Are you ready to become part of Australia s largest superannuation pool?

|

|

|

- Denis Burke

- 8 years ago

- Views:

Transcription

1 Are you ready to become part of Australia s largest superannuation pool?

2 This information is a summary based on Hayes Knight's understanding of the relevant legislation. It is general in nature and may not be relevant to individual circumstances. You should not do or refrain from doing anything in reliance on this information without obtaining suitable professional advice from your accountant or financial planner.

3 Tino Di Battista Director, SMSF Specialist Advisor Richard Callis - Manager Siva Peddareddy SMSF Specialist Advisor Matthew Nicolas SMSF Accountant super@hkm.com.au

4 1. Industry Overview / Growth 2. What is a SMSF 3. Why is it growing? 4. Case Study s The Smith s Accumulators The Jones s Retirees 5. Other Pension & Contribution Strategies 6. Questions

5 $Billions $516b $570b $403b $335b $58b $56.5b Corporate Funds (108 funds) Industry Funds (52 funds) Public Sector Funds (38 funds) Retail Funds (127 funds) SMSFs (531,742 funds) Statutory Funds

SMSFs (531,742 funds)")

6

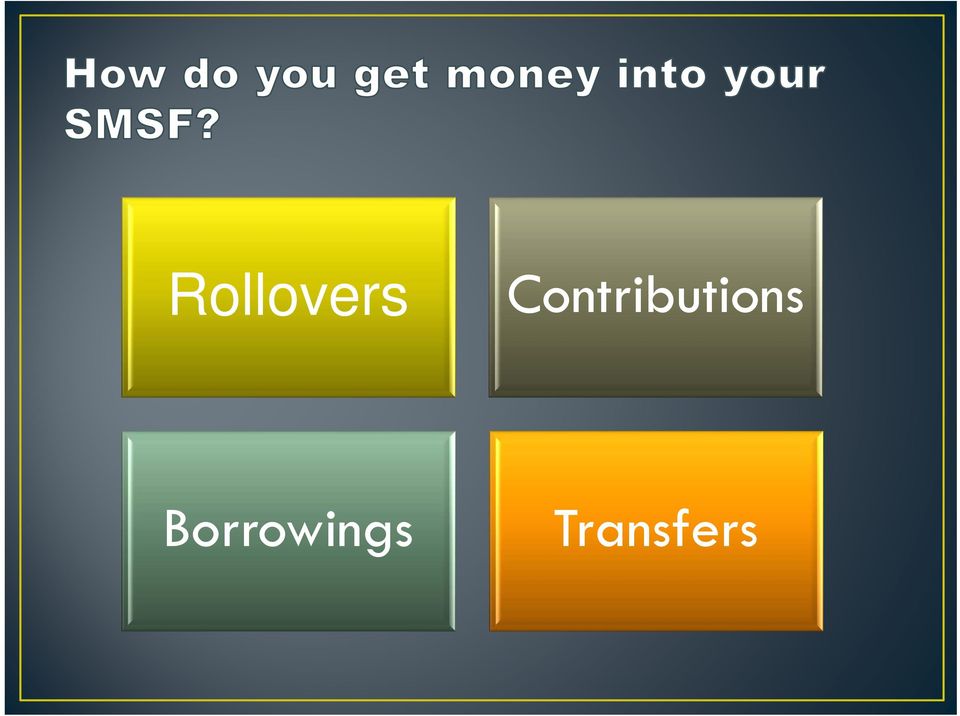

7 because Australians love choice & to have control over their retirement savings Income taxed at 15% Gains taxed at 10% Can directly invest in property - commercial & residential Franking credits (fully allocated) More flexibility Property development* Tax effective vehicle to build wealth for retirement

8

9 SMSF with Individual Trustees Individual Trustee 1 Individual Trustee 2 Same Person Self Managed Super Fund Same Person Member 1 Member 2

10 Director 1 Director 2 Corporate Trustee Same Person Self Managed Super Fund Same Person Member 1 Member 2

11 Individual vs Corporate Structure Individual Trustees Lower cost to establish Corporate Trustee Easier to keep assets separate Lower ongoing costs Reduced liability for clients? Less complex structure Estate planning benefits? Additional administrative when adding/removing members (e.g. deaths of member) ATO trustee penalties apply to each trustee (can be x4) Administration simpler adding & removing members is easy as trustee does not change, only change of director ATO trustee penalties only apply once ATO Penalties are payable from personal funds not from SMSF

12 Trustee Residents individuals over 18 Member Residents individuals over 18 Australian Resident Corporations Personal Legal representative

13 What is an SMSF - Recap

14

15 Rollovers Contributions Borrowings Transfers

16 Mr & Mrs Smith - Accumulators

17 Brad, 39 and Angelina, 36 Brad is an IT consultant earning $150,000 plus super Angelina is a dentist earning $180,000 plus super Angelina runs her own practice Their children are Chloe, 9 & Luke, 7 Their superannuation is in industry super funds They each have approximately $200,000 in Super

18 What their roles & responsibilities are as trustees The time, knowledge and skill The structure The costs and benefits required The purpose of their SMSF Sole Purpose Test Their investment strategy

19

20 Cash (Bank/CMA) Fixed Interest (Term deposits/bonds) Listed Australian Securities. International Securities Managed funds (Australian and international) Direct property (commercial and residential) Unlisted company s and trusts* Options, Warrants and CFD s Commodities Collectibles (Stay away)

Unlisted company s and")

21

22 Rollovers

23 Brad Angelina

24 Brad (Director) Brangelina Pty Ltd Angelina (Director) Smith Family SMSF Brad (Member) Angelia (Member)

25 Brad (Director) Brangelina Pty Ltd Angelina (Director) Smith Family SMSF Brad (Member) Angelia (Member)

26 Contributions

27 Concessional contributions Employer contributions (SGC) Salary sacrifice contributions Tax deductible member contributions Non-Concessional contributions Member contributions Spouse contributions Contribution splitting Some small business CGT proceeds

28 Brad earns $150,000 gross salary p.a. Employer contributions = $14,250 ($150,000 x 9.5%) Brad chooses to salary sacrifice a further $15,750 out of his pre-tax salary This uses up his concessional cap of $30,000 ($14,250 + $15,750) Brad chooses to have his super paid to his new SMSF By doing this, he reduces his taxable income to $134,250 ($150,000 - $15,750)

29 Brad SG no salary sacrifice Salary sacrifice $15,750 Difference Taxable Income $150,000 $134,250 $15,750 Tax & Medicare payable $48,696 $41,982 $6,714 Take home pay (after tax) $101,304 $92,268 $9,036 Extra money paid into super after tax (15% tax) Take home pay PLUS extra Super $0 $13,387 $13,387 $101,304 $105,655 $4,351

30 Transfers

31 Cash Commodities (i.e. Gold)

32 Determine if property is Business Real Property (BRP) Property is used wholly and exclusively in one or more business Decide if the investments fits into your Investment Strategy and does the Trust Deed allow it Check that un-encumbered Determine any Stamp Duty & CGT applicable Ensure transfer is made at arms length valuation

33 Potential for positive returns through rental income and capital gains Rental income taxed at 15%, capital gains taxed at 10% (maximum) Diversification of retirement savings Assets held within an SMSF are generally protected from creditors in the case of bankruptcy.

34 Brad and Angelina jointly own property leased to Angelina s dental practice Current market value is $900,000 Current rent is $45,000 per annum Rent is currently taxed at their marginal tax rates The property was transferred (inspecie) as a non-concessional contribution ($450,000 each) The SMSF will continue to lease the property to the dental practice Remember: Stamp duty and capital gains need to be considered on the transfer After discussions with HK, Brad & Angelina decide to transfer the property into their SMSF

35 Rental income taxed at 15%...but Angelina still claims at her (higher) marginal tax rate Costs incurred in the managing property (rates, depreciation, insurance) are tax deducible In pension phase (at least 55 years of age) income & gains are tax free (BUT rent paid by the practice will continue to be tax deductible)

36 Borrowings Limited Recourse Borrowing Arrangements (a.k.a. LRBA)

37 What does an LRBA Structure look like? Limited Recourse Loan Loan Repayments Beneficial Owner (SMSF) Property Bare Trust Legal Owner (Bare Trust Trustee)

38 Money still invested with their current industry super funds from 1 July 2015 to 30 June 2016 Starting balance Balance with only SG & return of 8.3%pa - after Year 1 Balance with only SG & return of 8.3%pa after Year 5 Brad $200,000 $225,841 $348,322 Angelina $200,000 $228,264 $362,226 Total $400,000 $454,105 $710,548 Figures are net of tax, fees, and compounded annually

39 Money moved into SMSF with salary sacrifice and property transfer. Period from 1 July 2015 to 30 June 2016 Starting balance Balance with Salary Sacrifice and property transfer strategy Year 1 Balance with Salary Sacrifice and property transfer strategy Year 5 Brad $200,000 $715,625 $1,005,446 Angelina $200,000 $704,660 $946,056 Total $400,000 $1,420,285 $1,951,502 By transferring property (earning rental income & growth) & Brad salary sacrificing up to max. $30,000 into super, their total balance after year 1 has increased by an additional $1,020,285

40 Just like Brad and Angelina implemented, the following strategies can be highly effective to boost retirement savings: Salary sacrificing Consolidating super Making after-tax contributions (non-concessional) Making good investment choices will also help!

41 Mr & Mrs Jones Retirees

42 John 56, and Joanna 60 years of age. They run a café business in premises valued at $1m owned by the business They derive a combined income of $200,000 from the business They jointly own a share portfolio valued at $740,000 They also own an investment property (residential) worth $800,000 Their superannuation is with Rest Super (retail super), each with $300,000 They have 3 adult children Angelina, Nick and George (living overseas)

43 Transfers

44 John and Joanna are nearing retirement They are keen to consolidate their personal assets They are seeking an income between $80,000 to $100,000 in retirement to support their current lifestyle Their Share Portfolio John and Joanna can transfer In-specie $740,000 (their total share portfolio) This is done as a $370,000 after tax contribution (non-concessional) by both John & Joanna Caution Bring forward rule is triggered Their Business The premises can also be transferred in specie assuming it satisfies the definition of Business Real Property BEWARE:

45 The share portfolio cost was $540,000, against current market of $740,000 (i.e. gain of $200,000) By transferring the shares to the SMSF a discounted capital gain of $100,000 will be triggered ($50,000 each) To minimise tax on the capital gain, John & Joanna can each make a personal contribution (tax deductible) up to $35,000, reducing the total capital gain to $30,000 Once the shares are in the SMSF John & Joanna can start a pension so that the dividends & any subsequent gains are tax free.

46 The main small business CGT concessions available are: - 15 year retirement exemption - Retirement exemption - 50% active asset Small Business Entity Test Aggregated Annual T/Over Connected entities Affiliates Eligibility Active Asset $6 Million Maximum Net Asset Value Test CGT Concession Stakeholder

47 Sale of Business Facts Business was purchased 20 years ago for $400,000 John and Joanna equally own the shares in the business The business was sold for $1.2 million (including business premises) The 15 year retirement exemption can be used as both John & Joanna are over 55 years of age and have owned the business for a continuous period of at least 15 years Important: This DOES NOT effect the normal contribution caps CGT Lifetime Cap: $1,355,000

48 How The proceeds from the sale of business are transferred to the SMSF by utilising the 15 year retirement exemption Benefits The entire capital gain on the sale is disregarded Boost their retirement savings (superannuation) Successfully exit the business & retire Receive pensions from the SMSF to support their lifestyle

49 John Joanna Starting balance $300,000 $300,000 Share portfolio $370,000 $370,000 Proceeds from sale of business $600,000 $600,000 Total Balance $1,270,000 $1,270,000 By transferring the assets to the SMSF, both balances have increased by $970,000

50 John & Joanna can convert their accumulation balance of $1,270,000 to an account based pension A minimum payment of 4% must be withdrawn each financial year This equates to a minimum pension of $51,000 Joanna pension will be tax-free as she s reached 60 years of age John pays tax on the taxable portion of his pension until he is 60

51 The $300,000 rollover from Rest Super is 100% taxable, the share transfer & business sale are tax-free Tax is payable on 24% of John s $51,000 pension prior to age 60 So, John will pay tax on only $12,240 of his pension AND receive a 15% tax rebate NOTE: The SMSF s earnings and any capital gains are 100% tax free (assuming in 100% pension phase) irrespective of John & Joanna s different tax treatment

52 This information is a summary based on Hayes Knight's understanding of the relevant legislation. It is general in nature and may not be relevant to individual circumstances. You should not do or refrain from doing anything in reliance on this information without obtaining suitable professional advice from your accountant or financial planner.

53 QUESTIONS? Tino: Richard: Siva: Matthew:

Self Managed Superannuation Funds

Self Managed Superannuation Funds You have as much choice and control over an investment property using your superannuation funds as you would by investing personally Self Managed Superannuation Funds

Self Managed Superannuation Funds You have as much choice and control over an investment property using your superannuation funds as you would by investing personally Self Managed Superannuation Funds

End of financial year planning tips May 2014

End of financial year planning tips May 2014 With the end of the financial year fast approaching, it is a good time to review financial planning strategies with a view to optimising your outcomes. This

End of financial year planning tips May 2014 With the end of the financial year fast approaching, it is a good time to review financial planning strategies with a view to optimising your outcomes. This

Is your. potential? Right Strategy.

Is your SMSF working to its full potential? Right Strategy. Right Time. While managing your own super provides investment flexibility and control, the biggest challenge is ensuring the decisions you make

Is your SMSF working to its full potential? Right Strategy. Right Time. While managing your own super provides investment flexibility and control, the biggest challenge is ensuring the decisions you make

May Newsletter #1. Your superannuation checklist. Getting Ready for Tax Time. Meet Bridget Kelly

May Newsletter #1 Getting Ready for Tax Time Tax time is fast approaching! To help you with your planning, we are sending out checklists about your superannuation, individual and business tax affairs,

May Newsletter #1 Getting Ready for Tax Time Tax time is fast approaching! To help you with your planning, we are sending out checklists about your superannuation, individual and business tax affairs,

Make sure your SMSF is.

Make sure your SMSF is. Super decisions You know first-hand that one of the biggest advantages of managing your own super is that you make the decisions. It s one of the main reasons you have an SMSF or

Make sure your SMSF is. Super decisions You know first-hand that one of the biggest advantages of managing your own super is that you make the decisions. It s one of the main reasons you have an SMSF or

Maximise your superannuation & Strategies for 30 June 2010

Maximise your superannuation & tax benefits Strategies for 30 June 2010 Like my old mate Kerry Packer used to say, "Pay your tax, but don't tip them. they're not doing that good a job. Paul Hogan 60 Minutes

Maximise your superannuation & tax benefits Strategies for 30 June 2010 Like my old mate Kerry Packer used to say, "Pay your tax, but don't tip them. they're not doing that good a job. Paul Hogan 60 Minutes

Smart strategies for maximising retirement income

Smart strategies for maximising retirement income 2010 Why you need to create a life-long income Australia has one of the highest life expectancies in the world and the average retirement length has increased

Smart strategies for maximising retirement income 2010 Why you need to create a life-long income Australia has one of the highest life expectancies in the world and the average retirement length has increased

Tax deductible superannuation contributions

Tax deductible superannuation contributions TB 35 TECHNICAL SERVICES ISSUED ON 29 OCTOBER 2014 ADVISER USE ONLY VERSION 1.1 Summary Employers and certain individuals can claim a tax deduction for contributions

Tax deductible superannuation contributions TB 35 TECHNICAL SERVICES ISSUED ON 29 OCTOBER 2014 ADVISER USE ONLY VERSION 1.1 Summary Employers and certain individuals can claim a tax deduction for contributions

Smart strategies for maximising retirement income 2012/13

Smart strategies for maximising retirement income 2012/13 Why you need to create a life long income Australia has one of the highest life expectancies in the world and the average retirement length has

Smart strategies for maximising retirement income 2012/13 Why you need to create a life long income Australia has one of the highest life expectancies in the world and the average retirement length has

A Financial Planning Technical Guide

Self Managed Superannuation Funds A Financial Planning Technical Guide Securitor Financial Group Limited ABN 48 009 189 495 AFSL 240687 Contents What is a self managed superannuation fund (SMSF)? 1 What

Self Managed Superannuation Funds A Financial Planning Technical Guide Securitor Financial Group Limited ABN 48 009 189 495 AFSL 240687 Contents What is a self managed superannuation fund (SMSF)? 1 What

Smart strategies for your super

Smart strategies for your super 2010 Make your super count Superannuation is still one of the best ways to accumulate wealth and save for your retirement. The main reason, of course, is the favourable

Smart strategies for your super 2010 Make your super count Superannuation is still one of the best ways to accumulate wealth and save for your retirement. The main reason, of course, is the favourable

Understanding Tax Version 1.0 Preparation Date: 1st July 2013

Understanding Tax Version 1.0 Preparation Date: 1st July 2013 This document provides some additional information to help you understand the financial planning concepts discussed in the SOA in relation

Understanding Tax Version 1.0 Preparation Date: 1st July 2013 This document provides some additional information to help you understand the financial planning concepts discussed in the SOA in relation

THE SMSF ESSENTIALS GUIDE. The ultimate starter guide to setting up, running and effectively using a Self Managed Superannaution Fund

THE SMSF ESSENTIALS GUIDE The ultimate starter guide to setting up, running and effectively using a Self Managed Superannaution Fund DISCLAIMER The purpose of this e-book is to provide information and

THE SMSF ESSENTIALS GUIDE The ultimate starter guide to setting up, running and effectively using a Self Managed Superannaution Fund DISCLAIMER The purpose of this e-book is to provide information and

End of Year Income and Tax Planning Individuals - June 2013

The tips below will assist you in your end of year income and tax planning strategies. These tips are not meant to be exhaustive nor applicable to each and every individual taxpayer. Further you should

The tips below will assist you in your end of year income and tax planning strategies. These tips are not meant to be exhaustive nor applicable to each and every individual taxpayer. Further you should

CLIENT FACT SHEET. If you are under age 65 you may make personal contributions to superannuation on your own behalf.

CLIENT FACT SHEET July 2010 Understanding superannuation and superannuation contributions Superannuation is an investment vehicle designed to assist Australians in saving for their retirement. The Government

CLIENT FACT SHEET July 2010 Understanding superannuation and superannuation contributions Superannuation is an investment vehicle designed to assist Australians in saving for their retirement. The Government

SMSF Contributions Getting Assets into your SMSF

Getting Assets into your SMSF Agenda What is a contribution? When is a contribution made? In-Specie transfer of assets Contribution caps Contribution strategies How can we help? What is a Contribution?

Getting Assets into your SMSF Agenda What is a contribution? When is a contribution made? In-Specie transfer of assets Contribution caps Contribution strategies How can we help? What is a Contribution?

Understanding tax Version 5.0

Understanding tax Version 5.0 This document provides some additional information to help you understand the financial planning concepts discussed in the SOA in relation to tax. This document has been published

Understanding tax Version 5.0 This document provides some additional information to help you understand the financial planning concepts discussed in the SOA in relation to tax. This document has been published

Understanding Superannuation

Understanding Superannuation Client Fact Sheet July 2012 Superannuation is an investment vehicle designed to assist Australians save for retirement. The Federal Government encourages saving through superannuation

Understanding Superannuation Client Fact Sheet July 2012 Superannuation is an investment vehicle designed to assist Australians save for retirement. The Federal Government encourages saving through superannuation

HOW TO BUY PROPERTY WITHIN YOUR SELF-MANAGED SUPERANNUATION FUND

HOW TO BUY PROPERTY WITHIN YOUR SELF-MANAGED SUPERANNUATION FUND COPYRIGHT All rights reserved. No part of this publication may be reproduced, stored in a retrieval system, or transmitted in any form or

HOW TO BUY PROPERTY WITHIN YOUR SELF-MANAGED SUPERANNUATION FUND COPYRIGHT All rights reserved. No part of this publication may be reproduced, stored in a retrieval system, or transmitted in any form or

Year-end Tax Planning Guide - 30 June 2013 BUSINESSES

Year-end Tax Planning Guide - 30 The end of the financial year is fast approaching. In the lead up to 30 June, this newsletter covers some of the year-end tax planning matters for your consideration. BUSINESSES

Year-end Tax Planning Guide - 30 The end of the financial year is fast approaching. In the lead up to 30 June, this newsletter covers some of the year-end tax planning matters for your consideration. BUSINESSES

2015 YEAR END TAX & SUPERANNUATION PLANNING GUIDE

2015 YEAR END TAX & SUPERANNUATION PLANNING GUIDE We are pleased to provide our year end tax planning guide for 2015. Tax Planning should be done on a regular basis throughout the year. However, these

2015 YEAR END TAX & SUPERANNUATION PLANNING GUIDE We are pleased to provide our year end tax planning guide for 2015. Tax Planning should be done on a regular basis throughout the year. However, these

A Guide to Investing in Property Using a Self Managed Super Fund

A Guide to Investing in Property Using a Self Managed Super Fund Why would I consider a SMSF? I already have a super fund. Self Managed Superannuation Funds (SMSF s) are the fastest growing sector of the

A Guide to Investing in Property Using a Self Managed Super Fund Why would I consider a SMSF? I already have a super fund. Self Managed Superannuation Funds (SMSF s) are the fastest growing sector of the

Self managed superannuation funds. A Financial Planning Technical Guide

Self managed superannuation funds A Financial Planning Technical Guide 2 Self managed superannuation funds What is a self managed 4 superannuation fund (SMSF)? What are the benefits? 4 What are the risks?

Self managed superannuation funds A Financial Planning Technical Guide 2 Self managed superannuation funds What is a self managed 4 superannuation fund (SMSF)? What are the benefits? 4 What are the risks?

Fact Sheet Tax on Super 2009/10

It pays to belong TM Key Focus A tax of 15% applies to concessional (i.e. before tax) contributions. All employer and salary sacrifice contributions will be taxed at the top marginal rate if your super

It pays to belong TM Key Focus A tax of 15% applies to concessional (i.e. before tax) contributions. All employer and salary sacrifice contributions will be taxed at the top marginal rate if your super

Self Managed Super Funds Take charge

Self Managed Super Funds Take charge Gain control of your financial future with a Self-Managed Super Fund (SMSF) About Markiewicz & Co. Markiewicz & Co. is one of Australia s leading full service investment

Self Managed Super Funds Take charge Gain control of your financial future with a Self-Managed Super Fund (SMSF) About Markiewicz & Co. Markiewicz & Co. is one of Australia s leading full service investment

BUSINESS SEMINAR SECURE YOUR BUSINESS AND FUTURE. www.idealtax.com.au

BUSINESS SEMINAR SECURE YOUR BUSINESS AND FUTURE www.idealtax.com.au SEMINAR OUTLINE 1. Federal Budget 2011 2. Small Business Benchmarks 3. Small Business Concessions 4. Tax Return Tips 5. Superannuation

BUSINESS SEMINAR SECURE YOUR BUSINESS AND FUTURE www.idealtax.com.au SEMINAR OUTLINE 1. Federal Budget 2011 2. Small Business Benchmarks 3. Small Business Concessions 4. Tax Return Tips 5. Superannuation

Superannuation. A Financial Planning Technical Guide

Superannuation A Financial Planning Technical Guide 2 Superannuation Contents Superannuation overview 4 Superannuation contributions 4 Superannuation taxation 7 Preservation 9 Beneficiary nomination 9

Superannuation A Financial Planning Technical Guide 2 Superannuation Contents Superannuation overview 4 Superannuation contributions 4 Superannuation taxation 7 Preservation 9 Beneficiary nomination 9

Contributions. Things you should know about making contributions to your SMSF BROUGHT TO YOU BY

Contributions Things you should know about making contributions to your SMSF BROUGHT TO YOU BY CONTENTS Non Concessional Contributions: Aged Under 65... 2 Non Concessional Contributions: Aged 65 to 74...

Contributions Things you should know about making contributions to your SMSF BROUGHT TO YOU BY CONTENTS Non Concessional Contributions: Aged Under 65... 2 Non Concessional Contributions: Aged 65 to 74...

New Ways For High Net Worth Individuals

New Ways For High Net Worth Individuals And Business Owners To Build Wealth Tax Effectively With Introduction A SMSF It may be that the SMSF is the absolute way of the future March 2010 Jeremy Cooper Head

New Ways For High Net Worth Individuals And Business Owners To Build Wealth Tax Effectively With Introduction A SMSF It may be that the SMSF is the absolute way of the future March 2010 Jeremy Cooper Head

SELF MANAGED SUPER FUNDS SMSF

JAMES MERCHAN BBUS (Banking & Finance), Ad.Dip Fin Planning [m] 0433 480 870 [w] 5976 3704 [e] jmerchan@mccombe.com.au SELF MANAGED SUPER FUNDS SMSF SMSF s are the fastest growing sector in the $1.4trillion

JAMES MERCHAN BBUS (Banking & Finance), Ad.Dip Fin Planning [m] 0433 480 870 [w] 5976 3704 [e] jmerchan@mccombe.com.au SELF MANAGED SUPER FUNDS SMSF SMSF s are the fastest growing sector in the $1.4trillion

Year-end Tax Planning Guide - 30 June 2014 BUSINESSES

Year-end Tax Planning Guide - 30 The end of the financial year is fast approaching. In the lead up to 30 June, this newsletter covers some of the year-end tax planning matters for your consideration. BUSINESSES

Year-end Tax Planning Guide - 30 The end of the financial year is fast approaching. In the lead up to 30 June, this newsletter covers some of the year-end tax planning matters for your consideration. BUSINESSES

THE TRUTH ABOUT SMSFs

THE TRUTH Doing it yourself with a Self Managed Super Fund ABOUT SMSFs by Nick Bedding 1 Doing it yourself with a Self Managed Super Fund Table of contents Introduction Chapter One What s it all about?

THE TRUTH Doing it yourself with a Self Managed Super Fund ABOUT SMSFs by Nick Bedding 1 Doing it yourself with a Self Managed Super Fund Table of contents Introduction Chapter One What s it all about?

SMSF strategy paper TB 95. Summary. In-specie transfers. Contents SMSF STRATEGY

TB 95 SMSF strategy paper Issued on 26 September 2012. Summary Self managed superannuation funds (SMSFs) have enjoyed a rapid rise in popularity in recent years. Much of the excitement can be attributed

TB 95 SMSF strategy paper Issued on 26 September 2012. Summary Self managed superannuation funds (SMSFs) have enjoyed a rapid rise in popularity in recent years. Much of the excitement can be attributed

Superannuation Tips and Traps. Kim Guest / Tim Sanderson March 2014

Superannuation Tips and Traps Kim Guest / Tim Sanderson March 2014 Disclaimer This presentation is given by a representative of Colonial First State Investments Limited AFS Licence 232468, ABN 98 002 348

Superannuation Tips and Traps Kim Guest / Tim Sanderson March 2014 Disclaimer This presentation is given by a representative of Colonial First State Investments Limited AFS Licence 232468, ABN 98 002 348

Your guide to super smart strategies.

Your guide to super smart strategies. What you ll find in this guide Learn more about super and discover how the super smart strategies can help you to grow your wealth, make the most of your super and

Your guide to super smart strategies. What you ll find in this guide Learn more about super and discover how the super smart strategies can help you to grow your wealth, make the most of your super and

WARNING. Disclaimer - This e-booklet contains general information only

WARNING Disclaimer - This e-booklet contains general information only This information has been prepared as a general guideline, and is not intended to be an exhaustive or a complete analysis of the topics

WARNING Disclaimer - This e-booklet contains general information only This information has been prepared as a general guideline, and is not intended to be an exhaustive or a complete analysis of the topics

1 What is the role of a financial planner when advising a client about retirement planning?

Questions with Guided Answers by Graeme Colley 2013 Reed International Books Australia Pty Limited trading as LexisNexis. Permission to download and make copies for classroom use is granted. Reproducing

Questions with Guided Answers by Graeme Colley 2013 Reed International Books Australia Pty Limited trading as LexisNexis. Permission to download and make copies for classroom use is granted. Reproducing

SELF MANAGED SUPERANNUATION

SELF MANAGED SUPERANNUATION Position Yourself INFORMATION PACK INFORMATION PACK SELF MANAGED SUPERANNUATION FUNDS SMSF INFORMATION SHEET MAKING THE MOST OF YOUR SUPERANNUATION Self Managed Superannuation

SELF MANAGED SUPERANNUATION Position Yourself INFORMATION PACK INFORMATION PACK SELF MANAGED SUPERANNUATION FUNDS SMSF INFORMATION SHEET MAKING THE MOST OF YOUR SUPERANNUATION Self Managed Superannuation

Understanding superannuation Version 5.0

Understanding superannuation Version 5.0 This document provides some additional information to help you understand the financial planning concepts discussed in the SOA in relation to superannuation. This

Understanding superannuation Version 5.0 This document provides some additional information to help you understand the financial planning concepts discussed in the SOA in relation to superannuation. This

Self-Managed Super Fund Basics and Buying Property with your SMSF Money

RETIRE WITH MORE Self-Managed Super Fund Basics and Buying Property with your SMSF Money YOUR GUIDE TO BUYING PROPERTY WITH YOUR SMSF MONEY $$$ Unit 1, 3 Robinson Place Rockingham WA 6168 admin@integratax.com.au

RETIRE WITH MORE Self-Managed Super Fund Basics and Buying Property with your SMSF Money YOUR GUIDE TO BUYING PROPERTY WITH YOUR SMSF MONEY $$$ Unit 1, 3 Robinson Place Rockingham WA 6168 admin@integratax.com.au

Product Disclosure Statement

AMP Retirement Savings Account Product Disclosure Statement Contents 1. About AMP Retirement Savings Account 2. How super works 3. Benefits of investing with AMP Retirement Savings Account 4. Risks of

AMP Retirement Savings Account Product Disclosure Statement Contents 1. About AMP Retirement Savings Account 2. How super works 3. Benefits of investing with AMP Retirement Savings Account 4. Risks of

SUPERANNUATION. Home Insurance. Super fundamentals. Foundations for your future

SUPERANNUATION Home Insurance Super fundamentals Foundations for your future As one of your most important financial investments, it s worth understanding how superannuation works. For many Australians,

SUPERANNUATION Home Insurance Super fundamentals Foundations for your future As one of your most important financial investments, it s worth understanding how superannuation works. For many Australians,

SMSF Solutions for Advisers & Accountants.

SMSF Solutions for Advisers & Accountants. 1 November 2015 www.multiport.com.au Multiport Pty Ltd ABN 76 097 695 988 AFS LICENCE NO: 291195 Contents Taking the hassle out of SMSF administration and compliance

SMSF Solutions for Advisers & Accountants. 1 November 2015 www.multiport.com.au Multiport Pty Ltd ABN 76 097 695 988 AFS LICENCE NO: 291195 Contents Taking the hassle out of SMSF administration and compliance

Smart End of Financial Year Strategies

Level 7,34 Charles St Parramatta Parramatt NSW 2150 PO Box 103 Parramatta NSW 2124 Phone: 02 9687 1966 Fax: 02 9635 3564 Web: www.carnegie.com.au Build Guide Protect Manage Wealth Smart End of Financial

Level 7,34 Charles St Parramatta Parramatt NSW 2150 PO Box 103 Parramatta NSW 2124 Phone: 02 9687 1966 Fax: 02 9635 3564 Web: www.carnegie.com.au Build Guide Protect Manage Wealth Smart End of Financial

Self Managed Super Funds

a guide to Self Managed Super Funds a guide to Self Managed Super Funds 1 disclaimer This ebook has been prepared by EJM Financial Services in conjunction with AMP Financial Planning Pty Limited, ABN 89

a guide to Self Managed Super Funds a guide to Self Managed Super Funds 1 disclaimer This ebook has been prepared by EJM Financial Services in conjunction with AMP Financial Planning Pty Limited, ABN 89

Self Managed Super Fund Service

Self Managed Super Fund Service Product Disclosure Statement Issued by the trustees Issue date: 15 April 2010 Prepared by Smartsuper Pty Ltd ABN 47 003 822 339 AFS Licence 247120 PO Box 529 North Sydney

Self Managed Super Fund Service Product Disclosure Statement Issued by the trustees Issue date: 15 April 2010 Prepared by Smartsuper Pty Ltd ABN 47 003 822 339 AFS Licence 247120 PO Box 529 North Sydney

21 st CENTURY US ACCOUNTING Q&A TRUST

21 st CENTURY US ACCOUNTING Q&A TRUST Q. WHAT IS A TRUST? A. A trust is a business structure that requires a trustee, a trust and beneficiaries. The trustee holds property and earns and distributes income

21 st CENTURY US ACCOUNTING Q&A TRUST Q. WHAT IS A TRUST? A. A trust is a business structure that requires a trustee, a trust and beneficiaries. The trustee holds property and earns and distributes income

Building and protecting your wealth the tax effective way

Building and protecting your wealth the tax effective way Strategies guide 2014/2015 The lead up to End of Financial Year (EOFY) provides a good opportunity to review your wealth creation plans. At this

Building and protecting your wealth the tax effective way Strategies guide 2014/2015 The lead up to End of Financial Year (EOFY) provides a good opportunity to review your wealth creation plans. At this

THE SUPER BRIEF. UPDATE!!!! ATO knocks back use of SMSF s to fund Buy/ Sell Agreement Life Insurance NEWSLETTER. page 1. ISSUE - October 2014

ISSUE - October 2014 THE SUPER BRIEF UPDATE!!!! ATO knocks back use of SMSF s to fund Buy/ Sell Agreement Life Insurance Clients often use an SMSF to hold life insurance when setting up a Buy Sell Agreement

ISSUE - October 2014 THE SUPER BRIEF UPDATE!!!! ATO knocks back use of SMSF s to fund Buy/ Sell Agreement Life Insurance Clients often use an SMSF to hold life insurance when setting up a Buy Sell Agreement

SUPERANNUATION. Home Insurance. Super fundamentals. Foundations for your future

SUPERANNUATION Home Insurance Super fundamentals Foundations for your future As one of your most important financial investments, it s worth understanding how superannuation works. For many Australians,

SUPERANNUATION Home Insurance Super fundamentals Foundations for your future As one of your most important financial investments, it s worth understanding how superannuation works. For many Australians,

Contributing to your super

SUP E R ANNUATION Contributing to your super GESB Super and West State Super ISSUE DATE: 1 July 2015 PREPARATION DATE: 26 June 2015 Government Employees Superannuation Board ABN 43 418 292 917 Contents

SUP E R ANNUATION Contributing to your super GESB Super and West State Super ISSUE DATE: 1 July 2015 PREPARATION DATE: 26 June 2015 Government Employees Superannuation Board ABN 43 418 292 917 Contents

A DIFFERENT KIND OF WEALTH MANAGEMENT FIRM. www.jaswealth.com.au. Superannuation 101. Everything you always wanted to know but were too afraid to ask

A DIFFERENT KIND OF WEALTH MANAGEMENT FIRM www.jaswealth.com.au Superannuation 101 Everything you always wanted to know but were too afraid to ask What is Superannuation? Superannuation 101 Contents What

A DIFFERENT KIND OF WEALTH MANAGEMENT FIRM www.jaswealth.com.au Superannuation 101 Everything you always wanted to know but were too afraid to ask What is Superannuation? Superannuation 101 Contents What

SMSF Trustee Companion

If you are thinking about setting up a SMSF, there are a number of decisions you will need to make regarding the structure, operation and management of your fund. To help you understand the process and

If you are thinking about setting up a SMSF, there are a number of decisions you will need to make regarding the structure, operation and management of your fund. To help you understand the process and

If you work in Australia, your employer may have to contribute to a superannuation fund for you under the Superannuation Guarantee system if you:

Superannuation is a tax advantaged way of saving for retirement and makes up two of the three pillars of the Government s retirement income policy. The three pillars are: A Government funded means-tested

Superannuation is a tax advantaged way of saving for retirement and makes up two of the three pillars of the Government s retirement income policy. The three pillars are: A Government funded means-tested

How super works. VicSuper FutureSaver Member Guide

How super works VicSuper FutureSaver Member Guide Date prepared 1 July 2015 The information in this document forms part of the VicSuper FutureSaver Product Disclosure Statement (PDS) dated 1 July 2015.

How super works VicSuper FutureSaver Member Guide Date prepared 1 July 2015 The information in this document forms part of the VicSuper FutureSaver Product Disclosure Statement (PDS) dated 1 July 2015.

End of Year Superannuation Fund Circular To all Super Fund Trustees

21 June 2013 End of Year Superannuation Fund Circular To all Super Fund Trustees Maximise year end opportunities and minimise risks The end of the financial year will be here before you know it. In this

21 June 2013 End of Year Superannuation Fund Circular To all Super Fund Trustees Maximise year end opportunities and minimise risks The end of the financial year will be here before you know it. In this

Making the Most of Your Super

Making the Most of Your Super For many people, super is one of the best ways to accumulate wealth. The Government provides tax benefits to encourage people to fund their own retirement. With more Australians

Making the Most of Your Super For many people, super is one of the best ways to accumulate wealth. The Government provides tax benefits to encourage people to fund their own retirement. With more Australians

Super and Tax Advantages for the Self Employed

YOUR SUPER Freelancers, the self-employed & super. If you are self-employed or a freelance or contract worker Media Super can help you understand your super and tax options, and what you can do to maximise

YOUR SUPER Freelancers, the self-employed & super. If you are self-employed or a freelance or contract worker Media Super can help you understand your super and tax options, and what you can do to maximise

AustChoice Super general reference guide (ACH.02)

") AustChoice Super general reference guide (ACH.02) Issued: 28 May 2015 This guide contains important information not included in the AustChoice Super PDS. We recommend you read this entire guide. The information

AustChoice Super general reference guide (ACH.02) Issued: 28 May 2015 This guide contains important information not included in the AustChoice Super PDS. We recommend you read this entire guide. The information

Tax tips and tax return checklist

Tax tips and tax return checklist To help you complete your tax return, the following lists outlines the payments that are classified as income and those that are classified as expenses across a range

Tax tips and tax return checklist To help you complete your tax return, the following lists outlines the payments that are classified as income and those that are classified as expenses across a range

Superannuation: dealing with life s changes

Booklet 2 Superannuation: dealing with life s changes MAStech Smart technical solutions made simple Contents Introduction 01 Introduction 03 Accessing your superannuation benefits 04 Conditions of release

Booklet 2 Superannuation: dealing with life s changes MAStech Smart technical solutions made simple Contents Introduction 01 Introduction 03 Accessing your superannuation benefits 04 Conditions of release

Personal deductible superannuation contributions

Last updated: 1 January 2011 Personal deductible superannuation contributions People who are entirely self employed, such as those operating their business as a sole trader or through a partnership, are

Last updated: 1 January 2011 Personal deductible superannuation contributions People who are entirely self employed, such as those operating their business as a sole trader or through a partnership, are

Retirement made easy. Helping you achieve your retirement goals. rest.com.au/restpension 1300 305 778

Retirement made easy Helping you achieve your retirement goals rest.com.au/restpension 1300 305 778 Helping you achieve your retirement goals As you near retirement you probably have a number of questions

Retirement made easy Helping you achieve your retirement goals rest.com.au/restpension 1300 305 778 Helping you achieve your retirement goals As you near retirement you probably have a number of questions

PRODUCT DISCLOSURE STATEMENT. 02 9331 8664 admin@nowinfinity.com.au www.nowinfinity.com.au PO BOX 1409 Potts Point NSW 1335 ABN 16 154 927 376

PRODUCT DISCLOSURE STATEMENT 02 9331 8664 admin@nowinfinity.com.au www.nowinfinity.com.au PO BOX 1409 Potts Point NSW 1335 ABN 16 154 927 376 SMSF Product Disclosure Statement CONTENTS SMSF Product Disclosure

PRODUCT DISCLOSURE STATEMENT 02 9331 8664 admin@nowinfinity.com.au www.nowinfinity.com.au PO BOX 1409 Potts Point NSW 1335 ABN 16 154 927 376 SMSF Product Disclosure Statement CONTENTS SMSF Product Disclosure

GUIDANCE NOTE - SMSFS & PROPERTY

GUIDANCE NOTE - SMSFS & PROPERTY GUIDANCE FOR CPA AUSTRALIA PUBLIC PRACTITIONERS FINANCIAL ADVISORY SERVICES The decision to establish a self-managed super fund (SMSF) requires careful consideration. While

GUIDANCE NOTE - SMSFS & PROPERTY GUIDANCE FOR CPA AUSTRALIA PUBLIC PRACTITIONERS FINANCIAL ADVISORY SERVICES The decision to establish a self-managed super fund (SMSF) requires careful consideration. While

End of Financial Year Strategies 2014. Aaron Steer AFP Senior Financial Planner

End of Financial Year Strategies 2014 Aaron Steer AFP Senior Financial Planner Disclaimer In preparing this information, Statewide Wealth did not take into account the investment objectives, financial

End of Financial Year Strategies 2014 Aaron Steer AFP Senior Financial Planner Disclaimer In preparing this information, Statewide Wealth did not take into account the investment objectives, financial

How To Save For Retirement

Booklet 1 Getting the best out of your superannuation savings MAStech Smart technical solutions made simple Contents Introduction 01 Introduction 03 Saving through super 08 How a super fund works 09 How

Booklet 1 Getting the best out of your superannuation savings MAStech Smart technical solutions made simple Contents Introduction 01 Introduction 03 Saving through super 08 How a super fund works 09 How

Superannuation What you can do before & after 30 June 2014. SuperStream

NEWS Winter 2014 P (03) 9585 1988 F (03) 9585 1437 E info@griffithsacc.com W griffithsacc.com Page 2 Federal Budget Emerging tax & superannuation issues Page 3 Superannuation What you can do before & after

NEWS Winter 2014 P (03) 9585 1988 F (03) 9585 1437 E info@griffithsacc.com W griffithsacc.com Page 2 Federal Budget Emerging tax & superannuation issues Page 3 Superannuation What you can do before & after

The Flexible Benefits Super Fund

The Flexible Benefits Super Fund Investing for Retirement Towers Watson 2014 Disclaimer The information in this presentation is general advice only. It is not personal advice. This presentation is not

The Flexible Benefits Super Fund Investing for Retirement Towers Watson 2014 Disclaimer The information in this presentation is general advice only. It is not personal advice. This presentation is not

Tax and your CSS benefit

CSF27 04/12 Tax and your CSS benefit Who should read this? All contributing CSS members. What is in this fact sheet? > > What should I know up front? > > My benefits in the CSS > > How are contributions

CSF27 04/12 Tax and your CSS benefit Who should read this? All contributing CSS members. What is in this fact sheet? > > What should I know up front? > > My benefits in the CSS > > How are contributions

Newsletter. Tax Planning 2014 Edition

Newsletter Tax Planning 2014 Edition FEATURED IN THIS ISSUE Employee Superannuation Payments Concessional Contributions Cap Non-Concessional Contributions Cap Small Business Concessions Reversed Write

Newsletter Tax Planning 2014 Edition FEATURED IN THIS ISSUE Employee Superannuation Payments Concessional Contributions Cap Non-Concessional Contributions Cap Small Business Concessions Reversed Write

Super taxes, caps, payments, thresholds and rebates

Fact Sheet Super taxes, caps, payments, thresholds and rebates This fact sheet provides a useful one-stop reference guide to the tax rates, caps, thresholds and rebates that apply or are related to superannuation

Fact Sheet Super taxes, caps, payments, thresholds and rebates This fact sheet provides a useful one-stop reference guide to the tax rates, caps, thresholds and rebates that apply or are related to superannuation

Advanced guide to capital gains tax concessions for small business 2013 14

Guide for small business operators Advanced guide to capital gains tax concessions for small business 2013 14 For more information visit ato.gov.au NAT 3359 06.2014 OUR COMMITMENT TO YOU We are committed

Guide for small business operators Advanced guide to capital gains tax concessions for small business 2013 14 For more information visit ato.gov.au NAT 3359 06.2014 OUR COMMITMENT TO YOU We are committed

HCG Fact Sheet 30 June 2014 End of Financial Year Tax planning strategies

HCG Fact Sheet 30 June 2014 End of Financial Year Tax planning strategies If you are an employee, consider Sacrificing your pre-tax salary or bonus into super rather than receiving it as cash so you can

HCG Fact Sheet 30 June 2014 End of Financial Year Tax planning strategies If you are an employee, consider Sacrificing your pre-tax salary or bonus into super rather than receiving it as cash so you can

Simplifying Statements of Advice. Retirement strategy example SOA

Simplifying Statements of Advice Retirement strategy example 10 February 2009 Development of FPA example Statements of Advice () Financial planners, politicians, and regulators alike share the common goals

Simplifying Statements of Advice Retirement strategy example 10 February 2009 Development of FPA example Statements of Advice () Financial planners, politicians, and regulators alike share the common goals

SALARY PACKAGING SUPERANNUATION GUIDE TO EMPLOYEES

SALARY PACKAGING SUPERANNUATION GUIDE TO EMPLOYEES Superannuation Introducing Salary Packaging Salary packaging has been made available to all staff of the University through the Enterprise Agreement process.

SALARY PACKAGING SUPERANNUATION GUIDE TO EMPLOYEES Superannuation Introducing Salary Packaging Salary packaging has been made available to all staff of the University through the Enterprise Agreement process.

Tax planning reminders for 30 June 2012

Tax planning reminders for 30 June 2012 Keep your receipts!... 1 Government Co-contributions... 1 Personal deductible contributions... 3 Split super with your spouse... 3 Employer Superannuation Contributions...

Tax planning reminders for 30 June 2012 Keep your receipts!... 1 Government Co-contributions... 1 Personal deductible contributions... 3 Split super with your spouse... 3 Employer Superannuation Contributions...

Guide for notice of intent to claim a tax deduction for personal super contributions 2014/2015

Guide for notice of intent to claim a tax deduction for personal super contributions 2014/2015 Under section 290-170 of the Income Tax Assessment Act 1997 Need Help? For more information about your eligibility

Guide for notice of intent to claim a tax deduction for personal super contributions 2014/2015 Under section 290-170 of the Income Tax Assessment Act 1997 Need Help? For more information about your eligibility

Structuring & Tax. Ensuring your plans for your super become a reality. By Ben Andreou Partner Head of Structuring & Tax

Structuring & Tax Ensuring your plans for your super become a reality By Ben Andreou Partner Head of Structuring & Tax December 2015 Table of Contents Page Why should you read this paper?... 3 Background...

Structuring & Tax Ensuring your plans for your super become a reality By Ben Andreou Partner Head of Structuring & Tax December 2015 Table of Contents Page Why should you read this paper?... 3 Background...

Super Strategies. 15 ways to retire with more.

Super Strategies. 15 ways to retire with more. FOURTH EDITION, FEBRUARY 2011 1 The Retirement Revolution. This book has been written to help you understand the key changes for superannuation and provide

Super Strategies. 15 ways to retire with more. FOURTH EDITION, FEBRUARY 2011 1 The Retirement Revolution. This book has been written to help you understand the key changes for superannuation and provide

Tax on contributions. Non-concessional (after tax) contribution caps. Age at 1 July 2015 Annual cap Tax rate Under 65 $180,000* Nil 65-74 $180,000 Nil

contribution caps. Age at 1 July 2015 Annual cap Tax rate Under 65 $180,000* Nil 65-74 $180,000 Nil") This section summarises the main Federal Government taxes that apply to superannuation at the time of preparation. For more information, contact MyLife MySuper on 1300 MYLIFE (695 433) or the Australian

This section summarises the main Federal Government taxes that apply to superannuation at the time of preparation. For more information, contact MyLife MySuper on 1300 MYLIFE (695 433) or the Australian

How super is taxed. VicSuper FutureSaver Member Guide

How super is taxed VicSuper FutureSaver Member Guide Date prepared 1 July 2015 The information in this document forms part of the VicSuper FutureSaver Product Disclosure Statement (PDS) dated 1 July 2015.

How super is taxed VicSuper FutureSaver Member Guide Date prepared 1 July 2015 The information in this document forms part of the VicSuper FutureSaver Product Disclosure Statement (PDS) dated 1 July 2015.

2016/17 Budget. 1. Effective Budget Night 7.30pm (AEST) 3 May 2016. 1.1 New lifetime cap for non-concessional superannuation contributions

3 May 2016. 1.1 New lifetime cap for non-concessional superannuation contributions") 2016/17 Budget Superannuation reform changes 1. Effective Budget Night 7.30pm (AEST) 3 May 2016 1.1 New lifetime cap for non-concessional superannuation contributions The government will introduce a $500,000

2016/17 Budget Superannuation reform changes 1. Effective Budget Night 7.30pm (AEST) 3 May 2016 1.1 New lifetime cap for non-concessional superannuation contributions The government will introduce a $500,000

borrow Want to in your SMSF?

borrow Want to to buy property in your SMSF? A Self Managed Super Fund (SMSF) gives you investment flexibility. Some typical investment options for SMSFs include term deposits, direct shares, and managed

borrow Want to to buy property in your SMSF? A Self Managed Super Fund (SMSF) gives you investment flexibility. Some typical investment options for SMSFs include term deposits, direct shares, and managed

Advanced guide to capital gains tax concessions for small business 2012 13

Guide for small business operators Advanced guide to capital gains tax concessions for small business 2012 13 For more information visit ato.gov.au NAT 3359 06.2013 OUR COMMITMENT TO YOU We are committed

Guide for small business operators Advanced guide to capital gains tax concessions for small business 2012 13 For more information visit ato.gov.au NAT 3359 06.2013 OUR COMMITMENT TO YOU We are committed

Your Super Guide. Product Disclosure Statement 15 December 2014 Nestlé Super Insured Accumulation category. Contents. Important Information

Australia Group Superannuation Fund Your Super Guide Product Disclosure Statement 15 December 2014 Nestlé Super Insured Accumulation category Contents 1 About Nestlé Super p2 2 How super works p2 3 Benefits

Australia Group Superannuation Fund Your Super Guide Product Disclosure Statement 15 December 2014 Nestlé Super Insured Accumulation category Contents 1 About Nestlé Super p2 2 How super works p2 3 Benefits

Your guide to a total solution Ascend self managed super

Your guide to a total solution Ascend self managed super The big picture ISSUE 2 - SEPTEMBER 2009 Components of an SMSF If one member only If 2 to 4 members What is a self managed super fund? Member trustee

Your guide to a total solution Ascend self managed super The big picture ISSUE 2 - SEPTEMBER 2009 Components of an SMSF If one member only If 2 to 4 members What is a self managed super fund? Member trustee

Super Saver Induction Booklet

VISION SUPER YOUR INDUSTRY SUPER FUND Super Saver Induction Booklet December 2013 99 Low fees and great value for money 99 Automatic Income Protection and Death & Disability cover 99 No commissions or

VISION SUPER YOUR INDUSTRY SUPER FUND Super Saver Induction Booklet December 2013 99 Low fees and great value for money 99 Automatic Income Protection and Death & Disability cover 99 No commissions or

Issued September 2015. Salary Sacrifice. Salary Sacrifice. Grow your super. and pay less tax

Issued 12 Salary December 10 Sacrifice Salary Sacrifice Issued September 2015 Grow your super and pay less tax What is salary sacrifice? Salary sacrifice is an arrangement with your employer to pay part

Issued 12 Salary December 10 Sacrifice Salary Sacrifice Issued September 2015 Grow your super and pay less tax What is salary sacrifice? Salary sacrifice is an arrangement with your employer to pay part

Understanding gearing Version 5.0

Understanding gearing Version 5.0 This document provides some additional information to help you understand the financial planning concepts discussed in the SOA in relation to gearing. This document has

Understanding gearing Version 5.0 This document provides some additional information to help you understand the financial planning concepts discussed in the SOA in relation to gearing. This document has

What is Superannuation and how do Self Managed Superannuation Funds Work?

What is Superannuation and how do Self Managed Superannuation Funds Work? Superannuation is a long-term arrangement that operates primarily to provide income in retirement. Superannuation involves employers,

What is Superannuation and how do Self Managed Superannuation Funds Work? Superannuation is a long-term arrangement that operates primarily to provide income in retirement. Superannuation involves employers,

Lump Sum My Retirement

Lump Sum My Retirement General advice warning The schemes administered by Super SA are exempt public sector schemes and therefore we are not required to hold an Australian Financial Services licence to

Lump Sum My Retirement General advice warning The schemes administered by Super SA are exempt public sector schemes and therefore we are not required to hold an Australian Financial Services licence to

Count. The. Report. Drive your wealth strategy this EOFY. Choosing to insure inside or outside super. Useful apps to monitor your spending

Count The Report Drive your wealth strategy this EOFY Choosing to insure inside or outside super Useful apps to monitor your spending WINTER 2015 ISSUE NO. 120 Welcome A message from the CEO Welcome to

Count The Report Drive your wealth strategy this EOFY Choosing to insure inside or outside super Useful apps to monitor your spending WINTER 2015 ISSUE NO. 120 Welcome A message from the CEO Welcome to

The Expatriate Financial Guide to

The Expatriate Financial Guide to Australian Tax Facts Australia Introduction Tax Year Assessment Basis Income Tax Taxation in Australia is mostly at a national/federal level with property taxes (council

The Expatriate Financial Guide to Australian Tax Facts Australia Introduction Tax Year Assessment Basis Income Tax Taxation in Australia is mostly at a national/federal level with property taxes (council

Tax and Small Business: Navigating the ATO minefield as June 30 draws closer

June 23, 2015 Tax and Small Business: Navigating the ATO minefield as June 30 draws closer The small business sector has variously been described as the engine room of the economy, as well as the biggest

June 23, 2015 Tax and Small Business: Navigating the ATO minefield as June 30 draws closer The small business sector has variously been described as the engine room of the economy, as well as the biggest

Some proven financial advice strategies

Some proven financial advice strategies There are numerous key financial advice strategies that may put you on the road to achieving your financial goals Debt Management Debt consolidation can lower repayments

Some proven financial advice strategies There are numerous key financial advice strategies that may put you on the road to achieving your financial goals Debt Management Debt consolidation can lower repayments

Financial Services with a Personal Touch

Financial Services with a Personal Touch CONCESSIONAL CONTRIBUTIONS CAP Concessional contributions include: employer contributions (including contributions made under a salary sacrifice arrangement) personal

Financial Services with a Personal Touch CONCESSIONAL CONTRIBUTIONS CAP Concessional contributions include: employer contributions (including contributions made under a salary sacrifice arrangement) personal

TAX TUTOR INSIDE IS YOUR TAX GUIDE FOR 2013-2014

TAX TUTOR INSIDE IS YOUR TAX GUIDE FOR 2013-2014 PERSONAL TAX PERSONAL INCOME TAX RATES 2013-2014 & 2012-2013 Taxable Income $0 - $18,200 Nil Tax Payable $18,201 - $37,000 19% of excess over $18,200 $37,001

TAX TUTOR INSIDE IS YOUR TAX GUIDE FOR 2013-2014 PERSONAL TAX PERSONAL INCOME TAX RATES 2013-2014 & 2012-2013 Taxable Income $0 - $18,200 Nil Tax Payable $18,201 - $37,000 19% of excess over $18,200 $37,001

n Print clearly, using a BLACK pen only. n Print X in ALL applicable boxes.

Self-managed superannuation fund annual return 2011 Who should complete this annual return? Only self-managed superannuation funds (SMSFs) can complete this annual return All other funds must complete

Self-managed superannuation fund annual return 2011 Who should complete this annual return? Only self-managed superannuation funds (SMSFs) can complete this annual return All other funds must complete

Investing in Property through your Self-Managed

smsfinstitute.com.au The SMSF Guide Book Investing in Property through your Self-Managed Benefits & complexities of adding property to your Superannuation investment portfolio! The General Advice The contents

smsfinstitute.com.au The SMSF Guide Book Investing in Property through your Self-Managed Benefits & complexities of adding property to your Superannuation investment portfolio! The General Advice The contents