Fundamentals of Preparing a Tax Return for Associations. John M. Barbery, CPA Barbery & Associates, CPA, Inc.

|

|

|

- Homer Douglas

- 8 years ago

- Views:

Transcription

1 Fundamentals of Preparing a Tax Return for Associations John M. Barbery, CPA Barbery & Associates, CPA, Inc.

2 Forms 1120H Entity taxed under Section 528. Tax rate is flat 30% (32% for timeshares). Must be filed timely. Election to file is binding (1120-A) Entity taxed under Section 277. Uses corporate tax rate schedule. 990 A few HOA s as defined by Sec 501(c) may qualify as tax exempt and may file Form 990 Types of Associations Condominium Management Associations built as homes for individuals Residential Real Estate Management Associations built as homes for individuals Timeshare Associations members hold rights to use or ownership interests in real property

3 Section 528 Allows filing of Form 1120H, provided specific requirements are met. Income and expenses are classified as either exempt or non-exempt Flat tax rate of 30% or 32% if timeshare Requirements for Section 528 Substantially Residential Test at least 85% of units must be used as residences. (85% of sq. ft for condos; 85% of lots zoned residential for HOA s) 60% Income Test 60% of gross income must consist of exempt function income 90% Expenditure Test 90% of expenses must be qualifying expenses Lack of Private Benefit No member may profit from net earnings

60% Income Test 60% of gross income must consist of exempt function income 90%")

4 Exempt v. Non-Exempt Function Income Exempt Function Income Must pass four tests to qualify as exempt: Source Test Amounts received must be for membership assessments from owners of residential units. Nature Test Amounts paid must be based solely on their membership in the association. Should be ratable. Purpose Test Amounts received must be for qualified purposes. Gross Income Test Tax exempt interest, excess assessments that are refunded or applied against future years and capital assessment are not included in gross income when computing the 60% test. Non-Exempt Function Income Revenue from non-association property Non-member s use of association property Amounts charged to association members for specific services (unless fees are charged ratably to all unit owners): Guest Fees Pool Passes Parking Fees Exempt Function Expenses v. Non-Exempt Expenses Exempt: Expenditures for activities provided to or on behalf of the association members. Non-Exempt Expenses directly incurred for the production of non-exempt income. Administrative expenses can be allocated however cannot exceed 10% or the 90% test will fail.

5 Section 277 Requires filing of Form 1120 or 1120-A Categorizes income and expenses into membership and non-membership. NOL losses generated on nonmembership activities follow Section 172 NOL rules. Membership v. Non-Membership Income Membership Income Income received by an association in their capacity as association members as opposed to customers in receipt of goods/services. Non-Membership Income Revenue derived from the following: Non-association property Non-members use of association property Amounts charged to association members for specific services

6 Membership v. Non-Membership Expenses Membership Expenses Expenses incurred for the benefit of the association Non-Membership Expenses Expenses directly incurred for the production of nonmember income and an allocation of administrative expenses. Revenue Ruling Election made on the tax return to carry over excess contributions from members to the following tax year without including that amount as taxable income. Election should be made by the members prior to filing the tax return. Not necessary to specify the amount of the election.

7 Capital Contributions Generally, replacement funds, capital improvement assessments, litigation and insurance proceeds. There are seven factors which determine whether a contribution is capital in nature: 1. Purpose of the assessment must be capital in nature 2. Must be advanced notice 3. Must be accounted for as a capital contribution 4. Must be held for the purpose only 5. Must be held in a separate bank account 6. Must be expended eventually for that purpose 7. Must increase the capital account of the unit owner IRC 118 and IRC 263 IRC 118: all contributions to capital are excluded from income IRC 263: No deduction can be taken for capital expenditures. Painting is not considered capital Intention and purpose are determining factors of whether an item is capital in nature.

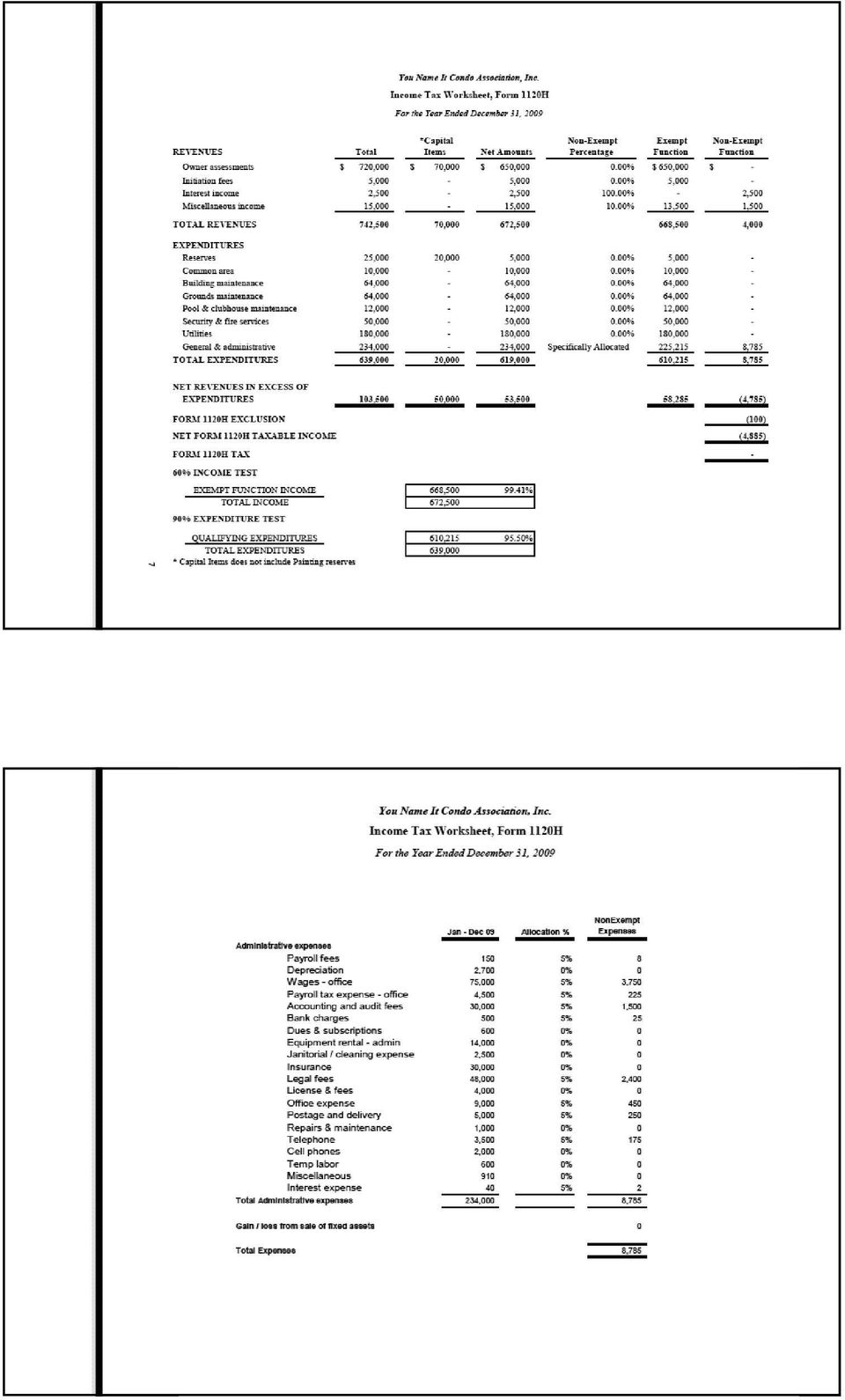

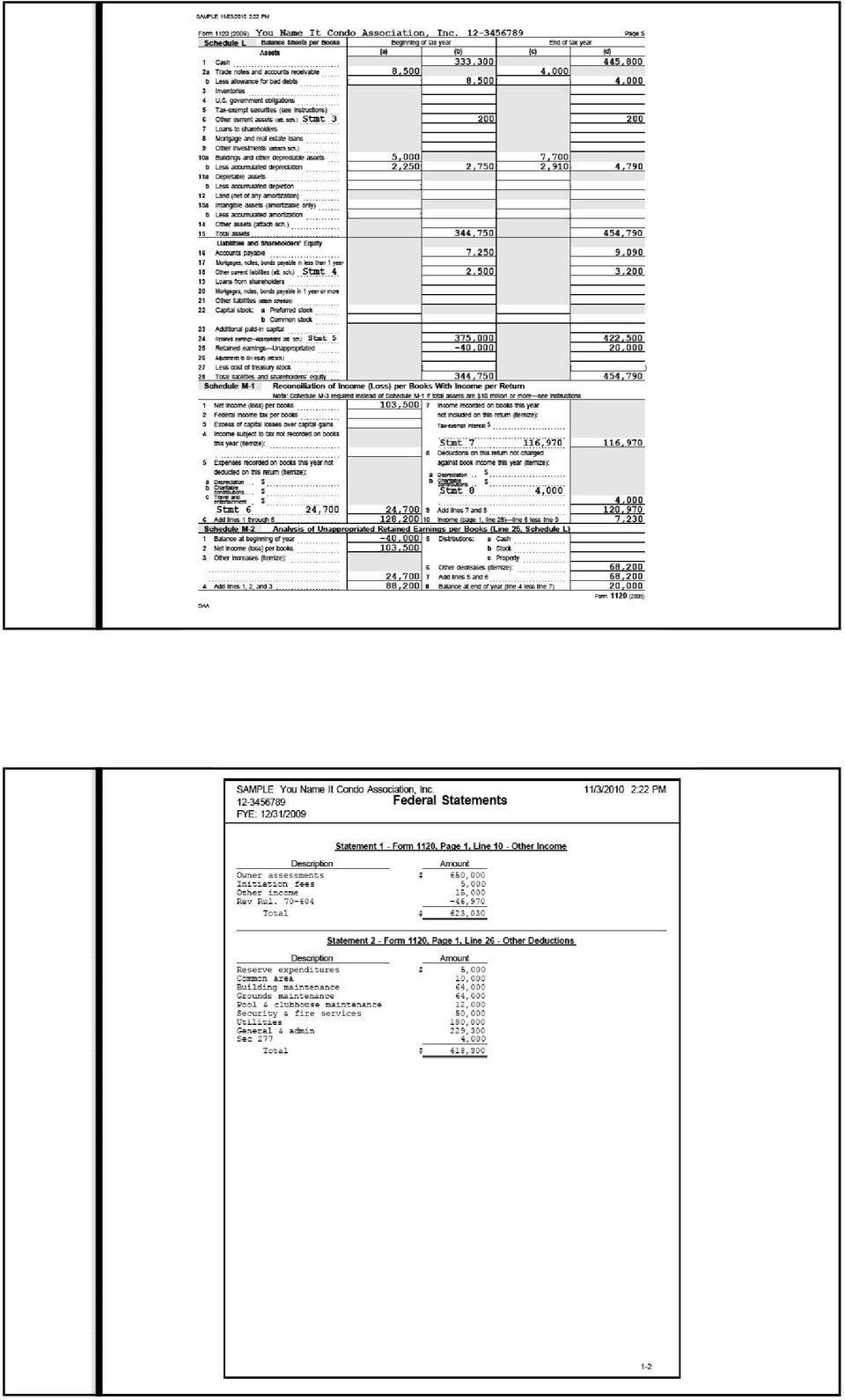

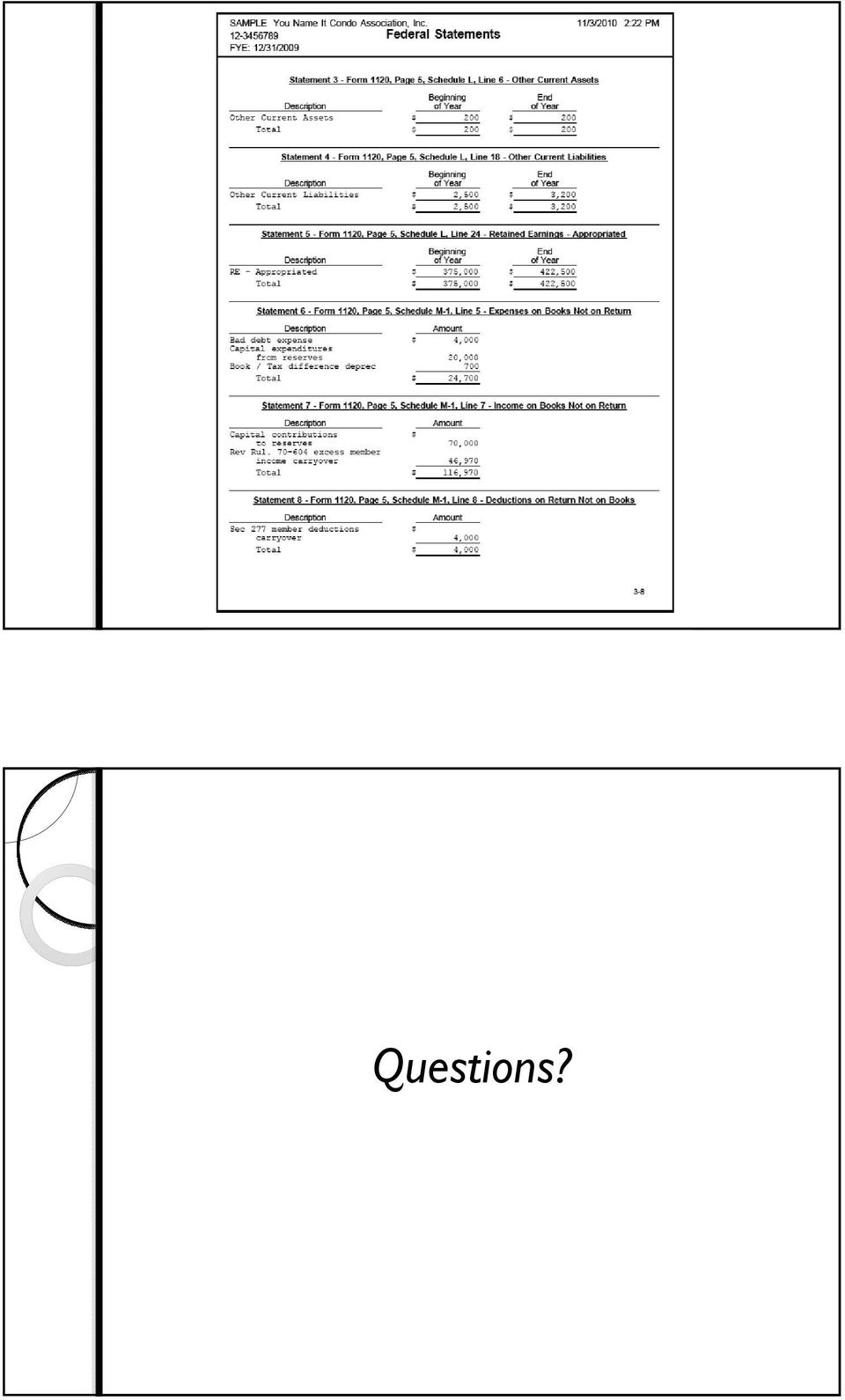

8 You Name It Condo Association, Inc. Example Tax Return and Work Papers

9

10

11

12

13 Questions?

CIRA Tax Principles. Agenda. Code and Case References for Condo and HOA Taxation. John Barbery, CPA, MST Mark Brechbill, CPA

CIRA Tax Principles Code and Case References for Condo and HOA Taxation John Barbery, CPA, MST Mark Brechbill, CPA Agenda Understanding the Basics Common CIRA tax principles Form 1120-H issues (Section

CIRA Tax Principles Code and Case References for Condo and HOA Taxation John Barbery, CPA, MST Mark Brechbill, CPA Agenda Understanding the Basics Common CIRA tax principles Form 1120-H issues (Section

CHAPTER VIII CONSUMPTION TAX. General

CHAPTER VIII CONSUMPTION TAX General Taxable Items General Transactions subject to Consumption Tax Criteria for Classification of Domestic and Overseas Transactions a. b. c. Non-taxable Transactions

CHAPTER VIII CONSUMPTION TAX General Taxable Items General Transactions subject to Consumption Tax Criteria for Classification of Domestic and Overseas Transactions a. b. c. Non-taxable Transactions

Full Condo Questionnaire

Full Condo Questionnaire Project Name: Project Address: City: State: Zip: HOA Contact: Loan must have a Gateway Mortgage Group loan number for CPM review. Clients that have a FNMA Seller/Servicer Number

Full Condo Questionnaire Project Name: Project Address: City: State: Zip: HOA Contact: Loan must have a Gateway Mortgage Group loan number for CPM review. Clients that have a FNMA Seller/Servicer Number

Fannie Mae Lender Full Review Condominium Questionnaire for Established Projects. 1. Project Name: 2. Name of Association:

Fannie Mae Lender Full Review Condominium Questionnaire for Established Projects 1. Project Name: 2. Name of Association: 3. Property address of Project (not condo unit being mortgaged): 4. What was the

Fannie Mae Lender Full Review Condominium Questionnaire for Established Projects 1. Project Name: 2. Name of Association: 3. Property address of Project (not condo unit being mortgaged): 4. What was the

"This document may not be used or cited as precedent. Section 6110(j)(3) of the Internal Revenue Code."

(3) of the Internal Revenue Code.") PRIVATE RULING 9131023 "This document may not be used or cited as precedent. Section 6110(j)(3) of the Internal Revenue Code." Dear * * * This is in reply to a letter dated October 30, 1990, and subsequent

PRIVATE RULING 9131023 "This document may not be used or cited as precedent. Section 6110(j)(3) of the Internal Revenue Code." Dear * * * This is in reply to a letter dated October 30, 1990, and subsequent

Chapter 32a Medical Care Savings Account Act

Chapter 32a Medical Care Savings Account Act 31A-32a-101 Title and scope. (1) This chapter is known as the "Medical Care Savings Account Act." (a) This chapter applies only to a medical care savings account

Chapter 32a Medical Care Savings Account Act 31A-32a-101 Title and scope. (1) This chapter is known as the "Medical Care Savings Account Act." (a) This chapter applies only to a medical care savings account

Financing Incentives March 5, 2009

Change picture on Slide Master Financing Incentives March 5, 2009 PRESENTED BY Robert A. Friedman Troutman Sanders LLP The Chrysler Building 405 Lexington Ave New York, NY 10174 (212) 704-6000 www.troutmansanders.com

Change picture on Slide Master Financing Incentives March 5, 2009 PRESENTED BY Robert A. Friedman Troutman Sanders LLP The Chrysler Building 405 Lexington Ave New York, NY 10174 (212) 704-6000 www.troutmansanders.com

FREDDIE MAC CONDO-PUD MATRIX Consult the Client Guide for complete condominium eligibility details

FREDDIE MAC CONDO-PUD MATRIX Consult the Client Guide for complete condominium eligibility details PROJECT CLASSIFICATION PROJECT TYPE ELIGIBILITY/LEGAL/DOCUMENTATION INSURANCE PUD PROJECTS ESTABLISHED

FREDDIE MAC CONDO-PUD MATRIX Consult the Client Guide for complete condominium eligibility details PROJECT CLASSIFICATION PROJECT TYPE ELIGIBILITY/LEGAL/DOCUMENTATION INSURANCE PUD PROJECTS ESTABLISHED

L. IRC 501(c)(15) - SMALL INSURANCE COMPANIES OR ASSOCIATIONS

(15) - SMALL INSURANCE COMPANIES OR ASSOCIATIONS") L. IRC 501(c)(15) - SMALL INSURANCE COMPANIES OR ASSOCIATIONS 1. Introduction The purpose of this section is to provide some background and an update in the area of IRC 501(c)(15) insurance companies or

L. IRC 501(c)(15) - SMALL INSURANCE COMPANIES OR ASSOCIATIONS 1. Introduction The purpose of this section is to provide some background and an update in the area of IRC 501(c)(15) insurance companies or

Ministry Of Finance VAT Department. VAT Guidance for Land and Property Version 4: November 1, 2015

Ministry Of Finance VAT Department VAT Guidance for Land and Property Version 4: November 1, 2015 Introduction This guide is intended to provide businesses supplying land and property within The Bahamas

Ministry Of Finance VAT Department VAT Guidance for Land and Property Version 4: November 1, 2015 Introduction This guide is intended to provide businesses supplying land and property within The Bahamas

Internal Revenue Service Number: 200439017 Release Date: 9/24/04 0061.28-03, 0061.29-00, 0277.00-00

Internal Revenue Service Number: 200439017 Release Date: 9/24/04 0061.28-03, 0061.29-00, 0277.00-00 -------------------------- --------------------------------------------- ----------------------------------

Internal Revenue Service Number: 200439017 Release Date: 9/24/04 0061.28-03, 0061.29-00, 0277.00-00 -------------------------- --------------------------------------------- ----------------------------------

State of Wisconsin Department of Revenue Limited Liability Companies (LLCs)

") State of Wisconsin Department of Revenue Limited Liability Companies (LLCs) Publication 119 (2/15) Table of Contents 2 Page I. INTRODUCTION... 4 II. DEFINITIONS APPLICABLE TO LLCS... 4 III. FORMATION OF

State of Wisconsin Department of Revenue Limited Liability Companies (LLCs) Publication 119 (2/15) Table of Contents 2 Page I. INTRODUCTION... 4 II. DEFINITIONS APPLICABLE TO LLCS... 4 III. FORMATION OF

General Information. Nonresident Step-by-Step Instructions

Illinois Department of Revenue Schedule NR IL-1040 Instructions 2014 General Information What is the purpose of Schedule NR? Schedule NR, Nonresident and Part-Year Resident Computation of Illinois Tax,

Illinois Department of Revenue Schedule NR IL-1040 Instructions 2014 General Information What is the purpose of Schedule NR? Schedule NR, Nonresident and Part-Year Resident Computation of Illinois Tax,

Presentation of Income and Deductions

TAXATION OF S CORPORATIONS Accounting 551T - Lecture 8 Schlesinger: Chapters 6-8 Robert A. Scharlach Presentation of Income and Deductions Two Categories Separately stated items Non-separately stated items

TAXATION OF S CORPORATIONS Accounting 551T - Lecture 8 Schlesinger: Chapters 6-8 Robert A. Scharlach Presentation of Income and Deductions Two Categories Separately stated items Non-separately stated items

Weidner & Associates, P.C.

Weidner & Associates, P.C. Certified Public Accountants 3002 South Oak Way Lakewood, CO 80227 MEMBER The Board of Directors and Members July 31, 2012 The Newport Place Condominiums Association, Inc. C/O

Weidner & Associates, P.C. Certified Public Accountants 3002 South Oak Way Lakewood, CO 80227 MEMBER The Board of Directors and Members July 31, 2012 The Newport Place Condominiums Association, Inc. C/O

ADMINISTRATIVE RELEASE. Maryland Income Tax. Administrative Release No. 6. Subject: Taxation of Pass-through Entities Having Nonresident Members.

Maryland Income Tax ADMINISTRATIVE RELEASE Administrative Release No. 6 Subject: Taxation of Pass-through Entities Having Nonresident Members. I. General Under 10-401 of the Tax-General Article, Annotated

Maryland Income Tax ADMINISTRATIVE RELEASE Administrative Release No. 6 Subject: Taxation of Pass-through Entities Having Nonresident Members. I. General Under 10-401 of the Tax-General Article, Annotated

26 CFR 601.105: Examination of returns and claims for refund, credit or abatement; determination of correct tax liability. (Also Part I, 172, 6411)

") Part III Administrative, Procedural, and Miscellaneous 26 CFR 601.105: Examination of returns and claims for refund, credit or abatement; determination of correct tax liability. (Also Part I, 172, 6411)

Part III Administrative, Procedural, and Miscellaneous 26 CFR 601.105: Examination of returns and claims for refund, credit or abatement; determination of correct tax liability. (Also Part I, 172, 6411)

San Francisco Business Tax Reform: Summary of Gross Receipts Tax Legislation Introduced on June 12, 2012

San Francisco Business Tax Reform: Summary of Gross Receipts Tax Legislation Introduced on June 12, 2012 Ben Rosenfield, Controller Ted Egan, Chief Economist Background At the request of the Mayor and

San Francisco Business Tax Reform: Summary of Gross Receipts Tax Legislation Introduced on June 12, 2012 Ben Rosenfield, Controller Ted Egan, Chief Economist Background At the request of the Mayor and

M. PUBLICLY SUPPORTED ORGANIZATIONS

M. PUBLICLY SUPPORTED ORGANIZATIONS The term "publicly supported organizations" generally refers to organizations described in IRC 170(b)(1)(A)(vi) and 509(a)(2). The purpose of this paper is to discuss

M. PUBLICLY SUPPORTED ORGANIZATIONS The term "publicly supported organizations" generally refers to organizations described in IRC 170(b)(1)(A)(vi) and 509(a)(2). The purpose of this paper is to discuss

Arizona Rentals & Concierge Services, LLC. Property Management Agreement

Arizona Rentals & Concierge Services, LLC ADRE License Number SE515963000 14245 W. Grand Ave. Suite #2 Surprise AZ. 85374 623-209-1656 WWW.arizonarentalservice.com mgt@arizonarentalservice.com Property

Arizona Rentals & Concierge Services, LLC ADRE License Number SE515963000 14245 W. Grand Ave. Suite #2 Surprise AZ. 85374 623-209-1656 WWW.arizonarentalservice.com mgt@arizonarentalservice.com Property

Restricted Stock Plans

Restricted Stock Plans Key Employee Incentives Some S and C Corporation Considerations Michael A. Coffey Lisa J. Tilley, CPA P.O. Box 12025 Roanoke, VA 24022-2025 Phone: (540) 345-4190 1-800-358-2116 Fax:

Restricted Stock Plans Key Employee Incentives Some S and C Corporation Considerations Michael A. Coffey Lisa J. Tilley, CPA P.O. Box 12025 Roanoke, VA 24022-2025 Phone: (540) 345-4190 1-800-358-2116 Fax:

Instructions for Completing Wisconsin Schedule I 2014

NOTE An individual who elects to claim a different amount of Internal Revenue Code sec. 179 expense deduction for Wisconsin than for federal tax purpose may use Schedule I to report that election. For

NOTE An individual who elects to claim a different amount of Internal Revenue Code sec. 179 expense deduction for Wisconsin than for federal tax purpose may use Schedule I to report that election. For

California. Franchise Tax Board. Forms & Instructions 100

California Forms & Instructions 100 2013 Corporation Tax Booklet Members of the Franchise Tax Board John Chiang, Chair Jerome E. Horton, Member Michael Cohen, Member For more information regarding business

California Forms & Instructions 100 2013 Corporation Tax Booklet Members of the Franchise Tax Board John Chiang, Chair Jerome E. Horton, Member Michael Cohen, Member For more information regarding business

City and County of San Francisco Office of the Treasurer & Tax Collector

City and County of San Francisco Office of the Treasurer & Tax Collector Gross Receipts Tax & Payroll Expense Tax Online Filing Instructions Tax Year 2014 R e v i s e d 12/19/2014 Table of Contents A Guide

City and County of San Francisco Office of the Treasurer & Tax Collector Gross Receipts Tax & Payroll Expense Tax Online Filing Instructions Tax Year 2014 R e v i s e d 12/19/2014 Table of Contents A Guide

City and County of San Francisco Office of the Treasurer & Tax Collector

City and County of San Francisco Office of the Treasurer & Tax Collector Gross Receipts Tax & Payroll Expense Tax Online Filing Instructions Tax Year 2014 R e v i s e d 2/19/2015 Table of Contents A Guide

City and County of San Francisco Office of the Treasurer & Tax Collector Gross Receipts Tax & Payroll Expense Tax Online Filing Instructions Tax Year 2014 R e v i s e d 2/19/2015 Table of Contents A Guide

Chapter 18. Corporations: Distributions Not in Complete Liquidation. Eugene Willis, William H. Hoffman, Jr., David M. Maloney and William A.

Chapter 18 Corporations: Distributions Not in Complete Liquidation Eugene Willis, William H. Hoffman, Jr., David M. Maloney and William A. Raabe Copyright 2004 South-Western/Thomson Learning Taxable Dividends

Chapter 18 Corporations: Distributions Not in Complete Liquidation Eugene Willis, William H. Hoffman, Jr., David M. Maloney and William A. Raabe Copyright 2004 South-Western/Thomson Learning Taxable Dividends

R. HOMEOWNERS' ASSOCIATIONS UNDER IRC 501(c)(4), 501(c)(7) AND 528

(4), 501(c)(7) AND 528") R. HOMEOWNERS' ASSOCIATIONS UNDER IRC 501(c)(4), 501(c)(7) AND 528 1. Introduction A discussion of the exemption of homeowners' associations was included in the 1981 CPE textbook. However, because of questions

R. HOMEOWNERS' ASSOCIATIONS UNDER IRC 501(c)(4), 501(c)(7) AND 528 1. Introduction A discussion of the exemption of homeowners' associations was included in the 1981 CPE textbook. However, because of questions

BEFORE THE TAX COMMISSION OF THE STATE OF IDAHO ) ) ) ) ) ) BACKGROUND

) ) ) ) ) BACKGROUND") BEFORE THE TAX COMMISSION OF THE STATE OF IDAHO In the Matter of the Protest of, Petitioners. DOCKET NO. 26198 DECISION BACKGROUND On December 19, 2013, the Audit Bureau (Audit of the Idaho State Tax Commission

BEFORE THE TAX COMMISSION OF THE STATE OF IDAHO In the Matter of the Protest of, Petitioners. DOCKET NO. 26198 DECISION BACKGROUND On December 19, 2013, the Audit Bureau (Audit of the Idaho State Tax Commission

AMT vs. NOL: When two worlds collide

AMT vs. NOL: When two worlds collide Michael L. Garcia The University of Tampa ABSTRACT The following case will enable students to comprehend and apply Federal Income Tax laws pertaining to the concepts

AMT vs. NOL: When two worlds collide Michael L. Garcia The University of Tampa ABSTRACT The following case will enable students to comprehend and apply Federal Income Tax laws pertaining to the concepts

SAMPLE CONDOMINIUM FINANCIAL STATEMENTS FOR THE YEARS ENDED DECEMBER 31, 2010 AND 2009

FINANCIAL STATEMENTS FOR THE YEARS ENDED DECEMBER 31, 2010 AND 2009 INDEX INDEPENDENT AUDITORS REPORT... 1 BALANCE SHEETS... 2 3 STATEMENTS OF OPERATIONS AND CHANGES IN MEMBERS EQUITY... 4 Administrative

FINANCIAL STATEMENTS FOR THE YEARS ENDED DECEMBER 31, 2010 AND 2009 INDEX INDEPENDENT AUDITORS REPORT... 1 BALANCE SHEETS... 2 3 STATEMENTS OF OPERATIONS AND CHANGES IN MEMBERS EQUITY... 4 Administrative

Determination, Eligibility, Rating & Evidence of Insurance: Condominium Associations

Determination, Eligibility, Rating & Evidence of Insurance: Condominium Associations National Flood Conference April 12, 2010 Panel: Moderator: Patty Latshaw, American Bankers Insurance Company of Florida

Determination, Eligibility, Rating & Evidence of Insurance: Condominium Associations National Flood Conference April 12, 2010 Panel: Moderator: Patty Latshaw, American Bankers Insurance Company of Florida

INFORMATION ON THE RENTAL OF RESIDENTIAL REAL PROPERTY

INFORMATION ON THE RENTAL OF RESIDENTIAL REAL PROPERTY STATE OF HAWAII DEPARTMENT OF TAXATION Benjamin J. Cayetano Governor Ray K. Kamikawa Director of Taxation Revised June, 1998 A MESSAGE FROM THE DIRECTOR

INFORMATION ON THE RENTAL OF RESIDENTIAL REAL PROPERTY STATE OF HAWAII DEPARTMENT OF TAXATION Benjamin J. Cayetano Governor Ray K. Kamikawa Director of Taxation Revised June, 1998 A MESSAGE FROM THE DIRECTOR

SPECIAL ALERT: MORTGAGE FORGIVENESS DEBT RELIEF ACT OF 2007 BRINGS TAX CHANGES TO REAL ESTATE

SPECIAL ALERT: MORTGAGE FORGIVENESS DEBT RELIEF ACT OF 2007 BRINGS TAX CHANGES TO REAL ESTATE By Patricia Hughes Mills, J.D., L.L.M. Associate Professor of Clinical Accounting University of Southern California

SPECIAL ALERT: MORTGAGE FORGIVENESS DEBT RELIEF ACT OF 2007 BRINGS TAX CHANGES TO REAL ESTATE By Patricia Hughes Mills, J.D., L.L.M. Associate Professor of Clinical Accounting University of Southern California

Page 1287 TITLE 26 INTERNAL REVENUE CODE 419

Page 1287 TITLE 26 INTERNAL REVENUE CODE 419 into account the plan s recent and anticipated financial experience, that the plan s available resources are not sufficient to pay benefits under the plan when

Page 1287 TITLE 26 INTERNAL REVENUE CODE 419 into account the plan s recent and anticipated financial experience, that the plan s available resources are not sufficient to pay benefits under the plan when

CHAPTER 9 Charitable Giving

CHAPTER 9 Charitable Giving DISCUSSION QUESTIONS 1. What factors must an individual consider before making a charitable gift? A donor needs to consider his charitable objectives and the desired timing

CHAPTER 9 Charitable Giving DISCUSSION QUESTIONS 1. What factors must an individual consider before making a charitable gift? A donor needs to consider his charitable objectives and the desired timing

Department of Legislative Services 2014 Session

Senate Bill 596 Budget and Taxation Department of Legislative Services 2014 Session FISCAL AND POLICY NOTE Revised (Senator Peters, et al.) SB 596 Ways and Means Income Tax Subtraction Modification - Mortgage

Senate Bill 596 Budget and Taxation Department of Legislative Services 2014 Session FISCAL AND POLICY NOTE Revised (Senator Peters, et al.) SB 596 Ways and Means Income Tax Subtraction Modification - Mortgage

California. Franchise Tax Board. Forms & Instructions 100

California Forms & Instructions 100 2014 Corporation Tax Booklet Members of the Franchise Tax Board John Chiang, Chair Jerome E. Horton, Member Michael Cohen, Member For more information regarding business

California Forms & Instructions 100 2014 Corporation Tax Booklet Members of the Franchise Tax Board John Chiang, Chair Jerome E. Horton, Member Michael Cohen, Member For more information regarding business

Form 990-EZ and supplemental forms and schedules. Sign and date: An officer must sign and date Form 990-EZ on page 4.

Federal Filing Instructions 2014 Name(s) as shown on return Your Social Security Number Date to file by: 08-17-2015 Form to be filed: Form 990-EZ and supplemental forms and schedules Sign and date: An

Federal Filing Instructions 2014 Name(s) as shown on return Your Social Security Number Date to file by: 08-17-2015 Form to be filed: Form 990-EZ and supplemental forms and schedules Sign and date: An

Project Address: City: State: Zip:

CONDOMINUM QUESTIONNAIRE Full Lender Review PLEASE ANSWER ALL QUESTIONS AND SIGN AND DATE THE CERTIFICATIONS AT BOTTOM OF THE QUESTIONNAIRE: This document must be completed by the HOA or Managing Agent;

CONDOMINUM QUESTIONNAIRE Full Lender Review PLEASE ANSWER ALL QUESTIONS AND SIGN AND DATE THE CERTIFICATIONS AT BOTTOM OF THE QUESTIONNAIRE: This document must be completed by the HOA or Managing Agent;

IRS Letter Ruling 200728048. Citation IRC Sections 501(c)(7), 528 Regulations Section 1.501(c)(7)-1 Revenue Rulings 75-494, 69-280, 74-99.

(7), 528 Regulations Section 1.501(c)(7)-1 Revenue Rulings 75-494, 69-280, 74-99.") IRS Letter Ruling 200728048 Cross Reference Data Topical Exempt organizations Form 990 Adverse determination Homeowners Association Access Summary Citation IRC Sections 501(c)(7), 528 Regulations Section

IRS Letter Ruling 200728048 Cross Reference Data Topical Exempt organizations Form 990 Adverse determination Homeowners Association Access Summary Citation IRC Sections 501(c)(7), 528 Regulations Section

Gleim CPA Review Updates to Regulation 2014 Edition, 1st Printing March 2014

Page 1 of 6 Gleim CPA Review Updates to Regulation 2014 Edition, 1st Printing March 2014 NOTE: Text that should be deleted is displayed with a line through the text. New text is shown with a blue background.

Page 1 of 6 Gleim CPA Review Updates to Regulation 2014 Edition, 1st Printing March 2014 NOTE: Text that should be deleted is displayed with a line through the text. New text is shown with a blue background.

The 2015 Landlord s Guide to tax, allowances and obligations

presents... The 2015 Landlord s Guide to tax, allowances and obligations While many people may have the desire to become a landlord of some sort, whether just owning a single flat as an investment, or

presents... The 2015 Landlord s Guide to tax, allowances and obligations While many people may have the desire to become a landlord of some sort, whether just owning a single flat as an investment, or

2015 -- S 0163 S T A T E O F R H O D E I S L A N D

======== LC000 ======== 01 -- S 01 S T A T E O F R H O D E I S L A N D IN GENERAL ASSEMBLY JANUARY SESSION, A.D. 01 A N A C T RELATING TO TAXATION - PERSONAL INCOME TAX Introduced By: Senators Goldin,

======== LC000 ======== 01 -- S 01 S T A T E O F R H O D E I S L A N D IN GENERAL ASSEMBLY JANUARY SESSION, A.D. 01 A N A C T RELATING TO TAXATION - PERSONAL INCOME TAX Introduced By: Senators Goldin,

PERSONAL INCOME TAX BULLETIN 2005-03

PERSONAL INCOME TAX BULLETIN 2005-03 Issued: October 12, 2005 First Revision: December 22, 2005 Second Revision: September 08, 2006 Deferred Compensation Under Nonqualified Plans Part I. Overview. (a)

PERSONAL INCOME TAX BULLETIN 2005-03 Issued: October 12, 2005 First Revision: December 22, 2005 Second Revision: September 08, 2006 Deferred Compensation Under Nonqualified Plans Part I. Overview. (a)

Line-by-Line Instructions for Schedule 1, Additions and Subtractions

and interest and send you a bill. If you annualize your income, you must complete and attach an MI-2210. Enter the penalty and interest amounts on the lines provided. Line 35: Refund. This includes any

and interest and send you a bill. If you annualize your income, you must complete and attach an MI-2210. Enter the penalty and interest amounts on the lines provided. Line 35: Refund. This includes any

How to Avoid Ten IRS Land Mines for Nonprofit Charities

How to Avoid Ten IRS Land Mines for Nonprofit Charities The drive to increase revenue leads many nonprofit organizations to start up business activities. Easy profits are expected, but tax traps waiting

How to Avoid Ten IRS Land Mines for Nonprofit Charities The drive to increase revenue leads many nonprofit organizations to start up business activities. Easy profits are expected, but tax traps waiting

TAXES & FINANCIAL MANAGEMENT

ASSOCIATION RESERVE FUNDS TAXES & FINANCIAL MANAGEMENT Presented by: www.cozbycpa.com Presenter Heather L. Cozby, CPA heather@cozbycpa.com CAI National Business Partners Council Member CAINE Program Committee

ASSOCIATION RESERVE FUNDS TAXES & FINANCIAL MANAGEMENT Presented by: www.cozbycpa.com Presenter Heather L. Cozby, CPA heather@cozbycpa.com CAI National Business Partners Council Member CAINE Program Committee

ERSOP Entrepreneur Rollover Stock Ownership Plan. Real Estate Management Company

Entrepreneur Rollover Stock Ownership Plan Real Estate Management Company First: Are you going to be Active or Passive? All of our clients have that entrepreneurial spirit, they choose ACTIVE. They are

Entrepreneur Rollover Stock Ownership Plan Real Estate Management Company First: Are you going to be Active or Passive? All of our clients have that entrepreneurial spirit, they choose ACTIVE. They are

PROPERTY MANAGEMENT AGREEMENT. Vacation Rental. between. Captain Cook & Associates (agent)

") PROPERTY MANAGEMENT AGREEMENT Vacation Rental between Captain Cook & Associates (agent) 1012 Kapahulu Avenue Suite 110 Honolulu, Hawaii 96816 Phone: (808)-735-5588 Fax: (808)-737-8733 and Address: (owner(s)

PROPERTY MANAGEMENT AGREEMENT Vacation Rental between Captain Cook & Associates (agent) 1012 Kapahulu Avenue Suite 110 Honolulu, Hawaii 96816 Phone: (808)-735-5588 Fax: (808)-737-8733 and Address: (owner(s)

REAL ESTATE OPERATIONS IN THE CORPORATE FORM -- WHEN DOES IT MAKE SENSE?

REAL ESTATE OPERATIONS IN THE CORPORATE FORM -- WHEN DOES IT MAKE SENSE? I. INTRODUCTION A. Historically real estate owned by partnership or limited partnership. B. Many circumstances favor the use of

REAL ESTATE OPERATIONS IN THE CORPORATE FORM -- WHEN DOES IT MAKE SENSE? I. INTRODUCTION A. Historically real estate owned by partnership or limited partnership. B. Many circumstances favor the use of

TAX INFORMATION RELEASE NO. 99-4

BENJAMIN J. CAYETANO GOVERNOR MAZIE HIRONO LT. GOVERNOR RAY K. KAMIKAWA DIRECTOR OF TAXATION MARIE Y. OKAMURA DEPUTY DIRECTOR Tel: (808) 587-1540 Fax: (808) 587-1560 STATE OF HAWAII DEPARTMENT OF TAXATION

BENJAMIN J. CAYETANO GOVERNOR MAZIE HIRONO LT. GOVERNOR RAY K. KAMIKAWA DIRECTOR OF TAXATION MARIE Y. OKAMURA DEPUTY DIRECTOR Tel: (808) 587-1540 Fax: (808) 587-1560 STATE OF HAWAII DEPARTMENT OF TAXATION

MEXICO TAXATION GUIDE

THE FLORES LAW FIRM Attorney and Counselor at Law 9901 IH-10 West, Suite 800 San Antonio, TX 78230 TEL. (210) 340-3800 FAX (210) 340-5200 MEXICO TAXATION GUIDE I. RECOGNIZED MEXICAN BUSINESS ENTITIES A.

THE FLORES LAW FIRM Attorney and Counselor at Law 9901 IH-10 West, Suite 800 San Antonio, TX 78230 TEL. (210) 340-3800 FAX (210) 340-5200 MEXICO TAXATION GUIDE I. RECOGNIZED MEXICAN BUSINESS ENTITIES A.

(Draft No. 2.1 H.577) Page 1 of 20 5/3/2016 - MCR 7:40 PM. The Committee on Finance to which was referred House Bill No. 577

Page 1 of 20 5/3/2016 - MCR 7:40 PM. The Committee on Finance to which was referred House Bill No. 577") (Draft No.. H.) Page of // - MCR :0 PM TO THE HONORABLE SENATE: The Committee on Finance to which was referred House Bill No. entitled An act relating to voter approval of electricity purchases by municipalities

(Draft No.. H.) Page of // - MCR :0 PM TO THE HONORABLE SENATE: The Committee on Finance to which was referred House Bill No. entitled An act relating to voter approval of electricity purchases by municipalities

Choice of Entity: Corporation or Limited Liability Company?

September 2012 Choice of Entity: Corporation or Limited Liability Company? By Gianfranco A. Pietrafesa* Attorney at Law There are many different types of business entities, including corporations, general

September 2012 Choice of Entity: Corporation or Limited Liability Company? By Gianfranco A. Pietrafesa* Attorney at Law There are many different types of business entities, including corporations, general

20. Income Tax Consequences at Death

20. Income Tax Consequences at Death When you die, your income tax situation changes: your estate becomes a separate taxpayer and your tax situation is more complicated. However, the situation also presents

20. Income Tax Consequences at Death When you die, your income tax situation changes: your estate becomes a separate taxpayer and your tax situation is more complicated. However, the situation also presents

AMENDMENT TO YOUR TRADITIONAL IRA

INDIVIDUAL RETIREMENT ANNUITY DISCLOSURE STATEMENT AMENDMENT This disclosure statement explains the rules governing a Traditional IRA. The term IRA will be used in this disclosure statement to refer to

INDIVIDUAL RETIREMENT ANNUITY DISCLOSURE STATEMENT AMENDMENT This disclosure statement explains the rules governing a Traditional IRA. The term IRA will be used in this disclosure statement to refer to

CITY OF GRAND PRAIRIE PUBLIC IMPROVEMENT DISTRICT POLICY AS ADOPTED BY THE CITY COUNCIL ON MARCH 1, 2011

CITY OF GRAND PRAIRIE PUBLIC IMPROVEMENT DISTRICT POLICY AS ADOPTED BY THE CITY COUNCIL ON MARCH 1, 2011 I. PURPOSE: A Public Improvement District (PID) is a tax assessment area established to provide

CITY OF GRAND PRAIRIE PUBLIC IMPROVEMENT DISTRICT POLICY AS ADOPTED BY THE CITY COUNCIL ON MARCH 1, 2011 I. PURPOSE: A Public Improvement District (PID) is a tax assessment area established to provide

G. IRC 501(c)(7) ORGANIZATION

(7) ORGANIZATION") G. IRC 501(c)(7) ORGANIZATION 1. Introduction Social and recreational clubs were originally granted exemption in the Revenue Act of 1916. Congress stated that the reason for their exemption was that the

G. IRC 501(c)(7) ORGANIZATION 1. Introduction Social and recreational clubs were originally granted exemption in the Revenue Act of 1916. Congress stated that the reason for their exemption was that the

Chapter 16 Accounting for Income Taxes

OTHER ACCOUNTING ISSUES Rate Considerations In the recent past there have been relatively stable tax rates, but historically the congress has adjusted tax rates on a periodic basis. The calculations of

OTHER ACCOUNTING ISSUES Rate Considerations In the recent past there have been relatively stable tax rates, but historically the congress has adjusted tax rates on a periodic basis. The calculations of

Divorce and Your PERA Retirement Benefits

Divorce and Your PERA Retirement Benefits This brochure is designed to provide PERA members, their spouses, and attorneys with information about the division of PERA retirement benefits in divorce proceedings

Divorce and Your PERA Retirement Benefits This brochure is designed to provide PERA members, their spouses, and attorneys with information about the division of PERA retirement benefits in divorce proceedings

CLIENT INSTRUCTIONS FOR IRREVOCABLE LIFE INSURANCE TRUSTS, ANNUAL EXCLUSION GIFTS & ADMINISTRATION

CLIENT INSTRUCTIONS FOR IRREVOCABLE LIFE INSURANCE TRUSTS, ANNUAL EXCLUSION GIFTS & ADMINISTRATION In General Life insurance ownership through an Irrevocable Life Insurance Trust ( ILIT ) can remove the

CLIENT INSTRUCTIONS FOR IRREVOCABLE LIFE INSURANCE TRUSTS, ANNUAL EXCLUSION GIFTS & ADMINISTRATION In General Life insurance ownership through an Irrevocable Life Insurance Trust ( ILIT ) can remove the

E. "SPONSORING ORGANIZATIONS" UNDER USDA CHILD AND ADULT CARE FOOD PROGRAM by Terrell Berkovsky and Amy Henchey

E. "SPONSORING ORGANIZATIONS" UNDER USDA CHILD AND ADULT CARE FOOD PROGRAM by Terrell Berkovsky and Amy Henchey 1. Introduction In recent months, the National Office has reviewed numerous applications

E. "SPONSORING ORGANIZATIONS" UNDER USDA CHILD AND ADULT CARE FOOD PROGRAM by Terrell Berkovsky and Amy Henchey 1. Introduction In recent months, the National Office has reviewed numerous applications

REAL ESTATE AND RENTAL INCOME TAXATION FREQUENTLY ASKED QUESTIONS (FAQS)

") ISO 9001:2008 CERTIFIED REAL ESTATE AND RENTAL INCOME TAXATION FREQUENTLY ASKED QUESTIONS (FAQS) 1. What is considered rental income for tax purposes? Rent, a premium or similar consideration is considered

ISO 9001:2008 CERTIFIED REAL ESTATE AND RENTAL INCOME TAXATION FREQUENTLY ASKED QUESTIONS (FAQS) 1. What is considered rental income for tax purposes? Rent, a premium or similar consideration is considered

SPECIAL REPORT: PROJECTED 2016 INFLATION-ADJUSTED TAX BRACKETS AND OTHER KEY FIGURES

SPECIAL REPORT: PROJECTED 2016 INFLATION-ADJUSTED TAX BRACKETS AND OTHER KEY FIGURES TABLE OF CONTENTS Tax rate schedules 3 Standard deductions 5 Kiddie tax 5 Personal exemption 5 Phase-out of personal

SPECIAL REPORT: PROJECTED 2016 INFLATION-ADJUSTED TAX BRACKETS AND OTHER KEY FIGURES TABLE OF CONTENTS Tax rate schedules 3 Standard deductions 5 Kiddie tax 5 Personal exemption 5 Phase-out of personal

PROFESSIONAL MORTGAGE SERVICES, INC. MORTGAGE BANKERS 10031 OLD OCEAN CITY BLVD., SUITE 216 BERLIN, MARYLAND 21811 (410)641-4300 FAX (410)641-3022

641-4300 FAX (410)641-3022") PROFESSIONAL MORTGAGE SERVICES, INC. MORTGAGE BANKERS 10031 OLD OCEAN CITY BLVD., SUITE 216 BERLIN, MARYLAND 21811 (410)641-4300 FAX (410)641-3022 Ineligible Projects The following are Ineligible Project

PROFESSIONAL MORTGAGE SERVICES, INC. MORTGAGE BANKERS 10031 OLD OCEAN CITY BLVD., SUITE 216 BERLIN, MARYLAND 21811 (410)641-4300 FAX (410)641-3022 Ineligible Projects The following are Ineligible Project

Section 529 Plans. (Tax-Free College Savings Plans)

") Section 529 Plans (Tax-Free College Savings Plans) by Kevin C. Curry Board Certified Tax Law Specialist Board Certified Estate Planning and Administration Specialist Kean Miller Hawthorne D Armond McCowan

Section 529 Plans (Tax-Free College Savings Plans) by Kevin C. Curry Board Certified Tax Law Specialist Board Certified Estate Planning and Administration Specialist Kean Miller Hawthorne D Armond McCowan

INTERPRETATION NOTE: NO. 35 (ISSUE 3) DATE: 31 March 2010

DATE: 31 March 2010") INTERPRETATION NOTE: NO. 35 (ISSUE 3) DATE: 31 March 2010 ACT : INCOME TAX ACT, NO. 58 OF 1962 (the Act) SECTION : PARAGRAPHS 1, 2(1A) AND 2(5) OF THE FOURTH SCHEDULE AND SECTION 23(k) SUBJECT : EMPLOYEES

INTERPRETATION NOTE: NO. 35 (ISSUE 3) DATE: 31 March 2010 ACT : INCOME TAX ACT, NO. 58 OF 1962 (the Act) SECTION : PARAGRAPHS 1, 2(1A) AND 2(5) OF THE FOURTH SCHEDULE AND SECTION 23(k) SUBJECT : EMPLOYEES

Debt Modifications: Tax Planning Options Including New 10-Year Potential Deferral Ann Galligan Kelley, Providence College, USA

Debt Modifications: Tax Planning Options Including New 10-Year Potential Deferral Ann Galligan Kelley, Providence College, USA ABSTRACT With the recent decline in the real estate market, many taxpayers,

Debt Modifications: Tax Planning Options Including New 10-Year Potential Deferral Ann Galligan Kelley, Providence College, USA ABSTRACT With the recent decline in the real estate market, many taxpayers,

Tax Issues Facing Exempt Organizations

Tax Issues Facing Exempt Organizations TODAY S AGENDA AND OBJECTIVES CHNA Timeline Refresher Unrelated Business Income Joint Ventures State Update 2 CHNA TIMING Effective for tax years beginning after

Tax Issues Facing Exempt Organizations TODAY S AGENDA AND OBJECTIVES CHNA Timeline Refresher Unrelated Business Income Joint Ventures State Update 2 CHNA TIMING Effective for tax years beginning after

2. Corporations Fully Exempt These corporations qualify for the full income tax exemption:

T. Exempt Corporations (G.S. 105-125, G.S. 105-130.11, G.S. 105-130.12) 1. Preliminary Statement Some types of corporations are fully exempt from income and franchise taxes, whereas others are conditionally

T. Exempt Corporations (G.S. 105-125, G.S. 105-130.11, G.S. 105-130.12) 1. Preliminary Statement Some types of corporations are fully exempt from income and franchise taxes, whereas others are conditionally

Private Letter Ruling Redacted Version No. 08-023

Private Letter Ruling Redacted Version No. 08-023 Corporation Income Tax and Franchise Tax and Individual Income Tax Credit for the Rehabilitation of Historic Structures in Downtown Development Districts

Private Letter Ruling Redacted Version No. 08-023 Corporation Income Tax and Franchise Tax and Individual Income Tax Credit for the Rehabilitation of Historic Structures in Downtown Development Districts

Selected Debt Restructuring Issues. Friday, January 22, 2010 Tax Law Section

Selected Debt Restructuring Issues Friday, January 22, 2010 Tax Law Section Robert E. August, Esq. Merline & Meacham, PA P.O. Box 10796 Greenville, SC 29603 p. (864) 242-4080 f. (864) 242-5758 baugust@merlineandmeacham.com

Selected Debt Restructuring Issues Friday, January 22, 2010 Tax Law Section Robert E. August, Esq. Merline & Meacham, PA P.O. Box 10796 Greenville, SC 29603 p. (864) 242-4080 f. (864) 242-5758 baugust@merlineandmeacham.com

Instructions for Form 4626

2015 Instructions for Form 4626 Department of the Treasury Internal Revenue Service Alternative Minimum Tax Corporations Section references are to the Internal Revenue Code unless otherwise noted. Future

2015 Instructions for Form 4626 Department of the Treasury Internal Revenue Service Alternative Minimum Tax Corporations Section references are to the Internal Revenue Code unless otherwise noted. Future

INTERPRETATION NOTE: NO. 64. DATE: 22 February 2012

INTERPRETATION NOTE: NO. 64 DATE: 22 February 2012 ACT : INCOME TAX ACT NO. 58 OF 1962 (the Act) SECTION : SECTION 10(1)(e) SUBJECT : INCOME TAX EXEMPTION: BODIES CORPORATE ESTABLISHED UNDER THE SECTIONAL

INTERPRETATION NOTE: NO. 64 DATE: 22 February 2012 ACT : INCOME TAX ACT NO. 58 OF 1962 (the Act) SECTION : SECTION 10(1)(e) SUBJECT : INCOME TAX EXEMPTION: BODIES CORPORATE ESTABLISHED UNDER THE SECTIONAL

Choice of Entity. Paul E. Costantino, CPA, MST Costantino Richards Rizzo, LLP, Wakefield

Choice of Entity Paul E. Costantino, CPA, MST Costantino Richards Rizzo, LLP, Wakefield I. Overview of Entities The entity selection process is one of the first steps in the formation of any business,

Choice of Entity Paul E. Costantino, CPA, MST Costantino Richards Rizzo, LLP, Wakefield I. Overview of Entities The entity selection process is one of the first steps in the formation of any business,

New Developments in Taxation for Financial Institutions: What s coming down the pipe? October 14, 2015

AUDIT TAX SYSTEMS RISK New Developments in Taxation for Financial Institutions: What s coming down the pipe? October 14, 2015 Presented by: Patrick Tuley, CPA: Tax Partner Topics of Interest Affordable

AUDIT TAX SYSTEMS RISK New Developments in Taxation for Financial Institutions: What s coming down the pipe? October 14, 2015 Presented by: Patrick Tuley, CPA: Tax Partner Topics of Interest Affordable

Divorce and Life Insurance. in brief

Divorce and Life Insurance in brief Divorce and Life Insurance Introduction In a divorce, property is divided between the spouses. In addition, a divorce decree may require that one spouse pay alimony

Divorce and Life Insurance in brief Divorce and Life Insurance Introduction In a divorce, property is divided between the spouses. In addition, a divorce decree may require that one spouse pay alimony

In a nutshell... From Issue 52, 2010-11 of Superannuation Quarterly, dated March 2011. ...the full article follows. Tax deductions for SMSFs

From Issue 52, 2010-11 of Superannuation Quarterly, dated March 2011 In a nutshell... Tax deductions for SMSFs This article looks at various tax deductions that are available to a complying Self Managed

From Issue 52, 2010-11 of Superannuation Quarterly, dated March 2011 In a nutshell... Tax deductions for SMSFs This article looks at various tax deductions that are available to a complying Self Managed

TECHNICAL EXPLANATION OF THE TAX PROVISIONS IN SENATE AMENDMENT 4594 TO H.R

TECHNICAL EXPLANATION OF THE TAX PROVISIONS IN SENATE AMENDMENT 4594 TO H.R. 5297, THE SMALL BUSINESS JOBS ACT OF 2010, SCHEDULED FOR CONSIDERATION BY THE SENATE ON SEPTEMBER 16, 2010 Prepared by the Staff

TECHNICAL EXPLANATION OF THE TAX PROVISIONS IN SENATE AMENDMENT 4594 TO H.R. 5297, THE SMALL BUSINESS JOBS ACT OF 2010, SCHEDULED FOR CONSIDERATION BY THE SENATE ON SEPTEMBER 16, 2010 Prepared by the Staff

no--asset 7 s asset 7 s

Bankruptcy Questions Answered! Attorney to Non- Attorney Robert McKenzie, EA, Esq. Types of Bankruptcies This is not an easy subject, but our goal is to distill it to key issues you need to know as a return

Bankruptcy Questions Answered! Attorney to Non- Attorney Robert McKenzie, EA, Esq. Types of Bankruptcies This is not an easy subject, but our goal is to distill it to key issues you need to know as a return

Estate and Trust Form 1041 Issues for Tax Return Preparers

Estate and Trust Form 1041 Issues for Tax Return Preparers Allocating Income and Deductions, Calculating DNI, Understanding Reporting Rules for Trusts, and More WEDNESDAY, FEBRUARY 27, 2013, 1:00-2:50

Estate and Trust Form 1041 Issues for Tax Return Preparers Allocating Income and Deductions, Calculating DNI, Understanding Reporting Rules for Trusts, and More WEDNESDAY, FEBRUARY 27, 2013, 1:00-2:50

Airbnb. General guidance on the taxation of rental income

Airbnb General guidance on the taxation of rental income This booklet was prepared by Ernst & Young LLP (EY) at the request of Airbnb. This booklet is intended solely for information purposes and no Airbnb

Airbnb General guidance on the taxation of rental income This booklet was prepared by Ernst & Young LLP (EY) at the request of Airbnb. This booklet is intended solely for information purposes and no Airbnb

Instructions for Limited Liability Company Reference Guide Sheet

Instructions for Limited Liability Company Reference Guide Sheet Parts I and II of these instructions provide information keyed to certain questions in the Limited Liability Company Reference Guide Sheet.

Instructions for Limited Liability Company Reference Guide Sheet Parts I and II of these instructions provide information keyed to certain questions in the Limited Liability Company Reference Guide Sheet.

Small Business Tax Saving Strategies for the 2012 Filing Season

Small Business Tax Saving Strategies for the 2012 Filing Season Few business sectors embody today s entrepreneurial spirit, drive for innovation and unwavering perseverance more than the small business

Small Business Tax Saving Strategies for the 2012 Filing Season Few business sectors embody today s entrepreneurial spirit, drive for innovation and unwavering perseverance more than the small business

New York State Tax Incentives for High-Tech Companies

New York State Tax Incentives for High-Tech Companies Issued July 2006 1 Table of Contents I. Relevant Terms... 2 II. Investment Tax Credit / Employment Incentive Credit... 2 III. Qualified Emerging Technology

New York State Tax Incentives for High-Tech Companies Issued July 2006 1 Table of Contents I. Relevant Terms... 2 II. Investment Tax Credit / Employment Incentive Credit... 2 III. Qualified Emerging Technology

Personal Income Tax Bulletin 2008-1. IRAs

PENNSYLVANIA DEPARTMENT OF REVENUE ISSUED: JANUARY 16, 2008 Section 1. Introduction. 1. FEDERAL TAX PERSPECTIVE. Personal Income Tax Bulletin 2008-1 IRAs When Congress enacted ERISA in 1974 to regulate

PENNSYLVANIA DEPARTMENT OF REVENUE ISSUED: JANUARY 16, 2008 Section 1. Introduction. 1. FEDERAL TAX PERSPECTIVE. Personal Income Tax Bulletin 2008-1 IRAs When Congress enacted ERISA in 1974 to regulate

Home Mortgage Disclosure Act - Regulation C

Home Mortgage Disclosure Act - Regulation C Revised Date: 12/20/2013 Introduction: The Home Mortgage Disclosure Act (HMDA), implemented by Regulation C, provides the members with loan data that can be

Home Mortgage Disclosure Act - Regulation C Revised Date: 12/20/2013 Introduction: The Home Mortgage Disclosure Act (HMDA), implemented by Regulation C, provides the members with loan data that can be

New York State Corporate Tax Reform Outline Part A of Chapter 59 of the Laws of 2014 Signed March 31, 2014 April 2014

Corporations Subject to [Bill 1 and 5; Law (TL) 209 unless otherwise noted] Unifies Articles 9-A (Corporate Franchise ) and 32 (Bank Franchise ). o Current Article 32 taxpayers are subject to the revised

Corporations Subject to [Bill 1 and 5; Law (TL) 209 unless otherwise noted] Unifies Articles 9-A (Corporate Franchise ) and 32 (Bank Franchise ). o Current Article 32 taxpayers are subject to the revised

My interest in real estate investment comes naturally. I. The Secrets to a Tax Free Life with Real Estate Investment BY LARRY STONE, CPA CTC

Chapter Five The Secrets to a Tax Free Life with Real Estate Investment BY LARRY STONE, CPA CTC My interest in real estate investment comes naturally. I inherited it from my father and grandfather. Both

Chapter Five The Secrets to a Tax Free Life with Real Estate Investment BY LARRY STONE, CPA CTC My interest in real estate investment comes naturally. I inherited it from my father and grandfather. Both

2015 Tax Implications. of Long Term Care Insurance (LTCi) for Individuals and Businesses. Tax Solutions Guide for Individuals and Businesses

for Individuals and Businesses. Tax Solutions Guide for Individuals and Businesses") Tax Solutions Guide for Individuals and Businesses 2015 Tax Implications of Long Term Care Insurance (LTCi) for Individuals and Businesses Insurance Strategies LTC1419 What are the Tax Implications of

Tax Solutions Guide for Individuals and Businesses 2015 Tax Implications of Long Term Care Insurance (LTCi) for Individuals and Businesses Insurance Strategies LTC1419 What are the Tax Implications of

Private Letter Ruling Redacted Version No. 07-017

Private Letter Ruling Redacted Version No. 07-017 Corporation Income Tax and Franchise Tax and Individual Income Tax Credit for the Rehabilitation of Historic Structures in Downtown Development Districts

Private Letter Ruling Redacted Version No. 07-017 Corporation Income Tax and Franchise Tax and Individual Income Tax Credit for the Rehabilitation of Historic Structures in Downtown Development Districts

Information Regarding U.S. Federal Income Tax Calculations in connection with the Acquisition of DIRECTV by AT&T

Information Regarding U.S. Federal Income Tax Calculations in connection with the Acquisition of DIRECTV by AT&T The following information is provided to illustrate how to determine taxable gain on DIRECTV

Information Regarding U.S. Federal Income Tax Calculations in connection with the Acquisition of DIRECTV by AT&T The following information is provided to illustrate how to determine taxable gain on DIRECTV

Taxation of Nonresidents and Individuals Who Change Residency

State of California Franchise Tax Board Taxation of Nonresidents and Individuals Who Change Residency FTB Publication 1100 (REV 04-2014) For forms and information, go to ftb.ca.gov and search for forms

State of California Franchise Tax Board Taxation of Nonresidents and Individuals Who Change Residency FTB Publication 1100 (REV 04-2014) For forms and information, go to ftb.ca.gov and search for forms

CONDOMINIUM GOVERNANCE FORM

CONDOMINIUM GOVERNANCE FORM DEPARTMENT OF BUSINESS AND PROFESSIONAL REGULATION Division of Florida Condominiums, Timeshares, and Mobile Homes 1940 North Monroe Street Tallahassee, Florida 32399-1030 Telephone:

CONDOMINIUM GOVERNANCE FORM DEPARTMENT OF BUSINESS AND PROFESSIONAL REGULATION Division of Florida Condominiums, Timeshares, and Mobile Homes 1940 North Monroe Street Tallahassee, Florida 32399-1030 Telephone:

Tax Relief for Natural Disasters

Page 1 of 6 January 2015 Bar Bulletin Tax Relief for Natural Disasters By Amber Quintal When a disaster strikes, those affected are left to start the sometimes long and painful process of rebuilding and

Page 1 of 6 January 2015 Bar Bulletin Tax Relief for Natural Disasters By Amber Quintal When a disaster strikes, those affected are left to start the sometimes long and painful process of rebuilding and

Our Fee Match Guarantee

THE LAW OFFICE OF MICHAEL J. HOWELL, P.A. 112 Executive Center 1 Corpus Christi Place, #112 Hilton Head Island, SC 29928 HiltonHeadEstatePlanning.com Michael J. Howell Licensed in Florida and South Carolina

THE LAW OFFICE OF MICHAEL J. HOWELL, P.A. 112 Executive Center 1 Corpus Christi Place, #112 Hilton Head Island, SC 29928 HiltonHeadEstatePlanning.com Michael J. Howell Licensed in Florida and South Carolina

LIENS. Lien: An encumbrance on property to secure a debt or to protect a claim for payment of a debt.

LIENS Lien: An encumbrance on property to secure a debt or to protect a claim for payment of a debt. Mechanic s Lien: A lien on real property to ensure payment for work performed and materials furnished

LIENS Lien: An encumbrance on property to secure a debt or to protect a claim for payment of a debt. Mechanic s Lien: A lien on real property to ensure payment for work performed and materials furnished

The Green Behind Rebuilding Green Tax Benefits to Incentivize Green

The Green Behind Rebuilding Green Tax Benefits to Incentivize Green presented by Teri Samples, CPA Tony Smith, CPA Steve George, PE, CEM Mueller Prost PC October 29, 2012 2012 Mueller Prost PC The Green

The Green Behind Rebuilding Green Tax Benefits to Incentivize Green presented by Teri Samples, CPA Tony Smith, CPA Steve George, PE, CEM Mueller Prost PC October 29, 2012 2012 Mueller Prost PC The Green

A Comparison of Entity Taxation

A Comparison of Entity Taxation Sean W. Brewer, CPA Daniel N. Messing, CPA Pugh & Company, P.C. 315 N. Cedar Bluff Road; Suite 200 Knoxville, TN 37923 Sole Proprietorships Single Owner Advantages Easy

A Comparison of Entity Taxation Sean W. Brewer, CPA Daniel N. Messing, CPA Pugh & Company, P.C. 315 N. Cedar Bluff Road; Suite 200 Knoxville, TN 37923 Sole Proprietorships Single Owner Advantages Easy

STATE OF NEW HAMPSHIRE DEPARTMENT OF REVENUE ADMINISTRATION IN THE MATTER OF THE PETITION OF. ABC, Inc., 123, LLC and an Individual

STATE OF NEW HAMPSHIRE DEPARTMENT OF REVENUE ADMINISTRATION IN THE MATTER OF THE PETITION OF ABC, Inc., 123, LLC and an Individual FOR A DECLARATORY RULING REDACTED DOCUMENT Document # 10391 Effective

STATE OF NEW HAMPSHIRE DEPARTMENT OF REVENUE ADMINISTRATION IN THE MATTER OF THE PETITION OF ABC, Inc., 123, LLC and an Individual FOR A DECLARATORY RULING REDACTED DOCUMENT Document # 10391 Effective