London Borough of Lewisham. Local Support Scheme Policy

|

|

|

- Clinton Goodwin

- 10 years ago

- Views:

Transcription

1 London Borough of Lewisham Local Support Scheme Policy January 2013

2 1. Introduction Context The Welfare Reform Act, which received royal assent in March 2012, represents the biggest change to the welfare state in 60 years. Its key objectives are to improve fairness, equity and affordability in the benefits system and to design it in a way that actively supports employment. The Act establishes a wide range of reforms, such as the introduction of a Universal Credit to replace a number of existing means-tested benefits, housing benefit and tax credits for people of working age, a total cap on household benefits of 500 per week for couples/lone parents and 350 per week for single people and significant changes to Local Housing Allowance (LHA) rates. It is intended to deliver the Government s proposals to cut the spending on benefits by an estimated 18 billion through: Improving work incentives. Simplifying the benefits system. Tackling administrative complexity. As part of this Act, the Department of Work and Pensions (DWP) has abolished Crisis Loans and Community Care Grants, which are key discretionary elements of the Social Fund scheme. They are being replaced by a combination of locally-based emergency welfare assistance schemes (run by local authorities, but funded by the DWP) and a nationally administered Advance of Benefit facility that will eventually replace Alignment Crisis Loans. This change is effective from 1 April Purpose Of The Policy Lewisham intends to continue providing a structured scheme that broadly supports the same needs as the previous Crisis Loan and Community Care Grant model this will be known as the Local Support Scheme. However, we will need to do this in a way that: Improves the administrative efficiency for both the claimant and the authority. Targets limited funds at those most in need.

rates.")

3 Ensures the sustainability of the scheme for future years. The purpose of this policy is to provide applicants, third-party organisations, officers and members with a clear understanding of how this new scheme will operate, including its design, eligibility criteria and delivery model. It is supported by a number of appendices, as indicated throughout the document. Aims Of The Policy In Lewisham, we want to support those people who are most financially vulnerable. This includes: People who are in crisis due to a disaster or other emergency. People who need support to regain independence after a period in institutional care. People who need support to regain a more settled way of life. People who are at risk of losing their independence and ending up in institutional care. In developing this scheme, we have endeavoured to ensure that those residents most in need are not simply awarded an Emergency Loan or Support Grant, but are instead also given an opportunity to access affordable credit and financial assistance as well as receiving an offer of preventative support. We anticipate that this will encourage them to build greater financial capability and resilience, thus reducing future reliance on the scheme or recourse to other harmful forms of support and credit, such as unlicensed lenders and payday loan companies.

4 2. Emergency Loans Purpose Of The Loan Emergency Loans can be applied for in three circumstances. These circumstances, which broadly mirror the previous Crisis Loan scheme, are as follows: To cover immediate short-term needs which will prevent serious risk to the health or safety of a person or their family. To help in an emergency or disaster situation such as a serious flood, causing substantial damage, loss or destruction to possessions and/or property by providing funding for urgently needed furniture, cookers, beds, household equipment, food and utilities and clothing and footwear. 1 n emergency or disaster situations, including For Rent in Advance, where it is part of a successful application for a Support Grant involving a planned resettlement process 2 Eligibility Criteria For The Loan Applicants for Emergency Loans must meet the following eligibility criteria: The applicant must be aged 16 or over. The applicant must be in receipt of a qualifying benefit (see Appendix 1). All applicants must have been resident in the borough of Lewisham for a minimum of six weeks prior to making their application. Where an applicant is of no fixed abode, the applicant must have a current benefit correspondence address in Lewisham that has been verified by the DWP. The applicant must not be an excluded person (see Appendix 1). The applicant must not have any savings, capital and/or insurances that can be relied on to meet the need for which they have made their application (see Appendix 1). 1 Loans for items cannot exceed 1,000 in value 2 The DWP Budgeting loan scheme will continue to make provision for Rent in Advance for applicants who are already in receipt of on-going benefits. The local scheme is designed to ensure that provision is in place for people who, because of a period of institutional care, would not have been eligible for benefits (and therefore a DWP budgeting loan).

5 The applicant must not have failed to repay a previous Emergency Loan or must be able to demonstrate that they are actively and consistently repaying a previous Emergency Loan. The applicant must not be eligible for financial assistance from the DWP, such as a Budgeting Loan or an Advance of Benefit facility. The application cannot be made as a result of financial loss associated with the imposition of a DWP sanction or disallowance. 3 The applicant must not be seeking support to pay for an excluded item (see Appendix 1). The applicant must be willing to sign up to the Credit Union terms and conditions for issuing and repaying the loan, including the application of a 2% monthly interest rate. The applicant must agree to all terms and conditions set out at the start of the application process. Application Process The primary method for making an application for an Emergency Loan will be via an online form available from the Lewisham website. For applicants who are not able to make an application online without support, they can either: Seek assistance from a third party or friends/family to complete the application on their behalf. In exceptional circumstances, make their application over the phone. The application process will ask a series of questions about the circumstances leading to the application for the Emergency Loan and determine the applicant s eligibility based on the criteria set out in this policy. The process will also determine the appropriate value of the loan based on the circumstances outlined in the application. All decisions regarding the award of Emergency Loans will not be based solely on need, but will also take into account the applicant s ability to repay and, where relevant, their repayment history. 3 Applicants who have been sanctioned by the DWP are eligible to apply for hardship loans via the DWP

.")

6 In some circumstances, it may be necessary for an applicant to produce supporting evidence linked to their application. In these circumstances, this will be identified as part of the application process and the contact will be made directly with the applicant to explain evidence requirements. Applications can be submitted online at any time but will be assessed between 9.00 and on normal working days. Upon receiving an application, the council will make decisions on whether to award the loan within two working days (unless the necessity for additional supporting evidence prevents us from doing so). Applicants will be notified of the decision via /telephone call/letter and informed of the next steps they need to take to collect their award or, in the case of a negative decision, how to request a Review. Making The Award The council intends to work in partnership with Lewisham Plus Credit Union for the administration and recovery of Emergency Loans. Those making successful applications to the Emergency Loan scheme will be referred to Lewisham Plus Credit Union who will make arrangements to disburse funds to them. Depending on individual circumstances, this may include: Visiting a named Credit Union branch in the borough. Opening a Credit Union account. Providing appropriate evidence (i.e. identity/bank details). Agreeing to the terms of repayment for the loan. Participating in wider discussions around financial management and budgeting. Applicants will be asked to present to the Credit Union to receive their loan on the next working day following the decision being made.

.")

7 The Credit Union will make arrangements to pay the value of the loan, as agreed by the Council, to the applicant. All subsequent contact regarding the administration and repayment of the loan will be between the applicant and the Credit Union. The value of the loan award will be based either: For items - on the schedule of rates for items based on an average high street price For living expenses on the 2011/12 DWP Crisis Loan rates The schedule of rates for items and living expenses will be reviewed on an annual basis (Appendix 2). Support For Those Whose Applications Are Unsuccessful As part of the online process, all unsuccessful applications will also be provided with additional information setting out other ways that they can meet their needs. This could include: Accessing food or furniture via a voluntary sector partner service. Presenting independently to the Credit Union for access to an affordable loan.

.")

8 3. Support Grants Purpose Of The Grant Under the Local Support Scheme, Support Grant packages or non-repayable grants (not exceeding 1,000) can be applied for by people who: Are re-establishing themselves in the community after a period of institutional or residential care. Need support to remain in the community rather than enter institutional or residential care. Are setting up home as part of a planned resettlement process. Need support to ease exceptional pressures on a person or family. Need support to care for a prisoner or young offender on temporary release. Eligibility For The Grant The eligibility for the Support Grant scheme is the same as the Emergency Loan scheme with the exception that: An applicant must be in receipt of (or about to be in receipt of) a qualifying benefit. You must be proven to be a resident of LB Lewisham for 6 weeks prior to date of application, or about to be resettled into accommodation in Lewisham borough or another Local Authority by LB Lewisham Housing Options as part of a planned programme of resettlement or discharge of housing duty And with the following additional requirements that: An applicant must not have been awarded a Support Grant in the previous 12 months. The provision of the service to meet the need for which the application has been made is not provided for under another statutory duty. Application Process

9 As with Emergency Loan, the primary method for making an application for a Support Grant will be via an online form available from the Lewisham website. Because the majority of applications for DWP Community Care Grants are completed jointly with an advocacy organisation, it will be possible (with the applicant s consent) for third parties to submit Support Grant applications on behalf of an applicant and receive notification of their progress. In rare circumstances where an applicant is unable to complete the online claim process, it will be possible for an application to be made over the phone. As with the DWP scheme, the nature of the grants being awarded means that most applications for Support Grants will also require the provision of further evidence regarding the individual or family s circumstances. Where evidence is required, this will be clearly set out in the online application process. Where possible, we will reduce the amount of evidence required by accepting verification from third parties when they are completing assisted applications. Upon receiving an application, the council will make decisions on whether to award the grant within nine working days (unless the necessity for additional supporting evidence prevents us from doing so). We may also signpost the applicant to another service within the Council if all or part of the need for which the application has been made can be met via another area or department. Applicants will be notified of the decision via or letter and informed of the how the award will be made. Making The Award Unlike the current DWP Community Care Grant scheme, the application process for Support Grants will not, in most cases, involve the applicant requesting a sum of money for resettlement needs. Instead, the circumstances presented by the individual applicant will determine the amount awarded by the Council, based on pre-set resettlement packages. A schedule of the award levels which have been set for these packages is included in Appendix 2. The Council intends to use a mixture of pre-paid cards/vouchers and locally sourced replacement items to meet the needs of successful applicants to the Support Grant scheme. As such, an applicant will be offered either:

10 Locally sourced second-hand items (for white goods all second hand items will have been safety checked and guaranteed for a minimum of sixty days). A voucher or prepaid card loaded to the value of the resettlement package, which can be used at specified stores to purchase agreed items. The decision on whether to award items or vouchers will be made by the Council on the basis of the need for which the application has been made and the availability of specific second-hand items.

11 4. Review Process A customer who is unhappy about the outcome of their application for an Emergency Loan or Support Grant is entitled to ask for a review of the decision provided that they have satisfied all the requirements set out within the scheme and can demonstrate that a material error has been made. All applicants will be advised of this right as part of the notification process. A review request can either be made by the applicant or on their behalf by a third-party and should outline in writing (i.e. or letter) the reasons why they do not agree with the decision. All requests must be received within 28 days of the applicant being notified of the original decision on their application. The review will be undertaken by a Benefits Manager within the Council s Benefit Service who has not been involved in the original application or decision-making process. The outcome of the review will be communicated to the applicant within 2 working days for Emergency Loans and 14 days for Support Grants. We will not accept review requests from applicants who do not meet the eligibility criteria, did not agree to the terms and conditions set out in the application process or subsequently failed to fully comply with these terms and conditions.

12 5. Management Of The Scheme The Local Support Scheme policy sets out a process of fair and equitable decision making for the disbursement of limited funding provided by the DWP. It is important to note that, as with the DWP scheme, if all funds from the scheme have been spent, it will not be possible to approve any further loans or grants, regardless of whether the individual applying has met the criteria set out here. In these circumstances, the Council will endeavour to identify alternative sources of support that may be available to individuals. It will not be possible to request a review of a decision on these grounds. The criteria set out in this policy have been designed to prevent funding being exhausted too quickly during the financial year. It is the intention of the Council to review the scheme during the first year to determine whether we are able to amend the criteria set out in this policy to enable us to more appropriately meet the needs of residents in future years.

13 Appendix 1: Glossary of terms For the purposes of applying this policy, qualifying benefit will mean: Income Support, Job Seekers Allowance (income based) Employment Support Allowance (income related) Pension Credit (any type) For the purposes of applying this policy, excluded person will mean: People in hospital or care homes (unless within 2 weeks of discharge) Prisoners, members of Religious Orders, persons in relevant education who do not qualify for Qualifying Benefits. Or a person subject to Immigration Control, which will mean: A person who is, or would be, treated as a Person From Abroad (PFA) but falls into a category where they have entitlement to IS, ESA(IR),JSA(IB) can be considered for an Emergency Loan (EL) in the normal way. A person who is, or would be, treated as a PFA for the purposes of IS,JSA(IB) or ESA(IR) and has no entitlement to those benefits can be considered for a EL only to alleviate the consequences of a disaster and will be classed as an Exceptional Person and will be required to provide evidence of the disaster. For the purposes of applying this policy, we will apply the following savings thresholds: for Support Grants: Working Age capital threshold 500 Pension Age threshold 1000 Applications for total payment in excess of these amounts which are considered for payment will have these excess capital amounts deducted from the award given Additionally, for emergency Loans we will consider whether any income, insurances and/ or capital available to the applicant and/or partner will be taken into account in meeting the need presented. For the purposes of applying this policy, excluded item will mean: a need which occurs outside the U.K. an educational or training need, including clothing or tools distinctive school uniform, sports clothes or equipment travelling expenses to and from school school meals in certain circumstances expenses in connection with court proceedings such as fees, fines or costs removal costs on permanent re-housing by the local authority following homelessness, a compulsory purchase order or closing order the cost of domestic assistance or respite care repairs to property owned by the local authority or public housing bodies

but falls into a category where they have entitlement to IS,")

14 medical, surgical, optical, aural or dental items or services. A medical item should not include everyday items needed because of a medical condition, for example, cotton sheets due to allergies to synthetics work-related expenses, for example fares, work clothes debts to Government Departments, for example Income Tax or National Insurance arrears investments Council Tax, water charges most housing costs, for example deposits, mortgages, rent, service charges, hostel charges, major repairs telephone costs travel costs In addition the following items are excluded from Support Grants: fuel and standing charges any expenses which the local authority has a statutory duty to provide any daily living expenses mobility need any travel expenses/costs holidays television or radio charges garaging, parking, purchase and running costs of any motor vehicle except where payment is considered for emergency travel expenses maternity or funeral expenses as they are covered through the regulated Social Fund any item/service provided by another Local Authority Department

15 Appendix 2: Schedule of award levels Items Household type Item Average high street cost 1 x bedframe (single) nil 1 X mattress nil 1x wardrobe (canvas) x bedding sets 2x 8.00= x quilt/pillow = x chest of drawers(canvas) Start up menu: Single person 1 x minicooker x table + chairs X sofa bed X pots and pans x crockery/cutlery x fridge inc delivery TOTAL PACKAGE x wardrobe (canvas) x quilt /pillow = x bedding sets 2x = x chest of drawers (canvas) x minicooker Start up menu: Couple 1x table + chairs X sofabed X pots and pans x crockery/cutlery x fridge inc delivery TOTAL PACKAGE x travel cot and mattress x cot bedding x mattress x bed x wardrobe (canvas) x quilt and pillows Lone parent + 1 child under 2yrs 1x bedding set x chest of drawers (canvas) x minicooker x table + 4 chairs X pots and pans x crockery/cutlery x fridge/freezer inc delivery TOTAL PACKAGE x bed (single) 2x X mattress 2x x wardrobe (canvas) x quilt and pillows Lone parent + 1 child 2yrs plus 4x bedding sets 32.00

35.00 1 x minicooker 85.00 Start up menu: Couple 1x table + chairs 80.00 1 X sofabed 170.00 1 X pots and pans 20.00 1 x crockery/cutlery 16.")

16 2 x chest of drawers (canvas) x minicooker x table + 4 chairs X pots and pans x crockery/cutlery x fridge/freezer inc delivery TOTAL PACKAGE x travel cot and mattress x cot bedding x wardrobe (canvas) x quilt /pillow = x bedding sets 2x = x chest of drawers (canvas) COUPLE + 1 child under 2yrs 1 x minicooker x table + chairs nil 1 X sofabed X pots and pans x crockery/cutlery x fridge inc delivery TOTAL PACKAGE Bed Double + mattress Bedding set double + duvet, sheet and 2x pillows Bed Single + mattress Bedding set single + duvet, sheet and pillow Couple plus 1 child 2yrs + 2 x chest of drawers (canvas) x minicooker x table + 4 chairs X pots and pans x crockery/cutlery x fridge/freezer inc delivery x wardrobe (canvas) TOTAL PACKAGE Amount per each additional child under 2yrs Cot/bedding/crockery/ Amount per each additional child 2ryrs plus Bed/bedding/crockery/ Cooker awarded for family unit with 2+children 169 Cooker (electric only) inc delivery 180 Fridge/freezer inc delivery Bed Single + mattress Bed Double + mattress Bedding set single + duvet, sheet and pillow Bedding set double + duvet, sheet and 2x pillows Single items Table and 4 chairs 80.00

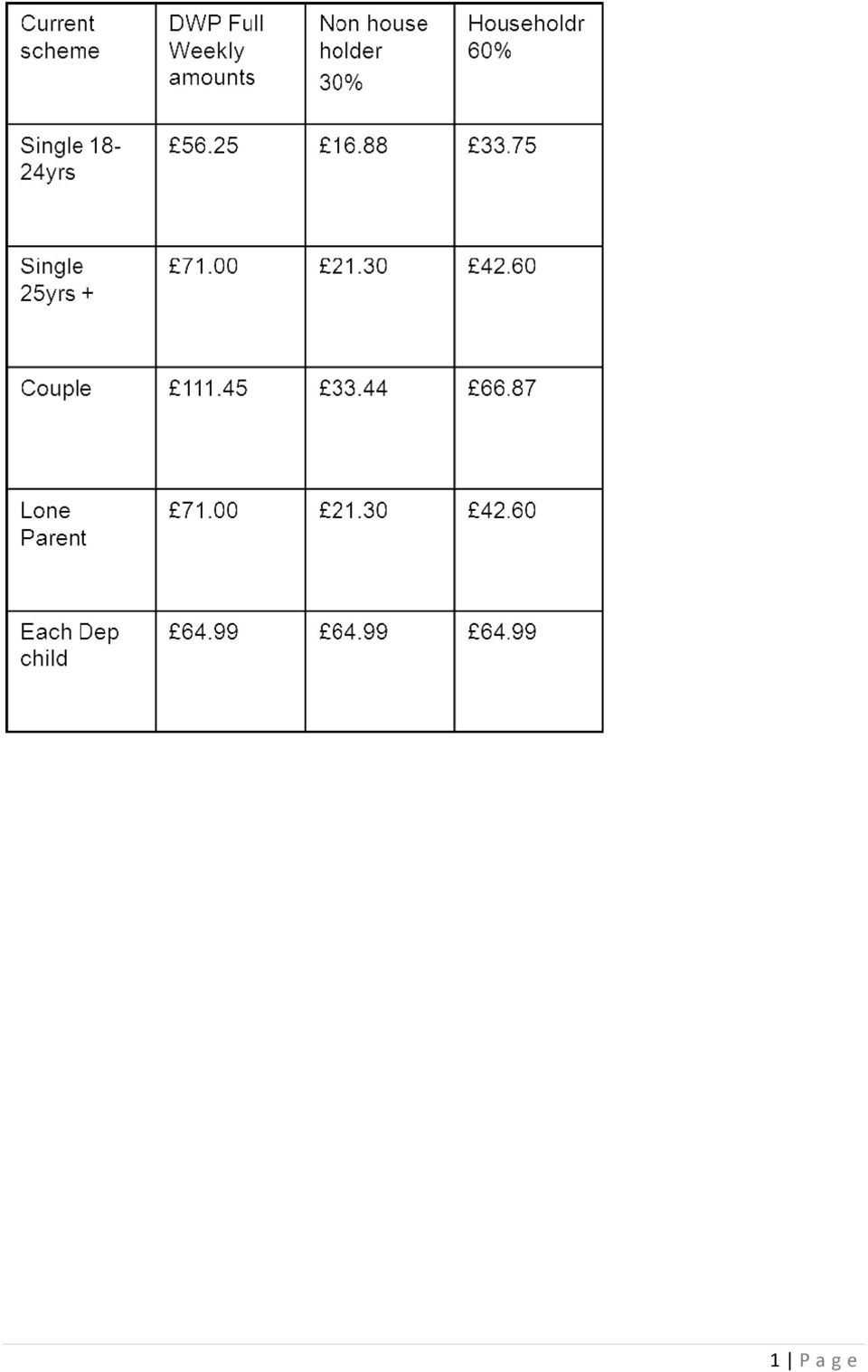

17 Wardrobe Chest of drawers Washing machine (inc delivery and installation) Crockery + cutlery Pots and pans x minicooker Clothing + footwear child under Clothing " child Clothing " child Clothing and footwear Adult (17yrs +) Living expenses Current scheme DWP full weekly Non amount householder Householder Single years Single 25 years Couple Lone parent Each dependent child

18

Wigan Council Local Welfare Support Policy. January 2016

Wigan Council Local Welfare Support Policy January 2016 Wigan Council Local Welfare Support Service Policy January 2016 1. Introduction 1.1 As part of the Welfare Reform Act 2012, the discretionary element

Wigan Council Local Welfare Support Policy January 2016 Wigan Council Local Welfare Support Service Policy January 2016 1. Introduction 1.1 As part of the Welfare Reform Act 2012, the discretionary element

Wakefield Council - Local Welfare Provision Scheme Policy (updated July 2014)

") Wakefield Council - Local Welfare Provision Scheme Policy (updated July 2014) 1. Background 1.1 From 1st April 2013 elements of the Social Fund; Community Care Grants (CCG) and Crisis Loans (CL) will be

Wakefield Council - Local Welfare Provision Scheme Policy (updated July 2014) 1. Background 1.1 From 1st April 2013 elements of the Social Fund; Community Care Grants (CCG) and Crisis Loans (CL) will be

UPDATED. XyxxYy. Benefit Changes. The Government is cutting benefits. 1 in 7 people will be affected. Are you prepared?

UPDATED Benefit Changes XyxxYy The Government is cutting benefits. 1 in 7 people will be affected. Are you prepared? 1 XyxxYy ARE YOU PREPARED FOR UNIVERSAL CREDIT? Most people in Sheffield who currently

UPDATED Benefit Changes XyxxYy The Government is cutting benefits. 1 in 7 people will be affected. Are you prepared? 1 XyxxYy ARE YOU PREPARED FOR UNIVERSAL CREDIT? Most people in Sheffield who currently

EAST AYRSHIRE COUNCIL CABINET: WEDNESDAY 13 MARCH 2013 WELFARE REFORM UPDATE ON IMPLEMENTATION ARRANGEMENTS

EAST AYRSHIRE COUNCIL CABINET: WEDNESDAY 13 MARCH 2013 WELFARE REFORM UPDATE ON IMPLEMENTATION ARRANGEMENTS Report by the Executive Director of Finance and Corporate Support 1. PURPOSE OF THE REPORT 1.1

EAST AYRSHIRE COUNCIL CABINET: WEDNESDAY 13 MARCH 2013 WELFARE REFORM UPDATE ON IMPLEMENTATION ARRANGEMENTS Report by the Executive Director of Finance and Corporate Support 1. PURPOSE OF THE REPORT 1.1

Sheffield Benefits Service

Sheffield Benefits Service April 2013 Housing Benefit & Council Tax Support for people of working age Housing Benefit and Council Tax Support Housing Benefit is a national welfare benefit, administered

Sheffield Benefits Service April 2013 Housing Benefit & Council Tax Support for people of working age Housing Benefit and Council Tax Support Housing Benefit is a national welfare benefit, administered

Crisis Policy Briefing Universal Credit: Frequently Asked Questions. July 2016

Crisis Policy Briefing Universal Credit: Frequently Asked Questions July 2016 Crisis Policy Briefing: Universal Credit Frequently Asked Questions 2 Introduction Universal Credit is the Government s new,

Crisis Policy Briefing Universal Credit: Frequently Asked Questions July 2016 Crisis Policy Briefing: Universal Credit Frequently Asked Questions 2 Introduction Universal Credit is the Government s new,

Universal Credit: Frequently Asked Questions October 2012

Universal Credit: Frequently Asked Questions October 2012 Introduction Universal Credit (UC) is the Government s new, simplified working age welfare system, rolling several benefits and tax credits into

Universal Credit: Frequently Asked Questions October 2012 Introduction Universal Credit (UC) is the Government s new, simplified working age welfare system, rolling several benefits and tax credits into

How to make a claim for benefits

GUIDE TO BENEFITS How to make a claim for benefits This is a basic guide to benefit entitlements; please ensure that you discuss with your Resettlement Officer before you make a claim for benefits. You

GUIDE TO BENEFITS How to make a claim for benefits This is a basic guide to benefit entitlements; please ensure that you discuss with your Resettlement Officer before you make a claim for benefits. You

APRIL 2015 CARE AND SUPPORT CHARGING POLICY

APRIL 2015 CARE AND SUPPORT CHARGING POLICY London Borough of Barking and Dagenham Care and Support Fairer Charging Policy 1.0 Introduction 1.1 The Care and Support Charging Policy is designed that the

APRIL 2015 CARE AND SUPPORT CHARGING POLICY London Borough of Barking and Dagenham Care and Support Fairer Charging Policy 1.0 Introduction 1.1 The Care and Support Charging Policy is designed that the

Fairer Contributions Policy

Appendix 6 Fairer Contributions Policy July 2011 Adult and Community Services Fairer Contributions Policy 1. Introduction 1.1 The Fairer Contributions Policy is designed to ensure that people pay a fair

Appendix 6 Fairer Contributions Policy July 2011 Adult and Community Services Fairer Contributions Policy 1. Introduction 1.1 The Fairer Contributions Policy is designed to ensure that people pay a fair

The Social Fund. Part of the Department for Work and Pensions

The Social Fund Part of the Department for Work and Pensions What is the Social Fund? If you are on a low income and faced with costs that are difficult to pay for out of your normal income, the Social

The Social Fund Part of the Department for Work and Pensions What is the Social Fund? If you are on a low income and faced with costs that are difficult to pay for out of your normal income, the Social

EXPLANATORY MEMORANDUM TO THE UNIVERSAL CREDIT (CONSEQUENTIAL, SUPPLEMENTARY, INCIDENTAL AND MISCELLANEOUS PROVISIONS) REGULATIONS 2013. 2013 No.

REGULATIONS 2013. 2013 No.") EXPLANATORY MEMORANDUM TO THE UNIVERSAL CREDIT (CONSEQUENTIAL, SUPPLEMENTARY, INCIDENTAL AND MISCELLANEOUS PROVISIONS) REGULATIONS 2013 2013 No. 630 1. This explanatory memorandum has been prepared by

EXPLANATORY MEMORANDUM TO THE UNIVERSAL CREDIT (CONSEQUENTIAL, SUPPLEMENTARY, INCIDENTAL AND MISCELLANEOUS PROVISIONS) REGULATIONS 2013 2013 No. 630 1. This explanatory memorandum has been prepared by

WELFARE REFORM UPDATE

APPENDIX B WELFARE REFORM UPDATE Benefit Cap The Benefit Cap is currently being implemented in Portsmouth. Household benefit payments will be capped at 500 per week for a family or single parent or 350

APPENDIX B WELFARE REFORM UPDATE Benefit Cap The Benefit Cap is currently being implemented in Portsmouth. Household benefit payments will be capped at 500 per week for a family or single parent or 350

Housing options for single parents

Formed from the merger of the National Council for One Parent Families and Gingerbread Factsheet For single parents in England and Wales February 2012 Freephone 0808 802 0925 Gingerbread Single Parent

Formed from the merger of the National Council for One Parent Families and Gingerbread Factsheet For single parents in England and Wales February 2012 Freephone 0808 802 0925 Gingerbread Single Parent

University of Bolton Hardship Fund Frequently Asked Questions Information Sheet

University of Bolton Hardship Fund Frequently Asked Questions Information Sheet What is the Hardship Fund? The Hardship Fund is to help students facing financial hardship. It can provide nonrepayable awards

University of Bolton Hardship Fund Frequently Asked Questions Information Sheet What is the Hardship Fund? The Hardship Fund is to help students facing financial hardship. It can provide nonrepayable awards

Policy and Procedures for the Recovery of Council tax and Business Rates

Scope and Purpose of this Policy Policy and Procedures for the Recovery of Council tax and Business Rates 1 The purpose is to establish a policy to ensure consistency, equality and probity in the collection

Scope and Purpose of this Policy Policy and Procedures for the Recovery of Council tax and Business Rates 1 The purpose is to establish a policy to ensure consistency, equality and probity in the collection

Council Tax Service Revenues and Benefits Unit Debt Recovery Policy 2015/16

Council Tax Service Revenues and Benefits Unit Debt Recovery Policy 2015/16 Version 1.8 April 2015 1 Contents Page No. 1. Recovery process up to the liability order stage 1 2. Hardship 4 3. Recovery process

Council Tax Service Revenues and Benefits Unit Debt Recovery Policy 2015/16 Version 1.8 April 2015 1 Contents Page No. 1. Recovery process up to the liability order stage 1 2. Hardship 4 3. Recovery process

In simple terms your return on investment of renting out a property is affected by two main things: rental income and your expenses.

Copyright 2015 Letcom property agents 2015 Table of Contents 1 Introduction...2 2 Return on Your Investment...2 2.1 Rental Income...2 2.2 Expenses...3 3 Agreements and Legal Requirements...3 3.1 Agency

Copyright 2015 Letcom property agents 2015 Table of Contents 1 Introduction...2 2 Return on Your Investment...2 2.1 Rental Income...2 2.2 Expenses...3 3 Agreements and Legal Requirements...3 3.1 Agency

Dealing with debt - toolkit Information from Southampton City Council. Step 5. Tackle the most important debts first

Dealing with debt - toolkit Information from Southampton City Council Step 5. Tackle the most important debts first Step 5. Tackle the most important debts first priority creditors. Some debts are more

Dealing with debt - toolkit Information from Southampton City Council Step 5. Tackle the most important debts first Step 5. Tackle the most important debts first priority creditors. Some debts are more

Application for Discretionary Housing Payment/Council Tax Discretionary Relief

Application for Discretionary Housing Payment/Council Tax Discretionary Relief Name & Address: Date of Issue: Council Tax Account Number: Email Address and Contact Number: Housing Benefit Claim Reference:

Application for Discretionary Housing Payment/Council Tax Discretionary Relief Name & Address: Date of Issue: Council Tax Account Number: Email Address and Contact Number: Housing Benefit Claim Reference:

Make your budget work for you

Welfare Reform Make your budget work for you www.milton-keynes.gov.uk/welfare-reform Make your budget work for you Why budget It s always a good idea to keep track of your money. Budgeting is keeping track

Welfare Reform Make your budget work for you www.milton-keynes.gov.uk/welfare-reform Make your budget work for you Why budget It s always a good idea to keep track of your money. Budgeting is keeping track

Business Debtline www.businessdebtline.org 0800 0838 018 BANKRUPTCY

BUSINESS DEBTLINE Business Debtline www.businessdebtline.org 0800 0838 018 BANKRUPTCY FACT SHEET NO. 10 NORTHERN IRELAND What is bankruptcy? Bankruptcy is a way of dealing with debts that you cannot pay.

BUSINESS DEBTLINE Business Debtline www.businessdebtline.org 0800 0838 018 BANKRUPTCY FACT SHEET NO. 10 NORTHERN IRELAND What is bankruptcy? Bankruptcy is a way of dealing with debts that you cannot pay.

Priority debt strategy chart

Priority debt strategy chart Compiled by Meg van Rooyen, Policy Manager and Deborah Shields, Information Manager, Money Advice Trust. Last updated February 2012 Using this list of sanctions as a guide,

Priority debt strategy chart Compiled by Meg van Rooyen, Policy Manager and Deborah Shields, Information Manager, Money Advice Trust. Last updated February 2012 Using this list of sanctions as a guide,

Crisis Policy Briefing Housing Benefit cuts. December 2011

Crisis Policy Briefing Housing Benefit cuts December 2011 Crisis Policy Briefing: Housing Benefit cuts 2 Overview Housing Benefit is vital in supporting people with their housing costs and in ensuring

Crisis Policy Briefing Housing Benefit cuts December 2011 Crisis Policy Briefing: Housing Benefit cuts 2 Overview Housing Benefit is vital in supporting people with their housing costs and in ensuring

LOCAL HOUSING ALLOWANCE SAFEGUARD POLICY. Flintshire Unified Benefits & Advisory Service Policy Document

LOCAL HOUSING ALLOWANCE SAFEGUARD POLICY Flintshire Unified Benefits & Advisory Service Policy Document Introduction The Local Housing Allowance is a new scheme of Housing Benefit for people living in

LOCAL HOUSING ALLOWANCE SAFEGUARD POLICY Flintshire Unified Benefits & Advisory Service Policy Document Introduction The Local Housing Allowance is a new scheme of Housing Benefit for people living in

16 18 Bursary scheme, 24+ Loans Bursary & ncn Discretionary Learner Support fund. Guidelines for the disbursement of funds in 2014/15 academic year

16 18 Bursary scheme, 24+ Loans Bursary & ncn Discretionary Learner Support fund Guidelines for the disbursement of funds in 2014/15 academic year CONTENTS Page 1. Background 3 2. ncn 16 18 Bursary Scheme,

16 18 Bursary scheme, 24+ Loans Bursary & ncn Discretionary Learner Support fund Guidelines for the disbursement of funds in 2014/15 academic year CONTENTS Page 1. Background 3 2. ncn 16 18 Bursary Scheme,

Application for a Discretionary Housing Payment

RBBNBDHP Benefit Ref : Date of issue:... To :........ Application for a Discretionary Housing Payment Please return this form by post to: Harrogate Borough Council, Benefit Services, PO Box 787, Harrogate,

RBBNBDHP Benefit Ref : Date of issue:... To :........ Application for a Discretionary Housing Payment Please return this form by post to: Harrogate Borough Council, Benefit Services, PO Box 787, Harrogate,

Introduction. Information on transferring payments to the UK 37. National Insurance Number 46. Jobseekers allowance 52.

Introduction XX Information on transferring payments to the UK 37 National Insurance Number 46 Jobseekers allowance 52 Crisis loans 60 Income support 65 Working Tax Credit 73 Statutory Sick Pay 78 Incapacity

Introduction XX Information on transferring payments to the UK 37 National Insurance Number 46 Jobseekers allowance 52 Crisis loans 60 Income support 65 Working Tax Credit 73 Statutory Sick Pay 78 Incapacity

Universal Credit and families: questions and answers

August 2015 Universal Credit and families: questions and answers Q. What is Universal Credit? Universal Credit is a new benefit that supports people who are on a low income or out of work, and helps ensure

August 2015 Universal Credit and families: questions and answers Q. What is Universal Credit? Universal Credit is a new benefit that supports people who are on a low income or out of work, and helps ensure

2014 No. 2672 SOCIAL CARE, ENGLAND. The Care and Support (Charging and Assessment of Resources) Regulations 2014

Regulations 2014") S T A T U T O R Y I N S T R U M E N T S 2014 No. 2672 SOCIAL CARE, ENGLAND The Care and Support (Charging and Assessment of Resources) Regulations 2014 Made - - - - 22nd October 2014 Laid before Parliament

S T A T U T O R Y I N S T R U M E N T S 2014 No. 2672 SOCIAL CARE, ENGLAND The Care and Support (Charging and Assessment of Resources) Regulations 2014 Made - - - - 22nd October 2014 Laid before Parliament

Get in on the Act. The Care Act 2014. Corporate

Get in on the Act The Care Act 2014 Corporate Get in on the Act The Care Act 2014 Background The Care Act was first published as a Bill in the House of Lords on 9 May 2013, following prelegislative scrutiny.

Get in on the Act The Care Act 2014 Corporate Get in on the Act The Care Act 2014 Background The Care Act was first published as a Bill in the House of Lords on 9 May 2013, following prelegislative scrutiny.

Other financial help

Other financial help Grants Health Costs Housing Costs Help with debt Extra money for families Other financial help Many families are missing out on extra money that is available. The following is a list

Other financial help Grants Health Costs Housing Costs Help with debt Extra money for families Other financial help Many families are missing out on extra money that is available. The following is a list

Phone: 01709 336065 Website: www.rotherham.gov.uk. Request for Discretionary Housing Payment

Rotherham Metropolitan Borough Council Housing and Council Tax Benefit Section Riverside House Main Street Rotherham S65 1UF Phone: 01709 336065 Website: www.rotherham.gov.uk Name and address Reference

Rotherham Metropolitan Borough Council Housing and Council Tax Benefit Section Riverside House Main Street Rotherham S65 1UF Phone: 01709 336065 Website: www.rotherham.gov.uk Name and address Reference

Residential mortgages general information

Residential mortgages general information Residential mortgages general information 2 Contents Who we are and what we do 2 Forms of security 2 Representative Example 2 Indication of possible further costs

Residential mortgages general information Residential mortgages general information 2 Contents Who we are and what we do 2 Forms of security 2 Representative Example 2 Indication of possible further costs

Contents. Introduction... Page. Rent...Page 3. Council Tax...Page 4. Water...Page 4. Gas and Electricity... Page 5. Energy Efficiency Page 6

The co a Contents Introduction... Page Rent...Page 3 Council Tax...Page 4 Water...Page 4 Gas and Electricity... Page 5 Energy Efficiency Page 6 TV Licence...Page 6 Cable/Satellite TV...Page 6 Landline/Mobile

The co a Contents Introduction... Page Rent...Page 3 Council Tax...Page 4 Water...Page 4 Gas and Electricity... Page 5 Energy Efficiency Page 6 TV Licence...Page 6 Cable/Satellite TV...Page 6 Landline/Mobile

December 2009 HOMELESS? This leaflet explains what happens if you make a homeless application and the rules we use.

December 2009 HOMELESS? This leaflet explains what happens if you make a homeless application and the rules we use. This leaflet can be supplied in community languages, large print, audio tape/cd or Braille.

December 2009 HOMELESS? This leaflet explains what happens if you make a homeless application and the rules we use. This leaflet can be supplied in community languages, large print, audio tape/cd or Braille.

Providing. more than a room. Guide to benefi ts, tax and insurance. The four agency SUPPORTED LODGINGS project May 2011

The four agency SUPPORTED LODGINGS project May 2011 funded by Communities and Local Government Providing more than a room Guide to benefi ts, tax and insurance The Four Agency Supported Lodgings Project

The four agency SUPPORTED LODGINGS project May 2011 funded by Communities and Local Government Providing more than a room Guide to benefi ts, tax and insurance The Four Agency Supported Lodgings Project

TERMS & CONDITIONS FULLY MANAGED SERVICE

TERMS & CONDITIONS FULLY MANAGED SERVICE For the purpose of this agreement the following definitions will apply:- Keywest Estate Agents Ltd shall be known as The Agent... shall be known as The Owner..

TERMS & CONDITIONS FULLY MANAGED SERVICE For the purpose of this agreement the following definitions will apply:- Keywest Estate Agents Ltd shall be known as The Agent... shall be known as The Owner..

Factsheet 56 Benefits for people under Pension Credit age

Factsheet 56 Benefits for people under Pension Credit age April 2016 About this factsheet This factsheet gives information about benefits for people under Pension Credit age (this is 63 years as of April

Factsheet 56 Benefits for people under Pension Credit age April 2016 About this factsheet This factsheet gives information about benefits for people under Pension Credit age (this is 63 years as of April

Mortgage Arrears Resolution Process (MARP) Booklet. Important information for customers experiencing financial difficulties

Booklet. Important information for customers experiencing financial difficulties") Mortgage Arrears Resolution Process (MARP) Booklet Important information for customers experiencing financial difficulties The Mortgage Arrears Resolution Process (MARP) We at Start Mortgages recognise

Mortgage Arrears Resolution Process (MARP) Booklet Important information for customers experiencing financial difficulties The Mortgage Arrears Resolution Process (MARP) We at Start Mortgages recognise

If instalments are not paid as they are due a reminder will be sent requiring payments to be brought up to date within 7 days.

APPENDIX 1 DEBT RECOVERY POLICY This debt recovery policy of South Lakeland District Council aims to maximise income from all revenue generating sources whilst incorporating a sympathetic approach to the

APPENDIX 1 DEBT RECOVERY POLICY This debt recovery policy of South Lakeland District Council aims to maximise income from all revenue generating sources whilst incorporating a sympathetic approach to the

APPLICATION FOR FINANCIAL ASSISTANCE

CHARITY NUMBER 1106218 APPLICATION FOR FINANCIAL ASSISTANCE ALTERNATIVELY APPLY ONLINE VIA THE TRUST S WEBSITE WWW.BRITISHGASENERGYTRUST.ORG.UK BEFORE COMPLETING THE APPLICATION FORM, PLEASE CAREFULLY

CHARITY NUMBER 1106218 APPLICATION FOR FINANCIAL ASSISTANCE ALTERNATIVELY APPLY ONLINE VIA THE TRUST S WEBSITE WWW.BRITISHGASENERGYTRUST.ORG.UK BEFORE COMPLETING THE APPLICATION FORM, PLEASE CAREFULLY

FACT SHEET. Money matters. Paying bills

12 FACT SHEET Money matters This fact sheet provides advice and information about how best to manage your money to make it easier to manage your household expenses. It also provides details of agencies

12 FACT SHEET Money matters This fact sheet provides advice and information about how best to manage your money to make it easier to manage your household expenses. It also provides details of agencies

A Landlord s Guide to Housing Benefit

A Landlord s Guide to Housing Benefit October 2009 A landlord s guide to Housing Benefit; Table of Contents Introduction...3 Standards Of Service...3 Processing Housing Benefit Claims...3 Changes in circumstances...3

A Landlord s Guide to Housing Benefit October 2009 A landlord s guide to Housing Benefit; Table of Contents Introduction...3 Standards Of Service...3 Processing Housing Benefit Claims...3 Changes in circumstances...3

HOUSING BENEFIT MONEY ADVICE TAX ESA CREDITS PENSION CREDIT JOBSEEKER S ALLOWANCE BEDROOM RENT/ FACTORING ARREARS TAX. Benefits & Debt Services Guide

TAX CREDITS JOBSEEKER S ALLOWANCE MONEY ADVICE ESA HOUSING BENEFIT PENSION CREDIT RENT/ FACTORING ARREARS BEDROOM TAX Benefits & Debt Services Guide We know that the benefits system can be complex and

TAX CREDITS JOBSEEKER S ALLOWANCE MONEY ADVICE ESA HOUSING BENEFIT PENSION CREDIT RENT/ FACTORING ARREARS BEDROOM TAX Benefits & Debt Services Guide We know that the benefits system can be complex and

LANDLORD INFORMATION PACK FOR RESIDENTIAL LETTINGS AND PROPERTY MANAGEMENT

LANDLORD INFORMATION PACK FOR RESIDENTIAL LETTINGS AND PROPERTY MANAGEMENT 25 High Street, Warwick, CV34 4BB 01926 492511 [email protected] www.godfrey-payton.co.uk Godfrey-Payton has a huge

LANDLORD INFORMATION PACK FOR RESIDENTIAL LETTINGS AND PROPERTY MANAGEMENT 25 High Street, Warwick, CV34 4BB 01926 492511 [email protected] www.godfrey-payton.co.uk Godfrey-Payton has a huge

POLICY FOR THE BREATHING SPACE SCHEME

POLICY FOR THE BREATHING SPACE SCHEME PREFACE The Council is participating in a regional scheme called Breathing Space. The scheme facilitates the provision of loans in accordance with powers given under

POLICY FOR THE BREATHING SPACE SCHEME PREFACE The Council is participating in a regional scheme called Breathing Space. The scheme facilitates the provision of loans in accordance with powers given under

Local Housing Allowance. Safeguard Policy

Local Housing Allowance Safeguard Policy Introduction: Under Local Housing Allowance housing benefit will usually be paid direct to the person applying for housing benefit (claimant). However, the purpose

Local Housing Allowance Safeguard Policy Introduction: Under Local Housing Allowance housing benefit will usually be paid direct to the person applying for housing benefit (claimant). However, the purpose

Keeping your home: home owners

Keeping your home: home owners What help can I get to pay my mortgage? What should I do if I can t pay my mortgage? Can a lender repossess my home? provided by the Citizens Information Board provided by

Keeping your home: home owners What help can I get to pay my mortgage? What should I do if I can t pay my mortgage? Can a lender repossess my home? provided by the Citizens Information Board provided by

How To Help The Council With Its Finances

COUNCIL TAX AND BUSINESS RATES RECOVERY PROCEDURE SECTIONS 1. The Council s Aims 2. The Revenues Service 3. The Legal Framework 4. Demand Notice 5. Joint & Several Liability 6. Instalments 7. Methods of

COUNCIL TAX AND BUSINESS RATES RECOVERY PROCEDURE SECTIONS 1. The Council s Aims 2. The Revenues Service 3. The Legal Framework 4. Demand Notice 5. Joint & Several Liability 6. Instalments 7. Methods of

Housing Benefit & Council Tax Reduction 2015-2016 Benefits Ref:

Housing Benefit & Council Tax Reduction 2015-2016 Benefits Ref: Housing Benefit and Council Tax Reductions are normally granted from the Monday following the day you apply so do not delay in making an

Housing Benefit & Council Tax Reduction 2015-2016 Benefits Ref: Housing Benefit and Council Tax Reductions are normally granted from the Monday following the day you apply so do not delay in making an

Pre-Action Protocol for Possession Claims based on Mortgage or Home Purchase Plan Arrears in Respect of Residential Property

Pre-Action Protocol for Possession Claims based on Mortgage or Home Purchase Plan Arrears in Respect of Residential Property PROTOCOLS Contents I INTRODUCTION 1 Preamble 2 Aims 3 Scope 4 Definitions II

Pre-Action Protocol for Possession Claims based on Mortgage or Home Purchase Plan Arrears in Respect of Residential Property PROTOCOLS Contents I INTRODUCTION 1 Preamble 2 Aims 3 Scope 4 Definitions II

There may be other deductions you can claim that are not included in this guide.

Claiming work-related expenses may 1. Guide This guide will help you work out what work-related expenses you can claim a tax deduction for and the conditions you must meet before you can claim your expenses.

Claiming work-related expenses may 1. Guide This guide will help you work out what work-related expenses you can claim a tax deduction for and the conditions you must meet before you can claim your expenses.

Rights of the borrower (mortgagor) Negotiating with the lender. Mortgage rescue schemes. Can I get any help with my mortgage

Negotiating with the lender. Mortgage rescue schemes. Can I get any help with my mortgage") Contents The need to act quickly Available options Rights of the borrower (mortgagor) Negotiating with the lender Going to court Mortgage rescue schemes Secured loans Can I get any help with my mortgage

Contents The need to act quickly Available options Rights of the borrower (mortgagor) Negotiating with the lender Going to court Mortgage rescue schemes Secured loans Can I get any help with my mortgage

The National Benevolent Charity. Application Form

The National Benevolent Charity Application Form The National Benevolent Charity was founded in 1812 by Peter Hervé to give pensions and allowances to the poor and distressed. Over 200 years later the

The National Benevolent Charity Application Form The National Benevolent Charity was founded in 1812 by Peter Hervé to give pensions and allowances to the poor and distressed. Over 200 years later the

Student Money Advice & Rights Team (SMART) Hardship Fund 2015/16

Hardship Fund 2015/16") Student Money Advice & Rights Team (SMART) Hardship Fund 2015/16 Please retain guidance notes for your information. The NEW SMART Hardship Fund (SHF) is available from 9 th November 2015 to provide extra

Student Money Advice & Rights Team (SMART) Hardship Fund 2015/16 Please retain guidance notes for your information. The NEW SMART Hardship Fund (SHF) is available from 9 th November 2015 to provide extra

DWP: Evaluation of Removal of the Spare Room Subsidy (Bedroom Tax)

") Housing Strategy and Development Briefing Note 14/10 DWP: Evaluation of Removal of the Spare Room Subsidy (Bedroom Tax) October 2014 Introduction Welcome to a series of regular briefings prepared by the

Housing Strategy and Development Briefing Note 14/10 DWP: Evaluation of Removal of the Spare Room Subsidy (Bedroom Tax) October 2014 Introduction Welcome to a series of regular briefings prepared by the

Guide to the Debt Recovery Process

Guide to the Debt Recovery Process How it works, and what we The debt recovery process can seem confusing and daunting. We aim to simplify it as much as we can, and to make clear from the outset what we

Guide to the Debt Recovery Process How it works, and what we The debt recovery process can seem confusing and daunting. We aim to simplify it as much as we can, and to make clear from the outset what we

How to Guide (Getting your Deferment Application Form right)

") How to Guide (Getting your Deferment Application Form right) Use these notes to help you complete your student loan Deferment Application Form If you need any help, please go to www.erudiostudentloans.co.uk

How to Guide (Getting your Deferment Application Form right) Use these notes to help you complete your student loan Deferment Application Form If you need any help, please go to www.erudiostudentloans.co.uk

APPENDIX 1. LB Lambeth Income and Debt Recovery Strategy 2015/17

APPENDIX 1 LB Lambeth Income and Debt Recovery Strategy 2015/17 For Lambeth council, responsible financial management is critical to enabling the delivery of over 100 core services efficiently and sustainably.

APPENDIX 1 LB Lambeth Income and Debt Recovery Strategy 2015/17 For Lambeth council, responsible financial management is critical to enabling the delivery of over 100 core services efficiently and sustainably.

BURSARY FUND/ DISCRETIONARY LEARNER SUPPORT FUND POLICY & PROCEDURES 2014/2015

BURSARY FUND/ DISCRETIONARY LEARNER SUPPORT FUND POLICY & PROCEDURES 2014/2015 16-18 Bursary Fund 19+ Bursary Fund 24+ Adult Learning Loan Bursary Fund Contents Introduction 3 Policy Aims 3 Criteria and

BURSARY FUND/ DISCRETIONARY LEARNER SUPPORT FUND POLICY & PROCEDURES 2014/2015 16-18 Bursary Fund 19+ Bursary Fund 24+ Adult Learning Loan Bursary Fund Contents Introduction 3 Policy Aims 3 Criteria and

Housing Register Application Form

Housing Register Application Form creating communities to be proud of Housing Register Application Form Page About Us...1 Section 1: You and Your Household...2 Section 2: Your Eligibility...4 Section 3:

Housing Register Application Form creating communities to be proud of Housing Register Application Form Page About Us...1 Section 1: You and Your Household...2 Section 2: Your Eligibility...4 Section 3:

DRAFT NORTHAMPTON BOROUGH COUNCIL CORPORATE DEBT POLICY

DRAFT NORTHAMPTON BOROUGH COUNCIL CORPORATE DEBT POLICY Revised Draft 6 th May 2010 DRAFT Corporate Debt policy May 2010 v0.6.doc 1 1 INTRODUCTION 1.1 The Council levies charges and rent for a variety

DRAFT NORTHAMPTON BOROUGH COUNCIL CORPORATE DEBT POLICY Revised Draft 6 th May 2010 DRAFT Corporate Debt policy May 2010 v0.6.doc 1 1 INTRODUCTION 1.1 The Council levies charges and rent for a variety

Your Money, Your Choice

Your Money, Your Choice With rising living costs many people are looking for help when it comes to making the most of their money. Find out what help is available for you. www.rotherham.gov.uk Together

Your Money, Your Choice With rising living costs many people are looking for help when it comes to making the most of their money. Find out what help is available for you. www.rotherham.gov.uk Together

Renting a property fact sheet

Renting a property fact sheet Renting a property with Cornwall Council For a lot of people renting a house for the first time can be scary. But it doesn t need to be. In this fact sheet you will find information

Renting a property fact sheet Renting a property with Cornwall Council For a lot of people renting a house for the first time can be scary. But it doesn t need to be. In this fact sheet you will find information

Council Tax Relief on the Grounds of Hardship

Council Tax Relief on the Grounds of Hardship 1. Introduction 1.1 The Local Government Finance Act 1992 section 13a has always allowed for a discretionary relief of Council Tax in exceptional circumstances

Council Tax Relief on the Grounds of Hardship 1. Introduction 1.1 The Local Government Finance Act 1992 section 13a has always allowed for a discretionary relief of Council Tax in exceptional circumstances

Scottish Welfare Fund. A Guide To Additional Support

Scottish Welfare Fund A Guide To Additional Support Introduction This leaflet provides information about additional support for both Scottish Welfare Fund applicants and Angus residents in general. There

Scottish Welfare Fund A Guide To Additional Support Introduction This leaflet provides information about additional support for both Scottish Welfare Fund applicants and Angus residents in general. There

Benefits if you are sick or disabled

Welfare Benefits Council Tax Benefit Housing Benefit Benefits if you are sick or disabled information from the Mind in Enfield Advice Team Social Fund Sickness and/or disability can happen to anyone at

Welfare Benefits Council Tax Benefit Housing Benefit Benefits if you are sick or disabled information from the Mind in Enfield Advice Team Social Fund Sickness and/or disability can happen to anyone at

DSA. Guide to a Debt Settlement Arrangement

nseirbhís Dócmhainneachta na héirea DSA Guide to a Debt Settlement Arrangement n Insolvency Service of Ireland A Debt Settlement Arrangement enables an eligible insolvent debtor to reach agreement with

nseirbhís Dócmhainneachta na héirea DSA Guide to a Debt Settlement Arrangement n Insolvency Service of Ireland A Debt Settlement Arrangement enables an eligible insolvent debtor to reach agreement with

Help us to help you Contact us and work in partnership with your local Council

February 2016 Version 6 Torridge District Council A Fair Collection and Recovery of Debt Policy Help us to help you Contact us and work in partnership with your local Council Torridge District Council

February 2016 Version 6 Torridge District Council A Fair Collection and Recovery of Debt Policy Help us to help you Contact us and work in partnership with your local Council Torridge District Council

Crisis Policy Briefing Housing Benefit cuts. July 2012

Crisis Policy Briefing Housing Benefit cuts July 2012 Crisis Policy Briefing: Housing Benefit cuts 2 Overview Housing Benefit is vital in supporting people with their housing costs and in ensuring people

Crisis Policy Briefing Housing Benefit cuts July 2012 Crisis Policy Briefing: Housing Benefit cuts 2 Overview Housing Benefit is vital in supporting people with their housing costs and in ensuring people

Social Work Services Charging Policy

Educational and Social Services Social Work Services Social Work Services Charging Policy Date Completed: 04/02/2014 Date of Equality Impact Assessment: 04/02/2014 Date approved by Cabinet: Date Review

Educational and Social Services Social Work Services Social Work Services Charging Policy Date Completed: 04/02/2014 Date of Equality Impact Assessment: 04/02/2014 Date approved by Cabinet: Date Review

Summary of the Redbridge Council Tax Reduction Scheme for 2016/17

Summary of the Redbridge Council Tax Reduction Scheme for 2016/17 Eligibility People entitled to Council Tax Reduction under this scheme for any week will be those: Of working age as defined by the Department

Summary of the Redbridge Council Tax Reduction Scheme for 2016/17 Eligibility People entitled to Council Tax Reduction under this scheme for any week will be those: Of working age as defined by the Department

Public Trustee (Fees & Charges Notice) (No.1) 2015. Public Trustee Act 1978, section 17 PUBLIC TRUSTEE (FEES AND CHARGES NOTICE) (NO.

(No.1) 2015. Public Trustee Act 1978, section 17 PUBLIC TRUSTEE (FEES AND CHARGES NOTICE) (NO.") Public Trustee (Fees & Charges Notice) (No.1) 2015 Section Public Trustee Act 1978, section 17 PUBLIC TRUSTEE (FEES AND CHARGES NOTICE) (NO.1) 2015 TABLE OF PROVISIONS Page PART 1 PRELIMINARY... 5 1. Short

Public Trustee (Fees & Charges Notice) (No.1) 2015 Section Public Trustee Act 1978, section 17 PUBLIC TRUSTEE (FEES AND CHARGES NOTICE) (NO.1) 2015 TABLE OF PROVISIONS Page PART 1 PRELIMINARY... 5 1. Short

Paying for your own residential care

Paying for your own residential care June 2015 Page 1 Contents How will I know whether my needs have to be met by residential care?... 3 How do I find a home?... 3 How much will I have to pay towards the

Paying for your own residential care June 2015 Page 1 Contents How will I know whether my needs have to be met by residential care?... 3 How do I find a home?... 3 How much will I have to pay towards the

ACCESSING YOUR SUPERANNUATION EARLY. 1. Relief from current financial burden

ACCESSING YOUR ANNUATION EARLY This factsheet focuses on Accessing Superannuation Early. This fact sheet is for information only. It is recommended that you get legal advice about your situation. For more

ACCESSING YOUR ANNUATION EARLY This factsheet focuses on Accessing Superannuation Early. This fact sheet is for information only. It is recommended that you get legal advice about your situation. For more

PIA. Guide to a Personal Insolvency Arrangement

nseirbhís Dócmhainneachta na héirea PIA Guide to a Personal Insolvency Arrangement n Insolvency Service of Ireland A Personal Insolvency Arrangement enables an eligible insolvent debtor to reach agreement

nseirbhís Dócmhainneachta na héirea PIA Guide to a Personal Insolvency Arrangement n Insolvency Service of Ireland A Personal Insolvency Arrangement enables an eligible insolvent debtor to reach agreement

Making Homes Affordable Labour s Plan for Housing

Making Homes Affordable Labour s Plan for Housing Labour Making Homes Affordable.indd 1 10/02/2016 15:47 Every person should have access to good quality, secure, affordable housing, appropriate to their

Making Homes Affordable Labour s Plan for Housing Labour Making Homes Affordable.indd 1 10/02/2016 15:47 Every person should have access to good quality, secure, affordable housing, appropriate to their