A8.800 Disbursing/Accounts Payable and Payroll. A8.847 Reconciliation of the Departmental Checking Account

|

|

|

- Robyn Lee

- 8 years ago

- Views:

Transcription

1 New Procedure Prepared by the Disbursing Office A8.800 Disbursing/Accounts Payable and Payroll A8.847 Reconciliation of the Departmental Checking Account 1. Purpose A8.847 January 2000 p 1 of 17 To provide procedures to perform monthly reconciliation of the Financial Management Information System (FMIS) Departmental Checking Account records to Bank records for review and control purposes. Check reconciliation is automated with the receipt of an electronic file of check numbers and check amounts of cashed checks from the Bank for each Departmental checking subaccount. The bank tape is run against the corresponding FMIS bank files identifying checks with non-matching check numbers and/or amounts and outstanding checks (uncashed)at the end of each month. Reconciliation activities address the listing of exceptions and the outstanding checks. 2. Responsibilities Reconciliation of the Departmental Checking account is a critical function for verification of cash balances at the University system level and detection of erroneous data entry in FMIS or Bank files. This is also a critical process for the detection of unauthorized Departmental checks (checks cashed at the Bank with no records in FMIS). a. The reconciler is responsible for conducting monthly reviews of Departmental checking account disbursement records and bank records to ensure proper maintenance of the checking account. b. The Fiscal Officer is responsible for ensuring that the Departmental checking account is being properly administered. The Fiscal Officer must review the findings of each reconciliation and initiate any appropriate action as required. c. The General Accounting and Loan Collection Office (GALC)is

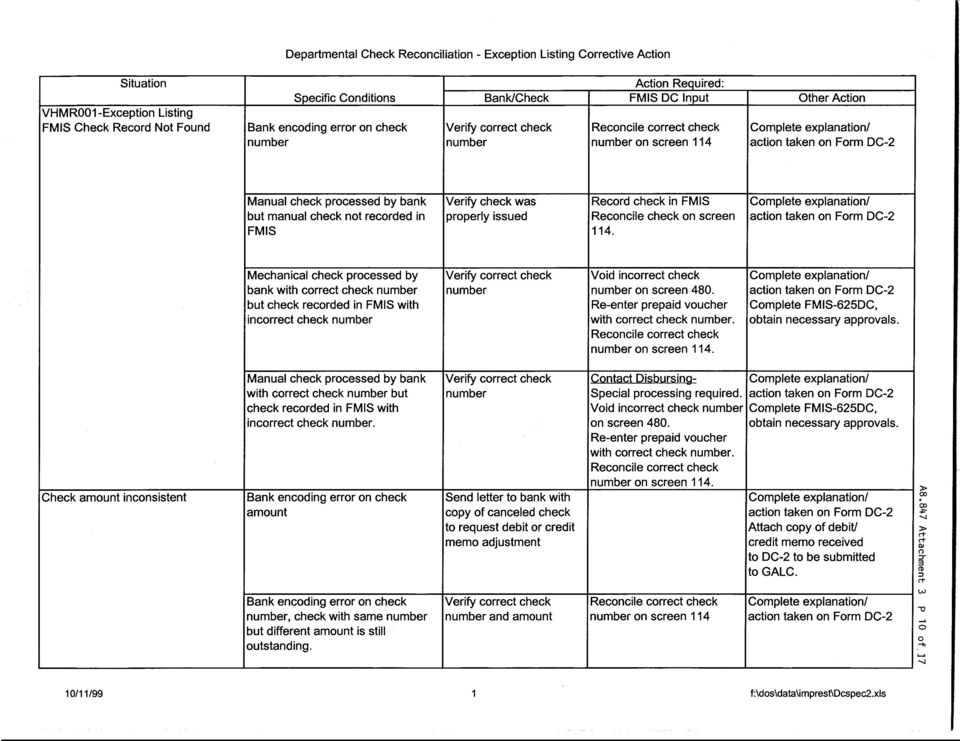

2 A8.847 p 2 of 17 responsible for the reconciliation of the pooled cash resources of the University of Hawai i General Account (UHGA concentration account). Monthly reconciliation of the UHGA cash balances require tracking of outstanding Departmental checks and reconciliation of exceptions. The General Accounting and Loan Collection Office will monitor the resolution of exception situations by Departmental personnel. 3. Guidelines a. The Fiscal Officer or the Campus/Department Head, who designates the reconciler, must ensure that the reconciler is an individual other than the custodian or the alternate. The Fiscal Officer may be the designated reconciler in those offices where staffing does not allow for the separation of duties. b. The reconciler will promptly conduct reconciliations at the end of each month and submit the original Departmental Checking Account Reconciliation, Form DC-2 (Attachment 1) to the General Accounting and Loan Collection Office (GALC),by the 30th day following the close of each month. The reconciliation report must be properly certified by the reconciler and the Fiscal Officer. If an exception is reported on the Check Reconciliation Report (VHMR001 - Attachment 2), clearly indicate the corrective action that is being initiated. c. If the reconciliation uncovers an exception situation, immediate action must be taken to resolve the situation. FMIS check records not found situations as reflected on the Check Reconciliation Report are extremely critical since the bank records reveal cashed checks which are not recorded in FMIS. The Exception Listing of the Check Reconciliation Report is a cumulative file that continues to list exceptions until they are resolved. Exceptions are resolved by the Bank when bank input errors are involved (e.g., erroneous check amount). Erroneous entries in FMIS require special corrective FMIS transactions (e.g., erroneous check number or amount entered on a manual check). Checks are to be manually reconciled on Screen 114 by the Reconciler upon resolution of the situation. Refer to the Departmental Checking User Guide for detailed instructions on the use of Screen 114.

3 A8.847 p 3 of 17 The Departmental Check Reconciliation - Exception Listing Corrective Action (Attachment 3)is a table that describes required actions to resolve various situations as reflected on the Exception Listing of the Check Reconciliation Report. Contact the General Accounting and Loan Collection Office for guidance in resolving situations listed on the Exception Listing. d. Campus/department units are responsible for maintaining proper documentation to support all Departmental checking account reconciliations including: 1) Departmental Checking Account Reconciliation (Form DC-2) 2) Check Reconciliation Report (VHMR001) 3) Check/Batch Log (Attachment 4) 4) Monthly Bank Statement 5) Canceled checks, bank debit/credit memos 6) Monthly Check Register (VHCR039) reflecting all Departmental checking account transactions (Attachment 5) 7) Consolidated Check Activity Report (VHMR094C), reflecting check numbers/ amounts of prior month s outstanding checks and current month s checks. (Attachment 6) 8) Voided Checks by Bank for the Month (VHMR094E) reflecting check numbers/amounts of voided checks (Attachment 7) 9) Any other relevant supporting documentation (e.g. FMIS- 625DC, follow-up letters on outstanding checks, stop payment orders, etc.) These documents are to be maintained in office files and made available for review upon request. 4. Procedures - Reconciliation a. Reconciliation Process

2) Check Reconciliation Report (VHMR001) 3) Check/Batch Log (Attachment 4) 4) Monthly Bank Statement 5) Canceled checks, bank debit/credit memos 6) Monthly Check Register (VHCR039)")

4 A8.847 p 4 of 17 The reconciliation process reviews the activities of the Departmental checking account for the specific month, resolves any identified exceptions, and reconciles the outstanding check balance. The reconciliation process must be performed on a timely basis. b. Reconciler's Activities 1) Obtain the unopened envelope containing the canceled checks and the bank statement for the month. a) Canceled checks are listed numerically on the bank statement. Matching of the Bank canceled check listing against the FMIS Departmental check file is automated and produces the Monthly Check Reconciliation Report VHMR001 - Exception Listing. b) Research each item on the Exception Listing and initiate appropriate action as described in the Departmental Check Reconciliation - Exception Listing Corrective Action (Attachment 3). Contact the General Accounting and Loan Collection Office for clarification if required. c) Based on the automated reconciliation, the Consolidated Check Activity Report (VHMR094C) is produced and displays the status of the prior month s outstanding check and the current month s checks as of the end of the month. The checks are sorted by check date and check number and appropriate follow-up action on the outstanding checks is to be initiated as follows: S S S The listing of outstanding checks must be reviewed for aging (number of days outstanding). It is suggested that letters of inquiry be sent to those vendors/payees that have been issued checks that are outstanding for a significant period (prior to the 180-day limit). Initiate any required action based on responses to inquiries. A follow-up stale dated check inquiry should be sent to vendors/payees for any outstanding

5 A8.847 p 5 of 17 check exceeding the 180-day limit (sample - Attachment 8). Technically, the checks are no longer negotiable and must be properly enfaced (updated) before it can be cashed. 2) Verify FMIS-625DC and related voided checks processed for that month against report VHMR094E - Voided Checks by Bank for Current Month. Verify all other voided checks (e.g. system voided checks due to check printing errors) against the VHMR094C - Consolidated Check Activity Report and Check/Batch Log. 3) Complete the Departmental Checking Account Reconciliation (Form DC-2). 4) Examine the Check/Batch Log, the Check Register (VHCR038), and the supply of unissued checks to account for all checks. Should any checks appear to be missing, immediate follow-up action is required including the issuances of stop payment orders if appropriate (Refer to A Special Departmental Checking Account Procedures). 5) Review canceled checks for unauthorized signatures, alterations, or irregular endorsements. If any incidents of altered checks or forgery are uncovered, initiate the procedures reflected in A Special Departmental Checking Account Procedures. c. Departmental Checking Account Reconciliation (Form DC-2) Complete the Departmental Checking Account Reconciliation (Form DC-2) as follows: 1) Date: Enter the month and year of the reconciliation. 2) FMIS Bank: Enter the Departmental Checking Bank number, (e.g ) 3) UH Campus/Department: Enter the appropriate campus and department (e.g. Agr-Bio Chem, Honolulu CC, etc.). 4) Custodian: Enter the name of the custodian of the Departmental checking account.

against the VHMR094C - Consolidated Check Activity Report and Check/Batch Log.")

6 A8.847 p 6 of 17 5) Cumulative Exception Listing: Enter the data reflected on the Check Reconciliation Report (VHMR001) - Cumulative Exception Listing on to the form. Provide an explanation and describe the action taken to resolve the situation. Refer to Attachment 3 for guidelines in resolving exception situations. 6) Reconciliation of Outstanding Checks: a) Enter the total outstanding amount from Consolidated Check Activity Report (VHMR094C). b) Enter any reconciling items - e.g. exception items listed as outstanding, difference in prepaid check amount, prepaid check not recorded, etc. Contact the General Accounting and Loan Collection Office for clarification if required. c) Enter the adjusted total outstanding check amount. 7) Reconciliation of Checks Cashed: a) Enter the Checks Cashed total from Consolidated Check Activity Report (VHMR094C). b) Enter the total unreconciled items for the month per Check Reconciliation (VHMR001) - Monthly Exception Listing. c) Enter the total manually reconciled checks for the month. d) Add items 7.a. and 7.b., subtract item 7.c. and enter total. e) Enter the Total Checks cashed per bank statement. f) Enter the difference of item 7.d and 7.e. Result should equal zero. Contact the General Accounting and Loan Collection Office for clarification if required. 8) Attach supporting documents: a) Copy of Bank Statement

Enter the adjusted total outstanding check amount.")

7 A8.847 p 7 of 17 b) Copy of Bank Debit or Credit memo issued to correct bank errors. 9) Reconciler, Fiscal Officer Signature and Date: The reconciler and the Fiscal Officer are to sign and date the form to certify the accuracy of the information provided. 5. Availability of Forms The Departmental Checking Account Reconciliation (Form DC-2) should be reproduced as required.

should be")

8

9

10

11

12

13

14

15

16

17

A8.800 Disbursing/Accounts Payable and Payroll. A8.845 Procedures to Establish, Close, and Change Custodian/ Alternate - Departmental Checking Account

New Procedure Prepared by the Disbursing Office A8.800 Disbursing/Accounts Payable and Payroll A8.845 Procedures to Establish, Close, and Change Custodian/ Alternate - Departmental Checking Account A8.845

New Procedure Prepared by the Disbursing Office A8.800 Disbursing/Accounts Payable and Payroll A8.845 Procedures to Establish, Close, and Change Custodian/ Alternate - Departmental Checking Account A8.845

This technical note discusses the different reports you can generate as well as the use of each report in reconciling bank accounts.

Article # 1241 Technical Note: Reports Useful for Reconciling the Bank Account Difficulty Level: Beginner Level AccountMate User Version(s) Affected: AccountMate 8 for SQL, Express and LAN AccountMate

Article # 1241 Technical Note: Reports Useful for Reconciling the Bank Account Difficulty Level: Beginner Level AccountMate User Version(s) Affected: AccountMate 8 for SQL, Express and LAN AccountMate

State Accounting Office

State Accounting Office State Accounting Manual Policies and Procedures Policy Number CM-100008 Section Name Cash Management Policy Name Bank Reconciliation Effective Date 3/13/2007 Revised Date I. Purpose/Scope

State Accounting Office State Accounting Manual Policies and Procedures Policy Number CM-100008 Section Name Cash Management Policy Name Bank Reconciliation Effective Date 3/13/2007 Revised Date I. Purpose/Scope

Department of Human Services Client Trust Fund 7290 Trust Accounting System Procedures

Human Services Client Trust Fund 7290 Trust Accounting System Procedures 03.004.00 Effective Date: September 12, 1997 Revised: December 28, 2015 Department of Human Services Client Trust Fund 7290 Trust

Human Services Client Trust Fund 7290 Trust Accounting System Procedures 03.004.00 Effective Date: September 12, 1997 Revised: December 28, 2015 Department of Human Services Client Trust Fund 7290 Trust

for Sage 100 ERP Bank Reconciliation Overview Document

for Sage 100 ERP Bank Reconciliation Document 2012 Sage Software, Inc. All rights reserved. Sage Software, Sage Software logos, and the Sage Software product and service names mentioned herein are registered

for Sage 100 ERP Bank Reconciliation Document 2012 Sage Software, Inc. All rights reserved. Sage Software, Sage Software logos, and the Sage Software product and service names mentioned herein are registered

Florida A & M University Bank Reconciliation Procedures

TABLE OF CONTENTS 1.0 OVERVIEW...2 2.0 DEFINITIONS...2 3.0 RESPONSIBILITIES..2 4.0 GENERAL PROCEDURES...2 4.1 BANK RECONCILIATIONS.2 4.2 RECORDS 6 1.0 Overview The University currently maintains four bank

TABLE OF CONTENTS 1.0 OVERVIEW...2 2.0 DEFINITIONS...2 3.0 RESPONSIBILITIES..2 4.0 GENERAL PROCEDURES...2 4.1 BANK RECONCILIATIONS.2 4.2 RECORDS 6 1.0 Overview The University currently maintains four bank

A8.800 Disbursing/Accounts Payable and Payroll

Prepared by the Disbursing Office This is a New Administrative Procedure A8.839 July 1996 A8.800 Disbursing/Accounts Payable and Payroll p 1 of 28 A8.839 Accounts Payable Processing 1. Purpose To establish

Prepared by the Disbursing Office This is a New Administrative Procedure A8.839 July 1996 A8.800 Disbursing/Accounts Payable and Payroll p 1 of 28 A8.839 Accounts Payable Processing 1. Purpose To establish

Department of Sociology Cash Handling Procedures Fiscal Year 2016

Department of Sociology Cash Handling Procedures Fiscal Year 2016 I. PURPOSE AND OVERVIEW In accordance with MAPP 05.01.01, Cash Handling, all cash transactions involving the University, its colleges,

Department of Sociology Cash Handling Procedures Fiscal Year 2016 I. PURPOSE AND OVERVIEW In accordance with MAPP 05.01.01, Cash Handling, all cash transactions involving the University, its colleges,

A8.700 TREASURY. This directive applies to all campuses of the University of Hawai i.

Prepared by Treasury Office. This amends A8.710 dated July 2001. A8.710 April 2005 A8.700 TREASURY P 1 of 5 A8.710 Credit Card Program 1. Purpose To provide uniform procedures for the processing of credit

Prepared by Treasury Office. This amends A8.710 dated July 2001. A8.710 April 2005 A8.700 TREASURY P 1 of 5 A8.710 Credit Card Program 1. Purpose To provide uniform procedures for the processing of credit

Cash, Petty Cash, Change Funds, and Credit Cards

CASH As public servants, it is our responsibility to safeguard taxpayer s dollars while adhering to laws and regulations governing processes over cash handling. Internal controls over cash are necessary

CASH As public servants, it is our responsibility to safeguard taxpayer s dollars while adhering to laws and regulations governing processes over cash handling. Internal controls over cash are necessary

Internal Controls and Political Committees

Internal Controls and Political Committees Under the Federal Election Campaign Act (FECA) and the Commission s regulations all political committees are required to file accurate and complete disclosure

Internal Controls and Political Committees Under the Federal Election Campaign Act (FECA) and the Commission s regulations all political committees are required to file accurate and complete disclosure

Prepared by General Accounting & Loan Collection Office. Replaces Administrative Procedure A8.651 dated July 1982. A8.651

Prepared by General Accounting & Loan Collection Office. Replaces Administrative Procedure A8.651 dated July 1982. A8.651 A8.600 Accounting April 2002 P 1 of 12 A8.651 Accounts Receivable 1. Purpose To

Prepared by General Accounting & Loan Collection Office. Replaces Administrative Procedure A8.651 dated July 1982. A8.651 A8.600 Accounting April 2002 P 1 of 12 A8.651 Accounts Receivable 1. Purpose To

The policy and procedural guidelines contained in this handbook are designed to:

BASIC POLICY STATEMENT The Mikva Challenge is committed to responsible financial management. The entire organization including the board of directors, administrators, and staff will work together to make

BASIC POLICY STATEMENT The Mikva Challenge is committed to responsible financial management. The entire organization including the board of directors, administrators, and staff will work together to make

POLICY & PROCEDURE DOCUMENT NUMBER: 3.3011. DIVISION: Finance & Administration. TITLE: Cash Operations Policy and Procedures. DATE: July 15, 2011

POLICY & PROCEDURE DOCUMENT NUMBER: 3.3011 DIVISION: Finance & Administration TITLE: Cash Operations Policy and Procedures DATE: July 15, 2011 Authorized by: K. Ann Mead, VP for Finance & Administration

POLICY & PROCEDURE DOCUMENT NUMBER: 3.3011 DIVISION: Finance & Administration TITLE: Cash Operations Policy and Procedures DATE: July 15, 2011 Authorized by: K. Ann Mead, VP for Finance & Administration

PROCEDURE. Accounts Payable

THE RICHARD STOCKTON COLLEGE OF NEW JERSEY PROCEDURE Accounts Payable Procedure Administrator: Associate Vice President for Administration and Finance Authority: N.J.S.A. 18A:64-6 Effective Date: January

THE RICHARD STOCKTON COLLEGE OF NEW JERSEY PROCEDURE Accounts Payable Procedure Administrator: Associate Vice President for Administration and Finance Authority: N.J.S.A. 18A:64-6 Effective Date: January

Overview A. What is the Visa Purchasing card?

Overview A. What is the Visa Purchasing card? The Purchasing Card is a Visa Card used by The University of Winnipeg employees to purchase materials and services up to $999.99 per item (excluding sales

Overview A. What is the Visa Purchasing card? The Purchasing Card is a Visa Card used by The University of Winnipeg employees to purchase materials and services up to $999.99 per item (excluding sales

APPENDIX A DRAFT Policy DIE-1 School Funds: Audit & Financial Monitoring Procedures

APPENDIX A DRAFT Policy DIE-1 School Funds: Audit & Financial Monitoring Procedures Administrative Guidelines Financial Monitoring Procedures The following Administrative Guidelines support the Principal

APPENDIX A DRAFT Policy DIE-1 School Funds: Audit & Financial Monitoring Procedures Administrative Guidelines Financial Monitoring Procedures The following Administrative Guidelines support the Principal

Reconciliation of Cash

2. Trial Balance Notes Trial Balance and Reconciliation of Cash Trial balance: w used to confirm that accounts receivable, program expenditures, and cash balance equal amount of funds authorized and should

2. Trial Balance Notes Trial Balance and Reconciliation of Cash Trial balance: w used to confirm that accounts receivable, program expenditures, and cash balance equal amount of funds authorized and should

Accounts Payable User Manual

Accounts Payable User Manual Confidential Information This document contains proprietary and valuable, confidential trade secret information of APPX Software, Inc., Richmond, Virginia Notice of Authorship

Accounts Payable User Manual Confidential Information This document contains proprietary and valuable, confidential trade secret information of APPX Software, Inc., Richmond, Virginia Notice of Authorship

Agency Escrow Accounting Standards.

Agency Escrow Accounting Standards. Title Insurers State regulatory divisions, financial institutions, national groups, and others rely on Title Insurance underwriters to develop programs and practices

Agency Escrow Accounting Standards. Title Insurers State regulatory divisions, financial institutions, national groups, and others rely on Title Insurance underwriters to develop programs and practices

Pitt County Schools Individual School Accounting. Internal Controls and Responsibilities Fiscal Year 2009-10

Individual School Accounting Internal Controls and Responsibilities Fiscal Year 2009-10 Individual School Accounting Internal Controls and Responsibilities Fiscal Year 2009-10 Contents Page Principal Statement

Individual School Accounting Internal Controls and Responsibilities Fiscal Year 2009-10 Individual School Accounting Internal Controls and Responsibilities Fiscal Year 2009-10 Contents Page Principal Statement

Unit 2 The Basic Accounting Cycle

Unit 2 The Basic Accounting Cycle Chapter 3 Chapter 4 Chapter 5 Chapter 6 Chapter 7 Chapter 8 Chapter 9 Business Transactions and the Accounting Equation Transactions That Affect Assets, Liabilities, and

Unit 2 The Basic Accounting Cycle Chapter 3 Chapter 4 Chapter 5 Chapter 6 Chapter 7 Chapter 8 Chapter 9 Business Transactions and the Accounting Equation Transactions That Affect Assets, Liabilities, and

ADMINISTRATIVE PRACTICE LETTER

ADMINISTRATIVE PRACTICE LETTER SUBJECT: PETTY CASH Section I - E Issue 6 Page 1 of 2 Effective 7/10/07 GENERAL Each petty cash fund is in the sole custody of a business manager who is responsible to the

ADMINISTRATIVE PRACTICE LETTER SUBJECT: PETTY CASH Section I - E Issue 6 Page 1 of 2 Effective 7/10/07 GENERAL Each petty cash fund is in the sole custody of a business manager who is responsible to the

Accounting for Cash. College Accounting. Heintz & Parry CASH INTERNAL CONTROL OPENING A CHECKING ACCOUNT

Heintz & Parry 0 th Edition Chapter 0 th Edition College Accounting Accounting for Cash CASH INTERNAL CONTROL Includes: Currency, coins, and checking accounts Checks received from customers Money orders

Heintz & Parry 0 th Edition Chapter 0 th Edition College Accounting Accounting for Cash CASH INTERNAL CONTROL Includes: Currency, coins, and checking accounts Checks received from customers Money orders

CASH HANDLING POLICY

COUNTY OF SAN LUIS OBISPO OFFICE OF THE AUDITOR-CONTROLLER CASH HANDLING POLICY Revised September 22, 2008 COUNTY OF SAN LUIS OBISPO OFFICE OF THE AUDITOR-CONTROLLER CASH HANDLING POLICY FORWARD This manual

COUNTY OF SAN LUIS OBISPO OFFICE OF THE AUDITOR-CONTROLLER CASH HANDLING POLICY Revised September 22, 2008 COUNTY OF SAN LUIS OBISPO OFFICE OF THE AUDITOR-CONTROLLER CASH HANDLING POLICY FORWARD This manual

B Resource Guide: Implementing Financial Controls

What s in this Guide: I. Definition: What are Financial Controls? II. Why Do You Need Financial Controls? III. Best Practices: Financial Controls to Consider I. Definition: What are Financial Controls?

What s in this Guide: I. Definition: What are Financial Controls? II. Why Do You Need Financial Controls? III. Best Practices: Financial Controls to Consider I. Definition: What are Financial Controls?

Archdiocese of Chicago Parish Self-Assessment Checklist

Self-Assessment Questions 1. Are written Parish Finance Council guidelines and norms defined, documented, and available to all Parish Finance Council members? 2. Are Archdiocesan best practices communicated

Self-Assessment Questions 1. Are written Parish Finance Council guidelines and norms defined, documented, and available to all Parish Finance Council members? 2. Are Archdiocesan best practices communicated

CASH RECONCILIATION & INTERNAL CONTROLS

CASH RECONCILIATION & INTERNAL CONTROLS Montana Clerks, Treasurers & Finance Officers Institute ~ May 2011 Presented by: Brenda Schneider, Superior; Doris Pinkerton, Forsyth & Darla Erickson, Local Government

CASH RECONCILIATION & INTERNAL CONTROLS Montana Clerks, Treasurers & Finance Officers Institute ~ May 2011 Presented by: Brenda Schneider, Superior; Doris Pinkerton, Forsyth & Darla Erickson, Local Government

Accounts Payable. Best Practices: Existing Control: Control Gap: Controls Evaluation and Gap Analysis. Purchasing

Accounts Payable Gap Analysis: POS identifies the following Best Practices as efficient and effective control processes for the above risk. Listed for comparison are the controls currently in place, if

Accounts Payable Gap Analysis: POS identifies the following Best Practices as efficient and effective control processes for the above risk. Listed for comparison are the controls currently in place, if

1501 BANKING RELATIONSHIPS

1501 BANKING RELATIONSHIPS Effective: December 1986 Revised: May 2013 Responsible Office: Treasurer Approval: Treasurer The Vice President for Finance and Treasurer is responsible for the efficient operations

1501 BANKING RELATIONSHIPS Effective: December 1986 Revised: May 2013 Responsible Office: Treasurer Approval: Treasurer The Vice President for Finance and Treasurer is responsible for the efficient operations

INTERNAL CONTROLS IC INTERNAL SELF-ASSESSMENT IMPREST CHECKING (BANK) ACCOUNTS INTERNAL CONTROLS SELF- ASSESSMENT FOR IMPREST CHECKING (BANK) ACCOUNTS

ACCOUNTS INTERNAL CONTROLS SELF- ASSESSMENT FOR IMPREST CHECKING (BANK) ACCOUNTS") ASSESSMENT TO BE COMPLETED INTERNAL CONTROLS IC INTERNAL CONTROLS SELF-ASSESSMENT The for Imprest Checking (Bank) Accounts was developed as a multipurpose tool to assess a unit s compliance with internal

ASSESSMENT TO BE COMPLETED INTERNAL CONTROLS IC INTERNAL CONTROLS SELF-ASSESSMENT The for Imprest Checking (Bank) Accounts was developed as a multipurpose tool to assess a unit s compliance with internal

UCLA Policy 360: Internal Control Guidelines for Campus Departments

UCLA Policy 360: Internal Control Guidelines for Campus Departments Issuing Officer: Assistant Vice Chancellor, Corporate Financial Services Responsible Dept: Financial Management Programs Effective Date:

UCLA Policy 360: Internal Control Guidelines for Campus Departments Issuing Officer: Assistant Vice Chancellor, Corporate Financial Services Responsible Dept: Financial Management Programs Effective Date:

Bank Account Reconciliation, Bank Account Access and Automated Clearing House (ACH) Transactions Review

Transactions Review") Internal Audit Department 350 South 5th Street, Suite 302 Minneapolis, MN 55415-1316 (612) 673-2056 Audit Team on the Engagement: Kelcie Brady, Student Intern Jacob L. Claeys Lauren Heir, Student Intern

Internal Audit Department 350 South 5th Street, Suite 302 Minneapolis, MN 55415-1316 (612) 673-2056 Audit Team on the Engagement: Kelcie Brady, Student Intern Jacob L. Claeys Lauren Heir, Student Intern

ABC School System Sample RFP. Request For Proposal. Banking Services

ABC School System Sample RFP Request For Proposal Banking Services PROPOSAL FOR BANKING SERVICES ABC School District I. OBJECTIVE The objective of this Request For Proposal is to identify the banking institution

ABC School System Sample RFP Request For Proposal Banking Services PROPOSAL FOR BANKING SERVICES ABC School District I. OBJECTIVE The objective of this Request For Proposal is to identify the banking institution

Vance County Schools Individual School Accounting

Individual School Accounting Internal Controls and Responsibilities Individual School Accounting Internal Controls and Responsibilities Contents Page Principal Statement of Understanding 3 Treasurer Statement

Individual School Accounting Internal Controls and Responsibilities Individual School Accounting Internal Controls and Responsibilities Contents Page Principal Statement of Understanding 3 Treasurer Statement

How To Reconcile Account Balance In Gpa

No.: G02 Page: 1 of 9 General: Depository bank account reconciliations must be submitted monthly to Statewide Fund Accounting prior to the end of the month following the period of the reconciliation. Earlier

No.: G02 Page: 1 of 9 General: Depository bank account reconciliations must be submitted monthly to Statewide Fund Accounting prior to the end of the month following the period of the reconciliation. Earlier

May 13, 2013. Mr. Steven T. Miller Acting Commissioner of Internal Revenue

United States Government Accountability Office Washington, DC 20548 May 13, 2013 Mr. Steven T. Miller Acting Commissioner of Internal Revenue Subject: Management Report: Improvements Are Needed to Enhance

United States Government Accountability Office Washington, DC 20548 May 13, 2013 Mr. Steven T. Miller Acting Commissioner of Internal Revenue Subject: Management Report: Improvements Are Needed to Enhance

004. Scope. This rule shall apply to all title insurers authorized to do business in Nebraska and all title insurance agents licensed in Nebraska.

Title 210 - NEBRASKA DEPARTMENT OF INSURANCE Chapter 34 - TITLE INSURANCE 001. Authority. This rule is adopted and promulgated by the Director of Insurance of the State of Nebraska pursuant to the Title

Title 210 - NEBRASKA DEPARTMENT OF INSURANCE Chapter 34 - TITLE INSURANCE 001. Authority. This rule is adopted and promulgated by the Director of Insurance of the State of Nebraska pursuant to the Title

Accounting and Administrative Manual Section 100: Accounting and Finance

No.: G-03 Page: 1 of 6 General: The application of good financial management requires the prompt reconciliation of accounts. Since departmental revenue and expenditure accounts are scrutinized monthly

No.: G-03 Page: 1 of 6 General: The application of good financial management requires the prompt reconciliation of accounts. Since departmental revenue and expenditure accounts are scrutinized monthly

1. Storeroom supplies -- For items stocked in the Palmer storeroom, use the Requisition for Supplies Form.

DISBURSEMENT PROCESSES Millersville University uses the Accounts Payable module of Banner Finance System to process vendor payments. After payroll, payments for goods and/or services represent the second

DISBURSEMENT PROCESSES Millersville University uses the Accounts Payable module of Banner Finance System to process vendor payments. After payroll, payments for goods and/or services represent the second

Florida A & M University

Florida A & M University AP PROCEDURES 3-8-2013 TABLE OF CONTENTS 1.0 OVERVIEW... 1 2.0 DEFINITIONS... 1 3.0 RESPONSIBILITIES... 2 4.0 GENERAL PROCEDURES... 3 4.1 DEPARTMENTAL FISCAL REPRESENTATIVES...

Florida A & M University AP PROCEDURES 3-8-2013 TABLE OF CONTENTS 1.0 OVERVIEW... 1 2.0 DEFINITIONS... 1 3.0 RESPONSIBILITIES... 2 4.0 GENERAL PROCEDURES... 3 4.1 DEPARTMENTAL FISCAL REPRESENTATIVES...

PROCEDURES for CAMPUS CASH MANAGEMENT POLICY ADM-0113 California State University, Sacramento. CASH HANDLING Updated February 2014

PROCEDURES for CAMPUS CASH MANAGEMENT POLICY ADM-0113 California State University, Sacramento CASH HANDLING Updated February 2014 I. ACCEPTING UNIVERSITY FUNDS II. III. IV. CASH CHANGE FUNDS SAFEGUARDING

PROCEDURES for CAMPUS CASH MANAGEMENT POLICY ADM-0113 California State University, Sacramento CASH HANDLING Updated February 2014 I. ACCEPTING UNIVERSITY FUNDS II. III. IV. CASH CHANGE FUNDS SAFEGUARDING

INTERNATIONAL BANKING AND CASH MANAGEMENT TULANE INTERNATIONAL

INTERNATIONAL BANKING AND CASH MANAGEMENT TULANE INTERNATIONAL RESPONSIBLE TULANE INTERNATIONAL OFFICIAL: Treasurer 1 RESPONSIBLE OFFICE: Tulane International Financial Office COORDINATING DEPARTMENTS:

INTERNATIONAL BANKING AND CASH MANAGEMENT TULANE INTERNATIONAL RESPONSIBLE TULANE INTERNATIONAL OFFICIAL: Treasurer 1 RESPONSIBLE OFFICE: Tulane International Financial Office COORDINATING DEPARTMENTS:

ABC Division Cash Handling Procedures Fiscal Year 20XX

ABC Division Cash Handling Procedures Fiscal Year 20XX I. PURPOSE AND OVERVIEW In accordance with MAPP 05.01.01, Cash Handling, all cash transactions involving the University, its colleges, or any departments

ABC Division Cash Handling Procedures Fiscal Year 20XX I. PURPOSE AND OVERVIEW In accordance with MAPP 05.01.01, Cash Handling, all cash transactions involving the University, its colleges, or any departments

Chapter 15: Accounts Payable and Purchases

Accounting Research Manager - Audit Private Accounting Research Manager Miller Interpretations and Other Resources Knowledge-Based Audit Procedures Chapter 15: Accounts Payable and Purchases Chapter 15:

Accounting Research Manager - Audit Private Accounting Research Manager Miller Interpretations and Other Resources Knowledge-Based Audit Procedures Chapter 15: Accounts Payable and Purchases Chapter 15:

Caused By 1. Time. 2. Errors. lags $ XXX. but not by bank (e.g., deposits. Add: Deposits recorded by business. Cash balance per bank statement

ILLUSTRATION 8-5 BANK RECONCILIATION FORMAT Balances Should Agree Bank Reconciliation (Date) balance per bank statement Add: Deposits recorded by business but not by bank (e.g., deposits in transit) Less:Charges

ILLUSTRATION 8-5 BANK RECONCILIATION FORMAT Balances Should Agree Bank Reconciliation (Date) balance per bank statement Add: Deposits recorded by business but not by bank (e.g., deposits in transit) Less:Charges

Oklahoma State University Policy and Procedures

Oklahoma State University Policy and Procedures COLLECTIONS, DEPOSIT AND CONTROL OF CASH OR CHECKS RECEIVED IN THE NAME OF OKLAHOMA STATE UNIVERSITY 3-0331 ADMINISTRATION & FINANCE May 2008 POLICY AND

Oklahoma State University Policy and Procedures COLLECTIONS, DEPOSIT AND CONTROL OF CASH OR CHECKS RECEIVED IN THE NAME OF OKLAHOMA STATE UNIVERSITY 3-0331 ADMINISTRATION & FINANCE May 2008 POLICY AND

ASSOCIATED STUDENTS, INCORPORATED CALIFORNIA STATE UNIVERSITY, LONG BEACH DATE REVISED: 04/10/2013

Cash Handling BACKGROUND AND PURPOSE...1 POLICY STATEMENT...2 WHO SHOULD KNOW THIS POLICY...2 DEFINITIONS...2 STANDARDS AND PROCEDURES...3 1.0 CONDITIONS FOR EMPLOYMENT IN CASH HANDLING ENVIRONMENT...3

Cash Handling BACKGROUND AND PURPOSE...1 POLICY STATEMENT...2 WHO SHOULD KNOW THIS POLICY...2 DEFINITIONS...2 STANDARDS AND PROCEDURES...3 1.0 CONDITIONS FOR EMPLOYMENT IN CASH HANDLING ENVIRONMENT...3

Standard Procedures and Controls for the Title Industry. Prepared by the ALTA Internal Auditing Committee ALTA

Standard Procedures and Controls for the Title Industry Prepared by the ALTA Internal Auditing Committee ALTA The American Land Title Association, founded in 1907, is the national trade association and

Standard Procedures and Controls for the Title Industry Prepared by the ALTA Internal Auditing Committee ALTA The American Land Title Association, founded in 1907, is the national trade association and

Prepared by the Disbursing Office This replaces Administrative Procedure A8.883 dated May 1992 A8.883 July 1996

Prepared by the Disbursing Office This replaces Administrative Procedure A8.883 dated May 1992 A8.883 July 1996 A8.800 Disbursing/Accounts Payable and Payroll p 1 of 11 A8.883 Student, Casual and Overload

Prepared by the Disbursing Office This replaces Administrative Procedure A8.883 dated May 1992 A8.883 July 1996 A8.800 Disbursing/Accounts Payable and Payroll p 1 of 11 A8.883 Student, Casual and Overload

DIXON MONTESSORI CHARTER SCHOOL FISCAL CONTROL POLICY

DIXON MONTESSORI CHARTER SCHOOL FISCAL CONTROL POLICY 1. Purpose The Dixon Montessori Charter School Board of Directors ( Board ) has reviewed and adopted the following policies and procedures to ensure

DIXON MONTESSORI CHARTER SCHOOL FISCAL CONTROL POLICY 1. Purpose The Dixon Montessori Charter School Board of Directors ( Board ) has reviewed and adopted the following policies and procedures to ensure

PURCHASING CARD POLICY AND PROCEDURES

PURCHASING CARD POLICY AND PROCEDURES 1. PURPOSE To establish policies and procedures for procuring goods and/or services using a Purchasing Card. Purchasing Cards are referred to throughout this policy

PURCHASING CARD POLICY AND PROCEDURES 1. PURPOSE To establish policies and procedures for procuring goods and/or services using a Purchasing Card. Purchasing Cards are referred to throughout this policy

CASH: CHECK CONTROLS C-173-15 ACCOUNTING MANUAL Page 1 CASH: CHECK CONTROLS. Contents. I. Introduction 2

ACCOUNTING MANUAL Page 1 CASH: CHECK CONTROLS Contents Page I. Introduction 2 II. Procedures for Blank Checks 2 A. Procurement 2 B. Storage 3 C. Blank Check Control Record 4 D. Control of Issuance and

ACCOUNTING MANUAL Page 1 CASH: CHECK CONTROLS Contents Page I. Introduction 2 II. Procedures for Blank Checks 2 A. Procurement 2 B. Storage 3 C. Blank Check Control Record 4 D. Control of Issuance and

INTERNAL CONTROL QUESTIONNAIRE OFFICE OF INTERNAL AUDIT UNIVERSITY OF THE VIRGIN ISLANDS

Cabinet Member or Representative responsible for completing this form: INSTRUCTIONS FOR COMPLETING THIS FORM: Answer each question by placing an X in the either the Yes, No,, or Applicable () column. Provide

Cabinet Member or Representative responsible for completing this form: INSTRUCTIONS FOR COMPLETING THIS FORM: Answer each question by placing an X in the either the Yes, No,, or Applicable () column. Provide

FS-06-SF3 School Funds Receipt Log; FS-04-SF2 Schools Funds Payment Request; FS-04-SF1 School Funds: Advance of Funds

Administrative SCHOOL FUNDS Responsibility: Legal References: Related References: Executive Superintendent of Business Services Nil FS-04-SF4 School Funds: Receipts; FS-06-SF3 School Funds Receipt Log;

Administrative SCHOOL FUNDS Responsibility: Legal References: Related References: Executive Superintendent of Business Services Nil FS-04-SF4 School Funds: Receipts; FS-06-SF3 School Funds Receipt Log;

COUNTY OF MENDOCINO CASH CONTROL AND ACCOUNTING STANDARD PRACTICE MANUAL F O R E W O R D

F O R E W O R D This Manual has been developed to provide basic guidance and to standardize operating procedures for all phases of handling cash. The policies and procedures contained in the Manual are

F O R E W O R D This Manual has been developed to provide basic guidance and to standardize operating procedures for all phases of handling cash. The policies and procedures contained in the Manual are

50.P.03: HANDLING CASH, CHECK, CREDIT CARD, AND ACH PAYMENTS

SOP OP: 50.P.03: HANDLING CASH, CHECK, CREDIT CARD, AND ACH PAYMENTS PURPOSE: The purpose of this School of Pharmacy Operating Policy and Procedure (SOP OP) is to establish procedures for handling all

SOP OP: 50.P.03: HANDLING CASH, CHECK, CREDIT CARD, AND ACH PAYMENTS PURPOSE: The purpose of this School of Pharmacy Operating Policy and Procedure (SOP OP) is to establish procedures for handling all

Learn about. How to deposit money. How to make withdrawals and write checks. How to keep track of your money

Cumberland Security Bank s Checking School Learn about How to deposit money How to make withdrawals and write checks How to keep track of your money Depositing Money You can deposit cash and/or checks

Cumberland Security Bank s Checking School Learn about How to deposit money How to make withdrawals and write checks How to keep track of your money Depositing Money You can deposit cash and/or checks

DCCCD BUSINESS PROCEDURES MANUAL. Revision Log

P a g e 9 Revision Log Sub-Section Revision Start Revision End Date Posted Summary of Changes 1.3.1 01/10/06 01/30/06 02/14/06 Added guideline that no credit card account numbers should be solicited or

P a g e 9 Revision Log Sub-Section Revision Start Revision End Date Posted Summary of Changes 1.3.1 01/10/06 01/30/06 02/14/06 Added guideline that no credit card account numbers should be solicited or

Company-wide Credit Card Policy

Company-wide Credit Card Policy Department: Corporate Finance Policy Number: CW-FIN-001-2008-11 Subject: Corporate Credit Cards Effective Date: 11/05/2008 Document Owner: Drew Hurt Title: Corporate Credit

Company-wide Credit Card Policy Department: Corporate Finance Policy Number: CW-FIN-001-2008-11 Subject: Corporate Credit Cards Effective Date: 11/05/2008 Document Owner: Drew Hurt Title: Corporate Credit

Ithaca College Accepting Cash and Checks Procedures

Ithaca College Accepting Cash and Checks Procedures I. Procedure Statement To minimize institutional risk, Ithaca College discourages individual departments from accepting cash and checks on its behalf.

Ithaca College Accepting Cash and Checks Procedures I. Procedure Statement To minimize institutional risk, Ithaca College discourages individual departments from accepting cash and checks on its behalf.

Accounting. Chapter 6

Accounting Chapter 6 Lesson 6-1 Money is referred to as cash in accounting Check Checking account When open a checking account sign a signature card for all people who are allowed to sign checks Deposit

Accounting Chapter 6 Lesson 6-1 Money is referred to as cash in accounting Check Checking account When open a checking account sign a signature card for all people who are allowed to sign checks Deposit

CASH: UNCLAIMED AND UNCASHED CHECKS C-173-78 ACCOUNTING MANUAL Page 1 CASH: UNCLAIMED AND UNCASHED CHECKS I. INTRODUCTION 2 II.

ACCOUNTING MANUAL Page 1 CASH: UNCLAIMED AND UNCASHED CHECKS Contents Page I. INTRODUCTION 2 II. DEFINITIONS 2 III. FOLLOW-UP ACTION 3 IV. TRANSFER OF CHECKS TO OUTSTANDING CHECK ACCOUNTS 5 V. ACCOUNTS

ACCOUNTING MANUAL Page 1 CASH: UNCLAIMED AND UNCASHED CHECKS Contents Page I. INTRODUCTION 2 II. DEFINITIONS 2 III. FOLLOW-UP ACTION 3 IV. TRANSFER OF CHECKS TO OUTSTANDING CHECK ACCOUNTS 5 V. ACCOUNTS

Bursar s Office Department Cash Receipting Training for Receipt Book, Pre Numbered Tickets and Cash Register Users.

Bursar s Office Department Cash Receipting Training for Receipt Book, Pre Numbered Tickets and Cash Register Users Updated 9/24/15 1 Receipt Book/Pre-numbered Ticket/Cash Register Users Customers of the

Bursar s Office Department Cash Receipting Training for Receipt Book, Pre Numbered Tickets and Cash Register Users Updated 9/24/15 1 Receipt Book/Pre-numbered Ticket/Cash Register Users Customers of the

LIVINGSTON COUNTY CREDIT CARD PROCEDURES

LIVINGSTON COUNTY CREDIT CARD PROCEDURES INTRODUCTION Livingston County is introducing an alternative approach to purchasing products and services through the use of credit cards. A credit card purchase

LIVINGSTON COUNTY CREDIT CARD PROCEDURES INTRODUCTION Livingston County is introducing an alternative approach to purchasing products and services through the use of credit cards. A credit card purchase

We encourage you to read the entire report so that you may have a complete understanding of the subject and results of the audit.

Office of Internal Audit Business Process/Turnover Audit Pulley Center May 2015 EXECUTIVE SUMMARY We performed a business process/turnover audit at Pulley Center, pursuant to the approved 2015 Internal

Office of Internal Audit Business Process/Turnover Audit Pulley Center May 2015 EXECUTIVE SUMMARY We performed a business process/turnover audit at Pulley Center, pursuant to the approved 2015 Internal

M O N T H E N D / Q U A R T E R L Y / Y E A R E N D C H E C K L I S T S & P R O C E D U R E S ACCOUNTS RECEIVABLE ACCOUNTS PAYABLE

M O N T H E N D / Q U A R T E R L Y / Y E A R E N D C H E C K L I S T S & P R O C E D U R E S ACCOUNTS RECEIVABLE ACCOUNTS PAYABLE PAYROLL GENERAL LEDGER PROCOM SOLUTIONS, INC. OAKLAND CENTER 8980-A ROUTE

M O N T H E N D / Q U A R T E R L Y / Y E A R E N D C H E C K L I S T S & P R O C E D U R E S ACCOUNTS RECEIVABLE ACCOUNTS PAYABLE PAYROLL GENERAL LEDGER PROCOM SOLUTIONS, INC. OAKLAND CENTER 8980-A ROUTE

Accounts Payable System Administration Manual

Accounts Payable System Administration Manual Confidential Information This document contains proprietary and valuable, confidential trade secret information of APPX Software, Inc., Richmond, Virginia

Accounts Payable System Administration Manual Confidential Information This document contains proprietary and valuable, confidential trade secret information of APPX Software, Inc., Richmond, Virginia

[Company Name] Accounting Policies and Procedures Manual

![[Company Name] Accounting Policies and Procedures Manual](/thumbs/40/20839575.jpg "[Company Name] Accounting Policies and Procedures Manual") [Company Name] Accounting Policies and Procedures Manual [Company Name] Accounting Policies and Procedures Manual Table of Contents Introduction 1 Division of Duties 2 Cash Receipts Procedures 4 Cash Disbursements

[Company Name] Accounting Policies and Procedures Manual [Company Name] Accounting Policies and Procedures Manual Table of Contents Introduction 1 Division of Duties 2 Cash Receipts Procedures 4 Cash Disbursements

Title IV Programs. Notes

1 Accounting Procedures for Title IV Programs CONTENTS A. Case Study Overview 3 B. Title IV Programs: Impact on Accounting 4 1. Title IV Programs 4 2. Program Similarities 4 3. Program Differences 5 C.

1 Accounting Procedures for Title IV Programs CONTENTS A. Case Study Overview 3 B. Title IV Programs: Impact on Accounting 4 1. Title IV Programs 4 2. Program Similarities 4 3. Program Differences 5 C.

MIROMAR TITLE COMPANY, LLC. Best Practices Manual

MIROMAR TITLE COMPANY, LLC Best Practices Manual January 1, 2016 Table of Contents Company Organization Introduction of Best Practices Pillar One Licensing Pillar Two Escrow Account Controls Pillar Three

MIROMAR TITLE COMPANY, LLC Best Practices Manual January 1, 2016 Table of Contents Company Organization Introduction of Best Practices Pillar One Licensing Pillar Two Escrow Account Controls Pillar Three

Write Checks the Right Way

Write Checks the Right Way Guide G-220 Revised by Fahzy Abdul-Rahman 1 Cooperative Extension Service College of Agricultural, Consumer and Environmental Sciences CHECKS VS. OTHER PAYMENT METHODS Checks

Write Checks the Right Way Guide G-220 Revised by Fahzy Abdul-Rahman 1 Cooperative Extension Service College of Agricultural, Consumer and Environmental Sciences CHECKS VS. OTHER PAYMENT METHODS Checks

Fiscal Procedure Sequence page number

Table of Contents Fiscal Procedure Sequence page number Treasurer Responsibilities Maintenance of General Ledger Financial Statements Financial Signature/Review Policy Insurance Protection Payroll Procedures

Table of Contents Fiscal Procedure Sequence page number Treasurer Responsibilities Maintenance of General Ledger Financial Statements Financial Signature/Review Policy Insurance Protection Payroll Procedures

SECTION 2.05 IMPREST CHECKING ACCOUNTS Contact: Accounting @ Extension 4170

SECTION 2.05 IMPREST CHECKING ACCOUNTS Contact: Accounting @ Extension 4170 A. Overview Imprest checking accounts are District-owned bank accounts operated by schools and departments. These accounts are

SECTION 2.05 IMPREST CHECKING ACCOUNTS Contact: Accounting @ Extension 4170 A. Overview Imprest checking accounts are District-owned bank accounts operated by schools and departments. These accounts are

ACCOUNTING POLICIES AND PROCEDURES SAMPLE MANUAL

(Name of Organization & logo) ACCOUNTING POLICIES AND PROCEDURES SAMPLE MANUAL (Date) Note: this sample manual is designed for nonprofit organizations with the following staff involved with accounting

(Name of Organization & logo) ACCOUNTING POLICIES AND PROCEDURES SAMPLE MANUAL (Date) Note: this sample manual is designed for nonprofit organizations with the following staff involved with accounting

THE CITY OF NEW YORK OFFICE OF THE COMPTROLLER INTERNAL CONTROL AND ACCOUNTABILITY DIRECTIVES

THE CITY OF NEW YORK OFFICE OF THE COMPTROLLER INTERNAL CONTROL AND ACCOUNTABILITY DIRECTIVES DIRECTIVE 11 - CASH ACCOUNTABILITY AND CONTROL INTRODUCTION AND SUMMARY The purpose of this Directive is to

THE CITY OF NEW YORK OFFICE OF THE COMPTROLLER INTERNAL CONTROL AND ACCOUNTABILITY DIRECTIVES DIRECTIVE 11 - CASH ACCOUNTABILITY AND CONTROL INTRODUCTION AND SUMMARY The purpose of this Directive is to

- 1 - School Based Funds Reference Guide

- 1 - School Based Funds Reference Guide - 2 - Index Contacts 3 Internal Control Tips 4 Handling Petty Cash 5 Steps to reconcile a bank account 6 Year end reporting 7 Sample Bank Reconciliation Sample

- 1 - School Based Funds Reference Guide - 2 - Index Contacts 3 Internal Control Tips 4 Handling Petty Cash 5 Steps to reconcile a bank account 6 Year end reporting 7 Sample Bank Reconciliation Sample

UNITED STATES BANKRUPTCY COURT NORTHERN & EASTERN DISTRICTS OF TEXAS REGION 6 MONTHLY OPERATING REPORT

ACCRUAL BASIS JUDGE: UNITED STATES BANKRUPTCY COURT NORTHERN & EASTERN DISTRICTS OF TEXAS REGION 6 MONTHLY OPERATING REPORT MONTH ENDING: MONTH YEAR IN ACCORDANCE WITH TITLE 28, SECTION 1746, OF THE UNITED

ACCRUAL BASIS JUDGE: UNITED STATES BANKRUPTCY COURT NORTHERN & EASTERN DISTRICTS OF TEXAS REGION 6 MONTHLY OPERATING REPORT MONTH ENDING: MONTH YEAR IN ACCORDANCE WITH TITLE 28, SECTION 1746, OF THE UNITED

How to set up a people based. accounting system that makes your. small business work for you. Thomas G. Post. Certified Public Accountant 281-351-2688

How to set up a people based accounting system that makes your small business work for you. By Thomas G. Post Certified Public Accountant 281-351-2688 www.texastaxman.com 1 Title How to set up a people

How to set up a people based accounting system that makes your small business work for you. By Thomas G. Post Certified Public Accountant 281-351-2688 www.texastaxman.com 1 Title How to set up a people

CR-370 CASH RECEIPTS

CR-370 CASH RECEIPTS 370.1 UNIT DEPOSITING PROCEDURES 370.2 GENERAL INTERNAL POLICIES RELATING TO THE CASHIER 370.3 TIMELY DEPOSITS 370.4 COUNTING THE ENTERPRISE UNIT DEPOSIT 370.5 PREPARING THE BANK DEPOSIT

CR-370 CASH RECEIPTS 370.1 UNIT DEPOSITING PROCEDURES 370.2 GENERAL INTERNAL POLICIES RELATING TO THE CASHIER 370.3 TIMELY DEPOSITS 370.4 COUNTING THE ENTERPRISE UNIT DEPOSIT 370.5 PREPARING THE BANK DEPOSIT

FINANCIAL CONTROLS POLICIES AND PROCEDURES FOR SMALL NONPROFIT ORGANIZATIONS

By Cindy Cumfer NOTE: These policies and procedures are designed for small nonprofits that do not have an administrator with financial expertise. They are set up to divide the fiscal control roles between

By Cindy Cumfer NOTE: These policies and procedures are designed for small nonprofits that do not have an administrator with financial expertise. They are set up to divide the fiscal control roles between

Introductions. Student Introductions. Purpose. Objectives (Continued) Objectives

Objectives") Introductions Instructor and student introductions Module overview 1 2 Your name Student Introductions Your expectations, questions, and concerns about checking accounts Purpose will teach you how to use

Introductions Instructor and student introductions Module overview 1 2 Your name Student Introductions Your expectations, questions, and concerns about checking accounts Purpose will teach you how to use

SAO Cash Management Group To Be Process Flow

Centralized Accounts Payable (AP) Disbursement Generate Checks and Positive Pay file Distribute Checks Review AP Reports Exception Processing Create Control Group in Peoplesoft Accounts Payable (HIGHLY

Centralized Accounts Payable (AP) Disbursement Generate Checks and Positive Pay file Distribute Checks Review AP Reports Exception Processing Create Control Group in Peoplesoft Accounts Payable (HIGHLY

Important Disclaimer. Copyright Information

Important Disclaimer This checklist is provided to assist churches in fulfilling the requirement of Book of Order provision G-10.0400, 4, d. The Book of Order does not require that the annual review of

Important Disclaimer This checklist is provided to assist churches in fulfilling the requirement of Book of Order provision G-10.0400, 4, d. The Book of Order does not require that the annual review of

State Accounting Office

State Accounting Office State Accounting Manual Policies and Procedures Policy Number CM-100005 Section Name Cash Management Policy Name Payroll Disbursement Effective Date 2/28/07 Revised Date I. Purpose

State Accounting Office State Accounting Manual Policies and Procedures Policy Number CM-100005 Section Name Cash Management Policy Name Payroll Disbursement Effective Date 2/28/07 Revised Date I. Purpose

New Account Conversion CHECKLIST

New Account Conversion CHECKLIST You may check the boxes next to the items you have completed (if any). And then print out and keep this checklist handy. As you continue completing items, simply check

New Account Conversion CHECKLIST You may check the boxes next to the items you have completed (if any). And then print out and keep this checklist handy. As you continue completing items, simply check

Finance and Administrative Services Finance Service Center

FINAL DRAFT Finance and Administrative Services Finance Service Center Service Level Agreement January 3, 2011 Table of Contents Section I. Departments and Effective Dates...1 Section II. Overview and

FINAL DRAFT Finance and Administrative Services Finance Service Center Service Level Agreement January 3, 2011 Table of Contents Section I. Departments and Effective Dates...1 Section II. Overview and

AAM 50. CASH. AAM 50.010 Treasury Investment (10-09)

") AAM 50. CASH 50.010 Treasury Investment 10/09 50.020 Accountability 10/09 50.030 Control 10/09 50.040 Receipt for Payments 10/09 50.050 Daily Record of Collections 10/09 50.060 Mail Collections 50.070

AAM 50. CASH 50.010 Treasury Investment 10/09 50.020 Accountability 10/09 50.030 Control 10/09 50.040 Receipt for Payments 10/09 50.050 Daily Record of Collections 10/09 50.060 Mail Collections 50.070

Chapter 7 Trustee. Internal Control Questionnaire

Chapter 7 Trustee Instructions for the trustee: The purpose of the (ICQ) is to provide the United States Trustee with an understanding of the internal controls and financial record keeping and reporting

Chapter 7 Trustee Instructions for the trustee: The purpose of the (ICQ) is to provide the United States Trustee with an understanding of the internal controls and financial record keeping and reporting

Accounting Policies and Procedures Manual

Accounting Policies and Procedures Manual Xxx Accounting Policies and Procedures Manual Table of Contents Introduction 1 Division of Duties 2 Cash Receipts Procedures 4 Cash Disbursements Procedures 6

Accounting Policies and Procedures Manual Xxx Accounting Policies and Procedures Manual Table of Contents Introduction 1 Division of Duties 2 Cash Receipts Procedures 4 Cash Disbursements Procedures 6

How To Account For A Wing

ASSETS Cash Wings may place funds in checking accounts, savings accounts, certificates of deposit (CDs), and/or money market accounts. All funds must be readily available without loss of principal. All

ASSETS Cash Wings may place funds in checking accounts, savings accounts, certificates of deposit (CDs), and/or money market accounts. All funds must be readily available without loss of principal. All

ASC Financial Policies Page i of 18 Originally Approved by BOT: November 2006 Revised: July 2014/Revisions approved by BOT

All Souls Church, Unitarian Financial Policies and Procedures Table of Contents Page A. Fiscal Year and Accounting System 1 B. Cash Management and Control 1 1. Types of Accounts 1 2. Opening/Closing Accounts

All Souls Church, Unitarian Financial Policies and Procedures Table of Contents Page A. Fiscal Year and Accounting System 1 B. Cash Management and Control 1 1. Types of Accounts 1 2. Opening/Closing Accounts

INTERNAL ACCOUNTING CONTROLS CHECKLIST FOR NTMA CHAPTERS

P R E C I S I O N INTERNAL ACCOUNTING CONTROLS CHECKLIST FOR NTMA CHAPTERS Presented at NTMA 2004 Annual Convention Palm Springs, CA February 2004 National Tooling & Machining Association 9300 Livingston

P R E C I S I O N INTERNAL ACCOUNTING CONTROLS CHECKLIST FOR NTMA CHAPTERS Presented at NTMA 2004 Annual Convention Palm Springs, CA February 2004 National Tooling & Machining Association 9300 Livingston

SUMMARY OF CORRECTIVE ACTION FOR SEGREGATION OF DUTIES AUDIT ISSUES

SUMMARY OF CORRECTIVE ACTION FOR SEGREGATION OF DUTIES AUDIT ISSUES CASH MANAGEMENT I. Checks a. All checks are restrictively endorsed, using the endorsement stamp maintained by the building secretary.

SUMMARY OF CORRECTIVE ACTION FOR SEGREGATION OF DUTIES AUDIT ISSUES CASH MANAGEMENT I. Checks a. All checks are restrictively endorsed, using the endorsement stamp maintained by the building secretary.

How To Manage A Corporation

Western Climate Initiative, Inc. Accounting Policies and Procedures Adopted May 8, 2013 WESTERN CLIMATE INITIATIVE, INC ACCOUNTING POLICIES AND PROCEDURES Adopted May 8, 2013 Table of Contents I. Introduction...

Western Climate Initiative, Inc. Accounting Policies and Procedures Adopted May 8, 2013 WESTERN CLIMATE INITIATIVE, INC ACCOUNTING POLICIES AND PROCEDURES Adopted May 8, 2013 Table of Contents I. Introduction...

Research Subject Incentive Payment Procedures. University Financial Services. Business Requirements. 1. Stakeholders & Business Units

Business Requirements This procedure provides guidance and direction for acquiring and accounting for operating advances. Operating advances are used for payments made to individuals as an incentive to

Business Requirements This procedure provides guidance and direction for acquiring and accounting for operating advances. Operating advances are used for payments made to individuals as an incentive to

Presbytery of Eastern Virginia Internal Control Manual Policy and Procedures

Presbytery of Eastern Virginia Internal Control Manual Policy and Procedures Revision 1, May 19, 2010 Page 1 of 12 List of Changes Date Revision Pages Affected Revision 1, May 19, 2010 Page 2 of 12 Introduction:

Presbytery of Eastern Virginia Internal Control Manual Policy and Procedures Revision 1, May 19, 2010 Page 1 of 12 List of Changes Date Revision Pages Affected Revision 1, May 19, 2010 Page 2 of 12 Introduction:

SCHEDULE. ANNUAL TRUST ACCOUNT REPORT (Sections 14 and 15) PART 1

PART 1") SCHEDULE TO: The Registrar The Real Estate Brokers Act ANNUAL TRUST ACCOUNT REPORT (Sections 14 and 15) PART 1 At the request of, being the authorized official of ("the "Broker"), I/we have reviewed the

SCHEDULE TO: The Registrar The Real Estate Brokers Act ANNUAL TRUST ACCOUNT REPORT (Sections 14 and 15) PART 1 At the request of, being the authorized official of ("the "Broker"), I/we have reviewed the

Audit of Controls over Government Travel Cards FINAL AUDIT REPORT

Audit of Controls over Government Travel Cards FINAL AUDIT REPORT ED-OIG/A19-B0010 March 2002 Our mission is to promote the efficiency, effectiveness, and integrity of the Department s programs and operations.

Audit of Controls over Government Travel Cards FINAL AUDIT REPORT ED-OIG/A19-B0010 March 2002 Our mission is to promote the efficiency, effectiveness, and integrity of the Department s programs and operations.

Invoicing Internal Procedure

Office of Research and Sponsored Programs Invoicing Internal Procedure Issued: January, 2008 Implemented: March, 2008 BACKGROUND San Francisco State University (SFSU) receives funding for sponsored projects

Office of Research and Sponsored Programs Invoicing Internal Procedure Issued: January, 2008 Implemented: March, 2008 BACKGROUND San Francisco State University (SFSU) receives funding for sponsored projects