Statement of Financial Accounting Standards No.150. Accounting for Certain Financial Instruments with Characteristics of Both Liabilities and Equity

|

|

|

- Hannah Welch

- 7 years ago

- Views:

Transcription

1 Statement of Financial Accounting Standards No.150 Accounting for Certain Financial Instruments with Characteristics of Both Liabilities and Equity

2 Introduction Established standards for how a company classifies and measures certain financial instruments with characteristics of both liabilities and equity. Requires these financial instruments to be recorded as liabilities because an obligation exists.

3 Definitions Financial Instrument Cash, an ownership interest, or a contract that imposes a contractual obligation to transfer cash or other financial instruments. Obligation A conditional or unconditional duty or responsibility to transfer assets or to issue equity shares.

4 Three Types of Financial Instruments to be Treated as Liabilities Those issued in the form of shares that embody an unconditional obligation to redeem the shares (mandatorily redeemable) by transferring assets at a specific date or upon an event that is certain to occur (example: preferred stock). Those that embody an obligation to repurchase the entity s shares or settle an obligation (examples: buy/sell agreements, capital credits). Those that embody an obligation to issue equity shares.

5 Mandatorily Redeemable Mandatorily redeemable financial instruments do not include those for which redemption is required only upon liquidation of the reporting entity (example: capital credits). Cooperative memberships would not typically be considered mandatorily redeemable because redemption is conditional upon terminating service or liquidation.

6 Summary of Provisions Required to recognize a liability at fair value for any redemption provisions covered by SFAS 150. Fair value can be the present value the amount expected to be settled upon occurrence of the redemption event or the redemption price at the balance sheet date.

7 Freestanding Financial Instruments SFAS 150 only applies to freestanding financial instruments which are those entered into separately or that are separately exercisable and legally detachable. A redemption provision embedded in a partnership or membership agreement is not freestanding.

8 Disclosure Requirements Nature and terms of financial instruments and the rights and obligations embodied in those instruments. Amount that would be paid or number of shares that would be issued and the fair value if the settlement were to occur at the reporting date. How changes in the fair value of the entities equity shares would affect settlement amounts.

9 Disclosure Requirements That May Not Apply The maximum amount that the issuer could be required to pay to redeem the instrument by physical settlement. The maximum number of shares that could be required to be issued. That a contract does not limit the amount the issuer could be required to pay or the number of shares to be issued.

10 Example: Stock to be Redeemed at Death of Holder Assume that the stock is to be redeemed at book value of the entity and that it represents the only shares in the entity. Because death is certain to occur, must classify as a liability.

11 Example: Stock to be Redeemed at Balance Sheet Death of Holder (cont) Total assets $2,400,000 Liabilities other than shares $1,800,000 Shares subject to mandatory redemption 600,000 Total Liabilities $2,400,000

12 Example: Stock to be Redeemed at Death of Holder (cont) Notes to Financial Statements Shares subject to mandatory redemption upon death of holder consist of: Common stock - $100 par value, 10,000 shares authorized, 5000 shares issued and outstanding $ 500,000 Retained earnings attributable to those shares 120,000 Accumulated other comprehensive income attributable to those shares (20,000) $ 600,000

$")

13 Example: Mandatorily Redeemable Shares at Fair Value Assume adoption of SFAS 150 on January 1, Assume stock is to be redeemed at Fair value. Assume fair value (which equals the redemption value) at 1/1/04 is $20 million. Assume book value at 1/1/04 is $15 million of which $10 million is paid-in capital.

14 Example: Mandatorily Redeemable Shares at Fair Value (cont) On 1/1/04, the company would recognize a $20 million liability by transferring $15 million out of equity and recording a cumulative transition adjustment loss in the income statement of $5 million. The balance sheet would show excess of liabilities over assets (deficit equity) of $5 million.

of $5")

15 Example: Mandatorily Redeemable Shares at Fair Value (cont) Assume 2004 net income attributable, on a pro-rata basis, to mandatorily redeemable shares (MRS) is $1 million and the fair value of those shares at 12/31/04 is $21.2 million. The 2004 income statement would show the following:

16 Example: Mandatorily Redeemable Shares at Fair Value (cont) Income before interest on MRS $ 1,000,000 Less interest expense on MRS 1,200,000 Income before cumulative effect of accounting change (200,000) Cumulative effect of acctg. change (5,000,000) Net loss $ (5,200,000)

Cumulative effect of acctg.")

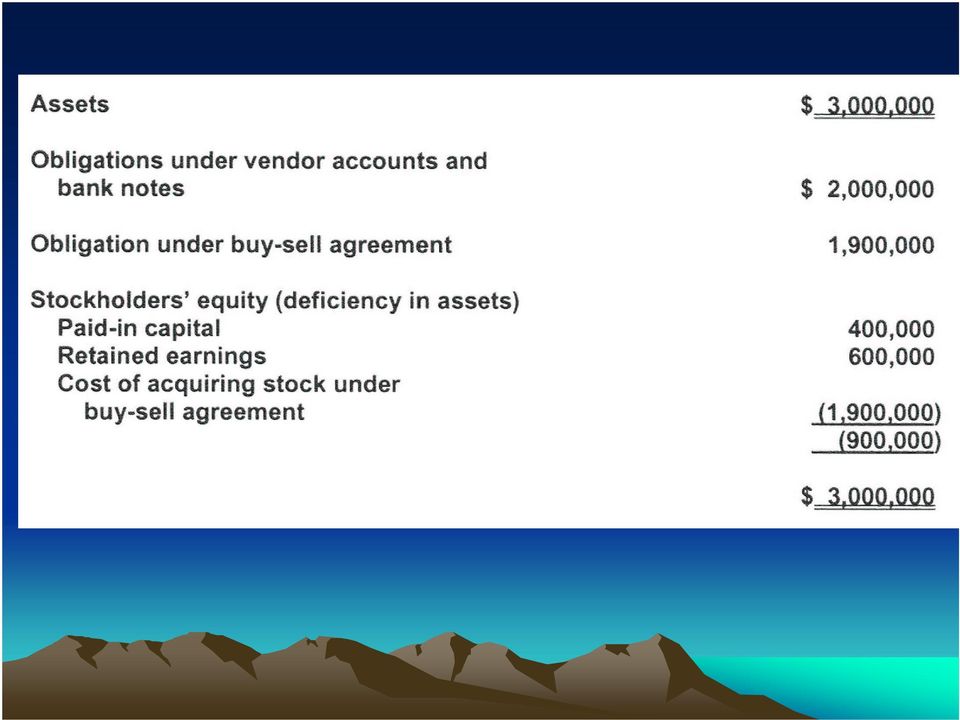

17 Example: Buy/Sell Agreement Requiring Redemption Upon Retirement Assume company enters buy/sell agreement (BSA) with majority shareholder after date of adoption of SFAS 150. Assume fair value assigned to majority shareholder s stock is $1.9 million at 12/31/04. The balance sheet at 12/31/04 would show the following:

18

19 Effective Date and Implementation Public Companies SFAS 150 is effective for financial instruments entered into or modified after May 31, 2003, or for existing financial instruments, for periods beginning after June 15, 2003.

20 Effective Date and Implementation Non-public Companies For instruments that are mandatorily redeemable on fixed dates for fixed or indexed amounts, SFAS 150 is effective for periods beginning after December 15, For all other financial instruments, SFAS 150 implementation has been deferred indefinitely.

21 The End Presented by: Blake Lackey, CPA Curtis Blakely & Co. P.C. P. O. Box 5486 Longview, TX

What Management Should Know Before Issuing Equity-Linked Instruments in Financing Transactions

What Management Should Know Before Issuing Equity-Linked Instruments in Financing Transactions October 2012 Table of Contents Navigating through the Guidance 2 ASC 480, Distinguishing Liabilities from

What Management Should Know Before Issuing Equity-Linked Instruments in Financing Transactions October 2012 Table of Contents Navigating through the Guidance 2 ASC 480, Distinguishing Liabilities from

IASB/FASB Meeting October 2009

IASB/FASB Meeting October 2009 IASB agenda reference 9 FASB memo reference 69 Project Financial Instruments with Characteristics of Topic Classification Approach 4.1 Introduction 1. Under Approach 4, all

IASB/FASB Meeting October 2009 IASB agenda reference 9 FASB memo reference 69 Project Financial Instruments with Characteristics of Topic Classification Approach 4.1 Introduction 1. Under Approach 4, all

The primary trigger for Equity Instruments to be treated as Debt

Equity Treated as Debt for Financial Statement Purposes? How the Structure of Certain Equity Instruments Can Cause Unintended Reporting Consequences. By: Ryan Koppe, CPA, CM&AA and CMAP Imagine being a

Equity Treated as Debt for Financial Statement Purposes? How the Structure of Certain Equity Instruments Can Cause Unintended Reporting Consequences. By: Ryan Koppe, CPA, CM&AA and CMAP Imagine being a

Indian Accounting Standard (Ind AS) 32 Financial Instruments: Presentation

32 Financial Instruments: Presentation") Indian Accounting Standard (Ind AS) 32 Financial Instruments: Presentation Contents Paragraphs Objective 2 3 Scope 4 10 Definitions 11 14 Presentation 15 50 Liabilities and equity 15 27 Puttable instruments

Indian Accounting Standard (Ind AS) 32 Financial Instruments: Presentation Contents Paragraphs Objective 2 3 Scope 4 10 Definitions 11 14 Presentation 15 50 Liabilities and equity 15 27 Puttable instruments

Ind AS 32 and Ind AS 109 - Financial Instruments Classification, recognition and measurement. June 2015

Ind AS 32 and Ind AS 109 - Financial Instruments Classification, recognition and measurement June 2015 Contents Executive summary Standards dealing with financial instruments under Ind AS Financial instruments

Ind AS 32 and Ind AS 109 - Financial Instruments Classification, recognition and measurement June 2015 Contents Executive summary Standards dealing with financial instruments under Ind AS Financial instruments

A PRACTICAL GUIDE TO THE CLASSIFICATION OF FINANCIAL INSTRUMENTS UNDER IAS 32 MARCH 2013. Liability or equity?

A PRACTICAL GUIDE TO THE CLASSIFICATION OF FINANCIAL INSTRUMENTS UNDER IAS 32 MARCH 2013 Liability or equity? Important Disclaimer: This document has been developed as an information resource. It is intended

A PRACTICAL GUIDE TO THE CLASSIFICATION OF FINANCIAL INSTRUMENTS UNDER IAS 32 MARCH 2013 Liability or equity? Important Disclaimer: This document has been developed as an information resource. It is intended

Adviser alert Liability or equity? A practical guide to the classification of financial instruments under IAS 32 (revised guide)

") Adviser alert Liability or equity? A practical guide to the classification of financial instruments under IAS 32 (revised guide) April 2013 Overview The Grant Thornton International IFRS team has published

Adviser alert Liability or equity? A practical guide to the classification of financial instruments under IAS 32 (revised guide) April 2013 Overview The Grant Thornton International IFRS team has published

Corporations: Organization, Stock Transactions, and Dividends

C H A P T E R 13 Corporations: Organization, Stock Transactions, and Dividends Financial Accounting 14e Warren Reeve Duchac human/istock/360/getty Images Advantages and Disadvantages of the Corporate Form

C H A P T E R 13 Corporations: Organization, Stock Transactions, and Dividends Financial Accounting 14e Warren Reeve Duchac human/istock/360/getty Images Advantages and Disadvantages of the Corporate Form

Title: Accounting for Convertible Debt Instruments That May Be Settled in Cash upon Conversion (Including Partial Cash Settlement)

") FASB STAFF POSITION No. APB 14-1 Title: Accounting for Convertible Debt Instruments That May Be Settled in Cash upon Conversion (Including Partial Cash Settlement) Date Posted: May 9, 2008 Introduction

FASB STAFF POSITION No. APB 14-1 Title: Accounting for Convertible Debt Instruments That May Be Settled in Cash upon Conversion (Including Partial Cash Settlement) Date Posted: May 9, 2008 Introduction

International Accounting Standard 32 Financial Instruments: Presentation

EC staff consolidated version as of 21 June 2012, EN EU IAS 32 FOR INFORMATION PURPOSES ONLY International Accounting Standard 32 Financial Instruments: Presentation Objective 1 [Deleted] 2 The objective

EC staff consolidated version as of 21 June 2012, EN EU IAS 32 FOR INFORMATION PURPOSES ONLY International Accounting Standard 32 Financial Instruments: Presentation Objective 1 [Deleted] 2 The objective

GOVERNMENT OF MALAYSIA

GOVERNMENT OF MALAYSIA Malaysian Public Sector Accounting Standards MPSAS 28 Financial Instruments: Presentation May 2014 MPSAS 28 - Financial Instruments: Presentation Acknowledgment The Malaysian Public

GOVERNMENT OF MALAYSIA Malaysian Public Sector Accounting Standards MPSAS 28 Financial Instruments: Presentation May 2014 MPSAS 28 - Financial Instruments: Presentation Acknowledgment The Malaysian Public

A. Retained Earnings the basic source of retained earnings is income from operations.

Chapter 16 Stockholders Equity: Retained Earnings LECTURE OUTLINE The material in this chapter is straight-forward and can be covered in two class periods. Students are often not familiar with dividend

Chapter 16 Stockholders Equity: Retained Earnings LECTURE OUTLINE The material in this chapter is straight-forward and can be covered in two class periods. Students are often not familiar with dividend

TIME WARNER CABLE INC. CONSOLIDATED BALANCE SHEET (Unaudited)

") CONSOLIDATED BALANCE SHEET June 30, December 31, 2011 2010 (in millions) ASSETS Current assets: Cash and equivalents...$ 3,510 $ 3,047 Receivables, less allowances of $86 million and $74 million as of

CONSOLIDATED BALANCE SHEET June 30, December 31, 2011 2010 (in millions) ASSETS Current assets: Cash and equivalents...$ 3,510 $ 3,047 Receivables, less allowances of $86 million and $74 million as of

Chapter 18 Shareholders Equity

Chapter 18 Shareholders Equity AACSB assurance of learning standards in accounting and business education require documentation of outcomes assessment. Although schools, departments, and faculty may approach

Chapter 18 Shareholders Equity AACSB assurance of learning standards in accounting and business education require documentation of outcomes assessment. Although schools, departments, and faculty may approach

Consolidated Balance Sheets March 31, 2001 and 2000

Financial Statements SEIKAGAKU CORPORATION AND CONSOLIDATED SUBSIDIARIES Consolidated Balance Sheets March 31, 2001 and 2000 Assets Current assets: Cash and cash equivalents... Short-term investments (Note

Financial Statements SEIKAGAKU CORPORATION AND CONSOLIDATED SUBSIDIARIES Consolidated Balance Sheets March 31, 2001 and 2000 Assets Current assets: Cash and cash equivalents... Short-term investments (Note

Chapter 19 Share Based Compensation and Earnings Per Share

SHARE-BASED COMPENSATION PLANS In accounting for stock-based compensation plans our objective is to: 1. Determine the value of the compensation, and 2. Expense the compensation over the periods in which

SHARE-BASED COMPENSATION PLANS In accounting for stock-based compensation plans our objective is to: 1. Determine the value of the compensation, and 2. Expense the compensation over the periods in which

STATE OF INDIANA. November 14, 2011. Board of Directors Foster Parent Services, Inc. 3798 W. Co. Road 500 S. Vallonia, IN 47281

` STATE OF INDIANA AN EQUAL OPPORTUNITY EMPLOYER STATE BOARD OF ACCOUNTS 302 WEST WASHINGTON STREET ROOM E418 INDIANAPOLIS, INDIANA 46204-2769 Telephone: (317) 232-2513 Fax: (317) 232-4711 Web Site: www.in.gov/sboa

` STATE OF INDIANA AN EQUAL OPPORTUNITY EMPLOYER STATE BOARD OF ACCOUNTS 302 WEST WASHINGTON STREET ROOM E418 INDIANAPOLIS, INDIANA 46204-2769 Telephone: (317) 232-2513 Fax: (317) 232-4711 Web Site: www.in.gov/sboa

Illinois Corporate Franchise Tax. Department of Revenue 3-21-2014 House Joint Committee of Revenue and Finance and State Government

Illinois Corporate Franchise Tax Department of Revenue 3-21-2014 House Joint Committee of Revenue and Finance and State Government Objectives Provide committee members with some basic accounting framework

Illinois Corporate Franchise Tax Department of Revenue 3-21-2014 House Joint Committee of Revenue and Finance and State Government Objectives Provide committee members with some basic accounting framework

SAMPLE CONSTRUCTION FINANCIAL STATEMENT

SAMPLE CONSTRUCTION FINANCIAL STATEMENT Construction Contacts: Tim Klimchock, CPA, CCIFP Manager, AEC Industry Group M. Scott Hursh, CPA, CCIFP Principal, AEC Industry Group 1.800.745.8233 Web Site: www.stambaugh-ness.com

SAMPLE CONSTRUCTION FINANCIAL STATEMENT Construction Contacts: Tim Klimchock, CPA, CCIFP Manager, AEC Industry Group M. Scott Hursh, CPA, CCIFP Principal, AEC Industry Group 1.800.745.8233 Web Site: www.stambaugh-ness.com

Assurance and accounting A Guide to Financial Instruments for Private

june 2011 www.bdo.ca Assurance and accounting A Guide to Financial Instruments for Private Enterprises and Private Sector t-for-profit Organizations For many entities adopting the Accounting Standards

june 2011 www.bdo.ca Assurance and accounting A Guide to Financial Instruments for Private Enterprises and Private Sector t-for-profit Organizations For many entities adopting the Accounting Standards

ASPE AT A GLANCE Section 3856 Financial Instruments

ASPE AT A GLANCE Section 3856 Financial Instruments December 2014 Section 3856 Financial Instruments Effective Date Fiscal years beginning on or after January 1, 2011 1 SCOPE Applies to all financial instruments

ASPE AT A GLANCE Section 3856 Financial Instruments December 2014 Section 3856 Financial Instruments Effective Date Fiscal years beginning on or after January 1, 2011 1 SCOPE Applies to all financial instruments

TRUST AND AGENCY FUNDS

TRUST AND AGENCY FUNDS THE TRUST AND AGENCY FUND SECTION CONSISTS OF OVER 1,500 DIFFERENT FUNDS MAINTAINED IN THE COUNTY'S ACCOUNTING SYSTEM. THEY ARE GROUPED BELOW BY MAJOR CATEGORY FOR REPORTING PURPOSES.

TRUST AND AGENCY FUNDS THE TRUST AND AGENCY FUND SECTION CONSISTS OF OVER 1,500 DIFFERENT FUNDS MAINTAINED IN THE COUNTY'S ACCOUNTING SYSTEM. THEY ARE GROUPED BELOW BY MAJOR CATEGORY FOR REPORTING PURPOSES.

FAS 123(R) avoiding the unexpected. G. Edgar Adkins, Jr., CPA

avoiding the unexpected. G. Edgar Adkins, Jr., CPA") FAS 123(R) avoiding the unexpected G. Edgar Adkins, Jr., CPA FAS 123(R) avoiding the unexpected 2 Statement of Financial Accounting Standards No. 123 (revised 2004), Share-Based Payment (FAS 123(R)) has

FAS 123(R) avoiding the unexpected G. Edgar Adkins, Jr., CPA FAS 123(R) avoiding the unexpected 2 Statement of Financial Accounting Standards No. 123 (revised 2004), Share-Based Payment (FAS 123(R)) has

Corporations: Organization, Stock Transactions, and Dividends

C H A P T E R 11 Corporations: Organization, Stock Transactions, and Dividends Corporate Financial Accounting 13e Warren Reeve Duchac human/istock/360/getty Images Characteristics of a Corporation (slide

C H A P T E R 11 Corporations: Organization, Stock Transactions, and Dividends Corporate Financial Accounting 13e Warren Reeve Duchac human/istock/360/getty Images Characteristics of a Corporation (slide

Module 22 Liabilities and Equity

IFRS for SMEs (2009) + Q&As IFRS Foundation: Training Material for the IFRS for SMEs Module 22 Liabilities and Equity IFRS Foundation: Training Material for the IFRS for SMEs including the full text of

IFRS for SMEs (2009) + Q&As IFRS Foundation: Training Material for the IFRS for SMEs Module 22 Liabilities and Equity IFRS Foundation: Training Material for the IFRS for SMEs including the full text of

E15-1. Understanding Shareholders Equity

E15-1. Understanding Shareholders Equity Preferred stock is a class of capital stock that pays dividends at a specified rate and that has preference over common stock in the payment of dividends and the

E15-1. Understanding Shareholders Equity Preferred stock is a class of capital stock that pays dividends at a specified rate and that has preference over common stock in the payment of dividends and the

Consolidated and other financial statements

Financial reporting developments A comprehensive guide Consolidated and other financial statements Noncontrolling interests, combined financial statements, and parent company financial statements Revised

Financial reporting developments A comprehensive guide Consolidated and other financial statements Noncontrolling interests, combined financial statements, and parent company financial statements Revised

Financial Accounting Series

Financial Accounting Series NO. 263-C DECEMBER 2004 Statement of Financial Accounting Standards No. 123 (revised 2004) Share-Based Payment Financial Accounting Standards Board of the Financial Accounting

Financial Accounting Series NO. 263-C DECEMBER 2004 Statement of Financial Accounting Standards No. 123 (revised 2004) Share-Based Payment Financial Accounting Standards Board of the Financial Accounting

Classification of a financial instrument that is mandatorily convertible into a variable number of shares upon a contingent non-viability event

STAFF PAPER IFRS Interpretations Committee Meeting July 2013 Project Paper topic New item for initial consideration Classification of a financial instrument that is mandatorily convertible into a variable

STAFF PAPER IFRS Interpretations Committee Meeting July 2013 Project Paper topic New item for initial consideration Classification of a financial instrument that is mandatorily convertible into a variable

QUINSAM CAPITAL CORPORATION INTERIM FINANCIAL STATEMENTS FOR THE THIRD QUARTER ENDED SEPTEMBER 30, 2015 (UNAUDITED AND EXPRESSED IN CANADIAN DOLLARS)

") INTERIM FINANCIAL STATEMENTS FOR THE THIRD QUARTER ENDED SEPTEMBER 30, (UNAUDITED AND EXPRESSED IN CANADIAN DOLLARS) NOTICE TO READER Under National Instrument 51-102, Part 4, subsection 4.3(3) (a), if

INTERIM FINANCIAL STATEMENTS FOR THE THIRD QUARTER ENDED SEPTEMBER 30, (UNAUDITED AND EXPRESSED IN CANADIAN DOLLARS) NOTICE TO READER Under National Instrument 51-102, Part 4, subsection 4.3(3) (a), if

The Depository Trust Company

The Depository Trust Company Unaudited Condensed Consolidated Financial Statements as of March 31, 2016 and December 31, 2015 and for the three months ended March 31, 2016 and 2015 THE DEPOSITORY TRUST

The Depository Trust Company Unaudited Condensed Consolidated Financial Statements as of March 31, 2016 and December 31, 2015 and for the three months ended March 31, 2016 and 2015 THE DEPOSITORY TRUST

Capital Assistance Program. Mandatorily Convertible Preferred Stock and Warrants

Capital Assistance Program Mandatorily Convertible Preferred Stock and Warrants Summary of Mandatorily Convertible Preferred Stock ( Convertible Preferred ) Terms Issuer: Application Process: Qualifying

Capital Assistance Program Mandatorily Convertible Preferred Stock and Warrants Summary of Mandatorily Convertible Preferred Stock ( Convertible Preferred ) Terms Issuer: Application Process: Qualifying

CORNING INCORPORATED AND SUBSIDIARY COMPANIES CONSOLIDATED STATEMENTS OF OPERATIONS (Unaudited; in millions, except per share amounts)

") CONSOLIDATED STATEMENTS OF OPERATIONS (Unaudited; in millions, except per share amounts) Three months ended March 31, 2006 2005 As Restated Net sales $ 1,262 $ 1,050 Cost of sales 689 621 Gross margin

CONSOLIDATED STATEMENTS OF OPERATIONS (Unaudited; in millions, except per share amounts) Three months ended March 31, 2006 2005 As Restated Net sales $ 1,262 $ 1,050 Cost of sales 689 621 Gross margin

IFRS IN PRACTICE. Accounting for convertible notes

IFRS IN PRACTICE Accounting for convertible notes 2 IFRS IN PRACTICE - ACCOUNTING FOR CONVERTIBLE NOTES TABLE OF CONTENTS Introduction 3 The basic requirements of IFRSs 4 Example 1 Convertible note in

IFRS IN PRACTICE Accounting for convertible notes 2 IFRS IN PRACTICE - ACCOUNTING FOR CONVERTIBLE NOTES TABLE OF CONTENTS Introduction 3 The basic requirements of IFRSs 4 Example 1 Convertible note in

RECREATIONAL FACILITY REVENUE BOND FUNDS IOWA STATE UNIVERSITY OF SCIENCE AND TECHNOLOGY

RECREATIONAL FACILITY REVENUE BOND FUNDS IOWA STATE UNIVERSITY OF SCIENCE AND TECHNOLOGY INDEPENDENT AUDITOR'S REPORT BASIC FINANCIAL STATEMENTS AND SUPPLEMENTARY INFORMATION JUNE 30, 2008 0961-8021-BC04

RECREATIONAL FACILITY REVENUE BOND FUNDS IOWA STATE UNIVERSITY OF SCIENCE AND TECHNOLOGY INDEPENDENT AUDITOR'S REPORT BASIC FINANCIAL STATEMENTS AND SUPPLEMENTARY INFORMATION JUNE 30, 2008 0961-8021-BC04

HSBC FINANCE CORPORATION

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-Q (Mark One) QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the quarterly period

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-Q (Mark One) QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the quarterly period

How To Account For Financial Instruments In Australian Accounting Standard

Compiled Accounting Standard AASB 132 Financial Instruments: Presentation This compiled Standard applies to annual reporting periods beginning on or after 1 July 2007. Early application is permitted. It

Compiled Accounting Standard AASB 132 Financial Instruments: Presentation This compiled Standard applies to annual reporting periods beginning on or after 1 July 2007. Early application is permitted. It

HKAS 39 Financial Instruments: Recognition and Measurement

1 Hong Kong Financial Reporting Standards: HKAS 39 Financial Instruments: Recognition and Measurement (Relevant to PBE Paper I Financial Reporting) Lindy W W Yau, ACA, FCCA, FAIA, FCPA and Morris Y M Kwok,

1 Hong Kong Financial Reporting Standards: HKAS 39 Financial Instruments: Recognition and Measurement (Relevant to PBE Paper I Financial Reporting) Lindy W W Yau, ACA, FCCA, FAIA, FCPA and Morris Y M Kwok,

Report of Independent Auditors and Consolidated Statements of Financial Condition for. Davidson Companies and Subsidiaries

Report of Independent Auditors and Consolidated Statements of Financial Condition for Davidson Companies and Subsidiaries REPORT OF INDEPENDENT AUDITORS To the Board of Directors Davidson Companies We

Report of Independent Auditors and Consolidated Statements of Financial Condition for Davidson Companies and Subsidiaries REPORT OF INDEPENDENT AUDITORS To the Board of Directors Davidson Companies We

ILLUSTRATION 5-1 BALANCE SHEET CLASSIFICATIONS

ILLUSTRATION 5-1 BALANCE SHEET CLASSIFICATIONS MAJOR BALANCE SHEET CLASSIFICATIONS ASSETS = LIABILITIES + OWNERS' EQUITY Current Assets Long-Term Investments Current Liabilities Long-Term Debt Capital

ILLUSTRATION 5-1 BALANCE SHEET CLASSIFICATIONS MAJOR BALANCE SHEET CLASSIFICATIONS ASSETS = LIABILITIES + OWNERS' EQUITY Current Assets Long-Term Investments Current Liabilities Long-Term Debt Capital

Issuer s accounting for debt and equity financings

Financial reporting developments A comprehensive guide Issuer s accounting for debt and equity financings November 2012 To our clients and other friends The accounting for the issuance of debt and equity

Financial reporting developments A comprehensive guide Issuer s accounting for debt and equity financings November 2012 To our clients and other friends The accounting for the issuance of debt and equity

Internal Revenue Service, Treasury 1.305 5

Internal Revenue Service, Treasury 1.305 5 1.305 5 Distributions on preferred stock. (a) In general. Under section 305(b)(4), a distribution by a corporation of its stock (or rights to acquire its stock)

Internal Revenue Service, Treasury 1.305 5 1.305 5 Distributions on preferred stock. (a) In general. Under section 305(b)(4), a distribution by a corporation of its stock (or rights to acquire its stock)

CPA Canada Financial Reporting Alert

FEBRUARY 2014 CPA Canada Financial Reporting Alert ASPE AMENDED 2013 Annual Improvements to Accounting Standards for Private Enterprises In October 2013, the Accounting Standards Board ( AcSB ) made several

FEBRUARY 2014 CPA Canada Financial Reporting Alert ASPE AMENDED 2013 Annual Improvements to Accounting Standards for Private Enterprises In October 2013, the Accounting Standards Board ( AcSB ) made several

Khan Resources Inc. Interim Consolidated Balance Sheets (Expressed in United States dollars) (All dollar amounts are in thousands) (Unaudited)

(All dollar amounts are in thousands) (Unaudited)") Interim Consolidated Balance Sheets (All dollar amounts are in thousands) March 31, September 30, 2008 2007 Assets Current Cash $ 32,105 $ 33,859 Accounts receivable 52 47 Prepaid expenses and other assets

Interim Consolidated Balance Sheets (All dollar amounts are in thousands) March 31, September 30, 2008 2007 Assets Current Cash $ 32,105 $ 33,859 Accounts receivable 52 47 Prepaid expenses and other assets

Consolidated Balance Sheets

Consolidated Balance Sheets March 31 2015 2014 2015 Assets: Current assets Cash and cash equivalents 726,888 604,571 $ 6,057,400 Marketable securities 19,033 16,635 158,608 Notes and accounts receivable:

Consolidated Balance Sheets March 31 2015 2014 2015 Assets: Current assets Cash and cash equivalents 726,888 604,571 $ 6,057,400 Marketable securities 19,033 16,635 158,608 Notes and accounts receivable:

CARDIOME PHARMA CORP.

Consolidated Financial Statements (Expressed in thousands of United States (U.S.) dollars) (Prepared in accordance with generally accepted accounting principles used in the United States of America (U.S.

Consolidated Financial Statements (Expressed in thousands of United States (U.S.) dollars) (Prepared in accordance with generally accepted accounting principles used in the United States of America (U.S.

Statement of Financial Accounting Standards No. 7. Consolidated Financial Statements

Statement of Financial Accounting Standards No. 7 Statement of Financial Accounting Standards No. 7 Consolidated Financial Statements 30 November 2004 Translated by Wei-heng Lin, Associate Professor (Chung

Statement of Financial Accounting Standards No. 7 Statement of Financial Accounting Standards No. 7 Consolidated Financial Statements 30 November 2004 Translated by Wei-heng Lin, Associate Professor (Chung

Dilutive Securities. Convertible Bonds and Convertible Preferred Stock. Chapter 18 Dilutive Securities and EPS. Learning Objectives

Chapter 18 Dilutive Securities and EPS Learning Objectives Understand and account for dilutive securities Understand how to account for stock options Understand the difference between a simple and complex

Chapter 18 Dilutive Securities and EPS Learning Objectives Understand and account for dilutive securities Understand how to account for stock options Understand the difference between a simple and complex

AMAZON.COM, INC. CONSOLIDATED STATEMENTS OF CASH FLOWS (in millions)

") CONSOLIDATED STATEMENTS OF CASH FLOWS CASH AND CASH EQUIVALENTS, BEGINNING OF PERIOD $ 8,084 $ 5,269 $ 3,777 OPERATING ACTIVITIES: Net income (loss) 274 (39) 631 Adjustments to reconcile net income (loss)

CONSOLIDATED STATEMENTS OF CASH FLOWS CASH AND CASH EQUIVALENTS, BEGINNING OF PERIOD $ 8,084 $ 5,269 $ 3,777 OPERATING ACTIVITIES: Net income (loss) 274 (39) 631 Adjustments to reconcile net income (loss)

FRS 14 FINANCIAL REPORTING STANDARDS CONTENTS. Paragraph

ACCOUNTING STANDARDS BOARD OCTOBER 1998 CONTENTS SUMMARY Paragraph Objective 1 Definitions 2 Scope 3-8 Measurement: Basic earnings per share 9-26 Earnings basic 10-13 Number of shares basic 14-26 Bonus

ACCOUNTING STANDARDS BOARD OCTOBER 1998 CONTENTS SUMMARY Paragraph Objective 1 Definitions 2 Scope 3-8 Measurement: Basic earnings per share 9-26 Earnings basic 10-13 Number of shares basic 14-26 Bonus

1. The primary forms of business organization are the proprietorship, the partnership, and the corporation.

Chapter 15 Stockholders Equity: Contributed Capital LECTURE OUTLINE This material in this chapter is straight-forward and can be covered in one or two class sessions. Treasury stock transactions under

Chapter 15 Stockholders Equity: Contributed Capital LECTURE OUTLINE This material in this chapter is straight-forward and can be covered in one or two class sessions. Treasury stock transactions under

Income Measurement and Profitability Analysis

PROFITABILITY ANALYSIS The following financial statements for Spencer Company will be used to demonstrate the calculation of the various ratios in profitability analysis. Spencer Company Comparative Balance

PROFITABILITY ANALYSIS The following financial statements for Spencer Company will be used to demonstrate the calculation of the various ratios in profitability analysis. Spencer Company Comparative Balance

Accounting Aspects of Capital Structures and Stock Based Compensation

Accounting Aspects of Capital Structures and Stock Based Compensation 1 Accounting Aspects Agenda Equity Instruments Accounting for Common Stock Accounting for Preferred Stock Accounting for Debt Accounting

Accounting Aspects of Capital Structures and Stock Based Compensation 1 Accounting Aspects Agenda Equity Instruments Accounting for Common Stock Accounting for Preferred Stock Accounting for Debt Accounting

NOTES TO THE FINANCIAL STATEMENTS

NOTES TO THE FINANCIAL STATEMENTS 1 SIGNIFICANT ACCOUNTING POLICIES (a) Statement of compliance These financial statements have been prepared in accordance with all applicable Hong Kong Financial Reporting

NOTES TO THE FINANCIAL STATEMENTS 1 SIGNIFICANT ACCOUNTING POLICIES (a) Statement of compliance These financial statements have been prepared in accordance with all applicable Hong Kong Financial Reporting

Introduction 1. Executive summary 2

The KPMG Guide: FRS 139, Financial Instruments: Recognition and Measurement i Contents Introduction 1 Executive summary 2 1. Scope of FRS 139 1.1 Financial instruments outside the scope of FRS 139 3 1.2

The KPMG Guide: FRS 139, Financial Instruments: Recognition and Measurement i Contents Introduction 1 Executive summary 2 1. Scope of FRS 139 1.1 Financial instruments outside the scope of FRS 139 3 1.2

CHAPTER 20 LONG TERM FINANCE: SHARES, DEBENTURES AND TERM LOANS

CHAPTER 20 LONG TERM FINANCE: SHARES, DEBENTURES AND TERM LOANS Q.1 What is an ordinary share? How does it differ from a preference share and debenture? Explain its most important features. A.1 Ordinary

CHAPTER 20 LONG TERM FINANCE: SHARES, DEBENTURES AND TERM LOANS Q.1 What is an ordinary share? How does it differ from a preference share and debenture? Explain its most important features. A.1 Ordinary

Philippine Financial Reporting Standards (Adopted by SEC as of December 31, 2011)

") Standards (Adopted by SEC as of December 31, 2011) Philippine Financial Reporting Framework for the Preparation and Presentation of Financial Statements Conceptual Framework Phase A: Objectives and qualitative

Standards (Adopted by SEC as of December 31, 2011) Philippine Financial Reporting Framework for the Preparation and Presentation of Financial Statements Conceptual Framework Phase A: Objectives and qualitative

International Financial Reporting Standard 2

International Financial Reporting Standard 2 Share-based Payment OBJECTIVE 1 The objective of this IFRS is to specify the financial reporting by an entity when it undertakes a share-based payment transaction.

International Financial Reporting Standard 2 Share-based Payment OBJECTIVE 1 The objective of this IFRS is to specify the financial reporting by an entity when it undertakes a share-based payment transaction.

CONTENTS MMI HOLDINGS LTD ANNUAL FINANCIAL STATEMENTS 30 JUNE 2015

CONTENTS MMI HOLDINGS LTD ANNUAL FINANCIAL STATEMENTS 30 JUNE Statement of financial position 238 Income statement 238 Statement of comprehensive income 239 Statement of changes in equity 239 Statement

CONTENTS MMI HOLDINGS LTD ANNUAL FINANCIAL STATEMENTS 30 JUNE Statement of financial position 238 Income statement 238 Statement of comprehensive income 239 Statement of changes in equity 239 Statement

ACCOUNTING STANDARDS BOARD OCTOBER 1998 FRS 14 FINANCIAL REPORTING STANDARD EARNINGS ACCOUNTING STANDARDS BOARD

ACCOUNTING STANDARDS BOARD OCTOBER 1998 FRS 14 14 EARNINGS FINANCIAL REPORTING STANDARD PER SHARE ACCOUNTING STANDARDS BOARD Financial Reporting Standard 14 Earnings per Share is issued by the Accounting

ACCOUNTING STANDARDS BOARD OCTOBER 1998 FRS 14 14 EARNINGS FINANCIAL REPORTING STANDARD PER SHARE ACCOUNTING STANDARDS BOARD Financial Reporting Standard 14 Earnings per Share is issued by the Accounting

Federal Home Loan Bank of San Francisco Announces Second Quarter Operating Results

News Release Federal Home Loan Bank of San Francisco Announces Second Quarter Operating Results San Francisco, The Federal Home Loan Bank of San Francisco today announced that its net income for the second

News Release Federal Home Loan Bank of San Francisco Announces Second Quarter Operating Results San Francisco, The Federal Home Loan Bank of San Francisco today announced that its net income for the second

Vol. 1, Chapter 4 Corporate Accounting

Vol. 1, Chapter 4 Corporate Accounting Problem 1 The high and low prices for McDonald s stock over the last 52 weeks were $35.91 and $27.36 respectively. The annual cash dividend yield is 1.9% of that

Vol. 1, Chapter 4 Corporate Accounting Problem 1 The high and low prices for McDonald s stock over the last 52 weeks were $35.91 and $27.36 respectively. The annual cash dividend yield is 1.9% of that

NovaCopper Inc. (An Exploration-Stage Company) Interim Consolidated Financial Statements August 31, 2014 Unaudited (expressed in US dollars)

Interim Consolidated Financial Statements August 31, 2014 Unaudited (expressed in US dollars)") (An ExplorationStage Company) Interim Consolidated Financial Statements Unaudited (expressed in US dollars) Table of Contents Consolidated Balance Sheets...3 Consolidated Statements of Loss and Comprehensive

(An ExplorationStage Company) Interim Consolidated Financial Statements Unaudited (expressed in US dollars) Table of Contents Consolidated Balance Sheets...3 Consolidated Statements of Loss and Comprehensive

D1. This Statement supersedes APB Opinion No. 25, Accounting for Stock Issued to Employees, and the following related interpretations of Opinion 25:

Appendix D AMENDMENTS TO EXISTING PRONOUNCEMENTS D1. This Statement supersedes APB Opinion No. 25, Accounting for Stock Issued to Employees, and the following related interpretations of Opinion 25: a.

Appendix D AMENDMENTS TO EXISTING PRONOUNCEMENTS D1. This Statement supersedes APB Opinion No. 25, Accounting for Stock Issued to Employees, and the following related interpretations of Opinion 25: a.

Half - Year Financial Report January June 2015

Deutsche Bank Capital Finance Trust I (a statutory trust formed under the Delaware Statutory Trust Act with its principle place of business in New York/New York/U.S.A.) Half - Year Financial Report January

Deutsche Bank Capital Finance Trust I (a statutory trust formed under the Delaware Statutory Trust Act with its principle place of business in New York/New York/U.S.A.) Half - Year Financial Report January

Chapter 18 Shareholders Equity

PAID-IN CAPITAL Fundamental Share Rights One of the most important features of the corporate form of business is the issuance of capital stock in exchange for capital contributions. Each share of capital

PAID-IN CAPITAL Fundamental Share Rights One of the most important features of the corporate form of business is the issuance of capital stock in exchange for capital contributions. Each share of capital

GUIDE TO ACCOUNTING STANDARDS FOR PRIVATE ENTERPRISES CHAPTER 45 FINANCIAL INSTRUMENTS

GUIDE TO ACCOUNTING STANDARDS FOR PRIVATE ENTERPRISES CHAPTER 45 FINANCIAL INSTRUMENTS DISCLAIMER This publication was prepared by the Chartered Professional Accountants of Canada (CPA Canada). It has

GUIDE TO ACCOUNTING STANDARDS FOR PRIVATE ENTERPRISES CHAPTER 45 FINANCIAL INSTRUMENTS DISCLAIMER This publication was prepared by the Chartered Professional Accountants of Canada (CPA Canada). It has

Equity-Liability Accounting Debate in Worker Co-operative Entities Members Shares

Journal of Co-Operative Accounting and Reporting Equity-Liability Accounting Debate in Worker Co-operative Entities Members Shares Lorea Andicoechea Lecturer at the University of the Basque Country, Department

Journal of Co-Operative Accounting and Reporting Equity-Liability Accounting Debate in Worker Co-operative Entities Members Shares Lorea Andicoechea Lecturer at the University of the Basque Country, Department

ACC 255 FINAL EXAM REVIEW PACKET (NEW MATERIAL)

") Page 1 ACC 255 FINAL EXAM REVIEW PACKET (NEW MATERIAL) Complete these sample exam problems/objective questions and check your answers with the solutions at the end of the review file and identify where

Page 1 ACC 255 FINAL EXAM REVIEW PACKET (NEW MATERIAL) Complete these sample exam problems/objective questions and check your answers with the solutions at the end of the review file and identify where

2-8. Identify whether each of the following items increases or decreases cash flow:

Problems 2-8. Identify whether each of the following items increases or decreases cash flow: Increase in accounts receivable Increase in notes payable Depreciation expense Increase in investments Decrease

Problems 2-8. Identify whether each of the following items increases or decreases cash flow: Increase in accounts receivable Increase in notes payable Depreciation expense Increase in investments Decrease

STATUTORY BOARD SB-FRS 32 FINANCIAL REPORTING STANDARD. Financial Instruments: Presentation Illustrative Examples

STATUTORY BOARD SB-FRS 32 FINANCIAL REPORTING STANDARD Financial Instruments: Presentation Illustrative Examples CONTENTS Paragraphs ACCOUNTING FOR CONTRACTS ON EQUITY INSTRUMENTS OF AN ENTITY Example

STATUTORY BOARD SB-FRS 32 FINANCIAL REPORTING STANDARD Financial Instruments: Presentation Illustrative Examples CONTENTS Paragraphs ACCOUNTING FOR CONTRACTS ON EQUITY INSTRUMENTS OF AN ENTITY Example

STATUTORY BOARD FINANCIAL REPORTING STANDARD SB-FRS 32. Financial Instruments: Presentation Illustrative Examples

STATUTORY BOARD FINANCIAL REPORTING STANDARD SB-FRS 32 Financial Instruments: Presentation Illustrative Examples CONTENTS Paragraphs ACCOUNTING FOR CONTRACTS ON EQUITY INSTRUMENTS OF AN ENTITY Example

STATUTORY BOARD FINANCIAL REPORTING STANDARD SB-FRS 32 Financial Instruments: Presentation Illustrative Examples CONTENTS Paragraphs ACCOUNTING FOR CONTRACTS ON EQUITY INSTRUMENTS OF AN ENTITY Example

Norfolk Southern Corporation and Subsidiaries Consolidated Statements of Income (Unaudited)

") Consolidated Statements of Income Fourth Quarter Years ended December 31, 2015 2014 2015 2014 ($ in millions, except per share amounts) Railway operating revenues Coal $ 433 $ 543 $ 1,823 $ 2,382 General

Consolidated Statements of Income Fourth Quarter Years ended December 31, 2015 2014 2015 2014 ($ in millions, except per share amounts) Railway operating revenues Coal $ 433 $ 543 $ 1,823 $ 2,382 General

Buy Sell For Business Owners

ADVISOR PLANNING CONCEPTS Buy Sell For Business Owners One of the major concerns facing owners of family or closely held businesses is how to effect an orderly transfer of the business to the next generation

ADVISOR PLANNING CONCEPTS Buy Sell For Business Owners One of the major concerns facing owners of family or closely held businesses is how to effect an orderly transfer of the business to the next generation

IFrS. Disclosure checklist. July 2011. kpmg.com/ifrs

IFrS Disclosure checklist July 2011 kpmg.com/ifrs Contents What s new? 1 1. General presentation 2 1.1 Presentation of financial statements 2 1.2 Changes in equity 12 1.3 Statement of cash flows 13 1.4

IFrS Disclosure checklist July 2011 kpmg.com/ifrs Contents What s new? 1 1. General presentation 2 1.1 Presentation of financial statements 2 1.2 Changes in equity 12 1.3 Statement of cash flows 13 1.4

Practice Review. Stockholders Equity Chapter

Practice Review Stockholders Equity Chapter Use the following information to answer questions 1-3. When Sample Corporation was formed on January 1, the corporate charter provided for 50,000 shares of $20

Practice Review Stockholders Equity Chapter Use the following information to answer questions 1-3. When Sample Corporation was formed on January 1, the corporate charter provided for 50,000 shares of $20

CHAPTER 15. Stockholders Equity ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Concepts for Analysis. Brief Exercises Exercises Problems

Concepts for Analysis. Brief Exercises Exercises Problems") CHAPTER 15 Stockholders Equity ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis *1. Stockholders rights; corporate form. 1, 2, 3, 4,

CHAPTER 15 Stockholders Equity ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis *1. Stockholders rights; corporate form. 1, 2, 3, 4,

CHAPTER 14. Long-Term Liabilities 1, 10, 14, 20 2, 3, 4, 9, 10, 11 1, 2, 3, 4, 5, 6, 7 5, 6, 7, 8, 11 3, 4, 6, 7, 8, 10 12, 13 11 12, 13, 14, 15

CHAPTER 14 Long-Term Liabilities ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Long-term liability; classification; definitions.

CHAPTER 14 Long-Term Liabilities ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Long-term liability; classification; definitions.

Shin Kong Investment Trust Co., Ltd. Financial Statements for the Years Ended December 31, 2014 and 2013 and Independent Auditors Report

Shin Kong Investment Trust Co., Ltd. Financial Statements for the Years Ended, 2014 and 2013 and Independent Auditors Report INDEPENDENT AUDITORS REPORT The Board of Directors and stockholder Shin Kong

Shin Kong Investment Trust Co., Ltd. Financial Statements for the Years Ended, 2014 and 2013 and Independent Auditors Report INDEPENDENT AUDITORS REPORT The Board of Directors and stockholder Shin Kong

CHAPTER 16. Dilutive Securities and Earnings Per Share ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Concepts for Analysis

Concepts for Analysis") CHAPTER 16 Dilutive Securities and Earnings Per Share ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Convertible debt and preferred

CHAPTER 16 Dilutive Securities and Earnings Per Share ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Convertible debt and preferred

Exhibit 1. General Motors Company and Subsidiaries Supplemental Material (Unaudited)

") Exhibit 1 General Motors Company and Subsidiaries The accompanying tables and charts include earnings before interest and taxes adjusted for special items, presented net of noncontrolling interests (EBIT-adjusted)

Exhibit 1 General Motors Company and Subsidiaries The accompanying tables and charts include earnings before interest and taxes adjusted for special items, presented net of noncontrolling interests (EBIT-adjusted)

Nufarm Finance (NZ) Limited Annual Report For the year ended 31 July 2013

Limited Annual Report For the year ended 31 July 2013") Nufarm Finance (NZ) Limited Annual Report For the year ended 31 July 2013 NUFARM FINANCE (NZ) LIMITED 1 Contents 2 Directors report 3 Company directory 4 Corporate governance 5-6 Auditor s report 7 Statement

Nufarm Finance (NZ) Limited Annual Report For the year ended 31 July 2013 NUFARM FINANCE (NZ) LIMITED 1 Contents 2 Directors report 3 Company directory 4 Corporate governance 5-6 Auditor s report 7 Statement

ACCOUNTING FOR SHARE CAPITAL

CHAPTER 7 ACCOUNTING FOR SHARE CAPITAL (Share and Share Capital : Nature and types) A Company is an artificial person created by law, having separate entity with a perpetual succession and a common seal.

CHAPTER 7 ACCOUNTING FOR SHARE CAPITAL (Share and Share Capital : Nature and types) A Company is an artificial person created by law, having separate entity with a perpetual succession and a common seal.

Equity Financing. Overview

13 Equity Financing Overview After discussing debt financing in Chapter 12, we now turn to the other kind of financing available to businesses equity financing. Like debt financing, equity financing, once

13 Equity Financing Overview After discussing debt financing in Chapter 12, we now turn to the other kind of financing available to businesses equity financing. Like debt financing, equity financing, once

Accounting for ESOP. IPCC Paper 5: Advanced Accounting Chapter 4. CA. Shruthi BN, Bangalore

Accounting for ESOP IPCC Paper 5: Advanced Accounting Chapter 4 CA. Shruthi BN, Bangalore Learning Objectives 1 After studying this unit, you will be able to learn the provisions of the Companies Act,

Accounting for ESOP IPCC Paper 5: Advanced Accounting Chapter 4 CA. Shruthi BN, Bangalore Learning Objectives 1 After studying this unit, you will be able to learn the provisions of the Companies Act,

ESOPs and Executive Compensation

1 ESOPs and Executive Compensation Who Benefits and How in an ESOP Company? Michael A. Coffey Managing Vice President Corporate Capital Resources, LLC. Lisa J. Tilley, CPA Senior Management Consultant

1 ESOPs and Executive Compensation Who Benefits and How in an ESOP Company? Michael A. Coffey Managing Vice President Corporate Capital Resources, LLC. Lisa J. Tilley, CPA Senior Management Consultant

New Accounting for Business Combinations and Minority Interests

New Accounting for Business Combinations and Minority Interests John Scott Senior Manager, Enterprise Group Travis Wolff January 19, 2010 Agenda Overview and background of the new standards- ASC 805 (FAS

New Accounting for Business Combinations and Minority Interests John Scott Senior Manager, Enterprise Group Travis Wolff January 19, 2010 Agenda Overview and background of the new standards- ASC 805 (FAS

INDUSTRIAL-ALLIANCE LIFE INSURANCE COMPANY. FIRST QUARTER 2000 Consolidated Financial Statements (Non audited)

") INDUSTRIAL-ALLIANCE LIFE INSURANCE COMPANY FIRST QUARTER 2000 Consolidated Financial Statements (Non audited) March 31,2000 TABLE OF CONTENTS CONSOLIDATED INCOME 2 CONSOLIDATED CONTINUITY OF EQUITY 3 CONSOLIDATED

INDUSTRIAL-ALLIANCE LIFE INSURANCE COMPANY FIRST QUARTER 2000 Consolidated Financial Statements (Non audited) March 31,2000 TABLE OF CONTENTS CONSOLIDATED INCOME 2 CONSOLIDATED CONTINUITY OF EQUITY 3 CONSOLIDATED

The McGraw-Hill Companies, Inc., 2013 Solutions Manual, Vol.2, Chapter 19 19 1

AACSB assurance of learning standards in accounting and business education require documentation of outcomes assessment. Although schools, departments, and faculty may approach assessment and its documentation

AACSB assurance of learning standards in accounting and business education require documentation of outcomes assessment. Although schools, departments, and faculty may approach assessment and its documentation

PART III. Consolidated Financial Statements of Hitachi, Ltd. and Subsidiaries: Independent Auditors Report 47

PART III Item 17. Financial Statements Consolidated Financial Statements of Hitachi, Ltd. and Subsidiaries: Schedule: Page Number Independent Auditors Report 47 Consolidated Balance Sheets as of March

PART III Item 17. Financial Statements Consolidated Financial Statements of Hitachi, Ltd. and Subsidiaries: Schedule: Page Number Independent Auditors Report 47 Consolidated Balance Sheets as of March

Transition to International Financial Reporting Standards

Transition to International Financial Reporting Standards Topps Tiles Plc In accordance with IFRS 1, First-time adoption of International Financial Reporting Standards ( IFRS ), Topps Tiles Plc, ( Topps

Transition to International Financial Reporting Standards Topps Tiles Plc In accordance with IFRS 1, First-time adoption of International Financial Reporting Standards ( IFRS ), Topps Tiles Plc, ( Topps

S CORPORATION STOCK REDEMPTION BUY-SELL (INCLUDING DISABILITY) (INCORPORATING THE SHORT TAX YEAR TECHNIQUE)

(INCORPORATING THE SHORT TAX YEAR TECHNIQUE)") S CORPORATION STOCK REDEMPTION BUY-SELL (INCLUDING DISABILITY) (INCORPORATING THE SHORT TAX YEAR TECHNIQUE) TECHNICAL PREFACE Life Insurance proceeds received by a C Corporation to fund a Stock Redemption

S CORPORATION STOCK REDEMPTION BUY-SELL (INCLUDING DISABILITY) (INCORPORATING THE SHORT TAX YEAR TECHNIQUE) TECHNICAL PREFACE Life Insurance proceeds received by a C Corporation to fund a Stock Redemption

Samsung Life Insurance Co., Ltd. Separate Financial Statements March 31, 2013 and 2012

Separate Financial Statements Index Page(s) Report of Independent Auditors 1-2 Separate Financial Statements Statements of Financial Position 3 Statements of Comprehensive Income 4 5 Statements of Changes

Separate Financial Statements Index Page(s) Report of Independent Auditors 1-2 Separate Financial Statements Statements of Financial Position 3 Statements of Comprehensive Income 4 5 Statements of Changes

How To Classify A Share Based Payment With A Contingent Settlement Feature In Ifrs 2

IASB Agenda ref 12D(i) STAFF PAPER IASB Meeting Project Paper topic 22 25 April 2014 Narrow-scope amendments to IFRS 2 Share-based Payment Classification of share-based payments in which the manner of

IASB Agenda ref 12D(i) STAFF PAPER IASB Meeting Project Paper topic 22 25 April 2014 Narrow-scope amendments to IFRS 2 Share-based Payment Classification of share-based payments in which the manner of

KOREAN AIR LINES CO., LTD. AND SUBSIDIARIES. Consolidated Financial Statements

Consolidated Financial Statements December 31, 2015 (With Independent Auditors Report Thereon) Contents Page Independent Auditors Report 1 Consolidated Statements of Financial Position 3 Consolidated Statements

Consolidated Financial Statements December 31, 2015 (With Independent Auditors Report Thereon) Contents Page Independent Auditors Report 1 Consolidated Statements of Financial Position 3 Consolidated Statements

The Kansai Electric Power Company, Incorporated and Subsidiaries

The Kansai Electric Power Company, Incorporated and Subsidiaries Consolidated Financial Statements for the Years Ended March 31, 2003 and 2002 and for the Six Months Ended September 30, 2003 and 2002 The

The Kansai Electric Power Company, Incorporated and Subsidiaries Consolidated Financial Statements for the Years Ended March 31, 2003 and 2002 and for the Six Months Ended September 30, 2003 and 2002 The

Financial Statements

ATB INVESTMENT MANAGEMENT INC. Financial Statements Year Ended March 31, 2015 Independent Auditor s Report.... 462 Statement of Financial Position.... 464 Statement of Changes in Equity... 465 Statement

ATB INVESTMENT MANAGEMENT INC. Financial Statements Year Ended March 31, 2015 Independent Auditor s Report.... 462 Statement of Financial Position.... 464 Statement of Changes in Equity... 465 Statement

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS Japan Airlines Corporation and Consolidated Subsidiaries Japan Airlines System Corporation, the holding company of the JAL group, was renamed Japan Airlines Corporation

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS Japan Airlines Corporation and Consolidated Subsidiaries Japan Airlines System Corporation, the holding company of the JAL group, was renamed Japan Airlines Corporation