Volume Title: The Financing of Large Corporations, Volume URL:

|

|

|

- John Walters

- 8 years ago

- Views:

Transcription

1 This PDF is a selection from an out-of-print volume from the National Bureau of Economic Research Volume Title: The Financing of Large Corporations, Volume Author/Editor: Albert Ralph Koch Volume Publisher: NBER Volume ISBN: Volume URL: Publication Date: 1943 Chapter Title: Short-Term Financing Chapter Author: Albert Ralph Koch Chapter URL: Chapter pages in book: (p )

2 .4. SHORT-TERM FINANCING WHEN A CONCERN DECIDES to expand its plant, increase its inventory, or extend additional credit to customers, it may borrow from a bank or finance company, secure credit from suppliers, retain more of its cash sales ddllars within the enterprise, or sell stocks and bonds. Thus short-term borrowings, funds retained from operations, and security sales are the major sources of funds utilized by business enterprises to finance their fixed and working capital requirements during periods of increasing business activity. The specific source of funds utilized may or may not be a matter of choice. In some growing profitable industries (for example, the automobile industry), the major part of capital expenditures has been financed out of funds retained from operations. Our sample of eight large automobile and truck companies expended $1,790 million on fixed capital and net additions to working capital and had available funds from operations of $1,876 million, over the period Long-term securities and short-term notes payable were retired net, while the "value of product" of the industry increased from $1,671 million in 1921 to $3,096 million in oln other industries (for example, the telephone industry), it has been easy for concerns to sell securities publicly.1 Still other industries (for example, meat packing) have relied on commercial banks for substantial amounts of funds. TOTAL SHORT-TERM FINANCING2 The relative importance of short-term indebtedness in the financial structure of a business enterprise depends a great deal on its industrial character. In 1937 the ratio of current liabilities to total assets varied as follows among broad industrial groupings: (3 Trade 34% Manufacturing 17 Railroads 7 Electric light and power 4 Telephones

3 62 The Financing of Large Corporations This variation with industry is also to be found among major subgroups and among individual corporations. The variation among companies within industries is often as great or greater than among industrial groups. This was, not true of the current assets/total assets ratio. The method of financing utilized by a given business concern is much more within its discretion than is the character of its assets structure, which is more largely determined by technological factors. The variation with size of concern is an inverse one for both manufacturing and trade. In 1937, the ratio of current liabilities to total assets for all corporate manufacturing was 17 percent, while in the large manufacturing sample it was only 9 percent. Explanations of these variations will become apparent as we discuss the components of total current liabilities. Structurally, large current liabilities/total assets ratios are usually associated with large current assets/total assets ratios but are characteristically smaller, as is shown below: Current Current Assets Liabilities Trade 63% 34% Manufacturing Electric light and power 6 4 Telephones 6 4 Railroads 4 7 Changes in current debt are also related to changes in current assets, as is shown in Chart 6. In this scatter diagram the changes in current assets of our combined sample of large manufacturing and trade concerns are plotted along with the annual changes in their current liabilities. Several interesting points concerning this relationship between changes in current assets and current liabilities can be noted. First, current liabilities increase and decrease with current assets. Second, the dollar volume of the annual. changes in current debt is less than in current assets. Third, current debt tends to show larger changes in connection with decreases than in connection with increases in current assets. When we analyze this relationship between current assets and current debt by narrower industrial groups, however, it is not so clear. Apparently when we deal with smaller aggregates of companies, individual differences in financing are highlighted, although such differences cancel out when the sample is enlarged. Over the two decades as a whole, the large manufacturing cor-

4 Short-Term Financing 63 CFIART 6 RELATIONSHIP BETWEEN ANNUAL CHANGES IN TOTAL CURRENT ASSETS AND TOTAL CURRENT LIABILITIES OF LARGE MANUFACTURING AND TRADE CORPORATIONS, 0 0 -J 2 I- w In In I z w -j I.. 0 I- 1Q TOTAL CURRENT LIAB%LITIES (IN MILLION DOLLARS) a Baied on A-26 and A-SO Dab Book. porations in our sample reduced short-term borrowings both absolutely and relative to alternative sources of funds. During this period these corporations reduced their current liabilities $615 million while expending $719 million on net additions to working capital; they spent more than $15 billion on fixed capital, retained more than $14 billion from operations and obtained over $2 billion new funds from security sales. In other words, these concerns obtained sufficient funds from operations and security sales to retire current indebtedness as well as to finance necessary fixed and working capital requirements. All of this reduction in current debt occurred during depression years. Since 1933, with the exception of 1938, the current debt of these companies has increased consistently. Among the major manufacturing groups all industries except automobiles, chemicals, and tobacco reduced their current debt. Although annual increases in current liabilities were more numerous than annual decreases, such increases were smaller, resulting in the cumulative reduction of

5 64 The Financing of Large Corporations 450 em 30 T P 1 P T traoe I I.. I I 23 25,l tv 33 current debt in most industries. Textiles had the greatest propor- tionate decrease in current liabilities, 39 percent, but this was less than the reduction in total liabilities, 44 percent. On the other hand, the OOU.AR5 trade concerns in our sample had an aggregate increase in current indebtedness of $88 million during this period. This 225 was small, however, compared to their expendi- depression. Among consistent tendency as a whole than in P 1 I TOTAL CURRCNT LIAUILITIC5 L p939 'S 30 Is Sn tures of $598 million on net additions to working capital. The annual changes in short-term debt of trading concerns fluctuated in a manner broadly similar to those of manufacturing companies, increasing in years of recovery and prosperity and decreasing in years of recession and the major trade groups there was a much more for short-term debt to increase over the period manufacturing. All groups except department stores, which exhibited no significant change in current liabilities, increased their short-term indebtedness. Although manufacturing corporations decreased the volume of funds secured from short-term sources relative to alternative sources from 1921 to 1932, they increased this volume from 1932 to The text chart shows the relationship between the current liabilities and total assets of large manufacturing and trade corporations annually. In trade, the level of the ratio was fairly constant up to 1929, after which it dropped precipitously until 1932, since which year it has increased irregularly. The current liabilities/total assets ratio among most of the major manufacturing groups also tended to decrease in the early thirties and then to increase gradually again. In only one manufacturing industry, petroleum, has the average ratio during recent years been below that of the twenties. For all of the major trade

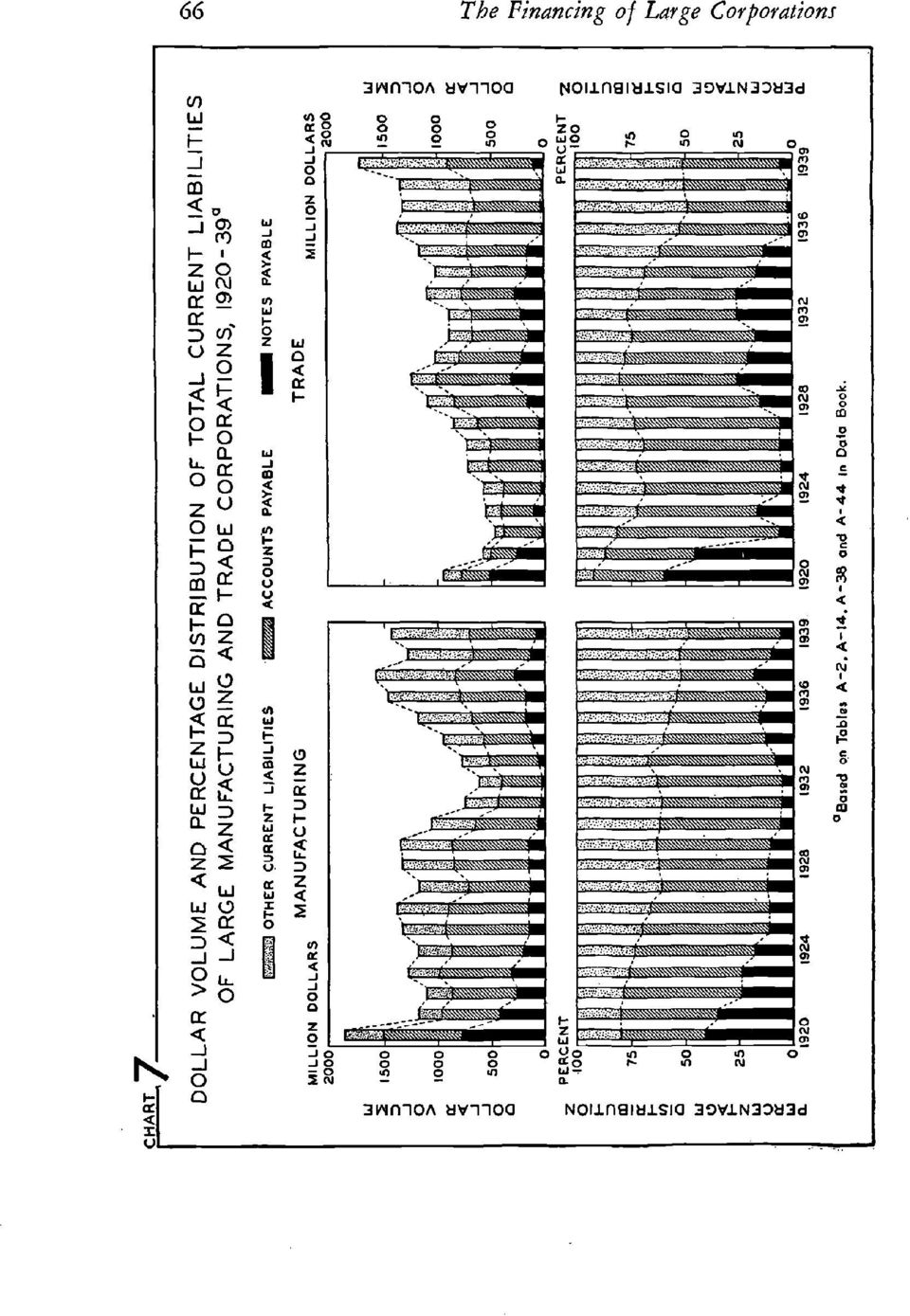

6 Short-Term Financing 65 groups there was a decrease ratio during the depression of the thirties, but by 1939 the ratio had increased again to0 the level of the first half of the twenties. COMPOSITION OF SHORT-TERM DEBT I The type of business 1 r in the current liabilities/total assets I T I PT I PT P T P ERCENT I 18 PT I I '' ' % MANUFA TOTAL CURRENT LIABILITIES financing we have been TO TOTAL ASSETS -S. I_SF,.v/ IllIllIllIlIllIl 0 discussing comes from 1921 ' '29 33 ' three main sources: (1) commercial banks, (2) mercantile creditors, and (3) miscellaneous sources, represented chiefly by accrued expenses. The relative volume of financing secured from these three groups is roughly indicated in business financial statements by the volume of notes payable, accounts payable, and various accruals recorded on yearend balance sheets. The dollar volume and percentage distribution of the three components of total current liabilities for our samples of large manufacturing and trade corporations are presented annually in Chart 7. Three striking facts can be noted. In the first place, the notes payable of the manufacturing sample have declined both in dollar amount and relative to accounts payable and other current liabilities. Although they increased in importance after the depression of the thirties, they fell off again in 1938, and in 1939 they were only slightly larger than their depression lows. In trade, the behavior of notes payable was significantly different, the level rémaining quite low during the expansion periods of the middle twenties and the late thirties. Second, there has been little change in the importance of accounts payable relative to the other two components of current liabilities in both major industrial categories. The dollar volume of accounts payable just about tripled in trade from 1920 to 1939, while in manufacturing it showed little change. Finally, other current liabilities have been a consistently increasing element of current debt in both groups since Notes Payable /'. ' TRADE Notes payable are fairly insignificant in the financial structure of big business; even in 1937 they were less than 2 percent of the total 12 B 4

commercial banks, (2) mercantile creditors, and (3) miscellaneous sources, represented chiefly by")

7

8 Short-Term Financing 67 assets of large manufacturing companies. Indeed, when we consider notes payable in comparison with cash holdings of big business we find cash holdings have I been consistently greater 8. ' I I I I I I I ' lilt I J NOTES PAYABLE TO TOTAL ASSETS PERCENT than bank loans: in 1932 they were over 35 times as great. Only two groups of I--T A A )E large corporations (meat 4 MANU FACT U 'I G packing and textiles) owed I ',' I banks on the average more -I- t ' than they had on deposit tv" \ ". should be under- during the past two dec '23 '25 27 '29 '31 '33 '35 ' ades. Large chemical cornpanies and chain variety stores had bank deposits almost 90 times as great as their debt to banks. Over the period studied the manufacturing corporations in our sample reduced notes payable by $751 million and the large trade corporations by $52 million. Most of this decrease occurred in five years. There was an expansion of bank borrowing by' big business in the middle thirties, the notes payable of our manufacturing sample soaring from $35 million in 1932 to $285 million in Bank loans appear to serve a function of convenience rather than of necessity for large, profitable, long-lived corporations. Generally speaking, when these concerns borrow from banks, they do so either because they consider it cheaper to obtain funds from banks than from other external sources, or because they desire to maintain close banking connections to facilitate possible future borrowings. This conclusion stood to apply to banks as sources of longer than seasonal credit to business enterprises.

E large corporations (meat 4 MANU FACT U 'I G packing and textiles) owed I ',' I banks on the average more -I- t '. -. - 2 than they had on deposit tv\" \ \".")

9 increased 68 The Financing of Large Corporations Unfortunately published data on bank loans are seldom available for intervals of less than a year. By restricting our analysis to year-end data, the importance of bank financing is underestimated for some industries (for example, rubber) whose balance sheets are published at a time of seasonal inactivity.6 These data are also restricted to the current indebtedness of big business to banks. Banks have been financing large corporations with intermediateterm credit through term or capital loans since At the end of 1939, the bank term loans of the manufacturing concerns in our sample totaled $85 million while their current notes payable amounted to million. Outstanding bank term loans as a percent of outstanding current notes payable of these concerns varied as follows for : Bank Term Notes Term Loans as Loans Payable a Percent of (millions) (millions) Notes Payable 1935 $100 $194 52% Looking more closely at the behavior of notes payable during the past two decades, we see that in large manufacturing concerns they decreased from 42 percent of current liabilities in 1920 to 6 percent in Trade showed an even greater decline, from 61 to 5 percent. In Chart 8 this decline in the notes payable of manufacturing and trade corporations is compared with that in "total loans commercial in form" of all national banks.7 This chart shows that changes in the bank loans of big corporations do not determine the course of all commercial loans of national banks. The borrowings of small and medium-sized corporations, partnerships, and individuals (including farmers and brokers) are very large. Both curves fell sharply in 1921 and 1922 when laçge meat packers, rubber companies, automobile companies, and mail-order houses were liquidating loans. At this time the two largest mailorder houses in the country managed as a result of substantial inventory liquidations to reduce their bank debt by over $50 million. During the rest of the twenties, although total commercial loans slightly, large manufacturing and trade corporations were using profits and the proceeds from security sales to retire notes payable. By 1929, these large concerns had few bank loans to liquidate; other business concerns, on the other hand, had been

10 Short-Term Financing 69 CHART 8 TOTAL COMMERCIAL LOANS OF ALL NATIONAL BANKS AND NOTES PAYABLE OF LARGE MANUFACTURING AND TRADE CORPORATiONS, NOTES PAYABLE MtLLION DOLLARS TOTAL LOANS MILLION DOLL.ARS ToiaI con buns are as of 30. See Pear,on I4unt. of in the United {Bureou of Business Research. University. 1940) pp Notes payable ore from Tabiss A2 and A 36 in Ogta Book. borrowing during the late twenties, and their liquidation of current debt in the early thirties sent the curve of total commercial loans into a downward plunge. If we consider the major groups within the manufacturing and trade sample, we find general agreement in the large picture but variation in details. Every one of the groups except miscellaneous chain stores decreased notes payable over the period Considerable difference appears, however, when we compare bank loans to total assets. The average notes payable/total assets ratio varied among the manufacturing groups as follows: Textiles Meat packing Rubber Tobacco Petroleum Food other than meat packing Machinery Automobiles and trucks Building materials and equipment Iron and steel Chemicals 8.4% The four industries on the top of the list, textiles, meat pack-

11 70 The Financing of Large Corporations ing, rubber, and tobacco, are all industries in which inventory is. an important part of total assets. The inventory loans of such industries are of two types. One is a good example of the classical, short-term, self-liquidating commercial loan. A meat packer, for example, borrows at the bank to pay for livestock, supplies, labor, and other costs. When his meat and by-products have been sold, he has the money to pay off his bank loan. The second type is, however, more than seasonal in character. When business expands or raw material prices rise, companies in these industries borrow to carry a larger dollar volume of inventory. These borrowings may last until business declines or prices fall. A similar variation is to be found among the trade groups. The notes payable/total assets ratio for the 19-year period as a whole varied as follows: Miscellaneous chain stores 5.6% Mail-order houses 3.2 Department stores 3.1 Chain grocery stores.6 Chain variety stores.1 The variation in the ratio during the past two decades among major groups in manufacturing and trade is less marked. In only two of the manufacturing industries (building materials and equipment, and petroleum) was the level of the ratio during the second decade higher than during the first decade. In the case of two industries (automobiles and trucks, and chemicals) the ratio during the thirties has been only a fraction of that during the twenties. In trade, the notes payable of mail-order houses averaged slightly higher during the thirties than during the twenties. On the 60 other hand, the average 50 notes payable/total assets 40 ratio of chain grocery stores during the thirties 30 was less than one-seventh 20 that during the twenties. l0 Since most cash is held in the form of bank deposits and since most notes payable are owed to banks, the ratio of cash holdings to notes payable gives a rough indication of the creditor-debtor relationship

12 Short-Term Financing 71 between banks and big business. In the text chart this ratio for our sample of 84 large manufacturing corporations is presented annually. Cash holdings of the manufacturing sample increased consistently from a low of 1.4 times notes payable in 1921 to a high of 35.1 in The annual average of the ratio for , 11.7, was over five times the average of The variation of the cash/notes payable ratio among major industrial classifications was very great. In manufacturing, the ratio for the two-decade span varied as follows: Chemicals 86.8 Iron and steel 31.6 Automobiles and trucks 31.0 Building materials and equipment 20.7 Machinery 16.7 Food other than meat packing 15.5 Petroleum 7.4 Tobacco 4.6 Rubber 2.1 Meat packing.9 Textiles.7 In trade, no one of the major groups had notes payable which averaged greater than cash holdings. The cash/notes payable ratio for the five groups during this period was: Chain variety stores 87.9 Chain grocery stores 37.0 Miscellaneous chain stores 2.8 Mail-order houses 2.3 Department stores 1.6 Accounts Payable Suppliers are of relatively slight importance in the financing of most large manufacturing corporations, but of some importance in financing certain large trade concerns. Their importance in both groups has, however, declined relative to alternative sources of financing. The dollar volume of the accounts payable of our manufacturing sample decreased by $175 million, and that of the trade sample increased by $62 million, from 1921 through As in the case of notes payable, most of this decrease occurred during the depression years. The annual changes in payables of both samples

13 72 The Financing of Large Corporations varied roughly with fluctuations in general business activity although there were some contra-cyclical movements (for example, the decrease in payables in 1937). Six major manufacturing groups reduced, and five increased, their accounts payable. Among the trade groups accounts payable were increased more consistently than in manufacturing. In chain variety stores, payables were decreased in only three years (1930, 1931, and 1937). Compared to total assets, the accounts payable of our sample of large manufacturing enterprises exhibited a downward trend. In addition, the accounts payable/total assets ratio varied positively with the business cycle. Among the major manufacturing groups the ratio for the two-decade span varied as follows: Automobiles and trucks 6.1% Petroleum 49 Rubber 4.0 Meat packing 3.7 Building materials and equipment 3.1 Iron and steel 2.3 Food other than meat packing 2.2 Machinery 2.2 Textiles 2.2 Chemicals 1.9 Tobacco 1.2 The high ratio in the automobile industry is due primarily to the practice of purchasing parts made to order. Parts makers customarily allow automobile manufacturers days' credit, a period somewhat longer than the process of assembling. The trend of this ratio in every one of these major industrial groups was downward in the thirties. During the thirties the level

14 Short-Term Financing 73 of the ratio decreased almost 50 percent from that of the twenties for both building materials and equipment, and petroleum. Accounts payable are a PERCENT I I I I I I I I I I I I T I I 2 more important source of 7 P 1 P T P 1 P I funds in trade than in manufacturing. The average ratio (6.2 percent) of accounts payable to total assets of our trade sample was over 70 percent greater than for our manufacturing sample (3.6 percent). Among the major trade groups, the variation period varying as follows: ----'--- /,, #' S...L_.. ';I TRADE ACCOUNTS PAYABLE TO TOTAL ASSETS I I I i I I i I I I I '23 '25 '21 '29 3l ' I FACT U RIM C was great, the ratio for the 19-year Chain grocery stores 13.2% Miscellaneous chain stores 12.2 Department stores 5.5 Mail-order houses 5.4 Chain variety stores 2.8 Over this period all these have decreased their trade payables relative to alternative sources of funds. Other studies in the National Bureau's Business Financing Project indicate that trade creditors are a more important source of funds for small manufacturing companies.9 The accounts payable/ total assets ratio of small manufacturing corporations is almost twice that of medium-sized and large corporations. In trade, however, the medium-sized corporations have the smallest ratio of accounts payable to total assets. The accounts payable/total assets ratios of all manufacturing and trade corporations in 1937 by asset size classes were as follows: 10 Manufacturing Trade Small (less than $500,000) 14.6% 20.3% Medium.sized ($500,000 b million) Large ($10 million and over) Other Current Liabilities Earlier in this chapter we noted..the increase in other current liabilities relative to notes and accounts payable during the past

15 I 74 The Financing of Large Corporations 'vu I 100 L Ix 200. I L I I. MANUFACTURING k IF OTUCH CURIIENt LIABILITIES I I I I I two decades. These other current liabilities are largely made up of obligations to employees, bondholders, stockholders and government. Most of the increase in other current liabilities occurred during the last half of the thirties and was due to increases in tax accruals and reserves. MILLION MIWOM These increases undoubtedly have been at least in part the result of uncertainty as to changes in corporate taxation. Some of them may in reality turn out to be surplus rather than liability reserves, in which case they will represent additional funds retained out of operations. In addition, some of the increase during the twenties may have been the result of a shift from a cash to an accrual method of recording expense, or Of the reporting in the early with accounts payable on years of accrued liabilities combined financial statements. It is difficult to analyze these early changes. For example, at a given point of time at which a balance sheet is drawn up, some labor services may have been utilized or "consumed" for which corresponding wage payments have not been made. Under a cash system of accounting, no charge to cost of sales would be recorded for these services until payment has been made for them, whereas under an accrual system such charges would be recorded even if payment has not been made. That part of the increase in accrued items which is the result of a shift in accounting method indicates a greater volume of funds retained from operations rather than an increase in the importance of the employee, bondholder, stockholder, or government as a source of funds. That is to say, under an accrual method of accounting, non-cash charges for unpaid but consumed services are debited-to cost of goods sold and hence lead to an understatement of the portion of the cash sales dollar which

16 Short-Term Financing 75 is undistributed and available, at least temporarily, for general corporate purposes. Another type of current indebtedness important in at least one manufacturing industry, aircraft and aircraft equipment, has been advance payments on government contracts. Since all the industries treated at length in this study have had a life of at least 20 years, the aircraft and aircraft equipment industry has been excluded. This industry, however, was a relatively insignificant part of the business economy of the United States in Total property expenditures of the United States Steel Corporation during these years, for example, were over five times greater than those of the 12 aircraft and aircraft equipment companies included in the Securities and Exchange Commission sample which were responsible for about four-fifths of the sales and total assets of the entire industry. The study by the SEC indicates that prepayments on contracts were the most important source of funds of 10 aircraft and 2 aircraft equipment companies for the period " Foreign military orders were the basis of most of these prepayments, the proceeds of which were kept on deposit with banks until utilized. During these years this source of funds provided slightly over $100, million, more than double total funds from operations or security sales.

FEDERAL RESERVE BULLETIN

FEDERAL RESERVE BULLETIN VOLUME 38 May 1952 NUMBER 5 Business expenditures for new plant and equipment and for inventory reached a new record level in 1951 together, they exceeded the previous year's total

FEDERAL RESERVE BULLETIN VOLUME 38 May 1952 NUMBER 5 Business expenditures for new plant and equipment and for inventory reached a new record level in 1951 together, they exceeded the previous year's total

Volume URL: http://www.nber.org/books/lutz45-1. Chapter Title: Liquidity Ratios and Cash Balances. Chapter URL: http://www.nber.

This PDF is a selection from an out-of-print volume from the National Bureau of Economic Research Volume Title: Corporate Cash Balances, 1914-43: Manufacturing and Trade Volume Author/Editor: Friedrich

This PDF is a selection from an out-of-print volume from the National Bureau of Economic Research Volume Title: Corporate Cash Balances, 1914-43: Manufacturing and Trade Volume Author/Editor: Friedrich

This week its Accounting and Beyond

This week its Accounting and Beyond Monday Morning Session Introduction/Accounting Cycle Afternoon Session Tuesday The Balance Sheet Wednesday The Income Statement The Cash Flow Statement Thursday Tools

This week its Accounting and Beyond Monday Morning Session Introduction/Accounting Cycle Afternoon Session Tuesday The Balance Sheet Wednesday The Income Statement The Cash Flow Statement Thursday Tools

STATEMENT OF CASH FLOWS AND WORKING CAPITAL ANALYSIS

C H A P T E R 1 0 STATEMENT OF CASH FLOWS AND WORKING CAPITAL ANALYSIS I N T R O D U C T I O N Historically, profit-oriented businesses have used the accrual basis of accounting in which the income statement,

C H A P T E R 1 0 STATEMENT OF CASH FLOWS AND WORKING CAPITAL ANALYSIS I N T R O D U C T I O N Historically, profit-oriented businesses have used the accrual basis of accounting in which the income statement,

Volume Publisher: Princeton University Press. Volume URL: http://www.nber.org/books/smit64-1. Chapter URL: http://www.nber.

This PDF is a selection from an out-of-print volume from the National Bureau of Economic Research Volume Title: Consumer Credit Costs, 1949 59 Volume Author/Editor: Paul F. Smith Volume Publisher: Princeton

This PDF is a selection from an out-of-print volume from the National Bureau of Economic Research Volume Title: Consumer Credit Costs, 1949 59 Volume Author/Editor: Paul F. Smith Volume Publisher: Princeton

Chapter URL: http://www.nber.org/chapters/c1737

This PDF is a selection from an out-of-print volume from the National Bureau of Economic Research Volume Title: Commercial Bank Activities in Urban Mortgage Financing Volume Author/Editor: Carl F Behrens

This PDF is a selection from an out-of-print volume from the National Bureau of Economic Research Volume Title: Commercial Bank Activities in Urban Mortgage Financing Volume Author/Editor: Carl F Behrens

Working Capital Concept & Animation

Working Capital Concept & Animation Meaning A measure of both a company's efficiency and its short-term financial health. The working capital is calculated as: Working Capital = Current Assets Current

Working Capital Concept & Animation Meaning A measure of both a company's efficiency and its short-term financial health. The working capital is calculated as: Working Capital = Current Assets Current

Chapter URL: http://www.nber.org/chapters/c5017

This PDF is a selection from an out-of-print volume from the National Bureau of Economic Research Volume Title: Industrial Demands upon the Money Market, 1919-57: A Study in Fund-Flow Analysis Volume Author/Editor:

This PDF is a selection from an out-of-print volume from the National Bureau of Economic Research Volume Title: Industrial Demands upon the Money Market, 1919-57: A Study in Fund-Flow Analysis Volume Author/Editor:

Volume Title: Accounts Receivable Financing. Volume Author/Editor: Raymond J. Saulnier and Neil H. Jacoby

This PDF is a selection from an out-of-print volume from the National Bureau of Economic Research Volume Title: Accounts Receivable Financing Volume Author/Editor: Raymond J. Saulnier and Neil H. Jacoby

This PDF is a selection from an out-of-print volume from the National Bureau of Economic Research Volume Title: Accounts Receivable Financing Volume Author/Editor: Raymond J. Saulnier and Neil H. Jacoby

9. Short-Term Liquidity Analysis. Operating Cash Conversion Cycle

9. Short-Term Liquidity Analysis. Operating Cash Conversion Cycle 9.1 Current Assets and 9.1.1 Cash A firm should maintain as little cash as possible, because cash is a nonproductive asset. It earns no

9. Short-Term Liquidity Analysis. Operating Cash Conversion Cycle 9.1 Current Assets and 9.1.1 Cash A firm should maintain as little cash as possible, because cash is a nonproductive asset. It earns no

State and Local Government Receipt and Expenditure Programs

SURVEY OF CUEEENT BUSINESS 11 by Karl O. Nygaard State and Local Government Receipt and Expenditure Programs local governments, in rendering a host of vital services, exercise important direct and indirect

SURVEY OF CUEEENT BUSINESS 11 by Karl O. Nygaard State and Local Government Receipt and Expenditure Programs local governments, in rendering a host of vital services, exercise important direct and indirect

Industrial Rent and Current Liabilities

This PDF is a selection from an out-of-print volume from the National Bureau of Economic Research Volume Title: The Pattern of Corporate Financial Structure: A Cross-Section View of Manufacturing, Mining,

This PDF is a selection from an out-of-print volume from the National Bureau of Economic Research Volume Title: The Pattern of Corporate Financial Structure: A Cross-Section View of Manufacturing, Mining,

Growth and Employment in Organised Industry

Growth and Employment in Organised Industry C.P. Chandrasekhar and Jayati Ghosh There is a general perception of industrial dynamism in the Indian economy at present, fed by reasonably high, even if not

Growth and Employment in Organised Industry C.P. Chandrasekhar and Jayati Ghosh There is a general perception of industrial dynamism in the Indian economy at present, fed by reasonably high, even if not

CH 23 STATEMENT OF CASH FLOWS SELF-STUDY QUESTIONS

C H 2 3, P a g e 1 CH 23 STATEMENT OF CASH FLOWS SELF-STUDY QUESTIONS (note from Dr. N: I have deleted questions for you to omit, but did not renumber the remaining questions) 1. The primary purpose of

C H 2 3, P a g e 1 CH 23 STATEMENT OF CASH FLOWS SELF-STUDY QUESTIONS (note from Dr. N: I have deleted questions for you to omit, but did not renumber the remaining questions) 1. The primary purpose of

Reporting and Analyzing Cash Flows QUESTIONS

Chapter 12 Reporting and Analyzing Cash Flows QUESTIONS 1. The purpose of the cash flow statement is to report all major cash receipts (inflows) and cash payments (outflows) during a period. It helps users

Chapter 12 Reporting and Analyzing Cash Flows QUESTIONS 1. The purpose of the cash flow statement is to report all major cash receipts (inflows) and cash payments (outflows) during a period. It helps users

E2-2: Identifying Financing, Investing and Operating Transactions?

E2-2: Identifying Financing, Investing and Operating Transactions? Listed below are eight transactions. In each case, identify whether the transaction is an example of financing, investing or operating

E2-2: Identifying Financing, Investing and Operating Transactions? Listed below are eight transactions. In each case, identify whether the transaction is an example of financing, investing or operating

Chapter 14. Working Capital Policy

Chapter 14 Working Capital Policy 1 Learning Outcomes Chapter 14 Discuss why working capital is needed and how working capital accounts are related. Describe the cash conversion cycle and how it can be

Chapter 14 Working Capital Policy 1 Learning Outcomes Chapter 14 Discuss why working capital is needed and how working capital accounts are related. Describe the cash conversion cycle and how it can be

Volume Author/Editor: John M. Chapman and associates. Volume URL: http://www.nber.org/books/chap40-1

This PDF is a selection from an out-of-print volume from the National Bureau of Economic Research Volume Title: Commercial Banks and Consumer Instalment Credit Volume Author/Editor: John M. Chapman and

This PDF is a selection from an out-of-print volume from the National Bureau of Economic Research Volume Title: Commercial Banks and Consumer Instalment Credit Volume Author/Editor: John M. Chapman and

Volume URL: http://www.nber.org/books/harr51-1. Chapter Title: Financing the Home Owners' Loan Corporation

This PDF is a selection from an out-of-print volume from the National Bureau of Economic Research Volume Title: History and Policies of the Home Owners' Loan Corporation Volume Author/Editor: C. Lowell

This PDF is a selection from an out-of-print volume from the National Bureau of Economic Research Volume Title: History and Policies of the Home Owners' Loan Corporation Volume Author/Editor: C. Lowell

Chapter 1. Introduction to Accounting and Business

1 Chapter 1 Introduction to Accounting and Business Learning Objective 1 Describe the nature of a business, the role of accounting, and ethics in business. Nature of Business and Accounting A business

1 Chapter 1 Introduction to Accounting and Business Learning Objective 1 Describe the nature of a business, the role of accounting, and ethics in business. Nature of Business and Accounting A business

Chapter URL: http://www.nber.org/chapters/c5003

This PDF is a selection from an out-of-print volume from the National Bureau of Economic Research Volume Title: Industrial Banking Companies and Their Credit Practices Volume Author/Editor: Raymond J.

This PDF is a selection from an out-of-print volume from the National Bureau of Economic Research Volume Title: Industrial Banking Companies and Their Credit Practices Volume Author/Editor: Raymond J.

Guide to Financial Statements Study Guide

Guide to Financial Statements Study Guide Overview (Topic 1) Three major financial statements: The Income Statement The Balance Sheet The Cash Flow Statement Objectives: Explain the underlying equation

Guide to Financial Statements Study Guide Overview (Topic 1) Three major financial statements: The Income Statement The Balance Sheet The Cash Flow Statement Objectives: Explain the underlying equation

(April 1, 2015 June 30, 2015)

") Financial Results Summary of Consolidated Financial Results For the Three-month Period Ended June 30, 2015 (IFRS basis) (April 1, 2015 June 30, 2015) *This document is an English translation of materials

Financial Results Summary of Consolidated Financial Results For the Three-month Period Ended June 30, 2015 (IFRS basis) (April 1, 2015 June 30, 2015) *This document is an English translation of materials

Comprehensive Business Budgeting

Management Accounting 137 Comprehensive Business Budgeting Goals and Objectives Profit planning, commonly called master budgeting or comprehensive business budgeting, is one of the more important techniques

Management Accounting 137 Comprehensive Business Budgeting Goals and Objectives Profit planning, commonly called master budgeting or comprehensive business budgeting, is one of the more important techniques

Chapter 002 Financial Statements, Taxes and Cash Flow

Multiple Choice Questions 1. The financial statement summarizing the value of a firm's equity on a particular date is the: a. income statement. B. balance sheet. c. statement of cash flows. d. cash flow

Multiple Choice Questions 1. The financial statement summarizing the value of a firm's equity on a particular date is the: a. income statement. B. balance sheet. c. statement of cash flows. d. cash flow

It is concerned with decisions relating to current assets and current liabilities

It is concerned with decisions relating to current assets and current liabilities Best Buy Co, NA s largest consumer electronics retailer, has performed extremely well over the past decade. Its stock sold

It is concerned with decisions relating to current assets and current liabilities Best Buy Co, NA s largest consumer electronics retailer, has performed extremely well over the past decade. Its stock sold

In this chapter, we build on the basic knowledge of how businesses

03-Seidman.qxd 5/15/04 11:52 AM Page 41 3 An Introduction to Business Financial Statements In this chapter, we build on the basic knowledge of how businesses are financed by looking at how firms organize

03-Seidman.qxd 5/15/04 11:52 AM Page 41 3 An Introduction to Business Financial Statements In this chapter, we build on the basic knowledge of how businesses are financed by looking at how firms organize

Volume Title: Conference on Research in Business Finance. Volume Author/Editor: Universities-National Bureau

This PDF is a selection from an out-of-print volume from the National Bureau of Economic Research Volume Title: Conference on Research in Business Finance Volume Author/Editor: Universities-National Bureau

This PDF is a selection from an out-of-print volume from the National Bureau of Economic Research Volume Title: Conference on Research in Business Finance Volume Author/Editor: Universities-National Bureau

Construction Economics & Finance. Module 6. Lecture-1

Construction Economics & Finance Module 6 Lecture-1 Financial management: Financial management involves planning, allocation and control of financial resources of a company. Financial management is essential

Construction Economics & Finance Module 6 Lecture-1 Financial management: Financial management involves planning, allocation and control of financial resources of a company. Financial management is essential

Solutions to Chapter 4. Measuring Corporate Performance

Solutions to Chapter 4 Measuring Corporate Performance 1. a. 7,018 Long-term debt ratio 0. 42 7,018 9,724 b. 4,794 7,018 6,178 Total debt ratio 0. 65 27,714 c. 2,566 Times interest earned 3. 75 685 d.

Solutions to Chapter 4 Measuring Corporate Performance 1. a. 7,018 Long-term debt ratio 0. 42 7,018 9,724 b. 4,794 7,018 6,178 Total debt ratio 0. 65 27,714 c. 2,566 Times interest earned 3. 75 685 d.

Consolidated Interim Earnings Report

Consolidated Interim Earnings Report For the Six Months Ended 30th September, 2003 23th Octorber, 2003 Hitachi Capital Corporation These financial statements were prepared for the interim earnings release

Consolidated Interim Earnings Report For the Six Months Ended 30th September, 2003 23th Octorber, 2003 Hitachi Capital Corporation These financial statements were prepared for the interim earnings release

TOPIC LEARNING OBJECTIVE

Topic Mapping 1 Transaction Analysis Understand the effect of various types of transactions on the accounting equation, accounting journal and accounting ledger. Concepts and Skills Accounting Equation

Topic Mapping 1 Transaction Analysis Understand the effect of various types of transactions on the accounting equation, accounting journal and accounting ledger. Concepts and Skills Accounting Equation

Chapter 18 Working Capital Management

Chapter 18 Working Capital Management Slide Contents Learning Objectives Principles Used in This Chapter 1. Working Capital Management and the Risk-Return Tradeoff 2. Working Capital Policy 3. Operating

Chapter 18 Working Capital Management Slide Contents Learning Objectives Principles Used in This Chapter 1. Working Capital Management and the Risk-Return Tradeoff 2. Working Capital Policy 3. Operating

6.3 PROFIT AND LOSS AND BALANCE SHEETS. Simple Financial Calculations. Analysing Performance - The Balance Sheet. Analysing Performance

63 COSTS AND COSTING 6 PROFIT AND LOSS AND BALANCE SHEETS Simple Financial Calculations Analysing Performance - The Balance Sheet Analysing Performance Analysing Financial Performance Profit And Loss Forecast

63 COSTS AND COSTING 6 PROFIT AND LOSS AND BALANCE SHEETS Simple Financial Calculations Analysing Performance - The Balance Sheet Analysing Performance Analysing Financial Performance Profit And Loss Forecast

CASH FLOW STATEMENT (AND FINANCIAL STATEMENT)

") CASH FLOW STATEMENT (AND FINANCIAL STATEMENT) - At the most fundamental level, firms do two different things: (i) They generate cash (ii) They spend it. Cash is generated by selling a product, an asset

CASH FLOW STATEMENT (AND FINANCIAL STATEMENT) - At the most fundamental level, firms do two different things: (i) They generate cash (ii) They spend it. Cash is generated by selling a product, an asset

FINANCIAL RESULTS FOR THE THREE MONTH ENDED JUNE 2013

FINANCIAL RESULTS FOR THE THREE MONTH ENDED JUNE 2013 Based on US GAAP Mitsubishi Corporation 2-3-1 Marunouchi, Chiyoda-ku, Tokyo, JAPAN 100-8086 http://www.mitsubishicorp.com/ Mitsubishi Corporation and

FINANCIAL RESULTS FOR THE THREE MONTH ENDED JUNE 2013 Based on US GAAP Mitsubishi Corporation 2-3-1 Marunouchi, Chiyoda-ku, Tokyo, JAPAN 100-8086 http://www.mitsubishicorp.com/ Mitsubishi Corporation and

Oklahoma State University Spears School of Business. Financial Statements

Oklahoma State University Spears School of Business Financial Statements Slide 2 Sources of Information Annual reports (10K) & Quarterly reports (10Q) SEC EDGAR Major databases COMPUSTAT(access through

Oklahoma State University Spears School of Business Financial Statements Slide 2 Sources of Information Annual reports (10K) & Quarterly reports (10Q) SEC EDGAR Major databases COMPUSTAT(access through

Volume URL: http://www.nber.org/books/fabr42-1. Chapter Title: Trends among Major Industrial Groups. Chapter URL: http://www.nber.

This PDF is a selection from an out-of-print volume from the National Bureau of Economic Research Volume Title: Employment in Manufacturing, 1899-1939: An Analysis of Its Relation to the Volume of Production

This PDF is a selection from an out-of-print volume from the National Bureau of Economic Research Volume Title: Employment in Manufacturing, 1899-1939: An Analysis of Its Relation to the Volume of Production

THE STATEMENT OF CASH FLOWS

THE STATEMENT OF CASH FLOWS Associate Professor PhD Cernusca Lucian University Aurel Vlaicu of Arad, luciancernusca_ro@yahoo.com Professor PhD Mates Dorel, West University of Timisoara Abstract: In today

THE STATEMENT OF CASH FLOWS Associate Professor PhD Cernusca Lucian University Aurel Vlaicu of Arad, luciancernusca_ro@yahoo.com Professor PhD Mates Dorel, West University of Timisoara Abstract: In today

Understanding Cash Flow Statements

Understanding Cash Flow Statements 2014 Level I Financial Reporting and Analysis IFT Notes for the CFA exam Contents 1. Introduction... 3 2. Components and Format of the Cash Flow Statement... 3 3. The

Understanding Cash Flow Statements 2014 Level I Financial Reporting and Analysis IFT Notes for the CFA exam Contents 1. Introduction... 3 2. Components and Format of the Cash Flow Statement... 3 3. The

Sri Lanka Accounting Standard-LKAS 7. Statement of Cash Flows

Sri Lanka Accounting Standard-LKAS 7 Statement of Cash Flows CONTENTS SRI LANKA ACCOUNTING STANDARD-LKAS 7 STATEMENT OF CASH FLOWS paragraphs OBJECTIVE SCOPE 1 3 BENEFITS OF CASH FLOW INFORMATION 4 5 DEFINITIONS

Sri Lanka Accounting Standard-LKAS 7 Statement of Cash Flows CONTENTS SRI LANKA ACCOUNTING STANDARD-LKAS 7 STATEMENT OF CASH FLOWS paragraphs OBJECTIVE SCOPE 1 3 BENEFITS OF CASH FLOW INFORMATION 4 5 DEFINITIONS

Understanding A Firm s Financial Statements

CHAPTER OUTLINE Spotlight: J&S Construction Company (http://www.jsconstruction.com) 1 The Lemonade Kids Financial statement (accounting statements) reports of a firm s financial performance and resources,

CHAPTER OUTLINE Spotlight: J&S Construction Company (http://www.jsconstruction.com) 1 The Lemonade Kids Financial statement (accounting statements) reports of a firm s financial performance and resources,

SOLUTIONS TO BRIEF EXERCISES

SOLUTIONS TO BRIEF EXERCISES B. Ex. 2.1 Walters Company's assets (machinery) will increase by $20,000. The company's liabilities will also increase by $20,000 to include the new obligation the company

SOLUTIONS TO BRIEF EXERCISES B. Ex. 2.1 Walters Company's assets (machinery) will increase by $20,000. The company's liabilities will also increase by $20,000 to include the new obligation the company

Indian Accounting Standard (Ind AS) 7 Statement of Cash Flows

7 Statement of Cash Flows") Contents Indian Accounting Standard (Ind AS) 7 Statement of Cash Flows Paragraphs OBJECTIVE SCOPE 1 3 BENEFITS OF CASH FLOW INFORMATION 4 5 DEFINITIONS 6 9 Cash and cash equivalents 7 9 PRESENTATION OF

Contents Indian Accounting Standard (Ind AS) 7 Statement of Cash Flows Paragraphs OBJECTIVE SCOPE 1 3 BENEFITS OF CASH FLOW INFORMATION 4 5 DEFINITIONS 6 9 Cash and cash equivalents 7 9 PRESENTATION OF

Volume Title: Accounts Receivable Financing. Volume Author/Editor: Raymond J. Saulnier and Neil H. Jacoby

This PDF is a selection from an out-of-print volume from the National Bureau of Economic Research Volume Title: Accounts Receivable Financing Volume Author/Editor: Raymond J. Saulnier and Neil H. Jacoby

This PDF is a selection from an out-of-print volume from the National Bureau of Economic Research Volume Title: Accounts Receivable Financing Volume Author/Editor: Raymond J. Saulnier and Neil H. Jacoby

6. Depreciation is a process of a. asset devaluation. b. cost accumulation. c. cost allocation. d. asset valuation.

1. A company purchased land for $72,000 cash. Real estate brokers' commission was $5,000 and $7,000 was spent for demolishing an old building on the land before construction of a new building could start.

1. A company purchased land for $72,000 cash. Real estate brokers' commission was $5,000 and $7,000 was spent for demolishing an old building on the land before construction of a new building could start.

16A SECURED SHORT-TERM FINANCING ACCOUNTS R ECEIVABLE F INANCING. Procedure for Pledging Accounts Receivable

App16A_SW_Brigham_778312 1/21/03 8:16 PM Page 16A-1 16A SECURED SHORT-TERM FINANCING This appendix discusses procedures for using accounts receivable and inventories as security for short-term loans. As

App16A_SW_Brigham_778312 1/21/03 8:16 PM Page 16A-1 16A SECURED SHORT-TERM FINANCING This appendix discusses procedures for using accounts receivable and inventories as security for short-term loans. As

GVEP Workshop Finance 101

GVEP Workshop Finance 101 Nairobi, January 2013 Agenda Introducing business finance Understanding financial statements Understanding cash flow LUNCH Reading and interpreting financial statements Evaluating

GVEP Workshop Finance 101 Nairobi, January 2013 Agenda Introducing business finance Understanding financial statements Understanding cash flow LUNCH Reading and interpreting financial statements Evaluating

Ternium Announces First Quarter 2015 Results

Sebastián Martí Ternium - Investor Relations +1 (866) 890 0443 +54 (11) 4018 2389 www.ternium.com Ternium Announces First Quarter 2015 Results Luxembourg, April 29, 2015 Ternium S.A. (NYSE: TX) today announced

Sebastián Martí Ternium - Investor Relations +1 (866) 890 0443 +54 (11) 4018 2389 www.ternium.com Ternium Announces First Quarter 2015 Results Luxembourg, April 29, 2015 Ternium S.A. (NYSE: TX) today announced

ACC 255 FINAL EXAM REVIEW PACKET (NEW MATERIAL)

") Page 1 ACC 255 FINAL EXAM REVIEW PACKET (NEW MATERIAL) Complete these sample exam problems/objective questions and check your answers with the solutions at the end of the review file and identify where

Page 1 ACC 255 FINAL EXAM REVIEW PACKET (NEW MATERIAL) Complete these sample exam problems/objective questions and check your answers with the solutions at the end of the review file and identify where

Volume Title: Trends and Cycles in the Commercial Paper Market. Volume URL: http://www.nber.org/books/seld63-1

This PDF is a selection from an out-of-print volume from the National Bureau of Economic Research Volume Title: Trends and Cycles in the Commercial Paper Market Volume Author/Editor: Richard T. Selden

This PDF is a selection from an out-of-print volume from the National Bureau of Economic Research Volume Title: Trends and Cycles in the Commercial Paper Market Volume Author/Editor: Richard T. Selden

NEPAL ACCOUNTING STANDARDS ON CASH FLOW STATEMENTS

NAS 03 NEPAL ACCOUNTING STANDARDS ON CASH FLOW STATEMENTS CONTENTS Paragraphs OBJECTIVE SCOPE 1-3 BENEFITS OF CASH FLOWS INFORMATION 4-5 DEFINITIONS 6-9 Cash and cash equivalents 7-9 PRESENTATION OF A

NAS 03 NEPAL ACCOUNTING STANDARDS ON CASH FLOW STATEMENTS CONTENTS Paragraphs OBJECTIVE SCOPE 1-3 BENEFITS OF CASH FLOWS INFORMATION 4-5 DEFINITIONS 6-9 Cash and cash equivalents 7-9 PRESENTATION OF A

Performance Review. Sample Company

Performance Review Sample Company For the period ended 12/31/2017 Provided By Page 1 / 18 This report is designed to assist you in your business' development. Below you will find your overall ranking,

Performance Review Sample Company For the period ended 12/31/2017 Provided By Page 1 / 18 This report is designed to assist you in your business' development. Below you will find your overall ranking,

Evaluate Performance: Balance Sheet

Excerpted from FastTrac GrowthVenture Financial statements and reports must be read together to learn the whole financial story. For example, an Income Statement may report a large sale to a new customer,

Excerpted from FastTrac GrowthVenture Financial statements and reports must be read together to learn the whole financial story. For example, an Income Statement may report a large sale to a new customer,

CASH FLOW STATEMENT. MODULE - 6A Analysis of Financial Statements. Cash Flow Statement. Notes

MODULE - 6A Cash Flow Statement 30 CASH FLOW STATEMENT In the previous lesson, you have learnt various types of analysis of financial statements and its tools such as comparative statements, common size

MODULE - 6A Cash Flow Statement 30 CASH FLOW STATEMENT In the previous lesson, you have learnt various types of analysis of financial statements and its tools such as comparative statements, common size

Deloitte GAAP 2014: FRS 102 - Volume B (UK Series)

") Deloitte GAAP 2014: UK Reporting - FRS 102 - Volume B (UK Series) Chapter B7: Free postage when you order online www.lexisnexis.co.uk/store or call 0845 370 1234 B7 Contents 1 Introduction 211 2 Scope

Deloitte GAAP 2014: UK Reporting - FRS 102 - Volume B (UK Series) Chapter B7: Free postage when you order online www.lexisnexis.co.uk/store or call 0845 370 1234 B7 Contents 1 Introduction 211 2 Scope

1. Define the operating and cash cycles. Why are they important?

Short-Term Planning Learning Objectives 1. Define the operating and cash cycles. Why are they important? 2. Define the different types of short-term financial policy 3. Understand the essentials of short-term

Short-Term Planning Learning Objectives 1. Define the operating and cash cycles. Why are they important? 2. Define the different types of short-term financial policy 3. Understand the essentials of short-term

Financial Terms & Calculations

Financial Terms & Calculations So much about business and its management requires knowledge and information as to financial measurements. Unfortunately these key terms and ratios are often misunderstood

Financial Terms & Calculations So much about business and its management requires knowledge and information as to financial measurements. Unfortunately these key terms and ratios are often misunderstood

The Business Credit Index

The Business Credit Index April 8 Published by the Credit Management Research Centre, Leeds University Business School April 8 1 April 8 THE BUSINESS CREDIT INDEX During the last ten years the Credit Management

The Business Credit Index April 8 Published by the Credit Management Research Centre, Leeds University Business School April 8 1 April 8 THE BUSINESS CREDIT INDEX During the last ten years the Credit Management

How To Read A University Or College'S Financial Statement

Understanding College and University Financial Statements By Rudy Fichtenbaum Professor of Economics Department of Economics Wright State University Dayton, OH 45435 (937) 775-3085 rfichtenbaum@sbcglobal.net

Understanding College and University Financial Statements By Rudy Fichtenbaum Professor of Economics Department of Economics Wright State University Dayton, OH 45435 (937) 775-3085 rfichtenbaum@sbcglobal.net

Understanding Financial Information for Bankruptcy Lawyers Understanding Financial Statements

Understanding Financial Information for Bankruptcy Lawyers Understanding Financial Statements In the United States, businesses generally present financial information in the form of financial statements

Understanding Financial Information for Bankruptcy Lawyers Understanding Financial Statements In the United States, businesses generally present financial information in the form of financial statements

CHAPTER 23. Statement of Cash Flows 1, 2, 7, 8, 12 3, 4, 5, 6, 16, 17, 19 9, 20 4, 5, 9, 10, 11 10, 13, 15, 16. 7. Worksheet adjustments.

CHAPTER 23 Statement of Cash Flows ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Format, objectives purpose, and source of statement.

CHAPTER 23 Statement of Cash Flows ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Format, objectives purpose, and source of statement.

Accounting Self Study Guide for Staff of Micro Finance Institutions

Accounting Self Study Guide for Staff of Micro Finance Institutions LESSON 2 The Balance Sheet OBJECTIVES The purpose of this lesson is to introduce the Balance Sheet and explain its components: Assets,

Accounting Self Study Guide for Staff of Micro Finance Institutions LESSON 2 The Balance Sheet OBJECTIVES The purpose of this lesson is to introduce the Balance Sheet and explain its components: Assets,

5. Provisions for decrease in value of marketable securities (-)

") Balance sheet ASSETS I. CURRENT ASSETS A. Liquid Assets: 1. Cash. 2. Cheques received. 3. Banks. 4. Cheques given and payment orders (-). 5. Other liquid assets. B. Marketable Securities: 1. Share certificates.

Balance sheet ASSETS I. CURRENT ASSETS A. Liquid Assets: 1. Cash. 2. Cheques received. 3. Banks. 4. Cheques given and payment orders (-). 5. Other liquid assets. B. Marketable Securities: 1. Share certificates.

UNDERSTANDING CANADIAN PUBLIC SECTOR FINANCIAL STATEMENTS

June 2014 UNDERSTANDING CANADIAN PUBLIC SECTOR FINANCIAL STATEMENTS www.bcauditor.com TABLE OF CONTENTS Who Will Find this Guide Helpful 3 What a Set of Public Sector Financial Statements Includes 5 The

June 2014 UNDERSTANDING CANADIAN PUBLIC SECTOR FINANCIAL STATEMENTS www.bcauditor.com TABLE OF CONTENTS Who Will Find this Guide Helpful 3 What a Set of Public Sector Financial Statements Includes 5 The

Investments and advances... 313,669

Consolidated Financial Statements of the Company The consolidated balance sheet, statement of income, and statement of equity of the Company are as follows. Please note the Company s consolidated financial

Consolidated Financial Statements of the Company The consolidated balance sheet, statement of income, and statement of equity of the Company are as follows. Please note the Company s consolidated financial

Statement of Cash Flow

Management Accounting 337 Statement of Cash Flow Cash is obviously an important asset to all, both individually and in business. A shortage or lack of cash may mean an inability to purchase needed inventory

Management Accounting 337 Statement of Cash Flow Cash is obviously an important asset to all, both individually and in business. A shortage or lack of cash may mean an inability to purchase needed inventory

ABOUT FINANCIAL RATIO ANALYSIS

ABOUT FINANCIAL RATIO ANALYSIS Over the years, a great many financial analysis techniques have developed. They illustrate the relationship between values drawn from the balance sheet and income statement

ABOUT FINANCIAL RATIO ANALYSIS Over the years, a great many financial analysis techniques have developed. They illustrate the relationship between values drawn from the balance sheet and income statement

Tejas Steel Supply, Inc.

Tejas Steel Supply, Inc. James B. Bexley Sam Houston State University Joe F. James Sam Houston State University Abstract This case study is designed to explore the credit needs and worthiness of Tejas

Tejas Steel Supply, Inc. James B. Bexley Sam Houston State University Joe F. James Sam Houston State University Abstract This case study is designed to explore the credit needs and worthiness of Tejas

ates on er 1958 sloan er 1959

ates on er 1958 lending to business during the last four quarters has been carried on under rapidly changing monetary and economic conditions, which have been reflected in changing interest rates charged

ates on er 1958 lending to business during the last four quarters has been carried on under rapidly changing monetary and economic conditions, which have been reflected in changing interest rates charged

ICAP GROUP S.A. FINANCIAL RATIOS EXPLANATION

ICAP GROUP S.A. FINANCIAL RATIOS EXPLANATION OCTOBER 2006 Table of Contents 1. INTRODUCTION... 3 2. FINANCIAL RATIOS FOR COMPANIES (INDUSTRY - COMMERCE - SERVICES) 4 2.1 Profitability Ratios...4 2.2 Viability

ICAP GROUP S.A. FINANCIAL RATIOS EXPLANATION OCTOBER 2006 Table of Contents 1. INTRODUCTION... 3 2. FINANCIAL RATIOS FOR COMPANIES (INDUSTRY - COMMERCE - SERVICES) 4 2.1 Profitability Ratios...4 2.2 Viability

STATEMENT BY STEPHEN S. GARDNER, VICE CHAIRMAN BOARD OF GOVERNORS OF THE FEDERAL RESERVE SYSTEM BEFORE THE

FOR RELEASE ON DELIVERY STATEMENT BY STEPHEN S. GARDNER, VICE CHAIRMAN BOARD OF GOVERNORS OF THE FEDERAL RESERVE SYSTEM BEFORE THE SUBCOMMITTEE ON TAXATION AND DEBT MANAGEMENT OF THE COMMITTEE ON FINANCE

FOR RELEASE ON DELIVERY STATEMENT BY STEPHEN S. GARDNER, VICE CHAIRMAN BOARD OF GOVERNORS OF THE FEDERAL RESERVE SYSTEM BEFORE THE SUBCOMMITTEE ON TAXATION AND DEBT MANAGEMENT OF THE COMMITTEE ON FINANCE

The Evolving External Orientation of Manufacturing: A Profile of Four Countries

The Evolving External Orientation of Manufacturing: A Profile of Four Countries José Campa and Linda S. Goldberg Changes in exchange rates, shifts in trade policy, and other international developments

The Evolving External Orientation of Manufacturing: A Profile of Four Countries José Campa and Linda S. Goldberg Changes in exchange rates, shifts in trade policy, and other international developments

Report Description. Business Counts. Top 10 States (by Business Counts) Page 1 of 16

Page 1 of 16") 5-Year County-Level Financial Profile Industry Report Architectural Services (SIC Code: 8712) in Prince George County, Maryland Sales Range: $500,000 - $999,999 Date: 11/07/08 Report Description This 5-Year

5-Year County-Level Financial Profile Industry Report Architectural Services (SIC Code: 8712) in Prince George County, Maryland Sales Range: $500,000 - $999,999 Date: 11/07/08 Report Description This 5-Year

Understanding Financial Statements: What do they say about your business?

Understanding Financial Statements: What do they say about your business? This workbook is not designed to be your only guide to understanding financial statements. A much wider range of resources is available

Understanding Financial Statements: What do they say about your business? This workbook is not designed to be your only guide to understanding financial statements. A much wider range of resources is available

INSTRUCTIONS FOR COMPLETING INSURANCE COMPANY FINANCIAL STATEMENTS

INSTRUCTIONS FOR COMPLETING INSURANCE COMPANY "DRAFT VERSION FOR FIRST REVIEW ONLY" Submitted to: Minstry of Finance and Economy Head of Insurance Department Republic of Armenia Submitted by: BearingPoint

INSTRUCTIONS FOR COMPLETING INSURANCE COMPANY "DRAFT VERSION FOR FIRST REVIEW ONLY" Submitted to: Minstry of Finance and Economy Head of Insurance Department Republic of Armenia Submitted by: BearingPoint

Chapter 8 Accounting for Receivables

Chapter 8 Accounting for Receivables Accounts Receivable Accounts Receivables are current assets. They are usually expected to be collected within 30 days. Allowance Method and Bad Debt Expense 2 methods:

Chapter 8 Accounting for Receivables Accounts Receivable Accounts Receivables are current assets. They are usually expected to be collected within 30 days. Allowance Method and Bad Debt Expense 2 methods:

Preparing Agricultural Financial Statements

Preparing Agricultural Financial Statements Thoroughly understanding your business financial performance is critical for success in today s increasingly competitive agricultural environment. Accurate records

Preparing Agricultural Financial Statements Thoroughly understanding your business financial performance is critical for success in today s increasingly competitive agricultural environment. Accurate records

Gross Sales (Gross Revenue): the total amount of money received from customers

: the total amount of money received from customers") Chapter 17 Financial Statements and Ratios 17.1: The Income Statement 17.1.1: Learn the terms used with income statements Income Statement: a financial statement used to summarize all income and expenses

Chapter 17 Financial Statements and Ratios 17.1: The Income Statement 17.1.1: Learn the terms used with income statements Income Statement: a financial statement used to summarize all income and expenses

Financial. Management FOR A SMALL BUSINESS

Financial Management FOR A SMALL BUSINESS 1 Agenda Welcome, Pre-Test, Agenda, and Learning Objectives Benefits of Financial Management Budgeting Bookkeeping Financial Statements Business Financing Key

Financial Management FOR A SMALL BUSINESS 1 Agenda Welcome, Pre-Test, Agenda, and Learning Objectives Benefits of Financial Management Budgeting Bookkeeping Financial Statements Business Financing Key

How To Calculate Financial Leverage Ratio

What Do Short-Term Liquidity Ratios Measure? What Is Working Capital? HOCK international - 2004 1 HOCK international - 2004 2 How Is the Current Ratio Calculated? How Is the Quick Ratio Calculated? HOCK

What Do Short-Term Liquidity Ratios Measure? What Is Working Capital? HOCK international - 2004 1 HOCK international - 2004 2 How Is the Current Ratio Calculated? How Is the Quick Ratio Calculated? HOCK

How to Assess Your Financial Planning and Loan Proposals By BizMove Management Training Institute

How to Assess Your Financial Planning and Loan Proposals By BizMove Management Training Institute Other free books by BizMove that may interest you: Free starting a business books Free management skills

How to Assess Your Financial Planning and Loan Proposals By BizMove Management Training Institute Other free books by BizMove that may interest you: Free starting a business books Free management skills

Chapter- 3B Statement of Changes in Financial Position and Working Capital (Fund

Chapter- 3B Statement of Changes in Financial Position and Working Capital (Fund BSNL, India For Internal Circulation Only 1 Statement of Changes in Financial Position and Working Capital (Fund) I. Statement

Chapter- 3B Statement of Changes in Financial Position and Working Capital (Fund BSNL, India For Internal Circulation Only 1 Statement of Changes in Financial Position and Working Capital (Fund) I. Statement

Ipx!up!hfu!uif Dsfeju!zpv!Eftfswf

Ipx!up!hfu!uif Dsfeju!zpv!Eftfswf Credit is the lifeblood of South Louisiana business, especially for the smaller firm. It helps the small business owner get started, obtain equipment, build inventory,

Ipx!up!hfu!uif Dsfeju!zpv!Eftfswf Credit is the lifeblood of South Louisiana business, especially for the smaller firm. It helps the small business owner get started, obtain equipment, build inventory,

MECHEL REPORTS THE 1Q 2015 FINANCIAL RESULTS

MECHEL REPORTS THE 1Q 2015 FINANCIAL RESULTS amounted to $1.1 billion Consolidated EBITDA(a) * amounted to $211 million Net loss attributable to shareholders of Mechel OAO amounted to $273 million Moscow,

MECHEL REPORTS THE 1Q 2015 FINANCIAL RESULTS amounted to $1.1 billion Consolidated EBITDA(a) * amounted to $211 million Net loss attributable to shareholders of Mechel OAO amounted to $273 million Moscow,

3,000 3,000 2,910 2,910 3,000 3,000 2,940 2,940

1. David Company uses the gross method to record its credit purchases, and it uses the periodic inventory system. On July 21, 20D, the company purchased goods that had an invoice price of $ with terms

1. David Company uses the gross method to record its credit purchases, and it uses the periodic inventory system. On July 21, 20D, the company purchased goods that had an invoice price of $ with terms

The BASICS of FINANCIAL STATEMENTS For Agricultural Producers

The BASICS of FINANCIAL STATEMENTS For Agricultural Producers Authors: James McGrann Francisco Abelló Doug Richardson Christy Waggoner Department of Agricultural Economics Texas Cooperative Extension Texas

The BASICS of FINANCIAL STATEMENTS For Agricultural Producers Authors: James McGrann Francisco Abelló Doug Richardson Christy Waggoner Department of Agricultural Economics Texas Cooperative Extension Texas

Volume Title: New-Automobile Finance Rates, 1924 62. Volume URL: http://www.nber.org/books/shay63-1

This PDF is a selection from an out-of-print volume from the National Bureau of Economic Research Volume Title: New-Automobile Finance Rates, 1924 62 Volume Author/Editor: Robert P. Shay Volume Publisher:

This PDF is a selection from an out-of-print volume from the National Bureau of Economic Research Volume Title: New-Automobile Finance Rates, 1924 62 Volume Author/Editor: Robert P. Shay Volume Publisher:

6. Show all your workings. icpar

CERTIFIED PUBLIC ACCOUNTANT FOUNDATION LEVEL 1 EXAMINATION F1.3: FINANCIAL ACCOUNTING MONDAY: 10 JUNE 2013 INSTRUCTIONS: 1. Time Allowed: 3 hours 15 minutes (15 minutes reading and 3 hours writing). 2.

CERTIFIED PUBLIC ACCOUNTANT FOUNDATION LEVEL 1 EXAMINATION F1.3: FINANCIAL ACCOUNTING MONDAY: 10 JUNE 2013 INSTRUCTIONS: 1. Time Allowed: 3 hours 15 minutes (15 minutes reading and 3 hours writing). 2.

Performance Review for Electricity Now

Performance Review for Electricity Now For the period ending 03/31/2008 Provided By Mark Dashkewytch 780-963-5783 Report prepared for: Electricity Now Industry: 23821 - Electrical Contractors Revenue:

Performance Review for Electricity Now For the period ending 03/31/2008 Provided By Mark Dashkewytch 780-963-5783 Report prepared for: Electricity Now Industry: 23821 - Electrical Contractors Revenue:

You have learnt about the financial statements

Analysis of Financial Statements 4 You have learnt about the financial statements (Income Statement and Balance Sheet) of companies. Basically, these are summarised financial reports which provide the

Analysis of Financial Statements 4 You have learnt about the financial statements (Income Statement and Balance Sheet) of companies. Basically, these are summarised financial reports which provide the

CHAPTER 26. Working Capital Management. Chapter Synopsis

CHAPTER 26 Working Capital Management Chapter Synopsis 26.1 Overview of Working Capital Any reduction in working capital requirements generates a positive free cash flow that the firm can distribute immediately

CHAPTER 26 Working Capital Management Chapter Synopsis 26.1 Overview of Working Capital Any reduction in working capital requirements generates a positive free cash flow that the firm can distribute immediately

CASH FLOW STATEMENT. On the statement, cash flows are segregated based on source:

CASH FLOW STATEMENT On the statement, cash flows are segregated based on source: Operating activities: involve the cash effects of transactions that enter into the determination of net income. Investing

CASH FLOW STATEMENT On the statement, cash flows are segregated based on source: Operating activities: involve the cash effects of transactions that enter into the determination of net income. Investing

Consolidated Financial Results for the Six Months Ended September 30, 2015 [Japanese GAAP]

![Consolidated Financial Results for the Six Months Ended September 30, 2015 [Japanese GAAP]](/thumbs/26/8778862.jpg "Consolidated Financial Results for the Six Months Ended September 30, 2015 [Japanese GAAP]") Consolidated Financial Results for the Six Months Ended September 30, 2015 [Japanese GAAP] November 6, 2015 Company name: Shibaura Electronics Co., Ltd. Stock exchange listing: Tokyo Stock Exchange Code

Consolidated Financial Results for the Six Months Ended September 30, 2015 [Japanese GAAP] November 6, 2015 Company name: Shibaura Electronics Co., Ltd. Stock exchange listing: Tokyo Stock Exchange Code

Chapter-3 Solutions to Problems

Chapter-3 Solutions to Problems P3-1. P3-2. Reviewing basic financial statements LG 1; Basic Income statement: In this one-year summary of the firm s operations, Technica, Inc. showed a net profit for

Chapter-3 Solutions to Problems P3-1. P3-2. Reviewing basic financial statements LG 1; Basic Income statement: In this one-year summary of the firm s operations, Technica, Inc. showed a net profit for

IPSAS 2 CASH FLOW STATEMENTS

IPSAS 2 CASH FLOW STATEMENTS Acknowledgment This International Public Sector Accounting Standard (IPSAS) is drawn primarily from International Accounting Standard (IAS) 7, Cash Flow Statements published

IPSAS 2 CASH FLOW STATEMENTS Acknowledgment This International Public Sector Accounting Standard (IPSAS) is drawn primarily from International Accounting Standard (IAS) 7, Cash Flow Statements published

Consolidated Balance Sheets March 31, 2001 and 2000

Financial Statements SEIKAGAKU CORPORATION AND CONSOLIDATED SUBSIDIARIES Consolidated Balance Sheets March 31, 2001 and 2000 Assets Current assets: Cash and cash equivalents... Short-term investments (Note

Financial Statements SEIKAGAKU CORPORATION AND CONSOLIDATED SUBSIDIARIES Consolidated Balance Sheets March 31, 2001 and 2000 Assets Current assets: Cash and cash equivalents... Short-term investments (Note

MOUNTAIN EQUIPMENT CO-OPERATIVE

Consolidated Financial Statements of MOUNTAIN EQUIPMENT CO-OPERATIVE KPMG LLP PO Box 10426 777 Dunsmuir Street Vancouver BC V7Y 1K3 Canada Telephone (604) 691-3000 Fax (604) 691-3031 Internet www.kpmg.ca

Consolidated Financial Statements of MOUNTAIN EQUIPMENT CO-OPERATIVE KPMG LLP PO Box 10426 777 Dunsmuir Street Vancouver BC V7Y 1K3 Canada Telephone (604) 691-3000 Fax (604) 691-3031 Internet www.kpmg.ca

IGAS 3. Cash Flow Statements. Government Accounting Standards Advisory Board. Contents

Cash Flow Statements Government Accounting Standards Advisory Board Contents Description Page Number 1. Introduction 3 2. Objective 3 3. Scope 3 4. Benefits of Cash Flow Information 4 5. Definitions 4

Cash Flow Statements Government Accounting Standards Advisory Board Contents Description Page Number 1. Introduction 3 2. Objective 3 3. Scope 3 4. Benefits of Cash Flow Information 4 5. Definitions 4