Capstone Solar Professionals

|

|

|

- Trevor Bruce

- 7 years ago

- Views:

Transcription

1 Capstone Solar Professionals DOO Solar Webinars for Developers, Owners, and Operators: How to Value Solar Energy Assets Ken Kramer Managing Director and co-founder, Rushton Atlantic, LLC Ken Kramer has more than 30 years experience building businesses and consulting on valuation and banking for clients on techniques that support finance, investment, insurance, taxation and financial reporting requirements. Kramer has served in industries that include manufacturing, transportation, telecommunications, power & energy, and infrastructure.

2 Why do you need to know? If you are building a solar PV system, you don t need an appraisal to determine costs, but For financing, you must document asset value (and debt service coverage) for: Sec cash grants Bank & bond debt Sale/leaseback financing Tax equity If acquiring an existing facility, you are primarily concerned with its earning power. Also What could possibly go wrong?

3 What is Value? Types of Value Scrap Value Auction Value Orderly Liquidation Value Fair Market Value in Exchange Fair Market Value in Place Fair Market Value in Continued Use

4 What is Value? Fair Market Value Fair Market Value is the estimated amount at which the appraised property might be expected to exchange between a willing buyer and a willing seller, neither being under compulsion, each having reasonable knowledge of all relevant facts.

5 What is Value? Fair Market Value When fair market value is established on the premise of continued use, it is assumed the buyer and the seller would be contemplating retention of the property at its present location for continuation as part of the current operations. An estimate of Fair Market Value arrived at on the premise of continued use does not represent the amount that might be realized from piecemeal disposition in the open market or from an alternative use of the property.

6 Approaches to Value Cost Approach Depreciated Replacement Cost New (RCN) Income Approach Net present value of projected after-tax cash flows Market Approach Based on comparable market transactions, if available

7 Approaches to Value Reconciliation Must consider all approaches to value Must consider all facts and circumstances surrounding each asset: Age Operating history Contracts Reason for weighting must be substantiated The market drives value more than any other approach to value.

8 Residual Value Net present value, as of residual date, of subsequent after-tax cash flows Deinstallation, transport and reinstallation of equipment Extension of PPA at existing location

9 Cash Flow Model Inputs Capacity 1,250 KW Capital cost $6,400,000 Solar power production 1,482,000 KWH Degradation 0.5% p.a. PPA Pricing $0.12/KWH SREC pricing $0.475/KWH Operating Expenses $52,649 (O&M, Insurance, Monitoring) Inflation 3% p.a Cash Grant 30% Depreciation 5-years MACRS w/ 15% basis reduction Tax Rate 40% Residual year 20 (inflated) $1,292,800 Discount Rate (After tax) 5.75%

10 Discount Rate - Weighted Average Cost of Capital WACC = [Kd x %D x (1-T)] + [Ke x %E] Kd = cost of debt capital 5.5% %D = proportion of debt to total capital 52% T = marginal tax rate 40% Ke = cost of equity capital 8.3% %E = proportion of equity to total capital 48% Ke = Rf + (ß x Rp) + Ru Rf = risk-free rate of return 3.8% ß = beta 0.9 Rp = common stock risk premium 5% Ru = unsystematic or additional risk premium 0

+ Ru Rf = risk-free rate of return")

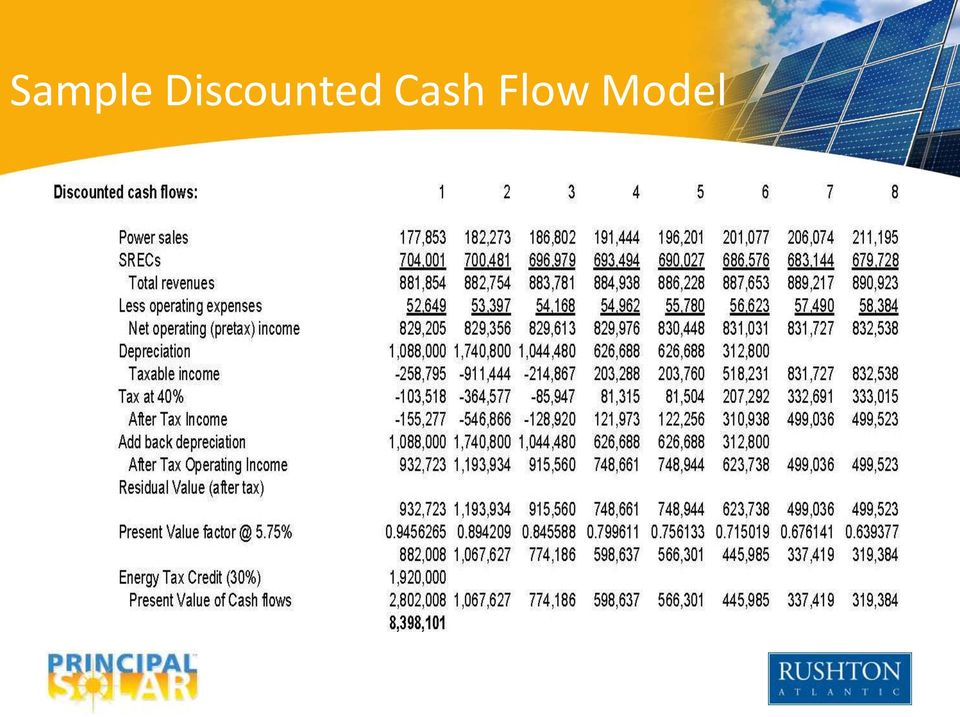

11 Sample Discounted Cash Flow Model

12 Sample Discounted Cash Flow Model (cont d.)

13 Sample Discounted Cash Flow Model (cont d.)

14 Sensitivities - what if?... Loss of residual Change in PPA rate Change in SREC revenue Less creditworthy offtaker higher discount rate Bonus vs. standard MACRS depreciation NOL carryforward Maintenance / Reserve / Insurance

15 NPV Impact of Pricing Changes Base Case Without residual Reduced PPA Rate Reduced SREC Revenue Higher Discount Rate Bonus Depreciation Tax Loss Carryforward Cost to move is not economic PPA reduction from $0.12 to $0.11/kwh Years 6-10 reduced by 50% Weaker off-taker WACC =10% All depreciation claimed in first year Project must absorb its own tax losses $8.398 $7.975 $8.271 $7.744 $7.120 $8.555 $8.301 (5%) (2%) (8%) (15%) 2% (1%)

16 Questions and Discussion Please enter your questions into the Chat window Ken Kramer Managing Director and co-founder Rushton Atlantic, LLC (646)

290-5069 ken.")

17 Questions John: Discuss valuations for 3 types of solar players 1. Equipment manufacturers like GT Solar 2. Panel manufacturers 3. Installers like principal solar Ken Kramer: I would not analogize a big public company to a solar PV installation, but a factory making panels or inverters would be analyzed similarly to what was done here. A solar system is an electron factory, with capital costs, operating costs, and revenue streams no different conceptually from a widget factory in terms of setting up a cash flow model.

18 Questions Scott: Renewable vs. Renewable, I read this morning about the Bonneville Power Authority in Washington state issued a new set of rules governing when they would buy hydropower preferentially over wind thus re-writing the contracts and revenue estimations that many wind generators were relying on. How can you account for something of this nature when valuing an asset with a 2-decade + life span? KK: The Bonneville situation shows that "stuff happens," and there may be greater (and less predictable) risks in selling power under a "binding" PPA than market participants currently realize. Not having seen this PPA, I would expect legal challenges due to what appear to be unilateral contract changes by Bonneville, but in general you need a cushion to handle the unknown, and there is apparently more unknown out there than we thought. If the world is a more complicated place, the discount rates used to analyze these transactions should be higher to reflect a higher levels of risk.

risks in selling power under a \"binding\" PPA than market participants currently realize.")

19 Questions Michael: How expensive is an official appraisal like you discuss here, who is typically paying that fee in the PV solar industry, and how often do you need a new appraisal? KK: Appraisals are typically done to support financings and acquisitions, generally upfront, but in some cases for periodic portfolio reviews as well. Price is typically a flat fee based on scope of work, calculated from man-hour estimates. The American Society of Appraisers does not allow fees as a percentage of appraised value, because of the obvious potential conflict of interest.

20 Questions Ken: Typically, what size of systems need appraisals? In kw or $ KK: We are not involved in the residential market, more in inside-the-fence commercial/industrial installations, starting in the hundreds of KW, up to utility-scale plants. Really depends on who is paying for the appraisal and what kind of financing is being used.

21 Questions Ken: What impact on valuation does the risk of losing the SREC income carry. This market is unstable and relies on local politics? KK: The finance world prefers to see the long-term contracts in SRECs, similar to long-term PPAs. Even if spot SREC markets are higher than long-term markets, it is difficult to base long-term project finance on the assumption those relationships will continue.

( ) ( )( ) ( ) 2 ( ) 3. n n = 100 000 1+ 0.10 = 100 000 1.331 = 133100

( )( ) ( ) 2 ( ) 3. n n = 100 000 1+ 0.10 = 100 000 1.331 = 133100") Mariusz Próchniak Chair of Economics II Warsaw School of Economics CAPITAL BUDGETING Managerial Economics 1 2 1 Future value (FV) r annual interest rate B the amount of money held today Interest is compounded

Mariusz Próchniak Chair of Economics II Warsaw School of Economics CAPITAL BUDGETING Managerial Economics 1 2 1 Future value (FV) r annual interest rate B the amount of money held today Interest is compounded

Direct Investment, Synthetic PPA s ABC Member Bulk Procurement. Garrett Sprague, A Better City

Direct Investment, Synthetic PPA s ABC Member Bulk Procurement Garrett Sprague, A Better City Barriers to Investing in Renewables 1. Many large institutions not aware of the opportunity. 2. Inertia of

Direct Investment, Synthetic PPA s ABC Member Bulk Procurement Garrett Sprague, A Better City Barriers to Investing in Renewables 1. Many large institutions not aware of the opportunity. 2. Inertia of

Power Purchase Agreement Financial Models in SAM 2013.1.15

Power Purchase Agreement Financial Models in SAM 2013.1.15 SAM Webinar Paul Gilman June 19, 2013 NREL is a national laboratory of the U.S. Department of Energy, Office of Energy Efficiency and Renewable

Power Purchase Agreement Financial Models in SAM 2013.1.15 SAM Webinar Paul Gilman June 19, 2013 NREL is a national laboratory of the U.S. Department of Energy, Office of Energy Efficiency and Renewable

1: Levelized Cost of Energy Calculation. Methodology and Sensitivity

1: Levelized Cost of Energy Calculation Methodology and Sensitivity What is LCOE? Levelized Cost of Energy (LCOE) is the constant unit cost (per kwh or MWh) of a payment stream that has the same present

1: Levelized Cost of Energy Calculation Methodology and Sensitivity What is LCOE? Levelized Cost of Energy (LCOE) is the constant unit cost (per kwh or MWh) of a payment stream that has the same present

Evaluating Cost Basis for Solar Photovoltaic Properties 1

Evaluating Cost Basis for Solar Photovoltaic Properties 1 The review of applications for payment under the Section 1603 program includes a determination as to whether the applicant has properly represented

Evaluating Cost Basis for Solar Photovoltaic Properties 1 The review of applications for payment under the Section 1603 program includes a determination as to whether the applicant has properly represented

TAX EQUITY INVESTMENTS OVERVIEW Frequently Asked Questions

2016 TAX EQUITY INVESTMENTS OVERVIEW Frequently Asked Questions prepared by Distributed Sun & DLA Piper LLP (US) February 25, 2016 Page 0 of 8 Table of Contents Disclaimer... 2 What are the tax-based incentives

2016 TAX EQUITY INVESTMENTS OVERVIEW Frequently Asked Questions prepared by Distributed Sun & DLA Piper LLP (US) February 25, 2016 Page 0 of 8 Table of Contents Disclaimer... 2 What are the tax-based incentives

Practice Bulletin No. 2

Practice Bulletin No. 2 INTERNATIONAL GLOSSARY OF BUSINESS VALUATION TERMS To enhance and sustain the quality of business valuations for the benefit of the profession and its clientele, the below identified

Practice Bulletin No. 2 INTERNATIONAL GLOSSARY OF BUSINESS VALUATION TERMS To enhance and sustain the quality of business valuations for the benefit of the profession and its clientele, the below identified

Paper F9. Financial Management. Friday 6 June 2014. Fundamentals Level Skills Module. The Association of Chartered Certified Accountants.

Fundamentals Level Skills Module Financial Management Friday 6 June 2014 Time allowed Reading and planning: Writing: 15 minutes 3 hours ALL FOUR questions are compulsory and MUST be attempted. Formulae

Fundamentals Level Skills Module Financial Management Friday 6 June 2014 Time allowed Reading and planning: Writing: 15 minutes 3 hours ALL FOUR questions are compulsory and MUST be attempted. Formulae

] (3.3) ] (1 + r)t (3.4)

![] (3.3) ] (1 + r)t (3.4)](/thumbs/39/18539117.jpg "] (3.3) ] (1 + r)t (3.4)") Present value = future value after t periods (3.1) (1 + r) t PV of perpetuity = C = cash payment (3.2) r interest rate Present value of t-year annuity = C [ 1 1 ] (3.3) r r(1 + r) t Future value of annuity

Present value = future value after t periods (3.1) (1 + r) t PV of perpetuity = C = cash payment (3.2) r interest rate Present value of t-year annuity = C [ 1 1 ] (3.3) r r(1 + r) t Future value of annuity

International Glossary of Business Valuation Terms*

40 Statement on Standards for Valuation Services No. 1 APPENDIX B International Glossary of Business Valuation Terms* To enhance and sustain the quality of business valuations for the benefit of the profession

40 Statement on Standards for Valuation Services No. 1 APPENDIX B International Glossary of Business Valuation Terms* To enhance and sustain the quality of business valuations for the benefit of the profession

Buying and Selling a Business Tax Considerations

Buying and Selling a Business Tax Considerations Presented by: Lisa LaSaracina, Partner, Tax Alex Morgan, Partner, Tax Introduction Buying or selling a business is a complex transaction. There are many

Buying and Selling a Business Tax Considerations Presented by: Lisa LaSaracina, Partner, Tax Alex Morgan, Partner, Tax Introduction Buying or selling a business is a complex transaction. There are many

Purchase Price Allocations for Solar Energy Systems for Financial Reporting Purposes

Purchase Price Allocations for Solar Energy Systems for Financial Reporting Purposes July 2015 505 9th Street NW Suite 800 Washington DC 20004 202.862.0556 www.seia.org Solar Energy Industries Association

Purchase Price Allocations for Solar Energy Systems for Financial Reporting Purposes July 2015 505 9th Street NW Suite 800 Washington DC 20004 202.862.0556 www.seia.org Solar Energy Industries Association

SMALL SOLAR. 2014 Nebraska Wind and Solar Conference and Exhibition. Guy C. Smith October 29, 2014

SMALL SOLAR 2014 Nebraska Wind and Solar Conference and Exhibition Guy C. Smith October 29, 2014 TYPES OF SOLAR PROJECTS Concentrated Solar Projects (CSP) Systems generate solar power using mirrors or

SMALL SOLAR 2014 Nebraska Wind and Solar Conference and Exhibition Guy C. Smith October 29, 2014 TYPES OF SOLAR PROJECTS Concentrated Solar Projects (CSP) Systems generate solar power using mirrors or

Discounted Cash Flow. Alessandro Macrì. Legal Counsel, GMAC Financial Services

Discounted Cash Flow Alessandro Macrì Legal Counsel, GMAC Financial Services History The idea that the value of an asset is the present value of the cash flows that you expect to generate by holding it

Discounted Cash Flow Alessandro Macrì Legal Counsel, GMAC Financial Services History The idea that the value of an asset is the present value of the cash flows that you expect to generate by holding it

Fundamentals Level Skills Module, Paper F9

Answers Fundamentals Level Skills Module, Paper F9 Financial Management June 2008 Answers 1 (a) Calculation of weighted average cost of capital (WACC) Cost of equity Cost of equity using capital asset

Answers Fundamentals Level Skills Module, Paper F9 Financial Management June 2008 Answers 1 (a) Calculation of weighted average cost of capital (WACC) Cost of equity Cost of equity using capital asset

Chapter 15: Selling a Business: Asset vs. Stock Sale

Chapter 15: Selling a Business: Asset vs. The purchase price of a business can depend on whether or not the sale is a stock or asset sale. For corporations, sellers always want to sell stock, while buyers

Chapter 15: Selling a Business: Asset vs. The purchase price of a business can depend on whether or not the sale is a stock or asset sale. For corporations, sellers always want to sell stock, while buyers

NIKE Case Study Solutions

NIKE Case Study Solutions Professor Corwin This case study includes several problems related to the valuation of Nike. We will work through these problems throughout the course to demonstrate some of the

NIKE Case Study Solutions Professor Corwin This case study includes several problems related to the valuation of Nike. We will work through these problems throughout the course to demonstrate some of the

Paper F9. Financial Management. Friday 6 December 2013. Fundamentals Level Skills Module. The Association of Chartered Certified Accountants

Fundamentals Level Skills Module Financial Management Friday 6 December 2013 Time allowed Reading and planning: Writing: 15 minutes 3 hours ALL FOUR questions are compulsory and MUST be attempted. Formulae

Fundamentals Level Skills Module Financial Management Friday 6 December 2013 Time allowed Reading and planning: Writing: 15 minutes 3 hours ALL FOUR questions are compulsory and MUST be attempted. Formulae

Introduction to Project Finance Analytic Methods

Introduction to Project Finance Analytic Methods Renewable Energy and Project Development and Financing for California Tribes Sacramento, CA Jack Whittier, McNeil Technologies January 2008 Why? Use a model

Introduction to Project Finance Analytic Methods Renewable Energy and Project Development and Financing for California Tribes Sacramento, CA Jack Whittier, McNeil Technologies January 2008 Why? Use a model

Paper F9. Financial Management. Friday 7 June 2013. Fundamentals Level Skills Module. The Association of Chartered Certified Accountants.

Fundamentals Level Skills Module Financial Management Friday 7 June 2013 Time allowed Reading and planning: Writing: 15 minutes 3 hours ALL FOUR questions are compulsory and MUST be attempted. Formulae

Fundamentals Level Skills Module Financial Management Friday 7 June 2013 Time allowed Reading and planning: Writing: 15 minutes 3 hours ALL FOUR questions are compulsory and MUST be attempted. Formulae

AN INTRODUCTION TO REAL ESTATE INVESTMENT ANALYSIS: A TOOL KIT REFERENCE FOR PRIVATE INVESTORS

AN INTRODUCTION TO REAL ESTATE INVESTMENT ANALYSIS: A TOOL KIT REFERENCE FOR PRIVATE INVESTORS Phil Thompson Business Lawyer, Corporate Counsel www.thompsonlaw.ca Rules of thumb and financial analysis

AN INTRODUCTION TO REAL ESTATE INVESTMENT ANALYSIS: A TOOL KIT REFERENCE FOR PRIVATE INVESTORS Phil Thompson Business Lawyer, Corporate Counsel www.thompsonlaw.ca Rules of thumb and financial analysis

Chapter 8: Theater Asset Valuation (Equipment)

") Chapter 8: Theater Asset Valuation (Equipment) Knowing how much the theater s furniture, fixtures and equipment are worth will determine the amount of goodwill that is being paid as part of the overall

Chapter 8: Theater Asset Valuation (Equipment) Knowing how much the theater s furniture, fixtures and equipment are worth will determine the amount of goodwill that is being paid as part of the overall

American Society of Appraisers. ASA Business Valuation Standards

American Society of Appraisers Business Valuation Standards This release of the approved Business Valuation Standards of the American Society of Appraisers contains all standards approved through February,

American Society of Appraisers Business Valuation Standards This release of the approved Business Valuation Standards of the American Society of Appraisers contains all standards approved through February,

Solar Power Purchase Agreements & Leases

Solar Power Purchase Agreements & Leases Angela Lipanovich, Esq. March 7, 2012 Copyright 2012, Estriatus Law. All rights reserved. Conditions of Usage and Disclaimer 1 Estriatus Law grants the following

Solar Power Purchase Agreements & Leases Angela Lipanovich, Esq. March 7, 2012 Copyright 2012, Estriatus Law. All rights reserved. Conditions of Usage and Disclaimer 1 Estriatus Law grants the following

Introduction to Tax Equity Structures Part II. Tom Stevens Bill Fisher Deloitte Tax LLP

Introduction to Tax Equity Structures Part II Tom Stevens Bill Fisher Deloitte Tax LLP September 29, 2014 Introduction to Tax Equity Structures Part I Summary of Qualifying Resources and Facilities Partnership

Introduction to Tax Equity Structures Part II Tom Stevens Bill Fisher Deloitte Tax LLP September 29, 2014 Introduction to Tax Equity Structures Part I Summary of Qualifying Resources and Facilities Partnership

Contribution 787 1,368 1,813 983. Taxable cash flow 682 1,253 1,688 858 Tax liabilities (205) (376) (506) (257)

(376) (506) (257)") Answers Fundamentals Level Skills Module, Paper F9 Financial Management June 2012 Answers 1 (a) Calculation of net present value (NPV) As nominal after-tax cash flows are to be discounted, the nominal

Answers Fundamentals Level Skills Module, Paper F9 Financial Management June 2012 Answers 1 (a) Calculation of net present value (NPV) As nominal after-tax cash flows are to be discounted, the nominal

NOTICE: For details of the project history please look under the Work Plan section of this website.

NOTICE: This Exposure Draft is available to show the historic evolution of the project. It does not include changes made by the Board following the consultation process and therefore should not be relied

NOTICE: This Exposure Draft is available to show the historic evolution of the project. It does not include changes made by the Board following the consultation process and therefore should not be relied

Discount rates for project appraisal

Discount rates for project appraisal We know that we have to discount cash flows in order to value projects We can identify the cash flows BUT What discount rate should we use? 1 The Discount Rate and

Discount rates for project appraisal We know that we have to discount cash flows in order to value projects We can identify the cash flows BUT What discount rate should we use? 1 The Discount Rate and

How To Calculate The Cost Of Capital Of A Firm

Sample Problems Chapter 10 Title: Cost of Debt 1. Costly Corporation plans a new issue of bonds with a par value of $1,000, a maturity of 28 years, and an annual coupon rate of 16.0%. Flotation costs associated

Sample Problems Chapter 10 Title: Cost of Debt 1. Costly Corporation plans a new issue of bonds with a par value of $1,000, a maturity of 28 years, and an annual coupon rate of 16.0%. Flotation costs associated

CHAPTER 12 RISK, COST OF CAPITAL, AND CAPITAL BUDGETING

CHAPTER 12 RISK, COST OF CAPITAL, AND CAPITAL BUDGETING Answers to Concepts Review and Critical Thinking Questions 1. No. The cost of capital depends on the risk of the project, not the source of the money.

CHAPTER 12 RISK, COST OF CAPITAL, AND CAPITAL BUDGETING Answers to Concepts Review and Critical Thinking Questions 1. No. The cost of capital depends on the risk of the project, not the source of the money.

The cost of capital. A reading prepared by Pamela Peterson Drake. 1. Introduction

The cost of capital A reading prepared by Pamela Peterson Drake O U T L I N E 1. Introduction... 1 2. Determining the proportions of each source of capital that will be raised... 3 3. Estimating the marginal

The cost of capital A reading prepared by Pamela Peterson Drake O U T L I N E 1. Introduction... 1 2. Determining the proportions of each source of capital that will be raised... 3 3. Estimating the marginal

MBA 8230 Corporation Finance (Part II) Practice Final Exam #2

Practice Final Exam #2") MBA 8230 Corporation Finance (Part II) Practice Final Exam #2 1. Which of the following input factors, if increased, would result in a decrease in the value of a call option? a. the volatility of the company's

MBA 8230 Corporation Finance (Part II) Practice Final Exam #2 1. Which of the following input factors, if increased, would result in a decrease in the value of a call option? a. the volatility of the company's

Understanding the changes to the Private Equity Valuation Guidelines.

Understanding the changes to the Private Equity Valuation Guidelines. 17 December 2012 Checked and checked again. A revised version of the International Private Equity and Venture Capital Valuation Guidelines

Understanding the changes to the Private Equity Valuation Guidelines. 17 December 2012 Checked and checked again. A revised version of the International Private Equity and Venture Capital Valuation Guidelines

Time allowed Formulae Sheet, Present Value and Annuity Tables are on

Fundamentals Level Skills Module Financial Management Friday 15 June 2012 Time allowed Reading and planning: Writing: 15 minutes 3 hours ALL FOUR questions are compulsory and MUST be attempted. Formulae

Fundamentals Level Skills Module Financial Management Friday 15 June 2012 Time allowed Reading and planning: Writing: 15 minutes 3 hours ALL FOUR questions are compulsory and MUST be attempted. Formulae

A Basic Introduction to the Methodology Used to Determine a Discount Rate

A Basic Introduction to the Methodology Used to Determine a Discount Rate By Dubravka Tosic, Ph.D. The term discount rate is one of the most fundamental, widely used terms in finance and economics. Whether

A Basic Introduction to the Methodology Used to Determine a Discount Rate By Dubravka Tosic, Ph.D. The term discount rate is one of the most fundamental, widely used terms in finance and economics. Whether

Business Valuation of Sample Industries, Inc. As of June 30, 2008

Business Valuation of Sample Industries, Inc. As of June 30, 2008 Prepared for: Timothy Jones, CEO ABC Actuarial, Inc. Prepared by: John Smith, CPA ACME Valuation Services, LLP 500 North Michigan Ave.

Business Valuation of Sample Industries, Inc. As of June 30, 2008 Prepared for: Timothy Jones, CEO ABC Actuarial, Inc. Prepared by: John Smith, CPA ACME Valuation Services, LLP 500 North Michigan Ave.

Business Valuation. Presented by: CPA Assurance http://www.cpaassurance.com

Business Valuation Presented by: CPA Assurance http://www.cpaassurance.com Presentation Summary Overview of business valuation approaches Standards of value Valuation adjustments Current developments Using

Business Valuation Presented by: CPA Assurance http://www.cpaassurance.com Presentation Summary Overview of business valuation approaches Standards of value Valuation adjustments Current developments Using

Impairment Testing Procedures and Pitfalls

Audio Conference Dial-in Number: 877.691.9300; Access Code: 4321206 Impairment Testing Procedures and Pitfalls November 3, 2009 Presenters: Cory J. Thompson, CFA, CIRA Ryan A. Gandre, CFA Moderator: Jay

Audio Conference Dial-in Number: 877.691.9300; Access Code: 4321206 Impairment Testing Procedures and Pitfalls November 3, 2009 Presenters: Cory J. Thompson, CFA, CIRA Ryan A. Gandre, CFA Moderator: Jay

GESTÃO FINANCEIRA II PROBLEM SET 5 SOLUTIONS (FROM BERK AND DEMARZO S CORPORATE FINANCE ) LICENCIATURA UNDERGRADUATE COURSE

LICENCIATURA UNDERGRADUATE COURSE") GESTÃO FINANCEIRA II PROBLEM SET 5 SOLUTIONS (FROM BERK AND DEMARZO S CORPORATE FINANCE ) LICENCIATURA UNDERGRADUATE COURSE 1 ST SEMESTER 2010-2011 Chapter 18 Capital Budgeting and Valuation with Leverage

GESTÃO FINANCEIRA II PROBLEM SET 5 SOLUTIONS (FROM BERK AND DEMARZO S CORPORATE FINANCE ) LICENCIATURA UNDERGRADUATE COURSE 1 ST SEMESTER 2010-2011 Chapter 18 Capital Budgeting and Valuation with Leverage

Business Valuation What You Need to Know. Frankel & Reichman LLP www.calcpaexpert.com

Business Valuation What You Need to Know Frankel & Reichman LLP www.calcpaexpert.com Presentation Summary Overview of business valuation approaches Standards of value Valuation adjustments Using a qualified

Business Valuation What You Need to Know Frankel & Reichman LLP www.calcpaexpert.com Presentation Summary Overview of business valuation approaches Standards of value Valuation adjustments Using a qualified

GridParity TM Finance Open Access to Financing + Solar Hosting Ivan La Frinere-Sandoval Ted Feierstein Robert Metcalf Stefan Kratz

GridParity TM Finance Open Access to Financing + Solar Hosting Ivan La Frinere-Sandoval Ted Feierstein Robert Metcalf Stefan Kratz The GridParity TM Finance Era Has Arrived The Dawn of Grid Parity Stanford

GridParity TM Finance Open Access to Financing + Solar Hosting Ivan La Frinere-Sandoval Ted Feierstein Robert Metcalf Stefan Kratz The GridParity TM Finance Era Has Arrived The Dawn of Grid Parity Stanford

Chapter 17 Corporate Capital Structure Foundations (Sections 17.1 and 17.2. Skim section 17.3.)

") Chapter 17 Corporate Capital Structure Foundations (Sections 17.1 and 17.2. Skim section 17.3.) The primary focus of the next two chapters will be to examine the debt/equity choice by firms. In particular,

Chapter 17 Corporate Capital Structure Foundations (Sections 17.1 and 17.2. Skim section 17.3.) The primary focus of the next two chapters will be to examine the debt/equity choice by firms. In particular,

Fundamentals Level Skills Module, Paper F9

Answers Fundamentals Level Skills Module, Paper F9 Financial Management June 2009 Answers 1 (a) Weighted average cost of capital (WACC) calculation Cost of equity of KFP Co = 4 0 + (1 2 x (10 5 4 0)) =

Answers Fundamentals Level Skills Module, Paper F9 Financial Management June 2009 Answers 1 (a) Weighted average cost of capital (WACC) calculation Cost of equity of KFP Co = 4 0 + (1 2 x (10 5 4 0)) =

Solar Photovoltaic System Valuation Techniques

Solar Photovoltaic System Valuation Techniques James F. Finlay VP, Commercial Real Estate Appraisal Manager Wells Fargo Bank RETECHS Los Angeles Chair, Real Estate Finance Committee, USGBC LA Southern

Solar Photovoltaic System Valuation Techniques James F. Finlay VP, Commercial Real Estate Appraisal Manager Wells Fargo Bank RETECHS Los Angeles Chair, Real Estate Finance Committee, USGBC LA Southern

Master Limited Partnerships (MLPs):

:") Master Limited Partnerships (MLPs): Frequently Asked Questions Yorkville Capital Management LLC www.yorkvillecapital.com 950 Third Avenue, 23 rd Floor New York, NY 10022 (212) 755-1970 Table of Contents

Master Limited Partnerships (MLPs): Frequently Asked Questions Yorkville Capital Management LLC www.yorkvillecapital.com 950 Third Avenue, 23 rd Floor New York, NY 10022 (212) 755-1970 Table of Contents

FNCE 301, Financial Management H Guy Williams, 2006

Stock Valuation Stock characteristics Stocks are the other major traded security (stocks & bonds). Options are another traded security but not as big as these two. - Ownership Stockholders are the owner

Stock Valuation Stock characteristics Stocks are the other major traded security (stocks & bonds). Options are another traded security but not as big as these two. - Ownership Stockholders are the owner

*** Discussion Draft Not for Distribution ***

*** Discussion Draft Not for Distribution *** Draft PV Cash Flow Analysis Falmouth Wind Turbines Options Analysis Process December 3, 2012 Sustainable Energy Advantage, LLC Assumptions: Modeling Inputs

*** Discussion Draft Not for Distribution *** Draft PV Cash Flow Analysis Falmouth Wind Turbines Options Analysis Process December 3, 2012 Sustainable Energy Advantage, LLC Assumptions: Modeling Inputs

Practice Exam (Solutions)

") Practice Exam (Solutions) June 6, 2008 Course: Finance for AEO Length: 2 hours Lecturer: Paul Sengmüller Students are expected to conduct themselves properly during examinations and to obey any instructions

Practice Exam (Solutions) June 6, 2008 Course: Finance for AEO Length: 2 hours Lecturer: Paul Sengmüller Students are expected to conduct themselves properly during examinations and to obey any instructions

Test 4 Created: 3:05:28 PM CDT 1. The buyer of a call option has the choice to exercise, but the writer of the call option has: A.

Test 4 Created: 3:05:28 PM CDT 1. The buyer of a call option has the choice to exercise, but the writer of the call option has: A. The choice to offset with a put option B. The obligation to deliver the

Test 4 Created: 3:05:28 PM CDT 1. The buyer of a call option has the choice to exercise, but the writer of the call option has: A. The choice to offset with a put option B. The obligation to deliver the

LECTURES ON REAL OPTIONS: PART I BASIC CONCEPTS

LECTURES ON REAL OPTIONS: PART I BASIC CONCEPTS Robert S. Pindyck Massachusetts Institute of Technology Cambridge, MA 02142 Robert Pindyck (MIT) LECTURES ON REAL OPTIONS PART I August, 2008 1 / 44 Introduction

LECTURES ON REAL OPTIONS: PART I BASIC CONCEPTS Robert S. Pindyck Massachusetts Institute of Technology Cambridge, MA 02142 Robert Pindyck (MIT) LECTURES ON REAL OPTIONS PART I August, 2008 1 / 44 Introduction

Fundamentals Level Skills Module, Paper F9. Section A. Mean growth in earnings per share = 100 x [(35 7/30 0) 1/3 1] = 5 97% or 6%

![Fundamentals Level Skills Module, Paper F9. Section A. Mean growth in earnings per share = 100 x [(35 7/30 0) 1/3 1] = 5 97% or 6%](/thumbs/40/20831119.jpg "Fundamentals Level Skills Module, Paper F9. Section A. Mean growth in earnings per share = 100 x [(35 7/30 0) 1/3 1] = 5 97% or 6%") Answers Fundamentals Level Skills Module, Paper F9 Financial Management June 2015 Answers Section A 1 A 2 D 3 D Mean growth in earnings per share = 100 x [(35 7/30 0) 1/3 1] = 5 97% or 6% 4 A 5 D 6 B 7

Answers Fundamentals Level Skills Module, Paper F9 Financial Management June 2015 Answers Section A 1 A 2 D 3 D Mean growth in earnings per share = 100 x [(35 7/30 0) 1/3 1] = 5 97% or 6% 4 A 5 D 6 B 7

Solar Leasing for Residential Photovoltaic Systems

Solar Leasing for Residential Photovoltaic Systems Introduction In the past year, the residential solar lease has received significant attention in the solar marketplace, primarily for its ability to leverage

Solar Leasing for Residential Photovoltaic Systems Introduction In the past year, the residential solar lease has received significant attention in the solar marketplace, primarily for its ability to leverage

Types of Leases. Lease Financing

Lease Financing Types of leases Tax treatment of leases Effects on financial statements Lessee s analysis Lessor s analysis Other issues in lease analysis Who are the two parties to a lease transaction?

Lease Financing Types of leases Tax treatment of leases Effects on financial statements Lessee s analysis Lessor s analysis Other issues in lease analysis Who are the two parties to a lease transaction?

Overview of Rooftop Solar PV Green Bank Financing Model

Overview of Rooftop Solar PV Green Bank Financing Model Sponsored by The Connecticut Clean Energy Finance and Investment Authority and The Coalition for Green Capital Developed by Bob Mudge & Ann Murray,

Overview of Rooftop Solar PV Green Bank Financing Model Sponsored by The Connecticut Clean Energy Finance and Investment Authority and The Coalition for Green Capital Developed by Bob Mudge & Ann Murray,

Some common mistakes to avoid in estimating and applying discount rates

Discount rates Some common mistakes to avoid in estimating and applying discount rates One of the most critical issues for an investor to consider in a strategic acquisition is to estimate how much the

Discount rates Some common mistakes to avoid in estimating and applying discount rates One of the most critical issues for an investor to consider in a strategic acquisition is to estimate how much the

Wind Power Business Models:

Wind Power Business Models: Deal Structures and Economics Project Financing Overview Mohammed Alam Alyra Renewable Energy Finance LLC Steve Krebs Baker Botts L.L.P. Wind Power Development Tutorial Hotel

Wind Power Business Models: Deal Structures and Economics Project Financing Overview Mohammed Alam Alyra Renewable Energy Finance LLC Steve Krebs Baker Botts L.L.P. Wind Power Development Tutorial Hotel

1 (a) NPV calculation Year 1 2 3 4 5 $000 $000 $000 $000 $000 Sales revenue 5,614 7,214 9,015 7,034. Contribution 2,583 3,283 3,880 2,860

NPV calculation Year 1 2 3 4 5 $000 $000 $000 $000 $000 Sales revenue 5,614 7,214 9,015 7,034. Contribution 2,583 3,283 3,880 2,860") Answers Fundamentals Level Skills Module, Paper F9 Financial Management December 2012 Answers 1 (a) NPV calculation Year 1 2 3 4 5 $000 $000 $000 $000 $000 Sales revenue 5,614 7,214 9,015 7,034 Variable

Answers Fundamentals Level Skills Module, Paper F9 Financial Management December 2012 Answers 1 (a) NPV calculation Year 1 2 3 4 5 $000 $000 $000 $000 $000 Sales revenue 5,614 7,214 9,015 7,034 Variable

METHOD FOR PROJECT APPRAISAL: NET PRESENT VALUE OR NPV The sum of discounted cash flows.

OBJECTIVE: ECONOMIC ANALYSIS OF A PROJECT, consisting of the operation of a new incineration plant by the municipality. In particular we are interested in the computaton of a Solid Waste Tariff, consistent

OBJECTIVE: ECONOMIC ANALYSIS OF A PROJECT, consisting of the operation of a new incineration plant by the municipality. In particular we are interested in the computaton of a Solid Waste Tariff, consistent

Valuing the Business

Valuing the Business 1. Introduction After deciding to buy or sell a business, the subject of "how much" becomes important. Determining the value of a business is one of the most difficult aspects of any

Valuing the Business 1. Introduction After deciding to buy or sell a business, the subject of "how much" becomes important. Determining the value of a business is one of the most difficult aspects of any

Examiner s report F9 Financial Management June 2013

Examiner s report F9 Financial Management June 2013 General Comments The examination consisted of four compulsory questions, each worth 25 marks. Most candidates attempted all four questions and there

Examiner s report F9 Financial Management June 2013 General Comments The examination consisted of four compulsory questions, each worth 25 marks. Most candidates attempted all four questions and there

Close the Deal with Finance. Ben Peters AEE Solar Market Analyst

Close the Deal with Finance Ben Peters AEE Solar Market Analyst Tuesday October 9, 2012 What is the Value of Solar? Sandia Labs PV Value A spreadsheet tool developed by Sandia National Laboratories It

Close the Deal with Finance Ben Peters AEE Solar Market Analyst Tuesday October 9, 2012 What is the Value of Solar? Sandia Labs PV Value A spreadsheet tool developed by Sandia National Laboratories It

CFS. Syllabus. Certified Finance Specialist. International benchmark in Finance profession

CFS Certified Finance Specialist Syllabus International benchmark in Finance profession Certified Finance Specialist Summary: This award will provide candidates the opportunity to gain advanced level knowledge

CFS Certified Finance Specialist Syllabus International benchmark in Finance profession Certified Finance Specialist Summary: This award will provide candidates the opportunity to gain advanced level knowledge

Paper F9. Financial Management. Friday 7 December 2012. Fundamentals Level Skills Module. The Association of Chartered Certified Accountants

Fundamentals Level Skills Module Financial Management Friday 7 December 2012 Time allowed Reading and planning: Writing: 15 minutes 3 hours ALL FOUR questions are compulsory and MUST be attempted. Formulae

Fundamentals Level Skills Module Financial Management Friday 7 December 2012 Time allowed Reading and planning: Writing: 15 minutes 3 hours ALL FOUR questions are compulsory and MUST be attempted. Formulae

Paper F9. Financial Management. Fundamentals Pilot Paper Skills module. The Association of Chartered Certified Accountants

Fundamentals Pilot Paper Skills module Financial Management Time allowed Reading and planning: Writing: 15 minutes 3 hours ALL FOUR questions are compulsory and MUST be attempted. Do NOT open this paper

Fundamentals Pilot Paper Skills module Financial Management Time allowed Reading and planning: Writing: 15 minutes 3 hours ALL FOUR questions are compulsory and MUST be attempted. Do NOT open this paper

Where to Turn When Banks Say No? MGI Pagán-Ortiz & Co., CPA, PSC

Where to Turn When Banks Say No? MGI Pagán-Ortiz & Co., CPA, PSC Factoring Definition FACTORING COMPANIES, typically buy a business's accounts receivable at a discount and collect the receivables themselves.

Where to Turn When Banks Say No? MGI Pagán-Ortiz & Co., CPA, PSC Factoring Definition FACTORING COMPANIES, typically buy a business's accounts receivable at a discount and collect the receivables themselves.

Matching Cash Flows and Discount Rates in Discounted Cash Flow Appraisals

Matching Cash Flows and Discount Rates in Discounted Cash Flow Appraisals Introduction by C. Donald Wiggins, DBA, ASA, CVA Business Valuation Review March 1999 There are many conceptual and practical problems

Matching Cash Flows and Discount Rates in Discounted Cash Flow Appraisals Introduction by C. Donald Wiggins, DBA, ASA, CVA Business Valuation Review March 1999 There are many conceptual and practical problems

What is the fair market

3 Construction Company Valuation Primer Fred Shelton, Jr., CPA, MBA, CVA EXECUTIVE SUMMARY This article explores the methods and techniques used in construction company valuation. Using an illustrative

3 Construction Company Valuation Primer Fred Shelton, Jr., CPA, MBA, CVA EXECUTIVE SUMMARY This article explores the methods and techniques used in construction company valuation. Using an illustrative

Corporate Finance: Final Exam

Corporate Finance: Final Exam Answer all questions and show necessary work. Please be brief. This is an open books, open notes exam. For partial credit, when discounting, please show the discount rate

Corporate Finance: Final Exam Answer all questions and show necessary work. Please be brief. This is an open books, open notes exam. For partial credit, when discounting, please show the discount rate

Business Valuations. Business Valuations. Shares Valuation Methods. Dividend valuation. method. P/E ratio. No growth. method.

Business Valuations 1. Objectives 1.1 Identify and discuss reasons for valuing businesses and financial assets. 1.2 Identify information requirements for the purposes of carrying out a valuation in a scenario.

Business Valuations 1. Objectives 1.1 Identify and discuss reasons for valuing businesses and financial assets. 1.2 Identify information requirements for the purposes of carrying out a valuation in a scenario.

MBA (3rd Sem) 2013-14 MBA/29/FM-302/T/ODD/13-14

2013-14 MBA/29/FM-302/T/ODD/13-14") Full Marks : 70 MBA/29/FM-302/T/ODD/13-14 2013-14 MBA (3rd Sem) Paper Name : Corporate Finance Paper Code : FM-302 Time : 3 Hours The figures in the right-hand margin indicate marks. Candidates are required

Full Marks : 70 MBA/29/FM-302/T/ODD/13-14 2013-14 MBA (3rd Sem) Paper Name : Corporate Finance Paper Code : FM-302 Time : 3 Hours The figures in the right-hand margin indicate marks. Candidates are required

Fundamentals Level Skills Module, Paper F9

Answers Fundamentals Level Skills Module, Paper F9 Financial Management December 2008 Answers 1 (a) Rights issue price = 2 5 x 0 8 = $2 00 per share Theoretical ex rights price = ((2 50 x 4) + (1 x 2 00)/5=$2

Answers Fundamentals Level Skills Module, Paper F9 Financial Management December 2008 Answers 1 (a) Rights issue price = 2 5 x 0 8 = $2 00 per share Theoretical ex rights price = ((2 50 x 4) + (1 x 2 00)/5=$2

This policy sets forth system-wide standards for financial accounting and reporting of leases.

Accounting for Leases Section: Accounting and Financial Reporting Title: Accounting for Leases Number: 05.281 Index POLICY.100 POLICY STATEMENT.110 POLICY RATIONALE.120 AUTHORITY.130 APPROVAL AND EFFECTIVE

Accounting for Leases Section: Accounting and Financial Reporting Title: Accounting for Leases Number: 05.281 Index POLICY.100 POLICY STATEMENT.110 POLICY RATIONALE.120 AUTHORITY.130 APPROVAL AND EFFECTIVE

Introduction to Discounted Cash Flow and Project Appraisal. Charles Ward

Introduction to Discounted Cash Flow and Project Appraisal Charles Ward Company investment decisions How firms makes investment decisions about real projects (not necessarily property) How to decide which

Introduction to Discounted Cash Flow and Project Appraisal Charles Ward Company investment decisions How firms makes investment decisions about real projects (not necessarily property) How to decide which

Question 1. Marking scheme. F9 ACCA June 2013 Exam: BPP Answers

Question 1 Text references. NPV is covered in Chapter 8 and real or nominal terms in Chapter 9. Financial objectives are covered in Chapter 1. Top tips. Part (b) requires you to explain the different approaches.

Question 1 Text references. NPV is covered in Chapter 8 and real or nominal terms in Chapter 9. Financial objectives are covered in Chapter 1. Top tips. Part (b) requires you to explain the different approaches.

Finance 2 for IBA (30J201) F. Feriozzi Re-sit exam June 18 th, 2012. Part One: Multiple-Choice Questions (45 points)

F. Feriozzi Re-sit exam June 18 th, 2012. Part One: Multiple-Choice Questions (45 points)") Finance 2 for IBA (30J201) F. Feriozzi Re-sit exam June 18 th, 2012 Part One: Multiple-Choice Questions (45 points) Question 1 Assume that capital markets are perfect. Which of the following statements

Finance 2 for IBA (30J201) F. Feriozzi Re-sit exam June 18 th, 2012 Part One: Multiple-Choice Questions (45 points) Question 1 Assume that capital markets are perfect. Which of the following statements

Week- 1: Solutions to HW Problems

Week- 1: Solutions to HW Problems 10-1 a. Payback A (cash flows in thousands): Annual Period Cash Flows Cumulative 0 ($5,000) ($5,000) 1 5,000 (0,000) 10,000 (10,000) 3 15,000 5,000 4 0,000 5,000 Payback

Week- 1: Solutions to HW Problems 10-1 a. Payback A (cash flows in thousands): Annual Period Cash Flows Cumulative 0 ($5,000) ($5,000) 1 5,000 (0,000) 10,000 (10,000) 3 15,000 5,000 4 0,000 5,000 Payback

LEASING MEDICAL EQUIPMENT? It s as Easy as ABC.

LEASING MEDICAL EQUIPMENT? It s as Easy as ABC. By Edward G. Detwiler, ASA The pleasantries of a newly signed lease often include smiles, handshakes, and conversation describing an agreement in which both

LEASING MEDICAL EQUIPMENT? It s as Easy as ABC. By Edward G. Detwiler, ASA The pleasantries of a newly signed lease often include smiles, handshakes, and conversation describing an agreement in which both

The Basics of Solar Tax Credits and Grants NH&RA 2011

The Basics of Solar Tax Credits and Grants NH&RA 2011 Introduction to Solar Tax Credits Solar credit is an investment tax credit (or ITC). It s called an Energy Tax Credit in Section 48 of Tax Code. Credit

The Basics of Solar Tax Credits and Grants NH&RA 2011 Introduction to Solar Tax Credits Solar credit is an investment tax credit (or ITC). It s called an Energy Tax Credit in Section 48 of Tax Code. Credit

Option Pricing Applications in Valuation!

Option Pricing Applications in Valuation! Equity Value in Deeply Troubled Firms Value of Undeveloped Reserves for Natural Resource Firm Value of Patent/License 73 Option Pricing Applications in Equity

Option Pricing Applications in Valuation! Equity Value in Deeply Troubled Firms Value of Undeveloped Reserves for Natural Resource Firm Value of Patent/License 73 Option Pricing Applications in Equity

Financing Solar Energy for Affordable Housing Projects. May 2009

Financing Solar Energy for Affordable Housing Projects May 2009 Overview Photovoltaic Systems. Installations of photovoltaic systems on the customer side (as opposed to the utility side) of the meter have

Financing Solar Energy for Affordable Housing Projects May 2009 Overview Photovoltaic Systems. Installations of photovoltaic systems on the customer side (as opposed to the utility side) of the meter have

CHAPTER 7: NPV AND CAPITAL BUDGETING

CHAPTER 7: NPV AND CAPITAL BUDGETING I. Introduction Assigned problems are 3, 7, 34, 36, and 41. Read Appendix A. The key to analyzing a new project is to think incrementally. We calculate the incremental

CHAPTER 7: NPV AND CAPITAL BUDGETING I. Introduction Assigned problems are 3, 7, 34, 36, and 41. Read Appendix A. The key to analyzing a new project is to think incrementally. We calculate the incremental

PAYBACK ON RESIDENTIAL PV SYSTEMS WITH PERFORMANCE BASED INCENTIVES AND RENEWABLE ENERGY CERTIFICATES

PAYBACK ON RESIDENTIAL PV SYSTEMS WITH PERFORMANCE BASED INCENTIVES AND RENEWABLE ENERGY CERTIFICATES Andy Black OnGrid Solar Energy Systems 4175 Renaissance Dr #4 San Jose, CA 95134, USA e-mail: andy@ongridnet

PAYBACK ON RESIDENTIAL PV SYSTEMS WITH PERFORMANCE BASED INCENTIVES AND RENEWABLE ENERGY CERTIFICATES Andy Black OnGrid Solar Energy Systems 4175 Renaissance Dr #4 San Jose, CA 95134, USA e-mail: andy@ongridnet

Source of Finance and their Relative Costs F. COST OF CAPITAL

F. COST OF CAPITAL 1. Source of Finance and their Relative Costs 2. Estimating the Cost of Equity 3. Estimating the Cost of Debt and Other Capital Instruments 4. Estimating the Overall Cost of Capital

F. COST OF CAPITAL 1. Source of Finance and their Relative Costs 2. Estimating the Cost of Equity 3. Estimating the Cost of Debt and Other Capital Instruments 4. Estimating the Overall Cost of Capital

1 (a) Net present value of investment in new machinery Year 1 2 3 4 5 $000 $000 $000 $000 $000 Sales income 6,084 6,327 6,580 6,844

Net present value of investment in new machinery Year 1 2 3 4 5 $000 $000 $000 $000 $000 Sales income 6,084 6,327 6,580 6,844") Answers Fundamentals Level Skills Module, Paper F9 Financial Management June 2013 Answers 1 (a) Net present value of investment in new machinery Year 1 2 3 4 5 $000 $000 $000 $000 $000 Sales income 6,084

Answers Fundamentals Level Skills Module, Paper F9 Financial Management June 2013 Answers 1 (a) Net present value of investment in new machinery Year 1 2 3 4 5 $000 $000 $000 $000 $000 Sales income 6,084

JUNE 2016. Investor Presentation

JUNE 2016 Investor Presentation Forward-Looking Statements This presentation contains forward-looking statements that involve risks and uncertainties, including statements regarding SolarCity s business;

JUNE 2016 Investor Presentation Forward-Looking Statements This presentation contains forward-looking statements that involve risks and uncertainties, including statements regarding SolarCity s business;

VALUATION CA Bhavik Shah 16 May 2015

VALUATION CA Bhavik Shah 16 May 2015 Presentation Overview Valuation Concept Purpose of Valuation Principal Methods of Valuation Net Assets Value (NAV) Method Price to Book Multiple (P/B) Method Price

VALUATION CA Bhavik Shah 16 May 2015 Presentation Overview Valuation Concept Purpose of Valuation Principal Methods of Valuation Net Assets Value (NAV) Method Price to Book Multiple (P/B) Method Price

Choice of Discount Rate

Choice of Discount Rate Discussion Plan Basic Theory and Practice A common practical approach: WACC = Weighted Average Cost of Capital Look ahead: CAPM = Capital Asset Pricing Model Massachusetts Institute

Choice of Discount Rate Discussion Plan Basic Theory and Practice A common practical approach: WACC = Weighted Average Cost of Capital Look ahead: CAPM = Capital Asset Pricing Model Massachusetts Institute

Institute of Chartered Accountant Ghana (ICAG) Paper 2.4 Financial Management

Paper 2.4 Financial Management") Institute of Chartered Accountant Ghana (ICAG) Paper 2.4 Financial Management Final Mock Exam 1 Marking scheme and suggested solutions DO NOT TURN THIS PAGE UNTIL YOU HAVE COMPLETED THE MOCK EXAM ii Financial

Institute of Chartered Accountant Ghana (ICAG) Paper 2.4 Financial Management Final Mock Exam 1 Marking scheme and suggested solutions DO NOT TURN THIS PAGE UNTIL YOU HAVE COMPLETED THE MOCK EXAM ii Financial

Tax Accounting Services. Goodwill impairment testing: Tax considerations

Tax Accounting Services Goodwill impairment testing: Tax considerations In financial accounting, goodwill is an asset representing the future economic benefits arising from other assets acquired in a business

Tax Accounting Services Goodwill impairment testing: Tax considerations In financial accounting, goodwill is an asset representing the future economic benefits arising from other assets acquired in a business

Actuarial Society of India

Actuarial Society of India Examination November 2006 CT2: Finance and Financial Reporting Indicative Solutions Page 1 of 7 Solution 1-10 Sol 1 Sol 2 Sol 3 Sol 4 Sol 5 Sol 6 Sol 7 Sol 8 Sol 9 Sol 10 E E

Actuarial Society of India Examination November 2006 CT2: Finance and Financial Reporting Indicative Solutions Page 1 of 7 Solution 1-10 Sol 1 Sol 2 Sol 3 Sol 4 Sol 5 Sol 6 Sol 7 Sol 8 Sol 9 Sol 10 E E

Retail Licence Exemptions for Solar Power Purchase Agreement Providers. Department of Finance Public Utilities July 2015

2/164 Balcatta Rd, Balcatta WA 6021 1300 897 441 www.carbonfootie.com.au Retail Licence Exemptions for Solar Power Purchase Agreement Providers Carbon Footie Submission to Draft Recommendations Report

2/164 Balcatta Rd, Balcatta WA 6021 1300 897 441 www.carbonfootie.com.au Retail Licence Exemptions for Solar Power Purchase Agreement Providers Carbon Footie Submission to Draft Recommendations Report

Financial Modeling & Valuation Stuart A. Neiberg, MAcc, CPA, CFA Director HealthCare Appraisers, Inc.

Financial Modeling & Valuation Stuart A. Neiberg, MAcc, CPA, CFA Director HealthCare Appraisers, Inc. Presentation Outline Why is Financial Modeling and Valuation Important? Industry Overview and Trends

Financial Modeling & Valuation Stuart A. Neiberg, MAcc, CPA, CFA Director HealthCare Appraisers, Inc. Presentation Outline Why is Financial Modeling and Valuation Important? Industry Overview and Trends

METHODS OF VALUATION FOR MERGERS AND ACQUISITIONS

Graduate School of Business Administration University of Virginia METHODS OF VALUATION FOR MERGERS AND ACQUISITIONS This note addresses the methods used to value companies in a merger and acquisitions

Graduate School of Business Administration University of Virginia METHODS OF VALUATION FOR MERGERS AND ACQUISITIONS This note addresses the methods used to value companies in a merger and acquisitions

Equity Analysis and Capital Structure. A New Venture s Perspective

Equity Analysis and Capital Structure A New Venture s Perspective 1 Venture s Capital Structure ASSETS Short- term Assets Cash A/R Inventories Long- term Assets Plant and Equipment Intellectual Property

Equity Analysis and Capital Structure A New Venture s Perspective 1 Venture s Capital Structure ASSETS Short- term Assets Cash A/R Inventories Long- term Assets Plant and Equipment Intellectual Property

Solar Photovoltaic System, Valuation and Leasing Overview

ASA-LA and SCCAI Annual Joint Dinner Common Sense Solar Solar Photovoltaic System, Valuation and Leasing Overview James Finlay, MRICS May 12, 2015 RICS - Solar Leasing 10/16/2014 1 Presentation Overview

ASA-LA and SCCAI Annual Joint Dinner Common Sense Solar Solar Photovoltaic System, Valuation and Leasing Overview James Finlay, MRICS May 12, 2015 RICS - Solar Leasing 10/16/2014 1 Presentation Overview

Rooftop Revenues. How Your Business Can Profit from Solar Energy.

Rooftop Revenues How Your Business Can Profit from Solar Energy. White Paper Introduction The decision to implement a solar PV system, once dismissed as an overly expensive investment, can now be backed

Rooftop Revenues How Your Business Can Profit from Solar Energy. White Paper Introduction The decision to implement a solar PV system, once dismissed as an overly expensive investment, can now be backed

Cash flow before tax 1,587 1,915 1,442 2,027 Tax at 28% (444) (536) (404) (568)

(536) (404) (568)") Answers Fundamentals Level Skills Module, Paper F9 Financial Management June 2014 Answers 1 (a) Calculation of NPV Year 1 2 3 4 5 $000 $000 $000 $000 $000 Sales income 5,670 6,808 5,788 6,928 Variable

Answers Fundamentals Level Skills Module, Paper F9 Financial Management June 2014 Answers 1 (a) Calculation of NPV Year 1 2 3 4 5 $000 $000 $000 $000 $000 Sales income 5,670 6,808 5,788 6,928 Variable

UNDERSTANDING SOLAR POWER CLAIMS:

UNDERSTANDING SOLAR POWER CLAIMS: Best Practices for Hosting, Leasing, and Owning Solar Generation Presenters: Jenny Heeter, NREL Robin Quarrier, CRS Bryce Smith, OneEnergy Renewables Feb 26, 2015 NREL

UNDERSTANDING SOLAR POWER CLAIMS: Best Practices for Hosting, Leasing, and Owning Solar Generation Presenters: Jenny Heeter, NREL Robin Quarrier, CRS Bryce Smith, OneEnergy Renewables Feb 26, 2015 NREL

Examiner s report F9 Financial Management June 2011

Examiner s report F9 Financial Management June 2011 General Comments Congratulations to candidates who passed Paper F9 in June 2011! The examination paper looked at many areas of the syllabus and a consideration

Examiner s report F9 Financial Management June 2011 General Comments Congratulations to candidates who passed Paper F9 in June 2011! The examination paper looked at many areas of the syllabus and a consideration

Assumptions: No transaction cost, same rate for borrowing/lending, no default/counterparty risk

Derivatives Why? Allow easier methods to short sell a stock without a broker lending it. Facilitates hedging easily Allows the ability to take long/short position on less available commodities (Rice, Cotton,

Derivatives Why? Allow easier methods to short sell a stock without a broker lending it. Facilitates hedging easily Allows the ability to take long/short position on less available commodities (Rice, Cotton,