How is Greek shipping surviving the crisis?

|

|

|

- Noel Wheeler

- 7 years ago

- Views:

Transcription

1 How is Greek shipping surviving the crisis? By Ted Petropoulos Head of Petrofin Research PSMI published in Nafs September 2011 Since mid 2008, the world economy, the banking industry and shipping have been in continuing difficulties. The slow down and erratic performance of the global economy and international trade has led to a slowdown in demand for shipping across most sectors with the primary exception of the LNG and offshore sectors. This couldn t have come at a worse time for shipping, since the good market of had laid the foundations of a gigantic ordering book, which more than doubled ship carrying capacity. The resultant market oversupply has led to the drastic erosion of vessel prices and vessel incomes. This has resulted in most companies running their fleets with negative cash flows, continuously dipping into their liquidity reserves. Freight rates recently reached very low levels with most vessels in both the dry and wet sectors barely covering their operating costs. The declining cash flow of the industry has also affected its ability to meet its financial obligations, resulting in across the board loan restructurings by banks, which had little choice but to provide. Of course, banks have started identifying and quietly reallocating assets among its clients, not only in an effort to shore up the creditworthiness of their shipping loan portfolios but primarily to avoid or delay taking losses. The shipping banking sector, as part of the continuous global banking crisis, has suffered greatly. The number of banks still actively engaged in ship lending has been reduced to a pitiful few with the list of existing banks becoming longer and longer.

2 As we all know, shipping is a capital intensive industry, which requires financial support, both for the acquisition of vessels, as well as for servicing its bank debt. The virtual absence of ship finance, even for the larger and creditworthy clients, involving secure transactions that meet even current adverse market criteria, has led to an implosion for the shipping industry, where liquidity is scarce and economising is the order of the day. For the shipping industry, which had gone through a period of drastic age, quality upgrading and growth in its fleet, with the resultant growth in lending, the adjustment to the catastrophic conditions prevalent over the last 4 years has been particularly painful. In the interests of brevity, I have not provided numbers (which have been previously reported in our Petrofin Bank Research and articles), but have kept to the main issues to present the background to the shipping industry s plight. Greek shipping suffered, in line with all the other countries shipping sectors, with the exception of the Chinese and other Far Eastern ones, where they have been to some extent protected by the growth of the Far East region, coastal trading, employment contracts and better support by both shipyards and Far Eastern banks. Greek owners have had to also deal with the adverse effects of the Greek crisis and the uncertainty this has generated both to them, as well as indirectly to financing institutions seeking to restrict Greek risk. Although, Greek shipping is an international offshore industry unaffected by Greece s plight, this demarcation has been hazy for some banks. As a conclusion, global shipping in general and Greek shipping in particular, have been labouring to meet their obligations under the most adverse conditions even encountered, whilst the industry s prospects, as to a recovery, remain hazy, at best. Let me repeat this article s headline question, How is Greek shipping surviving the crisis?

3 According to the latest Petrofin Research, recently published, (see graph 1), the total number of Greek companies in operation in 2009 (when the crisis started to affect shipping) was 773, whereas the 2012 figures show 718, a 7.1% decrease. However, it is fair to say that between 2005 and 2009 the number had risen from 690 to 773 companies. It is also reasonable to say that Greek shipping company numbers reflect (with lags) the fortunes of Greek shipping, although there are other factors that also have a bearing that shall be analysed below. Graph 1 It should be stressed, however, that the majority of the departing owners have been small owners with 1 2 vessels, which are usually consisting of overage vessels. Between 2009 and today, the total number of such small owners fell by 31. The exit of such small owners is largely expected in crisis years, as their vessels may find difficulty to find employment and to continue trading,

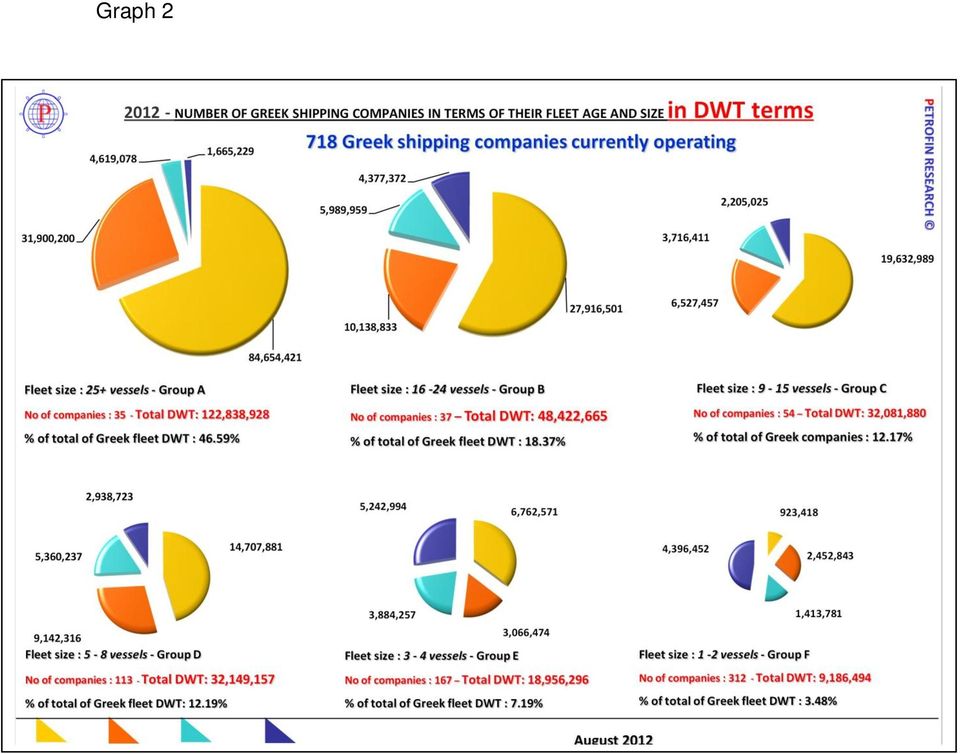

4 the costs of maintenance and surveys rise and holding on to such vessels may become uneconomic. Consequently, with scrap prices still supportive, small owners may choose to dispose of their last tonnage and await a future opportunity to re-enter the market later. Interestingly, the largest fleet size groups, consisting of 16 vessels and higher, have increased over the period from 66 to 72, demonstrating that larger owners have fared better during the crisis. These owners share of Greek shipping has risen progressively over the past decade and now accounts for 65% of the total, whereas the smallest sector (1 + 2 vessels) has shrunk to 10.7% in 2012, even though, they still account for 43.4% of the total number of Greek shipping companies. Readers may wish to refer to graph 2 which shows the breakdown of the whole Greek fleet in DWT terms between the six different owner sizes in terms of fleet size, fleet age and fleet numbers.

has shrunk to 10.")

5 Graph 2

6 Despite the crisis, the total Greek fleet rose from 237,288,216 DWT in 2009 to 263,635,420 in 2012, demonstrating the continuous growth in capacity of the Greek fleet. Moreover, the average age of the fleet has continued to fall and according to Petrofin Research, has now fallen to 8.7 years, a remarkably low figure. In conclusion, Greek shipping has thus far weathered the storm successfully. A secondary question that arises is how has it been able to do so? To a large part, the Greek shipping industry s performance to date can be attributed to its ability to adjust and cope in the face of adversity. Cost cutting, flexible solutions and proactive thinking have helped. More tangibly, most owners have continued to support their fleets by using their liquidity reserves and / or the sale of older vessels or unwanted assets. This financial commitment is and shall be tested to the maximum during the current cash flow squeeze, whereby loan repayments, if any, are being mainly achieved via owner cash injections. In many cases, cash strapped owners abandoned their new-buildings or reduced their fleets, to maintain their newbuilding orders. Undoubtedly, though, the main contributor to the success of Greek shipping has been the quite support and flexibility shown by banks. Banks, either due to their own internal weaknesses or realising that only through flexibility on their part would losses be averted, have restructured a very high percentage of loans, by adjusting the nearby loan installments and waiving minimum asset cover and other financial covenants. This has kicked the can down the road for a few years and the process has been profitable, as margins on restructured loans have increased. To a large extent, the young age of the Greek fleet has permitted this accommodation. However, there exists a time limit for such delays, as the banks' collateral vessels grow older and the banks more impatient. The continuous fall in vessel values has resulted in banks sitting on large uncovered loan exposures, which have lately been rising, rather than falling. Clearly, the toughest hurdles lie ahead for Greek shipping, as liquidity tightens further and bank finance dwindles. The tough conditions can be seen from a marked slowdown in new-building orders (down 31% y o y), as a direct result of lack of finance and the poor industry s prospects.

7 What has helped Greek shipping has been the low US Dollar interest rates even though loan margins have more than doubled over the last 4 years. In most cases, owners and banks are locked in a tight embrace, where they need to hold to each other, in order to keep on dancing. The key question that remains is how long will current conditions last? This is the most difficult question to assess. One thing that has been clear is that the recovery date has been slipping from 2012 to 2013 and now 2014 onwards. The main reasons for this delay is that the cancellation and slippage figures for vessels being delivered in 2012 have been less than anticipated and fresh ordering has continued, even at subdued levels. Shipyards are promoting their new eco design vessels, in order to drum up orders and fill up their rapidly vanishing forward order book. This, plus increased shipyard related new-building finance by Far Eastern financial institutions will undoubtedly keep the supply side growing. Any relief will have to come from the demand side, where current growth estimates are wobbly, at best. An optimistic scenario with a revitalised China and growth recovery is the West plus a restored banking system leading to an improved confidence by consumers, depositors and industrialists, does exist. Currently, though, the odds are for further difficult years ahead, for the Greek shipping industry. Under such continuing difficult conditions, we anticipate further consolidation in the total of Greek owners, with an even heavier concentration of the Greek fleet among the largest and financially more robust owners, with access to both capital and liquidity. Despite the above, we do not anticipate any shrinkage in the Greek fleet capacity, as more and more owners are seeking the purchase of young inexpensive vessels, in anticipation of a future recovery, as and when it shall materialise.

Marine Money - Alternative Funding Solutions for Dry Bulk by Soo Cheon Lee

Marine Money - Alternative Funding Solutions for Dry Bulk by Soo Cheon Lee Alternative Funding Solutions for Dry Bulk By Co-Founder & Chief Investment Officer, Soo Cheon Lee Marine Money August/September

Marine Money - Alternative Funding Solutions for Dry Bulk by Soo Cheon Lee Alternative Funding Solutions for Dry Bulk By Co-Founder & Chief Investment Officer, Soo Cheon Lee Marine Money August/September

THE FINANCIAL CRISIS: Is This a REPEAT OF THE 80 S FOR AGRICULTURE? Mike Boehlje and Chris Hurt, Department of Agricultural Economics

THE FINANCIAL CRISIS: Is This a REPEAT OF THE 80 S FOR AGRICULTURE? Mike Boehlje and Chris Hurt, Department of Agricultural Economics The current financial crisis in the capital markets combined with recession

THE FINANCIAL CRISIS: Is This a REPEAT OF THE 80 S FOR AGRICULTURE? Mike Boehlje and Chris Hurt, Department of Agricultural Economics The current financial crisis in the capital markets combined with recession

Global shipping. Heading southwards. Introduction. Quick links. Contacts

Global shipping Quick links Introduction Excess tonnage Access to finance has dried up The issues and options for owners and operators The issues and options for lenders Overall outlook Feedback and comments

Global shipping Quick links Introduction Excess tonnage Access to finance has dried up The issues and options for owners and operators The issues and options for lenders Overall outlook Feedback and comments

NATIONAL SURVEY OF HOME EQUITY LOANS

NATIONAL SURVEY OF HOME EQUITY LOANS Richard T. Curtin Director, Surveys of Consumers Survey Research Center The October 1998 WP51 The 1988, 1994, and 1997 National Surveys of Home Equity Loans were sponsored

NATIONAL SURVEY OF HOME EQUITY LOANS Richard T. Curtin Director, Surveys of Consumers Survey Research Center The October 1998 WP51 The 1988, 1994, and 1997 National Surveys of Home Equity Loans were sponsored

ALPHALINER Annual Review 2012

ALPHALINER Annual Review 2012 A market awash with capacity Overcapacity continued to plague the container shipping markets all through 2012. The container freight market saw its most volatile year while

ALPHALINER Annual Review 2012 A market awash with capacity Overcapacity continued to plague the container shipping markets all through 2012. The container freight market saw its most volatile year while

Statement by Kasper Rorsted Chairman of the Management Board Conference-Call November 11, 2015, 10.30 a.m.

Statement by Kasper Rorsted Chairman of the Management Board Conference-Call November 11, 2015, 10.30 a.m. Welcome to our conference call today. As you will have seen, this morning we sent out our news

Statement by Kasper Rorsted Chairman of the Management Board Conference-Call November 11, 2015, 10.30 a.m. Welcome to our conference call today. As you will have seen, this morning we sent out our news

2012 Survey of Credit Underwriting Practices

2012 Survey of Credit Underwriting Practices Office of the Comptroller of the Currency Washington, D.C. June 2012 Contents Introduction... 1 Part I: Overall Results... 3 Primary Findings... 3 Commentary

2012 Survey of Credit Underwriting Practices Office of the Comptroller of the Currency Washington, D.C. June 2012 Contents Introduction... 1 Part I: Overall Results... 3 Primary Findings... 3 Commentary

Monetary Authority of Singapore THEMATIC REVIEW OF CREDIT UNDERWRITING STANDARDS AND PRACTICES OF CORPORATE LENDING BUSINESS

Monetary Authority of Singapore THEMATIC REVIEW OF CREDIT UNDERWRITING STANDARDS AND PRACTICES OF CORPORATE LENDING BUSINESS MAS Information Paper February 2016 Contents 1 Executive Summary 1 2 Credit

Monetary Authority of Singapore THEMATIC REVIEW OF CREDIT UNDERWRITING STANDARDS AND PRACTICES OF CORPORATE LENDING BUSINESS MAS Information Paper February 2016 Contents 1 Executive Summary 1 2 Credit

Private Equity Funds; an unfolding story. By Ted Petropoulos. Nafs. March 2014

Private equity funds (PEFs) have been increasingly making the headlines, over the past year. Driven by their abundant liquidity and strongly held percep@on that shipping presents aarac@ve profit making

Private equity funds (PEFs) have been increasingly making the headlines, over the past year. Driven by their abundant liquidity and strongly held percep@on that shipping presents aarac@ve profit making

INFLATION REPORT PRESS CONFERENCE. Thursday 4 th February 2016. Opening remarks by the Governor

INFLATION REPORT PRESS CONFERENCE Thursday 4 th February 2016 Opening remarks by the Governor Good afternoon. At its meeting yesterday, the Monetary Policy Committee (MPC) voted 9-0 to maintain Bank Rate

INFLATION REPORT PRESS CONFERENCE Thursday 4 th February 2016 Opening remarks by the Governor Good afternoon. At its meeting yesterday, the Monetary Policy Committee (MPC) voted 9-0 to maintain Bank Rate

Prospects for the container shipping industry

Prospects for the container shipping industry IQPC Container Terminal Business 2009 Hamburg, December 8, 2008 Eric Heymann Sector Research Think Tank of Deutsche Bank Group Agenda 1 Weak economic environment

Prospects for the container shipping industry IQPC Container Terminal Business 2009 Hamburg, December 8, 2008 Eric Heymann Sector Research Think Tank of Deutsche Bank Group Agenda 1 Weak economic environment

Recent Developments in Small Business Finance

April 1 Recent Developments in Small Business Finance Introduction In 1, a Small Business Panel was formed by the Reserve Bank to advise it on the availability of finance to small business. At about the

April 1 Recent Developments in Small Business Finance Introduction In 1, a Small Business Panel was formed by the Reserve Bank to advise it on the availability of finance to small business. At about the

BROSTRÖM AB (publ) Reg No 556005-1467

Reg No 556005-1467") Broström is one of the leading logistics companies for the oil and chemical industry, focusing on industrial product and chemical tanker shipping and marine services. Broström is based all over the world

Broström is one of the leading logistics companies for the oil and chemical industry, focusing on industrial product and chemical tanker shipping and marine services. Broström is based all over the world

Risk management and sensitivities

8% Russia DISTRIBUTION OF OPERATING REVENUES 58% North Sea 34% Gulf of Mexico Risk management and sensitivities Prosafe operates on several continents and in various 11% unsecured debt segments of the

8% Russia DISTRIBUTION OF OPERATING REVENUES 58% North Sea 34% Gulf of Mexico Risk management and sensitivities Prosafe operates on several continents and in various 11% unsecured debt segments of the

EAST AYRSHIRE COUNCIL CABINET 21 OCTOBER 2009 TREASURY MANAGEMENT ANNUAL REPORT FOR 2008/2009 AND UPDATE ON 2009/10 STRATEGY

EAST AYRSHIRE COUNCIL CABINET 21 OCTOBER 2009 TREASURY MANAGEMENT ANNUAL REPORT FOR 2008/2009 AND UPDATE ON 2009/10 STRATEGY Report by Executive Head of Finance and Asset Management 1 PURPOSE OF REPORT

EAST AYRSHIRE COUNCIL CABINET 21 OCTOBER 2009 TREASURY MANAGEMENT ANNUAL REPORT FOR 2008/2009 AND UPDATE ON 2009/10 STRATEGY Report by Executive Head of Finance and Asset Management 1 PURPOSE OF REPORT

Clear weather on the horizon?

PwC annual Global Shipping Benchmarking Analysis Market Developments p / Sustainability p1 / Financial Performance review p17 / Companies covered by the analysis p Clear weather on the horizon? 3% of the

PwC annual Global Shipping Benchmarking Analysis Market Developments p / Sustainability p1 / Financial Performance review p17 / Companies covered by the analysis p Clear weather on the horizon? 3% of the

The Performance of Australian Industrial Projects

The Performance of Australian Industrial Projects Prepared for the Business Council of Australia by Rob Young, Independent Project Analysis, Inc May 2012 Executive Summary Independent Project Analysis,

The Performance of Australian Industrial Projects Prepared for the Business Council of Australia by Rob Young, Independent Project Analysis, Inc May 2012 Executive Summary Independent Project Analysis,

NORDEN RESULTS. 1 st quarter of 2013. Hellerup, Denmark 15 May 2013. Our business is global tramp shipping. NORDEN 1st quarter of 2013 results 1

NORDEN RESULTS 1 st quarter of 2013 Hellerup, Denmark 15 May 2013 NORDEN 1st quarter of 2013 results 1 AGENDA Group highlights Financial highlights Market update Full year financial guidance Q & A NORDEN

NORDEN RESULTS 1 st quarter of 2013 Hellerup, Denmark 15 May 2013 NORDEN 1st quarter of 2013 results 1 AGENDA Group highlights Financial highlights Market update Full year financial guidance Q & A NORDEN

RESTRUCTURING STUDY. International 2012. Sovereign debt crisis Effects on financing and the real economy

RESTRUCTURING STUDY International 2012 Sovereign debt crisis Effects on financing and the real economy Düsseldorf, September 2012 2 Contents Page A. Goal and methodology 4 B. Summary in brief 7 C. Key

RESTRUCTURING STUDY International 2012 Sovereign debt crisis Effects on financing and the real economy Düsseldorf, September 2012 2 Contents Page A. Goal and methodology 4 B. Summary in brief 7 C. Key

Investment insight. Fixed income the what, when, where, why and how TABLE 1: DIFFERENT TYPES OF FIXED INCOME SECURITIES. What is fixed income?

Fixed income investments make up a large proportion of the investment universe and can form a significant part of a diversified portfolio but investors are often much less familiar with how fixed income

Fixed income investments make up a large proportion of the investment universe and can form a significant part of a diversified portfolio but investors are often much less familiar with how fixed income

UK Problem Debt: Consumer Crisis or Efficient Market?

For immediate release UK Problem Debt: Consumer Crisis or Efficient Market? 08 May 2008 - The last decade has seen a major economic and social phenomenon in the UK: the huge growth of the consumer credit

For immediate release UK Problem Debt: Consumer Crisis or Efficient Market? 08 May 2008 - The last decade has seen a major economic and social phenomenon in the UK: the huge growth of the consumer credit

18 ECB FACTORS AFFECTING LENDING TO THE PRIVATE SECTOR AND THE SHORT-TERM OUTLOOK FOR MONEY AND LOAN DYNAMICS

Box 2 FACTORS AFFECTING LENDING TO THE PRIVATE SECTOR AND THE SHORT-TERM OUTLOOK FOR MONEY AND LOAN DYNAMICS The intensification of the financial crisis in the fourth quarter of 211 had a considerable

Box 2 FACTORS AFFECTING LENDING TO THE PRIVATE SECTOR AND THE SHORT-TERM OUTLOOK FOR MONEY AND LOAN DYNAMICS The intensification of the financial crisis in the fourth quarter of 211 had a considerable

2013 Survey of Credit Underwriting Practices

2013 Survey of Credit Underwriting Practices Office of the Comptroller of the Currency Washington, D.C. January 2014 Contents Introduction... 1 Part I: Overall Results... 3 Primary Findings... 3 Commentary

2013 Survey of Credit Underwriting Practices Office of the Comptroller of the Currency Washington, D.C. January 2014 Contents Introduction... 1 Part I: Overall Results... 3 Primary Findings... 3 Commentary

The Westpac Group third quarter 2011 sound core earnings growth

Media Release 16 August 2011 The Westpac Group third quarter 2011 sound core earnings growth Third quarter 2011 highlights (compared to results for the average of 1Q and 2Q 2011) 1 Cash earnings of approximately

Media Release 16 August 2011 The Westpac Group third quarter 2011 sound core earnings growth Third quarter 2011 highlights (compared to results for the average of 1Q and 2Q 2011) 1 Cash earnings of approximately

A LIFE-CYCLE AND GENERATIONAL PERSPECTIVE ON THE WEALTH AND INCOME OF MILLENNIALS

A LIFE-CYCLE AND GENERATIONAL PERSPECTIVE ON THE WEALTH AND INCOME OF MILLENNIALS William R. Emmons and Ray Boshara Young adulthood is the life stage when the greatest increases in income and wealth typically

A LIFE-CYCLE AND GENERATIONAL PERSPECTIVE ON THE WEALTH AND INCOME OF MILLENNIALS William R. Emmons and Ray Boshara Young adulthood is the life stage when the greatest increases in income and wealth typically

FRONTLINE LTD. INTERIM REPORT JULY - SEPTEMBER 2005. Highlights

FRONTLINE LTD. INTERIM REPORT JULY - SEPTEMBER Highlights Frontline reports net income of $73.8 million and earnings per share of $0.99 for the third quarter of. Frontline reports nine month results of

FRONTLINE LTD. INTERIM REPORT JULY - SEPTEMBER Highlights Frontline reports net income of $73.8 million and earnings per share of $0.99 for the third quarter of. Frontline reports nine month results of

BERYL Credit Pulse on High Yield Corporates

BERYL Credit Pulse on High Yield Corporates This paper will summarize Beryl Consulting 2010 outlook and hedge fund portfolio construction for the high yield corporate sector in light of the events of the

BERYL Credit Pulse on High Yield Corporates This paper will summarize Beryl Consulting 2010 outlook and hedge fund portfolio construction for the high yield corporate sector in light of the events of the

PIONEER INVESTMENT MANAGEMENT USA, INC. Moderator: Christine Seaver July 24, 2014 3:15 pm CT

Page 1 Following is an edited transcript from the July 24, 2014 conference call on Pioneer High Income Trust (ticker: PHT). Investment terms are defined at the end of the transcript. PIONEER INVESTMENT

Page 1 Following is an edited transcript from the July 24, 2014 conference call on Pioneer High Income Trust (ticker: PHT). Investment terms are defined at the end of the transcript. PIONEER INVESTMENT

THE RETURN OF CAPITAL EXPENDITURE OR CAPEX CYCLE IN MALAYSIA

PUBLIC BANK BERHAD ECONOMICS DIVISION MENARA PUBLIC BANK 146 JALAN AMPANG 50450 KUALA LUMPUR TEL : 03 2176 6000/666 FAX : 03 2163 9929 Public Bank Economic Review is published bi monthly by Economics Division,

PUBLIC BANK BERHAD ECONOMICS DIVISION MENARA PUBLIC BANK 146 JALAN AMPANG 50450 KUALA LUMPUR TEL : 03 2176 6000/666 FAX : 03 2163 9929 Public Bank Economic Review is published bi monthly by Economics Division,

UNIFE World Rail Market Study

UNIFE World Rail Market Study Status quo and outlook 2020 Commissioned by UNIFE, the European Rail Industry And conducted by The Boston Consulting Group 2 1 Executive Summary This is the third "World Rail

UNIFE World Rail Market Study Status quo and outlook 2020 Commissioned by UNIFE, the European Rail Industry And conducted by The Boston Consulting Group 2 1 Executive Summary This is the third "World Rail

LOAN APPROVALS, REPAYMENTS AND HOUSING CREDIT GROWTH 1

LOAN APPROVALS, REPAYMENTS AND HOUSING CREDIT GROWTH Introduction The majority of household borrowing is for the purchase of existing or new housing. Developments in borrowing for housing are important

LOAN APPROVALS, REPAYMENTS AND HOUSING CREDIT GROWTH Introduction The majority of household borrowing is for the purchase of existing or new housing. Developments in borrowing for housing are important

REPORT TO: THE SPECIAL MEETING OF THE MORAY COUNCIL ON 12 FEBRUARY 2015 TREASURY MANAGEMENT STRATEGY STATEMENT AND PRUDENTIAL INDICATORS

PAGE: 1 REPORT TO: THE SPECIAL MEETING OF THE MORAY COUNCIL ON 12 FEBRUARY 2015 SUBJECT: BY: TREASURY MANAGEMENT STRATEGY STATEMENT AND PRUDENTIAL INDICATORS CORPORATE DIRECTOR (CORPORATE SERVICES) 1.

PAGE: 1 REPORT TO: THE SPECIAL MEETING OF THE MORAY COUNCIL ON 12 FEBRUARY 2015 SUBJECT: BY: TREASURY MANAGEMENT STRATEGY STATEMENT AND PRUDENTIAL INDICATORS CORPORATE DIRECTOR (CORPORATE SERVICES) 1.

US GAAP and IFRS accounting and reporting issues for shipping companies Reminders and Updates

www.pwc.gr US GAAP and IFRS accounting and reporting issues for shipping companies Reminders and Updates 13 January 2014 Training Agenda 1. Accounting for long term debt 2. Capitalization of interest cost

www.pwc.gr US GAAP and IFRS accounting and reporting issues for shipping companies Reminders and Updates 13 January 2014 Training Agenda 1. Accounting for long term debt 2. Capitalization of interest cost

Monetary policy assessment of 13 September 2007 SNB aiming to calm the money market

Communications P.O. Box, CH-8022 Zurich Telephone +41 44 631 31 11 Fax +41 44 631 39 10 Zurich, 13 September 2007 Monetary policy assessment of 13 September 2007 SNB aiming to calm the money market The

Communications P.O. Box, CH-8022 Zurich Telephone +41 44 631 31 11 Fax +41 44 631 39 10 Zurich, 13 September 2007 Monetary policy assessment of 13 September 2007 SNB aiming to calm the money market The

PRESS RELEASE. Revenue as of March 31, 2011. Sharp growth in Bureau Veritas Q1 2011 revenue Revenue up 23% to 775 million Organic growth of 6.

1 PRESS RELEASE Neuilly-sur-Seine, France, May 4, 2011 Sharp growth in Bureau Veritas Q1 2011 revenue Revenue up 23% to 775 million Organic growth of 6.5% Frank Piedelièvre, Chairman and Chief Executive

1 PRESS RELEASE Neuilly-sur-Seine, France, May 4, 2011 Sharp growth in Bureau Veritas Q1 2011 revenue Revenue up 23% to 775 million Organic growth of 6.5% Frank Piedelièvre, Chairman and Chief Executive

Bondholders Report. Six months ended 30 September 2010

Six months ended 30 September 2010 Bondholders Report We would like to thank you for your investment in our business. We d also like for you to get to know us a bit better. This short report summarises

Six months ended 30 September 2010 Bondholders Report We would like to thank you for your investment in our business. We d also like for you to get to know us a bit better. This short report summarises

IFT Information Note: No. 160. Cash, Treasury and Working Capital Management. Treasury and Risk Management. 1. What is Treasury and Risk Management

1. What is relates to the provision of sufficient, and appropriate, liquidity for a company to fund its anticipated business requirements and the identification, and controlled management of, the financial

1. What is relates to the provision of sufficient, and appropriate, liquidity for a company to fund its anticipated business requirements and the identification, and controlled management of, the financial

BADGER DAYLIGHTING LTD. ANNOUNCES RESULTS FOR THE FIRST QUARTER ENDED MARCH 31, 2015

PRESS RELEASE TSX-BAD FOR IMMEDIATE DISTRIBUTION May 13, 2015 BADGER DAYLIGHTING LTD. ANNOUNCES RESULTS FOR THE FIRST QUARTER ENDED MARCH 31, 2015 Calgary, Alberta Badger Daylighting Ltd. is pleased to

PRESS RELEASE TSX-BAD FOR IMMEDIATE DISTRIBUTION May 13, 2015 BADGER DAYLIGHTING LTD. ANNOUNCES RESULTS FOR THE FIRST QUARTER ENDED MARCH 31, 2015 Calgary, Alberta Badger Daylighting Ltd. is pleased to

Unless otherwise stated, references to 2007 are made in relation to the first half of the year.

Standard Chartered PLC Pre-close Trading Update 26 June 2008 Standard Chartered PLC will be holding discussions with analysts and investors ahead of its close period for the half year ending 30 June 2008.

Standard Chartered PLC Pre-close Trading Update 26 June 2008 Standard Chartered PLC will be holding discussions with analysts and investors ahead of its close period for the half year ending 30 June 2008.

Still battling the storm

www.pwc.com Still battling the storm Global Shipping Benchmarking Analysis 2013 Table of contents Foreword 5 1. Market developments 6 1.1 General outlook 7 1.2 Characteristics of the market 9 1.3 Year

www.pwc.com Still battling the storm Global Shipping Benchmarking Analysis 2013 Table of contents Foreword 5 1. Market developments 6 1.1 General outlook 7 1.2 Characteristics of the market 9 1.3 Year

Adjusting to a Changing Economic World. Good afternoon, ladies and gentlemen. It s a pleasure to be with you here in Montréal today.

Remarks by David Dodge Governor of the Bank of Canada to the Board of Trade of Metropolitan Montreal Montréal, Quebec 11 February 2004 Adjusting to a Changing Economic World Good afternoon, ladies and

Remarks by David Dodge Governor of the Bank of Canada to the Board of Trade of Metropolitan Montreal Montréal, Quebec 11 February 2004 Adjusting to a Changing Economic World Good afternoon, ladies and

CREDIT RISK MANAGEMENT

GLOBAL ASSOCIATION OF RISK PROFESSIONALS The GARP Risk Series CREDIT RISK MANAGEMENT Chapter 1 Credit Risk Assessment Chapter Focus Distinguishing credit risk from market risk Credit policy and credit

GLOBAL ASSOCIATION OF RISK PROFESSIONALS The GARP Risk Series CREDIT RISK MANAGEMENT Chapter 1 Credit Risk Assessment Chapter Focus Distinguishing credit risk from market risk Credit policy and credit

SUB: STANDARD CHARTERED PLC (THE "COMPANY") STOCK EXCHANGE ANNOUNCEMENT

STOCK EXCHANGE ANNOUNCEMENT") April 26, 2016 To, Ms. D'souza AVP, Listing Department National Stock Exchange of India Exchange Plaza Bandra Complex Bandra (East) 400 001 Limited SUB: STANDARD CHARTERED PLC (THE "COMPANY") STOCK EXCHANGE

April 26, 2016 To, Ms. D'souza AVP, Listing Department National Stock Exchange of India Exchange Plaza Bandra Complex Bandra (East) 400 001 Limited SUB: STANDARD CHARTERED PLC (THE "COMPANY") STOCK EXCHANGE

Why is the Greek economy collapsing?

Why is the Greek economy collapsing? A simple tale of high multipliers and low exports Cinzia Alcidi and Daniel Gros 21 December 2012 W hy is Greece still mired in recession? Why has GDP fallen by close

Why is the Greek economy collapsing? A simple tale of high multipliers and low exports Cinzia Alcidi and Daniel Gros 21 December 2012 W hy is Greece still mired in recession? Why has GDP fallen by close

Quarterly Credit Conditions Survey Report

Quarterly Credit Conditions Survey Report Contents March 2014 Quarter Prepared by the Monetary Analysis & Programming Department Research & Economic Programming Division List of Tables and Charts 2 Background

Quarterly Credit Conditions Survey Report Contents March 2014 Quarter Prepared by the Monetary Analysis & Programming Department Research & Economic Programming Division List of Tables and Charts 2 Background

WHITE PAPER NO. 45 SECONDARY INVESTING IN PRIVATE EQUITY

WHITE PAPER NO. 45 SECONDARY INVESTING IN PRIVATE EQUITY Greycourt White Paper White Paper No. 45 A Brief Primer on Secondary Investing in Private Equity M uch has been written recently about secondary

WHITE PAPER NO. 45 SECONDARY INVESTING IN PRIVATE EQUITY Greycourt White Paper White Paper No. 45 A Brief Primer on Secondary Investing in Private Equity M uch has been written recently about secondary

Bank of America Merrill Lynch Banking & Insurance CEO Conference Bob Diamond

4 October 2011 Bank of America Merrill Lynch Banking & Insurance CEO Conference Bob Diamond Thank you and good morning. It s a pleasure to be here and I d like to thank our hosts for the opportunity to

4 October 2011 Bank of America Merrill Lynch Banking & Insurance CEO Conference Bob Diamond Thank you and good morning. It s a pleasure to be here and I d like to thank our hosts for the opportunity to

Project LINK Meeting New York, 20-22 October 2010. Country Report: Australia

Project LINK Meeting New York, - October 1 Country Report: Australia Prepared by Peter Brain: National Institute of Economic and Industry Research, and Duncan Ironmonger: Department of Economics, University

Project LINK Meeting New York, - October 1 Country Report: Australia Prepared by Peter Brain: National Institute of Economic and Industry Research, and Duncan Ironmonger: Department of Economics, University

Momentum in the housing market: affordability, indebtedness and risks

1 Momentum in the housing market: affordability, indebtedness and risks Speech given by Sir Jon Cunliffe, Deputy Governor Financial Stability, Member of the Monetary Policy Committee, Member of the Financial

1 Momentum in the housing market: affordability, indebtedness and risks Speech given by Sir Jon Cunliffe, Deputy Governor Financial Stability, Member of the Monetary Policy Committee, Member of the Financial

Deputy Governor Barbro Wickman-Parak The Swedish property federation, Stockholm. The property market and the financial crisis

SPEECH DATE: 17 June 2009 SPEAKER: LOCALITY: Deputy Governor Barbro Wickman-Parak The Swedish property federation, Stockholm SVERIGES RIKSBANK SE-103 37 Stockholm (Brunkebergstorg 11) Tel +46 8 787 00

SPEECH DATE: 17 June 2009 SPEAKER: LOCALITY: Deputy Governor Barbro Wickman-Parak The Swedish property federation, Stockholm SVERIGES RIKSBANK SE-103 37 Stockholm (Brunkebergstorg 11) Tel +46 8 787 00

BANK INTEREST RATE MARGINS

Reserve Bank of Australia Bulletin May BANK INTEREST RATE MARGINS Bank interest rate margins the difference between what interest rates banks borrow at and what they lend at have been the subject of much

Reserve Bank of Australia Bulletin May BANK INTEREST RATE MARGINS Bank interest rate margins the difference between what interest rates banks borrow at and what they lend at have been the subject of much

Agricultural borrowers are increasingly concerned

9 Agricultural Credit Standards Tighten By Jason Henderson, Vice President and Omaha Branch Executive Agricultural borrowers are increasingly concerned about access to credit. Amid economic weakness and

9 Agricultural Credit Standards Tighten By Jason Henderson, Vice President and Omaha Branch Executive Agricultural borrowers are increasingly concerned about access to credit. Amid economic weakness and

THE EURO AREA BANK LENDING SURVEY 3RD QUARTER OF 2014

THE EURO AREA BANK LENDING SURVEY 3RD QUARTER OF 214 OCTOBER 214 European Central Bank, 214 Address Kaiserstrasse 29, 6311 Frankfurt am Main, Germany Postal address Postfach 16 3 19, 666 Frankfurt am Main,

THE EURO AREA BANK LENDING SURVEY 3RD QUARTER OF 214 OCTOBER 214 European Central Bank, 214 Address Kaiserstrasse 29, 6311 Frankfurt am Main, Germany Postal address Postfach 16 3 19, 666 Frankfurt am Main,

A fresh perspective on Asset Based Lending (ABL)

") A fresh perspective on Asset Based Lending (ABL) While asset-based lending may often be considered last-resort funding, commercial borrowers of all types and sizes are using this flexible, cost-effective

A fresh perspective on Asset Based Lending (ABL) While asset-based lending may often be considered last-resort funding, commercial borrowers of all types and sizes are using this flexible, cost-effective

Statement to Parliamentary Committee

Statement to Parliamentary Committee Opening Remarks by Mr Glenn Stevens, Governor, in testimony to the House of Representatives Standing Committee on Economics, Sydney, 14 August 2009. The Bank s Statement

Statement to Parliamentary Committee Opening Remarks by Mr Glenn Stevens, Governor, in testimony to the House of Representatives Standing Committee on Economics, Sydney, 14 August 2009. The Bank s Statement

Outlook for Australian Property Markets 2010-2012. Perth

Outlook for Australian Property Markets 2010-2012 Perth Outlook for Australian Property Markets 2010-2012 Perth residential Population growth expected to remain at above average levels through to 2012

Outlook for Australian Property Markets 2010-2012 Perth Outlook for Australian Property Markets 2010-2012 Perth residential Population growth expected to remain at above average levels through to 2012

Svein Gjedrem: Prospects for the Norwegian economy

Svein Gjedrem: Prospects for the Norwegian economy Speech by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway), at Sparebank 1 SR-Bank Stavanger, Stavanger, 26 March 2010. The text below

Svein Gjedrem: Prospects for the Norwegian economy Speech by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway), at Sparebank 1 SR-Bank Stavanger, Stavanger, 26 March 2010. The text below

Contact: Ken Bond Deborah Hellinger Oracle Investor Relations Oracle Corporate Communications 1.650.607.0349 1.212.508.7935

For Immediate Release Contact: Ken Bond Deborah Hellinger Oracle Investor Relations Oracle Corporate Communications 1.650.607.0349 1.212.508.7935 ken.bond@oracle.com deborah.hellinger@oracle.com CLOUD

For Immediate Release Contact: Ken Bond Deborah Hellinger Oracle Investor Relations Oracle Corporate Communications 1.650.607.0349 1.212.508.7935 ken.bond@oracle.com deborah.hellinger@oracle.com CLOUD

Shared National Credits Program 2014 Leveraged Loan Supplement

Shared National Credits Program 2014 Leveraged Loan Supplement Board of Governors of the Federal Reserve System Federal Deposit Insurance Corporation Office of the Comptroller of the Currency Washington,

Shared National Credits Program 2014 Leveraged Loan Supplement Board of Governors of the Federal Reserve System Federal Deposit Insurance Corporation Office of the Comptroller of the Currency Washington,

Net income in the second quarter was 1.281 billion, compared to 538 million in the previous quarter and 578 million in the same quarter a year ago.

Press Presse Prensa For the business and financial press Munich/Erfurt, April 25, 2002 Siemens in the second quarter (January 1 to March 31) of fiscal 2002 Net income in the second quarter was 1.281 billion,

Press Presse Prensa For the business and financial press Munich/Erfurt, April 25, 2002 Siemens in the second quarter (January 1 to March 31) of fiscal 2002 Net income in the second quarter was 1.281 billion,

Deutsche Wohnen AG.» Investor Presentation. September 2010

Deutsche Wohnen AG» Investor Presentation September 21 1 » Agenda 1 2 3 4 Introduction to Deutsche Wohnen Portfolio Overview and Operations Financial Highlights Guidance and Strategic Objectives 2 » 1

Deutsche Wohnen AG» Investor Presentation September 21 1 » Agenda 1 2 3 4 Introduction to Deutsche Wohnen Portfolio Overview and Operations Financial Highlights Guidance and Strategic Objectives 2 » 1

2. The European insurance sector

2. The European insurance sector Insurance companies are still exposed to the low interest rate environment. Long-term interest rates are especially of importance to life insurers, since these institutions

2. The European insurance sector Insurance companies are still exposed to the low interest rate environment. Long-term interest rates are especially of importance to life insurers, since these institutions

X. INTERNATIONAL ECONOMIC DEVELOPMENT 1/

1/ X. INTERNATIONAL ECONOMIC DEVELOPMENT 1/ 10.1 Overview of World Economy Latest indicators are increasingly suggesting that the significant contraction in economic activity has come to an end, notably

1/ X. INTERNATIONAL ECONOMIC DEVELOPMENT 1/ 10.1 Overview of World Economy Latest indicators are increasingly suggesting that the significant contraction in economic activity has come to an end, notably

Cross Check. A Study of Qantas Financial Health. Almotairi Adhikari Saputro Vannadeth

Cross Check A Study of Qantas Financial Health Almotairi Adhikari Saputro Vannadeth 1 Financial Analysis of Qantas Airlines With Virgin Australia as benchmark (for the year 2011) Hamoud Almotairi Indra

Cross Check A Study of Qantas Financial Health Almotairi Adhikari Saputro Vannadeth 1 Financial Analysis of Qantas Airlines With Virgin Australia as benchmark (for the year 2011) Hamoud Almotairi Indra

Global Markets Update Signature Global Advisors

SIGNATURE GLOBAL ADVISORS MARKETS UPDATE AUGUST 3, 2011 The following comments come from an internal interview with Chief Investment Officer, Eric Bushell. They represent Signature s current market views

SIGNATURE GLOBAL ADVISORS MARKETS UPDATE AUGUST 3, 2011 The following comments come from an internal interview with Chief Investment Officer, Eric Bushell. They represent Signature s current market views

UK Economic Outlook. March 2015. The impact of lower oil prices on the UK economy

March 2015 UK Economic Outlook The impact of lower oil prices on the UK economy New job creation in the UK: which regions will benefit most from the digital revolution? www.pwc.co.uk/economics Contents

March 2015 UK Economic Outlook The impact of lower oil prices on the UK economy New job creation in the UK: which regions will benefit most from the digital revolution? www.pwc.co.uk/economics Contents

FOURTH QUARTER 2015. Financials. Safe Zephyrus is scheduled to commence a contract in Norway early Q3 2016.

FOURTH QUARTER 2015 Financials (Figures in brackets refer to the corresponding period of 2014) Full year 2015 Operating profit for 2015 amounted to USD 167 million (USD 248.3 million) and utilisation of

FOURTH QUARTER 2015 Financials (Figures in brackets refer to the corresponding period of 2014) Full year 2015 Operating profit for 2015 amounted to USD 167 million (USD 248.3 million) and utilisation of

Solutions to Chapter 4. Measuring Corporate Performance

Solutions to Chapter 4 Measuring Corporate Performance 1. a. 7,018 Long-term debt ratio 0. 42 7,018 9,724 b. 4,794 7,018 6,178 Total debt ratio 0. 65 27,714 c. 2,566 Times interest earned 3. 75 685 d.

Solutions to Chapter 4 Measuring Corporate Performance 1. a. 7,018 Long-term debt ratio 0. 42 7,018 9,724 b. 4,794 7,018 6,178 Total debt ratio 0. 65 27,714 c. 2,566 Times interest earned 3. 75 685 d.

INTEREST RATES: WHAT GOES UP MUST COME DOWN

3 INTEREST RATES: WHAT GOES UP MUST COME DOWN John M. Petersen Melvin Mark Capital Group, LLC What an interesting time to be asked to write something about interest rates! Our practice emphasis is commercial

3 INTEREST RATES: WHAT GOES UP MUST COME DOWN John M. Petersen Melvin Mark Capital Group, LLC What an interesting time to be asked to write something about interest rates! Our practice emphasis is commercial

Switzerland 2013 Article for Consultation Preliminary Conclusions Bern, March 18, 2013

Switzerland 2013 Article for Consultation Preliminary Conclusions Bern, March 18, 2013 With the exchange rate floor in place for over a year, the Swiss economy remains stable, though inflation remains

Switzerland 2013 Article for Consultation Preliminary Conclusions Bern, March 18, 2013 With the exchange rate floor in place for over a year, the Swiss economy remains stable, though inflation remains

The Future of Retirement The power of planning

The Future of Retirement The power of planning Singapore Report Foreword It has been our constant endeavour to make research available to our customers and distributors to create awareness for the need

The Future of Retirement The power of planning Singapore Report Foreword It has been our constant endeavour to make research available to our customers and distributors to create awareness for the need

The U.S. Financial Crisis:

JA Worldwide The U.S. Financial Crisis: Global Repercussions Introduction For many years, we have all heard talk of globalization. But what does it really mean? In the simplest of terms it refers to an

JA Worldwide The U.S. Financial Crisis: Global Repercussions Introduction For many years, we have all heard talk of globalization. But what does it really mean? In the simplest of terms it refers to an

Customer Financing. Nigel Taylor SVP Customer, Project and Structured Finance. Global Investor Forum 2009, Broughton, 1 st & 2 nd April 2009

Customer Financing Nigel Taylor SVP Customer, Project and Structured Finance Global Investor Forum 2009, Broughton, 1 st & 2 nd April 2009 1 Safe Harbour Statement Disclaimer This presentation includes

Customer Financing Nigel Taylor SVP Customer, Project and Structured Finance Global Investor Forum 2009, Broughton, 1 st & 2 nd April 2009 1 Safe Harbour Statement Disclaimer This presentation includes

Financial Crisis. How Firms in Eastern and Central Europe Fared through the Global Financial Crisis: Evidence from 2008 2010

Enterprise Surveys Enterprise Note Series Financial Crisis World Bank Group Enterprise Note No. 2 21 How Firms in Eastern and Central Europe Fared through the Global Financial Crisis: Evidence from 28

Enterprise Surveys Enterprise Note Series Financial Crisis World Bank Group Enterprise Note No. 2 21 How Firms in Eastern and Central Europe Fared through the Global Financial Crisis: Evidence from 28

2012 First Quarter Equity Market Review

Investment Insights 2012 First Quarter Equity Market Review By William Riegel, Head of Equity Investments After a volatile year in 2011, equity markets grew more confident in the first quarter of 2012.

Investment Insights 2012 First Quarter Equity Market Review By William Riegel, Head of Equity Investments After a volatile year in 2011, equity markets grew more confident in the first quarter of 2012.

wealth inequality The last three decades have witnessed The Stanford Center on Poverty and Inequality

national report card wealth inequality The Stanford Center on Poverty and Inequality By Edward N. Wolff Key findings After two decades of robust growth in middle class wealth, median net worth plummeted

national report card wealth inequality The Stanford Center on Poverty and Inequality By Edward N. Wolff Key findings After two decades of robust growth in middle class wealth, median net worth plummeted

Household Borrowing Behaviour: Evidence from HILDA

Household Borrowing Behaviour: Evidence from HILDA Ellis Connolly and Daisy McGregor* Over the 199s and the first half of the s, household debt grew strongly in response to lower nominal interest rates

Household Borrowing Behaviour: Evidence from HILDA Ellis Connolly and Daisy McGregor* Over the 199s and the first half of the s, household debt grew strongly in response to lower nominal interest rates

The CPA Australia Asia-Pacific Small Business Survey 2012. Australia, Hong Kong, Indonesia, Malaysia, New Zealand and Singapore

The CPA Australia Asia-Pacific Small Business Survey Australia, Hong Kong, Indonesia, Malaysia, New Zealand and Singapore CPA Australia Ltd ( CPA Australia ) is one of the world s largest accounting bodies

The CPA Australia Asia-Pacific Small Business Survey Australia, Hong Kong, Indonesia, Malaysia, New Zealand and Singapore CPA Australia Ltd ( CPA Australia ) is one of the world s largest accounting bodies

Executive Summary. 3 Attracting ~ ~ ~ ~ ~ ~ ~ ~ ~ ~

Visa Small Business REPORT AUGUST 0 Spend Insights Visa Small Business Spend Insights monitors the economic confidence of U.S. small business owners by analyzing Visa Business card spend data and responses

Visa Small Business REPORT AUGUST 0 Spend Insights Visa Small Business Spend Insights monitors the economic confidence of U.S. small business owners by analyzing Visa Business card spend data and responses

POSTBANK GROUP INTERIM MANAGEMENT STATEMENT AS OF MARCH 31, 2015

POSTBANK GROUP INTERIM MANAGEMENT STATEMENT AS OF MARCH 31, 2015 PRELIMINARY REMARKS MACROECONOMIC DEVELOPMENT BUSINESS PERFORMANCE PRELIMINARY REMARKS This document is an interim management statement

POSTBANK GROUP INTERIM MANAGEMENT STATEMENT AS OF MARCH 31, 2015 PRELIMINARY REMARKS MACROECONOMIC DEVELOPMENT BUSINESS PERFORMANCE PRELIMINARY REMARKS This document is an interim management statement

Is the global shipping industry heading for a new crisis?

Interview with Dagfinn Lunde Page 1 Is the global shipping industry heading for a new crisis Mr Dagfinn Lunde, Member of DVB s Board of Managing Directors responsible for Shipping Finance, was interviewed

Interview with Dagfinn Lunde Page 1 Is the global shipping industry heading for a new crisis Mr Dagfinn Lunde, Member of DVB s Board of Managing Directors responsible for Shipping Finance, was interviewed

Clint M. Hanni Partner Corporate Section of the Business Services Group

How to Negotiate Effectively with Your to Restructure a Loan PRESENTED BY: Clint M. Hanni Partner Corporate Section of the Business Services Group May 26, 2010 11:30 a.m. 1 p.m. Stoel Rives LLP One Utah

How to Negotiate Effectively with Your to Restructure a Loan PRESENTED BY: Clint M. Hanni Partner Corporate Section of the Business Services Group May 26, 2010 11:30 a.m. 1 p.m. Stoel Rives LLP One Utah

2014 Survey of Credit Underwriting Practices

2014 Survey of Credit Underwriting Practices Office of the Comptroller of the Currency Washington, D.C. December 2014 Contents Introduction... 1 Part I: Overall Results... 3 Primary Findings... 3 Commentary

2014 Survey of Credit Underwriting Practices Office of the Comptroller of the Currency Washington, D.C. December 2014 Contents Introduction... 1 Part I: Overall Results... 3 Primary Findings... 3 Commentary

The Great Eastern Shipping Company Limited Q1FY13 Conference call (August 10, 2012)

") The Great Eastern Shipping Company Limited Q1FY13 Conference call (August 10, 2012) Moderator: Good evening ladies and gentlemen. Welcome to GE Shipping s earnings call on declaration of its financial

The Great Eastern Shipping Company Limited Q1FY13 Conference call (August 10, 2012) Moderator: Good evening ladies and gentlemen. Welcome to GE Shipping s earnings call on declaration of its financial

Interim financial report for the period 1 January to 30 September 2011

Company announcement no. 11/ 18 November Page 1 of 9 Interim financial report for the period 1 January to 30 September Highlights Results improved in the third quarter with a gross profit of USD 8 million

Company announcement no. 11/ 18 November Page 1 of 9 Interim financial report for the period 1 January to 30 September Highlights Results improved in the third quarter with a gross profit of USD 8 million

Effects on pensioners from leaving the EU

Effects on pensioners from leaving the EU Summary 1.1 HM Treasury s short-term document presented two scenarios for the immediate impact of leaving the EU on the UK economy: the shock scenario and severe

Effects on pensioners from leaving the EU Summary 1.1 HM Treasury s short-term document presented two scenarios for the immediate impact of leaving the EU on the UK economy: the shock scenario and severe

Global Financials Update April 13, 2012

Global Financials Update April 13, 2012 Global Market Update After posting a fairly strong and consistent rally over much of the last six months, the global equity markets have changed course over the

Global Financials Update April 13, 2012 Global Market Update After posting a fairly strong and consistent rally over much of the last six months, the global equity markets have changed course over the

PwC FY 2013 Global Revenues Grow to US$32.1 billion

Press release Date EMBARGO 08:00 New York time Tuesday 1 October 2013 Contact Mike Davies + 44 20 7804 2378 Email: mike.davies@uk.pwc.com Mike Ascolese Tel: +1 646 471 8106 Email: mike.ascolese@us.pwc.com

Press release Date EMBARGO 08:00 New York time Tuesday 1 October 2013 Contact Mike Davies + 44 20 7804 2378 Email: mike.davies@uk.pwc.com Mike Ascolese Tel: +1 646 471 8106 Email: mike.ascolese@us.pwc.com

Supervisory Letter. Current Risks in Business Lending and Sound Risk Management Practices

Dollars in Billions Supervisory Letter Current Risks in Business Lending and Sound Risk Management Practices The September 2009 Financial Performance Report data reflects an increasing portion of loans

Dollars in Billions Supervisory Letter Current Risks in Business Lending and Sound Risk Management Practices The September 2009 Financial Performance Report data reflects an increasing portion of loans

How To Know The State Of Intermodal Trucking In The United States

The State of Intermodal Drayage David M. McLaughlin CONECT 2009 1 State of the Intermodal Industry Circa 2007 Consistent growth: 32% Increase 2000-2006 Dramatic increase in fuel costs from $1.40 per gallon

The State of Intermodal Drayage David M. McLaughlin CONECT 2009 1 State of the Intermodal Industry Circa 2007 Consistent growth: 32% Increase 2000-2006 Dramatic increase in fuel costs from $1.40 per gallon

Strategic priorities for UK businesses

Strategic priorities for UK businesses An independent report on the issues affecting today s CFOs Contents 03 04 06 09 10 11 Strategic priorities for UK businesses Executive summary The view from within:

Strategic priorities for UK businesses An independent report on the issues affecting today s CFOs Contents 03 04 06 09 10 11 Strategic priorities for UK businesses Executive summary The view from within:

367 Syngrou Avenue, 175 64 P. Faliro, Hellas Tel: 30 210 94 07 710-3, Fax: 30 210 94 07 716, e-mail: ten@tenn.gr Website: http://www.tenn.

TSAKOS ENERGY NAVIGATION LIMITED (TEN) 367 Syngrou Avenue, 175 64 P. Faliro, Hellas Tel: 30 210 94 07 710-3, Fax: 30 210 94 07 716, e-mail: ten@tenn.gr Website: http://www.tenn.gr Press Release March 19,

TSAKOS ENERGY NAVIGATION LIMITED (TEN) 367 Syngrou Avenue, 175 64 P. Faliro, Hellas Tel: 30 210 94 07 710-3, Fax: 30 210 94 07 716, e-mail: ten@tenn.gr Website: http://www.tenn.gr Press Release March 19,

Q4 2013 Investor Conference Call. February 19, 2014

Q4 2013 Investor Conference Call February 19, 2014 FORWARD-LOOKING STATEMENTS Certain statements in this document about our current and future plans, expectations and intentions, results, levels of activity,

Q4 2013 Investor Conference Call February 19, 2014 FORWARD-LOOKING STATEMENTS Certain statements in this document about our current and future plans, expectations and intentions, results, levels of activity,

2. Incidence, prevalence and duration of breastfeeding

2. Incidence, prevalence and duration of breastfeeding Key Findings Mothers in the UK are breastfeeding their babies for longer with one in three mothers still breastfeeding at six months in 2010 compared

2. Incidence, prevalence and duration of breastfeeding Key Findings Mothers in the UK are breastfeeding their babies for longer with one in three mothers still breastfeeding at six months in 2010 compared

Acerinox Press Release 2014 First Half Results. Page 0 / 10

Page 0 / 10 2014 First Half Results Acerinox's profit after taxes and minorities for the first half of 2014 is Euros 76.1 million, representing a rise of 373% on the same period in the prior year The Group's

Page 0 / 10 2014 First Half Results Acerinox's profit after taxes and minorities for the first half of 2014 is Euros 76.1 million, representing a rise of 373% on the same period in the prior year The Group's

COMMERCIAL LEASE TRENDS FOR 2014

COMMERCIAL LEASE TRENDS FOR 2014 Notes from a Presentation given by N B Maunder Taylor BSc (Hons) MRICS, Partner of Maunder Taylor The following is a written copy of the presentation given by Nicholas

COMMERCIAL LEASE TRENDS FOR 2014 Notes from a Presentation given by N B Maunder Taylor BSc (Hons) MRICS, Partner of Maunder Taylor The following is a written copy of the presentation given by Nicholas

ACE: Leader in the European Automotive Components Market

ACE: Leader in the European Automotive Components Market ACE 2012-2015 Strategy 21/12/2011 Following on from our Current Report in December 2010, ACE s management herein presents its 2011 update on the

ACE: Leader in the European Automotive Components Market ACE 2012-2015 Strategy 21/12/2011 Following on from our Current Report in December 2010, ACE s management herein presents its 2011 update on the

CHEMSYSTEMS. Report Abstract. Quarterly Business Analysis Quarter 1, 2012

CHEMSYSTEMS PPE PROGRAM Report Abstract Quarterly Business Analysis Petrochemical Cost Price and Margin for Olefins, Polyolefins, Vinyls, Aromatics, Styrenics, Polyester Intermediates and Propylene Derivatives.

CHEMSYSTEMS PPE PROGRAM Report Abstract Quarterly Business Analysis Petrochemical Cost Price and Margin for Olefins, Polyolefins, Vinyls, Aromatics, Styrenics, Polyester Intermediates and Propylene Derivatives.

Item No. 18 GREATER MANCHESTER FIRE & RESCUE AUTHORITY AUDIT COMMITTEE 23 RD JUNE 2010 AUTHORITY 24 TH JUNE 2010

GREATER MANCHESTER FIRE & RESCUE AUTHORITY Item No. 18 AUDIT COMMITTEE 23 RD JUNE 2010 AUTHORITY 24 TH JUNE 2010 TREASURY MANAGEMENT ANNUAL REPORT 2009/10 Report of the Treasurer 1. Introduction and Background

GREATER MANCHESTER FIRE & RESCUE AUTHORITY Item No. 18 AUDIT COMMITTEE 23 RD JUNE 2010 AUTHORITY 24 TH JUNE 2010 TREASURY MANAGEMENT ANNUAL REPORT 2009/10 Report of the Treasurer 1. Introduction and Background

Insurance Market Outlook

Munich Re Economic Research May 2016 Emerging countries in Asia still linchpin of global premium growth The offers a brief overview of how we expect the insurance markets to develop over the next ten years.

Munich Re Economic Research May 2016 Emerging countries in Asia still linchpin of global premium growth The offers a brief overview of how we expect the insurance markets to develop over the next ten years.