Consequences of 401(k) s 3. Pension Reform

|

|

|

- Kristina Ball

- 8 years ago

- Views:

Transcription

1 Policies to Strengthen the Employment Based Pension System for All 1. Pension Erosion 2. Unintended Consequences of 401(k) s 3. Pension Reform 1

s")

2 The Pension Problem Accumulatio Investments n Payout a Ghilarducci 2

3 3 1. Pension Erosion

4 Pension Funds Grow and Financialize Shares of Financial Assets by Sector Pension Funds 20% 26% Pension reserves (of life insurance companies) 5% 5% Private Pensions (includes federal pensions) 12% 15% State, local pension funds 5% 6% Mutual funds (401(k) and IRAs) 2% 22% Commercial banks 37% 31% Savings institutions 2% 5% Insurance (net of pension reserves) 1% 8% Finance companies 5% 4% Real estate investment 0.1% 0.6% Security brokers 1.% 5% 4 Total Assets (in trillions $)

1% 8% Finance companies 5% 4% Real estate investment 0.1% 0.6% Security brokers 1.")

5 Financialization of Pensions Private 47.5% 42.6% Pension Coverage DB 88% 36% 5 DC 12% 64%

6 Despite Growth in 401(k)s Pension Coverage Has Worsened (SIPP, author s calculations) Top One Third Middle One Third Lower One Third

7 Tax Expenditures Are Inefficient, Ineffective, and Unfair. Otherwise they are Ok 7

8 Tax Expenditures 6% of taxpayers with incomes over $100,000 per year get 50% of the tax subsidies. 401(k) tax breaks will grow 49% but they exceed the amount of aggregate savings If we limit tax breaks to contributions under $5,000 then all can have $400 per year 8

9 Pension Tax Expenditures Do Not Stimulate Private Savings or Wealth Creation U.S. Tax Expenditures for Employer Plans EXCEED Savings, in Billion Dollars TAX EXPENDITURES SAVINGS

10 Attanasioban ks, Wakefield 2004 CES IRAs in the US and TESSAs and ISAs in the UK represent little additions to saving, expensive methods to encourage HH saving. Bernheim 1999 N/A Review of literature recognizes difficulty Engelhardt 2000 HRS Previous studies overstate estimates on effectiveness of 401(k) saving effects due to measurement error (self-reported eligibility). 401(k) have not had a positive effect on raising the saving rate. Engen Gale 1997 SIPP There's a substitution effect in play, HH sometimes borrow, increase debt (shift to mortgages), decrease consumption to make contributions to these plans, so net saving has not increased Engen, Gale 2000 SIPP Effects of 401(k) are dependent on the level of earnings; low income earners see a net addition to wealth from 401(k) than high income earners. Engen, Gale, Scholz Engen, Gale, Scholz 1994 SIPP/IRS- Michigan Tax Panel 401(k) have not stimulated private saving or wealth. IRAs, 401(k) and Keoghs are to some extent substitutes in HHs portfolios. Nevertheless, a small portion of IRA contributions have increased private saving (very little/positive effect after taking into acct the decline in tax revenues) 1996 SIPP/SCF Saving incentives have a strong effect on the allocation of saving and wealth but not on the level. Gale, Scholz 1994 SCF reshuffle assets from other sources to IRA accounts Poterba, Venti, Wise Poterba, Venti, Wise 1994 SIPP After comparing the net worth of eligible HH with ineligible HH, 401(k) saving has a negligible effect in displacing other private saving 1995/96 /98 SIPP The growth of non-401(k) assets for contributors and non contributors have little effect on other forms of private saving; After testing data controlling for different factors (heterogeneity, home equity) 401(k) and IRA contributions are net additions to saving 10

, decrease consumption to make contributions to these plans, so net saving has not")

11 2. Unintended Effects of 401(k)s: Automatic Destabilizers 11

12 Unintended Effects of 401(k)s In Recessions Economic Effect DC plans Traditional DB 1. Direct consumption effect (on retirees) Decreases 2. Wealth effect on Decreases No effect consumption (on workers, 401(k) owners) 3. Labor supply effects (on workers and retirees) Increases Lowers because contributions increase and increases because of income Decreases Net Effect Destabilizing Stabilizing 12

Increases Lowers because contributions increase and")

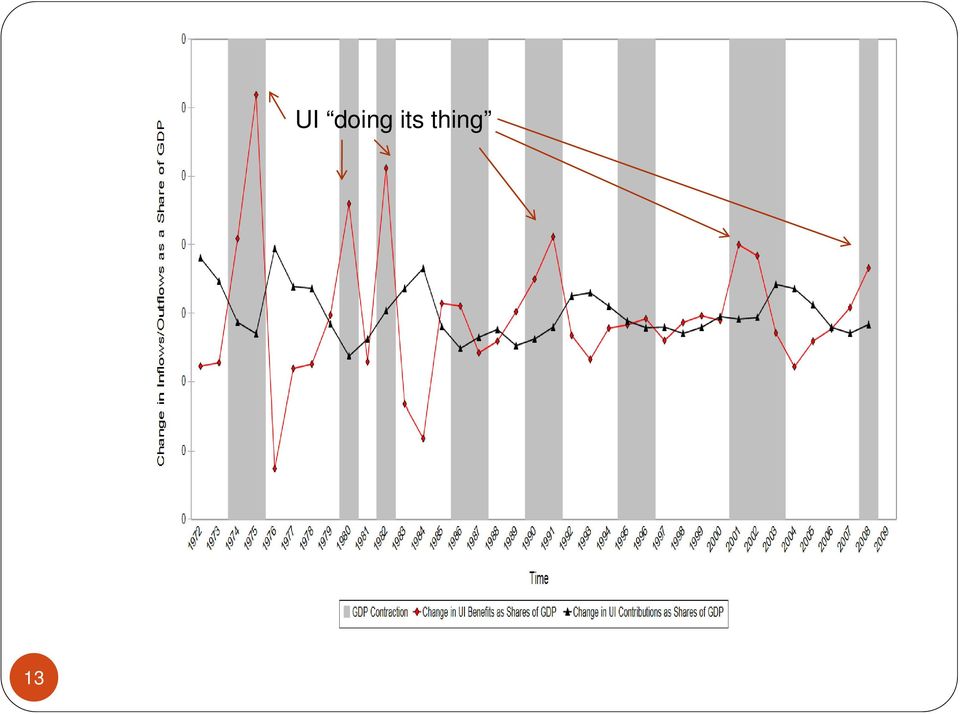

13 13 UI doing its thing

14 Social Security OASI 14

15 15 401(k) consumption increases in expansions!

16 Traditional and Non Traditional Automatic Mean De/Stabilizers Share of GDP Federal Income Tax Collections UI Outflow UI Inflow OASI Outflow OASI Inflow K Outflow K Inflow DI Outflow DI Inflow Medicare Outflow Medicare Inflow

17 ) Δ Y x Y α + δiz ε it + it real it t No al = β i + iδ min Potential t Y t ( real Potential ) Δ x = α + β Δ Y Y + δ Z + ε it i i t t i it it 17

18 Only 401(k) Plans Have Destabilizing Effects Program Flows* 1 Estimated impact of a change in the output potential gap on changes in the levels of program outflows/inflows OASI Outflows ** 401(k) Outflows ** DI Outflows ** UI Outflows ** 18 Federal Income Tax Collections **

19 3. Policy Recommendations for Private and Public Pensions 19

20 People want a retirement solution 83% say government should guarantee pensions. 81% say government should guarantee healthcare. 78% say government should raise minimum wage. 20

21 The Pension Problem Accumulatio Investments n Payout a Ghilarducci 21

22 Characteristics of a Good Pension System Universal Coverage Portable Between Jobs Pooled Assets Adequate Pensions Targeted Government Aid 22 Annuities not Lump Sums Payout at retirement, no early withdrawals

23 Characteristics ti Of Good Pension 401(K) Obama GRA System Auto-IRA GRAs Universal coverage No Almost Yes Portable No Yes Yes Pooled assets, efficiently administered No No Yes Adequate Pensions No No Yes Targeted Government Aid No Yes Yes Annuities No No Yes Payout at retirement, no withdrawals No No Yes [i] 23 23

24 CONTRIBUTIONS 5% of pay is split evenly between the employer and employee. Everyone gets a 24 $600 tax credit which is adjusted for

25 INVESTMENTS Professional Board invests the money in private markets managed by a Guaranteed Retirement Fund. 25 The guarantee will be

26 PAYOUT AT RETIREMENT GRA s will provide a yearly payout to the individual id adjusted for inflation. The accumulated funds cannot be 26 withdrawn before retirement.

27 Everybody wins! 27 Workers with Pensions and 401(k) s Wall Street Firms Private Employers with Pensions and 401(k) s. Public Employers with Pensions in Crises. Workers without Pensions.

28 Policies to Strengthen the Employment Based Pension System for All Teresa Ghilarducci Irene and Bernard Schwartz Professor of Economics New School for Social Research Beyond the 401(k) Project funded by the Rockefeller Foundation (with assistance from, Daniela Arias, Eloy Fisher, Bridget Fisher, Robbie Hiltonsmith, Lauren Schmitz and Joelle Lessler) 28

A Safe and Secure Retirement for All Americans Pension Reform in the United States

A Safe and Secure Retirement for All Americans Pension Reform in the United States Why We Need Pension Reform American workers face a retirement crisis. The extreme fragility of financial markets reveals

A Safe and Secure Retirement for All Americans Pension Reform in the United States Why We Need Pension Reform American workers face a retirement crisis. The extreme fragility of financial markets reveals

MORE MIDDLE CLASS WORKERS WILL BE POOR RETIREES

JUN 15 1 MORE MIDDLE CLASS WORKERS WILL BE POOR RETIREES by Teresa Ghilarducci, Bernard L. and Irene Schwartz Economics Professor at The New School for Social Research and Director of the Schwartz Center

JUN 15 1 MORE MIDDLE CLASS WORKERS WILL BE POOR RETIREES by Teresa Ghilarducci, Bernard L. and Irene Schwartz Economics Professor at The New School for Social Research and Director of the Schwartz Center

Retirement Readiness in New York City: Trends in Plan Sponsorship, Participation and Income Security

Retirement Readiness in New York City: Trends in Plan Sponsorship, Participation and Income Security Figures and Tables by the Schwartz Center for Economic Policy Analysis (SCEPA) Joelle Saad Lessler,

Retirement Readiness in New York City: Trends in Plan Sponsorship, Participation and Income Security Figures and Tables by the Schwartz Center for Economic Policy Analysis (SCEPA) Joelle Saad Lessler,

This PDF is a selection from a published volume from the National Bureau of Economic Research

This PDF is a selection from a published volume from the National Bureau of Economic Research Volume Title: College Choices: The Economics of Where to Go, When to Go, and How to Pay For It Volume Author/Editor:

This PDF is a selection from a published volume from the National Bureau of Economic Research Volume Title: College Choices: The Economics of Where to Go, When to Go, and How to Pay For It Volume Author/Editor:

THE EFFECTS OF SPECIAL SAVING PROGRAMS ON SAVING AND WEALTH. James M. Poterba. Steven F. Venti. David A. Wise

THE EFFECTS OF SPECIAL SAVING PROGRAMS ON SAVING AND WEALTH James M. Poterba Department of Economics National Bureau of Economic Research Massachusetts Institute of Technology 1050 Massachusetts Avenue

THE EFFECTS OF SPECIAL SAVING PROGRAMS ON SAVING AND WEALTH James M. Poterba Department of Economics National Bureau of Economic Research Massachusetts Institute of Technology 1050 Massachusetts Avenue

Volume URL: http://www.nber.org/books/wise94-1. Chapter Title: 401(k) Plans and Tax-Deferred Saving. Chapter Author: James M. Poterba, Steven F.

Plans and Tax-Deferred Saving. Chapter Author: James M. Poterba, Steven F.") This PDF is a selection from an outofprint volume from the National Bureau of Economic Research Volume Title: Studies in the Economics of Aging Volume Author/Editor: David A. Wise, editor Volume Publisher:

This PDF is a selection from an outofprint volume from the National Bureau of Economic Research Volume Title: Studies in the Economics of Aging Volume Author/Editor: David A. Wise, editor Volume Publisher:

Five Flaws of the Current Pension System

The Administration s Savings Accounts Proposals: A Critique Peter Orszag and Gene Sperling November 13, 2003 Five Flaws of the Current Pension System 1. Few People Participate in the Current System Limited

The Administration s Savings Accounts Proposals: A Critique Peter Orszag and Gene Sperling November 13, 2003 Five Flaws of the Current Pension System 1. Few People Participate in the Current System Limited

Liquidity Constraints in the U.S. Housing Market

Liquidity Constraints in the U.S. Housing Market Denis Gorea Virgiliu Midrigan May 215 Contents A Income Process 2 B Moments 4 C Mortgage duration 5 D Cash-out refinancing 5 E Housing turnover 6 F House

Liquidity Constraints in the U.S. Housing Market Denis Gorea Virgiliu Midrigan May 215 Contents A Income Process 2 B Moments 4 C Mortgage duration 5 D Cash-out refinancing 5 E Housing turnover 6 F House

The Impact of Individual Retirement Accounts on Savings Jonathan McCarthy and Han N. Pham

September 1995 Volume 1 Number 6 The Impact of Individual Retirement Accounts on Savings Jonathan McCarthy and Han N. Pham Bills to expand individual retirement accounts have been introduced in both houses

September 1995 Volume 1 Number 6 The Impact of Individual Retirement Accounts on Savings Jonathan McCarthy and Han N. Pham Bills to expand individual retirement accounts have been introduced in both houses

New Estimates of the Future Path of 401(k) Assets

Assets") New Estimates of the Future Path of 41(k) Assets By James Poterba MIT and NBER Steven Venti Dartmouth College and NBER David A. Wise Harvard University and NBER April 27 Abstract: Over the past two and

New Estimates of the Future Path of 41(k) Assets By James Poterba MIT and NBER Steven Venti Dartmouth College and NBER David A. Wise Harvard University and NBER April 27 Abstract: Over the past two and

The Future of Retirement Income Adequacy and Employer Pensions. Testimony of. Teresa Ghilarducci

The Future of Retirement Income Adequacy and Employer Pensions Testimony of Teresa Ghilarducci Director, Schwartz Center for Economic Policy Analysis Department of Economics The New School for Social Research

The Future of Retirement Income Adequacy and Employer Pensions Testimony of Teresa Ghilarducci Director, Schwartz Center for Economic Policy Analysis Department of Economics The New School for Social Research

The Return of Saving

Martin Feldstein the u.s. savings rate and the global economy The savings rate of American households has been declining for more than a decade and recently turned negative. This decrease has dramatically

Martin Feldstein the u.s. savings rate and the global economy The savings rate of American households has been declining for more than a decade and recently turned negative. This decrease has dramatically

Volume URL: http://www.nber.org/books/feld87-2. Chapter Title: Individual Retirement Accounts and Saving

This PDF is a selection from an out-of-print volume from the National Bureau of Economic Research Volume Title: Taxes and Capital Formation Volume Author/Editor: Martin Feldstein, ed. Volume Publisher:

This PDF is a selection from an out-of-print volume from the National Bureau of Economic Research Volume Title: Taxes and Capital Formation Volume Author/Editor: Martin Feldstein, ed. Volume Publisher:

How To Calculate Retirement Savings

May 2015 United States Government Accountability Office Report to the Ranking Member, Subcommittee on Primary Health and Retirement Security, Committee on Health, Education, Labor, and Pensions, U.S. Senate

May 2015 United States Government Accountability Office Report to the Ranking Member, Subcommittee on Primary Health and Retirement Security, Committee on Health, Education, Labor, and Pensions, U.S. Senate

Brokerage Accounts in the United States

Brokerage Accounts in the United States November 30, 2015 Constantijn W.A. Panis, PhD Advanced Analytical Consulting Group, Inc. 213-784-6400 stanpanis@aacg.com Michael J. Brien, PhD Deloitte Transaction

Brokerage Accounts in the United States November 30, 2015 Constantijn W.A. Panis, PhD Advanced Analytical Consulting Group, Inc. 213-784-6400 stanpanis@aacg.com Michael J. Brien, PhD Deloitte Transaction

Draft Legislation Social Security Individual Retirement Account

Draft Legislation Social Security Individual Retirement Account Problem 1. The solvency and sustainability of Social Security increasingly looms as a critical problem. As Americans continue to live longer

Draft Legislation Social Security Individual Retirement Account Problem 1. The solvency and sustainability of Social Security increasingly looms as a critical problem. As Americans continue to live longer

Individual Retirement Accounts (IRAs): Issues and Proposed Expansion

: Issues and Proposed Expansion") Individual Retirement Accounts (IRAs): Issues and Proposed Expansion Thomas L. Hungerford Specialist in Public Finance Jane G. Gravelle Senior Specialist in Economic Policy January 6, 2012 CRS Report for

Individual Retirement Accounts (IRAs): Issues and Proposed Expansion Thomas L. Hungerford Specialist in Public Finance Jane G. Gravelle Senior Specialist in Economic Policy January 6, 2012 CRS Report for

RETIREMENT SAVINGS TAX EXPENDITURES: THE NEED FOR REFUNDABLE TAX CREDITS

JUN 15 1 RETIREMENT SAVINGS TAX EXPENDITURES: THE NEED FOR REFUNDABLE TAX CREDITS by Teresa Ghilarducci, Bernard L. and Irene Schwartz Economics Professor at The New School for Social Research and Director

JUN 15 1 RETIREMENT SAVINGS TAX EXPENDITURES: THE NEED FOR REFUNDABLE TAX CREDITS by Teresa Ghilarducci, Bernard L. and Irene Schwartz Economics Professor at The New School for Social Research and Director

INVESTMENT COMPANY INSTITUTE

INVESTMENT COMPANY INSTITUTE PERSPECTIVE Vol. 6 / No. 1 January 2000 Perspective is a series of occasional papers published by the Investment Company Institute, the national association of the American

INVESTMENT COMPANY INSTITUTE PERSPECTIVE Vol. 6 / No. 1 January 2000 Perspective is a series of occasional papers published by the Investment Company Institute, the national association of the American

Retirement Savings Defaults: The Evolving US Experience. 2012 OECD-IOPS Global Forum J. Mark Iwry United States Department of the Treasury

Retirement Savings Defaults: The Evolving US Experience 2012 OECD-IOPS Global Forum J. Mark Iwry United States Department of the Treasury The material contained in these slides has been provided at the

Retirement Savings Defaults: The Evolving US Experience 2012 OECD-IOPS Global Forum J. Mark Iwry United States Department of the Treasury The material contained in these slides has been provided at the

SYSTEMATIC WITHDRAWALS AND TRANSFERS FROM TIAA TRADITIONAL

SYSTEMATIC WITHDRAWALS AND TRANSFERS FROM TIAA TRADITIONAL THE TIAA TRADITIONAL ANNUITY The TIAA Traditional Annuity is a guaranteed annuity backed by TIAA s claims-paying ability. In the accumulation

SYSTEMATIC WITHDRAWALS AND TRANSFERS FROM TIAA TRADITIONAL THE TIAA TRADITIONAL ANNUITY The TIAA Traditional Annuity is a guaranteed annuity backed by TIAA s claims-paying ability. In the accumulation

RETIREMENT ACCOUNTS (c) Gary R. Evans, 2006-2011, September 24, 2011. Alternative Retirement Financial Plans and Their Features

Gary R. Evans, 2006-2011, September 24, 2011. Alternative Retirement Financial Plans and Their Features") RETIREMENT ACCOUNTS (c) Gary R. Evans, 2006-2011, September 24, 2011. The various retirement investment accounts discussed in this document all offer the potential for healthy longterm returns with substantial

RETIREMENT ACCOUNTS (c) Gary R. Evans, 2006-2011, September 24, 2011. The various retirement investment accounts discussed in this document all offer the potential for healthy longterm returns with substantial

Alternative Retirement Financial Plans and Their Features

RETIREMENT ACCOUNTS Gary R. Evans, 2006-2013, November 20, 2013. The various retirement investment accounts discussed in this document all offer the potential for healthy longterm returns with substantial

RETIREMENT ACCOUNTS Gary R. Evans, 2006-2013, November 20, 2013. The various retirement investment accounts discussed in this document all offer the potential for healthy longterm returns with substantial

Macroeconomics Instructor Miller Fiscal Policy Practice Problems

Macroeconomics Instructor Miller Fiscal Policy Practice Problems 1. Fiscal policy refers to changes in A) state and local taxes and purchases that are intended to achieve macroeconomic policy objectives.

Macroeconomics Instructor Miller Fiscal Policy Practice Problems 1. Fiscal policy refers to changes in A) state and local taxes and purchases that are intended to achieve macroeconomic policy objectives.

Which retirement plan is right for you

Which retirement plan is right for you Facts to help you make an informed choice between the Iowa Public Employees Retirement System (IPERS) and the Iowa Association of Community College Trustees Defined

Which retirement plan is right for you Facts to help you make an informed choice between the Iowa Public Employees Retirement System (IPERS) and the Iowa Association of Community College Trustees Defined

Australia: Retirement Income and Annuities Markets. Contractual Savings Conference April 2008 Greg Brunner

Australia: Retirement Income and Annuities Markets Contractual Savings Conference April 2008 Greg Brunner Pension system Age pension in place since 1908, funded on a payas-you go basis Means testing. The

Australia: Retirement Income and Annuities Markets Contractual Savings Conference April 2008 Greg Brunner Pension system Age pension in place since 1908, funded on a payas-you go basis Means testing. The

Volume URL: http://www.nber.org/books/feld98-1. Chapter Author: James M. Poterba, David A. Wise. Chapter URL: http://www.nber.

This PDF is a selection from an out-of-print volume from the National Bureau of Economic Research Volume Title: Privatizing Social Security Volume Author/Editor: Martin Feldstein, editor Volume Publisher:

This PDF is a selection from an out-of-print volume from the National Bureau of Economic Research Volume Title: Privatizing Social Security Volume Author/Editor: Martin Feldstein, editor Volume Publisher:

How Washington Rates on Retirement Security and Defined Benefit Plan Issues

How Washington Rates on Retirement Security and Defined Benefit Plan Issues National Institute on Retirement Security Diane Oakley, Executive Director April 8, 2014 www.nirsonline.org About NIRS Nonprofit,

How Washington Rates on Retirement Security and Defined Benefit Plan Issues National Institute on Retirement Security Diane Oakley, Executive Director April 8, 2014 www.nirsonline.org About NIRS Nonprofit,

Fairer Government Incentives In A Lifetime Savings Framework

Fairer Government Incentives In A Lifetime Savings Framework The LifeSaver Dr. Ros Altmann ros.altmann@genesys.net 24th January 2002 Outline! UK savings situation! Barriers to saving! Government savings

Fairer Government Incentives In A Lifetime Savings Framework The LifeSaver Dr. Ros Altmann ros.altmann@genesys.net 24th January 2002 Outline! UK savings situation! Barriers to saving! Government savings

Notes - Gruber, Public Finance Chapter 20.3 A calculation that finds the optimal income tax in a simple model: Gruber and Saez (2002).

.") Notes - Gruber, Public Finance Chapter 20.3 A calculation that finds the optimal income tax in a simple model: Gruber and Saez (2002). Description of the model. This is a special case of a Mirrlees model.

Notes - Gruber, Public Finance Chapter 20.3 A calculation that finds the optimal income tax in a simple model: Gruber and Saez (2002). Description of the model. This is a special case of a Mirrlees model.

Crisis in Retirement - Are Aging Workers Heading for a Fiscal Cliff

McCombs Knowledge To Go April 7, 2015 Crisis in Retirement Professor Michael H. Granof Ernst & Young Distinguished Centennial Professor in Accounting Crisis in Retirement: Are Aging Workers Heading for

McCombs Knowledge To Go April 7, 2015 Crisis in Retirement Professor Michael H. Granof Ernst & Young Distinguished Centennial Professor in Accounting Crisis in Retirement: Are Aging Workers Heading for

The Retirement Savings Crisis: Is It Worse Than We Think? Media and Interested Parties Webinar June 20, 2013 11:00 a.m. ET

The Retirement Savings Crisis: Is It Worse Than We Think? Media and Interested Parties Webinar June 20, 2013 11:00 a.m. ET Agenda Welcome and Introductions Report Overview Detailed Findings Conclusions

The Retirement Savings Crisis: Is It Worse Than We Think? Media and Interested Parties Webinar June 20, 2013 11:00 a.m. ET Agenda Welcome and Introductions Report Overview Detailed Findings Conclusions

The Truth. About. Public Employee Retirement Plans

The Truth About Public Employee Retirement Plans Another Risky Scheme Anumber of right-wing ideologues are trying to sell taxpayers a bill of goods. These individuals have claimed that public employee

The Truth About Public Employee Retirement Plans Another Risky Scheme Anumber of right-wing ideologues are trying to sell taxpayers a bill of goods. These individuals have claimed that public employee

The Role of Tax Reform in Comprehensive Deficit Reduction and Fiscal Policy. Martin Feldstein

For Release on Delivery September 13, 2011 at 2 p.m. The Role of Tax Reform in Comprehensive Deficit Reduction and Fiscal Policy Martin Feldstein Thank you, Mr. Chairman. I am very pleased to have this

For Release on Delivery September 13, 2011 at 2 p.m. The Role of Tax Reform in Comprehensive Deficit Reduction and Fiscal Policy Martin Feldstein Thank you, Mr. Chairman. I am very pleased to have this

Effects on pensioners from leaving the EU

Effects on pensioners from leaving the EU Summary 1.1 HM Treasury s short-term document presented two scenarios for the immediate impact of leaving the EU on the UK economy: the shock scenario and severe

Effects on pensioners from leaving the EU Summary 1.1 HM Treasury s short-term document presented two scenarios for the immediate impact of leaving the EU on the UK economy: the shock scenario and severe

Pension Lump-Sum Distributions: Do Boomers Take Them or Save Them?

Pension Lump-Sum Distributions: Do Boomers Take Them or Save Them? I. Introduction Boomers are facing a retirement system different from the one their parents knew. A greater proportion of the previous

Pension Lump-Sum Distributions: Do Boomers Take Them or Save Them? I. Introduction Boomers are facing a retirement system different from the one their parents knew. A greater proportion of the previous

THE FUTURE OF EMPLOYER BASED HEALTH INSURANCE FOLLOWING HEALTH REFORM

THE FUTURE OF EMPLOYER BASED HEALTH INSURANCE FOLLOWING HEALTH REFORM National Congress on Health Insurance Reform Washington, D.C., January 20, 2011 Elise Gould, PhD Health Policy Research Director Economic

THE FUTURE OF EMPLOYER BASED HEALTH INSURANCE FOLLOWING HEALTH REFORM National Congress on Health Insurance Reform Washington, D.C., January 20, 2011 Elise Gould, PhD Health Policy Research Director Economic

On average, young retirees are not

How Financially Secure Are Young Retirees and Older Workers? FIGURE 1 Financial Status of People Age 51 to 59, by Work Status THOUSS OF DOLLARS 14 1 8 6 $82 RETIREES WORKERS $99 4 $41 $24 MEDIAN MEDIAN

How Financially Secure Are Young Retirees and Older Workers? FIGURE 1 Financial Status of People Age 51 to 59, by Work Status THOUSS OF DOLLARS 14 1 8 6 $82 RETIREES WORKERS $99 4 $41 $24 MEDIAN MEDIAN

Over the past 30 years, there has been a fundamental change

The shift from defined benefit pensions to 401(k) plans and the pension assets of the baby boom cohort James Poterba*, Steven Venti, and David A. Wise *Department of Economics, Massachusetts Institute

The shift from defined benefit pensions to 401(k) plans and the pension assets of the baby boom cohort James Poterba*, Steven Venti, and David A. Wise *Department of Economics, Massachusetts Institute

Financial Needs Analysis. Frank and Kathy Sample-Accumulator Hartford, Connecticut

Financial Needs Analysis Frank and Kathy Sample-Accumulator Hartford, Connecticut PREPARED BY: JANET LERNER, CFP - LERNER, STEVENSON & ASSOC. JUNE 8, 2012 Table of Contents Introduction... 4 Net Worth...

Financial Needs Analysis Frank and Kathy Sample-Accumulator Hartford, Connecticut PREPARED BY: JANET LERNER, CFP - LERNER, STEVENSON & ASSOC. JUNE 8, 2012 Table of Contents Introduction... 4 Net Worth...

The Effect of the Affordable Care Act on the Labor Supply, Savings, and Social Security of Older Americans

The Effect of the Affordable Care Act on the Labor Supply, Savings, and Social Security of Older Americans Eric French University College London Hans-Martin von Gaudecker University of Bonn John Bailey

The Effect of the Affordable Care Act on the Labor Supply, Savings, and Social Security of Older Americans Eric French University College London Hans-Martin von Gaudecker University of Bonn John Bailey

Risks and Rewards Newsletter

Article from: Risks and Rewards Newsletter October 2003 Issue No. 43 Pension Accounting & Personal Saving by Annamaria Lusardi, Jonathan Skinner and Steven Venti 1 Editor s Note: This article is reprinted

Article from: Risks and Rewards Newsletter October 2003 Issue No. 43 Pension Accounting & Personal Saving by Annamaria Lusardi, Jonathan Skinner and Steven Venti 1 Editor s Note: This article is reprinted

Now is the Time to Add Retirement Accounts to Social Security: The Guaranteed Retirement Account Proposal

Now is the Time to Add Retirement Accounts to Social Security: The Guaranteed Retirement Account Proposal Schwartz Center for Economic Policy Analysis (SCEPA), The New School Teresa Ghilarducci with Bridget

Now is the Time to Add Retirement Accounts to Social Security: The Guaranteed Retirement Account Proposal Schwartz Center for Economic Policy Analysis (SCEPA), The New School Teresa Ghilarducci with Bridget

TRENDS AND ISSUES. Do People Save Enough for Retirement?

Do People Save Enough for Retirement? Alicia H. Munnell, Boston College May 2005 EXECUTIVE SUMMARY This report looks at how much income individuals need in retirement and summarizes results from economic

Do People Save Enough for Retirement? Alicia H. Munnell, Boston College May 2005 EXECUTIVE SUMMARY This report looks at how much income individuals need in retirement and summarizes results from economic

What Happens When You Show Them the Money?: Lump Sum Distributions, Retirement Income Security, and Public Policy

What Happens When You Show Them the Money?: Lump Sum Distributions, Retirement Income Security, and Public Policy Leonard E. Burman Urban Institute Norma B. Coe MIT William G. Gale Brookings Institution

What Happens When You Show Them the Money?: Lump Sum Distributions, Retirement Income Security, and Public Policy Leonard E. Burman Urban Institute Norma B. Coe MIT William G. Gale Brookings Institution

College of Business Administration Savannah State University Personal Finance (BUSA 3000) Quiz 1 Fall 2011 Dr. William A. Dowling.

Quiz 1 Fall 2011 Dr. William A. Dowling.") College of Business Administration Savannah State University Personal Finance (BUSA 3000) Quiz 1 Fall 2011 Dr. William A. Dowling Exam Key Instructions: You are to answer each of the following. If the

College of Business Administration Savannah State University Personal Finance (BUSA 3000) Quiz 1 Fall 2011 Dr. William A. Dowling Exam Key Instructions: You are to answer each of the following. If the

IAPF Presentation. Retirement Income Industry Association. Steve Mitchell

IAPF Presentation Retirement Income Industry Association Steve Mitchell US Retirement Scheme Coverage 40% of households are not covered by an employer sponsored retirement scheme Percent of US Households

IAPF Presentation Retirement Income Industry Association Steve Mitchell US Retirement Scheme Coverage 40% of households are not covered by an employer sponsored retirement scheme Percent of US Households

Are U.S. Workers Ready for Retirement?

Are U.S. Workers Ready for Retirement? Trends in Plan Sponsorship, Participation, and Preparedness Joelle Saad-Lessler, Teresa Ghilarducci, and Kate Bahn 01 OVERVIEW For a secure retirement, workers need

Are U.S. Workers Ready for Retirement? Trends in Plan Sponsorship, Participation, and Preparedness Joelle Saad-Lessler, Teresa Ghilarducci, and Kate Bahn 01 OVERVIEW For a secure retirement, workers need

The Success of the U.S. Retirement System

The Success of the U.S. Retirement System Copyright 2012 by the Investment Company Institute. All rights reserved. Suggested citation: Brady, Peter, Kimberly Burham, and Sarah Holden. 2012. The Success

The Success of the U.S. Retirement System Copyright 2012 by the Investment Company Institute. All rights reserved. Suggested citation: Brady, Peter, Kimberly Burham, and Sarah Holden. 2012. The Success

How To Analyze Lump Sum Distribution From Retirement Saving Plans

This PDF is a selection from an out-of-print volume from the National Bureau of Economic Research Volume Title: Inquiries in the Economics of Aging Volume Author/Editor: David A. Wise, editor Volume Publisher:

This PDF is a selection from an out-of-print volume from the National Bureau of Economic Research Volume Title: Inquiries in the Economics of Aging Volume Author/Editor: David A. Wise, editor Volume Publisher:

6. Saving incentives in the US *

6. Saving incentives in the US * Surachai Khitatrakun and John Karl Scholz 6.1 INTRODUCTION The metaphor used to describe retirement preparation in the United States is the three-legged stool. The seat

6. Saving incentives in the US * Surachai Khitatrakun and John Karl Scholz 6.1 INTRODUCTION The metaphor used to describe retirement preparation in the United States is the three-legged stool. The seat

Retirement income planning Get ready. Take control. Start moving.

Retirement income planning Get ready. Take control. Start moving. Your future is too important to leave it to chance. That s why taking control of your retirement with an organized, practical approach

Retirement income planning Get ready. Take control. Start moving. Your future is too important to leave it to chance. That s why taking control of your retirement with an organized, practical approach

Chapter 12. Aggregate Expenditure and Output in the Short Run

Chapter 12. Aggregate Expenditure and Output in the Short Run Instructor: JINKOOK LEE Department of Economics / Texas A&M University ECON 203 502 Principles of Macroeconomics Aggregate Expenditure (AE)

Chapter 12. Aggregate Expenditure and Output in the Short Run Instructor: JINKOOK LEE Department of Economics / Texas A&M University ECON 203 502 Principles of Macroeconomics Aggregate Expenditure (AE)

Social Security and Retirement Savings Accounts

Social Security and Retirement Savings Accounts Francis E. Laatsch Department of Economics, Finance, and International Business University of Southern Mississippi Hattiesburg, Mississippi 39402 Daniel

Social Security and Retirement Savings Accounts Francis E. Laatsch Department of Economics, Finance, and International Business University of Southern Mississippi Hattiesburg, Mississippi 39402 Daniel

> The Role of Insurance in Wealth Planning

> The Role of Insurance in Wealth Planning Executive retirement solutions A S S A N T E E S T A T E A N D I N S U R A N C E S E R V I C E S I N C. Executive retirement solutions Everyone wants enough retirement

> The Role of Insurance in Wealth Planning Executive retirement solutions A S S A N T E E S T A T E A N D I N S U R A N C E S E R V I C E S I N C. Executive retirement solutions Everyone wants enough retirement

Recent Trends in Superannuation Fund Assets

Recent Trends in Superannuation Fund Assets The assets of superannuation funds have increased rapidly in the 99s. Along with managed funds more generally, this growth has been considerably faster than

Recent Trends in Superannuation Fund Assets The assets of superannuation funds have increased rapidly in the 99s. Along with managed funds more generally, this growth has been considerably faster than

16. Individual Retirement Accounts

16. Individual Retirement Accounts Introduction Through enactment of the Employee Retirement Income Security Act of 1974 (ERISA), Congress established individual retirement accounts (IRAs) to provide workers

16. Individual Retirement Accounts Introduction Through enactment of the Employee Retirement Income Security Act of 1974 (ERISA), Congress established individual retirement accounts (IRAs) to provide workers

RETIREMENT PLANNING 101. November 18, 2014

RETIREMENT PLANNING 101 November 18, 2014 WHEN YOU IMAGINE YOUR RETIREMENT, WHAT DO YOU SEE? THE RETIREMENT PLANNING ROAD MAP Implement Plan Basic Questions Crunching Numbers Tax-advantaged Retirement

RETIREMENT PLANNING 101 November 18, 2014 WHEN YOU IMAGINE YOUR RETIREMENT, WHAT DO YOU SEE? THE RETIREMENT PLANNING ROAD MAP Implement Plan Basic Questions Crunching Numbers Tax-advantaged Retirement

Financial Conduct Authority Retirement Income Market Data

Financial Conduct Authority Retirement Income Market Data July September 2015 Contents Introduction 1 1 Executive summary 2 2 Our sample 5 3 Consumer choices 6 4 Withdrawals 12 5 Use of regulated advisers

Financial Conduct Authority Retirement Income Market Data July September 2015 Contents Introduction 1 1 Executive summary 2 2 Our sample 5 3 Consumer choices 6 4 Withdrawals 12 5 Use of regulated advisers

PORTFOLIO RISK AND SELF-DIRECTED RETIREMENT SAVING PROGRAMS. James M. Poterba MIT and NBER. Revised October 2003 ABSTRACT

PORTFOLIO RISK AND SELF-DIRECTED RETIREMENT SAVING PROGRAMS James M. Poterba MIT and NBER Revised October 2003 ABSTRACT Defined contribution retirement plans expose retirement savers to financial market

PORTFOLIO RISK AND SELF-DIRECTED RETIREMENT SAVING PROGRAMS James M. Poterba MIT and NBER Revised October 2003 ABSTRACT Defined contribution retirement plans expose retirement savers to financial market

New Retirees Have Inadequate Retirement Account Balances: Analysis of the 2008 Survey of Income and Program Participation (SIPP), Wave 10 i

, Wave 10 i") FACT SHEET SCEPA s Retirement Income Security Project New Retirees Have Inadequate Retirement Account Balances: Analysis of the 2008 Survey of Income and Program Participation (SIPP), Wave 10 i By Joelle

FACT SHEET SCEPA s Retirement Income Security Project New Retirees Have Inadequate Retirement Account Balances: Analysis of the 2008 Survey of Income and Program Participation (SIPP), Wave 10 i By Joelle

Personal Needs Business Needs Estate/Wealth Transfer Planning

STEP 1: ASK YOURSELF WHY YOU NEED LIFE INSURANCE. Personal Needs Business Needs Estate/Wealth Transfer Planning Replace lost income from the premature death of a wage earner Pay off debts, mortgage, funeral

STEP 1: ASK YOURSELF WHY YOU NEED LIFE INSURANCE. Personal Needs Business Needs Estate/Wealth Transfer Planning Replace lost income from the premature death of a wage earner Pay off debts, mortgage, funeral

How Workers Use 401(k) Plans: The Participation, Contribution, and Withdrawal Decisions

Plans: The Participation, Contribution, and Withdrawal Decisions") How Workers Use 401(k) Plans: The Participation, Contribution, and Withdrawal Decisions William F. Bassett Department of Economics Brown University Providence, RI 02912 Michael J. Fleming Research and

How Workers Use 401(k) Plans: The Participation, Contribution, and Withdrawal Decisions William F. Bassett Department of Economics Brown University Providence, RI 02912 Michael J. Fleming Research and

Research perspective. The Evolving Role of IRAs in U.S. Retirement Planning

Research perspective 1401 H Street, NW, Suite 1200 Washington, DC 20005 202/326-5800 www.ici.org November 2009 Vol. 15, No. 3 The Evolving Role of IRAs in U.S. Retirement Planning Key Findings By any measure,

Research perspective 1401 H Street, NW, Suite 1200 Washington, DC 20005 202/326-5800 www.ici.org November 2009 Vol. 15, No. 3 The Evolving Role of IRAs in U.S. Retirement Planning Key Findings By any measure,

OECD PROJECT ON FINANCIAL INCENTIVES AND RETIREMENT SAVINGS Project Outline 2014-2016

OECD PROJECT ON FINANCIAL INCENTIVES AND RETIREMENT SAVINGS Project Outline 2014-2016 The OECD argues in favour of complementary private pension savings to boost overall saving for retirement. Financial

OECD PROJECT ON FINANCIAL INCENTIVES AND RETIREMENT SAVINGS Project Outline 2014-2016 The OECD argues in favour of complementary private pension savings to boost overall saving for retirement. Financial

FISCAL INCENTIVES AND RETIREMENT SAVINGS Project Outline 2014-2015

FISCAL INCENTIVES AND RETIREMENT SAVINGS Project Outline 2014-2015 The OECD argues in favour of complementary private pension savings to boost overall saving for retirement. Financial incentives may be

FISCAL INCENTIVES AND RETIREMENT SAVINGS Project Outline 2014-2015 The OECD argues in favour of complementary private pension savings to boost overall saving for retirement. Financial incentives may be

Retirement Saving in Australia

Garry Barrett UNSW Yi-Ping Tseng University of Melbourne November 2006 Overview Outline of Presentation 1 Introduction 2 Social Security in Australia 3 Voluntary private retirement saving 4 Mandated private

Garry Barrett UNSW Yi-Ping Tseng University of Melbourne November 2006 Overview Outline of Presentation 1 Introduction 2 Social Security in Australia 3 Voluntary private retirement saving 4 Mandated private

FINANCIAL PLANNER METHODOLOGY

FINANCIAL PLANNER METHODOLOGY The MeDirect Planning Tools are online investment planning solutions that provide wealth forecasting and investment advice. Our Planning Tools offer you two investment planning

FINANCIAL PLANNER METHODOLOGY The MeDirect Planning Tools are online investment planning solutions that provide wealth forecasting and investment advice. Our Planning Tools offer you two investment planning

The Economists Voice

The Economists Voice Volume 2, Issue 1 2005 Article 8 A Special Issue on Social Security Saving Social Security: The Diamond-Orszag Plan Peter A. Diamond Peter R. Orszag Summary Social Security is one

The Economists Voice Volume 2, Issue 1 2005 Article 8 A Special Issue on Social Security Saving Social Security: The Diamond-Orszag Plan Peter A. Diamond Peter R. Orszag Summary Social Security is one

The IRA Investor Profile: Traditional IRA Investors Activity, 2007 2013

ICI RESEARCH REPORT The IRA Investor Profile: Traditional IRA Investors Activity, 2007 2013 July 2015 The IRA Investor Database The Investment Company Institute and the Securities Industry and Financial

ICI RESEARCH REPORT The IRA Investor Profile: Traditional IRA Investors Activity, 2007 2013 July 2015 The IRA Investor Database The Investment Company Institute and the Securities Industry and Financial

SPECIAL REPORT. tax notes. Automatic Enrollment in IRAs: Costs and Benefits. By Benjamin H. Harris and Rachel M. Johnson. I.

Automatic Enrollment in IRAs: Costs and Benefits By Benjamin H. Harris and Rachel M. Johnson Benjamin H. Harris is a senior research associate at the Brookings Institution and is affiliated with the Urban-Brookings

Automatic Enrollment in IRAs: Costs and Benefits By Benjamin H. Harris and Rachel M. Johnson Benjamin H. Harris is a senior research associate at the Brookings Institution and is affiliated with the Urban-Brookings

The Facts of Life and Annuities

2 The Facts of Life and Annuities Introduction... 4 7 Key Facts... 5 Life Insurance Ownership Is Widespread, but Inadequate... 6 Most Individual Life Insurance Policies Are Permanent... 8 Why Life Insurance

2 The Facts of Life and Annuities Introduction... 4 7 Key Facts... 5 Life Insurance Ownership Is Widespread, but Inadequate... 6 Most Individual Life Insurance Policies Are Permanent... 8 Why Life Insurance

The Taxation of Distributions from Retirement Savings Plans

Congressional Budget Offi ce Background Paper The Taxation of from Retirement Savings Plans Previously Published as CBO Technical Paper 2004-06 April 2004 CONGRESS OF THE UNITED STATES Preface This paper

Congressional Budget Offi ce Background Paper The Taxation of from Retirement Savings Plans Previously Published as CBO Technical Paper 2004-06 April 2004 CONGRESS OF THE UNITED STATES Preface This paper

401k vs Traditional IRA

230B: Public Economics Tax Favored Retirement Accounts: IRAs and 401(k)s Emmanuel Saez Berkeley 1 RETIREMENT PROBLEM Individuals ability to work declines with aging Individuals continue to live after they

230B: Public Economics Tax Favored Retirement Accounts: IRAs and 401(k)s Emmanuel Saez Berkeley 1 RETIREMENT PROBLEM Individuals ability to work declines with aging Individuals continue to live after they

ANNUITIES: WHAT ARE THEY AND HOW ARE THEY USED

ANNUITIES: WHAT ARE THEY AND HOW ARE THEY USED (FORC Journal: Vol. 18 Edition 1 - Spring 2007) 1 An annuity is a contract under which the owner of the contract pays money or transfers assets to the obligor

ANNUITIES: WHAT ARE THEY AND HOW ARE THEY USED (FORC Journal: Vol. 18 Edition 1 - Spring 2007) 1 An annuity is a contract under which the owner of the contract pays money or transfers assets to the obligor

Self Invested Personal Pension

Self Invested Personal Pension Product providers for financial advisors A simple guide to securing your future Who are we? Wealth Options Ltd. is a leading distributor of innovative products to the Irish

Self Invested Personal Pension Product providers for financial advisors A simple guide to securing your future Who are we? Wealth Options Ltd. is a leading distributor of innovative products to the Irish

Among the most important investment

Employee Costs and Risks in 401(k) Plans The rapid growth of employer-sponsored 401(k) plans has been facilitated, in part, by the many advantages offered to participants. However, employees also may encounter

Employee Costs and Risks in 401(k) Plans The rapid growth of employer-sponsored 401(k) plans has been facilitated, in part, by the many advantages offered to participants. However, employees also may encounter

How To Understand The Economic And Social Costs Of Living In Australia

Australia s retirement provision: the decumulation challenge John Piggott Director CEPAR Outline of talk Introduction to Australian retirement policy Issues in Longevity Current retirement products in

Australia s retirement provision: the decumulation challenge John Piggott Director CEPAR Outline of talk Introduction to Australian retirement policy Issues in Longevity Current retirement products in

CPBI Saskatchewan Regional Council Alternative Investments - Worth the Effort?

CPBI Saskatchewan Regional Council Alternative Investments - Worth the Effort? PREPARED BY: Brendan George, Partner, George & Bell Consulting Inc. November 18 and 19, 2015 Agenda Current Economic Environment

CPBI Saskatchewan Regional Council Alternative Investments - Worth the Effort? PREPARED BY: Brendan George, Partner, George & Bell Consulting Inc. November 18 and 19, 2015 Agenda Current Economic Environment

ICI ReseaRCh Perspective

ICI ReseaRCh Perspective 1401 H Street, NW, Suite 1200 WashINgton, DC 20005 202/326-5800 www.ici.org march 2011 vol. 17, no. 3 WHAT S INSIDE 2 Introduction 5 Employee Demand for Pension Benefits 14 Why

ICI ReseaRCh Perspective 1401 H Street, NW, Suite 1200 WashINgton, DC 20005 202/326-5800 www.ici.org march 2011 vol. 17, no. 3 WHAT S INSIDE 2 Introduction 5 Employee Demand for Pension Benefits 14 Why

a t A g e 3 0 : A INVESTMENT COMPANY INSTITUTE PERSPECTIVE INTRODUCTION A little over 30 years ago, Congress enacted www.ici.org

INVESTMENT COMPANY INSTITUTE PERSPECTIVE Vol. 11 / No. 1 Februar y 20 05 Perspective is a series of occasional papers published by the Investment Company Institute, the national association of the U.S.

INVESTMENT COMPANY INSTITUTE PERSPECTIVE Vol. 11 / No. 1 Februar y 20 05 Perspective is a series of occasional papers published by the Investment Company Institute, the national association of the U.S.

CHAPTER 7: AGGREGATE DEMAND AND AGGREGATE SUPPLY

CHAPTER 7: AGGREGATE DEMAND AND AGGREGATE SUPPLY Learning goals of this chapter: What forces bring persistent and rapid expansion of real GDP? What causes inflation? Why do we have business cycles? How

CHAPTER 7: AGGREGATE DEMAND AND AGGREGATE SUPPLY Learning goals of this chapter: What forces bring persistent and rapid expansion of real GDP? What causes inflation? Why do we have business cycles? How

INVESTMENT COMPANY INSTITUTE RESEARCH IN BRIEF

Fundamentals INVESTMENT COMPANY INSTITUTE RESEARCH IN BRIEF Vol. 9 / No. 6 November 000 40 H Street, NW Suite 00 Washington, DC 0005 0/6-5800 www.ici.org Copyright 000 by the Investment Company Institute

Fundamentals INVESTMENT COMPANY INSTITUTE RESEARCH IN BRIEF Vol. 9 / No. 6 November 000 40 H Street, NW Suite 00 Washington, DC 0005 0/6-5800 www.ici.org Copyright 000 by the Investment Company Institute

Return-Free Tax Systems and Taxpayer Compliance Costs

Return-Free Tax Systems and Taxpayer Compliance Costs Presentation to the President s Advisory Panel on Federal Tax Reform by Eric J. Toder Urban Institute and Tax Policy Center May 17, 2005 Issues in

Return-Free Tax Systems and Taxpayer Compliance Costs Presentation to the President s Advisory Panel on Federal Tax Reform by Eric J. Toder Urban Institute and Tax Policy Center May 17, 2005 Issues in

Chapter 11 Building a Secure Retirement. Ken Long New River Community College Dublin, VA 24084 http://www.nr.cc.va/fin107

Chapter 11 Building a Secure Retirement Ken Long New River Community College Dublin, VA 24084 http://www.nr.cc.va/fin107 1 What does it mean to be vested? To be vested means you have worked long enough

Chapter 11 Building a Secure Retirement Ken Long New River Community College Dublin, VA 24084 http://www.nr.cc.va/fin107 1 What does it mean to be vested? To be vested means you have worked long enough

Shifting Income Sources of the Aged

Shifting Income Sources of the Aged by Chris E. Anguelov, Howard M. Iams, and Patrick J. Purcell* Traditional defined benefit pensions, once a major source of retirement income, are increasingly giving

Shifting Income Sources of the Aged by Chris E. Anguelov, Howard M. Iams, and Patrick J. Purcell* Traditional defined benefit pensions, once a major source of retirement income, are increasingly giving

Cato Institute Policy Analysis No. 73: Deductible IRAs Are Best for Workers

Cato Institute Policy Analysis No. 73: Deductible IRAs Are Best for Workers June 3, 1986 Peter J. Ferrara Peter J. Ferrara, a Washington attorney, is author of Social Security: The Inherent Contradiction

Cato Institute Policy Analysis No. 73: Deductible IRAs Are Best for Workers June 3, 1986 Peter J. Ferrara Peter J. Ferrara, a Washington attorney, is author of Social Security: The Inherent Contradiction

HOW MUCH SHOULD PEOPLE SAVE?

July 2014, Number 14-11 RETIREMENT RESEARCH HOW MUCH SHOULD PEOPLE SAVE? By Alicia H. Munnell, Anthony Webb, and Wenliang Hou* Introduction The National Retirement Risk Index (NRRI) shows that half of

July 2014, Number 14-11 RETIREMENT RESEARCH HOW MUCH SHOULD PEOPLE SAVE? By Alicia H. Munnell, Anthony Webb, and Wenliang Hou* Introduction The National Retirement Risk Index (NRRI) shows that half of

What three main functions do they have? Reducing transaction costs, reducing financial risk, providing liquidity

Unit 4 Test Review KEY Savings, Investment and the Financial System 1. What is a financial intermediary? Explain how each of the following fulfills that role: Financial Intermediary: Transforms funds into

Unit 4 Test Review KEY Savings, Investment and the Financial System 1. What is a financial intermediary? Explain how each of the following fulfills that role: Financial Intermediary: Transforms funds into

A U.S. Perspective on Annuity Lifetime Income Guarantees

A U.S. Perspective on Annuity Lifetime Income Guarantees Jacob M. Herschler June 8, 2011 Mexico City Agenda Defined Benefit and Defined Contribution plan trends in the U.S. and prospects for longevity

A U.S. Perspective on Annuity Lifetime Income Guarantees Jacob M. Herschler June 8, 2011 Mexico City Agenda Defined Benefit and Defined Contribution plan trends in the U.S. and prospects for longevity

Since 1960's, U.S. personal savings rate (fraction of income saved) averaged 7%, lower than 15% OECD average. Why? Why do we care?

averaged 7%, lower than 15% OECD average. Why? Why do we care?") Taxation and Personal Saving, G 22 Since 1960's, U.S. personal savings rate (fraction of income saved) averaged 7%, lower than 15% OECD average. Why? Why do we care? Efficiency issues 1. Negative consumption

Taxation and Personal Saving, G 22 Since 1960's, U.S. personal savings rate (fraction of income saved) averaged 7%, lower than 15% OECD average. Why? Why do we care? Efficiency issues 1. Negative consumption

ACTIVE VS. PASSIVE DECISIONS AND CROWD-OUT IN RETIREMENT SAVINGS ACCOUNTS: EVIDENCE FROM DENMARK

ACTIVE VS. PASSIVE DECISIONS AND CROWD-OUT IN RETIREMENT SAVINGS ACCOUNTS: EVIDENCE FROM DENMARK Raj Chetty, Harvard University and NBER John N. Friedman, Harvard University and NBER Soren Leth-Petersen,

ACTIVE VS. PASSIVE DECISIONS AND CROWD-OUT IN RETIREMENT SAVINGS ACCOUNTS: EVIDENCE FROM DENMARK Raj Chetty, Harvard University and NBER John N. Friedman, Harvard University and NBER Soren Leth-Petersen,

An Institutional IRA

An Institutional IRA SVP Thomas Johnson, Jr. New York Life Insurance Company May 13, 2010 The Company You Keep Components of an Institutional IRA (IIRA) What are the critical components of an Institutional

An Institutional IRA SVP Thomas Johnson, Jr. New York Life Insurance Company May 13, 2010 The Company You Keep Components of an Institutional IRA (IIRA) What are the critical components of an Institutional

Amajor objective of public policy toward pensions is to

Lump Sum Distributions from Pension Plans Lump Sum Distributions from Pension Plans: Recent Evidence and Issues for Policy and Research Abstract - We examine preretirement lump sum distributions (LSDs)

Lump Sum Distributions from Pension Plans Lump Sum Distributions from Pension Plans: Recent Evidence and Issues for Policy and Research Abstract - We examine preretirement lump sum distributions (LSDs)

Each copy of any part of a JSTOR transmission must contain the same copyright notice that appears on the screen or printed page of such transmission.

The Effect of Individual Retirement Accounts on Household Consumption and National Saving Author(s): Orazio P. Attanasio and Thomas DeLeire Source: The Economic Journal, Vol. 112, No. 481, (Jul., 2002),

The Effect of Individual Retirement Accounts on Household Consumption and National Saving Author(s): Orazio P. Attanasio and Thomas DeLeire Source: The Economic Journal, Vol. 112, No. 481, (Jul., 2002),

SAVING FOR RETIREMENT

CHARTING YOUR COURSE SERIES: SAVING FOR RETIREMENT Retirement planning for public sector employees Why save now? Starting to save early, being disciplined about saving enough, and prudently investing those

CHARTING YOUR COURSE SERIES: SAVING FOR RETIREMENT Retirement planning for public sector employees Why save now? Starting to save early, being disciplined about saving enough, and prudently investing those

PENSIONS POLICY INSTITUTE. Tax relief for pension saving in the UK

Tax relief for pension saving in the UK This report is sponsored by Age UK, the Institute and Faculty of Actuaries, Partnership and the TUC. The PPI is grateful for the support of the following sponsors

Tax relief for pension saving in the UK This report is sponsored by Age UK, the Institute and Faculty of Actuaries, Partnership and the TUC. The PPI is grateful for the support of the following sponsors

Wealth Strategies. www.rfawealth.com. Saving For Retirement: Tax Deductible vs Roth Contributions. www.rfawealth.com

www.rfawealth.com Wealth Strategies Saving For Retirement: Tax Deductible vs Roth Contributions Part 2 of 12 Your Guide to Saving for Retirement WEALTH STRATEGIES Page 1 Saving For Retirement: Tax Deductible

www.rfawealth.com Wealth Strategies Saving For Retirement: Tax Deductible vs Roth Contributions Part 2 of 12 Your Guide to Saving for Retirement WEALTH STRATEGIES Page 1 Saving For Retirement: Tax Deductible

What is Wealth Management?

What is Wealth Management? INVESTMENT AND INSURANCE PRODUCTS: NOT FDIC INSURED. NOT A BANK DEPOSIT. NOT INSURED BY ANY FEDERAL GOVERNMENT AGENCY. NOT BANK GUARANTEED. MAY LOSE VALUE The Wealth Management

What is Wealth Management? INVESTMENT AND INSURANCE PRODUCTS: NOT FDIC INSURED. NOT A BANK DEPOSIT. NOT INSURED BY ANY FEDERAL GOVERNMENT AGENCY. NOT BANK GUARANTEED. MAY LOSE VALUE The Wealth Management