Long-term Liabilities for Social Security and Employment Related Pensions

|

|

|

- Brianne Bates

- 8 years ago

- Views:

Transcription

1 GFSAC 15/14 Meeting of the IMF Government Finance Statistics Advisory Committee Washington, D.C. Long-term Liabilities for Social Security and Employment Related Pensions March 9 10, 2015 Prepared by Peter van de Ven DISCLAIMER: The views expressed herein are those of the author and should not be attributed to the IMF, its Executive Board, or its management. internationalinter

2

3 LONG-TERM LIABILITIES FOR SOCIAL SECURITY AND EMPLOYMENT RELATED PENSIONS Government Finance Statistics Advisory Committee Washington, D.C., 9 10 March 2015 Peter van de Ven Head of National Accounts, OECD

4 Introduction Recent crises have highlighted the relevance of government debt statistics Important to also incorporate the best available data on pension liabilities Purpose of this presentation: Outline the current challenges in obtaining comparable pension data Provide recommendations on how to address these challenges Summarise OECD activities currently underway 2

5 Challenges: Recording of Pension Liabilities/Entitlements Current guidance on recording of pension liabilities: GFSM 2014: For employment-related pension schemes, liabilities/entitlements should always be recognised For social security type of schemes: obligations not to be recognised, and only obligations minus Net Present Value of contributions to be recorded as a memorandum item (different from GFSM 2001) SNA 2008: Defined contribution schemes: liabilities equal accumulated assets Defined benefit schemes: Liabilities of employment-related pension schemes to be included However, sometimes these schemes are intertwined with generic social security type of pension schemes => SNA provides flexibility ESA 2010: liabilities of unfunded government sponsored pension schemes are not to be recognised Supplementary Table including all obligations/entitlement GFSM 2014 and SNA 2008 consistent, except for memorandum item 3

6 Challenges: Recording of Pension Liabilities/Entitlements In both standards (GFSM and SNA) still some lack of clarity regarding the recording of employment-related schemes which are intertwined with social security Need to arrive at clear criteria when pension liabilities should (not) be recognised and recorded Our opinion: in the end, the presence of a legal contract, e.g. an employment contract, is the only relevant criterion for recognising an explicit liability However, even having clear criteria may not provide internationally comparable data => Supplementary Table

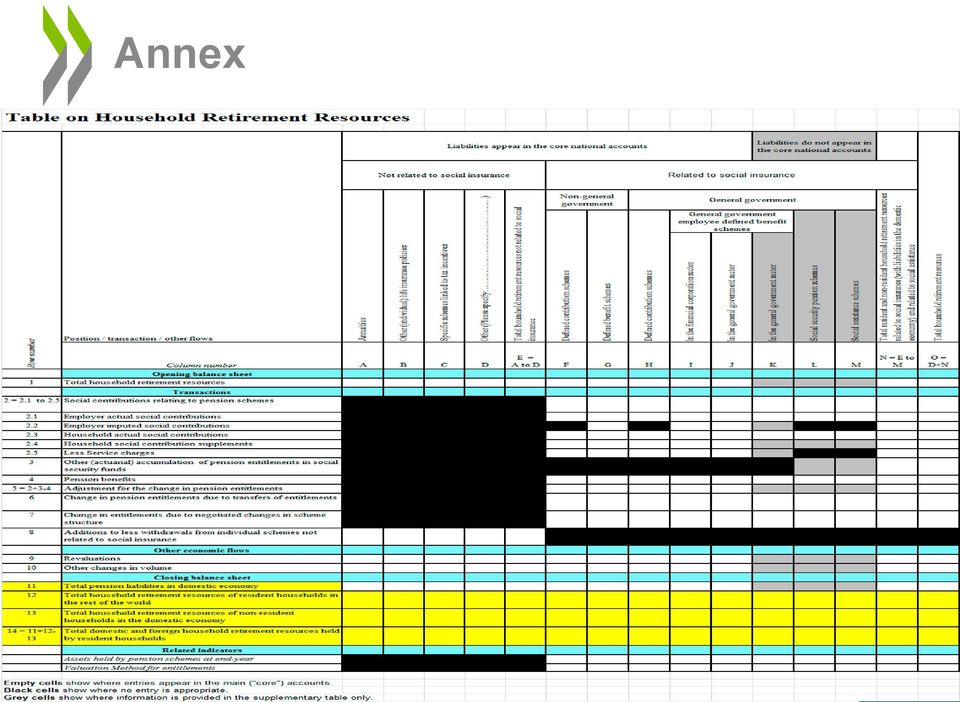

7 Challenges: Recording of Pension Liabilities/Entitlements Supplementary Table In addition to explicit liabilities recognised in the core system, it also provides information on implicit liabilities related to social security type of schemes New table on household retirement resources Includes social insurance types of schemes (counterpart of table 17.10) as well as other resources of households in preparation for retirement: Individual life insurance (e.g. annuities) Specific saving schemes Other individual resources Social assistance schemes Final design of the table: pending decision on how to account for cross-border holdings 5

as well as other resources of households in preparation for retirement: Individual life insurance (e.g.")

8 Challenges: Developing Internationally Comparable Estimates Methodologies for estimating pension liabilities may be quite different: Institutional arrangements for compiling data can vary Sources of information Regulations / laws for estimation Level of expertise readily available Differences in assumptions Discount rate; IPSAS recommends using yields from government debt securities with maturities similar to pension entitlements Salary rates; Accrued Benefit Obligations (ABO) vs. Projected Benefit Obligations (PBO) Time horizon and membership; Accrued-to-Date Liabilities vs. Closed Group vs. Open Group 6

vs. Projected Benefit Obligations (PBO) Time horizon and membership; Accrued-to-Date Liabilities vs. Closed Group vs.")

9 Implications for the Interpretation of Data on Government Debt Comprehensive and comparable analysis of liabilities not possible due to: Differences in interpretation of present international standards Differences in institutional set-up of pensions lead to differences in recognition of explicit liabilities, while material differences may not be that large Government debt does not take into account implicit liabilities Lack of standardised rules for measuring pension liabilities Lack of data more generally Analysis also requires consideration of accumulated assets Capacity to pay down debt by liquidating assets Capacity to generate income or offset future expenditures 7

10 Recommendations Presence of a legal contract as the sole criterion for determining whether a pension liability should be recognised and recorded in the core national accounts When estimating pension liabilities: Projected Benefit Obligations and Accrued-to-Date Liabilities Discount rates: yields of central government debt securities, or a fixed real discount rate as per Eurostat guidelines Pension Factsheet, including metadata on assumptions and methods used More generally, do not focus too much on single headline indicators, and provide additional data on contingent liabilities and accumulated assets 8

11 Next Steps Questionnaire to collect data on assets and liabilities related to government sponsored pension schemes Policy brief (with a methodological background paper) on implicit public pension debt Pension workshop in the fall of 2015 covering: International comparability of pension statistics Extent of required metadata Exchange best practices in the estimation/recording of pensions 9

12 Thank you for your attention! 10

13 Annex 11

Long-term Liabilities for Social Security and Employment Related Pensions

GFSAC 15/14 Meeting of the IMF Government Finance Statistics Advisory Committee Washington, D.C. Long-term Liabilities for Social Security and Employment Related Pensions March 9 10, 2015 Prepared by Peter

GFSAC 15/14 Meeting of the IMF Government Finance Statistics Advisory Committee Washington, D.C. Long-term Liabilities for Social Security and Employment Related Pensions March 9 10, 2015 Prepared by Peter

SNA/M1.14/2.2. 9th Meeting of the Advisory Expert Group on National Accounts, 8-10 September 2014, Washington DC. Agenda item: 2.2

SNA/M1.14/2.2 9th Meeting of the Advisory Expert Group on National Accounts, 8-10 September 2014, Washington DC Agenda item: 2.2 Introduction Table on household retirement resources 1 Funding retirement

SNA/M1.14/2.2 9th Meeting of the Advisory Expert Group on National Accounts, 8-10 September 2014, Washington DC Agenda item: 2.2 Introduction Table on household retirement resources 1 Funding retirement

Unfunded employer and social security pension schemes

EUROPEAN COMMISSION Statistical Office of the European Communities DIRECTORATE GENERAL STATISTICS Unfunded employer and social security pension schemes The Committee on Monetary, Financial and Balance

EUROPEAN COMMISSION Statistical Office of the European Communities DIRECTORATE GENERAL STATISTICS Unfunded employer and social security pension schemes The Committee on Monetary, Financial and Balance

The Treatment of Concessional Loans in the Government Accounts

GFSAC 15/18 Meeting of the IMF Government Finance Statistics Advisory Committee Washington, D.C. The Treatment of Concessional Loans in the Government Accounts Prepared by Julia Catz March 9 10, 2015 DISCLAIMER:

GFSAC 15/18 Meeting of the IMF Government Finance Statistics Advisory Committee Washington, D.C. The Treatment of Concessional Loans in the Government Accounts Prepared by Julia Catz March 9 10, 2015 DISCLAIMER:

General government pension obligations in Europe

General government pension obligations in Europe Reimund Mink 1 1. Introduction The population of Europe is ageing. This is not a new phenomenon, but a process common to almost all developed, and most

General government pension obligations in Europe Reimund Mink 1 1. Introduction The population of Europe is ageing. This is not a new phenomenon, but a process common to almost all developed, and most

RETAINED EARNINGS ON MUTUAL FUNDS, INSURANCE CORPORATIONS AND PENSION FUNDS

Fourth meeting of the Advisory Expert Group on National Accounts 30 January 8 February 2006, Frankfurt SNA/M1.06/29.1 Issue 42 Retained earnings of mutual funds, insurance companies and pension funds RETAINED

Fourth meeting of the Advisory Expert Group on National Accounts 30 January 8 February 2006, Frankfurt SNA/M1.06/29.1 Issue 42 Retained earnings of mutual funds, insurance companies and pension funds RETAINED

GFS in AFRICA. Meeting of the IMF Government Finance Statistics Advisory Committee Washington, D.C. GFSAC 15/05

GFSAC 15/05 Meeting of the IMF Government Finance Statistics Advisory Committee Washington, D.C. GFS in AFRICA March 9 10, 2015 Prepared by Majdeline El Rayess, Alberto Jiménez de Lucio, and Viera Karolova

GFSAC 15/05 Meeting of the IMF Government Finance Statistics Advisory Committee Washington, D.C. GFS in AFRICA March 9 10, 2015 Prepared by Majdeline El Rayess, Alberto Jiménez de Lucio, and Viera Karolova

Changes to National Accounts: The Impact of the Changes to the Treatment of Pensions in the National Accounts

Changes to National Accounts: The Impact of the Changes to the Treatment of Pensions in the National Accounts Authors: Robbie Jones and David Matthews Date: 17 September 2014 1 Introduction The UK National

Changes to National Accounts: The Impact of the Changes to the Treatment of Pensions in the National Accounts Authors: Robbie Jones and David Matthews Date: 17 September 2014 1 Introduction The UK National

GOVERNMENT FINANCE ST A TISTICS MANUAL

MANUAL GOVERNMENT FINANCE STATISTICS MANUAL 2014 I N T E R N A T I O N A L M O N E T A R Y F U N D MANUAL GOVERNMENT FINANCE STATISTICS MANUAL 2014 2014 I N T E R N A T I O N A L M O N E T A R Y F U N

MANUAL GOVERNMENT FINANCE STATISTICS MANUAL 2014 I N T E R N A T I O N A L M O N E T A R Y F U N D MANUAL GOVERNMENT FINANCE STATISTICS MANUAL 2014 2014 I N T E R N A T I O N A L M O N E T A R Y F U N

Table of Contents. Background and Certification Page 2 Introduction Page 3. Amortization Method Page 4

Racine County School Office Accounting and Sample Funding Report of Liabilities for Participants Post Employment Benefits as of January 1, 2011 Thru End of the Year December 31, 2011 January 2012 This

Racine County School Office Accounting and Sample Funding Report of Liabilities for Participants Post Employment Benefits as of January 1, 2011 Thru End of the Year December 31, 2011 January 2012 This

Government employer-sponsored unfunded pension plans -- Revised treatment in the Canadian System of National Accounts

I: Introduction Government employer-sponsored unfunded pension plans -- Revised treatment in the Canadian System of National Accounts by Patrick O'Hagan May 2003 In 2000, the Canadian System of National

I: Introduction Government employer-sponsored unfunded pension plans -- Revised treatment in the Canadian System of National Accounts by Patrick O'Hagan May 2003 In 2000, the Canadian System of National

The Definition of a Social Insurance Scheme and its Classification as Defined Benefit or Defined Contribution. John Pitzer.

The Definition of a Social Insurance Scheme and its Classification as Defined Benefit or Defined Contribution I. Introduction John Pitzer June 30, 2003 1. In an interview posted on this electronic discussion

The Definition of a Social Insurance Scheme and its Classification as Defined Benefit or Defined Contribution I. Introduction John Pitzer June 30, 2003 1. In an interview posted on this electronic discussion

Issues Related to the Introduction of ESA 2010 in Europe

Issues Related to the Introduction of ESA 2010 in Europe Gallo Gueye (Eurostat) Jens Gruetz (Eurostat) Paper Prepared for the IARIW 33 rd General Conference Rotterdam, the Netherlands, August 24-30, 2014

Issues Related to the Introduction of ESA 2010 in Europe Gallo Gueye (Eurostat) Jens Gruetz (Eurostat) Paper Prepared for the IARIW 33 rd General Conference Rotterdam, the Netherlands, August 24-30, 2014

Public Sector Debt - Instructions

Public Sector Debt - Instructions Under the auspices of the Task Force on Finance Statistics 1 the World Bank has developed a new database to disseminate quarterly data on government, and more broadly,

Public Sector Debt - Instructions Under the auspices of the Task Force on Finance Statistics 1 the World Bank has developed a new database to disseminate quarterly data on government, and more broadly,

Constructing the Supplementary Pension Table for the Netherlands

Discussion Paper Constructing the Supplementary Pension Table for the Netherlands The views expressed in this paper are those of the author(s) and do not necessarily reflect the policies of Statistics

Discussion Paper Constructing the Supplementary Pension Table for the Netherlands The views expressed in this paper are those of the author(s) and do not necessarily reflect the policies of Statistics

The previous article The public

Economic & Labour Market Review Vol 3 No 7 July 2009 FEATURE Fenella Maitland-Smith Bank of England (formerly Office for National Statistics) Government financial liabilities beyond public sector net debt

Economic & Labour Market Review Vol 3 No 7 July 2009 FEATURE Fenella Maitland-Smith Bank of England (formerly Office for National Statistics) Government financial liabilities beyond public sector net debt

EUROPEAN UNION ACCOUNTING RULE 12 EMPLOYEE BENEFITS

EUROPEAN UNION ACCOUNTING RULE 12 EMPLOYEE BENEFITS Page 2 of 18 I N D E X 1. Introduction... 3 2. Objective... 3 3. Scope... 4 4. Definitions... 5 5. Short-term employee benefits... 7 5.1 Recognition

EUROPEAN UNION ACCOUNTING RULE 12 EMPLOYEE BENEFITS Page 2 of 18 I N D E X 1. Introduction... 3 2. Objective... 3 3. Scope... 4 4. Definitions... 5 5. Short-term employee benefits... 7 5.1 Recognition

CITY OF AURORA, ILLINOIS POLICE PENSION FUND ANNUAL FINANCIAL REPORT. For the Year Ended December 31, 2014

ANNUAL FINANCIAL REPORT For the Year Ended December 31, 2014 TABLE OF CONTENTS Page(s) INDEPENDENT AUDITOR S REPORT... 3-4 MANAGEMENT S DISCUSSION AND ANALYSIS... MD&A 1-5 BASIC FINANCIAL STATEMENTS Statement

ANNUAL FINANCIAL REPORT For the Year Ended December 31, 2014 TABLE OF CONTENTS Page(s) INDEPENDENT AUDITOR S REPORT... 3-4 MANAGEMENT S DISCUSSION AND ANALYSIS... MD&A 1-5 BASIC FINANCIAL STATEMENTS Statement

GUIDELINES FOR RESPONDING TO THE GFSM 2014 ANNUAL GFS QUESTIONNAIRE

GFSY 2014 data request letter Table 1. of Revenue 1 Revenue 11 Taxes GUIDELINES FOR RESPONDING TO THE GFSM 2014 ANNUAL GFS QUESTIONNAIRE Overview of Changes in the GFSM 2014 classification system 111 Taxes

GFSY 2014 data request letter Table 1. of Revenue 1 Revenue 11 Taxes GUIDELINES FOR RESPONDING TO THE GFSM 2014 ANNUAL GFS QUESTIONNAIRE Overview of Changes in the GFSM 2014 classification system 111 Taxes

IMF COMMITTEE ON BALANCE OF PAYMENTS STATISTICS BALANCE OF PAYMENTS TECHNICAL EXPERT GROUP (BOPTEG)

") IMF COMMITTEE ON BALANCE OF PAYMENTS STATISTICS BALANCE OF PAYMENTS TECHNICAL EXPERT GROUP (BOPTEG) ISSUE PAPER: BOPTEG #19 RETAINED EARNINGS OF MUTUAL FUNDS AND OTHER COLLECTIVE INVESTMENT SCHEMES Prepared

IMF COMMITTEE ON BALANCE OF PAYMENTS STATISTICS BALANCE OF PAYMENTS TECHNICAL EXPERT GROUP (BOPTEG) ISSUE PAPER: BOPTEG #19 RETAINED EARNINGS OF MUTUAL FUNDS AND OTHER COLLECTIVE INVESTMENT SCHEMES Prepared

General Government debt: a quick way to improve comparability

General Government debt: a quick way to improve comparability DEMBIERMONT Christian* BIS Bank for International Settlements, Basel, Switzerland Christian.Dembiermont@bis.org In simple words the General

General Government debt: a quick way to improve comparability DEMBIERMONT Christian* BIS Bank for International Settlements, Basel, Switzerland Christian.Dembiermont@bis.org In simple words the General

An explanation of social assistance, pension schemes, insurance schemes and similar concepts

From: OECD Framework for Statistics on the Distribution of Household Income, Consumption and Wealth Access the complete publication at: http://dx.doi.org/10.1787/9789264194830-en An explanation of social

From: OECD Framework for Statistics on the Distribution of Household Income, Consumption and Wealth Access the complete publication at: http://dx.doi.org/10.1787/9789264194830-en An explanation of social

Guide to Transparency in Public Finances. Looking Beyond the Core Budget. Future Liabilities WWW.OPENBUDGETINDEX.ORG

Guide to Transparency in Public Finances Looking Beyond the Core Budget 5. Future Liabilities WWW.OPENBUDGETINDEX.ORG Introduction For more than a decade, civil society organizations around the world,

Guide to Transparency in Public Finances Looking Beyond the Core Budget 5. Future Liabilities WWW.OPENBUDGETINDEX.ORG Introduction For more than a decade, civil society organizations around the world,

Comparison of micro and macro frameworks

OECD Framework for Statistics on the Distribution of Household Income, Consumption and Wealth OECD 2013 Comparison of micro and macro frameworks The main framework developed for analysis of income at the

OECD Framework for Statistics on the Distribution of Household Income, Consumption and Wealth OECD 2013 Comparison of micro and macro frameworks The main framework developed for analysis of income at the

Financial services associated with insurance and pension schemes (Social insurance schemes)

") Financial services associated with insurance and pension schemes (Social insurance schemes) Regional Course on 2008 SNA (Special Topics): Improving Exhaustiveness of GDP Coverage 31 August-4 September

Financial services associated with insurance and pension schemes (Social insurance schemes) Regional Course on 2008 SNA (Special Topics): Improving Exhaustiveness of GDP Coverage 31 August-4 September

Eighteenth Meeting of the IMF Committee on Balance of Payments Statistics Washington, D.C., June 27 July 1, 2005

BOPCOM-05/9 Eighteenth Meeting of the IMF Committee on Balance of Payments Statistics Washington, D.C., June 27 July 1, 2005 Definition of Personal Remittances in the Balance of Payments Context Prepared

BOPCOM-05/9 Eighteenth Meeting of the IMF Committee on Balance of Payments Statistics Washington, D.C., June 27 July 1, 2005 Definition of Personal Remittances in the Balance of Payments Context Prepared

Pensions & Post-Retirement Benefits

FIN 551: Fundamental Analysis 1 Pensions & Post-Retirement Benefits The Issues Separate set of pension books Defined contribution vs. defined benefit plans» Problem exists with defined benefit plans Annual

FIN 551: Fundamental Analysis 1 Pensions & Post-Retirement Benefits The Issues Separate set of pension books Defined contribution vs. defined benefit plans» Problem exists with defined benefit plans Annual

ACCOUNTING STANDARDS BOARD NOVEMBER 2000 FRS 17 STANDARD FINANCIAL REPORTING ACCOUNTING STANDARDS BOARD

ACCOUNTING STANDARDS BOARD NOVEMBER 2000 FRS 17 17 RETIREMENT BENEFITS FINANCIAL REPORTING STANDARD ACCOUNTING STANDARDS BOARD Financial Reporting Standard 17 Retirement Benefits is issued by the Accounting

ACCOUNTING STANDARDS BOARD NOVEMBER 2000 FRS 17 17 RETIREMENT BENEFITS FINANCIAL REPORTING STANDARD ACCOUNTING STANDARDS BOARD Financial Reporting Standard 17 Retirement Benefits is issued by the Accounting

PENSION FUNDS AND LIFE INSURANCE COMPANIES

PENSION FUNDS AND LIFE INSURANCE COMPANIES Note by John Walton Formerly, Consultant to Eurostat, Units B1 and D2 This paper has been written in my personal capacity and the views in it do not represent

PENSION FUNDS AND LIFE INSURANCE COMPANIES Note by John Walton Formerly, Consultant to Eurostat, Units B1 and D2 This paper has been written in my personal capacity and the views in it do not represent

Prepared by Pierre Sola and Carlos Sánchez Muñoz Directorate General Statistics European Central Bank

UPDATE OF THE 1993 SNA - ISSUE No. 44a ISSUES PAPER FOR THE JULY 2005 AEG MEETING SNA/M1.05/10.2 THE DISTINCTION BETWEEN DEPOSITS AND LOANS IN MACRO-ECONOMIC STATISTICS Prepared by Pierre Sola and Carlos

UPDATE OF THE 1993 SNA - ISSUE No. 44a ISSUES PAPER FOR THE JULY 2005 AEG MEETING SNA/M1.05/10.2 THE DISTINCTION BETWEEN DEPOSITS AND LOANS IN MACRO-ECONOMIC STATISTICS Prepared by Pierre Sola and Carlos

Pension benefits with a guarantee and the advice requirement

Pension benefits with a guarantee and the advice requirement January 2016 This factsheet is intended to help pension scheme providers determine: whether certain types of pension benefits which contain

Pension benefits with a guarantee and the advice requirement January 2016 This factsheet is intended to help pension scheme providers determine: whether certain types of pension benefits which contain

Sixteenth Meeting of the IMF Committee on Balance of Payments Statistics Washington D.C., December 1 5, 2003

BOPCOM-03/23 Sixteenth Meeting of the IMF Committee on Balance of Payments Statistics Washington D.C., December 1 5, 2003 The Statistical Treatment of Unit Trusts Prepared by the South African Reserve

BOPCOM-03/23 Sixteenth Meeting of the IMF Committee on Balance of Payments Statistics Washington D.C., December 1 5, 2003 The Statistical Treatment of Unit Trusts Prepared by the South African Reserve

HOW HAS SHIFT TO DEFINED CONTRIBUTION PLANS AFFECTED SAVING?

September 2015, Number 15-16 RETIREMENT RESEARCH HOW HAS SHIFT TO DEFINED CONTRIBUTION PLANS AFFECTED SAVING? By Alicia H. Munnell, Jean-Pierre Aubry, and Caroline V. Crawford* Introduction Many commentators

September 2015, Number 15-16 RETIREMENT RESEARCH HOW HAS SHIFT TO DEFINED CONTRIBUTION PLANS AFFECTED SAVING? By Alicia H. Munnell, Jean-Pierre Aubry, and Caroline V. Crawford* Introduction Many commentators

Generic Local School District, Ohio Notes to the Basic Financial Statements For the Fiscal Year Ended June 30, 2015

Note 2 - Summary of Significant Accounting Policies Pensions For purposes of measuring the net pension liability, information about the fiduciary net position of the pension plans and additions to/deductions

Note 2 - Summary of Significant Accounting Policies Pensions For purposes of measuring the net pension liability, information about the fiduciary net position of the pension plans and additions to/deductions

INDEPENDENT AUDITOR S REPORT

To the members of The Duty Lawyer Service (Incorporated in Hong Kong with liability limited by guarantee) INDEPENDENT AUDITOR S REPORT We have audited the financial statements of The Duty Lawyer Service

To the members of The Duty Lawyer Service (Incorporated in Hong Kong with liability limited by guarantee) INDEPENDENT AUDITOR S REPORT We have audited the financial statements of The Duty Lawyer Service

The Treatment of Insurance in the SNA

The Treatment of Insurance in the SNA Peter Hill Statistical Division, United Nations Economic Commission for Europe April 1998 Introduction The treatment of insurance is one of the more complicated parts

The Treatment of Insurance in the SNA Peter Hill Statistical Division, United Nations Economic Commission for Europe April 1998 Introduction The treatment of insurance is one of the more complicated parts

Statistical standard for financial assets and liabilities 2013

Rationale The main purpose of classifying financial assets and liabilities is to provide consistent and relevant statistics that support economic analysis and macroeconomic management for New Zealand.

Rationale The main purpose of classifying financial assets and liabilities is to provide consistent and relevant statistics that support economic analysis and macroeconomic management for New Zealand.

Employee Stock Options Paper for the Advisory Expert Group on national accounts By Eurostat

SNA/M1.04/11 Employee Stock Options Paper for the Advisory Expert Group on national accounts By Eurostat Executive Summary This paper summarises research and discussions undertaken over the last four years

SNA/M1.04/11 Employee Stock Options Paper for the Advisory Expert Group on national accounts By Eurostat Executive Summary This paper summarises research and discussions undertaken over the last four years

Having taken into account the opinion of the CMFB and other expert groups, Eurostat has decided on the following issues:

, has decided on eight important accounting issues setting the guidelines to ensure a better comparability for the deficit and debt procedure in Member States. Following specific requests from some Member

, has decided on eight important accounting issues setting the guidelines to ensure a better comparability for the deficit and debt procedure in Member States. Following specific requests from some Member

Accounting and Reporting Policy FRS 102. Staff Education Note 9 Short-term employee benefits and termination benefits

Accounting and Reporting Policy FRS 102 Staff Education Note 9 Short-term employee benefits and termination benefits Disclaimer This Education Note has been prepared by FRC staff for the convenience of

Accounting and Reporting Policy FRS 102 Staff Education Note 9 Short-term employee benefits and termination benefits Disclaimer This Education Note has been prepared by FRC staff for the convenience of

July 2011. IAS 19 - Employee Benefits A closer look at the amendments made by IAS 19R

July 2011 IAS 19 - Employee Benefits A closer look at the amendments made by IAS 19R 2 Contents 1. Introduction 3 2. Executive summary 4 3. General changes made by IAS 19R 6 4. Changes in IAS 19R with

July 2011 IAS 19 - Employee Benefits A closer look at the amendments made by IAS 19R 2 Contents 1. Introduction 3 2. Executive summary 4 3. General changes made by IAS 19R 6 4. Changes in IAS 19R with

Adding Actuarial Information on Defined Benefit Pension Plans and Social Security to. the National Accounts

Adding Actuarial Information on Defined Benefit Pension Plans and Social Security to the National Accounts Dominque Durant (Banque de France-Autorite de contrôle prudentiel) David Lenze (Bureau of Economic

Adding Actuarial Information on Defined Benefit Pension Plans and Social Security to the National Accounts Dominque Durant (Banque de France-Autorite de contrôle prudentiel) David Lenze (Bureau of Economic

Presentation of the Gross External Debt Position

4 Presentation of the Gross External Debt Position Introduction 4. This chapter provides a table for the presentation of the gross external debt position and related memorandum tables. Data compiled using

4 Presentation of the Gross External Debt Position Introduction 4. This chapter provides a table for the presentation of the gross external debt position and related memorandum tables. Data compiled using

Eighteenth Meeting of the IMF Committee on Balance of Payments Statistics Washington, D.C., June 27 July 1, 2005

BOPCOM-05/29 Eighteenth Meeting of the IMF Committee on Balance of Payments Statistics Washington, D.C., June 27 July 1, 2005 The Treatment of Nonperforming Loans Prepared by the Statistics Department

BOPCOM-05/29 Eighteenth Meeting of the IMF Committee on Balance of Payments Statistics Washington, D.C., June 27 July 1, 2005 The Treatment of Nonperforming Loans Prepared by the Statistics Department

Accounting For Pensions

Accounting For Pensions Defined Benefit vs. Defined Contribution Plans Defining the Pension Obligation Accumulated Benefit Obligation Vested Benefit Obligation Projected Benefit Obligation Service Cost

Accounting For Pensions Defined Benefit vs. Defined Contribution Plans Defining the Pension Obligation Accumulated Benefit Obligation Vested Benefit Obligation Projected Benefit Obligation Service Cost

College of Physicians and Surgeons of British Columbia

Financial Statements OF College of Physicians and Surgeons of British Columbia FEBRUARY 29, 2012 Table of contents Independent Auditor s Report... 1 Statement of operations... 2 Statement of changes in

Financial Statements OF College of Physicians and Surgeons of British Columbia FEBRUARY 29, 2012 Table of contents Independent Auditor s Report... 1 Statement of operations... 2 Statement of changes in

Valuing the Business

Valuing the Business 1. Introduction After deciding to buy or sell a business, the subject of "how much" becomes important. Determining the value of a business is one of the most difficult aspects of any

Valuing the Business 1. Introduction After deciding to buy or sell a business, the subject of "how much" becomes important. Determining the value of a business is one of the most difficult aspects of any

Program and Budget Committee

E WO/PBC/19/23 ORIGINAL: ENGLISH DATE: JUNE 20, 2012 Program and Budget Committee Nineteenth Session Geneva, September 10 to 14, 2012 LONG-TERM FINANCING OF AFTER-SERVICE HEALTH INSURANCE (ASHI) IN WIPO

E WO/PBC/19/23 ORIGINAL: ENGLISH DATE: JUNE 20, 2012 Program and Budget Committee Nineteenth Session Geneva, September 10 to 14, 2012 LONG-TERM FINANCING OF AFTER-SERVICE HEALTH INSURANCE (ASHI) IN WIPO

Chapter 17 Pensions and Other Postretirement Benefits

Chapter 17 Pensions and Other Postretirement Benefits AACSB assurance of learning standards in accounting and business education require documentation of outcomes assessment. Although schools, departments,

Chapter 17 Pensions and Other Postretirement Benefits AACSB assurance of learning standards in accounting and business education require documentation of outcomes assessment. Although schools, departments,

BS2551 Money Banking and Finance. Institutional Investors

BS2551 Money Banking and Finance Institutional Investors Institutional investors pension funds, mutual funds and life insurance companies are the main players in securities markets in both the USA and

BS2551 Money Banking and Finance Institutional Investors Institutional investors pension funds, mutual funds and life insurance companies are the main players in securities markets in both the USA and

PRACTICE NOTE 22 THE AUDITORS CONSIDERATION OF FRS 17 RETIREMENT BENEFITS DEFINED BENEFIT SCHEMES

PRACTICE NOTE 22 THE AUDITORS CONSIDERATION OF FRS 17 RETIREMENT BENEFITS DEFINED BENEFIT SCHEMES Contents Introduction Background The audit approach Ethical issues Planning considerations Communication

PRACTICE NOTE 22 THE AUDITORS CONSIDERATION OF FRS 17 RETIREMENT BENEFITS DEFINED BENEFIT SCHEMES Contents Introduction Background The audit approach Ethical issues Planning considerations Communication

GN11A(ROI): CALCULATIONS REQUIRED UNDER THE FAMILY LAW ACT, 1995 OR THE FAMILY LAW (DIVORCE) ACT, 1996

: CALCULATIONS REQUIRED UNDER THE FAMILY LAW ACT, 1995 OR THE FAMILY LAW (DIVORCE) ACT, 1996") GN11A(ROI): CALCULATIONS REQUIRED UNDER THE FAMILY LAW ACT, 1995 OR THE FAMILY LAW (DIVORCE) ACT, 1996 Classification Practice Standard Legislation or Authority This Guidance Note must be read in conjunction

GN11A(ROI): CALCULATIONS REQUIRED UNDER THE FAMILY LAW ACT, 1995 OR THE FAMILY LAW (DIVORCE) ACT, 1996 Classification Practice Standard Legislation or Authority This Guidance Note must be read in conjunction

NATIONAL ENERGY EDUCATION DEVELOPMENT PROJECT, INC. Financial Statements and Supplemental Information

NATIONAL ENERGY EDUCATION DEVELOPMENT PROJECT, INC. Financial Statements and Supplemental Information (With Summarized Financial Information for the Year Ended December 31, 2011) and Report Thereon TABLE

NATIONAL ENERGY EDUCATION DEVELOPMENT PROJECT, INC. Financial Statements and Supplemental Information (With Summarized Financial Information for the Year Ended December 31, 2011) and Report Thereon TABLE

CHAPTER 20. Accounting for Pensions and Postretirement Benefits 1, 2, 3, 4, 5, 6, 7, 8, 9, 13, 14, 24

CHAPTER 20 Accounting for Pensions and Postretirement Benefits ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics 1. Basic definitions and concepts related to pension plans. Questions 1, 2, 3, 4, 5, 6,

CHAPTER 20 Accounting for Pensions and Postretirement Benefits ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics 1. Basic definitions and concepts related to pension plans. Questions 1, 2, 3, 4, 5, 6,

GUIDANCE NOTE 450 - COST OF DEATH AND DISABILITY BENEFITS - CERTIFICATES BY ACTUARIES UNDER SUB-SECTION 279(3) OF THE INCOME TAX ASSESSMENT ACT

OF THE INCOME TAX ASSESSMENT ACT") THE INSTITUTE OF ACTUARIES OF AUSTRALIA A.C.N. 000 423 656 GUIDANCE NOTE 450 - COST OF DEATH AND DISABILITY BENEFITS - CERTIFICATES BY ACTUARIES UNDER SUB-SECTION 279(3) OF THE INCOME TAX ASSESSMENT ACT

THE INSTITUTE OF ACTUARIES OF AUSTRALIA A.C.N. 000 423 656 GUIDANCE NOTE 450 - COST OF DEATH AND DISABILITY BENEFITS - CERTIFICATES BY ACTUARIES UNDER SUB-SECTION 279(3) OF THE INCOME TAX ASSESSMENT ACT

Receivables 1 relating to Defined Benefit Liabilities of superannuation entities

Receivables 1 relating to Defined Benefit Liabilities of superannuation entities The purpose of this paper is to provide relevant information for the Board to finalise the principles underpinning the recognition

Receivables 1 relating to Defined Benefit Liabilities of superannuation entities The purpose of this paper is to provide relevant information for the Board to finalise the principles underpinning the recognition

Domestic Relations. Journal of Ohio

Domestic Relations Stanley Morganstern, Esq. Editor-in-Chief Journal of Ohio Laurel G. Streim Esq. Associate Editor July / August 2006 Volume 18 Issue 4 IN THIS ISSUE: Valuing Pension Benefits in Divorce

Domestic Relations Stanley Morganstern, Esq. Editor-in-Chief Journal of Ohio Laurel G. Streim Esq. Associate Editor July / August 2006 Volume 18 Issue 4 IN THIS ISSUE: Valuing Pension Benefits in Divorce

ILLINOIS GOVERNMENT FINANCE OFFICERS ASSOCIATION RECOMMENDED PRACTICES FOR IMPLEMENTING GASB STATEMENT NOS. 67 AND 68 FEBRUARY 7, 2014

ILLINOIS GOVERNMENT FINANCE OFFICERS ASSOCIATION RECOMMENDED PRACTICES FOR IMPLEMENTING GASB STATEMENT NOS. 67 AND 68 FEBRUARY 7, 2014 In June 2012, the Governmental Accounting Standards Board (GASB) released

ILLINOIS GOVERNMENT FINANCE OFFICERS ASSOCIATION RECOMMENDED PRACTICES FOR IMPLEMENTING GASB STATEMENT NOS. 67 AND 68 FEBRUARY 7, 2014 In June 2012, the Governmental Accounting Standards Board (GASB) released

Sri Lanka Accounting Standard-LKAS 26. Accounting and Reporting by Retirement Benefit Plans

Sri Lanka Accounting Standard-LKAS 26 Accounting and Reporting by Retirement Benefit Plans -661- Sri Lanka Accounting Standard-LKAS 26 Accounting and Reporting by Retirement Benefit Plans Sri Lanka Accounting

Sri Lanka Accounting Standard-LKAS 26 Accounting and Reporting by Retirement Benefit Plans -661- Sri Lanka Accounting Standard-LKAS 26 Accounting and Reporting by Retirement Benefit Plans Sri Lanka Accounting

MIDDLESEX LONDON EMERGENCY MEDICAL SERVICES AUTHORITY

Financial Statements of MIDDLESEX LONDON EMERGENCY MEDICAL SERVICES AUTHORITY Year ended December 31, 2013 Statement of Financial Position December 31, 2013, with comparative information for 2012 Financial

Financial Statements of MIDDLESEX LONDON EMERGENCY MEDICAL SERVICES AUTHORITY Year ended December 31, 2013 Statement of Financial Position December 31, 2013, with comparative information for 2012 Financial

Options to Improve the Incorporation of PPPs into Debt Sustainability Analyses

4 th ANNUAL MEEETING OF PUBLIC-PRIVATE PARTNERSHIPS (PPPs) SENIOR OFFICIALS OECD Conference Centre Paris March 24-25 2011 Options to Improve the Incorporation of PPPs into Debt Sustainability Analyses

4 th ANNUAL MEEETING OF PUBLIC-PRIVATE PARTNERSHIPS (PPPs) SENIOR OFFICIALS OECD Conference Centre Paris March 24-25 2011 Options to Improve the Incorporation of PPPs into Debt Sustainability Analyses

Chapter 7. Financial Account

Chapter 7. Financial Account A. Concept and Coverage 7.1 The financial account will be defined, and its structure and purpose outlined along the lines of BPM5 paras. 313 342, BPT paras. 446 447, and the

Chapter 7. Financial Account A. Concept and Coverage 7.1 The financial account will be defined, and its structure and purpose outlined along the lines of BPM5 paras. 313 342, BPT paras. 446 447, and the

MACOMB COUNTY, MICHIGAN Notes to Basic Financial Statements December 31, 2014

Notes to Basic Financial Statements Note 8 Employees Retirement System Plan Description and Provision The County sponsors the Macomb County Employees Retirement System (the System ), a single employer

Notes to Basic Financial Statements Note 8 Employees Retirement System Plan Description and Provision The County sponsors the Macomb County Employees Retirement System (the System ), a single employer

COMPARISON OF INDIRECT COST MULTIPLIERS FOR VEHICLE MANUFACTURING

COMPARISON OF INDIRECT COST MULTIPLIERS FOR VEHICLE MANUFACTURING Technical Memorandum in support of Electric and Hybrid Electric Vehicle Cost Estimation Studies by Anant Vyas, Dan Santini, and Roy Cuenca

COMPARISON OF INDIRECT COST MULTIPLIERS FOR VEHICLE MANUFACTURING Technical Memorandum in support of Electric and Hybrid Electric Vehicle Cost Estimation Studies by Anant Vyas, Dan Santini, and Roy Cuenca

Employee Benefits* HKAS 19 Revised November 2009July 2011. Effective for annual periods beginning on or after 1 January 2005

HKAS 19 Revised November 2009July 2011 Effective for annual periods beginning on or after 1 January 2005 Hong Kong Accounting Standard 19 Employee Benefits* * This HKAS 19 is applicable for annual periods

HKAS 19 Revised November 2009July 2011 Effective for annual periods beginning on or after 1 January 2005 Hong Kong Accounting Standard 19 Employee Benefits* * This HKAS 19 is applicable for annual periods

Warwick Public School System

Warwick Public School System Actuarial Valuation Post Employment Benefits Other Than Pensions as of July 1, 2011 under Governmental Accounting Standards Board Statement No. 45 (GASB 45) (Estimated Disclosures

Warwick Public School System Actuarial Valuation Post Employment Benefits Other Than Pensions as of July 1, 2011 under Governmental Accounting Standards Board Statement No. 45 (GASB 45) (Estimated Disclosures

Q1 QUARTERLY GUIDE PENSIONS ACCOUNTING

Q1 QUARTERLY GUIDE PENSIONS ACCOUNTING As at 31 March 2015 Guidance for Finance Directors In association with 1 QUARTERLY GUIDE TO IAS 19 ASSUMPTIONS REPORT MARCH 2015 QUARTERLY GUIDE TO PENSIONS ACCOUNTING

Q1 QUARTERLY GUIDE PENSIONS ACCOUNTING As at 31 March 2015 Guidance for Finance Directors In association with 1 QUARTERLY GUIDE TO IAS 19 ASSUMPTIONS REPORT MARCH 2015 QUARTERLY GUIDE TO PENSIONS ACCOUNTING

Retirement Benefits in Hong Kong

Retirement Benefits in Hong Kong Introduction In Hong Kong, there are several types of retirement benefits sponsored by different parties as shown below. Government-sponsor - Old Age Allowances from the

Retirement Benefits in Hong Kong Introduction In Hong Kong, there are several types of retirement benefits sponsored by different parties as shown below. Government-sponsor - Old Age Allowances from the

International Accounting Standard 19 Employee Benefits

International Accounting Standard 19 Employee Benefits Objective The objective of this Standard is to prescribe the accounting and disclosure for employee benefits. The Standard requires an entity to recognise:

International Accounting Standard 19 Employee Benefits Objective The objective of this Standard is to prescribe the accounting and disclosure for employee benefits. The Standard requires an entity to recognise:

JOHN RALFE CONSULTING

Mr Andrew Lennard Accounting Standards Board Aldwych House 71-91 Aldwych London WC2B 4HN July 14th 2008 Dear Andrew Discussion Paper The Financial Reporting of Pensions January 2008 As you know I was a

Mr Andrew Lennard Accounting Standards Board Aldwych House 71-91 Aldwych London WC2B 4HN July 14th 2008 Dear Andrew Discussion Paper The Financial Reporting of Pensions January 2008 As you know I was a

Variable Annuity Pension Plans: A Balanced Approach to Retirement Risk

Variable Annuity Pension Plans: A Balanced Approach to Retirement Kelly Coffing, EA, FSA, MAAA Principal and Consulting Actuary Milliman, Seattle, Washington Grant Camp, EA, FSA, MAAA, Consulting Actuary

Variable Annuity Pension Plans: A Balanced Approach to Retirement Kelly Coffing, EA, FSA, MAAA Principal and Consulting Actuary Milliman, Seattle, Washington Grant Camp, EA, FSA, MAAA, Consulting Actuary

GN21: Actuarial Reporting on Post-Retirement Medical Plans

GN21: Actuarial Reporting on Post-Retirement Medical Plans Classification Recommended Practice Legislation or Authority Institute of Chartered Accountants in England and Wales. Accounting for Pensions

GN21: Actuarial Reporting on Post-Retirement Medical Plans Classification Recommended Practice Legislation or Authority Institute of Chartered Accountants in England and Wales. Accounting for Pensions

Financial Assets, Liabilities and Commitments

Financial Assets, Liabilities and Commitments Policy Statement Ref: A52923, 5.0 1 of 10 Policy name: Financial Assets, Liabilities and Commitments Policy number: Finance Key result areas: Finance Branch:

Financial Assets, Liabilities and Commitments Policy Statement Ref: A52923, 5.0 1 of 10 Policy name: Financial Assets, Liabilities and Commitments Policy number: Finance Key result areas: Finance Branch:

EXPLANATION OF PEP PLAN ISSUES

EXPLANATION OF PEP PLAN ISSUES Introduction Pension Equity Plans (PEPs), or more properly PEP formulas, provide for a benefit defined as an accumulated percentage of pay. PEP formulas often closely resemble

EXPLANATION OF PEP PLAN ISSUES Introduction Pension Equity Plans (PEPs), or more properly PEP formulas, provide for a benefit defined as an accumulated percentage of pay. PEP formulas often closely resemble

ADVISORY. KPMG Pensions Accounting Survey in the Netherlands. 2014 year-end preview and 2013 year-end retrospective. kpmg.nl

KPMG Pensions Accounting Survey in the Netherlands 2014 year-end preview and 2013 year-end retrospective kpmg.nl ADVISORY 2 KPMG Pensions Accounting Survey in the Netherlands Introduction 3 Headlines 4

KPMG Pensions Accounting Survey in the Netherlands 2014 year-end preview and 2013 year-end retrospective kpmg.nl ADVISORY 2 KPMG Pensions Accounting Survey in the Netherlands Introduction 3 Headlines 4

LDI Liability-driven investment ONS Office for National Statistics. See Company: trading status. Aggregate funding position. Closed (to new members)

") Glossary Active member In relation to an occupational pension scheme, a person who is in pensionable service under the scheme. Acronyms LDI Liability-driven investment ONS Office for National Statistics

Glossary Active member In relation to an occupational pension scheme, a person who is in pensionable service under the scheme. Acronyms LDI Liability-driven investment ONS Office for National Statistics

Governmental Accounting Standards Series

NO. 327-B JUNE 2012 Governmental Accounting Standards Series Statement No. 67 of the Governmental Accounting Standards Board Financial Reporting for Pension Plans an amendment of GASB Statement No. 25

NO. 327-B JUNE 2012 Governmental Accounting Standards Series Statement No. 67 of the Governmental Accounting Standards Board Financial Reporting for Pension Plans an amendment of GASB Statement No. 25

Jewish Community Foundation of San Diego. Consolidated Financial Statements and Supplemental Information

Jewish Community Foundation of San Diego Consolidated Financial Statements and Supplemental Information Years Ended June 30, 2015 and 2014 Consolidated Financial Statements and Supplemental Information

Jewish Community Foundation of San Diego Consolidated Financial Statements and Supplemental Information Years Ended June 30, 2015 and 2014 Consolidated Financial Statements and Supplemental Information

Client(s): Jon Traditional. Katie Traditional. Advisor:

: Jon Traditional. Katie Traditional. Advisor:") Table of Contents Table of Contents... 1 Disclaimer... 2 Basics of Life... 4 Survivor Costs... 5 Survivor Costs vs. Resources... 9 Survivor Portfolio... 13 Survivor Costs vs. Resources w/ Add'l... 17 Survivor

Table of Contents Table of Contents... 1 Disclaimer... 2 Basics of Life... 4 Survivor Costs... 5 Survivor Costs vs. Resources... 9 Survivor Portfolio... 13 Survivor Costs vs. Resources w/ Add'l... 17 Survivor

THE OPEN HEARTH ASSOCIATION, INC. Report on Audit of Financial Statements. December 31, 2011

Report on Audit of Financial Statements December 31, 2011 CONTENTS Independent Auditors Report 1-2 Statements of Financial Position December 31, 2011 and 2010 3 Statements of Activities for the Years Ended

Report on Audit of Financial Statements December 31, 2011 CONTENTS Independent Auditors Report 1-2 Statements of Financial Position December 31, 2011 and 2010 3 Statements of Activities for the Years Ended

Working Party on National Accounts

Unclassified STD/CSTAT/WPNA(2013)11 STD/CSTAT/WPNA(2013)11 Unclassified Organisation de Coopération et de Développement Économiques Organisation for Economic Co-operation and Development 10-Oct-2013 English

Unclassified STD/CSTAT/WPNA(2013)11 STD/CSTAT/WPNA(2013)11 Unclassified Organisation de Coopération et de Développement Économiques Organisation for Economic Co-operation and Development 10-Oct-2013 English

Subject 4: The Influence of International Accounting Standards on Pension and Insurance Programs and the Progress to a Global Standard

Subject 4: The Influence of International Accounting Standards on Pension and Insurance Programs and the Progress to a Global Standard Sir David Tweedie, Chairman of the IASB Wendy E. McFee, Mercer Human

Subject 4: The Influence of International Accounting Standards on Pension and Insurance Programs and the Progress to a Global Standard Sir David Tweedie, Chairman of the IASB Wendy E. McFee, Mercer Human

Regional Transportation Authority Pension Plan (A Pension Trust Fund of the Regional Transportation Authority)

") (A Pension Trust Fund of the Regional Transportation Authority) Financial Report Year Ended December 31, 2014 Table of Contents Page Independent Auditor s Report 1-2 Management s Discussion and Analysis

(A Pension Trust Fund of the Regional Transportation Authority) Financial Report Year Ended December 31, 2014 Table of Contents Page Independent Auditor s Report 1-2 Management s Discussion and Analysis

UNIVERSITY CITY CHILDREN S CENTER AND SUBSIDIARY CONSOLIDATED FINANCIAL STATEMENTS WITH SUPPLEMENTARY INFORMATION DECEMBER 31, 2014 AND 2013

AND SUBSIDIARY CONSOLIDATED FINANCIAL STATEMENTS WITH SUPPLEMENTARY INFORMATION DECEMBER 31, 2014 AND 2013 DECEMBER 31, 2014 AND 2013 Table of Contents Page Independent Auditors' Report 1 Consolidated

AND SUBSIDIARY CONSOLIDATED FINANCIAL STATEMENTS WITH SUPPLEMENTARY INFORMATION DECEMBER 31, 2014 AND 2013 DECEMBER 31, 2014 AND 2013 Table of Contents Page Independent Auditors' Report 1 Consolidated

OBJECTIVE SCOPE Paragraphs 1 6 DEFINITIONS 7 SHORT-TERM EMPLOYEE BENEFITS 8 23 Recognition and Measurement 10 22

160 Accounting Standard (AS) 15 Employee Benefits Contents OBJECTIVE SCOPE Paragraphs 1 6 DEFINITIONS 7 SHORT-TERM EMPLOYEE BENEFITS 8 23 Recognition and Measurement 10 22 All Short-term Employee Benefits

160 Accounting Standard (AS) 15 Employee Benefits Contents OBJECTIVE SCOPE Paragraphs 1 6 DEFINITIONS 7 SHORT-TERM EMPLOYEE BENEFITS 8 23 Recognition and Measurement 10 22 All Short-term Employee Benefits

Are Defined Benefit Funds still Beneficial?

Are Defined Benefit Funds still Beneficial? Prepared by Greg Einfeld Presented to the Actuaries Institute Financial Services Forum 30 April 1 May 2012 Melbourne This paper has been prepared for Actuaries

Are Defined Benefit Funds still Beneficial? Prepared by Greg Einfeld Presented to the Actuaries Institute Financial Services Forum 30 April 1 May 2012 Melbourne This paper has been prepared for Actuaries

United Cerebral Palsy, Inc. Financial Report September 30, 2013

Financial Report September 30, 2013 Contents Independent Auditor s Report 1 2 Financial Statements Statement Of Financial Position 3 Statement Of Activities 4 Statement Of Functional Expenses 5 Statement

Financial Report September 30, 2013 Contents Independent Auditor s Report 1 2 Financial Statements Statement Of Financial Position 3 Statement Of Activities 4 Statement Of Functional Expenses 5 Statement

APPALACHIAN REGIONAL COMMISSION FINANCIAL STATEMENTS

APPALACHIAN REGIONAL COMMISSION FINANCIAL STATEMENTS As of And For The Years Ended APPALACHIAN REGIONAL COMMISSION TABLE OF CONTENTS Page(s) Independent Auditor s Report... 1-3 Financial Statements Balance

APPALACHIAN REGIONAL COMMISSION FINANCIAL STATEMENTS As of And For The Years Ended APPALACHIAN REGIONAL COMMISSION TABLE OF CONTENTS Page(s) Independent Auditor s Report... 1-3 Financial Statements Balance

Financial statements. Sherbrooke Restoration Commission. March 31, 2015

Financial statements Sherbrooke Restoration Commission March 31, 2015 Contents Page Independent auditor s report 1 Statement of financial activities 2 Statement of financial position 3 Statement of changes

Financial statements Sherbrooke Restoration Commission March 31, 2015 Contents Page Independent auditor s report 1 Statement of financial activities 2 Statement of financial position 3 Statement of changes

The treatment of guarantees in UK public accounts and in the System of National Accounts

The treatment of guarantees in UK public accounts and in the System of National Accounts Jeff Golland, HM Treasury, UK Association de comptabilité nationale, Paris, 18 January 2006 Summary 2 Background

The treatment of guarantees in UK public accounts and in the System of National Accounts Jeff Golland, HM Treasury, UK Association de comptabilité nationale, Paris, 18 January 2006 Summary 2 Background

Lifestyle Assessment and Financial Overview (Part A)

") Achieving your lifestyle goals Lifestyle Assessment and Financial Overview (Part A) Thank you in advance for taking the time to provide the information requested overleaf. We believe that the creation,

Achieving your lifestyle goals Lifestyle Assessment and Financial Overview (Part A) Thank you in advance for taking the time to provide the information requested overleaf. We believe that the creation,

Fundamentals of Current Pension Funding and Accounting For Private Sector Pension Plans

Fundamentals of Current Pension Funding and Accounting For Private Sector Pension Plans An Analysis by the Pension Committee of the American Academy of Actuaries July 2004 The American Academy of Actuaries

Fundamentals of Current Pension Funding and Accounting For Private Sector Pension Plans An Analysis by the Pension Committee of the American Academy of Actuaries July 2004 The American Academy of Actuaries

IPSAS 25 EMPLOYEE BENEFITS

IPSAS 25 EMPLOYEE BENEFITS Acknowledgment This International Public Sector Accounting Standard (IPSAS) is drawn primarily from International Accounting Standard (IAS) 19, Employee Benefits published by

IPSAS 25 EMPLOYEE BENEFITS Acknowledgment This International Public Sector Accounting Standard (IPSAS) is drawn primarily from International Accounting Standard (IAS) 19, Employee Benefits published by

Chapter 10. Primary Distribution of Income Account

Chapter 10. Primary Distribution of Income Account A. Concept and Coverage 10.1 The purpose of the primary distribution of income account will be stated along the lines of the introduction to Chapter VII

Chapter 10. Primary Distribution of Income Account A. Concept and Coverage 10.1 The purpose of the primary distribution of income account will be stated along the lines of the introduction to Chapter VII

Accounting Discount Rate Assumption Calculating Spread Above Provincial Yields

Educational Note Supplement Accounting Discount Rate Assumption Calculating Spread Above Provincial Yields Task Force on Pension and Post-retirement Benefit Accounting Discount Rates August 2013 Document

Educational Note Supplement Accounting Discount Rate Assumption Calculating Spread Above Provincial Yields Task Force on Pension and Post-retirement Benefit Accounting Discount Rates August 2013 Document

Financial Statements of. Canadian Cancer Society, Saskatchewan Division. Year ended January 31, 2015

Financial Statements of Canadian Cancer Society, Saskatchewan Division Independent Auditor s report To the Board of Directors of the Canadian Cancer Society, Saskatchewan Division We have audited the accompanying

Financial Statements of Canadian Cancer Society, Saskatchewan Division Independent Auditor s report To the Board of Directors of the Canadian Cancer Society, Saskatchewan Division We have audited the accompanying

SUMITOMO DENSETSU CO., LTD. AND SUBSIDIARIES. Consolidated Financial Statements

SUMITOMO DENSETSU CO., LTD. AND SUBSIDIARIES Consolidated Financial Statements Report of Independent Public Accountants To the Board of Directors of Sumitomo Densetsu Co., Ltd. : We have audited the consolidated

SUMITOMO DENSETSU CO., LTD. AND SUBSIDIARIES Consolidated Financial Statements Report of Independent Public Accountants To the Board of Directors of Sumitomo Densetsu Co., Ltd. : We have audited the consolidated

BRITISH COLUMBIA INSTITUTE OF TECHNOLOGY

Consolidated Financial Statements of BRITISH COLUMBIA INSTITUTE OF TECHNOLOGY Consolidated Financial Statements Management Report Auditors' Report Consolidated Financial Statements Consolidated Statement

Consolidated Financial Statements of BRITISH COLUMBIA INSTITUTE OF TECHNOLOGY Consolidated Financial Statements Management Report Auditors' Report Consolidated Financial Statements Consolidated Statement

Report on Pension Charges in Ireland 2012

Report on Pension Charges in Ireland 2012 Table of Contents Executive Summary... 1 Preface... 21 Chapter 1 The Irish Pensions Landscape... 23 Chapter 2 Explaining Pension Charges... 31 Chapter 3 Research

Report on Pension Charges in Ireland 2012 Table of Contents Executive Summary... 1 Preface... 21 Chapter 1 The Irish Pensions Landscape... 23 Chapter 2 Explaining Pension Charges... 31 Chapter 3 Research

Updating BPM6 Issues for Consideration An Australian Perspective: The Treatment of Pension and Insurance Reserves

Twenty-Eighth Meeting of the IMF Committee on Balance of Payments Statistics Rio de Janeiro, Brazil October 27 29, 2015 BOPCOM 15/25 Updating BPM6 Issues for Consideration An Australian Perspective: The

Twenty-Eighth Meeting of the IMF Committee on Balance of Payments Statistics Rio de Janeiro, Brazil October 27 29, 2015 BOPCOM 15/25 Updating BPM6 Issues for Consideration An Australian Perspective: The