Employee Misclassification & Unemployment Insurance Audits

|

|

|

- Virgil Hill

- 7 years ago

- Views:

Transcription

1 Employee Misclassification & Unemployment Insurance Audits 2009 National Unemployment Insurance Conference Tom Crowley, UI Tax Chief USDOL/ETA/OUI

2 Urban Myths Dispelling Falsehoods, Rumors & Innuendo Employers are often perceived to be the bad guy Should not be - Most employers classify their employees properly and file & pay their taxes on-time Independent Contactors are inherently bad False Properly classified ICs play a crucial role in a vibrant and dynamic US economy Employee Classification is easy False Employers, Congress, Federal and state employment tax officials struggle to define employee and employment Abusers of Employee Misclassification will be targeted more in the future True

3 Auditing and Employee Misclassification Employee Misclassification What is it? Why do we care? Employer Audits What are they? How do we measure results? Future measures? State Task Force Initiatives Sharing Information

4 Employee Misclassification What is it? Misclassification occurs when a worker s employment status is incorrectly classified In the context of this discussion, we assume the worker was incorrectly classified as an independent contractor, instead of as an employee

5 Worker Classification Consequences of Abuse Employers gain unfair competitive advantage Workers denied access to: Affordable health care and retirement plans UI benefits Labor law protections afforded to employees Independent Contractors (IC) pay higher: FICA Quarterly estimated payments for federal & state taxes Health care costs Workers Compensation premiums If the IC unable to pay the above: Forces eligible workers out of the system Lowers tax revenue Further degrades UI coverage

6 Common Law, conjunctive ABC test for UI A - Direction and control, and B - Outside usual course / place of business, and C - Worker in an independent trade or business Used by the majority of states Many states use only A & C Others look to the IRS for guidance Employee Defined At the State UI Level

7 Common Law Often stated what does it mean? A system of law that is derived from judges' decisions, which arise from the judicial branch of government, rather than statutes or constitutions, which are derived from the legislative branch of government. Statutes trump common law until the statutes are litigated in court and become common law

8 Employee Defined At the Federal Level FUTA 3306(i) defines employee by reference, under IRC 3121(d) employee means (2) any individual who, under the usual common law rules applicable in determining the employeremployee relationship, has the status of employee; By Regulation in 26 CFR (d)-1 An employer / employee relationship exists when the employer has the right to control and direct the individual who performs the services It is sufficient if the employer has the right to do so. To determine direction and control, IRS initially used a 20 factor test, as described in Revenue Ruling Factor Test evolved into three types of evidence Behavioral a right to direct or control, instructions or training Financial worker opportunity for profit / loss, unreimbursed expenses Relationship right to terminate, permanency, benefits

9 IRS 20 factors Instructions Training Integration Service rendered personally Hiring, supervising, and paying assistants Continuing relationship Set hours of work Full-time work required Doing work on business owner s premises Accomplishing work in certain order or sequence Submission of oral or written reports Method of payment Payment of business or traveling expenses Furnishing tools and equipment Significant investment Realization of profit or loss Work for one entity at a time Offer their services to the general public Right to discharge Right to terminate

10 Employee Misclassification Employer Employee Consequences Employer substantially reduces costs by offloading employment tax and worker s compensation costs to the I.C. Misclassified employee s income substantially reduced by the amount of the increased employment tax responsibilities, unless employer subsidizes the taxes by increasing pay

11 Employee Misclassification Impact on Unemployment Insurance (UI) Taxes Reduced tax revenue for state and federal UI. Every 200,000 workers misclassified = $11 million lost FUTA and significantly more lost to state UI trust funds Benefits The de facto loss of UI coverage. Employee entitlement to UI, however, is based on the circumstances of their employment and their job separation, NOT the employer s UI reporting and payment history.

12 The Field Audit Function Citation from the Employment Security Manual (ESM) 3670 Objectives of a Field Audit Program. A comprehensive field audit program is vital to the administration of a State unemployment compensation (UC) system. A well-planned and cost effective field audit program, executed in coordination with central office activities and other unemployment insurance field undertakings, is an efficient means of ensuring compliance with State UC law and timely collection of taxes on an equitable basis.

13 ESM Audit Requirements An audit must include the following minimum requirements: 1. Commence with an opening interview with the employer or a designated representative; 2. Cover a minimum four calendar quarters; 3. Verify the business entity as a sole proprietor, partnership, corporation, joint venture, or other; 4. Document records examined and evidence obtained in tests used to verify payroll procedure, accuracy, and completeness; 5. Document records available and examined and the evidence obtained in the search for misclassified workers and payments; 6. Conclude with a closeout conference with the employer or a designated representative. If closure is not possible, explain in the report; and 7. Include a written report stating the auditor's final determination and all facts contributing to or supporting that determination.

14 What Is Important? Verify the employer (no fictitious employer - ID fraud) Verify employer reports all wages properly Verify employer classifies employees properly Validate reporting (do the math excess wage calculation) Investigate hidden wages (this is not misclassification) Bottom line Ensure wages reported properly to enable accurate tax payments and UI benefit payments (ultimately Job #1)

Investigate hidden wages (this is not misclassification) Bottom line Ensure wages")

15 Tax Performance System (TPS) (How We Currently Measure Audit Performance) TPS: A systematic review of state UI tax operations that occurs annually in every state. The field audit program is one of the areas that undergo examination every year. Primary objective: to promote and verify employer compliance with State laws, regulations and policies. Systems Review: An assessment of internal controls and systems Computed Measures % change in total wages resulting from audit Not benchmarked (no requirement) % of contributory employers audited 2% required % of total wages audited. (Annualized) Not benchmarked (no requirement)

16 Audit Selection Alternatives Random Selection Impartial Every employer has an equal chance of being selected Far-Reaching Outreach opportunity for all employers Thorough Randomization could select employers that would otherwise be omitted Most employers comply with the law most audits will be uncomplicated and without adjustments Targeted Selection Focused on employers more likely to be problematic Maximizes resources on areas likely to yield results Profile by Industry, Location, Past History, IRS leads Emphasizes search for misclassified employees Emphasizes enforcing UI coverage provisions Trying to select employers likely to be problematic most audits will be complicated and require adjustments Labor-intensive Less audits conducted using same resources

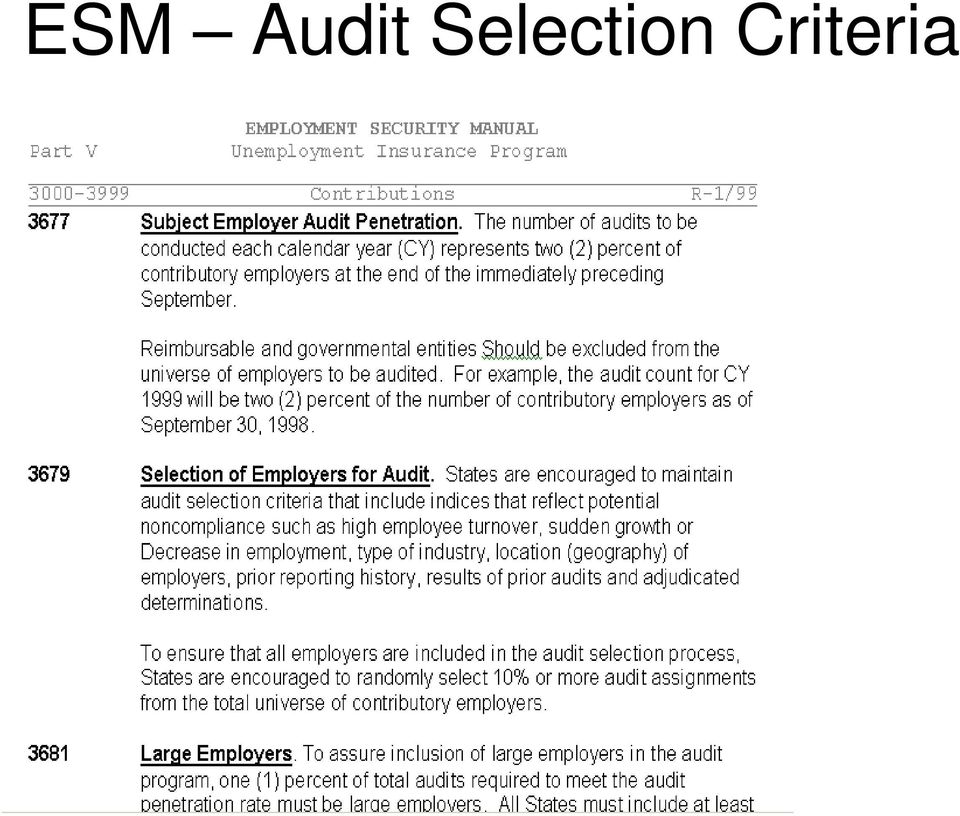

17 ESM Audit Selection Criteria

18 Audit Penetration Rate ESM Subject Employer Audit Penetration. The number of audits to be conducted each calendar year (CY) represents two (2) percent of contributory employers at the end of the immediately preceding September.

represents two (2) percent of contributory")

19 Penetration Rate Truth or Consequences MD - 140,000 employers X 2% = 2,800 audits required annually Audit 1 Granny with a domestic Audit 2 Landscaper with 10 employees, 20 permanent 1099 ICs, and 150 workers not included in any employer accounting records Audit 3 - Boeing 158,000 employees Each of these 3 audits counts equally MD has about 35 auditors auditing 2,400 grannies each year is easy, but what about the landscaper and the big employer?

20 Performance Consequences TPS Program Review (System Review & Acceptance Sample) failing 3 or more consecutive years requires corrective action plan Audit Penetration Rate State notified of failure each quarter by USDOL % Wage Change No benchmark (yet) % Wages Audited No benchmark (yet)

% Wages Audited No benchmark")

21 National Total for UI Tax Employer Audit Penetration Rate (Percent of Contributory Employer Audited Annually - 2% Required) Percent Number of States Average % Median % # States >= 2% # States >= 1% 0

22 US Total Wage Change From UI Employer Audits Percent Number of States Average % Median % # States >= 2% # States >= 3% 0

23 US Total - Annualized % of Total Wages Audited Percent Number of States Average % Median % # of States >= 2% # of States >= 1% 0

24 Field Audit Measurement Team Comprised of USDOL and State UI tax administrators CA, CT, FL, MI, PA, TX, WV 1 st Meeting Nov Questions to be answered: What tells you that you have conducted a successful audit? How would you measure that?

25 Field Audit Measurement Team Team members care passionately about the employer audit program State members work hard to fulfill the program s mission Computed Measures are valuable, but they do not measure the # of employee misclassifications detected Need to not only define how we measure, but also define what we measure. A basic, but key question: What is an audit? When states do audit work that does not meet ESM definitions, that data is not reported to USDOL Work is still being done, but it is not counted More to come.

26 State UI Tax Enforcement Activity Year # Audits # Misclassified Total Wages % Audits Resulting Workers Discovered in Change , ,262 $1,815,968, % , ,044 $2,022,483, % , ,064 $2,242,798, % , ,809 $2,235,658, % , ,998 $2,570,351, % , ,039 $9,290,360, % , ,109 $3,072,609, % National summary of State UI audit activity On average, UI tax audits detect 1.35 worker misclassifications per audit

27 State Task Force Initiatives

28 State Task Force Initiatives

29 New York Task Force Results

30 UI Tax Data-Sharing Efforts Historically, each state operated within their own silo Now, reaching out to include: IRS Questionable Employment Tax Practices (QETP), 1099-MISC HHS/SSA National Directory of New Hires (NDNH) Intra-state agencies (revenue, workers compensation, wage & hour, licensing, etc.) Interstate Efforts Considering data sharing among states for SUTA dumping violators Issues to Consider: Confidentiality and Disclosure rules Secure PII information from unauthorized and malicious access

31 Contact Information USDOL 200 Constitution Ave N.W. S-4231 Washington, DC 20210

Employee vs. Independent Contractor: Protecting Your Company

Attorney Stephen A. DiTullio DeWitt Ross & Stevens S.C. 2 E. Mifflin Street, Suite 600 Madison, WI 53703 (608) 252 9362 sad@dewittross.com 1 Background Facts & Statistics 60% of all businesses use independent

Attorney Stephen A. DiTullio DeWitt Ross & Stevens S.C. 2 E. Mifflin Street, Suite 600 Madison, WI 53703 (608) 252 9362 sad@dewittross.com 1 Background Facts & Statistics 60% of all businesses use independent

This section incorporates the IRS guidelines that are currently in effect.

Guidelines on How to Determine the Classification of Independent Contractors versus Employees Overview The University classifies and pays individuals who provide services as employees, unless the nature

Guidelines on How to Determine the Classification of Independent Contractors versus Employees Overview The University classifies and pays individuals who provide services as employees, unless the nature

Independent Contractor or Employee? Worker Classification Rules under IRS Guidelines

Independent Contractor or Employee? Worker Classification Rules under IRS Guidelines Christine F. Miller (512) 495-6039 (512) 505-6339 FAX Email: cmiller@mcginnislaw.com 1 Introduction What do AT&T, JPMorgan

Independent Contractor or Employee? Worker Classification Rules under IRS Guidelines Christine F. Miller (512) 495-6039 (512) 505-6339 FAX Email: cmiller@mcginnislaw.com 1 Introduction What do AT&T, JPMorgan

B. The History of the Law

An Advisory from the Attorney General s Fair Labor Division on M.G.L. c. 149, s. 148B 2008/1 1 The Office of the Attorney General (AGO) issues the following Advisory regarding M.G.L. c. 149, s. 148B, the

An Advisory from the Attorney General s Fair Labor Division on M.G.L. c. 149, s. 148B 2008/1 1 The Office of the Attorney General (AGO) issues the following Advisory regarding M.G.L. c. 149, s. 148B, the

Worker Classifications: Employee or Independent Contractor

Worker Classifications: Employee or Independent Contractor 1 Worker Misclassifications Worker classified as an independent contractor (1099-MISC) versus as an employee (W-2) Employer avoids paying income

Worker Classifications: Employee or Independent Contractor 1 Worker Misclassifications Worker classified as an independent contractor (1099-MISC) versus as an employee (W-2) Employer avoids paying income

Misclassified? The Fight Against Independent Contractors

Misclassified? The Fight Against Independent Contractors Christine E. Reinhard August 15, 2014 All Rights Reserved Schmoyer Reinhard LLP If It Looks Like a Duck 1 Questions of the Day Why are independent

Misclassified? The Fight Against Independent Contractors Christine E. Reinhard August 15, 2014 All Rights Reserved Schmoyer Reinhard LLP If It Looks Like a Duck 1 Questions of the Day Why are independent

Independent Contractor Versus Employee Status

12 Independent Contractor Versus Employee Status Failing to appropriately classify a worker as an employee or an independent contractor can have serious consequences. Companies that misclassify workers

12 Independent Contractor Versus Employee Status Failing to appropriately classify a worker as an employee or an independent contractor can have serious consequences. Companies that misclassify workers

SPECIAL REPORT CLASSIFYING WORKERS AS EMPLOYEES OR INDEPENDENT CONTRACTORS (04-03-14)

") SPECIAL REPORT CLASSIFYING WORKERS AS EMPLOYEES OR INDEPENDENT CONTRACTORS (04-03-14) This Special Report was written by Daniel P. Hale, J.D., CPCU, ARM, CRM, LIC, AIC, AIS, API of Marsh & McLennan Agency

SPECIAL REPORT CLASSIFYING WORKERS AS EMPLOYEES OR INDEPENDENT CONTRACTORS (04-03-14) This Special Report was written by Daniel P. Hale, J.D., CPCU, ARM, CRM, LIC, AIC, AIS, API of Marsh & McLennan Agency

PRESENT LAW AND BACKGROUND RELATING TO WORKER CLASSIFICATION FOR FEDERAL TAX PURPOSES

PRESENT LAW AND BACKGROUND RELATING TO WORKER CLASSIFICATION FOR FEDERAL TAX PURPOSES Scheduled for a Public Hearing before the SUBCOMMITTEE ON SELECT REVENUE MEASURES and the SUBCOMMITTEE ON INCOME SECURITY

PRESENT LAW AND BACKGROUND RELATING TO WORKER CLASSIFICATION FOR FEDERAL TAX PURPOSES Scheduled for a Public Hearing before the SUBCOMMITTEE ON SELECT REVENUE MEASURES and the SUBCOMMITTEE ON INCOME SECURITY

THE PEO ADVANTAGE. What is a Professional Employer Organization?

What is a Professional Employer Organization? THE PEO ADVANTAGE A Professional Employer Organization (PEO) is a business also known as employee leasing or staff leasing. PEO s provide small and midsized

What is a Professional Employer Organization? THE PEO ADVANTAGE A Professional Employer Organization (PEO) is a business also known as employee leasing or staff leasing. PEO s provide small and midsized

Misclassifying Employees vs. Independent Contractors: A New World of Forgiveness By Juliet L. Fink, JD

Misclassifying Employees vs. Independent Contractors: A New World of Forgiveness By Juliet L. Fink, JD On Sept. 21, 2011, the IRS announced a new voluntary disclosure program, the Voluntary Classification

Misclassifying Employees vs. Independent Contractors: A New World of Forgiveness By Juliet L. Fink, JD On Sept. 21, 2011, the IRS announced a new voluntary disclosure program, the Voluntary Classification

Employee vs. Independent Contractor: The Importance of Proper Classification

Employee vs. Independent Contractor: The Importance of Proper Classification Dominic L. Daher, MAcc, JD, LLM in Taxation Director of Internal Audit and Tax Compliance, University of San Francisco Dawn

Employee vs. Independent Contractor: The Importance of Proper Classification Dominic L. Daher, MAcc, JD, LLM in Taxation Director of Internal Audit and Tax Compliance, University of San Francisco Dawn

ASK THE EXPERTS. Customer Service

Ask the Experts If you ve got payroll and tax filing questions, we ve got answers! Read through our list of frequently asked questions below or if you can t find what you re looking for, please send your

Ask the Experts If you ve got payroll and tax filing questions, we ve got answers! Read through our list of frequently asked questions below or if you can t find what you re looking for, please send your

Preparing for an IRS Audit

Preparing for an IRS Audit And other common agency audit requests... Disclaimer: These materials and the oral presentation accompanying them are for educational purposes only, and do not constitute accounting

Preparing for an IRS Audit And other common agency audit requests... Disclaimer: These materials and the oral presentation accompanying them are for educational purposes only, and do not constitute accounting

Employee or Independent Contractor? Avoiding Misclassification. By: Kristin N. Zielmanski

Employee or Independent Contractor? Avoiding Misclassification By: Kristin N. Zielmanski Whether an individual working for your business qualifies as an employee or an independent contractor is a question

Employee or Independent Contractor? Avoiding Misclassification By: Kristin N. Zielmanski Whether an individual working for your business qualifies as an employee or an independent contractor is a question

Independent Contractors: Utah

CHRISTINA M. JEPSON AND NICOLE G. FARRELL, PARSONS BEHLE & LATIMER, WITH PRACTICAL LAW LABOR & EMPLOYMENT A Q&A guide to state law on independent contractor status for private employers in Utah. This Q&A

CHRISTINA M. JEPSON AND NICOLE G. FARRELL, PARSONS BEHLE & LATIMER, WITH PRACTICAL LAW LABOR & EMPLOYMENT A Q&A guide to state law on independent contractor status for private employers in Utah. This Q&A

www.safemt.com The Premium Audit Process How we determine your workers compensation premiums.

www.safemt.com The Premium Audit Process How we determine your workers compensation premiums. Are You Hiring Independent Contractors? If you hire someone to do work for you who is not your employee, you

www.safemt.com The Premium Audit Process How we determine your workers compensation premiums. Are You Hiring Independent Contractors? If you hire someone to do work for you who is not your employee, you

GUIDELINES FOR DETERMINING EMPLOYEE OR INDEPENDENT CONTRACTOR RELATIONSHIPS

GUIDELINES FOR DETERMINING EMPLOYEE OR INDEPENDENT CONTRACTOR RELATIONSHIPS Under University policy, contracts will generally only be entered into with independent contractors (IC). Independent contractors

GUIDELINES FOR DETERMINING EMPLOYEE OR INDEPENDENT CONTRACTOR RELATIONSHIPS Under University policy, contracts will generally only be entered into with independent contractors (IC). Independent contractors

Advisory on the Massachusetts Independent Contractor/Misclassification Law

Advisory on the Massachusetts Independent Contractor/Misclassification Law http://www.mass.gov/?pageid=cagoterminal&l=2&l0=home&l1=workplace+rights&sid=cago&b=te... Page 1 of 1 9/15/2008 The Official Website

Advisory on the Massachusetts Independent Contractor/Misclassification Law http://www.mass.gov/?pageid=cagoterminal&l=2&l0=home&l1=workplace+rights&sid=cago&b=te... Page 1 of 1 9/15/2008 The Official Website

North Carolina Department of State Treasurer

RICHARD H. MOORE TREASURER North Carolina Department of State Treasurer State and Local Government Finance Division and the Local Government Commission T. Vance Holloman DEPUTY TREASURER Memorandum #1079

RICHARD H. MOORE TREASURER North Carolina Department of State Treasurer State and Local Government Finance Division and the Local Government Commission T. Vance Holloman DEPUTY TREASURER Memorandum #1079

INDEPENDENT CONTRACTOR vs. EMPLOYEE:

INDEPENDENT CONTRACTOR vs. EMPLOYEE: IMPROPERLY TREATING A D.C. OR LMT AS AN INDEPENDENT CONTRACTOR INSTEAD OF AN EMPLOYEE CAN LEAD TO AN IRS AUDIT, FINES, PENALTIES AND PAYMENT OF UNCOLLECTED TAXES By,

INDEPENDENT CONTRACTOR vs. EMPLOYEE: IMPROPERLY TREATING A D.C. OR LMT AS AN INDEPENDENT CONTRACTOR INSTEAD OF AN EMPLOYEE CAN LEAD TO AN IRS AUDIT, FINES, PENALTIES AND PAYMENT OF UNCOLLECTED TAXES By,

Worker Misclassification Employment and Tax Considerations for Employers in Virginia

Worker Misclassification Employment and Tax Considerations for Employers in Virginia Presented by: Elinor H. Clendenin & Amanda M. Weaver October 27, 2015 Welcome Elinor H. Clendenin Associate Employee

Worker Misclassification Employment and Tax Considerations for Employers in Virginia Presented by: Elinor H. Clendenin & Amanda M. Weaver October 27, 2015 Welcome Elinor H. Clendenin Associate Employee

IRS Looks Closely at Independent Contractors

Hospitality Review Volume 11 Issue 1 Hospitality Review Volume 11/Issue 1 Article 2 1-1-1993 IRS Looks Closely at Independent Contractors John M. Tarras Michigan State University, shbsirc@msu.edu Follow

Hospitality Review Volume 11 Issue 1 Hospitality Review Volume 11/Issue 1 Article 2 1-1-1993 IRS Looks Closely at Independent Contractors John M. Tarras Michigan State University, shbsirc@msu.edu Follow

NORTH CAROLINA STATE UNIVERSITY EMPLOYEE VS. INDEPENDENT CONTRACTOR REFERENCE GUIDE

JULY 1, 2014 NORTH CAROLINA STATE UNIVERSITY EMPLOYEE VS. INDEPENDENT CONTRACTOR REFERENCE GUIDE DWAINE COOK NC STATE UNIVERSITY Campus Box 7205 Raleigh, NC 27695 Contents EMPLOYEE VS. INDEPENDENT CONTRACTOR

JULY 1, 2014 NORTH CAROLINA STATE UNIVERSITY EMPLOYEE VS. INDEPENDENT CONTRACTOR REFERENCE GUIDE DWAINE COOK NC STATE UNIVERSITY Campus Box 7205 Raleigh, NC 27695 Contents EMPLOYEE VS. INDEPENDENT CONTRACTOR

A Survey of Federal and State Actions to Counter Misclassification Fraud

A Survey of Federal and State Actions to Counter Misclassification Fraud Presented to: Washington Joint Legislative Taskforce on the Underground Economy in the Construction Industry September 10, 2008

A Survey of Federal and State Actions to Counter Misclassification Fraud Presented to: Washington Joint Legislative Taskforce on the Underground Economy in the Construction Industry September 10, 2008

Independent Contractor vs. Employer; Identifying the correct classification

Independent Contractor vs. Employer; Identifying the correct classification Version 3A February 15, 2013 Disclaimer: This guide is solely intended to be a free advisory source. All the information contained

Independent Contractor vs. Employer; Identifying the correct classification Version 3A February 15, 2013 Disclaimer: This guide is solely intended to be a free advisory source. All the information contained

Supported Living Transportation Services

FINANCIAL MANAGEMENT SERVICE (FMS) General Description: Self-Administered Services offer an alternative to Provider Agency Services by allowing persons with intellectual disabilities and related conditions,

FINANCIAL MANAGEMENT SERVICE (FMS) General Description: Self-Administered Services offer an alternative to Provider Agency Services by allowing persons with intellectual disabilities and related conditions,

Leased Employees and Employee Classification

llllcharles C. Shulman, Esq., LLC Employee Benefits, Employment & Executive Compensation Law www.ebeclaw.com www.employeebenefitslaw.info NJ Office & Mailing Address 632 Norfolk St., Teaneck, NJ 07666

llllcharles C. Shulman, Esq., LLC Employee Benefits, Employment & Executive Compensation Law www.ebeclaw.com www.employeebenefitslaw.info NJ Office & Mailing Address 632 Norfolk St., Teaneck, NJ 07666

Independent Contractors v. Employees

Independent Contractors v. Employees A Practical Guide for Parents Who Hire Household Help Diana Maier Attorney-At-Law 1 AGENDA Why do I need to know the difference between an independent contractor and

Independent Contractors v. Employees A Practical Guide for Parents Who Hire Household Help Diana Maier Attorney-At-Law 1 AGENDA Why do I need to know the difference between an independent contractor and

Testimony Submitted by Paul Trause, Washington State Employment Security Commissioner

Testimony Submitted to the U.S. Senate Committee on Finance Preserving Integrity, Preventing Overpayments and Eliminating Fraud in the Unemployment Insurance System Testimony Submitted by Paul Trause,

Testimony Submitted to the U.S. Senate Committee on Finance Preserving Integrity, Preventing Overpayments and Eliminating Fraud in the Unemployment Insurance System Testimony Submitted by Paul Trause,

Preparing For Your Unemployment Insurance (UI) Audit

Audit") Preparing For Your Unemployment Insurance (UI) Audit This page describes the preparation, expectations, and results of an Unemployment Insurance (UI) Audit. INTRODUCTION This page addresses the most frequently

Preparing For Your Unemployment Insurance (UI) Audit This page describes the preparation, expectations, and results of an Unemployment Insurance (UI) Audit. INTRODUCTION This page addresses the most frequently

Independent Contractor or Employee? 2016 Professional Development Institute

Independent Contractor or Employee? 2016 Professional Development Institute Agenda What s the Difference? Employee Independent Contractor Before Work Begins IC Form Guidance Independent Contractor & PERA

Independent Contractor or Employee? 2016 Professional Development Institute Agenda What s the Difference? Employee Independent Contractor Before Work Begins IC Form Guidance Independent Contractor & PERA

The Questionable Employment Tax Practices Initiative Progress Report

The Questionable Employment Tax Practices Initiative Progress Report April, 2011 QETP Oversight Team Members Include: Internal Revenue Service U.S. Department of Labor National Association of State Workforce

The Questionable Employment Tax Practices Initiative Progress Report April, 2011 QETP Oversight Team Members Include: Internal Revenue Service U.S. Department of Labor National Association of State Workforce

College Operating Procedures (COP)

") College Operating Procedures (COP) Procedure Title: Student Records Procedures Procedure Number: (FERPA) 03-1701 Originating Department: Provost/Vice President Academic Affairs Specific Authority: Family

College Operating Procedures (COP) Procedure Title: Student Records Procedures Procedure Number: (FERPA) 03-1701 Originating Department: Provost/Vice President Academic Affairs Specific Authority: Family

Frequently Asked Questions Regarding Registration with the Board. February 4, 2015

1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8430 www.pcaobus.org PCAOB Release 2003-011E The Mechanics of Registration 1. How can my firm apply for registration

1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8430 www.pcaobus.org PCAOB Release 2003-011E The Mechanics of Registration 1. How can my firm apply for registration

6.5.2 Individual Consultants

6.5.2 Individual Consultants There are legal distinctions and ramifications between retaining a consultant and hiring an employee. For example, the State incurs liabilities for withholding and/or the payment

6.5.2 Individual Consultants There are legal distinctions and ramifications between retaining a consultant and hiring an employee. For example, the State incurs liabilities for withholding and/or the payment

Independent Contractor? or employee?

Independent Contractor? or employee? W H AT Y O U N E E D T O K N O W ABOUT HIRING INDEPENDENT CONTRACTORS What is Worker Misclassification? At first glance, it might be hard they to tell the difference

Independent Contractor? or employee? W H AT Y O U N E E D T O K N O W ABOUT HIRING INDEPENDENT CONTRACTORS What is Worker Misclassification? At first glance, it might be hard they to tell the difference

Insurance Audit Form HELP

Top of the form has important information so we know who the insurance company is and exactly what policy year is being audited. If you save the form you will only need to do this once for every insurance

Top of the form has important information so we know who the insurance company is and exactly what policy year is being audited. If you save the form you will only need to do this once for every insurance

Tax Information for Small Businesses

Tax Information for Small Businesses Evelyn Williamson August 15, 2015 Eight Tips for Business Owners 1. Classify workers properly 2. Deposit trust fund employment taxes 3. Pay estimated tax payments 4.

Tax Information for Small Businesses Evelyn Williamson August 15, 2015 Eight Tips for Business Owners 1. Classify workers properly 2. Deposit trust fund employment taxes 3. Pay estimated tax payments 4.

Independent Contractor Misclassification A Problem for Uber or a Problem for You-ber?

Independent Contractor Misclassification A Problem for Uber or a Problem for You-ber? Ken Weber Baker, Donelson, Bearman, Caldwell & Berkowitz, P.C. 211 Commerce Street, Suite 800 Nashville, Tennessee

Independent Contractor Misclassification A Problem for Uber or a Problem for You-ber? Ken Weber Baker, Donelson, Bearman, Caldwell & Berkowitz, P.C. 211 Commerce Street, Suite 800 Nashville, Tennessee

WORKING DRAFT. Proposed Employee Misclassification Workers Compensation Coverage Model Act

WORKING DRAFT Proposed Employee Misclassification Workers Compensation Coverage Model Act To be considered by the NCOIL Workers Compensation Insurance Committee on July 10, 2009. Sponsored for discussion

WORKING DRAFT Proposed Employee Misclassification Workers Compensation Coverage Model Act To be considered by the NCOIL Workers Compensation Insurance Committee on July 10, 2009. Sponsored for discussion

A Taxing Question: Are CFI's employees or independent contractors?

A Taxing Question: Are CFI's employees or independent contractors? The question of proper classification of workers as either employees or independent contractors is a continuing source of controversy

A Taxing Question: Are CFI's employees or independent contractors? The question of proper classification of workers as either employees or independent contractors is a continuing source of controversy

Mastering Payroll Compliance THE TOP 10 MISTAKES THAT COST EMPLOYERS MONEY

Mastering Payroll Compliance THE TOP 10 MISTAKES THAT COST EMPLOYERS MONEY EXECUTIVE SUMMARY Businesses pay government agencies millions of dollars each year in compliance penalties. And in this economy,

Mastering Payroll Compliance THE TOP 10 MISTAKES THAT COST EMPLOYERS MONEY EXECUTIVE SUMMARY Businesses pay government agencies millions of dollars each year in compliance penalties. And in this economy,

WORKER CLASSIFICATION

100 Arbor Drive, Suite 108 Christiansburg, VA 24073 Voice: 540-381-9333 FAX: 540-381-8319 www.becpas.com Providing Professional Business Advisory & Consulting Services Douglas L. Johnston, II djohnston@becpas.com

100 Arbor Drive, Suite 108 Christiansburg, VA 24073 Voice: 540-381-9333 FAX: 540-381-8319 www.becpas.com Providing Professional Business Advisory & Consulting Services Douglas L. Johnston, II djohnston@becpas.com

Identifying Your Company s Employees: Its Tougher Than You Think!

Identifying Your Company s Employees: Its Tougher Than You Think! Independent Contractors Joint Employers 1 2011 Seyfarth Shaw LLP Independent Contractors Massachusetts Three-Prong Test: Freedom from control

Identifying Your Company s Employees: Its Tougher Than You Think! Independent Contractors Joint Employers 1 2011 Seyfarth Shaw LLP Independent Contractors Massachusetts Three-Prong Test: Freedom from control

Agenda. IRS Payroll Tax Audit Initiatives. Auditor of State David Yost 2011 Local Government Official s Conference Employment Tax Update

Auditor of State David Yost 2011 Local Government Official s Conference Employment Tax Update April 7, 2011 Janice M. Zajac, CPA, MBA, MB Agenda IRS Payroll Tax Audit Initiatives Independent Contractors

Auditor of State David Yost 2011 Local Government Official s Conference Employment Tax Update April 7, 2011 Janice M. Zajac, CPA, MBA, MB Agenda IRS Payroll Tax Audit Initiatives Independent Contractors

A recent Treasury Inspector General for Tax Administration

Daily Tax Report Reproduced with permission from Daily Tax Report, 192 DTR J-1, 10/3/14. Copyright 2014 by The Bureau of National Affairs, Inc. (800-372-1033) http://www.bna.com Tax Audits As the Internal

Daily Tax Report Reproduced with permission from Daily Tax Report, 192 DTR J-1, 10/3/14. Copyright 2014 by The Bureau of National Affairs, Inc. (800-372-1033) http://www.bna.com Tax Audits As the Internal

Independent Contracting

Independent Contracting USED BY PERMISSION From AAPA: 950 North Washington Street, Alexandria, VA 22314 www.aapa.org Deciding to practice as an independent contractor requires consideration of many factors.

Independent Contracting USED BY PERMISSION From AAPA: 950 North Washington Street, Alexandria, VA 22314 www.aapa.org Deciding to practice as an independent contractor requires consideration of many factors.

2014 Business Tax Organizer. Limited Liability Companies, S Corporations, C Corporations & Sole Proprietors

2014 Business Tax Organizer Limited Liability Companies, S Corporations, C Corporations & Sole Proprietors 1553 W. Todd Dr., Suite 112 Tempe, AZ 85283 (480) 517-0988 January 2015 Good Afternoon! We have

2014 Business Tax Organizer Limited Liability Companies, S Corporations, C Corporations & Sole Proprietors 1553 W. Todd Dr., Suite 112 Tempe, AZ 85283 (480) 517-0988 January 2015 Good Afternoon! We have

The Massachusetts Independent Contractor Law: Serious Problems and Difficult Choices for Businesses in Massachusetts

The Massachusetts Independent Contractor Law: Serious Problems and Difficult Choices for Businesses in Massachusetts By Robert M. Shea MORSE BARNES -BROWN PENDLETON PC The law firm built for business.

The Massachusetts Independent Contractor Law: Serious Problems and Difficult Choices for Businesses in Massachusetts By Robert M. Shea MORSE BARNES -BROWN PENDLETON PC The law firm built for business.

By: Alan H. Morgan, CPL amorgan1@flash.net (713) 805 6851

805 6851") By: Alan H. Morgan, CPL amorgan1@flash.net (713) 805 6851 The independent contractor status of land professionals has been challenged by the Internal Revenue Service and state employment agencies for many

By: Alan H. Morgan, CPL amorgan1@flash.net (713) 805 6851 The independent contractor status of land professionals has been challenged by the Internal Revenue Service and state employment agencies for many

Washington s Underground Economy Task force

Washington s Underground Economy Task force SEN. JEANNE KOHL- WELLES WASHINGTON DECEMBER 2010 NATIONAL CONFERENCE OF STATE LEGISLATURES Employee misclassification Most commonly, employee misclassification

Washington s Underground Economy Task force SEN. JEANNE KOHL- WELLES WASHINGTON DECEMBER 2010 NATIONAL CONFERENCE OF STATE LEGISLATURES Employee misclassification Most commonly, employee misclassification

Employee or Independent Contractor?

Employee or Independent Contractor? Introduction An important question arises when a church hires, retains or selects a new person to perform a particular job for the church - is the person an employee

Employee or Independent Contractor? Introduction An important question arises when a church hires, retains or selects a new person to perform a particular job for the church - is the person an employee

An independent licensee of the Blue Cross and Blue Shield Association GROUP CONTRACT APPLICATION GENERAL INFORMATION.

Group Hospitalization and Medical Services, Inc. doing business as CareFirst BlueCross BlueShield (CareFirst) 840 First Street, NE Washington, D.C. 20065 202-479-8000 An independent licensee of the Blue

Group Hospitalization and Medical Services, Inc. doing business as CareFirst BlueCross BlueShield (CareFirst) 840 First Street, NE Washington, D.C. 20065 202-479-8000 An independent licensee of the Blue

2012 Year End Accountant Guide

2012 Year End Accountant Guide For your clients using RUN Powered by ADP This guide contains information and critical dates to assist you with year end payroll and tax filing tasks. HR. Payroll. Benefits.

2012 Year End Accountant Guide For your clients using RUN Powered by ADP This guide contains information and critical dates to assist you with year end payroll and tax filing tasks. HR. Payroll. Benefits.

Preventing and Managing Independent Contractor Risks

Preventing and Managing Independent Contractor Risks Innovative Tax and Employment Law Strategies to Address Increasing Government and Private Enforcement Threats Charles Hurley (202) 263 3260 Andrew Rosenman

Preventing and Managing Independent Contractor Risks Innovative Tax and Employment Law Strategies to Address Increasing Government and Private Enforcement Threats Charles Hurley (202) 263 3260 Andrew Rosenman

When the IRS and DOL come knocking... (You can t pretend you re not home.)

") When the IRS and DOL come knocking... (You can t pretend you re not home.) What to Expect and How We Can Help Lisa Jones, Esq., CPC, QPA W hat We Will C over Why you? Overview of DOL/EBSA Initiatives A

When the IRS and DOL come knocking... (You can t pretend you re not home.) What to Expect and How We Can Help Lisa Jones, Esq., CPC, QPA W hat We Will C over Why you? Overview of DOL/EBSA Initiatives A

FICA WITHHOLDING & TAXATION OF DISABILITY BENEFITS. Information for Policyholders

FICA WITHHOLDING & TAXATION OF DISABILITY BENEFITS Information for Policyholders Step One As claim payments are made: Calculates and withholds the EMPLOYEE S portion of FICA liability based on information

FICA WITHHOLDING & TAXATION OF DISABILITY BENEFITS Information for Policyholders Step One As claim payments are made: Calculates and withholds the EMPLOYEE S portion of FICA liability based on information

Franchisee as Employee? An Analysis under Maryland and U.S. law

Franchisee as Employee? An Analysis under Maryland and U.S. law Presented by David L. Cahn, Esq. and Steven Bers, Esq. dcahn@wtplaw.com and sbers@wtplaw.com Coverall Commercial Cleaning cases a primer

Franchisee as Employee? An Analysis under Maryland and U.S. law Presented by David L. Cahn, Esq. and Steven Bers, Esq. dcahn@wtplaw.com and sbers@wtplaw.com Coverall Commercial Cleaning cases a primer

Rationale, Process and Procedures

Independent Contractors (IC) @ Kent State University Rationale, Process and Procedures Presented by: The Division of Business and Finance The Office of General Counsel The Division of Human Resources 1

Independent Contractors (IC) @ Kent State University Rationale, Process and Procedures Presented by: The Division of Business and Finance The Office of General Counsel The Division of Human Resources 1

THEME: INDEPENDENT CONTRACTOR vs. EMPLOYEE. By John W. Day, MBA

THEME: INDEPENDENT CONTRACTOR vs. EMPLOYEE By John W. Day, MBA ACCOUNTING TERM: Independent Contractor An individual who contracts with an entity to perform a service independent of the entity s management

THEME: INDEPENDENT CONTRACTOR vs. EMPLOYEE By John W. Day, MBA ACCOUNTING TERM: Independent Contractor An individual who contracts with an entity to perform a service independent of the entity s management

JAN 2 2 2016. changing and increasing numbers of individuals are facing. decisions on whether to choose to become entrepreneurs and go

THE SENATE TWENTY-EIGHTH LEGISLATURE, 0 STATE OF HAWAII JAN 0 A BILL FOR AN ACT S.B. NO.Mf RELATING TO EMPLOYMENT SECURITY. BE IT ENACTED BY THE LEGISLATURE OF THE STATE OF HAWAII: 0 SECTION. The legislature

THE SENATE TWENTY-EIGHTH LEGISLATURE, 0 STATE OF HAWAII JAN 0 A BILL FOR AN ACT S.B. NO.Mf RELATING TO EMPLOYMENT SECURITY. BE IT ENACTED BY THE LEGISLATURE OF THE STATE OF HAWAII: 0 SECTION. The legislature

Independent Contractor or Employee? How you should be classified

Independent Contractor or Employee? How you should be classified YOUR LEGAL RIGHTS Not all people who perform work for a company are employees. Instead, they may be independent contractors. Whether a person

Independent Contractor or Employee? How you should be classified YOUR LEGAL RIGHTS Not all people who perform work for a company are employees. Instead, they may be independent contractors. Whether a person

Payroll NATIONAL CROSS-REFERENCE

NATIONAL Payroll SUMMARY Federal and state wage and hour laws regulate the method of payment of wages, the payment of wages upon termination of employment, allowable deductions from employee paychecks,

NATIONAL Payroll SUMMARY Federal and state wage and hour laws regulate the method of payment of wages, the payment of wages upon termination of employment, allowable deductions from employee paychecks,

When is an individual an employee? A Solution for the Payroll Headache: Employee vs. Independent Contractor? Agenda

A Solution for the Payroll Headache: Employee vs. Independent Contractor? Presented by: Melanie Olson Consultant, HR to Go HR to Go 1730 I Street, Ste 240 Sacramento, Ca 95811 Phone: 916.444.6200 www.hrtogo.com

A Solution for the Payroll Headache: Employee vs. Independent Contractor? Presented by: Melanie Olson Consultant, HR to Go HR to Go 1730 I Street, Ste 240 Sacramento, Ca 95811 Phone: 916.444.6200 www.hrtogo.com

PAYCHEX. Mastering Payroll Compliance. 10 Missteps to Avoid

PAYCHEX Mastering Payroll Compliance 10 Missteps to Avoid Executive Summary. Businesses pay government agencies millions of dollars each year in labor and tax compliance penalties. And, in this economy

PAYCHEX Mastering Payroll Compliance 10 Missteps to Avoid Executive Summary. Businesses pay government agencies millions of dollars each year in labor and tax compliance penalties. And, in this economy

Independent Contractor or Employee? Avoiding Worker Misclassification Confusion

Independent Contractor or Employee? Avoiding Worker Misclassification Confusion Wednesday, October 7, 2015 11:30 a.m. 12:15 p.m. CDT Bruce Ely, John Hargrove, Summer Austin Davis babc.com ALABAMA I DISTRICT

Independent Contractor or Employee? Avoiding Worker Misclassification Confusion Wednesday, October 7, 2015 11:30 a.m. 12:15 p.m. CDT Bruce Ely, John Hargrove, Summer Austin Davis babc.com ALABAMA I DISTRICT

10 Facts About the Affordable Care Act and Worker Classification

Latham & Watkins Tax Controversy Practice Number 1611 November 18, 2013 10 Facts About the Affordable Care Act and Worker Classification Businesses subject to the Affordable Care Act s shared responsibility

Latham & Watkins Tax Controversy Practice Number 1611 November 18, 2013 10 Facts About the Affordable Care Act and Worker Classification Businesses subject to the Affordable Care Act s shared responsibility

G.S. 143B-426.38A Page 1

143B-426.38A. Government Data Analytics Center; State data-sharing requirements. (a) State Government Data Analytics. The State shall initiate across State agencies, departments, and institutions a data

143B-426.38A. Government Data Analytics Center; State data-sharing requirements. (a) State Government Data Analytics. The State shall initiate across State agencies, departments, and institutions a data

Independent Contractors and Unemployment Tax Issues

Independent Contractors and Unemployment Tax Issues William T. (Tommy) Simmons Legal Counsel to Commissioner Hope Andrade Commissioner Representing Employers Texas Workforce Commission tommy.simmons@twc.state.tx.us

Independent Contractors and Unemployment Tax Issues William T. (Tommy) Simmons Legal Counsel to Commissioner Hope Andrade Commissioner Representing Employers Texas Workforce Commission tommy.simmons@twc.state.tx.us

Terminating Unemployment Insurance Liability. Obligations as an Employer. Page 2 of 6

New York State Department of Labor Unemployment Insurance Division Harriman State Office Campus Albany, NY 12240-0322 www.labor.ny.gov 888-899-8810 Household Employers Guide for Unemployment Insurance

New York State Department of Labor Unemployment Insurance Division Harriman State Office Campus Albany, NY 12240-0322 www.labor.ny.gov 888-899-8810 Household Employers Guide for Unemployment Insurance

The legal ramifications of classifying employment: Employee v. independent contractor

The legal ramifications of classifying employment: Employee v. independent contractor ABSTRACT Ronald R. Rubenfield Robert Morris University In an attempt to properly assess taxes and collect penalties

The legal ramifications of classifying employment: Employee v. independent contractor ABSTRACT Ronald R. Rubenfield Robert Morris University In an attempt to properly assess taxes and collect penalties

How to Create a Payroll Procedures Manual! Presented by Max Muller!

How to Create a Payroll Procedures Manual! Presented by Max Muller! Overview! How to put it all together! Using the terminology! Employee distinction! How to eliminate improper actions! When to make an

How to Create a Payroll Procedures Manual! Presented by Max Muller! Overview! How to put it all together! Using the terminology! Employee distinction! How to eliminate improper actions! When to make an

Health savings accounts (HSAs) are individual accounts. HSA Programs for Groups: Employer Versus Employee Responsibilities.

are individual accounts. HSA Programs for Groups: Employer Versus Employee Responsibilities.") Health Care HSA Programs for Groups: Employer Versus Employee Responsibilities Employers implementing a health savings account (HSA) program face a shared compliance burden with their employees. The law

Health Care HSA Programs for Groups: Employer Versus Employee Responsibilities Employers implementing a health savings account (HSA) program face a shared compliance burden with their employees. The law

Independent Contractors RF Policies and Procedures

Office of Grants Management ARE YOU INDEPENDENT? Independent Contractors RF Policies and Procedures February 24, 2009 1 What Are Our Goals? Defining Independent Contractors (IC) Identifying and completing

Office of Grants Management ARE YOU INDEPENDENT? Independent Contractors RF Policies and Procedures February 24, 2009 1 What Are Our Goals? Defining Independent Contractors (IC) Identifying and completing

Clergy and Non Clergy Compensation

Clergy and Non Clergy Compensation Parish treasurers are responsible for monitoring the salary and housing compensation for clergy. They need to keep abreast of the median family income for their area.

Clergy and Non Clergy Compensation Parish treasurers are responsible for monitoring the salary and housing compensation for clergy. They need to keep abreast of the median family income for their area.

United States Trustee Program

United States Trustee Program Privacy Impact Assessment for the Credit Counseling/Debtor Education System (CC/DE System) Issued by: Larry Wahlquist, Privacy Point of Contact Reviewed by: Approved by: Vance

United States Trustee Program Privacy Impact Assessment for the Credit Counseling/Debtor Education System (CC/DE System) Issued by: Larry Wahlquist, Privacy Point of Contact Reviewed by: Approved by: Vance

INDUSTRIAL COMMISSION OF ARIZONA

INDUSTRIAL COMMISSION OF ARIZONA WORKERS COMPENSATION INFORMATION FOR THE INJURED WORKER Phoenix Office: Industrial Commission of Arizona 800 W. Washington Street Phoenix, Arizona 85007-2922 Claims Phone:

INDUSTRIAL COMMISSION OF ARIZONA WORKERS COMPENSATION INFORMATION FOR THE INJURED WORKER Phoenix Office: Industrial Commission of Arizona 800 W. Washington Street Phoenix, Arizona 85007-2922 Claims Phone:

January 19, 2007. Comptrollers Office. Independent Contractor vs. Employee Discussion EXCERPTS FROM IRS. Rev. Rul. 87-41 1987-1 C.B.

January 19, 2007 Comptrollers Office Independent Contractor vs. Employee Discussion EXCERPTS FROM IRS Rev. Rul. 87-41 1987-1 C.B. 296 Section 3111 -- Social Security Tax Liability Summary THE INTERNAL

January 19, 2007 Comptrollers Office Independent Contractor vs. Employee Discussion EXCERPTS FROM IRS Rev. Rul. 87-41 1987-1 C.B. 296 Section 3111 -- Social Security Tax Liability Summary THE INTERNAL

INITIAL REQUIRED NOTICES FOR BANKRUPTCY CLIENTS

INITIAL REQUIRED NOTICES FOR BANKRUPTCY CLIENTS You are hereby requesting the opportunity to consult with and obtain information and advice from Michael Jones and the Law Office of James P. Cronn ( Law

INITIAL REQUIRED NOTICES FOR BANKRUPTCY CLIENTS You are hereby requesting the opportunity to consult with and obtain information and advice from Michael Jones and the Law Office of James P. Cronn ( Law

CONTINGENT WORKERS: LEGAL ISSUES INVOLVING INDEPENDENT CONTRACTORS, TEMPORARY AND LEASED EMPLOYEES (WASHINGTON)

") CONTINGENT WORKERS: LEGAL ISSUES INVOLVING INDEPENDENT CONTRACTORS, TEMPORARY AND LEASED EMPLOYEES (WASHINGTON) This keynote outlines the risks and benefits of utilizing independent contractors, temporary

CONTINGENT WORKERS: LEGAL ISSUES INVOLVING INDEPENDENT CONTRACTORS, TEMPORARY AND LEASED EMPLOYEES (WASHINGTON) This keynote outlines the risks and benefits of utilizing independent contractors, temporary

GUIDANCE ON 90-DAY WAITING PERIOD LIMITATION UNDER PUBLIC HEALTH SERVICE ACT 2708 NOTICE 2012-59 I. INTRODUCTION

GUIDANCE ON 90-DAY WAITING PERIOD LIMITATION UNDER PUBLIC HEALTH SERVICE ACT 2708 NOTICE 2012-59 I. INTRODUCTION The Departments of Labor, Health and Human Services (HHS), and the Treasury (the Departments)

GUIDANCE ON 90-DAY WAITING PERIOD LIMITATION UNDER PUBLIC HEALTH SERVICE ACT 2708 NOTICE 2012-59 I. INTRODUCTION The Departments of Labor, Health and Human Services (HHS), and the Treasury (the Departments)

James R. Favor & Company

Sigma Alpha Epsilon Fraternity Independent Contractors A Review of Exposures & Risk Management Recommendations Since 1979 James R. Favor & Company has been developing and providing effective risk management

Sigma Alpha Epsilon Fraternity Independent Contractors A Review of Exposures & Risk Management Recommendations Since 1979 James R. Favor & Company has been developing and providing effective risk management

Construction Industry Workers Compensation Coverage Act. Approved by the NCOIL Executive Committee on November 22, 2009.

Construction Industry Workers Compensation Coverage Act Approved by the NCOIL Executive Committee on November 22, 2009. Table of Contents Page Numbers Section 1. Summary (1) Section 2. Definitions (1)

Construction Industry Workers Compensation Coverage Act Approved by the NCOIL Executive Committee on November 22, 2009. Table of Contents Page Numbers Section 1. Summary (1) Section 2. Definitions (1)

SNURE LAW OFFICE, PSC

SNURE LAW OFFICE, PSC A Professional Services Corporation Clark B. Snure Retired Of counsel Thomas G. Burke Joseph F. Quinn Brian K. Snure brian@snurelaw.com MEMORANDUM To: Washington Fire Protection Districts

SNURE LAW OFFICE, PSC A Professional Services Corporation Clark B. Snure Retired Of counsel Thomas G. Burke Joseph F. Quinn Brian K. Snure brian@snurelaw.com MEMORANDUM To: Washington Fire Protection Districts

News Release Date: 3/20/13

News Release Date: 3/20/13 Voluntary Worker Classification Settlement Program Expanded Cross References IR-2013-23, February 27, 2013 Announcement 2012-45 Announcement 2012-46 The Internal Revenue Service

News Release Date: 3/20/13 Voluntary Worker Classification Settlement Program Expanded Cross References IR-2013-23, February 27, 2013 Announcement 2012-45 Announcement 2012-46 The Internal Revenue Service

Statement of Colleen M. Kelley National President National Treasury Employees Union H.R. 4735

Statement of Colleen M. Kelley National President National Treasury Employees Union On H.R. 4735 Presented to House Committee on Oversight and Government Reform Subcommittee on Federal Workforce, Postal

Statement of Colleen M. Kelley National President National Treasury Employees Union On H.R. 4735 Presented to House Committee on Oversight and Government Reform Subcommittee on Federal Workforce, Postal

James R. Favor & Company

James R. Favor & Company Phi Delta Theta Fraternity Minimum Insurance Requirements for Independent Contractors Before Independent Contractor agreements are finalized and any work is performed, Written

James R. Favor & Company Phi Delta Theta Fraternity Minimum Insurance Requirements for Independent Contractors Before Independent Contractor agreements are finalized and any work is performed, Written

956 CMR: COMMONWEALTH HEALTH INSURANCE CONNECTOR AUTHORITY

10.01: General Provisions 10.02: Definitions 10.03: Employer HIRD Form 10.04: Employee HIRD Form 10.05: Other Provisions 10.01: General Provisions Scope and Purpose. 956 CMR 10.00 governs the filing requirements

10.01: General Provisions 10.02: Definitions 10.03: Employer HIRD Form 10.04: Employee HIRD Form 10.05: Other Provisions 10.01: General Provisions Scope and Purpose. 956 CMR 10.00 governs the filing requirements

FEDERAL CONTRACTOR VETERANS EMPLOYMENT REPORT VETS-4212

FEDERAL CONTRACTOR VETERANS EMPLOYMENT REPORT VETS-4212 OMB NO: 1293-0005 Expires: 11/30/2017 Persons are not required to respond to this collection of information unless it displays a valid OMB number.

FEDERAL CONTRACTOR VETERANS EMPLOYMENT REPORT VETS-4212 OMB NO: 1293-0005 Expires: 11/30/2017 Persons are not required to respond to this collection of information unless it displays a valid OMB number.

Federal Agencies Delay Nondiscrimination Requirements for Insured Group Health Plans under the Affordable Care Act

This email contains graphics - please enable images in your email client to display completely. January / February 2011 Newsletter In this Issue Nondiscrimination Requirements Delayed State Minimum Wage

This email contains graphics - please enable images in your email client to display completely. January / February 2011 Newsletter In this Issue Nondiscrimination Requirements Delayed State Minimum Wage

NPSA GENERAL PROVISIONS

NPSA GENERAL PROVISIONS 1. Independent Contractor. A. It is understood and agreed that CONTRACTOR (including CONTRACTOR s employees) is an independent contractor and that no relationship of employer-employee

NPSA GENERAL PROVISIONS 1. Independent Contractor. A. It is understood and agreed that CONTRACTOR (including CONTRACTOR s employees) is an independent contractor and that no relationship of employer-employee

The Small Business Guide To Employment Taxes

The Small Business Guide To Employment Taxes Roanoke Regional Small Business Development Center 210 S. Jefferson Street Roanoke, VA 24011 www.roanokesmallbusiness.org Roanoke Small Business Development

The Small Business Guide To Employment Taxes Roanoke Regional Small Business Development Center 210 S. Jefferson Street Roanoke, VA 24011 www.roanokesmallbusiness.org Roanoke Small Business Development

P.O.P. Premium Only Plan

P.O.P. Premium Only Plan The Premium Only Plan (P.O.P.) helps you and your employees save money with pre-tax premiums. Save money with P.O.P. The Premium Only Plan (P.O.P.) is an employee benefit program

P.O.P. Premium Only Plan The Premium Only Plan (P.O.P.) helps you and your employees save money with pre-tax premiums. Save money with P.O.P. The Premium Only Plan (P.O.P.) is an employee benefit program

How to Avoid Emerging Wage & Hour Risks: Exempt or Non- Exempt, Contractor Liability & Minimum Wage Hikes

How to Avoid Emerging Wage & Hour Risks: Exempt or Non- Exempt, Contractor Liability & Minimum Wage Hikes Jonathan C. Sterling, Shareholder, Carlton Fields Jorden Burt, P.A. The Onslaught Continues Wage

How to Avoid Emerging Wage & Hour Risks: Exempt or Non- Exempt, Contractor Liability & Minimum Wage Hikes Jonathan C. Sterling, Shareholder, Carlton Fields Jorden Burt, P.A. The Onslaught Continues Wage

Misclassification of Employees as Independent Contractors

O L A OFFICE OF THE LEGISLATIVE AUDITOR STATE OF MINNESOTA EVALUATION REPORT Misclassification of Employees as Independent Contractors NOVEMBER 2007 PROGRAM EVALUATION DIVISION Centennial Building Suite

O L A OFFICE OF THE LEGISLATIVE AUDITOR STATE OF MINNESOTA EVALUATION REPORT Misclassification of Employees as Independent Contractors NOVEMBER 2007 PROGRAM EVALUATION DIVISION Centennial Building Suite

Contingent Workers & Independent Contractors: Avoiding Misclassification Pitfalls. Presented by David Long-Daniels Greenberg Traurig, LLP

Contingent Workers & Independent Contractors: Avoiding Misclassification Pitfalls Presented by David Long-Daniels Greenberg Traurig, LLP Why are we here? Guidelines for making a determination as to whether

Contingent Workers & Independent Contractors: Avoiding Misclassification Pitfalls Presented by David Long-Daniels Greenberg Traurig, LLP Why are we here? Guidelines for making a determination as to whether

Coverage Questions for Subcontractors, General Contractors, and Independent Contractors

Coverage Questions for Subcontractors, General Contractors, and Independent Contractors 1. Which employers must carry workers' compensation coverage? 418.115 (a) (b) (c) (d) (e) All private employers regularly

Coverage Questions for Subcontractors, General Contractors, and Independent Contractors 1. Which employers must carry workers' compensation coverage? 418.115 (a) (b) (c) (d) (e) All private employers regularly

INFORMATION FOR ASBESTOS HANDLING LICENSE APPLICANTS

STATE OF NEW YORK > DEPARTMENT OF LABOR DIVISION OF SAFETY AND HEALTH LICENSE AND CERTIFICATE UNIT BUILDING 12, ROOM 161 STATE CAMPUS ALBANY, NY 12240 (518) 457>2735 GENERAL INFORMATION INFORMATION FOR

STATE OF NEW YORK > DEPARTMENT OF LABOR DIVISION OF SAFETY AND HEALTH LICENSE AND CERTIFICATE UNIT BUILDING 12, ROOM 161 STATE CAMPUS ALBANY, NY 12240 (518) 457>2735 GENERAL INFORMATION INFORMATION FOR

SECURING AND PAYING FOR CONSULTANTS AND INDEPENDENT CONTRACTORS

SECURING AND PAYING FOR CONSULTANTS AND INDEPENDENT CONTRACTORS PURPOSE The primary purpose of this policy and procedure statement is to guide the Seminary in three areas: (1) To properly classify employees,

SECURING AND PAYING FOR CONSULTANTS AND INDEPENDENT CONTRACTORS PURPOSE The primary purpose of this policy and procedure statement is to guide the Seminary in three areas: (1) To properly classify employees,