ITEM NO. 1 & 2. PUBLIC UTILITY COMMISSION OF OREGON STAFF REPORT PUBLIC MEETING DATE: September 22, 2005

|

|

|

- Arthur Poole

- 8 years ago

- Views:

Transcription

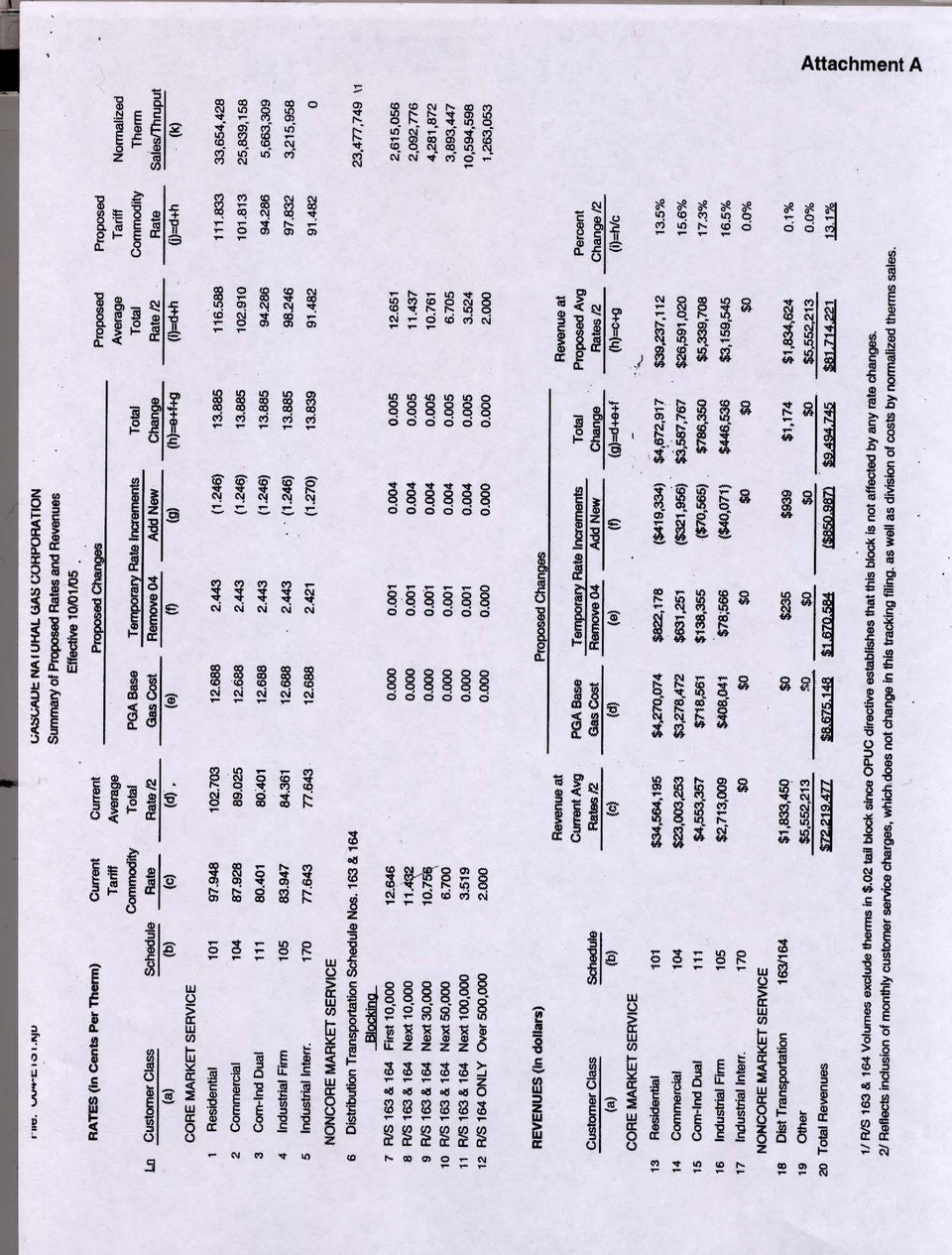

1 PUBLIC UTILITY COMMISSION OF OREGON STAFF REPORT PUBLIC MEETING DATE: September 22, 2005 ITEM NO. 1 & 2 REGULAR X CONSENT EFFECTIVE DATE October 1, 2005 DATE: TO: FROM: Public Utility Commission Ken Zimmerman, Lynn Kittilson and Ed Durrenberger THROUGH: Lee Sparling, Ed Busch, Judy Johnson and Bonnie Tatom SUBJECT: CASCADE NATURAL GAS: (Docket No. UG 164/Advice No. O ) Reflects changes in the cost of purchased gas and technical adjustments. (Docket No. UM 1214) Requests reauthorization of the PGA deferral mechanism. STAFF RECOMMENDATION: We recommend the Commission approve Cascade Natural Gas Corporation s (Cascade or company) request to waive statutory notice (L.S.N.) and allow the company s proposed tariff sheets in Advice No. CNG/O to become effective with service on and after October 1, This filing increases the company s annual revenues by $9.5 million, or 13.1%. We also recommend the Commission approve the company s request for reauthorization to use deferred accounting pursuant to its Purchased Gas Adjustment (PGA) balancing account. DISCUSSION: On August 15, 2005, Cascade submitted its annual gas cost tracking and technical adjustment filing, commonly known as its PGA filing. The PGA allows Cascade to adjust tariffs annually for known and measurable changes in purchased base gas costs and for changes in amortization rates relating to the PGA balancing account and other deferred accounts. This filing consisted of a proposed increase in annual revenues in Advice No. CNG/O (docketed as UG 164), effective October 1, In a concurrent filing docketed as UM 1214, Cascade requested reauthorization of deferrals under the company s PGA mechanism.

request to waive statutory notice (L.S.N.) and allow the company s proposed tariff sheets in Advice No.")

2 Page 2 On September 8, 2005, Cascade filed replacement tariff sheets to correct minor errors found by Staff, along with an L.S.N. The corrections do not revise the company s filed rates. Cascade requested that all proposed tariff sheets become effective October 1, UG 164 This application requests authority to increase rates to: (1) track increases in purchased gas costs, and (2) make technical adjustments to amortize Cascade s deferred revenue, gas cost, and Demand Side Management (DSM) accounts. The change in annual revenues is summarized below, and shown in Attachment A. PGA Base Gas Cost Change $ 8,675,148 Removal of Prior Year Temporary Credit Increment $ 1,670,584 Addition of New Temporary Credit Increment $ (850,987) Total Proposed Increase $ 9,494,745 With these changes, the monthly bill of a typical residential customer using 63 therms per month will increase by $8.74, or 13.5 percent, from $64.71 to $ In January, a typical residential customer's consumption of 131 therms would result in a billing increase from $ to $ A summary of the proposed tariff and revenue changes for Cascade s major rate schedules is shown in Attachment A. A summary that compares the impact of this year's proposed PGA rate changes, on both an annual and January basis, for Cascade, Avista and NW Natural residential customers is shown in Attachment B. A graph illustrating each of the three local distribution companies (LDCs ) effective residential rates on a comparable basis is found in Attachment C. The effective residential rate is calculated as follows: the proposed residential rate multiplied by 65 therms plus the monthly customer charge, divided by 65 therms. The graph shows that Cascade s residential customers have an effective rate of $ per therm, while Avista s and NW Natural s effective rates are $ and $ , respectively. The table on the top of the next page shows the rates the Commission has approved for Cascade's residential customers on Rate Schedule 101 between 2001 and 2004, and the current proposal.

accounts. The change in annual revenues is summarized below, and shown in Attachment A.")

3 Page 3 Customer Rate Per Percentage Date Charge Therm Change October 2001 $3.00 $ October 2002 $3.00 $ % October 2003 $3.00 $ % October 2004 $3.00 $ % October 2005 (Proposed) $3.00 $ % Cascade offers customer assistance programs. Specific information on these programs is readily available to customers on their monthly bills, by telephone, and on the company's web site. Staff Review of Gas Costs National and Regional Natural Gas Markets An unprecedented crisis 1 in the natural gas industry has evolved over the last 10 years. The price of natural gas has risen over 300% and, barring a dramatic reduction in demand or huge new supplies, will rise further. Moreover, because North American natural gas production has plateaued, 2 reliability of supply is now also an issue. It is clear that the mistakes of the middle to late 1990s in quantifying remaining North American natural gas reserves and the continuing construction of gas-fired generation to meet the US growing demand for electricity are primary causes of the current crisis. The nonsensical coupling of natural gas and oil prices 3 also contributed to a run-up in natural gas futures price which forced the cash market to follow. Since 1999, over 395 GW of new gas-fired generation has come on line, with more expected to be built. This is to meet electricity demand that is expected to grow at or near 2% a year through at least By 2015, power generation will likely consume nearly 11 Trillion cubic feet The percentage change reflects only the change in the rate per therm, and does not include the effect of the monthly customer charge on the bill. In 2005, when the rate per therm is combined with the monthly customer charge of $3.00, the average customer s bill is increased about 13.5%, as shown on Attachment B. 1 American Chemical Council, American Council for an Energy Efficient Economy, Matt Simmons, Joseph Riva, senior geologist Colorado School of Mines, Frank Clemente, Andrew Weissman, National Petroleum Council (which refrains from actually using the word crisis), the International Energy Agency, the US Energy Information Administration, Exxon/Mobile, Royal Dutch Shell, Chevron, Total, and Alan Greenspan. 2 See Andrew Weissman and the International Energy Agency in particular. 3 The two are generally not substitutable except in limited circumstances. Oil and natural gas prices were not historically linked and supply/demand for the two are not generally interconnected. Finally, the physical characteristics of the two are very different, as is their production.

4 Page 4 (Tcf) a year more natural gas than it did in This generation was constructed and continues to be constructed based on erroneous information that North American natural gas supplies would remain plentiful for many decades. 4 This, combined with the low upfront capital cost and generally low emissions of such generation compared to other options, made gas-fired generation seem a clear winner. This has left the US with a continually expanding demand for natural gas that it cannot supply domestically (or even from North America). In short, the US has now entered a chronic (continuing) undersupply situation 5, made worse by the over 232 Tcf of estimated US outer continental shelf and Rockies natural gas that remains off limits for production due to federal restrictions. The push to quickly build more LNG terminals in the US to access world natural gas supply is clear evidence of this US undersupply situation. Current Cash (Spot) Price of Natural Gas National prices for natural gas have risen consistently over the last year and are expected to continue to increase through the end of Many forecasters believe the upward trend will subside in the second or third quarter of The pattern of volatility in natural gas prices appears unabated during the last year, but did not become more intense. Intra-month volatility has been particularly pronounced over the last 2 years. The Henry Hub spot (cash) natural gas price began the period (October 2004) near $6.25/MMBtu, remained relatively constant at that level through February 2005, and began to increase noticeably in March The Henry Hub price is expected to close the period (September 2005) at about $8.80, a more than 40% increase in price from October Northwest natural gas cash prices followed the same general pattern as the Henry Hub, with a basis difference between the Henry Hub and the Northwest averaging about negative $1.25. Northwest prices began the period at $5.05 and ended at just over $7.60, a more than 50% increase in price. Price patterns in the Midwest and Northeast were similar to but not identical to those in the Northwest. The primary factors that appear to explain these changes in natural gas price are: 1. Increased consumer demand (particularly for electric generation), tight supplies, and record crude-oil prices 2. No significant change in LNG imports 3. Increases in Rockies production are primarily unconventional (more expensive) 4 A few claim large supplies remain untapped due to government restrictions. While it is true that large known supplies are off-limits due to government restrictions, these supplies are not large enough to avert the crisis. 5 Undersupply refers to both depletion of supply and the peaking of production capability in North America.

.")

5 Page 5 4. Continuing decline in US production 5. Continuing decline in Canadian production 6. Continuing growth in the US economy NYMEX Price NYMEX natural gas futures prices also increased noticeably over the period, particularly for winter gas supplies. The table below depicts the changes in the price for each month over the period on the NYMEX exchange as of August 11, As of September 13, the NYMEX price for most months through September 2006 was up, especially for the winter months which averaged almost $12. The average increase in the NYMEX price over the period since October 2004 is now %. A large share of this increase is the result of the shut-ins caused by Hurricane Katrina, but some is systemic and is likely to remain throughout the coming year. Month Price October 2004 Price August 11, 2005 Change % October 2005 $7.00 $ % November $7.00 $ % December $7.50 $ % January 2006 $7.60 $ % February $7.60 $ % March $7.40 $ % April $6.25 $ % May $6.20 $ % June $6.10 $ % July $6.00 $ % August $6.10 $ % September $6.05 $ % AVERAGES $6.73 $ % Over the last year the NYMEX has established a significant premium over current spot (cash) prices, averaging currently over $2 per MMBtu. As of September 14, 2005, forecasts of natural gas prices for the upcoming winter and beyond have congealed around several values, including the effects of Hurricane Katrina. First, the price at the Henry Hub is expected to be between $11.00 and $11.50 for the final quarter of This translates to an expected Northwest price of $9.75 to $ Prices at the Henry Hub are forecasted to decline slightly in 2006, averaging just below $8.50, or $7.25 for the Northwest. First, second, and third quarter prices for the Henry Hub in 2006 are expected to average $10.02, $7.53, and $7.20, respectively, according to the EIA. This translates to approximately $8.77, $6.28, and $5.95, respectively, expected for the Northwest. Changes in weather, demand, or supplies

6 Page 6 could, of course, lead to changes in these price forecasts or to the actual prices experienced. In addition to the factors listed above under Current Cash (Spot) Price of Natural Gas, other factors that appear important in explaining the NYMEX price are: 1. The tendency of many NYMEX traders to discount the notion that prices can be controlled through either supply or demand response (e.g., storage, conservation) 2. The tendency of NYMEX traders to focus more on bad news than good, and to place more credence in bad news than good 3. The role definition of NYMEX traders as price makers 4. NYMEX traders generally shallow knowledge of energy engineering and politics, apart from commodity economics 6 5. Treating natural gas as only a commodity 6 Gas Supply and Production The American Gas Association estimates that 57% (or 1,600 billion cubic feet) of the natural gas flowing to America s homes during the coldest month of the winter will come from domestic production. This estimated proportion is down by 7% from the 64% from domestic production in Natural gas from underground storage is expected to supply about 30% of the natural gas used during the peak winter month, followed by Canadian imports (10.8%), LNG (1.8%) and supplementals, such as propane-air facilities (0.3%). This indicates the increasing importance of storage gas and LNG in meeting US peak winter gas needs. Many factors can influence production. Hurricanes are certainly one of these factors. The effects of hurricane Katrina on natural gas production in the Gulf of Mexico were substantial. As of August 31 at 4 PM (EST), billion cubic feet per day of Gulf natural gas production was shut-in, equivalent to 83.46% of daily Gulf natural gas production (which is 10 Bcf per day). Prices reflected this reduced supply. The NYMEX price reached a high of nearly $11.50/MMBtu at the close of trading on 8/31. The Henry Hub spot price was $12.69/MMBtu on 8/31, up $2.84/MMBtu from the price of Friday, 8/26. At market locations across the Gulf region, price increases ranged up to $4.10/MMBtu with an average of $0.91/MMBtu. The overall average change in price was $0.58/MMBtu. The price at Northwest trading hubs also increased. The price at AECO went up to $8.75, while Sumas and Rocky Mountain gas increased to near $9.00. As of 6 An indication of both this ignorance and the treatment of natural gas as only a commodity is a quote in the text, Trading Natural Gas: A Nontechnical Guide at page 11, The supply of natural gas is essentially dependent on only one factor: price. This is nonsense since the major factors determining supply are physical (e.g., geology, physics and chemistry), both in terms of total supply and production.

7 Page 7 September 13, 2005, the price effects of Katrina on NYMEX, the Henry Hub, and other trading hubs across the country had dissipated to a large extent. However, as of this date, an increase of about $0.50/dekatherm over the pre-katrina price was visible at most Northwest hubs, while an $0.80/dekatherm increase was visible at the Henry Hub and about a $1.00/dekatherm increase was visible on NYMEX. It is unlikely that all of this price increase is due directly to Katrina, since prices were rising at all hubs and on NYMEX prior to Katrina. Katrina apparently has had little impact on receipts of shipments at the LNG terminal at Lake Charles, Louisiana. While no major shortages of natural gas have resulted thus far from Katrina, it now seems possible that shortages could be experienced this winter as a result of Katrina, depending on the severity of the winter. The Mineral Management Service reported on September 13, 2005 that Bcf/d, or 37.20% of daily gas production offshore remained shut-in as a result of Katrina. There are also concerns that it may be as long as four months before full natural gas production from the Gulf is restored. Cascade s Natural Gas Purchasing Strategy Portfolio theory has been accepted for the last two decades as the best means to deal with the risks involved in the purchasing of natural gas by LDCs. This theory is based upon a mathematics of diversification. The theory proposes that LDCs focus on selecting portfolios of gas supplies based on their overall risk-reward characteristics instead of merely compiling portfolios of purchases that each individually has attractive risk-reward characteristics. In a nutshell, LDCs in purchasing natural gas should select portfolios not individual supply options. Such a portfolio should display the three characteristics of balance, flexibility, and diversity, and should be based on the particular circumstances in which the purchases are made. And the greater the risks of price change or supply availability the greater the need to follow the diversity requirements of portfolio theory. The general elements of an effective LDC gas supply portfolio are laid out in the table below. All portfolios should include each of these options, if available, to the extent possible based on the set of physical, operational, and economic circumstances of the particular LDC. No. Portfolio Components 1 Base gas contracts 2 Seasonal contracts 3 Pricing in contracts mix of fixed prices and index prices 4 Contract take provisions flexible to allow daily nominations of less than 100% of MDQ without penalty 5 Storage 6 Multiple suppliers for all contract types (more than six for each type if possible)

8 Page 8 7 No single supplier with sufficient share to dominate gas supply 8 All gas contracts staggered in term 9 Load management, e.g., interruptible sales contracts, real time pricing sales contracts 10 Buy back contracts 11 Energy conservation, e.g., weatherization 12 Financial hedges, e.g., options, swaps, staggered in timing The current and likely to continue crisis in natural gas price and supply means that it is even more important that LDCs learn, understand, and apply portfolio practices in their gas purchasing. And because of the ongoing crisis, LDCs will need to work to expand these practices not only to include additional portfolio components but also to include more sophisticated means to evaluate portfolios. According to Cascade s responses to Staff s data requests regarding its filed 2005 PGA, the portfolio included in the 2005 PGA is based on the Company s actual gas supply contracted volumes and prices for the upcoming winter along with a small amount of Spot supply purchases which would be required to meet the load requirements associated with core customer weather-normalized volumes for the 12 months ending June 30, Cascade s purchasing process is straight forward. A needs forecast is prepared, the availability of existing supply-side and demand-side resources is assessed, expected weather is considered, and transport needs are assessed. This data is entered into the Sendout optimization model, and the model determines the level of unserved demand under each of the alternative weather forecasts (average, colder than normal, warmer than normal). An internal company committee then chooses the scenario which will guide gas purchases. All incremental gas supply needs are met through a bidding process at the available purchase hubs. Approximately 90% of the supply purchases of Cascade are hedged financially through swaps. The company has made an effort to quantify (although not compare with other options) the monetary impact of these swaps. In 2004, Cascade modified its procurement strategy to include physical gas supply purchases for up to 5 years. Cascade does not currently have any physical gas supply contracts with terms longer than 5 years, primarily, according to the company, because of concerns about the possible impact of a longer term commitment on Cascade s creditworthiness. While Cascade s gas purchasing process intuitively adheres to the portfolio philosophy, if not always portfolio methods, the process should apply portfolio methods more rigorously to achieve a balanced, diverse, and flexible purchasing strategy. Today Cascade does not explicitly apply portfolio theory and its associated mathematics. If applied, portfolio practices would add both more rigor and accountability to the purchasing process. This means Cascade does not directly assess the balance, flexibility, and diversity of its chosen or other alternative gas supply portfolios

9 Page 9 mathematically. Second, and on a more practical level, Cascade does not analyze the options it might employ to reduce the price it pays for natural gas. Through financial hedging Cascade fixes the price paid, but does not consider viable options for reducing the price paid. Bidding alone in not sufficient for this task, since bidding in a tight market such as natural gas has limited potential to reduce price paid. For example, contract pricing formulae that allow Cascade to change the index used for pricing (e.g., first-of-the-month vs. daily) or change from index to fixed pricing, could allow Cascade to take advantage of short-term decreases in market price and avoid short-term increases in market price. However, Cascade does seem to have an intuitive understanding of the benefits of balance, flexibility, and diversity in a gas supply portfolio. Adding the specifics of portfolio methods to this intuitive understanding would help Cascade see and consider the options which could be used to reduce its cost of gas. This is a very important objective in light of the trends in current natural gas markets toward higher and more volatile prices, and fewer options for LDCs to mitigate these trends. Cascade and Staff need to work constructively together over the next few months to ensure this objective is achieved in time for the next purchasing season, beginning in April Cascade, like many LDCs, perceives itself as overwhelmed by the current natural gas supply market, largely seeing itself at the mercy of this market. While it is true that LDCs have fewer options for controlling gas price than they had in the past and that natural gas is in crisis, it is false that LDCs are wholly at the mercy of the gas market. But taking advantage of these options will require more than just learning and applying portfolio methods and their associated mathematics. It will require that Cascade more directly and actively manage its gas supply cost on a monthly and sometimes even daily basis, especially during the peak winter period. It also means it will no longer be feasible for Cascade to financially hedge almost all volumes purchased unless the hedging strategy is in line with the general requirements of portfolio methods and the specific portfolio practices designed for the Cascade system and circumstances. Staff s analysis does not indicate that Cascade s current purchasing strategy is imprudent. However, Staff recommends that Cascade analyze and assess the impacts on its gas supply portfolio options, such as the following, for future natural gas purchases: 1. Use of larger variety of contracting formulae (e.g., index changes, flexible MDQ, flexible nominations, weather derivatives). 2. Expand bidding (e.g., combination supply/transport, bid for hedges). 3. Look into purchase partnerships with other LDCs or industrial customers. 4. Portfolio mix changes for study: a. More volumes purchased through contracts of 5 years or longer

10 Page 10 b. Direct LNG contracting c. Build/Purchase strategic storage (storage that allows the LDC to fine tune its purchases, thus reducing the total volumes of NG purchased and the purchase of high priced volumes during times of high need) d. Physical fixed price contracting e. Direct contracting for unconventional gas supplies 5. All this closely coordinated, of course, with demand-response and energy efficiency programs. Unfortunately, due to its relatively small load and level of natural gas purchases, Cascade s opportunities to actually implement many of these options to reduce purchase price may be limited. In addition, Cascade s size also mitigates against adding significant new personnel or resources for Cascade to more rigorously apply portfolio methods. Neither of these factors, however, relieves Cascade of its responsibility to more rigorously apply portfolio methods within the limits of its load and general financial circumstances. Cascade's Natural Gas Costs For the time during which Cascade purchased gas for the period October 2005 through September 2006, the average cash (spot) price in the Northwest was approximately $6.00/MMBtu, with prices noticeably higher during the last two months of the period (July and August 2005). The NYMEX price closed the period (September 2006) at over $9.00 ($7.75)/MMBtu, 7 with prices between $11 ($9.75) and $12 ($10.75) per MMBtu for the winter months of However, the NYMEX price for September 2006 ranged from $6.75 ($5.50) to near $7.25 ($6.00) during April and May of 2005, began to rise noticeably in early June, ending finally just over $9.00 ($7.75) at the end of August. After a spike during March and early April over $8.50 ($7.25), the NYMEX price for the winter months declined below $8.00 ($6.75) in April before beginning a climb in May which, thus far, has produced a high near $12.00 ($10.75). For the current PGA, Cascade proposes to pass through to its sales customers an average delivered natural gas cost of $ /therm ($6.89/dekatherm (MMBtu)) This delivered cost of gas is adjusted for normalized sales volumes and line losses, and an adjustment is made for revenue sensitivity. The result is the sales WACOG proposed by Cascade of $ This pass through proposal is reasonable. Noting once again that future natural gas prices are very likely to be even higher and perhaps more volatile, the changes proposed for Cascade s purchasing process should 7 Prices in parentheses are estimated Northwest prices based on an average basis difference from national price of ($1.25).

11 Page 11 help control its future cost of gas, thus limiting future increases and rate shock. Cascade appears to have intuitively applied portfolio purchasing practices in its purchase of physical gas and financial hedges. Such intuitive application may not work effectively to provide the greatest balance, diversity, and flexibility in Cascade s future gas supply portfolio. Consequently, it is important that Cascade improve its data gathering and analysis related to portfolio construction, to add both more rigor and more accountability to the process. Technical Adjustments - Deferred Accounts Cascade s application proposes to make technical adjustments in amortizing credit and debit balances in its deferred accounts. This activity consists of the following components, as shown on Attachment A. Removal of temporary credit increments currently in place, increasing revenues by $1,670,584. Addition of new temporary increments to refund $850,987 in net credit balances in the company s deferred revenue, gas cost and DSM accounts. The Commission previously authorized all of the deferred amounts subject to amortization. Staff has reviewed the company s technical adjustments and determined that the proposed amortizations are appropriate. The revised amortization increments are incorporated in the energy charge component of the company s primary rate schedules. The net revenue effect of adding the new temporary increments and removing the current increments is an increase of $819,597 on an annual basis. Earnings Review and 3% Test Until 1999, as a matter of policy, the Commission conducted earnings reviews for both prospective purchased gas costs changes and PGA-related deferrals. The Commission then adopted OAR , which requires an annual spring earnings review in lieu of an earnings review related to prospective purchased gas cost changes. In addition, Section (8) of the rule states that an earnings review is not applicable to amortization of deferred gas costs if the LDC assumes at least 33% of the responsibility for commodity cost differences in the risk sharing mechanism. Cascade s mechanism includes a 33% sharing level, so amortization of deferred gas costs in this PGA filing are exempt from an earnings review. ORS (6) and (7) states that the overall annual average rate impact of the amortizations authorized under the statute may not exceed 3% of the natural gas utility s

12 Page 12 gross revenues for the proceeding calendar year, unless the Commission finds that allowing a higher amortization rate is reasonable under the circumstances. Cascade s proposed amortizations are below the 3% cap and may be implemented as proposed. UM 1214 In this filing, Cascade requests reauthorization of deferrals pursuant to its automatic adjustment clause, the PGA mechanism. The information contained in the application is consistent with the requirements of ORS , and OAR The application states that continued deferral of these cost and revenue differences minimizes the frequency of rate changes and appropriately matches costs borne and benefits received by ratepayers, consistent with ORS (2)(e). The reasons cited for reauthorization are still valid. Staff recommends the Commission approve the request for reauthorizing the PGA deferral mechanism, effective October 1, PROPOSED COMMISSION MOTION: Cascade Natural Gas Corporation s request for: 1) amortization of deferred accounts, base gas cost changes, and rate changes as requested in Docket No. UG 164 be approved; 2) the associated tariff sheets of Advice No. CNG/O be allowed to go into effect October 1, 2005, and the L.S.N. be approved; and 3) reauthorization of deferred accounting for Cascade s Purchased Gas Cost Balancing Account mechanism, Schedule No. 177, for one year beginning October 1, 2005, be approved. Attachments

13

14 Comparison of Proposed Rate and Bill Increases for Oregon Local Distribution Companies by Class of Service (October 2005 PGAs) RATE IMPACTS BILL IMPACTS Current Proposed Change %-Change Average Current Proposed Change %-Change Annual Current Proposed Change %-Change Class of Rate Rate Rate Rate Rate January Customer January January January January Therms/ Customer Monthly Monthly Monthly Monthly Service Schedule per Therm per Therm per Therm per Therm Therms Charge Bill Bill Bill Bill Month Charge Bill Bill Bill Bill Residential Avista 410 $ $ % 114 $5.00 $ $ $ % 53 $5.00 $62.61 $76.30 $ % Cascade 101 $ $ % 131 $3.00 $ $ $ % 63 $3.00 $64.71 $73.45 $ % NW Natural 2 $ $ % 122 $6.00 $ $ $ % 59 $6.00 $71.36 $82.21 $ % Commercial Avista 420 $ $ % Cascade 104 $ $ % NW Natural 3 $ $ % Industrial Avista 424 $ $ % Cascade 105 $ $ % NW Natural 31 $ $ % Interruptible Avista 440 $ $ % Cascade 170 $ $ % NW Natural 32 $ $ % Attachment B

15 2005/06 Proposed Oregon Residential Rates Avista Utilities Residential rate At 65 therms + $5 service charge Cascade Natural Residential rate At 65 therms + $3 service charge NW Natural Residential rate At 65 therms + $6 service charge $ $ $ $ $ $ $0.00 $0.20 $0.40 $0.60 $0.80 $1.00 $1.20 $1.40 $1.60 Attachment C

NATURAL GAS PRICE VOLATILITY

NATURAL GAS PRICE VOLATILITY I. Summary This brief white paper on natural gas prices is intended to discuss the potential for natural gas prices to be very volatile during the winter of 2003-04. Prices

NATURAL GAS PRICE VOLATILITY I. Summary This brief white paper on natural gas prices is intended to discuss the potential for natural gas prices to be very volatile during the winter of 2003-04. Prices

Natural Gas: Winter 2012-13 Abundance! and Some Confusion

Natural Gas: Winter 2012-13 Abundance! and Some Confusion NASEO Winter Fuels Outlook Washington, D.C. October 10, 2012 Bruce B. Henning Vice President, Energy Regulatory and Market Analysis BHenning@icfi.com

Natural Gas: Winter 2012-13 Abundance! and Some Confusion NASEO Winter Fuels Outlook Washington, D.C. October 10, 2012 Bruce B. Henning Vice President, Energy Regulatory and Market Analysis BHenning@icfi.com

Understanding. Natural Gas Markets

Understanding Natural Gas Markets Table of Contents Overview 1 The North American Natural Gas Marketplace 3 Understanding Natural Gas Markets Natural Gas Demand 9 Natural Gas Supply 12 Summary 25 Glossary

Understanding Natural Gas Markets Table of Contents Overview 1 The North American Natural Gas Marketplace 3 Understanding Natural Gas Markets Natural Gas Demand 9 Natural Gas Supply 12 Summary 25 Glossary

NATURAL GAS PRICES TO REMAIN AT HIGHER LEVELS

I. Summary NATURAL GAS PRICES TO REMAIN AT HIGHER LEVELS This brief white paper on natural gas prices is intended to discuss the continued and sustained level of natural gas prices at overall higher levels.

I. Summary NATURAL GAS PRICES TO REMAIN AT HIGHER LEVELS This brief white paper on natural gas prices is intended to discuss the continued and sustained level of natural gas prices at overall higher levels.

Regulators Reconsider Utility Hedging Policies Given Shifts In Natural Gas Flow

RESEARCH North America Fossil Fuels Natural Gas Regulators Reconsider Utility Hedging Policies Given Shifts In Natural Gas Flow Utilities Prioritize Price Stability Over Cost Reduction In Fuel Procurement

RESEARCH North America Fossil Fuels Natural Gas Regulators Reconsider Utility Hedging Policies Given Shifts In Natural Gas Flow Utilities Prioritize Price Stability Over Cost Reduction In Fuel Procurement

Relationship Between Natural Gas. Distribution Companies

Relationship Between Natural Gas Supply, Transportation and Distribution Companies Cynthia H. McCarran Chief, Gas Policy and Supply/Office of Electric, Gas and Water New York State Department of Public

Relationship Between Natural Gas Supply, Transportation and Distribution Companies Cynthia H. McCarran Chief, Gas Policy and Supply/Office of Electric, Gas and Water New York State Department of Public

And Then There Was Abundance: Examining Natural Gas in 2012. Bruce McDowell Director, Policy Analysis American Gas Association bmcdowell@aga.

And Then There Was Abundance: Examining Natural Gas in 2012 Bruce McDowell Director, Policy Analysis American Gas Association bmcdowell@aga.org NOTICE: In issuing and making this presentation and publication

And Then There Was Abundance: Examining Natural Gas in 2012 Bruce McDowell Director, Policy Analysis American Gas Association bmcdowell@aga.org NOTICE: In issuing and making this presentation and publication

High Prices Show Stresses in New England Natural Gas Delivery System

February 7, 2014 High Prices Show Stresses in New England Natural Gas Delivery System Abstract. Since 2012, limited supply from the Canaport and Everett liquefied natural gas (LNG) terminals coupled with

February 7, 2014 High Prices Show Stresses in New England Natural Gas Delivery System Abstract. Since 2012, limited supply from the Canaport and Everett liquefied natural gas (LNG) terminals coupled with

Natural Gas Markets in 2006

Order Code RL33714 Natural Gas Markets in 2006 Updated December 12, 2006 Robert Pirog Specialist in Energy Economics and Policy Resources, Science, and Industry Division Natural Gas Markets in 2006 Summary

Order Code RL33714 Natural Gas Markets in 2006 Updated December 12, 2006 Robert Pirog Specialist in Energy Economics and Policy Resources, Science, and Industry Division Natural Gas Markets in 2006 Summary

Led by growth in Texas, the Southeast, and Northeast, power burn is headed for a January record

EIA - Natural Gas Weekly Update for week ending January 28, 2015 Release Date: January 29, 2015 Next Release: February 5, 2015 In the News: Led by growth in Texas, the Southeast, and Northeast, power burn

EIA - Natural Gas Weekly Update for week ending January 28, 2015 Release Date: January 29, 2015 Next Release: February 5, 2015 In the News: Led by growth in Texas, the Southeast, and Northeast, power burn

Natural Gas Year-In-Review 2006

Natural Gas Year-In-Review 2 This report provides an overview of the natural gas industry and markets in 2 with special focus on the first complete set of supply and disposition data for 2 from the Energy

Natural Gas Year-In-Review 2 This report provides an overview of the natural gas industry and markets in 2 with special focus on the first complete set of supply and disposition data for 2 from the Energy

Creating more Value out of Storage

Creating more Value out of Storage By Gary Howorth, Founder Energy-Redefined Introduction Gas Storage is a complicated business which carries with it large risks and potentially low rewards. Assets can

Creating more Value out of Storage By Gary Howorth, Founder Energy-Redefined Introduction Gas Storage is a complicated business which carries with it large risks and potentially low rewards. Assets can

LONG-TERM ASSESSMENT OF NATURAL GAS INFRASTRUCTURE TO SERVE ELECTRIC GENERATION NEEDS WITHIN ERCOT

LONG-TERM ASSESSMENT OF NATURAL GAS INFRASTRUCTURE TO SERVE ELECTRIC GENERATION NEEDS WITHIN ERCOT Prepared for The Electric Reliability Council of Texas JUNE 2013 Black & Veatch Holding Company 2011.

LONG-TERM ASSESSMENT OF NATURAL GAS INFRASTRUCTURE TO SERVE ELECTRIC GENERATION NEEDS WITHIN ERCOT Prepared for The Electric Reliability Council of Texas JUNE 2013 Black & Veatch Holding Company 2011.

LNG Poised to Significantly Increase its Share of Global Gas Market David Wood February 2004 Petroleum Review p.38-39

LNG Poised to Significantly Increase its Share of Global Gas Market David Wood February 2004 Petroleum Review p.38-39 For the past few years LNG has experienced high levels of activity and investment in

LNG Poised to Significantly Increase its Share of Global Gas Market David Wood February 2004 Petroleum Review p.38-39 For the past few years LNG has experienced high levels of activity and investment in

An Analysis of Spot and Futures Prices for Natural Gas: The Roles of Economic Fundamentals, Market Structure, Speculation, and Manipulation

An Analysis of Spot and Futures Prices for Natural Gas: The Roles of Economic Fundamentals, Market Structure, Speculation, and Manipulation Robert J. Shapiro and Nam D. Pham August 2006 S O N E C O N An

An Analysis of Spot and Futures Prices for Natural Gas: The Roles of Economic Fundamentals, Market Structure, Speculation, and Manipulation Robert J. Shapiro and Nam D. Pham August 2006 S O N E C O N An

OCTOBER 20, 2005 WASHINGTON, D.C.

REMARKS FOR WILLIAM M. FLYNN CHAIRMAN NEW YORK STATE PUBLIC SERVICE COMMISSION PRESENTATION TO: FEDERAL ENERGY REGULATORY COMMISSION OPEN MEETING OCTOBER 20, 2005 WASHINGTON, D.C. Good morning, Chairman

REMARKS FOR WILLIAM M. FLYNN CHAIRMAN NEW YORK STATE PUBLIC SERVICE COMMISSION PRESENTATION TO: FEDERAL ENERGY REGULATORY COMMISSION OPEN MEETING OCTOBER 20, 2005 WASHINGTON, D.C. Good morning, Chairman

investigating where the oil industry puts it money, then find programs that emulate that, i.e. follow the money.

WHY SHOULD FINANCIAL PLANNERS CONSIDER DIRECT OIL & GAS INVESTMENT PROGRAMS FOR THEIR CLIENTS? BY Martin J. Cohen, Cfp tm And Steven King, President Petroinvest Llc Should asset allocation in direct participation

WHY SHOULD FINANCIAL PLANNERS CONSIDER DIRECT OIL & GAS INVESTMENT PROGRAMS FOR THEIR CLIENTS? BY Martin J. Cohen, Cfp tm And Steven King, President Petroinvest Llc Should asset allocation in direct participation

Winter 2013-14 Energy Market Assessment Report to the Commission

Winter 2013-14 Energy Market Assessment Report to the Commission Docket No. AD06-3-000 October 2013 Disclaimer: The matters presented in this staff report do not necessarily represent the views of the

Winter 2013-14 Energy Market Assessment Report to the Commission Docket No. AD06-3-000 October 2013 Disclaimer: The matters presented in this staff report do not necessarily represent the views of the

Hedging Natural Gas Prices

Hedging Natural Gas Prices Luke Miller Assistant Professor of Finance Office of Economic Analysis & Business Research School of Business Administration Fort Lewis College Natural Gas Industry U.S. natural

Hedging Natural Gas Prices Luke Miller Assistant Professor of Finance Office of Economic Analysis & Business Research School of Business Administration Fort Lewis College Natural Gas Industry U.S. natural

Natural Gas Markets Update for the Ethanol Industry. Identifying Market Fundamentals and Managing Price Risk

Natural Gas Markets Update for the Ethanol Industry Identifying Market Fundamentals and Managing Price Risk Presentation Outline Natural Gas Market Update Demand Issues Supply Issues Implications for Ethanol

Natural Gas Markets Update for the Ethanol Industry Identifying Market Fundamentals and Managing Price Risk Presentation Outline Natural Gas Market Update Demand Issues Supply Issues Implications for Ethanol

Energy Ventures Analysis 1901 N. Moore St. Arlington, VA 22209 (703) 276 8900

276 8900") T H E I M P A C T O F E A R L Y C O A L R E T I R E M E N T S O N K E Y P O W E R M A R K E T S ISO = 46.6% Prepared for: National Mining Association Washington, DC Northwest = 41.3% MISO = 36.8% NYISO

T H E I M P A C T O F E A R L Y C O A L R E T I R E M E N T S O N K E Y P O W E R M A R K E T S ISO = 46.6% Prepared for: National Mining Association Washington, DC Northwest = 41.3% MISO = 36.8% NYISO

The Natural Gas-Electric Interface: Summary of Four Natural Gas-Electric Interdependency Assessments WIEB Staff November 30, 2012

Introduction. The Natural Gas-Electric Interface: Summary of Four Natural Gas-Electric Interdependency Assessments WIEB Staff November 30, 2012 The increased reliance on natural gas as the primary fuel

Introduction. The Natural Gas-Electric Interface: Summary of Four Natural Gas-Electric Interdependency Assessments WIEB Staff November 30, 2012 The increased reliance on natural gas as the primary fuel

Piedmont Natural Gas Company, Inc. Tennessee Index of Tariff & Service Regulations

Tennessee Index of Tariff & Service Regulations Rate Schedule 301 Rate Schedule 302 Rate Schedule 303 Rate Schedule 304 Rate Schedule 306 Rate Schedule 307 Rate Schedule 309 Rate Schedule 310 Rate Schedule

Tennessee Index of Tariff & Service Regulations Rate Schedule 301 Rate Schedule 302 Rate Schedule 303 Rate Schedule 304 Rate Schedule 306 Rate Schedule 307 Rate Schedule 309 Rate Schedule 310 Rate Schedule

Indiana Utility Regulatory Commission. Natural Gas Forum October 16, 2007

Indiana Utility Regulatory Commission Natural Gas Forum October 16, 2007 1 Today s Objectives Gas Supply Natural Gas Issues Energy efficiency Usage reduction continues Emerging Issues Forecast for Winter

Indiana Utility Regulatory Commission Natural Gas Forum October 16, 2007 1 Today s Objectives Gas Supply Natural Gas Issues Energy efficiency Usage reduction continues Emerging Issues Forecast for Winter

Note No. 141 April 1998. The United States enjoys a highly competitive natural gas market and an increasingly efficient

Privatesector P U B L I C P O L I C Y F O R T H E Note No. 141 April 1998 Development of Competitive Natural Gas Markets in the United States Andrej Juris The United States enjoys a highly competitive

Privatesector P U B L I C P O L I C Y F O R T H E Note No. 141 April 1998 Development of Competitive Natural Gas Markets in the United States Andrej Juris The United States enjoys a highly competitive

WP-07 Power Rate Case Workshop

WP-07 Power Rate Case Workshop Date of Workshop: Topic(s): , Overview Results BPA price forecast and comparison with other forecasts Assumptions Supply and demand fundamentals for the short / medium /

WP-07 Power Rate Case Workshop Date of Workshop: Topic(s): , Overview Results BPA price forecast and comparison with other forecasts Assumptions Supply and demand fundamentals for the short / medium /

Natural Gas Pipeline and Storage Infrastructure Projections Through 2030

Natural Gas Pipeline and Storage Infrastructure Projections Through 2030 October 20, 2009 Submitted to: The INGAA Foundation, Inc. 10 G Street NE Suite 700 Washington, DC 20002 Submitted by: ICF International

Natural Gas Pipeline and Storage Infrastructure Projections Through 2030 October 20, 2009 Submitted to: The INGAA Foundation, Inc. 10 G Street NE Suite 700 Washington, DC 20002 Submitted by: ICF International

2009 Avista Natural Gas IRP

2009 Avista Natural Gas IRP Technical Advisory Committee Meeting May 19, 2009 Portland, Oregon Agenda Introductions & Logistics Avista s IRP Process Demand Forecast Follow Up Supply and Infrastructure

2009 Avista Natural Gas IRP Technical Advisory Committee Meeting May 19, 2009 Portland, Oregon Agenda Introductions & Logistics Avista s IRP Process Demand Forecast Follow Up Supply and Infrastructure

CRS Report for Congress

Order Code RL33124 CRS Report for Congress Received through the CRS Web Oil and Gas Disruption From Hurricanes Katrina and Rita October 21, 2005 Lawrence Kumins and Robert Bamberger Specialists in Energy

Order Code RL33124 CRS Report for Congress Received through the CRS Web Oil and Gas Disruption From Hurricanes Katrina and Rita October 21, 2005 Lawrence Kumins and Robert Bamberger Specialists in Energy

GAO NATURAL GAS. Analysis of Changes in Market Price. Report to Congressional Committees and Members of Congress

GAO United States General Accounting Office Report to Congressional Committees and Members of Congress December 2002 NATURAL GAS Analysis of Changes in Market Price GAO-03-46 December 2002 NATURAL GAS

GAO United States General Accounting Office Report to Congressional Committees and Members of Congress December 2002 NATURAL GAS Analysis of Changes in Market Price GAO-03-46 December 2002 NATURAL GAS

Modeling the US Natural Gas Network

Modeling the US Natural Gas Network James Ellison Sandia National Laboratories, Critical Infrastructure Modeling and Simulation Group Abstract In order to better understand how the US natural gas network

Modeling the US Natural Gas Network James Ellison Sandia National Laboratories, Critical Infrastructure Modeling and Simulation Group Abstract In order to better understand how the US natural gas network

Trading Periods 3 Period Time 600 Seconds (10 minutes) Calendar Time per Period Compounding Interval 1 Day (30 seconds)

Calendar Time per Period Compounding Interval 1 Day (30 seconds)") RIT Case Brief COM2 Commodities 2 By Kevin Mak and Tom McCurdy The purpose of this case is to challenge traders ability to respond to the highly dynamic world of commodities trading. In this case, traders

RIT Case Brief COM2 Commodities 2 By Kevin Mak and Tom McCurdy The purpose of this case is to challenge traders ability to respond to the highly dynamic world of commodities trading. In this case, traders

Daniel Smith/Corbis 32

32 Daniel Smith/Corbis MONEY for NOTHING The Case for Eliminating US Fossil Fuel Subsidies Special tax provisions subsidize US oil, gas, and coal companies to the tune of $4.9 billion a year but have little

32 Daniel Smith/Corbis MONEY for NOTHING The Case for Eliminating US Fossil Fuel Subsidies Special tax provisions subsidize US oil, gas, and coal companies to the tune of $4.9 billion a year but have little

Role of Energy Efficiency in Rebalancing Natural Gas Markets

Role of Energy Efficiency in Rebalancing Natural Gas Markets R. Neal Elliott, Ph.D., P.E. Industrial Program Director ACEEE Washington, D.C. July 26, 2005 The American Council for an Energy Efficient Economy

Role of Energy Efficiency in Rebalancing Natural Gas Markets R. Neal Elliott, Ph.D., P.E. Industrial Program Director ACEEE Washington, D.C. July 26, 2005 The American Council for an Energy Efficient Economy

A Look at Western Natural Gas Infrastructure During the Recent El Paso Pipeline Disruption

A Look at Western Natural Gas Infrastructure During the Recent El Paso Pipeline Disruption This analysis examines the impact of the August 2000 El Paso Natural Gas Pipeline system disruption upon the ability

A Look at Western Natural Gas Infrastructure During the Recent El Paso Pipeline Disruption This analysis examines the impact of the August 2000 El Paso Natural Gas Pipeline system disruption upon the ability

An Introduction to Natural Gas

An Introduction to Natural Gas NYMEX settlement prices since 1995 $12.00 $10.00 $ / MMBTU $8.00 $6.00 $4.00 $2.00 $0.00 95'Jan Jul 96'Jan Jul 97'Jan Jul 98'Jan Jul 99'Jan Jul 00'Jan Jul 01'Jan Jul 02'Jan

An Introduction to Natural Gas NYMEX settlement prices since 1995 $12.00 $10.00 $ / MMBTU $8.00 $6.00 $4.00 $2.00 $0.00 95'Jan Jul 96'Jan Jul 97'Jan Jul 98'Jan Jul 99'Jan Jul 00'Jan Jul 01'Jan Jul 02'Jan

NWN OPUC Advice No. 15-11 / UG (UM 1635 / UG 221)

") ONITA R. KING Rates & Regulatory Affairs Tel: 503.721.2452 Fax: 503.721.2516 Email: ork@nwnatural.com July 31, 2015 NWN OPUC Advice No. 15-11 / UG (UM 1635 / UG 221) VIA ELECTRONIC FILING Public Utility

ONITA R. KING Rates & Regulatory Affairs Tel: 503.721.2452 Fax: 503.721.2516 Email: ork@nwnatural.com July 31, 2015 NWN OPUC Advice No. 15-11 / UG (UM 1635 / UG 221) VIA ELECTRONIC FILING Public Utility

State Heating Oil & Propane Program Final Report Winter 2004/2005

Commonwealth of Massachusetts Division of Energy Resources State Heating Oil & Propane Program Final Report Winter 2004/2005 May 2005 Mitt Romney Governor Kerry Healey Lt. Governor Beth Lindstrom Director,

Commonwealth of Massachusetts Division of Energy Resources State Heating Oil & Propane Program Final Report Winter 2004/2005 May 2005 Mitt Romney Governor Kerry Healey Lt. Governor Beth Lindstrom Director,

While there has been a lot of discussion

Pipelines Is North American Natural Gas Infrastructure Up to Complementing Wind, Solar? Donald F. Santa Jr. While there has been a lot of discussion within the electric power industry about integrating

Pipelines Is North American Natural Gas Infrastructure Up to Complementing Wind, Solar? Donald F. Santa Jr. While there has been a lot of discussion within the electric power industry about integrating

Natural Gas Contracts in New York State

Natural Gas Contracts in New York State Thomas G. Dvorsky Director, Office of Gas and Water New York State Department of Public Service Thomas_Dvorsky@dps.state.ny.us June 2007 LDC Gas Supply Portfolios

Natural Gas Contracts in New York State Thomas G. Dvorsky Director, Office of Gas and Water New York State Department of Public Service Thomas_Dvorsky@dps.state.ny.us June 2007 LDC Gas Supply Portfolios

Gas storage industry primer

Gas storage industry primer Gas storage industry primer General Underground natural gas storage facilities are a vital and complementary component of the North American natural gas transmission and distribution

Gas storage industry primer Gas storage industry primer General Underground natural gas storage facilities are a vital and complementary component of the North American natural gas transmission and distribution

One important issue in the debate about expediting the U.S. Department of Energy s LNG permitting

ACCF CENTER FOR POLICY RESEARCH SPECIAL REPORT NOVEMBER 2013 LNG EXPORTS: HOW MUCH WILL THEY IMPACT U.S. NATURAL GAS PRICES? BY MARGO THORNING, PH.D. SENIOR VICE PRESIDENT AND CHIEF ECONOMIST AMERICAN

ACCF CENTER FOR POLICY RESEARCH SPECIAL REPORT NOVEMBER 2013 LNG EXPORTS: HOW MUCH WILL THEY IMPACT U.S. NATURAL GAS PRICES? BY MARGO THORNING, PH.D. SENIOR VICE PRESIDENT AND CHIEF ECONOMIST AMERICAN

COAL MARKET FREQUENTLY ASKED QUESTIONS

COAL MARKET FREQUENTLY ASKED QUESTIONS Over the course of the past decade, numerous issues have arisen in the U.S. coal trading arena. Bankruptcies, standardized trading contracts, and liquidity are a

COAL MARKET FREQUENTLY ASKED QUESTIONS Over the course of the past decade, numerous issues have arisen in the U.S. coal trading arena. Bankruptcies, standardized trading contracts, and liquidity are a

Spectra Energy Reports First Quarter 2012 Results

Media: Analysts: Wendy Olson (713) 627-4072 (713) 627-4747 (24-hour media line) John Arensdorf (713) 627-4600 Date: May 4, 2012 Spectra Energy Reports First Quarter 2012 Results Reported net income from

Media: Analysts: Wendy Olson (713) 627-4072 (713) 627-4747 (24-hour media line) John Arensdorf (713) 627-4600 Date: May 4, 2012 Spectra Energy Reports First Quarter 2012 Results Reported net income from

Physical Natural Gas

Risk Management 101 Physical Natural Gas Gas Measurement Mcf Thousand cubic feet Volumetric measurement MMBtu Million British Thermal Units Heating value measurement of gas based on a standard heat value

Risk Management 101 Physical Natural Gas Gas Measurement Mcf Thousand cubic feet Volumetric measurement MMBtu Million British Thermal Units Heating value measurement of gas based on a standard heat value

Assessing Natural Gas Supply

Competitive Energy Services, LLC [Insert date] Competitive Energy Services Assessing Natural Gas Supply February 7, 2014 Assessing Natural Gas Supply Options for New England and their Impacts on Natural

Competitive Energy Services, LLC [Insert date] Competitive Energy Services Assessing Natural Gas Supply February 7, 2014 Assessing Natural Gas Supply Options for New England and their Impacts on Natural

(713) 627-5353 (713) 627-4747 (24-hour media line) (713) 627-4600. Date: May 3, 2013

627-5353 (713) 627-4747 (24-hour media line) (713) 627-4600. Date: May 3, 2013") Media: Analysts: Caitlin Currie (713) 627-5353 (713) 627-4747 (24-hour media line) John Arensdorf (713) 627-4600 Date: May 3, 2013 Spectra Energy Reports First Quarter 2013 Results Reported net income

Media: Analysts: Caitlin Currie (713) 627-5353 (713) 627-4747 (24-hour media line) John Arensdorf (713) 627-4600 Date: May 3, 2013 Spectra Energy Reports First Quarter 2013 Results Reported net income

Note No. 137 March 1998. Countries in Asia, Europe, and North and South America are introducing reforms to boost

Privatesector P U B L I C P O L I C Y F O R T H E Note No. 137 March 1998 Competition in the Natural Gas Industry The emergence of spot, financial, and pipeline capacity markets Andrej Juris Countries

Privatesector P U B L I C P O L I C Y F O R T H E Note No. 137 March 1998 Competition in the Natural Gas Industry The emergence of spot, financial, and pipeline capacity markets Andrej Juris Countries

The Impact of Fuel Costs on Electric Power Prices

The Impact of Fuel Costs on Electric Power Prices by Kenneth Rose 1 June 2007 1 Kenneth Rose is an independent consultant and a Senior Fellow with the Institute of Public Utilities (IPU) at Michigan State

The Impact of Fuel Costs on Electric Power Prices by Kenneth Rose 1 June 2007 1 Kenneth Rose is an independent consultant and a Senior Fellow with the Institute of Public Utilities (IPU) at Michigan State

The New Normal of Moderate Gas Prices: Challenges and Options for Gas Energy Efficiency Program Administrators

The New Normal of Moderate Gas Prices: Challenges and Options for Gas Energy Efficiency Program Administrators September 23, 2013 Ian M. Hoffman Electricity Markets and Policy Group Lawrence Berkeley National

The New Normal of Moderate Gas Prices: Challenges and Options for Gas Energy Efficiency Program Administrators September 23, 2013 Ian M. Hoffman Electricity Markets and Policy Group Lawrence Berkeley National

Natural Gas Assessment New York State Energy Plan 2009. December 2009

New York State Energy Plan 2009 December 2009 1 Overview This Assessment describes the workings of the natural gas market in New York and the northeast region, discusses current use and projected need

New York State Energy Plan 2009 December 2009 1 Overview This Assessment describes the workings of the natural gas market in New York and the northeast region, discusses current use and projected need

Agenda. Petroleum Management

Petroleum Management 1 Agenda Energy Advantage Background - Petroleum Fuels Market Petroleum Procurement Services Background - Hedging/Risk Management Canadian Petroleum Market Correlation and basis differential

Petroleum Management 1 Agenda Energy Advantage Background - Petroleum Fuels Market Petroleum Procurement Services Background - Hedging/Risk Management Canadian Petroleum Market Correlation and basis differential

Displacement of Coal with Natural Gas to Generate Electricity

Displacement of Coal with Natural Gas to Generate Electricity The American Coalition for Clean Coal Electricity (ACCCE) supports a balanced energy strategy that will ensure affordable and reliable energy,

Displacement of Coal with Natural Gas to Generate Electricity The American Coalition for Clean Coal Electricity (ACCCE) supports a balanced energy strategy that will ensure affordable and reliable energy,

Executive Summary 2003 NATURAL GAS INTEGRATED RESOURCE PLAN

Executive Summary 2003 NATURAL GAS INTEGRATED RESOURCE PLAN i TABLE OF CONTENTS The Company...iii Avista Utilities and The Regions Served...iii Integrated Resource Planning...iv Natural Gas Forecast...

Executive Summary 2003 NATURAL GAS INTEGRATED RESOURCE PLAN i TABLE OF CONTENTS The Company...iii Avista Utilities and The Regions Served...iii Integrated Resource Planning...iv Natural Gas Forecast...

COST RECOVERY MECHANISMS FOR PUBLIC UTILITIES IN NEW YORK STATE

COST RECOVERY MECHANISMS FOR PUBLIC UTILITIES IN NEW YORK STATE Staff Subcommittee on Gas, NARUC Annual Convention, Chicago, Illinois Sunday, November 15, 2009 Thomas G. Dvorsky New York State Public Service

COST RECOVERY MECHANISMS FOR PUBLIC UTILITIES IN NEW YORK STATE Staff Subcommittee on Gas, NARUC Annual Convention, Chicago, Illinois Sunday, November 15, 2009 Thomas G. Dvorsky New York State Public Service

Understanding California s Electricity Prices Updated April 2011

White Paper Understanding California s Electricity Prices Updated April 2011 Executive Summary Most industry experts conclude that average electricity prices throughout the U.S. will increase significantly

White Paper Understanding California s Electricity Prices Updated April 2011 Executive Summary Most industry experts conclude that average electricity prices throughout the U.S. will increase significantly

Financial News for Major Energy Companies Second Quarter 2005

Financial News for Major Energy Companies Second Quarter 2005 The "Financial News for Major Energy Companies" is issued quarterly to report recent trends in the financial performance of the major energy

Financial News for Major Energy Companies Second Quarter 2005 The "Financial News for Major Energy Companies" is issued quarterly to report recent trends in the financial performance of the major energy

An Assessment of Prices of Natural Gas Futures Contracts As A Predictor of Realized Spot Prices at the Henry Hub

An Assessment of Prices of Natural Gas Futures Contracts As A Predictor of Realized Spot Prices at the Henry Hub This article compares realized Henry Hub spot market prices for natural gas during the three

An Assessment of Prices of Natural Gas Futures Contracts As A Predictor of Realized Spot Prices at the Henry Hub This article compares realized Henry Hub spot market prices for natural gas during the three

On October 21, 2008, the Federal Reserve

Anticipated Recession Effects Gas Prices Natural Gas Prices in a Recession This is a preprint of an article published in Natural Gas & Electricity 2008, Dec., Wiley Periodicals, Inc. http://www3.interscience.wiley.com/cgi-bin/jhome/105559587

Anticipated Recession Effects Gas Prices Natural Gas Prices in a Recession This is a preprint of an article published in Natural Gas & Electricity 2008, Dec., Wiley Periodicals, Inc. http://www3.interscience.wiley.com/cgi-bin/jhome/105559587

NOIA s mission is to secure reliable access to the nation s valuable. and supplied in an environmentally responsible manner.

Energy Challenges for wisconsin and the NATion NOIA s mission is to secure reliable access to the nation s valuable offshore energy resources in order that they may be developed, produced and supplied

Energy Challenges for wisconsin and the NATion NOIA s mission is to secure reliable access to the nation s valuable offshore energy resources in order that they may be developed, produced and supplied

North American Natural Gas Midstream Infrastructure Through 2035: A Secure Energy Future

North American Natural Gas Midstream Infrastructure Through 2035: A Secure Energy Future Updated Supply Demand Outlook Background Executive Summary June 28, 2011 Sufficient midstream natural gas infrastructure,

North American Natural Gas Midstream Infrastructure Through 2035: A Secure Energy Future Updated Supply Demand Outlook Background Executive Summary June 28, 2011 Sufficient midstream natural gas infrastructure,

10 Myths and Realities of Natural Gas and Electricity Purchasing

6 Strategic Planning for Energy and the Environment 10 Myths and Realities of Natural Gas and Electricity Purchasing Craig Schultz, President Energy Buying Strategies, Inc. ABSTRACT In deregulated natural

6 Strategic Planning for Energy and the Environment 10 Myths and Realities of Natural Gas and Electricity Purchasing Craig Schultz, President Energy Buying Strategies, Inc. ABSTRACT In deregulated natural

Note No. 138 March 1998. Natural Gas Markets in the U.K.

Privatesector P U B L I C P O L I C Y F O R T H E Note No. 138 March 1998 Competition, industry structure, and market power of the incumbent Andrej Juris The deregulation of the U.K. natural gas industry

Privatesector P U B L I C P O L I C Y F O R T H E Note No. 138 March 1998 Competition, industry structure, and market power of the incumbent Andrej Juris The deregulation of the U.K. natural gas industry

Energy Efficiency s Role in Getting America Out of Its Energy Straightjacket

Energy Efficiency s Role in Getting America Out of Its Energy Straightjacket R. Neal Elliott, Ph.D., P.E. Industrial Program Director ACEEE Jan-06 Industrial Energy Prices 17.00 15.00 13.00 11.00 9.00

Energy Efficiency s Role in Getting America Out of Its Energy Straightjacket R. Neal Elliott, Ph.D., P.E. Industrial Program Director ACEEE Jan-06 Industrial Energy Prices 17.00 15.00 13.00 11.00 9.00

PROJECT EXPERIENCE Development/Transaction Support United States MANAGING DIRECTOR

Peter Abt Mr. Abt is a Managing Director in Black & Veatch s Management Consulting Division. He leads the division s Oil & Gas Strategy practice and holds primary responsibility for client management and

Peter Abt Mr. Abt is a Managing Director in Black & Veatch s Management Consulting Division. He leads the division s Oil & Gas Strategy practice and holds primary responsibility for client management and

(c) 2006-2014 Gary R. Evans. May be used for non-profit educational purposes only without permission of the author.

2006-2014 Gary R. Evans. May be used for non-profit educational purposes only without permission of the author.") The futures markets Introduction and Mechanics, using Natural Gas as the example (c) 2006-2014 Gary R. Evans. May be used for non-profit educational purposes only without permission of the author. Forward

The futures markets Introduction and Mechanics, using Natural Gas as the example (c) 2006-2014 Gary R. Evans. May be used for non-profit educational purposes only without permission of the author. Forward

Financial News for Major Energy Companies Third Quarter 2005

Financial News for Major Energy Companies Third Quarter 2005 The "Financial News for Major Energy Companies" is issued quarterly to report recent trends in the financial performance of the major energy

Financial News for Major Energy Companies Third Quarter 2005 The "Financial News for Major Energy Companies" is issued quarterly to report recent trends in the financial performance of the major energy

STEO Supplement: Why are oil prices so high?

STEO Supplement: Why are oil prices so high? During most of the 1990s, the West Texas Intermediate (WTI) crude oil price averaged close to $20 per barrel, before plunging to almost $10 per barrel in late

STEO Supplement: Why are oil prices so high? During most of the 1990s, the West Texas Intermediate (WTI) crude oil price averaged close to $20 per barrel, before plunging to almost $10 per barrel in late

GAO. NATURAL GAS Factors Affecting Prices and Potential Impacts on Consumers

GAO For Release on Delivery Expected at 8:30 a.m. CST Monday, February 13, 2006 United States Government Accountability Office Testimony Before the Permanent Subcommittee on Investigations, Committee on

GAO For Release on Delivery Expected at 8:30 a.m. CST Monday, February 13, 2006 United States Government Accountability Office Testimony Before the Permanent Subcommittee on Investigations, Committee on

Spectra Energy Reports Fourth Quarter and Year-End 2011 Results

Media: Analysts: Wendy Olson (713) 627-4072 (713) 627-4747 (24-hour media line) John Arensdorf (713) 627-4600 Date: February 2, 2012 Spectra Energy Reports Fourth Quarter and Year-End 2011 Results Company

Media: Analysts: Wendy Olson (713) 627-4072 (713) 627-4747 (24-hour media line) John Arensdorf (713) 627-4600 Date: February 2, 2012 Spectra Energy Reports Fourth Quarter and Year-End 2011 Results Company

The current decoupling of oil and gas prices, where prices of the two commodities move in different directions, negatively affects Gazprom s export

The current decoupling of oil and gas prices, where prices of the two commodities move in different directions, negatively affects Gazprom s export sales by driving up oil-indexed gas prices and leading

The current decoupling of oil and gas prices, where prices of the two commodities move in different directions, negatively affects Gazprom s export sales by driving up oil-indexed gas prices and leading

Natural Gas Wholesale Prices at PG&E Citygate as of November 7, 2006

QUARTERLY GAS ISSUES UPDATE December 26 I. Supply Issues Wholesale Natural Gas Prices Above normal temperatures and a lack of hurricane activity caused market prices to decrease in October. By November,

QUARTERLY GAS ISSUES UPDATE December 26 I. Supply Issues Wholesale Natural Gas Prices Above normal temperatures and a lack of hurricane activity caused market prices to decrease in October. By November,

Electricity Analysis Office Electricity Supply and Analysis Division California Energy Commission

NATURAL GAS PRICE VOLATILITY Randy Roesser Electricity Analysis Office Electricity Supply and Analysis Division California Energy Commission Presented at: California Energy Commission Sacramento, CA June

NATURAL GAS PRICE VOLATILITY Randy Roesser Electricity Analysis Office Electricity Supply and Analysis Division California Energy Commission Presented at: California Energy Commission Sacramento, CA June

CHAPTER 3: NATURAL GAS IN MONTANA: CURRENT TRENDS, FORECASTS AND THE CONNECTION WITH ELECTRIC GENERATION

CHAPTER 3: NATURAL GAS IN MONTANA: CURRENT TRENDS, FORECASTS AND THE CONNECTION WITH ELECTRIC GENERATION Many of the electricity generation plants proposed for Montana are planning to use natural gas.

CHAPTER 3: NATURAL GAS IN MONTANA: CURRENT TRENDS, FORECASTS AND THE CONNECTION WITH ELECTRIC GENERATION Many of the electricity generation plants proposed for Montana are planning to use natural gas.

WEST TEXAS GAS, INC. Rate Book #3 Page No. 1 211 N. COLORADO MIDLAND, TEXAS 79701-4696

WEST TEXAS GAS, INC. Rate Book #3 Page No. 1 211 N. COLORADO Canceling: Rate Book #2 Sheet No. Page No. 1A STANDARD RATE SCHEDULE SCHEDULE NO. 600 RESIDENTIAL SERVICE Applies to OKLAHOMA APPLICABILITY

WEST TEXAS GAS, INC. Rate Book #3 Page No. 1 211 N. COLORADO Canceling: Rate Book #2 Sheet No. Page No. 1A STANDARD RATE SCHEDULE SCHEDULE NO. 600 RESIDENTIAL SERVICE Applies to OKLAHOMA APPLICABILITY

Oil and Gas Price Forecast Update: Where are Oil and Gas Prices Heading?

RESERVOIR ENGINEERING SOFTWARE & SERVICES Oil and Gas Price Forecast Update: Where are Oil and Gas Prices Heading? Dale Struksnes, Manager - Reserve Evaluations April 13, 2010 Media Commentary on Oil and

RESERVOIR ENGINEERING SOFTWARE & SERVICES Oil and Gas Price Forecast Update: Where are Oil and Gas Prices Heading? Dale Struksnes, Manager - Reserve Evaluations April 13, 2010 Media Commentary on Oil and

Assessment of New York City Natural Gas Market Fundamentals and Life Cycle Fuel Emissions

Assessment of New York City Natural Gas Market Fundamentals and Life Cycle Fuel Emissions Prepared for: New York City Mayor s Office of Long-Term Planning and Sustainability Submitted by: ICF International

Assessment of New York City Natural Gas Market Fundamentals and Life Cycle Fuel Emissions Prepared for: New York City Mayor s Office of Long-Term Planning and Sustainability Submitted by: ICF International

Natural Gas and Electricity Coordination Experiences and Challenges

1 Natural Gas and Electricity Coordination Experiences and Challenges Challenges Facing the New England Power System Gordon van Welie, President and CEO, ISO New England 2015 IEEE Power & Energy Society

1 Natural Gas and Electricity Coordination Experiences and Challenges Challenges Facing the New England Power System Gordon van Welie, President and CEO, ISO New England 2015 IEEE Power & Energy Society

Michigan Residential Heating Oil and Propane Price Survey

Michigan Residential Heating Oil and Propane Price Survey 2013-2014 Heating Season This report summarizes the results of a survey of residential No. 2 distillate fuel oil (home heating oil) and propane

Michigan Residential Heating Oil and Propane Price Survey 2013-2014 Heating Season This report summarizes the results of a survey of residential No. 2 distillate fuel oil (home heating oil) and propane

RESIDENTIAL SERVICE RATE

Central Texas Service Area RATE SCHEDULE 10 APPLICABILITY RESIDENTIAL SERVICE RATE Applicable to a residential customer in a single dwelling, or in a dwelling unit of a multiple dwelling or residential

Central Texas Service Area RATE SCHEDULE 10 APPLICABILITY RESIDENTIAL SERVICE RATE Applicable to a residential customer in a single dwelling, or in a dwelling unit of a multiple dwelling or residential

NATion and north carolina

Energy Challenges for the NATion and north carolina NOIA s mission is to secure reliable access to the nation s valuable offshore energy resources in order that they may be developed, produced and supplied

Energy Challenges for the NATion and north carolina NOIA s mission is to secure reliable access to the nation s valuable offshore energy resources in order that they may be developed, produced and supplied

(c) 2006-2014 Gary R. Evans. May be used for non-profit educational purposes only without permission of the author.

2006-2014 Gary R. Evans. May be used for non-profit educational purposes only without permission of the author.") The futures markets Introduction and Mechanics (c) 2006-2014 Gary R. Evans. May be used for non-profit educational purposes only without permission of the author. Forward contracts... Forward contracts

The futures markets Introduction and Mechanics (c) 2006-2014 Gary R. Evans. May be used for non-profit educational purposes only without permission of the author. Forward contracts... Forward contracts

NATURAL GAS PRESENTATION

NATURAL GAS PRESENTATION Prepared for the Staff of the Delaware Public Service Commission Presented by Exeter Associates, Inc. HEDGING Despite the significant increases in gas from shale, the Henry Hub

NATURAL GAS PRESENTATION Prepared for the Staff of the Delaware Public Service Commission Presented by Exeter Associates, Inc. HEDGING Despite the significant increases in gas from shale, the Henry Hub

Short Term Energy Outlook Supplement: Constraints in New England likely to affect regional energy prices this winter

January 18, 2013 Short Term Energy Outlook Supplement: Constraints in New England likely to affect regional energy prices this winter Since November, New England has had the highest average spot natural

January 18, 2013 Short Term Energy Outlook Supplement: Constraints in New England likely to affect regional energy prices this winter Since November, New England has had the highest average spot natural

NERA Analysis of Energy Supplier Margins

7 December 2009 NERA Analysis of Energy Supplier Margins By Graham Shuttleworth Even though wholesale energy prices have fallen recently, gas and electricity suppliers are earning very little margin on

7 December 2009 NERA Analysis of Energy Supplier Margins By Graham Shuttleworth Even though wholesale energy prices have fallen recently, gas and electricity suppliers are earning very little margin on

Natural Gas Monthly. October 2015. Office of Oil, Gas, and Coal Supply Statistics www.eia.gov. U.S. Department of Energy Washington, DC 20585

Natural Gas Monthly October 2015 Office of Oil, Gas, and Coal Supply Statistics www.eia.gov U.S. Department of Energy Washington, DC 20585 This report was prepared by the U.S. Energy Information Administration

Natural Gas Monthly October 2015 Office of Oil, Gas, and Coal Supply Statistics www.eia.gov U.S. Department of Energy Washington, DC 20585 This report was prepared by the U.S. Energy Information Administration

Preparing for Changes in Market Design

Preparing for Changes in Market Design EMART Conference Didier Lebout, Strategy and Development Director Gazprom Marketing and Trading France Amsterdam, 21 November 2012 In this presentation GM&T Ltd:

Preparing for Changes in Market Design EMART Conference Didier Lebout, Strategy and Development Director Gazprom Marketing and Trading France Amsterdam, 21 November 2012 In this presentation GM&T Ltd:

Market Update. Natural Gas & Electricity. David Alicandri Vice President, Operations & Portfolio Management

Market Update Natural Gas & Electricity David Alicandri Vice President, Operations & Portfolio Management May 2015 Safe harbor statement Agenda Who We Are Natural Gas Market Update Electricity Update Questions

Market Update Natural Gas & Electricity David Alicandri Vice President, Operations & Portfolio Management May 2015 Safe harbor statement Agenda Who We Are Natural Gas Market Update Electricity Update Questions

Presentation to the State of Alaska Legislature. Liquid Natural Gas (LNG) NPV Analysis and Results

NPV Analysis and Results") Presentation to the State of Alaska Legislature Liquid Natural Gas (LNG) NPV Analysis and Results June 9, 2008 Key Conclusions LNG Projects Have Higher Capital Costs and Therefore Greater Risk than a Pipeline

Presentation to the State of Alaska Legislature Liquid Natural Gas (LNG) NPV Analysis and Results June 9, 2008 Key Conclusions LNG Projects Have Higher Capital Costs and Therefore Greater Risk than a Pipeline

Gulf Natural Gas Region

Gulf Gas Market: Overview and Focal Points Page 1 of 15 Gulf Natural Gas Region Colonial Gas Mainline TX NGPL TXOK Carthage LA Waha Tennessee Zone 0 Katy Freeport Cameron Sabine Pass Henry Texas Eastern

Gulf Gas Market: Overview and Focal Points Page 1 of 15 Gulf Natural Gas Region Colonial Gas Mainline TX NGPL TXOK Carthage LA Waha Tennessee Zone 0 Katy Freeport Cameron Sabine Pass Henry Texas Eastern

Web Meeting Summary NorthWestern Energy Electricity Technical Advisory Committee August 28, 2013

Web Meeting Summary NorthWestern Energy Electricity Technical Advisory Committee August 28, 2013 Attendance Those participating in the Energy Electricity Technical Advisory Committee (ETAC) meeting conducted

Web Meeting Summary NorthWestern Energy Electricity Technical Advisory Committee August 28, 2013 Attendance Those participating in the Energy Electricity Technical Advisory Committee (ETAC) meeting conducted

GENERAL INFORMATION - Continued. (General Information - Continued on Leaf No. 172)

") PSC NO: 9 GAS LEAF: 171 COMPANY: CONSOLIDATED EDISON COMPANY OF NEW YORK, INC. REVISION: 5 INITIAL EFFECTIVE DATE: 03/01/14 SUPERSEDING REVISION: 4 Special Adjustments 1. Weather Normalization Adjustment

PSC NO: 9 GAS LEAF: 171 COMPANY: CONSOLIDATED EDISON COMPANY OF NEW YORK, INC. REVISION: 5 INITIAL EFFECTIVE DATE: 03/01/14 SUPERSEDING REVISION: 4 Special Adjustments 1. Weather Normalization Adjustment

Spectra Energy Reports Fourth Quarter and Year-End 2015 Results

Date: February 3, 2016 Spectra Energy Reports Fourth Quarter and Year-End 2015 Results Year-End Highlights: 2015 distributable cash flow of $1.3 billion, with dividend coverage ratio of 1.3x, exceeding

Date: February 3, 2016 Spectra Energy Reports Fourth Quarter and Year-End 2015 Results Year-End Highlights: 2015 distributable cash flow of $1.3 billion, with dividend coverage ratio of 1.3x, exceeding

9 Hedging the Risk of an Energy Futures Portfolio UNCORRECTED PROOFS. Carol Alexander 9.1 MAPPING PORTFOLIOS TO CONSTANT MATURITY FUTURES 12 T 1)

") Helyette Geman c0.tex V - 0//0 :00 P.M. Page Hedging the Risk of an Energy Futures Portfolio Carol Alexander This chapter considers a hedging problem for a trader in futures on crude oil, heating oil and

Helyette Geman c0.tex V - 0//0 :00 P.M. Page Hedging the Risk of an Energy Futures Portfolio Carol Alexander This chapter considers a hedging problem for a trader in futures on crude oil, heating oil and

C. System Operations, Reliability Standards and Capacity Management

C. System Operations, Reliability Standards and Capacity Management 1. Demonstrate that the restructuring plan will maintain the standards and procedures for safety and reliability presently in effect

C. System Operations, Reliability Standards and Capacity Management 1. Demonstrate that the restructuring plan will maintain the standards and procedures for safety and reliability presently in effect

Effect of Increased Natural Gas Exports on Domestic Energy Markets

Effect of Increased Natural Gas Exports on Domestic Energy Markets as requested by the Office of Fossil Energy January 2012 This report was prepared by the U.S. Energy Information Administration (EIA),

Effect of Increased Natural Gas Exports on Domestic Energy Markets as requested by the Office of Fossil Energy January 2012 This report was prepared by the U.S. Energy Information Administration (EIA),

CONNECTICUT ENERGY PRICE REPORT

CONNECTICUT ENERGY PRICE REPORT 1/15/2015 DENOTES FALLING PRICES COMPARED TO YEAR EARLIER DENOTES FLAT PRICES COMPARED TO YEAR EARLIER DENOTES RISING PRICES COMPARED TO YEAR EARLIER CONNECTICUT RETAIL

CONNECTICUT ENERGY PRICE REPORT 1/15/2015 DENOTES FALLING PRICES COMPARED TO YEAR EARLIER DENOTES FLAT PRICES COMPARED TO YEAR EARLIER DENOTES RISING PRICES COMPARED TO YEAR EARLIER CONNECTICUT RETAIL

REVIEW OF NATURAL GAS SUPPLY PORTFOLIO OPTIONS FOR CENTRA GAS CENTRA GAS MANITOBA, INC.

Page 1 of 106 REVIEW OF NATURAL GAS SUPPLY PORTFOLIO OPTIONS FOR CENTRA GAS Prepared for: CENTRA GAS MANITOBA, INC. Submitted By: ICF INTERNATIONAL 9300 Lee Highway Fairfax, VA 22031 USA (703) 218-2758

Page 1 of 106 REVIEW OF NATURAL GAS SUPPLY PORTFOLIO OPTIONS FOR CENTRA GAS Prepared for: CENTRA GAS MANITOBA, INC. Submitted By: ICF INTERNATIONAL 9300 Lee Highway Fairfax, VA 22031 USA (703) 218-2758

Spectra Energy Builds a Business

» Introducing Spectra Energy Builds a Business CEO Fowler on Challenges Ahead By Martin Rosenberg Natural gas once again looms as an important fuel for electricity generation, given a spate of cancellations