A8.800 Disbursing/Accounts Payable and Payroll. A8.845 Procedures to Establish, Close, and Change Custodian/ Alternate - Departmental Checking Account

|

|

|

- Shanon Todd

- 8 years ago

- Views:

Transcription

1 New Procedure Prepared by the Disbursing Office A8.800 Disbursing/Accounts Payable and Payroll A8.845 Procedures to Establish, Close, and Change Custodian/ Alternate - Departmental Checking Account A8.845 December 1998 p 1 of 8 1. Purpose To provide procedures to establish, close, or change the custodian/alternate of the Departmental Checking account. The Departmental Checking Account Request, (Form DC-1 - Attachment 1), is used to initiate the required action. 2. Responsibilities a. Each Campus/Department Office that requires the establishment, closing, or changing of the custodian/ alternate of a Departmental checking account is responsible for submitting the original Departmental Checking Account Request to the Disbursing Office. b. The Disbursing Office is responsible for coordinating action requests internally within the University organization and the Financial Management Information System (FMIS)as well as externally with the Bank to open or close the Bank subaccount. c. The General Accounting and Loan Collection Office (GALC) will update records for proper execution of responsibilities. d. The Internal Auditor's Office will update records for proper execution of responsibilities.

, is used to initiate the required action. 2. Responsibilities a.")

2 p 2 of 8 3. Guidelines a. Establishment of a Bank Concentration Subaccount The Disbursing Office will coordinate requests to establish a Departmental Checking account by establishing a commercial Bank concentration subaccount and a corresponding FMIS Bank account. No cash is required to sustain the subaccount. b. Appointment of the Custodian and Alternate The Departmental check custodian and the Departmental check alternate should be regular, full-time University employees. In many situations, the custodians and alternates are clerks, account clerks, etc., who can provide a safeguard (separation of duties) for Departmental checking account operations. The duties of the Departmental check custodian/alternate and the approving authority must be strictly segregated. Designating a Fiscal Officer as a custodian will be considered as a last resort measure, and allowed only if the Fiscal Officer does not authorize the specific purchases and payments. Internal control against improprieties are strengthened by the separation of duties. Duties of the Departmental check reconciler and the vendor administrator are also to be segregated from the custodian/alternate. c. Authorization of Departmental Checking Account Request (Form DC-1) All Departmental Checking Account Requests must be approved by the Campus/Department Head (Dean/Director/ Provost/Chancellor/Vice-President) and the Fiscal Officer. The Fiscal Officer assumes responsibility for the proper execution of administrative duties while the Campus/Department Head is ultimately responsible for the proper administration of the Departmental Checking Account and will be held accountable.

3 p 3 of 8 4. Procedures a. Establishment Procedures 1) Campus/Department Office: a) Campus/Department Offices seeking to establish a Departmental checking account must submit the original Departmental Checking Account Request (Form DC-1) to the Disbursing Office for review at least one month in advance of expected implementation. b) The appointed custodian and the alternate are to be identified on the form with signature specimens provided. These appointments must be consistent with the guidelines for selection and separation of duties as specified in section 3.b of this procedure. 2) Disbursing Office: a) Upon approval by the Director of Financial Management & Controller, a Bank subaccount and a corresponding FMIS Bank will be established. A Bank signature card will be sent to the campus/department office with instructions to obtain the signature specimens of the custodian and the alternate. Black ink must be used for all signature specimens. The signature card will then be approved by the Director of Financial Management & Controller and the Secretary of the Board of Regents. The BOR corporate seal will also be affixed on the card. b) A transmittal memo will be sent to the Campus/ Department Head with the signature card and a copy of the approved Departmental Checking Account Request (Form DC-1). Copies of the approved Departmental Checking Account Request are also sent to GALC and the Internal Auditor. Campus/department units are responsible for the ordering of Departmental checks which must be printed in the established format. Printing of the

The appointed custodian and the alternate are to be identified on the form with signature specimens provided.")

4 p 4 of 8 checks are covered by a formal bid process and each campus/department unit is to order Departmental checks through the selected vendor. Contact the Disbursing Office for current information on the ordering of checks. 3) General Accounting and Loan Collection Office: The General Accounting and Loan Collection Office updates records for proper reconciliation of University cash balances. 4) Internal Auditor's Office: The Internal Auditor's Office updates records for the scheduling of audits. b. Close Procedures 1) Campus/Department Office: a) Campus/Department Offices requesting the closing of a Departmental checking account must submit an original Departmental Checking Account Request (Form DC-1) to the Disbursing Office. b) Request to close the Departmental checking account must be justified with an explanation of the situation unless the action was dictated by the Disbursing Office. 2) Disbursing Office: a) Upon approval of the Departmental checking account closing by the Director of Financial Management & Controller, the Disbursing Office will close the Bank subaccount and the corresponding FMIS Bank. b) The campus/department office will be sent a copy of the approved Departmental Checking Account Request (Form DC-1) for record purposes. Copies are also sent to GALC and the Internal Auditor. 3) General Accounting and Loan Collection Office:

Internal Auditor's Office: The Internal Auditor's Office updates records for the scheduling of audits. b.")

5 p 5 of 8 The General Accounting and Loan Collection Office will close Departmental checking records for the Department. 4) Internal Auditor's Office: The Internal Auditor's Office will close Departmental checking records for the Department. c. Change in Custodian/Alternate Procedures 1) Campus/Department Office: a) Campus/Department Offices requesting changes in custodians or alternates must submit the original Departmental Checking Account Request (Form DC-1) to the Disbursing Office. b) The appointed "New" custodian and/or the appointed "New" alternate are to be identified on the form and must provide signature specimens. These changes in appointments must be consistent with the guidelines for selection and separation of duties as specified in section 3.b of this procedure. 2) Disbursing Office: a) Upon approval by the Director of Financial Management & Controller, a copy of the approved Departmental Checking Account Request (Form DC-1) will be transmitted to the Campus/Department Head. Copies are also sent to GALC and the Internal Auditor. b) A bank signature card will be sent to the campus/department office with instructions to obtain the signature specimens of the custodian and the alternate. Both the custodian and alternate must sign the card because the card must reflect the current status and will supersede the previous card (i.e. Both custodian and alternate must sign even if only one has been replaced). Black ink must be used for all signature specimens. The signature card will be approved by the Director of Financial Management & Controller and the Secretary for the Board of Regents. The BOR corporate seal will also be affixed on the card before transmittal

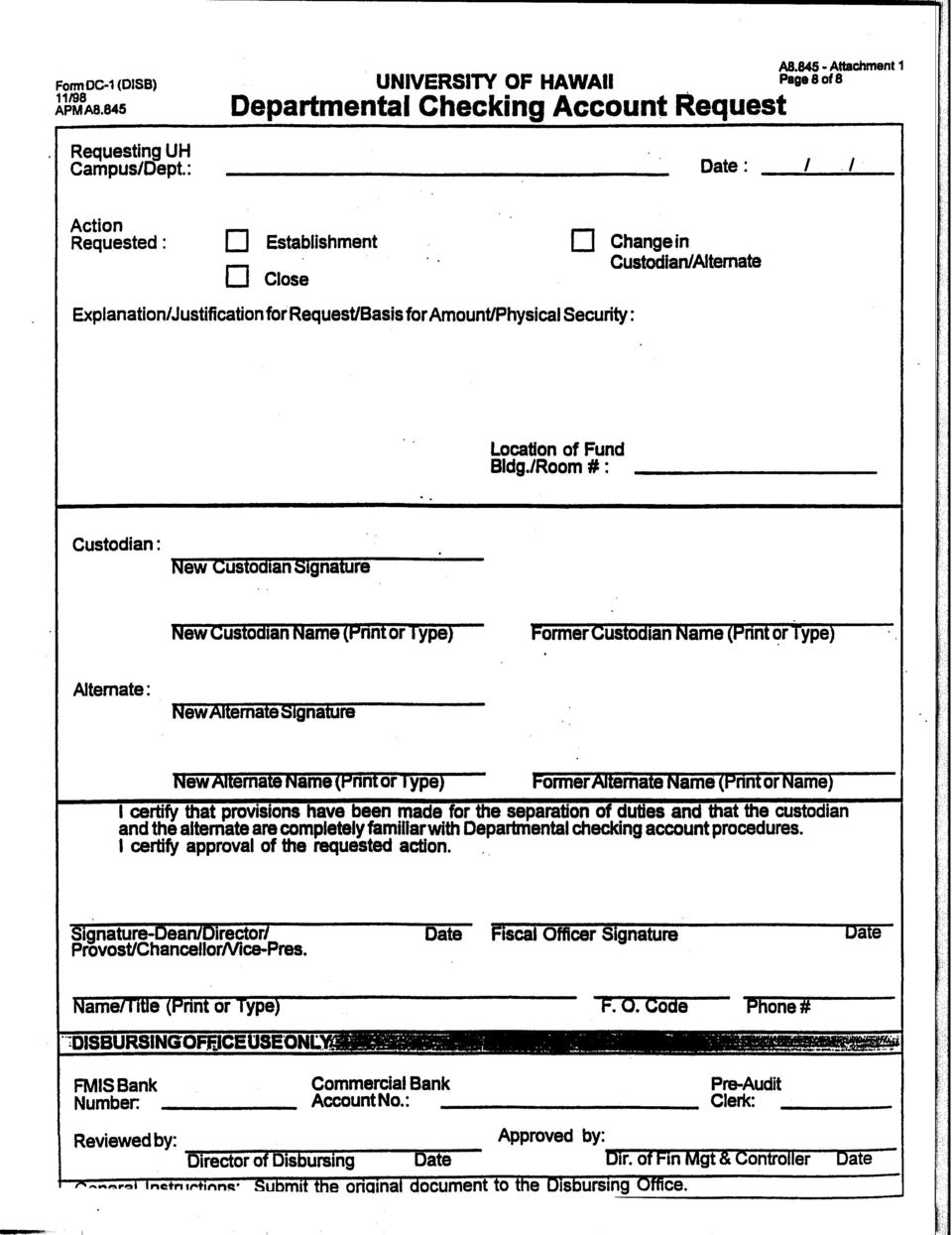

6 p 6 of 8 to the Bank. A copy of the completed bank signature card will be returned to the campus/department office to indicate completion of the process. 3) General Accounting and Loan Collection Office: The General Accounting and Loan Collection Office updates records for proper reconciliation of University cash balances. 4) Internal Auditor's Office: The Internal Auditor's Office will update records for proper execution of responsibilities. 5. Departmental Checking Account Request (Form DC-1) (Attachment 1) a. Detailed Instructions for Completing the "Departmental Checking Account Request" form 1) Requesting UH Campus/Dept.: Enter the appropriate campus and department (e.g. Agr-Bio Chem, Honolulu CC, etc.). 2) Date: Enter the month, day, and year on which the form is being submitted (e.g. 03/31/96). 3) Action Requested: Check the appropriate block. 4) Explanation/Justification for Request/Physical Security: Provide an explanation/justification for the request. Describe the physical security measures that will be instituted to safeguard the Departmental checking account (e.g. storage of checks in a safe with limited access, safety glass or a deadbolt installed in building, etc.). Attach a separate page if additional space is required. 5) Location of Fund - Bldg/Room #: Enter the name or number of the building and the room number in which the Departmental checks are kept. 6) Custodian/Alternate - Signature Specimen and Name: The custodian and alternate signature specimens and names are required for requests to establish a Departmental checking account.

Requesting UH Campus/Dept.: Enter the appropriate campus and department (e.g. Agr-Bio Chem, Honolulu CC, etc.). 2) Date: Enter the month, day, and year on which the form is being submitted (e.")

7 p 7 of 8 The new custodian/alternate signature specimen and name are required for any requested change in custodian/alternate. The former custodian/alternate must also be identified. 7) The Dean/Director/Provost/Chancellor/Vice-President and the Fiscal Officer are to sign and date the completed form to certify approval of the request and to certify provision for separation of duties and custodian/alternate familiarity with Departmental checking account procedures. Indicate the Name/Title of the Campus/Department Head, the Fiscal Officer's code and telephone number. Note: Do not fill in the bottom portion of the form. Central Office approval signatures will be reflected in this section. b. Availability of Forms The Departmental Checking Account Request (Form DC-l) should be reproduced as required.

should be reproduced as required.")

8

A8.800 Disbursing/Accounts Payable and Payroll. A8.847 Reconciliation of the Departmental Checking Account

New Procedure Prepared by the Disbursing Office A8.800 Disbursing/Accounts Payable and Payroll A8.847 Reconciliation of the Departmental Checking Account 1. Purpose A8.847 January 2000 p 1 of 17 To provide

New Procedure Prepared by the Disbursing Office A8.800 Disbursing/Accounts Payable and Payroll A8.847 Reconciliation of the Departmental Checking Account 1. Purpose A8.847 January 2000 p 1 of 17 To provide

How to set up a people based. accounting system that makes your. small business work for you. Thomas G. Post. Certified Public Accountant 281-351-2688

How to set up a people based accounting system that makes your small business work for you. By Thomas G. Post Certified Public Accountant 281-351-2688 www.texastaxman.com 1 Title How to set up a people

How to set up a people based accounting system that makes your small business work for you. By Thomas G. Post Certified Public Accountant 281-351-2688 www.texastaxman.com 1 Title How to set up a people

A8.700 TREASURY. This directive applies to all campuses of the University of Hawai i.

Prepared by Treasury Office. This amends A8.710 dated July 2001. A8.710 April 2005 A8.700 TREASURY P 1 of 5 A8.710 Credit Card Program 1. Purpose To provide uniform procedures for the processing of credit

Prepared by Treasury Office. This amends A8.710 dated July 2001. A8.710 April 2005 A8.700 TREASURY P 1 of 5 A8.710 Credit Card Program 1. Purpose To provide uniform procedures for the processing of credit

Prepared by General Accounting & Loan Collection Office. Replaces Administrative Procedure A8.651 dated July 1982. A8.651

Prepared by General Accounting & Loan Collection Office. Replaces Administrative Procedure A8.651 dated July 1982. A8.651 A8.600 Accounting April 2002 P 1 of 12 A8.651 Accounts Receivable 1. Purpose To

Prepared by General Accounting & Loan Collection Office. Replaces Administrative Procedure A8.651 dated July 1982. A8.651 A8.600 Accounting April 2002 P 1 of 12 A8.651 Accounts Receivable 1. Purpose To

Prepared by the Disbursing Office This replaces Administrative Procedure A8.883 dated May 1992 A8.883 July 1996

Prepared by the Disbursing Office This replaces Administrative Procedure A8.883 dated May 1992 A8.883 July 1996 A8.800 Disbursing/Accounts Payable and Payroll p 1 of 11 A8.883 Student, Casual and Overload

Prepared by the Disbursing Office This replaces Administrative Procedure A8.883 dated May 1992 A8.883 July 1996 A8.800 Disbursing/Accounts Payable and Payroll p 1 of 11 A8.883 Student, Casual and Overload

FINANCIAL AND PURCHASING RECORDS. Includes records showing a summary of receipts, disbursements and other activity against each account.

FINANCIAL AND PURCHASING RECORDS FN-1 Account Distribution Summaries (Treasurer s Report) Includes records showing a summary of receipts, disbursements and other activity against each account. Weekly/Monthly-

FINANCIAL AND PURCHASING RECORDS FN-1 Account Distribution Summaries (Treasurer s Report) Includes records showing a summary of receipts, disbursements and other activity against each account. Weekly/Monthly-

UCLA Policy 360: Internal Control Guidelines for Campus Departments

UCLA Policy 360: Internal Control Guidelines for Campus Departments Issuing Officer: Assistant Vice Chancellor, Corporate Financial Services Responsible Dept: Financial Management Programs Effective Date:

UCLA Policy 360: Internal Control Guidelines for Campus Departments Issuing Officer: Assistant Vice Chancellor, Corporate Financial Services Responsible Dept: Financial Management Programs Effective Date:

Important Disclaimer. Copyright Information

Important Disclaimer This checklist is provided to assist churches in fulfilling the requirement of Book of Order provision G-10.0400, 4, d. The Book of Order does not require that the annual review of

Important Disclaimer This checklist is provided to assist churches in fulfilling the requirement of Book of Order provision G-10.0400, 4, d. The Book of Order does not require that the annual review of

CASH: CASH CONTROLS C-173 ACCOUNTING MANUAL Page 1. Contents. I. Introduction 2. II. General Description of Cash Operations 2

ACCOUNTING MANUAL Page 1 CASH: CASH CONTROLS Contents I. Introduction 2 II. General Description of Cash Operations 2 III. Bank Account Controls 3 A. Regulations Governing Bank Accounts 3 B. Establishment

ACCOUNTING MANUAL Page 1 CASH: CASH CONTROLS Contents I. Introduction 2 II. General Description of Cash Operations 2 III. Bank Account Controls 3 A. Regulations Governing Bank Accounts 3 B. Establishment

The policy and procedural guidelines contained in this handbook are designed to:

BASIC POLICY STATEMENT The Mikva Challenge is committed to responsible financial management. The entire organization including the board of directors, administrators, and staff will work together to make

BASIC POLICY STATEMENT The Mikva Challenge is committed to responsible financial management. The entire organization including the board of directors, administrators, and staff will work together to make

Department of Human Services Client Trust Fund 7290 Trust Accounting System Procedures

Human Services Client Trust Fund 7290 Trust Accounting System Procedures 03.004.00 Effective Date: September 12, 1997 Revised: December 28, 2015 Department of Human Services Client Trust Fund 7290 Trust

Human Services Client Trust Fund 7290 Trust Accounting System Procedures 03.004.00 Effective Date: September 12, 1997 Revised: December 28, 2015 Department of Human Services Client Trust Fund 7290 Trust

Managing Research Subject Payments Draft

UNIVERSITY OF OREGON Managing Research Subject Payments Draft Rob Freytag, Brett Giles, Dan Patten, Martha Schumacher, Teri Rowe, Lynette Schenkel, Beverly Morehouse, Olivia Pierce, Marisa Zuskar THIS

UNIVERSITY OF OREGON Managing Research Subject Payments Draft Rob Freytag, Brett Giles, Dan Patten, Martha Schumacher, Teri Rowe, Lynette Schenkel, Beverly Morehouse, Olivia Pierce, Marisa Zuskar THIS

1. Storeroom supplies -- For items stocked in the Palmer storeroom, use the Requisition for Supplies Form.

DISBURSEMENT PROCESSES Millersville University uses the Accounts Payable module of Banner Finance System to process vendor payments. After payroll, payments for goods and/or services represent the second

DISBURSEMENT PROCESSES Millersville University uses the Accounts Payable module of Banner Finance System to process vendor payments. After payroll, payments for goods and/or services represent the second

c. Name of Accounts. All accounts of the Association, shall be in the Association s name.

Approved 09/09/13 Financial Policies & Procedures It is the purpose of these financial policies and procedures to provide guidance for all financial activities of Connecticut Junior Soccer Association

Approved 09/09/13 Financial Policies & Procedures It is the purpose of these financial policies and procedures to provide guidance for all financial activities of Connecticut Junior Soccer Association

CASH: CHECK CONTROLS C-173-15 ACCOUNTING MANUAL Page 1 CASH: CHECK CONTROLS. Contents. I. Introduction 2

ACCOUNTING MANUAL Page 1 CASH: CHECK CONTROLS Contents Page I. Introduction 2 II. Procedures for Blank Checks 2 A. Procurement 2 B. Storage 3 C. Blank Check Control Record 4 D. Control of Issuance and

ACCOUNTING MANUAL Page 1 CASH: CHECK CONTROLS Contents Page I. Introduction 2 II. Procedures for Blank Checks 2 A. Procurement 2 B. Storage 3 C. Blank Check Control Record 4 D. Control of Issuance and

Administrative Procedures and Forms DEPARTMENTAL DEPOSITS AND CASH RECEIPTING

Administrative Procedures and Forms DEPARTMENTAL DEPOSITS AND CASH RECEIPTING Revised July 1, 2009 Requirements for Implementing Department or Organization Cash Handling Procedures Recognizing the complex

Administrative Procedures and Forms DEPARTMENTAL DEPOSITS AND CASH RECEIPTING Revised July 1, 2009 Requirements for Implementing Department or Organization Cash Handling Procedures Recognizing the complex

SAMPLE FINANCIAL PROCEDURES MANUAL

SAMPLE FINANCIAL PROCEDURES MANUAL Approved by (organization s) Board of Directors on (date) I. GENERAL 1. The Board of Directors formulates financial policies, delegates administration of the financial

SAMPLE FINANCIAL PROCEDURES MANUAL Approved by (organization s) Board of Directors on (date) I. GENERAL 1. The Board of Directors formulates financial policies, delegates administration of the financial

This policy applies to all employees who hold or use petty cash funds, including the security, disbursement, reimbursement and use of these funds.

Policy Number: CS-1001-2013 Policy Title: Petty Cash Fund Policy Policy Owner: Chief Financial Officer Effective Date: April 17, 2013 1. PURPOSE The purpose of Mohawk College s Petty Cash Fund Policy (

Policy Number: CS-1001-2013 Policy Title: Petty Cash Fund Policy Policy Owner: Chief Financial Officer Effective Date: April 17, 2013 1. PURPOSE The purpose of Mohawk College s Petty Cash Fund Policy (

Ithaca College Accepting Cash and Checks Procedures

Ithaca College Accepting Cash and Checks Procedures I. Procedure Statement To minimize institutional risk, Ithaca College discourages individual departments from accepting cash and checks on its behalf.

Ithaca College Accepting Cash and Checks Procedures I. Procedure Statement To minimize institutional risk, Ithaca College discourages individual departments from accepting cash and checks on its behalf.

Research Subject Incentive Payment Procedures. University Financial Services. Business Requirements. 1. Stakeholders & Business Units

Business Requirements This procedure provides guidance and direction for acquiring and accounting for operating advances. Operating advances are used for payments made to individuals as an incentive to

Business Requirements This procedure provides guidance and direction for acquiring and accounting for operating advances. Operating advances are used for payments made to individuals as an incentive to

Prince Hall Grand Chapter, Order of the Eastern Star, Rite of Adoption, Hawaii and its Jurisdictions Inc. Basic Audit Procedures for All Chapters

Prince Hall Grand Chapter, Order of the Eastern Star, Rite of Adoption, Hawaii and its Jurisdictions Inc. Basic Audit Procedures for All Chapters Audit Committee The Audit Committee requires three members

Prince Hall Grand Chapter, Order of the Eastern Star, Rite of Adoption, Hawaii and its Jurisdictions Inc. Basic Audit Procedures for All Chapters Audit Committee The Audit Committee requires three members

ADMINISTRATIVE PRACTICE LETTER

ADMINISTRATIVE PRACTICE LETTER SUBJECT: PETTY CASH Section I - E Issue 6 Page 1 of 2 Effective 7/10/07 GENERAL Each petty cash fund is in the sole custody of a business manager who is responsible to the

ADMINISTRATIVE PRACTICE LETTER SUBJECT: PETTY CASH Section I - E Issue 6 Page 1 of 2 Effective 7/10/07 GENERAL Each petty cash fund is in the sole custody of a business manager who is responsible to the

Wake County. Accounts Receivable Policy and Board Ordinance. www.wakegov.com

Wake County Accounts Receivable Policy and Board Ordinance www.wakegov.com 1 Agenda Provide an overview of Wake County s accounts receivables and our collection efforts. Discuss highlights of our accounts

Wake County Accounts Receivable Policy and Board Ordinance www.wakegov.com 1 Agenda Provide an overview of Wake County s accounts receivables and our collection efforts. Discuss highlights of our accounts

Department of Sociology Cash Handling Procedures Fiscal Year 2016

Department of Sociology Cash Handling Procedures Fiscal Year 2016 I. PURPOSE AND OVERVIEW In accordance with MAPP 05.01.01, Cash Handling, all cash transactions involving the University, its colleges,

Department of Sociology Cash Handling Procedures Fiscal Year 2016 I. PURPOSE AND OVERVIEW In accordance with MAPP 05.01.01, Cash Handling, all cash transactions involving the University, its colleges,

ORDER AMENDING ACCOUNTING SYSTEM RULES FOR CIRCUIT COURTS

IN THE SUPREME COURT, STATE OF WYOMING OCTOBER TERM, A.D. 2013 In the Matter of the Amendment ) of the Accounting System Rules ) for Circuit Courts ) ORDER AMENDING ACCOUNTING SYSTEM RULES FOR CIRCUIT

IN THE SUPREME COURT, STATE OF WYOMING OCTOBER TERM, A.D. 2013 In the Matter of the Amendment ) of the Accounting System Rules ) for Circuit Courts ) ORDER AMENDING ACCOUNTING SYSTEM RULES FOR CIRCUIT

Petty Cash Procedure No.: 2007 PR1

Petty Cash No.: 2007 PR1 Policy Reference: N/A Category: Finance and Supply Management Department Responsible: Financial Services Current Approved Date: 2011 Nov 30 Objectives Departments operate petty

Petty Cash No.: 2007 PR1 Policy Reference: N/A Category: Finance and Supply Management Department Responsible: Financial Services Current Approved Date: 2011 Nov 30 Objectives Departments operate petty

COUNTY OF TRINITY CASH HANDLING PROCEDURES

COUNTY OF TRINITY CASH HANDLING PROCEDURES Prepared by the Trinity County Auditor/Controller s Office Revised October 1, 2009 TABLE OF CONTENTS I. Introduction--------------------------------------------------------------------1

COUNTY OF TRINITY CASH HANDLING PROCEDURES Prepared by the Trinity County Auditor/Controller s Office Revised October 1, 2009 TABLE OF CONTENTS I. Introduction--------------------------------------------------------------------1

Loyal Order of Moose Fraternal Education

Loyal Order of Moose Fraternal Education This booklet presents accounting and tax information that may or may not be right for your specific Fraternal Unit. In view of the complex, individual, and specific

Loyal Order of Moose Fraternal Education This booklet presents accounting and tax information that may or may not be right for your specific Fraternal Unit. In view of the complex, individual, and specific

Or download and view an electronic copy by visiting: www.sarasotagov.com

You can obtain copies of this report by contacting us at: Office of the City Auditor and Clerk 1565 1 st Street Sarasota, FL 34236 (941) 954-4135 Or download and view an electronic copy by visiting: www.sarasotagov.com

You can obtain copies of this report by contacting us at: Office of the City Auditor and Clerk 1565 1 st Street Sarasota, FL 34236 (941) 954-4135 Or download and view an electronic copy by visiting: www.sarasotagov.com

Community Ambulance Service District

Community Ambulance Service District For the period July 1, 2011 through June 30, 2013 Oklahoma State Auditor & Inspector Gary A. Jones, CPA, CFE This publication, issued by the Oklahoma State Auditor

Community Ambulance Service District For the period July 1, 2011 through June 30, 2013 Oklahoma State Auditor & Inspector Gary A. Jones, CPA, CFE This publication, issued by the Oklahoma State Auditor

COUNTY OF FLUVANNA ACCOUNTING & FINANCIAL REPORTING POLICIES AND PROCEDURES

COUNTY OF FLUVANNA ACCOUNTING & FINANCIAL REPORTING POLICIES AND PROCEDURES Consolidation of Capital Expenditures (1.2), Vendor Refunds and Credit Memos (1.3), and Adjusting Journal Entries (1.6) Adopted

COUNTY OF FLUVANNA ACCOUNTING & FINANCIAL REPORTING POLICIES AND PROCEDURES Consolidation of Capital Expenditures (1.2), Vendor Refunds and Credit Memos (1.3), and Adjusting Journal Entries (1.6) Adopted

Chapter 8. Internal Control. Chapter 8-1

8 Internal Control and Cash 8-1 Internal Control and Cash Internal Control Cash Controls Use of a Bank Reporting Cash The Sarbanes- Oxley Act Principles Limitations Control over cash receipts Control over

8 Internal Control and Cash 8-1 Internal Control and Cash Internal Control Cash Controls Use of a Bank Reporting Cash The Sarbanes- Oxley Act Principles Limitations Control over cash receipts Control over

Table of Contents. Transmittal Letter... 1. Executive Summary... 2-3. Background... 4-5. Objectives and Approach... 6. Issues Matrix...

Internal Audit Committee of Brevard County, Florida Internal Audit Review of Accounts Payable Prepared By: Internal Auditors of Brevard County September 22, 2010 Table of Contents Transmittal Letter...

Internal Audit Committee of Brevard County, Florida Internal Audit Review of Accounts Payable Prepared By: Internal Auditors of Brevard County September 22, 2010 Table of Contents Transmittal Letter...

Reconciliation of Cash

2. Trial Balance Notes Trial Balance and Reconciliation of Cash Trial balance: w used to confirm that accounts receivable, program expenditures, and cash balance equal amount of funds authorized and should

2. Trial Balance Notes Trial Balance and Reconciliation of Cash Trial balance: w used to confirm that accounts receivable, program expenditures, and cash balance equal amount of funds authorized and should

[LSC Name] Items Needed for Internal Audit [Audited as of Date]

![[LSC Name] Items Needed for Internal Audit [Audited as of Date]](/thumbs/30/14543766.jpg "[LSC Name] Items Needed for Internal Audit [Audited as of Date]") Items Needed for Internal Audit [Audited as of Date] The following items should be available in preparation for your internal audit: 1. General ledger for the last complete fiscal year and year to date

Items Needed for Internal Audit [Audited as of Date] The following items should be available in preparation for your internal audit: 1. General ledger for the last complete fiscal year and year to date

Pitt County Schools Individual School Accounting. Internal Controls and Responsibilities Fiscal Year 2009-10

Individual School Accounting Internal Controls and Responsibilities Fiscal Year 2009-10 Individual School Accounting Internal Controls and Responsibilities Fiscal Year 2009-10 Contents Page Principal Statement

Individual School Accounting Internal Controls and Responsibilities Fiscal Year 2009-10 Individual School Accounting Internal Controls and Responsibilities Fiscal Year 2009-10 Contents Page Principal Statement

Department of Consumer Affairs Cash Disbursements by Agency Checks

Internal Control Audit of the Department of Consumer Affairs Cash Disbursements by Agency Checks January 2008 Audit No. 2007-102 Internal Audit Office TABLE OF CONTENTS Report Summary Auditor s Report

Internal Control Audit of the Department of Consumer Affairs Cash Disbursements by Agency Checks January 2008 Audit No. 2007-102 Internal Audit Office TABLE OF CONTENTS Report Summary Auditor s Report

Missouri State Auditor March 2014 http://auditor.mo.gov Report No. 2014-016

Thomas A. Schweich Missouri State Auditor FOLLOW-UP REPORT ON AUDIT FINDINGS City of Marshfield March 2014 Report No. 2014-016 http://auditor.mo.gov Follow-Up Report on Audit Findings Table of Contents

Thomas A. Schweich Missouri State Auditor FOLLOW-UP REPORT ON AUDIT FINDINGS City of Marshfield March 2014 Report No. 2014-016 http://auditor.mo.gov Follow-Up Report on Audit Findings Table of Contents

Woodward County Emergency Medical Service District

Woodward County Emergency Medical Service District For the period July 1, 2011 through June 30, 2014 Oklahoma State Auditor & Inspector Gary A. Jones, CPA, CFE FOR THE PERIOD JULY 1, 2011 THROUGH JUNE

Woodward County Emergency Medical Service District For the period July 1, 2011 through June 30, 2014 Oklahoma State Auditor & Inspector Gary A. Jones, CPA, CFE FOR THE PERIOD JULY 1, 2011 THROUGH JUNE

Internal Control Guide & Resources

Internal Control Guide & Resources Section 5- Internal Control Activities & Best Practices Managers must establish internal control activities that support the five internal control components discussed

Internal Control Guide & Resources Section 5- Internal Control Activities & Best Practices Managers must establish internal control activities that support the five internal control components discussed

Department of Veterans Affairs

Audit Report Department of Veterans Affairs December 2013 OFFICE OF LEGISLATIVE AUDITS DEPARTMENT OF LEGISLATIVE SERVICES MARYLAND GENERAL ASSEMBLY This report and any related follow-up correspondence

Audit Report Department of Veterans Affairs December 2013 OFFICE OF LEGISLATIVE AUDITS DEPARTMENT OF LEGISLATIVE SERVICES MARYLAND GENERAL ASSEMBLY This report and any related follow-up correspondence

SUMMARY OF CORRECTIVE ACTION FOR SEGREGATION OF DUTIES AUDIT ISSUES

SUMMARY OF CORRECTIVE ACTION FOR SEGREGATION OF DUTIES AUDIT ISSUES CASH MANAGEMENT I. Checks a. All checks are restrictively endorsed, using the endorsement stamp maintained by the building secretary.

SUMMARY OF CORRECTIVE ACTION FOR SEGREGATION OF DUTIES AUDIT ISSUES CASH MANAGEMENT I. Checks a. All checks are restrictively endorsed, using the endorsement stamp maintained by the building secretary.

NRP Training Series 2001 Financial Record Keeping

NRP Training Series 2001 Financial Record Keeping Copyright 2001 Minneapolis NRP - All Rights Reserved What is the role of the Treasurer? Generally, the treasurer is responsible for compiling and keeping

NRP Training Series 2001 Financial Record Keeping Copyright 2001 Minneapolis NRP - All Rights Reserved What is the role of the Treasurer? Generally, the treasurer is responsible for compiling and keeping

STATE OF NEVADA Department of Administration Division of Human Resource Management CLASS SPECIFICATION TITLE GRADE EEO-4 CODE

STATE OF NEVADA Department of Administration Division of Human Resource Management CLASS SPECIFICATION TITLE GRADE EEO-4 CODE ACCOUNTANT TECHNICIAN III 34 C 7.140 SERIES DISCUSSION Positions allocated

STATE OF NEVADA Department of Administration Division of Human Resource Management CLASS SPECIFICATION TITLE GRADE EEO-4 CODE ACCOUNTANT TECHNICIAN III 34 C 7.140 SERIES DISCUSSION Positions allocated

NAPERVILLE CENTRAL HIGH SCHOOL ATHLETIC BOOSTER CLUB FINANCIAL GUIDELINES

The following list of guidelines is meant to be a blueprint for good financial reporting for the Naperville Central High School Athletic Booster Club (the Club). It is not meant to be an all-inclusive

The following list of guidelines is meant to be a blueprint for good financial reporting for the Naperville Central High School Athletic Booster Club (the Club). It is not meant to be an all-inclusive

INTERNAL CONTROL QUESTIONNAIRE OFFICE OF INTERNAL AUDIT UNIVERSITY OF THE VIRGIN ISLANDS

Cabinet Member or Representative responsible for completing this form: INSTRUCTIONS FOR COMPLETING THIS FORM: Answer each question by placing an X in the either the Yes, No,, or Applicable () column. Provide

Cabinet Member or Representative responsible for completing this form: INSTRUCTIONS FOR COMPLETING THIS FORM: Answer each question by placing an X in the either the Yes, No,, or Applicable () column. Provide

POLICY & PROCEDURE DOCUMENT NUMBER: 3.3011. DIVISION: Finance & Administration. TITLE: Cash Operations Policy and Procedures. DATE: July 15, 2011

POLICY & PROCEDURE DOCUMENT NUMBER: 3.3011 DIVISION: Finance & Administration TITLE: Cash Operations Policy and Procedures DATE: July 15, 2011 Authorized by: K. Ann Mead, VP for Finance & Administration

POLICY & PROCEDURE DOCUMENT NUMBER: 3.3011 DIVISION: Finance & Administration TITLE: Cash Operations Policy and Procedures DATE: July 15, 2011 Authorized by: K. Ann Mead, VP for Finance & Administration

ARKANSAS TECH UNIVERSITY

ARKANSAS TECH UNIVERSITY INVENTORY CONTROL MANUAL SEPTEMBER 2005 PROPERTY MANAGEMENT OFFICE 204 BRYAN EXT. 6087 FAX 968-0227 INTRODUCTION The purpose of this Inventory Manual is to present a uniform method

ARKANSAS TECH UNIVERSITY INVENTORY CONTROL MANUAL SEPTEMBER 2005 PROPERTY MANAGEMENT OFFICE 204 BRYAN EXT. 6087 FAX 968-0227 INTRODUCTION The purpose of this Inventory Manual is to present a uniform method

A8.800 Disbursing/Accounts Payable and Payroll

Prepared by the Disbursing Office This is a New Administrative Procedure A8.839 July 1996 A8.800 Disbursing/Accounts Payable and Payroll p 1 of 28 A8.839 Accounts Payable Processing 1. Purpose To establish

Prepared by the Disbursing Office This is a New Administrative Procedure A8.839 July 1996 A8.800 Disbursing/Accounts Payable and Payroll p 1 of 28 A8.839 Accounts Payable Processing 1. Purpose To establish

2.1. This policy ensures that the Town is pursuing the following objectives in terms of its bank accounts:

POLICY INDEX Policy: BANK ACCOUNTS Policy No.: FINAN-AC-POL08 Department: Financial Services By-Law No: N/A Division: Accounting Draft Completed: September 14, 2015 Prepared By: Justin Rousseau Approval

POLICY INDEX Policy: BANK ACCOUNTS Policy No.: FINAN-AC-POL08 Department: Financial Services By-Law No: N/A Division: Accounting Draft Completed: September 14, 2015 Prepared By: Justin Rousseau Approval

MANAGEMENT LETTER. Noncompliance Findings

MANAGEMENT LETTER Springfield Township 7617 Angola Road Holland, Ohio 43528-8602 To the Board of Trustees: We have audited the financial statements of Springfield Township,, (the Township) in accordance

MANAGEMENT LETTER Springfield Township 7617 Angola Road Holland, Ohio 43528-8602 To the Board of Trustees: We have audited the financial statements of Springfield Township,, (the Township) in accordance

REVOLVING FUND CHECKING ACCOUNTS. Revolving fund checking accounts are authorized with payments not to exceed $75.00 per purchase.

BUSINESS SERVICES DIVISION PROCEDURES MANUAL REVOLVING FUND CHECKING ACCOUNTS REVISED DATE 8/03 INTRODUCTION Revolving fund checking accounts are authorized with payments not to exceed $75.00 per purchase.

BUSINESS SERVICES DIVISION PROCEDURES MANUAL REVOLVING FUND CHECKING ACCOUNTS REVISED DATE 8/03 INTRODUCTION Revolving fund checking accounts are authorized with payments not to exceed $75.00 per purchase.

FISCAL POLICIES AND PROCEDURES

FISCAL POLICIES AND PROCEDURES SECTION 1.1 FINANCIAL RECORDS AND REPORTING Colorado Nonprofit Association's fiscal period begins January 1 and ends December 31. The financial records of the organization

FISCAL POLICIES AND PROCEDURES SECTION 1.1 FINANCIAL RECORDS AND REPORTING Colorado Nonprofit Association's fiscal period begins January 1 and ends December 31. The financial records of the organization

CORPORATE FINANCIAL STATEMENTS BALANCE SHEET (In thousands)

") CORPORATE FINANCIAL STATEMENTS BALANCE SHEET (In thousands) For the Year ASSETS Cash on hand & in Banks Accounts & Notes Receivable Prepaid Expenses Assets Furniture & Equipment Leasehold Improvements

CORPORATE FINANCIAL STATEMENTS BALANCE SHEET (In thousands) For the Year ASSETS Cash on hand & in Banks Accounts & Notes Receivable Prepaid Expenses Assets Furniture & Equipment Leasehold Improvements

Summary of Significant Revisions to the Accounting Procedures Manual For the Public Schools in the State of West Virginia

1-3 Not Specifically Addressed School personnel do not have statutory authority to enter into contracts or obligate board funds. Schools are not separate legal entities. 1-3 Not Specifically Addressed

1-3 Not Specifically Addressed School personnel do not have statutory authority to enter into contracts or obligate board funds. Schools are not separate legal entities. 1-3 Not Specifically Addressed

Arizona State Real Estate Department

A REPORT TO THE ARIZONA LEGISLATURE Financial Audit Division Procedural Review Arizona State Real Estate Department As of May 16, 2006 Debra K. Davenport Auditor General The Auditor General is appointed

A REPORT TO THE ARIZONA LEGISLATURE Financial Audit Division Procedural Review Arizona State Real Estate Department As of May 16, 2006 Debra K. Davenport Auditor General The Auditor General is appointed

FREQUENTLY ASKED QUESTIONS ABOUT THE LOCAL CHURCH AUDIT

FREQUENTLY ASKED QUESTIONS ABOUT THE LOCAL CHURCH AUDIT Updated 2014 Local Church Audit Frequently Asked Questions What is an audit? The Book of Discipline defines a local church audit is an independent

FREQUENTLY ASKED QUESTIONS ABOUT THE LOCAL CHURCH AUDIT Updated 2014 Local Church Audit Frequently Asked Questions What is an audit? The Book of Discipline defines a local church audit is an independent

A REPORT TO THE CITIZENS OF SALT LAKE COUNTY. BEN McADAMS, MAYOR. An Audit of the Key Controls of. Fleet Management.

A REPORT TO THE CITIZENS OF SALT LAKE COUNTY BEN McADAMS, MAYOR An Audit of the Key Controls of Fleet Management April 11, 2013 GREGORY P. HAWKINS SALT LAKE COUNTY AUDITOR Audit reports are available at

A REPORT TO THE CITIZENS OF SALT LAKE COUNTY BEN McADAMS, MAYOR An Audit of the Key Controls of Fleet Management April 11, 2013 GREGORY P. HAWKINS SALT LAKE COUNTY AUDITOR Audit reports are available at

[Company Name] Accounting Policies and Procedures Manual

![[Company Name] Accounting Policies and Procedures Manual](/thumbs/40/20839575.jpg "[Company Name] Accounting Policies and Procedures Manual") [Company Name] Accounting Policies and Procedures Manual [Company Name] Accounting Policies and Procedures Manual Table of Contents Introduction 1 Division of Duties 2 Cash Receipts Procedures 4 Cash Disbursements

[Company Name] Accounting Policies and Procedures Manual [Company Name] Accounting Policies and Procedures Manual Table of Contents Introduction 1 Division of Duties 2 Cash Receipts Procedures 4 Cash Disbursements

PROCEDURE. Accounts Payable

THE RICHARD STOCKTON COLLEGE OF NEW JERSEY PROCEDURE Accounts Payable Procedure Administrator: Associate Vice President for Administration and Finance Authority: N.J.S.A. 18A:64-6 Effective Date: January

THE RICHARD STOCKTON COLLEGE OF NEW JERSEY PROCEDURE Accounts Payable Procedure Administrator: Associate Vice President for Administration and Finance Authority: N.J.S.A. 18A:64-6 Effective Date: January

Office of Public Affairs Business Process Audit Final Report

Office of Public Affairs Business Process Audit Final Report May 2012 Executive Summary We performed a business process audit of the procurement cards, office supplies purchases, small purchase orders

Office of Public Affairs Business Process Audit Final Report May 2012 Executive Summary We performed a business process audit of the procurement cards, office supplies purchases, small purchase orders

FINANCIAL MANAGEMENT POLICIES AND PROCEDURES

FINANCIAL MANAGEMENT POLICIES AND PROCEDURES SAMPLE 1. GENERAL PURPOSE The purpose of these policies is to establish guidelines for developing financial goals and objectives, making financial decisions,

FINANCIAL MANAGEMENT POLICIES AND PROCEDURES SAMPLE 1. GENERAL PURPOSE The purpose of these policies is to establish guidelines for developing financial goals and objectives, making financial decisions,

ABC Division Cash Handling Procedures Fiscal Year 20XX

ABC Division Cash Handling Procedures Fiscal Year 20XX I. PURPOSE AND OVERVIEW In accordance with MAPP 05.01.01, Cash Handling, all cash transactions involving the University, its colleges, or any departments

ABC Division Cash Handling Procedures Fiscal Year 20XX I. PURPOSE AND OVERVIEW In accordance with MAPP 05.01.01, Cash Handling, all cash transactions involving the University, its colleges, or any departments

UNIVERSITY OF NEVADA, RENO WOLF PACK MEATS Internal Audit Report July 1, 2009 through February 28, 2011

UNIVERSITY OF NEVADA, RENO WOLF PACK MEATS Internal Audit Report July 1, 2009 through February 28, 2011 GENERAL OVERVIEW Wolf Pack Meats was established in 1967 and falls administratively under the College

UNIVERSITY OF NEVADA, RENO WOLF PACK MEATS Internal Audit Report July 1, 2009 through February 28, 2011 GENERAL OVERVIEW Wolf Pack Meats was established in 1967 and falls administratively under the College

Guidelines for Congregations Internal Control Best Practices

Guidelines for Congregations Internal Control Best Practices A resource provided by the Office of the Treasurer of the Evangelical Lutheran Church in America Congregations should establish and maintain

Guidelines for Congregations Internal Control Best Practices A resource provided by the Office of the Treasurer of the Evangelical Lutheran Church in America Congregations should establish and maintain

Tel. 202.332.3566 Fax 202.332.3672 www.martinwallcpa.com MANAGEMENT LETTER

Tel. 202.332.3566 Fax 202.332.3672 www.martinwallcpa.com MANAGEMENT LETTER In planning and performing our audit of the financial statements of the U.S. Nuclear Waste Technical Review Board (NWTRB) for

Tel. 202.332.3566 Fax 202.332.3672 www.martinwallcpa.com MANAGEMENT LETTER In planning and performing our audit of the financial statements of the U.S. Nuclear Waste Technical Review Board (NWTRB) for

WESTERN NEVADA COLLEGE THEATER DEPARTMENT Internal Audit Report July 1, 2009 through January 31, 2011

WESTERN NEVADA COLLEGE THEATER DEPARTMENT Internal Audit Report July 1, 2009 through January 31, 2011 GENERAL OVERVIEW The Western Nevada College (WNC) Theater Department falls administratively under the

WESTERN NEVADA COLLEGE THEATER DEPARTMENT Internal Audit Report July 1, 2009 through January 31, 2011 GENERAL OVERVIEW The Western Nevada College (WNC) Theater Department falls administratively under the

INTERNAL CONTROLS IC INTERNAL SELF-ASSESSMENT IMPREST CHECKING (BANK) ACCOUNTS INTERNAL CONTROLS SELF- ASSESSMENT FOR IMPREST CHECKING (BANK) ACCOUNTS

ACCOUNTS INTERNAL CONTROLS SELF- ASSESSMENT FOR IMPREST CHECKING (BANK) ACCOUNTS") ASSESSMENT TO BE COMPLETED INTERNAL CONTROLS IC INTERNAL CONTROLS SELF-ASSESSMENT The for Imprest Checking (Bank) Accounts was developed as a multipurpose tool to assess a unit s compliance with internal

ASSESSMENT TO BE COMPLETED INTERNAL CONTROLS IC INTERNAL CONTROLS SELF-ASSESSMENT The for Imprest Checking (Bank) Accounts was developed as a multipurpose tool to assess a unit s compliance with internal

STATE BOARD OF ACCOUNTS 302 West Washington Street Room E418 INDIANAPOLIS, INDIANA 46204-2765

STATE BOARD OF ACCOUNTS 302 West Washington Street Room E418 INDIANAPOLIS, INDIANA 46204-2765 REVIEW REPORT OF INDIANA PROFESSIONAL LICENSING AGENCY March 1, 2002 to April 30, 2005 TABLE OF CONTENTS Description

STATE BOARD OF ACCOUNTS 302 West Washington Street Room E418 INDIANAPOLIS, INDIANA 46204-2765 REVIEW REPORT OF INDIANA PROFESSIONAL LICENSING AGENCY March 1, 2002 to April 30, 2005 TABLE OF CONTENTS Description

Webster County Procurement Procedures and County Clerk

Thomas A. Schweich Missouri State Auditor FOLLOW-UP REPORT ON AUDIT FINDINGS Webster County Procurement Procedures and County Clerk November 2014 http://auditor.mo.gov Report No. 2014-118 Follow-Up Report

Thomas A. Schweich Missouri State Auditor FOLLOW-UP REPORT ON AUDIT FINDINGS Webster County Procurement Procedures and County Clerk November 2014 http://auditor.mo.gov Report No. 2014-118 Follow-Up Report

Accounting Policies and Procedures Manual

Accounting Policies and Procedures Manual Xxx Accounting Policies and Procedures Manual Table of Contents Introduction 1 Division of Duties 2 Cash Receipts Procedures 4 Cash Disbursements Procedures 6

Accounting Policies and Procedures Manual Xxx Accounting Policies and Procedures Manual Table of Contents Introduction 1 Division of Duties 2 Cash Receipts Procedures 4 Cash Disbursements Procedures 6

CASH HANDLING AND REPORTING

CASH HANDLING AND REPORTING A. Purpose The purpose of this policy is to outline procedures for the consistent cash management at The University of Texas Rio Grande Valley (UTRGV). B. Persons Affected This

CASH HANDLING AND REPORTING A. Purpose The purpose of this policy is to outline procedures for the consistent cash management at The University of Texas Rio Grande Valley (UTRGV). B. Persons Affected This

Seattle Public Schools Office of Internal Audit

Seattle Public Schools Office of Internal Audit Internal Audit Report September 1, 2011 through July 31, 2012 Issue Date: September 11, 2012 Executive Summary Background We completed an audit of the District

Seattle Public Schools Office of Internal Audit Internal Audit Report September 1, 2011 through July 31, 2012 Issue Date: September 11, 2012 Executive Summary Background We completed an audit of the District

Certified Administrator of School Finance and Operations (SFO )

") ASBO International Certified Administrator of School Finance and Operations (SFO ) Practice Questions for Preparation of the SFO Certification Exam Part 1: Accounting www.asbointl.org/certification Practice

ASBO International Certified Administrator of School Finance and Operations (SFO ) Practice Questions for Preparation of the SFO Certification Exam Part 1: Accounting www.asbointl.org/certification Practice

FASHION INSTITUTE OF TECHNOLOGY SELECTED FINANCIAL MANAGEMENT PRACTICES. Report 2006-S-71 OFFICE OF THE NEW YORK STATE COMPTROLLER

Thomas P. DiNapoli COMPTROLLER OFFICE OF THE NEW YORK STATE COMPTROLLER DIVISION OF STATE GOVERNMENT ACCOUNTABILITY Audit Objective... 2 Audit Results - Summary... 2 Background... 3 FASHION INSTITUTE OF

Thomas P. DiNapoli COMPTROLLER OFFICE OF THE NEW YORK STATE COMPTROLLER DIVISION OF STATE GOVERNMENT ACCOUNTABILITY Audit Objective... 2 Audit Results - Summary... 2 Background... 3 FASHION INSTITUTE OF

How To Account For A Wing

ASSETS Cash Wings may place funds in checking accounts, savings accounts, certificates of deposit (CDs), and/or money market accounts. All funds must be readily available without loss of principal. All

ASSETS Cash Wings may place funds in checking accounts, savings accounts, certificates of deposit (CDs), and/or money market accounts. All funds must be readily available without loss of principal. All

Checks and Balances Internal Controls. West Virginia State Auditor s Office Chief Inspector Division

Checks and Balances Internal Controls West Virginia State Auditor s Office Chief Inspector Division POP QUIZ Internal Controls Internal Controls The auditor will test the effectiveness of your internal

Checks and Balances Internal Controls West Virginia State Auditor s Office Chief Inspector Division POP QUIZ Internal Controls Internal Controls The auditor will test the effectiveness of your internal

DIXON MONTESSORI CHARTER SCHOOL FISCAL CONTROL POLICY

DIXON MONTESSORI CHARTER SCHOOL FISCAL CONTROL POLICY 1. Purpose The Dixon Montessori Charter School Board of Directors ( Board ) has reviewed and adopted the following policies and procedures to ensure

DIXON MONTESSORI CHARTER SCHOOL FISCAL CONTROL POLICY 1. Purpose The Dixon Montessori Charter School Board of Directors ( Board ) has reviewed and adopted the following policies and procedures to ensure

City of Brentwood. Thomas A. Schweich Missouri State Auditor FOLLOW-UP REPORT ON AUDIT FINDINGS. October 2013 Report No. 2013-109

Thomas A. Schweich Missouri State Auditor FOLLOW-UP REPORT ON AUDIT FINDINGS City of Brentwood October 2013 Report No. 2013-109 http://auditor.mo.gov Follow-Up Report on Audit Findings Table of Contents

Thomas A. Schweich Missouri State Auditor FOLLOW-UP REPORT ON AUDIT FINDINGS City of Brentwood October 2013 Report No. 2013-109 http://auditor.mo.gov Follow-Up Report on Audit Findings Table of Contents

Attachment 14 Financial Monitoring Tool November 2008

Office of Housing and Community Partnerships Attachment 14 Financial Monitoring Tool November 2008 Prepared by: Ohio Department of Development Community Development Division Office of Housing and Community

Office of Housing and Community Partnerships Attachment 14 Financial Monitoring Tool November 2008 Prepared by: Ohio Department of Development Community Development Division Office of Housing and Community

5:31-7 Appendix B LOCAL AUTHORITIES - ACCOUNTING AND AUDITING IF ANY ARE NOT APPLICABLE, INSERT N/A AS YOUR ANSWER. FIRE DISTRICT YEAR UNDER AUDIT

5:31-7 Appendix B LOCAL AUTHORITIES - ACCOUNTING AND AUDITING AUDIT QUESTIONNAIRE FOR FIRE DISTRICT AUDITS EACH QUESTION MUST BE ANSWERED. PLEASE CIRCLE YES OR NO. IF ANY ARE NOT APPLICABLE, INSERT N/A

5:31-7 Appendix B LOCAL AUTHORITIES - ACCOUNTING AND AUDITING AUDIT QUESTIONNAIRE FOR FIRE DISTRICT AUDITS EACH QUESTION MUST BE ANSWERED. PLEASE CIRCLE YES OR NO. IF ANY ARE NOT APPLICABLE, INSERT N/A

Bulletin 2009-002. Reporting Federal Student Loans Adult Education

Date Issued: February 2, 2009 Bulletin 2009-002 TO: FROM: SUBJECT: School District Treasurers Independent Public Accountants Mary Taylor, CPA Auditor of State Reporting Federal Student Loans Adult Education

Date Issued: February 2, 2009 Bulletin 2009-002 TO: FROM: SUBJECT: School District Treasurers Independent Public Accountants Mary Taylor, CPA Auditor of State Reporting Federal Student Loans Adult Education

TOWN OF CARLYLE POLICY MANUAL

TOWN OF CARLYLE POLICY MANUAL POLICY DESCRIPTION: POLICY NUMBER: IAC 0010 Internal Accounting Controls DATE APPROVED: March 26, 2008 DATE REVISED: October 12, 2011 Purpose of Policy: To promote and protect

TOWN OF CARLYLE POLICY MANUAL POLICY DESCRIPTION: POLICY NUMBER: IAC 0010 Internal Accounting Controls DATE APPROVED: March 26, 2008 DATE REVISED: October 12, 2011 Purpose of Policy: To promote and protect

2. The provisions of this chapter do not apply to payroll cheques, which shall be processed as outlined in Chapter 20.

ACCOUNTS PAYABLE AND DISBURSEMENTS INTRODUCTION 1. This chapter contains the policy and procedures relating to accounting and control for Accounts Payable and Disbursements. For ABACIS procedures, see

ACCOUNTS PAYABLE AND DISBURSEMENTS INTRODUCTION 1. This chapter contains the policy and procedures relating to accounting and control for Accounts Payable and Disbursements. For ABACIS procedures, see

Vance County Schools Individual School Accounting

Individual School Accounting Internal Controls and Responsibilities Individual School Accounting Internal Controls and Responsibilities Contents Page Principal Statement of Understanding 3 Treasurer Statement

Individual School Accounting Internal Controls and Responsibilities Individual School Accounting Internal Controls and Responsibilities Contents Page Principal Statement of Understanding 3 Treasurer Statement

Cash Handling Questionnaire

Cash Handling Questionnaire Internal Control Questionnaire Question Yes No N/A Remarks Because of the relatively high risk associated with transactions involving cash, universities should have a cash management

Cash Handling Questionnaire Internal Control Questionnaire Question Yes No N/A Remarks Because of the relatively high risk associated with transactions involving cash, universities should have a cash management

PROCEDURES for CAMPUS CASH MANAGEMENT POLICY ADM-0113 California State University, Sacramento. CASH HANDLING Updated February 2014

PROCEDURES for CAMPUS CASH MANAGEMENT POLICY ADM-0113 California State University, Sacramento CASH HANDLING Updated February 2014 I. ACCEPTING UNIVERSITY FUNDS II. III. IV. CASH CHANGE FUNDS SAFEGUARDING

PROCEDURES for CAMPUS CASH MANAGEMENT POLICY ADM-0113 California State University, Sacramento CASH HANDLING Updated February 2014 I. ACCEPTING UNIVERSITY FUNDS II. III. IV. CASH CHANGE FUNDS SAFEGUARDING

1501 BANKING RELATIONSHIPS

1501 BANKING RELATIONSHIPS Effective: December 1986 Revised: May 2013 Responsible Office: Treasurer Approval: Treasurer The Vice President for Finance and Treasurer is responsible for the efficient operations

1501 BANKING RELATIONSHIPS Effective: December 1986 Revised: May 2013 Responsible Office: Treasurer Approval: Treasurer The Vice President for Finance and Treasurer is responsible for the efficient operations

Working With Your Auditor

Working With Your Auditor Internal controls are used to ensure that financial statements are accurate and the plan is being operated effectively, efficiently and in compliance with laws and regulations.

Working With Your Auditor Internal controls are used to ensure that financial statements are accurate and the plan is being operated effectively, efficiently and in compliance with laws and regulations.

Florida A & M University

Florida A & M University AP PROCEDURES 3-8-2013 TABLE OF CONTENTS 1.0 OVERVIEW... 1 2.0 DEFINITIONS... 1 3.0 RESPONSIBILITIES... 2 4.0 GENERAL PROCEDURES... 3 4.1 DEPARTMENTAL FISCAL REPRESENTATIVES...

Florida A & M University AP PROCEDURES 3-8-2013 TABLE OF CONTENTS 1.0 OVERVIEW... 1 2.0 DEFINITIONS... 1 3.0 RESPONSIBILITIES... 2 4.0 GENERAL PROCEDURES... 3 4.1 DEPARTMENTAL FISCAL REPRESENTATIVES...

TWU CASH RECEIPTS POLICY

TWU CASH RECEIPTS POLICY The TWU Cash Receipts Policy provides procedures and guidelines to all University departments handling cash collections. Procedures have been established to encourage an effective

TWU CASH RECEIPTS POLICY The TWU Cash Receipts Policy provides procedures and guidelines to all University departments handling cash collections. Procedures have been established to encourage an effective

NOTICE REQUEST FOR PROPOSALS FOR INTERIM TOWN ACCOUNTANT SERVICES TOWN OF SCITUATE, MA

NOTICE REQUEST FOR PROPOSALS FOR INTERIM TOWN ACCOUNTANT SERVICES TOWN OF SCITUATE, MA The Town of Scituate, acting through its Chief Procurement Officer, seeks sealed proposals from qualified firms or

NOTICE REQUEST FOR PROPOSALS FOR INTERIM TOWN ACCOUNTANT SERVICES TOWN OF SCITUATE, MA The Town of Scituate, acting through its Chief Procurement Officer, seeks sealed proposals from qualified firms or

Supervisor Carges called the meeting to order at 7:00 p.m. and asked everyone present to say the Pledge to the Flag.

A regular meeting of the Town Board of the Town of Sweden was held at the Town Hall, 18 State Street, Brockport, New York, on Tuesday, September 23, 2014. Town Board Members present were Supervisor Robert

A regular meeting of the Town Board of the Town of Sweden was held at the Town Hall, 18 State Street, Brockport, New York, on Tuesday, September 23, 2014. Town Board Members present were Supervisor Robert

Guidelines for Congregations Internal Control Best Practices

Guidelines for Congregations Internal Control Best Practices A resource provided by the Office of the Treasurer of the Evangelical Lutheran Church in America In order to exercise good stewardship and care

Guidelines for Congregations Internal Control Best Practices A resource provided by the Office of the Treasurer of the Evangelical Lutheran Church in America In order to exercise good stewardship and care

Version Date: 10/16/2013

2004094 Accounting Documents (ADVANTAGE Financial System Input) This record series is used to input information into the ADVANTAGE Financial System. The files may contain, but are not limited to: copies

2004094 Accounting Documents (ADVANTAGE Financial System Input) This record series is used to input information into the ADVANTAGE Financial System. The files may contain, but are not limited to: copies

If a Not-for-profit organization has an organizational audit, it should be submitted with the property audit.

AUDIT REQUIREMENTS All WHEDA-financed & ARRA developments, unless notified previously, are required to submit an annual audited financial statement within 60 days of fiscal year end. If a Not-for-profit

AUDIT REQUIREMENTS All WHEDA-financed & ARRA developments, unless notified previously, are required to submit an annual audited financial statement within 60 days of fiscal year end. If a Not-for-profit

SAMPLE NPO Fiscal Policies & Procedures

SAMPLE NPO NOTE: The most important part of developing policies and procedures is that they are discussed and agreed upon within the organization. This template is designed to be used in conjunction with

SAMPLE NPO NOTE: The most important part of developing policies and procedures is that they are discussed and agreed upon within the organization. This template is designed to be used in conjunction with

WEST VIRGINIA DEPARTMENT OF TRANSPORTATION ADMINISTRATIVE PROCEDURES VOLUME VI, CHAPTER 10 CORRECTING RECEIPT ERRORS

WEST VIRGINIA DEPARTMENT OF TRANSPORTATION ADMINISTRATIVE PROCEDURES VOLUME VI, CHAPTER 10 SUBJECT: CHAPTER TITLE: PURCHASING INVOICE PROCESSING AND CORRECTING RECEIPT ERRORS TABLE OF CONTENTS I. INTRODUCTION

WEST VIRGINIA DEPARTMENT OF TRANSPORTATION ADMINISTRATIVE PROCEDURES VOLUME VI, CHAPTER 10 SUBJECT: CHAPTER TITLE: PURCHASING INVOICE PROCESSING AND CORRECTING RECEIPT ERRORS TABLE OF CONTENTS I. INTRODUCTION

Eugene Smith Executive Director of Athletics Department of Intercollegiate Athletics Arizona State University Box 872505 Tempe, AZ 85287-2505

January 16, 2003 Eugene Smith Executive Director of Athletics Department of Intercollegiate Athletics Arizona State University Box 872505 Tempe, AZ 85287-2505 Dear Mr. Smith: In accordance with National

January 16, 2003 Eugene Smith Executive Director of Athletics Department of Intercollegiate Athletics Arizona State University Box 872505 Tempe, AZ 85287-2505 Dear Mr. Smith: In accordance with National

PETTY CASH AND CHANGE FUNDS

PURPOSE To provide procedures and guidance to maintain an adequate system of internal control to protect petty cash and change funds from loss in accordance with ICSUAM Policy and ICSUAM 3103.11. SCOPE

PURPOSE To provide procedures and guidance to maintain an adequate system of internal control to protect petty cash and change funds from loss in accordance with ICSUAM Policy and ICSUAM 3103.11. SCOPE