Supply Elasticity. Professor Charles Fusi

|

|

|

- Silvester Fowler

- 7 years ago

- Views:

Transcription

1 Demand and Supply Elasticity Professor Charles Fusi

2 Economists have estimated that if the price of satellite delivered TV services decreases by a certain percentage, the demand for cable TV falls by about the same percentage, but a given percentage decline in the price of cable TV causes less than half of the percentage decrease in the demand d for satellite TV. What does this tell us about how consumers perceive consumption of cable TV versus satellite TV? This chapter will help you understand this question through the concept called the cross price elasticity of demand. 6A/ 19-2

3 Price Elasticity Price Elasticity Ranges Elasticity and Total Revenues Determinants of the Price Elasticity of Demand Cross Price Elasticity of Demand Income Elasticity of Demand Price Elasticity of Supply 6A/ 19-3

4 Price Elasticity of Demand (E p ) p The responsiveness of quantity demanded of a commodity to changes in its price Defined as the percentage change in quantity demanded divided by the percentage change in price 6A/ 19-4

5 Price Elasticity of Demand (E p ) p E p = Percentage change in quantity demanded Percentage change in price 6A/ 19-5

6 Example Price of oil increases 10% Quantity demanded decreases 1% E p = 1% +10% = 0.1 0% 6A/ 19-6

7 Question How would you interpret an elasticity of 0.1? Answer A 10% increase in the price of oil will lead to a 1% decrease in quantity demanded. 6A/ 19-7

8 Relative quantities only Elasticity is measuring the change in quantity relative to the change in price Always negative An increase in price decreases the quantity demanded, ceteris paribus By convention, the minus sign is ignored 6A/ 19-8

9 Calculating Elasticity E p = change in Q sum of quantities/2 or change in P sum of prices/2 E p = in Q (Q 1 + Q 2 )/2 in P (P 1 + P 2 )/2 6A/ 19-9

/2 in P (P 1 + P 2 )/2 6A/")

10 During a recent three month period, the price of natural gas decreased from $4.81 per 1,000 cubic feet to $4.44 per 1,000 cubic feet. During this period the total quantity of natural gas consumed in the United States increased from billion cubic feet per day to billion cubic feet per day. What is the price elasticity of demand? 6A/ 19-10

11 Use the elasticity formula: $4.81 $4.44 ( )/2 ($4.81+$4.44)/2 = 0.43 $ /2 $9.25/2 = 0.09 The price elasticity of 0.09 means that a 1% increase in price generated a 0.09% decrease in the quantity of oranges demanded 6A/ 19-11

12 Elastic Demand Percentage change in quantity demanded is larger than the percentage change in price Total expenditures and price are inversely related in the elastic region of the demand curve E p > 1 6A/ 19-12

13 Unit Elasticity of Demand Percentage change in quantity demanded is equal to the percentage change in price Total expenditures are invariant to price changes in the unit elastic region of the demand curve E p = 1 6A/ 19-13

14 Inelastic Demand Percentage change in quantity demanded is smaller than the percentage change in price Total expenditures and price are directly related in the inelastic region of the demand curve E p < 1 6A/ 19-14

15 Elastic demand % change in Q > % change in P; E p > 1 Unit elastic % change in Q = % change in P; E p = 1 Inelastic demand % change in Q < % change in P; E p < 1 6A/ 19-15

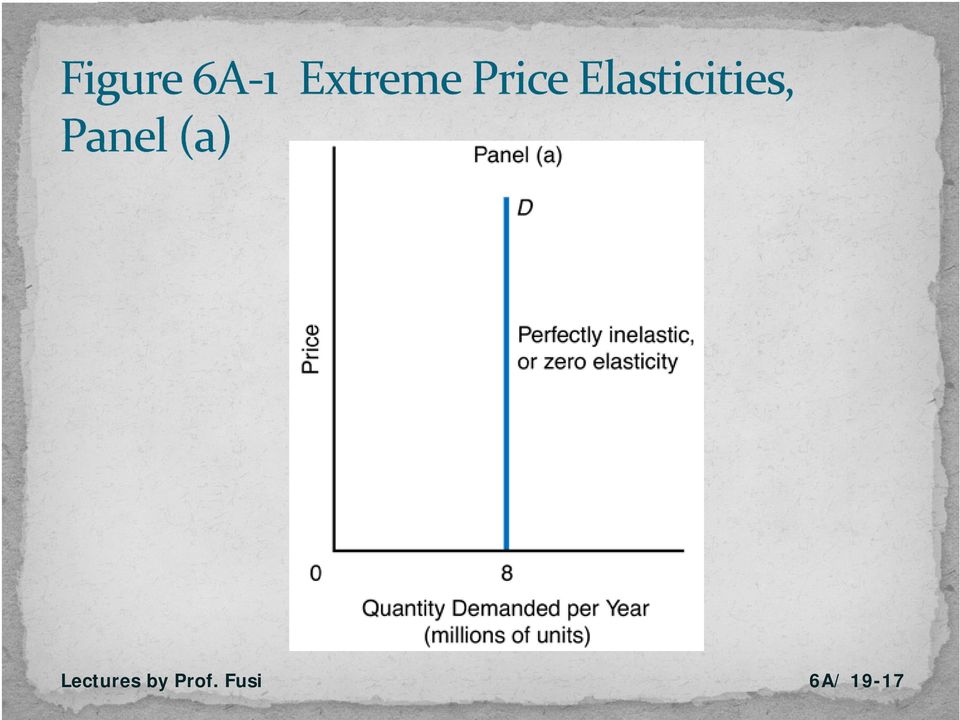

16 Extreme elasticities Perfectly Inelastic Demand A demand curve that is a vertical line It has only one quantity demanded for each price No matter what the price, quantity demanded does not change A demand that exhibits zero responsiveness to price changes 6A/ 19-16

17 6A/ 19-17

18 Extreme elasticities Perfectly Elastic Demand A demand curve that is a horizontal line It has only one price for every quantity. The slightest increase in price leads to zero quantity demanded. d d 6A/ 19-18

19 6A/ 19-19

20 When demand is elastic, a negative relationship exists between changes in price and changes in total revenues When demand is unit elastic, changes in price do not change total t revenues When demand is inelastic, a positive relationship exists between changes in price and total revenues 6A/ 19-20

21 6A/ 19-21

22 6A/ 19-22

23 6A/ 19-23

24 Elasticity revenue relationship Total revenues are the product of price times units sold. The law of demand states along a given curve, price is inverse to quantity. 6A/ 19-24

25 What happens to the product of price times quantity depends on which of the opposing forces exerts a greater force on total revenues This is what price elasticity of demand is designed to measure: responsiveness of quantity demanded to a change in price 6A/ 19-25

26 6A/ 19-26

27 Existence of substitutes The closer the substitutes and the more substitutes there are, the more elastic is demand Share of the budget The greater the share of the consumer s total budget spent on a good, the greater is the price elasticity 6A/ 19-27

28 The length of time allowed for adjustment The longer any price change persists, the greater is the elasticity of demand Price elasticity is greater in the long run than in the short run 6A/ 19-28

29 With more time for adjustment the demand curve becomes more elastic and quantity demanded falls by a greater amount In the short run, quantity demanded falls slightly 6A/ 19-29

30 Even if the market demand is inelastic, you have competitors. If you increase the price of your product, but your competitors do not raise the prices of their products, your competitors will pick off your customers. 6A/ 19-30

31 How to define the short run and the long run The short run is a time period too short for consumers to fully adjust to a price change The long run is a time period long enough for consumers to fully adjust to a change in price, other things constant 6A/ 19-31

32 Economists have found that estimated elasticities of demand are greater in the long run than in the short run. Remember that even though we are leaving off the negative sign, there is an inverse relationship between price and quantity demanded. 6A/ 19-32

33 6A/ 19-33

34 Cross Price Elasticity of Demand (E xy ) y The percentage change in the demand for one good (holding its price constant) divided by the percentage change in the price of a related good 6A/ 19-34

35 Formula for computing cross price elasticity of demand between good X and good Y E xy = xy % change in amount of good X demanded % change in price of good Y 6A/ 19-35

36 Substitutes E xy would be positive An increase in the price of X would increase the quantity of Y demanded d d at each price. Complements E xy would be negative An increase in the price of X would decrease the quantity of Y demanded at each price. 6A/ 19-36

37 Income Elasticity of Demand (E i ) i The percentage change in demand for any good, holding its price constant, divided by the percentage change in income The responsiveness of demand to changes in income, holding the good s relative price constant 6A/ 19-37

38 E i = E i Percentage change in demand Percentage change in income 6A/ 19-38

39 Calculating the income elasticity of demand E i = Change in quantity Change in income Average quantity Average income The income elasticity of demand can be either negative or positive. Remember that in calculating the income elasticity of demand, the price of the good is assumed to be constant. 6A/ 19-39

40 6A/ 19-40

41 From Table 6A 3, income elasticity of demand for Bluray discs: E i = 2/[(6+8)/2] = 2/7 $2000/[($4000+$60000)/2] 2/5 = A/ 19-41

42 During a few weeks in the depths of the Great Recession of the late 2000s, U.S. household income declined by 1 percent, while the amount of dental services that people purchased nationwide fell by 5.8 percent. Thus, the income elasticity of demand for U.S. dental services was equal to 5.8 ( 5.8%/ 1%). 6A/ 19-42

43 Price Elasticity of Supply (E s ) s The responsiveness of the quantity supplied of a commodity to a change in its price The percentage change in quantity supplied divided by the percentage change in price 6A/ 19-43

44 Formula for computing price elasticity of supply E S = Percentage change in quantity supplied Percentage change in price 6A/ 19-44

45 Classifying supply elasticities Perfectly Elastic Supply Quantity supplied falls to zero when there is the slightest decrease in price The supply curve is horizontal at a given price 6A/ 19-45

46 Classifying supply elasticities Perfectly Inelastic Supply Quantity supplied is constant no matter what happens to price The supply curve is vertical at a given price 6A/ 19-46

47 6A/ 19-47

48 Price elasticity of supply and length of time for adjustment 1. The longer the time allowed for adjustment, the more resources can flow into (out of) an industry through expansion (contraction) of existing firms. 2. The longer the time allowed for adjustment, the entry (exit) of firms increases (decreases) production in an industry. 6A/ 19-48

49 A study of prices and quantities of salmon supplied by Norwegian salmon farming firms shows that a 1 percent rise in the price of salmon induces a percentage increase in quantity supplied that is 28 times greater in the long run than that in the short run. In the long run, these firms have sufficient time to respond to a price increase by changing gvarieties and amounts of feed and capital equipment. 6A/ 19-49

50 6A/ 19-50

51 As time passes the supply curve rotates from S 1 to S 2 and quantity supplied rises to Q 1 6A/ 19-51

52 As time passes the supply curve rotates from S 1 to S 2 and quantity supplied rises to Q 1 6A/ 19-52

53 As time passes the supply curve rotates from S 1 to S 2 and quantity supplied rises to Q 1 As more time passes the supply curve rotates from S 2 to S 3 and quantity supplied rises from Q 1 to Q 2 6A/ 19-53

54 As time passes the supply curve rotates from S 1 to S 2 and quantity supplied rises to Q 1 As more time passes the supply curve rotates from S 2 to S 3 and quantity supplied rises from Q 1 to Q 2 6A/ 19-54

55 While most industry observers anticipated that a basic ipad would be priced at $1,000, Apple set its initial i i price at only $499 in Apple learned a lesson from its experience with the iphone in mid 2007: the estimated price elasticity of demand for smart cellphones like the iphone was about 1.4. The company set this lower price in anticipation that the demand for the new gadget would also be elastic, so a lower price would ultimately yield higher revenues. 6A/ 19-55

56 Researchers Austan Goolsbee and Amil Petrin estimated that the price elasticity of demand was elastic for cable TV and satellite TV. They also found that their cross price elasticities were positive, so they are substitutes. The cross price elasticities also suggest that consumers of satellite TV perceive cable TV to be less substitutable for satellite TV services than do cable TV consumers. 6A/ 19-56

57 Expressing and calculating the price elasticity of demand Percentage change in quantity demanded divided by the percentage change in price 6A/ 19-57

58 The relationship between the price elasticity of demand and total revenues When demand is elastic, price and total revenue are inversely related When demand is inelastic, price and total revenue are positively related When demand is unit elastic, total revenue does not change when price changes 6A/ 19-58

59 Factors that determine price elasticity of demand Availability of substitutes Percentage of a person s s budget spent on the good The length of time allowed for adjustment to a price change 6A/ 19-59

60 The cross price elasticity of demand and using it to determine whether two goods are substitutes or complements Percentage change in the demand d for one good divided d d by the percentage change in the price of a related good If cross elasticity is positive, the goods are substitutes. If cross elasticity is negative, the goods are complements. 6A/ 19-60

61 Income elasticity of demand Responsiveness of the demand for the good to a change in income Percentage change in the demand for a good divided by the percentage change in income. 6A/ 19-61

62 Classifying supply elasticities and how the length of time for adjustment affects price elasticity i of supply Elastic supply: price elasticity of supply is greater than 1 Inelastic supply: price elasticity i of supply is less than 1 Unit elastic supply: price elasticity of supply is equal to 1 The longer the time period for adjustment, t the more elastic is supply. 6A/ 19-62

Demand and Supply Elasticity

19 Demand and Supply Elasticity When the price of one type of television delivery service falls, people tend to switch in favor of buying that form of TV service and substitute away from alternative TV

19 Demand and Supply Elasticity When the price of one type of television delivery service falls, people tend to switch in favor of buying that form of TV service and substitute away from alternative TV

Chapter 6. Elasticity: The Responsiveness of Demand and Supply

Chapter 6. Elasticity: The Responsiveness of Demand and Supply Instructor: JINKOOK LEE Department of Economics / Texas A&M University ECON 202 504 Principles of Microeconomics Elasticity Demand curve:

Chapter 6. Elasticity: The Responsiveness of Demand and Supply Instructor: JINKOOK LEE Department of Economics / Texas A&M University ECON 202 504 Principles of Microeconomics Elasticity Demand curve:

Elasticity: The Responsiveness of Demand and Supply

Chapter 6 Elasticity: The Responsiveness of Demand and Supply Chapter Outline 61 LEARNING OBJECTIVE 61 The Price Elasticity of Demand and Its Measurement Learning Objective 1 Define the price elasticity

Chapter 6 Elasticity: The Responsiveness of Demand and Supply Chapter Outline 61 LEARNING OBJECTIVE 61 The Price Elasticity of Demand and Its Measurement Learning Objective 1 Define the price elasticity

Elasticity. Definition of the Price Elasticity of Demand: Formula for Elasticity: Types of Elasticity:

Elasticity efinition of the Elasticity of emand: The law of demand states that the quantity demanded of a good will vary inversely with the price of the good during a given time period, but it does not

Elasticity efinition of the Elasticity of emand: The law of demand states that the quantity demanded of a good will vary inversely with the price of the good during a given time period, but it does not

Elasticity. I. What is Elasticity?

Elasticity I. What is Elasticity? The purpose of this section is to develop some general rules about elasticity, which may them be applied to the four different specific types of elasticity discussed in

Elasticity I. What is Elasticity? The purpose of this section is to develop some general rules about elasticity, which may them be applied to the four different specific types of elasticity discussed in

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

Chapter 11 Perfect Competition - Sample Questions MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) Perfect competition is an industry with A) a

Chapter 11 Perfect Competition - Sample Questions MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) Perfect competition is an industry with A) a

Chapter 5 Elasticity of Demand and Supply. These slides supplement the textbook, but should not replace reading the textbook

Chapter 5 Elasticity of Demand and Supply These slides supplement the textbook, but should not replace reading the textbook 1 What is total revenue? Price multiplied by the quantity sold at that price

Chapter 5 Elasticity of Demand and Supply These slides supplement the textbook, but should not replace reading the textbook 1 What is total revenue? Price multiplied by the quantity sold at that price

Elasticity. Ratio of Percentage Changes. Elasticity and Its Application. Price Elasticity of Demand. Price Elasticity of Demand. Elasticity...

Elasticity and Its Application Chapter 5 All rights reserved. Copyright 21 by Harcourt, Inc. Requests for permission to make copies of any part of the work should be mailed to: Permissions Department,

Elasticity and Its Application Chapter 5 All rights reserved. Copyright 21 by Harcourt, Inc. Requests for permission to make copies of any part of the work should be mailed to: Permissions Department,

Principles of Economics: Micro: Exam #2: Chapters 1-10 Page 1 of 9

Principles of Economics: Micro: Exam #2: Chapters 1-10 Page 1 of 9 print name on the line above as your signature INSTRUCTIONS: 1. This Exam #2 must be completed within the allocated time (i.e., between

Principles of Economics: Micro: Exam #2: Chapters 1-10 Page 1 of 9 print name on the line above as your signature INSTRUCTIONS: 1. This Exam #2 must be completed within the allocated time (i.e., between

http://ezto.mhecloud.mcgraw-hill.com/hm.tpx

Page 1 of 17 1. Assume the price elasticity of demand for U.S. Frisbee Co. Frisbees is 0.5. If the company increases the price of each Frisbee from $12 to $16, the number of Frisbees demanded will Decrease

Page 1 of 17 1. Assume the price elasticity of demand for U.S. Frisbee Co. Frisbees is 0.5. If the company increases the price of each Frisbee from $12 to $16, the number of Frisbees demanded will Decrease

Elasticities of Demand

rice Elasticity of Demand 4.0 rinciples of Microeconomics, Fall 007 Chia-Hui Chen September 0, 007 Lecture 3 Elasticities of Demand Elasticity. Elasticity measures how one variable responds to a change

rice Elasticity of Demand 4.0 rinciples of Microeconomics, Fall 007 Chia-Hui Chen September 0, 007 Lecture 3 Elasticities of Demand Elasticity. Elasticity measures how one variable responds to a change

2011 Pearson Education. Elasticities of Demand and Supply: Today add elasticity and slope, cross elasticities

2011 Pearson Education Elasticities of Demand and Supply: Today add elasticity and slope, cross elasticities What Determines Elasticity? Influences on the price elasticity of demand fall into two categories:

2011 Pearson Education Elasticities of Demand and Supply: Today add elasticity and slope, cross elasticities What Determines Elasticity? Influences on the price elasticity of demand fall into two categories:

Elasticities of Demand and Supply

1 CHAPTER CHECKLIST Elasticities of Demand and Supply Chapter 5 1. Define, explain the factors that influence, and calculate the price elasticity of demand. 2. Define, explain the factors that influence,

1 CHAPTER CHECKLIST Elasticities of Demand and Supply Chapter 5 1. Define, explain the factors that influence, and calculate the price elasticity of demand. 2. Define, explain the factors that influence,

a. Meaning: The amount (as a percentage of total) that quantity demanded changes as price changes. b. Factors that make demand more price elastic

that quantity demanded changes as price changes. b. Factors that make demand more price elastic") Things to know about elasticity. 1. Price elasticity of demand a. Meaning: The amount (as a percentage of total) that quantity demanded changes as price changes. b. Factors that make demand more price

Things to know about elasticity. 1. Price elasticity of demand a. Meaning: The amount (as a percentage of total) that quantity demanded changes as price changes. b. Factors that make demand more price

OVERVIEW. 2. If demand is vertical, demand is perfectly inelastic. Every change in price brings no change in quantity.

7 PRICE ELASTICITY OVERVIEW 1. The elasticity of demand measures the responsiveness of 1 the buyer to a change in price. The coefficient of price elasticity is the percentage change in quantity divided

7 PRICE ELASTICITY OVERVIEW 1. The elasticity of demand measures the responsiveness of 1 the buyer to a change in price. The coefficient of price elasticity is the percentage change in quantity divided

Consumers face constraints on their choices because they have limited incomes.

Consumer Choice: the Demand Side of the Market Consumers face constraints on their choices because they have limited incomes. Wealthy and poor individuals have limited budgets relative to their desires.

Consumer Choice: the Demand Side of the Market Consumers face constraints on their choices because they have limited incomes. Wealthy and poor individuals have limited budgets relative to their desires.

Practice Questions Week 3 Day 1

Practice Questions Week 3 Day 1 Figure 4-1 Quantity Demanded $ 2 18 3 $ 4 14 4 $ 6 10 5 $ 8 6 6 $10 2 8 Price Per Pair Quantity Supplied 1. Figure 4-1 shows the supply and demand for socks. If a price

Practice Questions Week 3 Day 1 Figure 4-1 Quantity Demanded $ 2 18 3 $ 4 14 4 $ 6 10 5 $ 8 6 6 $10 2 8 Price Per Pair Quantity Supplied 1. Figure 4-1 shows the supply and demand for socks. If a price

ECON 103, 2008-2 ANSWERS TO HOME WORK ASSIGNMENTS

ECON 103, 2008-2 ANSWERS TO HOME WORK ASSIGNMENTS Due the Week of June 23 Chapter 8 WRITE [4] Use the demand schedule that follows to calculate total revenue and marginal revenue at each quantity. Plot

ECON 103, 2008-2 ANSWERS TO HOME WORK ASSIGNMENTS Due the Week of June 23 Chapter 8 WRITE [4] Use the demand schedule that follows to calculate total revenue and marginal revenue at each quantity. Plot

The formula to measure the rice elastici coefficient is Percentage change in quantity demanded E= Percentage change in price

a CHAPTER 6: ELASTICITY, CONSUMER SURPLUS, AND PRODUCER SURPLUS Introduction Consumer responses to changes in prices, incomes, and prices of related products can be explained by the concept of elasticity.

a CHAPTER 6: ELASTICITY, CONSUMER SURPLUS, AND PRODUCER SURPLUS Introduction Consumer responses to changes in prices, incomes, and prices of related products can be explained by the concept of elasticity.

Chapter 4 Elasticities of demand and supply. The price elasticity of demand

Chapter 4 Elasticities of demand and supply The price elasticity of demand measures the sensitivity of the quantity demanded of a good to a change in its price It is defined as: % change in quantity demanded

Chapter 4 Elasticities of demand and supply The price elasticity of demand measures the sensitivity of the quantity demanded of a good to a change in its price It is defined as: % change in quantity demanded

Elasticity. Demand is inelastic if it does not respond much to price changes, and elastic if demand changes a lot when the price changes.

Elasticity The price elasticity of demand measures the sensitivity of the quantity demanded to changes in the price. Demand is inelastic if it does not respond much to price changes, and elastic if demand

Elasticity The price elasticity of demand measures the sensitivity of the quantity demanded to changes in the price. Demand is inelastic if it does not respond much to price changes, and elastic if demand

Elasticity and Its Application

Elasticity and Its Application Chapter 5 All rights reserved. Copyright 2001 by Harcourt, Inc. Requests for permission to make copies of any part of the work should be mailed to: Permissions Department,

Elasticity and Its Application Chapter 5 All rights reserved. Copyright 2001 by Harcourt, Inc. Requests for permission to make copies of any part of the work should be mailed to: Permissions Department,

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

MBA 640 Survey of Microeconomics Fall 2006, Quiz 6 Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) A monopoly is best defined as a firm that

MBA 640 Survey of Microeconomics Fall 2006, Quiz 6 Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) A monopoly is best defined as a firm that

11 PERFECT COMPETITION. Chapter. Competition

Chapter 11 PERFECT COMPETITION Competition Topic: Perfect Competition 1) Perfect competition is an industry with A) a few firms producing identical goods B) a few firms producing goods that differ somewhat

Chapter 11 PERFECT COMPETITION Competition Topic: Perfect Competition 1) Perfect competition is an industry with A) a few firms producing identical goods B) a few firms producing goods that differ somewhat

Economics 100 Exam 2

Name: 1. During the long run: Economics 100 Exam 2 A. Output is limited because of the law of diminishing returns B. The scale of operations cannot be changed C. The firm must decide how to use the current

Name: 1. During the long run: Economics 100 Exam 2 A. Output is limited because of the law of diminishing returns B. The scale of operations cannot be changed C. The firm must decide how to use the current

17. If a good is normal, then the Engel curve A. Slopes upward B. Slopes downward C. Is vertical D. Is horizontal

Sample Exam 1 1. Suppose that when the price of hot dogs is $2 per package, there is a demand for 10,000 bags of hot dog buns. When the price of hot dogs is $3 per package, the demand for hot dog buns

Sample Exam 1 1. Suppose that when the price of hot dogs is $2 per package, there is a demand for 10,000 bags of hot dog buns. When the price of hot dogs is $3 per package, the demand for hot dog buns

Chapter 3 Quantitative Demand Analysis

Managerial Economics & Business Strategy Chapter 3 uantitative Demand Analysis McGraw-Hill/Irwin Copyright 2010 by the McGraw-Hill Companies, Inc. All rights reserved. Overview I. The Elasticity Concept

Managerial Economics & Business Strategy Chapter 3 uantitative Demand Analysis McGraw-Hill/Irwin Copyright 2010 by the McGraw-Hill Companies, Inc. All rights reserved. Overview I. The Elasticity Concept

4 THE MARKET FORCES OF SUPPLY AND DEMAND

4 THE MARKET FORCES OF SUPPLY AND DEMAND IN THIS CHAPTER YOU WILL Learn what a competitive market is Examine what determines the demand for a good in a competitive market Chapter Overview Examine what

4 THE MARKET FORCES OF SUPPLY AND DEMAND IN THIS CHAPTER YOU WILL Learn what a competitive market is Examine what determines the demand for a good in a competitive market Chapter Overview Examine what

Pre Test Chapter 3. 8.. DVD players and DVDs are: A. complementary goods. B. substitute goods. C. independent goods. D. inferior goods.

1. Graphically, the market demand curve is: A. steeper than any individual demand curve that is part of it. B. greater than the sum of the individual demand curves. C. the horizontal sum of individual

1. Graphically, the market demand curve is: A. steeper than any individual demand curve that is part of it. B. greater than the sum of the individual demand curves. C. the horizontal sum of individual

Pre-Test Chapter 18 ed17

Pre-Test Chapter 18 ed17 Multiple Choice Questions 1. (Consider This) Elastic demand is analogous to a and inelastic demand to a. A. normal wrench; socket wrench B. Ace bandage; firm rubber tie-down C.

Pre-Test Chapter 18 ed17 Multiple Choice Questions 1. (Consider This) Elastic demand is analogous to a and inelastic demand to a. A. normal wrench; socket wrench B. Ace bandage; firm rubber tie-down C.

An increase in the number of students attending college. shifts to the left. An increase in the wage rate of refinery workers.

1. Which of the following would shift the demand curve for new textbooks to the right? a. A fall in the price of paper used in publishing texts. b. A fall in the price of equivalent used text books. c.

1. Which of the following would shift the demand curve for new textbooks to the right? a. A fall in the price of paper used in publishing texts. b. A fall in the price of equivalent used text books. c.

Economics 326: Duality and the Slutsky Decomposition. Ethan Kaplan

Economics 326: Duality and the Slutsky Decomposition Ethan Kaplan September 19, 2011 Outline 1. Convexity and Declining MRS 2. Duality and Hicksian Demand 3. Slutsky Decomposition 4. Net and Gross Substitutes

Economics 326: Duality and the Slutsky Decomposition Ethan Kaplan September 19, 2011 Outline 1. Convexity and Declining MRS 2. Duality and Hicksian Demand 3. Slutsky Decomposition 4. Net and Gross Substitutes

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) The law of demand states that, other things remaining the same, the lower the price of a good,

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) The law of demand states that, other things remaining the same, the lower the price of a good,

SUPPLY AND DEMAND : HOW MARKETS WORK

SUPPLY AND DEMAND : HOW MARKETS WORK Chapter 4 : The Market Forces of and and demand are the two words that economists use most often. and demand are the forces that make market economies work. Modern

SUPPLY AND DEMAND : HOW MARKETS WORK Chapter 4 : The Market Forces of and and demand are the two words that economists use most often. and demand are the forces that make market economies work. Modern

Chapter 03 The Concept of Elasticity and Consumer and

Chapter 03 The Concept of Elasticity and Consumer and Multiple Choice Questions Use the following Figure 3.1 to answer questions 1-4: Figure 3.1 1. In Figure 3.1, if demand is considered perfectly elastic,

Chapter 03 The Concept of Elasticity and Consumer and Multiple Choice Questions Use the following Figure 3.1 to answer questions 1-4: Figure 3.1 1. In Figure 3.1, if demand is considered perfectly elastic,

Profit Maximization. 2. product homogeneity

Perfectly Competitive Markets It is essentially a market in which there is enough competition that it doesn t make sense to identify your rivals. There are so many competitors that you cannot single out

Perfectly Competitive Markets It is essentially a market in which there is enough competition that it doesn t make sense to identify your rivals. There are so many competitors that you cannot single out

The Free Market Approach. The Health Care Market. Sellers of Health Care. The Free Market Approach. Real Income

The Health Care Market Who are the buyers and sellers? Everyone is a potential buyer (consumer) of health care At any moment a buyer would be anybody who is ill or wanted preventive treatment such as a

The Health Care Market Who are the buyers and sellers? Everyone is a potential buyer (consumer) of health care At any moment a buyer would be anybody who is ill or wanted preventive treatment such as a

POTENTIAL OUTPUT and LONG RUN AGGREGATE SUPPLY

POTENTIAL OUTPUT and LONG RUN AGGREGATE SUPPLY Aggregate Supply represents the ability of an economy to produce goods and services. In the Long-run this ability to produce is based on the level of production

POTENTIAL OUTPUT and LONG RUN AGGREGATE SUPPLY Aggregate Supply represents the ability of an economy to produce goods and services. In the Long-run this ability to produce is based on the level of production

Introduction to microeconomics

RELEVANT TO ACCA QUALIFICATION PAPER F1 / FOUNDATIONS IN ACCOUNTANCY PAPER FAB Introduction to microeconomics The new Paper F1/FAB, Accountant in Business carried over many subjects from its Paper F1 predecessor,

RELEVANT TO ACCA QUALIFICATION PAPER F1 / FOUNDATIONS IN ACCOUNTANCY PAPER FAB Introduction to microeconomics The new Paper F1/FAB, Accountant in Business carried over many subjects from its Paper F1 predecessor,

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

Chapter 4 - Elasticity - Sample Questions MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) The slope of a demand curve depends on A) the units used

Chapter 4 - Elasticity - Sample Questions MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) The slope of a demand curve depends on A) the units used

Chapter 9: Perfect Competition

Chapter 9: Perfect Competition Perfect Competition Law of One Price Short-Run Equilibrium Long-Run Equilibrium Maximize Profit Market Equilibrium Constant- Cost Industry Increasing- Cost Industry Decreasing-

Chapter 9: Perfect Competition Perfect Competition Law of One Price Short-Run Equilibrium Long-Run Equilibrium Maximize Profit Market Equilibrium Constant- Cost Industry Increasing- Cost Industry Decreasing-

Managerial Economics

Managerial Economics Unit 1: Demand Theory Rudolf Winter-Ebmer Johannes Kepler University Linz Winter Term 2012/13 Winter-Ebmer, Managerial Economics: Unit 1 - Demand Theory 1 / 54 OBJECTIVES Explain the

Managerial Economics Unit 1: Demand Theory Rudolf Winter-Ebmer Johannes Kepler University Linz Winter Term 2012/13 Winter-Ebmer, Managerial Economics: Unit 1 - Demand Theory 1 / 54 OBJECTIVES Explain the

Demand and Consumer Behavior emand is a model of consumer behavior. It attempts to identify the factors

R. Larry Reynolds Demand and Consumer Behavior R. Larry Reynolds (005) Demand and Consumer Behavior emand is a model of consumer behavior. It attempts to identify the factors D that influence the choices

R. Larry Reynolds Demand and Consumer Behavior R. Larry Reynolds (005) Demand and Consumer Behavior emand is a model of consumer behavior. It attempts to identify the factors D that influence the choices

3. CONCEPT OF ELASTICITY

3. CONCET OF ELASTICIT The quantity demanded of a good is affected mainly by - changes in the price of a good, - changes in price of other goods, - changes in income and c - changes in other relevant factors.

3. CONCET OF ELASTICIT The quantity demanded of a good is affected mainly by - changes in the price of a good, - changes in price of other goods, - changes in income and c - changes in other relevant factors.

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

Chap 13 Monopolistic Competition and Oligopoly These questions may include topics that were not covered in class and may not be on the exam. MULTIPLE CHOICE. Choose the one alternative that best completes

Chap 13 Monopolistic Competition and Oligopoly These questions may include topics that were not covered in class and may not be on the exam. MULTIPLE CHOICE. Choose the one alternative that best completes

Demand, Supply and Elasticity

Demand, Supply and Elasticity CHAPTER 2 OUTLINE 2.1 Demand and Supply Definitions, Determinants and Disturbances 2.2 The Market Mechanism 2.3 Changes in Market Equilibrium 2.4 Elasticities of Supply and

Demand, Supply and Elasticity CHAPTER 2 OUTLINE 2.1 Demand and Supply Definitions, Determinants and Disturbances 2.2 The Market Mechanism 2.3 Changes in Market Equilibrium 2.4 Elasticities of Supply and

AP Microeconomics Chapter 12 Outline

I. Learning Objectives In this chapter students will learn: A. The significance of resource pricing. B. How the marginal revenue productivity of a resource relates to a firm s demand for that resource.

I. Learning Objectives In this chapter students will learn: A. The significance of resource pricing. B. How the marginal revenue productivity of a resource relates to a firm s demand for that resource.

Monopolistic Competition

In this chapter, look for the answers to these questions: How is similar to perfect? How is it similar to monopoly? How do ally competitive firms choose price and? Do they earn economic profit? In what

In this chapter, look for the answers to these questions: How is similar to perfect? How is it similar to monopoly? How do ally competitive firms choose price and? Do they earn economic profit? In what

Chapter 3 Market Demand, Supply, and Elasticity

Chapter 3 Market Demand, Supply, and Elasticity After reading chapter 3, MARKET DEMAND, SUPPLY, AND ELASTICITY, you should be able to: Discuss the Law of Demand and draw a Demand Curve. Distinguish between

Chapter 3 Market Demand, Supply, and Elasticity After reading chapter 3, MARKET DEMAND, SUPPLY, AND ELASTICITY, you should be able to: Discuss the Law of Demand and draw a Demand Curve. Distinguish between

Pre-Test Chapter 8 ed17

Pre-Test Chapter 8 ed17 Multiple Choice Questions 1. The APC can be defined as the fraction of a: A. change in income that is not spent. B. change in income that is spent. C. specific level of total income

Pre-Test Chapter 8 ed17 Multiple Choice Questions 1. The APC can be defined as the fraction of a: A. change in income that is not spent. B. change in income that is spent. C. specific level of total income

Figure 4-1 Price Quantity Quantity Per Pair Demanded Supplied $ 2 18 3 $ 4 14 4 $ 6 10 5 $ 8 6 6 $10 2 8

Econ 101 Summer 2005 In-class Assignment 2 & HW3 MULTIPLE CHOICE 1. A government-imposed price ceiling set below the market's equilibrium price for a good will produce an excess supply of the good. a.

Econ 101 Summer 2005 In-class Assignment 2 & HW3 MULTIPLE CHOICE 1. A government-imposed price ceiling set below the market's equilibrium price for a good will produce an excess supply of the good. a.

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question on the accompanying scantron.

Principles of Microeconomics, Quiz #5 Fall 2007 Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question on the accompanying scantron. 1) Perfect competition

Principles of Microeconomics, Quiz #5 Fall 2007 Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question on the accompanying scantron. 1) Perfect competition

Review of Fundamental Mathematics

Review of Fundamental Mathematics As explained in the Preface and in Chapter 1 of your textbook, managerial economics applies microeconomic theory to business decision making. The decision-making tools

Review of Fundamental Mathematics As explained in the Preface and in Chapter 1 of your textbook, managerial economics applies microeconomic theory to business decision making. The decision-making tools

Price Elasticity of Demand MATH 104 and MATH 184 Mark Mac Lean (with assistance from Patrick Chan) 2011W

2011W") Price Elasticity of Demand MATH 104 and MATH 184 Mark Mac Lean (with assistance from Patrick Chan) 2011W The rice elasticity of demand (which is often shortened to demand elasticity) is defined to be the

Price Elasticity of Demand MATH 104 and MATH 184 Mark Mac Lean (with assistance from Patrick Chan) 2011W The rice elasticity of demand (which is often shortened to demand elasticity) is defined to be the

Appendix B. Making Smart Choices

Appendix B Making Smart Choices Making Smart Choices The Law of Demand LEARNING OBJECTIVES B.1 Describe what determines your willingness to pay for a product/service B.2 Choice depends on marginal benefit,

Appendix B Making Smart Choices Making Smart Choices The Law of Demand LEARNING OBJECTIVES B.1 Describe what determines your willingness to pay for a product/service B.2 Choice depends on marginal benefit,

MICROECONOMIC PRINCIPLES SPRING 2001 MIDTERM ONE -- Answers. February 16, 2001. Table One Labor Hours Needed to Make 1 Pounds Produced in 20 Hours

MICROECONOMIC PRINCIPLES SPRING 1 MIDTERM ONE -- Answers February 1, 1 Multiple Choice. ( points each) Circle the correct response and write one or two sentences to explain your choice. Use graphs as appropriate.

MICROECONOMIC PRINCIPLES SPRING 1 MIDTERM ONE -- Answers February 1, 1 Multiple Choice. ( points each) Circle the correct response and write one or two sentences to explain your choice. Use graphs as appropriate.

Chapter. Perfect Competition CHAPTER IN PERSPECTIVE

Perfect Competition Chapter 10 CHAPTER IN PERSPECTIVE In Chapter 10 we study perfect competition, the market that arises when the demand for a product is large relative to the output of a single producer.

Perfect Competition Chapter 10 CHAPTER IN PERSPECTIVE In Chapter 10 we study perfect competition, the market that arises when the demand for a product is large relative to the output of a single producer.

Chapter 6 Competitive Markets

Chapter 6 Competitive Markets After reading Chapter 6, COMPETITIVE MARKETS, you should be able to: List and explain the characteristics of Perfect Competition and Monopolistic Competition Explain why a

Chapter 6 Competitive Markets After reading Chapter 6, COMPETITIVE MARKETS, you should be able to: List and explain the characteristics of Perfect Competition and Monopolistic Competition Explain why a

CHAPTER 10 MARKET POWER: MONOPOLY AND MONOPSONY

CHAPTER 10 MARKET POWER: MONOPOLY AND MONOPSONY EXERCISES 3. A monopolist firm faces a demand with constant elasticity of -.0. It has a constant marginal cost of $0 per unit and sets a price to maximize

CHAPTER 10 MARKET POWER: MONOPOLY AND MONOPSONY EXERCISES 3. A monopolist firm faces a demand with constant elasticity of -.0. It has a constant marginal cost of $0 per unit and sets a price to maximize

1. If the price elasticity of demand for a good is.75, the demand for the good can be described as: A) normal. B) elastic. C) inferior. D) inelastic.

normal. B) elastic. C) inferior. D) inelastic.") Chapter 20: Demand and Supply: Elasticities and Applications Extra Multiple Choice Questions for Review 1. If the price elasticity of demand for a good is.75, the demand for the good can be described as:

Chapter 20: Demand and Supply: Elasticities and Applications Extra Multiple Choice Questions for Review 1. If the price elasticity of demand for a good is.75, the demand for the good can be described as:

CHAPTER 4 ELASTICITY

CHAPTER 4 ELASTICITY Chapter in a Nutshell When economists use the word elasticity, they mean sensitivity. Price elasticity of demand is a measure of buyers sensitivity to price changes. The elasticity

CHAPTER 4 ELASTICITY Chapter in a Nutshell When economists use the word elasticity, they mean sensitivity. Price elasticity of demand is a measure of buyers sensitivity to price changes. The elasticity

I. Introduction to Taxation

University of Pacific-Economics 53 Lecture Notes #17 I. Introduction to Taxation Government plays an important role in most modern economies. In the United States, the role of the government extends from

University of Pacific-Economics 53 Lecture Notes #17 I. Introduction to Taxation Government plays an important role in most modern economies. In the United States, the role of the government extends from

Experiment 8: Entry and Equilibrium Dynamics

Experiment 8: Entry and Equilibrium Dynamics Everyone is a demander of a meal. There are approximately equal numbers of values at 24, 18, 12 and 8. These will change, due to a random development, after

Experiment 8: Entry and Equilibrium Dynamics Everyone is a demander of a meal. There are approximately equal numbers of values at 24, 18, 12 and 8. These will change, due to a random development, after

Chapter 3. The Concept of Elasticity and Consumer and Producer Surplus. Chapter Objectives. Chapter Outline

Chapter 3 The Concept of Elasticity and Consumer and roducer Surplus Chapter Objectives After reading this chapter you should be able to Understand that elasticity, the responsiveness of quantity to changes

Chapter 3 The Concept of Elasticity and Consumer and roducer Surplus Chapter Objectives After reading this chapter you should be able to Understand that elasticity, the responsiveness of quantity to changes

N. Gregory Mankiw Principles of Economics. Chapter 15. MONOPOLY

N. Gregory Mankiw Principles of Economics Chapter 15. MONOPOLY Solutions to Problems and Applications 1. The following table shows revenue, costs, and profits, where quantities are in thousands, and total

N. Gregory Mankiw Principles of Economics Chapter 15. MONOPOLY Solutions to Problems and Applications 1. The following table shows revenue, costs, and profits, where quantities are in thousands, and total

Supply and Demand Fundamental tool of economic analysis Used to discuss unemployment, value of $, protection of the environment, etc.

Supply and emand Fundamental tool of economic analysis Used to discuss unemployment, value of $, protection of the environment, etc. Chapter Outline: (a) emand is the consumer side of the market. (b) Supply

Supply and emand Fundamental tool of economic analysis Used to discuss unemployment, value of $, protection of the environment, etc. Chapter Outline: (a) emand is the consumer side of the market. (b) Supply

Chapter 3 Consumer Behavior

Chapter 3 Consumer Behavior Read Pindyck and Rubinfeld (2013), Chapter 3 Microeconomics, 8 h Edition by R.S. Pindyck and D.L. Rubinfeld Adapted by Chairat Aemkulwat for Econ I: 2900111 1/29/2015 CHAPTER

Chapter 3 Consumer Behavior Read Pindyck and Rubinfeld (2013), Chapter 3 Microeconomics, 8 h Edition by R.S. Pindyck and D.L. Rubinfeld Adapted by Chairat Aemkulwat for Econ I: 2900111 1/29/2015 CHAPTER

Managerial Economics & Business Strategy Chapter 8. Managing in Competitive, Monopolistic, and Monopolistically Competitive Markets

Managerial Economics & Business Strategy Chapter 8 Managing in Competitive, Monopolistic, and Monopolistically Competitive Markets I. Perfect Competition Overview Characteristics and profit outlook. Effect

Managerial Economics & Business Strategy Chapter 8 Managing in Competitive, Monopolistic, and Monopolistically Competitive Markets I. Perfect Competition Overview Characteristics and profit outlook. Effect

CHAPTER 7: AGGREGATE DEMAND AND AGGREGATE SUPPLY

CHAPTER 7: AGGREGATE DEMAND AND AGGREGATE SUPPLY Learning goals of this chapter: What forces bring persistent and rapid expansion of real GDP? What causes inflation? Why do we have business cycles? How

CHAPTER 7: AGGREGATE DEMAND AND AGGREGATE SUPPLY Learning goals of this chapter: What forces bring persistent and rapid expansion of real GDP? What causes inflation? Why do we have business cycles? How

NAME: INTERMEDIATE MICROECONOMIC THEORY SPRING 2008 ECONOMICS 300/010 & 011 Midterm II April 30, 2008

NAME: INTERMEDIATE MICROECONOMIC THEORY SPRING 2008 ECONOMICS 300/010 & 011 Section I: Multiple Choice (4 points each) Identify the choice that best completes the statement or answers the question. 1.

NAME: INTERMEDIATE MICROECONOMIC THEORY SPRING 2008 ECONOMICS 300/010 & 011 Section I: Multiple Choice (4 points each) Identify the choice that best completes the statement or answers the question. 1.

Practice Multiple Choice Questions Answers are bolded. Explanations to come soon!!

Practice Multiple Choice Questions Answers are bolded. Explanations to come soon!! For more, please visit: http://courses.missouristate.edu/reedolsen/courses/eco165/qeq.htm Market Equilibrium and Applications

Practice Multiple Choice Questions Answers are bolded. Explanations to come soon!! For more, please visit: http://courses.missouristate.edu/reedolsen/courses/eco165/qeq.htm Market Equilibrium and Applications

FISCAL POLICY* Chapter. Key Concepts

Chapter 11 FISCAL POLICY* Key Concepts The Federal Budget The federal budget is an annual statement of the government s expenditures and tax revenues. Using the federal budget to achieve macroeconomic

Chapter 11 FISCAL POLICY* Key Concepts The Federal Budget The federal budget is an annual statement of the government s expenditures and tax revenues. Using the federal budget to achieve macroeconomic

Learning Objectives. After reading Chapter 11 and working the problems for Chapter 11 in the textbook and in this Workbook, you should be able to:

Learning Objectives After reading Chapter 11 and working the problems for Chapter 11 in the textbook and in this Workbook, you should be able to: Discuss three characteristics of perfectly competitive

Learning Objectives After reading Chapter 11 and working the problems for Chapter 11 in the textbook and in this Workbook, you should be able to: Discuss three characteristics of perfectly competitive

Chapter 12. Aggregate Expenditure and Output in the Short Run

Chapter 12. Aggregate Expenditure and Output in the Short Run Instructor: JINKOOK LEE Department of Economics / Texas A&M University ECON 203 502 Principles of Macroeconomics Aggregate Expenditure (AE)

Chapter 12. Aggregate Expenditure and Output in the Short Run Instructor: JINKOOK LEE Department of Economics / Texas A&M University ECON 203 502 Principles of Macroeconomics Aggregate Expenditure (AE)

Theoretical Tools of Public Economics. Part-2

Theoretical Tools of Public Economics Part-2 Previous Lecture Definitions and Properties Utility functions Marginal utility: positive (negative) if x is a good ( bad ) Diminishing marginal utility Indifferences

Theoretical Tools of Public Economics Part-2 Previous Lecture Definitions and Properties Utility functions Marginal utility: positive (negative) if x is a good ( bad ) Diminishing marginal utility Indifferences

Market is a network of dealings between buyers and sellers.

Market is a network of dealings between buyers and sellers. Market is the characteristic phenomenon of economic life and the constitution of markets and market prices is the central problem of Economics.

Market is a network of dealings between buyers and sellers. Market is the characteristic phenomenon of economic life and the constitution of markets and market prices is the central problem of Economics.

6. Which of the following is likely to be the price elasticity of demand for food? a. 5.2 b. 2.6 c. 1.8 d. 0.3

Exercise 2 Multiple Choice Questions. Choose the best answer. 1. If a change in the price of a good causes no change in total revenue a. the demand for the good must be elastic. b. the demand for the good

Exercise 2 Multiple Choice Questions. Choose the best answer. 1. If a change in the price of a good causes no change in total revenue a. the demand for the good must be elastic. b. the demand for the good

Managerial Economics Prof. Trupti Mishra S.J.M. School of Management Indian Institute of Technology, Bombay. Lecture - 13 Consumer Behaviour (Contd )

") (Refer Slide Time: 00:28) Managerial Economics Prof. Trupti Mishra S.J.M. School of Management Indian Institute of Technology, Bombay Lecture - 13 Consumer Behaviour (Contd ) We will continue our discussion

(Refer Slide Time: 00:28) Managerial Economics Prof. Trupti Mishra S.J.M. School of Management Indian Institute of Technology, Bombay Lecture - 13 Consumer Behaviour (Contd ) We will continue our discussion

A. a change in demand. B. a change in quantity demanded. C. a change in quantity supplied. D. unit elasticity. E. a change in average variable cost.

1. The supply of gasoline changes, causing the price of gasoline to change. The resulting movement from one point to another along the demand curve for gasoline is called A. a change in demand. B. a change

1. The supply of gasoline changes, causing the price of gasoline to change. The resulting movement from one point to another along the demand curve for gasoline is called A. a change in demand. B. a change

Market Structure: Perfect Competition and Monopoly

WSG8 7/7/03 4:34 PM Page 113 8 Market Structure: Perfect Competition and Monopoly OVERVIEW One of the most important decisions made by a manager is how to price the firm s product. If the firm is a profit

WSG8 7/7/03 4:34 PM Page 113 8 Market Structure: Perfect Competition and Monopoly OVERVIEW One of the most important decisions made by a manager is how to price the firm s product. If the firm is a profit

Microeconomics Instructor Miller Practice Problems Labor Market

Microeconomics Instructor Miller Practice Problems Labor Market 1. What is a factor market? A) It is a market where financial instruments are traded. B) It is a market where stocks and bonds are traded.

Microeconomics Instructor Miller Practice Problems Labor Market 1. What is a factor market? A) It is a market where financial instruments are traded. B) It is a market where stocks and bonds are traded.

ELASTICITY. Answers to the Review Quizzes. Page 92

C h a p t e r 4 ELASTICITY Answers to the Review Quizzes Page 92 1. Why do we need a units-free measure of the responsiveness of the quantity demanded of a good or service to a change in its price? The

C h a p t e r 4 ELASTICITY Answers to the Review Quizzes Page 92 1. Why do we need a units-free measure of the responsiveness of the quantity demanded of a good or service to a change in its price? The

Chapter 7 Monopoly, Oligopoly and Strategy

Chapter 7 Monopoly, Oligopoly and Strategy After reading Chapter 7, MONOPOLY, OLIGOPOLY AND STRATEGY, you should be able to: Define the characteristics of Monopoly and Oligopoly, and explain why the are

Chapter 7 Monopoly, Oligopoly and Strategy After reading Chapter 7, MONOPOLY, OLIGOPOLY AND STRATEGY, you should be able to: Define the characteristics of Monopoly and Oligopoly, and explain why the are

Monopoly. Monopoly Defined

Monopoly In chapter 9 we described an idealized market system in which all firms are perfectly competitive. In chapter 11 we turn to one of the blemishes of the market system --the possibility that some

Monopoly In chapter 9 we described an idealized market system in which all firms are perfectly competitive. In chapter 11 we turn to one of the blemishes of the market system --the possibility that some

CHAPTER 4 Labor Demand Elasticities

CHAPTER 4 Labor Demand Elasticities In addition to the multiple choice problems listed below, complete the following end of chapter questions: Review questions 1,3, 4, 6 and 7. Problems 1, 2, 3 and 5.

CHAPTER 4 Labor Demand Elasticities In addition to the multiple choice problems listed below, complete the following end of chapter questions: Review questions 1,3, 4, 6 and 7. Problems 1, 2, 3 and 5.

DEMAND AND SUPPLY. Chapter. Markets and Prices. Demand. C) the price of a hot dog minus the price of a hamburger.

the price of a hot dog minus the price of a hamburger.") Chapter 3 DEMAND AND SUPPLY Markets and Prices Topic: Price and Opportunity Cost 1) A relative price is A) the slope of the demand curve B) the difference between one price and another C) the slope of

Chapter 3 DEMAND AND SUPPLY Markets and Prices Topic: Price and Opportunity Cost 1) A relative price is A) the slope of the demand curve B) the difference between one price and another C) the slope of

Suppose you are a seller with cost 13 who must pay a sales tax of 15. What is the lowest price you can sell at and not lose money?

Experiment 3 Suppose that sellers pay a tax of 15. If a seller with cost 5 sells to a buyer with value 45 at a price of 25, the seller earns a profit of and the buyer earns a profit of. Suppose you are

Experiment 3 Suppose that sellers pay a tax of 15. If a seller with cost 5 sells to a buyer with value 45 at a price of 25, the seller earns a profit of and the buyer earns a profit of. Suppose you are

Employment and Pricing of Inputs

Employment and Pricing of Inputs Previously we studied the factors that determine the output and price of goods. In chapters 16 and 17, we will focus on the factors that determine the employment level

Employment and Pricing of Inputs Previously we studied the factors that determine the output and price of goods. In chapters 16 and 17, we will focus on the factors that determine the employment level

14 : Elasticity of Supply

14 : Elasticity of Supply 1 Recap from Session Budget line and Consumer equilibrium Law of Equi Marginal utility Price, income and substitution effect Consumer Surplus Session Outline Elasticity of Supply

14 : Elasticity of Supply 1 Recap from Session Budget line and Consumer equilibrium Law of Equi Marginal utility Price, income and substitution effect Consumer Surplus Session Outline Elasticity of Supply

Chapter 12: Gross Domestic Product and Growth Section 1

Chapter 12: Gross Domestic Product and Growth Section 1 Key Terms national income accounting: a system economists use to collect and organize macroeconomic statistics on production, income, investment,

Chapter 12: Gross Domestic Product and Growth Section 1 Key Terms national income accounting: a system economists use to collect and organize macroeconomic statistics on production, income, investment,

4 ELASTICITY. Chapter. Price Elasticity of Demand. A) more elastic. B) less elastic. C) neither more nor less elastic. D) undefined.

more elastic. B) less elastic. C) neither more nor less elastic. D) undefined.") Chapter 4 ELASTICITY Price Elasticity of Demand Topic: The Price Elasticity of Demand 1) The slope of a demand curve depends on A) the units used to measure price and the units used to measure quantity.

Chapter 4 ELASTICITY Price Elasticity of Demand Topic: The Price Elasticity of Demand 1) The slope of a demand curve depends on A) the units used to measure price and the units used to measure quantity.

Business and Economic Applications

Appendi F Business and Economic Applications F1 F Business and Economic Applications Understand basic business terms and formulas, determine marginal revenues, costs and profits, find demand functions,

Appendi F Business and Economic Applications F1 F Business and Economic Applications Understand basic business terms and formulas, determine marginal revenues, costs and profits, find demand functions,

MERSİN UNIVERSITY FACULTY OF ECONOMICS AND ADMINISTRATIVE SCİENCES DEPARTMENT OF ECONOMICS MICROECONOMICS MIDTERM EXAM DATE 18.11.

MERSİN UNIVERSITY FACULTY OF ECONOMICS AND ADMINISTRATIVE SCİENCES DEPARTMENT OF ECONOMICS MICROECONOMICS MIDTERM EXAM DATE 18.11.2011 TİIE 12:30 STUDENT NAME AND NUMBER MULTIPLE CHOICE. Choose the one

MERSİN UNIVERSITY FACULTY OF ECONOMICS AND ADMINISTRATIVE SCİENCES DEPARTMENT OF ECONOMICS MICROECONOMICS MIDTERM EXAM DATE 18.11.2011 TİIE 12:30 STUDENT NAME AND NUMBER MULTIPLE CHOICE. Choose the one

Productioin OVERVIEW. WSG5 7/7/03 4:35 PM Page 63. Copyright 2003 by Academic Press. All rights of reproduction in any form reserved.

WSG5 7/7/03 4:35 PM Page 63 5 Productioin OVERVIEW This chapter reviews the general problem of transforming productive resources in goods and services for sale in the market. A production function is the

WSG5 7/7/03 4:35 PM Page 63 5 Productioin OVERVIEW This chapter reviews the general problem of transforming productive resources in goods and services for sale in the market. A production function is the

Practice Questions Week 8 Day 1

Practice Questions Week 8 Day 1 Multiple Choice Identify the choice that best completes the statement or answers the question. 1. The characteristics of a market that influence the behavior of market participants

Practice Questions Week 8 Day 1 Multiple Choice Identify the choice that best completes the statement or answers the question. 1. The characteristics of a market that influence the behavior of market participants

13 EXPENDITURE MULTIPLIERS: THE KEYNESIAN MODEL* Chapter. Key Concepts

Chapter 3 EXPENDITURE MULTIPLIERS: THE KEYNESIAN MODEL* Key Concepts Fixed Prices and Expenditure Plans In the very short run, firms do not change their prices and they sell the amount that is demanded.

Chapter 3 EXPENDITURE MULTIPLIERS: THE KEYNESIAN MODEL* Key Concepts Fixed Prices and Expenditure Plans In the very short run, firms do not change their prices and they sell the amount that is demanded.

7 AGGREGATE SUPPLY AND AGGREGATE DEMAND* Chapter. Key Concepts

Chapter 7 AGGREGATE SUPPLY AND AGGREGATE DEMAND* Key Concepts Aggregate Supply The aggregate production function shows that the quantity of real GDP (Y ) supplied depends on the quantity of labor (L ),

Chapter 7 AGGREGATE SUPPLY AND AGGREGATE DEMAND* Key Concepts Aggregate Supply The aggregate production function shows that the quantity of real GDP (Y ) supplied depends on the quantity of labor (L ),

The demand for cigarettes and other tobacco products. Anne-Marie Perucic Tobacco Control Economics Tobacco Free Initiative WHO

The demand for cigarettes and other tobacco products Anne-Marie Perucic Tobacco Control Economics Tobacco Free Initiative WHO Price (tax) increases and tobacco use in the words of the tobacco industry

The demand for cigarettes and other tobacco products Anne-Marie Perucic Tobacco Control Economics Tobacco Free Initiative WHO Price (tax) increases and tobacco use in the words of the tobacco industry

University of Lethbridge - Department of Economics ECON 1010 - Introduction to Microeconomics Instructor: Michael G. Lanyi. Lab #4

University of Lethbridge - Department of Economics ECON 1010 - Introduction to Microeconomics Instructor: Michael G. Lanyi Lab #4 Chapter 4 Elasticity MULTIPLE CHOICE. Choose the one alternative that best

University of Lethbridge - Department of Economics ECON 1010 - Introduction to Microeconomics Instructor: Michael G. Lanyi Lab #4 Chapter 4 Elasticity MULTIPLE CHOICE. Choose the one alternative that best

Answer: The relationship cannot be determined.

Question 1 Test 2, Second QR Section (version 3) In City X, the range of the daily low temperatures during... QA: The range of the daily low temperatures in City X... QB: 30 Fahrenheit Arithmetic: Ranges

Question 1 Test 2, Second QR Section (version 3) In City X, the range of the daily low temperatures during... QA: The range of the daily low temperatures in City X... QB: 30 Fahrenheit Arithmetic: Ranges