Global Investor Forum Market Perspectives / Strategy. Marwan Lahoud, Chief Strategy and Marketing Officer London, 11th/12th December 2013

|

|

|

- Noah Harper

- 7 years ago

- Views:

Transcription

1 Global Investor Forum Market Perspectives / Strategy Marwan Lahoud, Chief Strategy and Marketing Officer London, 11th/12th December 2013

2 Safe Harbour Statement Disclaimer This presentation includes forward-looking statements. Words such as anticipates, believes, estimates, expects, intends, plans, projects, may and similar expressions are used to identify these forward-looking statements. Examples of forward-looking statements include statements made about strategy, ramp-up and delivery schedules, introduction of new products and services and market expectations, as well as statements regarding future performance and outlook. By their nature, forward-looking statements involve risk and uncertainty because they relate to future events and circumstances and there are many factors that could cause actual results and developments to differ materially from those expressed or implied by these forward-looking statements. These factors include but are not limited to: Changes in general economic, political or market conditions, including the cyclical nature of some of EADS businesses; Significant disruptions in air travel (including as a result of terrorist attacks); Currency exchange rate fluctuations, in particular between the Euro and the U.S. dollar; The successful execution of internal performance plans, including cost reduction and productivity efforts; Product performance risks, as well as programme development and management risks; Customer, supplier and subcontractor performance or contract negotiations, including financing issues; Competition and consolidation in the aerospace and defence industry; Significant collective bargaining labour disputes; The outcome of political and legal processes, including the availability of government financing for certain programmes and the size of defence and space procurement budgets; Research and development costs in connection with new products; Legal, financial and governmental risks related to international transactions; Legal and investigatory proceedings and other economic, political and technological risks and uncertainties. As a result, EADS actual results may differ materially from the plans, goals and expectations set forth in such forward-looking statements. For a discussion of factors that could cause future results to differ from such forward-looking statements, see EADS Registration Document dated 3 April Any forward-looking statement contained in this presentation speaks as of the date of this presentation. EADS undertakes no obligation to publicly revise or update any forward-looking statements in light of new information, future events or otherwise.

3 Agenda 1. Our DNA 4 2. The world is evolving 7 3. The power of our portfolio Our strategy 18 Page 3

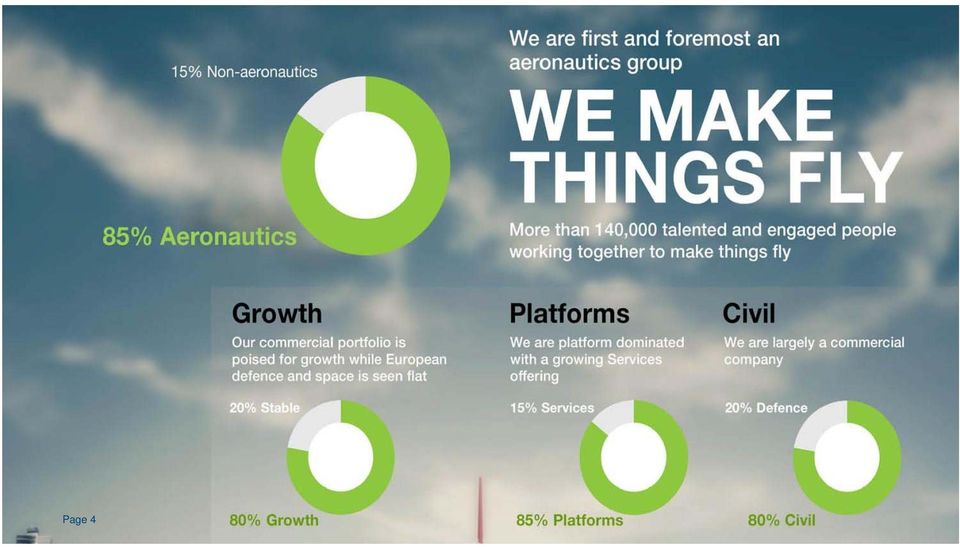

4 Page 4 Corporate Development

5 EADS STRICTLY CONFIDENTIAL ** Page 5 * At list prices ** France: 35%, Germany 35%, Spain 10%, UK 10% Corporate Development

6 Agenda 1. Our DNA 4 2. The world is evolving 7 3. The power of our portfolio Our strategy 18 Page 6

7 The economic world today The big economic clusters are still balanced Top 10 Top 10 countries Country GDP, 2012, US$ bn USA China 8221 Japan 5960 Germany 3430 France 2614 UK 2477 Brazil 2253 Russia 2030 Italy 2014 India 1842 World GDP: 72,2 US$ tn thereof: Top 10: 65% Top 20: 80% Page 7 Source: International Monetary Fund, Oct. 2013

8 Passenger Aircraft demand Asia-Pacific is the biggest market next to Europe and North America World demand for Large Commercial Aircraft North America Latin America Europe Middle East Africa CIS Asia-Pacific Region Number of LCA Asia-Pacific Europe 5827 North America 5521 Latin America 2279 Middle East 1999 CIS 1095 Africa 970 Total Passenger Aircraft: Page 8 Source: Airbus Global Market Forecast 2013

9 The top 20 countries in military budget in 2012 The US and Europe are the biggest markets, China not addressable Top Top 10 countries: Defence Budget 2012 CA US BZ UK NL ES FR GE IT IS KSAUAE IN RU CH SP JP RoK TW AU Country 2012, US$ bn USA 660 China 200 UK 62 Japan 58 Saudi Arabia 45 Germany 45 Russia 44 France 42 Brazil 40 India 39 World budget: 1636 US$ bn thereof: Top 10: 75% Top 20: 87% Page 9

10 The top 20 countries in military budget in 2020 Growth mainly in Asia and Middle East Top Top 10 countries: Defence Budget 2020 CA US BZ UK NL FR ES GE IT TU IS KSA IN RU CH SP JP RoK TW AU 2020 Country 2020, US$ bn* USA 564 China 370 Japan 63 UK 62 India 62 Saudi Arabia 57 Russia 54 Brazil 51 Germany 45 France 43 World budget: 1843 US$ bn thereof: Top 10: 74% Top 20: 86% * Arrows indicate change in budget Page 10

11 Agenda 1. Our DNA 4 2. The world is evolving 7 3. The power of our portfolio Our strategy 18 Page 11

12 EADS has built a strong position in the Aerospace, Defense and Space Industry Strong position in the markets we operate in: mostly Nr. 1 or Nr. 2 in the world Strong order backlog Strong Cash Position Top Credit Rating Unique capabilities in the Aerospace and Defence field Unique diversity to strengthen our global approach Page 12

13 Consistent Portfolio Contribution to Financial Targets Revenues Growth Revenues by Division Operating Profit Target 2015 in bn Guidance % 11% EBIT* before one off Including A350 Revenues & EBIT pre R&D and with remaining open % Pro forma as per H disclosure Airbus Commercial Defense Airbus Defense & Space Airbus Helicopters While strongest contributors are commercial products, defense remains resilient * pre-goodwill impairment and exceptionals 2015 ROS before one off targeted between 7% and 8% including the A350 dilution

14 Our portfolio provides value creation opportunities Business Dev. and Growth opportunities Strong Services component Global footprint Diversified portfolio Synergies Technology Talent development Sourcing synergies Privileged home country access Key provider of security critical capabilities Page 14

15 Synergies are materializing in dual-use of our products and technologies A330 FSTA Ariane 5 M51 EC725 EC225 Page 15

16 There are strong technological synergies Table of Contents Past and potentially future synergies between Defence/Space and Civilian In the last three decades For the future Stress analysis, materials, and flight control Digital computers Fly by wire 3D carbon technologies for structural equipment and high strain pieces for engines Digitalisation of air traffic control and network centric aircraft Increased autonomy and safety to deal with increased traffic Cyber Security New materials for structures, engines, and equipment Autonomous flight, Unmanned Aerial Vehicles, Optionally Piloted Vehicles Page 16

17 Agenda 1. Our DNA 4 2. The world is evolving 7 3. The power of our portfolio Our strategy 18 Page 17

18 Focus-Strategy on Commercial Leadership, Defence and Space Optimization and Value Creation 7 Strategic Priorities for the Group Strategic Implications Page 18 Strengthen market position and profitability while remaining a leader in commercial Aeronautics Preserve leading position in European Defence & Space and Government markets Exploit incremental innovation potential within our product programs, while preparing next-generation breakthroughs Focus on profitability, value creation, and market position - no need to chase growth at any cost; actively manage portfolio Adapt to a more global world and move closer to our international markets Focus services on and around our platforms Strengthen our value chain position We build a portfolio of strong divisions with cross-divisional processes and integrated functions (and shared services) where it delivers value We focus on our core business: Aeronautics (civil and military) and Space We leverage the strength of the Airbus commercial business to benefit the entire group We consolidate the bulk of our Defence and Space business into one division We keep our Helicopter business as a separate division due to its technical and market specificities Consequently, we rename and rebrand EADS to Airbus Group, a worldwide recognized brand We will use active portfolio management as a key lever to implement our strategy

19 The new organisation is structuring our businesses to be better positioned in the market Revenues: 36.9bn EBIT: 1.125m Employees: ~ Revenues 1 : 13.7bn EBIT 1 : 547m Employees 2 : ~ Revenues: 6.3bn EBIT: 311m Employees: ~ Offering Large commercial aircraft, Services Green aircraft for militarisation Defence, Security, Space products Related services Helicopters Related services Customers Airlines Airbus DS for militarization Mostly focusing on governmental and institutional Businesses as well as governmental / institutional customers Business model Commercial, B2B Programs funded through development phase where possible, B2G Strong commercial with customer funded defence programs, B2B, B2G Organization Logic Focus on the commercial aircraft business Joint customer base Synergies between previously dispersed activities Specific rotary wing technology Military versions derived from civil products Page 19 Note: 2012 figures 1: MBDA included at 37.5% 2: MBDA not included

Focus on Security Business

EADS Security & Defence Focus on Security Business Hervé Guillou Head of Defence and Communications Systems Global Investor Forum 2009, Broughton, 1 st & 2 nd April 2009 1 1 Safe Harbour Statement Disclaimer

EADS Security & Defence Focus on Security Business Hervé Guillou Head of Defence and Communications Systems Global Investor Forum 2009, Broughton, 1 st & 2 nd April 2009 1 1 Safe Harbour Statement Disclaimer

CASSIDIAN Evolution of the Defence & Security business in EADS

CASSIDIAN Evolution of the Defence & Security business in EADS Global Investor Forum, Toulouse 15-16 November 2010 Stefan Zoller CEO Cassidian 1 2 Disclaimer Disclaimer This presentation includes forward-looking

CASSIDIAN Evolution of the Defence & Security business in EADS Global Investor Forum, Toulouse 15-16 November 2010 Stefan Zoller CEO Cassidian 1 2 Disclaimer Disclaimer This presentation includes forward-looking

Security Business a Growth Path

Business a Growth Path North America Investor Forum 2010 New York, 18 th March 2010 Hervé Guillou Head of EADS Defence & Communications Systems Safe Harbour Statement 2 Disclaimer This presentation includes

Business a Growth Path North America Investor Forum 2010 New York, 18 th March 2010 Hervé Guillou Head of EADS Defence & Communications Systems Safe Harbour Statement 2 Disclaimer This presentation includes

Airbus Group. Marwan Lahoud Airbus Group, CSMO. London 10 December 2014

1 Airbus Group Marwan Lahoud Airbus Group, CSMO London 10 December 2014 Safe Harbour Statement 2 Disclaimer This presentation includes forward-looking statements. Words such as anticipates, believes, estimates,

1 Airbus Group Marwan Lahoud Airbus Group, CSMO London 10 December 2014 Safe Harbour Statement 2 Disclaimer This presentation includes forward-looking statements. Words such as anticipates, believes, estimates,

FY RESULTS 27 FEBRUARY 2015. Tom Enders I Chief Executive Officer Harald Wilhelm I Chief Financial Officer

1 FY RESULTS 27 FEBRUARY 2015 Tom Enders I Chief Executive Officer Harald Wilhelm I Chief Financial Officer SAFE HARBOUR STATEMENT 2 Disclaimer This presentation includes forward-looking statements. Words

1 FY RESULTS 27 FEBRUARY 2015 Tom Enders I Chief Executive Officer Harald Wilhelm I Chief Financial Officer SAFE HARBOUR STATEMENT 2 Disclaimer This presentation includes forward-looking statements. Words

Customer Financing. Nigel Taylor SVP Customer, Project and Structured Finance. Global Investor Forum 2009, Broughton, 1 st & 2 nd April 2009

Customer Financing Nigel Taylor SVP Customer, Project and Structured Finance Global Investor Forum 2009, Broughton, 1 st & 2 nd April 2009 1 Safe Harbour Statement Disclaimer This presentation includes

Customer Financing Nigel Taylor SVP Customer, Project and Structured Finance Global Investor Forum 2009, Broughton, 1 st & 2 nd April 2009 1 Safe Harbour Statement Disclaimer This presentation includes

Q1 RESULTS 2015 30 APRIL 2015. Harald Wilhelm I Chief Financial Officer

1 Q1 RESULTS 2015 30 APRIL 2015 Harald Wilhelm I Chief Financial Officer SAFE HARBOUR STATEMENT 2 Disclaimer This presentation includes forward-looking statements. Words such as anticipates, believes,

1 Q1 RESULTS 2015 30 APRIL 2015 Harald Wilhelm I Chief Financial Officer SAFE HARBOUR STATEMENT 2 Disclaimer This presentation includes forward-looking statements. Words such as anticipates, believes,

Airbus Group Reports Improved Nine-Month (9m) Results 2014

Results 2014") Airbus Group Reports Improved Nine-Month () Results Financial performance reflects operational progress, guidance confirmed Revenues increase four percent to 40.5 billion EBIT* before one-off rises 12

Airbus Group Reports Improved Nine-Month () Results Financial performance reflects operational progress, guidance confirmed Revenues increase four percent to 40.5 billion EBIT* before one-off rises 12

Airbus Group Achieves Record Revenues, EBIT* And Order Backlog In 2014

Airbus Group Achieves Record Revenues, EBIT* And Order Backlog In Revenues increase five percent to 60.7 billion Reported EBIT* up 54 percent to 4.0 billion with a 6.7% return on sales Earnings per share

Airbus Group Achieves Record Revenues, EBIT* And Order Backlog In Revenues increase five percent to 60.7 billion Reported EBIT* up 54 percent to 4.0 billion with a 6.7% return on sales Earnings per share

Cash Drivers and Enterprise Value

Cash Drivers and Enterprise Value Global Investor Forum 2009, Broughton, 1 st & 2 nd April 2009 Gérard Adsuar Corporate Executive Finance & Treasury, EADS 1 1 Safe Harbour Statement Disclaimer This presentation

Cash Drivers and Enterprise Value Global Investor Forum 2009, Broughton, 1 st & 2 nd April 2009 Gérard Adsuar Corporate Executive Finance & Treasury, EADS 1 1 Safe Harbour Statement Disclaimer This presentation

Commercial Update. John Leahy Chief Operating Officer Customers Airbus. Global Investor Forum 2009, Broughton, 1 st & 2 nd April 2009

Commercial Update John Leahy Chief Operating Officer Customers Airbus Global Investor Forum 2009, Broughton, 1 st & 2 nd April 2009 1 1 Safe Harbour Statement Disclaimer This presentation includes forward-looking

Commercial Update John Leahy Chief Operating Officer Customers Airbus Global Investor Forum 2009, Broughton, 1 st & 2 nd April 2009 1 1 Safe Harbour Statement Disclaimer This presentation includes forward-looking

Airbus Group Reports Robust First Quarter 2015 Results

Airbus Group Reports Robust First Quarter Results Solid operational performance supports EPS and cash flow, further enhanced by divestments Revenues 12.1 billion, EBIT* before one-off 651 million Earnings

Airbus Group Reports Robust First Quarter Results Solid operational performance supports EPS and cash flow, further enhanced by divestments Revenues 12.1 billion, EBIT* before one-off 651 million Earnings

Reliable Performance and Increasing Growth Hans-Peter Ring Chief Financial Officer EADS. North America Investor Forum New York 7 th October 2003

Reliable Performance and Increasing Growth Hans-Peter Ring Chief Financial Officer EADS North America Investor Forum New York 7 th October 2003 1 1 Solid and Resilient Performance Financial Highlights

Reliable Performance and Increasing Growth Hans-Peter Ring Chief Financial Officer EADS North America Investor Forum New York 7 th October 2003 1 1 Solid and Resilient Performance Financial Highlights

Eurocopter Delivering strong business growth

Eurocopter Delivering strong business growth Lutz Bertling Chief Executive Officer Eurocopter Page 1 Safe Harbour Statement Disclaimer This presentation includes forward-looking statements. Words such

Eurocopter Delivering strong business growth Lutz Bertling Chief Executive Officer Eurocopter Page 1 Safe Harbour Statement Disclaimer This presentation includes forward-looking statements. Words such

Global Investor Forum 2008

Global Investor Forum 2008 Airbus Financial Workshop Seville, 17 th / 18 th January 2008 1 Safe Harbor Statement Certain of the statements contained in this document are not historical facts but rather

Global Investor Forum 2008 Airbus Financial Workshop Seville, 17 th / 18 th January 2008 1 Safe Harbor Statement Certain of the statements contained in this document are not historical facts but rather

InformatIon Nine-month business update 2012 8 November 2012

Information Nine-month business update 2012 8 November 2012 Kuoni: higher turnover and improved operating earnings in the first nine months of 2012 Kuoni Group s turnover increased 17.5% to CHF 4476 million

Information Nine-month business update 2012 8 November 2012 Kuoni: higher turnover and improved operating earnings in the first nine months of 2012 Kuoni Group s turnover increased 17.5% to CHF 4476 million

Health Care Worldwide. Citi - European Credit Conference September 24, 2015 - London

Health Care Worldwide Citi - European Credit Conference September 24, 2015 - London Safe Harbor Statement This presentation contains forward-looking statements that are subject to various risks and uncertainties.

Health Care Worldwide Citi - European Credit Conference September 24, 2015 - London Safe Harbor Statement This presentation contains forward-looking statements that are subject to various risks and uncertainties.

Logistikkdagen 2006. Challenges & Problems linked to: Export/Import Special Markets Export/Import Special Products. Rolls-Royce

Logistikkdagen 2006 Challenges & Problems linked to: Export/Import Special Markets Export/Import Special Products Rolls-Royce Royce Diesels Bergen, Norway Berend van Hoek - VP Strategic Sourcing trusted

Logistikkdagen 2006 Challenges & Problems linked to: Export/Import Special Markets Export/Import Special Products Rolls-Royce Royce Diesels Bergen, Norway Berend van Hoek - VP Strategic Sourcing trusted

The aerospace industry: statistics and policy

The aerospace industry: statistics and policy Standard Note: SN/EP/00928 Last updated: 5 March 2015 Author: Chris Rhodes, David Hough and Matthew Ward Section Economic Policy and Statistics Section The

The aerospace industry: statistics and policy Standard Note: SN/EP/00928 Last updated: 5 March 2015 Author: Chris Rhodes, David Hough and Matthew Ward Section Economic Policy and Statistics Section The

Annual Results 2011 08 March 2012

Annual Results 2011 08 March 2012 Louis Gallois Chief Executive Officer Hans Peter Ring Chief Financial Officer Safe Harbour Statement 2 Disclaimer This presentation includes forward-looking statements.

Annual Results 2011 08 March 2012 Louis Gallois Chief Executive Officer Hans Peter Ring Chief Financial Officer Safe Harbour Statement 2 Disclaimer This presentation includes forward-looking statements.

Annual Results 2010. Louis Gallois Chief Executive Officer. Hans Peter Ring Chief Financial Officer

Annual Results 2010 Louis Gallois Chief Executive Officer Hans Peter Ring Chief Financial Officer Safe Harbour Statement 2 Disclaimer This presentation includes forward-looking statements. Words such as

Annual Results 2010 Louis Gallois Chief Executive Officer Hans Peter Ring Chief Financial Officer Safe Harbour Statement 2 Disclaimer This presentation includes forward-looking statements. Words such as

Chasing growth in a constrained environment

Chasing growth in a constrained environment Bernard Fontana CEO June 14, 2012 Agenda 1 Drivers of demand growth 2 Allocating the asset footprint according to demand 3 Growth from customer excellence &

Chasing growth in a constrained environment Bernard Fontana CEO June 14, 2012 Agenda 1 Drivers of demand growth 2 Allocating the asset footprint according to demand 3 Growth from customer excellence &

Q2 and Half-Year 2010 Results

Q2 and Half-Year 2010 Results July 27, 2010 27.07.2010 1 Key financials in billions of Q2 2009 Q2 2010 Revenue 19.6 25.1 EBIT Net profit (loss) Earnings (loss) per share (in ) (1.0) (1.1) (0.99) 2.1 1.3

Q2 and Half-Year 2010 Results July 27, 2010 27.07.2010 1 Key financials in billions of Q2 2009 Q2 2010 Revenue 19.6 25.1 EBIT Net profit (loss) Earnings (loss) per share (in ) (1.0) (1.1) (0.99) 2.1 1.3

Applus+ Group Results Presentation First Quarter 2015 7 May 2015

Applus+ Group Results Presentation First Quarter 2015 7 May 2015 DISCLAIMER This document may contain statements that constitute forward looking statements about Applus Services, SA ( Applus+ or the Company

Applus+ Group Results Presentation First Quarter 2015 7 May 2015 DISCLAIMER This document may contain statements that constitute forward looking statements about Applus Services, SA ( Applus+ or the Company

Standard Chartered today releases its Interim Management Statement for the third quarter of 2015.

Standard Chartered PLC Interim Management Statement 3 November 2015 Standard Chartered today releases its Interim Management Statement for the third quarter of 2015. Bill Winters, Group Chief Executive,

Standard Chartered PLC Interim Management Statement 3 November 2015 Standard Chartered today releases its Interim Management Statement for the third quarter of 2015. Bill Winters, Group Chief Executive,

Tungsten Corporation plc Results for the six months ending 31 October 2014

Tungsten Corporation plc Results for the six months ending 31 October 2014 January 2015 Important information This document contains forward-looking statements that may or may not prove accurate. For example,

Tungsten Corporation plc Results for the six months ending 31 October 2014 January 2015 Important information This document contains forward-looking statements that may or may not prove accurate. For example,

Allianz an opportunity

Jay Ralph, Member of the Board of Management Allianz an opportunity Commerzbank German Investment Seminar New York, January 2011 Agenda 1 Allianz at a glance 2 Business operations in the US 3 Summary and

Jay Ralph, Member of the Board of Management Allianz an opportunity Commerzbank German Investment Seminar New York, January 2011 Agenda 1 Allianz at a glance 2 Business operations in the US 3 Summary and

European airlines and the Asian market. A Lufthansa Consulting outlook towards the middle of the next decade

European airlines and the Asian market A Lufthansa Consulting outlook towards the middle of the next decade Lufthansa Consulting GmbH Von-Gablenz-Str. 2-6 50679 Köln Germany Registration: Local Court of

European airlines and the Asian market A Lufthansa Consulting outlook towards the middle of the next decade Lufthansa Consulting GmbH Von-Gablenz-Str. 2-6 50679 Köln Germany Registration: Local Court of

Fiscal Year 2015 1st Quarter Earnings Conference Call

Fiscal Year 2015 1st Quarter Earnings Conference Call January, 2015 www.jacobs.com worldwide Forward-Looking Statement Disclaimer Statements included in this presentation that are not based on historical

Fiscal Year 2015 1st Quarter Earnings Conference Call January, 2015 www.jacobs.com worldwide Forward-Looking Statement Disclaimer Statements included in this presentation that are not based on historical

www.pwc.co.uk/economics Global wage projections to 2030 September 2013

www.pwc.co.uk/economics Global wage projections to 2030 Summary: Wage gap between emerging and advanced economies will shrink significantly by 2030 By 2030, our projections in this report suggest that

www.pwc.co.uk/economics Global wage projections to 2030 Summary: Wage gap between emerging and advanced economies will shrink significantly by 2030 By 2030, our projections in this report suggest that

FIRST QUARTER REPORT 2008-04-25

FIRST QUARTER REPORT This presentation contains forward looking statements. Such statements are based on our current expectations and are subject to certain risks and uncertainties that could negatively

FIRST QUARTER REPORT This presentation contains forward looking statements. Such statements are based on our current expectations and are subject to certain risks and uncertainties that could negatively

Michele Genovese DG Research and Innovation Specific International Cooperation Activities

Michele Genovese DG Research and Innovation Specific International Cooperation Activities 1 2 1. Innovation in a changing, challenging world New Priorities 3 Recent changes in the global economic system

Michele Genovese DG Research and Innovation Specific International Cooperation Activities 1 2 1. Innovation in a changing, challenging world New Priorities 3 Recent changes in the global economic system

Why Study Aerospace Engineering? Deciding Your Future

Why Study Aerospace Engineering? Deciding Your Future A Global Industry A booming market with thousands of manufacturers and investors worldwide. The industry is dominated by major companies in the USA

Why Study Aerospace Engineering? Deciding Your Future A Global Industry A booming market with thousands of manufacturers and investors worldwide. The industry is dominated by major companies in the USA

Health Care Worldwide

Health Care Worldwide Barclays European High Yield and Leveraged Finance Conference October 30, 2014 London Barclays European High Yield and Leveraged Finance Conference, October 30, 2014 Copyright Page

Health Care Worldwide Barclays European High Yield and Leveraged Finance Conference October 30, 2014 London Barclays European High Yield and Leveraged Finance Conference, October 30, 2014 Copyright Page

Kuoni to focus on its core business as a service provider to the global travel industry

INFORMATION Zurich, 14 January 2015 Kuoni to focus on its core business as a service provider to the global travel industry Exit from tour operating activities Strategic initiatives to accelerate growth

INFORMATION Zurich, 14 January 2015 Kuoni to focus on its core business as a service provider to the global travel industry Exit from tour operating activities Strategic initiatives to accelerate growth

TO ACQUIRE FROM MICROSOFT CORPORATION

TO ACQUIRE FROM MICROSOFT CORPORATION AUGUST 11, 2009 MAURICE LÉVY CHAIRMAN AND CEO, PUBLICIS GROUPE DAVID KENNY MANAGING PARTNER, VIVAKI JEAN-MICHEL ETIENNE EXECUTIVE VP, GROUP CFO 1 Disclaimer Certain

TO ACQUIRE FROM MICROSOFT CORPORATION AUGUST 11, 2009 MAURICE LÉVY CHAIRMAN AND CEO, PUBLICIS GROUPE DAVID KENNY MANAGING PARTNER, VIVAKI JEAN-MICHEL ETIENNE EXECUTIVE VP, GROUP CFO 1 Disclaimer Certain

Our track record for innovation Your chance to shape the future. Engineering opportunities in France, Germany, Spain and UK:

Our track record for innovation Your chance to shape the future Engineering opportunities in France, Germany, Spain and UK: Over the next 20 years, faced with more financial and environmental pressures

Our track record for innovation Your chance to shape the future Engineering opportunities in France, Germany, Spain and UK: Over the next 20 years, faced with more financial and environmental pressures

Sound results for Alstom in 2015/16

PRESS RELEASE Sound results for Alstom in 2015/16 Record commercial year Very strong operational performance Strengthened balance sheet 2020 objectives confirmed 11 May 2016 Between 1 April 2015 and 31

PRESS RELEASE Sound results for Alstom in 2015/16 Record commercial year Very strong operational performance Strengthened balance sheet 2020 objectives confirmed 11 May 2016 Between 1 April 2015 and 31

Disclaimer. purposes only. Not for distribution in the United States, Japan, Australia, Italy or Canada.

8 April 2011 Disclaimer THIS PRESENTATION MAY NOT BE DISTRIBUTED, DIRECTLY OR INDIRECTLY, IN THE UNITED STATES, JAPAN, ITALY, AUSTRALIA, CANADA OR ANY OTHER COUNTRY IN WHICH THE DISTRIBUTION OR DIFFUSION

8 April 2011 Disclaimer THIS PRESENTATION MAY NOT BE DISTRIBUTED, DIRECTLY OR INDIRECTLY, IN THE UNITED STATES, JAPAN, ITALY, AUSTRALIA, CANADA OR ANY OTHER COUNTRY IN WHICH THE DISTRIBUTION OR DIFFUSION

Fleet and funding strategy Solid foundation for growth

Fleet and funding strategy Solid foundation for growth Erno Hildén, CFO Finnair Capital Markets Day, 22 May 2014 1 Disclaimer This document includes forward-looking statements. These forward-looking statements

Fleet and funding strategy Solid foundation for growth Erno Hildén, CFO Finnair Capital Markets Day, 22 May 2014 1 Disclaimer This document includes forward-looking statements. These forward-looking statements

Bank of America Merrill Lynch Banking & Financial Services Conference

Bank of America Merrill Lynch Banking & Financial Services Conference Manuel Medina Mora Chairman of the Global Consumer Banking Council November 17, 2010 Consumer Banking in Citicorp Agenda Our Business

Bank of America Merrill Lynch Banking & Financial Services Conference Manuel Medina Mora Chairman of the Global Consumer Banking Council November 17, 2010 Consumer Banking in Citicorp Agenda Our Business

Applus+ Group Results Presentation Third Quarter 2014 November 3rd 2014

Applus+ Group Results Presentation Third Quarter 2014 November 3rd 2014 DISCLAIMER This document may contain statements that constitute forward looking statements about Applus Services, SA ( Applus+ or

Applus+ Group Results Presentation Third Quarter 2014 November 3rd 2014 DISCLAIMER This document may contain statements that constitute forward looking statements about Applus Services, SA ( Applus+ or

The Key to Mobility. Creating Value with Financial Services. Fixed Income Investor Update - December 2010. Volkswagen Financial Services AG

The Key to Mobility Creating Value with Financial Services Fixed Income Investor Update - December 2010 Bernd Bode Head of Group Treasury and Investor Relations Volkswagen Financial Services Nils Allnoch

The Key to Mobility Creating Value with Financial Services Fixed Income Investor Update - December 2010 Bernd Bode Head of Group Treasury and Investor Relations Volkswagen Financial Services Nils Allnoch

Deutsche Bank. Andean Region Conference. London, May, 2016

Deutsche Bank Andean Region Conference London, May, 2016 This presentation may include forward-looking comments regarding the Company s business outlook and anticipated financial and operating results.

Deutsche Bank Andean Region Conference London, May, 2016 This presentation may include forward-looking comments regarding the Company s business outlook and anticipated financial and operating results.

Health Care Worldwide

Health Care Worldwide Goldman Sachs - Leveraged Finance Healthcare Conference March 4, 2014 New York Goldman Sachs Leveraged Finance Conference, Fresenius SE & Co. KGaA Copyright, March 4, 2014 Page 1

Health Care Worldwide Goldman Sachs - Leveraged Finance Healthcare Conference March 4, 2014 New York Goldman Sachs Leveraged Finance Conference, Fresenius SE & Co. KGaA Copyright, March 4, 2014 Page 1

Cazenove UK Companies Conference. Paul Brooks, Chief Financial Officer 18 April 2008

Cazenove UK Companies Conference Paul Brooks, Chief Financial Officer 18 April 2008 Overview Agenda Overview Strategic objectives Financial track record Summary 2 Overview Our vision For our people, data

Cazenove UK Companies Conference Paul Brooks, Chief Financial Officer 18 April 2008 Overview Agenda Overview Strategic objectives Financial track record Summary 2 Overview Our vision For our people, data

2014 Orders Received & Sales.... Joris.. Gröflin,. Chief. Financial.. Officer...

2014 Orders Received & Sales................................................... Joris.. Gröflin,. Chief. Financial.. Officer.................. Rieter Summary orders received & sales 2014 Double-digit sales

2014 Orders Received & Sales................................................... Joris.. Gröflin,. Chief. Financial.. Officer.................. Rieter Summary orders received & sales 2014 Double-digit sales

Raymond James Global Airline and Transportation Conference

Raymond James Global Airline and Transportation Conference United Continental Holdings, Inc. November 6, 2014 Jim Compton Vice Chairman and Chief Revenue Officer Safe Harbor Statement Certain statements

Raymond James Global Airline and Transportation Conference United Continental Holdings, Inc. November 6, 2014 Jim Compton Vice Chairman and Chief Revenue Officer Safe Harbor Statement Certain statements

UBS Global Financials Conference

UBS Global Financials Conference George Culmer, Group CFO Simon Lee, CEO International 11 May 21 AGENDA Overview George Culmer, CFO UK International Simon Lee, CEO International Emerging Markets Wrap up

UBS Global Financials Conference George Culmer, Group CFO Simon Lee, CEO International 11 May 21 AGENDA Overview George Culmer, CFO UK International Simon Lee, CEO International Emerging Markets Wrap up

A good start to the year, in line with expectations Danone continues to re-balance its model of growth

First-quarter 206 sales Press release Paris, April 9, 206 A good start to the year, in line with expectations Danone continues to re-balance its model of growth FIRST QUARTER 206 sales growth: +3.5% Solid

First-quarter 206 sales Press release Paris, April 9, 206 A good start to the year, in line with expectations Danone continues to re-balance its model of growth FIRST QUARTER 206 sales growth: +3.5% Solid

The Global Outlook for Aluminium in Transportation

The Global Outlook for Aluminium in Transportation l What is the future of aluminium in the transportation sector? l What are the key trends and drivers in the industry? l What is the aluminium market

The Global Outlook for Aluminium in Transportation l What is the future of aluminium in the transportation sector? l What are the key trends and drivers in the industry? l What is the aluminium market

March 2015 Debt Investor Update

March 2015 Debt Investor Update E u r o p e s O n l y U l t r a L o w C o s t C a r r i e r Proven, resilient business model Europe s lowest fares/lowest unit costs Europe s No 1, Traffic Europe s No 1,

March 2015 Debt Investor Update E u r o p e s O n l y U l t r a L o w C o s t C a r r i e r Proven, resilient business model Europe s lowest fares/lowest unit costs Europe s No 1, Traffic Europe s No 1,

H1 2015 Results. 12 August 2015

H1 2015 Results Agenda Agenda H1 2015 at a glance Building industry outlook 2015 Outlook 2015 2 Stable operating margins Group net sales increase of 20.1% to CHF 1 308 million In local currencies, net

H1 2015 Results Agenda Agenda H1 2015 at a glance Building industry outlook 2015 Outlook 2015 2 Stable operating margins Group net sales increase of 20.1% to CHF 1 308 million In local currencies, net

UBS Pan European Conference. Hervé Multon, SVP Strategy 1st June 2012

UBS Pan European Conference Hervé Multon, SVP Strategy 1st June 2012 2 / Thales in a snapshot Revenues: 13bn EBIT: 749m Leading positions in Defence & Security and Aerospace & Transport 33% of FY11 orders

UBS Pan European Conference Hervé Multon, SVP Strategy 1st June 2012 2 / Thales in a snapshot Revenues: 13bn EBIT: 749m Leading positions in Defence & Security and Aerospace & Transport 33% of FY11 orders

Makita Corporation. Consolidated Financial Results for the nine months ended December 31, 2007 (U.S. GAAP Financial Information)

") Makita Corporation Consolidated Financial Results for the nine months ended (U.S. GAAP Financial Information) (English translation of "ZAIMU/GYOSEKI NO GAIKYO" originally issued in Japanese language) CONSOLIDATED

Makita Corporation Consolidated Financial Results for the nine months ended (U.S. GAAP Financial Information) (English translation of "ZAIMU/GYOSEKI NO GAIKYO" originally issued in Japanese language) CONSOLIDATED

Boeing Capital Corporation. Current Aircraft Finance Market Outlook 2016. Copyright 2015 Boeing. All rights reserved.

Boeing Capital Corporation Current Aircraft Finance Market Outlook 2016 The 2016 Current Aircraft Finance Market Outlook forecasts continued strength in the primary aircraft finance sectors, with a growing

Boeing Capital Corporation Current Aircraft Finance Market Outlook 2016 The 2016 Current Aircraft Finance Market Outlook forecasts continued strength in the primary aircraft finance sectors, with a growing

Health Care Worldwide

Health Care Worldwide Credit Suisse Global Credit Products Conference September 18, 2014 Miami Credit Suisse Global Credit Products Conference, September 18, 2014 Copyright Page 1 Safe Harbor Statement

Health Care Worldwide Credit Suisse Global Credit Products Conference September 18, 2014 Miami Credit Suisse Global Credit Products Conference, September 18, 2014 Copyright Page 1 Safe Harbor Statement

Integrating Automotive and Financial Services

Integrating Automotive and Financial Services Frank Witter, CEO Volkswagen Financial Services AG Frank Fiedler, CFO Volkswagen Financial Services AG Ehra-Lessien, 11 March 2009 Agenda Financial Services

Integrating Automotive and Financial Services Frank Witter, CEO Volkswagen Financial Services AG Frank Fiedler, CFO Volkswagen Financial Services AG Ehra-Lessien, 11 March 2009 Agenda Financial Services

Delivering Sustainable Growth. Bill Seeger

GKN Delivering Sustainable Growth Bill Seeger Overview GKN is now well positioned to deliver sustainable growth following the completion of significant restructuring initiatives GKN s aim of delivering

GKN Delivering Sustainable Growth Bill Seeger Overview GKN is now well positioned to deliver sustainable growth following the completion of significant restructuring initiatives GKN s aim of delivering

Financial Information

Financial Information Solid results with in all key financial metrics of 23.6 bn, up 0.4% like-for like Adjusted EBITA margin up 0.3 pt on organic basis Net profit up +4% to 1.9 bn Record Free Cash Flow

Financial Information Solid results with in all key financial metrics of 23.6 bn, up 0.4% like-for like Adjusted EBITA margin up 0.3 pt on organic basis Net profit up +4% to 1.9 bn Record Free Cash Flow

Marketing and Sales Highlights of the Volkswagen Group. Investor Meeting London, 13 July 2006

Marketing and Sales Highlights of the Volkswagen Group Stefan Jacoby, Executive Vice President Marketing & Sales Volkswagen Group Investor Meeting London, 13 July 2006 1. Marketing and Sales structure

Marketing and Sales Highlights of the Volkswagen Group Stefan Jacoby, Executive Vice President Marketing & Sales Volkswagen Group Investor Meeting London, 13 July 2006 1. Marketing and Sales structure

Unilever First Half 2015 Results Paul Polman / Jean-Marc Huët 23 rd July 2015

Unilever First Half 2015 Results Paul Polman / Jean-Marc Huët 23 rd July 2015 SAFE HARBOUR STATEMENT This announcement may contain forward-looking statements, including forward-looking statements within

Unilever First Half 2015 Results Paul Polman / Jean-Marc Huët 23 rd July 2015 SAFE HARBOUR STATEMENT This announcement may contain forward-looking statements, including forward-looking statements within

Global Client Group The Gateway to AWM

Global Client Group The Gateway to AWM January 2013 For professional investors only Content 1 2 3 Deutsche Bank and Asset Global Client Group Our product and service offering 1 Deutsche Bank A global partner

Global Client Group The Gateway to AWM January 2013 For professional investors only Content 1 2 3 Deutsche Bank and Asset Global Client Group Our product and service offering 1 Deutsche Bank A global partner

Full year results. March 2012

2 0 1 1 Full year results March 2012 1 DISCLAIMER Safe Harbour Statement This presentation contains forward-looking statements (made pursuant to the safe harbour provisions of the Private Securities Litigation

2 0 1 1 Full year results March 2012 1 DISCLAIMER Safe Harbour Statement This presentation contains forward-looking statements (made pursuant to the safe harbour provisions of the Private Securities Litigation

Statement by Kasper Rorsted Chairman of the Management Board Conference-Call November 11, 2015, 10.30 a.m.

Statement by Kasper Rorsted Chairman of the Management Board Conference-Call November 11, 2015, 10.30 a.m. Welcome to our conference call today. As you will have seen, this morning we sent out our news

Statement by Kasper Rorsted Chairman of the Management Board Conference-Call November 11, 2015, 10.30 a.m. Welcome to our conference call today. As you will have seen, this morning we sent out our news

Schroders plc Bernstein Strategic Decisions Conference 1 October 2013

Schroders plc Bernstein Strategic Decisions Conference 1 October 2013 Massimo Tosato Executive Vice Chairman Schroders: a global business with AUM of over 255bn Depth and strength of investment resource:

Schroders plc Bernstein Strategic Decisions Conference 1 October 2013 Massimo Tosato Executive Vice Chairman Schroders: a global business with AUM of over 255bn Depth and strength of investment resource:

Agenda. Forward-looking Statements Denis Jasmin, Vice-President, Investor Relations

SECOND QUARTER 2013 Conference Call Notes August 2, 2013 2 Agenda Forward-looking Statements Denis Jasmin, Vice-President, Investor Relations President and CEO Remarks Robert G. Card, President and Chief

SECOND QUARTER 2013 Conference Call Notes August 2, 2013 2 Agenda Forward-looking Statements Denis Jasmin, Vice-President, Investor Relations President and CEO Remarks Robert G. Card, President and Chief

Airbus Progamme Review

Airbus Progamme Review Tom WILLIAMS Executive Vice President Programmes Global Investor Forum 2009, Broughton, 1 st & 2 nd April 2009 1 1 Safe Harbour Statement Disclaimer This presentation includes forward-looking

Airbus Progamme Review Tom WILLIAMS Executive Vice President Programmes Global Investor Forum 2009, Broughton, 1 st & 2 nd April 2009 1 1 Safe Harbour Statement Disclaimer This presentation includes forward-looking

Investor Visit Danske Bank

Investor Visit Danske Bank Martin Primus Head of Financial Communication/ Financial Analysis, AUDI AG May 28, 2014 Audi Group Key figures 2013 1,605,926 Production Audi brand 10.1% Operating return on

Investor Visit Danske Bank Martin Primus Head of Financial Communication/ Financial Analysis, AUDI AG May 28, 2014 Audi Group Key figures 2013 1,605,926 Production Audi brand 10.1% Operating return on

Protection notice / Copyright notice

Infrastructure & Cities (IC) Analyst Call Dr. Roland Busch Member of the Managing Board of Siemens AG CEO of Infrastructure & Cities Sector December 5, 2011 Protection notice / Copyright notice Safe Harbour

Infrastructure & Cities (IC) Analyst Call Dr. Roland Busch Member of the Managing Board of Siemens AG CEO of Infrastructure & Cities Sector December 5, 2011 Protection notice / Copyright notice Safe Harbour

4Q 2015 Earnings Conference Call January 27, 2016

4Q 2015 Earnings Conference Call January 27, 2016 Note: All results in this presentation reflect continuing operations unless otherwise noted. Cautionary Statement: This presentation includes statements

4Q 2015 Earnings Conference Call January 27, 2016 Note: All results in this presentation reflect continuing operations unless otherwise noted. Cautionary Statement: This presentation includes statements

J.P. MORGAN HIGH YIELD & LEVERAGED FINANCE CONFERENCE FEBRUARY 24, 2015

J.P. MORGAN HIGH YIELD & LEVERAGED FINANCE CONFERENCE FEBRUARY 24, 2015 DISCLAIMER This presentation contains, in addition to historical information, certain forward-looking statements within the meaning

J.P. MORGAN HIGH YIELD & LEVERAGED FINANCE CONFERENCE FEBRUARY 24, 2015 DISCLAIMER This presentation contains, in addition to historical information, certain forward-looking statements within the meaning

Danske Bank acquires Sampo Bank

P R E S S C O N F E R E N C E Danske Bank acquires Sampo Bank Expansion into the Finnish and Baltic markets Peter Straarup, Chairman of the Executive Board November 9, 2006 Danske Bank acquires Sampo Bank

P R E S S C O N F E R E N C E Danske Bank acquires Sampo Bank Expansion into the Finnish and Baltic markets Peter Straarup, Chairman of the Executive Board November 9, 2006 Danske Bank acquires Sampo Bank

Global outlook: Healthcare

Global outlook: Healthcare March 2014 healthcare 1 Today s presenters Ana Nicholls Managing Editor, Industry Briefing Economist Intelligence Unit Lauren Brayshaw Marketing executive Economist Intelligence

Global outlook: Healthcare March 2014 healthcare 1 Today s presenters Ana Nicholls Managing Editor, Industry Briefing Economist Intelligence Unit Lauren Brayshaw Marketing executive Economist Intelligence

Lockheed Martin Corporation

Lockheed Martin Corporation Portfolio Shaping Actions & 2 nd Quarter 2015 Financial Results July 20, 2015 11:00 am EDT Webcast login at www.lockheedmartin.com/investor Webcast replay & podcast available

Lockheed Martin Corporation Portfolio Shaping Actions & 2 nd Quarter 2015 Financial Results July 20, 2015 11:00 am EDT Webcast login at www.lockheedmartin.com/investor Webcast replay & podcast available

GET to 8 Daimler Trucks Path to Profitable Growth

GET to 8 Daimler Trucks Path to Profitable Growth Daimler Trucks and Daimler Buses Division Day Wörth, 30th November 2010 Andreas Renschler, Head of Daimler Trucks and Daimler Buses Current performance

GET to 8 Daimler Trucks Path to Profitable Growth Daimler Trucks and Daimler Buses Division Day Wörth, 30th November 2010 Andreas Renschler, Head of Daimler Trucks and Daimler Buses Current performance

Reach for the skies. The Aerospace Growth Partnership. Industry and government working together to secure the future for UK aerospace

Reach for the skies The Aerospace Growth Partnership Industry and government working together to secure the future for UK aerospace Maintaining our leadership as an aerospace nation The UK has a great

Reach for the skies The Aerospace Growth Partnership Industry and government working together to secure the future for UK aerospace Maintaining our leadership as an aerospace nation The UK has a great

BIS CEMLA Roundtable on Fiscal Policy, public debt management and government bond markets: issues for central banks

BIS CEMLA Roundtable on Fiscal Policy, public debt management and government bond markets: issues for central banks Is monetary policy constrained by fiscal policy? by Carlos Montoro 26-27 November 212

BIS CEMLA Roundtable on Fiscal Policy, public debt management and government bond markets: issues for central banks Is monetary policy constrained by fiscal policy? by Carlos Montoro 26-27 November 212

Ferrari posted a record Q3 2015 performance

Ferrari posted a record Q3 2015 performance Shipments were 1,949 units, up 21% Net revenues were up 9% (3% at constant currencies) to Euro 723 million EBIT reached Euro 141 million, 610bps margin increase

Ferrari posted a record Q3 2015 performance Shipments were 1,949 units, up 21% Net revenues were up 9% (3% at constant currencies) to Euro 723 million EBIT reached Euro 141 million, 610bps margin increase

Third quarter 2015. Vestas Wind Systems A/S. Copenhagen, 5 November 2015

Third quarter Vestas Wind Systems A/S Copenhagen, 5 November Disclaimer and cautionary statement This document contains forward-looking statements concerning Vestas financial condition, results of operations

Third quarter Vestas Wind Systems A/S Copenhagen, 5 November Disclaimer and cautionary statement This document contains forward-looking statements concerning Vestas financial condition, results of operations

Air Arabia. Investor Presentation FY 2015

Air Arabia Investor Presentation FY 2015 Disclaimer Information contained in this presentation is subject to change without notice, its accuracy is not guaranteed and it may not contain all material information

Air Arabia Investor Presentation FY 2015 Disclaimer Information contained in this presentation is subject to change without notice, its accuracy is not guaranteed and it may not contain all material information

FTI Consulting +44 (0)20 3727 1340 Richard Mountain / Susanne Yule

20 3727 1340 Richard Mountain / Susanne Yule") 13 October 2015 THIRD QUARTER 2015 INTERIM MANAGEMENT STATEMENT Highlights* 10.2% Group gross profit growth, good contributions from all four regions FX lowered gross profit by c. 7m (c. 18m YTD) Double-digit

13 October 2015 THIRD QUARTER 2015 INTERIM MANAGEMENT STATEMENT Highlights* 10.2% Group gross profit growth, good contributions from all four regions FX lowered gross profit by c. 7m (c. 18m YTD) Double-digit

2014 HALF YEAR RESULTS 4 September 2014

862m H1 2014 Revenues 2014 HALF YEAR RESULTS 4 September 2014 57% of Revenues for International in H1 2014 21,657 Employees In H1 2014 Disclaimer This presentation contains forward-looking statements (as

862m H1 2014 Revenues 2014 HALF YEAR RESULTS 4 September 2014 57% of Revenues for International in H1 2014 21,657 Employees In H1 2014 Disclaimer This presentation contains forward-looking statements (as

2016 Outlook of the Global Security Industry

Brochure More information from http://www.researchandmarkets.com/reports/3623776/ 2016 Outlook of the Global Security Industry Description: Being aware of future cyber threats and trends at the national

Brochure More information from http://www.researchandmarkets.com/reports/3623776/ 2016 Outlook of the Global Security Industry Description: Being aware of future cyber threats and trends at the national

REMARKS FOR ACQUISITION OF OXFORD AVIATION ACADEMY. May 16, 2012. Time: 1:00p.m. Speakers: Mr. Marc Parent, President and Chief Executive Officer

REMARKS FOR ACQUISITION OF OXFORD AVIATION ACADEMY May 16, 2012 Time: 1:00p.m. Speakers: Mr. Marc Parent, President and Chief Executive Officer Mr. Stephane Lefebvre, Vice President, Finance, and Chief

REMARKS FOR ACQUISITION OF OXFORD AVIATION ACADEMY May 16, 2012 Time: 1:00p.m. Speakers: Mr. Marc Parent, President and Chief Executive Officer Mr. Stephane Lefebvre, Vice President, Finance, and Chief

Figure 1: Global Aggregates: Industrial Production (% MoM Ann., 3M moving average)

") Figure 1: Global Aggregates: Industrial Production (% MoM Ann., 3M moving average) World Advanced Economies Emerging Market Economies Notes: Nowcasts are in red. World is the PPP-weighted average of US,

Figure 1: Global Aggregates: Industrial Production (% MoM Ann., 3M moving average) World Advanced Economies Emerging Market Economies Notes: Nowcasts are in red. World is the PPP-weighted average of US,

Head of Global Transaction Banking and

Head of Global Transaction Banking and Member of the Group Executive Committee 8. WestLB Deutschland Conference Frankfurt, 17 November 2010 Agenda 3Q2010 Highlights Global Transaction Banking (GTB) 1 Strong

Head of Global Transaction Banking and Member of the Group Executive Committee 8. WestLB Deutschland Conference Frankfurt, 17 November 2010 Agenda 3Q2010 Highlights Global Transaction Banking (GTB) 1 Strong

April 1, 2010. Rudi Ludwig, CEO Wilfried Trepels, CFO

Annual Financial i Statements t t 2009 April 1, 2010 Rudi Ludwig, CEO Wilfried Trepels, CFO 1 Agenda 1. Executive Summary 2. Background Market Performance 3. Business Performance 4. Financials 5. Next

Annual Financial i Statements t t 2009 April 1, 2010 Rudi Ludwig, CEO Wilfried Trepels, CFO 1 Agenda 1. Executive Summary 2. Background Market Performance 3. Business Performance 4. Financials 5. Next

Global Supply. 17 November 2011

Global Supply 17 November 2011 David Gosnell President, Global Supply and Procurement Supply goals: Enhancing margin and enabling growth Competitive advantage in cost will deliver gross margin expansion

Global Supply 17 November 2011 David Gosnell President, Global Supply and Procurement Supply goals: Enhancing margin and enabling growth Competitive advantage in cost will deliver gross margin expansion

Q2 and Half-Year 2016 Results. July 21, 2016

Q2 and Half-Year 2016 Results July 21, 2016 Contents Results for Q2 2016 Outlook for 2016 Development at the divisions Q2 and Half-Year 2016 Results / July 21, 2016 / Page 2 Highlights of Q2 2016 Strong

Q2 and Half-Year 2016 Results July 21, 2016 Contents Results for Q2 2016 Outlook for 2016 Development at the divisions Q2 and Half-Year 2016 Results / July 21, 2016 / Page 2 Highlights of Q2 2016 Strong

Overseas Business Strategy

Panasonic IR Day 2014 Overseas Business Strategy May 21, 2014 Panasonic Corporation Yoshihiko Yamada Notes: 1. This is an English translation from the original presentation in Japanese. 2. In this presentation,

Panasonic IR Day 2014 Overseas Business Strategy May 21, 2014 Panasonic Corporation Yoshihiko Yamada Notes: 1. This is an English translation from the original presentation in Japanese. 2. In this presentation,

Purchasing Managers Index (PMI ) series are monthly economic surveys of carefully selected companies compiled by Markit.

series are monthly economic surveys of carefully selected companies compiled by Markit.") PMI Purchasing Managers Index (PMI ) series are monthly economic surveys of carefully selected companies compiled by Markit. They provide an advance signal of what is really happening in the private sector

PMI Purchasing Managers Index (PMI ) series are monthly economic surveys of carefully selected companies compiled by Markit. They provide an advance signal of what is really happening in the private sector

ON TRACK TO MEET FULL YEAR EXPECTATIONS. Overview. Strategic Highlights. Alison Cooper, Chief Executive, commented

ON TRACK TO MEET FULL YEAR EXPECTATIONS Overview First quarter performance in line with guidance and on track to meet full year outlook US business performing well and to plan Tobacco net revenue up 16.6%

ON TRACK TO MEET FULL YEAR EXPECTATIONS Overview First quarter performance in line with guidance and on track to meet full year outlook US business performing well and to plan Tobacco net revenue up 16.6%

PRESS RELEASE. Revenue as of March 31, 2011. Sharp growth in Bureau Veritas Q1 2011 revenue Revenue up 23% to 775 million Organic growth of 6.

1 PRESS RELEASE Neuilly-sur-Seine, France, May 4, 2011 Sharp growth in Bureau Veritas Q1 2011 revenue Revenue up 23% to 775 million Organic growth of 6.5% Frank Piedelièvre, Chairman and Chief Executive

1 PRESS RELEASE Neuilly-sur-Seine, France, May 4, 2011 Sharp growth in Bureau Veritas Q1 2011 revenue Revenue up 23% to 775 million Organic growth of 6.5% Frank Piedelièvre, Chairman and Chief Executive

Building a World-Class Integrated Supply Chain

Building a World-Class Integrated Supply Chain Daniel Myers Executive Vice President Supply Chain 1 Forward-Looking Statements Forward-Looking Statements This slide presentation contains a number of forward-looking

Building a World-Class Integrated Supply Chain Daniel Myers Executive Vice President Supply Chain 1 Forward-Looking Statements Forward-Looking Statements This slide presentation contains a number of forward-looking

Solvay and INEOS to create a world-class PVC producer Solvay accelerates its transformation

Solvay and INEOS to create a world-class PVC producer Solvay accelerates its transformation May 7 th, 2013 Agenda A key milestone in Solvay s transformation Joint venture s strategic rationale INEOS overview

Solvay and INEOS to create a world-class PVC producer Solvay accelerates its transformation May 7 th, 2013 Agenda A key milestone in Solvay s transformation Joint venture s strategic rationale INEOS overview

The Global Cyber Security Market 2015-2025

Brochure More information from http://www.researchandmarkets.com/reports/3502775/ The Global Cyber Security Market 2015-2025 Description: Summary During the forecast period the demand for cyber security

Brochure More information from http://www.researchandmarkets.com/reports/3502775/ The Global Cyber Security Market 2015-2025 Description: Summary During the forecast period the demand for cyber security

The Future of Consumer Health Care

The Future of Consumer Health Care Coming Together To Lead The Consumer Health Care Industry 2 Creating a New Business Model in Consumer Health Care 3 Serve More Consumers In More Parts of the World, More

The Future of Consumer Health Care Coming Together To Lead The Consumer Health Care Industry 2 Creating a New Business Model in Consumer Health Care 3 Serve More Consumers In More Parts of the World, More

Introduction. Anders Runevad, Group President & CEO Marika Fredriksson, Executive VP & CFO

Introduction Anders Runevad, Group President & CEO Marika Fredriksson, Executive VP & CFO Aarhus, 12 June 2014 Disclaimer and cautionary statement This presentation contains forward-looking statements

Introduction Anders Runevad, Group President & CEO Marika Fredriksson, Executive VP & CFO Aarhus, 12 June 2014 Disclaimer and cautionary statement This presentation contains forward-looking statements