Lease vs.purchase Education Replay

|

|

|

- Emerald Bond

- 8 years ago

- Views:

Transcription

1 Lease vs.purchase Education Replay

2 Disclaimer This [lease/purchase analysis tool] is provided to you solely as a reference tool and neither International Business Machines Corporation (IBM) nor IBM Credit LLC (IBM Credit) is providing to you, or intends to provide or offer tax, accounting or legal advice. You are advised not to rely on this analysis. You are responsible for making your own analysis including: (i) accessing the adequacy and accuracy of the variables input to the model and (ii) determining whether the model contains all of the appropriate factors that may be relevant to your lease/purchase analysis. IBM and IBM Credit make no guarantee or representations with respect to the analysis, the analysis tool or the applicability of this analysis to your business or accounting methods. You should consult with your own financial advisors. Any tax or accounting treatment decisions made by you or on your behalf are solely your responsibility. 2

3 The bottom line IBM Global Financing offers financial solutions that are a better alternative to purchase Less expensive Provide more flexibility than purchase Avoid end of life disposal risk Let customer focus on business value of IT rather than IT asset issues 3

4 Lease vs purchase analysis Lease is a form of debt Does the firm feel it has available debt capacity? Two basic questions in lease vs purchase analysis Lease vs cash from operations Lease vs other forms of debt Technique used: Primary-Net present value of after-tax cash flows Which alternative maximizes the firm s value? Secondary-Period cash flow considerations 4

5 Lease vs purchase analysis questions Customer expected salvage value at end of useful life 5% a safe estimate for 36 month useful life Incremental borrowing rate What interest rate can it borrow at for comparable debt? Secured, term loan Not short term, line of credit Bottom line: Leasing is almost always more attractive than purchase for a 3 year useful life IBM Global Financing Residual Value position vs retail fair market value of asset 5

6 Lease vs purchase common misconceptions Lower interest rates make leasing unattractive Leasing is actually more attractive in a low interest rate environment Lease rates are lowered in a low interest rate environment Time value of money effect for MACRS reduced due to low interest rates Companies can expense IT purchases on their taxes IRS mandates all IT purchases are depreciated on a 5 year schedule Companies can expense IT assets on their financial books, if they consider them to have <1 year useful life. Financial accounting treatment does not affect after tax cash flow based analysis Leasing is more attractive for AMT taxpayers The effect is minimal with the new tax code 6

7 Addressing leasing objections Cash is free Cash has an opportunity cost-cash is limited Our interest rate is lower than IBM Global Financing s interest rate Fair Market Value leasing offers customers a strategic advantage Less expensive than purchase Provides more flexibility and less risk than ownership Can finance with low-cost short-term debt Short-term debt for short-term uses (working capital) Debt holder oversight Rising interest rates 7

Debt holder oversight Rising")

8 IBM Global Financing lease vs purchase tool Automates lease vs purchase analysis using industry-standard model Net Present Value after-tax cash flows analysis Period cash flows US and Canadian versions are now available on the IBM Global Financing PartnerWorld website /partnerworld/financing 8

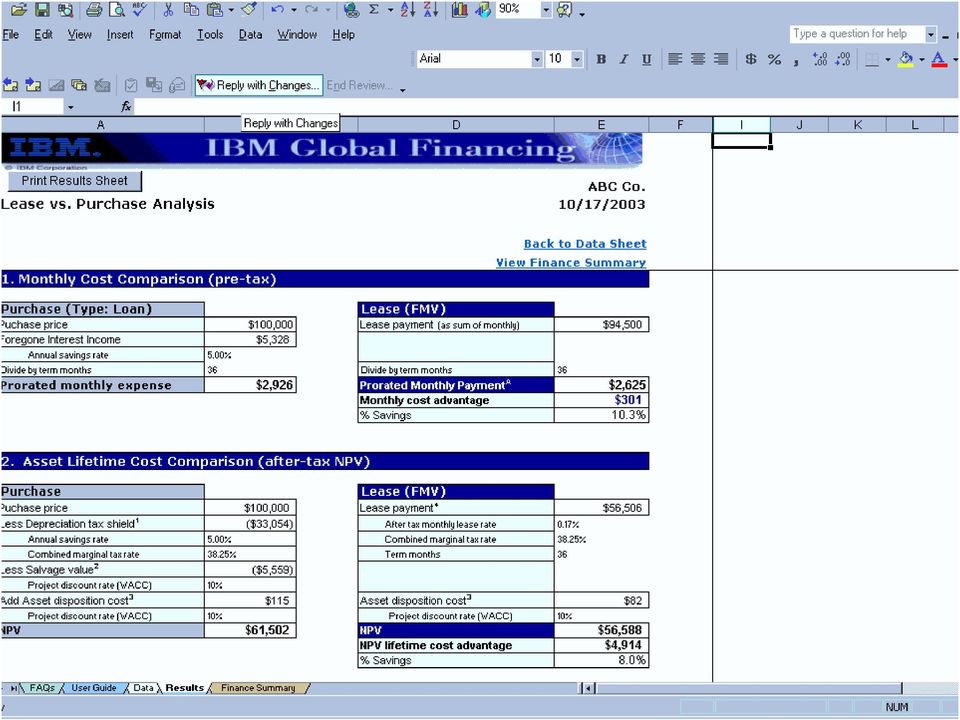

9 Lease vs purchase actual numbers Lease rate Purchase 36 month B lease P series $63K $55K(14.8% better) Assumptions Best credit 7% borrowing rate 5% salvage value This [lease/purchase analysis tool] is provided to you solely as a reference tool and neither International Business Machines Corporation (IBM) nor IBM Credit LLC (IBM Credit) is providing to you, or intends to provide or offer tax, accounting or legal advice. You are advised not to rely on this analysis. You are responsible for making your own analysis including: (i) accessing the adequacy and accuracy of the variables input to the model and (ii) determining whether the model contains all of the appropriate factors that may be relevant to your lease/purchase analysis. IBM and IBM Credit make no guarantee or representations with respect to the analysis, the analysis tool or the applicability of this analysis to your business or accounting methods. You should consult with your own financial advisors. Any tax or accounting treatment decisions made by you or on your behalf are solely your responsibility. 9

accessing the adequacy and accuracy of the variables input to the model and (ii) determining whether the model contains all of the")

10 10

11 11

12 12

13 13

14 Summary Fair Market Value leases are almost always better for the customer than purchase Lower economic cost Greater flexibility Less technology and financial risk 14

Manage Risk with Fixed Assets

Manage Risk with Fixed Assets Presented by: V. Lynn Lambert, CPA Lambert Lanoue & Smoker LLC www.lambertcpas.com Outline Analysis of Lease vs Purchase of Fixed Assets New IRS Repair Regulations Capital

Manage Risk with Fixed Assets Presented by: V. Lynn Lambert, CPA Lambert Lanoue & Smoker LLC www.lambertcpas.com Outline Analysis of Lease vs Purchase of Fixed Assets New IRS Repair Regulations Capital

Types of Leases. Lease Financing. FINC 3630 Yost

Lease Financing Types of Leases Operating Leases Financial Leases or Capital Leases Sale and Leaseback Arrangements Combination Leases Synthetic Leases Operating Leases Payments include maintenance and

Lease Financing Types of Leases Operating Leases Financial Leases or Capital Leases Sale and Leaseback Arrangements Combination Leases Synthetic Leases Operating Leases Payments include maintenance and

Types of Leases. Lease Financing

Lease Financing Types of leases Tax treatment of leases Effects on financial statements Lessee s analysis Lessor s analysis Other issues in lease analysis Who are the two parties to a lease transaction?

Lease Financing Types of leases Tax treatment of leases Effects on financial statements Lessee s analysis Lessor s analysis Other issues in lease analysis Who are the two parties to a lease transaction?

CHAPTER 7: NPV AND CAPITAL BUDGETING

CHAPTER 7: NPV AND CAPITAL BUDGETING I. Introduction Assigned problems are 3, 7, 34, 36, and 41. Read Appendix A. The key to analyzing a new project is to think incrementally. We calculate the incremental

CHAPTER 7: NPV AND CAPITAL BUDGETING I. Introduction Assigned problems are 3, 7, 34, 36, and 41. Read Appendix A. The key to analyzing a new project is to think incrementally. We calculate the incremental

Chapter 20 Lease Financing ANSWERS TO END-OF-CHAPTER QUESTIONS

Chapter 20 Lease Financing ANSWERS TO END-OF-CHAPTER QUESTIONS 20-1 a. The lessee is the party leasing the property. The party receiving the payments from the lease (that is, the owner of the property)

Chapter 20 Lease Financing ANSWERS TO END-OF-CHAPTER QUESTIONS 20-1 a. The lessee is the party leasing the property. The party receiving the payments from the lease (that is, the owner of the property)

By: Philip J. Clements and Cassie Glynn. October 2011

C TO S TAX CONVERSION By: Philip J. Clements and Cassie Glynn Fundamental Tax Planning Principles: October 2011 General Principles: When everything is done, you should find that income or gains are taxed

C TO S TAX CONVERSION By: Philip J. Clements and Cassie Glynn Fundamental Tax Planning Principles: October 2011 General Principles: When everything is done, you should find that income or gains are taxed

Basics of Lease Pricing

Basics of Lease Pricing 2014 ELFA Lease Accountants Conference Kathleen Walseth - U.S. Bank Equipment Finance Scott Thacker- Ivory Consulting Corporation 1 Disclaimer US Bankcorp and its affiliates and

Basics of Lease Pricing 2014 ELFA Lease Accountants Conference Kathleen Walseth - U.S. Bank Equipment Finance Scott Thacker- Ivory Consulting Corporation 1 Disclaimer US Bankcorp and its affiliates and

School Bus Financing for Municipalities

School Bus Financing for Municipalities 01 School Bus Financing for Municipalities Thomas Built Buses is committed to building buses that give you peace of mind day after day, mile after mile. And as the

School Bus Financing for Municipalities 01 School Bus Financing for Municipalities Thomas Built Buses is committed to building buses that give you peace of mind day after day, mile after mile. And as the

Power Purchase Agreement Financial Models in SAM 2013.1.15

Power Purchase Agreement Financial Models in SAM 2013.1.15 SAM Webinar Paul Gilman June 19, 2013 NREL is a national laboratory of the U.S. Department of Energy, Office of Energy Efficiency and Renewable

Power Purchase Agreement Financial Models in SAM 2013.1.15 SAM Webinar Paul Gilman June 19, 2013 NREL is a national laboratory of the U.S. Department of Energy, Office of Energy Efficiency and Renewable

The Insider s Guide to Leasing

The Insider s Guide to Leasing Table of Contents 1 The Power of Leasing 2 The 11 Advantages of Leasing 4 Cash Flow & Credit 6 Upgrading & Adding Equipment 7 Tax & Reporting Advantages 8 The Three Types

The Insider s Guide to Leasing Table of Contents 1 The Power of Leasing 2 The 11 Advantages of Leasing 4 Cash Flow & Credit 6 Upgrading & Adding Equipment 7 Tax & Reporting Advantages 8 The Three Types

THE LEASE VERSUS BUY DECISION

Over the past thirty years, U.S. Bancorp Equipment Finance has grown into one of the largest bank affiliated industrial finance companies in the nation. With total assets in excess of $8 Billion and offices

Over the past thirty years, U.S. Bancorp Equipment Finance has grown into one of the largest bank affiliated industrial finance companies in the nation. With total assets in excess of $8 Billion and offices

EMBA in Management & Finance. Corporate Finance. Eric Jondeau

EMBA in Management & Finance Corporate Finance EMBA in Management & Finance Lecture 5: Capital Budgeting For the Levered Firm Prospectus Recall that there are three questions in corporate finance. The

EMBA in Management & Finance Corporate Finance EMBA in Management & Finance Lecture 5: Capital Budgeting For the Levered Firm Prospectus Recall that there are three questions in corporate finance. The

Should I Lease or Buy?

No. 1339 Information Sheet August 2001 Should I Lease or Buy? Steven W. Martin, Fred Cooke, Jr., David Parvin, and Scott Stiles INTRODUCTION For many farms, machinery expense is the largest single production

No. 1339 Information Sheet August 2001 Should I Lease or Buy? Steven W. Martin, Fred Cooke, Jr., David Parvin, and Scott Stiles INTRODUCTION For many farms, machinery expense is the largest single production

Introduction to Tax Equity Structures Part II. Tom Stevens Bill Fisher Deloitte Tax LLP

Introduction to Tax Equity Structures Part II Tom Stevens Bill Fisher Deloitte Tax LLP September 29, 2014 Introduction to Tax Equity Structures Part I Summary of Qualifying Resources and Facilities Partnership

Introduction to Tax Equity Structures Part II Tom Stevens Bill Fisher Deloitte Tax LLP September 29, 2014 Introduction to Tax Equity Structures Part I Summary of Qualifying Resources and Facilities Partnership

Partnership Flip Structuring Tax Perspectives. Tom Stevens Deloitte Tax LLP

Partnership Flip Structuring Tax Perspectives Tom Stevens Deloitte Tax LLP September 30, 2014 Tax Incentives are Integral to Project Economics What if I can t monetize the incentives currently? 1-year

Partnership Flip Structuring Tax Perspectives Tom Stevens Deloitte Tax LLP September 30, 2014 Tax Incentives are Integral to Project Economics What if I can t monetize the incentives currently? 1-year

Below is more information regarding these tax benefits available to you between now and the end of 2012.

Acquiring new equipment between now and the end of 2012, you will be able to take advantage of the Section 179 and the Bonus 50% First Year depreciation deductions for 2012. In fact, Uncle Sam will be

Acquiring new equipment between now and the end of 2012, you will be able to take advantage of the Section 179 and the Bonus 50% First Year depreciation deductions for 2012. In fact, Uncle Sam will be

Understanding employer-granted stock options

Understanding employer-granted stock options Important information for option holders Employee stock options can be one of the most valuable benefits companies provide as part of a benefits package. However,

Understanding employer-granted stock options Important information for option holders Employee stock options can be one of the most valuable benefits companies provide as part of a benefits package. However,

Leasing and Factoring for SME Finance

Leasing and Factoring for SME Finance ADBI Seminar on SME Finance May 2006 Yasuo IZUMI 1 The v iews expressed in this paper are the v iews of the author and do not necessarily reflect the views or policies

Leasing and Factoring for SME Finance ADBI Seminar on SME Finance May 2006 Yasuo IZUMI 1 The v iews expressed in this paper are the v iews of the author and do not necessarily reflect the views or policies

MSUFCU Business Loan Application

MSUFCU Business Loan Application Section 1 - Credit Requested Total Funds Needed Less Funds Provided by You - ( ) Less Funds Provided by Others - ( ) Total Loan Needed Section 2 - Business Information

MSUFCU Business Loan Application Section 1 - Credit Requested Total Funds Needed Less Funds Provided by You - ( ) Less Funds Provided by Others - ( ) Total Loan Needed Section 2 - Business Information

Spin-Off of Time Warner Cable Inc. Tax Information Statement As of March 19, 2009

Spin-Off of Time Warner Cable Inc. Tax Information Statement As of March 19, 2009 On March 12, 2009, Time Warner Inc. ( Time Warner ) completed the spin-off (the Spin-Off ) of Time Warner s ownership interest

Spin-Off of Time Warner Cable Inc. Tax Information Statement As of March 19, 2009 On March 12, 2009, Time Warner Inc. ( Time Warner ) completed the spin-off (the Spin-Off ) of Time Warner s ownership interest

Leasing vs. Purchasing

How to overcome customers most common objections to financing Leasing vs. Purchasing Help your customers see the value of leasing their IT acquisitions The Equipment Leasing Association of America says

How to overcome customers most common objections to financing Leasing vs. Purchasing Help your customers see the value of leasing their IT acquisitions The Equipment Leasing Association of America says

How To Compare The Pros And Cons Of A Combine To A Lease Or Buy

Leasing vs. Buying Farm Machinery Department of Agricultural Economics MF-2953 www.agmanager.info Machinery and equipment expense typically represents a major cost in agricultural production. Purchasing

Leasing vs. Buying Farm Machinery Department of Agricultural Economics MF-2953 www.agmanager.info Machinery and equipment expense typically represents a major cost in agricultural production. Purchasing

A guide for managing your IRA inheritance. Maximize your inherited IRA and enhance your financial security.

A guide for managing your IRA inheritance Maximize your inherited IRA and enhance your financial security. Make the most of your inheritance by taking advantage of continued tax-deferred growth potential.

A guide for managing your IRA inheritance Maximize your inherited IRA and enhance your financial security. Make the most of your inheritance by taking advantage of continued tax-deferred growth potential.

Commercial Real Estate Investment: Opportunities for Income Generation in Today s Environment

Commercial Real Estate Investment: Opportunities for Income Generation in Today s Environment Prepared by Keith H. Reep, CCIM Real Estate Investment Consultant In this white paper 1 Advantages of investing

Commercial Real Estate Investment: Opportunities for Income Generation in Today s Environment Prepared by Keith H. Reep, CCIM Real Estate Investment Consultant In this white paper 1 Advantages of investing

Module 2: Preparing for Capital Venture Financing Financial Forecasting Methods TABLE OF CONTENTS

Module 2: Preparing for Capital Venture Financing Financial Forecasting Methods Module 2: Preparing for Capital Venture Financing Financial Forecasting Methods 1.0 FINANCIAL FORECASTING METHODS 1.01 Introduction

Module 2: Preparing for Capital Venture Financing Financial Forecasting Methods Module 2: Preparing for Capital Venture Financing Financial Forecasting Methods 1.0 FINANCIAL FORECASTING METHODS 1.01 Introduction

Equipment Leasing Terms

Equipment Leasing Terms This Glossary of Equipment Leasing Terms will help you understand the "Leasing Language" so when you are ready to acquire equipment you can make an educated decision. Accelerated

Equipment Leasing Terms This Glossary of Equipment Leasing Terms will help you understand the "Leasing Language" so when you are ready to acquire equipment you can make an educated decision. Accelerated

NORTH CENTRAL FARM MANAGEMENT EXTENSION COMMITTEE

NCFMEC-05 NORTH CENTRAL FARM MANAGEMENT EXTENSION COMMITTEE Purchasing and Leasing Farm Equipment Acknowledgements This publication is a product of the North Central Regional (NCR) Cooperative Extension

NCFMEC-05 NORTH CENTRAL FARM MANAGEMENT EXTENSION COMMITTEE Purchasing and Leasing Farm Equipment Acknowledgements This publication is a product of the North Central Regional (NCR) Cooperative Extension

Student Learning Outcomes

Chapter 15 Leases Part 2: Capital Leases Intermediate Accounting II Dr. Chula King Student Learning Outcomes Explain and use the criteria for determining whether a lease is capital or not Describe and

Chapter 15 Leases Part 2: Capital Leases Intermediate Accounting II Dr. Chula King Student Learning Outcomes Explain and use the criteria for determining whether a lease is capital or not Describe and

Agriculture & Business Management Notes...

Agriculture & Business Management Notes... Farm Machinery & Equipment -- Buy, Lease or Custom Hire Quick Notes... Selecting the best method to acquire machinery services presents a complex economic problem.

Agriculture & Business Management Notes... Farm Machinery & Equipment -- Buy, Lease or Custom Hire Quick Notes... Selecting the best method to acquire machinery services presents a complex economic problem.

Canadian Tire: Value Under the Hood

Canadian Tire: Value Under the Hood May 2006 Pershing Square Capital Management, L.P. Disclaimer Pershing Square Capital Management's ("Pershing") analysis and conclusions regarding Canadian Tire Corporation

Canadian Tire: Value Under the Hood May 2006 Pershing Square Capital Management, L.P. Disclaimer Pershing Square Capital Management's ("Pershing") analysis and conclusions regarding Canadian Tire Corporation

Financing for Municipalities

Financing for Municipalities 01 Financing for Municipalities At Daimler Truck Financial, every customer is important. We ve been doing business that way since day one, which is why we have been a leader

Financing for Municipalities 01 Financing for Municipalities At Daimler Truck Financial, every customer is important. We ve been doing business that way since day one, which is why we have been a leader

Chapter 18. Web Extension: Percentage Cost Analysis, Leasing Feedback, and Leveraged Leases

Chapter 18 Web Extension: Percentage Cost Analysis, Leasing Feedback, and Leveraged Leases Percentage Cost Analysis Anderson s lease-versus-purchase decision from Chapter 18 could also be analyzed using

Chapter 18 Web Extension: Percentage Cost Analysis, Leasing Feedback, and Leveraged Leases Percentage Cost Analysis Anderson s lease-versus-purchase decision from Chapter 18 could also be analyzed using

TAX EQUITY INVESTMENTS OVERVIEW Frequently Asked Questions

2016 TAX EQUITY INVESTMENTS OVERVIEW Frequently Asked Questions prepared by Distributed Sun & DLA Piper LLP (US) February 25, 2016 Page 0 of 8 Table of Contents Disclaimer... 2 What are the tax-based incentives

2016 TAX EQUITY INVESTMENTS OVERVIEW Frequently Asked Questions prepared by Distributed Sun & DLA Piper LLP (US) February 25, 2016 Page 0 of 8 Table of Contents Disclaimer... 2 What are the tax-based incentives

1. General Obligation Bonds (G.O.s): Bonds backed by the full taxing power of the issuer.

: Bonds backed by the full taxing power of the issuer.") S&P INDICES Fixed Income February 2010 S&P Fixed Income Indices: Municipal Bond Investor Tool Kit Key Terms Alternative Minimum Tax (AMT): An extra tax that some taxpayers are required to pay in addition

S&P INDICES Fixed Income February 2010 S&P Fixed Income Indices: Municipal Bond Investor Tool Kit Key Terms Alternative Minimum Tax (AMT): An extra tax that some taxpayers are required to pay in addition

A. To strategically utilize debt to fund mission critical projects;

Policy concerning: page 1 of 5 DEBT POLICY I. GOALS AND OBJECTIVES Teaching and learning form the core of Westfield State University s institutional mission. The university s strategic plan identifies

Policy concerning: page 1 of 5 DEBT POLICY I. GOALS AND OBJECTIVES Teaching and learning form the core of Westfield State University s institutional mission. The university s strategic plan identifies

Instructions for E-PLAN Financial Planning Template

Instructions for E-PLAN Financial Planning Template The EPLAN template will assist you in preparing financial projections for your existing business. The template uses Microsoft Excel to prepare your projected

Instructions for E-PLAN Financial Planning Template The EPLAN template will assist you in preparing financial projections for your existing business. The template uses Microsoft Excel to prepare your projected

University System of Maryland Accounting Practice

University System of Maryland Accounting Practice Preparation of interim financial statements General This accounting practice document is a current guide for preparing internal-use, interim financial

University System of Maryland Accounting Practice Preparation of interim financial statements General This accounting practice document is a current guide for preparing internal-use, interim financial

This material is derived from sources believed to be reliable, but its accuracy and the opinions based thereon are not guaranteed.

Using Debt Wisely INVESTMENT AND INSURANCE PRODUCTS: NOT FDIC INSURED NOT A BANK DEPOSIT NOT INSURED BY ANY FEDERAL GOVERNMENT AGENCY NO BANK GUARANTEE MAY LOSE VALUE Disclosures The information provided

Using Debt Wisely INVESTMENT AND INSURANCE PRODUCTS: NOT FDIC INSURED NOT A BANK DEPOSIT NOT INSURED BY ANY FEDERAL GOVERNMENT AGENCY NO BANK GUARANTEE MAY LOSE VALUE Disclosures The information provided

Insight into Deferred Taxes. How Do Deferred Taxes Arise?

Insight into Deferred Taxes How Do Deferred Taxes Arise? Differences exist between the accounting books and the tax books because of temporary differences» Depreciation» Inventory» Restructuring charges»

Insight into Deferred Taxes How Do Deferred Taxes Arise? Differences exist between the accounting books and the tax books because of temporary differences» Depreciation» Inventory» Restructuring charges»

CONSIDERATIONS IN BUYING AND SELLING A BUSINESS

CONSIDERATIONS IN BUYING AND SELLING A BUSINESS David H. Pettit, Esq. Feil, Pettit & Williams, PLC Charlottesville, VA I. Ownership A. Are the owners of sound mind and in agreement? B. Can the transaction

CONSIDERATIONS IN BUYING AND SELLING A BUSINESS David H. Pettit, Esq. Feil, Pettit & Williams, PLC Charlottesville, VA I. Ownership A. Are the owners of sound mind and in agreement? B. Can the transaction

A Business Loan Insurance Plan

A Business Loan Insurance Plan Are you personally responsible for business loans? Table of Contents Page Do You Have to Sign Twice for Your Business Loans? 2 A Potential Solution Using Life Insurance 3

A Business Loan Insurance Plan Are you personally responsible for business loans? Table of Contents Page Do You Have to Sign Twice for Your Business Loans? 2 A Potential Solution Using Life Insurance 3

Proposed Lease Accounting Changes: Impact on Asset Finance Deals

Proposed Lease Accounting Changes: Impact on Asset Finance Deals In August 2010, the International Accounting Standards Board ( IASB ) issued a proposal which, if adopted, will overhaul lease accounting

Proposed Lease Accounting Changes: Impact on Asset Finance Deals In August 2010, the International Accounting Standards Board ( IASB ) issued a proposal which, if adopted, will overhaul lease accounting

BA 351 CORPORATE FINANCE. John R. Graham Adapted from S. Viswanathan LECTURE 5 LEASING FUQUA SCHOOL OF BUSINESS DUKE UNIVERSITY

BA 351 CORPORATE FINANCE John R. Graham Adapted from S. Viswanathan LECTURE 5 LEASING FUQUA SCHOOL OF BUSINESS DUKE UNIVERSITY 1 Leasing has long been an important alternative to buying an asset. In this

BA 351 CORPORATE FINANCE John R. Graham Adapted from S. Viswanathan LECTURE 5 LEASING FUQUA SCHOOL OF BUSINESS DUKE UNIVERSITY 1 Leasing has long been an important alternative to buying an asset. In this

This policy sets forth system-wide standards for financial accounting and reporting of leases.

Accounting for Leases Section: Accounting and Financial Reporting Title: Accounting for Leases Number: 05.281 Index POLICY.100 POLICY STATEMENT.110 POLICY RATIONALE.120 AUTHORITY.130 APPROVAL AND EFFECTIVE

Accounting for Leases Section: Accounting and Financial Reporting Title: Accounting for Leases Number: 05.281 Index POLICY.100 POLICY STATEMENT.110 POLICY RATIONALE.120 AUTHORITY.130 APPROVAL AND EFFECTIVE

UNIVERSITY OF CINCINNATI DEPARTMENTAL MASTER LEASE FINANCING APPLICATION

DEPARTMENT DESCRIPTION OF EQUIPMENT TO BE FINANCED UNIVERSITY OF CINCINNATI DEPARTMENTAL MASTER LEASE FINANCING APPLICATION Minimum purchase amount to be financed under master lease is $50,000. Repayment

DEPARTMENT DESCRIPTION OF EQUIPMENT TO BE FINANCED UNIVERSITY OF CINCINNATI DEPARTMENTAL MASTER LEASE FINANCING APPLICATION Minimum purchase amount to be financed under master lease is $50,000. Repayment

Company Share Price Valuation using Free Cash Flow To Equity

Financial Modeling Templates Company Share Price Valuation using Free Cash Flow To Equity http://spreadsheetml.com/finance/valuation_freecashflowtoequity.shtml Copyright (c) 2009-2014, ConnectCode All

Financial Modeling Templates Company Share Price Valuation using Free Cash Flow To Equity http://spreadsheetml.com/finance/valuation_freecashflowtoequity.shtml Copyright (c) 2009-2014, ConnectCode All

FORACO INTERNATIONAL REPORTS Q3 2014

NEWS RELEASE FORACO INTERNATIONAL REPORTS Q3 2014 Toronto, Ontario / Marseille, France Tuesday, November 4, 2014 Foraco International SA (TSX:FAR) (the Company or Foraco ), a leading global provider of

NEWS RELEASE FORACO INTERNATIONAL REPORTS Q3 2014 Toronto, Ontario / Marseille, France Tuesday, November 4, 2014 Foraco International SA (TSX:FAR) (the Company or Foraco ), a leading global provider of

EVERYTHING YOU ALWAYS WANTED TO KNOW ABOUT 1031 EXCHANGE (BUT DIDN T KNOW YOU SHOULD ASK )

") EVERYTHING YOU ALWAYS WANTED TO KNOW ABOUT 1031 EXCHANGE (BUT DIDN T KNOW YOU SHOULD ASK ) Nancy N Grekin McCorriston Miller Mukai MacKinnon 5 Waterfront Plaza, 4 th Floor Honolulu, Hawaii 96813 529-7419

EVERYTHING YOU ALWAYS WANTED TO KNOW ABOUT 1031 EXCHANGE (BUT DIDN T KNOW YOU SHOULD ASK ) Nancy N Grekin McCorriston Miller Mukai MacKinnon 5 Waterfront Plaza, 4 th Floor Honolulu, Hawaii 96813 529-7419

Equipment Procurement To lease or to own?

Equipment Procurement To lease or to own? 2 nd TEFMA Grounds Workshop Massey University - October 2009 Common questions How do I work out which financing option is the cheapest? What are the tax implications?

Equipment Procurement To lease or to own? 2 nd TEFMA Grounds Workshop Massey University - October 2009 Common questions How do I work out which financing option is the cheapest? What are the tax implications?

Example Accounts Only

CaseWare Sole Trader Financial Statements NOTE: These financial statements include illustrative disclosures for a Sole Trader (Special Purpose). The information is not intended to be and is not comprehensive

CaseWare Sole Trader Financial Statements NOTE: These financial statements include illustrative disclosures for a Sole Trader (Special Purpose). The information is not intended to be and is not comprehensive

CHAPTER 25. P.25.16 The following data are furnished by the Hypothetical Leasing Ltd (HLL):

:") CHAPTER 25 Solved Problems P.25.16 The following data are furnished by the Hypothetical Leasing Ltd (HLL): Investment cost Rs 500 lakh Primary lease term 5 years Estimated residual value after the primary

CHAPTER 25 Solved Problems P.25.16 The following data are furnished by the Hypothetical Leasing Ltd (HLL): Investment cost Rs 500 lakh Primary lease term 5 years Estimated residual value after the primary

Key Person Life Insurance

Key Person Life Insurance The Concept Key person life insurance helps reimburse a business for economic loss when a key employee dies. The insurance covers the life of an employee who is critical to the

Key Person Life Insurance The Concept Key person life insurance helps reimburse a business for economic loss when a key employee dies. The insurance covers the life of an employee who is critical to the

Understanding Financial Statements. For Your Business

Understanding Financial Statements For Your Business Disclaimer The information provided is for informational purposes only, does not constitute legal advice or create an attorney-client relationship,

Understanding Financial Statements For Your Business Disclaimer The information provided is for informational purposes only, does not constitute legal advice or create an attorney-client relationship,

2014 FIRST QUARTER RESULTS CONFERENCE CALL. May 15th, 2014

2014 FIRST QUARTER RESULTS CONFERENCE CALL May 15th, 2014 DISCLAIMER This presentation has been prepared by Eurotech S.p.A.(or Eurotech ) and has to be read in conjunction with its oral presentation. The

2014 FIRST QUARTER RESULTS CONFERENCE CALL May 15th, 2014 DISCLAIMER This presentation has been prepared by Eurotech S.p.A.(or Eurotech ) and has to be read in conjunction with its oral presentation. The

INCOME STATEMENT. BALANCE SHEET (Beginning) WHAT'S MY CASH FLOW? Cash Flow Statements. For the 12 Months Ending 12/31/2005.

WHAT'S MY CASH FLOW? Cash Flow Statements. For the 12 Months Ending 12/31/2005.") Cash Flow Statements INCOME STATEMENT Revenue $ 800,000 Operating Expenses $ 770,000 Depreciation expense $ 20,000 Total expenses $ 790,000 Net Income $ 10,000 Explanation: Using the Income Statement,

Cash Flow Statements INCOME STATEMENT Revenue $ 800,000 Operating Expenses $ 770,000 Depreciation expense $ 20,000 Total expenses $ 790,000 Net Income $ 10,000 Explanation: Using the Income Statement,

Adapted, with permission, from The Canadian Institute of Chartered Accountants, Toronto, Canada, October, 1998.

Introduction to LEASING Adapted, with permission, from The Canadian Institute of Chartered Accountants, Toronto, Canada, October, 1998. COMMON LEASING TERMS The following list comprises some standard definitions

Introduction to LEASING Adapted, with permission, from The Canadian Institute of Chartered Accountants, Toronto, Canada, October, 1998. COMMON LEASING TERMS The following list comprises some standard definitions

SUMMARY PROSPECTUS. BlackRock Liquidity Funds Select Shares California Money Fund Select: BCBXX FEBRUARY 29, 2016

FEBRUARY 29, 2016 SUMMARY PROSPECTUS BlackRock Liquidity Funds Select Shares California Money Fund Select: BCBXX Before you invest, you may want to review the Fund s prospectus, which contains more information

FEBRUARY 29, 2016 SUMMARY PROSPECTUS BlackRock Liquidity Funds Select Shares California Money Fund Select: BCBXX Before you invest, you may want to review the Fund s prospectus, which contains more information

Topic 3: Accounts and finance

Topic 3: Accounts and finance 3.1 Sources of Finance LO1: Evaluate advantages & disadvantages of each form of finance. LO2: Evaluate appropriateness of source of finance for given situation. Short, Medium,

Topic 3: Accounts and finance 3.1 Sources of Finance LO1: Evaluate advantages & disadvantages of each form of finance. LO2: Evaluate appropriateness of source of finance for given situation. Short, Medium,

2015 FIRST HALF RESULTS CONFERENCE CALL. August 31st, 2015

2015 FIRST HALF RESULTS CONFERENCE CALL August 31st, 2015 DISCLAIMER This presentation has been prepared by Eurotech S.p.A.(or Eurotech ) and has to be read in conjunction with its oral presentation. The

2015 FIRST HALF RESULTS CONFERENCE CALL August 31st, 2015 DISCLAIMER This presentation has been prepared by Eurotech S.p.A.(or Eurotech ) and has to be read in conjunction with its oral presentation. The

Basics of Tax Leasing (1)

") Basics of Tax Leasing (1) 2007 ELFA Lease Accountants Conference Suresh Makam 914-899-7912 Citi Bankers Leasing Single Investor Lease Lessor purchases the equipment with equity or proceeds of recourse

Basics of Tax Leasing (1) 2007 ELFA Lease Accountants Conference Suresh Makam 914-899-7912 Citi Bankers Leasing Single Investor Lease Lessor purchases the equipment with equity or proceeds of recourse

Lease vs. Buy. Lease. Benefits of Leasing Various types to meet your needs. Optimize cash flow. No loan. Maintain credit.

www.stma.org Lease vs. Buy Deciding if you are going to lease or buy equipment depends on your situation. In general, leasing is more appropriate for businesses with limited capital or need equipment upgrades

www.stma.org Lease vs. Buy Deciding if you are going to lease or buy equipment depends on your situation. In general, leasing is more appropriate for businesses with limited capital or need equipment upgrades

AAA PUBLIC ADJUSTING GROUP, INC. (EXACT NAME OF REGISTRANT AS SPECIFIED IN ITS CHARTER)

") UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C. 20549 FORM 10-Q [ X] QUARTERLY REPORT PURSUANT TO SECTION 13 OF 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the quarterly period ended

UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C. 20549 FORM 10-Q [ X] QUARTERLY REPORT PURSUANT TO SECTION 13 OF 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the quarterly period ended

Comparison of IRA Limits

Comparison of IRA Limits REPORT Prepared for: Sam Sample 3/29/2011 Prepared by: Benjamin Edwards Financial Consultant CONTENTS Overview...3 Quick Comparison of Traditional. and Roth IRAs...5 Personal.

Comparison of IRA Limits REPORT Prepared for: Sam Sample 3/29/2011 Prepared by: Benjamin Edwards Financial Consultant CONTENTS Overview...3 Quick Comparison of Traditional. and Roth IRAs...5 Personal.

In connection with your investment at Lending Club, you may receive a Consolidated 1099 Package for 2015 containing certain tax forms.

Introduction In connection with your investment at Lending Club, you may receive a Consolidated 1099 Package for 2015 containing certain tax forms. This Tax Guide is designed to provide general information

Introduction In connection with your investment at Lending Club, you may receive a Consolidated 1099 Package for 2015 containing certain tax forms. This Tax Guide is designed to provide general information

The IBM 401(k) Plus Plan. Invest today for what you hope to accomplish tomorrow

Plus Plan. Invest today for what you hope to accomplish tomorrow") The IBM 401(k) Plus Plan Invest today for what you hope to accomplish tomorrow The IBM 401(k) Plus Plan Dollar-for-dollar company match, automatic company contributions, broad range of investment options

The IBM 401(k) Plus Plan Invest today for what you hope to accomplish tomorrow The IBM 401(k) Plus Plan Dollar-for-dollar company match, automatic company contributions, broad range of investment options

Accounting and Finance for Managers and Entrepreneurs

Accounting and Finance for Managers and Entrepreneurs Course Description This course covers what everything business people and managers need to know about accounting and finance. It is directed toward

Accounting and Finance for Managers and Entrepreneurs Course Description This course covers what everything business people and managers need to know about accounting and finance. It is directed toward

You can select the equipment by working with a vendor or a manufacturer, which offers leasing.

Why Should I Lease Equipment? As businesses prepare to compete and grow in a new millennium, many are searching for proven new ways to address their equipment financing challenge. The old ways won't meet

Why Should I Lease Equipment? As businesses prepare to compete and grow in a new millennium, many are searching for proven new ways to address their equipment financing challenge. The old ways won't meet

SBERBANK GROUP S IFRS RESULTS. March 2015

SBERBANK GROUP S IFRS RESULTS 2014 March 2015 SUMMARY OF PERFORMANCE FOR 2014 STATEMENT OF PROFIT OR LOSS Net profit reached RUB 290.3bn (or RUB 13.45 per ordinary share), compared to RUB 362.0bn (or RUB

SBERBANK GROUP S IFRS RESULTS 2014 March 2015 SUMMARY OF PERFORMANCE FOR 2014 STATEMENT OF PROFIT OR LOSS Net profit reached RUB 290.3bn (or RUB 13.45 per ordinary share), compared to RUB 362.0bn (or RUB

A Sole Proprietor Insured Buy-Sell Plan

A Sole Proprietor Insured Buy-Sell Plan At a sole proprietor s death, the business is dissolved and all business assets and liabilities become part of the sole proprietor's personal estate. Have you evaluated

A Sole Proprietor Insured Buy-Sell Plan At a sole proprietor s death, the business is dissolved and all business assets and liabilities become part of the sole proprietor's personal estate. Have you evaluated

Homeownership Preservation Policy for Residential Mortgage Assets. Section 110 of the Emergency Economic Stabilization Act (EESA)

") Homeownership Preservation Policy for Residential Mortgage Assets Section 110 of the Emergency Economic Stabilization Act (EESA) requires that each Federal property manager that holds, owns, or controls

Homeownership Preservation Policy for Residential Mortgage Assets Section 110 of the Emergency Economic Stabilization Act (EESA) requires that each Federal property manager that holds, owns, or controls

Study on Financing Growth Capital for SMEs

Study on Financing Growth Capital for SMEs Remarks by Marion G. Wrobel Vice-President, Policy and Operations Canadian Bankers Association for The Standing Senate Committee on Banking Trade and Commerce

Study on Financing Growth Capital for SMEs Remarks by Marion G. Wrobel Vice-President, Policy and Operations Canadian Bankers Association for The Standing Senate Committee on Banking Trade and Commerce

Financial Management. An Introduction

Financial Management An Introduction FINANCE Finance is the life-blood of business. Without finance neither any business can be started nor successfully run. Finance is needed to promote or establish business,

Financial Management An Introduction FINANCE Finance is the life-blood of business. Without finance neither any business can be started nor successfully run. Finance is needed to promote or establish business,

Class / Ticker Symbol Fund Name Class A Class C Class C1 Class I

Mutual Funds Prospectus August 31, 2011 Nuveen Municipal Bond Funds Dependable, tax-free income because it s not what you earn, it s what you keep. Class / Ticker Symbol Fund Name Class A Class C Class

Mutual Funds Prospectus August 31, 2011 Nuveen Municipal Bond Funds Dependable, tax-free income because it s not what you earn, it s what you keep. Class / Ticker Symbol Fund Name Class A Class C Class

INDIVIDUAL RETIREMENT CUSTODIAL ACCOUNT ADOPTION AGREEMENT

INDIVIDUAL RETIREMENT CUSTODIAL ACCOUNT ADOPTION AGREEMENT Please complete this application to establish a new Traditional IRA or Roth IRA. This application must be preceded or accompanied by a current

INDIVIDUAL RETIREMENT CUSTODIAL ACCOUNT ADOPTION AGREEMENT Please complete this application to establish a new Traditional IRA or Roth IRA. This application must be preceded or accompanied by a current

Partnership Flip Structure

Accounting for Investments in Alternative Energy Projects Maria Davis Deloitte & Touche LLP Partnership Flip Structure Developer Tax Equity Investor Cash distributions Period 1: 100% Period 2: 0% Period

Accounting for Investments in Alternative Energy Projects Maria Davis Deloitte & Touche LLP Partnership Flip Structure Developer Tax Equity Investor Cash distributions Period 1: 100% Period 2: 0% Period

CHAPTER 4. FINANCIAL STATEMENTS

CHAPTER 4. FINANCIAL STATEMENTS Accounting standards require statements that show the financial position, earnings, cash flows, and investment (distribution) by (to) owners. These measurements are reported,

CHAPTER 4. FINANCIAL STATEMENTS Accounting standards require statements that show the financial position, earnings, cash flows, and investment (distribution) by (to) owners. These measurements are reported,

13:11. Statement of Cash Flows. Chapter. Illustration. Statement of Cash Flows- summary. Overview

Overview Statement of Cash Flows Chapter 23 BECAUSE of the SCF, users of the financial statements get the best of both worlds! SCF bridges the gap created by paper income resulting from applying an accrual

Overview Statement of Cash Flows Chapter 23 BECAUSE of the SCF, users of the financial statements get the best of both worlds! SCF bridges the gap created by paper income resulting from applying an accrual

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 SCHEDULE 13D. Under the Securities Exchange Act of 1934. LRR Energy, L.P.

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 SCHEDULE 13D Under the Securities Exchange Act of 1934 LRR Energy, L.P. (Name of Issuer) Common Units Representing Limited Partner

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 SCHEDULE 13D Under the Securities Exchange Act of 1934 LRR Energy, L.P. (Name of Issuer) Common Units Representing Limited Partner

Accounting For Your Future INCORPORATION OF PROFESSIONALS IN ONTARIO. Details of the Legislation (Ontario Business Corporations Act)

") Accounting For Your Future INCORPORATION OF PROFESSIONALS IN ONTARIO Author: Hugh Faloon, CA, CFP, TEP, Tax Partner Status of Particular Professional Bodies The following professions have been allowed

Accounting For Your Future INCORPORATION OF PROFESSIONALS IN ONTARIO Author: Hugh Faloon, CA, CFP, TEP, Tax Partner Status of Particular Professional Bodies The following professions have been allowed

The mechanics of foreclosure are specific to the laws of the State in

Unraveling the Mystery of Cancellation of Indebtedness Income What Borrowers Need to Know of the Potential Tax Costs of Loan Workouts and Foreclosures by Edward J. Hannon, Partner, Corporate and Real Estate

Unraveling the Mystery of Cancellation of Indebtedness Income What Borrowers Need to Know of the Potential Tax Costs of Loan Workouts and Foreclosures by Edward J. Hannon, Partner, Corporate and Real Estate

Financing for Vocational Trucks

Financing for Vocational Trucks At Daimler Truck Financial, every customer is important. We ve been doing business that way since day one, which is why we have been a leader in the industry for close to

Financing for Vocational Trucks At Daimler Truck Financial, every customer is important. We ve been doing business that way since day one, which is why we have been a leader in the industry for close to

Consolidated Financial Results for Six Months Ended September 30, 2007

Consolidated Financial Results for Six Months Ended September 30, 2007 SOHGO SECURITY SERVICES CO., LTD (URL http://ir.alsok.co.jp/english) (Code No.:2331, TSE 1 st Sec.) Representative: Atsushi Murai,

Consolidated Financial Results for Six Months Ended September 30, 2007 SOHGO SECURITY SERVICES CO., LTD (URL http://ir.alsok.co.jp/english) (Code No.:2331, TSE 1 st Sec.) Representative: Atsushi Murai,

Action plan to prepare for the New Lease Accounting Standard

IBM Software Thought Leadership White Paper July 2011 Action plan to prepare for the New Lease Accounting Standard William Bosco, President, Leasing 101 Contents 2 Timing of the project 2 What is the project?

IBM Software Thought Leadership White Paper July 2011 Action plan to prepare for the New Lease Accounting Standard William Bosco, President, Leasing 101 Contents 2 Timing of the project 2 What is the project?

Non-Recourse Financing for a Self-Directed IRA Investment

Non-Recourse Financing for a Self-Directed IRA Investment Transaction Summary Date: September 2012 Property Description: 12,720 SF retail building built in 2001 in good condition. The property is 100%

Non-Recourse Financing for a Self-Directed IRA Investment Transaction Summary Date: September 2012 Property Description: 12,720 SF retail building built in 2001 in good condition. The property is 100%

Dealing with Operating Leases in Valuation. Aswath Damodaran. Stern School of Business. 44 West Fourth Street. New York, NY 10012

Dealing with Operating Leases in Valuation Aswath Damodaran Stern School of Business 44 West Fourth Street New York, NY 10012 adamodar@stern.nyu.edu Abstract Most firm valuation models start with the after-tax

Dealing with Operating Leases in Valuation Aswath Damodaran Stern School of Business 44 West Fourth Street New York, NY 10012 adamodar@stern.nyu.edu Abstract Most firm valuation models start with the after-tax

The IBM 401(k) Plus Plan. Invest today for what you hope to accomplish tomorrow

Plus Plan. Invest today for what you hope to accomplish tomorrow") The IBM 401(k) Plus Plan Invest today for what you hope to accomplish tomorrow The IBM 401(k) Plus Plan Dollar-for-dollar company match, automatic company contributions, broad range of investment options

The IBM 401(k) Plus Plan Invest today for what you hope to accomplish tomorrow The IBM 401(k) Plus Plan Dollar-for-dollar company match, automatic company contributions, broad range of investment options

Financing for Fleets

Financing for Fleets 01 Financing for Fleets At Daimler Truck Financial, every customer is important. We ve been doing business that way since day one, which is why we have been a leader in the industry

Financing for Fleets 01 Financing for Fleets At Daimler Truck Financial, every customer is important. We ve been doing business that way since day one, which is why we have been a leader in the industry

International Financial Reporting Standards (IFRS)

") FACT SHEET September 2011 IAS 7 Statement of Cash Flows (This fact sheet is based on the standard as at 1 January 2010.) Important note: This fact sheet is based on the requirements of the International

FACT SHEET September 2011 IAS 7 Statement of Cash Flows (This fact sheet is based on the standard as at 1 January 2010.) Important note: This fact sheet is based on the requirements of the International

Module 10 S Corporation/Corporation Study Guide Introduction

Module 10 Study Guide Introduction Running your own business presents many challenges. One of the most difficult is complying with complex and ever-changing tax laws. This small-business tax education

Module 10 Study Guide Introduction Running your own business presents many challenges. One of the most difficult is complying with complex and ever-changing tax laws. This small-business tax education

Permanent Benefit Group Life Insurance Under Code Section 79

Permanent Benefit Group Life Insurance Under Code Section 79 Expanding the Benefits of Group Life Insurance Advantages of Permanent Benefit Group Life Insurance. Giving employees the option to use cash

Permanent Benefit Group Life Insurance Under Code Section 79 Expanding the Benefits of Group Life Insurance Advantages of Permanent Benefit Group Life Insurance. Giving employees the option to use cash

Distribution of AbbVie Inc. Common Stock. Abbott Laboratories Shareholder Tax Basis Information

Distribution of AbbVie Inc. Common Stock Abbott Laboratories Shareholder Tax Basis Information If you did not receive the Distribution (as defined below) of AbbVie Inc. ("AbbVie") common stock on January

Distribution of AbbVie Inc. Common Stock Abbott Laboratories Shareholder Tax Basis Information If you did not receive the Distribution (as defined below) of AbbVie Inc. ("AbbVie") common stock on January

Chapter 1 The Scope of Corporate Finance

Chapter 1 The Scope of Corporate Finance MULTIPLE CHOICE 1. One of the tasks for financial managers when identifying projects that increase firm value is to identify those projects where a. marginal benefits

Chapter 1 The Scope of Corporate Finance MULTIPLE CHOICE 1. One of the tasks for financial managers when identifying projects that increase firm value is to identify those projects where a. marginal benefits

Life Insurance As An Asset Class Consumer Presentation

Life Insurance As An Asset Class Consumer Presentation Brought to you by: Pinney Insurance Center, Inc. 2266 Lava Ridge Court Roseville, CA 95661 www.pinneyinsurance.com Life Insurance As An Asset Class

Life Insurance As An Asset Class Consumer Presentation Brought to you by: Pinney Insurance Center, Inc. 2266 Lava Ridge Court Roseville, CA 95661 www.pinneyinsurance.com Life Insurance As An Asset Class

DTS CORPORATION and Consolidated Subsidiaries. Unaudited Quarterly Consolidated Financial Statements for the Three Months Ended June 30, 2008

DTS CORPORATION and Consolidated Subsidiaries Unaudited Quarterly Consolidated Financial Statements for the Three Months Ended June 30, 2008 DTS CORPORATION and Consolidated Subsidiaries Quarterly Consolidated

DTS CORPORATION and Consolidated Subsidiaries Unaudited Quarterly Consolidated Financial Statements for the Three Months Ended June 30, 2008 DTS CORPORATION and Consolidated Subsidiaries Quarterly Consolidated

Vice President, CJA and Associates Over 25 years experience in the insurance industry Extensive knowledge of employee benefit planning, especially

Vice President, CJA and Associates Over 25 years experience in the insurance industry Extensive knowledge of employee benefit planning, especially advanced planning techniques for small businesses Broad

Vice President, CJA and Associates Over 25 years experience in the insurance industry Extensive knowledge of employee benefit planning, especially advanced planning techniques for small businesses Broad

Review Notes Linked to the Lesser Performing of the S&P 500 Index and the Russell 2000 Index due September 23, 2019

Registration Statement No. 333-199966; Rule 433 August 27, 2015 JPMorgan Chase & Co. Structured Investments Review Notes Linked to the Lesser Performing of the S&P 500 Index and due September 23, 2019

Registration Statement No. 333-199966; Rule 433 August 27, 2015 JPMorgan Chase & Co. Structured Investments Review Notes Linked to the Lesser Performing of the S&P 500 Index and due September 23, 2019

An Insured Disability Salary Continuation Plan

An Insured Disability Salary Continuation Plan What would the financial impact on your business be if an owner or key employee became disabled? Table of Contents Page Ask Yourself 2 Odds of Becoming Disabled

An Insured Disability Salary Continuation Plan What would the financial impact on your business be if an owner or key employee became disabled? Table of Contents Page Ask Yourself 2 Odds of Becoming Disabled