DATE: March 4, 2016 Raymond J. Orlando, Chief Financial Officer FY 2013 School Based Expenditure Report (SBER) Overview

|

|

|

- Stanley Fox

- 8 years ago

- Views:

Transcription

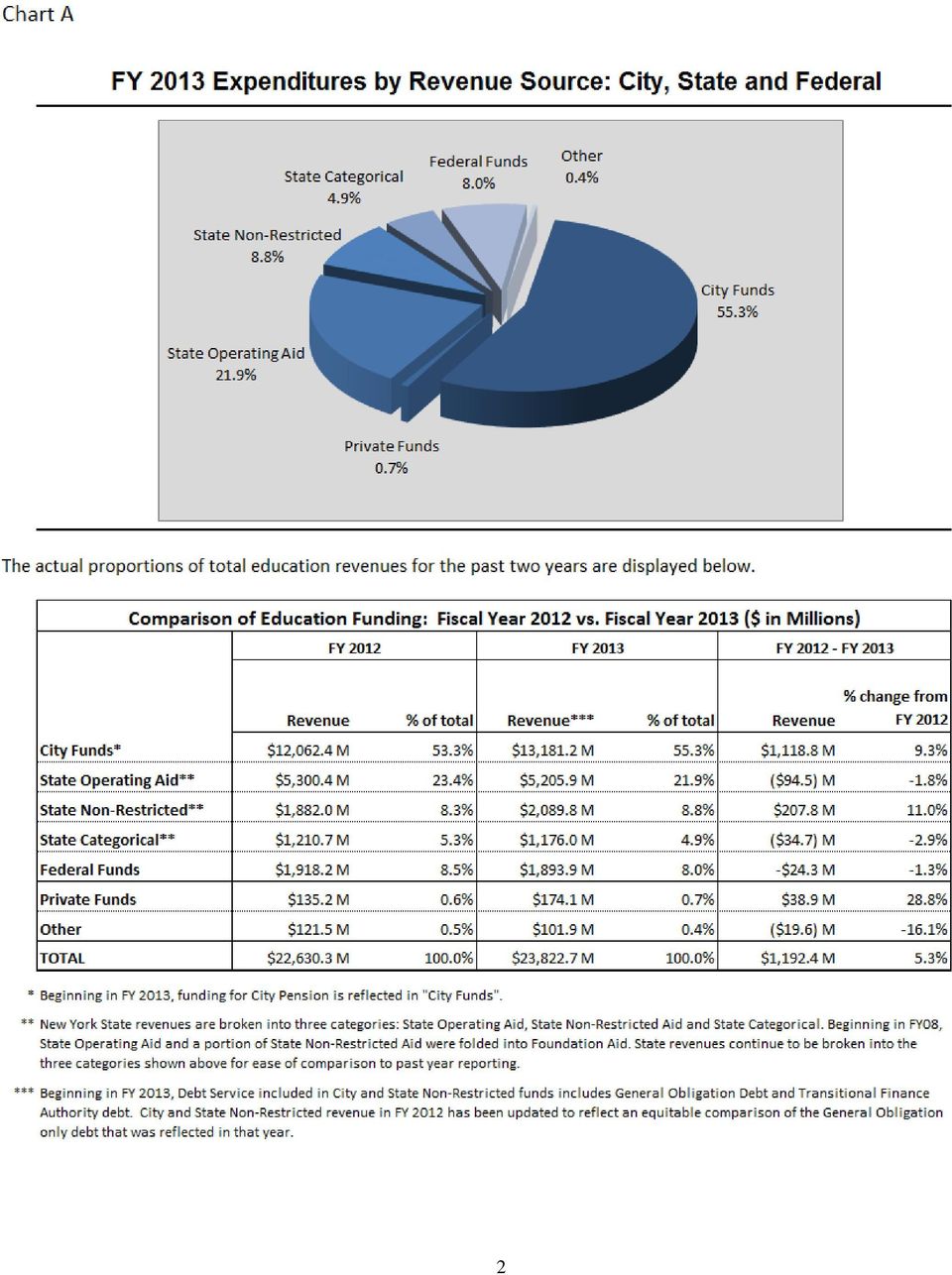

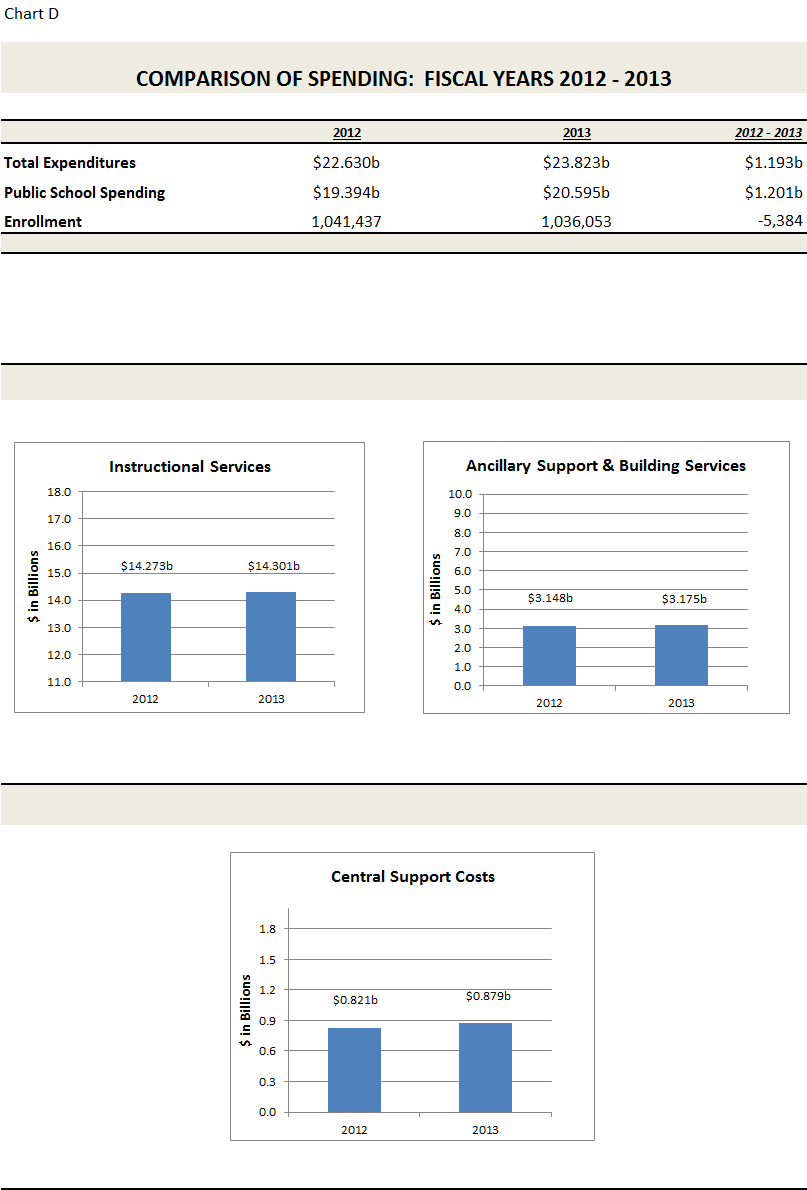

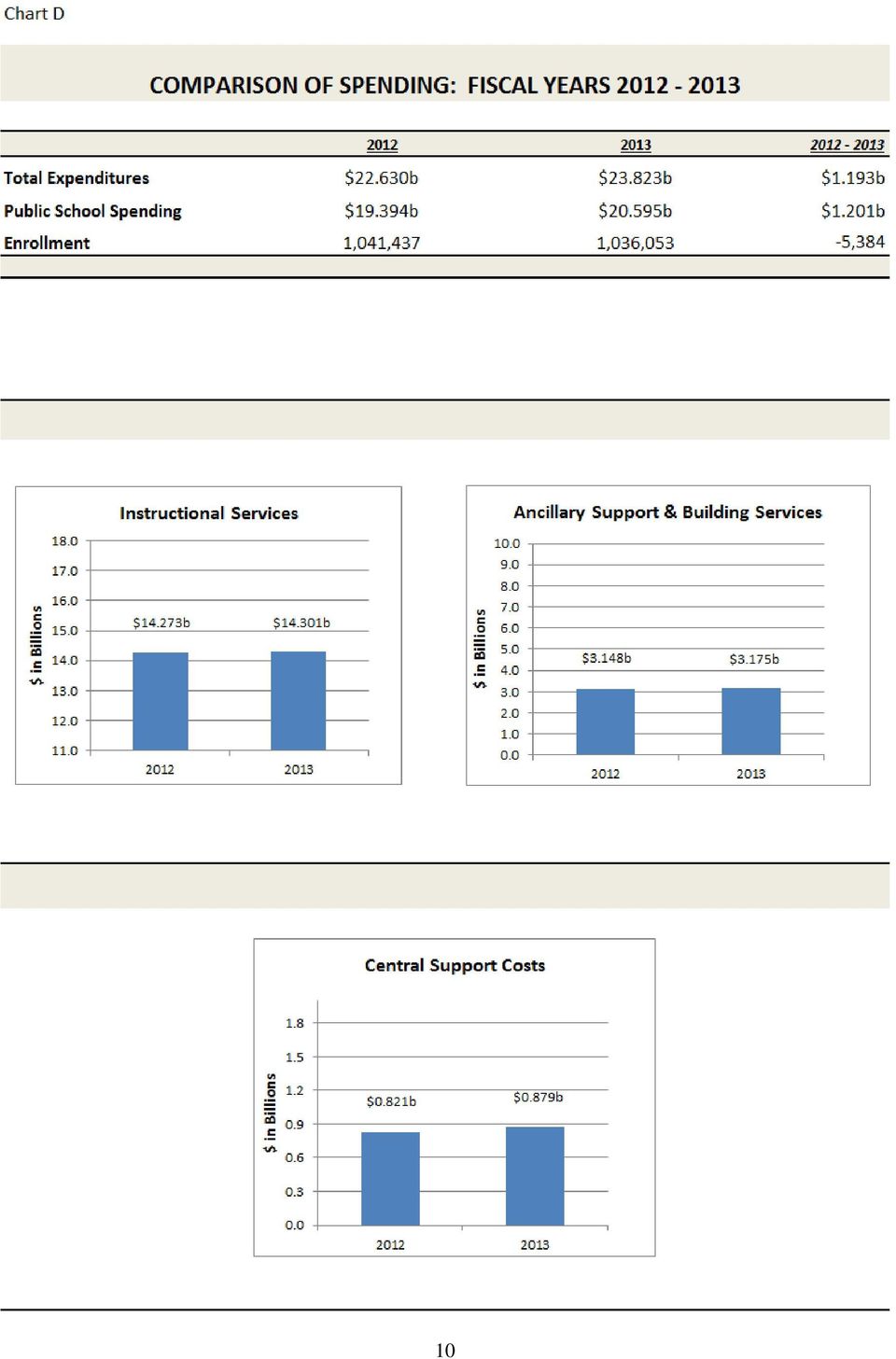

1 Carmen Fariña, Chancellor OFFICE OF THE CHIEF FINANCIAL OFFICER 52 Chambers Street, New York, NY DATE: March 4, 2016 FROM: SUBJECT: Raymond J. Orlando, Chief Financial Officer FY 2013 School Based Expenditure Report (SBER) Overview The FY 2013 School-Based Expenditure Report (SBER) presents fiscal year 2013 (FY 2013) expenditures for the New York City Department of Education (DOE). FY 2013 began on July 1, 2012 and ended on June 30, The financial data used in this report represents the DOE s 2013 year-end audited spending condition. Pupil enrollment data is based on audited school registers as of October 31, This memo contains a summary of FY 2013 SBER data as well as management comments on FY 2013 revenue and spending trends. FY 2013 REVENUE SUMMARY Overall, non-debt revenue sources supporting the DOE, including federal, state, city and private funding, increased by $107.0 million from the prior year. Starting in FY 2013, the funding reflected in the SBER for debt service will now include the DOE s entire debt, including General Obligation Debt adjusted for Pre- Payments, and Transitional Finance Authority debt. FY 2013 will serve as the baseline year for this new methodology. It is expected that using this methodology will more accurately reflect DOE obligations for debt service. Chart A reflects expenditures by FY 2013 source of federal, state, city, and private revenue supporting the DOE (inclusive of debt service and pension contributions): New York City tax levy support increased by $1.1 billion, an increase of 9.3% from FY New York City funding accounted for 55.3% to the DOE s $23.8 billion total. New York State funding increased by $78.6 million, or 0.9%. In FY 2013, aid from New York State accounted for 35.6% of DOE funds, compared to 37.1% in FY Federal funding declined $24.3 million, or 1.3% from FY Federal revenue sources constituted 8.0% of DOE funds. Private funding increased by $38.9 million, or 28.8% from FY In FY 2013, private funds accounted for 0.7% of DOE funds. Funds from other sources, largely capitally-funded pollution remediation costs, decreased by 16.1% from the prior year, and comprised 0.4% of total DOE funds. 1

2 2

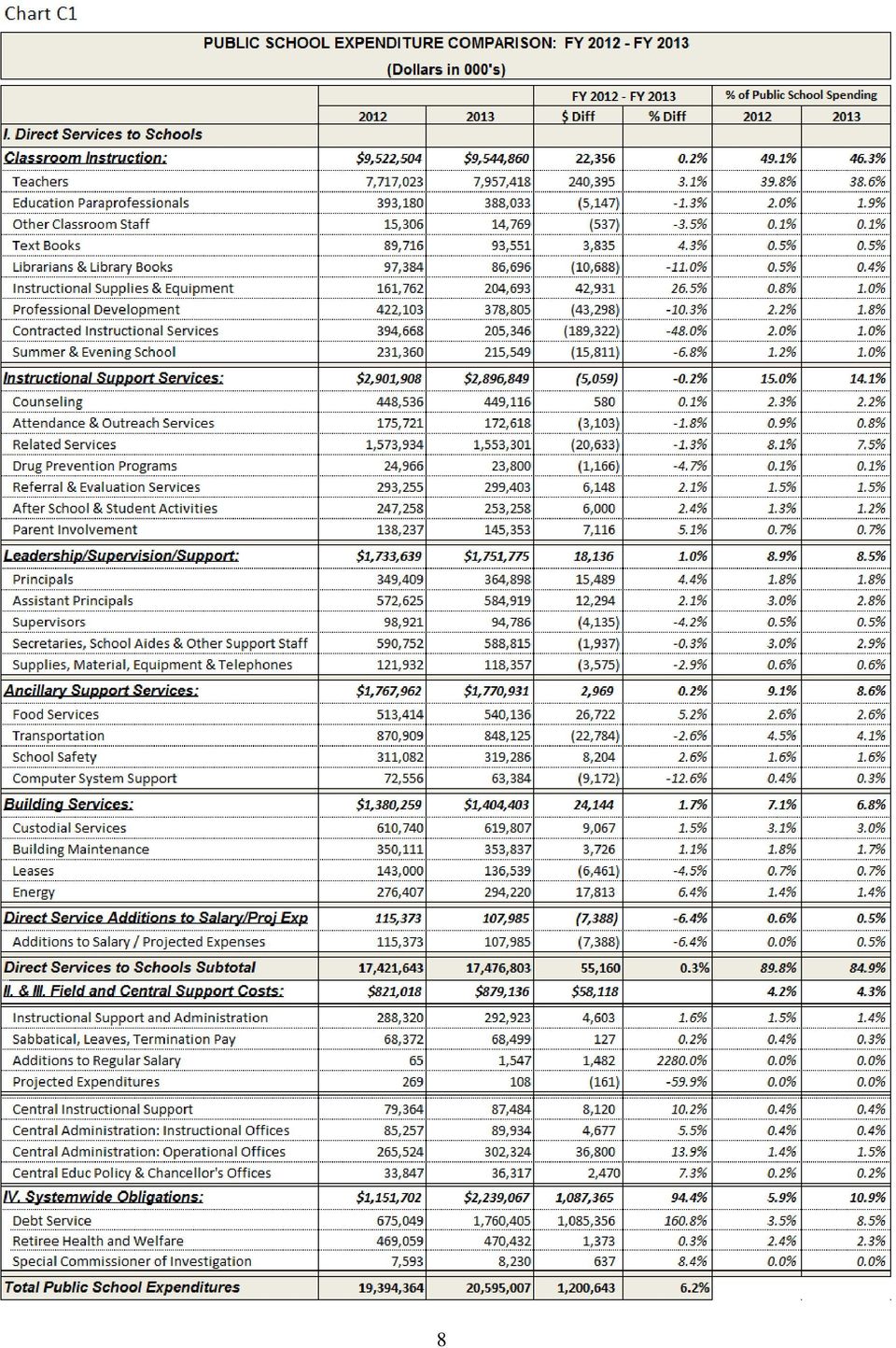

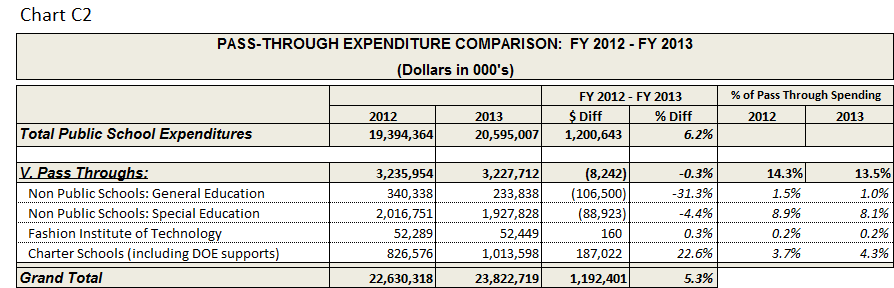

3 SUMMARY OF YEAR-OVER-YEAR SPENDING TRENDS: OVERALL As shown in Chart B, in FY 2013, overall DOE public school spending increased by a total of $1.2 billion. Much of that increase came from the DOE s System-wide Obligations, which increased by approximately $1.1 billion, due primarily to the new methodology for reflecting debt service in the SBER. Beginning in FY 2013, debt service now includes General Obligation Debt adjusted for Pre-Payments, and Transitional Finance Authority debt. Debt is responsible for nearly all of the System-wide Obligations increase. It is expected that using this methodology will more accurately reflect DOE obligations for debt service. Direct Services to Schools increased by $55.2 million and Central Support Costs increased $58.1 million. Pass-Through expenses declined slightly by a total of $8.2 million from FY 2012, but expenses fluctuated within this category. Charter school spending increased by $187.0 million, for example, while spending on services at non-public schools declined by $195.4 million. 3

4 SUMMARY OF YEAR-OVER-YEAR SPENDING TRENDS: BY CATEGORY I. DIRECT SERVICES TO SCHOOLS Direct Services to Schools increased by $55.2 million, or 0.32%, over FY Major contributors to the increased costs in this category were health insurance costs and pension contributions, which grew across all services by 7.6% and 6.0%, respectively a total increase of nearly $300 million. Health insurance growth is primarily determined by changes in contractual health insurance rates as negotiated between the City and the health insurance carriers, while the year-over-year increase in pension contributions is mostly affected by market rate conditions and actuarial valuations of liabilities and assets. The fringe benefit rate growth directly contributed to increases in staff costs, such as for teachers, counseling services, related services, and custodial services. FY 2013 was the first year NYSED received a flexibility waiver of the No Child Left Behind Act of 2001 (NCLB) under an ESEA regulatory initiative. The ESEA waiver was a major contributing factor to spending variances between FY 2012 and FY 2013, as noted where appropriate below. In this year, the mandate to provide Supplemental Educational Services (SES) was lifted. Concurrently, certain schools were newly designated by the state as Priority or Focus schools, and received additional resources. Under the waiver, all schools were released from the Title I mandates to set aside 1) 5% for tuition reimbursement for staff to become highly qualified and 2) 10% of their allocation to support professional development for their staff. This resulted in more flexibility for schools in aligning resources to meet student needs and increase outcomes. While there was overall growth in Direct Service to Schools spending, major changes within the category were in the following areas (refer to Chart C for details): Classroom Instruction increase of $22.4 million or 0.2% Instructional Support Services decrease of $5.1 million or 0.2% Leadership, Supervision and Support increase of $18.1 million or 1.0% Ancillary Support Services increase of $3.0 million or 0.2% Building Services increase of $24.1 million or 1.7% Additions to Salary/Projected Expenses decrease of $7.4 million or 6.4% Classroom Instruction Overall, this functional category increased by $22.4 million. Increases in teacher spending and instructional purchases were offset by decreases in contracted instructional services and professional development. As noted above, the ESEA waiver released schools from mandated professional development set-asides, and replaced the mandated SES programs with flexible Extended Learning Time (ELT) programs, resulting in substantial decreases in these latter two categories. Major changes in spending occurred in the following areas: Teacher spending increased by $240.4 million, or 3.1%, mainly due to increased health insurance and pension costs. Additionally, due to the continued growth of the Autism Spectrum Disorder (ASD) program for students with disabilities, associated costs are now applied to each expense category; 4

5 whereas historically all ASD program funding was captured in related services. As a result, expenditures for teacher services in the ASD program are now reflected under classroom instruction. Instructional Supplies and Equipment purchases increased by $42.9 million. Contributing factors include a limited surplus rollover program, which resulted in schools purchasing additional supplies in the current year, and the reinstatement of the Teachers Choice program, whereby teachers are reimbursed for supply purchases. Contractual Instructional Services and Professional Development experienced decreases, in the amounts of $189.3 million and $43.3 million respectively. This was primarily due to the ending of the mandated Title I SES program under the ESEA waiver. Instructional Support Services In this category, the flexibility under the ESEA waiver enabled schools to better align resources to meet student needs. This was a major driver of over $13.1 million in increased spending for after school programs, student activities, and parent involvement. As noted previously, ASD program costs are now applied to each expense category; whereas historically all program funding was captured in related services. As a result, expenditures for teachers previously captured for the ASD program in related services are now reflected under classroom instruction. Due to growth in the population of students with Instructional Education Plans (IEPs) who require special services, several categories comprising the Instructional Support Services saw increased spending. Attendance & Outreach Services and Drug Prevention Programs declined by $3.1 million and $1.2 million respectively. Leadership, Supervision and Support There was an increase of $18.1 million in expenses from the prior year in the School Leadership, Supervision and Support category. Due to new schools opening, spending for Principals and Assistant Principals combined increased by $27.7 million. This increase was offset by reductions in other areas in this category: Supervisors ($4.1 million), School Aides, Secretaries & Other Support Staff ($2.0 million), and Supplies, Materials, Equipment & Telephones ($3.6 million). Ancillary Support Services Ancillary Support Services, which includes food services, transportation, school safety, and computer system support, increased slightly by $3.0 million. Food Services spending increased by $26.7 million, attributable to new nutritional standards and increased food cost. There was a $22.8 million decrease in Transportation expenditures, primary due to cost savings resulting from rebids of select bus contracts. 5

6 Computer System Support decreased by $9.2 million. Three-year federal Title II Part D (Enhancing Education Through Technology) grants ended in FY 2012, directly contributing to a $5.5 million drop in this category. Additionally, application development and network maintenance costs continued to decline. Building Services Building Services, which includes spending on custodial services, building maintenance, and energy and leases, increased by $24.1 million, or 1.75%, over the previous year. Energy costs increased by $17.8 million, driving most of the increase in this category. Custodial services increased by $9.1 million, directly attributable to the fringe benefit rate increase. Building maintenance rose by $3.7 million, where increased costs following Hurricane Sandy were offset by a decline in pollution remediation outlays. Leasing costs decreased by $6.5 million. Additions to Salary/Projected Expenses In FY 2013, expenditures in this category declined by $7.4 million. This category included technical accounting transactions, e.g. delayed payroll actions, charge-backs and late journal entries that were directly related to technical transactions for alignment between the DOE and the City s accounting systems. II. FIELD SUPPORT COSTS Field Support costs increased by $6.1 million in FY The costs of salary and fringe benefits for staff in this category increased by $12.6 million. A technical adjustment to more accurately capture field support costs in the budgeting tool is reflected in the increase in this category, which is offset by a decrease due to Title II Part D (Enhancing Education Through Technology) grants ending in FY 2012, and declines in other areas. III. SYSTEM-WIDE COSTS Overall system-wide costs, including Central Administration and Central Instructional Support, increased by $52.1 million, or 11.2%, in FY This increase was primarily attributable to increased grant funding for these activities (most notably Race to the Top grants as part of American Recovering and Reinvestment Act funding), Special Education Student Information System (SESIS) support, and costs related to Hurricane Sandy. Race to The Top grants were used to develop and maintain data systems to support instruction and innovation in schools, support standards and assessment, and strengthen teacher and school leader effectiveness. SESIS support expenditures in this category reflected DOE s efforts to maintain a secure webbased system to manage special education cases and information. IV. SYSTEM-WIDE OBLIGATIONS System-wide Obligations increased by $1.1 billion in FY 2013, driven by debt service growth of $1.1 billion. As referenced earlier, beginning in FY 2013, debt will now include General Obligation Debt adjusted for Pre- Payments, and Transitional Finance Authority debt. In additional to this change, it is important to note that year-over-year changes in debt service are not uncommon due to a variety of potential factors, including but not limited to debt restructuring, principal payments, changing interest rates, prepayments, etc. These factors may not only impact total expenditures but also may cause irregularities in payment patterns. 6

7 V. NON-PUBLIC SCHOOLS AND PASS-THROUGHS Spending on non-public schools and other pass-through entities decreased by $8.2 million over the previous year. Carter Case spending declined by $64.3 million, contract school payments declined by $19.6 million, and special education Pre-K tuition fell by $56.6 million. These decreases were offset by an increase in charter school spending of $187.1 million. Twenty-two additional charter schools opened in FY 2013, and grades were added as many charters phased in, leading to substantially increased enrollment. 7

8 8

9 9

10 10

DATE: June 12, 2014 FROM: Raymond J. Orlando, Chief Financial Officer SUBJECT: FY 2012 School Based Expenditure Report (SBER) Overview

Overview") Carmen Fariña, Chancellor OFFICE OF THE CHIEF FINANCIAL OFFICER 52 Chambers Street, New York, NY 10007 DATE: June 12, 2014 FROM: Raymond J. Orlando, Chief Financial Officer SUBJECT: FY 2012 School Based

Carmen Fariña, Chancellor OFFICE OF THE CHIEF FINANCIAL OFFICER 52 Chambers Street, New York, NY 10007 DATE: June 12, 2014 FROM: Raymond J. Orlando, Chief Financial Officer SUBJECT: FY 2012 School Based

FY 2007 Revenue Sources: City, State and Federal

1 FISCAL YEAR 2007 EXPENDITURES This report presents fiscal year 2007 (FY07) expenditures for the New York City Department of Education (NYCDOE). The fiscal year runs from July 1 st through June 30 th.

1 FISCAL YEAR 2007 EXPENDITURES This report presents fiscal year 2007 (FY07) expenditures for the New York City Department of Education (NYCDOE). The fiscal year runs from July 1 st through June 30 th.

Special Education & Student Services

Special Education & Student Services PGCPS Board of Education FY 2016 Approved Annual Operating Budget Page 333 Associate Superintendent for Special Education & Student Services MISSION Mission: To provide

Special Education & Student Services PGCPS Board of Education FY 2016 Approved Annual Operating Budget Page 333 Associate Superintendent for Special Education & Student Services MISSION Mission: To provide

General Fund Expenditures

The general fund is used to report all financial expenditures related to the basic education programs and operations of the school system. Expenditures are grouped into object classes and categories as

The general fund is used to report all financial expenditures related to the basic education programs and operations of the school system. Expenditures are grouped into object classes and categories as

NEW PHILADELPHIA CITY SCHOOLS FIVE-YEAR FORECAST 2013-2017

Real Estate Tax Assumptions NEW PHILADELPHIA CITY SCHOOLS FIVE-YEAR FORECAST 2013-2017 REVENUE ASSUMPTIONS Real estate taxes had increased at approximately 1.1% to 2.0% through 2012 and a 1.5% increase

Real Estate Tax Assumptions NEW PHILADELPHIA CITY SCHOOLS FIVE-YEAR FORECAST 2013-2017 REVENUE ASSUMPTIONS Real estate taxes had increased at approximately 1.1% to 2.0% through 2012 and a 1.5% increase

California Virtual Academy @ San Diego Education Protection Account (EPA) Spending: Plan and Actual Fiscal Year 2013-14

Spending: Plan and Actual Fiscal Year 2013-14") California Virtual Academy @ San Diego Education Protection Account (EPA) Spending: Plan and Actual Fiscal Year 2013-14 Proposition 30, The Schools and Local Public Safety Protection Act of 2012, approved

California Virtual Academy @ San Diego Education Protection Account (EPA) Spending: Plan and Actual Fiscal Year 2013-14 Proposition 30, The Schools and Local Public Safety Protection Act of 2012, approved

VIRGINIA. Description of the Formula

VIRGINIA Description of the Formula The foundation formula is based on pupils in average daily membership (ADM) for the current year. Basic program funding is determined by multiplying total ADM by a per

VIRGINIA Description of the Formula The foundation formula is based on pupils in average daily membership (ADM) for the current year. Basic program funding is determined by multiplying total ADM by a per

A Guide to. NYC Public Schools Budget

A Guide to NYC Public Schools Budget Dear New York City Community Member, With 1.1 million students and over 1,700 schools, the New York City Department of Education (DOE) is the largest school system

A Guide to NYC Public Schools Budget Dear New York City Community Member, With 1.1 million students and over 1,700 schools, the New York City Department of Education (DOE) is the largest school system

Financial Landscape. Oceanside Union Free School District October 14, 2014

Financial Landscape Oceanside Union Free School District October 14, 2014 Topics of Discussion 1.Oceanside s Revenue & Funding Profile 2.Tax Cap 3.State Aid 4.Gap Elimination Adjustment 5.Unfunded Mandates

Financial Landscape Oceanside Union Free School District October 14, 2014 Topics of Discussion 1.Oceanside s Revenue & Funding Profile 2.Tax Cap 3.State Aid 4.Gap Elimination Adjustment 5.Unfunded Mandates

Analysis of Special Education Enrollments and Funding in Pennsylvania Rural and Urban School Districts

Analysis of Special Education Enrollments and Funding in Pennsylvania Rural and Urban School Districts By: William T. Hartman, Ph.D., Pennsylvania State University September 2015 Executive Summary This

Analysis of Special Education Enrollments and Funding in Pennsylvania Rural and Urban School Districts By: William T. Hartman, Ph.D., Pennsylvania State University September 2015 Executive Summary This

3/16/2012 SCHOOL FINANCE SCHOOL FINANCE SCHOOL FINANCE

SCHOOL FINANCE HB 2200 (formerly SB 450 bi-partisan plan) On Senate General Orders $74 base budget per pupil increase 2013 and 2014. Maximum LOB: 31% to 32% in 2013 and 33% in 2014. No mandatory election

SCHOOL FINANCE HB 2200 (formerly SB 450 bi-partisan plan) On Senate General Orders $74 base budget per pupil increase 2013 and 2014. Maximum LOB: 31% to 32% in 2013 and 33% in 2014. No mandatory election

Report on Board and System Administration Expenses. March 4, 2015

Report on Board and System Administration Expenses March 4, 2015 0 Table of Contents Alberta Education coding requirement... 1 Board & System Administration limit... 1 Alberta Education guidelines... 2

Report on Board and System Administration Expenses March 4, 2015 0 Table of Contents Alberta Education coding requirement... 1 Board & System Administration limit... 1 Alberta Education guidelines... 2

District of Columbia Retirement Board. Budget Oversight Hearing. Before the. Council of the District of Columbia Committee of the Whole

District of Columbia Retirement Board Budget Oversight Hearing Before the Council of the District of Columbia Committee of the Whole April 17, 2015 OPENING REMARKS Good afternoon, Chairman Mendelson and

District of Columbia Retirement Board Budget Oversight Hearing Before the Council of the District of Columbia Committee of the Whole April 17, 2015 OPENING REMARKS Good afternoon, Chairman Mendelson and

LEGISLATIVE SERVICES AGENCY OFFICE OF FISCAL AND MANAGEMENT ANALYSIS 301 State House (317) 232-9855

232-9855") LEGISLATIVE SERVICES AGENCY OFFICE OF FISCAL AND MANAGEMENT ANALYSIS 301 State House (317) 232-9855 FISCAL IMPACT STATEMENT LS 7482 DATE PREPARED: Mar 30, 2001 BILL NUMBER: SB 199 BILL AMENDED: Mar 29,

LEGISLATIVE SERVICES AGENCY OFFICE OF FISCAL AND MANAGEMENT ANALYSIS 301 State House (317) 232-9855 FISCAL IMPACT STATEMENT LS 7482 DATE PREPARED: Mar 30, 2001 BILL NUMBER: SB 199 BILL AMENDED: Mar 29,

HOW TO READ A FIVE-YEAR FORECAST. Tips and Explanations on Understanding a School District s Forecast

HOW TO READ A FIVE-YEAR FORECAST Tips and Explanations on Understanding a School District s Forecast INTRODUCTION Recognizing the importance of discussing school district finances, the Ohio Department

HOW TO READ A FIVE-YEAR FORECAST Tips and Explanations on Understanding a School District s Forecast INTRODUCTION Recognizing the importance of discussing school district finances, the Ohio Department

DEPT: EMPLOYEE FRINGE BENEFITS UNIT NO. 1950 FUND: General - 0001. Approximate Tax Levy Cost, Employee & Retiree Fringe Benefits: $138,193,986

BUDGET SUMMARY 2012 Actual 2013 Budget 2014 Budget 2013/2014 Change Health Benefit Expenditures $ 113,308,978 $ 118,502,180 $ 118,676,177 $ 173,997 Pension Related Expenditures 64,388,961 66,724,779 65,198,296

BUDGET SUMMARY 2012 Actual 2013 Budget 2014 Budget 2013/2014 Change Health Benefit Expenditures $ 113,308,978 $ 118,502,180 $ 118,676,177 $ 173,997 Pension Related Expenditures 64,388,961 66,724,779 65,198,296

NEW PHILADELPHIA CITY SCHOOLS FIVE-YEAR FORECAST 2015-2019

Real Estate Tax Assumptions NEW PHILADELPHIA CITY SCHOOLS FIVE-YEAR FORECAST 2015-2019 REVENUE ASSUMPTIONS Real estate taxes had increased at approximately 1.1% to 2.0% through 2013 and a 0.5% increase

Real Estate Tax Assumptions NEW PHILADELPHIA CITY SCHOOLS FIVE-YEAR FORECAST 2015-2019 REVENUE ASSUMPTIONS Real estate taxes had increased at approximately 1.1% to 2.0% through 2013 and a 0.5% increase

ATTACHMENT II: SUMMARY OF GENERAL FUND RECEIPTS

ATTACHMENT II: SUMMARY OF SUMMARY OF GENERAL FUND REVENUE AND TRANSFERS IN Over the Category Percent Change Real Estate Taxes - Current and Delinquent $1,783,844,578 $1,892,239,118 $1,896,564,376 $1,893,919,994

ATTACHMENT II: SUMMARY OF SUMMARY OF GENERAL FUND REVENUE AND TRANSFERS IN Over the Category Percent Change Real Estate Taxes - Current and Delinquent $1,783,844,578 $1,892,239,118 $1,896,564,376 $1,893,919,994

Budget Transparency Reporting: Personnel Expenditures

Personnel Expenditures Public Act 121 of 2009 requires school districts to post on-line certain financial data. This report approximates this format based on districts' Financial Information Database (FID)

Personnel Expenditures Public Act 121 of 2009 requires school districts to post on-line certain financial data. This report approximates this format based on districts' Financial Information Database (FID)

M D R w w w. s c h o o l d a t a. c o m 8 0 0-3 3 3-8 8 0 2

MDR s Guide to Federally Funded Education Programs Major federal programs in the Education Budget for Fiscal Year 2011 are listed below. Twenty-three programs were eliminated from the FY2011 budget, including

MDR s Guide to Federally Funded Education Programs Major federal programs in the Education Budget for Fiscal Year 2011 are listed below. Twenty-three programs were eliminated from the FY2011 budget, including

The Education Dollar. A Look at Spending and Funding Trends

The Education Dollar A Look at Spending and Funding Trends September 2015 Executive Summary This annual study examines school district spending and funding over a ten-year period. The study identifies

The Education Dollar A Look at Spending and Funding Trends September 2015 Executive Summary This annual study examines school district spending and funding over a ten-year period. The study identifies

SCHOOL FUNDING COMPLETE RESOURCE

[Type text] LEGISLATIVE SERVICE COMMISSION SCHOOL FUNDING COMPLETE RESOURCE Updated February 2011 [Type text] TABLE OF CONTENTS INTRODUCTION... 4 STATE OPERATING REVENUE... 8 Adequacy State Model Amount...

[Type text] LEGISLATIVE SERVICE COMMISSION SCHOOL FUNDING COMPLETE RESOURCE Updated February 2011 [Type text] TABLE OF CONTENTS INTRODUCTION... 4 STATE OPERATING REVENUE... 8 Adequacy State Model Amount...

THE SCHOOL BOARD OF BROWARD COUNTY, FLORIDA 2014-15 General Fund Revenue Amendment As of June 30, 2015

2014-15 General Fund Revenue Amendment PREVIOUS INCREASE/ REVISED ESTIMATED REVENUES BUDGET (DECREASE) BUDGET LOCAL SOURCES Ad valorem taxes - Current year $ 875,250,296 (10,548,437) 864,701,859 (A) Interest

2014-15 General Fund Revenue Amendment PREVIOUS INCREASE/ REVISED ESTIMATED REVENUES BUDGET (DECREASE) BUDGET LOCAL SOURCES Ad valorem taxes - Current year $ 875,250,296 (10,548,437) 864,701,859 (A) Interest

INFORMATION TECHNOLOGY

MISSION STATEMENT The Information Technology department provides technology, telecommunications and information systems leadership and strategic planning while ensuring efficient, cost effective implementation

MISSION STATEMENT The Information Technology department provides technology, telecommunications and information systems leadership and strategic planning while ensuring efficient, cost effective implementation

FORT HAYS STATE UNIVERSITY

FORT HAYS STATE UNIVERSITY Actual FY 2014 Agency Est. FY 2015 FY 2015 Agency Req. Agency Req. FY 2017 FY 2017 Operating Expenditures: State General Fund $ 32,656,997 $ 34,036,691 $ 33,988,112 $ 33,921,728

FORT HAYS STATE UNIVERSITY Actual FY 2014 Agency Est. FY 2015 FY 2015 Agency Req. Agency Req. FY 2017 FY 2017 Operating Expenditures: State General Fund $ 32,656,997 $ 34,036,691 $ 33,988,112 $ 33,921,728

BOARD OF EDUCATION OF THE TOWNSHP OF EASTAMPTON SCHOOL DISTRICT COUNTY OF BURLINGTON

BOARD OF EDUCATION OF THE TOWNSHP OF EASTAMPTON SCHOOL DISTRICT COUNTY OF BURLINGTON AUDITOR'S MANAGEMENT REPORT ON ADMINISTRATIVE FINDINGS - FINANCIAL, COMPLIANCE AND PERFORMANCE FOR THE FISCAL YEAR ENDED

BOARD OF EDUCATION OF THE TOWNSHP OF EASTAMPTON SCHOOL DISTRICT COUNTY OF BURLINGTON AUDITOR'S MANAGEMENT REPORT ON ADMINISTRATIVE FINDINGS - FINANCIAL, COMPLIANCE AND PERFORMANCE FOR THE FISCAL YEAR ENDED

NEW YORK. Description of the Formula. District-Based Components

NEW YORK NOTE: The following is a high level summary of the NYS school finance system and not an exhaustive or comprehensive description of every school aid formula used in the State. Description of the

NEW YORK NOTE: The following is a high level summary of the NYS school finance system and not an exhaustive or comprehensive description of every school aid formula used in the State. Description of the

Biennial VA529 Status Report July 2014

VA529 Oversight Report No. 1 Biennial VA529 Status Report July 2014 Profile: Programs Operated by VA529 as of March 31, 2014 CURRENT STATUS PrePAID InVEST CollegeWealth CollegeAmerica* Program type Defined

VA529 Oversight Report No. 1 Biennial VA529 Status Report July 2014 Profile: Programs Operated by VA529 as of March 31, 2014 CURRENT STATUS PrePAID InVEST CollegeWealth CollegeAmerica* Program type Defined

Loudoun County Public Schools Proposed Reorganization Plan May 8, 2015

Loudoun County Public Schools Proposed Reorganization Plan May 8, 2015 In order to sustain and build on the excellence of LCPS schools, the Superintendent has developed a cost-neutral reorganization plan.

Loudoun County Public Schools Proposed Reorganization Plan May 8, 2015 In order to sustain and build on the excellence of LCPS schools, the Superintendent has developed a cost-neutral reorganization plan.

WICKLIFFE BOARD OF EDUCATION 5-Year Financial Plan (SM-7) Assumptions: Fiscal Year 15 January 12, 2015

Assumptions: Fiscal Year 15 January 12, 2015") Exhibit 11 WICKLIFFE BOARD OF EDUCATION 5-Year Financial Plan (SM-7) Assumptions: Fiscal Year 15 January 12, 2015 The Ohio General Assembly enacted House Bill 412 requiring public school systems annually

Exhibit 11 WICKLIFFE BOARD OF EDUCATION 5-Year Financial Plan (SM-7) Assumptions: Fiscal Year 15 January 12, 2015 The Ohio General Assembly enacted House Bill 412 requiring public school systems annually

NEW YORK CITY SCHOOL CONSTRUCTION AUTHORITY A COMPONENT UNIT OF THE CITY OF NEW YORK

NEW YORK CITY SCHOOL CONSTRUCTION AUTHORITY A COMPONENT UNIT OF THE CITY OF NEW YORK Financial Statements (Together with Independent Auditors Report) Years Ended June 30, 2015 and 2014 New York City School

NEW YORK CITY SCHOOL CONSTRUCTION AUTHORITY A COMPONENT UNIT OF THE CITY OF NEW YORK Financial Statements (Together with Independent Auditors Report) Years Ended June 30, 2015 and 2014 New York City School

The NEVADA PLAN For School Finance An Overview

The NEVADA PLAN For School Finance An Overview Fiscal Analysis Division Legislative Counsel Bureau 2013 Legislative Session Nevada Plan for School Finance I. Overview of Public K-12 Education Finance

The NEVADA PLAN For School Finance An Overview Fiscal Analysis Division Legislative Counsel Bureau 2013 Legislative Session Nevada Plan for School Finance I. Overview of Public K-12 Education Finance

Realities: Difficult economic times present us with Structural Deficits that make it increasingly difficult to achieve our goals.

Goal: Maintain BASD assets and programming in support of the Roadmap to Educational Excellence 3.0 and the BASD Goals Realities: Difficult economic times present us with Structural Deficits that make it

Goal: Maintain BASD assets and programming in support of the Roadmap to Educational Excellence 3.0 and the BASD Goals Realities: Difficult economic times present us with Structural Deficits that make it

Operating Budget Data

Q00K00 Criminal Injuries Compensation Board Department of Public Safety and Correctional Services Operating Budget Data ($ in Thousands) FY 14 FY 15 FY 16 FY 15-16 % Change Actual Working Allowance Change

Q00K00 Criminal Injuries Compensation Board Department of Public Safety and Correctional Services Operating Budget Data ($ in Thousands) FY 14 FY 15 FY 16 FY 15-16 % Change Actual Working Allowance Change

Ohio Legislative Service Commission

Ohio Legislative Service Commission Fiscal Note & Local Impact Statement Jason Phillips and other LSC staff Bill: Am. H.B. 555 of the 129th G.A. Date: December 13, 2012 Status: As Enacted Sponsor: Reps.

Ohio Legislative Service Commission Fiscal Note & Local Impact Statement Jason Phillips and other LSC staff Bill: Am. H.B. 555 of the 129th G.A. Date: December 13, 2012 Status: As Enacted Sponsor: Reps.

November 20, 2012. Mr. Charles Maranzano, Superintendent Hopatcong Borough Board of Education PO Box 1029 Hopatcong, NJ 07843. Dear Mr.

November 20, 2012 Mr. Charles Maranzano, Superintendent Hopatcong Borough Board of Education PO Box 1029 Hopatcong, NJ 07843 Dear Mr. Maranzano: The New Jersey Department of Education has completed a review

November 20, 2012 Mr. Charles Maranzano, Superintendent Hopatcong Borough Board of Education PO Box 1029 Hopatcong, NJ 07843 Dear Mr. Maranzano: The New Jersey Department of Education has completed a review

School District Funding - How to Get the Most Money You Want

Funding Pennsylvania Public Schools TM 1 Introduction A recent study by the Pennsylvania School Boards Association determined that many citizens do not understand how Pennsylvania s public schools are

Funding Pennsylvania Public Schools TM 1 Introduction A recent study by the Pennsylvania School Boards Association determined that many citizens do not understand how Pennsylvania s public schools are

Accounting & Financial Management. Presentation available online at: link.charterschoolcorp.org/2015ops

Accounting & Financial Management Presentation available online at: link.charterschoolcorp.org/2015ops Accounting and Financial Management 2015 Post-Approval Training Richard Moreno Executive Director

Accounting & Financial Management Presentation available online at: link.charterschoolcorp.org/2015ops Accounting and Financial Management 2015 Post-Approval Training Richard Moreno Executive Director

I. GENERAL BACKGROUND

KENTUCKY Sheila E. Murray University of Kentucky I. GENERAL BACKGROUND State The watershed event for school finance in Kentucky was the 1989 Kentucky Supreme Court decision, Rose v. Council for Better

KENTUCKY Sheila E. Murray University of Kentucky I. GENERAL BACKGROUND State The watershed event for school finance in Kentucky was the 1989 Kentucky Supreme Court decision, Rose v. Council for Better

Deptford Township Board of Education. Proposed 2013-14 Budget

Deptford Township Board of Education Proposed 2013-14 Budget BUILDING A SCHOOL BUDGET Determine Revenues Estimate Expenditures Determine what is needed to achieve the instructional goals and objectives

Deptford Township Board of Education Proposed 2013-14 Budget BUILDING A SCHOOL BUDGET Determine Revenues Estimate Expenditures Determine what is needed to achieve the instructional goals and objectives

TABLE OF CONTENTS CENTRAL SERVICES FUND

TABLE OF CONTENTS Central Services Fund Overview... 83 Income Summary with Requirements by Department and by Category... 83 Central Services Fund Resources... 84 Central Services Fund Resources Allocation

TABLE OF CONTENTS Central Services Fund Overview... 83 Income Summary with Requirements by Department and by Category... 83 Central Services Fund Resources... 84 Central Services Fund Resources Allocation

WITH REPORTS OF INDEPENDENT AUDITORS

As of and for the Years Ended JUNE 30, 2013 AND JUNE 30, 2014 Financial Statements and Schedule of Expenditures of Federal Awards WITH REPORTS OF INDEPENDENT AUDITORS AUDITED FINANCIAL STATEMENTS Independent

As of and for the Years Ended JUNE 30, 2013 AND JUNE 30, 2014 Financial Statements and Schedule of Expenditures of Federal Awards WITH REPORTS OF INDEPENDENT AUDITORS AUDITED FINANCIAL STATEMENTS Independent

F. Purpose Codes. 5000 Instructional Services. 6000 System-Wide Support Services. 7000 Ancillary Services. 8000 Non-Programmed Charges

F. Purpose Codes Purpose means the reason for which something exists or is used. Purpose includes the activities or actions that are performed to accomplish the objectives of a local school administrative

F. Purpose Codes Purpose means the reason for which something exists or is used. Purpose includes the activities or actions that are performed to accomplish the objectives of a local school administrative

Understanding School Choice in Alachua County: Funding School Choice in Florida

Understanding School Choice in Alachua County: Funding School Choice in Florida Florida has been a leader in developing both public and private school alternative programs to address the challenges of

Understanding School Choice in Alachua County: Funding School Choice in Florida Florida has been a leader in developing both public and private school alternative programs to address the challenges of

STATE SPECIAL EDUCATION FUNDING CHANGES: FY 2014 - FY 2016

STATE SPECIAL EDUCATION FUNDING CHANGES: FY 2014 - FY 2016 Special Education Caseloads Task Force October 15, 2013 Tom Melcher, Director School Finance Division FY 2013 Funding General Education Revenue

STATE SPECIAL EDUCATION FUNDING CHANGES: FY 2014 - FY 2016 Special Education Caseloads Task Force October 15, 2013 Tom Melcher, Director School Finance Division FY 2013 Funding General Education Revenue

Washington, DC D F F D D D F F F C F D F D F F D F F F F D F F C C D OH WI. This chapter compares district and charter

HI F OR F TX C C B DE F F F D F F FL GA MA MO NC C F D F D F D D D C C D OH WI NJ NY Washington, F D F By Larry Maloney Introduction F F F This chapter compares district and charter school revenues in

HI F OR F TX C C B DE F F F D F F FL GA MA MO NC C F D F D F D D D C C D OH WI NJ NY Washington, F D F By Larry Maloney Introduction F F F This chapter compares district and charter school revenues in

GLOSSARY OF TERMS. BUILDING MANAGER Non-certified persons hired by the school district to manage and oversee the operation of a school.

GLOSSARY OF TERMS ACCUMULATIVE ENROLLMENT - The total number of students enrolled in a school year (beginning of the year enrollment plus any students added after that date), this count is used to determine

GLOSSARY OF TERMS ACCUMULATIVE ENROLLMENT - The total number of students enrolled in a school year (beginning of the year enrollment plus any students added after that date), this count is used to determine

*SB0002* S.B. 2 1 PUBLIC EDUCATION BUDGET AMENDMENTS. LEGISLATIVE GENERAL COUNSEL Approved for Filing: V. Ashby 03-07-16 8:49 AM

LEGISLATIVE GENERAL COUNSEL Approved for Filing: V. Ashby 03-07-16 8:49 AM S.B. 2 1 PUBLIC EDUCATION BUDGET AMENDMENTS 2 2016 GENERAL SESSION 3 STATE OF UTAH 4 Chief Sponsor: Lyle W. Hillyard 5 House Sponsor:

LEGISLATIVE GENERAL COUNSEL Approved for Filing: V. Ashby 03-07-16 8:49 AM S.B. 2 1 PUBLIC EDUCATION BUDGET AMENDMENTS 2 2016 GENERAL SESSION 3 STATE OF UTAH 4 Chief Sponsor: Lyle W. Hillyard 5 House Sponsor:

DEPT: EMPLOYEE FRINGE BENEFITS UNIT NO. 1950 FUND: General - 0001

BUDGET SUMMARY 2010 Actual 2011 Budget 2012 Budget 2011/2012 Change Health Benefit Expenditures $ 132,619,138 $ 138,642,087 $ 120,566,786 $ (18,075,301) Pension Related Expenditures 67,972,949 66,872,988

BUDGET SUMMARY 2010 Actual 2011 Budget 2012 Budget 2011/2012 Change Health Benefit Expenditures $ 132,619,138 $ 138,642,087 $ 120,566,786 $ (18,075,301) Pension Related Expenditures 67,972,949 66,872,988

Essential Programs & Services State Calculation for Funding Public Education (ED279):

:") Essential Programs & Services State Calculation for Funding Public Education (ED279): Maine s Funding Formula for Sharing the Costs of PreK-12 Education between State and Local: 1. Determine the EPS Defined

Essential Programs & Services State Calculation for Funding Public Education (ED279): Maine s Funding Formula for Sharing the Costs of PreK-12 Education between State and Local: 1. Determine the EPS Defined

The costs of charter and cyber charter schools. Research and policy implications for Pennsylvania school districts. Updated January 2014

The costs of charter and cyber charter schools Updated January 2014 Research and policy implications for Pennsylvania school districts Education Research & Policy Center 400 Bent Creek Blvd., Mechanicsburg,

The costs of charter and cyber charter schools Updated January 2014 Research and policy implications for Pennsylvania school districts Education Research & Policy Center 400 Bent Creek Blvd., Mechanicsburg,

Anchorage School District Fiscal Year 2002-2003 PROJECTED REVENUES AND EXPENDITURES SUMMARY

PROJECTED REVENUES AND EXPENDITURES SUMMARY Revenues and Fund Balance 2002-2003 2002-2003 Fund Local State Federal Revenues/Sources Expenditures Taxes Other General $ 113,758,901 $ 5,145,650 $ 224,510,449

PROJECTED REVENUES AND EXPENDITURES SUMMARY Revenues and Fund Balance 2002-2003 2002-2003 Fund Local State Federal Revenues/Sources Expenditures Taxes Other General $ 113,758,901 $ 5,145,650 $ 224,510,449

Quarterly Budget Report

City of Chicago Quarterly Report 3rd Quarter Mayor Rahm Emanuel Quarterly Report-3 rd Quarter Content and Purpose This quarterly report presents an overview of the City s operating revenues and expenditures

City of Chicago Quarterly Report 3rd Quarter Mayor Rahm Emanuel Quarterly Report-3 rd Quarter Content and Purpose This quarterly report presents an overview of the City s operating revenues and expenditures

GLCAC, Inc. - Head Start Program HEAD START Proposed Budget 2014/2015

Funded Enrollment: 417 PROGRAM AND BUDGET NARRATIVE Cost for Program Operations: $3,751,804 Cost for Training & Technical Assistance $42,370 T/TA funds are divided equally amongst every employee in our

Funded Enrollment: 417 PROGRAM AND BUDGET NARRATIVE Cost for Program Operations: $3,751,804 Cost for Training & Technical Assistance $42,370 T/TA funds are divided equally amongst every employee in our

Ridgewood Public Schools

Ridgewood Public Schools Summary of FY16 Budget Budget Supports Academics Extra-Curricular Activities Maintenance of Buildings & Grounds /Construction Budget Detail Tax Levy Tax Levy vs Home Assess. Impact

Ridgewood Public Schools Summary of FY16 Budget Budget Supports Academics Extra-Curricular Activities Maintenance of Buildings & Grounds /Construction Budget Detail Tax Levy Tax Levy vs Home Assess. Impact

WELCOME TO WEST LAFAYETTE JR/SR HIGH SCHOOL

WELCOME TO WEST LAFAYETTE JR/SR HIGH SCHOOL FEBRUARY 23, 2009 BUSINESSWEEK AWARD BusinessWeek has named West Lafayette High School as the highest academic performing high school in the State of Indiana

WELCOME TO WEST LAFAYETTE JR/SR HIGH SCHOOL FEBRUARY 23, 2009 BUSINESSWEEK AWARD BusinessWeek has named West Lafayette High School as the highest academic performing high school in the State of Indiana

How To Fund A School District

STATE OF THE SCHOOLS Preparing for FY16 and Beyond Rockbridge County Public Schools Budget Planning FY16 February 2015 Table of Contents Introduction...1 School Board Preparation of the Annual School

STATE OF THE SCHOOLS Preparing for FY16 and Beyond Rockbridge County Public Schools Budget Planning FY16 February 2015 Table of Contents Introduction...1 School Board Preparation of the Annual School

Planning a NCLB Title VA Program ODE April 2007

This document is a companion piece to the Planning a NCLB Title VA Program power point. The NCLB Title VA text and USDE Guidance referencing the items in the power point are listed by page number with

This document is a companion piece to the Planning a NCLB Title VA Program power point. The NCLB Title VA text and USDE Guidance referencing the items in the power point are listed by page number with

Georgia F D F F F F F D D A C F D D F C F F C C D OH WI. This chapter compares district and. charter school revenues statewide, and

B C B FL C F D D D F GA Grade based on % of Actual Funding Disparity F D F OH WI F Grad F D D A C F MA MO Grade based on % of Actual Funding Disparity Georgia D D D F F F By Meagan Batdorff Introduction

B C B FL C F D D D F GA Grade based on % of Actual Funding Disparity F D F OH WI F Grad F D D A C F MA MO Grade based on % of Actual Funding Disparity Georgia D D D F F F By Meagan Batdorff Introduction

Unaudited Actuals Charter Schools Enterprise Fund Expenses by Object

A. REVENUES 1) Revenue Limit Sources 8010-8099 2,430,393.56 3,750,106.00 54.3% 2) Federal Revenue 8100-8299 302,327.54 461,689.25 52.7% 3) Other State Revenue 8300-8599 984,557.86 1,500,453.12 52.4% 4)

A. REVENUES 1) Revenue Limit Sources 8010-8099 2,430,393.56 3,750,106.00 54.3% 2) Federal Revenue 8100-8299 302,327.54 461,689.25 52.7% 3) Other State Revenue 8300-8599 984,557.86 1,500,453.12 52.4% 4)

Working Document Committee of the Whole March 25, 2014

Working Document Committee of the Whole March 25, 2014 Introduction The 5-Year Budget is a working document. It is frequently being fine-tuned to take more details into account and updated as assumptions

Working Document Committee of the Whole March 25, 2014 Introduction The 5-Year Budget is a working document. It is frequently being fine-tuned to take more details into account and updated as assumptions

Province of Newfoundland and Labrador. Public Accounts Volume I Consolidated Summary Financial Statements

Province of Newfoundland and Labrador Public Accounts Volume I Consolidated Summary Financial Statements FOR THE YEAR ENDED MARCH 31, 2011 Province of Newfoundland and Labrador Public Accounts Volume I

Province of Newfoundland and Labrador Public Accounts Volume I Consolidated Summary Financial Statements FOR THE YEAR ENDED MARCH 31, 2011 Province of Newfoundland and Labrador Public Accounts Volume I

STATE OF WEST VIRGINIA PUBLIC SCHOOL SUPPORT PROGRAM EXECUTIVE SUMMARY For the 2000-01 Year

STATE OF WEST VIRGINIA PUBLIC SCHOOL SUPPORT PROGRAM EXECUTIVE SUMMARY For the 2000-01 Year The Public School Support Program is a plan of financial support for the public schools in the State of West

STATE OF WEST VIRGINIA PUBLIC SCHOOL SUPPORT PROGRAM EXECUTIVE SUMMARY For the 2000-01 Year The Public School Support Program is a plan of financial support for the public schools in the State of West

GENERAL FUND AND PUBLIC SAFETY FUND PROJECTION

2015 Charter Township of West Bloomfield Finance Department GENERAL FUND AND PUBLIC SAFETY FUND PROJECTION Fiscal Years Ended December 31, 2015 through 2024 Contents Finance Director s Report 3 Historical

2015 Charter Township of West Bloomfield Finance Department GENERAL FUND AND PUBLIC SAFETY FUND PROJECTION Fiscal Years Ended December 31, 2015 through 2024 Contents Finance Director s Report 3 Historical

CONGRESS OF THE UNITED STATES CONGRESSIONAL BUDGET OFFICE CBO. The Distribution of Household Income and Federal Taxes, 2008 and 2009

CONGRESS OF THE UNITED STATES CONGRESSIONAL BUDGET OFFICE Percent 70 The Distribution of Household Income and Federal Taxes, 2008 and 2009 60 50 Before-Tax Income Federal Taxes Top 1 Percent 40 30 20 81st

CONGRESS OF THE UNITED STATES CONGRESSIONAL BUDGET OFFICE Percent 70 The Distribution of Household Income and Federal Taxes, 2008 and 2009 60 50 Before-Tax Income Federal Taxes Top 1 Percent 40 30 20 81st

PROPOSED FY 2015-16 MINIMUM FOUNDATION PROGRAM FORMULA

PROPOSED FY 2015-16 MINIMUM FOUNDATION PROGRAM FORMULA The FY 2015-16 Minimum Foundation Program (MFP) formula was adopted by the State Board of Elementary and Secondary Education on March 6, 2015. The

PROPOSED FY 2015-16 MINIMUM FOUNDATION PROGRAM FORMULA The FY 2015-16 Minimum Foundation Program (MFP) formula was adopted by the State Board of Elementary and Secondary Education on March 6, 2015. The

Debt Management. Department Description

Department Description Debt Management conducts planning, structuring, and issuance activities for short-term and long-term financing to meet the City's cash flow needs and to provide funds for capital

Department Description Debt Management conducts planning, structuring, and issuance activities for short-term and long-term financing to meet the City's cash flow needs and to provide funds for capital

EASTLAND FAIRFIELD CAREER & TECHNICAL SCHOOLS FRANKLIN COUNTY SINGLE AUDIT

EASTLAND FAIRFIELD CAREER & TECHNICAL SCHOOLS FRANKLIN COUNTY SINGLE AUDIT FOR THE YEAR ENDED JUNE 30, 2014 EASTLAND-FAIRFIELD CAREER AND TECHNICAL SCHOOLS FRANKLIN COUNTY TABLE OF CONTENTS TITLE PAGE

EASTLAND FAIRFIELD CAREER & TECHNICAL SCHOOLS FRANKLIN COUNTY SINGLE AUDIT FOR THE YEAR ENDED JUNE 30, 2014 EASTLAND-FAIRFIELD CAREER AND TECHNICAL SCHOOLS FRANKLIN COUNTY TABLE OF CONTENTS TITLE PAGE

Financial Advisor s Report To Unitarian Universalist Congregations. Dan Brody UUA Financial Advisor

Financial Advisor s Report To Unitarian Universalist Congregations June 2008 Dan Brody UUA Financial Advisor http://www.uua.org/aboutus/governance/officers/financialadvisor/index.shtml dbrody@uua.org The

Financial Advisor s Report To Unitarian Universalist Congregations June 2008 Dan Brody UUA Financial Advisor http://www.uua.org/aboutus/governance/officers/financialadvisor/index.shtml dbrody@uua.org The

Charter School Financial Impact Model

Charter School Financial Impact Model Final Report September 11, 2014 MGT of America, Inc. MGT of America (MGT) was hired in May 2014 by the Board to conduct a review regarding the cost and fiscal impact

Charter School Financial Impact Model Final Report September 11, 2014 MGT of America, Inc. MGT of America (MGT) was hired in May 2014 by the Board to conduct a review regarding the cost and fiscal impact

DEPARTMENT OF EDUCATION CROSS-CUTTING SECTION INTRODUCTION. CFDA No. Program Name Listed as

June 2015 Department of Education Cross-Cutting Section ED DEPARTMENT OF EDUCATION CROSS-CUTTING SECTION INTRODUCTION This section contains compliance requirements that apply to more than one Department

June 2015 Department of Education Cross-Cutting Section ED DEPARTMENT OF EDUCATION CROSS-CUTTING SECTION INTRODUCTION This section contains compliance requirements that apply to more than one Department

Gov. Rec. FY 2015. Agency Req. FY 2016

UNIVERSITY OF KANSAS Actual FY 2014 Agency Est. Agency Req. Agency Req. FY 2017 FY 2017 Operating Expenditures: State General Fund $ 135,402,775 $ 137,384,253 $ 137,168,039 $ 136,930,098 $ 135,932,220

UNIVERSITY OF KANSAS Actual FY 2014 Agency Est. Agency Req. Agency Req. FY 2017 FY 2017 Operating Expenditures: State General Fund $ 135,402,775 $ 137,384,253 $ 137,168,039 $ 136,930,098 $ 135,932,220

Instructions to Auditors

General Instructions to Auditors Annual Financial Statements for Divisional Education Councils (DECs) and District Education Authorities (DEAs), the Commission scolaire francophone, Territoires du Nord-Ouest,

General Instructions to Auditors Annual Financial Statements for Divisional Education Councils (DECs) and District Education Authorities (DEAs), the Commission scolaire francophone, Territoires du Nord-Ouest,

Special Education Cross-Subsidies Fiscal Year 2013. Fiscal Year 2013. Report. To the. Legislature. As required by. Minnesota Statutes,

Special Education Cross-Subsidies Fiscal Year 2013 Fiscal Year 2013 Report To the Legislature As required by Minnesota Statutes, section 127A.065 COMMISSIONER: Special Education Cross-Subsidies Brenda

Special Education Cross-Subsidies Fiscal Year 2013 Fiscal Year 2013 Report To the Legislature As required by Minnesota Statutes, section 127A.065 COMMISSIONER: Special Education Cross-Subsidies Brenda

F I S C A L I M P A C T R E P O R T

Fiscal impact reports (FIRs) are prepared by the Legislative Finance Committee (LFC) for standing finance committees of the NM Legislature. The LFC does not assume responsibility for the accuracy of these

Fiscal impact reports (FIRs) are prepared by the Legislative Finance Committee (LFC) for standing finance committees of the NM Legislature. The LFC does not assume responsibility for the accuracy of these

BUDGET PRESENTATION. The Finance Department is proud to publish and disseminate budget information to the Board of Trustees and to our community.

New Deal Independent School District 401 South Auburn Avenue Post Office Box 280 New Deal, Texas 79350-0280 Steven L. Jerden, CPA, CGMA Chief Financial Officer August 11, 2015 The Honorable Board of Trustees

New Deal Independent School District 401 South Auburn Avenue Post Office Box 280 New Deal, Texas 79350-0280 Steven L. Jerden, CPA, CGMA Chief Financial Officer August 11, 2015 The Honorable Board of Trustees

Pennsylvania Charter Schools:

Education Research & Policy Center Pennsylvania Charter Schools: Charter/Cyber Charter Costs for Pennsylvania School Districts October 2010 ERPC Advisory Committee. Mr. Dale R. Keagy, CPA Retired School

Education Research & Policy Center Pennsylvania Charter Schools: Charter/Cyber Charter Costs for Pennsylvania School Districts October 2010 ERPC Advisory Committee. Mr. Dale R. Keagy, CPA Retired School

BUCKEYE VALLEY LOCAL SCHOOLS, DELAWARE COUNTY NOTES/ASSUMPTIONS TO FIVE-YEAR FORECAST FOR APPROVAL MAY 13, 2014

May 13, 2014 The following assumptions were used in projecting revenue and expenditures for Fiscal Year 2014 through 2018. This is the district s best estimates at this point in time. This forecast is

May 13, 2014 The following assumptions were used in projecting revenue and expenditures for Fiscal Year 2014 through 2018. This is the district s best estimates at this point in time. This forecast is

Operating Budget Data

Q00K00 Criminal Injuries Compensation Board Department of Public Safety and Correctional Services Operating Budget Data ($ in Thousands) FY 15 FY 16 FY 17 FY 16-17 % Change Actual Working Allowance Change

Q00K00 Criminal Injuries Compensation Board Department of Public Safety and Correctional Services Operating Budget Data ($ in Thousands) FY 15 FY 16 FY 17 FY 16-17 % Change Actual Working Allowance Change

Board of Education. Bloomfield Hills Schools Public Hearing Budget Update. June 19, 2014

Board of Education Bloomfield Hills Schools Public Hearing Budget Update June 19, 2014 Property Tax Millage Rates 2014 Tax Year changes 1 2014 Millage Rate Summary Tax Base Purpose # of Mills Non-Homestead

Board of Education Bloomfield Hills Schools Public Hearing Budget Update June 19, 2014 Property Tax Millage Rates 2014 Tax Year changes 1 2014 Millage Rate Summary Tax Base Purpose # of Mills Non-Homestead

Components 127th General Assembly 128th General Assembly

League of Women Voters of Ohio Comparison of the Components of the Education Provisions of Am. Sub. HB 119 (127th General Assembly) and Am. Sub. HB 1 (128th General Assembly) Updated February 2010 Components

League of Women Voters of Ohio Comparison of the Components of the Education Provisions of Am. Sub. HB 119 (127th General Assembly) and Am. Sub. HB 1 (128th General Assembly) Updated February 2010 Components

TENNESSEE STATE BOARD OF EDUCATION

Policy for Local School Systems To establish early childhood education and parent involvement programs of high quality, the State Board of Education adopts the following policy: 1. Subject to the rules,

Policy for Local School Systems To establish early childhood education and parent involvement programs of high quality, the State Board of Education adopts the following policy: 1. Subject to the rules,

Financial Analysis of United States Postal Service Financial Results and 10-K Statement. Fiscal Year 2014

Financial Analysis of United States Postal Service Financial Results and 10-K Statement Fiscal Year 2014 April 1, 2015 Contents Purpose of this Report... 1 Financial Facts at a Glance... 2 Chapter 1.

Financial Analysis of United States Postal Service Financial Results and 10-K Statement Fiscal Year 2014 April 1, 2015 Contents Purpose of this Report... 1 Financial Facts at a Glance... 2 Chapter 1.

MISSOURI. Gerri Ogle Coordinator, School Administrative Services Department of Elementary and Secondary Education I. GENERAL BACKGROUND.

MISSOURI Gerri Ogle Coordinator, School Administrative Services Department of Elementary and Secondary Education I. GENERAL BACKGROUND State The major portion of state funds for elementary and secondary

MISSOURI Gerri Ogle Coordinator, School Administrative Services Department of Elementary and Secondary Education I. GENERAL BACKGROUND State The major portion of state funds for elementary and secondary

2005 SCHOOL FINANCE LEGISLATION Funding and Distribution

2005 SCHOOL FINANCE LEGISLATION Funding and Distribution RESEARCH REPORT # 3-05 Legislative Revenue Office State Capitol Building 900 Court Street NE, H-197 Salem, Oregon 97301 (503) 986-1266 http://www.leg.state.or.us/comm/lro/home.htm

2005 SCHOOL FINANCE LEGISLATION Funding and Distribution RESEARCH REPORT # 3-05 Legislative Revenue Office State Capitol Building 900 Court Street NE, H-197 Salem, Oregon 97301 (503) 986-1266 http://www.leg.state.or.us/comm/lro/home.htm

DEFINITIONS OF IOWA SCHOOL FINANCE TERMS

DEFINITIONS OF IOWA SCHOOL FINANCE TERMS Accounting Accrual year-end reporting required by the Department of Education on the certified annual financial report. A district may be operating on a cash accounting

DEFINITIONS OF IOWA SCHOOL FINANCE TERMS Accounting Accrual year-end reporting required by the Department of Education on the certified annual financial report. A district may be operating on a cash accounting

Special Education Programs, Services, Finances: An Overview from Two Perspectives. Joint Annual Conference November 21-23, 2014 Chicago, Illinois

Special Education Programs, Services, Finances: An Overview from Two Perspectives Joint Annual Conference November 21-23, 2014 Chicago, Illinois Welcome Bruce Martin, Director of Business Services/CSBO,

Special Education Programs, Services, Finances: An Overview from Two Perspectives Joint Annual Conference November 21-23, 2014 Chicago, Illinois Welcome Bruce Martin, Director of Business Services/CSBO,

KANSAS DEPARTMENT FOR AGING AND DISABILITY SERVICES

KANSAS DEPARTMENT FOR AGING AND DISABILITY SERVICES Actual FY 2014 Agency Est. Agency Req. Agency Req. FY 2017 FY 2017 Operating Expenditures: State General Fund $ 561,860,405 $ 618,190,288 $ 632,670,211

KANSAS DEPARTMENT FOR AGING AND DISABILITY SERVICES Actual FY 2014 Agency Est. Agency Req. Agency Req. FY 2017 FY 2017 Operating Expenditures: State General Fund $ 561,860,405 $ 618,190,288 $ 632,670,211

Summary of Total Expenditures...1. Summary of General and Supplemental General Fund Expenditures..2. Instruction Expenditures 3

SOUTH CENTRAL Summary of Total Expenditures...1 Summary of General and Supplemental General Fund Expenditures..2 Instruction Expenditures 3 Sources of Revenue and Proposed Budget for 2005-06 (previously

SOUTH CENTRAL Summary of Total Expenditures...1 Summary of General and Supplemental General Fund Expenditures..2 Instruction Expenditures 3 Sources of Revenue and Proposed Budget for 2005-06 (previously

C98F00 Workers Compensation Commission. ($ in Thousands)

") C98F00 Workers Compensation Commission Operating Budget Data ($ in Thousands) FY 12 FY 13 FY 14 FY 13-14 % Change Actual Working Allowance Change Prior Year Special Fund $13,631 $13,961 $13,984 $23 0.2%

C98F00 Workers Compensation Commission Operating Budget Data ($ in Thousands) FY 12 FY 13 FY 14 FY 13-14 % Change Actual Working Allowance Change Prior Year Special Fund $13,631 $13,961 $13,984 $23 0.2%

Fund 73030 OPEB Trust

Focus Fund 73030,, was created to capture long term investment returns and make progress towards reducing the unfunded actuarial accrued liability under Governmental Accounting Standards Board (GASB) Statement

Focus Fund 73030,, was created to capture long term investment returns and make progress towards reducing the unfunded actuarial accrued liability under Governmental Accounting Standards Board (GASB) Statement

FY 14 Deficiency - Changes in Appropriations (in millions)

") FY 14 Deficiency Funding Sections 41-44 of PA 14-47, the FY 15 Revised Budget, makes various FY 14 appropriation increases and reductions that results in a Transportation Fund increase of $1 million offset

FY 14 Deficiency Funding Sections 41-44 of PA 14-47, the FY 15 Revised Budget, makes various FY 14 appropriation increases and reductions that results in a Transportation Fund increase of $1 million offset

Department of Civil Service

O FFICE OF THE NEW YORK STATE COMPTROLLER DIVISION OF STATE GOVERNMENT ACCOUNTABILITY Department of Civil Service Management of the Health Insurance Fund Balance Report 2009-S-48 Thomas P. DiNapoli Table

O FFICE OF THE NEW YORK STATE COMPTROLLER DIVISION OF STATE GOVERNMENT ACCOUNTABILITY Department of Civil Service Management of the Health Insurance Fund Balance Report 2009-S-48 Thomas P. DiNapoli Table

SCHOOL FINANCE IN COLORADO

SCHOOL FINANCE IN COLORADO Legislative Council Staff State Capitol Building, Room 029 200 East Colfax Avenue Denver, CO 80203 Phone: (303) 866-3521 April 2012 STATE OF COLORADO LEGISLATIVE COUNCIL COLORADO

SCHOOL FINANCE IN COLORADO Legislative Council Staff State Capitol Building, Room 029 200 East Colfax Avenue Denver, CO 80203 Phone: (303) 866-3521 April 2012 STATE OF COLORADO LEGISLATIVE COUNCIL COLORADO

83. Standard 9. Financial Resources. 1. Description. 1.1. Financial stability

83. Standard 9. Financial Resources 1. Description 1.1. Financial stability Bentley University has not reported an operating deficit since it became a not-for-profit organization in 1948. Fiscal year 2012

83. Standard 9. Financial Resources 1. Description 1.1. Financial stability Bentley University has not reported an operating deficit since it became a not-for-profit organization in 1948. Fiscal year 2012

Be it enacted by the People of the State of Illinois,

AN ACT concerning education. Be it enacted by the People of the State of Illinois, represented in the General Assembly: Section 1. This amendatory Act may be referred to as the Performance Evaluation Reform

AN ACT concerning education. Be it enacted by the People of the State of Illinois, represented in the General Assembly: Section 1. This amendatory Act may be referred to as the Performance Evaluation Reform

OREGON HEALTH INSURANCE EXCHANGE CORPORATION

OREGON HEALTH INSURANCE EXCHANGE CORPORATION FINANCIAL STATEMENTS and COMPLIANCE REPORTING for the fiscal years ended December 31, 2014 and 2013 Table of Contents Page FINANCIAL SECTION: INDEPENDENT AUDITOR

OREGON HEALTH INSURANCE EXCHANGE CORPORATION FINANCIAL STATEMENTS and COMPLIANCE REPORTING for the fiscal years ended December 31, 2014 and 2013 Table of Contents Page FINANCIAL SECTION: INDEPENDENT AUDITOR

PFMA CHECKLIST FOR PUBLIC ENTITIES CORPORATE MANAGEMENT

PFMA CHECKLIST FOR PUBLIC ENTITIES CORPORATE MANAGEMENT NO. SECTION DESCRIPTION ACTION YES NO N/A COMMENTS 1. 49 Accounting Authority In terms of section 49(3) the relevant treasury, in exceptional circumstances,

PFMA CHECKLIST FOR PUBLIC ENTITIES CORPORATE MANAGEMENT NO. SECTION DESCRIPTION ACTION YES NO N/A COMMENTS 1. 49 Accounting Authority In terms of section 49(3) the relevant treasury, in exceptional circumstances,

Financial Accounting for Student Transportation Services Cost, Allocation Methods and Salary and Fringe Benefit Limitations

Financial Accounting for Student Transportation Services Cost, Allocation Methods and Salary and Fringe Benefit Limitations June 2014 Division of School Finance Pupil Transportation 1500 Highway 36 West

Financial Accounting for Student Transportation Services Cost, Allocation Methods and Salary and Fringe Benefit Limitations June 2014 Division of School Finance Pupil Transportation 1500 Highway 36 West

Massachusetts Department of Revenue. Briefing Book FY2015 Consensus Revenue Estimate Hearing. December 11, 2013. Presented by: Amy Pitter COMMISSIONER

Massachusetts Department of Revenue Briefing Book FY2015 Consensus Revenue Estimate Hearing December 11, 2013 Presented by: Amy Pitter COMMISSIONER Kazim P. Ozyurt DIRECTOR OFFICE OF TAX POLICY ANALYSIS

Massachusetts Department of Revenue Briefing Book FY2015 Consensus Revenue Estimate Hearing December 11, 2013 Presented by: Amy Pitter COMMISSIONER Kazim P. Ozyurt DIRECTOR OFFICE OF TAX POLICY ANALYSIS