Intermediate 1120S Solving S Corp Problems. Handout

|

|

|

- Jared Stewart

- 9 years ago

- Views:

Transcription

1 Intermediate 1120S Solving S Corp Problems Handout June 2011

2 Table of Contents PART 1 Wage and Compensation Issues Loans to Shareholders 3 Reasonable Wage 4 Auto Policy and Health Insurance 5 Sample W-2 Reporting Auto/Health Correctly 6 Retirement Plan Contributions 7 Charitable Contributions 10 Home Office 11 PART 2 Distribution and Basis Issues The Golden Rule 12 Section 351 Tax Free Exchange Sample Statements 13 Calculating basis for a mid-year exchange 14 Sample Completed 351 Statements 18 Calculating Beginning Balance Sheet 19 Ending Balance Sheet 20 Schedule M-1 tie return to books 22 Schedule M-2 Undistributed Income 23 BIG Tax 24 External Basis 26 Example of Excess Distributions -- Debt Relief 27 Example of Excess Distributions Loan to Shareholder 28 TD 9428 Text Open Account TaxBuddha.com 2

3 Loans to Shareholders The issue is a loan may be recharacterized as wages under audit, subject to payroll tax, penalties and interest. Here s what sorts of bad things can happen under recharacterization: Employer A (Correctly classifies payment as wages) UI & ETT (3.5%) $ 245 $ 245 CA SDI (1.1%) 220 PIT (6%) 1,200 FUTA (6.2%) FICA (ER 7.65%) 1,530 1,530 FICA (EE 5.65%) 1,130 FIT (25%) 5,000 Total due for 1 year $ 1,831 $ 9,759 Employer B (Misclassifies payment as loan )* *This example is for one worker paid $20,000 that is recharacterized as Wages, not including penalty and interest. Elements for a good loan: 1.) Note 2.) Note recorded in corporate minutes 3.) Reasonable Interest Rate 4.) Payments made on note 5.) Cancelled checks to prove payments were made per Note TaxBuddha.com 3

1,130 FIT (25%) 5,000 Total due for 1 year $ 1,831 $ 9,759 Employer B (Misclassifies payment as loan )* *This example is for one worker paid $20,000 that is recharacterized as Wages, not")

4 Officer Compensation Reasonable Wage US Department of Labor, Bureau of Labor Statistics is NAICS code for Tax Preparers (I googled this number). Quarterly Census of Employment and Wages Series Id: ENU State: California Area: Contra Costa County, California Industry: NAICS Tax preparation services Owner: Private Size: All establishment sizes Type: Average Annual Pay Year Annual , , , , , , , ,494 : Preliminary. Series Id: ENU State: California Area: Contra Costa County, California Industry: NAICS Accounting and bookkeeping services Owner: Private Size: All establishment sizes Type: Average Annual Pay So it s better to be a bookkeeper than a tax preparer. Year Annual (P) Souce: TaxBuddha.com 4

5 Automobile Policy SAMPLE CORPORATE POLICY to be adopted at a Board of Director s Meeting for an Accountable Plan: The corporation establishes a policy of reimbursing employees for miles driven for the corporation, in an amount equal to the maximum allowable federal deduction per mile, provided the employee submits an expense report documenting the date, mileage, and the business purpose for the trip. Health Insurance The rules about deducting health insurance were relaxed about , now allows a plan in the name of the individual to be paid by the corporation (reimbursed), but greater than 2% shareholders health benefit is not deductible to the corporation. You ll want to include health insurance benefits as part of the officer compensation package voted on at a Board of Director s Meeting also TaxBuddha.com 5

, but greater than 2%")

6 Sample W-2 The proper way to report Auto/Health If you re reporting personal use of a corporate owned automobile, or company paid health insurance for a more than 2% shareholder, you include the value(s) in Box 1 and Box 16, and in Box 14. The taxable benefit is included as wage in Boxes 1 and 16, but not included as wage base for Social Security nor Medicare in boxes 3 and 5. These benefits are not FICA taxable. Include a note or notes in Box 14 as Auto and/or Health with the amounts. These are not deductions for the corporation as either Auto or Health, the corporation deducts these expenses as wage. It becomes income to the employee, and must be reported. The shareholder may be able to deduct the amounts from their personal Form Auto use income is probably just taxable. Health insurance may be deducted as Self-Employed Health Insurance to the limit of wages TaxBuddha.com 6

7 Retirement plan contributions Retirement plan contributions for sole-owner S Corporations can be somewhat confusing. This article is ONLY about SEP s and 401(k)s for 100% owners of S Corporations with no other employees. I don t discuss tax returns for retirement plans. I have also not included the catch up contribution limits for the 401(k). I m presuming in my example the shareholder is under 50 years old. Employees need to be considered in retirement planning, so if you have other employees or expect to have employees someday, I d use a professional administrator. There are two different sources of contributions to retirement plans: Employee and Employer. Money withheld from employees through payroll is called an Elective Deferral. These amounts are excluded from income tax, but are still subject to FICA, FUTA and SDI taxes. Money contributed by an employer is not only excluded from the employee s income tax, but also not subject to FICA, FUTA nor SDI tax, because it is not payroll. The limits on contributions from either source are based on W-2 income. The limits do not include the pass through amounts from the K-1, as these are not earned income. The amount on the K-1 is irrelevant for the retirement plan contribution calculation. When the employer, the S Corporation, makes a contribution towards the shareholder s retirement plan, it is deducted at the corporate level. There is no box on the K-1 to pass through a retirement plan contribution. That pesky 2% rule applies to fringe benefits. I guess a retirement plan is a mainstream benefit? (A side note: Health Insurance IS a fringe benefit, so technically, >2% shareholder health insurance is supposed to be added to the shareholder W-2 in boxes 1 and 17, with the code Health and the amount in box 14. SE Health Insurance is then deducted by the shareholder on the front of their personal 1040 as they are able. Health insurance fringe benefit is not subject to FICA, etc., and not passed through on the K-1, although it sometimes appears there because we don t have control over the W-2). SEP (Simplified Employee Pension) Contribution Deadline and Limits Contributions to a SEP may be made up to the due date of the employer s return, including extensions, and you can set up the plan as you make the contribution. Shareholder Elective Deferrals from the W-2 income do not exist for SEP plans for an S Corporation TaxBuddha.com 7

8 Employer limits for excludable contributions are the lesser of 25% of the shareholder s W-2 wage (sole-proprietors and partners must calculate 25% of 80%, so being a corporation allows an extra 5% contribution), or $46,000 for 2008 ($49,000 for 2009) (IRS Notice ) 401(k) Plan Contribution Deadline and Limits 401(k) plan company contributions are due by the due date of the employer s return including extensions (same as the SEP), but the plan must be established on or before year end (different from the SEP). Elective Deferral payments are normally due within 7 days of the payroll date. You need to pay a professional administrator to write your 401(k) plan to make sure the plan documents allow for the maximum contributions. Shareholder Elective Deferral contributions are limited to the lesser of 100% of employee salary or $15,500 ($16,500 for 2009). Employer contributions to a shareholder 401(k) are limited to 25% of W-2 (Medicare income from box 5), with a maximum of $46,000 ($49,000 for 2009). For the 401(k), the combination of employee deferrals and employer contributions is limited to $46,000 ($49,000 for 2009) so if your W-2 wage is $199,500 you can t get $15,500 Elective Deferral plus another $46k from the corporation. Which is Best? Let s run a comparison for a 100% shareholder of an S Corporation, Bob, who is 46, in 2008 with no other employees who wants to maximize his contribution to his retirement plan. Bob has W-2 wage of $100,000 and K-1 of $60,000 before making a retirement plan contribution. Bob wants to contribute the maximum allowable, and has set up his retirement plan with his pension administrator well in advance. With the SEP The rule is the corporation may contribute the lesser of 25% of W-2 wage or $46,000, so Bob s S corporation contributes $25,000. Bob s W-2 shows $100,000 for all taxes. Bob s K-1 shows $35,000. With the 401(k) The rule is Elective Deferral is the lesser of 100% of W-2 wage or $15,500, so Bob elects $15,500. This happened before year-end, because it came out of Bob s paychecks. Bob s W-2 box 1 and 17 taxable income is lower by $15,500, but FICA, FUTA and SDI are still calculated at the $100,000 wage (ok, ok $100,000 for FICA, $7,000 for FUTA and $86,698 for SDI) TaxBuddha.com 8

9 The rule for the corporate contribution is the lesser of 25% of W-2 wage, or $46,000, so Bob s corporation contributes $25,000 more. Bob s K-1 says $35,000. If you plan ahead, like Bob did, the 401(k) allows more contributions, particularly at lower W-2 wage numbers because the Elective Deferral can be up to 100% of wages. Pages 7-9 are a reprint of an article published in California Enrolled Agent November 2009 Issue, pages TaxBuddha.com 9

10 Charitable Contributions are not deducted by the corporation, they pass thru to the Shareholder for them to deduct to the extent allowable on their personal Schedule A. For a charitable contribution of $1500, for example, here s what shows up on Page 3 of the 1120S: And on the K-1: 2011 TaxBuddha.com 10

11 Home Office Potentially construed as disguised wages Elements for a good home office: 1). Rental agreement between corporation and landlord 2.) Reasonable Rent Charged (not a huge loss or gain) 3.) Cancelled Checks for Rent Paid 4.) 1099-Misc for Rent Paid (box 1) 5.) Schedule E Speers v. Commissioner TC Memo Code Section 280A(a) no deduction, but exception is in Section 280A(c). Rent Paid 2011 TaxBuddha.com 11

no deduction, but exception is in Section 280A(c).")

12 The Golden Rule Income is taxed at least. Once taxed, TaxBuddha.com 12

13 Sample Section 351 Tax Free Exchange Statement 1.) Name and ID of company 2.) Date of Asset Transfer 3.) FMV and Basis of transferred assets 4.) Date of any PLR regarding transfer. Any liabilities assumed by the corporation need to be for a business purpose, and less than the basis of the contributed property, otherwise it is relief of debt and is a taxable event. See Publication 544 for more information TaxBuddha.com 13

14 2011 TaxBuddha.com 14

15 2011 TaxBuddha.com 15

16 2011 TaxBuddha.com 16

17 2011 TaxBuddha.com 17

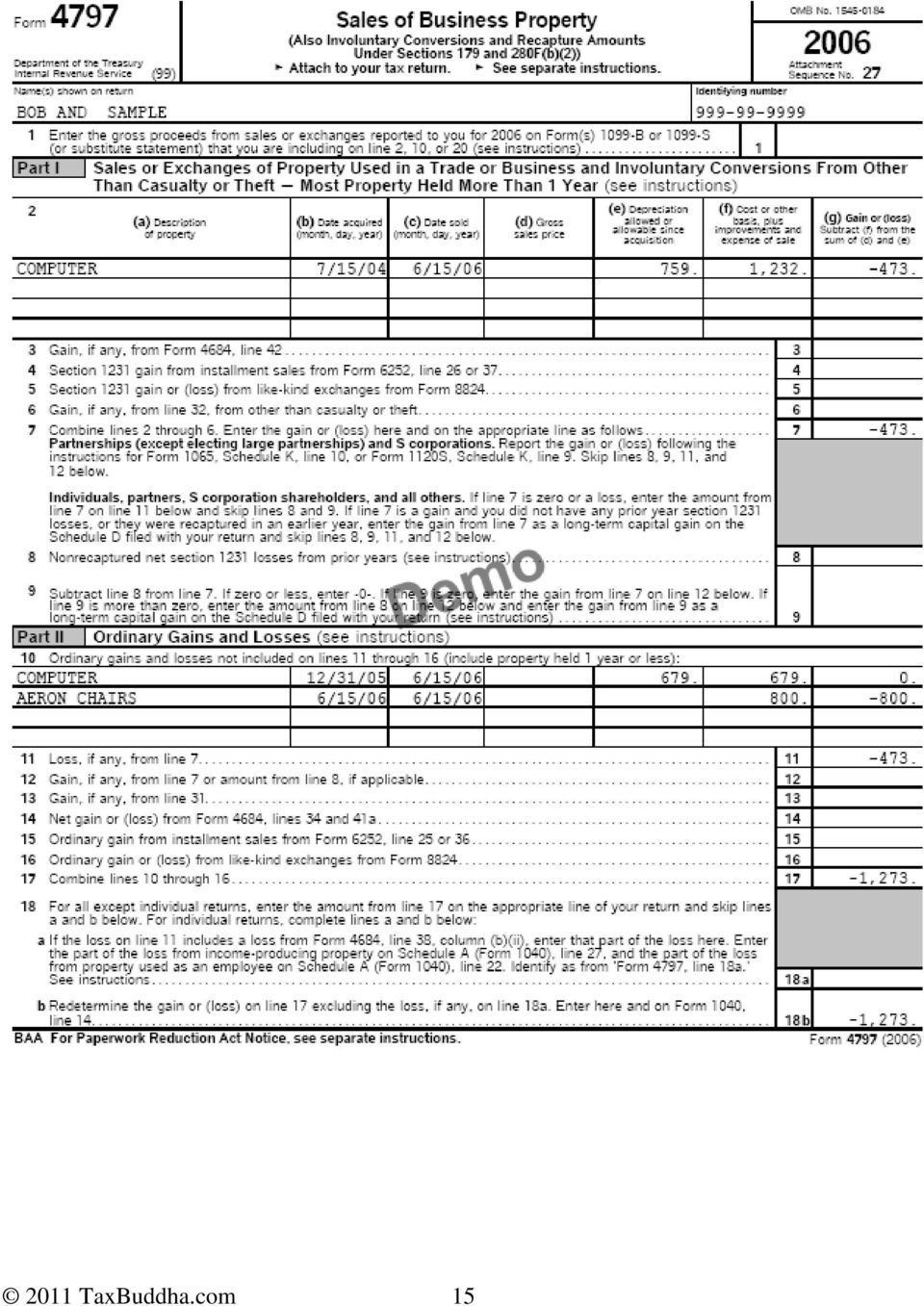

18 Transferors' Code Section 351 Disclosure Statement Name: Bob Sample TIN: Tax Year: 2006 Taxpayer submits the following statement pursuant to the requirements of Reg (a): On 6/15/06 the taxpayer transferred the property listed below to: Name of Corporation: S-Corp of Junk TIN: Address: 1442 A Walnut St #365 Berkeley CA Description of Property Transferred Tax Basis at Property Date of Transfer FMV Computer 04 $473 $200 Computer 05 $0 $300 Aeron Chairs $800 $800 Cash $2,000 $2, Transferors' liabilities assumed by the corporation on the exchange: When and under what circumstances Business Reason Amount and Description as created for assumption $432 Note against Computer 05 Purchase 12/31/05 Attaches to property 2011 TaxBuddha.com 18

19 Beginning Balance Sheet <- Calculated 2011 TaxBuddha.com 19

20 Ending Balance Sheet 1120S Not Eligible for Special Depreciation Used Assets! 2011 TaxBuddha.com 20

21 Ending Balance Sheet 2011 TaxBuddha.com 21

22 Schedule M-1 Ties Tax Return to Books. Accounting income vs. Tax income TaxBuddha.com 22

23 Schedule M-2 Schedule M-2 holds the undistributed income or loss that may affect future tax consequences for the corporation. Losses are different from distributions. Bob has taken the reserve money under the tray in the register he s taken a loss against his contribution for stock in our example. And here s a more interesting example, where the cash register drawer analogy works. The Distributions are like taking money out of the register drawer at year end. It doesn t affect taxation, except when the owner takes more money than was available essentially new income to the owner. Schedule M-2, Column B is for tax exempt income which adjusts basis. Schedule M-2, Column C is for S corporations that were previously C Corporations it keeps track of income that was taxed to the corporation during C status, but has yet to be distributed to the shareholders. If you were never a C corporation, this column will be bank TaxBuddha.com 23

24 BIG Tax, Built In Gains tax applies when you convert a C Corporation to an S Corporation and you have unrealized gains. If the C Corporation has assets that have appreciated, often real estate, the tax on the gain for those assets retains its character and will be taxed at 35% if the assets are sold/disposed of. In our example above, we have a building with a basis of $100,000 that appraised for $1,000,000. GET AN APPRAISAL at conversion! You ll need it if you sell the asset before 10 years have elapsed. You can avoid the BIG tax using the following strategies: 1.) Sell something with a Built In Loss 2.) 1031 Exchange the property with another 3.) Wait 10 years until you sell, or if you have an income limitation. Use loss carryforwards against the income generated by the gain TaxBuddha.com 24

25 Here s an example of BIG tax, if you had an appraisal of $1,000,000 on conversion and sold for 1,500,000. You see the tax is 35% on line TaxBuddha.com 25

26 External Basis Aka Skin in the game this is what the shareholder has invested in the corporation that has been previously taxed, or taxed in the current year. Losses are limited to loss of previously taxed income. Calculate this at the end of each year, and leave yourself a worksheet. This can be different from the internal basis, and is difficult to re-create without lots of time. It s important when terminating the corporation, or selling the stock. Shareholder Basis is increased by Purchase of Stock by shareholder Income from Corporation taxed to shareholder Contributions Qualified Loans made to the corporation (more than a guarantee has to be cash-like) Shareholder Basis is reduced by Business losses taken Section 179 Non-Deductible Expenses Repayment of Qualified Loans Distributions Shareholder selling their stock Charitable contributions 2011 TaxBuddha.com 26

27 Added Credit Card Not OK Better, but relief of debt TaxBuddha.com 27

28 2011 TaxBuddha.com 28 Best so far.

29

30

31

32

33

34

35

36

WithumSmith+Brown, PC Certified Public Accountants and Consultants BE IN A POSITION OF STRENGTH. withum.com

1 Objectives for Today s Webinar What are the different types of K-1s? K-1 line items where do they end up? My income is greater than the cash I received why would that be? 2 What is a Schedule K-1 Form?

1 Objectives for Today s Webinar What are the different types of K-1s? K-1 line items where do they end up? My income is greater than the cash I received why would that be? 2 What is a Schedule K-1 Form?

S Corporation vs. LLC in California Here is an overview of the differences between doing business as an S corporation or as an LLC.

S Corporation vs. LLC in California Here is an overview of the differences between doing business as an S corporation or as an LLC. After you have read this article, we can discuss in detail what would

S Corporation vs. LLC in California Here is an overview of the differences between doing business as an S corporation or as an LLC. After you have read this article, we can discuss in detail what would

S Corporation Tax Organizer

S Corporation Tax Organizer CLIENT INFORMATION S Corporation Name: Email: Date of Incorporation: EIN#: Best Phone#: Corporate Address: Tax Period City: State: ZIP Code: What date was the corporation first

S Corporation Tax Organizer CLIENT INFORMATION S Corporation Name: Email: Date of Incorporation: EIN#: Best Phone#: Corporate Address: Tax Period City: State: ZIP Code: What date was the corporation first

PARTNERSHIP/LLC TAX ORGANIZER (FORM 1065)

") Enclosed is an organizer that provide to our tax clients to assist in gathering the information necessary to prepare the current year tax returns. The Internal Revenue Service matches information returns

Enclosed is an organizer that provide to our tax clients to assist in gathering the information necessary to prepare the current year tax returns. The Internal Revenue Service matches information returns

An Overview of Tax Filing Requirements for Real Estate Broker/Agents

An Overview of Tax Filing Requirements for Real Estate Broker/Agents A two-partner, 25 person firm with 80 years history servicing clients in the areas of: real estate, auditing, accounting, tax, valuation

An Overview of Tax Filing Requirements for Real Estate Broker/Agents A two-partner, 25 person firm with 80 years history servicing clients in the areas of: real estate, auditing, accounting, tax, valuation

Self Employed & Single Member LLC Tax Organizer

Self Employed & Single Member LLC Tax Organizer CLIENT INFORMATION Business Name (DBA): Email: Date of Formation: EIN#: Best Phone#: Business Address: Tax Period City: State: ZIP Code: What date was the

Self Employed & Single Member LLC Tax Organizer CLIENT INFORMATION Business Name (DBA): Email: Date of Formation: EIN#: Best Phone#: Business Address: Tax Period City: State: ZIP Code: What date was the

S-Corporation Tax Organizer Form 1120-S

S-Corporation Tax Organizer Form 1120-S This organizer is provided to help you gather and organize information that will be needed in the preparation of your S-Corporation tax returns. If you are a first

S-Corporation Tax Organizer Form 1120-S This organizer is provided to help you gather and organize information that will be needed in the preparation of your S-Corporation tax returns. If you are a first

OptRight Online: 2013 Year End Customer Guide

November 2013 Wells Fargo Business Payroll Services OptRight Online: 2013 Year End Customer Guide 2013 Wells Fargo Bank N.A. All rights reserved. Member FDIC. Welcome to the 2013 year-end customer guide

November 2013 Wells Fargo Business Payroll Services OptRight Online: 2013 Year End Customer Guide 2013 Wells Fargo Bank N.A. All rights reserved. Member FDIC. Welcome to the 2013 year-end customer guide

Year-End Fringe Benefit Reporting and Other Reporting Requirements

and Other Reporting Requirements November 2013 TO: RE: All Business Clients Year-End Fringe Benefit Reporting and Other Reporting Requirements DATE: November 20, 2013 Certain fringe benefits paid for or

and Other Reporting Requirements November 2013 TO: RE: All Business Clients Year-End Fringe Benefit Reporting and Other Reporting Requirements DATE: November 20, 2013 Certain fringe benefits paid for or

Randall A. Lenz CORPORATION/S-CORPORATION TAX ORGANIZER (1120, 1120S) COMPREHENSIVE

COMPREHENSIVE") Randall A. Lenz Attorney-at-Law Certified Public Accountant 199 14 th Street, NE Suite 1907 Atlanta, Georgia 30309-3688 (404) 815-1731, Cell (404) 323-1731, FAX (404) 815-0717 [email protected]

Randall A. Lenz Attorney-at-Law Certified Public Accountant 199 14 th Street, NE Suite 1907 Atlanta, Georgia 30309-3688 (404) 815-1731, Cell (404) 323-1731, FAX (404) 815-0717 [email protected]

2015 Savvy Year-End Tax Planning Thoughts & Ideas

2015 Savvy Year-End Tax Planning Thoughts & Ideas JONATHAN GASSMAN CFP, CPA/PFS November 11, 2015 2015 Tax Rates Ordinary Income Qualified Dividends & Long-Term Capital Gains 10% 15% 25% 28% 2015 Rates

2015 Savvy Year-End Tax Planning Thoughts & Ideas JONATHAN GASSMAN CFP, CPA/PFS November 11, 2015 2015 Tax Rates Ordinary Income Qualified Dividends & Long-Term Capital Gains 10% 15% 25% 28% 2015 Rates

A Comparison of Entity Taxation

A Comparison of Entity Taxation Sean W. Brewer, CPA Daniel N. Messing, CPA Pugh & Company, P.C. 315 N. Cedar Bluff Road; Suite 200 Knoxville, TN 37923 Sole Proprietorships Single Owner Advantages Easy

A Comparison of Entity Taxation Sean W. Brewer, CPA Daniel N. Messing, CPA Pugh & Company, P.C. 315 N. Cedar Bluff Road; Suite 200 Knoxville, TN 37923 Sole Proprietorships Single Owner Advantages Easy

Tax Return Questionnaire - 2015 Tax Year

SPECTRUM Spectrum Financial Resources LLP FINANCIAL 15021 Ventura Boulevard #341 310.963.4322 T RESOURCES Sherman Oaks, CA 91403 303.942.4322 F www.spectrum-cpa.com Tax Return Questionnaire - 2015 Tax

SPECTRUM Spectrum Financial Resources LLP FINANCIAL 15021 Ventura Boulevard #341 310.963.4322 T RESOURCES Sherman Oaks, CA 91403 303.942.4322 F www.spectrum-cpa.com Tax Return Questionnaire - 2015 Tax

Objectives. Discuss S corp fringe benefits.

S Corporations Objectives Define an S corp. Identify the benefits of being an S corp. Determine how an entity elects to be an S corp. Establish how an S corp is taxed. Describe the S corp shareholder s

S Corporations Objectives Define an S corp. Identify the benefits of being an S corp. Determine how an entity elects to be an S corp. Establish how an S corp is taxed. Describe the S corp shareholder s

Presentation for. CSEA IRS/Practitioner Fall Seminars. S Corporation. Darrell Early, IRS. Date September 27, 2012

Presentation for CSEA IRS/Practitioner Fall Seminars S Corporation Darrell Early, IRS Date September 27, 2012 Agenda What is an S Corporation? Why would a Corporation make the S election? How does a Corporation

Presentation for CSEA IRS/Practitioner Fall Seminars S Corporation Darrell Early, IRS Date September 27, 2012 Agenda What is an S Corporation? Why would a Corporation make the S election? How does a Corporation

Fleming, Tawfall & Company, P.C. 2015 Tax Questionnaire

Fleming, Tawfall & Company, P.C. 2015 Tax Questionnaire COMPLETION OF THIS TAX QUESTIONNAIRE, ALONG WITH YOUR SIGNATURE, IS MANDATORY FOR THE 2015 TAX SEASON. Date of Spouse s Date of Name Birth Name Birth

Fleming, Tawfall & Company, P.C. 2015 Tax Questionnaire COMPLETION OF THIS TAX QUESTIONNAIRE, ALONG WITH YOUR SIGNATURE, IS MANDATORY FOR THE 2015 TAX SEASON. Date of Spouse s Date of Name Birth Name Birth

Martin A. Darocha, CPA Tax and accounting services for individuals and their businesses, estates and trusts. 2015 PAYROLL TAX TOOLKIT December 2014

, CPA Tax and accounting services for individuals and their businesses, estates and trusts. 2015 PAYROLL TAX TOOLKIT December 2014 Following is a brief summary of payroll tax information for 2015. If you

, CPA Tax and accounting services for individuals and their businesses, estates and trusts. 2015 PAYROLL TAX TOOLKIT December 2014 Following is a brief summary of payroll tax information for 2015. If you

RE: - 2015 W-2 REPORTING REQUIREMENTS FOR FRINGE BENEFITS TO BE ADDED TO EMPLOYEES' W-2 AS COMPENSATION

December 2015 To Our Clients: RE: - 2015 W-2 REPORTING REQUIREMENTS FOR FRINGE BENEFITS TO BE ADDED TO EMPLOYEES' W-2 AS COMPENSATION - SPECIAL RULES FOR S-CORPORATION SHAREHOLDERS In this letter, we will

December 2015 To Our Clients: RE: - 2015 W-2 REPORTING REQUIREMENTS FOR FRINGE BENEFITS TO BE ADDED TO EMPLOYEES' W-2 AS COMPENSATION - SPECIAL RULES FOR S-CORPORATION SHAREHOLDERS In this letter, we will

2013 Federal Income Tax Update with The American Taxpayer Relief Act of 2012

THE UNIVERSITY OF TENNESSEE 2013 SINGLETON B. WOLFE MEMORIAL TAX CONFERENCE OCTOBER 31, 2013 2013 Federal Income Tax Update with The American Taxpayer Relief Act of 2012 JOHN D. HOUSTON, CPA Certified

THE UNIVERSITY OF TENNESSEE 2013 SINGLETON B. WOLFE MEMORIAL TAX CONFERENCE OCTOBER 31, 2013 2013 Federal Income Tax Update with The American Taxpayer Relief Act of 2012 JOHN D. HOUSTON, CPA Certified

Module 10 S Corporation/Corporation Workbook Introduction

Module 10 Workbook Introduction Running your own business presents many challenges. One of the most difficult is complying with complex and ever-changing tax laws. This small-business tax education program

Module 10 Workbook Introduction Running your own business presents many challenges. One of the most difficult is complying with complex and ever-changing tax laws. This small-business tax education program

S Corporations General Overview

S Corporations General Overview Richard Furlong Jr. Senior Stakeholder Liaison Define an S Corp An "S corporation" is a an entity that qualifies as a small business corporation that has an S election in

S Corporations General Overview Richard Furlong Jr. Senior Stakeholder Liaison Define an S Corp An "S corporation" is a an entity that qualifies as a small business corporation that has an S election in

Choosing the Right Entity for Maximum Tax Benefits for Your Construction Company

Choosing the Right Entity for Maximum Tax Benefits for Your Construction Company Timely re-evaluation of choice of entity will enhance the shareholder value of your contractor client By Theran J. Welsh

Choosing the Right Entity for Maximum Tax Benefits for Your Construction Company Timely re-evaluation of choice of entity will enhance the shareholder value of your contractor client By Theran J. Welsh

Tax Planning Checklist

Tax Planning Checklist For the year ended 31 March 2014 Contents Year end tax planning checklist 1 General tips on minimising tax 4 Help us to process your records efficiently and quickly 5 Help yourself

Tax Planning Checklist For the year ended 31 March 2014 Contents Year end tax planning checklist 1 General tips on minimising tax 4 Help us to process your records efficiently and quickly 5 Help yourself

PARTNERSHIP/LLC TAX ORGANIZER FORM 1065 (LONG VERSION)

") PARTNERSHIP/LLC TAX ORGANIZER FORM 1065 (LONG VERSION) Enclosed is an organizer that I (we) provide to our tax clients to assist in gathering the information necessary to prepare the current year tax returns.

PARTNERSHIP/LLC TAX ORGANIZER FORM 1065 (LONG VERSION) Enclosed is an organizer that I (we) provide to our tax clients to assist in gathering the information necessary to prepare the current year tax returns.

by: Jana B. Bacon, CPA

Community Bank Auditors Group IRS Requirements Impacting Employee and Customer Tax Filings June 4, 2014 by: Jana B. Bacon, CPA MEMBER OF PKF NORTH AMERICA, AN ASSOCIATION OF LEGALLY INDEPENDENT FIRMS 2013

Community Bank Auditors Group IRS Requirements Impacting Employee and Customer Tax Filings June 4, 2014 by: Jana B. Bacon, CPA MEMBER OF PKF NORTH AMERICA, AN ASSOCIATION OF LEGALLY INDEPENDENT FIRMS 2013

Home Based Business Tax Opportunities RICHEY, MAY & CO., LLP 9605 S. KINGSTON CT., STE. 200 ENGLEWOOD, CO 80112 WWW.RICHEYMAY.COM

Home Based Business Tax Opportunities RICHEY, MAY & CO., LLP 9605 S. KINGSTON CT., STE. 200 ENGLEWOOD, CO 80112 WWW.RICHEYMAY.COM 1 Disclaimer: Use of Information: The information in this summary is provided

Home Based Business Tax Opportunities RICHEY, MAY & CO., LLP 9605 S. KINGSTON CT., STE. 200 ENGLEWOOD, CO 80112 WWW.RICHEYMAY.COM 1 Disclaimer: Use of Information: The information in this summary is provided

1/5/2016. S Corporations. Objectives. Define an S Corp

S Corporations Objectives Define an S corp. Identify the benefits of being an S corp. Determine how an entity elects to be an S corp. Establish how an S corp is taxed. Describe the S corp shareholder s

S Corporations Objectives Define an S corp. Identify the benefits of being an S corp. Determine how an entity elects to be an S corp. Establish how an S corp is taxed. Describe the S corp shareholder s

2015 YEAR-END INDIVIDUAL TAX PLANNING LETTER

2015 YEAR-END INDIVIDUAL TAX PLANNING LETTER Dear Reliance Accounting Clients, At this point in 2015, with the end of the year and the income tax filing deadline on the horizon, tax planning presents more

2015 YEAR-END INDIVIDUAL TAX PLANNING LETTER Dear Reliance Accounting Clients, At this point in 2015, with the end of the year and the income tax filing deadline on the horizon, tax planning presents more

Matheson Associates, LLC 110 S. Jefferson Road Whippany, NJ 07981 973 428 8885

1 R Matheson Associates, LLC 110 S. Jefferson Road Whippany, NJ 07981 973 428 8885 Business Owner's Compliance Checklist Set-up accounting procedures and system for income and expense tracking for tax

1 R Matheson Associates, LLC 110 S. Jefferson Road Whippany, NJ 07981 973 428 8885 Business Owner's Compliance Checklist Set-up accounting procedures and system for income and expense tracking for tax

PARTNERSHIP/LLC TAX ORGANIZER FORM 1065

PARTNERSHIP/LLC TAX ORGANIZER FORM 1065 Enclosed is an organizer that I (we) provide to our tax clients to assist in gathering the informatio n necessary to prepare the current year tax returns. The Internal

PARTNERSHIP/LLC TAX ORGANIZER FORM 1065 Enclosed is an organizer that I (we) provide to our tax clients to assist in gathering the informatio n necessary to prepare the current year tax returns. The Internal

PAYCHEX. Mastering Payroll Compliance. 10 Missteps to Avoid

PAYCHEX Mastering Payroll Compliance 10 Missteps to Avoid Executive Summary. Businesses pay government agencies millions of dollars each year in labor and tax compliance penalties. And, in this economy

PAYCHEX Mastering Payroll Compliance 10 Missteps to Avoid Executive Summary. Businesses pay government agencies millions of dollars each year in labor and tax compliance penalties. And, in this economy

U.S. Income Tax Return for an S Corporation

Form 1120S U.S. Income Tax Return for an S Corporation Do not file this form unless the corporation has filed or is attaching Form 2553 to elect to be an S corporation. Information about Form 1120S and

Form 1120S U.S. Income Tax Return for an S Corporation Do not file this form unless the corporation has filed or is attaching Form 2553 to elect to be an S corporation. Information about Form 1120S and

2015 YEAR-END REFERENCE GUIDE AND CHECK LIST IMPORTANT TAX INFORMATION

2015 YEAR-END REFERENCE GUIDE AND CHECK LIST IMPORTANT TAX INFORMATION This document contains important information that is needed to ensure the accuracy of your W-2 s and other year-end tax returns. Please

2015 YEAR-END REFERENCE GUIDE AND CHECK LIST IMPORTANT TAX INFORMATION This document contains important information that is needed to ensure the accuracy of your W-2 s and other year-end tax returns. Please

Social Security Number: Occupation: Email Address: Current Address (if not listed on W2 form or 1099 Taxpayer Name: Spouse Name: form):

:") For New Clients only - please submit with your forms and documentations TAX RETURN QUESTIONNAIRE - TAX YEAR 2014 Current Address (if not listed on W2 form or 1099 Taxpayer Name: Spouse Name: form): Phone

For New Clients only - please submit with your forms and documentations TAX RETURN QUESTIONNAIRE - TAX YEAR 2014 Current Address (if not listed on W2 form or 1099 Taxpayer Name: Spouse Name: form): Phone

Partnership & LLC s Tax Organizer Form 1065

Partnership & LLC s Tax Organizer Form 1065 This organizer is provided to help you gather and organize information that will be needed in the preparation of your partnership tax returns. If you are a first

Partnership & LLC s Tax Organizer Form 1065 This organizer is provided to help you gather and organize information that will be needed in the preparation of your partnership tax returns. If you are a first

Business Resource Group

YEAR-END FRINGE BENEFIT & PAYROLL REPORTING December 2014 Business Resource Group David Piscorik Tammy Carter Janet McCaskill Julie Miller Trish Meade Elana Jones [email protected] [email protected]

YEAR-END FRINGE BENEFIT & PAYROLL REPORTING December 2014 Business Resource Group David Piscorik Tammy Carter Janet McCaskill Julie Miller Trish Meade Elana Jones [email protected] [email protected]

EMPLOYEE STOCK OPTIONS

TAX LETTER May 2015 EMPLOYEE STOCK OPTIONS FOREIGN EXCHANGE GAINS AND LOSSES CAREGIVER AND INFIRM DEPENDENT CREDITS MAKING TAX INSTALMENTS EARNED INCOME FOR RRSP PURPOSES AROUND THE COURTS EMPLOYEE STOCK

TAX LETTER May 2015 EMPLOYEE STOCK OPTIONS FOREIGN EXCHANGE GAINS AND LOSSES CAREGIVER AND INFIRM DEPENDENT CREDITS MAKING TAX INSTALMENTS EARNED INCOME FOR RRSP PURPOSES AROUND THE COURTS EMPLOYEE STOCK

Understanding your Forms W-2 and 1042-S

Understanding your Forms W-2 and 1042-S Each year, employees will receive a Form W-2 that provides details of prior year earnings, taxes withheld and other miscellaneous data (such as cost of employer

Understanding your Forms W-2 and 1042-S Each year, employees will receive a Form W-2 that provides details of prior year earnings, taxes withheld and other miscellaneous data (such as cost of employer

Tax Planning and Reporting for a Small Business

Table of Contents Welcome... 3 What Do You Know? Tax Planning and Reporting for a Small Business... 4 Pre-Test... 5 Tax Obligation Management... 6 Business Taxes... 6 Federal Income Tax Forms... 7 Discussion

Table of Contents Welcome... 3 What Do You Know? Tax Planning and Reporting for a Small Business... 4 Pre-Test... 5 Tax Obligation Management... 6 Business Taxes... 6 Federal Income Tax Forms... 7 Discussion

General Information. Illinois Department of Revenue Schedule NR IL-1040 Instructions

Illinois Department of Revenue Schedule NR IL-1040 Instructions What is the purpose of Schedule NR? Schedule NR, Nonresident and Part-Year Resident Computation of Illinois Tax, allows you, a nonresident

Illinois Department of Revenue Schedule NR IL-1040 Instructions What is the purpose of Schedule NR? Schedule NR, Nonresident and Part-Year Resident Computation of Illinois Tax, allows you, a nonresident

1420 n. CLAREMONT BLVD., SUITE 101-B TEL (909) 398-4737 CLAREMONT, CALIFORNIA 91711 FAX (909) 398-4733

398-4737 CLAREMONT, CALIFORNIA 91711 FAX (909) 398-4733") 1420 n. CLAREMONT BLVD., SUITE 101-B TEL (909) 398-4737 CLAREMONT, CALIFORNIA 91711 FAX (909) 398-4733 www.nicholscpas.com Email: [email protected] January 12, 2015 RE: 2014 Tax Returns It is hard to

1420 n. CLAREMONT BLVD., SUITE 101-B TEL (909) 398-4737 CLAREMONT, CALIFORNIA 91711 FAX (909) 398-4733 www.nicholscpas.com Email: [email protected] January 12, 2015 RE: 2014 Tax Returns It is hard to

CHOOSING THE RIGHT BUSINESS STRUCTURE

CHOOSING THE RIGHT BUSINESS STRUCTURE One type of business structure is not necessarily better than another, therefore, it is important to evaluate your needs now and into the future, and consider the

CHOOSING THE RIGHT BUSINESS STRUCTURE One type of business structure is not necessarily better than another, therefore, it is important to evaluate your needs now and into the future, and consider the

Business Types and Payroll Taxes

Minority Business Development Division (MBDD) Prince George s County Office of Central Services Legal Issues and Taxes Facing Small and Minority Businesses October 26, 2010 Business Types and Payroll Taxes

Minority Business Development Division (MBDD) Prince George s County Office of Central Services Legal Issues and Taxes Facing Small and Minority Businesses October 26, 2010 Business Types and Payroll Taxes

Tax Return Questionnaire - 2013 Tax Year

Print this form out, take some time to fill it out, and bring it with you when you come to the office. This will save you time and money, and help us help you more effectively. Tax Return Questionnaire

Print this form out, take some time to fill it out, and bring it with you when you come to the office. This will save you time and money, and help us help you more effectively. Tax Return Questionnaire

2013 TAX PLANNING TIPS FOR INDIVIDUALS

2013 TAX PLANNING TIPS FOR INDIVIDUALS The 2012 American Taxpayer Relief Act, which was enacted in early January 2013, was a sweeping tax package that included permanent extension of the Bush-era tax cuts

2013 TAX PLANNING TIPS FOR INDIVIDUALS The 2012 American Taxpayer Relief Act, which was enacted in early January 2013, was a sweeping tax package that included permanent extension of the Bush-era tax cuts

INTERNATIONAL TAX COMPLIANCE FOR GOVERNMENT CONTRACTORS

INTERNATIONAL TAX COMPLIANCE FOR GOVERNMENT CONTRACTORS Mark T. Gossart Alison N. Dougherty September 26, 2012 2012 All Rights Reserved 805 King Farm Boulevard Suite 300 Rockville, Maryland 20850 301.231.6200

INTERNATIONAL TAX COMPLIANCE FOR GOVERNMENT CONTRACTORS Mark T. Gossart Alison N. Dougherty September 26, 2012 2012 All Rights Reserved 805 King Farm Boulevard Suite 300 Rockville, Maryland 20850 301.231.6200

Tax Preparation Checklist

Tax Preparation Checklist Being prepared for tax season could expedite your return and reduce your taxes. We have prepared a list of common items that are present with most returns. Taxpayer Checklist

Tax Preparation Checklist Being prepared for tax season could expedite your return and reduce your taxes. We have prepared a list of common items that are present with most returns. Taxpayer Checklist

Analyzing Business Tax Returns. Partnership Corporation S-Corporation LLC

Analyzing Business Tax Returns Partnership Corporation S-Corporation LLC 1 Partnership Definition: A partnership is formed when two or more individuals form a business and share in the profits, losses

Analyzing Business Tax Returns Partnership Corporation S-Corporation LLC 1 Partnership Definition: A partnership is formed when two or more individuals form a business and share in the profits, losses

2011 INDIVIDUAL INCOME TAX QUESTIONNAIRE. Please explain or attach supporting documentation if you answer YES to any of the following questions.

INDIVIDUAL INCOME TAX QUESTIONNAIRE This questionnaire asks for pertinent information that is necessary for the preparation of your 2010 income tax returns. Your cooperation in completing the questionnaire

INDIVIDUAL INCOME TAX QUESTIONNAIRE This questionnaire asks for pertinent information that is necessary for the preparation of your 2010 income tax returns. Your cooperation in completing the questionnaire

2011 Tax And Financial Planning Tables

2011 Tax and Financial PLanning Tables Investment Planning 2011 Tax And Financial Planning Tables Tax planning is an important component for your overall financial plan. 2011 Tax and Financial PLanning

2011 Tax and Financial PLanning Tables Investment Planning 2011 Tax And Financial Planning Tables Tax planning is an important component for your overall financial plan. 2011 Tax and Financial PLanning

Denver Tax Group, LLC CHADWICK ELLIOTT 1888 Sherman Street SUITE 650 DENVER, CO 80203 (0) Organizer Mailing Slip

Organizer Mailing Slip") Denver Tax Group, LLC CHADWICK ELLIOTT Sherman Street SUITE 0 DENVER, CO 00, (0) Organizer Mailing Slip TAX ORGANIZER TO:, FROM: Denver Tax Group, LLC Sherman Street SUITE 0 DENVER CO 00 (0) -0 Enclosed

Denver Tax Group, LLC CHADWICK ELLIOTT Sherman Street SUITE 0 DENVER, CO 00, (0) Organizer Mailing Slip TAX ORGANIZER TO:, FROM: Denver Tax Group, LLC Sherman Street SUITE 0 DENVER CO 00 (0) -0 Enclosed

Business Entity Selection

Business Entity Selection Chris Stevenson, Esq. Drummond Woodsum [email protected] (t) 800-727-1941 General Issues A corporation can generate double taxation as profits are taxed at the corporate level

Business Entity Selection Chris Stevenson, Esq. Drummond Woodsum [email protected] (t) 800-727-1941 General Issues A corporation can generate double taxation as profits are taxed at the corporate level

1120-S S Corp Return Preparation Tips. Presented by Tony Nitti, CPA, MT National Tax Services Group

0 1120-S S Corp Return Preparation Tips Presented by Tony Nitti, CPA, MT National Tax Services Group A QUICK PRIMER 1 S Corporations generally do not pay tax at the entity level. Instead, the income or

0 1120-S S Corp Return Preparation Tips Presented by Tony Nitti, CPA, MT National Tax Services Group A QUICK PRIMER 1 S Corporations generally do not pay tax at the entity level. Instead, the income or

Clergy and Non Clergy Compensation

Clergy and Non Clergy Compensation Parish treasurers are responsible for monitoring the salary and housing compensation for clergy. They need to keep abreast of the median family income for their area.

Clergy and Non Clergy Compensation Parish treasurers are responsible for monitoring the salary and housing compensation for clergy. They need to keep abreast of the median family income for their area.

TAX CONSIDERATIONS BUSINESSES. Marty Verdick

TAX CONSIDERATIONS FOR SMALL BUSINESSES Marty Verdick RSM McGladrey, Inc. Overview of Topics General federal tax issues Federal tax incentives Entity selection tax issues State tax issues Sales & use tax

TAX CONSIDERATIONS FOR SMALL BUSINESSES Marty Verdick RSM McGladrey, Inc. Overview of Topics General federal tax issues Federal tax incentives Entity selection tax issues State tax issues Sales & use tax

YEAR END PAYROLL NEWSLETTER

December 2015 YEAR END PAYROLL NEWSLETTER Year-end is once again rapidly approaching and the time to properly account for all taxable and non-taxable income which may affect your payroll is here. Fortunately

December 2015 YEAR END PAYROLL NEWSLETTER Year-end is once again rapidly approaching and the time to properly account for all taxable and non-taxable income which may affect your payroll is here. Fortunately

Tax Return Questionnaire - 2014 Tax Year

Print this form out, take some time to fill it out, and bring it with you when you come to the office. This will save you time and money, and help us help you more effectively. Tax Return Questionnaire

Print this form out, take some time to fill it out, and bring it with you when you come to the office. This will save you time and money, and help us help you more effectively. Tax Return Questionnaire

What is my Tax Reporting Status as a Mary Kay Consultant?

Our Mission Our goal as a CPA firm is to provide quality tax compliance and financial assurance services to the general public, as all CPA firms do. However, our top priority is to communicate and educate

Our Mission Our goal as a CPA firm is to provide quality tax compliance and financial assurance services to the general public, as all CPA firms do. However, our top priority is to communicate and educate

3. If you received any interest from a "Seller Financed" mortgage, provide: Name and Address of Payer Social Security Number Amount

Print this form out, take some time to fill it out, and bring it with you when you come to the office. This will save you time and money, and help us help you more effectively. Tax Return Questionnaire

Print this form out, take some time to fill it out, and bring it with you when you come to the office. This will save you time and money, and help us help you more effectively. Tax Return Questionnaire

Valuation of S-Corporations

Valuation of S-Corporations Prepared by: Presented by: Hugh H. Woodside, ASA, CFA Empire Valuation Consultants, LLC 777 Canal View Blvd., Suite 200 Rochester, NY 14623 Phone: (585) 475-9260 Fax: (585)

Valuation of S-Corporations Prepared by: Presented by: Hugh H. Woodside, ASA, CFA Empire Valuation Consultants, LLC 777 Canal View Blvd., Suite 200 Rochester, NY 14623 Phone: (585) 475-9260 Fax: (585)

SC REVENUE RULING #06-12. All previous advisory opinions and any oral directives in conflict herewith.

State of South Carolina Department of Revenue 301 Gervais Street, P. O. Box 125, Columbia, South Carolina 29214 Website Address: http://www.sctax.org SC REVENUE RULING #06-12 SUBJECT: Tax Rate Reduction

State of South Carolina Department of Revenue 301 Gervais Street, P. O. Box 125, Columbia, South Carolina 29214 Website Address: http://www.sctax.org SC REVENUE RULING #06-12 SUBJECT: Tax Rate Reduction

Considerations in the Health Care Company Tax Status Conversion from C Corporation to Pass-Through Entity

Health Care Forensic Analysis Insights Considerations in the Health Care Company Tax Status Conversion from C Corporation to Pass-Through Entity Robert F. Reilly, CPA For a variety of economic and taxation

Health Care Forensic Analysis Insights Considerations in the Health Care Company Tax Status Conversion from C Corporation to Pass-Through Entity Robert F. Reilly, CPA For a variety of economic and taxation

E I N A N D A N D A S S O C I A T E S. F. James Weinand & Associates Certified Public Accountants, PS

J A N D A S S O C I A T E S F W E I N A N D F. James Weinand & Associates Certified Public Accountants, PS 6322 Lake Grove St. S.W. Lakewood, WA 98499 Telephone: (253) 584-7966 Fax: (253) 584-0330 AFWA

J A N D A S S O C I A T E S F W E I N A N D F. James Weinand & Associates Certified Public Accountants, PS 6322 Lake Grove St. S.W. Lakewood, WA 98499 Telephone: (253) 584-7966 Fax: (253) 584-0330 AFWA

S Corporation Tax Update

S Corporation Tax Update Fifty Third Annual Arkansas Federal Tax Institute Jillian G. Yant, CPA Overview S Corporation Basis Tax Extenders Net Investment Income Tax Reasonable Compensation Late S Elections

S Corporation Tax Update Fifty Third Annual Arkansas Federal Tax Institute Jillian G. Yant, CPA Overview S Corporation Basis Tax Extenders Net Investment Income Tax Reasonable Compensation Late S Elections

2014 Tax Organizer. Thank you for taking the time to complete this Tax Organizer.

2014 Tax Organizer This Tax Organizer is designed to help you collect and report the information needed to prepare your 2014 income tax return. The attached worksheets cover income, deductions, and credits,

2014 Tax Organizer This Tax Organizer is designed to help you collect and report the information needed to prepare your 2014 income tax return. The attached worksheets cover income, deductions, and credits,

tax planning strategies

tax planning strategies In addition to saving income taxes for the current and future years, tax planning can reduce eventual estate taxes, maximize the amount of funds you will have available for retirement,

tax planning strategies In addition to saving income taxes for the current and future years, tax planning can reduce eventual estate taxes, maximize the amount of funds you will have available for retirement,

Important Information Morgan Stanley SIMPLE IRA Summary

SIMPLE IRA Summary September 2013 Important Information Morgan Stanley SIMPLE IRA Summary The following is intended to provide you with basic information on the roles and services that Morgan Stanley Smith

SIMPLE IRA Summary September 2013 Important Information Morgan Stanley SIMPLE IRA Summary The following is intended to provide you with basic information on the roles and services that Morgan Stanley Smith

Chapter 18. Corporations: Distributions Not in Complete Liquidation. Eugene Willis, William H. Hoffman, Jr., David M. Maloney and William A.

Chapter 18 Corporations: Distributions Not in Complete Liquidation Eugene Willis, William H. Hoffman, Jr., David M. Maloney and William A. Raabe Copyright 2004 South-Western/Thomson Learning Taxable Dividends

Chapter 18 Corporations: Distributions Not in Complete Liquidation Eugene Willis, William H. Hoffman, Jr., David M. Maloney and William A. Raabe Copyright 2004 South-Western/Thomson Learning Taxable Dividends

Choice of Entity. Paul E. Costantino, CPA, MST Costantino Richards Rizzo, LLP, Wakefield

Choice of Entity Paul E. Costantino, CPA, MST Costantino Richards Rizzo, LLP, Wakefield I. Overview of Entities The entity selection process is one of the first steps in the formation of any business,

Choice of Entity Paul E. Costantino, CPA, MST Costantino Richards Rizzo, LLP, Wakefield I. Overview of Entities The entity selection process is one of the first steps in the formation of any business,

IRS Issues Reliance Proposed Regulations On Some Net Investment Income Tax Issues. Background

/////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////// Special Report Series on Section 1411

/////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////// Special Report Series on Section 1411

Agenda. IRS Payroll Tax Audit Initiatives. Auditor of State David Yost 2011 Local Government Official s Conference Employment Tax Update

Auditor of State David Yost 2011 Local Government Official s Conference Employment Tax Update April 7, 2011 Janice M. Zajac, CPA, MBA, MB Agenda IRS Payroll Tax Audit Initiatives Independent Contractors

Auditor of State David Yost 2011 Local Government Official s Conference Employment Tax Update April 7, 2011 Janice M. Zajac, CPA, MBA, MB Agenda IRS Payroll Tax Audit Initiatives Independent Contractors

Trader Entities. Should You Incorporate Your Trading Business?

Trader Entities Should You Incorporate Your Trading Business? A Little Accountant Humor What is the difference between an introverted accountant and an extroverted accountant? A Little Accountant Humor

Trader Entities Should You Incorporate Your Trading Business? A Little Accountant Humor What is the difference between an introverted accountant and an extroverted accountant? A Little Accountant Humor

2012 PAYROLL RATES AND LIMITS. Employee Withholding Rate Wage Base Dollar Amount

2012 PAYROLL RATES AND LIMITS Gross Maximum Employee Withholding Rate Wage Base Dollar Amount FICA/Social Security 4.20% * $110,100 $4,624.20 FICA/Medicare Portion 1.45% No Limit No Limit Total FICA 7.65%

2012 PAYROLL RATES AND LIMITS Gross Maximum Employee Withholding Rate Wage Base Dollar Amount FICA/Social Security 4.20% * $110,100 $4,624.20 FICA/Medicare Portion 1.45% No Limit No Limit Total FICA 7.65%

How To Pay Federal Income Tax In Philly

Employers Guide Summary of Payroll Tax Guidelines Table of Contents Page Income Tax 1-2 Federal Withholding Fica Tax State Income Tax Local Tax Unemployment Taxes 3 Federal Tax Deposit Coupons 4 Pennsylvania

Employers Guide Summary of Payroll Tax Guidelines Table of Contents Page Income Tax 1-2 Federal Withholding Fica Tax State Income Tax Local Tax Unemployment Taxes 3 Federal Tax Deposit Coupons 4 Pennsylvania

Client Tax Organizer Worksheet

PAGE 1 OF 7 The asks about pertinent tax items necessary for preparing the most accurate tax return possible. Please answer all applicable questions and attach a statement when necessary for additional

PAGE 1 OF 7 The asks about pertinent tax items necessary for preparing the most accurate tax return possible. Please answer all applicable questions and attach a statement when necessary for additional

Business Entity Conversions: Income Tax Consequences You May Not Anticipate

Presenting a live 110-minute teleconference with interactive Q&A Business Entity Conversions: Income Tax Consequences You May Not Anticipate Understanding and Navigating Complex Federal Income Tax Implications

Presenting a live 110-minute teleconference with interactive Q&A Business Entity Conversions: Income Tax Consequences You May Not Anticipate Understanding and Navigating Complex Federal Income Tax Implications

ACTIONABLE STRATEGIES FOR REDUCING MEDICARE TAXES

ACTIONABLE STRATEGIES FOR REDUCING MEDICARE TAXES Medicare taxes increased in 2013 for high-income earners. Timely action can help reduce the impact of higher taxes. KEY TAKEAWAYS High-income taxpayers

ACTIONABLE STRATEGIES FOR REDUCING MEDICARE TAXES Medicare taxes increased in 2013 for high-income earners. Timely action can help reduce the impact of higher taxes. KEY TAKEAWAYS High-income taxpayers

PEDRICK & COMPANY, LLC 103 CENTRAL AVENUE HINESVILLE, GA 31313. Organizer

PEDRICK & COMPANY, LLC 103 CENTRAL AVENUE HINESVILLE, GA 31313 Organizer 2013 Tax Organizer ORG0 This Tax Organizer is designed to help you collect and report the information needed to prepare your 2013

PEDRICK & COMPANY, LLC 103 CENTRAL AVENUE HINESVILLE, GA 31313 Organizer 2013 Tax Organizer ORG0 This Tax Organizer is designed to help you collect and report the information needed to prepare your 2013

Test 3 Review. Student:

Test 3 Review Student: 1. A credit sale of $2,500 to a customer would result in: A. A debit to the Accounts Receivable account in the general ledger and a debit to the customer's account in the accounts

Test 3 Review Student: 1. A credit sale of $2,500 to a customer would result in: A. A debit to the Accounts Receivable account in the general ledger and a debit to the customer's account in the accounts

T.C. Memo. 2013-180 UNITED STATES TAX COURT. GLASS BLOCKS UNLIMITED, Petitioner v. COMMISSIONER OF INTERNAL REVENUE, Respondent

T.C. Memo. 2013-180 UNITED STATES TAX COURT GLASS BLOCKS UNLIMITED, Petitioner v. COMMISSIONER OF INTERNAL REVENUE, Respondent Docket No. 3396-11. Filed August 7, 2013. Fredrick Blodgett (an officer),

T.C. Memo. 2013-180 UNITED STATES TAX COURT GLASS BLOCKS UNLIMITED, Petitioner v. COMMISSIONER OF INTERNAL REVENUE, Respondent Docket No. 3396-11. Filed August 7, 2013. Fredrick Blodgett (an officer),

TOOLBOX CS PRODUCT PROFILE

TOOLBOX CS PRODUCT PROFILE CS PROFESSIONAL SUITE QUICK ACCESS TO KEY UTILITIES ToolBox CS, puts key utilities at your fingertips tools such as calculators, calculating tax forms you can use throughout

TOOLBOX CS PRODUCT PROFILE CS PROFESSIONAL SUITE QUICK ACCESS TO KEY UTILITIES ToolBox CS, puts key utilities at your fingertips tools such as calculators, calculating tax forms you can use throughout

Willamette Management Associates

Valuation Analyst Considerations in the C Corporation Conversion to Pass-Through Entity Tax Status Robert F. Reilly, CPA For a variety of economic and taxation reasons, this year may be a particularly

Valuation Analyst Considerations in the C Corporation Conversion to Pass-Through Entity Tax Status Robert F. Reilly, CPA For a variety of economic and taxation reasons, this year may be a particularly

LLC, S-Corp, Small Business Worksheet

LLC, S-Corp, Small Business Worksheet As with all our forms, you may submit this information electronically using our secure online submit forms. Using this PDF as a work paper and submitting the information

LLC, S-Corp, Small Business Worksheet As with all our forms, you may submit this information electronically using our secure online submit forms. Using this PDF as a work paper and submitting the information

YOU MUST SIGN THE ATTACHED ENGAGEMENT AGREEMENT AND RETURN IT AT THE TIME OF YOUR APPOINTMENT OR WITH YOUR TAX RETURN DOCUMENTATION.

Bennett Accounting, LLC 624 W. Gurley St., Suite E Prescott, AZ 86305 (928) 445-1351 (928) 445-8135 FAX YOU MUST SIGN THE ATTACHED ENGAGEMENT AGREEMENT AND RETURN IT AT THE TIME OF YOUR APPOINTMENT OR

Bennett Accounting, LLC 624 W. Gurley St., Suite E Prescott, AZ 86305 (928) 445-1351 (928) 445-8135 FAX YOU MUST SIGN THE ATTACHED ENGAGEMENT AGREEMENT AND RETURN IT AT THE TIME OF YOUR APPOINTMENT OR

2012 Year End Accountant Guide

2012 Year End Accountant Guide For your clients using RUN Powered by ADP This guide contains information and critical dates to assist you with year end payroll and tax filing tasks. HR. Payroll. Benefits.

2012 Year End Accountant Guide For your clients using RUN Powered by ADP This guide contains information and critical dates to assist you with year end payroll and tax filing tasks. HR. Payroll. Benefits.

By: Michael Shelby, CPA, MST

By: Michael Shelby, CPA, MST Introduction Michael K. Shelby, CPA, MST Principal of Michael K. Shelby, CPA, LLC Main office in Lanham, Satellite office in Annapolis Currently staff of 5, need to add at

By: Michael Shelby, CPA, MST Introduction Michael K. Shelby, CPA, MST Principal of Michael K. Shelby, CPA, LLC Main office in Lanham, Satellite office in Annapolis Currently staff of 5, need to add at

HSBC Securities (USA) Inc. Instructions for 1099/5498 Recipients 2008

Inc. Instructions for 1099/5498 Recipients 2008") HSBC Securities (USA) Inc. Instructions for 1099/5498 Recipients 2008 Dear Investor, Please note: In June of 2008, Pershing LLC ( Pershing ) became the clearing agent for HSBC Securities (USA) Inc. ( HSBC

HSBC Securities (USA) Inc. Instructions for 1099/5498 Recipients 2008 Dear Investor, Please note: In June of 2008, Pershing LLC ( Pershing ) became the clearing agent for HSBC Securities (USA) Inc. ( HSBC