4 b) Where to Record Revenue. 4 5 c) When to Record Revenue Recognition of Unrestricted Revenue Recognition of Restricted Revenue Sources

|

|

|

- Willa Ross

- 8 years ago

- Views:

Transcription

1 Revenue Recognition Policy Guidelines These guidelines are organized within the following sections: Pages I. Purpose 1 II. Responsibilities 1 III. Definitions 2-3 IV. Major Sources of Revenue and Normal Categorization 4 a) Identification of Type of Revenue 4 b) Where to Record Revenue 4 5 c) When to Record Revenue 6-11 Recognition of Unrestricted Revenue Recognition of Restricted Revenue Sources I. Purpose: In support of the Revenue Recognition Policy this guideline relates to the appropriate accounting of revenue from various sources for restricted and unrestricted purposes in accordance with the Restricted Fund Method of Accounting [Canadian Institute of Chartered Accountants (CICA) Handbook (HB) ]. The Revenue Recognition Policy addresses external revenue transactions between the University of Saskatchewan and non-university entities (Note that Chart 2 entities as recorded in Unifi are considered non-university entities.). Revenue transactions between University entities (i.e. between colleges and units) should be recorded as internal cost recoveries. Three overarching issues will be addressed: a) Identification of external revenue restrictions: Whether the revenue to be recorded is classified as restricted purpose or unrestricted purpose. b) Where to record revenue (fund classification): Whether the revenue is recorded in a restricted or unrestricted fund. c) When to record revenue: When does the University have the obligation to record the revenue? II. Responsibilities: Financial Services Division is responsible for recording revenue and setting up accounts receivable for grant and contract revenue transactions in the Student Financial Aid, Research and Capital Restricted Funds. Financial Services Division is responsible for recording investment income and setting up accounts receivable for any funds which are invested by the University either self-managed or as part of the University investment pool. Corporate Administration is responsible for recording real estate income and setting up accounts receivable for University properties under its administration. 1

2 Colleges and units are responsible for recording revenue, setting up accounts receivable and recording deferred revenue in the General Fund (see definition below) for activity managed at the college or unit level. III. Definitions: Contract - a reciprocal agreement between two or more parties creating enforceable obligations. The University of Saskatchewan requires that the agreement be in writing, signed by the duly authorized University personnel in accordance with the University Signing Authority Policy. Common features of most contracts: Contract defines the scope and nature of the work; Contract establishes the term of the contract, the cash flows, reporting requirements and duration; Contract details any obligations the University must fulfill before it is eligible to access subsequent year s revenues; Contract specifies what is to happen to any unspent resources; Contract often contains requirements for regular invoicing. Contribution - a non-reciprocal transfer to a not-for-profit organization of cash or other assets or a non-reciprocal settlement or cancellation of its liabilities. Government funding provided to a not-for-profit organization is considered to be a contribution [CICA HB (b)]. Examples include grants, gifts and bequests but do not include sales of services or product to government. Contribution Receivable - should be recognized as an asset when it meets the following criteria: a) The amount to be received can be reasonably estimated; and b) Ultimate collection is reasonably assured. [CICA HB ] For purposes of revenue recognition, contributions include contributions receivable. The University has determined that one of the critical elements to meeting the contribution receivable criteria is the existence of a formal agreement, evidenced by signed documentation, regarding the contribution. Signed documentation is evidence of both parties formal commitment to the specific nature and terms of the agreed-upon arrangement. Endowment Contribution - is a type of restricted contribution subject to externally imposed stipulations specifying that the resources contributed be maintained permanently, although the constituent assets may change from time to time. Endowment Fund - a self-balancing set of accounts which report the accumulation of endowment contributions. Only endowment contributions and investment income subject to restrictions stipulating that it be added to the principal amount of the endowment fund would be reported as revenue of the endowment fund. Allocations of resources to the endowment fund that result from the imposition of internal restrictions are recorded as interfund transfers. [CICA HB (e)(ii)] Fund - a self balancing set of accounts recording cash and other financial resources, together with all related liabilities and residual equities or balances, and changes therein, 2

3 which are segregated for the purpose of carrying on specific activities or attaining certain objectives in accordance with special regulations, restrictions, or limitations. General Fund - a self-balancing set of accounts which reports all unrestricted revenue and restricted contributions for which no corresponding restricted fund is presented. The fund balance represents net assets that are not subject to externally imposed restrictions. [CICA HB (e)(iii)] For the University of Saskatchewan, the General Fund encompasses all Operating Funds and Ancillary Funds. Grant - financial support for a particular subject area or field without formal detailed stipulations. Consistent with characteristics identified in policies and guidelines developed by Research Services, the following are often present in a grant: Flexibility exists to revise the course of the work as it proceeds without the approval of the sponsor; Payment of the grant is not linked to the timeliness or contents of the results and is usually paid in advance or through a series of advances; No restrictions are placed on the publication of results as they are intended for public dissemination; Sponsor does not reserve to itself rights to the commercial exploitation of results; Principal Investigator or any co-investigator(s) cannot be compensated under the project. Investment Income - revenue arising from the use by others of University assets including, but not exclusive to, the following categories: Interest - on a time proportion basis; Royalties - as they accrue, in accordance with the terms of the relevant agreement; Dividends - when the shareholder's right to receive payment is established; Realized gains and losses - in the period in which they occur; Unrealized gains and losses - in the period in which they occur, as GAAP applicable. Investment income will be considered to be restricted or unrestricted based on the restrictions imposed on the resources originally contributed. Real Estate Income - income generated from real estate, such as lease or rent payments Restricted Contribution - a contribution subject to externally imposed stipulations that specify the purpose for which the contributed asset is to be used. A contribution restricted for the purchase of a capital asset or a contribution of the capital asset itself is a type of restricted contribution. [CICA HB (b)(i)] Restricted Fund - a self-balancing set of accounts the elements of which are restricted or relate to the use of restricted resources. Only restricted contributions, other than endowment contributions, and other externally restricted revenue would be reported as revenue in a restricted fund. Allocations of resources that result from the imposition of internal restrictions are recorded as interfund transfers to the restricted fund. [CICA HB (e)(i)]. 3

(iii)] For the University of Saskatchewan, the General Fund encompasses all Operating Funds and Ancillary Funds.")

4 The University of Saskatchewan utilizes three types of restricted funds: Student Financial Aid, Research and Capital. Sale of Services or Products - any sale of a good or service to parties external to the University. Student Fees - tuition and fees as defined in University Policy 4.33 Tuition and Fees Authorization. Unrestricted Revenue - neither restricted nor endowed; available for general use IV. Major Sources of Revenue and Normal Categorization: Revenue Restricted Unrestricted Student fees x Sales of services and products x Grants x Contracts x x Gifts and bequests (including gift-in-kind) x x Income from investments x x Real estate income x x Miscellaneous income x x The three overarching issues discussed in the Purpose section should be addressed as follows: a) Identification of Type of Revenue: [See Major Sources of Revenue and Normal Categorization table above]: Student fees and the sale of services and products are always considered unrestricted forms of revenue. Grants are always considered restricted contributions since by definition they are financial support for a particular subject area or field. Contracts may be for unrestricted purposes or for restricted purposes (e.g. where external third parties attach stipulations as to how contractual funds may be spent). Gifts and bequests may be received as unrestricted contributions or restricted contributions (i.e. where external third parties attach stipulations as to their use). Income from investments and real estate income may be unrestricted or restricted revenue, based on the original investment and any external restrictions. Miscellaneous income may be unrestricted or restricted revenue, based on the source of income and any external restrictions. b) Where to Record Revenue (Fund Classification): [See Decision Tree Illustration for Organizations below]: Student fees and the sale of services and products, always considered unrestricted forms of revenue, are recorded in the General Fund. Grants received as restricted contributions for Student Financial Aid, Research or Capital purposes, are recorded in the applicable restricted fund. 4

")

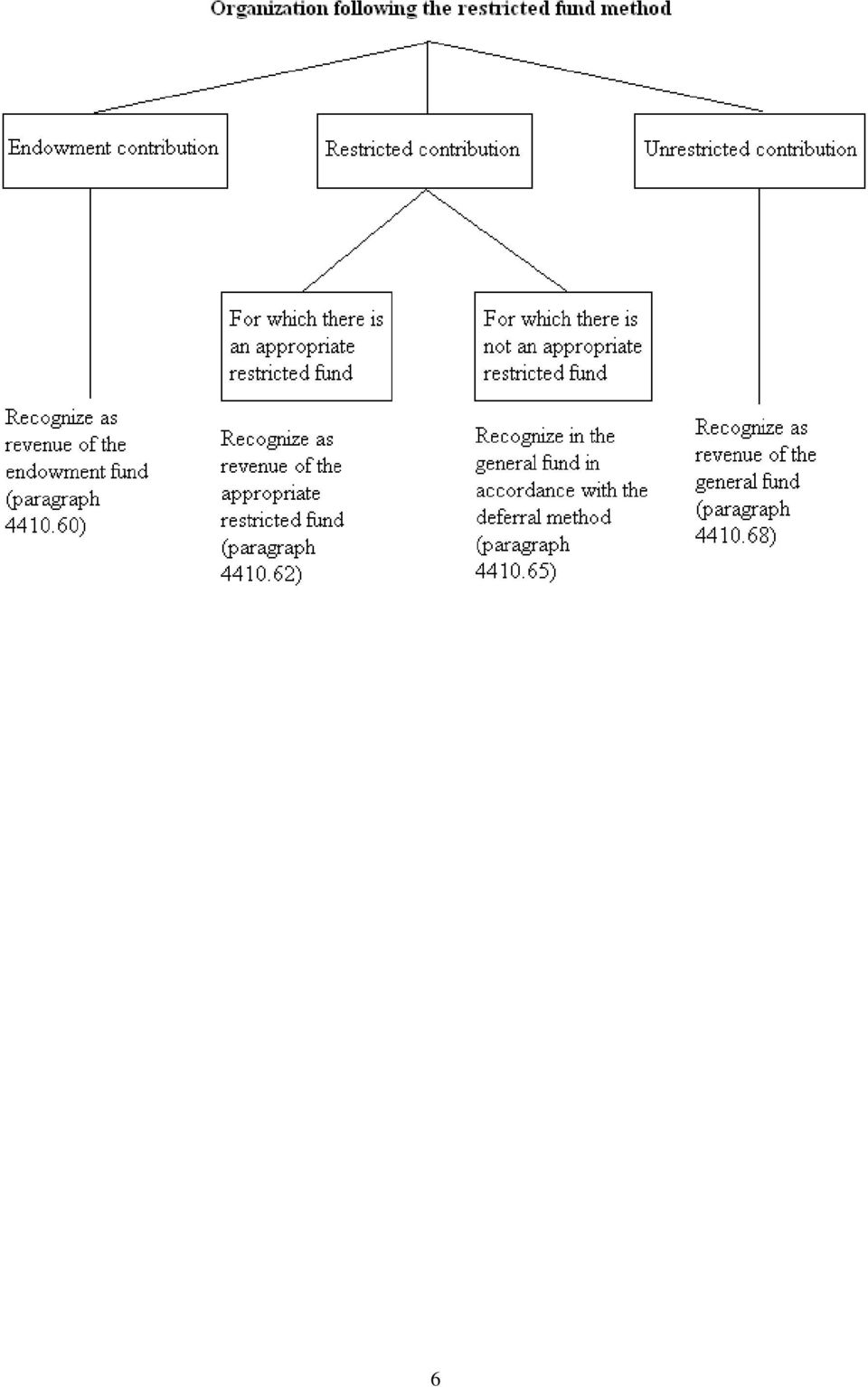

5 Grants received as restricted contributions where there is no specific restricted fund are recorded in the General Fund. This revenue must then be deferred and recognized as applicable matching expenses are recorded. Unrestricted contract revenue is recorded in the General Fund. Contract revenue restricted for Student Financial Aid, Research or Capital purposes is recorded in the applicable restricted fund. Contract revenue restricted for purposes where there is no specific restricted fund is recorded in the General Fund. Gifts and bequests, received as unrestricted contributions, are recorded in the General Fund. Gifts and bequests, received as restricted contributions for Student Financial Aid, Research or Capital purposes, are recorded in the applicable restricted fund. Gifts and bequests received as restricted contributions where there is no specific restricted fund are recorded in the General Fund. This revenue must then be deferred and recognized as applicable matching expenses are recorded. Income from investments and real estate income are recorded in a restricted fund or unrestricted fund based on the terms mandated by the original grant, contract, gift or bequest. Miscellaneous income from unrestricted sources is recorded in the General Fund. Miscellaneous income for Student Financial Aid, Research or Capital purposes is recorded in the applicable restricted fund. Miscellaneous income received with restrictions where there is no specific restricted fund is recorded in the General Fund. This revenue must then be deferred and recognized as applicable matching expenses are recorded. Endowment contributions are recorded in the Endowment (restricted) Fund Application: CICA HB Decision Tree Illustration for Organizations, such as the University of Saskatchewan, using the Restricted Fund Method: 5

6 6

7 c) When to Record Revenue: [See tables below: Recognition of Unrestricted Revenue Sources and Recognition of Restricted Revenue Sources ]: Recognition of Unrestricted Revenue Sources: Type of Unrestricted Revenue Student Fees (type of sales and service) Sales of Services and Products Contracts Gifts and Bequests (including gift-in-kind) Income from Investments Real Estate Income Miscellaneous Income Timing of Recognition record as revenue in the year courses and seminars are held defer revenue if for future period course or seminar prorate revenue if course or seminar spans the fiscal year-end record as revenue when product sold or service provided (set up accounts receivable, if payment not received) defer deposits on sale until transfer of risks and rewards of ownership record revenue as the service or contract activity is performed ensure enforceable obligations have been met record as revenue in period funds received or receivable pledges are not recorded until received record as revenue when reasonable assurance exists regarding measurement and collectability record as revenue in period funds earned (set up accounts receivable, if not received) record as revenue in period funds earned (set up accounts receivable, if not received) CICA Handbook Reference Student Fees (Unrestricted): Student fees are recorded as revenue in the General Fund in the time period in which the course or seminar occurs. If student fees are received prior to when the course or seminar occurs, this revenue must be deferred as a liability (deferred revenue) until earned. If the course or seminar overlaps fiscal periods, revenue must be prorated between periods. For example, if a course ran from January to June of a calendar year, at April 30 (the University s year-end), record 4/6 th of the revenue generated from student fees and defer 2/6 th of the revenue generated from student fees. 7

defer deposits on sale until transfer of risks and rewards of")

8 8

9 Sales of Services and Products (Unrestricted): Sales of services and products are recorded as revenue in the General Fund at the time the product is sold or the service is provided. If payment is not received at the time the product is sold or the service is provided, an account receivable should be set up in UniFi for the sale of product or service that took place. Deposits on future sales are recorded as deferred revenue (a liability) and would be applied against the total of the good or service at the time the sale is recorded (i.e. at the time the seller transfers the risks and rewards of ownership to the buyer). Contracts (Unrestricted): Unrestricted contracts are recorded as revenue in the General Fund as the service or contract activity is performed, provided that at the time of performance ultimate collection is reasonably assured. If payment is not simultaneously received, revenue should still be recorded and a corresponding accounts receivable set up in the period that the service or contract activity is performed. Gifts and Bequests (Unrestricted): Unrestricted gifts and bequests are recorded as revenue in the General Fund in the period received or receivable, if ultimate collection if reasonably assured. Due to uncertainty surrounding ultimate collection, accounts receivable are not recorded for pledged gifts and bequests. Investment Income (Unrestricted): Unrestricted investment income is recorded as revenue in the General Fund when reasonable assurance exists regarding measurement and collectability. Real Estate Income (Unrestricted): Unrestricted real estate income is recorded as revenue in the General Fund in the period earned. Real estate income earned but not received is accrued in the General Fund. Miscellaneous Income (Unrestricted): Unrestricted miscellaneous income is recorded as revenue in the General Fund in the period earned. Miscellaneous income earned but not received is accrued in the General Fund. 9

: Unrestricted contracts are recorded as revenue in the General Fund as the service or contract activity is performed, provided that at the time of performance ultimate")

10 Recognition of Restricted Revenue Sources: Type of Restricted Revenue Grants, with a corresponding restricted fund (i.e. for research, student financial aid, capital) Grants, without a corresponding restricted fund Contracts, with a corresponding restricted fund (i.e. for research, student financial aid, capital) Contracts, without a corresponding restricted fund Gifts and bequests (including gift-in-kind), with a corresponding restricted fund (i.e. for research, student financial aid, capital, endowment) Gifts and bequests (including gift-in-kind), without a corresponding restricted fund Income from investments, with a corresponding restricted fund (i.e. for research, student financial aid, capital) Income from investments, without a corresponding restricted fund Real estate income, with a corresponding restricted fund (i.e. for research, student financial aid, capital) Real estate income, without a corresponding restricted fund Miscellaneous income, with a corresponding restricted fund (i.e. for research, student financial aid, capital) Timing of Recognition record as revenue upon receipt of signed documentation (set up accounts receivable, if funding not received) consider implications of multi-year agreements (see below) record as revenue upon receipt of signed documentation (set up accounts receivable, if funding not received) consider implications of multi-year agreements (see below) defer revenue if for future period expenses record revenue as the service or contract activity is performed (set up accounts receivable, if payment not received) ensure enforceable obligations have been met record revenue as the service or contract activity is performed (set up accounts receivable, if payment not received) ensure enforceable obligations have been met defer revenue if for future period expenses record as revenue in period funds received or receivable pledges are not recorded until received record as revenue in period funds received or receivable pledges are not recorded until received defer revenue if for specific expenses that have not yet been incurred record as revenue when reasonable assurance exists regarding measurement and collectability record as revenue when reasonable assurance exists regarding measurement and collectability defer revenue if for specific expenses that have not yet been incurred record as revenue in period earned (set up accounts receivable, if not received) record as revenue in period earned (set up accounts receivable, if not received) defer revenue if for specific expenses that have not yet been incurred record as revenue in period funds earned (set up accounts receivable, if not received) CICA Handbook Reference

Income from investments, without a corresponding restricted fund Real estate income, with a corresponding restricted fund (i.e. for research, student financial aid, capital) Real estate income, without a corresponding restricted fund Miscellaneous income, with a corresponding restricted fund (i.")

11 Miscellaneous income, without a corresponding restricted fund record as revenue in period funds earned (set up accounts receivable, if not received) defer revenue if for specific expenses that have not yet been incurred Grants (Corresponding Restricted Fund): Restricted grants are recorded as revenue in the corresponding restricted fund if we have documentation (i.e. signed agreement has been received) which allows the amount to be reasonably estimated and if ultimate collection is reasonably assured. If payment is not received, revenue should still be recorded and a corresponding account receivable set up when the documentation is received. Grants (No Corresponding Restricted Fund): Restricted grants with no corresponding restricted fund are recorded as revenue in the General Fund when a signed agreement has been received which allows the amount to be reasonably estimated and if ultimate collection is reasonably assured. If payment is not received, revenue should still be recorded and a corresponding account receivable set up when the documentation is received. If the grant or contract is restricted for expenditures of one of more future periods, it is deferred and recorded as revenue in the same period or periods as the related expenses are recorded. Note: Grants may be annual or multi-year agreements. Multi-year agreements generally fall in one of two categories: 1. Agreements where each subsequent year s funding is subject to an approval process, such as appropriation in Parliament: In this instance, the first year s funding is recorded as revenue in the appropriate fund when documentation (e.g. signed agreement or award letter) is received which allows the amount to be reasonably estimated and if ultimate collection is reasonably assured. One subsequent year s funding is recorded as revenue (set up as accounts receivable, if payment has not been received) on the anniversary date as most funding agencies recognize and approve annual cash flows for liabilities. For example, assume a 5 year agreement for $100,000 began January 1, with $20,000 to be received on signing and $20,000 on each subsequent anniversary date. On receipt of the signed agreement, Year 1, $20,000 would be recorded as revenue (if the funding did not accompany the signed agreement, an accounts receivable would be set up). At January 1, Year 2 another $20,000 is recorded, debiting accounts receivable and crediting revenue for the subsequent year s funding that will be received in the upcoming fiscal year, because the amount to be received can be reasonably estimated and assuming ultimate collection is reasonably assured. 2. Agreements where each subsequent year s funding is NOT subject to an annual approval process: When agreements are not subject to an annual approval process, the entire value of the agreement will be recorded as revenue when documentation (e.g. signed agreement or award letter) is received if reasonable assurance exists as to ultimate collectability. Contracts (Corresponding Restricted Fund): 11

: Restricted grants with no corresponding restricted fund are recorded as revenue in the General Fund when a signed agreement has been received which allows")

12 Restricted contracts are recorded as revenue in the corresponding restricted fund as the service or contract activity is performed, provided that at the time of performance ultimate collection is reasonably assured. If payment is not simultaneously received, revenue should still be recorded and a corresponding account receivable set up. 12

13 Contracts (No Corresponding Restricted Fund): Restricted contracts with no corresponding restricted fund are recorded as revenue in the General Fund as the service or contract activity is performed, provided that at the time of performance ultimate collection is reasonably assured. If payment is not simultaneously received, revenue should still be recorded and a corresponding account receivable set up. Gifts and Bequests (Corresponding Restricted Fund): Restricted gifts and bequests are recorded as revenue in the corresponding restricted fund when received or receivable, if ultimate collection is reasonably assured. Due to uncertainty surrounding ultimate collection, accounts receivable are not recorded for pledged gifts and bequests. Gifts and Bequests (No Corresponding Restricted Fund): Restricted gifts and bequests with no corresponding restricted fund are recorded as revenue in the General Fund when received or receivable, if ultimate collection if reasonably assured. If the gift or bequest is restricted for expenditures of one of more future periods, it is deferred and recorded as revenue in the same period or periods as the related expenses are recorded. Due to uncertainty surrounding ultimate collection, accounts receivable are not recorded for pledged gifts and bequests. Investment Income (Corresponding Restricted Fund): Investment income on restricted funds is recorded as revenue of the appropriate fund, as restrictions mandate, when reasonable assurance exits regarding measurement and collectability. Investment Income (No Corresponding Restricted Fund): Investment income earned on contributions restricted for purposes other than one of the established Restricted Fund types is recorded in the General Fund when reasonable assurance exits regarding measurement and collectability.. If the investment income is restricted for expenditures of one of more future periods, it is deferred and recorded as revenue in the same period or periods as the related expenses are recorded. Real Estate Income (Corresponding Restricted Fund): Real estate income on restricted funds is recorded as revenue of the appropriate fund in the period earned, as restrictions mandate. Real estate income earned but not received is accrued in the appropriate fund as restrictions mandate. Real Estate Income (No Corresponding Restricted Fund): Real estate income on funds restricted for purposes other than one of the established Restricted Fund types is recorded in the General Fund in the period earned. Real estate income earned but not received is accrued in the appropriate fund as restrictions mandate. 13

: Restricted gifts and bequests are recorded as revenue in the corresponding restricted fund when received or receivable, if ultimate collection is")

14 If the real estate income is restricted for expenditures of one of more future periods, it is deferred and recorded as revenue in the same period or periods as the related expenses are recorded. Miscellaneous Income (Corresponding Restricted Fund): Miscellaneous income on restricted funds is recorded as revenue of the appropriate fund in the period earned, as restrictions mandate. Miscellaneous income earned but not received is accrued in the appropriate fund as restrictions mandate. Miscellaneous Income (No Corresponding Restricted Fund): Miscellaneous income on funds restricted for purposes other than one of the established Restricted Fund types is recorded in the General Fund in the period earned. Miscellaneous income earned but not received is accrued in the appropriate fund as restrictions mandate. If the miscellaneous income is restricted for expenditures of one of more future periods, it is deferred and recorded as revenue in the same period or periods as the related expenses are recorded. 14

: Miscellaneous income on funds restricted for purposes other than one of the established Restricted Fund types is recorded in the General Fund")

ASNPO AT A GLANCE Contributions

ASNPO AT A GLANCE Contributions March 2013 Contributions 1 Effective Date Fiscal years beginning on or after January 1, 2012 SCOPE Applies to: Contributions, related investment income and contributions

ASNPO AT A GLANCE Contributions March 2013 Contributions 1 Effective Date Fiscal years beginning on or after January 1, 2012 SCOPE Applies to: Contributions, related investment income and contributions

MAKE-A-WISH FOUNDATION OF MASSACHUSETTS AND RHODE ISLAND, INC. Financial Statements. August 31, 2014. (With Independent Auditors Report Thereon)

") MAKE-A-WISH FOUNDATION OF MASSACHUSETTS Financial Statements (With Independent Auditors Report Thereon) Table of Contents Page Independent Auditors Report 1 Statement of Financial Position 3 Statement

MAKE-A-WISH FOUNDATION OF MASSACHUSETTS Financial Statements (With Independent Auditors Report Thereon) Table of Contents Page Independent Auditors Report 1 Statement of Financial Position 3 Statement

Huron University College. Financial Statements April 30, 2012

Financial Statements April 30, June 27, Independent Auditor s Report To the Executive Board of Huron University College We have audited the accompanying financial statements of Huron University College,

Financial Statements April 30, June 27, Independent Auditor s Report To the Executive Board of Huron University College We have audited the accompanying financial statements of Huron University College,

The Colleges of the Seneca Financial Statements May 31, 2007 and 2006

Financial Statements PricewaterhouseCoopers LLP 1100 Bausch & Lomb Place Rochester NY 14604-2705 Telephone (585) 232 4000 Facsimile (585) 454 6594 Report of Independent Auditors To the Board of Trustees

Financial Statements PricewaterhouseCoopers LLP 1100 Bausch & Lomb Place Rochester NY 14604-2705 Telephone (585) 232 4000 Facsimile (585) 454 6594 Report of Independent Auditors To the Board of Trustees

Financial Statements. August 31, 2013 and 2012. (With Independent Auditors Report Thereon)

") Financial Statements (With Independent Auditors Report Thereon) Table of Contents Page Independent Auditors Report 1 Statements of Financial Position 2 Statement of Activities Year ended August 31, 2013

Financial Statements (With Independent Auditors Report Thereon) Table of Contents Page Independent Auditors Report 1 Statements of Financial Position 2 Statement of Activities Year ended August 31, 2013

XIV. Accounting for Gifts, Endowment Earnings and Other Projects

XIV. Accounting for Gifts, Endowment Earnings and Other Projects A. Overview: RIT receives gifts and other income to support the operations of the University. Gifts that are restricted for use by the donor

XIV. Accounting for Gifts, Endowment Earnings and Other Projects A. Overview: RIT receives gifts and other income to support the operations of the University. Gifts that are restricted for use by the donor

United Cerebral Palsy, Inc. Financial Report September 30, 2013

Financial Report September 30, 2013 Contents Independent Auditor s Report 1 2 Financial Statements Statement Of Financial Position 3 Statement Of Activities 4 Statement Of Functional Expenses 5 Statement

Financial Report September 30, 2013 Contents Independent Auditor s Report 1 2 Financial Statements Statement Of Financial Position 3 Statement Of Activities 4 Statement Of Functional Expenses 5 Statement

MULTNOMAH BIBLE COLLEGE AND SEMINARY INDEPENDENT AUDITOR S REPORT AND FINANCIAL STATEMENTS

MULTNOMAH BIBLE COLLEGE AND SEMINARY INDEPENDENT AUDITOR S REPORT AND FINANCIAL STATEMENTS JUNE 30, 2007 AND 2006 CONTENTS PAGE INDEPENDENT AUDITOR S REPORT 1 FINANCIAL STATEMENTS Statements of financial

MULTNOMAH BIBLE COLLEGE AND SEMINARY INDEPENDENT AUDITOR S REPORT AND FINANCIAL STATEMENTS JUNE 30, 2007 AND 2006 CONTENTS PAGE INDEPENDENT AUDITOR S REPORT 1 FINANCIAL STATEMENTS Statements of financial

University of Central Florida Foundation, Inc. (A Discrete Component Unit of the University of Central Florida) Financial Report June 30, 2014

Financial Report June 30, 2014") University of Central Florida Foundation, Inc. (A Discrete Component Unit of the University of Central Florida) Financial Report June 30, 2014 Contents Independent Auditor s Report 1 Management s Discussion

University of Central Florida Foundation, Inc. (A Discrete Component Unit of the University of Central Florida) Financial Report June 30, 2014 Contents Independent Auditor s Report 1 Management s Discussion

The Students Union, The University of Calgary. Financial Statements June 30, 2014

The Students Union, The University of Calgary Financial Statements June 30, November 18, Independent Auditor s Report To the Members of The Students Union, The University of Calgary We have audited the

The Students Union, The University of Calgary Financial Statements June 30, November 18, Independent Auditor s Report To the Members of The Students Union, The University of Calgary We have audited the

SAMPLE AUDITOR S OPINION LETTER

SAMPLE AUDITOR S OPINION LETTER INDEPENDENT AUDITORS REPORT To the Board of Directors XYZ Organization Washington, D.C. We have audited the accompanying statement of financial position of XYZ Organization

SAMPLE AUDITOR S OPINION LETTER INDEPENDENT AUDITORS REPORT To the Board of Directors XYZ Organization Washington, D.C. We have audited the accompanying statement of financial position of XYZ Organization

Governmental Accounting

Governmental Accounting 1 Beginning At the turn of the century governments began to establish separate cash accounts to manage dedicated resources. These separate cash accounts gradually evolved into the

Governmental Accounting 1 Beginning At the turn of the century governments began to establish separate cash accounts to manage dedicated resources. These separate cash accounts gradually evolved into the

Christian Children s Fund of Canada. Financial Statements March 31, 2015

Christian Children s Fund of Canada Financial Statements Index to Financial Statements Page INDEPENDENT AUDITOR S REPORT 1-2 STATEMENT OF FINANCIAL POSITION 3 STATEMENT OF OPERATIONS 4 STATEMENT OF CHANGES

Christian Children s Fund of Canada Financial Statements Index to Financial Statements Page INDEPENDENT AUDITOR S REPORT 1-2 STATEMENT OF FINANCIAL POSITION 3 STATEMENT OF OPERATIONS 4 STATEMENT OF CHANGES

Accounting for Colleges & Universities. Chapter 17

Accounting for Colleges & Universities Chapter 17 Learning Objectives Understand why most government C&Us choose to report as business-type only special purpose governments Explain unique aspects of C&U

Accounting for Colleges & Universities Chapter 17 Learning Objectives Understand why most government C&Us choose to report as business-type only special purpose governments Explain unique aspects of C&U

SeriousFun Children's Network, Inc. and Subsidiaries

SeriousFun Children's Network, Inc. and Subsidiaries Consolidated Financial Statements and Independent Auditor's Report (With Supplementary Information) December 31, 2015 and 2014 Index Page Independent

SeriousFun Children's Network, Inc. and Subsidiaries Consolidated Financial Statements and Independent Auditor's Report (With Supplementary Information) December 31, 2015 and 2014 Index Page Independent

Department of Health & Human Services Recommended Chart-of-Accounts Smart Start - Local Partnerships

Department of Health & Human Services Recommended Chart-of-Accounts Smart Start - Local Partnerships Account Classes Funds Control Accounts 1XXXXXXX Unrestricted 2XXXXXXX Temporarily Restricted 3XXXXXXX

Department of Health & Human Services Recommended Chart-of-Accounts Smart Start - Local Partnerships Account Classes Funds Control Accounts 1XXXXXXX Unrestricted 2XXXXXXX Temporarily Restricted 3XXXXXXX

UNIVERSITY OF VICTORIA FOUNDATION FINANCIAL STATEMENTS MARCH 31, 2015. Statement of Administrative Responsibility for Financial Statements 2

UNIVERSITY OF VICTORIA FOUNDATION FINANCIAL STATEMENTS MARCH 31, 2015 Page Statement of Administrative Responsibility for Financial Statements 2 Independent Auditors' Report 3 Statement of Financial Position

UNIVERSITY OF VICTORIA FOUNDATION FINANCIAL STATEMENTS MARCH 31, 2015 Page Statement of Administrative Responsibility for Financial Statements 2 Independent Auditors' Report 3 Statement of Financial Position

Halton Women's Place Financial Statements For the year ended March 31, 2014

Financial Statements For the year ended March 31, 2014 Contents Page Independent Auditors' Report Financial Statements Statement of Financial Position 1 Statement of Changes in Net Assets 2 Statement of

Financial Statements For the year ended March 31, 2014 Contents Page Independent Auditors' Report Financial Statements Statement of Financial Position 1 Statement of Changes in Net Assets 2 Statement of

SOS CHILDREN S VILLAGES USA, INC.

FINANCIAL STATEMENTS AND REPORT OF INDEPENDENT CERTIFIED PUBLIC ACCOUNTANTS DECEMBER 31, 2014 AND 2013 TABLE OF CONTENTS REPORT OF INDEPENDENT CERTIFIED PUBLIC ACCOUNTANTS 1-2 Page FINANCIAL STATEMENTS

FINANCIAL STATEMENTS AND REPORT OF INDEPENDENT CERTIFIED PUBLIC ACCOUNTANTS DECEMBER 31, 2014 AND 2013 TABLE OF CONTENTS REPORT OF INDEPENDENT CERTIFIED PUBLIC ACCOUNTANTS 1-2 Page FINANCIAL STATEMENTS

SOS CHILDREN S VILLAGES USA, INC.

FINANCIAL STATEMENTS AND REPORT OF INDEPENDENT CERTIFIED PUBLIC ACCOUNTANTS DECEMBER 31, 2015 AND 2014 TABLE OF CONTENTS REPORT OF INDEPENDENT CERTIFIED PUBLIC ACCOUNTANTS 1-2 Page FINANCIAL STATEMENTS

FINANCIAL STATEMENTS AND REPORT OF INDEPENDENT CERTIFIED PUBLIC ACCOUNTANTS DECEMBER 31, 2015 AND 2014 TABLE OF CONTENTS REPORT OF INDEPENDENT CERTIFIED PUBLIC ACCOUNTANTS 1-2 Page FINANCIAL STATEMENTS

FIRST UNITED METHODIST CHURCH OF FORT WORTH

FIRST UNITED METHODIST CHURCH OF FORT WORTH Fort Worth, Texas Consolidated Financial Statements Years Ended December 31, 2012 and 2011 Consolidated Financial Statements Years Ended December 31, 2012 and

FIRST UNITED METHODIST CHURCH OF FORT WORTH Fort Worth, Texas Consolidated Financial Statements Years Ended December 31, 2012 and 2011 Consolidated Financial Statements Years Ended December 31, 2012 and

NATIONAL LEADERSHIP ROUNDTABLE ON CHURCH MANAGEMENT

WWW.MCB-CPA.COM INDEX Page Independent Auditors Report 1 Financial Statements: Statement of Financial Position 2 Statement of Activities 3 Statement of Functional Expenses 4 Statement of Cash Flows 5 Notes

WWW.MCB-CPA.COM INDEX Page Independent Auditors Report 1 Financial Statements: Statement of Financial Position 2 Statement of Activities 3 Statement of Functional Expenses 4 Statement of Cash Flows 5 Notes

JAMES A. MICHENER ART MUSEUM

FINANCIAL STATEMENTS YEAR ENDED DECEMBER 31, 2010 CONTENTS INDEPENDENT AUDITOR'S REPORT 1 FINANCIAL STATEMENTS Statement of Financial Position 2 Statement of Activities 3 Statement of Functional Expenses

FINANCIAL STATEMENTS YEAR ENDED DECEMBER 31, 2010 CONTENTS INDEPENDENT AUDITOR'S REPORT 1 FINANCIAL STATEMENTS Statement of Financial Position 2 Statement of Activities 3 Statement of Functional Expenses

Foundation for Canadian Parks and Wilderness

Foundation for Canadian Parks and Wilderness Financial Statements For the years ended March 31, 2008 and 2007 Financial Statements For the years ended March 31, 2008 and 2007 Contents Auditors' Report

Foundation for Canadian Parks and Wilderness Financial Statements For the years ended March 31, 2008 and 2007 Financial Statements For the years ended March 31, 2008 and 2007 Contents Auditors' Report

Cerebral Palsy of Westchester, Inc. Financial Statements (Together with Independent Auditors Report)

") Cerebral Palsy of Westchester, Inc. Financial Statements (Together with Independent Auditors Report) Years Ended December 31, 2015 and 2014 FINANCIAL STATEMENTS (Together with Independent Auditors Report)

Cerebral Palsy of Westchester, Inc. Financial Statements (Together with Independent Auditors Report) Years Ended December 31, 2015 and 2014 FINANCIAL STATEMENTS (Together with Independent Auditors Report)

Centre for Addiction and Mental Health. Financial Statements March 31, 2014

Centre for Addiction and Mental Health Financial Statements June 4, Independent Auditor s Report To the Trustees of Centre for Addiction and Mental Health We have audited the accompanying financial statements

Centre for Addiction and Mental Health Financial Statements June 4, Independent Auditor s Report To the Trustees of Centre for Addiction and Mental Health We have audited the accompanying financial statements

DALLAS MISSION FOR LIFE d.b.a. DALLAS LIFE

FINANCIAL STATEMENTS With Independent Auditors Report Table of Contents Independent Auditors Report 1 Financial Statements Statement of Financial Position 3 Statement of Activities 4 Statement of Cash

FINANCIAL STATEMENTS With Independent Auditors Report Table of Contents Independent Auditors Report 1 Financial Statements Statement of Financial Position 3 Statement of Activities 4 Statement of Cash

Charities Review Council Financial Session. Barbara Clare MAP for Nonprofits Chief Financial Officer bclare@mapfornonprofits.org

Charities Review Council Financial Session Barbara Clare MAP for Nonprofits Chief Financial Officer bclare@mapfornonprofits.org Session Objectives Review and understanding of basic financial statement

Charities Review Council Financial Session Barbara Clare MAP for Nonprofits Chief Financial Officer bclare@mapfornonprofits.org Session Objectives Review and understanding of basic financial statement

BIRD STUDIES CANADA/ ÉTUDES D OISEAUX CANADA

Financial Statements of BIRD STUDIES CANADA/ ÉTUDES D OISEAUX CANADA KPMG LLP Telephone 519-747-8800 115 King Street South Fax 519-747-8830 2 nd Floor Internet www.kpmg.ca Waterloo ON N2J 5A3 INDEPENDENT

Financial Statements of BIRD STUDIES CANADA/ ÉTUDES D OISEAUX CANADA KPMG LLP Telephone 519-747-8800 115 King Street South Fax 519-747-8830 2 nd Floor Internet www.kpmg.ca Waterloo ON N2J 5A3 INDEPENDENT

Orange County s United Way

Financial Statements Years Ended June 30, 2015 and 2014 The report accompanying these financial statements was issued by BDO USA, LLP, a Delaware limited liability partnership and the U.S. member of BDO

Financial Statements Years Ended June 30, 2015 and 2014 The report accompanying these financial statements was issued by BDO USA, LLP, a Delaware limited liability partnership and the U.S. member of BDO

Jewish Community Foundation of San Diego. Consolidated Financial Statements and Supplemental Information

Jewish Community Foundation of San Diego Consolidated Financial Statements and Supplemental Information Years Ended June 30, 2015 and 2014 Consolidated Financial Statements and Supplemental Information

Jewish Community Foundation of San Diego Consolidated Financial Statements and Supplemental Information Years Ended June 30, 2015 and 2014 Consolidated Financial Statements and Supplemental Information

MANITOBA DENTAL ASSISTANTS ASSOCIATION Financial Statements December 31, 2011

Financial Statements December 31, 2011 December 4, 2012 INDEPENDENT AUDITORS' REPORT To the Directors of Manitoba Dental Assistants Association We have audited the accompanying financial statements of

Financial Statements December 31, 2011 December 4, 2012 INDEPENDENT AUDITORS' REPORT To the Directors of Manitoba Dental Assistants Association We have audited the accompanying financial statements of

National Safety Council. Consolidated Financial Report June 30, 2014 and 2013

Consolidated Financial Report June 30, 2014 and 2013 Contents Independent Auditor s Report 1 2 Financial Statements Consolidated statements of financial position 3 Consolidated statements of activities

Consolidated Financial Report June 30, 2014 and 2013 Contents Independent Auditor s Report 1 2 Financial Statements Consolidated statements of financial position 3 Consolidated statements of activities

Cincinnati Public Radio, Inc. and Subsidiary

Cincinnati Public Radio, Inc. and Subsidiary Consolidated Financial Statements with Accompanying Information June 30, 2013, with Summarized Comparative Totals for June 30, 2012, and Independent Auditors

Cincinnati Public Radio, Inc. and Subsidiary Consolidated Financial Statements with Accompanying Information June 30, 2013, with Summarized Comparative Totals for June 30, 2012, and Independent Auditors

CANADIAN GAAP IFRS COMPARISON SERIES

WWW.BDO.CA ASSURANCE AND ACCOUNTING CANADIAN GAAP IFRS COMPARISON SERIES Issue 13: Income Taxes Both IFRS and Canadian GAAP are principle based frameworks and, from a conceptual standpoint, many of the

WWW.BDO.CA ASSURANCE AND ACCOUNTING CANADIAN GAAP IFRS COMPARISON SERIES Issue 13: Income Taxes Both IFRS and Canadian GAAP are principle based frameworks and, from a conceptual standpoint, many of the

American Society for Eighteenth Century Studies

Lid Report on Financial Statements Contents Page Independent Auditor's Report 1-2 Financial Statements Statement of Assets, Liabilities and Net Assets - Modified Cash Basis 3 Statement of Revenues, Support,

Lid Report on Financial Statements Contents Page Independent Auditor's Report 1-2 Financial Statements Statement of Assets, Liabilities and Net Assets - Modified Cash Basis 3 Statement of Revenues, Support,

Financial Statements Together with Report of Independent Certified Public Accountants FJC. March 31, 2015 and 2014

Financial Statements Together with Report of Independent Certified Public Accountants FJC TABLE OF CONTENTS Page Report of Independent Certified Public Accountants 1-2 Financial Statements Statements of

Financial Statements Together with Report of Independent Certified Public Accountants FJC TABLE OF CONTENTS Page Report of Independent Certified Public Accountants 1-2 Financial Statements Statements of

25. Introduction to School Accounting

Financial and Education Law Training Program Page 25-1 25. Background and Introduction During the early years of American education, financial records were not extensive because local school systems were

Financial and Education Law Training Program Page 25-1 25. Background and Introduction During the early years of American education, financial records were not extensive because local school systems were

College of Physicians and Surgeons of British Columbia

Financial Statements OF College of Physicians and Surgeons of British Columbia FEBRUARY 29, 2012 Table of contents Independent Auditor s Report... 1 Statement of operations... 2 Statement of changes in

Financial Statements OF College of Physicians and Surgeons of British Columbia FEBRUARY 29, 2012 Table of contents Independent Auditor s Report... 1 Statement of operations... 2 Statement of changes in

METROPOLITAN COMMUNITY CHURCH OF TORONTO FINANCIAL STATEMENTS DECEMBER 31, 2013

FINANCIAL STATEMENTS CONTENTS Page INDEPENDENT AUDITOR'S REPORT 1-2 FINANCIAL STATEMENTS Statement of Financial Position 3 Statement of Operations 4 Statement of Changes in Net Assets 5 Statement of Cash

FINANCIAL STATEMENTS CONTENTS Page INDEPENDENT AUDITOR'S REPORT 1-2 FINANCIAL STATEMENTS Statement of Financial Position 3 Statement of Operations 4 Statement of Changes in Net Assets 5 Statement of Cash

Financial statements. Standardbred Canada (Incorporated under the Animal Pedigree Act) October 31, 2012

October 31, 2012") Financial statements Standardbred Canada (Incorporated under the Animal Pedigree Act) (Incorporated under the Animal Pedigree Act) Contents Page Independent Auditors Report 1-2 Statement of operations

Financial statements Standardbred Canada (Incorporated under the Animal Pedigree Act) (Incorporated under the Animal Pedigree Act) Contents Page Independent Auditors Report 1-2 Statement of operations

FLORIDA HIGH SCHOOL FOR ACCELERATED LEARNING - WEST PALM BEACH CAMPUS, INC. d/b/a QUANTUM HIGH SCHOOL

LEARNING - WEST PALM BEACH CAMPUS, INC. Financial Statements with Independent Auditors Reports Thereon June 30, 2015 CONTENTS Page Management s Discussion and Analysis 1 6 Report of Independent Auditors

LEARNING - WEST PALM BEACH CAMPUS, INC. Financial Statements with Independent Auditors Reports Thereon June 30, 2015 CONTENTS Page Management s Discussion and Analysis 1 6 Report of Independent Auditors

CURE INTERNATIONAL, INC.

FINANCIAL STATEMENTS AND REPORT OF INDEPENDENT CERTIFIED PUBLIC ACCOUNTANTS JUNE 30, 2015 TABLE OF CONTENTS REPORT OF INDEPENDENT CERTIFIED PUBLIC ACCOUNTANTS 1-2 Page FINANCIAL STATEMENTS Statements of

FINANCIAL STATEMENTS AND REPORT OF INDEPENDENT CERTIFIED PUBLIC ACCOUNTANTS JUNE 30, 2015 TABLE OF CONTENTS REPORT OF INDEPENDENT CERTIFIED PUBLIC ACCOUNTANTS 1-2 Page FINANCIAL STATEMENTS Statements of

The Wood s Homes Foundation. Financial Statements December 31, 2014

Financial Statements April 22, 2015 Independent Auditor s Report To the Board of Directors of Wood s Homes Foundation We have audited the accompanying financial statements of Wood s Homes Foundation, which

Financial Statements April 22, 2015 Independent Auditor s Report To the Board of Directors of Wood s Homes Foundation We have audited the accompanying financial statements of Wood s Homes Foundation, which

University of Central Florida Foundation, Inc. (A Discrete Component Unit of the University of Central Florida)

") University of Central Florida Foundation, Inc. (A Discrete Component Unit of the University of Central Florida) Single Audit Report Year Ended June 30, 2015 Contents Independent Auditor s Report 1 Management

University of Central Florida Foundation, Inc. (A Discrete Component Unit of the University of Central Florida) Single Audit Report Year Ended June 30, 2015 Contents Independent Auditor s Report 1 Management

ALAMO COLLEGES FOUNDATION, INC. (A Texas nonprofit Foundation) AUDITED FINANCIAL STATEMENTS. Year Ended December 31, 2012

AUDITED FINANCIAL STATEMENTS. Year Ended December 31, 2012") R. D. Harrison, CPA Certified Public Accountant Member American Institute of Certified Public Accountants Registered with the Public Company Accounting Oversight Board ALAMO COLLEGES FOUNDATION, INC. AUDITED

R. D. Harrison, CPA Certified Public Accountant Member American Institute of Certified Public Accountants Registered with the Public Company Accounting Oversight Board ALAMO COLLEGES FOUNDATION, INC. AUDITED

Accounting and Reporting for Public Colleges and Universities. Objectives

Accounting and Reporting for Public Colleges and Universities 2012-2013 NACUBO Intermediate Accounting Objectives Upon completion of these materials, you will be able to Comprehend the reporting and recognition

Accounting and Reporting for Public Colleges and Universities 2012-2013 NACUBO Intermediate Accounting Objectives Upon completion of these materials, you will be able to Comprehend the reporting and recognition

ST. CLOUD PREPARATORY ACADEMY, INC. Basic Financial Statements and Supplemental Information. For the year ended June 30, 2015

ST. CLOUD PREPARATORY ACADEMY, INC. Basic Financial Statements and Supplemental Information For the year ended June 30, 2015 TABLE OF CONTENTS INDEPENDENT AUDITORS REPORT 1-2 MANAGEMENT S DISCUSSION AND

ST. CLOUD PREPARATORY ACADEMY, INC. Basic Financial Statements and Supplemental Information For the year ended June 30, 2015 TABLE OF CONTENTS INDEPENDENT AUDITORS REPORT 1-2 MANAGEMENT S DISCUSSION AND

Case Western Reserve University Consolidated Financial Statements for the Year Ending June 30, 2001

Contents Report of Independent Accountants 1 Part 1 Consolidated Financial Statements Consolidated Balance Sheet 2 Consolidated Statement of Activities 3 Consolidated Statement of Cash Flows 4 Part 2 Summary

Contents Report of Independent Accountants 1 Part 1 Consolidated Financial Statements Consolidated Balance Sheet 2 Consolidated Statement of Activities 3 Consolidated Statement of Cash Flows 4 Part 2 Summary

SeaChange Capital Partners, Inc. Financial Statements. December 31, 2014 and 2013

Financial Statements Board of Directors SeaChange Capital Partners, Inc. Independent Auditors Report We have audited the accompanying financial statements of SeaChange Capital Partners, Inc. (SeaChange),

Financial Statements Board of Directors SeaChange Capital Partners, Inc. Independent Auditors Report We have audited the accompanying financial statements of SeaChange Capital Partners, Inc. (SeaChange),

Financial Statements of. Canadian Cancer Society, Saskatchewan Division. Year ended January 31, 2015

Financial Statements of Canadian Cancer Society, Saskatchewan Division Independent Auditor s report To the Board of Directors of the Canadian Cancer Society, Saskatchewan Division We have audited the accompanying

Financial Statements of Canadian Cancer Society, Saskatchewan Division Independent Auditor s report To the Board of Directors of the Canadian Cancer Society, Saskatchewan Division We have audited the accompanying

California Fire Foundation Financial Statements December 31, 2013 and 2012

Financial Statements Financial Statements Contents INDEPENDENT AUDITORS' REPORT...1 FINANCIAL STATEMENTS Statement of Financial Position...2 Statement of Activities...3 Statements of Functional Expenses...4

Financial Statements Financial Statements Contents INDEPENDENT AUDITORS' REPORT...1 FINANCIAL STATEMENTS Statement of Financial Position...2 Statement of Activities...3 Statements of Functional Expenses...4

The Children's Museum of Memphis, Inc. Financial Statements June 30, 2015 and 2014

The Children's Museum of Memphis, Inc. Financial Statements June 30, 2015 and 2014 Table of Contents June 30, 2015 and 2014 Page Independent Auditor s Report... 3 Financial Statements Statements of Financial

The Children's Museum of Memphis, Inc. Financial Statements June 30, 2015 and 2014 Table of Contents June 30, 2015 and 2014 Page Independent Auditor s Report... 3 Financial Statements Statements of Financial

Statement of Principles

Statement of Principles Improvements to Not-for-Profit Standards (Applicable to Private and Public Sector Not-for-Profit Organizations that Use the Not-for-Profit Standards as their Primary Source of GAAP)

Statement of Principles Improvements to Not-for-Profit Standards (Applicable to Private and Public Sector Not-for-Profit Organizations that Use the Not-for-Profit Standards as their Primary Source of GAAP)

UNIVERSITY OF DENVER (COLORADO SEMINARY) Financial Statements and OMB A-133 Single Audit Reports. June 30, 2015 and 2014

Financial Statements and OMB A-133 Single Audit Reports. June 30, 2015 and 2014") Financial Statements and OMB A-133 Single Audit Reports June 30, 2015 and 2014 (With Independent Auditors Report Thereon) Table of Contents Independent Auditors Report 1 Financial Statements Statement

Financial Statements and OMB A-133 Single Audit Reports June 30, 2015 and 2014 (With Independent Auditors Report Thereon) Table of Contents Independent Auditors Report 1 Financial Statements Statement

Notes to Financial Statements - Summary of Significant Accounting Policies (1)

") Audited Financial Statements June 30, 2011 and 2010 Contents Independent Auditors' Report... 1 Financial Statements: Statements of Financial Position... 2 Statement of Activities... 3 Statement of Cash

Audited Financial Statements June 30, 2011 and 2010 Contents Independent Auditors' Report... 1 Financial Statements: Statements of Financial Position... 2 Statement of Activities... 3 Statement of Cash

SIERRA PACIFIC SYNOD OF THE EVANGELICAL LUTHERAN CHURCH IN AMERICA FINANCIAL STATEMENTS WITH INDEPENDENT AUDITOR S REPORT

SIERRA PACIFIC SYNOD OF THE EVANGELICAL LUTHERAN CHURCH IN AMERICA FINANCIAL STATEMENTS WITH INDEPENDENT AUDITOR S REPORT YEARS ENDED SM Relax. We got this. Relax. Relax. We got We this. got this. INDEPENDENT

SIERRA PACIFIC SYNOD OF THE EVANGELICAL LUTHERAN CHURCH IN AMERICA FINANCIAL STATEMENTS WITH INDEPENDENT AUDITOR S REPORT YEARS ENDED SM Relax. We got this. Relax. Relax. We got We this. got this. INDEPENDENT

University of South Florida System and DSO/Component Unit Quarterly Financial Reports QUARTER 3 FOR FISCAL YEAR 2014-2015

University of South Florida System and DSO/Component Unit Quarterly Financial Reports QUARTER 3 FOR FISCAL YEAR 2014-2015 Period Ended March 31, 2015 FY 2015 QUARTER 3 REPORT MARCH 31, 2015 INDEX University

University of South Florida System and DSO/Component Unit Quarterly Financial Reports QUARTER 3 FOR FISCAL YEAR 2014-2015 Period Ended March 31, 2015 FY 2015 QUARTER 3 REPORT MARCH 31, 2015 INDEX University

Consolidated Financial Statements Milton Academy

Consolidated Financial Statements Milton Academy June 30, 2011 and 2010 Consolidated Financial Statements Table of Contents Consolidated Financial Statements: Independent Auditors Report 1 Consolidated

Consolidated Financial Statements Milton Academy June 30, 2011 and 2010 Consolidated Financial Statements Table of Contents Consolidated Financial Statements: Independent Auditors Report 1 Consolidated

Boston College Financial Statements May 31, 2007 and 2006

Financial Statements Index Page(s) Report of Independent Auditors... 1 Financial Statements Statement of Financial Position... 2 Statement of Activities... 3 Statement of Cash Flows... 4...5-15 PricewaterhouseCoopers

Financial Statements Index Page(s) Report of Independent Auditors... 1 Financial Statements Statement of Financial Position... 2 Statement of Activities... 3 Statement of Cash Flows... 4...5-15 PricewaterhouseCoopers

TOPIC ACCOUNTING PRINCIPLES SUB-SECTION 03.00.00 SUB-SECTION INDEX REVISION NUMBER 99-004

Page 1 of 1 TOPIC ACCOUNTING PRINCIPLES SUB-SECTION 03.00.00 SECTION ISSUANCE DATE JUNE 30, 1999 SUB-SECTION INDEX REVISION NUMBER 99-004 03 Accounting Principles 10 Organization Structure of State Government

Page 1 of 1 TOPIC ACCOUNTING PRINCIPLES SUB-SECTION 03.00.00 SECTION ISSUANCE DATE JUNE 30, 1999 SUB-SECTION INDEX REVISION NUMBER 99-004 03 Accounting Principles 10 Organization Structure of State Government

CAPE BRETON BUSINESS PARTNERSHIP INC.

Financial Statements of CAPE BRETON BUSINESS PARTNERSHIP INC. INDEPENDENT AUDITORS' REPORT To the Directors of Cape Breton Business Partnership Inc. We have audited the accompanying financial statements

Financial Statements of CAPE BRETON BUSINESS PARTNERSHIP INC. INDEPENDENT AUDITORS' REPORT To the Directors of Cape Breton Business Partnership Inc. We have audited the accompanying financial statements

MONTCLAIR STATE UNIVERSITY FOUNDATION, INC. JUNE 30, 2012 AND 2011 INDEPENDENT AUDITOR S REPORT

FINANCIAL STATEMENTS JUNE 30, 2012 AND 2011 AND INDEPENDENT AUDITOR S REPORT FINANCIAL STATEMENTS JUNE 30, 2012 AND 2011 TABLE OF CONTENTS Pages Independent Auditor s Report 3 Financial Statements: Statements

FINANCIAL STATEMENTS JUNE 30, 2012 AND 2011 AND INDEPENDENT AUDITOR S REPORT FINANCIAL STATEMENTS JUNE 30, 2012 AND 2011 TABLE OF CONTENTS Pages Independent Auditor s Report 3 Financial Statements: Statements

85.52 Investments. 85.52.10 July 1, 2003. About investments. Short-term investments. 85.52.20 June 1, 2003 85.52.10

85.52.10 85.52 Investments 85.52.10 July 1, 2003 About investments Investments are made as authorized by law and/or contractual agreement. Investment purchase and sale transactions are to be reported for

85.52.10 85.52 Investments 85.52.10 July 1, 2003 About investments Investments are made as authorized by law and/or contractual agreement. Investment purchase and sale transactions are to be reported for

Accounting Policies & Procedures Manual

Accounting Policies & Procedures Manual Updated and Approved: 1 CAWST Accounting Policies & Procedures Index 1. Accounting Policies APL100 Financial statement concepts and accountability APL210 Cash and

Accounting Policies & Procedures Manual Updated and Approved: 1 CAWST Accounting Policies & Procedures Index 1. Accounting Policies APL100 Financial statement concepts and accountability APL210 Cash and

Pensacola Habitat For Humanity, Inc. Pensacola, Florida. Audited Financial Statements. With Supplementary Information

Pensacola, Florida Audited Financial Statements With Supplementary Information June 30, 2014 Pensacola, Florida Audited Financial Statements With Supplementary Information June 30, 2014 CONTENTS PAGE Independent

Pensacola, Florida Audited Financial Statements With Supplementary Information June 30, 2014 Pensacola, Florida Audited Financial Statements With Supplementary Information June 30, 2014 CONTENTS PAGE Independent

A Review of Bill Sansum Diabetes Center, 2014

WILLIAM SANSUM DIABETES CENTER FINANCIAL STATEMENTS DECEMBER 31, 2014 WILLIAM SANSUM DIABETES CENTER TABLE OF CONTENTS December 31, 2014 Independent Auditor's Report.. 1-2 Statement of Financial Position......3

WILLIAM SANSUM DIABETES CENTER FINANCIAL STATEMENTS DECEMBER 31, 2014 WILLIAM SANSUM DIABETES CENTER TABLE OF CONTENTS December 31, 2014 Independent Auditor's Report.. 1-2 Statement of Financial Position......3

MEDICAL MINISTRY USA dba MEDICAL MINISTRY INTERNATIONAL

Financial Statements Together with Independent Auditors Report For the Year Ended SWALM & ASSOCIATES, P.C. Certified Public Accountants FINANCIAL STATEMENTS Table of Contents Page Independent Auditors

Financial Statements Together with Independent Auditors Report For the Year Ended SWALM & ASSOCIATES, P.C. Certified Public Accountants FINANCIAL STATEMENTS Table of Contents Page Independent Auditors

THE ASPEN EDUCATION FOUNDATION FINANCIAL STATEMENTS. June 30, 2013

FINANCIAL STATEMENTS June 30, 2013 FINANCIAL STATEMENTS June 30, 2013 TABLE OF CONTENTS ITEM PAGE NUMBER Independent Auditor s Report 1 Statement of Financial Position 2 Statement of Activities 3 Statement

FINANCIAL STATEMENTS June 30, 2013 FINANCIAL STATEMENTS June 30, 2013 TABLE OF CONTENTS ITEM PAGE NUMBER Independent Auditor s Report 1 Statement of Financial Position 2 Statement of Activities 3 Statement

Summary Comparison of Canadian Public Sector Accounting Standards

February 2011 Summary Comparison of Canadian Public Sector Accounting Standards With th e CI CA Han dboo k Part V www.bcauditor.com Location: 8 Bastion Square Victoria, British Columbia V8V 1X4 Office

February 2011 Summary Comparison of Canadian Public Sector Accounting Standards With th e CI CA Han dboo k Part V www.bcauditor.com Location: 8 Bastion Square Victoria, British Columbia V8V 1X4 Office

Northeastern University Consolidated Financial Statements June 30, 2011 and 2010

Consolidated Financial Statements Index Page(s) Report of Independent Auditors... 1 Consolidated Financial Statements Consolidated Statements of Financial Position... 2 Consolidated Statement of Activities...

Consolidated Financial Statements Index Page(s) Report of Independent Auditors... 1 Consolidated Financial Statements Consolidated Statements of Financial Position... 2 Consolidated Statement of Activities...

BENEVOLENT HEALTHCARE FOUNDATION DBA PROJECT C.U.R.E. FINANCIAL STATEMENTS MAY 31, 2014

BENEVOLENT HEALTHCARE FOUNDATION DBA PROJECT C.U.R.E. FINANCIAL STATEMENTS MAY 31, 2014 C O N T E N T S Independent Auditors Report 2-3 Statements of Financial Position 4 Statements of Activities 5 Statements

BENEVOLENT HEALTHCARE FOUNDATION DBA PROJECT C.U.R.E. FINANCIAL STATEMENTS MAY 31, 2014 C O N T E N T S Independent Auditors Report 2-3 Statements of Financial Position 4 Statements of Activities 5 Statements

Texas Department of Assistive and Rehabilitative Services (538) - Unaudited

- Unaudited") Note 1: Summary of Significant Accounting Policies Entity The Texas Department of Assistive and Rehabilitative Services ( DARS ) is an agency of the State of Texas and its financial records comply with

Note 1: Summary of Significant Accounting Policies Entity The Texas Department of Assistive and Rehabilitative Services ( DARS ) is an agency of the State of Texas and its financial records comply with

THE UNIVERSITY OF NORTH FLORIDA FOUNDATION, INC. Financial Statements and Supplementary Information. June 30, 2004 and 2003

Financial Statements and Supplementary Information June 30, 2004 and 2003 (With Independent Auditors Report Thereon) Table of Contents Independent Auditors Report 1-2 Required Supplementary Information:

Financial Statements and Supplementary Information June 30, 2004 and 2003 (With Independent Auditors Report Thereon) Table of Contents Independent Auditors Report 1-2 Required Supplementary Information:

Galapagos Conservancy. Financial Report March 31, 2013

Financial Report March 31, 2013 Contents Independent Auditor s Report 1 Financial Statements Balance Sheet 2 Statement Of Activities 3 Statement Of Functional Expenses 4 Statement Of Cash Flows 5 Notes

Financial Report March 31, 2013 Contents Independent Auditor s Report 1 Financial Statements Balance Sheet 2 Statement Of Activities 3 Statement Of Functional Expenses 4 Statement Of Cash Flows 5 Notes

SunGard Brokerage & Securities Services, LLC Unaudited Statement of Financial Condition June 30, 2013

Unaudited Statement of Financial Condition Index Page(s) Financial Statements Statement of Financial Condition... 3 Notes to the Financial Statements... 4 9 Statement of Financial Condition Assets Note(s)

Unaudited Statement of Financial Condition Index Page(s) Financial Statements Statement of Financial Condition... 3 Notes to the Financial Statements... 4 9 Statement of Financial Condition Assets Note(s)

Consolidated Financial Statements

Consolidated Financial Statements For the Year Ended April 30, 2009 U N I V E R S I T Y O F S A S K A T C H E W A N 1 2008/09 Annual Report Statement of Administrative Responsibility for Financial Reporting

Consolidated Financial Statements For the Year Ended April 30, 2009 U N I V E R S I T Y O F S A S K A T C H E W A N 1 2008/09 Annual Report Statement of Administrative Responsibility for Financial Reporting

Vassar College Financial Statements June 30, 2013 and 2012

Financial Statements Index Page(s) Independent Auditor s Report...1 Financial Statements Statements of Financial Position...2 Statements of Activities...3-4 Statements of Cash Flows...5...6 27 To the Board

Financial Statements Index Page(s) Independent Auditor s Report...1 Financial Statements Statements of Financial Position...2 Statements of Activities...3-4 Statements of Cash Flows...5...6 27 To the Board

VANCOUVER COMMUNITY COLLEGE

Financial Statements of VANCOUVER COMMUNITY COLLEGE KPMG Enterprise Metrotower II 4720 Kingsway, Suite 2400 Burnaby, BC V5H 4N2 Canada Telephone (604) 527-3600 Fax (604) 527-3636 Internet www.kpmg.ca/enterprise

Financial Statements of VANCOUVER COMMUNITY COLLEGE KPMG Enterprise Metrotower II 4720 Kingsway, Suite 2400 Burnaby, BC V5H 4N2 Canada Telephone (604) 527-3600 Fax (604) 527-3636 Internet www.kpmg.ca/enterprise

MARTIN METHODIST COLLEGE FINANCIAL STATEMENTS AND SUPPLEMENTARY INFORMATION JUNE 30, 2011 AND 2010

FINANCIAL STATEMENTS AND SUPPLEMENTARY INFORMATION Table of Contents Page INDEPENDENT AUDITORS REPORT... 1 FINANCIAL STATEMENTS Statements of Financial Position... 2 5 Statements of Activities... 6 9 Statements

FINANCIAL STATEMENTS AND SUPPLEMENTARY INFORMATION Table of Contents Page INDEPENDENT AUDITORS REPORT... 1 FINANCIAL STATEMENTS Statements of Financial Position... 2 5 Statements of Activities... 6 9 Statements

ST. MARTIN'S EPISCOPAL CHURCH

ST. MARTIN'S EPISCOPAL CHURCH FINANCIAL STATEMENTS AND INDEPENDENT AUDITORS' REPORT FOR THE YEARS ENDED DECEMBER 31,2010 (AUDITED) AND DECEMB:ER 31, 2009 (REVIEWED) CONTENTS Page INDEPENDENT AUDITORS'

ST. MARTIN'S EPISCOPAL CHURCH FINANCIAL STATEMENTS AND INDEPENDENT AUDITORS' REPORT FOR THE YEARS ENDED DECEMBER 31,2010 (AUDITED) AND DECEMB:ER 31, 2009 (REVIEWED) CONTENTS Page INDEPENDENT AUDITORS'

CELTIC BUSINESS DEVELOPMENT CORPORATION INC.

Financial Statements of CELTIC BUSINESS DEVELOPMENT CORPORATION INC. YEAR ENDED MARCH 31, 2015 Financial Statements Year ended March 31, 2015 Contents Page Independent Auditor s Report 1. Consolidated

Financial Statements of CELTIC BUSINESS DEVELOPMENT CORPORATION INC. YEAR ENDED MARCH 31, 2015 Financial Statements Year ended March 31, 2015 Contents Page Independent Auditor s Report 1. Consolidated

Financial Statements of RED RIVER COLLEGE. Year ended June 30, 2009

Financial Statements of RED RIVER COLLEGE KPMG LLP Telephone (204) 957-1770 Chartered Accountants Fax (204) 957-0808 Suite 2000 One Lombard Place Internet www.kpmg.ca Winnipeg MB R3B 0X3 Canada AUDITORS'

Financial Statements of RED RIVER COLLEGE KPMG LLP Telephone (204) 957-1770 Chartered Accountants Fax (204) 957-0808 Suite 2000 One Lombard Place Internet www.kpmg.ca Winnipeg MB R3B 0X3 Canada AUDITORS'

Financial Statements. Canadian Baptist Ministries December 31, 2014

Financial Statements Canadian Baptist Ministries INDEPENDENT AUDITORS' REPORT To the Members of Canadian Baptist Ministries We have audited the accompanying financial statements of Canadian Baptist Ministries,

Financial Statements Canadian Baptist Ministries INDEPENDENT AUDITORS' REPORT To the Members of Canadian Baptist Ministries We have audited the accompanying financial statements of Canadian Baptist Ministries,

book 4: financials The Law Foundation Of Ontario

book 4: financials The Law Foundation Of Ontario audited financial statements To The Trustees of The Law Foundation of Ontario We have audited the accompanying financial statements of The Law Foundation

book 4: financials The Law Foundation Of Ontario audited financial statements To The Trustees of The Law Foundation of Ontario We have audited the accompanying financial statements of The Law Foundation

Financial Statements and Supplementary Information of SHERIDAN COLLEGE INSTITUTE OF TECHNOLOGY AND ADVANCED LEARNING

Financial Statements and Supplementary Information of SHERIDAN COLLEGE INSTITUTE OF Year ended March 31, 2014 KPMG LLP Chartered Accountants Box 976 21 King Street West Suite 700 Hamilton ON L8N 3R1 Telephone

Financial Statements and Supplementary Information of SHERIDAN COLLEGE INSTITUTE OF Year ended March 31, 2014 KPMG LLP Chartered Accountants Box 976 21 King Street West Suite 700 Hamilton ON L8N 3R1 Telephone

Lougheed House Conservation Society. (a not-for-profit organization) Financial Statements December 31, 2013

Financial Statements December 31, 2013") Financial Statements Collins Barrow Calgary LLP 1400 First Alberta Place 777 8 th Avenue S.W. Calgary, Alberta, Canada T2P 3R5 Independent Auditors' Report T. 403.298.1500 F. 403.298.5814 e-mail: calgary@collinsbarrow.com

Financial Statements Collins Barrow Calgary LLP 1400 First Alberta Place 777 8 th Avenue S.W. Calgary, Alberta, Canada T2P 3R5 Independent Auditors' Report T. 403.298.1500 F. 403.298.5814 e-mail: calgary@collinsbarrow.com

USING QUICKBOOKS TO RECORD RESTRICTED TRANSACTIONS

USING QUICKBOOKS TO RECORD RESTRICTED TRANSACTIONS Recording Pledges Pledges are unconditional promises that a donor gives to your organization, which could include a promise for money over a period of

USING QUICKBOOKS TO RECORD RESTRICTED TRANSACTIONS Recording Pledges Pledges are unconditional promises that a donor gives to your organization, which could include a promise for money over a period of

NATIONAL COALITION FOR CANCER SURVIVORSHIP, INC. D/B/A CANCER SURVIVORS COALITION FINANCIAL STATEMENTS AND INDEPENDENT AUDITORS' REPORT

FINANCIAL STATEMENTS AND INDEPENDENT AUDITORS' REPORT WWW.MCB-CPA.COM FINANCIAL STATEMENTS TABLE OF CONTENTS Page Independent Auditors Report 1 Financial Statements: Statements of Financial Position 2

FINANCIAL STATEMENTS AND INDEPENDENT AUDITORS' REPORT WWW.MCB-CPA.COM FINANCIAL STATEMENTS TABLE OF CONTENTS Page Independent Auditors Report 1 Financial Statements: Statements of Financial Position 2

NONPROFITS ASSISTANCE FUND FINANCIAL STATEMENTS YEARS ENDED MARCH 31, 2015 AND 2014

FINANCIAL STATEMENTS YEARS ENDED TABLE OF CONTENTS YEARS ENDED INDEPENDENT AUDITORS' REPORT 1 FINANCIAL STATEMENTS STATEMENTS OF FINANCIAL POSITION 3 STATEMENTS OF ACTIVITIES 5 STATEMENTS OF CASH FLOWS

FINANCIAL STATEMENTS YEARS ENDED TABLE OF CONTENTS YEARS ENDED INDEPENDENT AUDITORS' REPORT 1 FINANCIAL STATEMENTS STATEMENTS OF FINANCIAL POSITION 3 STATEMENTS OF ACTIVITIES 5 STATEMENTS OF CASH FLOWS

THE OPEN HEARTH ASSOCIATION, INC. Report on Audit of Financial Statements. December 31, 2011

Report on Audit of Financial Statements December 31, 2011 CONTENTS Independent Auditors Report 1-2 Statements of Financial Position December 31, 2011 and 2010 3 Statements of Activities for the Years Ended

Report on Audit of Financial Statements December 31, 2011 CONTENTS Independent Auditors Report 1-2 Statements of Financial Position December 31, 2011 and 2010 3 Statements of Activities for the Years Ended

CANADIAN BREAST CANCER FOUNDATION

Financial Statements of CANADIAN BREAST CANCER FOUNDATION Table of Contents Independent Auditors' Report Balance Sheet... 1 Statement of Revenue, Expenses and Allocations... 2 Statement of Changes in Fund

Financial Statements of CANADIAN BREAST CANCER FOUNDATION Table of Contents Independent Auditors' Report Balance Sheet... 1 Statement of Revenue, Expenses and Allocations... 2 Statement of Changes in Fund

A Guide to for Financial Instruments in the Public Sector

November 2011 www.bdo.ca Assurance and accounting A Guide to Accounting for Financial Instruments in the Public Sector In June 2011, the Public Sector Accounting Standards Board released Section PS3450,

November 2011 www.bdo.ca Assurance and accounting A Guide to Accounting for Financial Instruments in the Public Sector In June 2011, the Public Sector Accounting Standards Board released Section PS3450,

FINANCIAL STATEMENTS TOGETHER WITH REPORT OF INDEPENDENT CERTIFIED PUBLIC ACCOUNTANTS THE NEW YORK INSTITUTE FOR SPECIAL EDUCATION

FINANCIAL STATEMENTS TOGETHER WITH REPORT OF INDEPENDENT CERTIFIED PUBLIC ACCOUNTANTS THE NEW YORK INSTITUTE FOR SPECIAL EDUCATION C O N T E N T S Page Report of Independent Certified Public Accountants

FINANCIAL STATEMENTS TOGETHER WITH REPORT OF INDEPENDENT CERTIFIED PUBLIC ACCOUNTANTS THE NEW YORK INSTITUTE FOR SPECIAL EDUCATION C O N T E N T S Page Report of Independent Certified Public Accountants

OPEN OPTIONS, INC. d/b/a UNITED CEREBRAL PALSY OF GREATER KANSAS CITY FINANCIAL STATEMENTS. Years Ended June 30, 2014 and 2013

FINANCIAL STATEMENTS Years Ended June 30, 2014 and 2013 STATEMENTS OF FINANCIAL POSITION June 30, 2014 and 2013 A S S E T S 2014 2013 CURRENT ASSETS Cash and cash equivalents $ 761,322 $ 648,987 Investments

FINANCIAL STATEMENTS Years Ended June 30, 2014 and 2013 STATEMENTS OF FINANCIAL POSITION June 30, 2014 and 2013 A S S E T S 2014 2013 CURRENT ASSETS Cash and cash equivalents $ 761,322 $ 648,987 Investments

Non-SLG Not-for-Profit Organizations: SFAS 116 and 117 Approach. Chapter 16

Non-SLG Not-for-Profit Organizations: SFAS 116 and 117 Approach Chapter 16 Learning Objectives Understand the sources of GAAP for nongovernment not-for-profit organizations Explain basis of accounting

Non-SLG Not-for-Profit Organizations: SFAS 116 and 117 Approach Chapter 16 Learning Objectives Understand the sources of GAAP for nongovernment not-for-profit organizations Explain basis of accounting

Financial Statements. Young Women's Christian Association of Greater Toronto December 31, 2014

Financial Statements Young Women's Christian Association of Greater Toronto INDEPENDENT AUDITORS' REPORT To the Members of Young Women's Christian Association of Greater Toronto REPORT ON THE FINANCIAL

Financial Statements Young Women's Christian Association of Greater Toronto INDEPENDENT AUDITORS' REPORT To the Members of Young Women's Christian Association of Greater Toronto REPORT ON THE FINANCIAL

ST. MARY SEMINARY AND GRADUATE SCHOOL OF THEOLOGY (OUR LADY OF THE LAKE) FINANCIAL REPORT. JUNE 30, 2015 and 2014

FINANCIAL REPORT. JUNE 30, 2015 and 2014") ST. MARY SEMINARY AND GRADUATE SCHOOL OF THEOLOGY FINANCIAL REPORT JUNE 30, 2015 and 2014 CONTENTS Page INDEPENDENT AUDITORS' REPORT ON THE FINANCIAL STATEMENTS 1 FINANCIAL STATEMENTS Statements of financial

ST. MARY SEMINARY AND GRADUATE SCHOOL OF THEOLOGY FINANCIAL REPORT JUNE 30, 2015 and 2014 CONTENTS Page INDEPENDENT AUDITORS' REPORT ON THE FINANCIAL STATEMENTS 1 FINANCIAL STATEMENTS Statements of financial

SAMPLE PSAB COLLEGE ILLUSTRATIVE FINANCIAL STATEMENTS FIRST-TIME ADOPTER

SAMPLE PSAB COLLEGE ILLUSTRATIVE FINANCIAL STATEMENTS FIRST-TIME ADOPTER Illustrative PSAB Financial Statements The purpose of this publication is to assist colleges in preparing their first Public Sector

SAMPLE PSAB COLLEGE ILLUSTRATIVE FINANCIAL STATEMENTS FIRST-TIME ADOPTER Illustrative PSAB Financial Statements The purpose of this publication is to assist colleges in preparing their first Public Sector

WASHINGTON ANIMAL RESCUE LEAGUE

WWW.MCB-CPA.COM FINANCIAL STATEMENTS TABLE OF CONTENTS Page Independent Auditors Report 1 Financial Statements: Statements of Financial Position 2 Statements of Activities and Changes in Net Assets 3-4

WWW.MCB-CPA.COM FINANCIAL STATEMENTS TABLE OF CONTENTS Page Independent Auditors Report 1 Financial Statements: Statements of Financial Position 2 Statements of Activities and Changes in Net Assets 3-4