APPENDIX IX-A. 2. Use of the Child Support Guidelines As a Rebuttable Presumption -... no change

|

|

|

- Nicholas Murphy

- 9 years ago

- Views:

Transcription

1 APPENDIX IX-A CONSIDERATIONS IN THE USE OF CHILD SUPPORT GUIDELINES (Includes Amendments Through Those Effective February 13, 2007 [February 14, 2006]) 1. Philosophy of the Child Support Guidelines - 2. Use of the Child Support Guidelines As a Rebuttable Presumption - 3. Deviating from the Child Support Guidelines - 4. The Income Shares Approach to Sharing Child-Rearing Expenses - 5. Economic Basis for the Child Support Guidelines - 6. Economic Principles Included in the Child Support Guidelines - 7. Assumptions Included in the Child Support Guidelines a. Intact Family Spending Patterns as the Standard for Support Orders - b. Standard of Living - c. Marginal-Cost Estimation - d. The Rothbarth Marginal Cost Estimator - e. National versus New Jersey Spending on Children - f. Visitation and Shared Parenting - g. Effect of a Child's Age - h. Self-Support Reserve - The self-support reserve is a factor in calculating a child support award only when one or both of the parents have income at or near the poverty level. The self-support reserve is 105% of the U.S. poverty guideline for one person. It attempts to ensure that the obligor has sufficient income to maintain a basic subsistence level and the incentive to work so that child support can be paid. A child support award is adjusted to reflect the self-support reserve only if its payment would reduce the obligor=s net income below the reserve and the custodial parent=s (or the Parent of the Primary Residence=s) net income is greater than 105% of the poverty guideline. The latter condition is necessary to ensure that custodial parents can meet their basic needs so that they can care for the children. As of January 24, 2007 [January 24, 2006], the self-support reserve is $ [$198.00] (this amount is 105% of the poverty guideline for one person). i. Income Tax Withholding

2 j. Spending of Child Support Order - k. Sharing of Child-Rearing Expenses - 8. Expenses Included in the Child Support Schedules - 9. Expenses That May Be Added to the Basic Child Support Obligation Adjustments to the Support Obligation Defining Income Imputing Income to Parents. 13. Adjustments for Visitation Time Shared-Parenting Arrangements a. The Support Guidelines and Shared Parenting - b. Parties Defined. c. Criteria for Determining a Shared-Parenting Award - d. e. If a shared-parenting award is inappropriate due to the PPR=s limited household income, a sole-custody award shall be calculated. Shared-Parenting Primary Household Net Income Thresholds (2.0 x 2007 [2006] Poverty Guideline) Total Persons in Household Weekly Net Income Annual Net Income 2 $527 [$508] $27,380 [$26,400] 3 $660 [$638] $34,340 [$33,200] 4 $794 [$769] $41,300 [$40,000] 5 $928 [$900] $48,260 [$46,800] 6 $1,062 [$1,031] $55,220 [$53,600] 7 $1,196 [$1,162] $62,180 [$60,400] 8 $1,330 [$1,292] $69,140 [$67,200] f. Relative Spending on Children and Shared-Parenting Situations

3 g. Assumptions of the Shared-Parenting Adjustment - h. Calculating the Shared-Parenting Adjustment - i. Note on Controlled Expenses - j. Non-Compliance with Parenting Plan Split-Parenting Arrangements Child in the Custody of a Third Party Adjustments for the Age of the Children College or Other Post-Secondary Education Expenses Determining Child Support and Alimony or Spousal Support Simultaneously Extreme Parental Income Situations - Although these guidelines apply to all actions to establish and modify child support awards, extremely low or high parental income situations make the Appendix IX-F awards inappropriate due to the limitations of the economic data. The guidelines listed below apply to extreme parental income situations. a. Obligors With Net Income Less Than the U.S. Poverty Guideline. If an obligor's net income, after deducting that person=s share of the total support award, is less than 105% of the U.S. poverty guideline for one person (net income of $206 [$198] per week as of January 24, 2007 [January 24, 2006] or as published annually in the Federal Register), the court shall carefully review the obligor's income and living expenses to determine the maximum amount of child support that can reasonably be ordered without denying the obligor the means of self-support at a minimum subsistence level. If an obligee=s income is less than 105% of the poverty guideline, no self-support reserve adjustment shall be made regardless of the obligor=s income. When assessing whether an obligee has sufficient net income to permit the application of the self-support reserve for an obligor, the court may consider the effect of the obligee=s share of the child support obligation (note that this amount is not calculated on either worksheet). Thus, at the court=s discretion, the obligor self-support reserve may not be applied if obligee=s net income minus the obligee=s child support obligation is less than 105% of the poverty guideline for one person. In all cases, a fixed dollar amount shall be ordered to establish the principle of the parent's support obligation and to provide a basis for an upward modification should the obligor's income increase in the future. In these circumstances, the support award should be between $5.00 per week and the support amount at $170 combined net weekly income for the appropriate number of children. b. Parents with a Combined Net Annual Income In Excess of $150, Other Factors that May Require an Adjustment to a Guidelines-Based Award -... no change - 3 -

4 22. Stipulated Agreements. 23. Modification of Support Awards. 24. Effect of Emancipation of a Child Support for a Child Who has Reached Majority Health Insurance for Children. 27. Unpredictable, Non-Recurring Unreimbursed Health-Care In Excess of $250 Per Child Per Year Distribution of Worksheets and Financial Affidavits - I 29. Background Reports and Publications

5 APPENDIX IX-B USE OF THE CHILD SUPPORT GUIDELINES (Includes Amendments Through Those Effective February 13, 2007 [February 14, 2006]) Completion and Filing of the Worksheet General Information Use of Weekly Amounts Rounding to Whole Dollars and Percentages Defining Parental Roles Selection of a Worksheet - 1 -

6 Line Instructions for the Sole-Parenting Worksheet Caption Lines 1 through 5 Determining Income Gross Income - Sources of Income - Income from self-employment or operation of a business. Sporadic Income Military Pay In-Kind Income - Alimony, Spousal Support, and/or Separate Maintenance Received - Types of Income Excluded from Gross Income Collecting and Verifying Income Information Taxable and Non-Taxable Income - 1. Income Not Subject to Federal Income Tax 2. Income Not Subject to New Jersey State Income Tax Note on Social Security Taxes: Social Security tax withholding (FICA) for high-income persons may vary during the year. In the early part of the year, 6.2% is withheld on the first $97,500 [$94,200] of gross earnings (for wage earners in 2007 [2006]). After the maximum $6,045 [$5,840] is withheld, no additional FICA taxes are withheld. Thus, pay stubs issued early in the year may understate net income, while those issued later in the year may overstate it. To estimate weekly FICA taxes, amortize the annual FICA tax using the number of weeks employed or use the Appendix IX-H combined tax tables. Note that self-employed persons must pay the full FICA tax (12.4%) up to the $97,500 [$94,200] limit and the full Medicare tax rate (2.9%) on all earned income. Analyzing Income Tax Returns - Line 1 Gross Taxable Income Line 1a Mandatory Retirement Contributions - 2 -

for high-income persons may vary during the year.")

7 Line 1b Alimony Paid Line 1c Alimony Received Line 2 Adjusted Gross Taxable Income Line 2a Withholding Taxes Line 2b Prior Child Support Orders Line 2c Mandatory Union Dues Line 2d Other-Dependent Deduction Line 3 Net Taxable Income Line 4 Non-Taxable Income Line 5 Net Income Line 6 Percentage Share of Income Line 7-3 -

8 Basic Child Support Amount Line 8 Adding Net Work- Related Child Care Costs to the Basic Obligation Line 9 Adding Health Insurance Costs for the Child to the Basic Obligation Line 10 Adding Predictable and Recurring Unreimbursed Health Care to the Basic Obligation Line 11 Adding Court- Approved Predictable and Recurring Extraordinary Expenses to the Basic Support Amount Line 12 Deducting Government Benefits Paid to or for the Child Line 13 Calculating the Total Child Support Amount - 4 -

9 Line 14 Parental Share of the Total Child Support Obligation Line 15 Credit for Child- Care Payments Line 16 Credit for Payment of Child's Health Insurance Cost Line 17 Credit for Payment of Child's Predictable and Recurring Unreimbursed Health Care Line 18 Credit for Payment of Court- Approved Extraordinary Expenses Line 19 Adjustment for Parenting Time Variable Expenses Line 20 Figuring Each Parent's Net Support Obligation - 5 -

10 Lines 21, 22, and 23 Adjusting the Child Support Order for Other- Dependents Line 21 Line 20 CS Obligation With Other-Dependent Deduction Line 22 Line 20 CS Obligation Without Other-Dependent Deduction Line 23 Obligation Adjusted for Other Dependents Lines 24, 25, and 26 Maintaining a Self-Support Reserve To ensure that the obligor parent retains sufficient net income to live at a minimum subsistence level and has the incentive to work, that parent's net child support award is tested against 105% of the U.S. poverty guideline for one person. If the NCP s net income after deducting the child support award is less than the self-support reserve, the order should be adjusted. No such adjustment shall occur, however, if the custodial parent s net income is less than the self-support reserve. This priority is necessary to ensure that custodial parents can meet their basic needs while caring for the child(ren). The poverty guideline will be disseminated by the AOC each February or when it is published in the Federal Register. The self-support reserve test is applied as follows: 1. Subtract the obligor's child support obligation from that person's net income. 2. If the difference is greater than 105% of the poverty guideline for one person ($206 [$198] per week as of January 24, 2007 [January 24, 2006]), the self-support reserve is preserved and the obligor's support obligation is the child support order. 3. If the difference is less than 105% of the poverty guideline for one person and the custodial parent s net income is greater than 105% of the poverty guideline, the obligor's child support order is the difference between the obligor's net income and the 105% of the poverty guideline for one person. In determining whether the application of the self-support reserve is appropriate, the court may need to impute income to a parent as provided in Appendix IX-A. The court should also consider a parent s actual living expenses and the custodial parent s share of the support obligation (see Appendix IX-A, paragraph 20)

11 Line 24 Self-Support Reserve Test Line 25 Maximum Child Support Order Line 26 Child Support Order - 7 -

12 Line Instructions for the Shared-Parenting Worksheet Caption Lines 1 through 5 Determining Income Gross Income Sources of Income Income from self-employment or operation of a business. Sporadic Income Military Pay In-Kind Income Alimony, Spousal Support, and/or Separate Maintenance Received Types of Income Excluded from Gross Income - Collecting and Verifying Income Information Taxable and Non-Taxable Income - 1. Income Not Subject to Federal Income Tax 2. Income Not Subject to New Jersey State Income Tax Note on Social Security Taxes: Social Security tax withholding (FICA) for high-income persons may vary during the year. In the early part of the year, 6.2% is withheld on the first $97,500 [$94,200] of gross earnings (for wage earners in 2007 [2006]). After the maximum $6,045 [$5,840] is withheld, no additional FICA taxes are withheld. Thus, pay stubs issued early in the year may understate net income, while those issued later in the year may overstate it. To estimate weekly FICA taxes, amortize the annual FICA tax using the number of weeks employed or use the Appendix IX-H combined tax tables. Note that self-employed persons must pay the full FICA tax (12.4%) up to the $97,500 [$94,200] limit and the full Medicare tax rate (2.9%) on all earned income. Analyzing Income Tax Returns - Line 1 Gross Taxable Income Line 1a Mandatory Retirement Contributions 1

for high-income persons may vary during the year.")

13 Line 1b Alimony Paid Line 1c Alimony Received Line 2 Adjusted Gross Taxable Income Line 2a Withholding Taxes Line 2b no change Prior Child Support Orders Line 2c Mandatory Union Dues Line 2d Other-Dependent Deduction Line 3 Net Taxable Income Line 4 Non-Taxable Income Line 5 Net Income Line 6 Percentage Share of Income Line 7 2

14 Number of Overnights with Each Parent Line 8 Percentage of Overnights with Each Parent Line 9 Basic Child Support Amount Line 10 PAR Shared Parenting Fixed Expenses Line 11 Deducting Government Benefits Paid to or for the Child Line 12 Shared Parenting Basic Child Support Amount Line 13 PAR Share of Shared Parenting Basic Child Support Amount Line 14 PAR Shared Parenting Variable Expenses Line 15 3

15 PAR Adjusted Shared Parenting Basic Child Support Amount Lines 16 through 20 Figuring Supplemental Expenses to be Added to the Shared Parenting Basic Child Support Amount Line 16 no change Adding Net Work-Related Child Care Costs Line 17 Adding Health Insurance Costs for the Child Line 18 Adding Predictable and Recurring Unreimbursed Health Care Line 19 Adding Court- Approved Predictable and Recurring Extraordinary Expenses Line 20 no change Total Supplemental Expenses Line 21 4

16 PAR's Share of the Total Supplemental Expenses Line 22 Credit for PAR's Child-Care Payments Line 23 Credit for PAR's Payment of Child's Health Insurance Cost Line 24 Credit for PAR's Payment of Unreimbursed Health Care Line 25 Credit for PAR's Payment of Court-Approved Extraordinary Expenses Line 26 PAR's Total Payments for Supplemental Expenses Line 27 PAR's Net Supplemental Expenses Line 28 PAR's Net Child Support Obligation Lines 29, 30, and 5

17 31 Adjusting the Child Support Obligation for Other Dependents Line 29 Line 28 PAR CS Obligation WITH Other Dependent Deduction Line 30 Line 28 PAR CS Obligation WITHOUT Other Dependent Deduction Line 31 Adjusted PAR CS Obligation Lines 32 and 33 Maintaining a Self-Support Reserve To ensure that the PAR retains sufficient net income to live at a minimum subsistence level and has the incentive to work, that parent's net child support award is tested against 105% of the U.S. poverty guideline for one person. If the PAR s net income after deducting the child support award is less than the self-support reserve, the order should be adjusted. No such adjustment shall occur, however, if the PPR s net income is less than the self-support reserve. This priority is necessary to ensure that a PPR can meet his or her basic needs while caring for the child(ren). The poverty guideline will be disseminated by the AOC each February or when it is published in the Federal Register. The self-support reserve test is applied as follows: 1. Subtract obligor s child support obligation from that person's net income. 2. If the difference is greater than 105% of the poverty guideline for one person ($206 [$198] per week as of January 24, 2007 [January 24, 2006]), the self-support reserve is preserved and the obligor's support obligation is the child support order. 3. If the difference is less than 105% of the poverty guideline for one person and the PPR s net income is greater than 105% of the poverty guideline, the obligor's order is the difference between the obligor's net income and the 105% of the poverty guideline for one person. In determining whether the application of the obligor self-support reserve is appropriate, the court may: impute income to a parent as provided in Appendix IX-A, take into account a parent s actual living expenses, and/or consider the PPR s support obligation to the children (see Appendix IX-A, paragraph 20). NOTE: In some family situations, (e.g., the PPR's income exceeds the PAR's income and 6

18 shared parenting times are near equal), the PPR may owe child support to the PAR (in such cases, the PAR's obligation is a negative number). If this occurs, the self-support reserve should be tested using the PPR's net income and the absolute value of the PAR's negative obligation. In all cases, the PPR should be given the priority with regard to the self-support reserve. Line 32 Self-Support Reserve Test Line 33 PAR's Maximum Child Support Order Line 34 Child Support Order Line 35 PPR Household Income Test 7

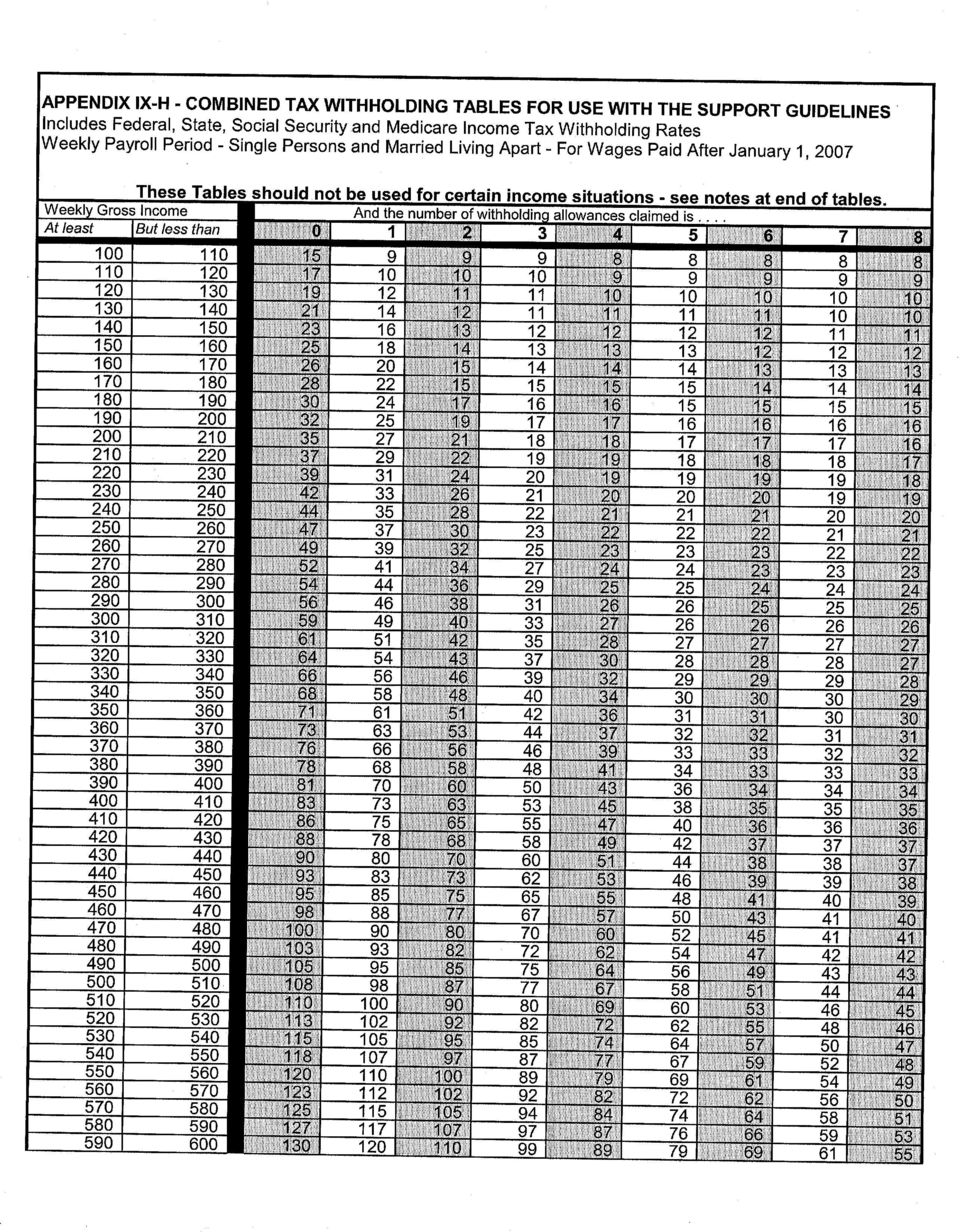

19 COMMENTS ON THE USE OF THE COMBINED TAX TABLES Limitations of this Table - This table should not be used if either parent: (1) has income from non-wage income that is not subject to the same taxes as wages (such as alimony or Social Security disability - see Appendix IX-B), (2) claims mandatory retirement contributions, or (3) has a married marital status for tax withholding purposes. Withholding Taxes vs. Year-End Tax Obligations - This table is based on withholding rates. It is meant to provide an estimate of how much after-tax income an individual has available to pay child support at the end of each week. Year-end tax obligations, adjustments, credits, and tax refunds (e.g., earned income credit, filing as head of household, personal deductions for children) are not considered in this table and may result in taxes that differ from the amount withheld by an employer. When applying the support guidelines, withholding taxes and/or net income should be adjusted based on year-end tax obligations after reviewing tax returns if such an adjustment would more accurately reflect net income available to either parent in future years. Withholding Allowances - For assumptions regarding the number of withholding allowances permitted by an individual, see Appendix IX-B, Line 2a. Self-Employed Persons - This table gives the withholding tax for employees who are paid wages for their services. It assumes that the employer is paying half of the Social Security and Medicare taxes for the employee (7.65%). To estimate the combined tax for self-employed persons earning less than $97,500, multiply gross taxable income by and add the result to the table amount. For persons earning above $97,500, multiply gross income by.0145 (Medicare), add $116 (FICA max), and add the sum to the table amount. IMPORTANT: Although this formula will provide an estimate of self-employment income taxes, a careful review of the most recent personal and business tax returns will provide a more accurate tax figure for self-employed persons. Also, see IRS Pubs 505 and SE and App. IX-B (Determining Income). Non-Taxable Income - Some forms of income (e.g., Social Security, VA, Worker's Comp) are not subject to state or federal income tax. Such income is added to taxable income after combined withholding taxes are deducted. Do not combine non-taxable income with gross taxable income when using these tables. (See Appendix IX-B - Determining Income). Alimony Income - Alimony received is subject to federal and state income tax, but not FICA or Medicare tax. If the combined tax tables are used for gross income that includes alimony, deduct the FICA/Medicare tax for the amount of the alimony (0.0765) from the combined withholding tax. Social Security Tax (FICA) - This table gives the correct amount of combined withholding tax only if wages for income tax and Social Security are the same. The Social Security tax withholding rate for wage earners is The maximum amount of FICA tax for one year ($6,045/year or $116/week) is averaged into the table for income ranges above $97,500. Refer to IRS Publication 15 for more information. Note that some forms of income are not subject to FICA and Medicare tax (interest income, rents, dealing in property). These forms of income should be excluded from gross income when estimating a parent's taxes. Also, self-employed persons must pay the full FICA/Medicare tax on 92.35% of their gross income (See IRS Publication 533 and Schedule SE). Medicare Tax - The Medicare tax withholding rate for wage earners is for all incomes. Federal Income Tax - This table includes federal income tax withholding rates as published by the IRS (see Publication 15, Revised January 2007). To determine the amount of federal income tax for incomes greater than those shown in this table, refer to these IRS Publications. New Jersey Income Tax - This table includes tax withholding rates published by the NJ Division of Taxation (see NJ-WT, effective January 2007). To determine New Jersey withholding tax for incomes greater than those shown on this table, refer to Publication NJ-WT and New Withholding Rate tables. Note: Appendix IX-H amended February 13, 2007 to be effective immediately.

20

21

22

23

24

25

26

27

28

29

30

Appendix IX-B USE OF THE CHILD SUPPORT GUIDELINES (Includes Amendments through those effective May 1, 2015) GENERAL INFORMATION

GENERAL INFORMATION") Appendix IX-B USE OF THE CHILD SUPPORT GUIDELINES (Includes Amendments through those effective May 1, 2015) GENERAL INFORMATION Completion and Filing of the Worksheet A child support guidelines worksheet

Appendix IX-B USE OF THE CHILD SUPPORT GUIDELINES (Includes Amendments through those effective May 1, 2015) GENERAL INFORMATION Completion and Filing of the Worksheet A child support guidelines worksheet

How to determine CHILD SUPPORT in New Jersey By Mark Gruber Esq.

How to determine CHILD SUPPORT in New Jersey By Mark Gruber Esq. It is the law that both parents contribute to the support of children that they bring into this world. New Jersey has promulgated guidelines

How to determine CHILD SUPPORT in New Jersey By Mark Gruber Esq. It is the law that both parents contribute to the support of children that they bring into this world. New Jersey has promulgated guidelines

IX-A CONSIDERATIONS IN THE USE OF CHILD SUPPORT GUIDELINES

New Jersey Rules of Court Appendix IX-A CONSIDERATIONS IN THE USE OF CHILD SUPPORT GUIDELINES (Includes amendments through those effective May 1, 2015) 1. Philosophy of the Child Support Guidelines These

New Jersey Rules of Court Appendix IX-A CONSIDERATIONS IN THE USE OF CHILD SUPPORT GUIDELINES (Includes amendments through those effective May 1, 2015) 1. Philosophy of the Child Support Guidelines These

South Carolina CHILD SUPPORT GUIDELINES

South Carolina CHILD SUPPORT GUIDELINES 2014 EDITION Table of Contents 1. Introduction... 1 2. Use Of The Guidelines... 1 3. Determination of Child Support Awards... 3 A. Income... 3 1. Definition... 3

South Carolina CHILD SUPPORT GUIDELINES 2014 EDITION Table of Contents 1. Introduction... 1 2. Use Of The Guidelines... 1 3. Determination of Child Support Awards... 3 A. Income... 3 1. Definition... 3

(c) The net income of the parent remaining after withholding required by law or as a condition of employment; 4

The net income of the parent remaining after withholding required by law or as a condition of employment; 4") 137-050-0760 Rebuttals (1) The presumption that the guideline support amount as provided in OAR 137-050-0700 through OAR 137-050-0755 is the correct support amount may be rebutted by a finding that sets

137-050-0760 Rebuttals (1) The presumption that the guideline support amount as provided in OAR 137-050-0700 through OAR 137-050-0755 is the correct support amount may be rebutted by a finding that sets

CHAPTER 9 CHILD SUPPORT GUIDELINES

May 2013 CHILD SUPPORT GUIDELINES Ch 9, p.i CHAPTER 9 CHILD SUPPORT GUIDELINES Rule 9.1 Rule 9.2 Rule 9.3 Rule 9.4 Rule 9.5 Rule 9.6 Rule 9.7 Rule 9.8 Rule 9.9 Rule 9.10 Rule 9.11 Rule 9.12 Rule 9.13 Rule

May 2013 CHILD SUPPORT GUIDELINES Ch 9, p.i CHAPTER 9 CHILD SUPPORT GUIDELINES Rule 9.1 Rule 9.2 Rule 9.3 Rule 9.4 Rule 9.5 Rule 9.6 Rule 9.7 Rule 9.8 Rule 9.9 Rule 9.10 Rule 9.11 Rule 9.12 Rule 9.13 Rule

KANSAS CHILD SUPPORT GUIDELINES Pursuant to Kansas Supreme Court Administrative Order No. 261 Amended March 26, 2012. Effective April 1, 2012

KANSAS CHILD SUPPORT GUIDELINES Pursuant to Kansas Supreme Court Administrative Order No. 261 Amended March 26, 2012 Effective April 1, 2012 TABLE OF CONTENTS I. USE OF THE GUIDELINES... 1 II. DEFINITIONS

KANSAS CHILD SUPPORT GUIDELINES Pursuant to Kansas Supreme Court Administrative Order No. 261 Amended March 26, 2012 Effective April 1, 2012 TABLE OF CONTENTS I. USE OF THE GUIDELINES... 1 II. DEFINITIONS

1) to minimize the economic impact on. 2) to promote joint parental responsibility. 3) to meet the child s survival needs in

to minimize the economic impact on. 2) to promote joint parental responsibility. 3) to meet the child s survival needs in") Preamble These guidelines shall take effect on August 1, 2013 and shall be applied to all child support orders and judgments entered after the effective date. There shall be a rebuttable presumption that

Preamble These guidelines shall take effect on August 1, 2013 and shall be applied to all child support orders and judgments entered after the effective date. There shall be a rebuttable presumption that

Child Support Computation 03EN025I

Child Support Computation 03EN025I Purpose of form The purpose of the Child Support Computation form is to calculate a child support obligation pursuant to 43 O.S. Sections 118A 118I, effective July 1,

Child Support Computation 03EN025I Purpose of form The purpose of the Child Support Computation form is to calculate a child support obligation pursuant to 43 O.S. Sections 118A 118I, effective July 1,

Child Support Guidelines

Child Support Guidelines 1999 Edition TABLE OF CONTENTS I. INTRODUCTION... 1 II. USE OF GUIDELINES... 2 III. DETERMINATION OF CHILD SUPPORT AWARDS... 3 A. Income... 3 1. Definition... 3 2. Gross Income...

Child Support Guidelines 1999 Edition TABLE OF CONTENTS I. INTRODUCTION... 1 II. USE OF GUIDELINES... 2 III. DETERMINATION OF CHILD SUPPORT AWARDS... 3 A. Income... 3 1. Definition... 3 2. Gross Income...

How to Fill out the Child Support Guidelines Affidavit. Form DR-305

How to Fill out the Child Support Guidelines Affidavit Form DR-305 Child Support Guidelines Affidavit, DR- 305 form (PDF Fill-In PDF 651 KB) Child Support Guidelines Affidavit, DR- 305 form (PDF Fill-In

How to Fill out the Child Support Guidelines Affidavit Form DR-305 Child Support Guidelines Affidavit, DR- 305 form (PDF Fill-In PDF 651 KB) Child Support Guidelines Affidavit, DR- 305 form (PDF Fill-In

HOW TO CALCULATE CHILD SUPPORT UNDER CIVIL RULE 90.3

HOW TO CALCULATE CHILD SUPPORT UNDER CIVIL RULE 90.3 This booklet contains instructions for the following forms: DR-105 DR-305 DR-306 DR-307 DR-308 Petition for Dissolution of Marriage (the child support

HOW TO CALCULATE CHILD SUPPORT UNDER CIVIL RULE 90.3 This booklet contains instructions for the following forms: DR-105 DR-305 DR-306 DR-307 DR-308 Petition for Dissolution of Marriage (the child support

IDAHO CHILD SUPPORT GUIDELINES

IDAHO CHILD SUPPORT GUIDELINES Section 1. Introduction. The Child Support Guidelines are intended to give specific guidance for evaluating evidence in child support proceedings. Acknowledging there are

IDAHO CHILD SUPPORT GUIDELINES Section 1. Introduction. The Child Support Guidelines are intended to give specific guidance for evaluating evidence in child support proceedings. Acknowledging there are

RULES OF TENNESSEE DEPARTMENT OF HUMAN SERVICES CHILD SUPPORT SERVICES DIVISION CHAPTER 1240-2-4 CHILD SUPPORT GUIDELINES TABLE OF CONTENTS

RULES OF TENNESSEE DEPARTMENT OF HUMAN SERVICES CHILD SUPPORT SERVICES DIVISION CHAPTER 1240-2-4 CHILD SUPPORT GUIDELINES TABLE OF CONTENTS 1240-2-4-.01 Legal Basis, Scope, and Purpose 1240-2-4-.06 Retroactive

RULES OF TENNESSEE DEPARTMENT OF HUMAN SERVICES CHILD SUPPORT SERVICES DIVISION CHAPTER 1240-2-4 CHILD SUPPORT GUIDELINES TABLE OF CONTENTS 1240-2-4-.01 Legal Basis, Scope, and Purpose 1240-2-4-.06 Retroactive

OFFICE OF THE ATTORNEY GENERAL 2013 TAX CHARTS

OFFICE OF THE ATTORNEY GENERAL 2013 TAX CHARTS Pursuant to 154.061 of the Texas Family Code, the Office of the Attorney General of Texas, as the Title IV-D agency, has promulgated the following tax charts

OFFICE OF THE ATTORNEY GENERAL 2013 TAX CHARTS Pursuant to 154.061 of the Texas Family Code, the Office of the Attorney General of Texas, as the Title IV-D agency, has promulgated the following tax charts

RULES OF TENNESSEE DEPARTMENT OF HUMAN SERVICES CHILD SUPPORT SERVICES DIVISION CHAPTER 1240-2-4 CHILD SUPPORT GUIDELINES TABLE OF CONTENTS

RULES OF TENNESSEE DEPARTMENT OF HUMAN SERVICES CHILD SUPPORT SERVICES DIVISION CHAPTER 1240-2-4 CHILD SUPPORT GUIDELINES TABLE OF CONTENTS 1240-2-4-.01 Legal Basis, Scope, and Purpose 1240-2-4-.06 Retroactive

RULES OF TENNESSEE DEPARTMENT OF HUMAN SERVICES CHILD SUPPORT SERVICES DIVISION CHAPTER 1240-2-4 CHILD SUPPORT GUIDELINES TABLE OF CONTENTS 1240-2-4-.01 Legal Basis, Scope, and Purpose 1240-2-4-.06 Retroactive

INCOME SHARES & CALCULATION OF CHILD SUPPORT NET INCOME

INCOME SHARES & CALCULATION OF CHILD SUPPORT NET INCOME 1 THEILLINOIS FAMILYLAW STUDYCOMMITTEE VOTED TO RETAIN THE NET INCOME APPROACH The Illinois Family Law Study Committee Formed in 2008 by House Resolution

INCOME SHARES & CALCULATION OF CHILD SUPPORT NET INCOME 1 THEILLINOIS FAMILYLAW STUDYCOMMITTEE VOTED TO RETAIN THE NET INCOME APPROACH The Illinois Family Law Study Committee Formed in 2008 by House Resolution

Florida Child Support Worksheet and Guidelines

Florida Child Support Worksheet and Guidelines Florida Statute (s. 61.30, F.S.) requires guidelines to be used in establishing new child support obligations or modifying child support in a Florida court.

Florida Child Support Worksheet and Guidelines Florida Statute (s. 61.30, F.S.) requires guidelines to be used in establishing new child support obligations or modifying child support in a Florida court.

Social Security and Taxes

Social Security and Taxes Social Security is a safety net for the middle class and a lifeline for millions more. For more than 60 percent of Americans age 65 and over, it provides over 50 percent of their

Social Security and Taxes Social Security is a safety net for the middle class and a lifeline for millions more. For more than 60 percent of Americans age 65 and over, it provides over 50 percent of their

CHAPTER 75-02-04.1 CHILD SUPPORT GUIDELINES

CHAPTER 75-02-04.1 CHILD SUPPORT GUIDELINES Section 75-02-04.1-01 De nitions 75-02-04.1-02 Determination of Support Amount - General Instructions 75-02-04.1-03 Determination of Child Support Obligation

CHAPTER 75-02-04.1 CHILD SUPPORT GUIDELINES Section 75-02-04.1-01 De nitions 75-02-04.1-02 Determination of Support Amount - General Instructions 75-02-04.1-03 Determination of Child Support Obligation

Arizona Child Support Guidelines Child Outcome Based Support Model

Arizona Child Support Guidelines Child Outcome Based Support Model The guideline model and principles contained herein have been approved by the Arizona Judicial Council on 03-25-10 and revisions were

Arizona Child Support Guidelines Child Outcome Based Support Model The guideline model and principles contained herein have been approved by the Arizona Judicial Council on 03-25-10 and revisions were

Federal Percentage Method of Withholding For Payroll Paid January 23 December 31, 2015 Source: IRS Notice 1036 (January 2015)

") Federal Percentage Method of Withholding For Payroll Paid January 23 December 31, 2015 Procedures used to calculate federal taxes withheld*: 1. Obtain the employee s gross wage for the payroll period.

Federal Percentage Method of Withholding For Payroll Paid January 23 December 31, 2015 Procedures used to calculate federal taxes withheld*: 1. Obtain the employee s gross wage for the payroll period.

- all the money you receive in a year - money from wages, tips, interest you earn, dividends, capital gains, etc.

4D Income Taxes there are 5 different categories Single You must be unmarried at the end of the year. Married filing jointly this is how most married people will file. Married filing separately occasionally,

4D Income Taxes there are 5 different categories Single You must be unmarried at the end of the year. Married filing jointly this is how most married people will file. Married filing separately occasionally,

2011 Revisions to the North Carolina Child Support Guidelines

FAMILY LAW BULLETIN NO. 24 DECEMBER 2010 2011 Revisions to the North Carolina Child Support Guidelines Cheryl Daniels Howell States are required by federal law to establish child support guidelines as

FAMILY LAW BULLETIN NO. 24 DECEMBER 2010 2011 Revisions to the North Carolina Child Support Guidelines Cheryl Daniels Howell States are required by federal law to establish child support guidelines as

Questions and Answers for the Additional Medicare Tax

Questions and Answers for the Additional Medicare Tax On Nov. 26, 2013, the IRS issued final regulations (TD 9645) implementing the Additional Medicare Tax as added by the Affordable Care Act (ACA). The

Questions and Answers for the Additional Medicare Tax On Nov. 26, 2013, the IRS issued final regulations (TD 9645) implementing the Additional Medicare Tax as added by the Affordable Care Act (ACA). The

South Carolina CHILD SUPPORT GUIDELINES

South Carolina CHILD SUPPORT GUIDELINES 2006 EDITION Table of Contents 1. INTRODUCTION... 1 2. USE OF THE GUIDELINES... 1 3. DETERMINATION OF CHILD SUPPORT AWARDS... 3 3.1 INCOME...3 3.1.1 Definition...3

South Carolina CHILD SUPPORT GUIDELINES 2006 EDITION Table of Contents 1. INTRODUCTION... 1 2. USE OF THE GUIDELINES... 1 3. DETERMINATION OF CHILD SUPPORT AWARDS... 3 3.1 INCOME...3 3.1.1 Definition...3

University of Northern Iowa

University of Northern Iowa Direct Deposit of Payroll Authorization Form Name (Please Print) (Last, First, MI) UNI ID# I hereby authorize the University of Northern Iowa to initiate direct deposit credit

University of Northern Iowa Direct Deposit of Payroll Authorization Form Name (Please Print) (Last, First, MI) UNI ID# I hereby authorize the University of Northern Iowa to initiate direct deposit credit

Federal Income Tax Information January 29, 2016 Page 2. 2016 Federal Income Tax Withholding Information - PERCENTAGE METHOD

Federal Income Tax Information January 29, 2016 Page 2 - PERCENTAGE METHOD ALLOWANCE TABLE Dollar Amount of Withholding Allowances Number of Biweekly Monthly Withholding Pay Period Pay Period Allowances

Federal Income Tax Information January 29, 2016 Page 2 - PERCENTAGE METHOD ALLOWANCE TABLE Dollar Amount of Withholding Allowances Number of Biweekly Monthly Withholding Pay Period Pay Period Allowances

DISCLOSURE STATEMENT

DISCLOSURE STATEMENT for Individual Retirement Annuities Home Office: Wilmington, Delaware Administrative Office: P.O. Box 19032 Greenville, SC 29602-9032 Telephone 866-262-1161 The following information

DISCLOSURE STATEMENT for Individual Retirement Annuities Home Office: Wilmington, Delaware Administrative Office: P.O. Box 19032 Greenville, SC 29602-9032 Telephone 866-262-1161 The following information

Child Support Computation for Period Prior to July 1, 2009

Child Support Computation for Period Prior to July 1, 2009 03EN005I Purpose of form The purpose of Form 03EN005E, Child Support Computation for Period Prior to July 1, 2009, is to calculate judgments in

Child Support Computation for Period Prior to July 1, 2009 03EN005I Purpose of form The purpose of Form 03EN005E, Child Support Computation for Period Prior to July 1, 2009, is to calculate judgments in

Check if this is an amended filing

Fill in this information to identify your case: Debtor 1 Debtor 2 (Spouse, if filing) United States Bankruptcy Court for the: District of of Case number (If known) Check if this is an amended filing Official

Fill in this information to identify your case: Debtor 1 Debtor 2 (Spouse, if filing) United States Bankruptcy Court for the: District of of Case number (If known) Check if this is an amended filing Official

Official Form 22A 2 Chapter 7 Means Test Calculation 12/13

Fill in this information to identify your case: Check one only as directed in lines 40 or 42: Debtor 1 Debtor 2 (Spouse, if filing) United States Bankruptcy Court for the: District of (State) Case number

Fill in this information to identify your case: Check one only as directed in lines 40 or 42: Debtor 1 Debtor 2 (Spouse, if filing) United States Bankruptcy Court for the: District of (State) Case number

ATTENTION: NEW NC-4 WITHHOLDING FORMS ENCLOSED

North Carolina Department of Revenue ATTENTION: NEW NC-4 WITHHOLDING FORMS ENCLOSED IMMEDIATE ACTION REQUIRED North Carolina Department of Revenue TO: IMPORTANT NOTICE: NEW NC-4 REQUIRED FOR PAYMENTS BEGINNING

North Carolina Department of Revenue ATTENTION: NEW NC-4 WITHHOLDING FORMS ENCLOSED IMMEDIATE ACTION REQUIRED North Carolina Department of Revenue TO: IMPORTANT NOTICE: NEW NC-4 REQUIRED FOR PAYMENTS BEGINNING

Form CT-W4P Withholding Certificate for Pension or Annuity Payments 2015. Complete this certifi cate in blue or black ink only.

Department of Revenue Services State of Connecticut (Rev. 12/14) Form CT-W4P Withholding Certificate for Pension or Annuity Payments 2015 Complete this certifi cate in blue or black ink only. CT-W4P Form

Department of Revenue Services State of Connecticut (Rev. 12/14) Form CT-W4P Withholding Certificate for Pension or Annuity Payments 2015 Complete this certifi cate in blue or black ink only. CT-W4P Form

Companion Guide to Child Support Worksheet and Schedules

Companion Guide to Child Support Worksheet and Schedules Companion Guide to the Child Support Worksheet and Schedules Introduction This Companion Guide is authored by the Staff of the Georgia Child Support

Companion Guide to Child Support Worksheet and Schedules Companion Guide to the Child Support Worksheet and Schedules Introduction This Companion Guide is authored by the Staff of the Georgia Child Support

Your Guide to Setting Support Amounts $ % dcf.wisconsin.gov

Your Guide to Setting Support Amounts WI BUREAU OF CHILD SUPPORT $ % Percentage of Income Standard Income for child support Guidelines Serial family parents Low-income payers High-income payers Shared-placement

Your Guide to Setting Support Amounts WI BUREAU OF CHILD SUPPORT $ % Percentage of Income Standard Income for child support Guidelines Serial family parents Low-income payers High-income payers Shared-placement

Withholding Certificate for Pension or Annuity Payments

Web 12-14 NC-4P Withholding Certificate for Pension or Annuity Payments PURPOSE. Form NC-4P is for North Carolina residents who are recipients of income from pensions, annuities, and certain other deferred

Web 12-14 NC-4P Withholding Certificate for Pension or Annuity Payments PURPOSE. Form NC-4P is for North Carolina residents who are recipients of income from pensions, annuities, and certain other deferred

NORTHEAST INVESTORS TRUST. 125 High Street Boston, MA 02110 Telephone: 800-225-6704

NORTHEAST INVESTORS TRUST traditional IRA INVESTOR S KIT 125 High Street Boston, MA 02110 Telephone: 800-225-6704 Table of Contents NORTHEAST INVESTORS TRUST TRADITIONAL IRA DISCLOSURE STATEMENT...1 INTRODUCTION...1

NORTHEAST INVESTORS TRUST traditional IRA INVESTOR S KIT 125 High Street Boston, MA 02110 Telephone: 800-225-6704 Table of Contents NORTHEAST INVESTORS TRUST TRADITIONAL IRA DISCLOSURE STATEMENT...1 INTRODUCTION...1

Official Form B 22A2 Chapter 7 Means Test Calculation 12/14

Fill in this information to identify your case: Debtor 1 Debtor 2 (Spouse, if filing) United States Bankruptcy Court for the: District District of of (State) Case number (If known) Check the appropriate

Fill in this information to identify your case: Debtor 1 Debtor 2 (Spouse, if filing) United States Bankruptcy Court for the: District District of of (State) Case number (If known) Check the appropriate

Cut here and give this certificate to your employer. Keep the top portion for your records. North Carolina Department of Revenue

Web 2-15 NC-4 Employee s Withholding Allowance Certificate PURPOSE - Complete Form NC-4, Employee s Withholding Allowance Certificate, so that your employer can withhold the correct amount of State income

Web 2-15 NC-4 Employee s Withholding Allowance Certificate PURPOSE - Complete Form NC-4, Employee s Withholding Allowance Certificate, so that your employer can withhold the correct amount of State income

CHILD SUPPORT: Questions and Answers

CHILD SUPPORT: Questions and Answers A PUBLICATION OF THE ASSOCIATION OF THE BAR OF THE CITY OF NEW YORK FUND, INC. JUNE 2002 Introduction Are you a parent living in New York City and raising children

CHILD SUPPORT: Questions and Answers A PUBLICATION OF THE ASSOCIATION OF THE BAR OF THE CITY OF NEW YORK FUND, INC. JUNE 2002 Introduction Are you a parent living in New York City and raising children

The FHLBI may, in its discretion, allow applicants to follow the income guidelines of other funding sources where differences exist.

Attachment D Income Guidelines For all FHLBI Affordable Housing Program (AHP) projects (including competitive AHP and the Homeownership Set-aside Programs) sponsors and members are required to use the

Attachment D Income Guidelines For all FHLBI Affordable Housing Program (AHP) projects (including competitive AHP and the Homeownership Set-aside Programs) sponsors and members are required to use the

Slide 2. Income Taxes

Slide 1 Taxes Income taxes have been a part of American life since 1909 when the 16 th Amendment to the Constitution was ratified. You can t avoid taxes, so you might as well understand how taxes are structured

Slide 1 Taxes Income taxes have been a part of American life since 1909 when the 16 th Amendment to the Constitution was ratified. You can t avoid taxes, so you might as well understand how taxes are structured

Understanding Your Pay and Form W-2

Understanding Your Pay and Form W-2 Table of Contents 3 Welcome to Understanding Your Pay 3 How is My Pay Calculated? 3 Gross Wages 4 Pre-Tax Deductions 4 Income Taxes 5 Employment Taxes 5 Post-Tax Deductions

Understanding Your Pay and Form W-2 Table of Contents 3 Welcome to Understanding Your Pay 3 How is My Pay Calculated? 3 Gross Wages 4 Pre-Tax Deductions 4 Income Taxes 5 Employment Taxes 5 Post-Tax Deductions

Supplement to IRA Custodial Agreements

Supplement to IRA Custodial Agreements Effective December 31, 2014, the update below will be made to the American Century Custodial agreements for the following retirement accounts: Traditional IRAs, Roth

Supplement to IRA Custodial Agreements Effective December 31, 2014, the update below will be made to the American Century Custodial agreements for the following retirement accounts: Traditional IRAs, Roth

How much can I deduct if I am an active participant in a qualified plan?... 2

Table of Contents What is an Individual Retirement Account (IRA)?...................................... 1 Who may establish a Traditional IRA?............................................... 1 How much

Table of Contents What is an Individual Retirement Account (IRA)?...................................... 1 Who may establish a Traditional IRA?............................................... 1 How much

HOW TO CALCULATE CHILD SUPPORT +/-

HOW TO CALCULATE CHILD SUPPORT +/- This packet contains instructions needed to complete a Child Support Order and the Parents Worksheet for Child Support for those who do not want to use the FREE online

HOW TO CALCULATE CHILD SUPPORT +/- This packet contains instructions needed to complete a Child Support Order and the Parents Worksheet for Child Support for those who do not want to use the FREE online

How To Calculate Tax In The United States

TAXATION OF U.S. EXPATRIATES gtn.com C O N T E N T S 1. Introduction 1 2. Case Study Facts 2 3. U.S. Income Taxation Overview 4 Federal Income Tax Calculation 5 Foreign Earned Income and Housing Exclusions

TAXATION OF U.S. EXPATRIATES gtn.com C O N T E N T S 1. Introduction 1 2. Case Study Facts 2 3. U.S. Income Taxation Overview 4 Federal Income Tax Calculation 5 Foreign Earned Income and Housing Exclusions

Important Information Morgan Stanley SIMPLE IRA Summary

SIMPLE IRA Summary September 2013 Important Information Morgan Stanley SIMPLE IRA Summary The following is intended to provide you with basic information on the roles and services that Morgan Stanley Smith

SIMPLE IRA Summary September 2013 Important Information Morgan Stanley SIMPLE IRA Summary The following is intended to provide you with basic information on the roles and services that Morgan Stanley Smith

Tax Subsidies for Health Insurance An Issue Brief

Tax Subsidies for Health Insurance An Issue Brief Prepared by the Kaiser Family Foundation July 2008 Tax Subsidies for Health Insurance Most workers pay both federal and state taxes for wages paid to them

Tax Subsidies for Health Insurance An Issue Brief Prepared by the Kaiser Family Foundation July 2008 Tax Subsidies for Health Insurance Most workers pay both federal and state taxes for wages paid to them

Income, Gift, and Estate Tax Update

Income, Gift, and Estate Tax Update Individual Income Tax Rates p. 1 Phil Harris Department of Agricultural and Applied Economics University of Wisconsin-Madison Marriage Penalty Relief p. 1 Capital Gains

Income, Gift, and Estate Tax Update Individual Income Tax Rates p. 1 Phil Harris Department of Agricultural and Applied Economics University of Wisconsin-Madison Marriage Penalty Relief p. 1 Capital Gains

FICA WITHHOLDING & TAXATION OF DISABILITY BENEFITS. Information for Policyholders

FICA WITHHOLDING & TAXATION OF DISABILITY BENEFITS Information for Policyholders Step One As claim payments are made: Calculates and withholds the EMPLOYEE S portion of FICA liability based on information

FICA WITHHOLDING & TAXATION OF DISABILITY BENEFITS Information for Policyholders Step One As claim payments are made: Calculates and withholds the EMPLOYEE S portion of FICA liability based on information

Individual Retirement Arrangements (IRAs)

") Department of the Treasury Internal Revenue Service Publication 590 Cat. No. 15160x Individual Retirement Arrangements (IRAs) (Including Roth IRAs and Education IRAs) For use in preparing 1999 Returns

Department of the Treasury Internal Revenue Service Publication 590 Cat. No. 15160x Individual Retirement Arrangements (IRAs) (Including Roth IRAs and Education IRAs) For use in preparing 1999 Returns

BMO Funds State Street Bank and Trust Company Universal Individual Retirement Account Disclosure Statement. Part One: Description of Traditional IRAs

BMO Funds State Street Bank and Trust Company Universal Individual Retirement Account Disclosure Statement Part One: Description of Traditional IRAs Part One of the Disclosure Statement describes the rules

BMO Funds State Street Bank and Trust Company Universal Individual Retirement Account Disclosure Statement Part One: Description of Traditional IRAs Part One of the Disclosure Statement describes the rules

2013 Michigan Child Support Formula Manual

2013 Michigan Child Support Formula Manual Effective: January 1, 2013 State Court Administrative Office Friend of the Court Bureau Lansing, Michigan 2013 Michigan Child Support Formula Manual Effective:

2013 Michigan Child Support Formula Manual Effective: January 1, 2013 State Court Administrative Office Friend of the Court Bureau Lansing, Michigan 2013 Michigan Child Support Formula Manual Effective:

CONGRESS OF THE UNITED STATES CONGRESSIONAL BUDGET OFFICE CBO. The Distribution of Household Income and Federal Taxes, 2008 and 2009

CONGRESS OF THE UNITED STATES CONGRESSIONAL BUDGET OFFICE Percent 70 The Distribution of Household Income and Federal Taxes, 2008 and 2009 60 50 Before-Tax Income Federal Taxes Top 1 Percent 40 30 20 81st

CONGRESS OF THE UNITED STATES CONGRESSIONAL BUDGET OFFICE Percent 70 The Distribution of Household Income and Federal Taxes, 2008 and 2009 60 50 Before-Tax Income Federal Taxes Top 1 Percent 40 30 20 81st

STATE OF CONNECTICUT COMMISSION FOR CHILD SUPPORT GUIDELINES

STATE OF CONNECTICUT COMMISSION FOR CHILD SUPPORT GUIDELINES Child Support and Arrearage Guidelines Effective July 1, 2015 This booklet contains the Child Support and Arrearage Guidelines regulations adopted

STATE OF CONNECTICUT COMMISSION FOR CHILD SUPPORT GUIDELINES Child Support and Arrearage Guidelines Effective July 1, 2015 This booklet contains the Child Support and Arrearage Guidelines regulations adopted

WITHHOLDING CERTIFICATE FOR PENSION OR ANNUITY PAYMENTS

WITHHOLDING CERTIFICATE FOR PENSION OR ANNUITY PAYMENTS Type or Print Your Full Name Your Social Security Number Home Address (Number and Street or Rural Route) Claim or Identification Number (if any)

WITHHOLDING CERTIFICATE FOR PENSION OR ANNUITY PAYMENTS Type or Print Your Full Name Your Social Security Number Home Address (Number and Street or Rural Route) Claim or Identification Number (if any)

Withholding Certificate for Pension or Annuity Payments

Withholding Certificate for Pension or Annuity Payments Type or Print Your Full Name Your Social Security Number Home Address (Number and Street or Rural Route) Claim or Identification Number (if any)

Withholding Certificate for Pension or Annuity Payments Type or Print Your Full Name Your Social Security Number Home Address (Number and Street or Rural Route) Claim or Identification Number (if any)

10/8/2015. KANSAS CHILD SUPPORT GUIDELINES Pursuant to Kansas Supreme Court Administrative Order No. 284. Effective January 1, 2016

10/8/2015 KANSAS CHILD SUPPORT GUIDELINES Pursuant to Kansas Supreme Court Administrative Order No. 284 Effective January 1, 2016 TABLE OF CONTENTS I. USE OF THE GUIDELINES... 1 II. DEFINITIONS AND EXPLANATION...

10/8/2015 KANSAS CHILD SUPPORT GUIDELINES Pursuant to Kansas Supreme Court Administrative Order No. 284 Effective January 1, 2016 TABLE OF CONTENTS I. USE OF THE GUIDELINES... 1 II. DEFINITIONS AND EXPLANATION...

Withholding Certificate for Pension or Annuity Payments

NC-4P Web 11-13! Withholding Certificate for Pension or Annuity Payments North Carolina Department of Revenue Important: You must complete a new Form NC-4P for tax year 2014. As a result of recent law

NC-4P Web 11-13! Withholding Certificate for Pension or Annuity Payments North Carolina Department of Revenue Important: You must complete a new Form NC-4P for tax year 2014. As a result of recent law

Withholding Certificate for Pension or Annuity Payments

Withholding Certificate for Pension or Annuity Payments Type or Print Your Full Name Your Social Security Number Home Address (Number and Street or Rural Route) Claim or Identification Number (if any)

Withholding Certificate for Pension or Annuity Payments Type or Print Your Full Name Your Social Security Number Home Address (Number and Street or Rural Route) Claim or Identification Number (if any)

Civil Action No. V- - CHILD SUPPORT ORDER ADDENDUM

IN THE SUPERIOR COURT OF HOUSTON COUNTY STATE OF GEORGIA, Plaintiff Civil Action No. V- - vs, Defendant CHILD SUPPORT ORDER ADDENDUM Instructions: All parts of this Addendum must be completed and it must

IN THE SUPERIOR COURT OF HOUSTON COUNTY STATE OF GEORGIA, Plaintiff Civil Action No. V- - vs, Defendant CHILD SUPPORT ORDER ADDENDUM Instructions: All parts of this Addendum must be completed and it must

Important Information About. Tax Withholding and Railroad Retirement Payments

Important Information About Tax Withholding and Railroad Retirement Payments For use with Form RRB W-4P U.S. Railroad Retirement Board 844 North Rush Street Chicago, IL 60611-2092 www.rrb.gov TXB-25 (01-15)

Important Information About Tax Withholding and Railroad Retirement Payments For use with Form RRB W-4P U.S. Railroad Retirement Board 844 North Rush Street Chicago, IL 60611-2092 www.rrb.gov TXB-25 (01-15)

STATE OF VERMONT. Defendant Name V. FINANCIAL AFFIDAVIT (813A) Other: Street Address (if different from Street Address)

Other: Street Address (if different from Street Address)") STATE OF VERMONT SUPERIOR COURT Unit Plaintiff Name DOB FAMILY DIVISION Docket No. Defendant Name DOB V. FINANCIAL AFFIDAVIT (813A) I am: Plaintiff Defendant Other: Name Street Address (if different from

STATE OF VERMONT SUPERIOR COURT Unit Plaintiff Name DOB FAMILY DIVISION Docket No. Defendant Name DOB V. FINANCIAL AFFIDAVIT (813A) I am: Plaintiff Defendant Other: Name Street Address (if different from

Oregon Withholding Tax Formulas

Oregon Withholding Tax Formulas Effective January 1, 2016 To: Oregon employers The Oregon Withholding Tax Formulas include: Things you need to know. Phase-out information for high income employees. Frequently

Oregon Withholding Tax Formulas Effective January 1, 2016 To: Oregon employers The Oregon Withholding Tax Formulas include: Things you need to know. Phase-out information for high income employees. Frequently

GENERAL INSTRUCTIONS FOR COMPLETING YOUR RETURN

GENERAL INSTRUCTIONS FOR COMPLETING YOUR RETURN PITTSBURGH CITY & SCHOOL DISTRICT The City of Pittsburgh Earned Income Tax is levied at the rate of 1% under ACT 511. The Pittsburgh School District Earned

GENERAL INSTRUCTIONS FOR COMPLETING YOUR RETURN PITTSBURGH CITY & SCHOOL DISTRICT The City of Pittsburgh Earned Income Tax is levied at the rate of 1% under ACT 511. The Pittsburgh School District Earned

Individual Retirement Arrangements (IRAs)

") Department of the Treasury Internal Revenue Service Publication 590 Cat. No. 15160x Individual Retirement Arrangements (IRAs) (Including Roth IRAs and Education IRAs) For use in preparing 2000 Returns

Department of the Treasury Internal Revenue Service Publication 590 Cat. No. 15160x Individual Retirement Arrangements (IRAs) (Including Roth IRAs and Education IRAs) For use in preparing 2000 Returns

Oregon Child Support Program Presentation before the 2004 Family Law Conference. October 2004 Child Support For the College Age Child

CSP Oregon Child Support Program Presentation before the 2004 Family Law Conference October 2004 Child Support For the College Age Child Contents Discussion Paper 1 Calculating Support 1 The Child Only

CSP Oregon Child Support Program Presentation before the 2004 Family Law Conference October 2004 Child Support For the College Age Child Contents Discussion Paper 1 Calculating Support 1 The Child Only

Tax Withholding and Estimated Tax

Department of the Treasury Internal Revenue Service Publication 505 Cat. No. 15008E Tax Withholding and Estimated Tax For use in 2013 Get forms and other Information faster and easier by: Internet IRS.gov

Department of the Treasury Internal Revenue Service Publication 505 Cat. No. 15008E Tax Withholding and Estimated Tax For use in 2013 Get forms and other Information faster and easier by: Internet IRS.gov

IN THE COURT OF COMMON PLEAS OF OTTAWA COUNTY, OHIO JUVENILE DIVISION STANDARD CHILD SUPPORT ORDERS

JC-7 IN THE COURT OF COMMON PLEAS OF OTTAWA COUNTY, OHIO JUVENILE DIVISION STANDARD CHILD SUPPORT ORDERS 1. So long as private health insurance is being provided for the minor child(ren) in accordance

JC-7 IN THE COURT OF COMMON PLEAS OF OTTAWA COUNTY, OHIO JUVENILE DIVISION STANDARD CHILD SUPPORT ORDERS 1. So long as private health insurance is being provided for the minor child(ren) in accordance

IT-2105-I. New York State New York City Yonkers MCTMT

Department of Taxation and Finance Instructions for Form IT-2105 Estimated Tax Payment Voucher for Individuals New York State New York City Yonkers MCTMT IT-2105-I Did you know? You can pay your estimated

Department of Taxation and Finance Instructions for Form IT-2105 Estimated Tax Payment Voucher for Individuals New York State New York City Yonkers MCTMT IT-2105-I Did you know? You can pay your estimated

Health Reimbursement Arrangements (HRA) As a Tax Free Employee Benefit

As a Tax Free Employee Benefit") CHILDCARE SOLUTIONS 2101 Richmond Road Beachwood, Ohio 44122 216-831-7333 [email protected] Health Reimbursement Arrangements (HRA) As a Tax Free Employee Benefit Internal Revenue Service Department

CHILDCARE SOLUTIONS 2101 Richmond Road Beachwood, Ohio 44122 216-831-7333 [email protected] Health Reimbursement Arrangements (HRA) As a Tax Free Employee Benefit Internal Revenue Service Department

DEPARTMENT OF HEALTH AND HUMAN SERVICES DIVISION OF WELFARE AND SUPPORTIVE SERVICES CHILD SUPPORT ENFORCEMENT MANUAL CHAPTER V

DEPARTMENT OF HEALTH AND HUMAN SERVICES DIVISION OF WELFARE AND SUPPORTIVE SERVICES CHILD SUPPORT ENFORCEMENT MANUAL CHAPTER V SUPPORT OBLIGATIONS (500) Section 500 MTL 712 1 Oct 12 TABLE OF CONTENTS CHAPTER

DEPARTMENT OF HEALTH AND HUMAN SERVICES DIVISION OF WELFARE AND SUPPORTIVE SERVICES CHILD SUPPORT ENFORCEMENT MANUAL CHAPTER V SUPPORT OBLIGATIONS (500) Section 500 MTL 712 1 Oct 12 TABLE OF CONTENTS CHAPTER

Important Tax Information About Payments From Your TSP Account

Important Tax Information About Payments From Your TSP Account Except as noted below for uniformed services accounts, amounts paid to you from your Thrift Savings Plan (TSP) account are taxable income

Important Tax Information About Payments From Your TSP Account Except as noted below for uniformed services accounts, amounts paid to you from your Thrift Savings Plan (TSP) account are taxable income

Basic Income-Withholding Order Guidelines on Allocation for Multiple Orders for Private Employers

Basic Income-Withholding Order Guidelines on Allocation for Multiple Orders for Private Employers Updated November 2005 Table of Contents BASIC INCOME-WITHHOLDING ORDER GUIDELINES FOR PRIVATE EMPLOYERS

Basic Income-Withholding Order Guidelines on Allocation for Multiple Orders for Private Employers Updated November 2005 Table of Contents BASIC INCOME-WITHHOLDING ORDER GUIDELINES FOR PRIVATE EMPLOYERS

Frequently Asked Questions About Child Support

Frequently Asked Questions About Child Support Rev December 2015 TABLE OF CONTENTS CHAPTER PAGE NUMBER CHILD SUPPORT OVERVIEW...1 Child Support Process.....3 CHAPTER 1: GENERAL INFORMATION.4 Division of

Frequently Asked Questions About Child Support Rev December 2015 TABLE OF CONTENTS CHAPTER PAGE NUMBER CHILD SUPPORT OVERVIEW...1 Child Support Process.....3 CHAPTER 1: GENERAL INFORMATION.4 Division of

Member / Beneficiary Request To Withdraw Contributions / Elect Rollover

Orange County Employees Retirement System 2223 E. Wellington Avenue. Suite 100 Santa Ana, CA 92701 (714) 558-6200 www.ocers.org Member / Beneficiary Request To Withdraw Contributions / Elect Rollover Please

Orange County Employees Retirement System 2223 E. Wellington Avenue. Suite 100 Santa Ana, CA 92701 (714) 558-6200 www.ocers.org Member / Beneficiary Request To Withdraw Contributions / Elect Rollover Please

How Your Retirement Benefits Are Taxed

State of Wisconsin Department of Revenue How Your Retirement Benefits Are Taxed For Use in Preparing 2014 Returns Publication 126 (12/14) Printed on Recycled Paper TABLE OF CONTENTS Page I. Introduction...3

State of Wisconsin Department of Revenue How Your Retirement Benefits Are Taxed For Use in Preparing 2014 Returns Publication 126 (12/14) Printed on Recycled Paper TABLE OF CONTENTS Page I. Introduction...3

IT-2105-I (5/15) New York State New York City Yonkers MCTMT

New York State New York City Yonkers MCTMT") New York State Department of Taxation and Finance Instructions for Form IT-2105 Estimated Tax Payment Voucher for Individuals New York State New York City Yonkers MCTMT IT-2105-I (5/15) Did you know? You

New York State Department of Taxation and Finance Instructions for Form IT-2105 Estimated Tax Payment Voucher for Individuals New York State New York City Yonkers MCTMT IT-2105-I (5/15) Did you know? You