares must be returned for no consideration to the issuing entity if the employee terminates the employment relationship to work for a competitor. The effect of that provision on the grant-date fair value of the equity shares shall not be considered. If the issuing entity receives those shares (or their equivalent value in cash or other assets), an entity shall account for that event by recognizing a credit in the income statement upon receipt of the shares. 19 Illustration 15 (paragraph B154) provides an example of the accounting for an award that contains a clawback feature. 19 The event is recognized in the income statement because the resulting transaction takes place with an employee (or former employee) as a result of the current (or prior) employment relationship rather than as a result of the employee s role as an equity owner. 51

because cash payoffs from the awards")

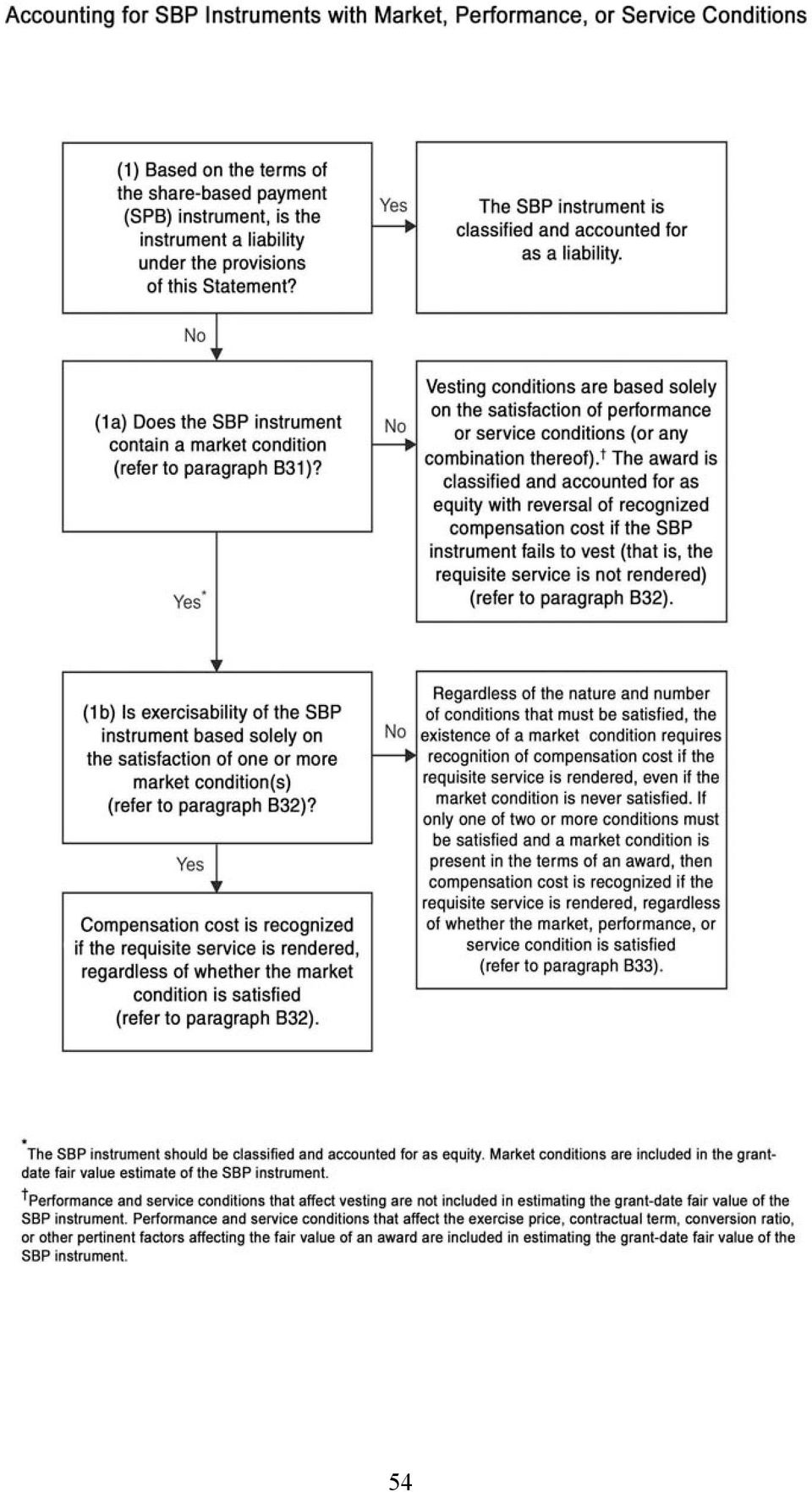

15 MARKET, PERFORMANCE, AND SERVICE CONDITIONS Market, Performance, and Service Conditions That Affect Vesting and Exercisability B31. An employee s share-based payment award becomes vested at the date that the employee s right to receive or retain shares, other equity instruments, or cash under the award is no longer contingent on satisfaction of either a service condition or a performance condition. This Statement distinguishes among market conditions, performance conditions, and service conditions that are included in the terms of an award as conditions for that award to vest or to become exercisable (paragraph 25E). Other conditions that do not meet the definitions of market conditions, performance conditions, or service conditions are discussed in paragraph B35 (paragraph 26F). B32. Analysis of the market, performance, or service conditions (or any combination thereof) that are explicitly stated or implicit in the terms of an award is required to determine (a) the requisite service period over which compensation cost is recognized and (b) whether recognized compensation cost may be reversed if an award fails to vest (or become exercisable) (paragraphs 26D and 26E). If exercisability (or the ability to retain the award 20 ) is based solely on one or more market conditions, then compensation cost for that award is recognized if the employee renders the requisite service, even if the market condition is not satisfied. 21 If vesting is based solely on one or more performance or service conditions, then compensation cost is not recognized (and any previously recognized cost is reversed) if the award does not vest (that is, the requisite service is not rendered). Illustrations 4 and 5 (paragraphs B59 B81) are examples of awards in which vesting is based solely on performance or service conditions. B33. Vesting (or exercisability) may be conditional on satisfying two or more types of conditions (for example, vesting and exercisability occur upon satisfying both a market and a performance condition) or may be conditional on satisfying one of two or more types of conditions (for example, vesting and exercisability occur upon satisfying either a market condition or a performance condition). Regardless of the nature and number of conditions that must be satisfied, the existence of a market condition requires recognition of compensation cost if the requisite service is rendered, even if the market condition is never satisfied. If only one of two or more conditions must be satisfied and a market condition is present in the terms of an award, then compensation cost is recognized if the requisite service is rendered, regardless of whether the market, performance, or service condition is satisfied. Paragraphs B47 B49 illustrate this principle. 20 For example, an award of equity shares may contain a market condition that affects the employee s ability to retain those shares. 21 Awards containing market conditions may have an explicit, implicit, or derived service period. An explicit service period is explicitly stated as part of the terms of the share-based payment arrangement. An implicit service period is inferred from an analysis of other terms of the arrangement, including other explicit service or performance conditions. A derived service period is derived from certain valuation techniques used to estimate grant-date fair value, as described in paragraphs B47 and B48. Paragraphs B38 B41 provide guidance on explicit, implicit, and derived service periods. 52

16 Market, Performance, and Service Conditions That Affect Factors Other Than Vesting and Exercisability B34. Market, performance, and service conditions may affect an award s exercise price, contractual term, quantity, conversion ratio, or other pertinent factors that are relevant in measuring an award s fair value. For instance, an award s quantity may double, or an award s contractual term may be extended, if a company-wide revenue target is achieved. Market conditions that affect an award s fair value (including exercisability) are included in the estimate of grant-date fair value (paragraph 26F). Performance or service conditions that affect vesting are excluded from the estimate of grant-date fair value, but performance or service conditions that affect an award s fair value (excluding those that affect vesting) are included in the estimate of grant-date fair value (paragraph 26F). Illustrations 5 (paragraphs B76 B81), 6 (paragraphs B82 B84), and 8 (paragraphs B92 B95) provide further guidance on how performance conditions (excluding those that affect vesting) that affect an award s fair value are included in the estimate of grant-date fair value. B35. An award may include conditions that are not market, performance, or service conditions. For example, a share award that will vest based on the appreciation in the price of a basic commodity such as gold is indexed to both the value of that commodity and the issuing entity s shares. If factors that affect the fair value or vesting conditions of a share-based payment instrument are dependent on conditions other than market, performance, or service conditions, that instrument is classified as a liability for purposes of this Statement (paragraph 26F). 22 Any such conditions are included in the fair value estimate of the award. B36. The following flowchart provides guidance on determining how to account for an award based on the existence of market, performance, or service conditions (or any combination thereof). 22 This conclusion would not change even if the entity granting the share-based payment instrument is a producer of the commodity whose price changes are part or all of the conditions that affect an award s fair value or vesting conditions. 53

are included in the estimate of grant-date fair value (paragraph 26F).")

17 54

18 ESTIMATING THE REQUISITE SERVICE PERIOD OF AWARDS WITH MARKET, PERFORMANCE, AND SERVICE CONDITIONS B37. Paragraph 25E of this Statement requires that compensation cost be recognized over the requisite employee service period. The requisite service period for an award that has only a service condition is presumed to be the vesting period, unless there is clear evidence to the contrary. If a market, performance, or service condition requires future service for vesting (or exercisability), an entity cannot define a prior period as the requisite service period. Estimating the requisite service period requires an analysis of all relevant facts and circumstances, including other employment agreements and an enterprise s past practices; moreover, that estimate should ignore nonsubstantive vesting conditions. The requisite service period for awards with market, performance, or service conditions (or any combination thereof) should be consistent with assumptions used in estimating the grant-date fair value of those awards. Explicit, Implicit, Derived, and Requisite Service Periods B38. A requisite service period may be explicit, implicit, or derived. An explicit service period is one that is explicitly stated in the terms of the share-based payment arrangement. For example, an arrangement that states that the award vests after three years of continuous employee service from a given date (usually the grant date) has an explicit service period of three years, which also is the requisite service period. An implicit service period is one that is not explicit in the terms of the share-based payment arrangement but may be inferred from an analysis of those terms and other explicit performance or service conditions. For instance, if a share option vests upon the completion of a new product design and the design is expected to be completed in 18 months, the implicit service period is 18 months, which also would be the estimated requisite service period. Derived service periods are relevant only for awards with market conditions that affect exercisability (or exercise price) or the ability to retain the award. Derived service periods are implied by, or can be derived from, certain valuation techniques used to estimate fair value. For example, the derived service period for a share award that can be retained by the employee only if the share price increases by 25 percent at any time during a 5-year period can be derived from the valuation technique used to estimate fair value. That derived service period represents the duration of the most frequent path of a path-dependent option-pricing model on which the market condition is satisfied. If the derived service period was assumed to be three years, the estimated requisite service period is three years and all compensation cost would be recognized over that period, unless the market condition was satisfied at an earlier date. 23 If the market condition is satisfied prior to the end of the requisite service period, any unrecognized compensation cost is recognized immediately upon satisfaction. The 23 Compensation cost would not be recognized beyond three years even if after the grant date it was probable that the market condition would not be satisfied within that period. Compensation cost equal to the fair value of the award at grant date would be recognized (not reversed) even if the market condition was not satisfied any time during the five-year period, provided that the employee renders services during the requisite service period, which is defined by the derived service period. 55

, an entity cannot define a prior period as the requisite service period.")

19 requisite service period is not adjusted if the market condition is not satisfied by the end of that period. B39. Awards with performance and service conditions may have multiple explicit and implicit service periods. For example, a share option might specify that vesting occurs at the earlier of three years of continuous employee service or when the employee completes a specified project. The employer estimates that the project will be completed within the next 18 months. That award contains an explicit service period of 3 years related to the service condition, and an implicit service period of 18 months related to the performance condition. If it is probable 24 that the performance condition will be achieved, the requisite service period over which compensation cost is recognized is 18 months, the implicit service period related to the performance condition, because it is shorter than 3 years. B40. The initial estimate of the requisite service period based on explicit or implicit service periods shall be adjusted for the actual outcomes of the related service or performance conditions that affect vesting of the award. Such adjustments will occur because the entity revises its estimates of the probability of satisfying different conditions or combinations of conditions. For example, if an award vests upon the earlier of the satisfaction of a four-year service condition or the satisfaction of multiple performance conditions, then the entity will initially determine which outcomes are probable of achievement. If initially the four-year service condition is probable of achievement and the performance conditions are not, the requisite service period is four years. If the performance conditions become probable of achievement one year into the four-year requisite service period and the entity estimates that the performance conditions will be achieved by the end of the second year, the requisite service period is revised to two years. B41. Awards with combinations of market, performance, and service conditions may contain multiple explicit, implicit, and derived service periods. For such awards, the estimate of the requisite service period shall be based on an analysis of all vesting and exercisability conditions; all explicit, implicit, and derived service periods; and the probability that performance or service conditions will be satisfied. If vesting (or exercisability) is based on satisfying both (a) market and (b) performance or service conditions, and it is probable that the performance or service condition(s) will be satisfied, the initial estimate of the requisite service period generally is the longest of the explicit, implicit, and derived service periods. If vesting (or exercisability) is based on satisfying either (a) market or (b) performance or service conditions, and it is probable that the performance or service condition(s) will be satisfied, the initial estimate of the requisite service period generally is the shortest of the explicit, implicit, and derived service periods. 24 Probable is used in the same sense as in FASB Statement No. 5, Accounting for Contingencies: the future event or events are likely to occur (paragraph 3). 56

20 Share-Based Payment Arrangement with a Performance Condition and Multiple Service Periods B42. On December 31, 20X4, Enterprise T enters into an arrangement with its chief executive officer (CEO) relating to 40,000 share options on its stock with an exercise price of $30 per option. The arrangement is structured such that 10,000 share options will vest or be forfeited in each of the next 4 years (20X5 to 20X8) depending on whether annual performance targets for each year related to Enterprise T s revenues and net income are achieved. All of the annual performance targets are set at the inception of the arrangement. Each tranche of 10,000 share options is accounted for as a separate award with its own service inception date, grant-date fair value, and one-year requisite service period, because the arrangement specifies an independent performance condition for a stated period of service. The requisite service required to be provided in exchange for the first award (pertaining to 20X5) is independent of the requisite service required to be provided in exchange for each consecutive award; the failure to satisfy one year s performance condition has no effect on the outcome of any preceding or subsequent period. This arrangement is similar to an arrangement that would have provided a $10,000 cash bonus for each year for satisfaction of the same performance conditions. The service inception date for each tranche is the beginning of each year. B43. If the arrangement had instead provided that the compensation committee would establish the annual performance target during January of each year, the grant date for each award would be the date in January of each year when the annual performance targets are established by the compensation committee. The fair value measurement of compensation cost for each tranche would be affected because not all of the key terms and conditions of each award are known until the compensation committee sets the performance targets and, therefore, the grant dates are those dates. B44. If in addition to the annual performance targets being satisfied for a period, each successive award in the arrangement described in paragraph B42 (for example, the second award pertaining to 20X6) also required that the annual performance targets related to the preceding award (for example, the first award pertaining to 20X5) be satisfied in order for the successive award to vest, the requisite service provided in exchange for each preceding award is not independent of the requisite service provided in exchange for each successive award. In contrast to the arrangement described in paragraph B42, failure to achieve the annual performance targets in 20X5 results in forfeiture of all awards. In that circumstance, all awards have the same service inception date and the same grant date (January 1, 20X5); however, each award has its own explicit service period (for example, the 20X5 grant has a one-year service period, the 20X6 grant has a two-year service period, and so on). Share-Based Payment Arrangement with a Service Condition and Multiple Service Periods B45. The CEO of Enterprise T enters into a five-year employment contract on January 1, 20X5. The contract stipulates that the CEO will be issued 10,000 fully vested share options at the end of each year (50,000 share options in total). The exercise price of each tranche will be equal to the market price at the date of issuance (December 31 of each 57

21 year in the five-year contractual term). Grant date cannot occur until the end of each year when the at-the-money share options are issued, the exercise price is known, and the CEO begins to benefit from, or be adversely affected by, subsequent changes in the price of the employer s equity shares (paragraphs B57 and B58). The contract structure including the quantity of share options to be granted each year (level quantity), the fact that options are fully vested when they are issued, and the determination of the exercise price at the end of each period indicate that the requisite service provided in exchange for the first award (pertaining to 20X5) is independent of the requisite service provided in exchange for each consecutive award. In other words, the terms of the share-based compensation arrangement provide evidence that each tranche is structured to compensate the CEO for one year of service. Consequently, each tranche is treated as a separate award with its own service inception date, grant date, and one-year service period. B46. However, if the contract was changed such that the exercise price is set at the current market price at January 1, 20X5, for all 50,000 share options, then (a) all tranches have the same service inception date and grant date (January 1, 20X5) and (b) each tranche is a separate award with its own explicit service period (for example, the 20X5 grant has a one-year service period, the 20X6 grant has a two-year service period, and so on). Share-Based Payment Arrangement with Market and Service Conditions and Multiple Service Periods B47. On January 1, 20X5, Enterprise T grants to 5 executives 200,000 share options on its stock with an exercise price of $30 per option. The award specifies that vesting (or exercisability) will occur upon the earlier of (a) the share price reaching and maintaining at least $70 per share for 30 consecutive trading days and (b) the completion of 8 years of service. That award contains an explicit service period of eight years related to the service condition and a derived service period related to the market condition. B48. An enterprise shall make its best estimate of the derived service period related to a market condition. If an enterprise uses a lattice model, it will estimate the derived service period based on the model s results (the derived service period is not an input of that model). A market condition may be satisfied on some paths of the lattice and not be satisfied on other paths of the lattice. On the paths of the lattice on which the market condition is satisfied, that satisfaction will occur at different times during the contractual term of the award. For purposes of this Statement, the derived service period is equal to the mode of the distribution of outcomes in which the market condition is satisfied (that is, the duration of the most frequent path on which the market condition is satisfied). For this example, the mode is assumed to be six years. As described in paragraph B41, if an award s vesting (or exercisability) is conditional upon the achievement of either (a) a market condition or (b) performance or service conditions, the requisite service period is generally the shortest of the explicit, implicit, and derived service periods. In this 58

22 example, the requisite service period over which compensation cost should be attributed is six years (shorter of eight and six years). 25 B49. Continuing with the example in paragraph B47, assume the market condition is actually satisfied in February 20X9 (based on market prices for the prior 30 days). In that case, Enterprise T shall immediately recognize any unrecognized compensation cost, as no further service is required to earn the award. If the market condition is not satisfied but the executives render the six years of requisite service, compensation cost shall not be reversed under any circumstances. ILLUSTRATIVE COMPUTATIONS AND OTHER GUIDANCE Illustration 1 Definition of Employee B50. This Statement defines an employee as an individual over whom the grantor of a share-based compensation award exercises or has the right to exercise sufficient control to establish an employer-employee relationship based on common law as illustrated in case law and currently under U.S. Internal Revenue Service Revenue Ruling (refer to Appendix E for a complete definition of employee). An example of whether that condition exists follows. Company A issues options to members of its Advisory Board, which is separate and distinct from Company A s board of directors. Members of the Advisory Board have specific knowledge and expertise within Company A s industry and are granted stock options as compensation for advising Company A on such matters as policy development, strategic planning, and product development. The Advisory Board members are appointed for two-year terms and meet four times a year for one day. Members receive a fixed number of options for each meeting. Based on an evaluation of the relationship between Company A and the Advisory Board members, Company A concludes that the Advisory Board members do not meet the common law definition of an employee. Accordingly, the awards to the Advisory Board members are accounted for as awards to nonemployees under the provisions of this Statement. B51. Additionally, paragraph 8 (footnote 5a) of this Statement requires that nonemployee directors acting in their role as members of an entity s board of directors be treated as employees if those directors were (a) elected by the entity s shareholders or (b) appointed to a board position that will be filled by shareholder election when the existing term expires. However, that requirement applies only to awards granted to them for their services as directors. Awards granted to those individuals for nondirector services should be accounted for as nonemployee compensation in accordance with paragraphs 8 10 of this Statement. Additionally, consolidated groups may contain multiple boards of 25 However, an entity may grant a fully vested deep-out-of-the-money share option, which is the equivalent of an award with both a market condition and a service condition. The explicit service period associated with the explicit service condition is zero. The derived service period associated with the market condition of the share option is assumed to be six years. The initial estimate of the requisite service period for an award with both market and nonmarket conditions is generally the longest of the explicit, implicit, and derived service periods. Therefore, compensation cost associated with the share options should be recognized over the six-year derived service period. 59

23 directors; this guidance applies only (a) to the nonemployee directors acting in their role as members of a parent entity s board of directors and (b) to nonemployee members of a consolidated subsidiary s board of directors to the extent that those members are elected by shareholders that are not controlled directly or indirectly by the parent or another member of the consolidated group. Illustration 2 Service Inception Date and Grant Date B52. This Statement distinguishes the service inception date from the grant date (refer to paragraph 25E and Appendix E of this Statement). The service inception date is the first day of the requisite service period over which compensation cost shall be attributed. Grant date is the date when the employer and employee have a mutual understanding of the key terms and conditions of the share-based compensation arrangement and all necessary authorizations (other than perfunctory authorizations) of those terms and conditions have occurred (Appendix E). B53. Substantive employee service received in exchange for a share-based payment arrangement may be provided prior to grant date; hence, the service inception date can precede the grant date of a share-based payment arrangement either because (a) the necessary authorizations have been obtained but the key terms and conditions are not mutually understood or (b) there is a mutual understanding of the key terms and conditions but the necessary authorizations have not been obtained. B54. Enterprise T offers a high-level position to an individual on April 1, 20X5; Enterprise T s CEO and board of directors have approved the offer. In addition to salary and other benefits, Enterprise T offers to grant 10,000 shares of Enterprise T stock that vest upon the completion of 5 years of service (the market price of Enterprise T s stock is $25 on April 1, 20X5). The share award will begin vesting on the date the offer is accepted. The individual accepts the offer on April 2, 20X5; however, she is unable to begin providing her services to Enterprise T until June 2, 20X5 (that is, substantive employment begins on June 2, 20X5). The individual also does not receive a salary or participate in other employee benefits until June 2, 20X5. On June 2, 20X5, the market price of Enterprise T stock is $40 (as there has been some speculation that Enterprise T has become an acquisition target). In this example, the service inception date is June 2, 20X5, the first date that the individual begins providing substantive employee services to Enterprise T. The grant date is the same date because that is when the individual would meet the definition of an employee. The grant-date fair value of the share award is $400,000 (10,000 $40). B55. If the service inception date has occurred but grant date has not yet occurred, either because there is not a mutual understanding of the key terms and conditions of the award or because other-than-perfunctory approvals have not been obtained, an enterprise shall accrue compensation cost using the share price and other pertinent factors in effect at each subsequent reporting date to estimate the award s fair value until the grant date occurs, at which time the estimate of the award s fair value would be fixed. 60

24 B56. Therefore, if the offer described in paragraph B54 had not been approved by the board of directors at the service inception date of June 2, 20X5 (and that approval was not considered perfunctory) and the approval was obtained on August 5, 20X5, then the grant date would be August 5, 20X5. The service inception date would continue to be June 2, 20X5, and that date would precede the grant date (August 5, 20X5), the date when all necessary authorizations are obtained. If the market price of Enterprise T s stock is $38 per share on August 5, 20X5, the grant-date fair value of the share award is $380,000 (10,000 $38). The recognized compensation cost for the period between June 2, 20X5, and August 5, 20X5, would have been based on the fair value of the share at each balance sheet date using the then-current share price and other pertinent factors with a cumulative adjustment for the effect of changes in share price until the grant date occurs. Illustration 3 Determining the Grant Date B57. The definition of grant date requires that an employer and an employee have a mutual understanding of the key terms and conditions of the share-based compensation arrangement (paragraph 17 and Appendix E). Those terms may be (a) included in a formal, written agreement or an informal, oral arrangement or (b) established by an enterprise s past practice. A mutual understanding of the key terms and conditions means that there is sufficient basis for both the employer and the employee to understand the nature of the relationship established by the award, including both the compensatory relationship and the equity relationship subsequent to the date of grant. The grant date for an award will be the date that an employee begins to benefit from, or be adversely affected by, subsequent changes in the price of the employer s equity shares. In order to assess that financial exposure, the employer and employee must agree to the key terms and conditions; that is, there must be a mutual understanding. Additionally, to have a grant date for an award to an employee, the recipient of that award must meet the definition of employee in Appendix E. B58. The determination of the grant date shall be based on the relevant facts and circumstances. For instance, a look-back share option may be granted with an exercise price equal to the lower of the current share price or the share price one year hence. The ultimate exercise price is not known at the date of grant, but it cannot be greater than the current share price. In this case, the relationship between the exercise price and the current share price provides a sufficient basis to understand both the compensatory and equity relationship established by the award; the recipient begins to benefit from, or be adversely affected by, subsequent changes in the price of the employer s equity shares. However, if a share option s exercise price is to be set equal to the share price one year hence, the recipient does not begin to benefit from, or be adversely affected by, subsequent changes in the price of the employer s equity shares. 26 Therefore, grant date would not occur until one year hence. (However, the service inception date would occur 26 Awards of share options whose exercise price is determined solely by reference to a future share price would not provide a sufficient basis to understand the nature of the compensatory and equity relationships established by the award until the exercise price is known. 61

25 at the date the share option is given and the entity would account for the arrangement as noted in paragraph B55.) Illustration 4 Accounting for Share Options with Service Conditions B59. Enterprise T, a public entity, grants employee share options with a maximum term of 10 years. The exercise price of each share option equals the market price of its shares on the grant date. All share options vest at the end of three years (cliff vesting), which is an explicit service (and requisite service) period of three years. The share options do not qualify for tax purposes as incentive stock options. The corporate tax rate is 35 percent. B60. The following table shows assumptions and information about share options granted on January 1, 20X5. Share options granted 900,000 Employees granted options 3,000 Expected forfeitures per year 3.0% Share price at the grant date $30 Exercise price $30 Contractual term (CT) of options 10 years Risk-free interest rate over CT 1.5 to 4.3% Expected volatility over CT 40 to 60% Expected dividend yield 1.0% Suboptimal exercise factor 27 2 B61. Using as inputs the last 7 items from the table above, Enterprise T s lattice-based valuation model produces a fair value estimate of $14.69 per option. Enterprise T uses a lattice model because that model more fully captures and better reflects the characteristics of the instruments being valued and it is practicable to use that model. B62. Total compensation cost recognized over the vesting period (requisite service period) should be the fair value determined at the grant date of all share options that actually vest. Paragraph 26 of this Statement requires an enterprise to estimate at the grant date the number of share options for which the requisite service is expected to be rendered (which, in this illustration, is the number of share options probable 28 of vesting). If that estimate changes, it shall be accounted for as a change in estimate and its 27 A suboptimal exercise factor of two means that exercise is expected to occur when the share price reaches two times the share option s exercise price. Option-pricing theory generally holds that the optimal (or profit-maximizing) time to exercise an option is at the end of the option s term; therefore, if an option is exercised prior to the end of its term, that exercise is referred to as suboptimal. Suboptimal exercise also is referred to as early exercise. Suboptimal or early exercise affects the expected term of an option. Early exercise can be incorporated into option-pricing models through various means. In this illustration, Enterprise T has sufficient information to reasonably estimate early exercise and has incorporated it as a function of Enterprise T s future stock price changes (or the option s intrinsic value). In this case, the factor of 2 indicates that early exercise would be expected to occur, on average, if the stock price reaches $60 per share ($30 2). 28 Refer to footnote

26 cumulative effects (from applying the change retrospectively) recognized in the period of change. Enterprise T estimates at the grant date the number of share options that will vest and subsequently adjusts compensation cost for changes in the assumed rate of forfeitures and differences between expectations and actual experience. This illustration assumes that none of the compensation cost is capitalized as part of the cost to produce inventory or other assets. B63. The estimate of the expected number of forfeitures considers historical employee turnover rates and expectations about the future. Enterprise T has experienced historical turnover rates of approximately 3 percent per year for employees at the grantees level having nonvested share options, and it expects that rate to continue. Therefore, Enterprise T estimates the total value of the award at the grant date based on an expected forfeiture rate of 3 percent per year. Actual forfeitures are 5 percent in 20X5, but no adjustments to cost are recognized in 20X5 because Enterprise T still expects actual forfeitures to average 3 percent per year over the 3-year vesting period. At December 31, 20X6, however, management decides that the rate of forfeitures is likely to continue to increase through 20X7, and the assumed forfeiture rate for the entire award is changed to 6 percent per year. Adjustments to cumulative cost to reflect the higher forfeiture rate are made at the end of 20X6. At the end of 20X7 when the award becomes vested, actual forfeitures have averaged 6 percent per year, and no further adjustment is necessary. Share Options with Cliff Vesting B64. The first set of calculations illustrates the accounting for the award of share options on January 1, 20X5, assuming that the share options granted vest at the end of three years. (Paragraphs B70 B75 illustrate the accounting for an award assuming graded vesting in which a specified portion of the share options granted vest at the end of each year.) The number of share options expected to vest is estimated at the grant date to be 821,406 (900, ). Thus, as shown in Table 1, the estimated fair value of the award at January 1, 20X5, is $12,066,454 (821,406 $14.69), and the compensation cost to be recognized during each year of the 3-year vesting period is $4,022,151 ($12,066,454 3). The journal entries to recognize compensation cost and related deferred tax benefit at Enterprise T s effective tax rate of 35 percent are as follows for 20X5: Compensation cost $4,022,151 Additional paid-in capital $4,022,151 To recognize compensation cost. Deferred tax asset $1,407,753 Deferred tax benefit $1,407,753 To recognize the deferred tax asset for the temporary difference related to compensation cost ($4,022, = $1,407,753). The net after-tax effect on income of recognizing compensation cost for 20X5 is $2,614,398 ($4,022,151 $1,407,753). 63

27 B65. Absent a change in estimate, the same journal entries would be made to recognize compensation cost and related tax effects for 20X6 and 20X7, resulting in a net after-tax cost for each year of $2,614,398. However, at the end of 20X6, management changes its estimated employee forfeiture rate from 3 percent to 6 percent per year. The revised number of share options expected to vest is 747,526 (900, ). Accordingly, the revised cumulative compensation cost to be recognized by the end of 20X7 is $10,981,157 (747,526 $14.69). The cumulative adjustment to reflect the effect of adjusting the forfeiture rate is the difference between two-thirds of the revised cost of the award and the cost already recognized for 20X5 and 20X6. The related journal entries and the computations follow. At December 31, 20X6, to adjust for new forfeiture rate: Revised total compensation cost $10,981,157 Revised cumulative cost as of 12/31/X6 ($10,981,157 ⅔) $ 7,320,771 Cost already recognized in 20X5 and 20X6 ($4,022,151 2) 8,044,302 Adjustment to cost at 12/31/X6 $ (723,531) The related journal entries are: Additional paid-in capital $723,531 Compensation cost $723,531 To adjust previously recognized compensation cost and equity to reflect a higher estimated forfeiture rate. Deferred tax expense $253,236 Deferred tax asset $253,236 To adjust the deferred tax accounts to reflect the tax effect of increasing the estimated forfeiture rate ($723, = $253,236). For 20X7: Compensation cost $3,660,386 Additional paid-in capital $3,660,386 To recognize compensation cost ($10,981,157 3 = $3,660,386). Deferred tax asset $1,281,135 Deferred tax benefit $1,281,135 To recognize the deferred tax asset for additional compensation cost ($3,660, = $1,281,135). At December 31, 20X7, the entity would examine its actual forfeitures and make any necessary adjustments to reflect compensation cost for the number of shares that actually vested. 64