Borrower Interest Rate Date Form

|

|

|

- Linda Jackson

- 8 years ago

- Views:

Transcription

1 Correspondent Lending Compliance Quick Reference Closing Requirements This section describes Plaza s policies for loan delivered for purchase through our Correspondent channel. Unless otherwise mentioned herein, Plaza s requirements are the same as the FNMA/FHLMC/GNMA secondary market standards, and loans must comply with all applicable federal and state regulatory requirements set by STATE, RESPA, HUD, VA, AIR, MDIA /TILA and all other mortgage lending regulations. If in doubt, contact your local closing department for assistance. Regulatory and Disclosure Requirements GSE, HUD and Dodd-Frank Act Appraisal Independence Requirements (AIRs) Evidence of Net Tangible Benefit to borrower State-Specific High-Cost regulations Home Ownership and Equity Protection Act (HOEPA) Interest Rate Set Date Borrower Interest Rate Set Date Is Required Effective April 1, 2010 The Home Ownership and Equity Protection Act (HOEPA) requires specific interest rate data for higher-priced mortgage loans (HPML) to be reported to HMDA and the Agencies. To ensure regulatory compliance, Plaza Home Mortgage will require and review for documentation of the borrower interest rate set date. To comply with this requirement, include one of the following in the loan file labeled as HPML Interest Rate Set Date. Rate lock agreement with the borrower that includes the borrower s last name, property address and last date the interest rate was set with the borrower prior to consummation. A screen-print of a populated FFIEC rate spread calculator from website at or Completed Interest Rate Set Date form as outlined below, or

Evidence of Net Tangible Benefit to borrower State-Specific High-Cost regulations Home")

2 Borrower Interest Rate Date Form To ensure compliance with the (HOEPA) Higher Priced Mortgage (HPML) regulation, HMDA reporting requirements, and Agency delivery requirements, the last date the interest rate was set with the borrower prior to consummation is required. To meet this requirement, complete the form and include in the closed loan file. Borrower s Last Name: Property Address: Last date the interest rate was set with the borrower prior to consummation: / / Reference, for more information regarding Higher Priced Mortgages: The FFIEC Rate Spread Calculator may be found at: Evidence of Truth-in-Lending (TIL) delivery/receipt Signed Overnight Delivery & Courier Receipts Now Accepted as Proof of Receipt for TIL Plaza Home Mortgage will accept signed overnight delivery and courier receipts as proof of receipt of the Truth-in-Lending document by the borrower. Acceptable options are: Fax: Initial and re-disclosed TILs delivered to the borrower(s) by fax will be considered received by the borrower(s) on the date they sign and date the TIL disclosure. Other methods of documenting receipt, such as time/date stamps in the fax header, or fax confirmation sheets, are not sufficient.

3 Overnight delivery: Initial and re-disclosed TILs shipped overnight to the borrower(s), will be considered received by the borrower(s): on the date they sign and date the TIL disclosure, or the date of overnight delivery and courier receipts /E-Sign: Sellers who deliver the documents through their approved E-Sign Technology software may deliver the TIL in this manner; Plaza Home Mortgage will review the audit trail accompanying the E-Disclosure loan file to determine the date received. Face-to-Face: Sellers may continue to deliver disclosures face-to-face. Plaza Home Mortgage will consider the TIL to be received by the borrower(s) on the date they sign and date the TIL disclosure. Presumption of Receipt: Sellers may continue to utilize the presumption of receipt three (3) business days from the date of mailing. The Seller must document the mail date, and Plaza Home Mortgage will consider the TIL to be received by the borrower(s) three business days from that mail date. Some examples of documentation include, but are not limited to, a Certificate of Mailing and postal receipt. Evidence of appraisal delivery/receipt Plaza Home Mortgage requires all appraisals for loans submitted for sale to comply with AIRs as a condition of purchase. Clients who sell loans to Plaza Home Mortgage must adopt the appropriate structure, and written policies and procedures to implement all state, federal and GSE appraisal requirements and certify, represent and warrant that their appraisal process and appraisal reports for all loans are in full compliance with rules and regulations. This includes the approach to appraiser selection and engagement. Correspondent Uses a Single Appraisal Management Company (AMC) for All Appraisal Orders AMC must be authorized by Lender to act on its behalf and the AMC is not acting on behalf of the seller for any third party originations. The AMC selects, retains and provides for payment of all compensation to the appraiser on Lender s behalf. The appraiser s client is the Lender (i.e. the appraiser selected and retained by the AMC identifies the Lender as the (Lender/Client) on the appraisal report). Substantive communications between any member of a Lender s loan production staff or a broker/originator and an appraiser or AMC that relates to or would have an impact on value are not allowed under the AIRs. Appraisal Delivery Requirements

on the date they sign and date the TIL disclosure.")

4 To comply with the Equal Credit Opportunity Act (ECOA) and Regulation B, Plaza requires that borrowers are provided a copy of any appraisal report concerning the borrower s property promptly upon completion and in any event no less than three days prior to the closing of the loan. The closing of the loan is defined at the date the security instrument and note are executed. The borrower may waive this three day requirement. Refer to the Appraisal Delivery Waiver paragraph at the end of this Section for additional information. Confirmation of Delivery of the Appraisal Either one or both of the following is acceptable as evidence of compliance with the appraisal delivery requirements: Documentation in the loan file indicating the date and method of delivery of the appraisal to the borrower and supporting that the appraisal was received by the borrower at least three business days prior to closing unless a waiver is provided. Refer to Appraisal Delivery Waiver in this Section for additional information. An acknowledgement of receipt of the appraisal signed by all borrowers at or before closing. The acknowledgement must include the following: 1. The names of the borrowers 2. The subject property address 3. A statement that the borrower received the appraisal at least three business days prior to closing. This can be accomplished with a generic statement that specifically states the appraisal was received three days prior to closing or the actual date it was received by the borrower, which must be a date at least three (3) business days prior to the loan closing. 4. Must be signed and dated by all borrowers. POA signature is acceptable if other documents were executed in the manner and it is properly documented. Plaza Home Mortgage reviews loans prior to purchase to ensure compliance with AIRs. In connection with this review, Plaza Home Mortgage considers a variety of factors, including the following: 1. Does the Lender/Client name on the appraisal match the lender of the loan? 2. Does the loan file include documentation showing the date, method of delivery, and delivery date of the appraisal report to the borrower (if known)? Notes: Mail delivery is calculated using the following: o Include Monday through Saturday o Include both the day mailed and the day delivered o Exclude Sunday and legal holidays.

5 Examples: o First Class Mail, and faxed deliveries are deemed received the third day after mailing, including the date mailed. For example, a package mailed on Wednesday (day one) is deemed received on Friday (day three). o Overnight Mail is deemed received the day after the package is sent. o Hand delivered is deemed received on the delivery date. o Does the date and the method of delivery in the loan file evidence that the borrower received a copy of the appraisal report, at least three business days prior to loan closing? o Note: Sundays and legal holidays may not be included in the three business day calculation. However, all of the following may be included in the three business day calculation: o The appraisal delivery day o The loan closing (document execution) day o Saturday Example 1 Over an average week: The borrower receives the appraisal on Monday. Monday is counted as day one, Tuesday is day two, Wednesday is day three, and the loan may close (documents executed) on or after Wednesday. Example 2 Including a weekend: The borrower receives a copy of the appraisal on Friday. Friday is day one, Saturday is day two, Monday is day three, and the loan may close (documents executed) on or after Monday. Example 3 Including a legal holiday: The borrower receives a copy of the appraisal on Friday. Friday is day one, Saturday is day two, Monday is a legal holiday, Tuesday is day three, and the loan may close (documents executed) on or after Tuesday. o Does the file contain evidence that all appraisals, including any review appraisal (if an additional appraisal or appraisal review was used by the Client to underwrite the loan), were received by the borrower at least three business days prior to loan closing? See examples above. o If the borrower elected to waive the three-day requirement for receiving a copy of the appraisal, does the file contain documentation that confirms the borrower s waiver of this three-day requirement? o Does the loan file contain the Lender Acknowledgment or other certification that the lender s appraisal process and the appraisal are compliant?

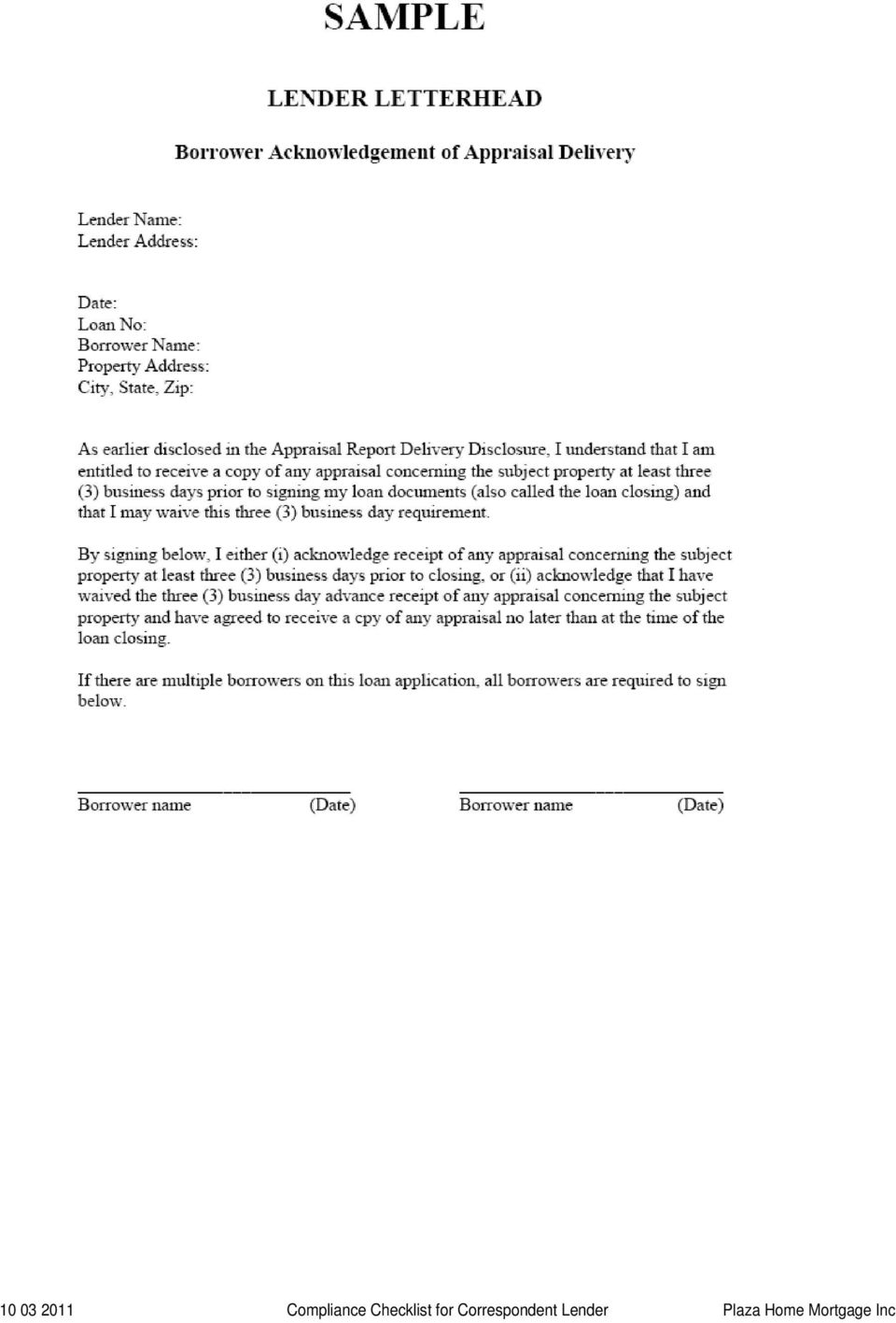

6 Appraisal Delivery Waiver AIR allows the borrower to waive the three business day delivery requirement. Appraisal delivery waivers are only to be used in the event that the timing of the appraisal completion conflicts with meeting the required delivery time frame based on the scheduled closing date. Use of waivers is subject to the following conditions: 1. The practice of requirement a blanket waiver for the three business day delivery requirement on all loans is unacceptable. 2. The Appraisal Receipt Waiver must be executed by the borrower at least 3 business days prior to closing. 3. In all circumstances, the date and method of delivery of each appraisal to the borrower, even if delivered by hand at closing, must be documented in the delivered loan file. Appraisal delivery waivers that do not meet the above criteria will result in the loan being ineligible for purchase by Plaza Home Mortgage. Appraisal Form Samples Plaza Home Mortgage requires that Clients adopt appropriate disclosures to ensure AIR awareness and compliance by all parties connected to the origination of loans and to the appraisal process. To assist clients with this Plaza Home Mortgage has developed the following forms to assist clients in their compliance. o Appraisal Report Delivery Disclosure o Appraisal Delivery Letter to Borrower o Borrower Acknowledgement of Appraisal Delivery o Lender Acknowledgement o Appraisal Receipt Waiver

7 Date: Borrower Name: Loan No: Case No: Property Address: SAMPLE LENDER LETTERHEAD Appraisal Report Delivery Disclosure If we used an appraisal report in connection with your mortgage loan application, you are entitled to receive a copy of the appraisal report at least three business days prior to your loan closing. While we try to provide you with the appraisal reports in a timely manner, there may be times when it is not feasible. In that case, if you wish to exercise your right to waive the three business day review, you must execute the waiver form at least three business days prior to loan closing. We will still provide you with a copy of the appraisal report no later than loan closing. You will not be required to pay an additional amount to us to receive a copy of the appraisal report. Any appraisal report used in connection with your loan application was prepared solely for our use in evaluating a request for an extension of credit. The appraisal should not be relied upon by any other person or entity. We make no express or implied representation or warranty of any kind, and we expressly disclaim any liability to any person or entity with respect to the property valuation.

8 SAMPLE LENDER LETTERHEAD Appraisal Delivery Letter to Borrower [Lender Name] [Lender Address] [Borrower Name] [Borrower Street Address] [Borrower City, State, and Zip] Date: [date] Method of Delivery [1st Class Mail, Overnight Delivery, , Facsimile, etc.] Dear Borrower: In compliance with the Fannie Mae, Freddie Mac, HUD and Dodd-Frank Act Appraisal Independence Requirements (AIRs), enclosed is a copy of the appraisal report(s) or valuation that may be used in connection with your current loan application. To comply with our lending policies, we may provide you with multiple appraisal reports for the following reasons: 1) our underwriting policies require more than one appraisal to evaluate your loan application; 2) our appraisal quality process produced a review appraisal report in addition to the originally ordered appraisal report; or 3) we received a request for reconsideration of value from you or on your behalf resulting in a new appraisal report or a revised value on your originally ordered appraisal report. Please note that at this time we may not have fully determined the acceptability of the enclosed appraisal(s) or valuation for use in connection with your loan application. The appraisal(s) or valuation used in connection with your loan application was or were prepared solely for our use in evaluating your loan application. The appraisal(s) or valuation should not be relied upon by any other person or entity. We make no express or implied representation or warranty of any kind, and we expressly disclaim any liability to any person or entity with respect to the appraisal(s) or valuation. Please also be advised that an appraiser must follow certain professional appraisal standards and is not allowed to discuss the appraisal(s) or valuation with you or provide a copy directly to you. If we used an appraisal report(s) or valuation in connection with your mortgage loan application you are entitled to receive a copy of the appraisal report(s) or valuation at least three business days prior to your loan closing. While we try to provide you with the appraisal report(s) or valuation in a timely manner, there may be times when it is not feasible. In that case, if you wish to exercise your right to waive the three business day review, you must execute the waiver from at least three business days prior to loan closing. We will still provide you with a copy of the appraisal report(s) or valuation no later than loan closing. You will not be required to pay an additional amount to us to receive a copy of the appraisal report.

![] Dear Borrower: In compliance with the Fannie Mae, Freddie Mac, HUD and Dodd-Frank Act Appraisal Independence Requirements (AIRs), enclosed is a copy of the appraisal report(s) or valuation that may](/docs-images/43/14187505/images/page_8.jpg "be used in connection with your current loan application.")

9

10 Borrower(s) Name: Property Address: City, State, Zip: Lender Acknowledgement SAMPLE PROVIDE ON LENDER LETTERHEAD Lender acknowledges that it complies with all Fannie Mae, Freddie Mac, HUD and Dodd-Frank Appraiser Independence Requirements ( AIRs ) that are effective 4/1/11. The Lender has developed and implemented the structure, policies and procedures required in order to ensure that all residential mortgage loans are in compliance with the AIRs, and that all appraisals used for those mortgages, were obtained in a manner consistent with the AIR requirements. Specifically, in addition to the above acknowledgment, as to this Loan, Lender acknowledges adherence to the following statements: No mortgage broker that originates mortgage loans on behalf of Lender ( Mortgage Broker ) and no member of Lender s sales or loan production staff, as well as any other member of Lender's staff who is likewise prohibited under the AIRs, played any role in selecting, retaining, recommending, or influencing the selection of an appraiser. No Mortgage Broker and no member of Lender s sales or loan production staff, as well as any other member of Lender's staff who is likewise prohibited under the AIRs, had any substantive communications with an appraiser or a designated and authorized appraisal management company ("AMC") of Lender relating to or having an impact on valuation, including ordering the appraisal, managing the appraisal assignment, or disputing any aspect of an appraisal. Lender has not provided a list of approved appraisers or AMCs to a Mortgage Broker or any member of Lender's sales or loan production staff, including any member of Lender's staff who is likewise prohibited under the AIRs. Lender has not allowed a Mortgage Broker to select a Lender designated or authorized AMC or an appraiser. However, a Lender may direct a Mortgage Broker to contact a single AMC, to initiate a request for an appraisal, provided that Lender has specifically authorized and designated the single AMC to act on its behalf and not on behalf of the Mortgage Broker. The appraiser was engaged directly by the Lender through it s designated and authorized AMC. The Lender certifies that neither the appraiser nor the AMC have any financial or other interest in the property or credit transaction. No Mortgage Broker, borrower, property seller, or real estate agent compensated in any manner, the appraiser. Lender s name appears on the appraisal as the Lender/Client. Lender has provided to the borrower a copy of any and all appraisals that were used to establish value for lending purposes in connection with the underwriting of the loan not less than three (3) business days prior to the loan closing, whether or not credit was granted or denied Lender maintains in the loan file a copy of the dated appraisal report and cover letter, including the method of delivery and date of delivery. This Acknowledgment by Lender as to the above-referenced Loan is a certification, representation and warranty of Lender and is incorporated into the Loan Purchase Agreement and Seller s Guide, effective as of the date specified below. Acknowledgment By: Lender Name: (Signature) Duly authorized Officer or Manager of Lender Name Title Date

CORRESPONDENT SELLER GUIDE

SECTION 1.0: INTRODUCTION TO CORRESPONDENT LENDING... 5 1.1 Eligibility...5 1.2 Regulatory Compliance...5 1.3 Submission Process...5 1.4 Loan Set Up...5 1.5 Rate Lock and Commitment Term...6 1.6 Fee Schedule...6

SECTION 1.0: INTRODUCTION TO CORRESPONDENT LENDING... 5 1.1 Eligibility...5 1.2 Regulatory Compliance...5 1.3 Submission Process...5 1.4 Loan Set Up...5 1.5 Rate Lock and Commitment Term...6 1.6 Fee Schedule...6

Appraiser Independence Requirements Frequently Asked Questions (FAQs) November 2010

November 2010") Appraiser Independence Requirements Frequently Asked Questions (FAQs) November 2010 The Appraiser Independence Requirements (AIR) were developed by Fannie Mae, the Federal Housing Finance Agency (FHFA),

Appraiser Independence Requirements Frequently Asked Questions (FAQs) November 2010 The Appraiser Independence Requirements (AIR) were developed by Fannie Mae, the Federal Housing Finance Agency (FHFA),

Home Valuation Code of Conduct Frequently Asked Questions (FAQs) Updated March 2010

Updated March 2010") Home Valuation Code of Conduct Frequently Asked Questions (FAQs) Updated March 2010 To help enhance the integrity of the home appraisal process in the mortgage finance industry, in March 2008, Fannie Mae

Home Valuation Code of Conduct Frequently Asked Questions (FAQs) Updated March 2010 To help enhance the integrity of the home appraisal process in the mortgage finance industry, in March 2008, Fannie Mae

Update on CFPB s TILA- RESPA Integrated Disclosure Rule

Update on CFPB s TILA- RESPA Integrated Disclosure Rule Mortgage Bankers Ruth A. Dillingham, Special Counsel First American Title Insurance Company This presentation is for informational purposes only

Update on CFPB s TILA- RESPA Integrated Disclosure Rule Mortgage Bankers Ruth A. Dillingham, Special Counsel First American Title Insurance Company This presentation is for informational purposes only

Overview The Regulation The Loan Estimate (LE) The Closing Disclosure (CD) Loan Estimate (LE) Application Date LE Responsibility

The Closing Disclosure (CD) Loan Estimate (LE) Application Date LE Responsibility") To support your preparation efforts when implementing the TILA-RESPA Integrated Disclosure (TRID) rule effective for applications dated on or after October 3, 2015, we have created this Helpful Tips for

To support your preparation efforts when implementing the TILA-RESPA Integrated Disclosure (TRID) rule effective for applications dated on or after October 3, 2015, we have created this Helpful Tips for

FIRST COMMUNITY MORTGAGE, INC.

FIRST COMMUNITY MORTGAGE, INC. REG Z & TRUTH IN LENDING ACT Background: On July 30, 2008 Congress enacted the Housing and Economic Recovery Act (HERA) which contained a section called the Mortgage Disclosure

FIRST COMMUNITY MORTGAGE, INC. REG Z & TRUTH IN LENDING ACT Background: On July 30, 2008 Congress enacted the Housing and Economic Recovery Act (HERA) which contained a section called the Mortgage Disclosure

A New Era in Closings CFPB s Final Rule for Integrated Mortgage Disclosures. Michelle L. Korsmo Chief Executive Officer Steven Gottheim Counsel

A New Era in Closings CFPB s Final Rule for Integrated Mortgage Disclosures Michelle L. Korsmo Chief Executive Officer Steven Gottheim Counsel Agenda Basics: Why We re Here Final Rule The New Forms Evaluating

A New Era in Closings CFPB s Final Rule for Integrated Mortgage Disclosures Michelle L. Korsmo Chief Executive Officer Steven Gottheim Counsel Agenda Basics: Why We re Here Final Rule The New Forms Evaluating

TILA-RESPA Integrated Disclosure (TRID) Correspondent Division. Overview. Loan Estimate (LE) Key points. Topic The Regulation

Correspondent Division. Overview. Loan Estimate (LE) Key points. Topic The Regulation") Overview The Regulation The Consumer Financial Protection Bureau (CFPB) issued a final rule amending Regulation Z (Truth in Lending Act) and Regulation X (Real Estate Settlement Procedures Act) to integrate

Overview The Regulation The Consumer Financial Protection Bureau (CFPB) issued a final rule amending Regulation Z (Truth in Lending Act) and Regulation X (Real Estate Settlement Procedures Act) to integrate

VA Authorized Agent Agreement

VA Authorized Agent Agreement This VA Authorized Agent Agreement (the Agreement ), entered into this day of, 20 (the Effective Date ) by and between Data Mortgage Inc., d/b/a Essex Mortgage ( Lender )

VA Authorized Agent Agreement This VA Authorized Agent Agreement (the Agreement ), entered into this day of, 20 (the Effective Date ) by and between Data Mortgage Inc., d/b/a Essex Mortgage ( Lender )

Equal Credit Opportunity Act (ECOA) Valuations Rule

Valuations Rule") MAY 2, 2013 Equal Credit Opportunity Act (ECOA) Valuations Rule SMALL ENTITY COMPLIANCE GUIDE 1 Table of Contents 1. Introduction... 5 I. What is the purpose of this guide?... 6 II. Who should read this

MAY 2, 2013 Equal Credit Opportunity Act (ECOA) Valuations Rule SMALL ENTITY COMPLIANCE GUIDE 1 Table of Contents 1. Introduction... 5 I. What is the purpose of this guide?... 6 II. Who should read this

When do I have to start following the TILA-RESPA rule and using the new Integrated Disclosures?

............................................................................................. Overview of the TILA-RESPA Rule.............................................................................................

............................................................................................. Overview of the TILA-RESPA Rule.............................................................................................

The New Mortgage Servicing Rules. FMS East Coast Regional Conference September 17, 2013

The New Mortgage Servicing Rules FMS East Coast Regional Conference September 17, 2013 What are the new Mortgage Servicing Rules? Ability to Repay/Qualified Mortgage Rule 2013 HOEPA Rule Loan Originator

The New Mortgage Servicing Rules FMS East Coast Regional Conference September 17, 2013 What are the new Mortgage Servicing Rules? Ability to Repay/Qualified Mortgage Rule 2013 HOEPA Rule Loan Originator

CFPB THE NEW DISCLOSURE FORMS AND REQUIREMENTS BE READY!!

CFPB THE NEW DISCLOSURE FORMS AND REQUIREMENTS BE READY!! CELIA C. FLOWERS FLOWERS DAVIS, P.L.L.C. and EAST TEXAS TITLE COMPANY Tyler, Texas 75701 TILA and RESPA History 2012 TEXAS LAND TITLE INSTITUTE

CFPB THE NEW DISCLOSURE FORMS AND REQUIREMENTS BE READY!! CELIA C. FLOWERS FLOWERS DAVIS, P.L.L.C. and EAST TEXAS TITLE COMPANY Tyler, Texas 75701 TILA and RESPA History 2012 TEXAS LAND TITLE INSTITUTE

Principal Lending Manager Education Curriculum Outline 40 Hours

Principal Lending Manager Education Curriculum Outline 40 Hours Utah Division of Real Estate PO Box 146711 Salt Lake City, UT 84114-6711 Subject Matter Number of Hours 1. General Mortgage Industry Knowledge

Principal Lending Manager Education Curriculum Outline 40 Hours Utah Division of Real Estate PO Box 146711 Salt Lake City, UT 84114-6711 Subject Matter Number of Hours 1. General Mortgage Industry Knowledge

TRID FAQ TILA/RESPA Integrated Disclosure Frequently Asked Questions

TRID FAQ TILA/RESPA Integrated Disclosure Frequently Asked Questions 242 W. SUNSET, STE.201 SAN ANTONIO, TX 78209 210-828-5844 DOCS@BAIRDLAW.COM Table of Contents GENERAL QUESTIONS... 3 1. What is TRID?...

TRID FAQ TILA/RESPA Integrated Disclosure Frequently Asked Questions 242 W. SUNSET, STE.201 SAN ANTONIO, TX 78209 210-828-5844 DOCS@BAIRDLAW.COM Table of Contents GENERAL QUESTIONS... 3 1. What is TRID?...

Kentucky Housing Corporation Closing Agent Agreement

Kentucky Housing Corporation Closing Agent Agreement Kentucky Housing Corporation ( KHC ) has established required standards of performance and conduct for any closing agent ( Closing Agent ) conducting

Kentucky Housing Corporation Closing Agent Agreement Kentucky Housing Corporation ( KHC ) has established required standards of performance and conduct for any closing agent ( Closing Agent ) conducting

Rules and Regulations

23289 Rules and Regulations Federal Register Vol. 74, No. 95 Tuesday, May 19, 2009 This section of the FEDERAL REGISTER contains regulatory documents having general applicability and legal effect, most

23289 Rules and Regulations Federal Register Vol. 74, No. 95 Tuesday, May 19, 2009 This section of the FEDERAL REGISTER contains regulatory documents having general applicability and legal effect, most

ADVISORY MEMORANDUM KATHY BURNS, DIRECTOR OF HOMEOWNERSHIP COMPLIANCE DOCUMENTATION REQUIREMENTS

ADVISORY MEMORANDUM TO: FROM: ALL MASSHOUSING LENDERS KATHY BURNS, DIRECTOR OF HOMEOWNERSHIP DATE: NOVEMBER 15, 2010 RE: COMPLIANCE DOCUMENTATION REQUIREMENTS The purpose of this Advisory is to provide

ADVISORY MEMORANDUM TO: FROM: ALL MASSHOUSING LENDERS KATHY BURNS, DIRECTOR OF HOMEOWNERSHIP DATE: NOVEMBER 15, 2010 RE: COMPLIANCE DOCUMENTATION REQUIREMENTS The purpose of this Advisory is to provide

A Primer for a New Era in Closings: For loan applications received beginning August 1, 2015 some info courtesy of ALTA

A Primer for a New Era in Closings: For loan applications received beginning August 1, 2015 some info courtesy of ALTA A New Era in Closings Applicable Loans Final rule applies to most consumer mortgages,

A Primer for a New Era in Closings: For loan applications received beginning August 1, 2015 some info courtesy of ALTA A New Era in Closings Applicable Loans Final rule applies to most consumer mortgages,

CLARIFICATION OF MAJOR CHANGES. Integrated Mortgage Disclosures

CLARIFICATION OF MAJOR CHANGES Integrated Mortgage Disclosures One of the mortgage industry s most anticipated provisions of the Dodd-Frank Act has been the integration of the Truth-in-Lending Act (TILA)

CLARIFICATION OF MAJOR CHANGES Integrated Mortgage Disclosures One of the mortgage industry s most anticipated provisions of the Dodd-Frank Act has been the integration of the Truth-in-Lending Act (TILA)

Regulation Z Appraisals for Higher Priced Mortgage Loans

Regulation Z Appraisals for Higher Priced Mortgage Loans (12 CFR 1026.35 (c)) October 31, 201 3 In January 2013, the Consumer Financial Protection Bureau and the federal financial institution regulators

Regulation Z Appraisals for Higher Priced Mortgage Loans (12 CFR 1026.35 (c)) October 31, 201 3 In January 2013, the Consumer Financial Protection Bureau and the federal financial institution regulators

Table of Contents. Table of Contents... 1. Chapter 1 Introduction... 3. 1.1 Goals & Objectives... 3 1.2 Required Review... 3 1.3 Applicability...

[ Client]... 1 Chapter 1 Introduction... 3 1.1 Goals & Objectives... 3 1.2 Required Review... 3 1.3 Applicability... 4 Chapter 2 Accountability and Monitoring... 5 2.1 Internal Controls... 5 Chapter 3

[ Client]... 1 Chapter 1 Introduction... 3 1.1 Goals & Objectives... 3 1.2 Required Review... 3 1.3 Applicability... 4 Chapter 2 Accountability and Monitoring... 5 2.1 Internal Controls... 5 Chapter 3

HERE ARE FIVE THINGS YOU WILL NEED TO KNOW BEFORE THE NEW RULES TAKE EFFECT OCTOBER 3, 2015

5 THINGS TO KNOW BEFORE OCTOBER 3RD, 2015 As a result of the 20 financial meltdown, the Consumer Financial Protection Bureau (CFPB) has published a new set of game changing rules and forms that will impact

5 THINGS TO KNOW BEFORE OCTOBER 3RD, 2015 As a result of the 20 financial meltdown, the Consumer Financial Protection Bureau (CFPB) has published a new set of game changing rules and forms that will impact

Homeownership Counseling (12 CFR 1024.20)

") (12 CFR 1024.20) The Consumer Financial Protection Bureau s (CFPB) new mortgage rules include new requirements for providing federally-related mortgage loan applicants with a list of homeownership counseling

(12 CFR 1024.20) The Consumer Financial Protection Bureau s (CFPB) new mortgage rules include new requirements for providing federally-related mortgage loan applicants with a list of homeownership counseling

A Primer on the New CFPB Regulations Governing Residential Closings. Navigating the New Forms (Loan Estimate and Closing Disclosure.

A Primer on the New CFPB Regulations Governing Residential Closings. Navigating the New Forms (Loan Estimate and Closing Disclosure.) For loan applications received beginning October 3, 2015. Disclaimer:

A Primer on the New CFPB Regulations Governing Residential Closings. Navigating the New Forms (Loan Estimate and Closing Disclosure.) For loan applications received beginning October 3, 2015. Disclaimer:

BROKER APPLICATION CHECKLIST

Thank you for your interest in becoming an approved broker with LDWholesale, a division of loandepot, LLC. Our application process is fast and simple: 1. Complete the following templates*, sign and print.

Thank you for your interest in becoming an approved broker with LDWholesale, a division of loandepot, LLC. Our application process is fast and simple: 1. Complete the following templates*, sign and print.

BROKER AGREEMENT. NOW THEREFORE, in consideration of promises, covenants and agreements hereinafter contain, the parties agree as follows:

THIS AGREEMENT is entered into in the State of California this day of 2006, between Crestline Funding Corporation, hereinafter referred to as Crestline Funding, and, hereinafter referred to as Broker.

THIS AGREEMENT is entered into in the State of California this day of 2006, between Crestline Funding Corporation, hereinafter referred to as Crestline Funding, and, hereinafter referred to as Broker.

GLOSSARY OF TERMS. Amortization Repayment of a debt in regular installments of principal and interest, rather than interest only payments

GLOSSARY OF TERMS Ability to Repay (ATR) The Ability to Repay rule protects consumers from taking on mortgages that exceed their financial means, by mandating the documentation / proof of income and assets.

GLOSSARY OF TERMS Ability to Repay (ATR) The Ability to Repay rule protects consumers from taking on mortgages that exceed their financial means, by mandating the documentation / proof of income and assets.

TRID. What are the Timing Requirements for Revisions to a Loan Estimate?

TRID What is TRID? TRID is an acronym for TILA- RESPA Integrated Disclosure (also referred to as the TILA-RESPA Rule) and applies to most closed-end Borrower credit transactions secured by real property.

TRID What is TRID? TRID is an acronym for TILA- RESPA Integrated Disclosure (also referred to as the TILA-RESPA Rule) and applies to most closed-end Borrower credit transactions secured by real property.

Home Valuation Code of Conduct

I. Appraiser Independence Safeguards Home Valuation Code of Conduct A. An appraiser must be, at a minimum, licensed or certified by the state in which the property to be appraised is located. B. No employee,

I. Appraiser Independence Safeguards Home Valuation Code of Conduct A. An appraiser must be, at a minimum, licensed or certified by the state in which the property to be appraised is located. B. No employee,

Advanced AMC, Inc. Appraiser Services Agreement (Independent Contractor Agreement)

") Advanced AMC, Inc.. Appraiser Services Agreement (Independent Contractor Agreement) This Appraiser Services Agreement ( Agreement ) shall be effective as of the Effective Date by and between Advanced AMC,

Advanced AMC, Inc.. Appraiser Services Agreement (Independent Contractor Agreement) This Appraiser Services Agreement ( Agreement ) shall be effective as of the Effective Date by and between Advanced AMC,

Section 1.35 Compliance Overview

Section 1.35 Compliance Overview In This Section This section contains the following topics: Overview... 2 Related Bulletins... 2 Nationwide Mortgage Licensing System Registry (S.A.F.E. Act)... 3 Nationwide

Section 1.35 Compliance Overview In This Section This section contains the following topics: Overview... 2 Related Bulletins... 2 Nationwide Mortgage Licensing System Registry (S.A.F.E. Act)... 3 Nationwide

TILA-RESPA INTEGRATED DISCLOSURE (TRID) AT A GLANCE COPYRIGHT 2015 AMERICAN FINANCIAL RESOURCES, INC. ALL RIGHTS RESERVED

AT A GLANCE COPYRIGHT 2015 AMERICAN FINANCIAL RESOURCES, INC. ALL RIGHTS RESERVED") TILA-RESPA INTEGRATED DISCLOSURE (TRID) AT A GLANCE Last Revised: 8/28/2015 TABLE OF CONTENTS What is TRID?...3 Forms...4-7 - Loan Estimate - Closing Disclosure - Change of Circumstance Delivery Methods

TILA-RESPA INTEGRATED DISCLOSURE (TRID) AT A GLANCE Last Revised: 8/28/2015 TABLE OF CONTENTS What is TRID?...3 Forms...4-7 - Loan Estimate - Closing Disclosure - Change of Circumstance Delivery Methods

Break Out Session: Mortgage Loan Underwriting and Pricing

Break Out Session: Mortgage Loan Underwriting and Pricing Agenda Ability to Repay (ATR)/Qualified Mortgages (QMs) Effective Date: Applications received on or after January 10, 2014 2013 Home Ownership

Break Out Session: Mortgage Loan Underwriting and Pricing Agenda Ability to Repay (ATR)/Qualified Mortgages (QMs) Effective Date: Applications received on or after January 10, 2014 2013 Home Ownership

How To Write A Disclosure Form

Office of Consumer Protection Truth-In-Lending Real Estate Settlement Procedures Act Integrated Disclosures Webinar February 11, 2015 The information contained in this presentation is for informational

Office of Consumer Protection Truth-In-Lending Real Estate Settlement Procedures Act Integrated Disclosures Webinar February 11, 2015 The information contained in this presentation is for informational

Are you a Table Funding Partner? Are you a Correspondent?

Thank you for joining RenasantConnect s appraisal ordering service for Table Funding Partners and Correspondent Lenders. Renasant Bank and SettlementOne Valuation are pleased to present you with tailored

Thank you for joining RenasantConnect s appraisal ordering service for Table Funding Partners and Correspondent Lenders. Renasant Bank and SettlementOne Valuation are pleased to present you with tailored

Purchase Funded (Delegated UW)

") Lender: Lender Requirements: $250 Application Processing Fee (Non Refundable) Minimum 2 years in business (Housing Finance Agency recommendation needed if less than 2 years) Minimum 2 years history (2

Lender: Lender Requirements: $250 Application Processing Fee (Non Refundable) Minimum 2 years in business (Housing Finance Agency recommendation needed if less than 2 years) Minimum 2 years history (2

Broker Quality Control Policy Manual Table of Contents. Table of Contents. [Sample Client]

![Broker Quality Control Policy Manual Table of Contents. Table of Contents. [Sample Client]](/thumbs/40/20869026.jpg "Broker Quality Control Policy Manual Table of Contents. Table of Contents. [Sample Client]") TABLE OF CONTENTS... 1 CHAPTER 1 INTRODUCTION... 3 1.1 GOALS AND OBJECTIVES... 3 1.2 REQUIRED REVIEW... 3 1.3 APPLICABILITY... 3 CHAPTER 2 ACCOUNTABILITY AND MONITORING... 4 2.1 INTERNAL CONTROLS... 4

TABLE OF CONTENTS... 1 CHAPTER 1 INTRODUCTION... 3 1.1 GOALS AND OBJECTIVES... 3 1.2 REQUIRED REVIEW... 3 1.3 APPLICABILITY... 3 CHAPTER 2 ACCOUNTABILITY AND MONITORING... 4 2.1 INTERNAL CONTROLS... 4

CFPB Integrated Mortgage Disclosures

CFPB Integrated Mortgage Disclosures Today s Goal To help you not only understand the rule changes, but make sure you have the tools, resources and support to take action to implement in your credit union

CFPB Integrated Mortgage Disclosures Today s Goal To help you not only understand the rule changes, but make sure you have the tools, resources and support to take action to implement in your credit union

Fair Lending and HMDA Compliance

Office of Consumer Protection Consumer Compliance Policy & Outreach Fair Lending and HMDA Compliance February 20, 2015 The information contained in this presentation is for informational purposes only

Office of Consumer Protection Consumer Compliance Policy & Outreach Fair Lending and HMDA Compliance February 20, 2015 The information contained in this presentation is for informational purposes only

3/5/2015. Next Steps to prepare for compliance

NEW CLOSING DISCLOSURE FORMS Next Steps to prepare for compliance Presented by: Summary of where we are with the implementation of the new closing disclosure form promulgated by the CFPB Summary so far

NEW CLOSING DISCLOSURE FORMS Next Steps to prepare for compliance Presented by: Summary of where we are with the implementation of the new closing disclosure form promulgated by the CFPB Summary so far

MORTGAGE BROKER AGREEMENT

MORTGAGE BROKER AGREEMENT This Mortgage Broker Agreement (the "Agreement") is entered into by and between: ST. CLOUD MORTGAGE, a California Corporation (the "Lender"), and (the "Mortgage Broker") as of

MORTGAGE BROKER AGREEMENT This Mortgage Broker Agreement (the "Agreement") is entered into by and between: ST. CLOUD MORTGAGE, a California Corporation (the "Lender"), and (the "Mortgage Broker") as of

TILA-RESPA INTEGRATED MORTGAGE DISCLOSURES

TILA-RESPA INTEGRATED MORTGAGE DISCLOSURES Explaining the New Rule History Timing Purpose Coverage? Changes Definition of an Application Loan Estimate Closing Disclosure Variations/Tolerances 5 Things

TILA-RESPA INTEGRATED MORTGAGE DISCLOSURES Explaining the New Rule History Timing Purpose Coverage? Changes Definition of an Application Loan Estimate Closing Disclosure Variations/Tolerances 5 Things

Brief Walk Through of TRID. Presented by: Scott Meerstein MGIC Inside Sales

Brief Walk Through of TRID Presented by: Scott Meerstein MGIC Inside Sales The information presented in this presentation is for general information only, and is based on guidelines and practices generally

Brief Walk Through of TRID Presented by: Scott Meerstein MGIC Inside Sales The information presented in this presentation is for general information only, and is based on guidelines and practices generally

Dodd Frank Mortgage Reform 2014

Dodd Frank Mortgage Reform 2014 Business Partner Deck v1 12.16.13 Overview RULE EFFECTIVE DATE Loan Originator Compensation - TILA Loans closed and paid on or after 1/01/14 Ability to Repay/Qualified Mortgages

Dodd Frank Mortgage Reform 2014 Business Partner Deck v1 12.16.13 Overview RULE EFFECTIVE DATE Loan Originator Compensation - TILA Loans closed and paid on or after 1/01/14 Ability to Repay/Qualified Mortgages

Appraiser Application Checklist

Appraiser Application Checklist Application Requirements: (please initial all blanks) Complete the online sign up process on our website, www.eamc1.com, and provide the following: Basic Company Information

Appraiser Application Checklist Application Requirements: (please initial all blanks) Complete the online sign up process on our website, www.eamc1.com, and provide the following: Basic Company Information

Community bankers. regulatory environment. grow mortgage revenue. in today s ever-changing, helping community banks

Community bankers helping community banks grow mortgage revenue in today s ever-changing, regulatory environment. We re community bankers just like you. Triumph Mortgage partners with community banks of

Community bankers helping community banks grow mortgage revenue in today s ever-changing, regulatory environment. We re community bankers just like you. Triumph Mortgage partners with community banks of

First Source Capital Mortgage, Inc.

First Source Capital Mortgage, Inc. Please submit the following items along with your application package to expedite your approval process. If you have any questions or need additional information please

First Source Capital Mortgage, Inc. Please submit the following items along with your application package to expedite your approval process. If you have any questions or need additional information please

CFPB Mortgage Amendments. Get Caught Up!

CFPB Mortgage Amendments Get Caught Up! Agenda HPML Appraisal Requirements High Cost Mortgage QM Points and Fees QM Cure Provision HPML Escrow Requirements HMDA Revisions Loan Estimate Form Closing Disclosure

CFPB Mortgage Amendments Get Caught Up! Agenda HPML Appraisal Requirements High Cost Mortgage QM Points and Fees QM Cure Provision HPML Escrow Requirements HMDA Revisions Loan Estimate Form Closing Disclosure

20 Hour Mortgage Loan Originator SAFE Comprehensive Course Number: 1013 Provider ID: 1400024

20 Hour Mortgage Loan Originator SAFE Comprehensive Course Number: 1013 Provider ID: 1400024 Day 1 Agenda (1.0 hour) Session 1 - Part I: (1.0 hour) Session 1 - Part II: (1.5 hours) Session 2: Mortgage

20 Hour Mortgage Loan Originator SAFE Comprehensive Course Number: 1013 Provider ID: 1400024 Day 1 Agenda (1.0 hour) Session 1 - Part I: (1.0 hour) Session 1 - Part II: (1.5 hours) Session 2: Mortgage

Guide to Completing the Closing Disclosure The following list highlights requirements needed to complete each section of the Closing Disclosure (CD).

.") Guide to Completing the Closing Disclosure The following list highlights requirements needed to complete each section of the Closing Disclosure (CD). Page 1 Closing Information Date Issued Date the CD

Guide to Completing the Closing Disclosure The following list highlights requirements needed to complete each section of the Closing Disclosure (CD). Page 1 Closing Information Date Issued Date the CD

Real Estate Lending A Document Compliance Overview. Judi Mortenson Lending Manager

Real Estate Lending A Document Compliance Overview Judi Mortenson Lending Manager Agenda Introduction Goal of todays session: Create awareness of the documents and signatures that are required for real

Real Estate Lending A Document Compliance Overview Judi Mortenson Lending Manager Agenda Introduction Goal of todays session: Create awareness of the documents and signatures that are required for real

RESPA REFORM. J. Tom Minor Karen W. Ingle

RESPA REFORM J. Tom Minor Karen W. Ingle RESPA Reform Purpose of the RESPA reform Protect consumers from unnecessarily high settlement costs Improve and standardize the Good Faith Estimate Provide an easy

RESPA REFORM J. Tom Minor Karen W. Ingle RESPA Reform Purpose of the RESPA reform Protect consumers from unnecessarily high settlement costs Improve and standardize the Good Faith Estimate Provide an easy

November 6, 2012. The Honorable Richard Cordray Director Consumer Financial Protection Bureau 1700 G Street NW Washington, DC 20006-4702

November 6, 2012 The Honorable Richard Cordray Director Consumer Financial Protection Bureau 1700 G Street NW Washington, DC 20006-4702 Re: Integrated Mortgage Disclosures under the Real Estate Settlement

November 6, 2012 The Honorable Richard Cordray Director Consumer Financial Protection Bureau 1700 G Street NW Washington, DC 20006-4702 Re: Integrated Mortgage Disclosures under the Real Estate Settlement

ALTERATIONS, MODIFICATIONS OR AMENDMENTS ARE ACCEPTED TO THIS AGREEMENT.

TPO Approval Checklist For Business Purpose Loans ***(This Broker Package is for Brokers who will only be Brokering Commercial Real Estate Loans or Residential Business Purpose Loans)*** NO ALTERATIONS,

TPO Approval Checklist For Business Purpose Loans ***(This Broker Package is for Brokers who will only be Brokering Commercial Real Estate Loans or Residential Business Purpose Loans)*** NO ALTERATIONS,

Mission: to make markets for consumer financial products and services work for Americans.

TRID with Norman Roos, Robinson and Cole LLP William McCue, McCue Mortgage Company Lawrence Garfinkel, Hunt Leibert Jacobson P.C. Jeremy Potter, Norcom Mortgage Agenda Introduction Overview and Framework

TRID with Norman Roos, Robinson and Cole LLP William McCue, McCue Mortgage Company Lawrence Garfinkel, Hunt Leibert Jacobson P.C. Jeremy Potter, Norcom Mortgage Agenda Introduction Overview and Framework

TITLE I-RESIDENTIAL MORTGAGE LOAN ORIGINATION STANDARDS

TITLE I-RESIDENTIAL MORTGAGE LOAN ORIGINATION STANDARDS Residential Mortgage Origination: Adds a number of new regulations and requirements to mortgage loan originators. The bill requires originators to

TITLE I-RESIDENTIAL MORTGAGE LOAN ORIGINATION STANDARDS Residential Mortgage Origination: Adds a number of new regulations and requirements to mortgage loan originators. The bill requires originators to

The Federal Register published the proposed rule on August 23, 2012.

CFPB Issues Draft RESPA-TILA Proposed Rules On July 9, the Consumer Financial Protection Bureau ( Bureau or CFPB ) released draft proposed rules and model forms that combine the required disclosures under

CFPB Issues Draft RESPA-TILA Proposed Rules On July 9, the Consumer Financial Protection Bureau ( Bureau or CFPB ) released draft proposed rules and model forms that combine the required disclosures under

DEPARTMENT OF REGULATORY AGENCIES DIVISION OF REAL ESTATE MORTGAGE LOAN ORIGINATORS 4CCR 725-3. NOTICE OF PROPOSED RULEMAKING HEARING March 16, 2011

DEPARTMENT OF REGULATORY AGENCIES DIVISION OF REAL ESTATE MORTGAGE LOAN ORIGINATORS 4CCR 725-3 NOTICE OF PROPOSED RULEMAKING HEARING March 16, 2011 5-1-2 MORTGAGE LOAN ORIGINATOR DISCLOSURES Pursuant to

DEPARTMENT OF REGULATORY AGENCIES DIVISION OF REAL ESTATE MORTGAGE LOAN ORIGINATORS 4CCR 725-3 NOTICE OF PROPOSED RULEMAKING HEARING March 16, 2011 5-1-2 MORTGAGE LOAN ORIGINATOR DISCLOSURES Pursuant to

Utah Housing Corporation (UHC) Lender/Seller Participation Application

Lender/Seller Participation Application") Utah Housing Corporation (UHC) Lender/Seller Participation Application All Lenders/Sellers requesting to participate in UHC's Single Family Mortgage Loan Programs must complete this Application and submit

Utah Housing Corporation (UHC) Lender/Seller Participation Application All Lenders/Sellers requesting to participate in UHC's Single Family Mortgage Loan Programs must complete this Application and submit

4. ACCESS TO THE SITE

Service Agreement for Mortgage Lenders & Appraisers for compliance with the Appraisal Independence regulation included in the Dodd-Frank Wall Street Reform and Consumer Protection Act. This Service Agreement

Service Agreement for Mortgage Lenders & Appraisers for compliance with the Appraisal Independence regulation included in the Dodd-Frank Wall Street Reform and Consumer Protection Act. This Service Agreement

Policy Guidance on Supervisory and Enforcement Considerations Relevant to Mortgage

BILLING CODE: 4810-AM-P BUREAU OF CONSUMER FINANCIAL PROTECTION Policy Guidance on Supervisory and Enforcement Considerations Relevant to Mortgage Brokers Transitioning to Mini-Correspondent Lenders AGENCY:

BILLING CODE: 4810-AM-P BUREAU OF CONSUMER FINANCIAL PROTECTION Policy Guidance on Supervisory and Enforcement Considerations Relevant to Mortgage Brokers Transitioning to Mini-Correspondent Lenders AGENCY:

CUNA s COMPLIANCE HIGHLIGHTS

CUNA s COMPLIANCE HIGHLIGHTS TILA/RESPA INTEGRATED MORTGAGE DISCLOSURES For more than 30 years, Federal law has required lenders to provide two different disclosure forms to consumers applying for a mortgage.

CUNA s COMPLIANCE HIGHLIGHTS TILA/RESPA INTEGRATED MORTGAGE DISCLOSURES For more than 30 years, Federal law has required lenders to provide two different disclosure forms to consumers applying for a mortgage.

Chapter 5. How to Process VA Loans and Submit Them to VA Overview

Chapter 5. How to Process VA Loans and Submit Them to VA Overview In this Chapter This chapter contains the following topics. Topic Topic name See Page 1 Refinancing Loans 5-2 2 Processing Procedures 5-3

Chapter 5. How to Process VA Loans and Submit Them to VA Overview In this Chapter This chapter contains the following topics. Topic Topic name See Page 1 Refinancing Loans 5-2 2 Processing Procedures 5-3

8 Hour SAFE Comprehensive 2014 Mortgage Loan Originator Course Participant Guide

8 Hour SAFE Comprehensive 2014 Mortgage Loan Originator Course Participant Guide Presented by the Florida Association of Mortgage Brokers School 8 Hour SAFE Comprehensive 2014 Mortgage Loan Originator

8 Hour SAFE Comprehensive 2014 Mortgage Loan Originator Course Participant Guide Presented by the Florida Association of Mortgage Brokers School 8 Hour SAFE Comprehensive 2014 Mortgage Loan Originator

Overview. General Requirements

Truth in Lending Act Overview Congress passed legislation increasing the amount and type of credit information disclosed to the consumer through Title I of the Consumer Credit Protection Act of 1968, known

Truth in Lending Act Overview Congress passed legislation increasing the amount and type of credit information disclosed to the consumer through Title I of the Consumer Credit Protection Act of 1968, known

CFPB and Lenders. A presentation on the Consumer Financial Protection Bureau and its impact on the lending industry

CFPB and Lenders A presentation on the Consumer Financial Protection Bureau and its impact on the lending industry What is the Consumer Financial Protection Bureau (CFPB)? Independent agency of the United

CFPB and Lenders A presentation on the Consumer Financial Protection Bureau and its impact on the lending industry What is the Consumer Financial Protection Bureau (CFPB)? Independent agency of the United

CFPB Regulations. Review & Enforcement

CFPB Regulations Review & Enforcement Agenda Welcome Overview 2014 Regulations Loan Originator Compensation and Training, Certification, and Identifier Disclosure High-Cost/HOEPA Mortgage Loans & Homeownership

CFPB Regulations Review & Enforcement Agenda Welcome Overview 2014 Regulations Loan Originator Compensation and Training, Certification, and Identifier Disclosure High-Cost/HOEPA Mortgage Loans & Homeownership

CityLIFT Oakland/East Bay Program Overview Non-Approved Lender Participation Application

CityLIFT Oakland/East Bay Program Overview Non-Approved Lender Participation Application DUE BY: Monday, December 23, 2013, 5:00 pm. Dear Lender: The Unity Council Homeownership Center (TUC HOC) is administering

CityLIFT Oakland/East Bay Program Overview Non-Approved Lender Participation Application DUE BY: Monday, December 23, 2013, 5:00 pm. Dear Lender: The Unity Council Homeownership Center (TUC HOC) is administering

Completed Broker Application should be submitted to your MSC Account Executive. MSC Account Executive E-mail: Phone:

Broker Name: _ MSC Account Executive: Completed Broker Application should be submitted to your MSC Account Executive. MSC Account Executive E-mail: _ Phone: BROKER APPLICATON CHECKLIST All of the following

Broker Name: _ MSC Account Executive: Completed Broker Application should be submitted to your MSC Account Executive. MSC Account Executive E-mail: _ Phone: BROKER APPLICATON CHECKLIST All of the following

TILA/RESPA Integrated Disclosures. BRIAN A. NETTLEINGHAM Attorney/Shareholder Regulatory Compliance Group

TILA/RESPA Integrated Disclosures BRIAN A. NETTLEINGHAM Attorney/Shareholder Regulatory Compliance Group BACKGROUND Dodd-Frank Wall Street Reform Act Created the Consumer Financial Protection Bureau National

TILA/RESPA Integrated Disclosures BRIAN A. NETTLEINGHAM Attorney/Shareholder Regulatory Compliance Group BACKGROUND Dodd-Frank Wall Street Reform Act Created the Consumer Financial Protection Bureau National

MORTGAGE PARTICIPATING LENDER AGREEMENT

MORTGAGE PARTICIPATING LENDER AGREEMENT This Agreement, entered into this day of, by and between the South Dakota Housing Development Authority ( SDHDA ), 3060 East Elizabeth Street, Pierre, South Dakota,

MORTGAGE PARTICIPATING LENDER AGREEMENT This Agreement, entered into this day of, by and between the South Dakota Housing Development Authority ( SDHDA ), 3060 East Elizabeth Street, Pierre, South Dakota,

TILA-RESPA Integrated Mortgage Disclosures

TILA-RESPA Integrated Mortgage Disclosures Supreme Lending 2015 Distribution to the general public is prohibited. This is not considered an advertisement as defined by 12 CFR 226.2(a)(2). Supreme Lending

TILA-RESPA Integrated Mortgage Disclosures Supreme Lending 2015 Distribution to the general public is prohibited. This is not considered an advertisement as defined by 12 CFR 226.2(a)(2). Supreme Lending

CUNA s SUMMARY OF THE CFPB s MORTGAGE LENDING RULES Spring 2013

MANDATORY ESCROW ACCOUNTS Effective: June 1, 2013 REGULATION Requires escrow accounts be maintained for five years (rather than the current one year) for higher-priced mortgage loans. A higher-priced mortgage

MANDATORY ESCROW ACCOUNTS Effective: June 1, 2013 REGULATION Requires escrow accounts be maintained for five years (rather than the current one year) for higher-priced mortgage loans. A higher-priced mortgage

January 20, 2015 Updated Changes:

Get Ready! Get Set! August 1, 2015 is Around the Corner THE COMBINED TILA AND RESPA MORTGAGE DISCLOSURES (Memo Updated on 1/27/15 to include the changes below) As most of you are probably aware, a major

Get Ready! Get Set! August 1, 2015 is Around the Corner THE COMBINED TILA AND RESPA MORTGAGE DISCLOSURES (Memo Updated on 1/27/15 to include the changes below) As most of you are probably aware, a major

PRIME BROKERAGE CLEARANCE SERVICES AGREEMENT SIA FORM 151

Legent Clearing Account Number PRIME BROKERAGE CLEARANCE SERVICES AGREEMENT SIA FORM 151 1 LC12 07/05 Customer Agreement for Prime Brokerage Clearance Services: Customer Name: Account Number: This Agreement

Legent Clearing Account Number PRIME BROKERAGE CLEARANCE SERVICES AGREEMENT SIA FORM 151 1 LC12 07/05 Customer Agreement for Prime Brokerage Clearance Services: Customer Name: Account Number: This Agreement

!"#$%&%'()#'*+,,#"-&.(*(+,,./0&$/"1()#"0'22

#'*+,,#-&.(*(+,,./0&$/1()#0'22") !"#$%&%'()#'*+,,#"-&.(*(+,,./0&$/"1()#"0'22 Congratulations on taking the first step in getting pre-approved for a mortgage with The Dan Keller Group at Hometown Lending! In this packet, you will find

!"#$%&%'()#'*+,,#"-&.(*(+,,./0&$/"1()#"0'22 Congratulations on taking the first step in getting pre-approved for a mortgage with The Dan Keller Group at Hometown Lending! In this packet, you will find

LOAN PURCHASE AGREEMENT (VERSION 1.2013)

") LOAN PURCHASE AGREEMENT (VERSION 1.2013) This Loan Purchase Agreement ( Agreement ) is entered into as of the date written below, by and between Community Banc Mortgage Corp. ("BancMac"), a duly organized

LOAN PURCHASE AGREEMENT (VERSION 1.2013) This Loan Purchase Agreement ( Agreement ) is entered into as of the date written below, by and between Community Banc Mortgage Corp. ("BancMac"), a duly organized

TRID. Loan Estimate and Closing Disclosure Cross-reference Guide 07.01.2015. 2015 Temenos USA. All rights reserved

TRID T I L A-RESPA INTEGRAT E D D I S C L O S U R E S Loan Estimate and Closing Disclosure Cross-reference Guide 07.01.2015 2015 Temenos USA. All rights reserved w: temenos.com/tricomply p: 205.991.5636

TRID T I L A-RESPA INTEGRAT E D D I S C L O S U R E S Loan Estimate and Closing Disclosure Cross-reference Guide 07.01.2015 2015 Temenos USA. All rights reserved w: temenos.com/tricomply p: 205.991.5636

Notice of Mortgage Loan Originator Pre-Licensure and Continuing Education SAFE Act Approved Course Topic List (Revised May 22, 2012)

") Notice of Mortgage Loan Originator Pre-Licensure and Continuing Education SAFE Act Approved Course Topic List (Revised May 22, 2012) Purpose The purpose of this notice is to assist NMLS approved course

Notice of Mortgage Loan Originator Pre-Licensure and Continuing Education SAFE Act Approved Course Topic List (Revised May 22, 2012) Purpose The purpose of this notice is to assist NMLS approved course

CHAPTER 3: LENDER APPROVAL 7 CFR 3555.51

3.1 INTRODUCTION CHAPTER 3: LENDER APPROVAL 7 CFR 3555.51 A lender is defined as an entity that originates, services, or holds a loan guaranteed by the Agency. The SFHGLP is not intended to promote risky

3.1 INTRODUCTION CHAPTER 3: LENDER APPROVAL 7 CFR 3555.51 A lender is defined as an entity that originates, services, or holds a loan guaranteed by the Agency. The SFHGLP is not intended to promote risky

ATR/QM FAQs. Table of Contents. General

Table of Contents General... 1 Ability to Repay (ATR)/Qualified Mortgage (QM)... 2 ATR Eligibility... 2 Qualifying Ratios... 3 Employment/Income... 4 Verifying Employment History (Employment Gaps)... 4

Table of Contents General... 1 Ability to Repay (ATR)/Qualified Mortgage (QM)... 2 ATR Eligibility... 2 Qualifying Ratios... 3 Employment/Income... 4 Verifying Employment History (Employment Gaps)... 4

Wells Fargo Settlement Agent Communications

Wells Fargo Settlement Agent Communications News for Wells Fargo Settlement Agents September 14, 2015 Wells Fargo says thank you! When the Consumer Financial Protection Bureau (CFPB) announced the TILA

Wells Fargo Settlement Agent Communications News for Wells Fargo Settlement Agents September 14, 2015 Wells Fargo says thank you! When the Consumer Financial Protection Bureau (CFPB) announced the TILA

CFPB FINAL RULES SUN WEST IMPLEMENTATION GUIDE

CFPB FINAL RULES SUN WEST IMPLEMENTATION GUIDE January 02, 2015 In case of any queries regarding the information available in this guide, please reach us at qmteam@swmc.com. Sun West Mortgage Company,

CFPB FINAL RULES SUN WEST IMPLEMENTATION GUIDE January 02, 2015 In case of any queries regarding the information available in this guide, please reach us at qmteam@swmc.com. Sun West Mortgage Company,

TILA-RESPA Integrated Disclosure Rule

TILA-RESPA Integrated Disclosure Rule May 13, 2015 Joseph J. Reilly Partner Benjamin K. Olson Partner 1 Key Changes Effective for applications received by the creditor or mortgage broker on or after August

TILA-RESPA Integrated Disclosure Rule May 13, 2015 Joseph J. Reilly Partner Benjamin K. Olson Partner 1 Key Changes Effective for applications received by the creditor or mortgage broker on or after August

Disclosure Process. 1 WSL:1241 Issued: 09/04/15

NYCB Gemstone Closing Disclosure Process 1 WSL:1241 Issued: 09/04/15 Items being covered today: Closing Disclosure Overview Gemstone Process Flow Overview Walkthroughs of the new modules in Gemstone The

NYCB Gemstone Closing Disclosure Process 1 WSL:1241 Issued: 09/04/15 Items being covered today: Closing Disclosure Overview Gemstone Process Flow Overview Walkthroughs of the new modules in Gemstone The

Ability to Repay/Qualified Mortgages FAQ

The Ability to Repay (ATR)/Qualified Mortgages (QM) provisions of the Dodd-Frank Wall Street Reform and Consumer Protection Act require lenders to make a reasonable, good faith determination of a borrower

The Ability to Repay (ATR)/Qualified Mortgages (QM) provisions of the Dodd-Frank Wall Street Reform and Consumer Protection Act require lenders to make a reasonable, good faith determination of a borrower

NORTH AMERICAN TITLE COMPANY Like Clockwork. www.nat.com/cfpb

NORTH AMERICAN TITLE COMPANY Like Clockwork www.nat.com/cfpb UNDERSTANDING THE NEW LOAN ESTIMATE AND CLOSING DISCLOSURE FORMS American Title, we want to make sure all of our customers have the information

NORTH AMERICAN TITLE COMPANY Like Clockwork www.nat.com/cfpb UNDERSTANDING THE NEW LOAN ESTIMATE AND CLOSING DISCLOSURE FORMS American Title, we want to make sure all of our customers have the information

Table of Contents. Table of Contents... 1. Chapter 1 Introduction... 4. 1.1 Goals and Objectives... 4 1.2 Required Review... 5 1.3 Applicability...

... 1 Chapter 1 Introduction... 4 1.1 Goals and Objectives... 4 1.2 Required Review... 5 1.3 Applicability... 5 Chapter 2 Accountability and Monitoring... 6 2.1 Internal Controls... 6 2.2 Monitoring Underwriters...

... 1 Chapter 1 Introduction... 4 1.1 Goals and Objectives... 4 1.2 Required Review... 5 1.3 Applicability... 5 Chapter 2 Accountability and Monitoring... 6 2.1 Internal Controls... 6 2.2 Monitoring Underwriters...

Ability to Repay and Qualified Mortgage Rule

Ability to Repay and Qualified Mortgage Rule The Consumer Financial Protection Bureau adopted a rule that implements the Ability to Repay and Qualified Mortgage ( ATR/QM ) provisions of the Dodd-Frank

Ability to Repay and Qualified Mortgage Rule The Consumer Financial Protection Bureau adopted a rule that implements the Ability to Repay and Qualified Mortgage ( ATR/QM ) provisions of the Dodd-Frank

Please be sure to only initial below the description of the category of how you would like to do business with AFR.

Dear Lending Partner, It is our pleasure to introduce the different ways you can do business with American Financial Resources Wholesale and Correspondent Lending Divisions. To better serve you, you will

Dear Lending Partner, It is our pleasure to introduce the different ways you can do business with American Financial Resources Wholesale and Correspondent Lending Divisions. To better serve you, you will

Correspondent Seller Eligibility Policy

1.0 Purpose and Scope The Correspondent Lending Division of Impac Mortgage Corp. (Impac) provides guidance for the purchase of Impac-qualified closed loans from correspondent sellers. This policy outlines

1.0 Purpose and Scope The Correspondent Lending Division of Impac Mortgage Corp. (Impac) provides guidance for the purchase of Impac-qualified closed loans from correspondent sellers. This policy outlines

BEXIL AMERICAN MORTGAGE INC./AMERICAN MORTGAGE NETWORK BROKER GUIDE

BEXIL AMERICAN MORTGAGE INC./AMERICAN MORTGAGE NETWORK BROKER GUIDE This Broker Guide ( Guide ), as supplemented and amended from time to time by Bexil American Mortgage Inc./American Mortgage Network

BEXIL AMERICAN MORTGAGE INC./AMERICAN MORTGAGE NETWORK BROKER GUIDE This Broker Guide ( Guide ), as supplemented and amended from time to time by Bexil American Mortgage Inc./American Mortgage Network

MLO COMPENSATION, REGULATION Z, AND DODD-FRANK ACT

MLO COMPENSATION, REGULATION Z, AND DODD-FRANK ACT Vermont Mortgage Bankers Association & Mortgage Bankers/Brokers Association of NH Mortgage Compliance Conference Thursday, March 3, 2011 Sean P. Mahoney

MLO COMPENSATION, REGULATION Z, AND DODD-FRANK ACT Vermont Mortgage Bankers Association & Mortgage Bankers/Brokers Association of NH Mortgage Compliance Conference Thursday, March 3, 2011 Sean P. Mahoney

The New Mortgage Lending Process: A 2014 Check-Up and 2015 Planning

The New Mortgage Lending Process: A 2014 Check-Up and 2015 Planning Copyright 2012 Tata Consultancy Services Limited No Legal Advice, Opinions, or Services Provided This presentation does not constitute

The New Mortgage Lending Process: A 2014 Check-Up and 2015 Planning Copyright 2012 Tata Consultancy Services Limited No Legal Advice, Opinions, or Services Provided This presentation does not constitute

LOAN SUBMISSION PROCEDURES

INTRODUCTION Brokers upload or manually enter data files and required documents via the website. Data files and documents submitted prior to 2:00 pm CT (Birmingham Fulfillment Center) or 4:00 p.m. PT (San

INTRODUCTION Brokers upload or manually enter data files and required documents via the website. Data files and documents submitted prior to 2:00 pm CT (Birmingham Fulfillment Center) or 4:00 p.m. PT (San

BROWN, FOWLER & ALSUP A Professional Corporation Attorneys at Law MEMORANDUM

BROWN, FOWLER & ALSUP A Professional Corporation Attorneys at Law J. Alton Alsup 10333 Richmond, Suite 860 Telephone 713/468-0400 Board Certified in Residential Real Estate Law Texas Board of Legal Specialization

BROWN, FOWLER & ALSUP A Professional Corporation Attorneys at Law J. Alton Alsup 10333 Richmond, Suite 860 Telephone 713/468-0400 Board Certified in Residential Real Estate Law Texas Board of Legal Specialization

BULLETIN. DESKTOP UNDERWRITER SCHEDULE (Expanded Use Version) 2. Among other things, the New DU Schedule addresses and/or provides for:

2. Among other things, the New DU Schedule addresses and/or provides for:") DU-09-01 Effective Date: August 11, 2009 BULLETIN DESKTOP UNDERWRITER SCHEDULE (Expanded Use Version) 1. This Bulletin is issued in accordance with the section of the Fannie Mae Software Subscription Agreement

DU-09-01 Effective Date: August 11, 2009 BULLETIN DESKTOP UNDERWRITER SCHEDULE (Expanded Use Version) 1. This Bulletin is issued in accordance with the section of the Fannie Mae Software Subscription Agreement

2015 Fidelity National Title Group

Five Things You Need to Know Before August 2015 WHAT IS THE CFPB? THE NEW LINGO Dodd-Frank Act --Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 CFPB Consumer Financial Protection Bureau

Five Things You Need to Know Before August 2015 WHAT IS THE CFPB? THE NEW LINGO Dodd-Frank Act --Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 CFPB Consumer Financial Protection Bureau