BEFORE YOU CLOSE: WHAT ABOUT TITLE GUARANTY REQUIREMENTS?

|

|

|

- Rafe McBride

- 8 years ago

- Views:

Transcription

1 BEFORE YOU CLOSE: WHAT ABOUT TITLE GUARANTY REQUIREMENTS? TABLE OF CONTENTS 1. How do I issue a Closing Protection Letter? -- Sample Closing Protection Letter 2. What kind of abstracting is required before and after closing? -- Title Guaranty Pre- and Post-Closing Options 3. When can the Form 900 be used? -- Non-Purchasing Financing Memo 4. When do we require a survey and what must it show? -- Affidavit of No New Improvements 5. Which endorsements should I choose? -- Comparison of Comprehensive 1 and Comprehensive 2 Endorsements 6. How do I give mechanic s lien coverage? -- Statement on Use of the Mechanics Notice and Lien Registry 7. How do I calculate premiums when the coverage is over $500,000? -- Premium Calculation Examples 8. How much information should I show on Schedule B exceptions? 9. Where do I show judgments that are in an attorney s title opinion? -- Iowa Code Section B Priority of recorded purchase money mortgage lien 10. Can I issue an owner s certificate? -- Title Guaranty Composite Mortgage Affidavit Unlocking New Opportunities Settlement Service Workshop March 11, 2014 Bob Skelley, Title Guaranty Residential Underwriter

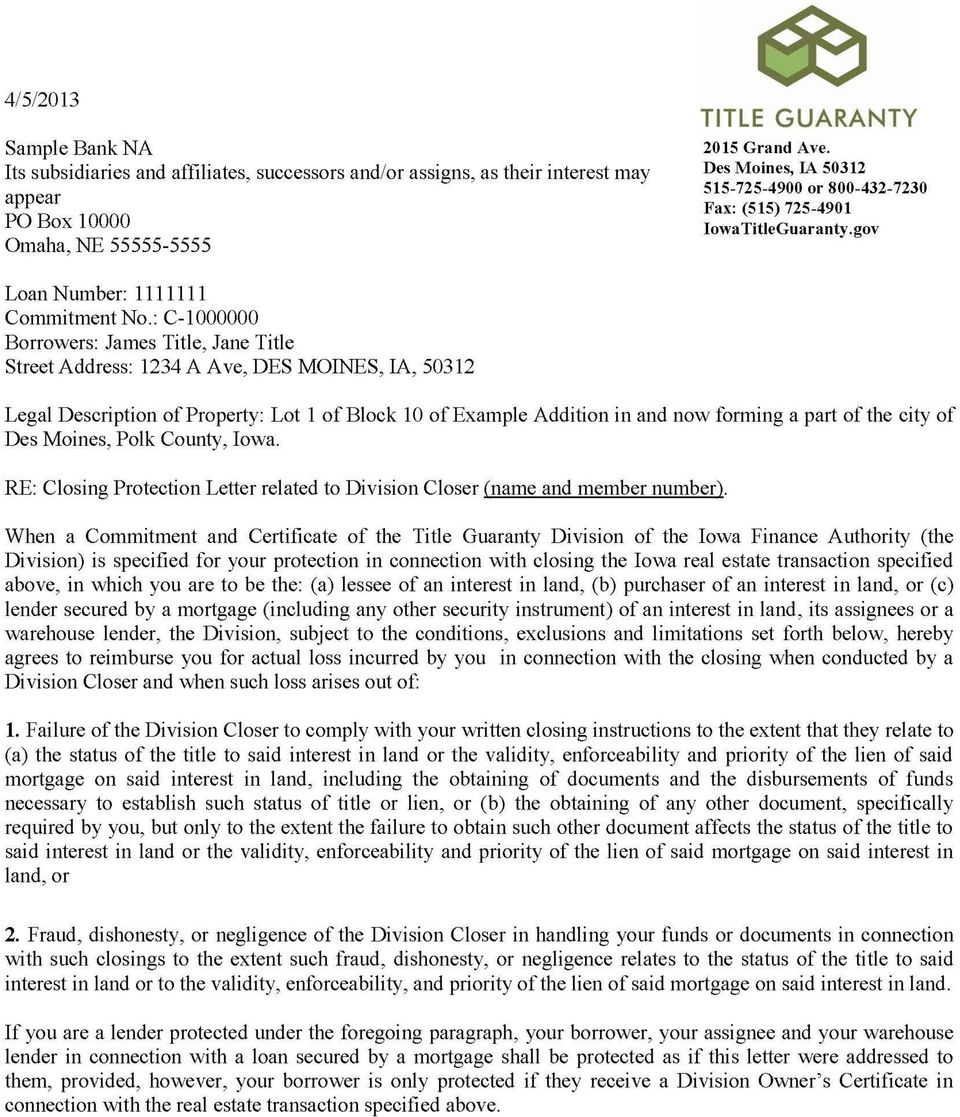

2 1. How do I issue a Closing Protection Letter? Title Guaranty Closing Protection Letters are a separate insurance policy to indemnify lenders and owners against acts or omissions on the part of division closers based upon the closing instructions. The protection from a Closing Protection Letter includes theft of settlement funds and failure to comply with written closing instructions that impact the title to the property. Closing Protection Letters may be issued only by participating attorneys, abstractors, and independent closers who have been approved as division closers. Application forms may be downloaded from the Title Guaranty website at There is no charge to issue a Closing Protection Letter. Closing Protection Letters include a GAP Rider at no charge. It is not necessary to issue the GAP Coverage Endorsement with a Closing Protection Letter. The GAP Rider guarantees the time period from the Effective Date of the Commitment through the date and time the deed and/or mortgage to be guaranteed are recorded. The abstractor must perform a Pre-Closing Search Certification ( day of closing search ) and if any adverse matters are disclosed, the closer may proceed to closing only after consulting with the participating attorney who examined the abstract and upon fulfilling any terms and conditions the participating attorney may require. The mortgage and any other appropriate documents must be filed immediately after closing. The division closer listed on the Closing Protection Letter MUST be the individual who is conducting the closing, including handling disbursements. Each Closing Protection Letter must be issued with a transaction-specific Title Guaranty Commitment. Blanket Closing Protection Letters are not available. If you issue a Closing Protection Letter, you must use the Rapid Certificate Program. In many closing instructions, the lender requires delivery of their lender s certificate within a deadline. The only way to meet this deadline and comply with the closing instructions may be to use the Rapid Certificate Program. If the closing does not occur, or if the details of the transaction change to the point that the Closing Protection Letter is no longer accurate, the field issuer is required to cancel the Closing Protection Letter. Attached is a sample of a Title Guaranty Closing Protection Letter.

3

4

5

6

7 2. What kind of abstracting is required before and after closing? The chart below, Title Guaranty Pre- and Post-Closing Options, describes the abstracting options available to the lender based upon certain scenarios. Of course, it is always an option to continue the abstract prior to closing and re-continue the abstract after closing, but depending upon the circumstances of the transaction, there may be other alternatives available. The abstractor must be involved in the transaction at some point, either pre- or post-closing. It is never an option to forego an abstractor s search throughout the entire closing process.

8 TITLE GUARANTY PRE- AND POST-CLOSING OPTIONS CPL or non-cpl Commitment? Purchase or Refinance CPL transaction CPL transaction Commitment required Commitment required Pre-Closing Options Post-Closing Options Purchase Abstract continuation Abstract continuation, or Post-Closing Search, or Search of recorded documents Refinance Abstract continuation or, Form Abstract continuation, or Form 901, or Search of recorded documents Non-CPL No commitment Purchase Abstract continuation Post-Closing Search, or abstract continuation Non-CPL No commitment Purchase Lien and title search Abstract continuation Non-CPL No commitment Refinance Form 900 1, or lien and title search, or abstract continuation Form 901, or abstract continuation Non-CPL With commitment Purchase Abstract continuation Post-Closing Search, or abstract continuation Non-CPL With commitment Refinance Form 900 1, or abstract continuation Form 901, or abstract continuation 1 Unless disqualified for the particular transaction NOTES: Attorney title opinions are mandatory for commitments and certificates issued by division staff, abstractors, and independent closers. Attorney title opinions are optional for commitments and certificates issued by attorneys. A CPL transaction requires the issuance of a commitment. A commitment must be based upon an abstract continuation or, in the case of a refinance, a Form 900 (unless disqualified). For a non-cpl purchase transaction where there is no commitment, the pre-closing options are either an abstract continuation or a lien and title search. If the abstract is continued pre-closing, the post-closing options are a Post-Closing Search or a final abstract continuation. If a lien and title search is performed pre-closing, then the only post-closing option is a final abstract continuation. There must be an abstract continuation either pre-closing or post-closing (or both). For a non-cpl refinance transaction where there is no commitment, the pre-closing options are either a Form 900 (unless disqualified), a lien and title search, or an abstract continuation. The post-closing options are either a Form 901 or an abstract continuation.

9 3. When can the Form 900 be used? The Title Guaranty Forms 900 and 901, (also called a Report of Title ) are designed to be a cost- and timesaving abstractor search tool to be used for simple non-purchase transactions. The Form 900/901 may be used for: The refinance of an existing mortgage by the same titleholders. A second, or junior, mortgage taken out by the same titleholders. A new mortgage taken out by the titleholders of the property when there is no current mortgage. The memo below is reprinted from the current Title Guaranty Manual and the Staff Supplement and outlines when the Form 900/901 may or may not be used. Mortgage secures residential property; There must be a residence on the property. The current zoning of the property does not necessarily disqualify the use of the Form 900/901. How the property is assessed does not necessarily disqualify the use of the Form 900/901. The number of acres is not a major consideration in determining whether or not a property is residential. Evidence of a farming operation, which will disqualify the use of the Form 900, may be the presence of several farming outbuildings or the presence of row crops on the parcel. A property that is deemed mixed use, in other words with a residence and a farming operation, is deemed agricultural and disqualifies the use of the Form 900/901. The deed vesting title in the borrower: There must be no change in the titleholders of the property since the last full-value deed, except: o A quit claim deed which removes a titleholder or titleholders or which adds a spouse as a titleholder may be accepted if there is no court proceeding. The abstractor must search the name of the person(s) being added to the title. o A deed which removes a titleholder that arises out of a court proceeding (i.e., a dissolution or an estate), may be accepted if in the opinion of the examining attorney, there is enough information in the Form 900 concerning the court proceeding for the attorney to render a proper title opinion. No court proceeding or recording regarding the legal description or possible encroachment exists that would require preparation of an abstract or abstract update; The legal description on the new mortgage must be the same as the legal description on the last fullvalue deed, except: o The exact same property (no more nor less land) that is described in a different manner may be accepted (i.e., the property was described by metes and bounds and is now described by a Plat of Survey ). o A change in the legal description that minimally reduces the size of the property may be accepted (i.e., removing the road right-of-way from the legal description). If not otherwise disqualified: The Form 900/901 may be used for the refinance of a residential rental property. The Form 900/901 may be used for the refinance of property that is owned by an entity or a trust. The Form 900/901 may be used for the refinance of a condominium unit.

10 Title Guaranty Manual: Article VI: Non-Purchase Financing Staff Supplement: Chapter 6. Non-Purchase Financing The Title Guaranty Report of Title is defined in Chapter 9 of the Iowa Administrative Code as a written or electronic short form of the abstract of title covering the borrower title, liens and encumbrances. This shall not be utilized by Participants when a titleholder is obtaining purchase financing. The Title Guaranty Report of Title may be utilized by Participants when a titleholder refinances or obtains an additional mortgage when the following criteria are satisfied: Mortgage secures an amount not more than $1,000,000; Mortgage secures residential property; (The number of acres is no longer a major consideration of whether a property is residential or ag land. There must be a 1-4 family residence and no evidence of a farming operation. A property with mixed use is deemed agricultural.) The deed vesting title in the borrower: o shows documentary transfer tax computed on the full value of the property (hereinafter referred to as the recorded full value deed ) or o is a tax, guardian, executor, administrator, receiver, referee assignee, or sheriff deed that has been recorded in the applicable county recorder s office for more than 10 years, and no action against said deed is found (refer to Iowa Code section ), then the deed may be relied upon as the root for the search; The current transaction is not a construction loan; (The Form 900, however, can be used when refinancing a construction loan into the end loan.) Name searches are run on the grantees in the recorded full value deed and any subsequent owners; No court proceeding or recording regarding the legal description or possible encroachment exists that would require preparation of an abstract or abstract update; and (This means there has been no change in the legal description of the property since the last abstract continuation. This scenario arises when an abstract covers a large parcel of several acres (usually an acreage) and the borrowers wish to refinance only a small part of the parcel, usually where the house is located. This poses some serious concerns regarding survey matters too.) The current transaction is not a payoff or refinancing of a real estate installment sale contract. (This is a change to the prior rules which would allow the Form 900 when refinancing an real estate installment contract.) (Note: the Form 900 may now be used when there is no current institutional mortgage on the property.) A Title Guaranty Report of Title may be used in other non-purchase financing transactions with written approval from the Division. (The Form 900 may be approved if there is a prior Title Guaranty certificate covering the property.)

11 4. When do we require a survey and what must it show? Title Guaranty requires a survey or a Real Property Inspection Report (RPIR), (sometimes called a Mortgage Inspection Report or a Mortgage Survey), in order to give survey coverage with a lender s certificate when the loan amount is more than $750,000. A survey or RPIR is required to give survey coverage with an owner s certificate of any amount if the Standard Exception Waiver Endorsement waiving standard exceptions #2 and #3 is issued. The drawing must show the lot lines and dimensions of the property, the location of the house and all improvements, all easements, setback lines, the driveway, and the street, and must show no possible encroachments. An ALTA survey is acceptable, but because of the cost it is not necessary if a RPIR is available. A RPIR is typically drawn by a surveyor or an engineering company. The RPIR must be signed by the surveyor and must be dated within six (6) months of the date of closing. For refinance transactions, an older RPIR may be accepted if it is accompanied by an executed Affidavit of No New Improvements (see sample below). A drawing by an appraiser usually does not meet our requirements because the appraiser normally does not search the public records for easements and setback lines. A copy of the plat of subdivision usually does not meet our requirements because it does not show the location of all improvements. A Foundation Survey usually does not meet our requirements because it is most often drawn before a new house is completed. A RPIR is not required if the property is a condominium. A RPIR is not required if the lender is granting a first mortgage and a junior mortgage where each mortgage is less than $750,000 but the aggregate or combined amounts exceed $750,000. If the lender does not require survey coverage or the comprehensive endorsement, the RPIR is not required. Title Guaranty recommends that the closer secure in writing a statement from the lender that they are waiving any requirement for survey coverage. Below is a link to the State of Iowa s web site, Commerce Department, Iowa Professional Licensing Bureau, for a list of licensed engineers and surveyors in the state:

12 State of Iowa County of: Commitment: AFFIDAVIT OF NO NEW IMPROVEMENTS RESIDENTIAL REAL PROPERTY INSPECTION REPORT (2014) The undersigned, being first duly sworn, deposes and states as follows: 1. I/We am/are the owner(s) of record described in the above referenced Commitment for title coverage. 2. I/We have not made or caused to be made any structural improvements or structural additions to existing improvements on the premises described in the above referenced Commitment since (date), except: 3. No structural improvements or additions to existing improvements were made on any adjacent property, which encroach (however slight the encroachment may be) onto the premises described in the above referenced Commitment since (date), except 4. I/We further state that the real property inspection report/drawing made by dated (a copy of which is attached hereto and made a part hereof,) is a correct and complete representation of all improvements now located on the premises in the above referenced Commitment and on all adjacent properties, except for. I/We have undertaken a complete and thorough investigation as to the condition of the premises and do not claim lack of knowledge or ignorance of fact should a difference, in fact, exist between the real property inspection report/drawing and the actual condition of the premises at the time of this affidavit. 5. This affidavit is given to the Title Guaranty Division, as an inducement to issue survey coverage on the Lender Certificate of title coverage to be applied for under the above Commitment, over questions of parties in possession, survey matters, and easements not shown of record. Dated: (Signature) (Typed Name) State of County of Signed and sworn or affirmed to before me on (date) By (name(s) of individual(s)) making statement. Signature and title of notarial officer Place notary stamp or seal here: My commission expires: NOTE: This affidavit is to be used only for a refinance of a residential property (residential building with 4 units or less). If any disclosures are made, contact Title Guaranty as an updated real property inspection report/drawing or survey may be required.

onto the premises described in the")

13 5. Which endorsements should I choose? The lender s closing instructions should clearly indicate which Title Guaranty endorsements are required by the lender. If there is any question or ambiguity, you should ask. The buyer(s) should tell their attorney, the lender, the closer, or the field issuer which endorsements, if any, they require. If you issue the Standard Exception Waiver Endorsement, the buyer(s) should tell you which of the five standard exceptions they want to have waived. The endorsement must be appropriate for the details of that transaction. For instance: To issue a Condominium Endorsement, the property must be a condominium (not a townhome or single family dwelling) with a legal description that describes the condominium in accordance with the provisions of Iowa Code Section 499.B. To issue a Planned Unit Development Endorsement, the property must be located within a planned unit development. To issue a Variable Rate Mortgage Endorsement, the mortgage must include a variable rate or ARM provision. To issue either Manufactured Housing Unit Endorsement, the property must include a mobile home, a modular home, or a manufactured home and not be located within a mobile home park or a manufactured housing community (i.e., ownership of the home, but a lease of the land). The owner of the manufactured home must also own the land upon which it is situated. To issue a Location Endorsement, there must be a residence located at the address of the property. To issue an Encroachment Endorsement or an Adverse Encroachment Endorsement, there must be an actual encroachment onto the subject property or from the subject property onto adjacent property, respectively. If there is a Rider to the guaranteed mortgage, the lender may require a corresponding endorsement from Title Guaranty, if available and if appropriate based upon underwriting standards. However, any appropriate endorsement may be issued, regardless of whether or not there is a Rider to the mortgage. Below is a comparison of the Comprehensive 1 Improved Land Endorsement and the Comprehensive 2 Lender s Restrictions, Encroachments, Minerals Endorsement.

14 COMPARISON OF COMPREHENSIVE 1 IMPROVED LAND ENDORSEMENT AND COMPREHENSIVE 2 LENDER S RESTRICTIONS, ENCROACHMENTS, MINERALS Comprehensive 1 Improved Land Free May not be issued for a construction loan Must have CMA to issue this endorsement: all survey, encroachment matters or other items disclosed on the CMA will appear as exceptions on Schedule B Part I Provides coverage for present violations of any any covenants, conditions, and restrictions Comprehensive 2 Lender s Restrictions, etc. $15.00 charge Based upon ALTA Form 9 endorsement May not be issued for a construction loan, vacant land, unsubdivided land, land platted by a county auditor, or land where mining operations are active and surface rights are in current use. Must have CMA to issue this endorsement: all survey, encroachment matters or other items disclosed on the CMA will appear as exceptions on Schedule B Part I Provides coverage for present violations of any covenants, conditions, and restrictions Provides some coverage for any future violations of any covenants, conditions, and restrictions occurring prior to the acquisition of title to the land. Provides some coverage for encroachments onto easements shown on Schedule B Provides some coverage for encroachments onto easements shown on Schedule B, and also encroachments onto adjoining land or any encroachment onto the subject property from adjoining land. Provides coverage for damage resulting from the future exercise of any right to use the surface of the subject property for the extraction or development of minerals. If there are other questions about which endorsement to use, feel free to provide the party with copies of both endorsements for them to compare and decide which one to use.

15 6. How do I give mechanic s lien coverage? The Iowa Secretary of State implemented the Mechanic s Notice and Lien Registry (MNLR) on January 1, The Registry is found on the Secretary s web site at On June 18, 2013, Title Guaranty issued a Statement on Use of the Mechanic s Notice and Lien Registry (reprinted below). As of June 18, 2013, Title Guaranty: No longer requires lien waivers from all contractors and subcontractors that have provided materials or labor to a construction project. No longer requires a list of all contractors or subcontractors that have provided materials or labor to a construction project. No longer solicits or accepts letters of credit from general contractors. As of June 18, 2013, Title Guaranty now requires or recommends: The closer or settlement agent is required to search the MNLR on the day of closing. It is recommended that the closer or settlement agent search the MNLR at the time the preliminary title opinion is written or at least one week in advance of closing to obtain a heads-up of any lien waivers or releases of mechanic s liens that may be needed. It is recommended that the closer or settlement agent search the MNLR at the time the mortgage is funded/filed in the case of a refinance. The issuer of any certificate in which mechanic s lien coverage is granted (lender or owner) is required to check the MNLR prior to issuing the certificate(s). There are a number of potential fields on the MNLR that may be searched depending upon the information available: MNLR number, legal description, tax parcel identification number, property address, property owner, general contractor/owner builder/subcontractor, or date-county-posting. Title Guaranty recommends that the closer and field issuer search more than one field and then document the results of that search with the date and time the search was performed. The closer or field issuer may engage the services of the abstractor to perform the search. Many abstractors are currently searching for and reporting mechanic s liens only, but they may be willing to search for Commencements of Work and Preliminary Notices if specifically requested. It is important that the closer or field issuer be aware of just what is being searched by the abstractor. Or, Title Guaranty will also accept the results of a search by the closer or field issuer without involving the abstractor. The closer and the field issuer must collect lien waivers or a proof of payment from any general or subcontractor who has posted a Commencement of Work or a Preliminary Notice to the MNLR as of the date and time of the search. The closer and the field issuer must obtain a release and satisfaction of any unreleased mechanic s lien that is posted to the MNLR as of the date and time of the search. The closer or field issuer is encouraged to post to the MNLR any lien waiver or a release and satisfaction of a mechanic s lien that they obtain in the course of their search, but Title Guaranty does not require the closer or field issuer to post these documents. If a release and satisfaction of a mechanic s lien or a lien waiver for a Commencement of Work or Preliminary Notice is not available, Title Guaranty requires the closer and field issuer to take the steps necessary to protect the buyer and/or the first lien status of the mortgage.

16 Statement on Use of the Mechanics Notice and Lien Registry June 18, 2013 Title Guaranty (TG) issues coverage, including priority over mechanic s liens, assuring the lender that the mortgage is in valid first lien position on the real estate. The process for issuing Title Guaranty commitments and certificates has not changed abstractors, attorneys and closing agents are to assure clear title in property transactions. TG expects all parties to follow the professional standards of practice set forth by the Iowa Land Title Association for the certification of abstracts and the Iowa State Bar Association for the writing of title opinions. The Mechanics Notice and Lien Registry (MNLR), a statewide web-based database located at the Secretary of State s office, replaces the filing of mechanics liens at the Clerk of Court, and as such, is necessary to assure that there are no liens superior or senior to the recorded mortgage. This is similar to the previous search of the clerk of courts office for mechanics liens. In order to preserve lien rights against residential real estate, the general contractor or owner/builder must post a Commencement of Work on the MNLR not less than 10 days after work begins on a property. A subcontractor must post a Preliminary Notice on the MNLR before the balance due is paid to the general contractor or the owner-builder. The Title Guaranty Board requires all Division closers to search the Mechanics Notice and Lien Registry at the time of closing and obtain either a lien waiver, proof of payment, or satisfaction from every contractor or material supplier that has posted a Commencement of Work, Preliminary Notice, or Mechanic s Lien on the MNLR. We believe that this process provides a secure, streamlined review, reducing regulation, yet efficiently determines lien risks. Title Guaranty will no longer require or accept letters of credit from builders. It is also no longer necessary to send copies of lien waivers to TG. The website to perform a search is: The search results can be printed out with a date and time stamp to prove when the search was completed (see search result print preview below).

17 7. How do I calculate premiums when the coverage is over $500,000? The Title Guaranty web site includes a premium calculator that will provide a quote for coverage amounts of $1,000,000 and under: For coverage amounts in excess of $1,000,000 please contact Title Guaranty for a premium quote. The $ base premium for purchase transactions (and the $90.00 base premium for refinance transactions) pays for coverage amounts up to and including $500,000. For a lender s certificate for more than $500,000 the premium would be $ (or $90.00 if it s a refinance) plus $1 for every $1,000 in coverage over $500,000. For instance, for a loan amount of $650,000 the lender s premium would be $ for a purchase ($ plus $150.00) or $ for a refinance ($90.00 plus $150.00). If you have a purchase transaction where the purchase price of the home is over $500,000 the premium for the owner s certificate (with no lender s coverage) is calculated the same way ($ plus $1 per $1,000 in coverage over $500,000). If the purchase price AND the mortgage amount are both over $500,000 you would calculate the premium based on the larger amount (usually the owner s) in the same way--$25.00 for the basic concurrent policy premium, plus $1 per $1,000 over $500,000 and the lender s premium would be a flat $ So, for a purchase price of $800,000 and a mortgage amount of $600,000 the premium would be $ ($25.00 base premium plus $ ($1 per $1,000 over $500,000) for the owner s certificate and $ for the lender s). Any endorsements for which there is a charge are still $ Commitments and Closing Protection Letters, including the GAP Rider, are still free. See the Chart below for samples of premium quotes based upon certain scenarios.

pays for coverage amounts up to and including $500,000. For a lender s certificate for more than $500,000 the premium would be $110.00 (or $90.")

18 Premium Calculation Examples Below are examples of how to calculate the Title Guaranty premium for various transactions. #1 Refinance Transaction Lender Coverage: $450,000 Lender Endorsements: EPA, Comp, Loc Lender Premium: $90.00 Owner Coverage: n/a Owner Endorsements: Owner Premium: None Total Premium Due: $90.00 #2 Refinance Transaction Lender Coverage: $800,000 Lender Endorsements: EPA, Comp, Var. Rat Lender Premium: $90 + $300 = $390 Owner Coverage: n/a Owner Endorsements: Owner Premium: None Total Premium Due: $ Base premium of $90 plus $1 per $1,000 over $500,000 #3 Sale Transaction Lender Coverage: $300,000 Lender Endorsements: EPA, Comp Lender Premium: $ Owner Coverage: $400,000 Owner Endorsements: None Owner Premium: Free Total Premium Due: $ #4 Sale Transaction Lender Coverage: $418,000 Lender Endorsements: EPA, Comp, Condo Lender Premium: $110 + $15 = $ Owner Coverage: $800,000 Owner Endorsements: None Owner Premium: $25 + $300 = $ Total Premium Due: $ Base premium of $110 plus $15 for condo; base premium of $25 plus $1 per $1,000 over $500K #5 Sale Transaction Lender Coverage: $600,000 Lender Endorsements: EPA, Comp, PUD Lender Premium: $110 + $15 = $ Owner Coverage: $950,000 Owner Endorsements: None Owner Premium: $25 + $450 = $ Total Premium Due: $ $1 per $1,000 over $500K is calculated on the higher coverage amount only #6 Sale Transaction Lender Coverage: $850,000 Lender Endorsements: EPA, Comp, Loc Lender Premium: $ Owner Coverage: $1,350,000 Owner Endorsements: Standard Ex Waiver Owner Premium: $25 + $850 + $15 = $890 Total Premium Due: $1, No discount for coverage amounts over $1,000,000

19 8. How much information should be shown on the Schedule B exceptions? The exceptions you show on Schedule B of a lender s certificate or an owner s certificate should include enough information that an interested party is able to locate the document based upon the information in the exception. In the case of documents recorded with the county recorder s office, the exception should include the name(s) of the parties, the filing date, and the book and page and/or document number of the recorded document. In the case of documents filed with the clerk of court, the exception should include the case number, filing date, and the name of the parties. Showing the amount of any judgment, costs, or interest is optional. Describing the title of the document or the type of document that is the subject of the exception is a good idea, such as utility easement, shared driveway agreement, restrictive covenants, etc. In the case of an easement, it is also a good idea to describe the property that the easement covers, such as the north 10 feet. It is acceptable, but not necessary, to elaborate as to the terms and conditions of the exception. Title Guaranty recognizes that in many cases with field issued commitments and certificates, the issuer will simply cut and paste from the attorney s title opinions, and this is also acceptable. Referring to an exception by the abstract entry number only is not acceptable.

of the parties, the filing date, and the book and page and/or document number of the")

20 9. Where do I show judgments that are in an attorney s title opinion? Any unpaid, unreleased judgments that are a lien on the guaranteed premises must be shown on Schedule B of any Title Guaranty lender s or owner s certificate, except: A judgment or lien that is being paid in installments (except a judgment or lien which attaches to the property in its entirety on the date entered) may be left off Schedule B if: o A review of the payment schedule reveals that the judgment is paid current through the date and filing date of the mortgage; or o A partial release and satisfaction through the date and filing date of the mortgage is filed with the Clerk of Court. An unpaid, unreleased judgment against the buyer, that is (1) being paid in installments, and (2) a lien in its entirety on the property upon the date entered, must be shown on Schedule B, Part 1 of the lender s certificate and Schedule B of the owner s certificate, even if the debtor is current in paying the installments. If the mortgage does not qualify as a purchase money mortgage (see Iowa Code Section B below), any unpaid, unreleased judgments against the buyer(s) that are currently a lien against the property must be shown in Schedule B, Part I, of the lender s certificate and on Schedule B of the owner s certificate. If the mortgage does qualify as a purchase money mortgage according to the statute, any unpaid, unreleased judgments against the buyer(s) that are currently a lien against the property may be shown in Schedule B, Part II, of the lender s certificate and on Schedule B of the owner s certificate. Any unpaid, unreleased judgments against the seller(s) that are currently a lien against the property must be shown in Schedule B, Part I, of the lender s certificate and on Schedule B of the owner s certificate. All unpaid, unreleased judgments against the buyer(s) or seller(s) must be shown on Schedule B of the owner s certificate. This includes any unpaid, unreleased judgments that are being paid in installments, even if the debtor is current in the installments. Paid but unreleased judgments against the buyer/borrower or the seller: If there is a judgment or judgments against either the buyer/borrower or the seller that the closer has paid off at closing, you may be able to issue the lender s certificate as a Rapid Certificate by showing the judgment(s) on Schedule B, Part I, as exceptions and then issuing an Endorsement Against Loss Lien for each of the judgments. Title Guaranty then asks that you take whatever steps are necessary to obtain a release of each judgment. You must be able to provide evidence showing that the judgment was paid off at closing. The Rapid Certificate Program may not be used to insure over judgments that were paid in a prior transaction. The Mortgage Release Program cannot help to release judgments. Title Guaranty does not require buyers searches, but strongly recommends that, if the abstractor does not perform a buyers search, then the mortgage should meet the statutory definition and qualify as a PMM. When showing a judgment in a title opinion, Title Guaranty requests that the examining attorney: Show whether or not the mortgage qualifies as a Purchase Money Mortgage State whether or not the mortgage is a first lien on the property (not a first mortgage lien ). Show the details of the judgment, including case number, names of parties, date the judgment was entered and against whom, amount of the judgment including unpaid costs or interest, any modifications of the judgment, and any payments made toward satisfaction of the judgment. State whether or not the judgment is superior or inferior to the guaranteed mortgage.

21 654.12B Priority of recorded purchase money mortgage lien. 1. The lien created by a recorded purchase money mortgage shall have priority over and is senior to preexisting judgments against the purchaser and any other right, title, interest, or lien arising either directly or indirectly by, through, or under the purchaser. A mortgage is a purchase money mortgage to the extent it is either: a. Taken or retained by the seller of the real estate to secure all or part of its price, including all costs in connection with the purchase. b. Taken by a lender who, by making an advance or incurring an obligation, provides funds to enable the purchaser to acquire rights in the real estate, including all costs in connection with the purchase, if the funds are in fact so used. Except when it is a refinancing of an existing purchase money mortgage between the same lender and purchaser and no new funds are advanced, a mortgage given to secure funds which are used to pay off another mortgage is not a purchase money mortgage. 2. If more than one purchase money mortgage exists, the first mortgage to be recorded has priority. In order to be entitled to the rights provided by this section, the mortgage must contain a recital that it is a purchase money mortgage. However, failure to include the recital in the mortgage shall not prevent a mortgage otherwise qualifying as a purchase money mortgage from being a purchase money mortgage for purposes other than this section. The rights in this section are in addition to, and the obligations are not in derogation of, all rights provided by common law. 95 Acts, ch 175, 2; 96 Acts, ch 1137, 1, 2; 2013 Acts, ch 30, 261

22 10. Can I order an owner s certificate? Title Guaranty owner s coverage is free under the following conditions: 1. The transaction is a purchase, or the borrowers are paying off a real estate contract and replacing it with a mortgage, or the borrowers are paying off a construction loan used to build a new home and replacing it with a mortgage. 2. A lender s certificate will be issued at the same time as the owner s certificate (otherwise called concurrent certificates). 3. The fair market value (usually the purchase price or appraised value) of the property is $500,000 or less. 4. The residential property will be the primary residence of the borrowers (not a second home, vacation home, or rental property). If the purchase transaction does not meet these four conditions, owner s coverage is still available at a nominal cost. An Owner Certificate will not be issued for less than the sale price of the property and in no event for less than the full value of the real property. The amount of owner s coverage is based upon the fair market value of the property. This is usually the purchase price, but it can also be the appraised value or the assessed value of the property. The buyers may obtain an owner s certificate, even if the loan amount is greater than the purchase price. Applying for owner s coverage is easy, but it is not automatic. The borrowers must signify their intent to accept the free owner s certificate by checking the Yes box in paragraph 3 of the For Purchaser(s) section of the Composite Mortgage Affidavit.

23 Composite Mortgage Affidavit Commitment No. Loan No. For Seller(s)/Owner(s) 1. No labor, materials or equipment have been furnished in the last 90 days, before the date of closing, on the property located at:. 2. To the best of my knowledge, there are no public improvements affecting the above described property prior to the date of closing that would cause a special property tax assessment against such property after the date of closing. 3. To the best of my knowledge, there are no unrecorded contracts, options, leases, easements or other agreements or interests affecting the above described property. 4. The improvements located upon the above described property are wholly contained within the property boundary and setback lines; and further that neighboring buildings, fences, walkways, driveways, eaves, drains, etc., do not encroach upon the above described property. 5. I am familiar with the covenants, conditions or restrictions, if any, for the above described property, and there are no known violations of said covenants, conditions or restrictions. 6. The undersigned affiant(s) knows that the matters herein stated are true and indemnify the Title Guaranty Division of the Iowa Finance Authority against loss, costs, damages and expenses of every kind incurred by it by reason of its reliance on the statements made herein. (Signature) (Typed Name) State of County of Signed and sworn or affirmed to before me on (date) by (name(s) of individual(s)) making statement. Signature and title of notarial officer Place notary stamp or seal here: My commission expires:. For Purchaser(s) 1. Confirm that the above described property is/will will not be my primary place of residence. 2. Confirm marital status: married single 3. For Purchasers, free Owner s coverage is available for the full purchase price of owner-occupied properties valued up to and including $500,000, when issued with Lender s Coverage. Check YES to receive coverage or NO to decline coverage. Purchase Price $. (Signature) (Typed Name) State of County of Signed and sworn or affirmed to before me on (date) by (name(s) of individual(s)) making statement. Signature and title of notarial officer Place notary stamp or seal here: My commission expires:.

24 ALTA Best Practices Framework: Title Insurance and Settlement Company Best Practices Version 2.0 Published July 19, 2013 ALTA Best Practices Framework: Title Insurance and Settlement Company Best Practices Version 2.0 Published July 19, 2013 Page 1 of 8 Copyright 2013 American Land Title Association. All rights reserved. For more information about the ALTA Best Practices Framework, visit

25 ALTA Best Practices Framework: Title Insurance and Settlement Company Best Practices Version 2.0 Published July 19, 2013 ALTA Best Practices Framework The ALTA Best Practices Framework has been developed to assist lenders in satisfying their responsibility to manage third party vendors. The ALTA Best Practices Framework is comprised of the following documentation needed by a company electing to implement such a program. ALTA Best Practices Framework: Title Insurance and Settlement Company Best Practices ALTA Best Practices Framework: Assessment Procedures ALTA Best Practices Framework: Certification Package (Package includes 3 Parts) Version History and Notes Date Version Notes 1/2/2013 None Publication of the ALTA Title Insurance and Settlement Company Best Practices, approved by the ALTA Board of Governors on December 20, /19/ Publication of the revised ALTA Title Insurance and Settlement Company Best Practices, along with other documents in the ALTA Best Practices Framework, approved by the ALTA Board of Governors on July 19, Page 2 of 8 Copyright 2013 American Land Title Association. All rights reserved. For more information about the ALTA Best Practices Framework, visit

26 ALTA Best Practices Framework: Title Insurance and Settlement Company Best Practices Version 2.0 Published July 19, 2013 Mission Statement Title Insurance and Settlement Company Best Practices ALTA seeks to guide its membership on best practices to protect consumers, promote quality service, provide for ongoing employee training, and meet legal and market requirements. These practices are voluntary and designed to help members illustrate to consumers and clients the industry s professionalism and best practices to help ensure a positive and compliant real estate settlement experience. These best practices are not intended to encompass all aspects of title or settlement company activity. ALTA is publishing these best practices for the mortgage lending and real estate settlement industry. ALTA accepts comments from stakeholders as the Association seeks to continually improve these best practices. A formal committee of ALTA members regularly reviews and makes improvements to these best practices, seeking comment on each revision. Definitions Background Check: A background check is the process of compiling and reviewing both confidential and public employment, address, and criminal records of an individual or an organization. Background checks may be limited in geographic scope. This provision and use of these reports are subject to the limitations of federal and state law. Company: The entity implementing these best practices. Escrow: A transaction in which an impartial third party acts in a fiduciary capacity for the seller, buyer, borrower, or lender in performing the closing for a real estate transaction according to local practice and custom. The escrow holders have fiduciary responsibility for prudent processing, safeguarding and accounting for funds and documents entrusted to them. Escrow Trust Account: An account to hold funds in trust for third parties, including parties to a real estate transaction. These funds are held subject to a fiduciary capacity as established by written instructions. Federally Insured Financial Institutions: A financial institution that has its deposits insured by an instrumentality of the federal government, including the Federal Deposit Insurance Corporation (FDIC) and National Credit Union Administration (NCUA). Licenses: Title Agent or Producer License or registration, or any other business licensing requirement as required by state law, or a license to practice law, where applicable. Non-public Personal Information: Personally identifiable data such as information provided by a customer on a form or application, information about a customer s transactions, or any other information about a customer which is otherwise unavailable to the general public. NPI includes first name or first initial and last name coupled with any of the following: Social Security Number, driver s license number, state-issued ID number, credit card number, debit card number, or other financial account numbers. Page 3 of 8 Copyright 2013 American Land Title Association. All rights reserved. For more information about the ALTA Best Practices Framework, visit

27 ALTA Best Practices Framework: Title Insurance and Settlement Company Best Practices Version 2.0 Published July 19, 2013 Positive Pay or Reverse Positive Pay: Any system by which the authenticity of a check is determined before payment is made by the financial institution against which the check is written. Settlement: In some areas called a closing. The process of completing a real estate transaction in accordance with written instructions during which deeds, mortgages, leases and other required instruments are executed and/or delivered, an accounting between the parties is made, the funds are disbursed and the appropriate documents are recorded. Trial Balance: A list of all open individual escrow ledger record balances at the end of the reconciliation period. Three-Way Reconciliation: A three-way reconciliation is a method for discovering shortages (intentional or otherwise), charges that must be reimbursed or any type of errors or omissions that must be corrected in relation to an Escrow Trust Account. This requires the escrow trial balance, the book balance and the reconciled bank balance to be compared. If all three parts do not agree, the difference shall be investigated and corrected. Best Practices 1. Best Practice: Establish and maintain current License(s) as required to conduct the business of title insurance and settlement services. Purpose: Maintaining state mandated insurance licenses and corporate registrations (as applicable) helps ensure the Company remains in good standing with the state. Procedures to meet this best practice: Establish and maintain applicable business License(s). Establish and maintain compliance with Licensing, registration, or similar requirements with the applicable state regulatory department or agency. Establish and maintain appropriate compliance with ALTA s Policy Forms Licensing requirement. 2. Best Practice: Adopt and maintain appropriate written procedures and controls for Escrow Trust Accounts allowing for electronic verification of reconciliation. Purpose: Appropriate and effective escrow controls and staff training help title and settlement companies meet client and legal requirements for the safeguarding of client funds. These procedures help ensure accuracy and minimize the exposure to loss of client funds. Settlement companies may engage outside contractors to conduct segregation of trust accounting duties. Procedures to meet this best practice: Escrow funds and operating accounts are separately maintained. o Escrow funds or other funds the Company maintains under a fiduciary duty to another are not commingled with the Company s operating account or an employee or manager s personal account. Escrow Trust Accounts are prepared with Trial Balances. Page 4 of 8 Copyright 2013 American Land Title Association. All rights reserved. For more information about the ALTA Best Practices Framework, visit

28 ALTA Best Practices Framework: Title Insurance and Settlement Company Best Practices Version 2.0 Published July 19, 2013 o On at least a monthly basis, Escrow Trust Accounts are prepared with Trial Balances ( Three-Way Reconciliation ), listing all open escrow balances. Escrow Trust Accounts are reconciled. o On at least a daily basis, reconciliation of the receipts and disbursements of the Escrow Trust Account is performed o On at least a monthly basis, a Three-Way Reconciliation is performed reconciling the bank statement, check book and Trial Balances. o Segregation of duties is in place to help ensure the reliability of the reconciliation and reconciliations are conducted by someone other than those with signing authority. o Results of the reconciliation are reviewed by management and are accessible electronically by the Company s contracted underwriter(s). Escrow Trust Accounts are properly identified. o Accounts are identified as escrow or trust accounts. Appropriate identification appears on all account-related documentation including bank statements, bank agreements, disbursement checks and deposit tickets. Outstanding file balances are documented. Transactions are conducted by authorized employees only. o Only those employees whose authority has been defined to authorize bank transactions may do so. Appropriate authorization levels are set by the Company and reviewed for updates annually. Former employees are immediately deleted as listed signatories on all bank accounts. Unless directed by the beneficial owner, Escrow Trust Accounts are maintained in Federally Insured Financial Institutions. Utilize Positive Pay or Reverse Positive Pay, Automated Clearing House blocks and international wire blocks, if available. o Background Checks are completed in the hiring process. At least every three years, obtain Background Checks going back five years for all employees who have access to customer funds. Ongoing training is conducted for employees in management of escrow funds and escrow accounting. 3. Best Practice: Adopt and maintain a written privacy and information security program to protect Non-public Personal Information as required by local, state and federal law. Purpose: Federal and state laws (including the Gramm-Leach-Bliley Act) require title companies to develop a written information security program that describes the procedures they employ to protect Nonpublic Personal Information. The program must be appropriate to the Company s size and complexity, the nature and scope of the Company s activities, and the sensitivity of the customer information the Company handles. A Company evaluates and adjusts its program in light of relevant circumstances, including changes in the Company s business or operations, or the results of security testing and monitoring. Procedures to meet this best practice: Physical security of Non-public Personal Information. Page 5 of 8 Copyright 2013 American Land Title Association. All rights reserved. For more information about the ALTA Best Practices Framework, visit

PASSAIC VALLEY TITLE SERVICE, INC. ALTA Best Practices Manual

PASSAIC VALLEY TITLE SERVICE, INC. ALTA Best Practices Manual July 2015 Page 1 of 7 1. Best Practice: Passaic Valley Title Service, Inc. [PVTS] has established and maintains all of the necessary License(s)

PASSAIC VALLEY TITLE SERVICE, INC. ALTA Best Practices Manual July 2015 Page 1 of 7 1. Best Practice: Passaic Valley Title Service, Inc. [PVTS] has established and maintains all of the necessary License(s)

ALTA Title Insurance & Settlement Company Best Practices

ALTA Title Insurance & Settlement Company Best Practices N e w C a s t l e T i t l e 7 5 0 N o r t h 3 r d S t r e e t, S u i t e B ( 6 0 8 ) 7 8 3-9 2 6 5 ( 6 0 8 ) 7 8 3-9 2 6 6 5 / 2 2 / 2 0 1 5 0 5/22/15

ALTA Title Insurance & Settlement Company Best Practices N e w C a s t l e T i t l e 7 5 0 N o r t h 3 r d S t r e e t, S u i t e B ( 6 0 8 ) 7 8 3-9 2 6 5 ( 6 0 8 ) 7 8 3-9 2 6 6 5 / 2 2 / 2 0 1 5 0 5/22/15

Title Insurance and Settlement Company Best Practices

Title Insurance and Settlement Company Best Practices Wednesday, January 2, 2013 Mission Statement Title Insurance and Settlement Company Best Practices ALTA seeks to guide its membership on best practices

Title Insurance and Settlement Company Best Practices Wednesday, January 2, 2013 Mission Statement Title Insurance and Settlement Company Best Practices ALTA seeks to guide its membership on best practices

Fidelity Land Title, Ltd. Title Insurance and Settlement Company Best Practices

Fidelity Land Title, Ltd. Title Insurance and Settlement Company Best Practices Title Insurance and Settlement Company Best Practices Mission Statement ALTA seeks to guide its membership on best practices

Fidelity Land Title, Ltd. Title Insurance and Settlement Company Best Practices Title Insurance and Settlement Company Best Practices Mission Statement ALTA seeks to guide its membership on best practices

Hogan Land Title Company Best Practices In full compliance with ALTA. Updated August 2015

Hogan Land Title Company Best Practices In full compliance with ALTA Updated August 2015 Hogan Land Title 2015 Mission Statement Hogan Land Title Company has developed this Best Practices Manual in accordance

Hogan Land Title Company Best Practices In full compliance with ALTA Updated August 2015 Hogan Land Title 2015 Mission Statement Hogan Land Title Company has developed this Best Practices Manual in accordance

CHICAGO TITLE INSURANCE COMPANY LOAN POLICY SCHEDULE A

LOAN POLICY SCHEDULE A POLICY NUMBER 72307-555555 Agent File No. : 55-555555 Lender Loan No. : 55-55555555 DATE OF POLICY AMOUNT OF INSURANCE $250,000.00 1. Name of Insured: Bank of America and/or its

LOAN POLICY SCHEDULE A POLICY NUMBER 72307-555555 Agent File No. : 55-555555 Lender Loan No. : 55-55555555 DATE OF POLICY AMOUNT OF INSURANCE $250,000.00 1. Name of Insured: Bank of America and/or its

SCHEDULE OF RATES FOR TITLE INSURANCE THE STATE OF LOUISIANA. LIRC#s: DEMT-130142099 DEMT- 130142690

SCHEDULE OF RATES FOR TITLE INSURANCE IN THE STATE OF LOUISIANA FILED WITH THE LOUISIANA DEPARTMENT OF INSURANCE TO BE EFFECTIVE AS TO ORDERS RECEIVED ON OR AFTER October 1, 2015 LIRC#s: DEMT-130142099

SCHEDULE OF RATES FOR TITLE INSURANCE IN THE STATE OF LOUISIANA FILED WITH THE LOUISIANA DEPARTMENT OF INSURANCE TO BE EFFECTIVE AS TO ORDERS RECEIVED ON OR AFTER October 1, 2015 LIRC#s: DEMT-130142099

TRUE TITLE BEST PRACTICES

TRUE TITLE BEST PRACTICES Mission Statement The American Land Title Association (ALTA) seeks to guide its membership on best practices to protect consumers, promote quality service, provide for ongoing

TRUE TITLE BEST PRACTICES Mission Statement The American Land Title Association (ALTA) seeks to guide its membership on best practices to protect consumers, promote quality service, provide for ongoing

SCHEDULE OF RATES FOR TITLE INSURANCE IN THE STATE OF OHIO

SCHEDULE OF RATES FOR TITLE INSURANCE IN THE STATE OF OHIO EFFECTIVE AS TO ORDERS RECEIVED ON OR AFTER DECEMBER 1, 2008 OHPC-125878699 Ohio Title Insurance Rating Bureau, Inc. 2715 Tuller Parkway Dublin,

SCHEDULE OF RATES FOR TITLE INSURANCE IN THE STATE OF OHIO EFFECTIVE AS TO ORDERS RECEIVED ON OR AFTER DECEMBER 1, 2008 OHPC-125878699 Ohio Title Insurance Rating Bureau, Inc. 2715 Tuller Parkway Dublin,

CHAPTER 10 COMMONLY USED ENDORSEMENTS

CHAPTER 10 COMMONLY USED ENDORSEMENTS This section contains various endorsements that are commonly used with Owner and/or Mortgagee policies. ATG Basic Forms and Procedures - Illinois Page 10-1 COMMONLY

CHAPTER 10 COMMONLY USED ENDORSEMENTS This section contains various endorsements that are commonly used with Owner and/or Mortgagee policies. ATG Basic Forms and Procedures - Illinois Page 10-1 COMMONLY

SCHEDULE OF RATES FOR TITLE INSURANCE IN THE STATE OF OHIO

SCHEDULE OF RATES FOR TITLE INSURANCE IN THE STATE OF OHIO EFFECTIVE AS TO ORDERS RECEIVED ON OR AFTER OCTOBER 1, 2010 OHPC #: SHNF-126711624 Ohio Title Insurance Rating Bureau, Inc. 2715 Tuller Parkway

SCHEDULE OF RATES FOR TITLE INSURANCE IN THE STATE OF OHIO EFFECTIVE AS TO ORDERS RECEIVED ON OR AFTER OCTOBER 1, 2010 OHPC #: SHNF-126711624 Ohio Title Insurance Rating Bureau, Inc. 2715 Tuller Parkway

Title 33: PROPERTY. Chapter 9: MORTGAGES OF REAL PROPERTY. Table of Contents

Title 33: PROPERTY Chapter 9: MORTGAGES OF REAL PROPERTY Table of Contents Subchapter 1. GENERAL PROVISIONS... 3 Section 501. FORMS... 3 Section 501-A. "POWER OF SALE"... 3 Section 502. ENTRY BY MORTGAGEE...

Title 33: PROPERTY Chapter 9: MORTGAGES OF REAL PROPERTY Table of Contents Subchapter 1. GENERAL PROVISIONS... 3 Section 501. FORMS... 3 Section 501-A. "POWER OF SALE"... 3 Section 502. ENTRY BY MORTGAGEE...

UNDERWRITING BULLETIN - TEXAS

UNDERWRITING BULLETIN - TEXAS No. 01 DATE: May 7, 2010 RE: General Underwriting Guidelines The purpose of this initial Bulletin is to provide concise summaries of WFG s underwriting positions in areas

UNDERWRITING BULLETIN - TEXAS No. 01 DATE: May 7, 2010 RE: General Underwriting Guidelines The purpose of this initial Bulletin is to provide concise summaries of WFG s underwriting positions in areas

COMMONWEALTH LAND TITLE INSURANCE COMPANY

COMMONWEALTH LAND TITLE INSURANCE COMPANY TITLE INSURANCE RATES AND CHARGES FOR THE STATE OF MAINE EFFECTIVE: NOVEMBER 12, 2012 (Unless Otherwise Specified Herein) TABLE OF CONTENTS SECTION 1... 1 TITLE

COMMONWEALTH LAND TITLE INSURANCE COMPANY TITLE INSURANCE RATES AND CHARGES FOR THE STATE OF MAINE EFFECTIVE: NOVEMBER 12, 2012 (Unless Otherwise Specified Herein) TABLE OF CONTENTS SECTION 1... 1 TITLE

Chicago Title Insurance Company www.northcarolina.ctt.com

Chicago Title Insurance Company www.northcarolina.ctt.com THE CHICAGO ENHANCED HOMEOWNER S POLICY UNDERWRITING REQUIREMENTS AT A GLANCE The Property must: Be a One-to Four residential homeplace Be Improved

Chicago Title Insurance Company www.northcarolina.ctt.com THE CHICAGO ENHANCED HOMEOWNER S POLICY UNDERWRITING REQUIREMENTS AT A GLANCE The Property must: Be a One-to Four residential homeplace Be Improved

DELAWARE TITLE INSURANCE RATING BUREAU RATING MANUAL EFFECTIVE AS AMENDED THROUGH 03/01/2015

DELAWARE TITLE INSURANCE RATING BUREAU RATING MANUAL EFFECTIVE AS AMENDED THROUGH 03/01/2015 MANUAL OF DELAWARE TITLE INSURANCE RATING BUREAU 150 Strafford Avenue, Suite 215 P.O. Box 393 Wayne, Pennsylvania

DELAWARE TITLE INSURANCE RATING BUREAU RATING MANUAL EFFECTIVE AS AMENDED THROUGH 03/01/2015 MANUAL OF DELAWARE TITLE INSURANCE RATING BUREAU 150 Strafford Avenue, Suite 215 P.O. Box 393 Wayne, Pennsylvania

Title Insurance Commitment

Form No. 1343 ALTA Plain Language Commitment Title Insurance Commitment ISSUED BY Issued By AGREEMENT TO ISSUE POLICY We agree to issue policy to you according to the terms of the Commitment. When we show

Form No. 1343 ALTA Plain Language Commitment Title Insurance Commitment ISSUED BY Issued By AGREEMENT TO ISSUE POLICY We agree to issue policy to you according to the terms of the Commitment. When we show

MANUAL OF THE TITLE INSURANCE RATING BUREAU OF PENNSYLVANIA

MANUAL OF THE TITLE INSURANCE RATING BUREAU OF PENNSYLVANIA 150 Strafford Avenue, Suite 215 P.O. Box 395 Wayne, Pennsylvania 19087-0395 Phone: (610) 995-9995 E-mail: TIRBOP@titlebureaus.com NOTICE THIS

MANUAL OF THE TITLE INSURANCE RATING BUREAU OF PENNSYLVANIA 150 Strafford Avenue, Suite 215 P.O. Box 395 Wayne, Pennsylvania 19087-0395 Phone: (610) 995-9995 E-mail: TIRBOP@titlebureaus.com NOTICE THIS

First American Title Insurance Company COMMITMENT INFORMATION SHEET

COMMITMENT INFORMATION SHEET The Title Insurance Commitment is a legal contract between you and the Company. It is issued to show the basis on which we will issue a Title Insurance Policy to you. The Policy

COMMITMENT INFORMATION SHEET The Title Insurance Commitment is a legal contract between you and the Company. It is issued to show the basis on which we will issue a Title Insurance Policy to you. The Policy

Real Estate Finance: Missouri Mark Murray, Armstrong Teasdale LLP

Real Estate Finance: Missouri Mark Murray, Armstrong Teasdale LLP This Article is published by Practical Law Company on its PLC Law Department web service at http://us.practicallaw.com/3-500-4162. A Q&A

Real Estate Finance: Missouri Mark Murray, Armstrong Teasdale LLP This Article is published by Practical Law Company on its PLC Law Department web service at http://us.practicallaw.com/3-500-4162. A Q&A

First American Title Insurance Company

COMMITMENT INFORMATION SHEET The Title Insurance Commitment is a legal contract between you and the Company. It is issued to show the basis on which we will issue a Title Insurance Policy to you. The Policy

COMMITMENT INFORMATION SHEET The Title Insurance Commitment is a legal contract between you and the Company. It is issued to show the basis on which we will issue a Title Insurance Policy to you. The Policy

ALTA Commitment (6-17-06) Commitment Page 1 Commitment Number: NCSJEF

Commitment Page 1 Commitment Number: NCSJEF") = ALTA Commitment (6-17-06) Commitment Page 1 - NCS 1125 17th Street, Suite 750 Denver, Colorado 80202 Phone: (303)876-1112 Fax:(877)235-9185 DATE: FILE NUMBER: PROPERTY ADDRESS:, OWNER/BUYER: / YOUR REFERENCE

= ALTA Commitment (6-17-06) Commitment Page 1 - NCS 1125 17th Street, Suite 750 Denver, Colorado 80202 Phone: (303)876-1112 Fax:(877)235-9185 DATE: FILE NUMBER: PROPERTY ADDRESS:, OWNER/BUYER: / YOUR REFERENCE

Agency Escrow Accounting Standards.

Agency Escrow Accounting Standards. Title Insurers State regulatory divisions, financial institutions, national groups, and others rely on Title Insurance underwriters to develop programs and practices

Agency Escrow Accounting Standards. Title Insurers State regulatory divisions, financial institutions, national groups, and others rely on Title Insurance underwriters to develop programs and practices

Real Estate Lawyers Association of North Carolina Standards of Practice May 9, 2011 Version Purpose:

Real Estate Lawyers Association of North Carolina Standards of Practice May 9, 2011 Version Purpose: Formed in February 2011 by a group of attorneys licensed to practice law in North Carolina, the Real

Real Estate Lawyers Association of North Carolina Standards of Practice May 9, 2011 Version Purpose: Formed in February 2011 by a group of attorneys licensed to practice law in North Carolina, the Real

RATE AND RULES FOR THE STATE OF OHIO

RATE AND RULES FOR THE STATE OF OHIO EFFECTIVE: MARCH 1, 2015 WFG National Title Insurance Company 2711 Middleburg Drive, Suite 312 Columbia, SC 29204 Ph: (803) 799-4747 Fax: (803) 799-4443 INDEX OTIRB

RATE AND RULES FOR THE STATE OF OHIO EFFECTIVE: MARCH 1, 2015 WFG National Title Insurance Company 2711 Middleburg Drive, Suite 312 Columbia, SC 29204 Ph: (803) 799-4747 Fax: (803) 799-4443 INDEX OTIRB

CHICAGO TITLE INSURANCE COMPANY

CHICAGO TITLE INSURANCE COMPANY TITLE INSURANCE RATES AND CHARGES FOR THE STATE OF MAINE EFFECTIVE: NOVEMBER 12, 2012 (Unless Otherwise Specified Herein) TABLE OF CONTENTS SECTION I... 1 DEFINITIONS...

CHICAGO TITLE INSURANCE COMPANY TITLE INSURANCE RATES AND CHARGES FOR THE STATE OF MAINE EFFECTIVE: NOVEMBER 12, 2012 (Unless Otherwise Specified Herein) TABLE OF CONTENTS SECTION I... 1 DEFINITIONS...

WHAT IS TITLE INSURANCE?

WHAT IS TITLE INSURANCE? A title is the collective ownership records of a piece of real estate, including the transfer of any property rights and any loans using the property as collateral. A clear line

WHAT IS TITLE INSURANCE? A title is the collective ownership records of a piece of real estate, including the transfer of any property rights and any loans using the property as collateral. A clear line

Real Estate Finance: Arizona Clare H. Abel, Burch & Cracchiolo, P.A.

Real Estate Finance: Arizona Clare H. Abel, Burch & Cracchiolo, P.A. This Article is published by Practical Law Company on its PLC Real Estate web service at http://us.practicallaw.com/3-500-5703. A Q&A

Real Estate Finance: Arizona Clare H. Abel, Burch & Cracchiolo, P.A. This Article is published by Practical Law Company on its PLC Real Estate web service at http://us.practicallaw.com/3-500-5703. A Q&A

SCHEDULE OF RATES INDIANA

SCHEDULE OF RATES FOR THE STATE OF INDIANA Effective as of July 1, 2013 WFG National Title Insurance Company 2711 Middleburg Drive, Suite 312 Columbia, SC 29204 Ph: (803) 799-4747 Fax: (803) 799-4443 TABLE

SCHEDULE OF RATES FOR THE STATE OF INDIANA Effective as of July 1, 2013 WFG National Title Insurance Company 2711 Middleburg Drive, Suite 312 Columbia, SC 29204 Ph: (803) 799-4747 Fax: (803) 799-4443 TABLE

ISSUED BY. This Commitment shall not be valid or binding until countersigned by an authorized officer of the Company or an agent of the Company.

Commitment for Title Insurance ISSUED BY Commitment First American Title Insurance Company 5011612 - NCS-533241FL6NY FIRST AMERICAN TITLE INSURANCE COMPANY, a California corporation (the Company ), for

Commitment for Title Insurance ISSUED BY Commitment First American Title Insurance Company 5011612 - NCS-533241FL6NY FIRST AMERICAN TITLE INSURANCE COMPANY, a California corporation (the Company ), for

Glossary of Title Insurance Terms

Glossary of Title Insurance Terms abstract of title The condensed history of the title to a particular parcel of real estate, consisting of a summary of the original grant and all subsequent conveyances

Glossary of Title Insurance Terms abstract of title The condensed history of the title to a particular parcel of real estate, consisting of a summary of the original grant and all subsequent conveyances

LAND TITLE INSURANCE CORPORATION RATE MANUAL FOR THE STATE OF ARKANSAS

LAND TITLE INSURANCE CORPORATION RATE MANUAL FOR THE STATE OF ARKANSAS ALL COUNTIES 3033 East First Avenue, Suite 605 Denver, CO 80206 Effective: January 1, 2015 1 TABLE OF CONTENTS Owner's Insurance 's

LAND TITLE INSURANCE CORPORATION RATE MANUAL FOR THE STATE OF ARKANSAS ALL COUNTIES 3033 East First Avenue, Suite 605 Denver, CO 80206 Effective: January 1, 2015 1 TABLE OF CONTENTS Owner's Insurance 's

RATE AND RULES ARIZONA

RATE AND RULES FOR THE STATE OF ARIZONA EFFECTIVE DATE: February 15, 2014 WFG National Title Insurance Company 2711 Middleburg Drive, Suite 206 Columbia, SC 29204 Ph: (803) 799-4747 Fax: (803) 799-4443

RATE AND RULES FOR THE STATE OF ARIZONA EFFECTIVE DATE: February 15, 2014 WFG National Title Insurance Company 2711 Middleburg Drive, Suite 206 Columbia, SC 29204 Ph: (803) 799-4747 Fax: (803) 799-4443

All inquiries concerning the charges for title insurance and forms in this manual should be directed to the following:

This manual is for the use of Stewart Title Guaranty Company's ( Stewart or Underwriter ) Title Insurance Policy Issuing Attorneys, Agents, and Offices. Any other use or reproduction of this manual is

This manual is for the use of Stewart Title Guaranty Company's ( Stewart or Underwriter ) Title Insurance Policy Issuing Attorneys, Agents, and Offices. Any other use or reproduction of this manual is

Land Title Endorsement Manual. Feb 2015

Land Title Endorsement Manual Feb 2015 Welcome- There are two ways to find endorsements in this manual. 1) Use the table. -On the following pages is a table listing endorsement numbers, a brief description,

Land Title Endorsement Manual Feb 2015 Welcome- There are two ways to find endorsements in this manual. 1) Use the table. -On the following pages is a table listing endorsement numbers, a brief description,

Florida Foreclosure Attorneys, PLLC 4855 Technology Way, Suite 630 Boca Raton, FL 33431 Phone: 561-391-8600 Fax: Chicago Title Insurance Company

Florida Foreclosure Attorneys, PLLC 4855 Technology Way, Suite 630 Boca Raton, FL 33431 Phone: 561-391-8600 Fax: Chicago Title Insurance Company COMMITMENT FOR TITLE INSURANCE SCHEDULE A 1. Effective Date:

Florida Foreclosure Attorneys, PLLC 4855 Technology Way, Suite 630 Boca Raton, FL 33431 Phone: 561-391-8600 Fax: Chicago Title Insurance Company COMMITMENT FOR TITLE INSURANCE SCHEDULE A 1. Effective Date:

RESIDENCE TRANSACTION EXPENSES - HOME PURCHASE

Items Payable In Connection With Loan: (Section 800 on HUD-I) Loan Origination Charge Line 801 The FTR allows for up to 1% of the loan amount to be reimbursed if lender charges are assessed in lieu of

Items Payable In Connection With Loan: (Section 800 on HUD-I) Loan Origination Charge Line 801 The FTR allows for up to 1% of the loan amount to be reimbursed if lender charges are assessed in lieu of

Model Policies and Procedures. Revised: January, 2014

Model Policies and Procedures Revised: January, 2014 Acknowledgement: A special thank you to the undaunting and relentless professionals of the Escrow Institute of California National Affairs Committee.

Model Policies and Procedures Revised: January, 2014 Acknowledgement: A special thank you to the undaunting and relentless professionals of the Escrow Institute of California National Affairs Committee.

Real Estate Ownership: Arizona Clare H. Abel, Burch & Cracchiolo, P.A.

Real Estate Ownership: Arizona Clare H. Abel, Burch & Cracchiolo, P.A. This Article is published by Practical Law Company on its PLC Real Estate web service at http://us.practicallaw.com/8-500-5927. A

Real Estate Ownership: Arizona Clare H. Abel, Burch & Cracchiolo, P.A. This Article is published by Practical Law Company on its PLC Real Estate web service at http://us.practicallaw.com/8-500-5927. A

FIDELITY NATIONAL TITLE INSURANCE COMPANY

FIDELITY NATIONAL TITLE INSURANCE COMPANY TITLE INSURANCE RATES AND CHARGES FOR THE STATE OF TENNESSEE EFFECTIVE: July 19, 2012 (Unless Otherwise Noted Herein) Table of Contents All Counties... 1 1.0 Master

FIDELITY NATIONAL TITLE INSURANCE COMPANY TITLE INSURANCE RATES AND CHARGES FOR THE STATE OF TENNESSEE EFFECTIVE: July 19, 2012 (Unless Otherwise Noted Herein) Table of Contents All Counties... 1 1.0 Master

Lawyers Title 620 N. Grandstaff Drive, Auburn, IN 46706

Lawyers Title 620 N. Grandstaff Drive, Auburn, IN 46706 American Land Title Association ALTA Commitment Form Adopted 6-17-06 FIDELITY NATIONAL TITLE INSURANCE COMPANY SCHEDULE A Loan No.: 37-5-19B Title

Lawyers Title 620 N. Grandstaff Drive, Auburn, IN 46706 American Land Title Association ALTA Commitment Form Adopted 6-17-06 FIDELITY NATIONAL TITLE INSURANCE COMPANY SCHEDULE A Loan No.: 37-5-19B Title

Title Insurance and Settlement Company Best Practices. American Land Title Association

Title Insurance and Settlement Company Best Practices American Land Title Association Current Forces at Work Dodd Frank Wall Street Reform & Consumer Protection Act of 2010 Established the Consumer Financial

Title Insurance and Settlement Company Best Practices American Land Title Association Current Forces at Work Dodd Frank Wall Street Reform & Consumer Protection Act of 2010 Established the Consumer Financial

NON-RESIDENTS PURCHASING REAL PROPERTY IN THE U.S.

NON-RESIDENTS PURCHASING REAL PROPERTY IN THE U.S. A. The Attorneys Role in the Purchase of Real Estate The purchase of real estate in the U.S. without the proper assistance can become a complex transaction.

NON-RESIDENTS PURCHASING REAL PROPERTY IN THE U.S. A. The Attorneys Role in the Purchase of Real Estate The purchase of real estate in the U.S. without the proper assistance can become a complex transaction.

T-17 - Planned Unit Development. You must send this email before 5pm tomorrow to receive credit for this seminar!

Welcome to TRGC s Internet Conference Training Program. At the end of this seminar you will be given a password that shows you attended the entirety of this seminar. You will need to send an email to ict@trgc.com

Welcome to TRGC s Internet Conference Training Program. At the end of this seminar you will be given a password that shows you attended the entirety of this seminar. You will need to send an email to ict@trgc.com

CHICAGO TITLE INSURANCE COMPANY

CHICAGO TITLE INSURANCE COMPANY By: Mark Griffith State Underwriting Counsel, Chicago Title Insurance Company Construction loans present a unique set of circumstances requiring special consideration when

CHICAGO TITLE INSURANCE COMPANY By: Mark Griffith State Underwriting Counsel, Chicago Title Insurance Company Construction loans present a unique set of circumstances requiring special consideration when

Title Insurance and Settlement Company Best Practices. American Land Title Association

Title Insurance and Settlement Company Best Practices American Land Title Association Future of the Land Title Industry Working groups helping to identify steps to ensure the title industry continues to

Title Insurance and Settlement Company Best Practices American Land Title Association Future of the Land Title Industry Working groups helping to identify steps to ensure the title industry continues to

Chapter 16. Transfer of Ownership Rights and Interests A. TITLE AND EVIDENCE OF GOOD AND MARKETABLE TITLE DEFINITION OF TITLE

Chapter 16 Transfer of Ownership Rights and Interests A. TITLE AND EVIDENCE OF GOOD AND MARKETABLE TITLE DEFINITION OF TITLE In Georgia, the title to real property is the means or the evidence by which

Chapter 16 Transfer of Ownership Rights and Interests A. TITLE AND EVIDENCE OF GOOD AND MARKETABLE TITLE DEFINITION OF TITLE In Georgia, the title to real property is the means or the evidence by which

Standard Procedures and Controls for the Title Industry. Prepared by the ALTA Internal Auditing Committee ALTA

Standard Procedures and Controls for the Title Industry Prepared by the ALTA Internal Auditing Committee ALTA The American Land Title Association, founded in 1907, is the national trade association and

Standard Procedures and Controls for the Title Industry Prepared by the ALTA Internal Auditing Committee ALTA The American Land Title Association, founded in 1907, is the national trade association and

STANDARD LAND PURCHASE AND SALE AGREEMENT [#505] (With Contingencies)

![STANDARD LAND PURCHASE AND SALE AGREEMENT [#505] (With Contingencies)](/thumbs/40/20844275.jpg "STANDARD LAND PURCHASE AND SALE AGREEMENT [#505] (With Contingencies)") STANDARD LAND PURCHASE AND SALE AGREEMENT [#505] (With Contingencies) The parties make this Agreement this day of,. This Agreement supersedes and replaces all obligations made in any prior Contract To

STANDARD LAND PURCHASE AND SALE AGREEMENT [#505] (With Contingencies) The parties make this Agreement this day of,. This Agreement supersedes and replaces all obligations made in any prior Contract To

Title/Settlement Agent Application

Title/Settlement Agent Application Completed Forms MUST be returned to Live Well Financial, Inc.: Email: counterpartyapproval@livewellfinancial.com *This application to be returned to above email address

Title/Settlement Agent Application Completed Forms MUST be returned to Live Well Financial, Inc.: Email: counterpartyapproval@livewellfinancial.com *This application to be returned to above email address

Chicago Title Insurance Company

Chicago Title Insurance Company COMMITMENT FOR TITLE INSURANCE Issued by Chicago Title Insurance Company Chicago Title Insurance Company, a Nebraska Corporation ('Company'), for a valuable consideration,

Chicago Title Insurance Company COMMITMENT FOR TITLE INSURANCE Issued by Chicago Title Insurance Company Chicago Title Insurance Company, a Nebraska Corporation ('Company'), for a valuable consideration,

Fidelity National Title Company

Fidelity National Title Company PRELIMINARY REPORT In response to the application for a policy of title insurance referenced herein, Fidelity National Title Company hereby reports that it is prepared to

Fidelity National Title Company PRELIMINARY REPORT In response to the application for a policy of title insurance referenced herein, Fidelity National Title Company hereby reports that it is prepared to

TEXAS HOME EQUITY AFFIDAVIT AND AGREEMENT (First Lien)

") After Recording Please Return To: [Company Name] [Name of Natural Person] [Street Address] [City, State, Zip Code] [To Be Recorded With Security Instrument. Space Above This Line for Recording Data] TEXAS

After Recording Please Return To: [Company Name] [Name of Natural Person] [Street Address] [City, State, Zip Code] [To Be Recorded With Security Instrument. Space Above This Line for Recording Data] TEXAS

NOW PLEASE REVIEW THIS PACKAGE AND FOLLOW THE INSTRUCTIONS TO GET YOU SALE STARTED.

Thank you for contacting EnTrust Title Agency, LLC. Please find enclosed our for sale by owner package. This includes all of the required documents for selling property in the State of Ohio in addition

Thank you for contacting EnTrust Title Agency, LLC. Please find enclosed our for sale by owner package. This includes all of the required documents for selling property in the State of Ohio in addition

TOP 20 TITLE ISSUES In no particular order, here are brief summaries of the top 20 title issues that can arise in a real estate transaction: 1. Trusts 2. Power of Attorney 3. Death 4. Divorce 5. Foreclosure

TOP 20 TITLE ISSUES In no particular order, here are brief summaries of the top 20 title issues that can arise in a real estate transaction: 1. Trusts 2. Power of Attorney 3. Death 4. Divorce 5. Foreclosure

Real Estate Finance: Vermont

View the online version at http://us.practicallaw.com/4-575-9565 Real Estate Finance: Vermont R. PRESCOTT JAUNICH AND KANE H. SMART, DOWNS RACHLIN MARTIN PLLC, WITH PRACTICAL LAW REAL ESTATE A Q&A guide

View the online version at http://us.practicallaw.com/4-575-9565 Real Estate Finance: Vermont R. PRESCOTT JAUNICH AND KANE H. SMART, DOWNS RACHLIN MARTIN PLLC, WITH PRACTICAL LAW REAL ESTATE A Q&A guide

First American Title Insurance Company COMMITMENT INFORMATION SHEET

First American Title Insurance Company COMMITMENT INFORMATION SHEET The Title Insurance Commitment is a legal contract between you and the Company. It is issued to show the basis on which we will issue

First American Title Insurance Company COMMITMENT INFORMATION SHEET The Title Insurance Commitment is a legal contract between you and the Company. It is issued to show the basis on which we will issue

TITLE & ESCROW OVERVIEW

WE MAKE COMPLEX EASY. TITLE & ESCROW OVERVIEW The following materials are intended only for educational and informational purposes. They do not contain a complete analysis of the laws, regulations and

WE MAKE COMPLEX EASY. TITLE & ESCROW OVERVIEW The following materials are intended only for educational and informational purposes. They do not contain a complete analysis of the laws, regulations and

ESCROW FEES AND CHARGES

ESCROW FEES AND CHARGES FOR USE IN THE STATE OF ARIZONA (Unless Otherwise Specified Herein) Table of Contents GENERAL RULES...1 CHAPTER I PURCHASE TRANSACTION RATES...2 1.1. RESIDENTIAL TRANSACTIONS...2

ESCROW FEES AND CHARGES FOR USE IN THE STATE OF ARIZONA (Unless Otherwise Specified Herein) Table of Contents GENERAL RULES...1 CHAPTER I PURCHASE TRANSACTION RATES...2 1.1. RESIDENTIAL TRANSACTIONS...2

California Land Title Association