Asset/liability Management for Universal Life. Grant Paulsen Rimcon Inc. November 15, 2001

|

|

|

- Meghan Carter

- 10 years ago

- Views:

Transcription

1 Asset/liability Management for Universal Life Grant Paulsen Rimcon Inc. November 15, 2001

2

3 Step 1: Split the product in two Premiums Reinsurance Premiums Benefits Policyholder fund Risk charges Expense charges Surrender charges MER/spread Insurance Fund Expenses Taxes Return of fund on death or surrender Net death benefit (face value)

4 Step 2: Match the policyholder fund For index linked accounts, buy the underlying index Track liability balances on at least a weekly basis Compare asset returns with index returns and identify sources of tracking error asset/liability mismatch transaction costs backdating tracking of assets to index (i.e. exchange traded funds, index futures) tax effects

tax effects")

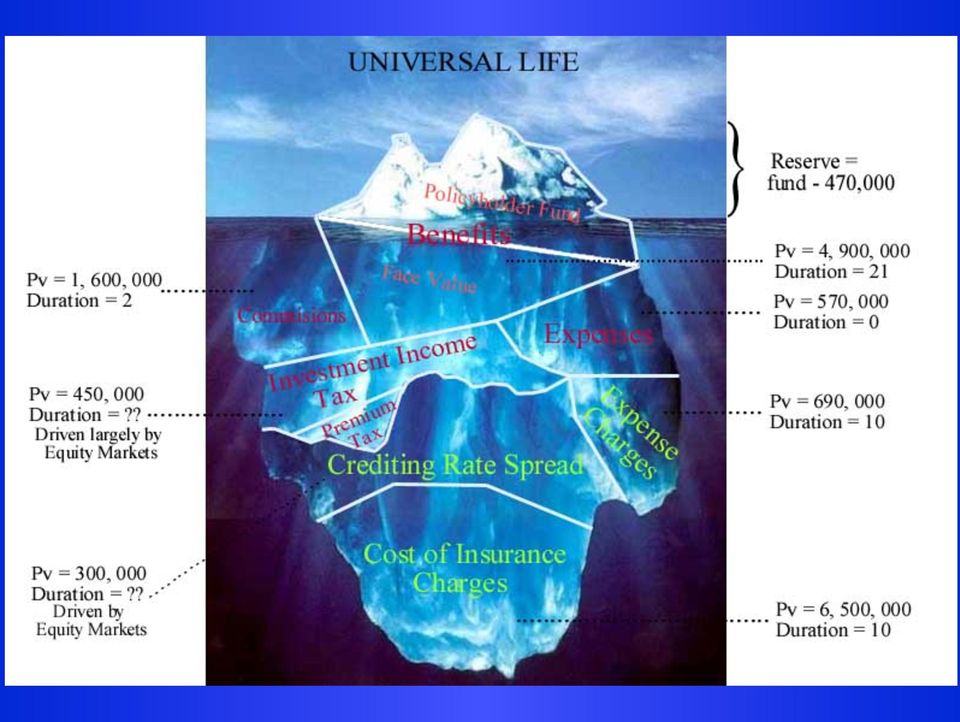

5 Step 3: Match the insurance fund (the hard part) Reserve components of a typical UL policy: Present value Duration Risk charges 6,488, Net benefits (4,881,908) 21 Ceded premiums (2,157,152) 20 Ceded benefits 2,435, Expense charges 693, Expenses (566,236)?? Surrender charges 248,522?? Commissions (1,641,296) 2 Investment income tax (455,153)?? Crediting rate margin 304,609?? Net total 468,811 Note: figures vary (a lot) depending on age of policyholder, age of policy, policy features, fund types, MER levels, modeling assumptions.

depending on age of policyholder, age of policy, policy features, fund types, MER levels,")

6 If interest rates fall 1% Present value Risk charges 6,488,404 7,163,944 Net benefits (4,881,908) (6,475,137) Net 1,606, ,807 A 1% rate decline removes $917,689 worth of profitability from the line of business. Reserves will increase by roughly this amount.

7 The largest risk is in the risk (COI) charge vs. net benefit cash flows 1,400,000 Annual Risk Charge Cash Flows 1,200,000 1,000, , , , ,

8 0 (200,000) (400,000) (600,000) (800,000) (1,000,000) (1,200,000) Annual Death Benefit Cash Flows (net of fund) (1,400,000)

(1,400,000) 0 10 20")

9 Combined COI Charge +Death Benefit Cash Flows 1,000,000 Combined Cash Flows for 1000 Policies ($1 million of annual premium) Reinvestment is assumed at product pricing rate 500,000 0 (500,000) (1,000,000) (1,500,000) ALM Problem: How do we lock in the reinvestment rate at time of issue

10 Inter-segment Notes Combined Risk Charge + Benefit Cash Flows 1,000, , Use the cash to buy long-dated assets that better match the liability profile. 0 (500,000) 1. Sell this cash flow to annuities. (1,000,000) (1,500,000) $ Annuity Asset & Liability Cash Flows 800, , , , , , , , Sell the asset that the inter-segment note replaces and transfer the cash from Annuities to Universal Life

11 Other cash flow components Ceded cash flows premiums and benefits usually have similar durations small positive cash flow (pricing vs. reserving assumptions) long duration offsets some death benefit cash flows Expense charges generally fixed same duration as premiums Expenses interest rate theoretically = inflation + real interest rate higher interest rates => higher inflation theoretical duration is zero how does valuation model treat inflation? Surrender charges short term (generally 5 years or less) surrenders (fund depletion) fall when interest rates rise

12 Problem cash flow components Crediting rate margin depends on fund size => higher fund returns mean larger fund and more crediting rate cash flows when equity markets fall, future MER cash flows decline too movement from equity linked to GICs reduces MERs in high-return scenarios, fewer policies lapse effective duration very sensitive to model assumptions and can only be determined through scenario testing do you believe the current 2-3% MERs will hold up for 40 years? Investment income tax based on a 5-year moving average of 10-year Cda bond yields you have to pay IIT even if equity returns are negative Expenses interest rate theoretically = inflation + real interest rate

13 Summary UL is far more complicated than most other insurance products interest rate risk is potentially huge. Cash flow dynamics are complex, and don t depend only on interest rates. Duration (including key rate duration) is not sufficient. Assumptions (including policyholder behavior) have a large impact on cash flow dynamics (and reserves). You need a well thought out model. You need to understand the valuation software well enough to be sure it is implementing the model correctly. You need to sensitivity test the key assumptions.

Canadian Life Insurance Company Asset/Liability Management Summary Report as at: 31-Jan-08 interest rates as of: 29-Feb-08 Run: 2-Apr-08 20:07 Book

Canadian Life Insurance Company Asset/Liability Management Summary Report as at: 31Jan08 interest rates as of: 29Feb08 Run: 2Apr08 20:07 Book Book Present Modified Effective Projected change in net present

Canadian Life Insurance Company Asset/Liability Management Summary Report as at: 31Jan08 interest rates as of: 29Feb08 Run: 2Apr08 20:07 Book Book Present Modified Effective Projected change in net present

Pricing exercise based on a collection of actuarial assumptions Assumptions generally divided into two sets

Whole Life Pricing Pricing exercise based on a collection of actuarial assumptions Assumptions generally divided into two sets Company specific: Mortality, Lapsation, Expenses, Dividends, etc. Prescription

Whole Life Pricing Pricing exercise based on a collection of actuarial assumptions Assumptions generally divided into two sets Company specific: Mortality, Lapsation, Expenses, Dividends, etc. Prescription

Inter-Segment Notes for Life Insurance Companies. Sound Business and Financial Practices

Guideline Subject: Category: for Life Insurance Companies Sound Business and Financial Practices No: E-12 Date: June 2000 Revised: July 2010 Introduction This guideline establishes OSFI s expectations

Guideline Subject: Category: for Life Insurance Companies Sound Business and Financial Practices No: E-12 Date: June 2000 Revised: July 2010 Introduction This guideline establishes OSFI s expectations

Principles-Based Update - Annuities

Principles-Based Update - Annuities SEAC Fall 2008 Meeting Concurrent Session Life Insurance Cheryl Tibbits, FIAA, FSA, MAAA Towers Perrin November 20, 2008 Current Status of PBA for Annuities Variable

Principles-Based Update - Annuities SEAC Fall 2008 Meeting Concurrent Session Life Insurance Cheryl Tibbits, FIAA, FSA, MAAA Towers Perrin November 20, 2008 Current Status of PBA for Annuities Variable

Hedging at Your Insurance Company

Hedging at Your Insurance Company SEAC Spring 2007 Meeting Winter Liu, FSA, MAAA, CFA June 2007 2006 Towers Perrin Primary Benefits and Motives of Establishing Hedging Programs Hedging can mitigate some

Hedging at Your Insurance Company SEAC Spring 2007 Meeting Winter Liu, FSA, MAAA, CFA June 2007 2006 Towers Perrin Primary Benefits and Motives of Establishing Hedging Programs Hedging can mitigate some

Asset/Liability Management and Innovative Investments

Asset/Liability Management and Innovative Investments By Sylvain Goulet, & Mukund G. Diwan INTRODUCTION Asset/Liability Management ( ALM ) is of course a management tool to optimize investment returns

Asset/Liability Management and Innovative Investments By Sylvain Goulet, & Mukund G. Diwan INTRODUCTION Asset/Liability Management ( ALM ) is of course a management tool to optimize investment returns

The Empire Life Insurance Company

The Empire Life Insurance Company Condensed Interim Consolidated Financial Statements For the six months ended June 30, 2015 Unaudited Issue Date: August 7, 2015 DRAFT NOTICE OF NO AUDITOR REVIEW OF CONDENSED

The Empire Life Insurance Company Condensed Interim Consolidated Financial Statements For the six months ended June 30, 2015 Unaudited Issue Date: August 7, 2015 DRAFT NOTICE OF NO AUDITOR REVIEW OF CONDENSED

Valuation of Universal Life Insurance Contract Liabilities

Educational Note Valuation of Universal Life Insurance Contract Liabilities Committee on Life Insurance Financial Reporting February 2012 Document 212012 Ce document est disponible en français 2012 Canadian

Educational Note Valuation of Universal Life Insurance Contract Liabilities Committee on Life Insurance Financial Reporting February 2012 Document 212012 Ce document est disponible en français 2012 Canadian

THE CHALLENGE OF LOWER

Recent interest rates have declined to levels not seen in many years. Although the downward trend has reversed, low interest rates have already had a major impact on the life insurance industry. INTEREST

Recent interest rates have declined to levels not seen in many years. Although the downward trend has reversed, low interest rates have already had a major impact on the life insurance industry. INTEREST

THE EMPIRE LIFE INSURANCE COMPANY

THE EMPIRE LIFE INSURANCE COMPANY Condensed Interim Consolidated Financial Statements For the nine months ended September 30, 2013 Unaudited Issue Date: November 6, 2013 These condensed interim consolidated

THE EMPIRE LIFE INSURANCE COMPANY Condensed Interim Consolidated Financial Statements For the nine months ended September 30, 2013 Unaudited Issue Date: November 6, 2013 These condensed interim consolidated

Session 9b L&H Insurance in a Low Interest Rate Environment. Christian Liechti

Session 9b L&H Insurance in a Low Interest Rate Environment Christian Liechti L&H Insurance in a Low Interest Rate Environment SOA Annual Symposium 24-25 June 2013 Macau, China Christian Liechti Swiss

Session 9b L&H Insurance in a Low Interest Rate Environment Christian Liechti L&H Insurance in a Low Interest Rate Environment SOA Annual Symposium 24-25 June 2013 Macau, China Christian Liechti Swiss

Actuary s Guide to Reporting on Insurers of Persons Policy Liabilities. Senior Direction, Supervision of Insurers and Control of Right to Practice

Actuary s Guide to Reporting on Insurers of Persons Policy Liabilities Senior Direction, Supervision of Insurers and Control of Right to Practice September 2015 Legal deposit - Bibliothèque et Archives

Actuary s Guide to Reporting on Insurers of Persons Policy Liabilities Senior Direction, Supervision of Insurers and Control of Right to Practice September 2015 Legal deposit - Bibliothèque et Archives

Effective Financial Planning for Life Insurance Companies

6 th Global Conference of Actuaries Effective Financial Planning for Life Insurance Companies Presentation by Kim Hoong CHIN Senior Manager and Consultant Asia Financial Services Topics Recent worldwide

6 th Global Conference of Actuaries Effective Financial Planning for Life Insurance Companies Presentation by Kim Hoong CHIN Senior Manager and Consultant Asia Financial Services Topics Recent worldwide

Session 4: Universal Life

Session 4: Universal Life US GAAP for International Life Insurers Bill Horbatt SFAS 97 Effective 1989 Applicability Limited-Payment Contracts Universal Life-Type Contracts Investment Contracts 2 2 Universal

Session 4: Universal Life US GAAP for International Life Insurers Bill Horbatt SFAS 97 Effective 1989 Applicability Limited-Payment Contracts Universal Life-Type Contracts Investment Contracts 2 2 Universal

CHAPTER 57 - LIFE AND HEALTH REINSURANCE AGREEMENTS

TITLE 210 - NEBRASKA DEPARTMENT OF INSURANCE CHAPTER 57 - LIFE AND HEALTH REINSURANCE AGREEMENTS 001. Authority. This regulation is adopted and promulgated by the Director of Insurance of the State of

TITLE 210 - NEBRASKA DEPARTMENT OF INSURANCE CHAPTER 57 - LIFE AND HEALTH REINSURANCE AGREEMENTS 001. Authority. This regulation is adopted and promulgated by the Director of Insurance of the State of

Session 11: Reinsurance Accounting

Session : Reinsurance Accounting US GAAP for International Life Insurers Hong Kong August 7 Charles Carroll, Ernst & Young Reinsurance Accounting Common Types of Reinsurance Accounting Guidance Short Duration

Session : Reinsurance Accounting US GAAP for International Life Insurers Hong Kong August 7 Charles Carroll, Ernst & Young Reinsurance Accounting Common Types of Reinsurance Accounting Guidance Short Duration

MANAGING RISK IN LIFE INSURANCE: A STUDY OF CHAGING RISK FACTORS OVER THE LAST 10 YEARS IN TAIWAN AND DRAWING LESSONS FOR ALL

MANAGING RISK IN LIFE INSURANCE: A STUDY OF CHAGING RISK FACTORS OVER THE LAST 10 YEARS IN TAIWAN AND DRAWING LESSONS FOR ALL Simon Walpole & Ophelia Au Young Deloitte Actuarial & Insurance Solutions,

MANAGING RISK IN LIFE INSURANCE: A STUDY OF CHAGING RISK FACTORS OVER THE LAST 10 YEARS IN TAIWAN AND DRAWING LESSONS FOR ALL Simon Walpole & Ophelia Au Young Deloitte Actuarial & Insurance Solutions,

STATUTORY CALENDAR YEAR INTEREST RATES BASED ON THE 1980 AMENDMENTS TO THE NAIC STANDARD VALUATION AND NONFORFEITURE LAWS. Valuation Interest Rate

BASED ON THE 1980 AMENDMENTS TO THE NAIC STANDARD VALUATION AND NONFORFEITURE LAWS A. Life Insurance Valuation and Nonforfeiture Rates: (years) Valuation Rate Nonforfeiture Rate1 2006 2006 10 or less 4.50

BASED ON THE 1980 AMENDMENTS TO THE NAIC STANDARD VALUATION AND NONFORFEITURE LAWS A. Life Insurance Valuation and Nonforfeiture Rates: (years) Valuation Rate Nonforfeiture Rate1 2006 2006 10 or less 4.50

GLOSSARY. A contract that provides for periodic payments to an annuitant for a specified period of time, often until the annuitant s death.

The glossary contains explanations of certain terms and definitions used in this prospectus in connection with us and our business. The terms and their meanings may not correspond to standard industry

The glossary contains explanations of certain terms and definitions used in this prospectus in connection with us and our business. The terms and their meanings may not correspond to standard industry

Pricing Lapse-Supported Products

Pricing Lapse-Supported Products Southeastern Actuaries Conference June 21, 2007 Stephanie Grass Direct Dial: (314) 719-5915 Lapse-supported products are common in both the US and the Canadian insurance

Pricing Lapse-Supported Products Southeastern Actuaries Conference June 21, 2007 Stephanie Grass Direct Dial: (314) 719-5915 Lapse-supported products are common in both the US and the Canadian insurance

TABLE OF CONTENTS. Executive Summary 3. Introduction 5. Purposes of the Joint Research Project 6

TABLE OF CONTENTS Executive Summary 3 Introduction 5 Purposes of the Joint Research Project 6 Background 7 1. Contract and timeframe illustrated 7 2. Liability measurement bases 9 3. Earnings 10 Consideration

TABLE OF CONTENTS Executive Summary 3 Introduction 5 Purposes of the Joint Research Project 6 Background 7 1. Contract and timeframe illustrated 7 2. Liability measurement bases 9 3. Earnings 10 Consideration

Universal Life Insurance

Universal Life Insurance Lecture: Weeks 11-12 Thanks to my friend J. Dhaene, KU Leuven, for ideas here drawn from his notes. Lecture: Weeks 11-12 (STT 456) Universal Life Insurance Spring 2015 - Valdez

Universal Life Insurance Lecture: Weeks 11-12 Thanks to my friend J. Dhaene, KU Leuven, for ideas here drawn from his notes. Lecture: Weeks 11-12 (STT 456) Universal Life Insurance Spring 2015 - Valdez

Unbundling Insurance Contracts

IASB/FASB meeting 16 February 2011 Agenda paper 3J UFS Unbundling Insurance Contracts Leonard Reback February 16, 2011 Overview Potential benefits and costs from unbundling Single Premium Immediate Annuity

IASB/FASB meeting 16 February 2011 Agenda paper 3J UFS Unbundling Insurance Contracts Leonard Reback February 16, 2011 Overview Potential benefits and costs from unbundling Single Premium Immediate Annuity

Practice Education Course Individual Life and Annuities Exam June 2011 TABLE OF CONTENTS

Practice Education Course Individual Life and Annuities Exam June 2011 TABLE OF CONTENTS THIS EXAM CONSISTS OF SEVEN (7) WRITTEN ANSWER QUESTIONS WORTH 51 POINTS AND EIGHT (8) MULTIPLE CHOICE QUESTIONS

Practice Education Course Individual Life and Annuities Exam June 2011 TABLE OF CONTENTS THIS EXAM CONSISTS OF SEVEN (7) WRITTEN ANSWER QUESTIONS WORTH 51 POINTS AND EIGHT (8) MULTIPLE CHOICE QUESTIONS

NEDGROUP LIFE FINANCIAL MANAGEMENT PRINCIPLES AND PRACTICES OF ASSURANCE COMPANY LIMITED. A member of the Nedbank group

NEDGROUP LIFE ASSURANCE COMPANY LIMITED PRINCIPLES AND PRACTICES OF FINANCIAL MANAGEMENT A member of the Nedbank group We subscribe to the Code of Banking Practice of The Banking Association South Africa

NEDGROUP LIFE ASSURANCE COMPANY LIMITED PRINCIPLES AND PRACTICES OF FINANCIAL MANAGEMENT A member of the Nedbank group We subscribe to the Code of Banking Practice of The Banking Association South Africa

Disclosure of European Embedded Value as of March 31, 2015

UNOFFICIAL TRANSLATION Although the Company pays close attention to provide English translation of the information disclosed in Japanese, the Japanese original prevails over its English translation in

UNOFFICIAL TRANSLATION Although the Company pays close attention to provide English translation of the information disclosed in Japanese, the Japanese original prevails over its English translation in

How To Become A Life Insurance Agent

Traditional, investment, and risk management actuaries in the life insurance industry Presentation at California Actuarial Student Conference University of California, Santa Barbara April 4, 2015 Frank

Traditional, investment, and risk management actuaries in the life insurance industry Presentation at California Actuarial Student Conference University of California, Santa Barbara April 4, 2015 Frank

VALUATION OF DEBT CONTRACTS AND THEIR PRICE VOLATILITY CHARACTERISTICS QUESTIONS See answers below

VALUATION OF DEBT CONTRACTS AND THEIR PRICE VOLATILITY CHARACTERISTICS QUESTIONS See answers below 1. Determine the value of the following risk-free debt instrument, which promises to make the respective

VALUATION OF DEBT CONTRACTS AND THEIR PRICE VOLATILITY CHARACTERISTICS QUESTIONS See answers below 1. Determine the value of the following risk-free debt instrument, which promises to make the respective

Tax-Exempt Rules for Life Insurance And the changes that are coming! Dominik Briault, FSA, FCIA Director, Actuarial Marketing Services

Tax-Exempt Rules for Life Insurance And the changes that are coming! Dominik Briault, FSA, FCIA Director, Actuarial Marketing Services This material is for information purposes only and shouldn t be construed

Tax-Exempt Rules for Life Insurance And the changes that are coming! Dominik Briault, FSA, FCIA Director, Actuarial Marketing Services This material is for information purposes only and shouldn t be construed

Variable Annuity Living Benefits

Variable Annuity Living Benefits Darryl Wagner, Deloitte Consulting Agenda Types of Living Benefits Introduction to FAS133 Definition of a Derivative Identifying Embedded Derivatives Valuing Contracts

Variable Annuity Living Benefits Darryl Wagner, Deloitte Consulting Agenda Types of Living Benefits Introduction to FAS133 Definition of a Derivative Identifying Embedded Derivatives Valuing Contracts

PNB Life Insurance Inc. Risk Management Framework

1. Capital Management and Management of Insurance and Financial Risks Although life insurance companies are in the business of taking risks, the Company limits its risk exposure only to measurable and

1. Capital Management and Management of Insurance and Financial Risks Although life insurance companies are in the business of taking risks, the Company limits its risk exposure only to measurable and

Personal Retirement Analysis. Jim Sample. for. New Scenario (5/26/2014 4:04:47 AM) Prepared By Neal Frankle Sample Financial Plan

Prepared By Neal Frankle Sample Financial Plan") Personal Retirement Analysis for Jim Sample Prepared By Neal Frankle Sample Financial Plan IMPORTANT: The illustrations or other information generated by this report regarding the likelihood of various

Personal Retirement Analysis for Jim Sample Prepared By Neal Frankle Sample Financial Plan IMPORTANT: The illustrations or other information generated by this report regarding the likelihood of various

THE EMPIRE LIFE INSURANCE COMPANY

THE EMPIRE LIFE INSURANCE COMPANY Condensed Interim Consolidated Financial Statements For the six months ended June 30, 2013 Unaudited Issue Date: August 9, 2013 These condensed interim consolidated financial

THE EMPIRE LIFE INSURANCE COMPANY Condensed Interim Consolidated Financial Statements For the six months ended June 30, 2013 Unaudited Issue Date: August 9, 2013 These condensed interim consolidated financial

A chapter on Valuation basis covering the following minimum criteria should also be displayed on the web-site of the Insurers.

L-42 42- Valuation Basis (Life Insurance) A chapter on Valuation basis covering the following minimum criteria should also be displayed on the web-site of the Insurers. Data The company maintains the Policy

L-42 42- Valuation Basis (Life Insurance) A chapter on Valuation basis covering the following minimum criteria should also be displayed on the web-site of the Insurers. Data The company maintains the Policy

SURVEY ON ASSET LIABILITY MANAGEMENT PRACTICES OF CANADIAN LIFE INSURANCE COMPANIES

QUESTIONNAIRE SURVEY ON ASSET LIABILITY MANAGEMENT PRACTICES OF CANADIAN LIFE INSURANCE COMPANIES MARCH 2001 2001 Canadian Institute of Actuaries Document 20113 Ce questionnaire est disponible en français

QUESTIONNAIRE SURVEY ON ASSET LIABILITY MANAGEMENT PRACTICES OF CANADIAN LIFE INSURANCE COMPANIES MARCH 2001 2001 Canadian Institute of Actuaries Document 20113 Ce questionnaire est disponible en français

An Assessment of No Lapse Guarantee Products and Alternatives. Prepared and Researched by

An Assessment of No Lapse Guarantee Products and Alternatives Prepared and Researched by No Lapse Guarantee (NLG) products continue to be very popular with clients, primarily for their low cost and guaranteed

An Assessment of No Lapse Guarantee Products and Alternatives Prepared and Researched by No Lapse Guarantee (NLG) products continue to be very popular with clients, primarily for their low cost and guaranteed

ON THE RISK ADJUSTED DISCOUNT RATE FOR DETERMINING LIFE OFFICE APPRAISAL VALUES BY M. SHERRIS B.A., M.B.A., F.I.A., F.I.A.A. 1.

ON THE RISK ADJUSTED DISCOUNT RATE FOR DETERMINING LIFE OFFICE APPRAISAL VALUES BY M. SHERRIS B.A., M.B.A., F.I.A., F.I.A.A. 1. INTRODUCTION 1.1 A number of papers have been written in recent years that

ON THE RISK ADJUSTED DISCOUNT RATE FOR DETERMINING LIFE OFFICE APPRAISAL VALUES BY M. SHERRIS B.A., M.B.A., F.I.A., F.I.A.A. 1. INTRODUCTION 1.1 A number of papers have been written in recent years that

U.S. GAAP, From Basic Application to Current Topics Seminar August 31 September 1, 2009. 4A: Universal Life and Deferred Annuities Under GAAP (Basic)

") U.S. GAAP, From Basic Application to Current Topics Seminar August 31 September 1, 2009 4A: Universal Life and Deferred Annuities Under GAAP (Basic) Mark Freedman GAAP for Universal Life and Deferred Annuity

U.S. GAAP, From Basic Application to Current Topics Seminar August 31 September 1, 2009 4A: Universal Life and Deferred Annuities Under GAAP (Basic) Mark Freedman GAAP for Universal Life and Deferred Annuity

Main Business Indicators

Supplementary Financial Data Main Business Indicators (1) Policies in Force and New Policies 1) Policies in Force (Number of policies, millions of yen, %) As of March 31 2015 2014 Individual insurance

Supplementary Financial Data Main Business Indicators (1) Policies in Force and New Policies 1) Policies in Force (Number of policies, millions of yen, %) As of March 31 2015 2014 Individual insurance

AXA s approach to Asset Liability Management. HELVEA Insurance Capital Adequacy and Solvency Day April 28th, 2005

AXA s approach to Asset Liability Management HELVEA Insurance Capital Adequacy and Solvency Day April 28th, 2005 ALM in AXA has always been based on a long-term view Even though Solvency II framework is

AXA s approach to Asset Liability Management HELVEA Insurance Capital Adequacy and Solvency Day April 28th, 2005 ALM in AXA has always been based on a long-term view Even though Solvency II framework is

retirement income solutions *Advisor Design guide for Life s brighter under the sun What s inside Retirement income solutions advisor guide USE ONLY

Retirement income solutions advisor guide *Advisor USE ONLY Design guide for retirement income solutions What s inside Discussing retirement needs with clients Retirement income product comparison Creating

Retirement income solutions advisor guide *Advisor USE ONLY Design guide for retirement income solutions What s inside Discussing retirement needs with clients Retirement income product comparison Creating

SOA 2012 Life & Annuity Symposium May 21-22, 2012. Session 31 PD, Life Insurance Illustration Regulation: 15 Years Later

SOA 2012 Life & Annuity Symposium May 21-22, 2012 Session 31 PD, Life Insurance Illustration Regulation: 15 Years Later Moderator: Kurt A. Guske, FSA, MAAA Presenters: Gayle L. Donato, FSA, MAAA Donna

SOA 2012 Life & Annuity Symposium May 21-22, 2012 Session 31 PD, Life Insurance Illustration Regulation: 15 Years Later Moderator: Kurt A. Guske, FSA, MAAA Presenters: Gayle L. Donato, FSA, MAAA Donna

Insured Annuities: Beyond the Basics

Insured Annuities: Beyond the Basics Achieving a great after-tax return on fixed-income assets John M. Nicola, CLU, CHFC, CFP Table of Contents Introduction.................................. 3 Insured

Insured Annuities: Beyond the Basics Achieving a great after-tax return on fixed-income assets John M. Nicola, CLU, CHFC, CFP Table of Contents Introduction.................................. 3 Insured

IAA PAPER VALUATION OF RISK ADJUSTED CASH FLOWS AND THE SETTING OF DISCOUNT RATES THEORY AND PRACTICE

Introduction This document refers to sub-issue 11G of the IASC Insurance Issues paper and proposes a method to value risk-adjusted cash flows (refer to the IAA paper INSURANCE LIABILITIES - VALUATION &

Introduction This document refers to sub-issue 11G of the IASC Insurance Issues paper and proposes a method to value risk-adjusted cash flows (refer to the IAA paper INSURANCE LIABILITIES - VALUATION &

Life Insurance risk management in the Insurance company : CSOB case studies

Life Insurance risk management in the Insurance company : CSOB case studies Content Topics : case study Life Insurance risk management, 1. Life Insurance 2. Case study what is life insurance product and

Life Insurance risk management in the Insurance company : CSOB case studies Content Topics : case study Life Insurance risk management, 1. Life Insurance 2. Case study what is life insurance product and

Disclosure of Market Consistent Embedded Value as at March 31, 2015

May 20, 2015 Sompo Japan Nipponkoa Himawari Life Insurance, Inc. Disclosure of Market Consistent Embedded Value as at March 31, 2015 Sompo Japan Nipponkoa Himawari Life Insurance, Inc. ( Himawari Life,

May 20, 2015 Sompo Japan Nipponkoa Himawari Life Insurance, Inc. Disclosure of Market Consistent Embedded Value as at March 31, 2015 Sompo Japan Nipponkoa Himawari Life Insurance, Inc. ( Himawari Life,

Kansas City 1Life Insurance Company

Kansas City 1Life Insurance Company 2011 First Quarter Report Includes our subsidiaries: Sunset Life Insurance Company of America Old American Insurance Company Sunset Financial Services, Inc. Post Office

Kansas City 1Life Insurance Company 2011 First Quarter Report Includes our subsidiaries: Sunset Life Insurance Company of America Old American Insurance Company Sunset Financial Services, Inc. Post Office

Agenda. Session 3: GAAP for Traditional Non-Par Products SFAS 60 and SFAS 97 Limited Pay. Amsterdam 2007 Tom Herget PolySystems, Inc.

Session 3: GAAP for Traditional Non-Par Products SFAS 60 and SFAS 97 Limited Pay Amsterdam 2007 Tom Herget PolySystems, Inc. Agenda Overview Long Duration Contracts Benefit Reserves Deferred Policy Acquisition

Session 3: GAAP for Traditional Non-Par Products SFAS 60 and SFAS 97 Limited Pay Amsterdam 2007 Tom Herget PolySystems, Inc. Agenda Overview Long Duration Contracts Benefit Reserves Deferred Policy Acquisition

Life Insurance Corporation (Singapore)Pte Ltd UEN 201210695E MANAGEMENT REPORT 31/12/2014

Pte Ltd UEN 201210695E MANAGEMENT REPORT 31/12/2014") Life Insurance Corporation (Singapore)Pte Ltd UEN 201210695E MANAGEMENT REPORT 31/12/2014 LIFE INSURANCE CORPORATION (SINGAPORE) PTE. LTD. For the financial year from 1 January 2014 to 31 December 2014

Life Insurance Corporation (Singapore)Pte Ltd UEN 201210695E MANAGEMENT REPORT 31/12/2014 LIFE INSURANCE CORPORATION (SINGAPORE) PTE. LTD. For the financial year from 1 January 2014 to 31 December 2014

National specific template Log NS.09 best estimate assumptions for life insurance risks

National specific template Log NS.09 best estimate assumptions for life insurance risks CELL(S) ITEM INSTRUCTIONS N/A General Comment This template is applicable to life insurers and life reinsurers. The

National specific template Log NS.09 best estimate assumptions for life insurance risks CELL(S) ITEM INSTRUCTIONS N/A General Comment This template is applicable to life insurers and life reinsurers. The

>Most investors spend the majority of their time thinking and planning

Generating Retirement Income using a Systematic Withdrawal Plan SPECIAL REPORT >Most investors spend the majority of their time thinking and planning around how best to save for retirement. But once you

Generating Retirement Income using a Systematic Withdrawal Plan SPECIAL REPORT >Most investors spend the majority of their time thinking and planning around how best to save for retirement. But once you

FINANCIAL REVIEW. 18 Selected Financial Data 20 Management s Discussion and Analysis of Financial Condition and Results of Operations

2012 FINANCIAL REVIEW 18 Selected Financial Data 20 Management s Discussion and Analysis of Financial Condition and Results of Operations 82 Quantitative and Qualitative Disclosures About Market Risk 88

2012 FINANCIAL REVIEW 18 Selected Financial Data 20 Management s Discussion and Analysis of Financial Condition and Results of Operations 82 Quantitative and Qualitative Disclosures About Market Risk 88

Olav Jones, Head of Insurance Risk

Getting you there. What is Risk Management of an Insurance Company, a view of a Head of Insurance Risk? Olav Jones, Head of Insurance Risk Olav Jones 29-11-2006 1 Agenda I. Risk Management in Insurance

Getting you there. What is Risk Management of an Insurance Company, a view of a Head of Insurance Risk? Olav Jones, Head of Insurance Risk Olav Jones 29-11-2006 1 Agenda I. Risk Management in Insurance

INSTITUTE AND FACULTY OF ACTUARIES EXAMINATION

INSTITUTE AND FACULTY OF ACTUARIES EXAMINATION 30 April 2015 (am) Subject SA2 Life Insurance Specialist Applications Time allowed: Three hours INSTRUCTIONS TO THE CANDIDATE 1. Enter all the candidate and

INSTITUTE AND FACULTY OF ACTUARIES EXAMINATION 30 April 2015 (am) Subject SA2 Life Insurance Specialist Applications Time allowed: Three hours INSTRUCTIONS TO THE CANDIDATE 1. Enter all the candidate and

SOA Annual Symposium Shanghai. November 5-6, 2012. Shanghai, China. Session 2a: Capital Market Drives Investment Strategy.

SOA Annual Symposium Shanghai November 5-6, 2012 Shanghai, China Session 2a: Capital Market Drives Investment Strategy Genghui Wu Capital Market Drives Investment Strategy Genghui Wu FSA, CFA, FRM, MAAA

SOA Annual Symposium Shanghai November 5-6, 2012 Shanghai, China Session 2a: Capital Market Drives Investment Strategy Genghui Wu Capital Market Drives Investment Strategy Genghui Wu FSA, CFA, FRM, MAAA

Bond Valuation. What is a bond?

Lecture: III 1 What is a bond? Bond Valuation When a corporation wishes to borrow money from the public on a long-term basis, it usually does so by issuing or selling debt securities called bonds. A bond

Lecture: III 1 What is a bond? Bond Valuation When a corporation wishes to borrow money from the public on a long-term basis, it usually does so by issuing or selling debt securities called bonds. A bond

Plan of Operation of Phoenix Life Insurance Company

THIS PLAN OF OPERATION AND RELATED ACTUARIAL PROJECTION HAVE BEEN PREPARED SOLELY FOR USE OF THE NEW YORK INSURANCE DEPARTMENT UNDER SECTION 7312 OF THE NEW YORK INSURANCE LAW AND IN ACCORDANCE WITH THE

THIS PLAN OF OPERATION AND RELATED ACTUARIAL PROJECTION HAVE BEEN PREPARED SOLELY FOR USE OF THE NEW YORK INSURANCE DEPARTMENT UNDER SECTION 7312 OF THE NEW YORK INSURANCE LAW AND IN ACCORDANCE WITH THE

Financial Engineering g and Actuarial Science In the Life Insurance Industry

Financial Engineering g and Actuarial Science In the Life Insurance Industry Presentation at USC October 31, 2013 Frank Zhang, CFA, FRM, FSA, MSCF, PRM Vice President, Risk Management Pacific Life Insurance

Financial Engineering g and Actuarial Science In the Life Insurance Industry Presentation at USC October 31, 2013 Frank Zhang, CFA, FRM, FSA, MSCF, PRM Vice President, Risk Management Pacific Life Insurance

INTRODUCTION. DONALD DUVAL Director of Research AON Consulting, United Kingdom

DONALD DUVAL Director of Research AON Consulting, United Kingdom INTRODUCTION I have a rather narrower subject matter than David and inevitably some of what I am going to say actually goes over the grounds

DONALD DUVAL Director of Research AON Consulting, United Kingdom INTRODUCTION I have a rather narrower subject matter than David and inevitably some of what I am going to say actually goes over the grounds

Universal Life Insurance Duration Measures

Universal Life Insurance Duration Measures Peter Alonzi Professor of Economics and Finance Brennan School of Business Dominican University 7900 W. Division Fine Arts 220-C River Forest, Illinois 60305

Universal Life Insurance Duration Measures Peter Alonzi Professor of Economics and Finance Brennan School of Business Dominican University 7900 W. Division Fine Arts 220-C River Forest, Illinois 60305

Understanding Sun Par Protector and Sun Par Accumulator

LIFE INSURANCE Participating whole life Understanding Sun Par Protector and Sun Par Accumulator POLICYHOLDER DIVIDENDS Sun Par Protector and Sun Par Accumulator are participating life insurance products.

LIFE INSURANCE Participating whole life Understanding Sun Par Protector and Sun Par Accumulator POLICYHOLDER DIVIDENDS Sun Par Protector and Sun Par Accumulator are participating life insurance products.

Equity-Based Insurance Guarantees Conference November 18-19, 2013. Atlanta, GA. GAAP and Statutory Valuation of Variable Annuities

Equity-Based Insurance Guarantees Conference November 18-19, 2013 Atlanta, GA GAAP and Statutory Valuation of Variable Annuities Heather Remes GAAP and Statutory Valuation of Variable Annuities Heather

Equity-Based Insurance Guarantees Conference November 18-19, 2013 Atlanta, GA GAAP and Statutory Valuation of Variable Annuities Heather Remes GAAP and Statutory Valuation of Variable Annuities Heather

THE INSURANCE BUSINESS (SOLVENCY) RULES 2015

RULES 2015") THE INSURANCE BUSINESS (SOLVENCY) RULES 2015 Table of Contents Part 1 Introduction... 2 Part 2 Capital Adequacy... 4 Part 3 MCR... 7 Part 4 PCR... 10 Part 5 - Internal Model... 23 Part 6 Valuation... 34

THE INSURANCE BUSINESS (SOLVENCY) RULES 2015 Table of Contents Part 1 Introduction... 2 Part 2 Capital Adequacy... 4 Part 3 MCR... 7 Part 4 PCR... 10 Part 5 - Internal Model... 23 Part 6 Valuation... 34

Institute of Actuaries of India

Institute of Actuaries of India INDICATIVE SOLUTION May 2012 Examination Subject SA2 Life Insurance Introduction The indicative solution has been written by the Examiners with the aim of helping candidates.

Institute of Actuaries of India INDICATIVE SOLUTION May 2012 Examination Subject SA2 Life Insurance Introduction The indicative solution has been written by the Examiners with the aim of helping candidates.

Special Considerations relating to December 31, 2015 Reserves and Other Solvency Issues

Andrew M. Cuomo Governor Anthony Albanese Acting Superintendent November 13, 2015 These considerations pertain to life insurance companies and fraternal benefit societies doing business in New York, and

Andrew M. Cuomo Governor Anthony Albanese Acting Superintendent November 13, 2015 These considerations pertain to life insurance companies and fraternal benefit societies doing business in New York, and

LIFE INSURANCE RATING METHODOLOGY CREDIT RATING AGENCY OF

LIFE INSURANCE RATING METHODOLOGY CREDIT RATING AGENCY OF BANGLADESH LIMITED 1 CRAB S RATING PROCESS An independent and professional approach of the CRAB is designed to ensure reliable, consistent and

LIFE INSURANCE RATING METHODOLOGY CREDIT RATING AGENCY OF BANGLADESH LIMITED 1 CRAB S RATING PROCESS An independent and professional approach of the CRAB is designed to ensure reliable, consistent and

Insights. Investment strategy design for defined contribution pension plans. An Asset-Liability Risk Management Challenge

Insights Investment strategy design for defined contribution pension plans Philip Mowbray [email protected] The widespread growth of Defined Contribution (DC) plans as the core retirement savings

Insights Investment strategy design for defined contribution pension plans Philip Mowbray [email protected] The widespread growth of Defined Contribution (DC) plans as the core retirement savings

Fair value of insurance liabilities: unit linked / variable business

Fair value of insurance liabilities: unit linked / variable business The fair value treatment of unit linked / variable business differs from that of the traditional policies; below a description of a

Fair value of insurance liabilities: unit linked / variable business The fair value treatment of unit linked / variable business differs from that of the traditional policies; below a description of a

Annuities and decumulation phase of retirement. Chris Daykin UK Government Actuary Chairman, PBSS Section of IAA

Annuities and decumulation phase of retirement Chris Daykin UK Government Actuary Chairman, PBSS Section of IAA CASH LUMP SUM AT RETIREMENT CASH INSTEAD OF PENSION > popular with pension scheme members

Annuities and decumulation phase of retirement Chris Daykin UK Government Actuary Chairman, PBSS Section of IAA CASH LUMP SUM AT RETIREMENT CASH INSTEAD OF PENSION > popular with pension scheme members

Repercussions of a Sustained Low Interest Rate Environment on Life Insurance Products

Repercussions of a Sustained Low Interest Rate Environment on Life Insurance Products All life insurance companies ( carriers ) are financial intermediaries. They buy investments like bonds and then repackage

Repercussions of a Sustained Low Interest Rate Environment on Life Insurance Products All life insurance companies ( carriers ) are financial intermediaries. They buy investments like bonds and then repackage

Life Insurance Corporation (Singapore)Pte Ltd UEN 201210695E MANAGEMENT REPORT 31/12/2013

Pte Ltd UEN 201210695E MANAGEMENT REPORT 31/12/2013") Life Insurance Corporation (Singapore)Pte Ltd UEN 201210695E MANAGEMENT REPORT 31/12/2013 LIFE INSURANCE CORPORATION (SINGAPORE) PTE. LTD. For the financial period from 1 January 2013 to 31 December 2013

Life Insurance Corporation (Singapore)Pte Ltd UEN 201210695E MANAGEMENT REPORT 31/12/2013 LIFE INSURANCE CORPORATION (SINGAPORE) PTE. LTD. For the financial period from 1 January 2013 to 31 December 2013

SECONDARY GUARANTEES FOR UNIT LINKED LIFE INSURANCE THE NEED, FEATURES AND RESERVING

SECONDARY GUARANTEES FOR UNIT LINKED LIFE INSURANCE THE NEED, FEATURES AND RESERVING By Irvinder Singh Kohli, Rajneet Kaur, Ritu Behl & Ankur Goel ABSTRACT This paper introduces ULIP products and talks

SECONDARY GUARANTEES FOR UNIT LINKED LIFE INSURANCE THE NEED, FEATURES AND RESERVING By Irvinder Singh Kohli, Rajneet Kaur, Ritu Behl & Ankur Goel ABSTRACT This paper introduces ULIP products and talks

Financial Economics and Canadian Life Insurance Valuation

Report Financial Economics and Canadian Life Insurance Valuation Task Force on Financial Economics September 2006 Document 206103 Ce document est disponible en français 2006 Canadian Institute of Actuaries

Report Financial Economics and Canadian Life Insurance Valuation Task Force on Financial Economics September 2006 Document 206103 Ce document est disponible en français 2006 Canadian Institute of Actuaries

Guidance for the Development of a Models-Based Solvency Framework for Canadian Life Insurance Companies

Guidance for the Development of a Models-Based Solvency Framework for Canadian Life Insurance Companies January 2010 Background The MCCSR Advisory Committee was established to develop proposals for a new

Guidance for the Development of a Models-Based Solvency Framework for Canadian Life Insurance Companies January 2010 Background The MCCSR Advisory Committee was established to develop proposals for a new

Asset Liability Management for Australian Life Insurers Anton Kapel Zac Roberts

Asset Liability Management for Australian Life Insurers Anton Kapel Zac Roberts Copyright 2006, the Tillinghast Business of Towers Perrin. All rights reserved. A licence to publish is granted to the Institute

Asset Liability Management for Australian Life Insurers Anton Kapel Zac Roberts Copyright 2006, the Tillinghast Business of Towers Perrin. All rights reserved. A licence to publish is granted to the Institute

Valuation Report on Prudential Annuities Limited as at 31 December 2003. The investigation relates to 31 December 2003.

PRUDENTIAL ANNUITIES LIMITED Returns for the year ended 31 December 2003 SCHEDULE 4 Valuation Report on Prudential Annuities Limited as at 31 December 2003 1. Date of investigation The investigation relates

PRUDENTIAL ANNUITIES LIMITED Returns for the year ended 31 December 2003 SCHEDULE 4 Valuation Report on Prudential Annuities Limited as at 31 December 2003 1. Date of investigation The investigation relates