Rev Re i v sed e Scheduled VI Dhinal Shah Charte Chart re r d Accoun Accoun a t nt

|

|

|

- Jason McKinney

- 9 years ago

- Views:

Transcription

1 Revised Scheduled VI Dhinal Shah Chartered Accountant

2 Structure of Presentation Setting the Context Structure of Revised Schedule VI Key Changes Key Points

3 Setting the Context

4 Setting the Context Towards International Format: Harmonize and synchronize the disclosure requirements with Internatinal formats & in the direction of Ind AS (IFRS converged AS) For e. g. Certain concepts like current/ non current classification ofassets and liabilities, Elimination of concept of schedule and such information will now be provided in the notes to accounts Applicability Applicable to all Companies (except Banking and Insurance Companies) Applicability date: Financial years commencing on or after 1 April 2011 Can a company apply Revised Schedule VI early from 1 January 2011?

Applicability date:")

5 Setting the Context Format No option to use horizontal format for presentation of BS No option to use functional classification of expenses Each item of the face of the BS and P&L shall be cross referenced to any related information in notes to accounts Revised Schedule VI has flexibility Addition, deletion, amendment, substitution, tion modification of line/sub line items AS/ Act override Revised Schedule VI Balance between providing excessive detail or excessive aggregation

6 Concept of Materiality Revised schedule VI specifically recognizes concept of materiality Existing schedule VI materiality threshold Expenses exceeding 1% of the total revenue or Rs. 5,000, whichever is higher, shall be shown as a separate and distinct item Revised schedule VI materiality threshold Items of income or expense which exceeds 1% of the revenue from operations or Rs 100,000 whichever is higher

7 Structure of Revised Schedule VI

8 Balance Sheet Revised Format (Rupees in )

9 Balance Sheet Revised Format (Rupees in )

10 P&L Revised Format (Rupees in )

11 P&L Revised Format (Rupees in )

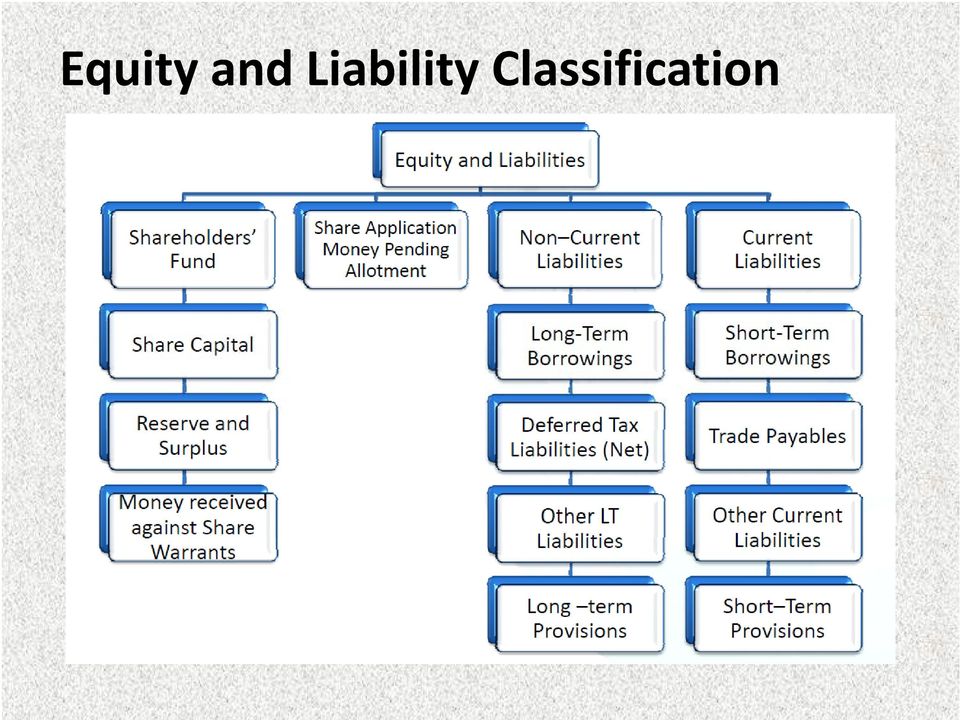

12 Equity and Liability Classification

13 Assets Classification

14 Key Changes

15 New Disclosures Current/ non current classification If an asset or a liability has both the portions, company will need to break the same into current and non current portions e.g., Current maturities of a long term borrowing will have to be separated and classified under the head other current liabilities Will Impact Working Capital, Current Ratio & Debt Equity Ratios Loans and Advances from Related Parties Revised schedule VI requires separate disclosure for loans and advance received from and given to related parties

16 New Disclosures Commitments Requires disclosure of all commitments (including commitments other than capital commitments) Loan Defaults Requires disclosure of all defaults df in repayment of loans and interest Currently CARO requires only defaults in repayment of dues to financial institutions, banks and debenture holders to be specified Terms of repayment of term loans & other loans to be disclosed (earlier only debentures) Shares of each class held by: Holding Company Ultimate Holding Company Subsidiaries or Associates of Above 2

Shares of each class held by: Holding Company Ultimate Holding Company Subsidiaries or Associates")

17 New Disclosures Shareholder s Funds Additional Disclosures Reconciliation of no. of shares outstanding at beginning and end of reporting period Rights, preferences and restrictions of each class of shares including restrictions on distribution of dividends and repayment py of capital Details of shareholders holding more than 5% shares Details of shares issuable under options and contracts/ commitments Unpaid calls by directors and officers shall be shown separately For 5 years immediately preceding the date of BS disclose aggregate number & class of shares : pursuant to contract(s) without payment being received in cash (presently to be given throughout the life of the Company) bonus shares (presently to be given throughout the life of the Company) bought back (presently not required)

without payment being received in cash (presently to be given throughout the life of")

18 New Disclosures Share Application money pending allotment Not exceeding issued capital and not refundable disclosure after shareholders h fund and before liability If refundable other current liability Additional Disclosures of Share Application Money Terms & Conditions Number of shares to be issued Amount of premium period before which shareswill be allotted Whether company has sufficient authorized capital to allot the shares out of application money Period for which it is pending beyond the date of allotment mentioned in offer document with reasons Investments With respect to Investments, separate disclosure required for investment in controlled special purpose entities What is meant by controlled special purpose entities

19 Disclosures No Longer Required Profit and Loss Account Commission, brokerage and non trade discounts Balance Sheet Investments purchased and sold during the year Investments, sundry debtors andloans & advances pertaining to companies under the same management Break up of Bank Balances between Scheduled & Other Banks, Break up between current account, call account & deposit accounts, Details of names, amount, maximum amounts with non scheduled hdldbanks Notes Managerial remuneration and computation of net profits for calculation of commission Licensed capacity, installed capacity and actual production Balance sheet Abstract & Company s General Profile under Part IV

20 Accounting No Longer Required Dividend Existing Schedule VI required the parent company to recognize dividend declared by subsidiary companies even after the date of the balance sheet if they were pertaining to the period ending on or before the balance sheet date. Such requirement no longer exists in Revised Schedule VI Whether the dividend recognized in the previous year needs to be derecognized and the previous year financial statement to be restated? By virtue of AS 4, Subsidiary Co will provide for proposed p dividend and if holding Co., would not recognise same, how to deal with it in Consolidated Accounts?

21 Disclosures Modified Debtors Currently, dbt debtors Outstanding t for a period exceeding 6 months based on billing date Revised schedule VI requires debtors outstanding for a period exceeding 6 months from the date they became due for payment Capital advances Currently, capital advances can be presented as part of Capital Work in Progress / Fixed Assets Revised Schedule VI requires the same to be presented separately under the head Loans & Advances Profit & Loss Account Appropriation / Reserves & Surplus Appropriation of Profit & Loss to be presented under Reserves & Surplus Debit Balance of Profit & Loss to be shown as a negative figure under Surplus Reserves & Surplus balance will be shown after adjusting negative balance of P&L, even if negative

22 Key Points

23 Important Definitions Current/ Non Current asset An asset is classified as current when it satisfies any of the following criteria: It is expected to be realized in, or is intended for sale or consumption in, the company s normal operating cycle; It is held primarily for the purpose of being traded; It is expected to be realized within ihi twelve months after the reporting date; or It is cash or cash equivalent unless it is restricted from being exchanged or used to settle a liability for at least twelve months after the reporting date. Current/ Non Current liability A liability shall be classified as current when it satisfies any of the following criteria: It is expected to be settled in the company s normal operating cycle; It is held primarily for the purpose p of being traded; It is due to be settled within twelve months after the reporting date; or The company does not have an unconditional right to defer settlement of the liability for at least twelve months after the reporting date.

24 Important Definitions Operating Cycle It is the time between the acquisition of assets for processing and their realization in cash or cash equivalents. Where the normal operating cycle cannot be identified, it is assumed to have a duration of 12 month Trade Receivable A receivable shall be classified as a Trade Receivable if it is in respect of the amount due on account of goods sold or services rendered in the normalcourse ofbusiness Trade Payable A payable shall be classified as a Trade Payable if it is in respect of the amount due on account of goods purchased or services received in the normal course of business

25 Key Points Commitments Earlier Schedule VI only capital commitments. Revised Schedule VI requires the disclosure of all commitments, i.e., including other commitments. What is the nature of commitments that will get covered under this disclosure requirement? Trade Receivable/ Payable classification Liability for purchase of fixed assets/ receivable for sale of Fixed Assets not to be classified as Trade Payable/ Trade Receivable Investment Investments Basis ofvaluation (Revised) Vs ModeofValuation of (earlier) Long Term investments carried at other than cost Current Investment (individual investments)

26 Key Points Current and Non Current Classification Deferred Tax should always be classified as Non Current Capital advances to be classified as non current assets Unconditional right to defer settlement of liability Non compliance of debt covenants e.g. quarterly information, non payment of monthly interest. Most loan agreements have a clause that in case of non compliance of anyclause theloanwill bepayable ondemand. Classification of Long term investment expected to be realized within 12 months from the BS date as current investment Employee Benefits like Bonus/ Incentives, Post employment obligations e.g. Gratuity and Pension, Other long term benefits e.g. Accumulated compensated absence

27 Key issues related to Balance Sheet Current and non current classification some questions Company A has taken a loan which is repayable py on demand. However, based on the past experience, it is not expected that the lender will demand the repayment within next 12 months. Company B has taken a 5 year loan. The loan contains certain debt covenants, e.g., filing of quarterly information. The company defaulted in filing of such information in the previous quarter, with the effect that loan has become repayable on demand. However, based on the past experience, the management believes that df default lis minor and the bank will not demand dthe repayment of loan. It has also started the process of getting waiver for this default. After the reporting period and before the approval of the financial statements for issue, the bank agreed to waive the default and not to demand payment as a consequence of the default. A company has taken a 5 year term loan. Out of abundant caution, the bank includes a covenant that it has a right to recall the loan on demand even where the company hasnot violated anyof the debt covenants.

28 Key Points Share Capital Shareholder holding more than 5% shares Classification of preference shares Different classes of Preference Shares to be treated separately. Does it mean that a company should compulsorily classify preference shares based on their substance, i.e., ie redeemable preference shares should always be classified as liability? Disclosure of Preference Shares for companies following AS 30 to 32 on Financial Instruments.

29 Key Points Disclosure Level of disclosure pertaining to default/continuing default in repayment of loans & interest in each case i.e. category wise or loan wise within the category? Details of continuing default (in case of long term borrowing) and default (in case of short term borrowing) as on the balance sheet date in repayment of loans and interest shall be specified separately in each case". The wordings give rise to following issues: Default pertaining to borrowing apart from banks and FI s are also required for items such as bonds/ debentures, deposits, finance lease obligations Defaults other than repayment of loan and interest, e.g., compliance with debt covenants not required to be disclosed

30 Key Points Disclosure Loans and Advances to related parties Details of Loans and Advances given to related parties to be disclosed What details need to be disclosed are not specified? Whether disclosures required to be made in addition to AS 18 (& ASI 13) Disclosure for information about items that do not qualify for recognition in financial statements Postponement of Revenue Recognition Disputed Cases Remote Liability Not Contingent

31 Key Issues Profit and Loss Account Quantitative Information Nature of Company Manufacturing companies Trading companies Companies rendering or supplying li services Company that falls in more than one category Disclosures Required Raw materials under broad heads Goods purchased under broad heads Purchases of goods traded under broad heads Gross income derived from services rendered dunder broad dheads It will be sufficient compliance with the requirements, if purchases, sales and consumption of raw materialand and the gross income from services rendered are shown under broad heads

32 Key Issues Profit and Loss Account Quantitative Information Is a Company required to disclose quantitative details or not? Will a manufacturing company disclose purchase, sale or consumption of raw material? What is meant by good purchased in case of manufacturing companies? Does a manufacturing or a trading company required to disclose sales? How should broad heads for Work in Progress be disclosed? Whether broad heads of Opening and Closing Inventory should also be disclosed?

33 Key Issues Profit and Loss Account Excise Duty, Sales Tax and VAT Revised Schedule VI requires excise duty to be presented as deduction from revenue of a non finance company in the notes No specific requirement for presentation of VAT and Sales Tax Issues AS 9 Revenue Recognition requires excise duty to be shown as deduction from sales on the face of P&L Account (and not in notes) No notified AS deals with accounting for VAT. However, the ICAI GN requires that revenue recognized should be net of VAT Service Tax??

34 Key Issues Profit and Loss Account Accounting and disclosure of share of profit/ loss in Partnership Firms Whether disclosures for Names of all Partners, Total Capital and Share (Profit/ Loss Sharing Ratio) of Each Partner should be disclosed for LLP also? Proposed dividend accounting and disclosure Whether dividend income for finance companies should be taken to main revenue or Other Income?

35 Key Issues Disclosure Meaning of other operating revenues for non finance companies Where should Profit on Sale of Fixed Assets be classified Other Operating Revenue/ Other Income? Should the net gains arising on foreign exchange fluctuations be included under the head Other Operating Revenues or Other Income? Disclosure of value of imports and expenditure in foreign currency whether accrual or cash? Does Small and Medium Company as defined under Companies (Accounting Standards) Rules, 2006 need to disclose Diluted EPS?

36 Key Issues Takeaways Comparative Numbers To commence exercise of validating previous year numbers in Revised Schedule VI Format Changes to be made MIS/ IT systems to collate information of current/ non current portions of each asset and liabilities Break up of Employee Benefit Liabilities in Current and Non Current to be obtained from Independent Actuary. Review Loan Agreements to avoid becoming current liability in case of non compliance of minor clauses Additional time and efforts for the Companies and Auditors to understand and implement changes Use of judgment to maintain balance between excessive information and over aggregation

37 Differential Comparison SN Particular Existing Revised 1 Net Working Capital Current assets and Liabilities are shown together under application of funds. Net Working Capital appears on balance sheet Assets & Liabilities are to be bifurcated into current & Non current and shown separately. Hence, Net Working Capital will not be appearing in Balance sheet 2 Fixed Assets No bifurcation required into Tangible & Intangible assets 3 Borrowings Short term & long term borrowings are grouped together under the head Loan funds sub head Secured/ Unsecured Fixed assets to be shown under non current assets and it has to be bifurcated in to Tangible & Intangible assets Long term borrowings to be shown under non current liabilities and short term borrowings to be shown under current liabilities with separate disclosure of secured/ unsecured loans. Period and amount of continuing default as on the balance sheet date in repayment py of loans and interest to be separately specified

38 Differential Comparison SN Particular Existing Revised 4 Finance lease obligation Finance lease obligations are included in current liabilities Finance lease obligations are to be grouped under the head non current Liabilities 5 Deposits Lease deposits are part of loans & Lease deposits to be disclosed as long advances term loans & advances under the head non current assets 6 Investments Both current & non current investments to be disclosed under the head investments Current and non current investments are to be disclosed separately under current assets & non current assets respectively 7 Loans & Advances Loans & Advances are disclosed along with current assets Loans & Advance to subsidiaries & others to be disclosed separately Loans & Advances to be broken up in long term & short term and to be disclosed under non current & current assets respectively. Loans & Advance from related parties & others to be disclosed separately.

39 Differential Comparison SN Particular Existing Revised 8 DTA/ DTL Deferred Tax assets/ liabilities to be disclosed separately DTA/ DTL to be disclosed under non current assets/ liabilities as applicable 9 Cash & Bank Balances 10 Profit & Loss (Dr Balance) Bank balance to be bifurcated in scheduled banks & others P&L debit balance to be shown under the head Miscellaneous expenditure & losses Bank balances in relation to earmarked balances, held as margin money, deposits with more than 12 months maturity, each to be shown Separately. Debit balance of Profit and Loss Account to be shown as negative figure under the head Surplus. Therefore, reserve & surplus balance can be negative 11 Format A company has an option to use horizontal format for presentation of financial statements. A company will not have option to use horizontal format for presentation of financial statements.

40 Differential Comparison SN Particular Existing Revised 13 Other current No separate disclosure of Current Current maturities of long term debt to liabilities maturities of long term debt. No separate disclosure of Current maturities of finance lease Obligation be disclosed under other current Liabilities. Current maturities of finance lease obligation to be disclosed 14 Purchases Purchases, Opening & closing stock, Goods traded din by the company to be giving break up in respect of each class of goods traded in indicating the quantities thereof disclosed in broad heads notes. Disclosure of quantitative details of goods is much diluted. 15 Expense Function wise & Nature wise Classification based on nature of Classification in P & L expenses A/c. 16 Finance Cost To be classified in fixed loans & other loans To be classified as interest expense, other borrowing costs & Gain/ Loss on forex transactions/ translations. 17 Foreign exchange gain/ loss Gain/ Loss on foreign currency transaction to be shown under finance cost Gain/ Loss on foreign currency transaction to be separated into finance costs and other expenses

41 THANKS

Welcome to workshop on revised schedule VI. K. Chandra Sekhar Company Secretary Ace Designers Limited, Bangalore

Welcome to workshop on revised schedule VI K. Chandra Sekhar Company Secretary Ace Designers Limited, Bangalore 1 Relevant provisions Indian Companies Act, 1956 Rules Notifications Circulars Accounting

Welcome to workshop on revised schedule VI K. Chandra Sekhar Company Secretary Ace Designers Limited, Bangalore 1 Relevant provisions Indian Companies Act, 1956 Rules Notifications Circulars Accounting

Webcast on Revised Schedule VI. CA. Pankajj Goel

Webcast on Revised Schedule VI CA. Pankajj Goel Overview Background and Applicability Significant Features Major Changes Structure of Revised Schedule VI Form of Balance Sheet Statement of Profit and Loss

Webcast on Revised Schedule VI CA. Pankajj Goel Overview Background and Applicability Significant Features Major Changes Structure of Revised Schedule VI Form of Balance Sheet Statement of Profit and Loss

B S R & Co. Revised Schedule VI Key changes and issues

B S R & Co. Revised Schedule VI Key changes and issues 19 th march2013 Introduction Overall approach Interim Financial Reporting Clause 41 application Key changes related to balance sheet Agenda Key changes

B S R & Co. Revised Schedule VI Key changes and issues 19 th march2013 Introduction Overall approach Interim Financial Reporting Clause 41 application Key changes related to balance sheet Agenda Key changes

COUNCIL FOR THE INDIAN SCHOOL CERTIFICATE EXAMINATIONS P-35,36, Sector VI, Pushp Vihar, New Delhi-110017 NEW DELHI ISC ACCOUNTS

COUNCIL FOR THE INDIAN SCHOOL CERTIFICATE EXAMINATIONS P-35,36, Sector VI, Pushp Vihar, New Delhi-110017 NEW DELHI ISC ACCOUNTS Guidelines pertaining to Revised Schedule VI of Part I & II of Companies

COUNCIL FOR THE INDIAN SCHOOL CERTIFICATE EXAMINATIONS P-35,36, Sector VI, Pushp Vihar, New Delhi-110017 NEW DELHI ISC ACCOUNTS Guidelines pertaining to Revised Schedule VI of Part I & II of Companies

WIPRO DOHA LLC FINANCIAL STATEMENTS AS AT AND FOR THE YEAR ENDED MARCH 31, 2016

WIPRO DOHA LLC FINANCIAL STATEMENTS AS AT AND FOR THE YEAR ENDED MARCH 31, 2016 WIPRO DOHA LLC BALANCE SHEET (Amount in ` except share and per share data, unless otherwise stated) As at March 31, 2016

WIPRO DOHA LLC FINANCIAL STATEMENTS AS AT AND FOR THE YEAR ENDED MARCH 31, 2016 WIPRO DOHA LLC BALANCE SHEET (Amount in ` except share and per share data, unless otherwise stated) As at March 31, 2016

Brief Report on Closing of Accounts (connection) for the Term Ended March 31, 2007

for the Term Ended March 31, 2007") MARUHAN Co., Ltd. Brief Report on Closing of (connection) for the Term Ended March 31, 2007 (Amounts less than 1 million yen omitted) 1.Business Results for the term ended on March, 2007 (From April 1,

MARUHAN Co., Ltd. Brief Report on Closing of (connection) for the Term Ended March 31, 2007 (Amounts less than 1 million yen omitted) 1.Business Results for the term ended on March, 2007 (From April 1,

Indian Accounting Standard (Ind AS) 7 Statement of Cash Flows

7 Statement of Cash Flows") Contents Indian Accounting Standard (Ind AS) 7 Statement of Cash Flows Paragraphs OBJECTIVE SCOPE 1 3 BENEFITS OF CASH FLOW INFORMATION 4 5 DEFINITIONS 6 9 Cash and cash equivalents 7 9 PRESENTATION OF

Contents Indian Accounting Standard (Ind AS) 7 Statement of Cash Flows Paragraphs OBJECTIVE SCOPE 1 3 BENEFITS OF CASH FLOW INFORMATION 4 5 DEFINITIONS 6 9 Cash and cash equivalents 7 9 PRESENTATION OF

Oracle (OFSS) Processing Services Limited. Directors Report

Processing Services Limited. Directors Report") Directors Report Dear Members, Your Directors take pleasure in bringing you the Sixth Annual Report of your Company along with the Audited Accounts of the Company for the financial year from April 01,

Directors Report Dear Members, Your Directors take pleasure in bringing you the Sixth Annual Report of your Company along with the Audited Accounts of the Company for the financial year from April 01,

Sri Lanka Accounting Standard-LKAS 7. Statement of Cash Flows

Sri Lanka Accounting Standard-LKAS 7 Statement of Cash Flows CONTENTS SRI LANKA ACCOUNTING STANDARD-LKAS 7 STATEMENT OF CASH FLOWS paragraphs OBJECTIVE SCOPE 1 3 BENEFITS OF CASH FLOW INFORMATION 4 5 DEFINITIONS

Sri Lanka Accounting Standard-LKAS 7 Statement of Cash Flows CONTENTS SRI LANKA ACCOUNTING STANDARD-LKAS 7 STATEMENT OF CASH FLOWS paragraphs OBJECTIVE SCOPE 1 3 BENEFITS OF CASH FLOW INFORMATION 4 5 DEFINITIONS

Statement of Cash Flows

STATUTORY BOARD FINANCIAL REPORTING STANDARD SB-FRS 7 Statement of Cash Flows This version of SB-FRS 7 does not include amendments that are effective for annual periods beginning after 1 January 2014.

STATUTORY BOARD FINANCIAL REPORTING STANDARD SB-FRS 7 Statement of Cash Flows This version of SB-FRS 7 does not include amendments that are effective for annual periods beginning after 1 January 2014.

International Accounting Standard 7 Statement of cash flows *

International Accounting Standard 7 Statement of cash flows * Objective Information about the cash flows of an entity is useful in providing users of financial statements with a basis to assess the ability

International Accounting Standard 7 Statement of cash flows * Objective Information about the cash flows of an entity is useful in providing users of financial statements with a basis to assess the ability

Fixed Assets. Name: SudhirJain M. No.: 213157

Fixed Assets Name: SudhirJain M. No.: 213157 Agenda AS- 10 Accounting for Fixed Assets Introduction & Scope Definitions and other relevant provisions Relevant provisions of other Accounting Standards applicable

Fixed Assets Name: SudhirJain M. No.: 213157 Agenda AS- 10 Accounting for Fixed Assets Introduction & Scope Definitions and other relevant provisions Relevant provisions of other Accounting Standards applicable

NEPAL ACCOUNTING STANDARDS ON CASH FLOW STATEMENTS

NAS 03 NEPAL ACCOUNTING STANDARDS ON CASH FLOW STATEMENTS CONTENTS Paragraphs OBJECTIVE SCOPE 1-3 BENEFITS OF CASH FLOWS INFORMATION 4-5 DEFINITIONS 6-9 Cash and cash equivalents 7-9 PRESENTATION OF A

NAS 03 NEPAL ACCOUNTING STANDARDS ON CASH FLOW STATEMENTS CONTENTS Paragraphs OBJECTIVE SCOPE 1-3 BENEFITS OF CASH FLOWS INFORMATION 4-5 DEFINITIONS 6-9 Cash and cash equivalents 7-9 PRESENTATION OF A

NEW SCHEDULE VI (SECTION 221)

") NEW SCHEDULE VI (SECTION 221) The Schedule VI has been revised by MCA and is applicable for all Balance Sheet made after 31st March, 2011. The Format has done away with earlier two options of format of

NEW SCHEDULE VI (SECTION 221) The Schedule VI has been revised by MCA and is applicable for all Balance Sheet made after 31st March, 2011. The Format has done away with earlier two options of format of

5N PLUS INC. Condensed Interim Consolidated Financial Statements (Unaudited) For the three month periods ended March 31, 2016 and 2015 (in thousands

For the three month periods ended March 31, 2016 and 2015 (in thousands") Condensed Interim Consolidated Financial Statements (Unaudited) (in thousands of United States dollars) Condensed Interim Consolidated Statements of Financial Position (in thousands of United States dollars)

Condensed Interim Consolidated Financial Statements (Unaudited) (in thousands of United States dollars) Condensed Interim Consolidated Statements of Financial Position (in thousands of United States dollars)

FINANCIAL DISCLOSURES FOR THE QUARTER ENDED JUNE 30, 2013

REGISTRATION NO 104: DATE OF REGISTRATION WITH IRDA : NOVEMBER 15, 2000 FINANCIAL DISCLOSURES FOR THE QUARTER ENDED JUNE 30, 2013 Form No Description Pages L-01 REVENUE ACCOUNT 2-5 L-02 PROFIT & LOSS ACCOUNT

REGISTRATION NO 104: DATE OF REGISTRATION WITH IRDA : NOVEMBER 15, 2000 FINANCIAL DISCLOSURES FOR THE QUARTER ENDED JUNE 30, 2013 Form No Description Pages L-01 REVENUE ACCOUNT 2-5 L-02 PROFIT & LOSS ACCOUNT

41. The company agrees to comply with the following provisions:

41. The company agrees to comply with the following provisions: I) Preparation and Submission of Financial Results a) The financial results filed and published in compliance with this clause shall be prepared

41. The company agrees to comply with the following provisions: I) Preparation and Submission of Financial Results a) The financial results filed and published in compliance with this clause shall be prepared

Revised Schedule VI to the Companies Act

Revised Schedule VI to the Companies Act Applicable w. e. f. Financial Year : 2011 2012 1 st & 2 nd Floor, H.K. House, Ashram Road, Ahmedabad 380009 Insight into Schedule VI There is a need to change almost

Revised Schedule VI to the Companies Act Applicable w. e. f. Financial Year : 2011 2012 1 st & 2 nd Floor, H.K. House, Ashram Road, Ahmedabad 380009 Insight into Schedule VI There is a need to change almost

Transition to International Financial Reporting Standards

Transition to International Financial Reporting Standards Topps Tiles Plc In accordance with IFRS 1, First-time adoption of International Financial Reporting Standards ( IFRS ), Topps Tiles Plc, ( Topps

Transition to International Financial Reporting Standards Topps Tiles Plc In accordance with IFRS 1, First-time adoption of International Financial Reporting Standards ( IFRS ), Topps Tiles Plc, ( Topps

(unaudited expressed in Canadian Dollars)

") Condensed Consolidated Interim Financial Statements of CARGOJET INC. For the three month periods ended (unaudited expressed in Canadian Dollars) This page intentionally left blank Condensed Consolidated

Condensed Consolidated Interim Financial Statements of CARGOJET INC. For the three month periods ended (unaudited expressed in Canadian Dollars) This page intentionally left blank Condensed Consolidated

Suruhanjaya Syarikat Malaysia Taxonomy Tagging List Templates ssmt_20131231

Suruhanjaya Syarikat Malaysia Taxonomy Tagging List Templates ssmt_20131231 A view of financial and non financial elements as may be presented in set of financial statements. Content Page [010000] Filing

Suruhanjaya Syarikat Malaysia Taxonomy Tagging List Templates ssmt_20131231 A view of financial and non financial elements as may be presented in set of financial statements. Content Page [010000] Filing

Statement of Cash Flows

HKAS 7 Revised February November 2014 Hong Kong Accounting Standard 7 Statement of Cash Flows HKAS 7 COPYRIGHT Copyright 2014 Hong Kong Institute of Certified Public Accountants This Hong Kong Financial

HKAS 7 Revised February November 2014 Hong Kong Accounting Standard 7 Statement of Cash Flows HKAS 7 COPYRIGHT Copyright 2014 Hong Kong Institute of Certified Public Accountants This Hong Kong Financial

Indian Accounting Standard (Ind AS) 27. Consolidated and Separate Financial Statements

27. Consolidated and Separate Financial Statements") Indian Accounting Standard (Ind AS) 27 Consolidated and Separate Financial Statements Contents Paragraphs Scope 1-3 Definitions 4-8 Presentation of Consolidated Financial 9-11 Statements Scope of Consolidated

Indian Accounting Standard (Ind AS) 27 Consolidated and Separate Financial Statements Contents Paragraphs Scope 1-3 Definitions 4-8 Presentation of Consolidated Financial 9-11 Statements Scope of Consolidated

FINANCIAL STATEMENT 2010

FINANCIAL STATEMENT 2010 CONTENTS Independent Auditors Report------------------------------ 2 Consolidated Balance Sheets ------------------------------ 3 Consolidated Statements of Operations ----------------

FINANCIAL STATEMENT 2010 CONTENTS Independent Auditors Report------------------------------ 2 Consolidated Balance Sheets ------------------------------ 3 Consolidated Statements of Operations ----------------

PART III. Consolidated Financial Statements of Hitachi, Ltd. and Subsidiaries: Independent Auditors Report 47

PART III Item 17. Financial Statements Consolidated Financial Statements of Hitachi, Ltd. and Subsidiaries: Schedule: Page Number Independent Auditors Report 47 Consolidated Balance Sheets as of March

PART III Item 17. Financial Statements Consolidated Financial Statements of Hitachi, Ltd. and Subsidiaries: Schedule: Page Number Independent Auditors Report 47 Consolidated Balance Sheets as of March

Insurance Broker Guidance Notes

Balance Sheet Liabilities 1. Other liabilities include items below: 1.1. Borrowings refers to the amount outstanding including accrued interest in respect of any overdraft arrangements or loans taken by

Balance Sheet Liabilities 1. Other liabilities include items below: 1.1. Borrowings refers to the amount outstanding including accrued interest in respect of any overdraft arrangements or loans taken by

G8 Education Limited ABN: 95 123 828 553. Accounting Policies

G8 Education Limited ABN: 95 123 828 553 Accounting Policies Table of Contents Note 1: Summary of significant accounting policies... 3 (a) Basis of preparation... 3 (b) Principles of consolidation... 3

G8 Education Limited ABN: 95 123 828 553 Accounting Policies Table of Contents Note 1: Summary of significant accounting policies... 3 (a) Basis of preparation... 3 (b) Principles of consolidation... 3

HARMONIC DRIVE SYSTEMS INC. AND CONSOLIDATED SUBSIDIARIES CONSOLIDATED FINANCIAL STATEMENTS MARCH 31, 2013

HARMONIC DRIVE SYSTEMS INC. AND CONSOLIDATED SUBSIDIARIES CONSOLIDATED FINANCIAL STATEMENTS MARCH 31, 2013 HARMONIC DRIVE SYSTEMS INC. AND CONSOLIDATED SUBSIDIARIES CONSOLIDATED BALANCE SHEETS ASSETS

HARMONIC DRIVE SYSTEMS INC. AND CONSOLIDATED SUBSIDIARIES CONSOLIDATED FINANCIAL STATEMENTS MARCH 31, 2013 HARMONIC DRIVE SYSTEMS INC. AND CONSOLIDATED SUBSIDIARIES CONSOLIDATED BALANCE SHEETS ASSETS

Cash Flow Statements

Compiled Accounting Standard AASB 107 Cash Flow Statements This compiled Standard applies to annual reporting periods beginning on or after 1 July 2007. Early application is permitted. It incorporates

Compiled Accounting Standard AASB 107 Cash Flow Statements This compiled Standard applies to annual reporting periods beginning on or after 1 July 2007. Early application is permitted. It incorporates

INDUSTRIAL-ALLIANCE LIFE INSURANCE COMPANY. FIRST QUARTER 2000 Consolidated Financial Statements (Non audited)

") INDUSTRIAL-ALLIANCE LIFE INSURANCE COMPANY FIRST QUARTER 2000 Consolidated Financial Statements (Non audited) March 31,2000 TABLE OF CONTENTS CONSOLIDATED INCOME 2 CONSOLIDATED CONTINUITY OF EQUITY 3 CONSOLIDATED

INDUSTRIAL-ALLIANCE LIFE INSURANCE COMPANY FIRST QUARTER 2000 Consolidated Financial Statements (Non audited) March 31,2000 TABLE OF CONTENTS CONSOLIDATED INCOME 2 CONSOLIDATED CONTINUITY OF EQUITY 3 CONSOLIDATED

Note 2 SIGNIFICANT ACCOUNTING

Note 2 SIGNIFICANT ACCOUNTING POLICIES BASIS FOR THE PREPARATION OF THE FINANCIAL STATEMENTS The consolidated financial statements have been prepared in accordance with International Financial Reporting

Note 2 SIGNIFICANT ACCOUNTING POLICIES BASIS FOR THE PREPARATION OF THE FINANCIAL STATEMENTS The consolidated financial statements have been prepared in accordance with International Financial Reporting

Dumfries Mutual Insurance Company Financial Statements For the year ended December 31, 2010

Dumfries Mutual Insurance Company Financial Statements For the year ended December 31, 2010 Contents Independent Auditors' Report 2 Financial Statements Balance Sheet 3 Statement of Operations and Unappropriated

Dumfries Mutual Insurance Company Financial Statements For the year ended December 31, 2010 Contents Independent Auditors' Report 2 Financial Statements Balance Sheet 3 Statement of Operations and Unappropriated

$ 2,035,512 98,790 6,974,247 2,304,324 848,884 173,207 321,487 239,138 (117,125) 658,103

658,103") FINANCIAL SECTION CONSOLIDATED BALANCE SHEETS Aioi Insurance Company, Limited (Formerly The Dai-Tokyo Fire and Marine Insurance Company, Limited) and March 31, and ASSETS Cash and cash equivalents... Money

FINANCIAL SECTION CONSOLIDATED BALANCE SHEETS Aioi Insurance Company, Limited (Formerly The Dai-Tokyo Fire and Marine Insurance Company, Limited) and March 31, and ASSETS Cash and cash equivalents... Money

How To Write An Audit On Jet Airways Training Academy

INDEPENDENT AUDITOR'S REPORT TO THE MEMBERS OF JET AIRWAYS TRAINING ACADEMY PRIVATE LIMITED Report on the Standalone Financial Statements We have audited the accompanying financial statements of JET AIRWAYS

INDEPENDENT AUDITOR'S REPORT TO THE MEMBERS OF JET AIRWAYS TRAINING ACADEMY PRIVATE LIMITED Report on the Standalone Financial Statements We have audited the accompanying financial statements of JET AIRWAYS

1-3Q of FY2014 87.43 78.77 1-3Q of FY2013 74.47 51.74

January 30, 2015 Resona Holdings, Inc. Consolidated Financial Results for the Third Quarter of Fiscal Year 2014 (Nine months ended December 31, 2014/Unaudited) Code number: 8308 Stock

January 30, 2015 Resona Holdings, Inc. Consolidated Financial Results for the Third Quarter of Fiscal Year 2014 (Nine months ended December 31, 2014/Unaudited) Code number: 8308 Stock

ANADOLU ANONİM TÜRK SİGORTA ŞİRKETİ DETAILED BALANCE SHEET

ASSETS I- Current Assets Audited Current Period Audited Previous Period A- Cash and Cash Equivalents 14 1.606.048.714 1.153.712.216 1- Cash 14 37.347 49.256 2- Cheques Received 3- Banks 14 1.356.733.446

ASSETS I- Current Assets Audited Current Period Audited Previous Period A- Cash and Cash Equivalents 14 1.606.048.714 1.153.712.216 1- Cash 14 37.347 49.256 2- Cheques Received 3- Banks 14 1.356.733.446

Data Compilation Financial Data

Data Compilation Financial Data CONTENTS 1. Transition of Significant Management Indicators, etc. Japan Post Group (Consolidated) 122 Japan Post Holdings Co., Ltd. (Non-consolidated) 122 Japan Post Co.,

Data Compilation Financial Data CONTENTS 1. Transition of Significant Management Indicators, etc. Japan Post Group (Consolidated) 122 Japan Post Holdings Co., Ltd. (Non-consolidated) 122 Japan Post Co.,

SIGNIFICANT ACCOUNTING POLICIES AND NOTES TO ACCOUNTS. Corporate Information

SIGNIFICANT ACCOUNTING POLICIES AND NOTES TO ACCOUNTS Corporate Information Central Railside Warehouse Company Limited is a Public Company in India and incorporated under the provisions of the Companies

SIGNIFICANT ACCOUNTING POLICIES AND NOTES TO ACCOUNTS Corporate Information Central Railside Warehouse Company Limited is a Public Company in India and incorporated under the provisions of the Companies

Accounting and Reporting Policy FRS 102. Staff Education Note 1 Cash flow statements

Staff Education Note 1: Cash flow Statements Accounting and Reporting Policy FRS 102 Staff Education Note 1 Cash flow statements Disclaimer This Education Note has been prepared by FRC staff for the convenience

Staff Education Note 1: Cash flow Statements Accounting and Reporting Policy FRS 102 Staff Education Note 1 Cash flow statements Disclaimer This Education Note has been prepared by FRC staff for the convenience

The Kansai Electric Power Company, Incorporated and Subsidiaries

The Kansai Electric Power Company, Incorporated and Subsidiaries Consolidated Financial Statements for the Years Ended March 31, 2003 and 2002 and for the Six Months Ended September 30, 2003 and 2002 The

The Kansai Electric Power Company, Incorporated and Subsidiaries Consolidated Financial Statements for the Years Ended March 31, 2003 and 2002 and for the Six Months Ended September 30, 2003 and 2002 The

CA CPT SAMPLE PAPER FUNDAMENTAL ACCOUNTING (60MARKS)

") CA CPT SAMPLE PAPER FUNDAMENTAL ACCOUNTING (60MARKS) 1. Which of the following provide frame work and accounting policies so that the financial statements of different enterprises become comparable? (a)

CA CPT SAMPLE PAPER FUNDAMENTAL ACCOUNTING (60MARKS) 1. Which of the following provide frame work and accounting policies so that the financial statements of different enterprises become comparable? (a)

Residual carrying amounts and expected useful lives are reviewed at each reporting date and adjusted if necessary.

87 Accounting Policies Intangible assets a) Goodwill Goodwill represents the excess of the cost of an acquisition over the fair value of identifiable net assets and liabilities of the acquired company

87 Accounting Policies Intangible assets a) Goodwill Goodwill represents the excess of the cost of an acquisition over the fair value of identifiable net assets and liabilities of the acquired company

Earnings Per Share. Contents. Accounting Standard (AS) 20

20") 306 Accounting Standard (AS) 20 Earnings Per Share Contents OBJECTIVE SCOPE Paragraphs 1-3 DEFINITIONS 4-7 PRESENTATION 8-9 MEASUREMENT 10-43 Basic Earnings Per Share 10-25 Earnings-Basic 11-14 Per Share-Basic

306 Accounting Standard (AS) 20 Earnings Per Share Contents OBJECTIVE SCOPE Paragraphs 1-3 DEFINITIONS 4-7 PRESENTATION 8-9 MEASUREMENT 10-43 Basic Earnings Per Share 10-25 Earnings-Basic 11-14 Per Share-Basic

ASPE AT A GLANCE Section 3856 Financial Instruments

ASPE AT A GLANCE Section 3856 Financial Instruments December 2014 Section 3856 Financial Instruments Effective Date Fiscal years beginning on or after January 1, 2011 1 SCOPE Applies to all financial instruments

ASPE AT A GLANCE Section 3856 Financial Instruments December 2014 Section 3856 Financial Instruments Effective Date Fiscal years beginning on or after January 1, 2011 1 SCOPE Applies to all financial instruments

Consolidated Financial Results for Six Months Ended September 30, 2007

Consolidated Financial Results for Six Months Ended September 30, 2007 SOHGO SECURITY SERVICES CO., LTD (URL http://ir.alsok.co.jp/english) (Code No.:2331, TSE 1 st Sec.) Representative: Atsushi Murai,

Consolidated Financial Results for Six Months Ended September 30, 2007 SOHGO SECURITY SERVICES CO., LTD (URL http://ir.alsok.co.jp/english) (Code No.:2331, TSE 1 st Sec.) Representative: Atsushi Murai,

DESIGNIT OSLO A/S STANDALONE FINANCIAL STATEMENTS AS OF AND FOR THE YEAR ENDED MARCH 31, 2016

DESIGNIT OSLO A/S STANDALONE FINANCIAL STATEMENTS AS OF AND FOR THE YEAR ENDED MARCH 31, 2016 Payables include balances due to Micro & Small Enterprises ` NIL as on 31 st March 2016. *Trade 1. Company

DESIGNIT OSLO A/S STANDALONE FINANCIAL STATEMENTS AS OF AND FOR THE YEAR ENDED MARCH 31, 2016 Payables include balances due to Micro & Small Enterprises ` NIL as on 31 st March 2016. *Trade 1. Company

Data Compilation Financial Data

Data Compilation Financial Data CONTENTS 1. Transition of Significant Management Indicators, etc. Japan Post Group (Consolidated) 124 Japan Post Service Co., Ltd. (Non-consolidated) 125 Japan Post Holdings

Data Compilation Financial Data CONTENTS 1. Transition of Significant Management Indicators, etc. Japan Post Group (Consolidated) 124 Japan Post Service Co., Ltd. (Non-consolidated) 125 Japan Post Holdings

Consolidated Financial Statements

Consolidated Financial Statements For the year ended February 20, 2016 Nitori Holdings Co., Ltd. Consolidated Balance Sheet Nitori Holdings Co., Ltd. and consolidated subsidiaries As at February 20, 2016

Consolidated Financial Statements For the year ended February 20, 2016 Nitori Holdings Co., Ltd. Consolidated Balance Sheet Nitori Holdings Co., Ltd. and consolidated subsidiaries As at February 20, 2016

Notes on the parent company financial statements

316 Financial statements Prudential plc Annual Report 2012 Notes on the parent company financial statements 1 Nature of operations Prudential plc (the Company) is a parent holding company. The Company

316 Financial statements Prudential plc Annual Report 2012 Notes on the parent company financial statements 1 Nature of operations Prudential plc (the Company) is a parent holding company. The Company

IFrS. Disclosure checklist. July 2011. kpmg.com/ifrs

IFrS Disclosure checklist July 2011 kpmg.com/ifrs Contents What s new? 1 1. General presentation 2 1.1 Presentation of financial statements 2 1.2 Changes in equity 12 1.3 Statement of cash flows 13 1.4

IFrS Disclosure checklist July 2011 kpmg.com/ifrs Contents What s new? 1 1. General presentation 2 1.1 Presentation of financial statements 2 1.2 Changes in equity 12 1.3 Statement of cash flows 13 1.4

EXPLANATORY NOTES. 1. Summary of accounting policies

1. Summary of accounting policies Reporting Entity Taranaki Regional Council is a regional local authority governed by the Local Government Act 2002. The Taranaki Regional Council group (TRC) consists

1. Summary of accounting policies Reporting Entity Taranaki Regional Council is a regional local authority governed by the Local Government Act 2002. The Taranaki Regional Council group (TRC) consists

2.1 Fixed Assets are stated at cost of acquisition less depreciation.

SCHEDULE - 16 SIGNIFICANT ACCOUNTING POLICIES 1. ACCOUNTING CONVENTION 1.1 The financial statements are drawn up in accordance with the Regulatory provisions of section 11(1) of the Insurance Act, 1938;

SCHEDULE - 16 SIGNIFICANT ACCOUNTING POLICIES 1. ACCOUNTING CONVENTION 1.1 The financial statements are drawn up in accordance with the Regulatory provisions of section 11(1) of the Insurance Act, 1938;

Consolidated Summary Report <under Japanese GAAP>

Consolidated Summary Report for the three months ended June 30, 2014 July 31, 2014 Company name: Mitsubishi UFJ Financial Group, Inc. Stock exchange listings: Tokyo, Nagoya, New York

Consolidated Summary Report for the three months ended June 30, 2014 July 31, 2014 Company name: Mitsubishi UFJ Financial Group, Inc. Stock exchange listings: Tokyo, Nagoya, New York

5 BUSINESS ACCOUNTING STANDARD CASH FLOW STATEMENT I. GENERAL PROVISIONS II. KEY DEFINITIONS

APPROVED by Resolution No. 1 of 18 December 2003 of the Standards Board of the Public Establishment the Institute of Accounting of the Republic of Lithuania 5 BUSINESS ACCOUNTING STANDARD CASH FLOW STATEMENT

APPROVED by Resolution No. 1 of 18 December 2003 of the Standards Board of the Public Establishment the Institute of Accounting of the Republic of Lithuania 5 BUSINESS ACCOUNTING STANDARD CASH FLOW STATEMENT

Consolidated Balance Sheets

Consolidated Balance Sheets March 31 2015 2014 2015 Assets: Current assets Cash and cash equivalents 726,888 604,571 $ 6,057,400 Marketable securities 19,033 16,635 158,608 Notes and accounts receivable:

Consolidated Balance Sheets March 31 2015 2014 2015 Assets: Current assets Cash and cash equivalents 726,888 604,571 $ 6,057,400 Marketable securities 19,033 16,635 158,608 Notes and accounts receivable:

Online Disclosures Relating to Notice of the 101st Annual Shareholders Meeting

Online Disclosures Relating to Notice of the 101st Annual Shareholders Meeting Notes to Consolidated Financial Statements Notes to Non-Consolidated Financial Statements (From April 1, 2015 to March 31,

Online Disclosures Relating to Notice of the 101st Annual Shareholders Meeting Notes to Consolidated Financial Statements Notes to Non-Consolidated Financial Statements (From April 1, 2015 to March 31,

Ratio Analysis. A) Liquidity Ratio : - 1) Current ratio = Current asset Current Liability

Liquidity Ratio : - 1) Current ratio = Current asset Current Liability") A) Liquidity Ratio : - Ratio Analysis 1) Current ratio = Current asset Current Liability 2) Quick ratio or Acid Test ratio = Quick Asset Quick liability Quick Asset = Current Asset Stock Quick Liability

A) Liquidity Ratio : - Ratio Analysis 1) Current ratio = Current asset Current Liability 2) Quick ratio or Acid Test ratio = Quick Asset Quick liability Quick Asset = Current Asset Stock Quick Liability

NEPAL ACCOUNTING STANDARDS ON PRESENTATION OF FINANCIAL STATEMENTS

NAS 01 NEPAL ACCOUNTING STANDARDS ON PRESENTATION OF FINANCIAL STATEMENTS CONTENTS Paragraphs OBJECTIVE SCOPE 1-4 PURPOSE OF FINANCIAL STATEMENTS 5 Responsibility for financial statements 6 Components

NAS 01 NEPAL ACCOUNTING STANDARDS ON PRESENTATION OF FINANCIAL STATEMENTS CONTENTS Paragraphs OBJECTIVE SCOPE 1-4 PURPOSE OF FINANCIAL STATEMENTS 5 Responsibility for financial statements 6 Components

1. Parent company accounting policies

Financial Statements Notes to the parent company financial statements 1. Parent company accounting policies Basis of preparation The separate financial statements of the Company are presented as required

Financial Statements Notes to the parent company financial statements 1. Parent company accounting policies Basis of preparation The separate financial statements of the Company are presented as required

Consolidated Balance Sheets March 31, 2001 and 2000

Financial Statements SEIKAGAKU CORPORATION AND CONSOLIDATED SUBSIDIARIES Consolidated Balance Sheets March 31, 2001 and 2000 Assets Current assets: Cash and cash equivalents... Short-term investments (Note

Financial Statements SEIKAGAKU CORPORATION AND CONSOLIDATED SUBSIDIARIES Consolidated Balance Sheets March 31, 2001 and 2000 Assets Current assets: Cash and cash equivalents... Short-term investments (Note

MATRIX IT LTD. AND ITS SUBSIDIARIES CONSOLIDATED FINANCIAL STATEMENTS

CONSOLIDATED FINANCIAL STATEMENTS AS OF DECEMBER 31, 2013 CONSOLIDATED FINANCIAL STATEMENTS AS OF DECEMBER 31, 2013 NIS IN THOUSANDS INDEX Page Auditors' Reports 2-4 Consolidated Statements of Financial

CONSOLIDATED FINANCIAL STATEMENTS AS OF DECEMBER 31, 2013 CONSOLIDATED FINANCIAL STATEMENTS AS OF DECEMBER 31, 2013 NIS IN THOUSANDS INDEX Page Auditors' Reports 2-4 Consolidated Statements of Financial

Consolidated financial statements

Summary of significant accounting policies Basis of preparation DSM s consolidated financial statements have been prepared in accordance with International Financial Reporting Standards (IFRS) as adopted

Summary of significant accounting policies Basis of preparation DSM s consolidated financial statements have been prepared in accordance with International Financial Reporting Standards (IFRS) as adopted

Accounting and Reporting Policy FRS 102. Staff Education Note 14 Credit unions - Illustrative financial statements

Accounting and Reporting Policy FRS 102 Staff Education Note 14 Credit unions - Illustrative financial statements Disclaimer This Education Note has been prepared by FRC staff for the convenience of users

Accounting and Reporting Policy FRS 102 Staff Education Note 14 Credit unions - Illustrative financial statements Disclaimer This Education Note has been prepared by FRC staff for the convenience of users

TUCKAMORE CAPITAL MANAGEMENT INC.

Consolidated Interim Financial Statements of TUCKAMORE CAPITAL MANAGEMENT INC. Three and Six Months Ended June 30, 2013 and 2012 (Unaudited) These statements have not been reviewed by an independent firm

Consolidated Interim Financial Statements of TUCKAMORE CAPITAL MANAGEMENT INC. Three and Six Months Ended June 30, 2013 and 2012 (Unaudited) These statements have not been reviewed by an independent firm

CEMATRIX CORPORATION Consolidated Financial Statements (in Canadian dollars) September 30, 2015

September 30, 2015") Consolidated Financial Statements September 30, 2015 Management s Responsibility for Financial Reporting and Notice of No Auditor Review of the Interim Consolidated Financial Statements for the Three and

Consolidated Financial Statements September 30, 2015 Management s Responsibility for Financial Reporting and Notice of No Auditor Review of the Interim Consolidated Financial Statements for the Three and

Capitalisation of borrowing costs. From theory to practice April 2009

Capitalisation of borrowing costs From theory to practice April 2009 Capitalisation of borrowing costs 1 Introduction The International Accounting Standards Board (IASB) issued a revised version of IAS

Capitalisation of borrowing costs From theory to practice April 2009 Capitalisation of borrowing costs 1 Introduction The International Accounting Standards Board (IASB) issued a revised version of IAS

Investments and advances... 344,499

Consolidated Financial Statements of the Company The consolidated balance sheet, statement of income, and statement of equity of the Company are as follows. Please note the Company s consolidated financial

Consolidated Financial Statements of the Company The consolidated balance sheet, statement of income, and statement of equity of the Company are as follows. Please note the Company s consolidated financial

Foreign Currency Translation

Statement of Accounting Standards Foreign Currency Translation Prepared by the Accounting Standards Board and the Public Sector Accounting Standards Board of the Australian Accounting Research Foundation

Statement of Accounting Standards Foreign Currency Translation Prepared by the Accounting Standards Board and the Public Sector Accounting Standards Board of the Australian Accounting Research Foundation

CONSOLIDATED STATEMENT OF INCOME

CONSOLIDATED STATEMENT OF INCOME 4 th quarter (a) 3 rd quarter 4 th quarter 2009 Sales 40,157 40,180 36,228 Excise taxes (4,397) (4,952) (4,933) Revenues from sales 35,760 35,228 31,295 Purchases, net

CONSOLIDATED STATEMENT OF INCOME 4 th quarter (a) 3 rd quarter 4 th quarter 2009 Sales 40,157 40,180 36,228 Excise taxes (4,397) (4,952) (4,933) Revenues from sales 35,760 35,228 31,295 Purchases, net

Anadolu Hayat Emeklilik Anonim Şirketi Consolidated Balance Sheet As At 31 December 2015 (Currency: Turkish Lira (TRY))

)") Consolidated Balance Sheet As At ASSETS I- Current Assets A- Cash and Cash Equivalents 14 302,999,458 216,428,429 1- Cash 14 3,385 27,952 2- Cheques Received 3- Banks 14 145,598,543 87,301,020 4- Cheques

Consolidated Balance Sheet As At ASSETS I- Current Assets A- Cash and Cash Equivalents 14 302,999,458 216,428,429 1- Cash 14 3,385 27,952 2- Cheques Received 3- Banks 14 145,598,543 87,301,020 4- Cheques

Cathay Life Insurance Co., Ltd. Financial Statements As of December 31, 2006 and 2007 With Independent Auditors Report

Financial Statements With Independent Auditors Report The reader is advised that these financial statements have been prepared originally in Chinese. These financial statements do not include additional

Financial Statements With Independent Auditors Report The reader is advised that these financial statements have been prepared originally in Chinese. These financial statements do not include additional

Consolidated Interim Earnings Report

Consolidated Interim Earnings Report For the Six Months Ended 30th September, 2003 23th Octorber, 2003 Hitachi Capital Corporation These financial statements were prepared for the interim earnings release

Consolidated Interim Earnings Report For the Six Months Ended 30th September, 2003 23th Octorber, 2003 Hitachi Capital Corporation These financial statements were prepared for the interim earnings release

Life Business Guidance Notes

REVENUE ACCOUNT Income 1. Policyholders fund brought forward refers to policyholders fund and investment linked fund brought forward from the preceding financial/calendar year. It should correspond with

REVENUE ACCOUNT Income 1. Policyholders fund brought forward refers to policyholders fund and investment linked fund brought forward from the preceding financial/calendar year. It should correspond with

Exposure Draft. Guidance Note on Accounting for Derivative Contracts

Exposure Draft Guidance Note on Accounting for Derivative Contracts (Last date of comments: January 21, 2015) Issued by Research Committee The Institute of Chartered Accountants of India (Set up by an

Exposure Draft Guidance Note on Accounting for Derivative Contracts (Last date of comments: January 21, 2015) Issued by Research Committee The Institute of Chartered Accountants of India (Set up by an

Unaudited Interim Consolidated Financial Statements and Footnotes July 3, 2011

Unaudited Interim Consolidated Financial Statements and Footnotes July 3, 2011 1 MEXICAN RESTAURANTS, INC. AND SUBSIDIARIES CONSOLIDATED BALANCE SHEETS (unaudited) 7/3/2011 1/2/2011 ASSETS Current assets:

Unaudited Interim Consolidated Financial Statements and Footnotes July 3, 2011 1 MEXICAN RESTAURANTS, INC. AND SUBSIDIARIES CONSOLIDATED BALANCE SHEETS (unaudited) 7/3/2011 1/2/2011 ASSETS Current assets:

A Guide to for Financial Instruments in the Public Sector

November 2011 www.bdo.ca Assurance and accounting A Guide to Accounting for Financial Instruments in the Public Sector In June 2011, the Public Sector Accounting Standards Board released Section PS3450,

November 2011 www.bdo.ca Assurance and accounting A Guide to Accounting for Financial Instruments in the Public Sector In June 2011, the Public Sector Accounting Standards Board released Section PS3450,

International Accounting Standard 1 Presentation of Financial Statements

IAS 1 Presentation of Financial Statements International Accounting Standard 1 Presentation of Financial Statements Objective 1 This Standard prescribes the basis for presentation of general purpose financial

IAS 1 Presentation of Financial Statements International Accounting Standard 1 Presentation of Financial Statements Objective 1 This Standard prescribes the basis for presentation of general purpose financial

AcuityAds Inc. Condensed Consolidated Interim Financial Statements. Three months ended March 31, 2014 and 2013 (Unaudited)

") AcuityAds Inc. Condensed Consolidated Interim Financial Statements Condensed Consolidated Interim Statements of Financial Position March 31, December 31, 2014 2013 Assets Current assets: Cash $ 446,034

AcuityAds Inc. Condensed Consolidated Interim Financial Statements Condensed Consolidated Interim Statements of Financial Position March 31, December 31, 2014 2013 Assets Current assets: Cash $ 446,034

SCHEDULE-17 SIGNIFICANT ACCOUNTING POLICIES 1. GENERAL BASIS OF PREPARATION

SCHEDULE-17 SIGNIFICANT ACCOUNTING POLICIES 1. GENERAL BASIS OF PREPARATION The financial statements have been prepared and presented under historical cost convention on accrual basis of accounting unless

SCHEDULE-17 SIGNIFICANT ACCOUNTING POLICIES 1. GENERAL BASIS OF PREPARATION The financial statements have been prepared and presented under historical cost convention on accrual basis of accounting unless

CIMA Managerial Level Paper F2 FINANCIAL MANAGEMENT (REVISION SUMMARIES)

") CIMA Managerial Level Paper F2 FINANCIAL MANAGEMENT (REVISION SUMMARIES) Chapter Title Page number 1 The regulatory framework 3 2 What is a group 9 3 Group accounts the statement of financial position

CIMA Managerial Level Paper F2 FINANCIAL MANAGEMENT (REVISION SUMMARIES) Chapter Title Page number 1 The regulatory framework 3 2 What is a group 9 3 Group accounts the statement of financial position

Volex Group plc. Transition to International Financial Reporting Standards Supporting document for 2 October 2005 Interim Statement. 1.

Volex Group plc Transition to International Financial Reporting Standards Supporting document for 2 October 2005 Interim Statement 1. Introduction The consolidated financial statements of Volex Group plc

Volex Group plc Transition to International Financial Reporting Standards Supporting document for 2 October 2005 Interim Statement 1. Introduction The consolidated financial statements of Volex Group plc

Consolidated Financial Statements (In Canadian dollars) ACUITYADS INC. Years ended December 31, 2013, 2012 and 2011

ACUITYADS INC. Years ended December 31, 2013, 2012 and 2011") Consolidated Financial Statements ACUITYADS INC. KPMG LLP Telephone (416) 228-7000 Yonge Corporate Centre Fax (416) 228-7123 4100 Yonge Street Suite 200 Internet www.kpmg.ca Toronto ON M2P 2H3 Canada To

Consolidated Financial Statements ACUITYADS INC. KPMG LLP Telephone (416) 228-7000 Yonge Corporate Centre Fax (416) 228-7123 4100 Yonge Street Suite 200 Internet www.kpmg.ca Toronto ON M2P 2H3 Canada To

MITSUI SUMITOMO INSURANCE COMPANY, LIMITED AND SUBSIDIARIES. CONSOLIDATED BALANCE SHEETS March 31, 2005 and 2006

CONSOLIDATED BALANCE SHEETS March 31, 2005 and 2006 2005 2006 ASSETS Investments - other than investments in affiliates: Securities available for sale: Fixed maturities, at fair value 3,043,851 3,193,503

CONSOLIDATED BALANCE SHEETS March 31, 2005 and 2006 2005 2006 ASSETS Investments - other than investments in affiliates: Securities available for sale: Fixed maturities, at fair value 3,043,851 3,193,503

Consolidated Financial Results

UFJ Holdings, Inc. November 25, 2003 For the Six Months Ended September 30, 2003 UFJ Holdings, Inc. today reported the company's consolidated financial results for the six months ended September 30, 2003.

UFJ Holdings, Inc. November 25, 2003 For the Six Months Ended September 30, 2003 UFJ Holdings, Inc. today reported the company's consolidated financial results for the six months ended September 30, 2003.

Accounting for ESOP. IPCC Paper 5: Advanced Accounting Chapter 4. CA. Shruthi BN, Bangalore

Accounting for ESOP IPCC Paper 5: Advanced Accounting Chapter 4 CA. Shruthi BN, Bangalore Learning Objectives 1 After studying this unit, you will be able to learn the provisions of the Companies Act,

Accounting for ESOP IPCC Paper 5: Advanced Accounting Chapter 4 CA. Shruthi BN, Bangalore Learning Objectives 1 After studying this unit, you will be able to learn the provisions of the Companies Act,

5. Provisions for decrease in value of marketable securities (-)

") Balance sheet ASSETS I. CURRENT ASSETS A. Liquid Assets: 1. Cash. 2. Cheques received. 3. Banks. 4. Cheques given and payment orders (-). 5. Other liquid assets. B. Marketable Securities: 1. Share certificates.

Balance sheet ASSETS I. CURRENT ASSETS A. Liquid Assets: 1. Cash. 2. Cheques received. 3. Banks. 4. Cheques given and payment orders (-). 5. Other liquid assets. B. Marketable Securities: 1. Share certificates.

Abbey plc ( Abbey or the Company ) Interim Statement for the six months ended 31 October 2007

Interim Statement for the six months ended 31 October 2007") Abbey plc ( Abbey or the Company ) Interim Statement for the six months ended 31 October 2007 The Board of Abbey plc reports a profit before taxation of 18.20m which compares with a profit of 22.57m for

Abbey plc ( Abbey or the Company ) Interim Statement for the six months ended 31 October 2007 The Board of Abbey plc reports a profit before taxation of 18.20m which compares with a profit of 22.57m for

Quarterly report containing interim financial statements of the Capital Group for Q1 of the financial year 2013-2014

Quarterly report containing interim financial statements of the Capital Group for Q1 of the financial year 2013-2014 covering the period from 01-07-2013 to 30-09-2013 Publication date: 14 November 2013

Quarterly report containing interim financial statements of the Capital Group for Q1 of the financial year 2013-2014 covering the period from 01-07-2013 to 30-09-2013 Publication date: 14 November 2013

STATEMENT OF COMPLIANCE AND BASIS OF MEASUREMENT

Accounting policies REPORTING ENTITY The Waikato Regional Council is a territorial local authority governed by the Local Government Act 2002, and is domiciled in New Zealand. The main purpose of prospective

Accounting policies REPORTING ENTITY The Waikato Regional Council is a territorial local authority governed by the Local Government Act 2002, and is domiciled in New Zealand. The main purpose of prospective

Consolidated financial statements

Rexam Annual Report 83 Consolidated financial statements Consolidated financial statements: Independent auditors report to the members of Rexam PLC 84 Consolidated income statement 87 Consolidated statement

Rexam Annual Report 83 Consolidated financial statements Consolidated financial statements: Independent auditors report to the members of Rexam PLC 84 Consolidated income statement 87 Consolidated statement

Western Energy Services Corp. Condensed Consolidated Financial Statements September 30, 2015 and 2014 (Unaudited)

") Condensed Consolidated Financial Statements September 30, 2015 and 2014 (Unaudited) Condensed Consolidated Balance Sheets (Unaudited) (thousands of Canadian dollars) Note September 30, 2015 December 31,

Condensed Consolidated Financial Statements September 30, 2015 and 2014 (Unaudited) Condensed Consolidated Balance Sheets (Unaudited) (thousands of Canadian dollars) Note September 30, 2015 December 31,

FOREIGN CURRENCY TRANSACTIONS 8-16. Initial Recognition 8-10. Reporting at Subsequent Balance Sheet Dates 11-12

108 Accounting Standard (AS) 11 The Effects of Changes in Foreign Exchange Rates Contents OBJECTIVE SCOPE Paragraphs 1-6 DEFINITIONS 7 FOREIGN CURRENCY TRANSACTIONS 8-16 Initial Recognition 8-10 Reporting

108 Accounting Standard (AS) 11 The Effects of Changes in Foreign Exchange Rates Contents OBJECTIVE SCOPE Paragraphs 1-6 DEFINITIONS 7 FOREIGN CURRENCY TRANSACTIONS 8-16 Initial Recognition 8-10 Reporting

SUMITOMO DENSETSU CO., LTD. AND SUBSIDIARIES. Consolidated Financial Statements

SUMITOMO DENSETSU CO., LTD. AND SUBSIDIARIES Consolidated Financial Statements Report of Independent Public Accountants To the Board of Directors of Sumitomo Densetsu Co., Ltd. : We have audited the consolidated

SUMITOMO DENSETSU CO., LTD. AND SUBSIDIARIES Consolidated Financial Statements Report of Independent Public Accountants To the Board of Directors of Sumitomo Densetsu Co., Ltd. : We have audited the consolidated

Nature of operations and basis of preparation (Note 1) Commitments and contingencies (Note 10) Subsequent events (Note 12)

Commitments and contingencies (Note 10) Subsequent events (Note 12)") Unaudited Interim Consolidated Financial Statements For the nine months ended September 30, 2005 Contents Interim Consolidated Financial Statements Interim Consolidated Balance Sheets Interim Consolidated

Unaudited Interim Consolidated Financial Statements For the nine months ended September 30, 2005 Contents Interim Consolidated Financial Statements Interim Consolidated Balance Sheets Interim Consolidated

Chapter Twelve. Current Liabilities. Current Liabilities for Competing Companies

Chapter Twelve Current Liabilities and Contingencies 1. Define current liabilities & identify common CL 2. Account for accruals 3. Account for deferrals 4. Account for compensated absences 5. How to report

Chapter Twelve Current Liabilities and Contingencies 1. Define current liabilities & identify common CL 2. Account for accruals 3. Account for deferrals 4. Account for compensated absences 5. How to report

SAGICOR FINANCIAL CORPORATION

Interim Financial Statements Nine-months ended September 30, 2015 FINANCIAL RESULTS FOR THE CHAIRMAN S REVIEW The Sagicor Group recorded net income from continuing operations of US $60.4 million for the

Interim Financial Statements Nine-months ended September 30, 2015 FINANCIAL RESULTS FOR THE CHAIRMAN S REVIEW The Sagicor Group recorded net income from continuing operations of US $60.4 million for the

Large Company Limited. Report and Accounts. 31 December 2009

Registered number 123456 Large Company Limited Report and Accounts 31 December 2009 Report and accounts Contents Page Company information 1 Directors' report 2 Statement of directors' responsibilities

Registered number 123456 Large Company Limited Report and Accounts 31 December 2009 Report and accounts Contents Page Company information 1 Directors' report 2 Statement of directors' responsibilities

Accounting 500 4A Balance Sheet Page 1

Accounting 500 4A Balance Sheet Page 1 I. PURPOSE A. The Balance Sheet shows the financial position of the company at a specific point in time (a date) 1. This differs from the Income Statement which measures

Accounting 500 4A Balance Sheet Page 1 I. PURPOSE A. The Balance Sheet shows the financial position of the company at a specific point in time (a date) 1. This differs from the Income Statement which measures