Merchant Processing. Trends and Truths. Roger Raney TransFirst Regional Sales Manager

|

|

|

- Pierce Anthony

- 10 years ago

- Views:

Transcription

1 Merchant Processing Trends and Truths Karen Miles US Rice Producers Association Financial Director Roger Raney TransFirst Regional Sales Manager Andrea Cruz-Lawson Cadence Bank N.A. VP Treasury Mgt. Sales Officer

2 Panel Discussion What do you need in a Merchant Services partner? What do you want in a Merchant Services partner? What keeps you up at night critical business challenges? As my advisor, tell me what I don t know?

3 Panel Discussion What do you need in a Merchant Services partner? Help translating my existing merchant statement & identify cost saving efficiencies. High level of customer service with prompt response times. Settlement transmission time frames for Visa, MasterCard, Discover, American Express? Guidance on which to accept?

4 Panel Discussion What do you want in a Merchant Services partner? Web integration that provides reconciliation reporting. E-Commerce point of sale web presence to accept payments. Dynamic payment options to pay multiple accounts with multiple credit cards.

5 Panel Discussion What keeps you up at night critical business challenges? Am I protecting our corporate interests, what is my liability in the event of a security breach. How can I control expenses & manage surcharges to increase my bottom line? What is merchant insurance, does my current policy provide me with sufficient coverage?

6 Panel Discussion As my advisor, tell me what I don t know? PCI Compliance Guidelines, what you are responsible for. How to avoid downgrades and the disadvantages of Daily Discounting. The benefits of partnering with a Direct Processor vs. an Independent Sales Office (ISO).

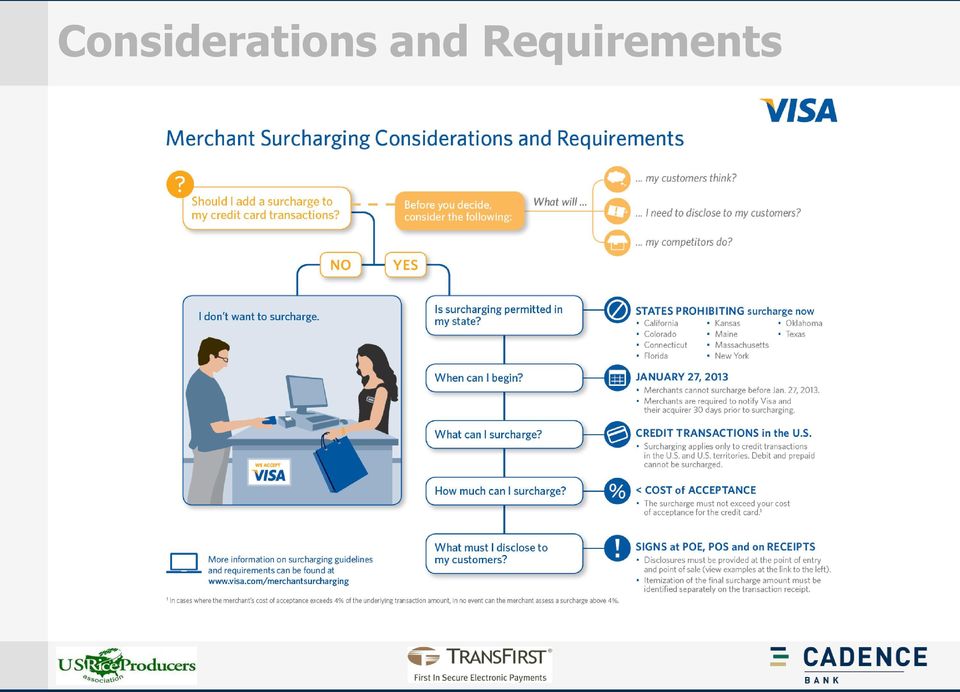

7 Agenda Surcharges Here we go! Why EMV and Why Now? Achieving PCI-DDS Compliance The Square Good News or Not So Good News

8 Surcharges Here we go! Merchants who choose to surcharge will be required to follow certain requirements, including disclosure of surcharge practices to customers at the store entry point and at the point of sale. The following information and resources are available to assist merchants who opt to surcharge in preparing for these changes: Merchants who choose to surcharge must notify Visa and their acquirer 30 days prior to beginning to surcharge

9 Considerations and Requirements

10 Surcharge Notification Sample We impose a surcharge on credit cards that is not greater than our cost of acceptance

11 Why EMV and Why Now?

12 What is EMV-Europay MasterCard and Visa EMV is based on strong cryptography (both symmetric and asymmetric) and elaborate key management; a fundamental EMV principle is to digitally sign payment data to ensure transaction integrity. As opposed to magnetic stripe technology, a chip is extremely difficult to crack; card authentication and PIN verification are performed automatically and objectively by the chip. EMV s dynamic data feature basically says if you can t prevent data from being stolen, make the stolen data useless because dynamic data is only useful for the sole transaction it characterizes, nothing more.

13 Why EMV and Why Now? There are many reasons why EMV chip technology makes sense for the United States. These are some of the major factors: It is the consensus amongst observers although there are no published fraud numbers in the U.S. like there are in other domestic markets that physical world fraud in the U.S. is already above the global average and still on the rise.

14 Differences and Benefits of EMV EMV chip card transactions improve security against fraud compared to magnetic stripe card transactions that rely on the holder's signature and visual inspection of the card to check for features such as hologram. The supposed increased protection from fraud has allowed banks and credit card issuers to push through a 'liability shift' such that merchants are now liable.

15 Liability Shift Dates United States Liability Shift Dates American Express is implementing a liability shift for point of sale terminals in October, For pay at the pump, at gas stations, the liability shift is October, Discover is implementing a liability shift on October 1, For pay at the pump at gas stations, the liability shift is October 1, Maestro is implementing a liability shift of April 19, 2013, for international cards used in the United States.

16 Liability Shift Dates United States Liability Shift Dates MasterCard is implementing a liability shift for point of sale terminals in October, For pay at the pump, at gas stations, the liability shift is October, For ATMs, the liability shift date is in October Visa is implementing a liability shift for point of sale terminals on October 1, For pay at the pump, at gas stations, the liability shift is October 1, For ATMs, the liability shift date is October 1, 2017.

17 Differences and Benefits of EMV Cardholder Inconvenience Abroad With market penetration of EMV technology deployment growing around the world, in particular the nearly 100% coverage in the Single Euro Payment Area (SEPA) and soon to be in Canada, the magnetic stripe technology becomes more and more archaic. Mobile and Contactless Implementing EMV chip technology in the United States will speed up mobile and contactless payments and make them more secure. The devices that accept EMV chip cards are dual contact/contactless devices. By installing these devices to accept EMV, merchants are also readying themselves to accept mobile and contactless payments as well.

18 EMV and the Technology Innovation Program Effective 1 October 2012, Visa expanded the Technology Innovation Program (TIP) to the U.S. TIP rewards merchants that have invested in EMV technology by eliminating the requirement to validate compliance with the Payment Card Industry Data Security Standard (PCI DSS) for any year in which at least 75 percent of the eligible merchant s Visa transactions originate from dual-interface EMV chip-enabled terminals Terminals must be enabled to support both EMV contact and contactless chip acceptance, including mobile contactless payments based on NFC (near field communication) technology. Contact chip-only or contactlessonly terminals will not qualify for the U.S. program.

technology.")

19 Technology Innovation Program To qualify for the program and receive its benefits, U.S. merchants must meet all of the following criteria: The merchant must have validated PCI DSS compliance within the previous 12 months or have submitted to Visa (via their acquirer) a defined remediation plan for achieving compliance, based on a gap analysis. The merchant must have confirmed that sensitive authentication data (i.e., full contents of magnetic stripe, CVV2 and/or PIN data) is not stored, as defined in the PCI DSS. At least 75 percent of the merchant s total transaction count must originate from dual-interface (contact / contactless) enabled chip-reading device terminals. The merchant must not be involved in a breach of cardholder data. A breached merchant may qualify for TIP if they have subsequently validated PCI DSS compliance.

enabled chip-reading device terminals.")

20 Achieving PCI-DDS Compliance

21 What is PCI-DDS The Payment Card Industry Data Security Standard (PCI DSS) is a set of requirements designed to ensure that ALL companies that process, store or transmit credit card information maintain a secure environment. Essentially any merchant that has a Merchant ID (MID). The Payment Card Industry Security Standards Council (PCI SSC) was launched on September 7, 2006 to manage the ongoing evolution of the Payment Card Industry (PCI) security standards with focus on improving payment account security throughout the transaction process.

22 Who Does PCI-DDS Apply to PCI applies to ALL organizations or merchants, regardless of size or number of transactions, that accepts, transmits or stores any cardholder data. Said another way, if any customer of that organization ever pays the merchant directly using a credit card or debit card, then the PCI DSS requirements apply. Utilizing a third-party processor does not exempt PCI compliant requirements. Merely using a third-party company does not exclude a company from PCI compliance. It may cut down on their risk exposure and consequently reduce the effort to validate compliance. However, it does not mean they can ignore PCI.

23 PCI Compliance Levels and Requirements

24 PCI-DDS Penalties Potential penalties for Non-Compliance are as follows: The consequences of not being PCI compliant range from $5,000 to $500,000, which is levied by banks and credit card institutions. Banks may fine based on forensic research they must perform to remediate noncompliance. Credit card institutions may levy fines as a punishment for noncompliance and propose a timeline of increasing fines. The following table is an example of a time-cost schedule which Visa uses.

25 Branch Consequences Even if a company is 100% PCI compliant and validated, a breach in cardholder data may still occur. Cardholder Breaches can result in the following losses for a merchant. $50-$90 fine per cardholder data compromised Suspension of credit card acceptance by a merchant s credit card account provider Loss of reputation with customers, suppliers, and partners Possible civil litigation from breached customers Loss of customer trust which effects future sales For more information on PCI Data Security Standards (PCI DSS)

26 The Square Good News or Not So Good News

27 The Square Overview Founded in February of 2009 by Jack Dorsey who is also the founder of Twitter.com, Square has seen tremendous growth in a very short amount of time. Much of the company s success can be attributed to the fact that Square has ingeniously broken the mold of credit card processing by removing the traditional barriers-to-entry that restricted processing services to actual businesses and instead brings credit card acceptance to the individual, or essentially anyone and everyone.

28 The Square Overview Signing up for the service is simple: iphone, ipad and Android users simply fill out a quick form, download the Square app, and then await the arrival of the Square up reader in the mail. The Square credit card reader plugs into the headphone jack of the phone or tablet thereby making it a mobile credit card terminal. In fact, Square s model has been so successful that it has attracted big name competitors such as Intuit (GoPayment) and North American Bancard (Pay Anywhere), as well as numerous others both domestically and internationally.

29 The Square The Good Merchants have two pricing options: First, pay a single flat rate of 2.75% for swiped transactions and 3.5% + $0.15 per typed transaction (as of this review). Or, pay a flat monthly fee of $275 and 0% on swiped transactions up to $250,000 in processing per year (keyed transactions still cost 3.5% + $0.15 each). Although the transaction rate for the first pricing option is higher than the Qualified rate of most traditional merchant accounts, it is comparable to the Mid-Qualified and Non-Qualified downgrade surcharges that about 80% of most transactions experience with a traditional merchant account anyway. The rate is, however, much more expensive than the Interchange Pass-through rate pricing model. The second pricing model becomes lessand-less expensive once merchants swipe more than $10,000 in sales per month, but there is no savings for keyed transactions.

30 The Square The Not So Good Square does not verify the credit history of its customers prior to approving an account, so it sets a few limitations to avoid potential losses to fraud. Square states that there is no limit to the amount of money that can be accepted per transaction or per month through its service which is only partially true. Instead of setting processing limitations and denying transactions once users reach their limit, which is something most other processors do, the company relies on two tactics to mitigate potential losses due to fraud. The tactics allow merchants to accept an unlimited amount of credit card sales, but with a catch. (see next slide)

31 The Square The Not So Good Square places holds on funds of card-not-present sales for 30 days if more than $2,002 is charged within any rolling seven day period. This means that if merchants key-in $2,100 in sales within a seven day period (either in a single transaction or in multiple transactions), the extra $98 ($2,100 $2,002 = $98) will be held by Square for 30 days. This policy appears to generate much confusion among users because Square does not provide any warning before the $2,002 limit is reached.

32 The Square The Not So Good Square appears to rely on undisclosed algorithmic risk factors to place automatic holds on transactions that it deems suspicious. The system appears to flag a high number of legitimate transactions and can cause serious problems for some merchants. Numerous merchants report that Square never notified them of the hold, or the reason for placing it, and they only discovered it only when they stopped receiving deposits from their sales.

33 Square Customer Service and Complaints The majority of the complaints fall into three areas: Virtually non-existent phone support, misunderstanding and non-disclosure of the $2,002 cardnot-present deposit hold policy, and reports of random fund holding exceeding 30 days with no explanation or communication from Square. The company appears to rely too heavily on customer service provided by , a Twitter support page, and a support blog. This can pose a big drawback for many merchants, especially for those who are not willing to wait for an response. For more information:

34 Questions Karen Miles US Rice Producers Association Financial Director Roger Raney TransFirst, LLC Regional Sales Manager Andrea Cruz-Lawson Cadence Bank N.A. VP Treasury Mgt. Sales Officer Thank you for coming!

Card Network Update Chip (EMV) Acceptance in the United States At-A-Glance

Acceptance in the United States At-A-Glance") Card Network Update Chip (EMV) Acceptance in the United States At-A-Glance Allegiance Merchant Services is committed to assisting you in navigating through the various considerations that you may face

Card Network Update Chip (EMV) Acceptance in the United States At-A-Glance Allegiance Merchant Services is committed to assisting you in navigating through the various considerations that you may face

Payment Methods. The cost of doing business. Michelle Powell - BASYS Processing, Inc.

Payment Methods The cost of doing business Michelle Powell - BASYS Processing, Inc. You ve got to spend money, to make money Major Industry Topics Industry Process Flow PCI DSS Compliance Risks of Non-Compliance

Payment Methods The cost of doing business Michelle Powell - BASYS Processing, Inc. You ve got to spend money, to make money Major Industry Topics Industry Process Flow PCI DSS Compliance Risks of Non-Compliance

What is Interchange. How Complex is Interchange?

What is Interchange The foundation of the entire Bankcard Processing industry s cost structure. Interchange is the wholesale price, charged by Card Issuing Bank, for Authorization and Settlement of a credit

What is Interchange The foundation of the entire Bankcard Processing industry s cost structure. Interchange is the wholesale price, charged by Card Issuing Bank, for Authorization and Settlement of a credit

What Merchants Need to Know About EMV

Effective November 1, 2014 1. What is EMV? EMV is the global standard for card present payment processing technology and it s coming to the U.S. EMV uses an embedded chip in the card that holds all the

Effective November 1, 2014 1. What is EMV? EMV is the global standard for card present payment processing technology and it s coming to the U.S. EMV uses an embedded chip in the card that holds all the

Table of Contents. Overview. What is payment processing? Who s Who. Types of Payment Solutions. Online Transactions. Interchange Process

Overview Credit Card Processing 101 is your go-to handbook for navigating the payments industry. This document provides a quick and thorough understanding on how businesses accept electronic payments,

Overview Credit Card Processing 101 is your go-to handbook for navigating the payments industry. This document provides a quick and thorough understanding on how businesses accept electronic payments,

Understand the Business Impact of EMV Chip Cards

Understand the Business Impact of EMV Chip Cards 3 What About Mail/Telephone Order and ecommerce? 3 What Is EMV 3 How Chip Cards Work 3 Contactless Technology 4 Background: Behind the Curve 4 Liability

Understand the Business Impact of EMV Chip Cards 3 What About Mail/Telephone Order and ecommerce? 3 What Is EMV 3 How Chip Cards Work 3 Contactless Technology 4 Background: Behind the Curve 4 Liability

The Comprehensive, Yet Concise Guide to Credit Card Processing

The Comprehensive, Yet Concise Guide to Credit Card Processing Written by David Rodwell CreditCardProcessing.net Terms of Use This ebook was created to provide educational information regarding payment

The Comprehensive, Yet Concise Guide to Credit Card Processing Written by David Rodwell CreditCardProcessing.net Terms of Use This ebook was created to provide educational information regarding payment

University Policy Accepting Credit Cards to Conduct University Business

BROWN UNIVERSITY University Policy Accepting Credit Cards to Conduct University Business Purpose Brown University requires all departments that are involved with credit card handling to do so in compliance

BROWN UNIVERSITY University Policy Accepting Credit Cards to Conduct University Business Purpose Brown University requires all departments that are involved with credit card handling to do so in compliance

Credit Card Processing, Point of Sale, ecommerce

Credit Card Processing, Point of Sale, ecommerce Compliance, Self Auditing, and More John Benson Kurt Willey HACKS REGULATIONS Greater Risk for Merchants Topics Compliance Changes Scans Self Audits

Credit Card Processing, Point of Sale, ecommerce Compliance, Self Auditing, and More John Benson Kurt Willey HACKS REGULATIONS Greater Risk for Merchants Topics Compliance Changes Scans Self Audits

Merchant Services Tool Kit TEXPO 2013

Merchant Services Tool Kit TEXPO 2013 Surcharges Visa Information Website Site Preview and PDF s: www.visa.com/merchantsurcharging Materials Notification of Intent to Surcharge Merchants who choose to

Merchant Services Tool Kit TEXPO 2013 Surcharges Visa Information Website Site Preview and PDF s: www.visa.com/merchantsurcharging Materials Notification of Intent to Surcharge Merchants who choose to

Preparing for EMV chip card acceptance

Preparing for EMV chip card acceptance Ben Brown Vice President, Regional Sales Manager, Wells Fargo Merchant Services Lily Page Vice President, Wholesale ereceivables, Wells Fargo Merchant Services June

Preparing for EMV chip card acceptance Ben Brown Vice President, Regional Sales Manager, Wells Fargo Merchant Services Lily Page Vice President, Wholesale ereceivables, Wells Fargo Merchant Services June

EMV and Restaurants: What you need to know. Mike English. October 2014. Executive Director, Product Development Heartland Payment Systems

October 2014 EMV and Restaurants: What you need to know Mike English Executive Director, Product Development Heartland Payment Systems 2014 Heartland Payment Systems, Inc. All trademarks, service marks

October 2014 EMV and Restaurants: What you need to know Mike English Executive Director, Product Development Heartland Payment Systems 2014 Heartland Payment Systems, Inc. All trademarks, service marks

EMV in Hotels Observations and Considerations

EMV in Hotels Observations and Considerations Just in: EMV in the Mail Customer Education: Credit Card companies have already started customer training for the new smart cards. 1 Questions to be Answered

EMV in Hotels Observations and Considerations Just in: EMV in the Mail Customer Education: Credit Card companies have already started customer training for the new smart cards. 1 Questions to be Answered

EMV and Small Merchants:

September 2014 EMV and Small Merchants: What you need to know Mike English Executive Director, Product Development Heartland Payment Systems 2014 Heartland Payment Systems, Inc. All trademarks, service

September 2014 EMV and Small Merchants: What you need to know Mike English Executive Director, Product Development Heartland Payment Systems 2014 Heartland Payment Systems, Inc. All trademarks, service

Visa Recommended Practices for EMV Chip Implementation in the U.S.

CHIP ADVISORY #20, UPDATED JULY 11, 2012 Visa Recommended Practices for EMV Chip Implementation in the U.S. Summary As issuers, acquirers, merchants, processors and vendors plan and begin programs to adopt

CHIP ADVISORY #20, UPDATED JULY 11, 2012 Visa Recommended Practices for EMV Chip Implementation in the U.S. Summary As issuers, acquirers, merchants, processors and vendors plan and begin programs to adopt

Fall Conference November 19 21, 2013 Merchant Card Processing Overview

Fall Conference November 19 21, 2013 Merchant Card Processing Overview Agenda Industry Definition Process Flows Processing Costs Chargeback's Payment Card Industry (PCI) Guidelines for Convenience Fees

Fall Conference November 19 21, 2013 Merchant Card Processing Overview Agenda Industry Definition Process Flows Processing Costs Chargeback's Payment Card Industry (PCI) Guidelines for Convenience Fees

Chip Card (EMV ) CAL-Card FAQs

CAL-Card FAQs") U.S. Bank Chip Card (EMV ) CAL-Card FAQs Below are answers to some frequently asked questions about the migration to U.S. Bank chipenabled CAL-Cards. This guide can help ensure that you are prepared for

U.S. Bank Chip Card (EMV ) CAL-Card FAQs Below are answers to some frequently asked questions about the migration to U.S. Bank chipenabled CAL-Cards. This guide can help ensure that you are prepared for

Card Acceptance Best Practices to Manage Rates and Minimize Risk

Card Acceptance Best Practices to Manage Rates and Minimize Risk Kim Jackson VP, Transfund Merchant Services April 23, 2014 BOK Financial is registered with the National Association of State Boards of

Card Acceptance Best Practices to Manage Rates and Minimize Risk Kim Jackson VP, Transfund Merchant Services April 23, 2014 BOK Financial is registered with the National Association of State Boards of

PCI Compliance Overview

PCI Compliance Overview 1 PCI DSS Payment Card Industry Data Security Standard Standard that is applied to: Merchants Service Providers (Banks, Third party vendors, gateways) Systems (Hardware, software)

PCI Compliance Overview 1 PCI DSS Payment Card Industry Data Security Standard Standard that is applied to: Merchants Service Providers (Banks, Third party vendors, gateways) Systems (Hardware, software)

Redwood Merchant Services. Merchant Processing Terminology

ACH - Automated Clearing House for member banks to process electronic payments or withdrawals. (Credits or debits to a bank account) through the Federal Reserve Bank. Acquiring Bank - Licensed Visa/MasterCard

ACH - Automated Clearing House for member banks to process electronic payments or withdrawals. (Credits or debits to a bank account) through the Federal Reserve Bank. Acquiring Bank - Licensed Visa/MasterCard

Payment Processing considerations to comply with IRS and PCI-DSS regulations and policies

itransact Presents Payment Processing considerations to comply with IRS and PCI-DSS regulations and policies Learning Objectives At the end of this course you will be able to: Prepare for IRS 6050w and

itransact Presents Payment Processing considerations to comply with IRS and PCI-DSS regulations and policies Learning Objectives At the end of this course you will be able to: Prepare for IRS 6050w and

Saint Louis University Merchant Card Processing Policy & Procedures

Saint Louis University Merchant Card Processing Policy & Procedures Overview: Policies and procedures for processing credit card transactions and properly storing credit card data physically and electronically.

Saint Louis University Merchant Card Processing Policy & Procedures Overview: Policies and procedures for processing credit card transactions and properly storing credit card data physically and electronically.

Credit/Debit Card Processing Requirements and Best Practices. Adele Honeyman Oregon State Treasury Training Specialist

Credit/Debit Card Processing Requirements and Best Practices Adele Honeyman Oregon State Treasury Training Specialist 1 What? What do I need to know about excepting credit cards? Who s involved, how it

Credit/Debit Card Processing Requirements and Best Practices Adele Honeyman Oregon State Treasury Training Specialist 1 What? What do I need to know about excepting credit cards? Who s involved, how it

PCI DSS Payment Card Industry Data Security Standard. Merchant compliance guidelines for level 4 merchants

Appendix 2 PCI DSS Payment Card Industry Data Security Standard Merchant compliance guidelines for level 4 merchants CONTENTS 1. What is PCI DSS? 2. Why become compliant? 3. What are the requirements?

Appendix 2 PCI DSS Payment Card Industry Data Security Standard Merchant compliance guidelines for level 4 merchants CONTENTS 1. What is PCI DSS? 2. Why become compliant? 3. What are the requirements?

Accepting Payment Cards and ecommerce Payments

Policy V. 4.1.1 Responsible Official: Vice President for Finance and Treasurer Effective Date: September 29, 2010 Accepting Payment Cards and ecommerce Payments Policy Statement The University of Vermont

Policy V. 4.1.1 Responsible Official: Vice President for Finance and Treasurer Effective Date: September 29, 2010 Accepting Payment Cards and ecommerce Payments Policy Statement The University of Vermont

Frequently Asked Questions

PCI Compliance Frequently Asked Questions Table of Content GENERAL INFORMATION... 2 PAYMENT CARD INDUSTRY DATA SECURITY STANDARD (PCI DSS)...2 Are all merchants and service providers required to comply

PCI Compliance Frequently Asked Questions Table of Content GENERAL INFORMATION... 2 PAYMENT CARD INDUSTRY DATA SECURITY STANDARD (PCI DSS)...2 Are all merchants and service providers required to comply

Clark Brands Payment Methods Manual. First Data Locations

Clark Brands Payment Methods Manual First Data Locations Table of Contents Introduction... 3 Valid Card Types... 3 Authorization Numbers, Merchant ID Numbers and Request for Copy Fax Numbers... 4 Other

Clark Brands Payment Methods Manual First Data Locations Table of Contents Introduction... 3 Valid Card Types... 3 Authorization Numbers, Merchant ID Numbers and Request for Copy Fax Numbers... 4 Other

Information Technology

Credit Card Handling Security Standards Overview Information Technology This document is intended to provide guidance to merchants (colleges, departments, organizations or individuals) regarding the processing

Credit Card Handling Security Standards Overview Information Technology This document is intended to provide guidance to merchants (colleges, departments, organizations or individuals) regarding the processing

Mitigating Fraud Risk Through Card Data Verification

Risk Management Best Practices 11 September 2014 Mitigating Fraud Risk Through Card Data Verification AP, Canada, CEMEA, LAC, U.S. Issuers, Processors With a number of cardholder payment options (e.g.,

Risk Management Best Practices 11 September 2014 Mitigating Fraud Risk Through Card Data Verification AP, Canada, CEMEA, LAC, U.S. Issuers, Processors With a number of cardholder payment options (e.g.,

EMV and Restaurants What you need to know! November 19, 2014

EMV and Restaurants What you need to know! Mike English Executive Director of Product Development Kristi Kuehn Sr. Director, Compliance November 9, 204 Agenda EMV overview Timelines Chip Card Liability

EMV and Restaurants What you need to know! Mike English Executive Director of Product Development Kristi Kuehn Sr. Director, Compliance November 9, 204 Agenda EMV overview Timelines Chip Card Liability

U.S. Bank. U.S. Bank Chip Card FAQs for Program Administrators. In this guide you will find: Explaining Chip Card Technology (EMV)

") U.S. Bank U.S. Bank Chip Card FAQs for Program Administrators Here are some frequently asked questions Program Administrators have about the replacement of U.S. Bank commercial cards with new chip-enabled

U.S. Bank U.S. Bank Chip Card FAQs for Program Administrators Here are some frequently asked questions Program Administrators have about the replacement of U.S. Bank commercial cards with new chip-enabled

Policy Title: Payment Cards Policy Effective Date: 5/5/2010. Policy Number: FA-PO-1214 Date of Last Revision: 11/5/2014

Policy Title: Effective Date: 5/5/2010 Policy Number: FA-PO-1214 Date of Last Revision: 11/5/2014 Oversight Department: Financial Services Next Review Date: 10/1/2016 1. PURPOSE The for Radford University

Policy Title: Effective Date: 5/5/2010 Policy Number: FA-PO-1214 Date of Last Revision: 11/5/2014 Oversight Department: Financial Services Next Review Date: 10/1/2016 1. PURPOSE The for Radford University

EMV : Frequently Asked Questions for Merchants

EMV : Frequently Asked Questions for Merchants The information in this document is offered on an as is basis, without warranty of any kind, either expressed, implied or statutory, including but not limited

EMV : Frequently Asked Questions for Merchants The information in this document is offered on an as is basis, without warranty of any kind, either expressed, implied or statutory, including but not limited

EMV Frequently Asked Questions for Merchants May, 2014

EMV Frequently Asked Questions for Merchants May, 2014 Copyright 2014 Vantiv All rights reserved. Disclaimer The information in this document is offered on an as is basis, without warranty of any kind,

EMV Frequently Asked Questions for Merchants May, 2014 Copyright 2014 Vantiv All rights reserved. Disclaimer The information in this document is offered on an as is basis, without warranty of any kind,

Merchant Account Glossary of Terms

Merchant Account Glossary of Terms From offshore merchant accounts to the truth behind free merchant accounts, get answers to some of the most common and frequently asked questions. If you cannot find

Merchant Account Glossary of Terms From offshore merchant accounts to the truth behind free merchant accounts, get answers to some of the most common and frequently asked questions. If you cannot find

PCI 3.1 Changes. Jon Bonham, CISA Coalfire System, Inc.

PCI 3.1 Changes Jon Bonham, CISA Coalfire System, Inc. Agenda Introduction of Coalfire What does this have to do with the business office Changes to version 3.1 EMV P2PE Questions and Answers Contact Information

PCI 3.1 Changes Jon Bonham, CISA Coalfire System, Inc. Agenda Introduction of Coalfire What does this have to do with the business office Changes to version 3.1 EMV P2PE Questions and Answers Contact Information

Payment Card Industry (PCI) Data Security Standard

Data Security Standard") Payment Card Industry (PCI) Data Security Standard Attestation of Compliance for Self-Assessment Questionnaire D Service Providers For use with PCI DSS Version 3.1 Revision 1.1 July 2015 Section 1: Assessment

Payment Card Industry (PCI) Data Security Standard Attestation of Compliance for Self-Assessment Questionnaire D Service Providers For use with PCI DSS Version 3.1 Revision 1.1 July 2015 Section 1: Assessment

Attestation of Compliance for Onsite Assessments Service Providers

Attestation of Compliance Service Providers Payment Card Industry (PCI) Data Security Standard Attestation of Compliance for Onsite Assessments Service Providers Version 2.0 October 2010 Instructions for

Attestation of Compliance Service Providers Payment Card Industry (PCI) Data Security Standard Attestation of Compliance for Onsite Assessments Service Providers Version 2.0 October 2010 Instructions for

OpenEdge Research & Development Group April 2015

2015: Security, Merchant Readiness & the Coming Liability Shift OpenEdge Research & Development Group April 2015 [email protected] openedgepay.com 2015: Security, Merchant Table of Contents The

2015: Security, Merchant Readiness & the Coming Liability Shift OpenEdge Research & Development Group April 2015 [email protected] openedgepay.com 2015: Security, Merchant Table of Contents The

TNHFMA 2011 Fall Institute October 12, 2011 TAKING OUR CUSTOMERS BUSINESS FORWARD. The Cost of Payment Card Data Theft and Your Business

TAKING OUR CUSTOMERS BUSINESS FORWARD The Cost of Payment Card Data Theft and Your Business Aaron Lego Director of Business Development Presentation Agenda Items we will cover: 1. Background on Payment

TAKING OUR CUSTOMERS BUSINESS FORWARD The Cost of Payment Card Data Theft and Your Business Aaron Lego Director of Business Development Presentation Agenda Items we will cover: 1. Background on Payment

Are You Ready For PCI v 3.0. Speaker: Corbin DelCarlo Institution: McGladrey LLP Date: October 6, 2014

Are You Ready For PCI v 3.0 Speaker: Corbin DelCarlo Institution: McGladrey LLP Date: October 6, 2014 Today s Presenter Corbin Del Carlo QSA, PA QSA Director, National Leader PCI Services Practice 847.413.6319

Are You Ready For PCI v 3.0 Speaker: Corbin DelCarlo Institution: McGladrey LLP Date: October 6, 2014 Today s Presenter Corbin Del Carlo QSA, PA QSA Director, National Leader PCI Services Practice 847.413.6319

Apple Pay. Frequently Asked Questions UK

Apple Pay Frequently Asked Questions UK Version 1.0 (July 2015) First Data Merchant Solutions is a trading name of First Data Europe Limited, a private limited company incorporated in England (company

Apple Pay Frequently Asked Questions UK Version 1.0 (July 2015) First Data Merchant Solutions is a trading name of First Data Europe Limited, a private limited company incorporated in England (company

The Impact of Emerging Payment Technologies on Retail and Hospitality Businesses. National Computer Corporation www.nccusa.com

The Impact of Emerging Payment Technologies on Retail and Hospitality Businesses The Impact of Emerging Payment Technologies on Retail and Hospitality Businesses Making the customer payment process convenient,

The Impact of Emerging Payment Technologies on Retail and Hospitality Businesses The Impact of Emerging Payment Technologies on Retail and Hospitality Businesses Making the customer payment process convenient,

Key Steps to Meeting PCI DSS 2.0 Requirements Using Sensitive Data Discovery and Masking

Key Steps to Meeting PCI DSS 2.0 Requirements Using Sensitive Data Discovery and Masking SUMMARY The Payment Card Industry Data Security Standard (PCI DSS) defines 12 high-level security requirements directed

Key Steps to Meeting PCI DSS 2.0 Requirements Using Sensitive Data Discovery and Masking SUMMARY The Payment Card Industry Data Security Standard (PCI DSS) defines 12 high-level security requirements directed

EMV FAQs. Contact us at: [email protected]. Visit us online: VancoPayments.com

EMV FAQs Contact us at: [email protected] Visit us online: VancoPayments.com What are the benefits of EMV cards to merchants and consumers? What is EMV? The acronym EMV stands for an organization formed

EMV FAQs Contact us at: [email protected] Visit us online: VancoPayments.com What are the benefits of EMV cards to merchants and consumers? What is EMV? The acronym EMV stands for an organization formed

Table of Contents The Market for Merchant Services... 1 The Basics of Payment Processing... 2 Authorization Settlement Funding... 2 Authorization...

Table of Contents The Market for Merchant Services... 1 The Basics of Payment Processing... 2 Authorization Settlement Funding... 2 Authorization... 2 Settlement... 2 Funding... 2 Credit Card Processing

Table of Contents The Market for Merchant Services... 1 The Basics of Payment Processing... 2 Authorization Settlement Funding... 2 Authorization... 2 Settlement... 2 Funding... 2 Credit Card Processing

Apple Pay. Frequently Asked Questions UK Launch

Apple Pay Frequently Asked Questions UK Launch Version 1.0 2015 First Data Corporation. All Rights Reserved. All trademarks, service marks and trade names referenced in this material are the property of

Apple Pay Frequently Asked Questions UK Launch Version 1.0 2015 First Data Corporation. All Rights Reserved. All trademarks, service marks and trade names referenced in this material are the property of

CPIM Academy. Cash 257 Merchant Services and Revenue Collection

CPIM Academy Cash 257 Merchant Services and Revenue Collection 2015 Objectives Feel prepared to discuss/understand basics of merchant processing Understand Service Fees Difference between credit and debit

CPIM Academy Cash 257 Merchant Services and Revenue Collection 2015 Objectives Feel prepared to discuss/understand basics of merchant processing Understand Service Fees Difference between credit and debit

How Online Payments Really Work

Insights for Businesses How Online Payments Really Work If you re thinking about setting up an online store, you re in good company. Shoppers are increasingly turning to online options, as their access

Insights for Businesses How Online Payments Really Work If you re thinking about setting up an online store, you re in good company. Shoppers are increasingly turning to online options, as their access

FAQ s for Payment Card Processing at the University

FAQ s for Payment Card Processing at the University 1) We are thinking about taking credit cards for payments. What do we need to know? 2) Who is the PCPC (Payment Card Process Coordinator)? 3) What is

FAQ s for Payment Card Processing at the University 1) We are thinking about taking credit cards for payments. What do we need to know? 2) Who is the PCPC (Payment Card Process Coordinator)? 3) What is

Glossary ACH Acquirer Assessments: AVS Authorization Back End: Backbilling Basis Point Batch

Glossary ACH: Automated Clearing House; an electronic payment network most commonly associated with payroll direct deposit, recurring payments, and is the network most commonly used to settle merchant

Glossary ACH: Automated Clearing House; an electronic payment network most commonly associated with payroll direct deposit, recurring payments, and is the network most commonly used to settle merchant

Guide to Processing Card Payments

Wells Fargo Merchant Services Guide to Processing Card Payments Welcome! Thank you for selecting Wells Fargo Merchant Services! This Welcome Kit brings together all the information you need to get started,

Wells Fargo Merchant Services Guide to Processing Card Payments Welcome! Thank you for selecting Wells Fargo Merchant Services! This Welcome Kit brings together all the information you need to get started,

It is important to note, the payment brands and acquirers are responsible for enforcing compliance, not the PCI council.

PCI FAQ And MYTHS FREQUENTLY ASKED QUESTIONS (FAQ): Q: What is PCI? A: The Payment Card Industry Data Security Standard (PCI DSS) is a set of requirements designed to ensure that ALL companies that process,

PCI FAQ And MYTHS FREQUENTLY ASKED QUESTIONS (FAQ): Q: What is PCI? A: The Payment Card Industry Data Security Standard (PCI DSS) is a set of requirements designed to ensure that ALL companies that process,

CAL POLY POMONA FOUNDATION. Policy for Accepting Payment (Credit) Card and Ecommerce Payments

Card and Ecommerce Payments") CAL POLY POMONA FOUNDATION Policy for Accepting Payment (Credit) Card and Ecommerce Payments 1 PURPOSE The purpose of this policy is to establish business processes and procedures for accepting payment

CAL POLY POMONA FOUNDATION Policy for Accepting Payment (Credit) Card and Ecommerce Payments 1 PURPOSE The purpose of this policy is to establish business processes and procedures for accepting payment

A Guide to EMV. Version 1.0 May 2011. Copyright 2011 EMVCo, LLC. All rights reserved.

A Guide to EMV Version 1.0 May 2011 Objective Provide an overview of the EMV specifications and processes What is EMV? Why EMV? Position EMV in the context of the wider payments industry Define the role

A Guide to EMV Version 1.0 May 2011 Objective Provide an overview of the EMV specifications and processes What is EMV? Why EMV? Position EMV in the context of the wider payments industry Define the role

CardControl. Credit Card Processing 101. Overview. Contents

CardControl Credit Card Processing 101 Overview Credit card processing is a very complex and important system for anyone that sells goods. This guide will hopefully help educate and inform new and old

CardControl Credit Card Processing 101 Overview Credit card processing is a very complex and important system for anyone that sells goods. This guide will hopefully help educate and inform new and old

How Do I Understand Credit Card Processing Fees?

How Do I Understand Credit Card Processing Fees? Credit card processing rates and fees are often misunderstood and confusing, so we are committed to helping you understand the various costs associated

How Do I Understand Credit Card Processing Fees? Credit card processing rates and fees are often misunderstood and confusing, so we are committed to helping you understand the various costs associated

1/18/10. Walt Conway. PCI DSS in Context. Some History The Digital Dozen Key Players Cardholder Data Outsourcing Conclusions. PCI in Higher Education

PCI in Higher Education Walter Conway, QSA 403 Labs, LLC Walt Conway PCI consultant, blogger, trainer, speaker, author Former Visa VP Help schools become PCI compliant Represent Higher Education at PCI

PCI in Higher Education Walter Conway, QSA 403 Labs, LLC Walt Conway PCI consultant, blogger, trainer, speaker, author Former Visa VP Help schools become PCI compliant Represent Higher Education at PCI

Your Compliance Classification Level and What it Means

General Information What are the Payment Card Industry (PCI) Data Security Standards? The PCI Data Security Standards represents a common set of industry tools and measurements to help ensure the safe

General Information What are the Payment Card Industry (PCI) Data Security Standards? The PCI Data Security Standards represents a common set of industry tools and measurements to help ensure the safe

The Interlink Network and Maestro U.S.A. Network rules and regulations (collectively National/International Networks );

;") Chapter 7000 CREDIT AND DEBIT CARD COLLECTION TRANSACTIONS (T/L 675) This Treasury Financial Manual (TFM) chapter consolidates existing guidance and provides the requirements that Federal Government agencies

Chapter 7000 CREDIT AND DEBIT CARD COLLECTION TRANSACTIONS (T/L 675) This Treasury Financial Manual (TFM) chapter consolidates existing guidance and provides the requirements that Federal Government agencies

PCI DSS FAQ. The twelve requirements of the PCI DSS are defined as follows:

What is PCI DSS? PCI DSS is an acronym for Payment Card Industry Data Security Standards. PCI DSS is a global initiative intent on securing credit and banking transactions by merchants & service providers

What is PCI DSS? PCI DSS is an acronym for Payment Card Industry Data Security Standards. PCI DSS is a global initiative intent on securing credit and banking transactions by merchants & service providers

Credit Card Processing Overview

CardControl 3.0 Credit Card Processing Overview Overview Credit card processing is a very complex and important system for anyone that sells goods. This guide will hopefully help educate and inform new

CardControl 3.0 Credit Card Processing Overview Overview Credit card processing is a very complex and important system for anyone that sells goods. This guide will hopefully help educate and inform new

PCI Data Security Standards. Presented by Pat Bergamo for the NJTC February 6, 2014

PCI Data Security Standards Presented by Pat Bergamo for the NJTC February 6, 2014 Introduction 3/3/2014 2 Your Speaker Patrick Bergamo, CISSP Director of Information Security & Delivery Delta Corporate

PCI Data Security Standards Presented by Pat Bergamo for the NJTC February 6, 2014 Introduction 3/3/2014 2 Your Speaker Patrick Bergamo, CISSP Director of Information Security & Delivery Delta Corporate

PCI and EMV Compliance Checkup

PCI and EMV Compliance Checkup ATM Security Jim Pettitt Director, ATM Security Diebold Incorporated Agenda ATM threats today Top of mind risk PCI Impact on Security U.S. EMV Migration Conclusions / recommendations

PCI and EMV Compliance Checkup ATM Security Jim Pettitt Director, ATM Security Diebold Incorporated Agenda ATM threats today Top of mind risk PCI Impact on Security U.S. EMV Migration Conclusions / recommendations

Office of Finance and Treasury

Office of Finance and Treasury How to Accept & Process Credit and Debit Card Transactions Procedure Related Policy Title Credit Card Processing Policy For University Merchant Locations Responsible Executive

Office of Finance and Treasury How to Accept & Process Credit and Debit Card Transactions Procedure Related Policy Title Credit Card Processing Policy For University Merchant Locations Responsible Executive

The Science of Credit Card Processing

The Science of Credit Card Processing Page 1 Credit Card Processing How does credit card processing work? You may receive credit card payments from customers from a variety of sources. You may swipe their

The Science of Credit Card Processing Page 1 Credit Card Processing How does credit card processing work? You may receive credit card payments from customers from a variety of sources. You may swipe their

With the Target breach on everyone s mind, you may find these Customer Service Q & A s helpful.

With the Target breach on everyone s mind, you may find these Customer Service Q & A s helpful. Breach Overview Q: Media reports are stating that Target experienced a data breach. Can you provide more

With the Target breach on everyone s mind, you may find these Customer Service Q & A s helpful. Breach Overview Q: Media reports are stating that Target experienced a data breach. Can you provide more

What is EMV? What is different?

U.S. consumers are receiving new debit and credit cards with embedded chip technology that better stores and protects cardholder information. These new chip cards are part of the new card standard, Europay,

U.S. consumers are receiving new debit and credit cards with embedded chip technology that better stores and protects cardholder information. These new chip cards are part of the new card standard, Europay,

Steps for staying PCI DSS compliant Visa Account Information Security Guide October 2009

Steps for staying PCI DSS compliant Visa Account Information Security Guide October 2009 The guide describes how you can make sure your business does not store sensitive cardholder data Contents 1 Contents

Steps for staying PCI DSS compliant Visa Account Information Security Guide October 2009 The guide describes how you can make sure your business does not store sensitive cardholder data Contents 1 Contents

Payment Card Industry (PCI) Data Security Standard Self-Assessment Questionnaire B and Attestation of Compliance

Data Security Standard Self-Assessment Questionnaire B and Attestation of Compliance") Payment Card Industry (PCI) Data Security Standard Self-Assessment Questionnaire B and Attestation of Compliance Merchants with Only Imprint Machines or Only Standalone, Dial-out Terminals Electronic Cardholder

Payment Card Industry (PCI) Data Security Standard Self-Assessment Questionnaire B and Attestation of Compliance Merchants with Only Imprint Machines or Only Standalone, Dial-out Terminals Electronic Cardholder

mobile payment acceptance Solutions Visa security best practices version 3.0

mobile payment acceptance Visa security best practices version 3.0 Visa Security Best Practices for, Version 3.0 Since Visa s first release of this best practices document in 2011, we have seen a rapid

mobile payment acceptance Visa security best practices version 3.0 Visa Security Best Practices for, Version 3.0 Since Visa s first release of this best practices document in 2011, we have seen a rapid

EMV and Chip Cards Key Information On What This Is, How It Works and What It Means

EMV and Chip Cards Key Information On What This Is, How It Works and What It Means Document Purpose This document is intended to provide information about the concepts behind and the processes involved

EMV and Chip Cards Key Information On What This Is, How It Works and What It Means Document Purpose This document is intended to provide information about the concepts behind and the processes involved

WASHINGTON STATE UNIVERSITY MERCHANT ACCOUNT AGREEMENT FOR UNIVERSITY DEPARTMENTS

WASHINGTON STATE UNIVERSITY MERCHANT ACCOUNT AGREEMENT FOR UNIVERSITY DEPARTMENTS I. Introduction, Background and Purpose This Merchant Account Agreement (the Merchant Agreement or Agreement ) is entered

WASHINGTON STATE UNIVERSITY MERCHANT ACCOUNT AGREEMENT FOR UNIVERSITY DEPARTMENTS I. Introduction, Background and Purpose This Merchant Account Agreement (the Merchant Agreement or Agreement ) is entered

The Cost of Payment Card Data Theft and Your Business. Aaron Lego Director of Business Development

The Cost of Payment Card Data Theft and Your Business Aaron Lego Director of Business Development Presentation Agenda Items we will cover: 1. Background on Payment Card Industry Data Security Standards

The Cost of Payment Card Data Theft and Your Business Aaron Lego Director of Business Development Presentation Agenda Items we will cover: 1. Background on Payment Card Industry Data Security Standards

Dates VISA MasterCard Discover American Express. support EMV. International ATM liability shift 2

Network Updates Summer 2013 We are committed to working closely with you on achieving your business goals. As a part of this commitment, we carefully monitor Network changes and summarize them for your

Network Updates Summer 2013 We are committed to working closely with you on achieving your business goals. As a part of this commitment, we carefully monitor Network changes and summarize them for your

Secure Payments Framework Workgroup

Secure Payments Framework Workgroup EMV for the US Hospitality Industry Version 1.0 About HTNG Hotel Technology Next Generation (HTNG) is a non-profit association with a mission to foster, through collaboration

Secure Payments Framework Workgroup EMV for the US Hospitality Industry Version 1.0 About HTNG Hotel Technology Next Generation (HTNG) is a non-profit association with a mission to foster, through collaboration

Payment Card Industry Data Security Standard Training. Chris Harper Vice President of Technical Services Secure Enterprise Computing, Inc.

Payment Card Industry Data Security Standard Training Chris Harper Vice President of Technical Services Secure Enterprise Computing, Inc. March 27, 2012 Agenda Check-In 9:00-9:30 PCI Intro and History

Payment Card Industry Data Security Standard Training Chris Harper Vice President of Technical Services Secure Enterprise Computing, Inc. March 27, 2012 Agenda Check-In 9:00-9:30 PCI Intro and History

Payment Card Industry (PCI) Data Security Standard

Data Security Standard") Payment Card Industry (PCI) Data Standard Attestation of Compliance for Self-Assessment Questionnaire D Service Providers Version 3.1 April 2015 Section 1: Assessment Information Instructions for Submission

Payment Card Industry (PCI) Data Standard Attestation of Compliance for Self-Assessment Questionnaire D Service Providers Version 3.1 April 2015 Section 1: Assessment Information Instructions for Submission

Emerging Trends in the Payment Ecosystem: The Good, the Bad and the Ugly DAN KRAMER

Emerging Trends in the Payment Ecosystem: The Good, the Bad and the Ugly DAN KRAMER SHAZAM, Senior Vice President Agenda The Ugly Fraud The Bad EMV? The Good Tokenization and Other Emerging Payment Options

Emerging Trends in the Payment Ecosystem: The Good, the Bad and the Ugly DAN KRAMER SHAZAM, Senior Vice President Agenda The Ugly Fraud The Bad EMV? The Good Tokenization and Other Emerging Payment Options