New Standards on Subsidiaries and Joint Arrangements

|

|

|

- Philippa Higgins

- 8 years ago

- Views:

Transcription

1 New Standards on Subsidiaries and Joint Arrangements May 2015 Flash In September 2014, the Canadian Accounting Standards Board (AcSB) issued into Part II of the CPA Canada Handbook Accounting, Accounting Standards for Private Enterprises (ASPE) new Section 1591, Subsidiaries, which replaces Section 1590 of the same title and Accounting Guideline 15, Consolidation of Variable Interest Entities (AcG-15). At the same time, the AcSB also issued new Section 3056, Interests in Joint Arrangements, which replaces Section 3055, Interests in Joint Ventures, and amended Section 3051, Investments. The issuance of these new and amended sections also resulted in consequential amendments to various standards. Sections 1591 and 3056, amended Section 3051 and the consequential amendments to other standards apply to fiscal years beginning on or after January 1, Earlier application is permitted. The objective of this publication is to describe: the key differences and similarities between the new and replaced standards; the nature of the consequential amendments; in addition, it will remind readers about the main principles of Sections 1590 and 3055 that were retained in the new sections. This publication also discusses the consequential amendments to Section 4450, Reporting Controlled and Related Entities by Not-for-Profit Organizations, in Part III of the CPA Canada Handbook Accounting, Accounting Standards for Not-for-Profit Organizations.

2 Section 1591, Subsidiaries Why was Section 1591 issued? Since its publication, AcG-15 has often been criticized for the resulting practical issues relating to identifying and accounting for variable interest entities (VIE). Preparers still consider this guideline to be very complex and difficult to apply. In replacing Section 1590 and AcG-15 with Section 1591, the AcSB aims to promote the use of judgment by including new guidance to determine when control is obtained through means other than equity interests (for example, contractual arrangements). Comparison of the guidance of Section 1590 and AcG-15 and Section 1591 The key differences and similarities in assessing control and accounting for subsidiaries between Section 1590 and AcG-15 and Section 1591 are summarized below: Comparison of guidance Purpose and scope Definitions Assessing control through equity and voting interests Assessing control through potential voting interests Assessing control through contractual rights Accounting for subsidiaries Contractual arrangements between enterprises under common control are now scoped out of Section 1591 No changes to the definitions of control and subsidiary No significant changes No changes New guidance on determining whether an enterprise controls another enterprise through contractual rights Same accounting policy choices (cost method, equity method or consolidation); however, the accounting for the interest in the enterprise may be predicated on how the enterprise controls the subsidiary Purpose and scope Similar to Section 1590, Section 1591 establishes standards for subsidiaries in an enterprise s general purpose financial statements. Section 1591 carries forward the same scope exclusions as Section 1590 and some of the exclusions of AcG-15. An important new element that was added to the exclusions from the scope of Section 1591 pertains to the exclusion of accounting for contractual arrangements between enterprises under common control. This addition may have significant consequences for enterprises that were forced to consolidate enterprises that were under common control due to relationships arising from contractual arrangements such as guarantees, lease agreements or loans receivable. As a result of this change, these 2

3 enterprises will no longer have to assess whether a contractual arrangement with such an enterprise results in a control relationship; instead they can account for the contractual arrangement in accordance with the relevant standard in the CPA Canada Handbook Accounting (e.g., Section 3065, Leases). Definitions Section 1591 does not change the definitions of control or subsidiary presented in Section Thus, control of an enterprise is still defined as the continuing power to determine its strategic operating, investing and financing policies without the co-operation of others and a subsidiary is still an enterprise controlled by another enterprise (the parent) that has the right and ability to obtain future economic benefits from the resources of the enterprise and is exposed to the related risks. Nevertheless, Section 1591 specifies that in addition to being acquired through an equity interest in a subsidiary, control may be acquired by other means such as contractual arrangements or a combination of voting interests, potential voting interests or contractual arrangements. Control through equity and voting interests Section 1591 does not change any of the guidance in Section 1590 regarding the presumption that: 1) control exists when an individual or an enterprise owns, directly or indirectly, an equity interest that carries the right to elect the majority of the members of the other enterprise s board of directors; and 2) control does not exist when such rights do not exist. However, this presumption may be overcome by other factors. The greater an enterprise s voting interest is above the 50% level, the more persuasive the other factors must be in overcoming this presumption. Additionally, in Section 1591, the concept of control still depends on the ability to exercise the right to elect the majority of the board of directors and determine the strategic operating, investing and financing policies and not on its actual exercise; this consideration is an important concept in evaluating control. Control through potential voting interests Section 1591 does not make any changes to the guidance on potential voting interests from Section It asserts that control may exist, even when an enterprise does not own a majority voting interest, if the enterprise owns rights (for example, options, warrants or convertible securities) that, if exercised or converted provide the holder with the ability to elect the majority of the members of the board of directors. Thus, in assessing control, the holder of such rights must take potential voting interests into account to determine its ability to control another enterprise by exercising the rights or converting the securities, and conversely, the ability of others to dilute the enterprise s voting interest if they exercise their rights or convert their securities. 3

4 Control through contractual rights (when equity interests and potential voting interests are not the dominant factor in determining control) Section 1591 includes guidance to determine whether an enterprise controls another through contractual rights. Section 1590 does not contain such guidance; however, AcG-15 provides guidance to clarify how to assess whether control is conferred by other arrangements. This assessment is done by: 1) assessing whether the enterprise holds a variable interest (contractual, ownership or other pecuniary interests in an enterprise that change with changes in the fair value of an enterprise s net assets exclusive of variable interests) in the potential VIE; 2) determining if the enterprise is a VIE; and 3) assessing who is the primary beneficiary of the VIE (the entity that has a variable interest, or combination of variable interests, that will absorb a majority of the enterprise s expected losses, receive a majority of the enterprise s expected residual returns, or both). The guidance in AcG-15 is quite prescriptive and rules based and sets out specific criteria to be met for an enterprise to be identified as a VIE. Section 1591 does not carry forward the concepts of VIE, variable interests and primary beneficiary; instead, it prescribes a more qualitative assessment with greater use of professional judgment. Under Section 1591, when equity interests and potential voting rights are not the dominant factor in determining control, an enterprise must analyze all of its contractual rights 1 and consider all facts and circumstances when determining whether it controls another enterprise. The two conditions that must be satisfied for an enterprise to have control through contractual rights are the following: 1. The enterprise holds rights that are sufficient to direct the strategic operating, investing and financing policies of the other enterprise without the co-operation of others; and 2. The enterprise has the right and ability to obtain the future economic benefits and is exposed to the related risks of the other enterprise. Although the AcSB wanted to encourage the use of professional judgment, it provides some additional guidance in Section 1591 to assist enterprises in evaluating whether the two above conditions are met. As a result, enterprises are required to consider the following facts and circumstances when assessing if the contractual rights are sufficient to give one enterprise control over the other, without however limiting the use of professional judgment: The degree of its involvement at inception of the other enterprise in determining its purpose and design (although, on its own, involvement in design is not sufficient to confer control); 1 Section 1591 provides the following examples of contractual arrangements (non-exhaustive): supply arrangements, management contracts, lease agreements, licence agreements, royalty contracts, other sales contracts and finance arrangements, call rights or put rights related to the other enterprise and liquidation rights. 4

assessing whether the enterprise holds a variable interest (contractual, ownership or other pecuniary interests in an enterprise that change with changes in the fair")

5 How decisions are made about the strategic policies that could notably determine: the right and ability to obtain future economic benefits and related risks; who has the continuing ability to direct the activities of the other enterprise; and who receives the economic benefits and is exposed to the related risks from those activities; The risks to which the other enterprise was designed to be exposed, the risks it was designed to pass on to the parties involved with it and whether the enterprise is exposed to some or all of those risks; Whether one enterprise has the continuing unilateral ability in the contractual arrangement to direct the strategic policies of the other enterprise. Section 1591 also includes further guidance with respect to specific situations, in particular when: the other enterprise is designed so that the direction of its activities is predetermined unless and until particular circumstances arise or events occur (operating on autopilot); an enterprise has given an explicit or implicit commitment to ensure that another enterprise continues to operate as designed, which may increase its incentive to obtain rights sufficient to give it power because of its increased exposure to variability of future economic benefits and to the related risks; or an enterprise is in a position, through call or put rights or liquidation rights in a contractual agreement, to have power over activities that are closely related to the other enterprise. Lastly, Section 1591 introduces the concept of protective rights, which are rights designed to protect the interest of the enterprise holding those rights but do not confer control. For example, veto rights that allow an enterprise to participate in or prevent events or transactions that are not in the normal course of the other enterprise s operations do not confer control. Accounting for subsidiaries Section 1591 provides accounting policy choices to account for subsidiaries, some of which are predicated on how the enterprise controls them: Consolidate all its subsidiaries; Account for its interest in subsidiaries: - controlled through voting interests, potential voting interests or a combination thereof using: 5

6 the equity method; or the cost method; - controlled through contractual arrangements or in combination with voting interests, potential voting interests, or a combination thereof according to the nature of the contractual arrangements in accordance with the applicable section. It should be noted that when an enterprise elects to account for its subsidiaries using either the cost or the equity method, it would not be required to perform a control assessment on other enterprises that it may control by means other than equity interest. Similar to Section 1590, Section 1591 requires all interests in subsidiaries be accounted for using the same method. Disclosure Consolidated financial statements While Section 1591 makes some changes to the wording in this section for consistency with the nature and spirit of the changes made to the standards on subsidiaries, it maintains the Section 1590 disclosure requirements and includes the AcG-15 requirement pertaining to the disclosure of significant restrictions affecting the access to VIE s assets. This disclosure now makes the AcG-15 disclosure applicable to all consolidated subsidiaries rather than just VIEs. Disclosure Non-consolidated financial statements Section 1591 maintains the Section 1590 disclosure requirements, specifying that they now apply only to subsidiaries controlled through voting interests, potential voting interests, or a combination thereof. Effective date and transition Sections 1591 and the related consequential amendments apply to fiscal years beginning on or after January 1, 2016; however, earlier application is permitted. If an enterprise elects to account for its subsidiaries using the cost or equity method on transition to Section 1591, the transitional provisions of Section 1591 do not apply. Similarly, when an enterprise elects to consolidate its subsidiaries on transition to Section 1591, it is not required to make retrospective adjustments to its previous accounting for its involvement with enterprises that were not previously consolidated and continue not to be consolidated following the adoption of Section The same principle applies for enterprises that are consolidated and must continue to be consolidated under Section

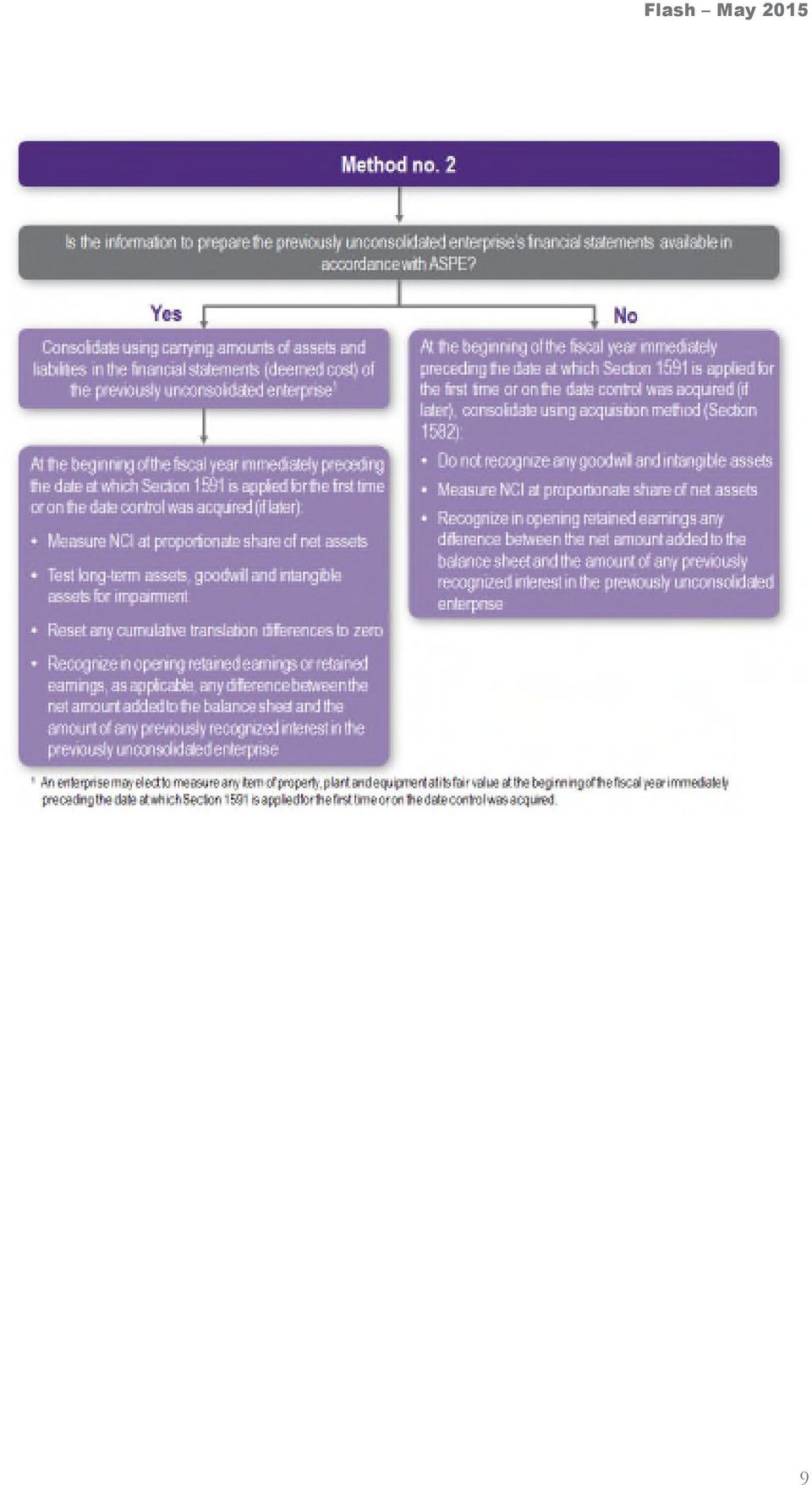

7 While Section 1591 applies retrospectively, there is some relief provided in situations where an enterprise is required to: consolidate a subsidiary that was not consolidated previously; no longer consolidate a subsidiary that was consolidated previously. The next two sections discuss each of these transitional provisions in more detail. Transitional guidance Consolidate a subsidiary that was not consolidated previously The following two tables summarize the transitional provisions and the methods available in Section 1591 when an enterprise applies or chooses to apply for the first time the consolidation method of accounting for its subsidiaries. Both methods convey how to measure the assets and liabilities of subsidiaries that were not consolidated previously and the non-controlling interests (NCI), if any, in those subsidiaries. The enterprise must select one of these two methods for each previously unconsolidated subsidiary and must use financial information prepared in accordance with ASPE: 7

8 8

9 9

10 Transitional guidance No longer consolidate a subsidiary that was consolidated previously The following table presents the steps an enterprise must perform at the beginning of the fiscal year immediately preceding the date at which Section 1591 is applied for the first time or on the date the interest is obtained (if later) when accounting for an interest in an enterprise that was previously consolidated: Consequential amendments Section 1500, First-time Adoption Section 1500 has been amended to permit a first-time adopter of ASPE to apply the transitional provisions in Section 1591 if it decides to consolidate its subsidiaries for the first time upon transition. Section 1601, Consolidated Financial Statements Following the issuance of Section 1591, guidance on how to consolidate a subsidiary in Section 1590 was moved to Section 1601 so that all the guidance is contained in one section. 10

11 Section 3056, Interests in Joint Arrangements Why was Section 3056 issued? Under Section 3055, an enterprise that has an interest in a joint venture, with the meaning given to this term in that section (refer to section Terminology and definitions in this publication) could elect to proportionately consolidate that interest or use the cost or equity method. However, the AcSB believes that proportionate consolidation was not always a faithful representation of the nature of the interest in a joint arrangement. In many cases, the investor has rights only to the net assets of an enterprise used to carry out the activities of the joint arrangement rather than rights to the individual assets of the joint arrangement and obligations for its individual liabilities. Nevertheless, the application of the proportionate consolidation method results in the investor recognizing, in its balance sheet, its share of the assets and liabilities of the jointly controlled enterprise, based on its level of equity interest when in reality, it has only rights to the net assets. The AcSB s objective, in replacing Section 3055 with Section 3056, is to change the accounting policy choices available to investors in joint arrangements to ensure the financial reporting of these interests better reflect the nature of the interest and, consequently, the rights and the obligations therein. Comparison of the guidance of Sections 3055 and 3056 The key accounting differences and similarities in accounting between Sections 3055 and 3056 are summarized below: Comparison of guidance Purpose and scope Terminology and definitions Interests in a joint arrangement held by an investor who does not share joint control Types of joint arrangements Recognition Contributions and transactions No conceptual changes Various changes in terminology used, but no conceptual changes in the definitions No changes in requirements No change in the broad types of joint arrangements Withdrawal of the proportionate consolidation method and different accounting methods based on the type of joint arrangement Withdrawal of the requirements in Section 3055 to defer and amortize the portion of a gain that does not relate to the amount of cash received or fair value of other assets received Purpose and scope The issuance of Section 3056 has not resulted in any conceptual changes in the purpose and scope. The Section still establishes standards for interests in arrangements in which the investor has joint control. As is the case with Section 3055, Section 3056 does not deal with accounting by joint arrangements themselves. 11

12 Section 3056 continues to apply when economic activities meet the definitions and criteria outlined in the section, even though such activities may not be referred to as joint arrangements. Conversely, the section does not apply when economic activities do not meet these same definitions and criteria, even though they may be referred to as joint arrangements. Terminology and definitions Section 3055 refers to a joint venture as an economic activity resulting from a contractual arrangement whereby two or more venturers jointly control the economic activity. It also refers to a venturer as a party to a joint venture: 1) having joint control over that joint venture; 2) having the right and ability to obtain future economic benefits from the resources of the joint venture; and 3) being exposed to the related risks. With the publication of Section 3056, the definitions presented in Section 3055 remain unchanged, including the definition of joint control; however, the AcSB made some terminology changes. Going forward, a joint arrangement is the term used to describe the economic activity identified by the term joint venture in Section Additionally, Section 3056 refers to an investor rather than a venturer. Unlike Section 3055, it does not provide a specific definition of an investor. Interests in a joint arrangement held by an investor who does not share joint control As is the case in Section 3055, Section 3056 states that the interest of an investor who does not have joint control over the joint arrangement qualifies as an investment and is subject to the requirements of Section 3051 or Section 3856, Financial Instruments. Types of joint arrangements Section 3056 does not change the types of joint arrangements in which an investor may have an interest; these remain as follows: jointly controlled operations; jointly controlled assets; jointly controlled enterprises. Accounting for an interest in a joint arrangement Section 3055 allows for an accounting policy choice to account for an interest in a joint venture regardless of the category to which the joint venture belongs. The accounting policy choices are the: proportionate consolidation method; 12

having joint control over that joint venture; 2) having the right and ability to obtain future economic benefits from the resources of")

13 equity method; cost method. With the issuance of Section 3056, determining the correct type of joint arrangement is important because the accounting method for an investor s interest will depend on the category. The proportionate consolidation method is no longer permitted. The next three sections of this publication discuss the three types of joint arrangements in more detail and the recognition requirements for each type of interest. Jointly controlled operations In a jointly controlled operation, the investors use their own assets and resources and incur their own liabilities and expenses rather than establish a corporation, partnership or other enterprise that is separate from the investors. The assets remain under the control and ownership of each investor. For example, investors may combine their operations, resources and expertise to carry out an activity jointly, such as manufacturing, distributing or marketing a product. The contractual arrangement between the investors usually provides means by which the revenue from the sale of any good or services and any expense incurred in common are shared. In this context, an investor in a jointly controlled operation is considered to have rights to the individual assets and obligations for the individual liabilities; therefore it must recognize: in its balance sheet, the assets that it controls and the liabilities that it incurs; and in its income statement, its share of the revenue of the joint arrangement and its share of the expenses incurred by the joint arrangement. This method is similar to proportionate consolidation, but instead of using the investor s ownership interest in the joint arrangement solely to determine its share of assets, liabilities, revenue and expenses of the joint arrangement, this method requires the investor to consider all the facts and circumstances related to its interest (e.g., contractual arrangements). Jointly controlled assets This type of joint arrangement refers to contractual arrangements whereby one or more assets are under joint control, and often joint ownership of the investors and are dedicated to the purpose of the joint arrangement. The investors may take a share of the output from the assets and each bears a share of the expenses incurred. This type of joint arrangement also does not involve the establishment of a corporation, partnership or other structure that is separate from the investors. One example of this type of arrangement is a jointly controlled rental property for which each investor receives a share of the rental revenues and incurs a share of the expenses. An investor in jointly controlled 13

14 assets, similar to a jointly controlled operation, also has rights to individual assets and obligations for individual liabilities; as a result, the investor must recognize: in its balance sheet, its share of the jointly controlled assets and its share of any liabilities incurred jointly with the other investors in relation to the joint arrangement; and in its income statement, any revenue from the sale or use of its share of the output of the joint arrangement, and its share of any expenses incurred by the joint arrangement. This accounting is also similar to the proportionate consolidation method, but it requires the determination of the share of assets, liabilities, revenues and expenses to be based on the facts and circumstances in the arrangement rather than solely based on ownership interests. Jointly controlled enterprises Contrary to the two aforementioned categories of joint arrangements, a jointly controlled enterprise involves the establishment of a separate entity (e.g., corporation, partnership or other structure) to achieve the activities of the joint arrangement. As the entity has its own legal status, it owns the assets of the joint arrangement, incurs liabilities and expenses and earns revenue; the investors have an interest in the enterprise. A jointly controlled enterprise generally confers separation between the investors and the assets and obligations of the joint arrangement, so that the investors have rights only to the net assets of the jointly controlled enterprise. However, there may be situations where investors enter into a separate contractual arrangement or there are other facts and circumstances that counteract the legal form of this entity such that the substance of the arrangement is that the investors, in fact, do not have an interest in the net assets of the jointly controlled enterprise, rather, they have rights to the individual assets and obligations for the individual liabilities. An appendix to Section 3056, which is an integral part of the section, has been added to assist investors in determining if they have a right to the net assets of the jointly controlled enterprise or rights to the individual assets and obligations for the individual liabilities relating to such arrangement. This appendix includes factors an investor should consider in its analysis, a table with the common terms in contractual arrangements that provide evidence of the substance of the interest and a decision tree summarizing the process to analyze the arrangement. An investor with an interest in a jointly controlled enterprise must make an accounting policy choice to account for its interests to: use the equity method; use the cost method; 14

15 perform an analysis of its interests in all of its joint arrangements that are jointly controlled enterprises to determine the nature of the interests and apply an accounting policy that is consistent therewith: - for those interests that represent interests in the net assets, the investor accounts for them using the equity or the cost method; - for those interests the investor determines represent rights to the individual assets and obligations for the individual liabilities, it accounts for them on the same basis as jointly controlled operations or assets as appropriate; that is, by accounting for its share of the assets, liabilities, revenues and expenses, based on all the relevant facts and circumstances of the arrangement. All interests in jointly controlled enterprises must be accounted for by applying the same accounting method (i.e. the equity method, the cost method or the analysis of the interests). The three steps in analyzing the substance of an investor s interest in a jointly controlled enterprise are to look at its legal form and the terms of the contractual arrangement, and to consider other facts and circumstances. When reviewing the other facts and circumstances of the arrangement, the investor should ascertain whether the jointly controlled enterprise: carries activities primarily aim to provide the investors with an output (which indicates that the investors have rights to substantially all the economic benefits of the assets held in the enterprise); and depends on the investors on a continuous basis to settling the liabilities from the activities it conducts (which indicates that the investors essentially have an obligation for the liabilities of the enterprise). When both of these criteria are met, in substance, the investors have rights to the individual assets and obligations for the individual liabilities relating to the jointly controlled enterprise. Contributions and transactions For contributions to a joint arrangement, Section 3056 has removed the requirement of Section 3055 to defer and amortize the portion of a gain that does not relate to the amount of cash received or fair value of other assets received that do not represent a claim on the assets of the joint arrangement. The other basic principles of accounting for contributions and transactions with joint arrangements remain unchanged; in particular, a gain or loss from a transaction with a joint arrangement is recognized in the financial statements of the investor only to the extent of the interests of the non-related investors. The guidance also remains unchanged related to a transaction between an investor and a 15

16 joint arrangement that provides evidence of a decline in the value of the assets received or transferred. Impairment Section 3056 does not include requirements regarding impairment of an interest in a joint arrangement accounted for using the equity or the cost method; rather, it refers to Section 3051 for guidance. According to the requirements of Section 3051, an investor must assess whether there are any indications that an investment may be impaired; this requirement is consistent with the guidance in Section Assessing impairment of an investor s share of any assets of a joint arrangement that are recorded in the investor s balance sheet is subject to the impairment requirements of the relevant standards (e.g., Section 3063, Impairment of Long-lived Assets, or Section 3064, Goodwill and Intangible Assets). Presentation and disclosure Section 3056 carries forward the presentation requirements of Section 3055 that require the presentation of certain items separately in the balance sheet, notably the interests in joint arrangements accounted for using the equity method or accounted for using the cost method. Income from those investments must also be presented separately in the income statement. As there is no longer an accounting policy choice for jointly controlled operations and jointly controlled assets, Section 3056 only requires disclosure of the method used to account for interests in a jointly controlled enterprise. Investors accounting for their interests in joint arrangements using the cost or equity method must provide all the relevant disclosures for investments accounted for using either of those methods included in Section Illustrative examples Contrary to Section 3055, Section 3056 does not include any illustrative examples with regard to the application of the standard s principles. The examples presented in Section 3055 are related to accounting for contributions to a joint venture and transactions in the normal course of operations between a venturer and a joint venture. In the examples presented, the venturer uses the proportionate consolidation method. These examples have not been adapted to reflect the requirements in Section Effective date and transition Section 3056 and the related consequential amendments apply to fiscal years beginning on or after January 1, 2016; however, earlier application is permitted. It is important to note that if an investor elects to early adopt Section 3056, it must also apply the amendments to Section 3051 at the same time. 16

17 Section 3056 provides specific transitional provisions where an investor must: transition from proportionate consolidation to the cost or equity method; or transition from the cost or equity method to accounting for the investor s interests in the individual assets and liabilities of a joint arrangement. The next two sections discuss each of these transitional provisions in more detail. Transition guidance From proportionate consolidation to the cost or equity method The following chart presents the steps of the transitional provisions of Section 3056 to be applied to evaluate an interest in a joint arrangement when the assets and liabilities were previously proportionately consolidated: 17

18 Transition guidance From the cost or equity method to accounting for the investor s interests in the individual assets and liabilities of a joint arrangement The following chart presents the three different options an investor has to choose from when measuring its share of the assets and liabilities of the joint arrangement: Consequential amendments Section 1500, First-time Adoption Section 1500 has been amended to permit a first-time adopter of ASPE to apply the transitional provisions in Section Section 1506, Accounting Changes Section 1506 was amended to clarify that the accounting policy choice related to jointly controlled enterprises is exempted from meeting the relevance and reliability criteria. Section 1520, Income Statement Section 1520 has been amended to reflect the requirement to present separately, on the face of the income statement, the income from investments in joint arrangements accounted for using the cost or equity method. Section 1521, Balance Sheet Section 1521 was amended to reflect the requirement to present separately, on the face of the balance sheet, investments in joint arrangements accounted for using the cost or equity method. 18

19 Amendments to Section 3051, Investments Section 3051 was amended as a result of the issuance of the new standards on subsidiaries and joint arrangements. The amendments: clarify that the scope includes investments subject to significant influence and certain other non-financial instruments, such as works of art and other tangible assets held for investment purpose, but does not include interests in subsidiaries and in joint arrangements unless they are accounted for using the cost or equity method; and add guidance on contributions and other transactions between an investor and an equity-accounted investee that is consistent with the guidance in Section Effective date and transition Section 3051 and the related consequential amendments apply to fiscal years beginning on or after January 1, 2016; however, earlier application is permitted. It is important to note that if an enterprise elects to early adopt Section 3051, it must also apply Section 3056 at the same time. The amendments to Section 3051 may be applied prospectively. Consequential amendments Section 1500, First-time Adoption Section 1500 has been amended to permit a first-time adopter of ASPE to apply the transitional provisions in amended Section Section 3831, Non-monetary Transactions Section 3831 has been amended to refer to the guidance in Section 3051, in addition to the guidance in Section 3056, on the accounting for gains or losses from non-monetary transactions. Consequential amendments to Section 4450, Reporting Controlled and Related Entities by Not-for-Profit Organizations, of Part III of the CPA Canada Handbook Accounting, Accounting Standards for Not-for-Profit Organizations In the case of a not-for-profit organization with an interest in a joint venture, 2 proportionate consolidation is still permitted. However, since this method is not one of the choices available under Section 3056, Section 4450 has been amended to include the definition of proportionate consolidation. 2 The terminology used in Section 3055 continues to be used in Section

20 About Raymond Chabot Grant Thornton Raymond Chabot Grant Thornton LLP is a leading accounting and advisory firm providing audit, tax and advisory services to private and public organizations. Together with Grant Thornton LLP in Canada, Raymond Chabot Grant Thornton LLP has approximately 4,300 people in offices across Canada. Raymond Chabot Grant Thornton LLP is a member firm within Grant Thornton International Ltd (Grant Thornton International). Grant Thornton International and the member firms are not a worldwide partnership. Services are delivered independently by the member firms. We have made every effort to ensure information in this publication is accurate as of its issue date. Nevertheless, information or views expressed are neither official statements of position, nor should they be considered technical advice for you or your organization without consulting a professional business adviser. For more information about this topic, please contact your Raymond Chabot Grant Thornton adviser. Translation. In case of discrepancy, the French text shall prevail. 20

Background Information and Basis for Conclusions Section 1591 CPA Canada Handbook Accounting, Part II

Subsidiaries Background Information and Basis for Conclusions Section 1591 CPA Canada Handbook Accounting, Part II Foreword In September 2014, the Accounting Standards Board (AcSB) released SUBSIDIARIES,

Subsidiaries Background Information and Basis for Conclusions Section 1591 CPA Canada Handbook Accounting, Part II Foreword In September 2014, the Accounting Standards Board (AcSB) released SUBSIDIARIES,

Section 1591, Subsidiaries

Financial Reporting Alert ASPE MAY 2015 Section 1591, Subsidiaries In September 2014, the Accounting Standards Board (AcSB) issued Section 1591, Subsidiaries, set out in Part II (Accounting Standards for

Financial Reporting Alert ASPE MAY 2015 Section 1591, Subsidiaries In September 2014, the Accounting Standards Board (AcSB) issued Section 1591, Subsidiaries, set out in Part II (Accounting Standards for

Issue 19: Joint Arrangements and Associates

www.bdo.ca Assurance and accounting Comparison Series Issue 19: Joint Arrangements and Associates Both and are principle based frameworks, and from a conceptual standpoint many of the general principles

www.bdo.ca Assurance and accounting Comparison Series Issue 19: Joint Arrangements and Associates Both and are principle based frameworks, and from a conceptual standpoint many of the general principles

ASPE at a Glance. Standards Included in Topic

ASPE AT A GLANCE ASPE AT A GLANCE This publication has been compiled to assist users in gaining a high level overview of Accounting Standards for Private Enterprises (ASPE) included in Part II of the CPA

ASPE AT A GLANCE ASPE AT A GLANCE This publication has been compiled to assist users in gaining a high level overview of Accounting Standards for Private Enterprises (ASPE) included in Part II of the CPA

Accounting developments

Flash Accounting developments New standards for business combinations and non-controlling interests In January 2009, the Accounting Standards Board (AcSB) of the Canadian Institute of Chartered Accountants

Flash Accounting developments New standards for business combinations and non-controlling interests In January 2009, the Accounting Standards Board (AcSB) of the Canadian Institute of Chartered Accountants

Adviser alert Under control? A practical guide to IFRS 10 Consolidated Financial Statements

Adviser alert Under control? A practical guide to IFRS 10 Consolidated Financial Statements August 2012 Overview The Grant Thornton International IFRS team has published a new guide, Under Control? A Practical

Adviser alert Under control? A practical guide to IFRS 10 Consolidated Financial Statements August 2012 Overview The Grant Thornton International IFRS team has published a new guide, Under Control? A Practical

Investments in Associates and Joint Ventures

STATUTORY BOARD FINANCIAL REPORTING STANDARD SB-FRS 28 Investments in Associates and Joint Ventures This standard applies for annual periods beginning on or after 1 January 2013. Earlier application is

STATUTORY BOARD FINANCIAL REPORTING STANDARD SB-FRS 28 Investments in Associates and Joint Ventures This standard applies for annual periods beginning on or after 1 January 2013. Earlier application is

Investments in Associates and Joint Ventures

International Accounting Standard 28 Investments in Associates and Joint Ventures In April 2001 the International Accounting Standards Board (IASB) adopted IAS 28 Accounting for Investments in Associates,

International Accounting Standard 28 Investments in Associates and Joint Ventures In April 2001 the International Accounting Standards Board (IASB) adopted IAS 28 Accounting for Investments in Associates,

Summary Comparison of Part II of the CICA Handbook Accounting

Summary Comparison the CICA Accounting to XFI Version in Part V As December 31, 2009 1. This comparison has been prepared by the staff the Accounting Standards Board (AcSB) and has not been approved by

Summary Comparison the CICA Accounting to XFI Version in Part V As December 31, 2009 1. This comparison has been prepared by the staff the Accounting Standards Board (AcSB) and has not been approved by

Adviser alert Example Consolidated Financial Statements 2012

Adviser alert Example Consolidated Financial Statements 2012 October 2012 Overview The Grant Thornton International IFRS team has published the 2012 version of the Reporting under IFRS: Example Consolidated

Adviser alert Example Consolidated Financial Statements 2012 October 2012 Overview The Grant Thornton International IFRS team has published the 2012 version of the Reporting under IFRS: Example Consolidated

2 This Standard shall be applied by all entities that are investors with joint control of, or significant influence over, an investee.

International Accounting Standard 28 Investments in Associates and Joint Ventures Objective 1 The objective of this Standard is to prescribe the accounting for investments in associates and to set out

International Accounting Standard 28 Investments in Associates and Joint Ventures Objective 1 The objective of this Standard is to prescribe the accounting for investments in associates and to set out

Investments in Associates and Joint Ventures

IFAC Board Exposure Draft 50 October 2013 Comments due: February 28, 2014 Proposed International Public Sector Accounting Standard Investments in Associates and Joint Ventures This Exposure Draft 50, Investments

IFAC Board Exposure Draft 50 October 2013 Comments due: February 28, 2014 Proposed International Public Sector Accounting Standard Investments in Associates and Joint Ventures This Exposure Draft 50, Investments

Adviser alert Example Consolidated Financial Statements 2011 October 2011

Adviser alert Example Consolidated Financial Statements 2011 October 2011 Overview The Grant Thornton International IFRS team have published the 2011 version of the Reporting under IFRS: Example Consolidated

Adviser alert Example Consolidated Financial Statements 2011 October 2011 Overview The Grant Thornton International IFRS team have published the 2011 version of the Reporting under IFRS: Example Consolidated

New Developments Summary

April 15, 2008 NDS 2008-17 Revised for FASB Codification July 1, 2009 New Developments Summary Business combinations FASB Statement 141 (revised 2007) (ASC 805) Summary On December 4, 2007, the FASB issued

April 15, 2008 NDS 2008-17 Revised for FASB Codification July 1, 2009 New Developments Summary Business combinations FASB Statement 141 (revised 2007) (ASC 805) Summary On December 4, 2007, the FASB issued

CPA Canada Financial Reporting Alert

FEBRUARY 2014 CPA Canada Financial Reporting Alert ASPE AMENDED 2013 Annual Improvements to Accounting Standards for Private Enterprises In October 2013, the Accounting Standards Board ( AcSB ) made several

FEBRUARY 2014 CPA Canada Financial Reporting Alert ASPE AMENDED 2013 Annual Improvements to Accounting Standards for Private Enterprises In October 2013, the Accounting Standards Board ( AcSB ) made several

International Accounting Standard 27 (IAS 27), Consolidated and Separate Financial Statements

, Consolidated and Separate Financial Statements") International Accounting Standard 27 (IAS 27), Consolidated and Separate Financial Statements By BRIAN FRIEDRICH, MEd, CGA, FCCA(UK), CertIFR and LAURA FRIEDRICH, MSc, CGA, FCCA(UK), CertIFR Updated By

International Accounting Standard 27 (IAS 27), Consolidated and Separate Financial Statements By BRIAN FRIEDRICH, MEd, CGA, FCCA(UK), CertIFR and LAURA FRIEDRICH, MSc, CGA, FCCA(UK), CertIFR Updated By

New Accounting for Business Combinations and Non-controlling Interests

IFRS ADVISORY SERVICES New Accounting for Business Combinations and Non-controlling Interests August 2008 KPMG LLP The proposed new accounting standards for business combinations and non-controlling interests

IFRS ADVISORY SERVICES New Accounting for Business Combinations and Non-controlling Interests August 2008 KPMG LLP The proposed new accounting standards for business combinations and non-controlling interests

Adopting the consolidation suite of standards

IFRS PRACTICE ISSUES Adopting the consolidation suite of standards Transition to IFRSs 10, 11 and 12 January 2013 kpmg.com/ifrs Contents Simplifications provide relief 1 1. Extent of relief depends on

IFRS PRACTICE ISSUES Adopting the consolidation suite of standards Transition to IFRSs 10, 11 and 12 January 2013 kpmg.com/ifrs Contents Simplifications provide relief 1 1. Extent of relief depends on

IFRS Hot Topics. Full Text Edition February 2013. ottopics...

IFRS Hot Topics Full Text Edition February 2013 ottopics... Grant Thornton International Ltd (Grant Thornton International) and the member firms are not a worldwide partnership. Services are delivered

IFRS Hot Topics Full Text Edition February 2013 ottopics... Grant Thornton International Ltd (Grant Thornton International) and the member firms are not a worldwide partnership. Services are delivered

Consolidation (Topic 810)

") No. 2015-02 February 2015 Consolidation (Topic 810) Amendments to the Consolidation Analysis An Amendment of the FASB Accounting Standards Codification The FASB Accounting Standards Codification is the

No. 2015-02 February 2015 Consolidation (Topic 810) Amendments to the Consolidation Analysis An Amendment of the FASB Accounting Standards Codification The FASB Accounting Standards Codification is the

Accounting Standards for Private Enterprises

Accounting Standards for Private Enterprises CICA Handbook Accounting, Part II Background Information and Basis for Conclusions Foreword In December 2009, the Accounting Standards Board (AcSB) released

Accounting Standards for Private Enterprises CICA Handbook Accounting, Part II Background Information and Basis for Conclusions Foreword In December 2009, the Accounting Standards Board (AcSB) released

IFRS compared to Canadian GAAP: An overview

IFRS compared to Canadian GAAP: An overview Third Edition 2010 KPMG IN CANADA IFRS compared to Canadian GAAP: An overview Third Edition 2010 Managing the transition to IFRS The Canadian Accounting Standards

IFRS compared to Canadian GAAP: An overview Third Edition 2010 KPMG IN CANADA IFRS compared to Canadian GAAP: An overview Third Edition 2010 Managing the transition to IFRS The Canadian Accounting Standards

Consolidations (Topic 810)

") No. 2009-17 December 2009 Consolidations (Topic 810) Improvements to Financial Reporting by Enterprises Involved with Entities An Amendment of the FASB Accounting Standards Codification TM The FASB Accounting

No. 2009-17 December 2009 Consolidations (Topic 810) Improvements to Financial Reporting by Enterprises Involved with Entities An Amendment of the FASB Accounting Standards Codification TM The FASB Accounting

INTERNATIONAL FINANCIAL REPORTING BULLETIN 2011/06

INTERNATIONAL FINANCIAL REPORTING BULLETIN 2011/06 ACCOUNTING FOR SUBSIDIARIES, JOINT ARRANGEMENTS AND ASSOCIATES, AND DISCLOSURES OF INTERESTS IN OTHER ENTITIES Background The International Accounting

INTERNATIONAL FINANCIAL REPORTING BULLETIN 2011/06 ACCOUNTING FOR SUBSIDIARIES, JOINT ARRANGEMENTS AND ASSOCIATES, AND DISCLOSURES OF INTERESTS IN OTHER ENTITIES Background The International Accounting

IPSAS 7 INVESTMENTS IN ASSOCIATES

IPSAS 7 INVESTMENTS IN ASSOCIATES Acknowledgment This International Public Sector Accounting Standard (IPSAS) is drawn primarily from International Accounting Standard (IAS) 28 (Revised 2003), Investments

IPSAS 7 INVESTMENTS IN ASSOCIATES Acknowledgment This International Public Sector Accounting Standard (IPSAS) is drawn primarily from International Accounting Standard (IAS) 28 (Revised 2003), Investments

Similarities and differences*

Investment Management & Real Estate Similarities and differences* Global Reporting Revolution June 2007 *connectedthinking Contents How to use this publication 01 Summary of Similarities and Difference

Investment Management & Real Estate Similarities and differences* Global Reporting Revolution June 2007 *connectedthinking Contents How to use this publication 01 Summary of Similarities and Difference

Defining Issues. FASB Issues New Consolidation Guidance. February 2015, No. 15-6. Key Facts

Defining Issues February 2015, No. 15-6 FASB Issues New Consolidation Guidance On February 18, 2015, the FASB issued a new consolidation standard to improve targeted areas of the consolidation guidance

Defining Issues February 2015, No. 15-6 FASB Issues New Consolidation Guidance On February 18, 2015, the FASB issued a new consolidation standard to improve targeted areas of the consolidation guidance

ILLUSTRATIVE FINANCIAL STATEMENTS YEAR ENDED 31 DECEMBER 2013 International Financial Reporting Standards

ILLUSTRATIVE FINANCIAL STATEMENTS YEAR ENDED 31 DECEMBER 2013 International Financial Reporting Standards 2 A Layout (International) Group Ltd Annual report and financial statements For the year ended

ILLUSTRATIVE FINANCIAL STATEMENTS YEAR ENDED 31 DECEMBER 2013 International Financial Reporting Standards 2 A Layout (International) Group Ltd Annual report and financial statements For the year ended

International Accounting Standard 28 Investments in Associates

International Accounting Standard 28 Investments in Associates Scope 1 This Standard shall be applied in accounting for investments in associates. However, it does not apply to investments in associates

International Accounting Standard 28 Investments in Associates Scope 1 This Standard shall be applied in accounting for investments in associates. However, it does not apply to investments in associates

IPSAS 7 INVESTMENTS IN ASSOCIATES

IPSAS 7 INVESTMENTS IN ASSOCIATES Acknowledgment This International Public Sector Accounting Standard (IPSAS) is drawn primarily from International Accounting Standard (IAS) 28 (Revised 2003), Investments

IPSAS 7 INVESTMENTS IN ASSOCIATES Acknowledgment This International Public Sector Accounting Standard (IPSAS) is drawn primarily from International Accounting Standard (IAS) 28 (Revised 2003), Investments

Assurance and accounting A Guide to Financial Instruments for Private

june 2011 www.bdo.ca Assurance and accounting A Guide to Financial Instruments for Private Enterprises and Private Sector t-for-profit Organizations For many entities adopting the Accounting Standards

june 2011 www.bdo.ca Assurance and accounting A Guide to Financial Instruments for Private Enterprises and Private Sector t-for-profit Organizations For many entities adopting the Accounting Standards

Example Consolidated Financial Statements. International Financial Reporting Standards (IFRS) Illustrative Corporation Group 31 December 2010

Illustrative Corporation Group 31 December 2010") Example Consolidated Financial Statements International Financial Reporting Standards (IFRS) Illustrative Corporation Group 1 Introduction 2010 The preparation of financial statements in accordance with

Example Consolidated Financial Statements International Financial Reporting Standards (IFRS) Illustrative Corporation Group 1 Introduction 2010 The preparation of financial statements in accordance with

IFRS compared to US GAAP: An overview

compared to GAAP: An overview November 2014 kpmg.com/ifrs KPMG s Global Institute KPMG s Global Institute provides information and resources to help board and audit committee members gain insight and access

compared to GAAP: An overview November 2014 kpmg.com/ifrs KPMG s Global Institute KPMG s Global Institute provides information and resources to help board and audit committee members gain insight and access

Summary of Certain Differences between SFRS and US GAAP

Summary of Certain Differences between and SUMMARY OF CERTAIN DIFFERENCES BETWEEN AND The combined financial statements and the pro forma consolidated financial information of our Group included in this

Summary of Certain Differences between and SUMMARY OF CERTAIN DIFFERENCES BETWEEN AND The combined financial statements and the pro forma consolidated financial information of our Group included in this

International Financial Reporting Standard 3 Business Combinations

International Financial Reporting Standard 3 Business Combinations Objective 1 The objective of this IFRS is to improve the relevance, reliability and comparability of the information that a reporting

International Financial Reporting Standard 3 Business Combinations Objective 1 The objective of this IFRS is to improve the relevance, reliability and comparability of the information that a reporting

Clearly IFRS. Moving ahead in an IFRS world A practical guide to implementing. IFRS 10 Consolidated Financial Statements

Clearly IFRS Moving ahead in an IFRS world A practical guide to implementing IFRS 10 Consolidated Financial Statements Contents At a glance...2 Scope...3 New control model...4 Areas where a change in the

Clearly IFRS Moving ahead in an IFRS world A practical guide to implementing IFRS 10 Consolidated Financial Statements Contents At a glance...2 Scope...3 New control model...4 Areas where a change in the

Applying VIE Guidance to Common Control Leasing Arrangements

Applying VIE Guidance to Common Control Leasing Arrangements HIGHLIGHTS OF THE UPDATE... 1 APPENDIX A FREQUENTLY ASKED QUESTIONS... 4 APPENDIX B DEFINITION OF A PUBLIC BUSINESS ENTITY... 9 APPENDIX C ILLUSTRATIVE

Applying VIE Guidance to Common Control Leasing Arrangements HIGHLIGHTS OF THE UPDATE... 1 APPENDIX A FREQUENTLY ASKED QUESTIONS... 4 APPENDIX B DEFINITION OF A PUBLIC BUSINESS ENTITY... 9 APPENDIX C ILLUSTRATIVE

AS 27 Financial Reporting of Interests in Joint Ventures

CA. B. Ganesh AS 21 Consolidated Financial Statements AS 23 Accounting for Investments in Associates in Consolidated Financial Statements AS 27 Financial Reporting of Interests in Joint Ventures Case studies

CA. B. Ganesh AS 21 Consolidated Financial Statements AS 23 Accounting for Investments in Associates in Consolidated Financial Statements AS 27 Financial Reporting of Interests in Joint Ventures Case studies

Investments in Associates

Indian Accounting Standard (Ind AS) 28 Investments in Associates Investments in Associates Contents Paragraphs SCOPE 1 DEFINITIONS 2-12 Significant Influence 6-10 Equity Method 11-12 APPLICATION OF THE

Indian Accounting Standard (Ind AS) 28 Investments in Associates Investments in Associates Contents Paragraphs SCOPE 1 DEFINITIONS 2-12 Significant Influence 6-10 Equity Method 11-12 APPLICATION OF THE

An Overview. September 2011

An Overview September 2011 September 2011 Insights into IFRS: An overview 1 INSIGHTS INTO IFRS: AN OVERVIEW Insights into IFRS: An overview brings together all of the individual overview sections from

An Overview September 2011 September 2011 Insights into IFRS: An overview 1 INSIGHTS INTO IFRS: AN OVERVIEW Insights into IFRS: An overview brings together all of the individual overview sections from

Statement of Financial Accounting Standards No. 7. Consolidated Financial Statements

Statement of Financial Accounting Standards No. 7 Statement of Financial Accounting Standards No. 7 Consolidated Financial Statements 30 November 2004 Translated by Wei-heng Lin, Associate Professor (Chung

Statement of Financial Accounting Standards No. 7 Statement of Financial Accounting Standards No. 7 Consolidated Financial Statements 30 November 2004 Translated by Wei-heng Lin, Associate Professor (Chung

Income Taxes STATUTORY BOARD SB-FRS 12 FINANCIAL REPORTING STANDARD

STATUTORY BOARD SB-FRS 12 FINANCIAL REPORTING STANDARD Income Taxes This version of the Statutory Board Financial Reporting Standard does not include amendments that are effective for annual periods beginning

STATUTORY BOARD SB-FRS 12 FINANCIAL REPORTING STANDARD Income Taxes This version of the Statutory Board Financial Reporting Standard does not include amendments that are effective for annual periods beginning

NEPAL ACCOUNTING STANDARDS ON INVESTMENT IN ASSOCIATES

NAS 25 NEPAL ACCOUNTING STANDARDS ON INVESTMENT IN ASSOCIATES CONTENTS Paragraphs SCOPE 1-2 DEFINITIONS 3-13 Significant influence 7-11 Equity method 12-13 APPLICATION OF THE EQUITY METHOD 14-33 Impairment

NAS 25 NEPAL ACCOUNTING STANDARDS ON INVESTMENT IN ASSOCIATES CONTENTS Paragraphs SCOPE 1-2 DEFINITIONS 3-13 Significant influence 7-11 Equity method 12-13 APPLICATION OF THE EQUITY METHOD 14-33 Impairment

IFRS 10 Consolidated Financial Statements

S U M M A R Y IFRS 10 Consolidated Financial Statements Overview IFRS 10 replaces the part of IAS 27 Consolidated and Separate Financial Statements that addresses accounting for subsidiaries on consolidation.

S U M M A R Y IFRS 10 Consolidated Financial Statements Overview IFRS 10 replaces the part of IAS 27 Consolidated and Separate Financial Statements that addresses accounting for subsidiaries on consolidation.

International Accounting Standard 21 The Effects of Changes in Foreign Exchange Rates

International Accounting Standard 21 The Effects of Changes in Foreign Exchange Rates Objective 1 An entity may carry on foreign activities in two ways. It may have transactions in foreign currencies or

International Accounting Standard 21 The Effects of Changes in Foreign Exchange Rates Objective 1 An entity may carry on foreign activities in two ways. It may have transactions in foreign currencies or

IPSAS 7 ACCOUNTING FOR INVESTMENTS IN ASSOCIATES

IPSAS 7 ACCOUNTING FOR INVESTMENTS IN ASSOCIATES Acknowledgment This International Public Sector Accounting Standard is drawn primarily from International Accounting Standard (IAS) 28, Accounting for Investments

IPSAS 7 ACCOUNTING FOR INVESTMENTS IN ASSOCIATES Acknowledgment This International Public Sector Accounting Standard is drawn primarily from International Accounting Standard (IAS) 28, Accounting for Investments

Financial Accounting Series

Financial Accounting Series NO. 299-A DECEMBER 2007 Statement of Financial Accounting Standards No. 141 (revised 2007) Business Combinations Financial Accounting Standards Board of the Financial Accounting

Financial Accounting Series NO. 299-A DECEMBER 2007 Statement of Financial Accounting Standards No. 141 (revised 2007) Business Combinations Financial Accounting Standards Board of the Financial Accounting

ASPE AT A GLANCE Section 3856 Financial Instruments

ASPE AT A GLANCE Section 3856 Financial Instruments December 2014 Section 3856 Financial Instruments Effective Date Fiscal years beginning on or after January 1, 2011 1 SCOPE Applies to all financial instruments

ASPE AT A GLANCE Section 3856 Financial Instruments December 2014 Section 3856 Financial Instruments Effective Date Fiscal years beginning on or after January 1, 2011 1 SCOPE Applies to all financial instruments

NOT-FOR-PROFIT ORGANIZATIONS: NEW DIRECTIONS

DECEMBER 2010 WWW.BDO.CA ASSURANCE AND ACCOUNTING NOT-FOR-PROFIT ORGANIZATIONS: NEW DIRECTIONS In December 2010, the Accounting Standards Board (AcSB) and the Public Sector Accounting Board (PSAB) each

DECEMBER 2010 WWW.BDO.CA ASSURANCE AND ACCOUNTING NOT-FOR-PROFIT ORGANIZATIONS: NEW DIRECTIONS In December 2010, the Accounting Standards Board (AcSB) and the Public Sector Accounting Board (PSAB) each

Sri Lanka Accounting Standard LKAS 28. Investments in Associates

Sri Lanka Accounting Standard LKAS 28 Investments in Associates CONTENTS SRI LANKA ACCOUNTING STANDARD LKAS 28 INVESTMENTS IN ASSOCIATES paragraphs SCOPE 1 DEFINITIONS 2 12 Significant influence 6 10 Equity

Sri Lanka Accounting Standard LKAS 28 Investments in Associates CONTENTS SRI LANKA ACCOUNTING STANDARD LKAS 28 INVESTMENTS IN ASSOCIATES paragraphs SCOPE 1 DEFINITIONS 2 12 Significant influence 6 10 Equity

FASB Issues PCC Alternative for Identifiable Intangible Assets in a Business Combination

FASB Issues PCC Alternative for Identifiable Intangible Assets in a Business Combination February 25, 2015 Highlights of the Update In This Update Highlights of the Update... 1 Appendix A Frequently Asked

FASB Issues PCC Alternative for Identifiable Intangible Assets in a Business Combination February 25, 2015 Highlights of the Update In This Update Highlights of the Update... 1 Appendix A Frequently Asked

Financial Services Investment Companies (Topic 946)

") No. 2013-08 June 2013 Financial Services Investment Companies (Topic 946) Amendments to the Scope, Measurement, and Disclosure Requirements An Amendment of the FASB Accounting Standards Codification The

No. 2013-08 June 2013 Financial Services Investment Companies (Topic 946) Amendments to the Scope, Measurement, and Disclosure Requirements An Amendment of the FASB Accounting Standards Codification The

UNDERSTANDING CANADIAN PUBLIC SECTOR FINANCIAL STATEMENTS

June 2014 UNDERSTANDING CANADIAN PUBLIC SECTOR FINANCIAL STATEMENTS www.bcauditor.com TABLE OF CONTENTS Who Will Find this Guide Helpful 3 What a Set of Public Sector Financial Statements Includes 5 The

June 2014 UNDERSTANDING CANADIAN PUBLIC SECTOR FINANCIAL STATEMENTS www.bcauditor.com TABLE OF CONTENTS Who Will Find this Guide Helpful 3 What a Set of Public Sector Financial Statements Includes 5 The

GUYANA GOLDFIELDS INC.

Interim Consolidated Financial Statements MANAGEMENT'S RESPONSIBILITY FOR FINANCIAL REPORTING The accompanying unaudited interim consolidated financial statements of Guyana Goldfields Inc. (An exploration

Interim Consolidated Financial Statements MANAGEMENT'S RESPONSIBILITY FOR FINANCIAL REPORTING The accompanying unaudited interim consolidated financial statements of Guyana Goldfields Inc. (An exploration

International Financial Reporting Standards (IFRS)

") FACT SHEET June 2010 IFRS 3 Business Combinations (This fact sheet is based on the standard as at 1 January 2010.) Important note: This fact sheet is based on the requirements of the International Financial

FACT SHEET June 2010 IFRS 3 Business Combinations (This fact sheet is based on the standard as at 1 January 2010.) Important note: This fact sheet is based on the requirements of the International Financial

Consolidated and Separate Financial Statements

Compiled Accounting Standard AASB 127 Consolidated and Separate Financial Statements This compiled Standard applies to annual reporting periods beginning on or after 1 July 2007. Early application is permitted.

Compiled Accounting Standard AASB 127 Consolidated and Separate Financial Statements This compiled Standard applies to annual reporting periods beginning on or after 1 July 2007. Early application is permitted.

Proposed Statement of Financial Accounting Standards

FEBRUARY 14, 2001 Financial Accounting Series EXPOSURE DRAFT (Revised) Proposed Statement of Financial Accounting Standards Business Combinations and Intangible Assets Accounting for Goodwill Limited Revision

FEBRUARY 14, 2001 Financial Accounting Series EXPOSURE DRAFT (Revised) Proposed Statement of Financial Accounting Standards Business Combinations and Intangible Assets Accounting for Goodwill Limited Revision

JGAAP-IFRS comparison. English version 3.0 [equivalent of Japanese version 4.0]

![JGAAP-IFRS comparison. English version 3.0 [equivalent of Japanese version 4.0]](/thumbs/24/3831703.jpg "JGAAP-IFRS comparison. English version 3.0 [equivalent of Japanese version 4.0]") - comparison English version 3.0 [equivalent of Japanese version 4.0] Contents Contents... 2 Introduction... 3 Presentation of Financial Statements, Accounting Policies, Changes in Accounting Estimates

- comparison English version 3.0 [equivalent of Japanese version 4.0] Contents Contents... 2 Introduction... 3 Presentation of Financial Statements, Accounting Policies, Changes in Accounting Estimates

CHAPTER NINE Group accounts

CHAPTER NINE Group accounts 9.1 GROUP ACCOUNTS 9.1.1 Introduction 9.1.1.1 Authorities shall account for Group Accounts in accordance with IFRS 3 Business Combinations, IAS 27 Consolidated and Separate

CHAPTER NINE Group accounts 9.1 GROUP ACCOUNTS 9.1.1 Introduction 9.1.1.1 Authorities shall account for Group Accounts in accordance with IFRS 3 Business Combinations, IAS 27 Consolidated and Separate

NEPAL ACCOUNTING STANDARDS ON BUSINESS COMBINATIONS

NAS 21 NEPAL ACCOUNTING STANDARDS ON BUSINESS COMBINATIONS CONTENTS Paragraphs OBJECTIVE 1 SCOPE 2-14 Identifying a business combination 5-10 Business combinations involving entities under common control

NAS 21 NEPAL ACCOUNTING STANDARDS ON BUSINESS COMBINATIONS CONTENTS Paragraphs OBJECTIVE 1 SCOPE 2-14 Identifying a business combination 5-10 Business combinations involving entities under common control

08FR-003 Business Combinations IFRS 3 revised 11 January 2008. Key points

08FR-003 Business Combinations IFRS 3 revised 11 January 2008 Contents Background Overview Revised IFRS 3 Revised IAS 27 Effective date and transition Key points The IASB has issued revisions to IFRS 3

08FR-003 Business Combinations IFRS 3 revised 11 January 2008 Contents Background Overview Revised IFRS 3 Revised IAS 27 Effective date and transition Key points The IASB has issued revisions to IFRS 3

A Guide to for Financial Instruments in the Public Sector

November 2011 www.bdo.ca Assurance and accounting A Guide to Accounting for Financial Instruments in the Public Sector In June 2011, the Public Sector Accounting Standards Board released Section PS3450,

November 2011 www.bdo.ca Assurance and accounting A Guide to Accounting for Financial Instruments in the Public Sector In June 2011, the Public Sector Accounting Standards Board released Section PS3450,

Consolidated Financial Statements

STATUTORY BOARD FINANCIAL REPORTING STANDARD SB-FRS 110 Consolidated Financial Statements This standard applies for annual periods beginning on or after 1 January 2013. Earlier application is permitted

STATUTORY BOARD FINANCIAL REPORTING STANDARD SB-FRS 110 Consolidated Financial Statements This standard applies for annual periods beginning on or after 1 January 2013. Earlier application is permitted

GUIDE TO ACCOUNTING STANDARDS FOR PRIVATE ENTERPRISES CHAPTER 45 FINANCIAL INSTRUMENTS

GUIDE TO ACCOUNTING STANDARDS FOR PRIVATE ENTERPRISES CHAPTER 45 FINANCIAL INSTRUMENTS DISCLAIMER This publication was prepared by the Chartered Professional Accountants of Canada (CPA Canada). It has

GUIDE TO ACCOUNTING STANDARDS FOR PRIVATE ENTERPRISES CHAPTER 45 FINANCIAL INSTRUMENTS DISCLAIMER This publication was prepared by the Chartered Professional Accountants of Canada (CPA Canada). It has

ASPE Financial Statement Presentation and Disclosure Checklist

ASPE Financial Statement Presentation and Checklist June 2014 ABOUT THIS CHECKLIST... 3 FINANCIAL STATEMENTS... 4 GENERALLY ACCEPTED ACCOUNTING PRINCIPLES (SECTION 1100)... 4 FINANCIAL STATEMENT PRESENTATION

ASPE Financial Statement Presentation and Checklist June 2014 ABOUT THIS CHECKLIST... 3 FINANCIAL STATEMENTS... 4 GENERALLY ACCEPTED ACCOUNTING PRINCIPLES (SECTION 1100)... 4 FINANCIAL STATEMENT PRESENTATION

Adviser alert Liability or equity? A practical guide to the classification of financial instruments under IAS 32 (revised guide)

") Adviser alert Liability or equity? A practical guide to the classification of financial instruments under IAS 32 (revised guide) April 2013 Overview The Grant Thornton International IFRS team has published

Adviser alert Liability or equity? A practical guide to the classification of financial instruments under IAS 32 (revised guide) April 2013 Overview The Grant Thornton International IFRS team has published

NEED TO KNOW. IFRS 10 Consolidated Financial Statements

NEED TO KNOW IFRS 10 Consolidated Financial Statements 2 IFRS 10 Consolidated Financial Statements SUMMARY In May 2011 the International Accounting Standards Board (IASB) published a package of five new

NEED TO KNOW IFRS 10 Consolidated Financial Statements 2 IFRS 10 Consolidated Financial Statements SUMMARY In May 2011 the International Accounting Standards Board (IASB) published a package of five new

Indian Accounting Standard (Ind AS) 21 The Effects of Changes in Foreign Exchange Rates

21 The Effects of Changes in Foreign Exchange Rates") Indian Accounting Standard (Ind AS) 21 The Effects of Changes in Foreign Exchange Rates Contents Paragraph OBJECTIVE 1-2 SCOPE 3-7 DEFINITIONS 8-16 Elaboration on the definitions 9-16 Functional currency

Indian Accounting Standard (Ind AS) 21 The Effects of Changes in Foreign Exchange Rates Contents Paragraph OBJECTIVE 1-2 SCOPE 3-7 DEFINITIONS 8-16 Elaboration on the definitions 9-16 Functional currency

International Accounting Standard 12 Income Taxes. Objective. Scope. Definitions IAS 12

International Accounting Standard 12 Income Taxes Objective The objective of this Standard is to prescribe the accounting treatment for income taxes. The principal issue in accounting for income taxes

International Accounting Standard 12 Income Taxes Objective The objective of this Standard is to prescribe the accounting treatment for income taxes. The principal issue in accounting for income taxes

The Effects of Changes in Foreign Exchange Rates

HKAS 21 Revised July 2012May 2014 Hong Kong Accounting Standard 21 The Effects of Changes in Foreign Exchange Rates HKAS 21 COPYRIGHT Copyright 2014 Hong Kong Institute of Certified Public Accountants

HKAS 21 Revised July 2012May 2014 Hong Kong Accounting Standard 21 The Effects of Changes in Foreign Exchange Rates HKAS 21 COPYRIGHT Copyright 2014 Hong Kong Institute of Certified Public Accountants

CENTURY ENERGY LTD. FORM 51-102F1 MANAGEMENT DISCUSSION AND ANALYSIS FOR THE YEAR ENDED AUGUST 31, 2014

CENTURY ENERGY LTD. FORM 51-102F1 MANAGEMENT DISCUSSION AND ANALYSIS FOR THE YEAR ENDED AUGUST 31, 2014 The following management s discussion and analysis ( MD&A ), prepared as of December 11, 2014, should

CENTURY ENERGY LTD. FORM 51-102F1 MANAGEMENT DISCUSSION AND ANALYSIS FOR THE YEAR ENDED AUGUST 31, 2014 The following management s discussion and analysis ( MD&A ), prepared as of December 11, 2014, should

Consolidated Statement of Financial Position Sumitomo Corporation and Subsidiaries As of March 31, 2016 and 2015. Millions of U.S.

Consolidated Statement of Financial Position Sumitomo Corporation and Subsidiaries As of March 31, 2016 and 2015 ASSETS Current assets: Cash and cash equivalents 868,755 895,875 $ 7,757 Time deposits 11,930

Consolidated Statement of Financial Position Sumitomo Corporation and Subsidiaries As of March 31, 2016 and 2015 ASSETS Current assets: Cash and cash equivalents 868,755 895,875 $ 7,757 Time deposits 11,930

A&W Food Services of Canada Inc. Consolidated Financial Statements December 30, 2012 and January 1, 2012 (in thousands of dollars)

") A&W Food Services of Canada Inc. Consolidated Financial Statements December 30, and January 1, (in thousands of dollars) February 12, 2013 Independent Auditor s Report To the Shareholders of A&W Food Services

A&W Food Services of Canada Inc. Consolidated Financial Statements December 30, and January 1, (in thousands of dollars) February 12, 2013 Independent Auditor s Report To the Shareholders of A&W Food Services

CANADIAN GAAP IFRS COMPARISON SERIES

WWW.BDO.CA ASSURANCE AND ACCOUNTING CANADIAN GAAP IFRS COMPARISON SERIES Issue 13: Income Taxes Both IFRS and Canadian GAAP are principle based frameworks and, from a conceptual standpoint, many of the

WWW.BDO.CA ASSURANCE AND ACCOUNTING CANADIAN GAAP IFRS COMPARISON SERIES Issue 13: Income Taxes Both IFRS and Canadian GAAP are principle based frameworks and, from a conceptual standpoint, many of the

Condensed Consolidated Statement of Operations and Comprehensive Income (Loss) 3. Condensed Consolidated Balance Sheet 4

3. Condensed Consolidated Balance Sheet 4") CONSOLIDATED FINANCIAL STATEMENTS For the fiscal year ended March 31, 2014 INDEX Page Condensed Consolidated Statement of Operations and Comprehensive Income (Loss) 3 Condensed Consolidated Balance Sheet

CONSOLIDATED FINANCIAL STATEMENTS For the fiscal year ended March 31, 2014 INDEX Page Condensed Consolidated Statement of Operations and Comprehensive Income (Loss) 3 Condensed Consolidated Balance Sheet

Philippine Financial Reporting Standards (Adopted by SEC as of December 31, 2011)

") Standards (Adopted by SEC as of December 31, 2011) Philippine Financial Reporting Framework for the Preparation and Presentation of Financial Statements Conceptual Framework Phase A: Objectives and qualitative

Standards (Adopted by SEC as of December 31, 2011) Philippine Financial Reporting Framework for the Preparation and Presentation of Financial Statements Conceptual Framework Phase A: Objectives and qualitative

Business Combinations

59 CHAP TER 3 Business Combinations A Note On Relevant Accounting Standards 3-0. During the period until 2011 when IFRSs are incorporated into Canadian GAAP, the CICA Handbook contains two different Sections

59 CHAP TER 3 Business Combinations A Note On Relevant Accounting Standards 3-0. During the period until 2011 when IFRSs are incorporated into Canadian GAAP, the CICA Handbook contains two different Sections

Investments in Associates

HKAS 28 Revised June 2011July 2012 Effective for annual periods beginning on or after 1 January 2005* Hong Kong Accounting Standard 28 Investments in Associates *HKAS 28 is applicable for annual periods

HKAS 28 Revised June 2011July 2012 Effective for annual periods beginning on or after 1 January 2005* Hong Kong Accounting Standard 28 Investments in Associates *HKAS 28 is applicable for annual periods

Reporting under IFRSs. Example consolidated financial statements 2013 and guidance notes

Reporting under IFRSs Example consolidated financial statements 2013 and guidance notes Important Disclaimer: This document has been developed as an information resource. It is intended as a guide only

Reporting under IFRSs Example consolidated financial statements 2013 and guidance notes Important Disclaimer: This document has been developed as an information resource. It is intended as a guide only

Transition to International Financial Reporting Standards

Transition to International Financial Reporting Standards Topps Tiles Plc In accordance with IFRS 1, First-time adoption of International Financial Reporting Standards ( IFRS ), Topps Tiles Plc, ( Topps

Transition to International Financial Reporting Standards Topps Tiles Plc In accordance with IFRS 1, First-time adoption of International Financial Reporting Standards ( IFRS ), Topps Tiles Plc, ( Topps

Business Combinations

HKFRS 3 (Revised) Revised July November 2014 Effective for annual periods beginning on or after 1 July 2009 Hong Kong Financial Reporting Standard 3 (Revised) Business Combinations COPYRIGHT Copyright

HKFRS 3 (Revised) Revised July November 2014 Effective for annual periods beginning on or after 1 July 2009 Hong Kong Financial Reporting Standard 3 (Revised) Business Combinations COPYRIGHT Copyright

Consolidated Financial Statements. FUJIFILM Holdings Corporation and Subsidiaries. March 31, 2015 with Report of Independent Auditors

Consolidated Financial Statements FUJIFILM Holdings Corporation and Subsidiaries March 31, 2015 with Report of Independent Auditors Consolidated Financial Statements March 31, 2015 Contents Report of Independent

Consolidated Financial Statements FUJIFILM Holdings Corporation and Subsidiaries March 31, 2015 with Report of Independent Auditors Consolidated Financial Statements March 31, 2015 Contents Report of Independent

Consolidated and other financial statements

Financial reporting developments A comprehensive guide Consolidated and other financial statements Noncontrolling interests, combined financial statements, and parent company financial statements Revised

Financial reporting developments A comprehensive guide Consolidated and other financial statements Noncontrolling interests, combined financial statements, and parent company financial statements Revised

Consolidated Financial Statements

AASB Standard AASB 10 August 2011 Consolidated Financial Statements Obtaining a Copy of this Accounting Standard This Standard is available on the AASB website: www.aasb.gov.au. Alternatively, printed

AASB Standard AASB 10 August 2011 Consolidated Financial Statements Obtaining a Copy of this Accounting Standard This Standard is available on the AASB website: www.aasb.gov.au. Alternatively, printed

The Effects of Changes in Foreign Exchange Rates

Indian Accounting Standard (Ind AS) 21 The Effects of Changes in Foreign Exchange Rates (This Indian Accounting Standard includes paragraphs set in bold type and plain type, which have equal authority.

Indian Accounting Standard (Ind AS) 21 The Effects of Changes in Foreign Exchange Rates (This Indian Accounting Standard includes paragraphs set in bold type and plain type, which have equal authority.

This Executive Summary is part of McGladrey s A Guide to Accounting for Business Combinations and should be read in conjunction with that guide.

Executive Summary This Executive Summary is part of McGladrey s A Guide to Accounting for Business Combinations and should be read in conjunction with that guide. Introduction The current guidance on accounting

Executive Summary This Executive Summary is part of McGladrey s A Guide to Accounting for Business Combinations and should be read in conjunction with that guide. Introduction The current guidance on accounting

How To Understand The Concept Of Control In Ifrs 10

IFRS Group Accounting Standards: application guidance April 2014 IFRS Group Accounting Standards: application guidance April 2014 Crown copyright 2014 You may re-use this information (excluding logos)

IFRS Group Accounting Standards: application guidance April 2014 IFRS Group Accounting Standards: application guidance April 2014 Crown copyright 2014 You may re-use this information (excluding logos)

BLACKHEATH RESOURCES INC. FINANCIAL STATEMENTS 31 DECEMBER 2011