4 4 Credit Cards.notebook January 15, Using your learning device to help you, list at least five major credit card companies.

|

|

|

- Erin Jennings

- 8 years ago

- Views:

Transcription

1 Warm-up: Using your learning device to help you, list at least five major credit card companies. Warm-up: Using your learning device to help you, list at least five major credit card companies.

2 Objectives Become familiar with the basic vocabulary of credit cards. Compute an average daily balance. Key Terms credit card impulse buying revolving charge account charge card Truth in Lending Act Fair Credit Billing Act Fair Debt Collection Practices Act debit card Electronic Funds Transfer Act average daily balance mean

3 Vocabulary: impulse buying revolving charge account when a consumer purchases something to which they suddenly were attracted to and had no intention of buying. An account where the entire bill does not have to be paid in full each month. There is a minimum monthly payment, and there is a finance charge the month following any month the bill is not paid in full. Truth in Lending Act This act protects you if your card is lost or stolen. If this happens, notify the creditor who issued the card immediately. You may be partially responsible for charges made by unauthorized users of cards you lose. The maximum liability is $50. You are not responsible for any charges that occur after you notify the creditor. Credit card vs. Charge Card vs. Debit Card A credit card is a plastic card that entitles its holder to make Credit Card purchases and pay for them later. A charge card is a special type of credit card. It allows the cardholder to make purchases in places that accept the card. The monthly bill for all purchases must be paid in full. Charge There is no Card interest charged. Popular charge cards used today include Diner s Club and certain types of American Express cards. Most people informally use the words charge card and credit card interchangeably. A debit card is not a credit or charge card, because there is no creditor extending credit. If you open a debit account, you deposit money into your account, and the debit card acts like an electronic check. You are deducting money directly from your account each time you make a purchase using the Debit Card debit card. You cannot make purchases that exceed the balance in your debit card account. Keeping a record of your debit card activity is exactly like keeping the check register

4 Think & Discuss What do I need to know to use credit cards? What are the monthly responsibilities of a credit card holder? Why might a customer prefer to shop at a store that accepts credit cards over a store that does not accept credit cards? cards/

5 Revolving credit cards can have high interest rates, so it is important to verify that the finance charge on your monthly statement is correct. APR Credit Card Quiz using your BYLD complete the quiz with the link below. finance/debt management/credit cardquiz.htm Importance of Your Credit Score Quiz score/

6 night live/video/dont buy stuff/27169/

7 Answer $50, the maximum liability under the Truth in Lending Act.

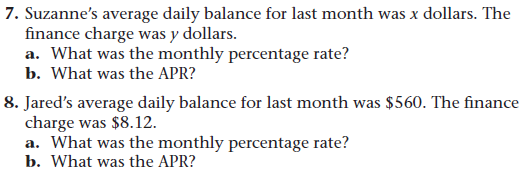

8 Answer 12x The average daily balance is the average of the amounts you owed each day of the billing period. It changes due to purchases made and payments made.

9

10 Finance charges are not charged if, in the previous month, the revolving credit card bill was paid in full. If you pay your card in full every month, you will never pay a finance charge.

11

12 HW p.197 #2-5 & 8

13

14

15

16

lesson six banking services supplemental materials 04/09

lesson six banking services supplemental materials 04/09 banking terms account Money deposited with a financial institution for investment and/or safekeeping purposes. assets Items of monetary value (e.g.,

lesson six banking services supplemental materials 04/09 banking terms account Money deposited with a financial institution for investment and/or safekeeping purposes. assets Items of monetary value (e.g.,

Take Charge of Credit Cards

Take Charge of Credit Cards Get Ready to Take Charge of Your Finances Introductory Level What is Credit? Credit- something is received in exchange for a promise to pay back money in the future Borrower

Take Charge of Credit Cards Get Ready to Take Charge of Your Finances Introductory Level What is Credit? Credit- something is received in exchange for a promise to pay back money in the future Borrower

Students will: Explain the importance of financial literacy. Explain the importance of taking responsibility for personal financial decisions.

Cars, Cards and Currency Lesson 1: Keep the Currency Lesson Description Students participate in a discussion of the general features of a $1 bill. They learn that although currency is valued, people often

Cars, Cards and Currency Lesson 1: Keep the Currency Lesson Description Students participate in a discussion of the general features of a $1 bill. They learn that although currency is valued, people often

Presentation Slides. Lesson Seven. Credit 04/09

Presentation Slides $ Lesson Seven Credit 04/09 advantages and disadvantages of using credit advantages: Able to buy needed items now Don t have to carry cash Creates a record of purchases More convenient

Presentation Slides $ Lesson Seven Credit 04/09 advantages and disadvantages of using credit advantages: Able to buy needed items now Don t have to carry cash Creates a record of purchases More convenient

Lesson 8: Credit Cards Types of Credit Card Accounts

1 Lesson 8: Credit Cards Types of Credit Card Accounts 1. Bank Card Examples: Visa, MasterCard, Discover, American Express Revolving Credit can pay all or some of the bill with the remaining balance put

1 Lesson 8: Credit Cards Types of Credit Card Accounts 1. Bank Card Examples: Visa, MasterCard, Discover, American Express Revolving Credit can pay all or some of the bill with the remaining balance put

Using Credit to Your Advantage Credit Cards and Loans Participant Guide

Hands on Banking Using Credit to Your Advantage The Hands on Banking program is a free public service provided by Wells Fargo. You may also access the program anytime at www.handsonbanking.org & www.elfuturoentusmanos.org

Hands on Banking Using Credit to Your Advantage The Hands on Banking program is a free public service provided by Wells Fargo. You may also access the program anytime at www.handsonbanking.org & www.elfuturoentusmanos.org

Advantages and Disadvantages of Using Credit

1 Lesson 7: About Credit Why Get Credit? To establish a credit history. Advantages and Disadvantages of Using Credit 1. Advantages Able to buy needed items now. Don t have to carry cash. Creates a record

1 Lesson 7: About Credit Why Get Credit? To establish a credit history. Advantages and Disadvantages of Using Credit 1. Advantages Able to buy needed items now. Don t have to carry cash. Creates a record

Responsibilities of Credit. Chapter 18

Responsibilities of Credit Chapter 18 Responsibilities of Consumer Credit To Yourself To Your Creditors Creditors to You Loan Offer I (Mr. Vesper) will loan you $100.00 today if you agree to pay me $105.00

Responsibilities of Credit Chapter 18 Responsibilities of Consumer Credit To Yourself To Your Creditors Creditors to You Loan Offer I (Mr. Vesper) will loan you $100.00 today if you agree to pay me $105.00

Credit Cards. The Language of Credit. Student Loans. Installment Loans 12/17/2015. Quick Response. Unit 4 - Good Debt, Bad Debt: Using Credit Wisely

Quick Response Explain how you think credit cards work. How much do you have to pay every month? What happens if you pay late? What kinds of fees are involved? Unit 4 - Good Debt, Bad Debt: Using Credit

Quick Response Explain how you think credit cards work. How much do you have to pay every month? What happens if you pay late? What kinds of fees are involved? Unit 4 - Good Debt, Bad Debt: Using Credit

How To Understand The Benefits Of Credit Cards

Personal Finance Program TOPIC 4 CREDIT CARDS Credit Cards LESSON 11 Comparing costs and benefits of buying on credit is key to making a good purchase decision. Spending and Credit Standards, Jump$tart

Personal Finance Program TOPIC 4 CREDIT CARDS Credit Cards LESSON 11 Comparing costs and benefits of buying on credit is key to making a good purchase decision. Spending and Credit Standards, Jump$tart

VISA Variable Credit Card Agreement, Overdraft Protection Agreement, and Truth In Lending Disclosure Statement

VISA Variable Credit Card Agreement, Overdraft Protection Agreement, and Truth In Lending Disclosure Statement This is your Cardholder Agreement with Provident Credit Union which outlines the terms to

VISA Variable Credit Card Agreement, Overdraft Protection Agreement, and Truth In Lending Disclosure Statement This is your Cardholder Agreement with Provident Credit Union which outlines the terms to

The Eight Money Smart for Young Adults Modules

The Eight Money Smart for Young Adults Modules 1 1 Module 1: Bank On It 2 2 Module 2: Check It Out 3 3 Check It Out Benefits of checking accounts Types of checking accounts Understanding banking fees Opening

The Eight Money Smart for Young Adults Modules 1 1 Module 1: Bank On It 2 2 Module 2: Check It Out 3 3 Check It Out Benefits of checking accounts Types of checking accounts Understanding banking fees Opening

Teacher's Guide. Lesson Six. Banking Services 04/09

Teacher's Guide $ Lesson Six Banking Services 04/09 banking services websites Students will make wise choices about their banking services once they understand such fundamentals as: selecting and managing

Teacher's Guide $ Lesson Six Banking Services 04/09 banking services websites Students will make wise choices about their banking services once they understand such fundamentals as: selecting and managing

STUDENT MODULE 8.1 ONLINE SHOPPING AND CREDIT CARDS PAGE 1

STUDENT MODULE 8.1 ONLINE SHOPPING AND CREDIT CARDS PAGE 1 Standard 8: The student will describe and explain interest, credit cards, and online commerce. Credit Cards: More Than Plastic Austin receives

STUDENT MODULE 8.1 ONLINE SHOPPING AND CREDIT CARDS PAGE 1 Standard 8: The student will describe and explain interest, credit cards, and online commerce. Credit Cards: More Than Plastic Austin receives

LINX EDUCATIONAL INSTRUCTOR S GUIDE

EXTRA CREDIT: UNDERSTANDING THE DO S & DON TS OF USING CREDIT TAKING CHARGE OF CREDIT: 10 TIPS TO CREDIT DISCIPLINE Use the following suggestions as guidelines to self-discipline to keep your credit in

EXTRA CREDIT: UNDERSTANDING THE DO S & DON TS OF USING CREDIT TAKING CHARGE OF CREDIT: 10 TIPS TO CREDIT DISCIPLINE Use the following suggestions as guidelines to self-discipline to keep your credit in

Credit Card Agreement for GM Card in Capital One, N.A.

Credit Card Agreement for GM Card in Capital One, N.A. There are two parts to this Credit Card Agreement: Capital One Pricing Information and the Capital One Customer Agreement. The Pricing Information

Credit Card Agreement for GM Card in Capital One, N.A. There are two parts to this Credit Card Agreement: Capital One Pricing Information and the Capital One Customer Agreement. The Pricing Information

Teacher's Guide. Lesson Seven. Credit 04/09

Teacher's Guide $ Lesson Seven Credit 04/09 credit websites Consumers may use credit frequently, but many struggle to manage it wisely. To optimize credit and make sound financial decisions, students need

Teacher's Guide $ Lesson Seven Credit 04/09 credit websites Consumers may use credit frequently, but many struggle to manage it wisely. To optimize credit and make sound financial decisions, students need

If you have not established credit, several options can help you obtain a credit card:

Credit Cards The Basics. Do you understand what credit is and how to use it wisely? Like many of today's teenagers and college students, you appreciate the convenience and relative safety of credit cards.

Credit Cards The Basics. Do you understand what credit is and how to use it wisely? Like many of today's teenagers and college students, you appreciate the convenience and relative safety of credit cards.

Credit and Debit Card Scams

Credit and Debit Card Scams What is a credit card scam? It happens when someone uses your credit or debit card information without your permission. It may be as complicated as someone posing as a representative

Credit and Debit Card Scams What is a credit card scam? It happens when someone uses your credit or debit card information without your permission. It may be as complicated as someone posing as a representative

In July 2010, credit card rules will change. In the meantime, here is a guide to current rules, with information about the changes to come, to help

2 In July 2010, credit card rules will change. In the meantime, here is a guide to current rules, with information about the changes to come, to help you when you consider which credit card offer you might

2 In July 2010, credit card rules will change. In the meantime, here is a guide to current rules, with information about the changes to come, to help you when you consider which credit card offer you might

Personal Finance. Mao Ding & Tara Hansen

Personal Finance Mao Ding & Tara Hansen Banking Accounts Checking Account Checking account is either zero interest or very low interest bearing Checking account can have infinitely many transactions No

Personal Finance Mao Ding & Tara Hansen Banking Accounts Checking Account Checking account is either zero interest or very low interest bearing Checking account can have infinitely many transactions No

lesson seven about credit overheads

lesson seven about credit overheads advantages and disadvantages of using credit advantages: Able to buy needed items now Don t have to carry cash Creates a record of purchases More convenient than writing

lesson seven about credit overheads advantages and disadvantages of using credit advantages: Able to buy needed items now Don t have to carry cash Creates a record of purchases More convenient than writing

Lesson 13 Take Control of Debt: Become a Savvy Borrower

Lesson 13 Take Control of Debt: Become a Savvy Borrower Lesson Description After reviewing the difference between term loans and revolving credit, students analyze a fictitious character s use of credit

Lesson 13 Take Control of Debt: Become a Savvy Borrower Lesson Description After reviewing the difference between term loans and revolving credit, students analyze a fictitious character s use of credit

Credit and Debt Management module

Credit and Debt Management module Trainer s introduction Credit and debt probably cause more serious consumer problems than any other topic. It s relatively easy to take on debt, but harder to manage it

Credit and Debt Management module Trainer s introduction Credit and debt probably cause more serious consumer problems than any other topic. It s relatively easy to take on debt, but harder to manage it

Revolving credit: A consumer line of credit that can be used up to a certain limit or paid down at any time.

TEACHER GUIDE 8.1 CREDIT CARDS AND ONLINE SHOPPING PAGE 1 Standard 8: The student will describe and explain interest, credit cards, and online commerce. Credit Cards: More Than Plastic Priority Academic

TEACHER GUIDE 8.1 CREDIT CARDS AND ONLINE SHOPPING PAGE 1 Standard 8: The student will describe and explain interest, credit cards, and online commerce. Credit Cards: More Than Plastic Priority Academic

Update: On November 4, 2009, the day that this revised brochure was to go to print,

In May 2009, President Obama signed into law the Credit Card Accountability Responsibility and Disclosure Act (CARD Act) to strengthen consumer credit card protections. The bulk of the new law becomes

In May 2009, President Obama signed into law the Credit Card Accountability Responsibility and Disclosure Act (CARD Act) to strengthen consumer credit card protections. The bulk of the new law becomes

Chapter Objectives. Chapter 6. Short Term Credit Management. Major Topics. Reasons for Using Credit. How to Get Credit. Disadvantages of Using Credit

Chapter Objectives Chapter 6. Short Term Credit Management To evaluate reasons for and against using credit and decide whether or not credit is appropriate for you. To be able to take the necessary steps

Chapter Objectives Chapter 6. Short Term Credit Management To evaluate reasons for and against using credit and decide whether or not credit is appropriate for you. To be able to take the necessary steps

Understanding Credit

Teacher's Guide $ Lesson Seven Understanding Credit 01/11 understanding credit websites websites for understanding credit The internet is probably the most extensive and dynamic source of information in

Teacher's Guide $ Lesson Seven Understanding Credit 01/11 understanding credit websites websites for understanding credit The internet is probably the most extensive and dynamic source of information in

Take Charge of Credit Cards Note Taking Guide

2.4.1.L1 Note taking guide Take Charge of Credit Cards Note Taking Guide Total Points Earned Total Points Possible Percentage What is credit? A credit card is a form of credit! What is interest? What is

2.4.1.L1 Note taking guide Take Charge of Credit Cards Note Taking Guide Total Points Earned Total Points Possible Percentage What is credit? A credit card is a form of credit! What is interest? What is

MODULE 3 // CREDIT, DEBIT & PREPAID CARDS HALL OF FAME: AGES 18+

MODULE 3 // CREDIT, DEBIT & PREPAID CARDS HALL OF FAME: AGES 18+ MODULE 3 // FINANCIAL FOOTBALL PROGRAM Financial Football is an interactive game designed to acquaint students with the personal financial

MODULE 3 // CREDIT, DEBIT & PREPAID CARDS HALL OF FAME: AGES 18+ MODULE 3 // FINANCIAL FOOTBALL PROGRAM Financial Football is an interactive game designed to acquaint students with the personal financial

0.00% Introductory APR for seven cycles

Account Opening Disclosures Interest Rates and Interest Charges St. Mary s Bank Visa Platinum Business Annual Percentage Rate (APR) for Purchases APR for Balance Transfers APR for Cash or ATM Advances

Account Opening Disclosures Interest Rates and Interest Charges St. Mary s Bank Visa Platinum Business Annual Percentage Rate (APR) for Purchases APR for Balance Transfers APR for Cash or ATM Advances

Using Credit to Your Advantage.

Using Credit to Your Advantage. Topic Overview. The Using Credit To Your Advantage topic will provide participants with all the basic information they need to understand credit what it is and how to make

Using Credit to Your Advantage. Topic Overview. The Using Credit To Your Advantage topic will provide participants with all the basic information they need to understand credit what it is and how to make

The ABCs of Credit Credit Scores Establishing Credit Maintaining Good Credit Credit Cards Managing Credit Challenges

The ABCs of Credit Credit Scores Establishing Credit Maintaining Good Credit Credit Cards Managing Credit Challenges CREDIT DEFINITIONS Credit Trust given to another person for future payment of a loan,

The ABCs of Credit Credit Scores Establishing Credit Maintaining Good Credit Credit Cards Managing Credit Challenges CREDIT DEFINITIONS Credit Trust given to another person for future payment of a loan,

The Basics of Accounting ACCT 201

The Basics of Accounting ACCT 201 Content Accounting definition Accounting equation Accounting elements Asset, Liabilities, & Equity Transactions Accounts Receivable vs Accounts Payable Retained Earnings

The Basics of Accounting ACCT 201 Content Accounting definition Accounting equation Accounting elements Asset, Liabilities, & Equity Transactions Accounts Receivable vs Accounts Payable Retained Earnings

Cash or Credit? LESSON LESSON DESCRIPTION AND BACKGROUND TIME REQUIRED MATERIALS ECONOMIC AND PERSONAL FINANCE CONCEPTS ADDITIONAL RESOURCES

LESSON Cash or Credit? LESSON DESCRIPTION AND BACKGROUND Most students are aware of the variety of payment options available to consumers. Cash, checks, debit cards, and credit cards are often used by

LESSON Cash or Credit? LESSON DESCRIPTION AND BACKGROUND Most students are aware of the variety of payment options available to consumers. Cash, checks, debit cards, and credit cards are often used by

Brought to you by PEPCO FCU. Seminar objectives

Take Charge: Wise Use of Credit Cards Brought to you by PEPCO FCU Seminar objectives Learn: Benefits and costs of credit cards How to build a good credit history Warning signs of too much debt How to figure

Take Charge: Wise Use of Credit Cards Brought to you by PEPCO FCU Seminar objectives Learn: Benefits and costs of credit cards How to build a good credit history Warning signs of too much debt How to figure

Personal Finance Standards (Assignment Code #22210)

") Personal Finance Standards (Assignment Code #22210) Rationale Statement: A citizen that lives within his or her income has more control over his or her life while expanding choices. Having the knowledge

Personal Finance Standards (Assignment Code #22210) Rationale Statement: A citizen that lives within his or her income has more control over his or her life while expanding choices. Having the knowledge

Credit card: permits consumers to purchase items while deferring payment

General Payment Systems Cash: portable, no authentication, instant purchasing power, allows for micropayments, no transaction fee for using it, anonymous But Easily stolen, no float time, can t easily

General Payment Systems Cash: portable, no authentication, instant purchasing power, allows for micropayments, no transaction fee for using it, anonymous But Easily stolen, no float time, can t easily

About Credit. Financial Literacy

About Credit Financial Literacy What is Credit? Credit is the ability to borrow money with a promise of future payment. Why borrow? Goals - car, appliances, furniture, etc Home Education Health Plan your

About Credit Financial Literacy What is Credit? Credit is the ability to borrow money with a promise of future payment. Why borrow? Goals - car, appliances, furniture, etc Home Education Health Plan your

This APR may be applied to your account if you: apply?:

Interest Rates and Interest Charges Annual Percentage Rate (APR) for Purchases APR for Balance Transfers APR for Cash Advances 6.49%a, 7.49%b, 8.49%c, 9.49%d 6.49%a, 7.49%b, 8.49%c, 9.49%d 6.49%a, 7.49%b,

Interest Rates and Interest Charges Annual Percentage Rate (APR) for Purchases APR for Balance Transfers APR for Cash Advances 6.49%a, 7.49%b, 8.49%c, 9.49%d 6.49%a, 7.49%b, 8.49%c, 9.49%d 6.49%a, 7.49%b,

It s Your Paycheck! Glossary of Terms

Annual percentage rate The percentage cost of credit on an annual basis and the total cost of credit to the consumer. APR combines the interest paid over the life of the loan and all fees that are paid

Annual percentage rate The percentage cost of credit on an annual basis and the total cost of credit to the consumer. APR combines the interest paid over the life of the loan and all fees that are paid

WHAT IS A CREDIT CARD?

WHAT IS A CREDIT CARD? A credit card allows you to make purchases based on your promise to pay for the good and/or services. Credit cards allow the holder to get something today and pay for it later. BEFORE

WHAT IS A CREDIT CARD? A credit card allows you to make purchases based on your promise to pay for the good and/or services. Credit cards allow the holder to get something today and pay for it later. BEFORE

Credit Card. Application. Money Smarts for Kids. Money Skills for Life. Member FDIC. What to Know About Credit Cards. Completing a Credit Application

Credit Card Application What to Know About Credit Cards What do I need to know about applying for credit? A credit card is used to charge things, like a meal in a restaurant, clothes for school or on-line

Credit Card Application What to Know About Credit Cards What do I need to know about applying for credit? A credit card is used to charge things, like a meal in a restaurant, clothes for school or on-line

Using Banking Services

Teacher's Guide $ Lesson Six Using Banking Services 04/09 using banking services websites websites for banking services The internet is probably the most extensive and dynamic source of information in

Teacher's Guide $ Lesson Six Using Banking Services 04/09 using banking services websites websites for banking services The internet is probably the most extensive and dynamic source of information in

GFCU_FusionBookofMoney.qxd 4/15/11 9:47 PM Page 1. Give Yourself Some Credit! A Greylock Federal Credit Union Financial Literacy Guide

GFCU_FusionBookofMoney.qxd 4/15/11 9:47 PM Page 1 Give Yourself Some Credit! A Greylock Federal Credit Union Financial Literacy Guide GFCU_FusionBookofMoney.qxd 4/15/11 9:47 PM Page 2 Contents How Does

GFCU_FusionBookofMoney.qxd 4/15/11 9:47 PM Page 1 Give Yourself Some Credit! A Greylock Federal Credit Union Financial Literacy Guide GFCU_FusionBookofMoney.qxd 4/15/11 9:47 PM Page 2 Contents How Does

MOBILOIL FCU 1810 N Major Dr Beaumont, TX 77713 CREDIT CARD AGREEMENT AND DISCLOSURE STATEMENT

MOBILOIL FCU 1810 N Major Dr Beaumont, TX 77713 CREDIT CARD AGREEMENT AND DISCLOSURE STATEMENT Annual Percentage Rate (APR) for purchases and cash advances 2.99% fixed rate (purchases and/or cash advances)

MOBILOIL FCU 1810 N Major Dr Beaumont, TX 77713 CREDIT CARD AGREEMENT AND DISCLOSURE STATEMENT Annual Percentage Rate (APR) for purchases and cash advances 2.99% fixed rate (purchases and/or cash advances)

Taking Control of Your Finances A Plan to Reduce Debt and Build Savings

Taking Control of Your Finances A Plan to Reduce Debt and Build Savings From Credit to Debt A Slippery Slope Purchasing on credit reflects confidence in our ability to pay We often use credit to buy what

Taking Control of Your Finances A Plan to Reduce Debt and Build Savings From Credit to Debt A Slippery Slope Purchasing on credit reflects confidence in our ability to pay We often use credit to buy what

Visa Account Rates, Fees and Terms

Visa Account Rates, Fees and Terms INTEREST RATES AND INTEREST CHARGES Annual Percentage Rate (APR) for Purchases, Cash Advances, and Balance Transfers Visa Classic 8.9% to 17..9% Visa Platinum 8.4% to

Visa Account Rates, Fees and Terms INTEREST RATES AND INTEREST CHARGES Annual Percentage Rate (APR) for Purchases, Cash Advances, and Balance Transfers Visa Classic 8.9% to 17..9% Visa Platinum 8.4% to

Teacher Background Looking at statistics one might easily see that the United States is a nation of

Personal Finance Program LESSON 11 Credit Cards Comparing costs and benefits of buying on credit is key to making a good purchase decision. Money Management Standards, Jump$tart Coalition Benchmarks Teacher

Personal Finance Program LESSON 11 Credit Cards Comparing costs and benefits of buying on credit is key to making a good purchase decision. Money Management Standards, Jump$tart Coalition Benchmarks Teacher

HOME EQUITY LINE OF CREDIT

Creditor: STANFORD FEDERAL CREDIT UNION HOME EQUITY LINE OF CREDIT This disclosure contains important information about our Home Equity Line of Credit. You should read it carefully and keep a copy for

Creditor: STANFORD FEDERAL CREDIT UNION HOME EQUITY LINE OF CREDIT This disclosure contains important information about our Home Equity Line of Credit. You should read it carefully and keep a copy for

Standard 7: The student will identify the procedures and analyze the responsibilities of borrowing money.

TEACHER GUIDE 7.2 BORROWING MONEY PAGE 1 Standard 7: The student will identify the procedures and analyze the responsibilities of borrowing money. It Is In Your Interest Priority Academic Student Skills

TEACHER GUIDE 7.2 BORROWING MONEY PAGE 1 Standard 7: The student will identify the procedures and analyze the responsibilities of borrowing money. It Is In Your Interest Priority Academic Student Skills

Margin Account Disclosure Statement

Margin Account Disclosure Statement COR Clearing ( COR ) is furnishing this document to you to provide some basic facts about purchasing securities on margin and to alert you to the risks involved with

Margin Account Disclosure Statement COR Clearing ( COR ) is furnishing this document to you to provide some basic facts about purchasing securities on margin and to alert you to the risks involved with

Loan Lessons. The Low-Down on Loans, Interest and Keeping Your Head Above Water. Course Objectives Learn About:

usbank.com/student financialgenius.usbank.com Course Objectives Learn About: Different Types of Loans How to Qualify for a Loan Different Types of Interest Loan Lessons The Low-Down on Loans, Interest

usbank.com/student financialgenius.usbank.com Course Objectives Learn About: Different Types of Loans How to Qualify for a Loan Different Types of Interest Loan Lessons The Low-Down on Loans, Interest

03.04. Overview. Goal. Time Frame. We become what we behold. We shape our tools and then our tools shape us. Marshall McLuhan

Section 03 Unit 04 Banking Services Credit Cards 03.04. We become what we behold. We shape our tools and then our tools shape us. Marshall McLuhan Overview A credit card can be a useful financial tool.

Section 03 Unit 04 Banking Services Credit Cards 03.04. We become what we behold. We shape our tools and then our tools shape us. Marshall McLuhan Overview A credit card can be a useful financial tool.

KEMBA FINANCIAL CREDIT UNION MASTERCARD/VISA PLATINUM ACCOUNT DETAILS. Either $5 or 3% of the amount of each transfer, whichever is greater

KEMBA FINANCIAL CREDIT UNION MASTERCARD/VISA PLATINUM ACCOUNT DETAILS Interest Rates and Interest Charges Annual Percentage Rate (APR) for Purchases VISA Platinum Rewards Variable 7.99% to 13.99% when

KEMBA FINANCIAL CREDIT UNION MASTERCARD/VISA PLATINUM ACCOUNT DETAILS Interest Rates and Interest Charges Annual Percentage Rate (APR) for Purchases VISA Platinum Rewards Variable 7.99% to 13.99% when

Lessons for Teens - Money Management and Accessibility

Money Management: Help Dollars Make Sense Emily Burris Hester, Coordinator Student Financial Management Center Lesson 2: Opening an independent bank account If your child does not already have some sort

Money Management: Help Dollars Make Sense Emily Burris Hester, Coordinator Student Financial Management Center Lesson 2: Opening an independent bank account If your child does not already have some sort

VISA Platinum Disclosures

VISA Platinum Disclosures Annual Percentage Rate Grace Period for repayment of balances for purchases Method of computing the balance for purchases Annual fee See Current Rate Sheet 25 Days Average Daily

VISA Platinum Disclosures Annual Percentage Rate Grace Period for repayment of balances for purchases Method of computing the balance for purchases Annual fee See Current Rate Sheet 25 Days Average Daily

Student Loans and Credit Reports

Student Loans and Credit Reports Presented by: Debbie Murphy We Will Discuss: The role of credit in personal finance Review of credit terms and factors Impact of student loans on reports and scores Next

Student Loans and Credit Reports Presented by: Debbie Murphy We Will Discuss: The role of credit in personal finance Review of credit terms and factors Impact of student loans on reports and scores Next

Teacher's Guide. Lesson Eight. Credit Cards 04/09

Teacher's Guide $ Lesson Eight Credit Cards 04/09 credit cards websites Before students use credit cards, it's important that they familiarize themselves with: the advantages and disadvantages of credit

Teacher's Guide $ Lesson Eight Credit Cards 04/09 credit cards websites Before students use credit cards, it's important that they familiarize themselves with: the advantages and disadvantages of credit

Credit Card Pros and Cons

Program Name Staff Responsible for Lesson Canton City Schools ABLE/ESOL Dodie Jerzyk Date(s) Used Feb. 15-16, 2011 Civics Category Civics Objective Time Frame II Civic Participation 29 Consumer Economics

Program Name Staff Responsible for Lesson Canton City Schools ABLE/ESOL Dodie Jerzyk Date(s) Used Feb. 15-16, 2011 Civics Category Civics Objective Time Frame II Civic Participation 29 Consumer Economics

Understanding Credit Cards

Understanding Credit Cards INTRODUCTION This brochure can help you understand how credit cards work, become familiar with common terms offered with a credit card, and avoid the dangers of using credit

Understanding Credit Cards INTRODUCTION This brochure can help you understand how credit cards work, become familiar with common terms offered with a credit card, and avoid the dangers of using credit

Loan Lessons. The Low-Down on Loans, Interest and Keeping Your Head Above Water. Course Objectives Learn About:

Loan Lessons Course Objectives Learn About: Different Types of Loans How to Qualify for a Loan Different Types of Interest The Low-Down on Loans, Interest and Keeping Your Head Above Water usbank.com/financialeducation

Loan Lessons Course Objectives Learn About: Different Types of Loans How to Qualify for a Loan Different Types of Interest The Low-Down on Loans, Interest and Keeping Your Head Above Water usbank.com/financialeducation

ELECTRONIC FUND TRANSFERS AGREEMENT AND DISCLOSURE

ELECTRONIC FUND TRANSFERS AGREEMENT AND DISCLOSURE This Electronic Fund Transfers Agreement and Disclosure is the contract which covers your and our rights and responsibilities concerning the electronic

ELECTRONIC FUND TRANSFERS AGREEMENT AND DISCLOSURE This Electronic Fund Transfers Agreement and Disclosure is the contract which covers your and our rights and responsibilities concerning the electronic

Credit Cards Compare Credit Card Offers

Credit Cards Teens are interested in credit cards, and why not? Advertising makes buying look easy when paying by plastic. But there can be high costs associated with using credit cards. Teens need to

Credit Cards Teens are interested in credit cards, and why not? Advertising makes buying look easy when paying by plastic. But there can be high costs associated with using credit cards. Teens need to

Student Activities. Lesson Five. Credit Cards 04/09

Student Activities $ Lesson Five Credit Cards 04/09 shopping for credit Credit card costs and features can vary greatly. This exercise will give you a chance to shop for and compare the costs and features

Student Activities $ Lesson Five Credit Cards 04/09 shopping for credit Credit card costs and features can vary greatly. This exercise will give you a chance to shop for and compare the costs and features

Credit Cards: Advantages & Disadvantages

Credit Cards: Advantages & Disadvantages Latino Community Credit Union & Latino Community Development Center CREDIT CARDS: BUILDING A better FUTURE ADVANTAGES AND DISADVANTAGES Latino Community Credit

Credit Cards: Advantages & Disadvantages Latino Community Credit Union & Latino Community Development Center CREDIT CARDS: BUILDING A better FUTURE ADVANTAGES AND DISADVANTAGES Latino Community Credit

ELECTRONIC FUND TRANSFERS AGREEMENT AND DISCLOSURE

ELECTRONIC FUND TRANSFERS AGREEMENT AND DISCLOSURE This Electronic Fund Transfers Agreement and Disclosure is the contract which covers your and our rights and responsibilities concerning the electronic

ELECTRONIC FUND TRANSFERS AGREEMENT AND DISCLOSURE This Electronic Fund Transfers Agreement and Disclosure is the contract which covers your and our rights and responsibilities concerning the electronic

$uccessful Start and the Office of Student Services Present: EVALUATING CREDIT CARD OFFERS

$uccessful Start and the Office of Student Services Present: EVALUATING CREDIT CARD OFFERS SESSION OBJECTIVES Discuss the importance of credit and credit management Identify how to establish new credit

$uccessful Start and the Office of Student Services Present: EVALUATING CREDIT CARD OFFERS SESSION OBJECTIVES Discuss the importance of credit and credit management Identify how to establish new credit

Credit Card Agreement for VISA Signature and World MasterCard in Capital One Bank (USA), N.A.

, N.A.") Credit Card Agreement for VISA Signature and World MasterCard in Capital One Bank (USA), N.A. There are two parts to this Credit Card Agreement: Capital One Pricing Information and the Capital One Customer

Credit Card Agreement for VISA Signature and World MasterCard in Capital One Bank (USA), N.A. There are two parts to this Credit Card Agreement: Capital One Pricing Information and the Capital One Customer

Chapter 06. What is Consumer Credit? Chapter 6 Learning Objectives. Introduction to Consumer Credit

Chapter 06 Introduction to Consumer Credit McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. 6-1 Chapter 6 Learning Objectives 1. Define consumer credit and analyze

Chapter 06 Introduction to Consumer Credit McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. 6-1 Chapter 6 Learning Objectives 1. Define consumer credit and analyze

Student Activities. Lesson Three. Credit Cards 07/13

Student Activities $ Lesson Three Credit Cards 07/13 shopping for credit Credit card costs and features can vary greatly. This exercise will give you a chance to shop for and compare the costs and features

Student Activities $ Lesson Three Credit Cards 07/13 shopping for credit Credit card costs and features can vary greatly. This exercise will give you a chance to shop for and compare the costs and features

TOP TRUMPS Comparisons of how to pay for goods and services online

Cash Cash is legal tender in the form of bank notes and coins Small value purchases e.g. cafes, shops Pocket money Repaying friends Cash is physically transferred from one person to the next, usually face-to-face

Cash Cash is legal tender in the form of bank notes and coins Small value purchases e.g. cafes, shops Pocket money Repaying friends Cash is physically transferred from one person to the next, usually face-to-face

Credit Cards CARD TRANSACTIONS AND YOU. Credit Cards. A consumer education programme by:

Credit Cards CARD TRANSACTIONS AND YOU Credit Cards A consumer education programme by: CONTENTS 1 Introduction 2 What is a credit card and how it works Applying for a credit card 3 Application process

Credit Cards CARD TRANSACTIONS AND YOU Credit Cards A consumer education programme by: CONTENTS 1 Introduction 2 What is a credit card and how it works Applying for a credit card 3 Application process

Lesson Description. Concepts. Objectives. Content Standards. Cards, Cars and Currency Lesson 3: Banking on Debit Cards

Lesson Description After discussing basic information about debit cards, students work in pairs to balance a bank account statement and calculate the costs of using a debit card irresponsibly. The students

Lesson Description After discussing basic information about debit cards, students work in pairs to balance a bank account statement and calculate the costs of using a debit card irresponsibly. The students

Mortgage Loans. Understand the Terms of Your Loan before You Sign. Mortgage Loans. Standard Home Equity Loans or Second Mortgages

Mortgage Loans Understand the Terms of Your Loan before You Sign This brochure can help you determine what is best for your situation, become familiar with mortgage loan terms, and learn what is involved

Mortgage Loans Understand the Terms of Your Loan before You Sign This brochure can help you determine what is best for your situation, become familiar with mortgage loan terms, and learn what is involved

Charges for making payable to staff Charges for sending out payments made payable to customers

PATTI CHIARI - "A COMPARISON OF CURRENT ACCOUNTS" TABLE SHOWING SIMILARITIES AND DIFFERENCES BETWEEN THE "STANDARD CONDITIONS" IN PATTICHIARI AND THOSE ADOPTED BY THE BANK 1 Account details 2 CURRENT OPERATIONS

PATTI CHIARI - "A COMPARISON OF CURRENT ACCOUNTS" TABLE SHOWING SIMILARITIES AND DIFFERENCES BETWEEN THE "STANDARD CONDITIONS" IN PATTICHIARI AND THOSE ADOPTED BY THE BANK 1 Account details 2 CURRENT OPERATIONS

Welcome! Please Sign in and Fill out the forms: AARP Participant Agreement Student Information/Pre-Assessment

Welcome! Please Sign in and Fill out the forms: AARP Participant Agreement Student Information/Pre-Assessment 1 Sponsored by and developed in collaboration with AARP FOUNDATION FINANCES 50+ TAKING CONTROL

Welcome! Please Sign in and Fill out the forms: AARP Participant Agreement Student Information/Pre-Assessment 1 Sponsored by and developed in collaboration with AARP FOUNDATION FINANCES 50+ TAKING CONTROL

ELECTRONIC FUND TRANSFERS AGREEMENT AND DISCLOSURE

ELECTRONIC FUND TRANSFERS AGREEMENT AND DISCLOSURE This Electronic Fund Transfers Agreement and Disclosure is the contract which covers your and our rights and responsibilities concerning the electronic

ELECTRONIC FUND TRANSFERS AGREEMENT AND DISCLOSURE This Electronic Fund Transfers Agreement and Disclosure is the contract which covers your and our rights and responsibilities concerning the electronic

What We Need to Know About. Credit Management & Credit Repair for Entrepreneurs

What We Need to Know About. Credit Management & Credit Repair for Entrepreneurs What is Credit? When someone lends you money, and you pay them back with interest, they have extended you credit. Credit

What We Need to Know About. Credit Management & Credit Repair for Entrepreneurs What is Credit? When someone lends you money, and you pay them back with interest, they have extended you credit. Credit

Protecting the Rights of Victims of Identity Theft

Protecting the Rights of Victims of Identity Theft II Congreso Internacional del Derecho de los Mercados Bogotá, Colombia Marzo 2015 The views expressed in this presentation are mine and are not necessarily

Protecting the Rights of Victims of Identity Theft II Congreso Internacional del Derecho de los Mercados Bogotá, Colombia Marzo 2015 The views expressed in this presentation are mine and are not necessarily

Actorcard Prepaid Visa Card Terms & Conditions

Actorcard Prepaid Visa Card Terms & Conditions These Terms & Conditions apply to your Actorcard prepaid Visa debit card. Please read them carefully. In these Terms & Conditions: "Account" means the prepaid

Actorcard Prepaid Visa Card Terms & Conditions These Terms & Conditions apply to your Actorcard prepaid Visa debit card. Please read them carefully. In these Terms & Conditions: "Account" means the prepaid

ELECTRONIC FUND TRANSFERS AGREEMENT AND DISCLOSURE

ELECTRONIC FUND TRANSFERS AGREEMENT AND DISCLOSURE This Electronic Fund Transfers Agreement and Disclosure is the contract which covers your and our rights and responsibilities concerning the electronic

ELECTRONIC FUND TRANSFERS AGREEMENT AND DISCLOSURE This Electronic Fund Transfers Agreement and Disclosure is the contract which covers your and our rights and responsibilities concerning the electronic

for Newcomers and New Canadians Module 2 How to Build Credit In Canada Student Workbook

for Newcomers and New Canadians Module 2 How to Build Credit In Canada Student Workbook Welcome! This workshop is about credit. Credit is buying something now, but paying for it later. Credit can be useful

for Newcomers and New Canadians Module 2 How to Build Credit In Canada Student Workbook Welcome! This workshop is about credit. Credit is buying something now, but paying for it later. Credit can be useful

Consumer Decision Making Contest 2001-2002 Study Guide ATM/Debit Cards

Consumer Decision Making Contest 2001-2002 Study Guide ATM/Debit Cards The popularity of ATM (automated teller machine) and debit cards is rising. ATM cards have a longer history than debit cards, but

Consumer Decision Making Contest 2001-2002 Study Guide ATM/Debit Cards The popularity of ATM (automated teller machine) and debit cards is rising. ATM cards have a longer history than debit cards, but

ELECTRONIC FUND TRANSFERS AGREEMENT AND DISCLOSURE

ELECTRONIC FUND TRANSFERS AGREEMENT AND DISCLOSURE This Electronic Fund Transfers Agreement and Disclosure is the contract which covers your and our rights and responsibilities concerning the electronic

ELECTRONIC FUND TRANSFERS AGREEMENT AND DISCLOSURE This Electronic Fund Transfers Agreement and Disclosure is the contract which covers your and our rights and responsibilities concerning the electronic

Credit Report Forensics. Boston University Financial Assistance February 15, 2012 Christina Coviello, Senior Assistant Director

Credit Report Forensics Boston University Financial Assistance February 15, 2012 Christina Coviello, Senior Assistant Director Today s Agenda: What is credit? What is a credit report? How to get a copy

Credit Report Forensics Boston University Financial Assistance February 15, 2012 Christina Coviello, Senior Assistant Director Today s Agenda: What is credit? What is a credit report? How to get a copy

THE LOCAL FEDERAL CREDIT UNION ELECTRONIC FUNDS TRANSFER AGREEMENT AND DISCLOSURE

THE LOCAL FEDERAL CREDIT UNION ELECTRONIC FUNDS TRANSFER AGREEMENT AND DISCLOSURE This Electronic Funds Transfer Agreement is the contract which covers your and our rights and responsibilities concerning

THE LOCAL FEDERAL CREDIT UNION ELECTRONIC FUNDS TRANSFER AGREEMENT AND DISCLOSURE This Electronic Funds Transfer Agreement is the contract which covers your and our rights and responsibilities concerning

ELECTRONIC FUND TRANSFERS AGREEMENT AND DISCLOSURE

ELECTRONIC FUND TRANSFERS AGREEMENT AND DISCLOSURE This Electronic Fund Transfers Agreement and Disclosure is the contract which covers your and our rights and responsibilities concerning the electronic

ELECTRONIC FUND TRANSFERS AGREEMENT AND DISCLOSURE This Electronic Fund Transfers Agreement and Disclosure is the contract which covers your and our rights and responsibilities concerning the electronic

ELECTRONIC FUND TRANSFERS AGREEMENT AND DISCLOSURE WITH APPLICATION

ELECTRONIC FUND TRANSFERS AGREEMENT AND DISCLOSURE WITH APPLICATION This Electronic Fund Transfers Agreement and Disclosure is the contract which covers your and our rights and responsibilities concerning

ELECTRONIC FUND TRANSFERS AGREEMENT AND DISCLOSURE WITH APPLICATION This Electronic Fund Transfers Agreement and Disclosure is the contract which covers your and our rights and responsibilities concerning

Travis County Credit Union MasterCard Credit Card Agreement & Truth in Lending Disclosure

Travis County Credit Union MasterCard Credit Card Agreement & Truth in Lending Disclosure Please retain for personal records This is your MasterCard Credit Card Agreement and Truth-In-Lending disclosure.

Travis County Credit Union MasterCard Credit Card Agreement & Truth in Lending Disclosure Please retain for personal records This is your MasterCard Credit Card Agreement and Truth-In-Lending disclosure.

What will happen to my home?

What will happen to my home? Information about your home when bankruptcy occurs. This section covers the questions you are most likely to want answered about your home if you are made bankrupt: Will I

What will happen to my home? Information about your home when bankruptcy occurs. This section covers the questions you are most likely to want answered about your home if you are made bankrupt: Will I

Take a Liability Risk Quiz: How Well Do You Know Hidden IRS Pitfalls When Lending?

5 Questions Take a Liability Risk Quiz: How Well Do You Know Hidden IRS Pitfalls When Lending? 1 If no federal tax lien has been filed, my collateral is safe. true 1 Your collateral can be seized without

5 Questions Take a Liability Risk Quiz: How Well Do You Know Hidden IRS Pitfalls When Lending? 1 If no federal tax lien has been filed, my collateral is safe. true 1 Your collateral can be seized without

Personal Loans 101: Understanding

Personal Loans 101: Understanding Small Dollar Loans If you are looking for a small loan, you may not be sure where to turn. Most banks and credit unions do not lend small amounts of money. Payday loans

Personal Loans 101: Understanding Small Dollar Loans If you are looking for a small loan, you may not be sure where to turn. Most banks and credit unions do not lend small amounts of money. Payday loans

The first step is to know. coming in so you know how much money you can spend.

Debt Management Budgeting 101 The first step is to know how much money is coming in so you know how much money you can spend. Budgeting Basics: Determine wants vs needs Determine your short term and long

Debt Management Budgeting 101 The first step is to know how much money is coming in so you know how much money you can spend. Budgeting Basics: Determine wants vs needs Determine your short term and long

Establishing Credit Smart investing@your library Series

4 Establishing Credit Credit is the opportunity to borrow money to use now and then repay over time at an agreed upon cost. It s a convenience and an important financial tool if used wisely. Smart investing@your

4 Establishing Credit Credit is the opportunity to borrow money to use now and then repay over time at an agreed upon cost. It s a convenience and an important financial tool if used wisely. Smart investing@your

Lesson 12 Take Control of Debt: Not All Loans Are the Same

Lesson 12 Take Control of Debt: Not All Loans Are the Same Lesson Description This lesson examines the features of a loan with a fixed period of repayment (term loan). After distinguishing these loans

Lesson 12 Take Control of Debt: Not All Loans Are the Same Lesson Description This lesson examines the features of a loan with a fixed period of repayment (term loan). After distinguishing these loans

ELECTRONIC FUNDS TRANSFER

ELECTRONIC FUNDS TRANSFER Ledyard National Bank Main Street Hanover Office 38 S Main St Hanover, NH 03755 June 25, 2012 This disclosure contains information about terms, fees, and interest rates for some

ELECTRONIC FUNDS TRANSFER Ledyard National Bank Main Street Hanover Office 38 S Main St Hanover, NH 03755 June 25, 2012 This disclosure contains information about terms, fees, and interest rates for some

CONSUMER ELECTRONIC FUNDS TRANSFER AND DEBIT CARD AGREEMENT

We, us and our refer to. CONSUMER ELECTRONIC FUNDS TRANSFER AND DEBIT CARD AGREEMENT You and your apply to any individual who has an Account with us and is authorized to initiate the applicable EFTs. Account

We, us and our refer to. CONSUMER ELECTRONIC FUNDS TRANSFER AND DEBIT CARD AGREEMENT You and your apply to any individual who has an Account with us and is authorized to initiate the applicable EFTs. Account

Credit vs. Debit National Conference of State Legislators. Jean Ann Fox Director of Financial Services Consumer Federation of America

Credit vs. Debit National Conference of State Legislators Jean Ann Fox Director of Financial Services Consumer Federation of America Plastic Payments Debit Cards Pay Me Now Paid from funds in an account

Credit vs. Debit National Conference of State Legislators Jean Ann Fox Director of Financial Services Consumer Federation of America Plastic Payments Debit Cards Pay Me Now Paid from funds in an account

PATTI CHIARI - "A COMPARISON OF CURRENT ACCOUNTS"

PATTI CHIARI - "A COMPARISON OF CURRENT ACCOUNTS" TABLE SHOWING SIMILARITIES AND DIFFERENCES BETWEEN THE "STANDARD CONDITIONS" IN PATTICHIARI AND THOSE ADOPTED BY THE BANK inserire il logo della banca

PATTI CHIARI - "A COMPARISON OF CURRENT ACCOUNTS" TABLE SHOWING SIMILARITIES AND DIFFERENCES BETWEEN THE "STANDARD CONDITIONS" IN PATTICHIARI AND THOSE ADOPTED BY THE BANK inserire il logo della banca