ECONOMIC OUTLOOK. Skøyen 15 September 2015 Rolf Albriktsen Kristoffer Eide Hoen

|

|

|

- Martina Blair

- 7 years ago

- Views:

Transcription

1 ECONOMIC OUTLOOK Skøyen 15 September 2015 Rolf Albriktsen Kristoffer Eide Hoen

2 Norway: Slower growth ahead Moderate forecasts for building construction, high activity in civil engineering Increasing regional differences Sweden: High levels of activity in the markets Growth driven by residential buildings Denmark: Upturn in the economy The construction sector remains weak 2

3 THE ECONOMY Photo: Creative Commons/whiz-ka

4 GLOBAL ECONOMY GDP GROWTH GDP growth (%) Euro zone Germany United Kingdom USA China Stock market turbulence and signs of weaker growth in China However, growth forecasts remain positive Commodity prices will remain low for some time Zero growth in the European construction and civil engineering sector in the last four quarters Wide differences between countries Global Source: IMF (9 July 2015)

5 INTERNATIONAL ECONOMIES GDP GROWTH Stock market turbulence and signs of weaker growth in China However, growth forecasts remain positive Commodity prices will remain low for some time Zero growth in the European construction sector in the last four quarters Wide differences between countries 5 Source: Eurostat

6 Construction market Q Q Level of production in Q Level as % of 2010 figures EU 94 Germany 107 UK 103 France 88 Italy 68 Spain 91 Poland 103 Finland 106 Sweden 116 Denmark 112 Norway 124 Source: Eurostat

7 MODERATE GROWTH IN THE NORWEGIAN ECONOMY GROWTH FORECASTS FOR NORWAY Dashed line = Veidekke's projection from March A period of more moderate economic growth The GDP for mainland Norway is predicted to rise by roughly 1 1.5% in 2015 and 2016 Continuing low interest rates, with further cuts expected Increased investment from the public sector: Municipal finances Tax relief Infrastructure Regional differences in development Dependency on the oil industry is an important explanatory factor 7

8 MODERATE GROWTH IN THE NORWEGIAN ECONOMY GROWTH FORECASTS FOR NORWAY A period of more moderate economic growth The GDP for mainland Norway is predicted to rise by roughly 1 1.5% in 2015 and 2016 Continuing low interest rates, with further cuts expected Increased investment from the public sector Municipal finances Tax relief Infrastructure Regional differences in development Dependency on the oil industry is an important explanatory factor 8

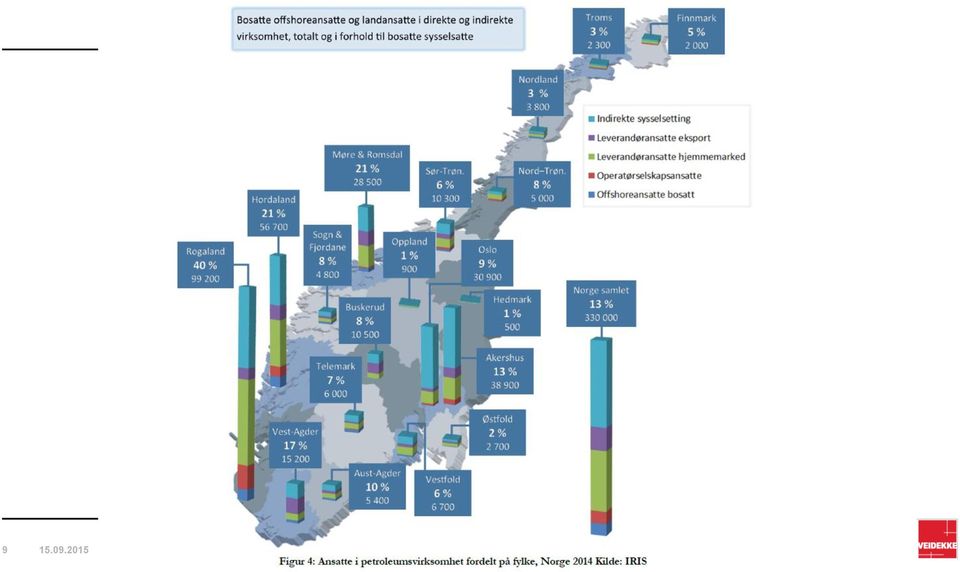

9

10 HEADING FOR AN UPTURN GROWTH FORECASTS FOR SWEDEN GDP growth is high, as expected: Growth rate of 2.5 3% this year and next year Record-low interest rates Positive development for households Improvements in the employment market Good growth in incomes and consumption Households' confidence in the economy will nevertheless remain moderate Dashed line = Veidekke's projection from March 10

11 GROWTH FROM A LOW LEVEL GROWTH FORECASTS FOR DENMARK The economic outlook is brighter than for many years GDP growth of 2% in 2015, may rise to 2.5% in House prices picking up in metropolitan areas May counteract imbalances in the wake of the financial crisis Housing wealth vs. level of debt in households Increased activity vs. overcapacity Dashed line = Veidekke's projection from March 11

12 NORWEGIAN CONSTRUCTION MARKET: MODERATE FORECASTS, REGIONAL DIFFERENCES Veidekke's new HQ in Skøyen

13 INCREASING PRODUCTION PRODUCTION INDEX FOR CONSTRUCTION The production index rose by 1% in Q2 1.5% more than in the same quarter in 2014 Civil engineering: Production picked up sharply this year Up 5.2% from Q1 to Q2 Building construction: Stable activity for residential and non-residential buildings Growth largely due to public non-residential buildings Private non-residential buildings declining slightly 13

14 NEW RESIDENTIAL AND CIVIL ENGINEERING PROJECTS CONTINUED GOOD INFLOW OF NEW ORDERS 14

15 THE RESIDENTIAL MARKET: HOUSE PRICES ROSE MORE THAN EXPECTED HOUSE PRICES The residential market is still dominated by rising prices and stable sales Low interest rates and good access to credit People moving to metropolitan areas In August the price of existing apartments was around 4% higher than in January 2015 The forecast of 5% growth in 2015 and 3% in 2016 remains unchanged The decline in the Norwegian economy and prospects of rising unemployment will affect price growth Dashed line = Veidekke's projection from March 15

16 WEAKER MARKET IN ROGALAND DECLINING DEMAND FOR RESIDENTIAL BUILDINGS AND PRIVATE NON-RESIDENTIAL BUILDINGS IN ROGALAND 16

stable The situation in oil-dependent areas is pulling the residential market down Homes taking longer to sell Source: Finn / Norwegian Real Estate Association (EFF)")

17 THE RESIDENTIAL MARKET: INCREASING REGIONAL DIFFERENCES HOUSE PRICES AND TRENDS Continued good growth in prices in the Oslo and Bergen metropolitan areas Days on the Market (DOM) stable The situation in oil-dependent areas is pulling the residential market down Homes taking longer to sell Source: Finn / Norwegian Real Estate Association (EFF) 17

18 THE RESIDENTIAL MARKET: HOUSING STARTS REGISTERED RESIDENTIAL BUILDING PERMITS Dashed line = Veidekke's projection from March Strong growth in the number of housing starts in the first half of the year Good housing sales through the winter this year Work has started on projects that were put on ice in We expect a flatter development through the autumn and winter Around 30,000 housing starts in 2015 Expected to decline to around 27,000 in 2016 Areas dependent on the oil industry will see a sharp decline 18

19 REGIONAL DIFFERENCES IN HOUSING STARTS 19

20 SLOWER GROWTH WITHIN NON-RESIDENTIAL BUILDINGS REGISTERED NON-RESIDENTIAL BUILDING PERMITS Start-up of non-residential buildings has been declining A growing number of new public building projects will stabilise start-up figures Construction projects for oil-related industries will fall Other private construction projects will stabilise Drivers for the start-up of non-residential buildings Private: Employment, interest rates and income trends Public: State and municipal finances, interest rates and centralisation Dashed line = Veidekke's projection from March 20

21 CIVIL ENGINEERING INVESTMENTS IN CIVIL ENGINEERING (VOLUME 2011 PRICES) Mrd. NOK %* +4%* +7%* +2%* +10%* 5% growth in the civil engineering market this year and next year Transport continues to lead the growth in civil engineering The growth within municipal infrastructure will probably continue going forwards Development and upgrading of power plants continues to grow at 10 12% p.a. Roads Railway Other public Power Other private Source: Statistics Norway and Veidekke * Annual growth rate (Note "Other public" has passed "Power") 21

A number of major transport infrastructure projects will come up for tender in 2015 2016 Relevant projects (worth more than NOK 500 million) total more than NOK 50 billion in Norway Fv714")

22 EXAMPLES OF MAJOR PROJECTS E10 Evenes Sortland (NOK 3,000 mill.) E6 Helgeland Sør (NOK 3,000 mill.) A number of major transport infrastructure projects will come up for tender in Relevant projects (worth more than NOK 500 million) total more than NOK 50 billion in Norway Fv714 Laksevegen (NOK 600 mill.) Fv659 Nordøyvegen (NOK 600 mill.) Rv555 Sotra (NOK 5,000 mill.) Rv4 Roa-Gran (NOK 1,000 mill.) E134 Kongsberg (NOK 2,000 mill.) E39 Rogfast (NOK 8,000 mill.) E18 Rugtvedt Dørdal (NOK 2,500 mill.) PPP Løten (NOK 3,000 mill.) Oslo Central Station (NOK 1,000 mill.) E18 Tvedestrand Arendal (NOK 5,000 mill.) 22

23 CONSTRUCTION MARKETS IN NORWAY SUMMARY INVESTMENTS IN CONSTRUCTION (VOLUME 2011 PRICES) Continued high levels of activity in the construction and civil engineering market in 2015 and 2016 Growth of around 2% in the total market Residential investments to rise by approx. 2% p.a. Private non-residential buildings falling, -2% p.a. 3% annual growth for public non-residential buildings Continued growth from a high level of activity within civil engineering Source: Statistics Norway and Veidekke * Annual growth rate

24 Brf Hovås Park, Gothenburg SWEDISH CONSTRUCTION MARKET HIGH LEVELS OF ACTIVITY

25 CONSTRUCTION COMPANIES' CONFIDENCE INDICATOR 25

26 HEALTHY RESIDENTIAL MARKET HOUSING STARTS Healthy market development so far in 2015 The start-up rate has passed 40,000 units Price growth has picked up in the cities Positive underlying driving forces Improvements in the labour market Low interest rates greater purchasing power Growth projections for residential investments revised upwards to 15% Unchanged at 3% in 2016 Dashed line = Veidekke's projection from March 26

27 HEALTHY RESIDENTIAL MARKET HOUSE PRICES AND FORECASTS Healthy market development so far in 2015 The start-up rate has passed 40,000 units Price growth has picked up in the cities Positive underlying driving forces Improvements in the labour market Low interest rates greater purchasing power Growth projections for residential investments revised upwards to 15% Unchanged at 3% in 2016 Dashed line = Veidekke's projection from March 27

28 HEALTHY RESIDENTIAL MARKET POPULATION. ANNUAL GROWTH (%) Healthy market development so far in 2015 The start-up rate has passed 40,000 units Price growth has picked up in the cities Positive underlying driving forces Improvements in the labour market Low interest rates greater purchasing power Growth projections for residential investments revised upwards to 15% Unchanged at 3% in 2016 Dashed line = Veidekke's projection from March 28

29 HEALTHY RESIDENTIAL MARKET THE COST OF BUYING A HOME Healthy market development so far in 2015 The start-up rate has passed 40,000 units Price growth has picked up in the cities Positive underlying driving forces Improvements in the labour market Low interest rates greater purchasing power Growth projections for residential investments revised upwards to 15% Unchanged at 3% in * Swedbank's housing affordability index ("Boindex"), which measures the purchasing power of households after housing expenditures. Index: 100 = good purchasing power, a higher score = greater purchasing power.

30 HEALTHY RESIDENTIAL MARKET THE COST OF BUYING A HOME Healthy market development so far in 2015 The start-up rate has passed 40,000 units Price growth has picked up in the cities Positive underlying driving forces Improvements in the labour market Low interest rates greater purchasing power Growth projections for residential investments revised upwards to 15% in 2015 Unchanged at 3% in * Swedbank's housing affordability index ("Boindex"), which measures the purchasing power of households after housing expenditures. Index: 100 = good purchasing power, a higher score = greater purchasing power.

31 PROGRESS FOR PRIVATE NON-RESIDENTIAL BUILDINGS Pyramiden SEB's new offices in Stockholm Moderately positive market development in 2015 Investment figures show +4% in H1 2015, compared with H Industrial investment estimates for 2015 show solid growth However this trend is not reflected in the number of projects started The underlying driving forces indicate good prospects in 2016 Unemployment fell by more than 1.5% in Q2 Retail sales averaging 4% year-on-year The general economic situation entails increased demand for capacity The positive forecasts for the period remain unchanged 5% growth in 2015, rising to 7% in

32 PROGRESS FOR PRIVATE NON-RESIDENTIAL BUILDINGS INVESTMENTS IN CONSTRUCTION AND CIVIL ENGINEERING FOR A SAMPLE OF INDUSTRIES Estimate from May the same year Diff. % Industrial 6.1 bill. 5.9 bill. -3% Shops 2.0 bill. 3.8 bill. +80% Industrial and storage Commercial property development companies 9.6 bill bill. +7% 30.3 bill bill. +29% Source: Statistics Sweden Moderately positive market development in 2015 Investment figures show +4% in H1 2015, compared with H Industrial investment estimates for 2015 show solid growth However this trend is not reflected in the number of projects started The underlying driving forces indicate good prospects in 2016 Unemployment fell by more than 1.5% in Q2 Retail sales averaging 4% year-on-year The general economic situation entails increased demand for capacity The positive forecasts for the period remain unchanged 5% growth in 2015, rising to 7% in

33 PROGRESS FOR PRIVATE NON-RESIDENTIAL BUILDINGS BUILDING PERMITS FOR PRIVATE NON-RESIDENTIAL BUILDINGS Moderately positive market development in 2015 Investment figures show +4% in H1 2015, compared with H Industrial investment estimates for 2015 show solid growth However this trend is not reflected in the number of projects started The underlying driving forces indicate good prospects in 2016 Unemployment fell by more than 1.5% in Q2 Retail sales averaging 4% year-on-year The general economic situation entails increased demand for capacity The positive forecasts for the period remain unchanged 5% growth in 2015, rising to 7% in 2016 Dashed line = Veidekke's projection from March 33

34 PROGRESS FOR PRIVATE NON-RESIDENTIAL BUILDINGS LABOUR MARKET Moderately positive market development in 2015 Investment figures show +4% in H1 2015, compared with H Industrial investment estimates for 2015 show solid growth However this trend is not reflected in the number of projects started The underlying driving forces indicate good prospects in 2016 Unemployment fell by more than 1.5% in Q2 Retail sales averaging 4% year-on-year The general economic situation entails increased demand for capacity The positive forecasts for the period remain unchanged 5% growth in 2015, rising to 7% in 2016 Dashed line = Veidekke's projection from March 34

35 PROGRESS FOR PRIVATE NON-RESIDENTIAL BUILDINGS LABOUR MARKET Moderately positive market development in 2015 Investment figures show +4% in H1 2015, compared with H Industrial investment estimates for 2015 show solid growth However this trend is not reflected in the number of projects started The underlying driving forces indicate good prospects in 2016 Unemployment fell by more than 1.5% in Q2 Retail sales averaging 4% year-on- year The general economic situation entails increased demand for capacity The positive forecasts for the period remain unchanged 5% growth in 2015, rising to 7% in 2016 Dashed line = Veidekke's projection from March 35

36 PUBLIC NON-RESIDENTIAL BUILDINGS MORE MODERATE BUILDING PERMITS PUBLIC NON-RESIDENTIAL BUILDINGS The predicted decline seems to be under way Decrease in building permits in H Investments in H % Weak starting point for the rest of 2015 and 2016 An extended period of growth is now behind us Cutbacks in several parts of the public sector The forecasts have been revised downwards for 2015 to 0% investment growth The forecast of decline of 5% in 2016 remains unchanged. 36 Dashed line = Veidekke's projection from March Source: Statistics Sweden

37 THE CIVIL ENGINEERING MARKET INVESTMENTS IN CIVIL ENGINEERING (VOLUME 2011 PRICES) Source: Statistics Sweden and Veidekke * Annual growth rate Positive market development in civil engineering in 2015 Investment growth of 5% in H1 2015, compared with H Railway and power are positive drivers, road construction down Moderate forecast for civil engineering investments in The extraction industry is being affected by weak commodity prices Municipal technical facilities are facing budget cuts The power sector is moderating its investment plans after many years of high investments Transport projects are increasing as a result of growth in railways Moderate road investments in the period up to the end of 2016 Forecast adjusted down to 2% for 2015 Flat in

38 THE CIVIL ENGINEERING MARKET INVESTMENTS IN CIVIL ENGINEERING (VOLUME 2011 PRICES) Positive market development in civil engineering in 2015 Investment growth of 5% in H1 2015, compared with H Railway and power are positive drivers, road construction down Moderate forecast for civil engineering investments in The extraction industry is being affected by weak commodity prices Municipal technical facilities are facing budget cuts The power sector is moderating its investment plans after many years of high investments Transport projects are increasing as a result of growth in railways Moderate road investments in the period up to the end of 2016 Forecast adjusted down to 2% for 2015 Flat in

39 THE CIVIL ENGINEERING MARKET INVESTMENTS IN CIVIL ENGINEERING (VOLUME 2011 PRICES) Source: Statistics Sweden and Veidekke * Annual growth rate Positive market development in civil engineering in 2015 Investment growth of 5% in H1 2015, compared with H Railway and power are positive drivers, road construction down Moderate forecast for civil engineering investments in The extraction industry is being affected by weak commodity prices Municipal technical facilities are facing budget cuts The power sector is moderating its investment plans after many years of high investments Transport projects are increasing as a result of growth in railways Moderate road investments in the period up to the end of 2016 Forecast adjusted down to 2% for 2015 Flat in

40 CONSTRUCTION MARKETS IN SWEDEN SUMMARY INVESTMENTS IN CONSTRUCTION (VOLUME 2011 PRICES) Source: Statistics Sweden and Veidekke * Annual growth rate Swedish market expected to remain strong throughout the forecast period Investment growth of 7% in 2015 and 3% in 2016 The private sector is the main driver in Residential market +9% Private sector non-residential buildings +6% Moderate growth in public sector demand Public sector non-residential buildings down 3% Moderate growth in transport projects in the period, but with major regional projects in start-up phase 40

41 DANISH CONSTRUCTION MARKET CONSTRUCTION SECTOR REMAINS WEAK Frederiksberg Centret

42 PRIVATE NON-RESIDENTIAL BUILDINGS GROWTH FROM A LOW LEVEL PRIVATE NON-RESIDENTIAL BUILDINGS The general economic recovery has not yet impacted construction and civil engineering The decline is continuing in the market for private nonresidential buildings Still a high level of vacancies, especially offices, which must be absorbed before new dynamics can be created The growth forecast for investments has been downgraded Adjusted down to 0% for 2015 due to weak performance so far this year. Unchanged at 10% growth for 2016 Despite some growth in 2016, the market will continue to be demanding throughout the forecast period Dashed line = Veidekke's projection 42

Still some markets with very low activity The private segment is expected to pick up slightly in 2016 due to a general improvement in the economy Forecast for 2015 adjusted down")

43 DENMARK CONSTRUCTION SECTOR REMAINS WEAK INVESTMENTS IN CONSTRUCTION. FIXED PRICES (DKK) Still some markets with very low activity The private segment is expected to pick up slightly in 2016 due to a general improvement in the economy Forecast for 2015 adjusted down due to weak performance so far this year Public sector segments within civil engineering and nonresidential buildings are expected to decline in the period due to the need for budget cutbacks Source: Statistics Denmark and Veidekke * Annual growth rate

44 SUMMARY

45 e 2015f 2016f SCANDINAVIAN CONSTRUCTION MARKET TOWARDS 2016 Investments in construction, NOK billion* 2011 prices (volume) %** +2%** %** Source: Veidekke, Statistics Sweden, Statistics Denmark and Statistics Norway * Exchange rates for Q ** Compound annual growth rate (CAGR) in

46 APPENDIX

47 FORECASTS Level 2013 BNOK 2014 Growth 2015 Growth 2016 Growth Growth rate Residential 114-5% 3% 1% 2% Private non-res. 50 5% -2% -1% -2% Public non-res. 25 5% 3% 3% 3% Civil engineering 59 6% 6% 5% 5% Constr. total 248 1% 3% 2% 2% Number of units Legend: Unchanged forecast Adjusted down / up Source: Statistics Norway and Veidekke

48 FORECASTS Level BSEK Growth 2015 Growth 2016 Growth Growth rate Residential 97 20% 15% 3% 9% Private non-res % 5% 7% 6% Public non-res % 0% -5% -3% Civil engineering 67 7% 2% 1% 1% Constr. total % 7% 3% 5% Legend: Unchanged forecast Adjusted down / up Number of units Source: Statistics Sweden and Veidekke 48

49 FORECASTS Level 2013 BDKK 2014 Growth 2015 Growth 2016 Growth Growth rate Residential 47 9% 0% 10% 5% Private non-res. 17-4% 0% 10% 5% Public non-res. 17-3% -5% 0% -3% Civil engineering 32 8% -5% 0% -3% Constr. total 112 5% -2% 6% 2% Legend: Unchanged forecast Adjusted down / up Source: Statistics Denmark and Veidekke 49

Svein Gjedrem: Prospects for the Norwegian economy

Svein Gjedrem: Prospects for the Norwegian economy Speech by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway), at Sparebank 1 SR-Bank Stavanger, Stavanger, 26 March 2010. The text below

Svein Gjedrem: Prospects for the Norwegian economy Speech by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway), at Sparebank 1 SR-Bank Stavanger, Stavanger, 26 March 2010. The text below

EUROSYSTEM STAFF MACROECONOMIC PROJECTIONS FOR THE EURO AREA

EUROSYSTEM STAFF MACROECONOMIC PROJECTIONS FOR THE EURO AREA On the basis of the information available up to 22 May 2009, Eurosystem staff have prepared projections for macroeconomic developments in the

EUROSYSTEM STAFF MACROECONOMIC PROJECTIONS FOR THE EURO AREA On the basis of the information available up to 22 May 2009, Eurosystem staff have prepared projections for macroeconomic developments in the

Monetary policy and the economic outlook Governor Svein Gjedrem SR-banken, Stavanger 19 March 2004

Monetary policy and the economic outlook Governor Svein Gjedrem SR-banken, Stavanger 9 March SG SR-banken Stavanger, 9 March Monetary policy regulation. Monetary policy shall be aimed at stability in the

Monetary policy and the economic outlook Governor Svein Gjedrem SR-banken, Stavanger 9 March SG SR-banken Stavanger, 9 March Monetary policy regulation. Monetary policy shall be aimed at stability in the

Jarle Bergo: Monetary policy and the outlook for the Norwegian economy

Jarle Bergo: Monetary policy and the outlook for the Norwegian economy Speech by Mr Jarle Bergo, Deputy Governor of Norges Bank, at the Capital markets seminar, hosted by Terra-Gruppen AS, Gardermoen,

Jarle Bergo: Monetary policy and the outlook for the Norwegian economy Speech by Mr Jarle Bergo, Deputy Governor of Norges Bank, at the Capital markets seminar, hosted by Terra-Gruppen AS, Gardermoen,

Price projection 2013

Price projection 2013 CONTENTS 1. PRICE PROJECTION 2013 3 2. ECONOMIC SITUATION 3 2.1. Finland 4 2.2. Sweden 5 2.3. Norway 5 2.4. Denmark 5 2.5. United Kingdom 5 2.6. The Netherlands 5 3. CURRENCY EXCHANGE

Price projection 2013 CONTENTS 1. PRICE PROJECTION 2013 3 2. ECONOMIC SITUATION 3 2.1. Finland 4 2.2. Sweden 5 2.3. Norway 5 2.4. Denmark 5 2.5. United Kingdom 5 2.6. The Netherlands 5 3. CURRENCY EXCHANGE

Svein Gjedrem: The economic situation in Norway

Svein Gjedrem: The economic situation in Norway Address by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway), to invited foreign embassy representatives, Norges Bank, 21 March 2002. Please

Svein Gjedrem: The economic situation in Norway Address by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway), to invited foreign embassy representatives, Norges Bank, 21 March 2002. Please

Economic Review, April 2012

Economic Review, April 2012 Author Name(s): Malindi Myers, Office for National Statistics Abstract This note provides some wider economic analysis to support the Statistical Bulletin relating to the latest

Economic Review, April 2012 Author Name(s): Malindi Myers, Office for National Statistics Abstract This note provides some wider economic analysis to support the Statistical Bulletin relating to the latest

Taxation trends in the European Union EU27 tax ratio fell to 39.3% of GDP in 2008 Steady decline in top corporate income tax rate since 2000

DG TAXUD 95/2010-28 June 2010 Taxation trends in the European Union EU27 tax ratio fell to 39.3% of GDP in 2008 Steady decline in top corporate income tax rate since 2000 The overall tax-to-gdp ratio 1

DG TAXUD 95/2010-28 June 2010 Taxation trends in the European Union EU27 tax ratio fell to 39.3% of GDP in 2008 Steady decline in top corporate income tax rate since 2000 The overall tax-to-gdp ratio 1

The Norwegian economy

The Norwegian economy Slower speed ahead, but still growth Strong mechanisms support mainland economy Wriggle room to smooth business cycles Rune Bjerke CEO Just how bad is it? Slower speed ahead but still

The Norwegian economy Slower speed ahead, but still growth Strong mechanisms support mainland economy Wriggle room to smooth business cycles Rune Bjerke CEO Just how bad is it? Slower speed ahead but still

Sponda CMD 21 September 2010. Penna Urrila Senior Economist Confederation of Finnish Industries EK

Finnish Lisää tähän Economy otsikko on the Road to Recovery? Sponda CMD 21 September 2 Penna Urrila Senior Economist Confederation of Finnish Industries EK Main Topics 1. Short-term Outlook for Finland

Finnish Lisää tähän Economy otsikko on the Road to Recovery? Sponda CMD 21 September 2 Penna Urrila Senior Economist Confederation of Finnish Industries EK Main Topics 1. Short-term Outlook for Finland

Equity per share (NOK) 147 123 131 Equity ratio 39 % 38 % 36 % Non-current net asset value per share (NOK) (EPRA NNNAV) 2) 184 152 165

147 123 131 Equity ratio 39 % 38 % 36 % Non-current net asset value per share (NOK) (EPRA NNNAV) 2) 184 152 165") REPORT FOR Q2 AND THE FIRST 6 MONTHS OF 2015 KEY FIGURES Amounts in NOK million Q2 2015 Q2 2014 30.06.15 30.06.14 2014 Net rental income 501 450 1 005 904 1 883 Fair value adjustments in investment properties

REPORT FOR Q2 AND THE FIRST 6 MONTHS OF 2015 KEY FIGURES Amounts in NOK million Q2 2015 Q2 2014 30.06.15 30.06.14 2014 Net rental income 501 450 1 005 904 1 883 Fair value adjustments in investment properties

X. INTERNATIONAL ECONOMIC DEVELOPMENT 1/

1/ X. INTERNATIONAL ECONOMIC DEVELOPMENT 1/ 10.1 Overview of World Economy Latest indicators are increasingly suggesting that the significant contraction in economic activity has come to an end, notably

1/ X. INTERNATIONAL ECONOMIC DEVELOPMENT 1/ 10.1 Overview of World Economy Latest indicators are increasingly suggesting that the significant contraction in economic activity has come to an end, notably

UK Economic Forecast Q3 2014

UK Economic Forecast Q3 2014 David Kern, Chief Economist at the BCC The main purpose of the BCC Economic Forecast is to articulate a BCC view on economic topics that are relevant to our members, and to

UK Economic Forecast Q3 2014 David Kern, Chief Economist at the BCC The main purpose of the BCC Economic Forecast is to articulate a BCC view on economic topics that are relevant to our members, and to

South African Reserve Bank. Statement of the Monetary Policy Committee. Issued by Lesetja Kganyago, Governor of the South African Reserve Bank

South African Reserve Bank Press Statement Embargo Delivery 21 July 2016 Statement of the Monetary Policy Committee Issued by Lesetja Kganyago, Governor of the South African Reserve Bank The UK vote to

South African Reserve Bank Press Statement Embargo Delivery 21 July 2016 Statement of the Monetary Policy Committee Issued by Lesetja Kganyago, Governor of the South African Reserve Bank The UK vote to

INFLATION REPORT PRESS CONFERENCE. Thursday 4 th February 2016. Opening remarks by the Governor

INFLATION REPORT PRESS CONFERENCE Thursday 4 th February 2016 Opening remarks by the Governor Good afternoon. At its meeting yesterday, the Monetary Policy Committee (MPC) voted 9-0 to maintain Bank Rate

INFLATION REPORT PRESS CONFERENCE Thursday 4 th February 2016 Opening remarks by the Governor Good afternoon. At its meeting yesterday, the Monetary Policy Committee (MPC) voted 9-0 to maintain Bank Rate

Strategy Document 1/03

Strategy Document / Monetary policy in the period 5 March to 5 June Discussed by the Executive Board at its meeting of 5 February. Approved by the Executive Board at its meeting of 5 March Background Norges

Strategy Document / Monetary policy in the period 5 March to 5 June Discussed by the Executive Board at its meeting of 5 February. Approved by the Executive Board at its meeting of 5 March Background Norges

Jarle Bergo: Monetary policy and cyclical developments

Jarle Bergo: Monetary policy and cyclical developments Speech by Mr Jarle Bergo, Deputy Governor of Norges Bank (Central Bank of Norway), at Sparebanken Sogn og Fjordane, Førde, 18 October 2004. The text

Jarle Bergo: Monetary policy and cyclical developments Speech by Mr Jarle Bergo, Deputy Governor of Norges Bank (Central Bank of Norway), at Sparebanken Sogn og Fjordane, Førde, 18 October 2004. The text

Why is inflation low?

Why is inflation low? MONETARY POLICY REPORT 5 Inflation has been low in Sweden in recent years and fell further in the latter part of, mainly because the rate of price increase for services slowed down.

Why is inflation low? MONETARY POLICY REPORT 5 Inflation has been low in Sweden in recent years and fell further in the latter part of, mainly because the rate of price increase for services slowed down.

Per Jansson: Some aspects of the economic situation

Per Jansson: Some aspects of the economic situation Speech by Mr Per Jansson, Deputy Governor of the Sveriges Riksbank, at Nordea, Stockholm, 3 March. * * * Today, I will talk about the assessment of the

Per Jansson: Some aspects of the economic situation Speech by Mr Per Jansson, Deputy Governor of the Sveriges Riksbank, at Nordea, Stockholm, 3 March. * * * Today, I will talk about the assessment of the

Outlook for European Real Estate in 2013. Mark Charlton, Head of Research & Forecasting

Outlook for European Real Estate in 2013 Mark Charlton, Head of Research & Forecasting Tuesday 20 th November 2012 Europe - uncertainty continues to buffet sentiment Oct 06 Oct 07 Oct 08 Oct 09 Oct 10

Outlook for European Real Estate in 2013 Mark Charlton, Head of Research & Forecasting Tuesday 20 th November 2012 Europe - uncertainty continues to buffet sentiment Oct 06 Oct 07 Oct 08 Oct 09 Oct 10

UK Economic Forecast Q1 2015

UK Economic Forecast Q1 2015 David Kern, Chief Economist at the BCC The main purpose of the BCC Economic Forecast is to articulate a BCC view on economic topics that are relevant to our members, and to

UK Economic Forecast Q1 2015 David Kern, Chief Economist at the BCC The main purpose of the BCC Economic Forecast is to articulate a BCC view on economic topics that are relevant to our members, and to

No boom, (probably) no bust

no bust") No boom, (probably) no bust Global Economic & Market Outlook Riga May 10, 2016 Harald Magnus Andreassen +47 23 23 82 60 hma@swedbank.no The global economy: Growth is normal 3 OK, growth in rich countries

No boom, (probably) no bust Global Economic & Market Outlook Riga May 10, 2016 Harald Magnus Andreassen +47 23 23 82 60 hma@swedbank.no The global economy: Growth is normal 3 OK, growth in rich countries

Dwelling prices, total. Apartment prices. House prices. Net wages

Macro Research Macro Research - The Estonian Economy 22 September, 215 The Estonian Economy Newsletter Risks at the housing market Growth of house prices one of the fastest in Europe House prices have

Macro Research Macro Research - The Estonian Economy 22 September, 215 The Estonian Economy Newsletter Risks at the housing market Growth of house prices one of the fastest in Europe House prices have

Stability in the Eurozone: Challenges and Solutions

Stability in the Eurozone: Challenges and Solutions Ludger Schuknecht Director General Economic and Fiscal Policy Strategy; International Economy and Finance IMFS Working Lunch, Frankfurt (Main), 15 July

Stability in the Eurozone: Challenges and Solutions Ludger Schuknecht Director General Economic and Fiscal Policy Strategy; International Economy and Finance IMFS Working Lunch, Frankfurt (Main), 15 July

Insurance Market Outlook

Munich Re Economic Research May 2014 Premium growth is again slowly gathering momentum After a rather restrained 2013 (according to partly preliminary data), we expect growth in global primary insurance

Munich Re Economic Research May 2014 Premium growth is again slowly gathering momentum After a rather restrained 2013 (according to partly preliminary data), we expect growth in global primary insurance

Except for China (& Ukraine), OK?

, OK?") Except for China (& Ukraine), OK? Global economic & market outlook Riga, May 28, 2014 Harald Magnus Andreassen +47 23 23 82 60 hma@swedbank.no Usually, it has paid well off to be a sober optimist Usually,

Except for China (& Ukraine), OK? Global economic & market outlook Riga, May 28, 2014 Harald Magnus Andreassen +47 23 23 82 60 hma@swedbank.no Usually, it has paid well off to be a sober optimist Usually,

Background. Key points

Background Employment forecasts over the three years to March 2018 1 are presented in this report. These employment forecasts will inform the Ministry s advice relating to immigration priorities, and priority

Background Employment forecasts over the three years to March 2018 1 are presented in this report. These employment forecasts will inform the Ministry s advice relating to immigration priorities, and priority

Domestic steel market overview

Domestic steel market overview Chifipa Mhango Chief Economist: ArcelorMittal South Africa Investor Session: Cape Town & Johannesburg September 2011 The Economy in a nutshell Global overview Advanced economies

Domestic steel market overview Chifipa Mhango Chief Economist: ArcelorMittal South Africa Investor Session: Cape Town & Johannesburg September 2011 The Economy in a nutshell Global overview Advanced economies

Main trends in industry in 2014 and thoughts on future developments. (April 2015)

") Main trends in industry in 2014 and thoughts on future developments (April 2015) Development of the industrial sector in 2014 After two years of recession, industrial production returned to growth in 2014.

Main trends in industry in 2014 and thoughts on future developments (April 2015) Development of the industrial sector in 2014 After two years of recession, industrial production returned to growth in 2014.

NEWS FROM DANMARKS NATIONALBANK

1ST QUARTER 2015 N0 1 NEWS FROM DANMARKS NATIONALBANK PROSPECT OF HIGHER GROWTH IN DENMARK Danmarks Nationalbank adjusts its forecast of growth in the Danish economy this year and next year upwards. GDP

1ST QUARTER 2015 N0 1 NEWS FROM DANMARKS NATIONALBANK PROSPECT OF HIGHER GROWTH IN DENMARK Danmarks Nationalbank adjusts its forecast of growth in the Danish economy this year and next year upwards. GDP

2. UK Government debt and borrowing

2. UK Government debt and borrowing How well do you understand the current UK debt position and the options open to Government to reduce the deficit? This leaflet gives you a general background to the

2. UK Government debt and borrowing How well do you understand the current UK debt position and the options open to Government to reduce the deficit? This leaflet gives you a general background to the

The adjustment of the Spanish Real Estate Sector. May 2011

The adjustment of the Spanish Real Estate Sector May 2011 Although struck by the crisis, Spain is a solid economy, showing signs of recovery Spain resumes an upward trend In the closing months of 2010,

The adjustment of the Spanish Real Estate Sector May 2011 Although struck by the crisis, Spain is a solid economy, showing signs of recovery Spain resumes an upward trend In the closing months of 2010,

European perspective

Fiscal policy challenges from a European perspective Ludger Schuknecht Director General Economic and Fiscal Policy Strategy; International Economy and Finance Federal Ministry of Finance, Germany Banco

Fiscal policy challenges from a European perspective Ludger Schuknecht Director General Economic and Fiscal Policy Strategy; International Economy and Finance Federal Ministry of Finance, Germany Banco

Chapter 3 Demand and production

Chapter 3 Demand and production 3.1 Goods consumption index 1995=1. Seasonally adjusted volume 4 2 22 4 2 21 118 2 118 11 11 114 114 1 Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Source: Statistics

Chapter 3 Demand and production 3.1 Goods consumption index 1995=1. Seasonally adjusted volume 4 2 22 4 2 21 118 2 118 11 11 114 114 1 Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Source: Statistics

Deputy Governor Barbro Wickman-Parak The Swedish property federation, Stockholm. The property market and the financial crisis

SPEECH DATE: 17 June 2009 SPEAKER: LOCALITY: Deputy Governor Barbro Wickman-Parak The Swedish property federation, Stockholm SVERIGES RIKSBANK SE-103 37 Stockholm (Brunkebergstorg 11) Tel +46 8 787 00

SPEECH DATE: 17 June 2009 SPEAKER: LOCALITY: Deputy Governor Barbro Wickman-Parak The Swedish property federation, Stockholm SVERIGES RIKSBANK SE-103 37 Stockholm (Brunkebergstorg 11) Tel +46 8 787 00

Business cycles, monetary policy and property markets Governor Svein Gjedrem Næringseiendom 2005 26 April 2005

Business cycles, monetary policy and property markets Governor Svein Gjedrem Næringseiendom 5 April 5 Projected consumer price inflation 5-year horizon. Annual rise. Per cent Employers organisations Employees

Business cycles, monetary policy and property markets Governor Svein Gjedrem Næringseiendom 5 April 5 Projected consumer price inflation 5-year horizon. Annual rise. Per cent Employers organisations Employees

2013 global economic outlook: Are promising growth trends sustainable? Timothy Hopper, Ph.D., Chief Economist, TIAA-CREF January 24, 2013

2013 global economic outlook: Are promising growth trends sustainable? Timothy Hopper, Ph.D., Chief Economist, TIAA-CREF January 24, 2013 U.S. stock market performance in 2012 * +12.59% total return +6.35%

2013 global economic outlook: Are promising growth trends sustainable? Timothy Hopper, Ph.D., Chief Economist, TIAA-CREF January 24, 2013 U.S. stock market performance in 2012 * +12.59% total return +6.35%

DTZ Foresight European Fair Value Q3 2010 Non-core markets drive temperature rise

DTZ Foresight European Fair Value Q3 Non-core markets drive temperature rise 18 November Contents Overview 1 Fair Value Index 2 Fair Value Classifications 3 European Market Classifications 4 European versus

DTZ Foresight European Fair Value Q3 Non-core markets drive temperature rise 18 November Contents Overview 1 Fair Value Index 2 Fair Value Classifications 3 European Market Classifications 4 European versus

South African Reserve Bank. Statement of the Monetary Policy Committee. Issued by Lesetja Kganyago, Governor of the South African Reserve Bank

South African Reserve Bank PRESS STATEMENT EMBARGO DELIVERY 17 March 2016 Statement of the Monetary Policy Committee Issued by Lesetja Kganyago, Governor of the South African Reserve Bank Since the previous

South African Reserve Bank PRESS STATEMENT EMBARGO DELIVERY 17 March 2016 Statement of the Monetary Policy Committee Issued by Lesetja Kganyago, Governor of the South African Reserve Bank Since the previous

Quarterly Economic Commentary

Quarterly Economic Commentary David Duffy Kieran McQuinn Ciara Morley Daniel Foley Winter 2015 The forecasts in this Commentary are based on data available by 11 December 2015. Draft completed 11 December

Quarterly Economic Commentary David Duffy Kieran McQuinn Ciara Morley Daniel Foley Winter 2015 The forecasts in this Commentary are based on data available by 11 December 2015. Draft completed 11 December

Meeting with Analysts

CNB s New Forecast (Inflation Report IV/) Meeting with Analysts Tibor Hlédik Prague, 7 November, Outline Assumptions of the forecast The new macroeconomic forecast Comparison with the previous forecast

CNB s New Forecast (Inflation Report IV/) Meeting with Analysts Tibor Hlédik Prague, 7 November, Outline Assumptions of the forecast The new macroeconomic forecast Comparison with the previous forecast

Statistics Netherlands. Macroeconomic Imbalances Factsheet

Macroeconomic Imbalances Factsheet Introduction Since the outbreak of the credit crunch crisis in 2008, and the subsequent European debt crisis, it has become clear that there are large macroeconomic imbalances

Macroeconomic Imbalances Factsheet Introduction Since the outbreak of the credit crunch crisis in 2008, and the subsequent European debt crisis, it has become clear that there are large macroeconomic imbalances

The global economy Banco de Portugal Lisbon, 24 September 2013 Mr. Pier Carlo Padoan OECD Deputy Secretary-General and Chief Economist

The global economy Banco de Portugal Lisbon, 24 September 213 Mr. Pier Carlo Padoan OECD Deputy Secretary-General and Chief Economist Summary of presentation Global economy slowly exiting recession but

The global economy Banco de Portugal Lisbon, 24 September 213 Mr. Pier Carlo Padoan OECD Deputy Secretary-General and Chief Economist Summary of presentation Global economy slowly exiting recession but

Economic and Market Outlook. EU Automobile Industry

Economic and Market Outlook EU Automobile Industry March 2015 Report 1 of 4 2015 CONTENTS EU ECONOMIC FORECASTS... 2 PASSENGER CARS... 4 REGISTRATIONS... 4 WORLD... 4 THE EUROPEAN UNION... 6 PRODUCTION...

Economic and Market Outlook EU Automobile Industry March 2015 Report 1 of 4 2015 CONTENTS EU ECONOMIC FORECASTS... 2 PASSENGER CARS... 4 REGISTRATIONS... 4 WORLD... 4 THE EUROPEAN UNION... 6 PRODUCTION...

Gross fixed capital formation: new figures old problems

KfW Investment Barometer Germany: September Frankfurt, 7 th October Gross fixed capital formation: new figures old problems R&D expenditure now officially counts as investment. The investment rates of

KfW Investment Barometer Germany: September Frankfurt, 7 th October Gross fixed capital formation: new figures old problems R&D expenditure now officially counts as investment. The investment rates of

Labour market outlook, spring 2015 SUMMARY

Labour market outlook, spring 2015 SUMMARY Ura 2015:4 Labour market outlook Spring 2015 Summary The next few years will be characterised both by continued improvements in job growth and more people entering

Labour market outlook, spring 2015 SUMMARY Ura 2015:4 Labour market outlook Spring 2015 Summary The next few years will be characterised both by continued improvements in job growth and more people entering

Trends in the European Investment Fund Industry. in the First Quarter of 2016

Quarterly Statistical Release May 2016, N 65 This release and other statistical releases are available on Efama s website (www.efama.org) Trends in the European Investment Fund Industry in the First Quarter

Quarterly Statistical Release May 2016, N 65 This release and other statistical releases are available on Efama s website (www.efama.org) Trends in the European Investment Fund Industry in the First Quarter

Economic Outlook for Europe and Finland

Economic Outlook for Europe and Finland Finnish-British Chamber of Commerce 15 March 213 Seppo Honkapohja Member of the Board Bank of Finland 1 World economy: World industrial output improved, but international

Economic Outlook for Europe and Finland Finnish-British Chamber of Commerce 15 March 213 Seppo Honkapohja Member of the Board Bank of Finland 1 World economy: World industrial output improved, but international

International Women's Day PwC Women in Work Index

www.pwc.co.uk International Women's Day Women in Work Index Women in Work Index UK rises four places to 14 th position within the OECD, returning to its position in 2000. The third annual update of the

www.pwc.co.uk International Women's Day Women in Work Index Women in Work Index UK rises four places to 14 th position within the OECD, returning to its position in 2000. The third annual update of the

Statement to Parliamentary Committee

Statement to Parliamentary Committee Opening Remarks by Mr Glenn Stevens, Governor, in testimony to the House of Representatives Standing Committee on Economics, Sydney, 14 August 2009. The Bank s Statement

Statement to Parliamentary Committee Opening Remarks by Mr Glenn Stevens, Governor, in testimony to the House of Representatives Standing Committee on Economics, Sydney, 14 August 2009. The Bank s Statement

Monetary Policy Report

Monetary Policy Report February 15 S V E R I G E S R I K S B A N K Correction 15--13 Two figures on page 3 were switched around in the previous version of the report. This meant that references to Figures

Monetary Policy Report February 15 S V E R I G E S R I K S B A N K Correction 15--13 Two figures on page 3 were switched around in the previous version of the report. This meant that references to Figures

The economic outlook and monetary policy

The economic outlook and monetary policy Governor Svein Gjedrem SR-Bank, Stavanger March 5 Interest rates and inflation Per cent Market rate Real interest rate Neutral real interest rate Inflation SR-Bank

The economic outlook and monetary policy Governor Svein Gjedrem SR-Bank, Stavanger March 5 Interest rates and inflation Per cent Market rate Real interest rate Neutral real interest rate Inflation SR-Bank

Svein Gjedrem: Monetary policy and the economic outlook

Svein Gjedrem: Monetary policy and the economic outlook Speech by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway), at SR-banken, Stavanger, 19 March 2004. The text below may differ slightly

Svein Gjedrem: Monetary policy and the economic outlook Speech by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway), at SR-banken, Stavanger, 19 March 2004. The text below may differ slightly

The National Budget 2015

The National Budget 215 214-215 The National Budget 215 1 Contents: page 1. Introduction... 2 2. The Norwegian economy... 3 3. Economic policy... 8 3.1 Fiscal policy... 8 3.2 Tax policy... 17 3.3 Monetary

The National Budget 215 214-215 The National Budget 215 1 Contents: page 1. Introduction... 2 2. The Norwegian economy... 3 3. Economic policy... 8 3.1 Fiscal policy... 8 3.2 Tax policy... 17 3.3 Monetary

Meeting with Analysts

CNB s New Forecast (Inflation Report II/2015) Meeting with Analysts Petr Král Prague, 11 May, 2015 1 Outline Assumptions of the forecast The new macroeconomic forecast Comparison with the previous forecast

CNB s New Forecast (Inflation Report II/2015) Meeting with Analysts Petr Král Prague, 11 May, 2015 1 Outline Assumptions of the forecast The new macroeconomic forecast Comparison with the previous forecast

The U.S. and Midwest Economy in 2016: Implications for Supply Chain Firms

The U.S. and Midwest Economy in 2016: Implications for Supply Chain Firms Rick Mattoon Senior Economist and Economic Advisor Federal Reserve Bank of Chicago Right Place Supply Chain Management Conference

The U.S. and Midwest Economy in 2016: Implications for Supply Chain Firms Rick Mattoon Senior Economist and Economic Advisor Federal Reserve Bank of Chicago Right Place Supply Chain Management Conference

Financial Stability 2/12. Charts

Financial Stability /1 Charts Chart 1.1 Vulnerabilities in the Norwegian banking sector and external sources of risk to the banking sector 1) Vulnerability in banking sector External sources of risk to

Financial Stability /1 Charts Chart 1.1 Vulnerabilities in the Norwegian banking sector and external sources of risk to the banking sector 1) Vulnerability in banking sector External sources of risk to

Foreign real estate investments in Norway

NORWEGIAN ECONOMY ROCK SOLID Foreign real estate investments in Norway Catella Real Estate AG KAG Dr. Andreas Kneip MIPIM 2012 As at 2012-03-07 Table of content I. Catella Real Estate AG KAG....... 3 II.

NORWEGIAN ECONOMY ROCK SOLID Foreign real estate investments in Norway Catella Real Estate AG KAG Dr. Andreas Kneip MIPIM 2012 As at 2012-03-07 Table of content I. Catella Real Estate AG KAG....... 3 II.

Joint Economic Forecast Spring 2013. German Economy Recovering Long-Term Approach Needed to Economic Policy

Joint Economic Forecast Spring 2013 German Economy Recovering Long-Term Approach Needed to Economic Policy Press version Embargo until: Thursday, 18 April 2013, 11.00 a.m. CEST Joint Economic Forecast

Joint Economic Forecast Spring 2013 German Economy Recovering Long-Term Approach Needed to Economic Policy Press version Embargo until: Thursday, 18 April 2013, 11.00 a.m. CEST Joint Economic Forecast

The Riksbank's Business Survey STRONG DOMESTIC DEMAND BUT DIFFICULT TO RAISE PRICES

The Riksbank's Business Survey STRONG DOMESTIC DEMAND BUT DIFFICULT TO RAISE PRICES FEBRUARY 2016 The Riksbank s Business Survey in February 2016 1 Swedish companies are now more optimistic about the

The Riksbank's Business Survey STRONG DOMESTIC DEMAND BUT DIFFICULT TO RAISE PRICES FEBRUARY 2016 The Riksbank s Business Survey in February 2016 1 Swedish companies are now more optimistic about the

Domestic Activity. Graph 6.2 Terms of Trade Log scale, 2013/14 average = 100

6. Economic Outlook 6 The International Economy The outlook for GDP growth of Australia s major trading partners (MTPs) is unchanged from the November Statement. Over the next few years, growth is expected

6. Economic Outlook 6 The International Economy The outlook for GDP growth of Australia s major trading partners (MTPs) is unchanged from the November Statement. Over the next few years, growth is expected

THE STATE OF THE ECONOMY

THE STATE OF THE ECONOMY CARLY HARRISON Portland State University Following data revisions, the economy continues to grow steadily, but slowly, in line with expectations. Gross domestic product has increased,

THE STATE OF THE ECONOMY CARLY HARRISON Portland State University Following data revisions, the economy continues to grow steadily, but slowly, in line with expectations. Gross domestic product has increased,

The economic situation and monetary policy

The economic situation and monetary policy Statistics Sweden 6 October 14 Deputy Governor Per Jansson Topics I will discuss today Recent monetary policy (including the most recent decision on 3 September)

The economic situation and monetary policy Statistics Sweden 6 October 14 Deputy Governor Per Jansson Topics I will discuss today Recent monetary policy (including the most recent decision on 3 September)

MACROECONOMIC OVERVIEW

MACROECONOMIC OVERVIEW MAY 20 Koç Holding CONTENTS Global Economy... 3 Global Financial Markets... 3 Global Economic Growth Forecasts... 3 Turkey Macroeconomic Indicators... Economic Growth... Industrial

MACROECONOMIC OVERVIEW MAY 20 Koç Holding CONTENTS Global Economy... 3 Global Financial Markets... 3 Global Economic Growth Forecasts... 3 Turkey Macroeconomic Indicators... Economic Growth... Industrial

The current economic situation in Germany. Deutsche Bundesbank Monthly Report February 2015 5

The current economic situation in Germany Deutsche Bundesbank 5 6 Overview Global economy German economy emerging from sluggish phase faster than expected The global economy looks to have expanded in the

The current economic situation in Germany Deutsche Bundesbank 5 6 Overview Global economy German economy emerging from sluggish phase faster than expected The global economy looks to have expanded in the

Economic and Steel Market Outlook 2014-2015

Economic and Steel Market Outlook 2014-2015 Q1-2014 Report from EUROFER s Economic Committee 1) 23 rd January 2014 EU macro-economic overview (y-o-y change in %) EUROFER Forecast January 2014 EU 2012 2013

Economic and Steel Market Outlook 2014-2015 Q1-2014 Report from EUROFER s Economic Committee 1) 23 rd January 2014 EU macro-economic overview (y-o-y change in %) EUROFER Forecast January 2014 EU 2012 2013

Unaudited Half Year Financial Report January June 2013. Creating career prospects and deploying targeted professional skills.

Creating career prospects and deploying targeted professional skills Amadeus FiRe AG Unaudited Half Year Financial Report January June 2013 Unaudited Half Year Financial Report, January June 2013 1 Unaudited

Creating career prospects and deploying targeted professional skills Amadeus FiRe AG Unaudited Half Year Financial Report January June 2013 Unaudited Half Year Financial Report, January June 2013 1 Unaudited

Equity per share (NOK) 135 123 131 Equity ratio 37 % 39 % 36 % Non-current net asset value per share (NOK) (EPRA NNNAV) 2) 170 153 165

135 123 131 Equity ratio 37 % 39 % 36 % Non-current net asset value per share (NOK) (EPRA NNNAV) 2) 170 153 165") REPORT Q1/2015 KEY FIGURES Amounts in NOK million Q1 2015 Q1 2014 31.12.14 Net rental income 503 454 1 883 Fair value adjustments in investment properties and interest rate derivatives 1 294-9 281 Profit

REPORT Q1/2015 KEY FIGURES Amounts in NOK million Q1 2015 Q1 2014 31.12.14 Net rental income 503 454 1 883 Fair value adjustments in investment properties and interest rate derivatives 1 294-9 281 Profit

Energies andnergies in Sweden - A Strategic Perspective

Capital market day Stockholm, Sweden November 30, 2001 FöreningsSparbanken Birgitta Johansson-Hedberg President and CEO Stability and growth opportunities in a turbulent environment 3 Our strategic approach

Capital market day Stockholm, Sweden November 30, 2001 FöreningsSparbanken Birgitta Johansson-Hedberg President and CEO Stability and growth opportunities in a turbulent environment 3 Our strategic approach

RESULTS FOR THE 1ST HALF OF 2011

CORPORATE PRESS RELEASE N 00 PARIS, JULY 28, 2011 SNCF GROUP FINANCIAL INFORMATION RESULTS FOR THE 1ST HALF OF 2011 Revenue up 9.5%, including one-third from acquisitions All divisions show growth in revenue

CORPORATE PRESS RELEASE N 00 PARIS, JULY 28, 2011 SNCF GROUP FINANCIAL INFORMATION RESULTS FOR THE 1ST HALF OF 2011 Revenue up 9.5%, including one-third from acquisitions All divisions show growth in revenue

INTERIM REPORT SECOND QUARTER 2015 CEO ARNE MJØS OSLO, 27 AUGUST 2015

INTERIM REPORT SECOND QUARTER 2015 CEO ARNE MJØS OSLO, 27 AUGUST 2015 Highlights of the second quarter Revenue NOK 114 million, unchanged from last year. Improved EBITDA of NOK 9.9 million, 8.6 % margin

INTERIM REPORT SECOND QUARTER 2015 CEO ARNE MJØS OSLO, 27 AUGUST 2015 Highlights of the second quarter Revenue NOK 114 million, unchanged from last year. Improved EBITDA of NOK 9.9 million, 8.6 % margin

Summary. Economic Update 1 / 7 May 2016

Economic Update Economic Update 1 / 7 Summary 2 Global World GDP is forecast to grow only 2.4% in 2016, weighed down by emerging market weakness and increasing uncertainty. 3 Eurozone The modest eurozone

Economic Update Economic Update 1 / 7 Summary 2 Global World GDP is forecast to grow only 2.4% in 2016, weighed down by emerging market weakness and increasing uncertainty. 3 Eurozone The modest eurozone

Media-Saturn posts strong increase in earnings METRO GROUP generates better operating performance net debt at record low

10 February 2015 1/9 Media-Saturn posts strong increase in earnings METRO GROUP generates better operating performance net debt at record low EBIT before special items totals 1,024 million (Q1 2013/14:

10 February 2015 1/9 Media-Saturn posts strong increase in earnings METRO GROUP generates better operating performance net debt at record low EBIT before special items totals 1,024 million (Q1 2013/14:

2013 2014e 2015f. www.economics.gov.nl.ca. Real GDP Growth (%)

") The global economy recorded modest growth in 2014. Real GDP rose by 3.4%, however, economic performance varied by country and region (see table). Several regions turned in a lackluster performance. The

The global economy recorded modest growth in 2014. Real GDP rose by 3.4%, however, economic performance varied by country and region (see table). Several regions turned in a lackluster performance. The

Economic Survey 3/2012. Norwegian economy. Economic trends

Economic trends Economic growth among Norway's trading partners has declined markedly in 2012, and is now very low. Both the majority of European countries and the USA are reporting high and rising unemployment.

Economic trends Economic growth among Norway's trading partners has declined markedly in 2012, and is now very low. Both the majority of European countries and the USA are reporting high and rising unemployment.

How To Get Through The Month Of August

London Market Snapshot October 2015 10/15 Global Macro Overview Global equities experienced their sharpest falls since 2011, with most major markets moving into correction territory (a fall of more than

London Market Snapshot October 2015 10/15 Global Macro Overview Global equities experienced their sharpest falls since 2011, with most major markets moving into correction territory (a fall of more than

Eurozone. EY Eurozone Forecast September 2013

Eurozone EY Eurozone Forecast September 213 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Luxembourg Malta Netherlands Portugal Slovakia Slovenia Spain Outlook for Finland

Eurozone EY Eurozone Forecast September 213 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Luxembourg Malta Netherlands Portugal Slovakia Slovenia Spain Outlook for Finland

Spain Economic Outlook. Rafael Doménech EUI-nomics 2015 Debating the Economic Conditions in the Euro Area and Beyond Firenze, 24th of April, 2015

Spain Economic Outlook Rafael Doménech EUI-nomics 2015 Debating the Economic Conditions in the Euro Area and Beyond Firenze, 24th of April, 2015 The outlook one year ago: the risks were to the upside for

Spain Economic Outlook Rafael Doménech EUI-nomics 2015 Debating the Economic Conditions in the Euro Area and Beyond Firenze, 24th of April, 2015 The outlook one year ago: the risks were to the upside for

Will It Be Another Roller Coaster Ride. For The Security and Fire Systems. Market? Contact: Tim Page Press Release No: 29

Press Article www.bsria.co.uk Will It Be Another Roller Coaster Ride For The Security and Fire Systems Market? Contact: Tim Page Press Release No: 29 Release date: Immediate Date: 16/11/09 The latest report

Press Article www.bsria.co.uk Will It Be Another Roller Coaster Ride For The Security and Fire Systems Market? Contact: Tim Page Press Release No: 29 Release date: Immediate Date: 16/11/09 The latest report

Convergence Programme Denmark 2015

Convergence Programme Denmark 2015 March 2015 Index 1. Challenges, Goals and Strategy towards 2020... 3 1.1 The macroeconomic scenario towards 2020... 3 1.2 Goals and strategy towards 2020... 6 2. The

Convergence Programme Denmark 2015 March 2015 Index 1. Challenges, Goals and Strategy towards 2020... 3 1.1 The macroeconomic scenario towards 2020... 3 1.2 Goals and strategy towards 2020... 6 2. The

How To Know How The Falling Oil Price Affects The Global Economy And Inflation

Effects of the falling oil price on the global economy MONETARY POLICY REPORT FEBRUARY 2015 45 Prices on the world market for oil have fallen rapidly since the summer of 2014. Measured in US dollars, the

Effects of the falling oil price on the global economy MONETARY POLICY REPORT FEBRUARY 2015 45 Prices on the world market for oil have fallen rapidly since the summer of 2014. Measured in US dollars, the

Insurance Market Outlook

Munich Re Economic Research May 2016 Emerging countries in Asia still linchpin of global premium growth The offers a brief overview of how we expect the insurance markets to develop over the next ten years.

Munich Re Economic Research May 2016 Emerging countries in Asia still linchpin of global premium growth The offers a brief overview of how we expect the insurance markets to develop over the next ten years.

The outlook for the Norwegian economy with particular focus on the business sector in Vesterålen

The outlook for the Norwegian economy with particular focus on the business sector in Vesterålen Governor Svein Gjedrem Sortland, October Mainland GDP in Norway Annual growth. Per cent 99 99 99 99 99 Sources:

The outlook for the Norwegian economy with particular focus on the business sector in Vesterålen Governor Svein Gjedrem Sortland, October Mainland GDP in Norway Annual growth. Per cent 99 99 99 99 99 Sources:

Markit Global Business Outlook Survey

News Release EMBARGOED UNTIL: :1 (UK), 1 March 14 Markit Global Business Outlook Survey Developed world set to lead strengthening global upturn in 14 Global business optimism hits two-year high Improved

News Release EMBARGOED UNTIL: :1 (UK), 1 March 14 Markit Global Business Outlook Survey Developed world set to lead strengthening global upturn in 14 Global business optimism hits two-year high Improved

Project LINK Meeting New York, 20-22 October 2010. Country Report: Australia

Project LINK Meeting New York, - October 1 Country Report: Australia Prepared by Peter Brain: National Institute of Economic and Industry Research, and Duncan Ironmonger: Department of Economics, University

Project LINK Meeting New York, - October 1 Country Report: Australia Prepared by Peter Brain: National Institute of Economic and Industry Research, and Duncan Ironmonger: Department of Economics, University

Introduction on monetary policy

Introduction on monetary policy Riksdag Committee on Finance 6 March Governor Stefan Ingves Today's presentation The Swedish economy and monetary policy - where are we heading? The Swedish economy has

Introduction on monetary policy Riksdag Committee on Finance 6 March Governor Stefan Ingves Today's presentation The Swedish economy and monetary policy - where are we heading? The Swedish economy has

Unaudited Financial Report

RECRUITING SERVICES Amadeus FiRe AG Unaudited Financial Report Quarter I - 2015 Temporary Staffing. Permanent Placement Interim Management. Training www.amadeus-fire.de Unaudited Amadeus FiRe Group Financial

RECRUITING SERVICES Amadeus FiRe AG Unaudited Financial Report Quarter I - 2015 Temporary Staffing. Permanent Placement Interim Management. Training www.amadeus-fire.de Unaudited Amadeus FiRe Group Financial

Unaudited Nine Months Financial Report

RECRUITING SERVICES Amadeus FiRe AG Unaudited Nine Months Financial Report January to September 2015 Temporary Staffing. Permanent Placement Interim Management. Training www.amadeus-fire.de Unaudited Nine

RECRUITING SERVICES Amadeus FiRe AG Unaudited Nine Months Financial Report January to September 2015 Temporary Staffing. Permanent Placement Interim Management. Training www.amadeus-fire.de Unaudited Nine

Economic and Market Report. EU Automotive Industry Quarter 3 2015

Economic and Market Report EU Automotive Industry Quarter 3 2015 December 2015 CONTENTS EU Economic Outlook... 2 Passenger cars... 4 Registrations... 4 World... 4 The European Union... 7 Production...

Economic and Market Report EU Automotive Industry Quarter 3 2015 December 2015 CONTENTS EU Economic Outlook... 2 Passenger cars... 4 Registrations... 4 World... 4 The European Union... 7 Production...

6. Economic Outlook. The International Economy. Graph 6.2 Terms of Trade Log scale, 2012/13 average = 100

6. Economic Outlook The International Economy Growth of Australia s major trading partners is expected to be around its long-run average in 015 and 016 (Graph 6.1). Forecasts for 015 have been revised

6. Economic Outlook The International Economy Growth of Australia s major trading partners is expected to be around its long-run average in 015 and 016 (Graph 6.1). Forecasts for 015 have been revised

Interim report. January 1 June 30, 2013. Peter Wågström President and CEO Ann-Sofie Danielsson Chief Financial Officer

Interim report January 1 June 3, Peter Wågström President and CEO Ann-Sofie Danielsson Chief Financial Officer Isbjerget Housing Project, Aarhus August 16, 1 Q2 in brief Orders received: SEK 17,798 M (15,453)

Interim report January 1 June 3, Peter Wågström President and CEO Ann-Sofie Danielsson Chief Financial Officer Isbjerget Housing Project, Aarhus August 16, 1 Q2 in brief Orders received: SEK 17,798 M (15,453)

Investment and Investment Finance in Croatia, how can the EIB contribute? Dario Scannapieco and Debora Revoltella European Investment Bank

Investment and Investment Finance in Croatia, how can the EIB contribute? Dario Scannapieco and Debora Revoltella European Investment Bank 24 March 2014 Outline EU and Croatia key challenges The Investment

Investment and Investment Finance in Croatia, how can the EIB contribute? Dario Scannapieco and Debora Revoltella European Investment Bank 24 March 2014 Outline EU and Croatia key challenges The Investment

UNIFE World Rail Market Study

UNIFE World Rail Market Study Status quo and outlook 2020 Commissioned by UNIFE, the European Rail Industry And conducted by The Boston Consulting Group 2 1 Executive Summary This is the third "World Rail

UNIFE World Rail Market Study Status quo and outlook 2020 Commissioned by UNIFE, the European Rail Industry And conducted by The Boston Consulting Group 2 1 Executive Summary This is the third "World Rail

CEO Terje Mjøs. Oslo, 16 July 2014. Q2 2014 Presentation

CEO Terje Mjøs Oslo, 16 July 20 20 Presentation Part I ` Report o Highlights o Group o Segments Part II o Outlook Summary Appendix 20 presentation 2 Highlights Record high order backlog Strategic wins

CEO Terje Mjøs Oslo, 16 July 20 20 Presentation Part I ` Report o Highlights o Group o Segments Part II o Outlook Summary Appendix 20 presentation 2 Highlights Record high order backlog Strategic wins

Account of monetary policy 2014

Account of monetary policy S V E R I G E S R I K S B A N K Account of monetary policy The Riksbank is an authority under the Riksdag, the Swedish Parliament, with responsibility for monetary policy in

Account of monetary policy S V E R I G E S R I K S B A N K Account of monetary policy The Riksbank is an authority under the Riksdag, the Swedish Parliament, with responsibility for monetary policy in

The Lindorff European Credit Outlook

The Lindorff European Credit Outlook 2015 CEO s Corner 3 Summary 4 Status Denmark 6 Finland 8 Germany 10 Norway 12 Spain 14 Sweden 16 The Netherlands 18 Forecasts The Lindorff Credit Outlook Survey 20

The Lindorff European Credit Outlook 2015 CEO s Corner 3 Summary 4 Status Denmark 6 Finland 8 Germany 10 Norway 12 Spain 14 Sweden 16 The Netherlands 18 Forecasts The Lindorff Credit Outlook Survey 20

187/2014-5 December 2014. EU28, euro area and United States GDP growth rates % change over the previous quarter

187/2014-5 December 2014 This News Release has been revised following an error in the data for Gross Fixed Capital Formation. This affects both the growth of GFCF and its contribution to GDP growth. All

187/2014-5 December 2014 This News Release has been revised following an error in the data for Gross Fixed Capital Formation. This affects both the growth of GFCF and its contribution to GDP growth. All

OIL AND THE NORWEGIAN ECONOMY GOVERNOR ØYSTEIN OLSEN NTNU, 29 SEPTEMBER 2015

OIL AND THE NORWEGIAN ECONOMY GOVERNOR ØYSTEIN OLSEN NTNU, 9 SEPTEMBER 15 GDP per capita relative to OECD Index. OECD = 1. Purchasing power adjusted 15 Norway Mainland Norway 15 1 1 5 197 1975 198 1985

OIL AND THE NORWEGIAN ECONOMY GOVERNOR ØYSTEIN OLSEN NTNU, 9 SEPTEMBER 15 GDP per capita relative to OECD Index. OECD = 1. Purchasing power adjusted 15 Norway Mainland Norway 15 1 1 5 197 1975 198 1985

THE ECONOMIC OUTLOOK DEPUTY GOVERNOR JON NICOLAISEN KRISTIANSAND, 3 OCTOBER 2014

THE ECONOMIC OUTLOOK DEPUTY GOVERNOR JON NICOLAISEN KRISTIANSAND, OCTOBER Norges Bank is the central bank of Norway «It devolves upon the Storting to supervise the monetary affairs of the Realm» The Constitution

THE ECONOMIC OUTLOOK DEPUTY GOVERNOR JON NICOLAISEN KRISTIANSAND, OCTOBER Norges Bank is the central bank of Norway «It devolves upon the Storting to supervise the monetary affairs of the Realm» The Constitution

Data Centres that never, never, ever go down

Data Centres that never, never, ever go down Investing in Norwegian Data Centres 13 February 2013 J. Byrne Murphy - Chairman DigiPlex Group of Companies My Topics Today Investing In Norwegian Data Centres

Data Centres that never, never, ever go down Investing in Norwegian Data Centres 13 February 2013 J. Byrne Murphy - Chairman DigiPlex Group of Companies My Topics Today Investing In Norwegian Data Centres