THE IRA GENERAL S PLAN SM ADDRESSING THE CONCERNS OF THE AFFLUENT SENIOR CITIZEN

|

|

|

- Bruce Hines

- 8 years ago

- Views:

Transcription

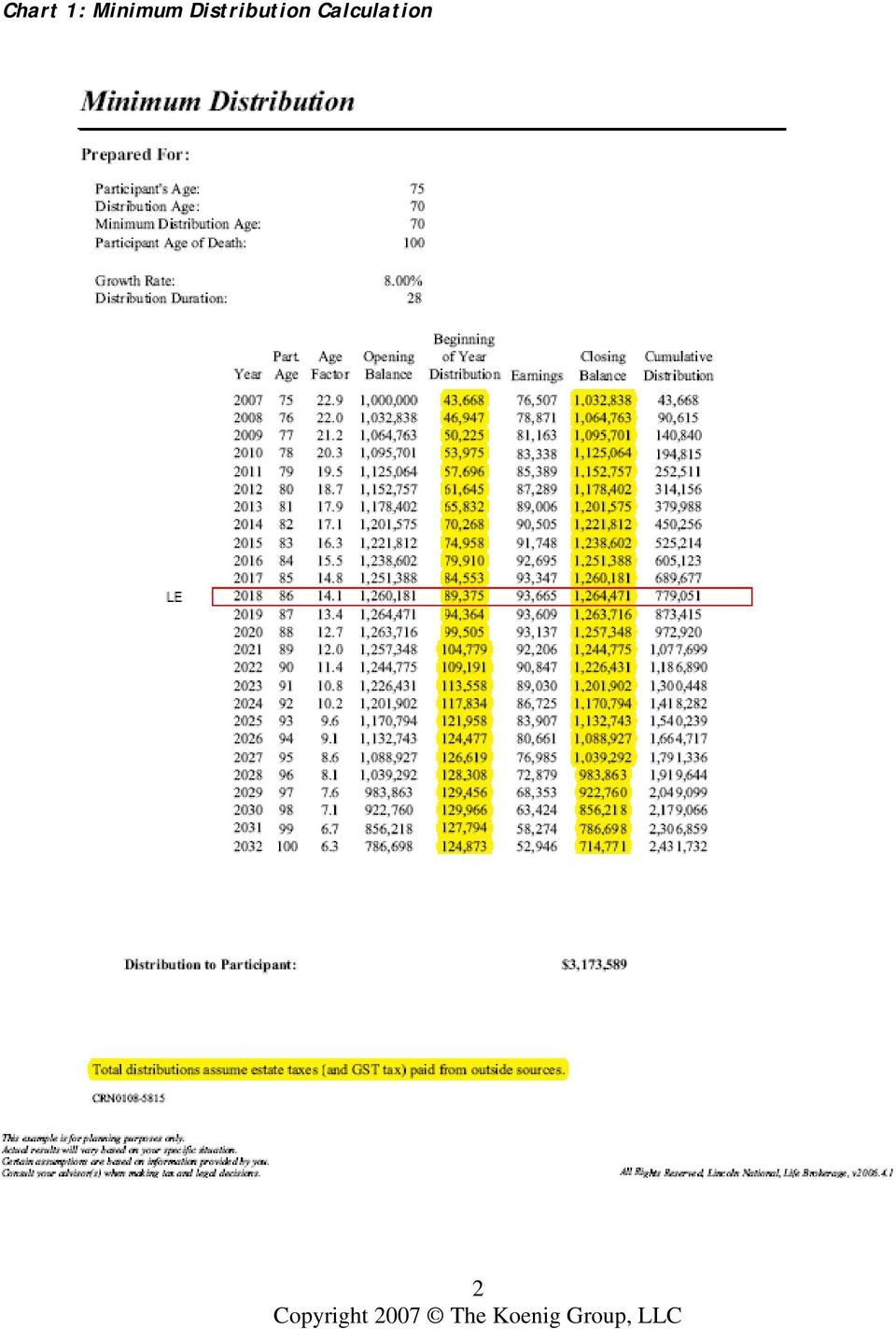

1 THE IRA GENERAL S PLAN SM ADDRESSING THE CONCERNS OF THE AFFLUENT SENIOR CITIZEN BY JOEL KOENIG, CLU AND ALISON L. SEGALL, CLU, CHFC MEMBERS THE KOENIG GROUP, LLC LOOKING BACK IN HISTORY TO PROJECT THE FUTURE People are living longer and many, even the most affluent, are concerned about maintaining their comfortable lifestyle along with independence from being dependent on their spouses and/or their children. In the 1940 s there were 5,800 Centenarians living in the United States. In the year 2000, that number had grown to over 58,000. In the year 2035, the number of people living beyond age 100 will grow to over 158,000! When we combine the increasing longevity of our aging population with the next problem facing them: the higher rates of inflation for our affluent older clients, there will be a growing need for larger income, particularly from their IRA s. IRA S AND QUALIFIED PLANS ARE THE BEST ASSETS FOR WEALTH ACCUMULATION BUT ARE THE WORST ASSETS FOR ESTATE DISTRIBUTION Under today s wealth transfer laws, there is a $2.0 million exemption from estate taxes at the death of the decedent. In 2009, that exemption will increase to $3.5 million. An affluent client can gift assets up to $12,000 per person each year without limitation, plus up to $1.0 million more during their lifetime. If they use the $1.0 million lifetime exemption up, the amount available as an exemption at death is reduced as well. Let us suppose our client (age 75) has assets that include one or two residences, a stock, bond and investment portfolio that is in excess of $1-2 million and an IRA that exceeds $1.0 million. Like most people, our client was advised by her CPA and financial advisor to take required minimum distributions (RMD s) from the IRA. The attached Chart 1 assumes the client takes the annual required minimum distributions (RMD) and that the IRA grows at 8%. 1

2 Chart 1: Minimum Distribution Calculation 2

3 THE HIGH COST OF DYING WITH AN IRA If our client has a taxable estate at his or her death and has a $1.0 million or larger IRA in their estate, the IRA may be subject to double taxation: Estate Tax as high as 45% and Income in Respect of a Decedent (IRD - Income Taxes) as high as 35%. The total taxes when adding the state inheritance and state income taxes in high taxed states such as NY, NJ, PA, Conn, DC, MD, VA, IL, CA and many others can be as high as 75% of the entire IRA, when distributed at the client s death. AN ALTERNATIVE STRATEGY OUR IRA GENERAL S PLAN SM Let us assume that our 75-year-old client lives to age 90 (15 years) and the IRA has earned 8% per year. At the client s death, the 1.0 million initial IRA of today would be includible in the client s taxable estate at a value of $1,226,431. The net after-tax value to the client s heirs (children) would be approximately $404,722. If the IRA assets were to be distributed to the client s grandchildren, there would be an additional Generation Skipping Transfer Tax further reducing the net amount going to the client s heirs. For the client with a medium sized estate (under $10 million) the IRA General s Plan SM strategy is an excellent way of addressing the following three concerns: 1. Living too long the longevity risk 2. The risk of inflation post-retirement 3. The high cost of dying with a large taxable IRA Larger estate owners (with assets over $10 million) owning large IRA s should consider using our alternative LIRA II Plan SM. The original General s plan was developed about 10 years ago. The General s tax attorney had referred us to his client (a retired and widowed three star general) to help design a plan to reduce his taxable estate of $4.0 million and to increase his distributions to his heirs. We implemented our first hedged program for this 83-year-old general and named it The General s Plan SM. He wanted to be able to protect his income against living too long, to increase his income and he wished to reduce his current income taxes and ultimately his estate taxes. The plan we put into place combined a tax-favored, guaranteed lifetime income using a single premium immediate annuity (SPIA) with a wealth replacement vehicle (life insurance) owned by a trust (outside his taxable estate) for the benefit of his heirs. By implementing the plan, he successfully accomplished four goals: 1. He reduced the current taxation on his fixed income securities, while at the same time greatly increasing his after-tax yield as compared to all of his fixed income securities. 3

and the IRA has earned 8% per year.")

4 2. He protected his income stream at a much higher level while guaranteeing the income regardless of how long he lives. 3. He protected the value of the annuity principal if he died early through the wealth replacement trust with life insurance. 4. He reduced his estate tax liability by over $500,000, thereby, increasing the net amount going to his heirs. Today, 10 years later, some even greater planning opportunities exist through the repositioning of the client s large IRA assets into our IRA General s Plan SM. Under this arrangement, we can successfully address the client s concerns while also leveraging the IRA assets to: 1. Significantly increase the guaranteed income payments over the client s lifetime with the same net amounts going to their heirs or 2. Increase the guaranteed income payments over the client s lifetime and significantly increase the net amounts to children and /or grandchildren. CHART 2 PROJECTS THE NEW GUARANTEED INCOME FROM A SPIA OVER THE CLIENT S LIFETIME $1,000,000 SPIA Example Based on Female Age 75 Year Monthly Income Annual Income % Yield Net to Heirs through age , , % 0 4

5 IN CHART 3, WE COMPARE THE ANNUITY S GUARANTEED LIFE INCOME WITH A SYSTEMATIC WITHDRAWAL OF THE SAME AMOUNT FROM THE IRA GROWING AT 8% AND 10%. 8% Growh Taking Disbursements Equal to Guaranteed SPIA Income 10% Growh Taking Disbursements Equal to Guaranteed SPIA Income Guaranteed SPIA Annual IRA End of Yr IRA End of Yr Income Yr Age Value Income 8% Yr Age Value Income 8% ,000,000 1,080, ,000,000 1,100, , (147,723) 1,006, (147,723) 1,047, , (147,723) 927, (147,723) 989, , (147,723) 842, (147,723) 926, , (147,723) 750, (147,723) 856, , (147,723) 650, (147,723) 779, , (147,723) 543, (147,723) 694, , (147,723) 427, (147,723) 601, , (147,723) 302, (147,723) 499, , (147,723) 166, (147,723) 387, , (147,723) 20, (147,723) 263, , (20,441) (0) (147,723) 127, , (0) (0) (127,201) (0) 147, (0) (0) (0) (0) 147, (0) (0) (0) (0) 147, (0) (0) (0) (0) 5

989,760 147,723 4 78 (147,723) 842,556 4 78 (147,723) 926,241 147,723 5 79 (147,723) 750,419 5 79 (147,723) 856,369 147,723 6 80 (147,723) 650,912 6 80 (147,723) 779,511 147,723 7 81")

6 CHART 4- COMPARES THE NET TO HEIRS AT THE CLIENT S DEATH (AGE 90) OF BOTH ALTERNATIVES Net to Heirs Comparison of Alternatives Net to Heirs Net to Heirs Net to Heirs Yr Age SPIA Growth ,000, , , ,000, , , ,000, , , ,000, , , ,000, , , ,000, , , ,000, , , ,000, , , ,000,000 99, , ,000,000 54, , ,000,000 3,745 86, ,000,000 (0) 41, ,000,000 (0) (0) ,000,000 (0) (0) ,000,000 (0) (0) ,000,000 (0) (0) Potential Qualified Plan Taxation at Death Income Tax 22% Net Value to Heirs 33% Federal Estate Tax 45% 6

(0) 14 88 1,000,000 (0) (0) 15 89 1,000,000 (0) (0) 16 90 1,000,000 (0) (0) Potential Qualified Plan Taxation at Death Income Tax 22% Net Value to Heirs 33% Federal")

7 IN SUMMARY The IRA General s Plan SM addresses the three concerns facing our affluent senior citizens when applied to their large IRA s. 1. Living too Long 2. Higher rates of Inflation for the aging population 3. The high cost of IRA wealth transfer due to the double taxation By annuitizing the IRA using a high yielding single premium immediate annuity (SPIA) the client s IRA income will be increased dramatically over the RMD s and it will provide the guarantee of never outliving the client s IRA. When the IRA is self-annuitized under the same assumptions, even if it s earning a high rate of return of 8-10% per year, it still places the longevity risk squarely on the client. At the client s death, the SPIA, like a company pension plan, provides no remainder to be included in the taxable estate. By creating the wealth replacement trust using assets from other existing trusts (such as Credit Shelter Trusts or funded Irrevocable trusts) or by using some of the significantly higher annuity cash flow, the client s heirs can receive a higher after-tax distribution than from the IRA through the life insurance death benefits. The principal risk of this strategy is the early death of the client, prior to life expectancy. By designing the wealth replacement death benefit to decrease as the client s annual annuity payments are paid over a longer period, the IRA General s Plan will address the longevity risk, the mortality risk, the inflation risk and the risk of high taxes on the IRA (as high as 75% combined estate and income taxes) at the client s death. 7

8 ABOUT THE AUTHORS Joel Koenig is the Managing Member of The Koenig Group, LLC, a registered investment advisor and consulting organization located in Chevy Chase, Maryland. Alison L. Segall, CLU, ChFC is also a Member of the firm. Our firm specializes in executive benefits and wealth preservation planning for business owners, senior executives, entrepreneurs and high income and high net worth individuals. We have also created strategic alliance relationships with CPA and Law Firms. Joel Koenig s Bio Joel graduated from the University of Michigan and attended NYU Graduate School of Business. He has had considerable experience as a consultant and broker implementing executive benefit plans funded with corporate-owned life insurance (COLI) for senior executives of large public corporations. He was an original partner of M Financial Corporation and an officer and director of The Management Compensation Group, Inc. (MCG), The Todd Organization, Inc. and National Philanthropic Affiliates. Joel currently serves on the editorial board of Trusts & Estates Magazine (Insurance). He has written numerous articles for the magazine including his article on Wealth Preservation for the Affluent Client with large Qualified Plan and IRA Balances published in May, The article dealt with rolling back a large IRA account balance into a new diminimus qualified profit sharing plan and purchasing a large life insurance policy inside the qualified plan. The plan was known as the LIRA Plan SM. In Revenue Ruling and then in Revenue Procedure , the IRS issued new rules regarding the valuation of such life insurance policies that were being transferred out of the profit sharing plan. In July 2001, he wrote another article for Trusts & Estates entitled: The World without Death Taxes. Joel at the NYC Estate Planning Council and The Arizona Institute of the American Society of Financial Services Professionals highlighted the same subject in It was also his topic as a main platform speaker at the 2004 annual meeting of AALU (the Association for Advanced Life Underwriting.) In October of 2002, he participated at the NYU Annual Tax Institute and lectured on The Fiduciary Liability Prevention Plan, a topic he reviewed in the July 2002 issue of Trusts & Estates Magazine in his article entitled: Diffuse this Time Bomb. He spoke on the same subject at the January 2003 Annual Meeting of the International Forum. Joel has served on the Advisory Board of Directors for The International Forum. He also has lectured extensively at Estate Planning Councils, The Association for Advanced Life Underwriting (AALU), The International Forum, American Society of CLU Seminars and numerous industry meetings. He has been a contributing author for the American College's Advanced Pension Planning course and The AALU Handbook on Split Dollar. Currently, he also serves on the Charitable planning sub-committee of AALU, having a sub-specialty in Charitable Tax Planning. He has also been published in The CLU Journal, Keeping Current, Life Association News. 8

9 Alison Segall s Bio Alison Segall, CLU, ChFC, has over 19 years of experience in estate and business planning for affluent people. She has worked as an advanced planning specialist for Wolf & Cohen Financial Group, Thomas Financial Group (both M Financial Group firms) and CIGNA which later became Lincoln Financial. In 2003, Alison became a partner of The Koenig Group LLC. Since joining The Koenig Group, Alison has been involved in working closely with CPA firms and Law firms and their clients in New York, Washington, DC and Florida providing strategies for very wealthy older clients to help them increase their legacies to their children, grandchildren and to their family charities and also providing strategies for high net worth/high income professionals and entrepreneurs to help them plan for a variety of needs including asset protection, inadequate retirement income and healthcare needs both pre and post retirement, and ultimately wealth transfer. Alison is a specialist in the technical uses of life insurance in wealth and estate planning, as well as, business planning and executive benefits. She has created and conducted numerous workshops including continuing education seminars for insurance and other financial professionals, attorneys and CPAs on the uses of life insurance in estate and business planning. Alison has a degree from the College of William & Mary in Williamsburg, Virginia. She received her Chartered Life Underwriter and Chartered Financial Consultant designations from the American College in Bryn Mawr, PA. She is an active member of the Washington, DC Estate Planning Council and is currently serving a two year term on the board of the National Capital Chapter of the Society of Financial Services Professionals. Joel and Alison are reached at (301) or joel@koeniggroup.com or alison@koeniggroup.com 9

ADVANCED ESTATE AND CHARITABLE TAX PLANNING FOR THE VERY HIGH-NET WORTH CLIENT WITH A LARGE IRA

ADVANCED ESTATE AND CHARITABLE TAX PLANNING FOR THE VERY HIGH-NET WORTH CLIENT WITH A LARGE IRA BY JOEL KOENIG, MANAGING MEMBER THE KOENIG GROUP, LLC SOPHISTICATED ESTATE AND WEALTH PRESENTATION PLANNING

ADVANCED ESTATE AND CHARITABLE TAX PLANNING FOR THE VERY HIGH-NET WORTH CLIENT WITH A LARGE IRA BY JOEL KOENIG, MANAGING MEMBER THE KOENIG GROUP, LLC SOPHISTICATED ESTATE AND WEALTH PRESENTATION PLANNING

Retirement Planning and Wealth Management

Retirement Planning and Wealth Management Kurt Rohrs Principal Advisor, Inc. www.swretire.com About, Inc. Principal Advisor Kurt Rohrs is the Principal Financial Advisor with, Inc. specializing in Financial

Retirement Planning and Wealth Management Kurt Rohrs Principal Advisor, Inc. www.swretire.com About, Inc. Principal Advisor Kurt Rohrs is the Principal Financial Advisor with, Inc. specializing in Financial

Wealth Structuring and Estate Planning. Your vision and your legacy. Life s better when we re connected

Wealth Structuring and Estate Planning Your vision and your legacy Life s better when we re connected Inside 1 Helping you shape the future 2 The elements of wealth structuring 4 The power and flexibility

Wealth Structuring and Estate Planning Your vision and your legacy Life s better when we re connected Inside 1 Helping you shape the future 2 The elements of wealth structuring 4 The power and flexibility

Diabetes Partnership of Cleveland s Planned Giving Guide

Diabetes Partnership of Cleveland s Planned Giving Guide Diabetes Partnership of Cleveland s Planned Giving Guide TABLE OF CONTENTS Life Insurance Gifts Page 2 Charitable Gifts of IRAs.Page 3 Charitable

Diabetes Partnership of Cleveland s Planned Giving Guide Diabetes Partnership of Cleveland s Planned Giving Guide TABLE OF CONTENTS Life Insurance Gifts Page 2 Charitable Gifts of IRAs.Page 3 Charitable

HERMENZE & MARCANTONIO LLC ADVANCED ESTATE PLANNING TECHNIQUES - 2015

HERMENZE & MARCANTONIO LLC ADVANCED ESTATE PLANNING TECHNIQUES - 2015 I. Overview of federal, Connecticut, and New York estate and gift taxes. A. Federal 1. 40% tax rate. 2. Unlimited estate and gift tax

HERMENZE & MARCANTONIO LLC ADVANCED ESTATE PLANNING TECHNIQUES - 2015 I. Overview of federal, Connecticut, and New York estate and gift taxes. A. Federal 1. 40% tax rate. 2. Unlimited estate and gift tax

IRAs Unique strategies for transferring wealth and giving to charity

IRAs Unique strategies for transferring wealth and giving to charity 8/24/2011 IRA Strategy #1: Giving to charity during your lifetime Applies to IRA owners who do not need their IRA distributions for

IRAs Unique strategies for transferring wealth and giving to charity 8/24/2011 IRA Strategy #1: Giving to charity during your lifetime Applies to IRA owners who do not need their IRA distributions for

UNITED STATES HOLOCAUST MEMORIAL MUSEUM

Honor the last generation. Enlighten the next. Leave a legacy bequest to the Museum. Retirement Plan Assets: A Smart Way to Secure Your Legacy UNITED STATES HOLOCAUST MEMORIAL MUSEUM 100 Raoul Wallenberg

Honor the last generation. Enlighten the next. Leave a legacy bequest to the Museum. Retirement Plan Assets: A Smart Way to Secure Your Legacy UNITED STATES HOLOCAUST MEMORIAL MUSEUM 100 Raoul Wallenberg

Prepared For: The Client Family

Annuity Maximization Estate Planning and Deferred Annuities - Annuitization Prepared For: The Client Family Insurance products are issued by: John Hancock Life Insurance Company (U.S.A.), Boston, MA and

Annuity Maximization Estate Planning and Deferred Annuities - Annuitization Prepared For: The Client Family Insurance products are issued by: John Hancock Life Insurance Company (U.S.A.), Boston, MA and

An n u i t y. Preserving Hard-Earned Annuity Assets. t r a n s a m e r i c a 1

An n u i t y Maximization Strategy Preserving Hard-Earned Annuity Assets t r a n s a m e r i c a 1 Alternatives to help protect financial assets, increase current income stream, or decrease income tax

An n u i t y Maximization Strategy Preserving Hard-Earned Annuity Assets t r a n s a m e r i c a 1 Alternatives to help protect financial assets, increase current income stream, or decrease income tax

A Powerful Way to Plan: The Grantor Retained Annuity Trust

Strategic Thinking A Powerful Way to Plan: The Grantor Retained Annuity Trust According to The Taxpayer Relief Act of 2010, the estate and gift exemption amount has been increased temporarily, for 2011

Strategic Thinking A Powerful Way to Plan: The Grantor Retained Annuity Trust According to The Taxpayer Relief Act of 2010, the estate and gift exemption amount has been increased temporarily, for 2011

Client Profile. Platinum Financial

Client Profile CA Mr. Smith is 62 and Mrs. Smith is 61 Their annual income is $300,000 Their total net worth is $5 M which includes $1 M of IRA and some rental properties and brokerage account They have

Client Profile CA Mr. Smith is 62 and Mrs. Smith is 61 Their annual income is $300,000 Their total net worth is $5 M which includes $1 M of IRA and some rental properties and brokerage account They have

Annuity Maximization Strategy

Annuity Maximization Strategy Preserving Hard-Earned Annuity Assets t r a n s a m e r i c a 1 Alternatives to help protect financial assets, increase current income stream, or decrease income tax liabilities

Annuity Maximization Strategy Preserving Hard-Earned Annuity Assets t r a n s a m e r i c a 1 Alternatives to help protect financial assets, increase current income stream, or decrease income tax liabilities

Client Profile: 66-year-old single uninsurable woman with a long-term care (LTC) concern and $2M of investable assets

concern and $2M of investable assets") GFI Supplements LTC Client Profile: 66-year-old single uninsurable woman with a long-term care (LTC) concern and $2M of investable assets Client Goal: To provide a future income stream to cover a long-term

GFI Supplements LTC Client Profile: 66-year-old single uninsurable woman with a long-term care (LTC) concern and $2M of investable assets Client Goal: To provide a future income stream to cover a long-term

MAXIMIZATION ANNUITY STRATEGY. An estate planning technique for individuals who own deferred annuities with sizable growth.

ANNUITY MAXIMIZATION STRATEGY An estate planning technique for individuals who own deferred annuities with sizable growth. Transamerica Occidental Life Insurance Company Preserving Hard-Earned Assets As

ANNUITY MAXIMIZATION STRATEGY An estate planning technique for individuals who own deferred annuities with sizable growth. Transamerica Occidental Life Insurance Company Preserving Hard-Earned Assets As

IRA Tax Fundamentals and Strategies

IRA Tax Fundamentals and Strategies Today s Objectives Today I ll demonstrate how you can improve your legacy by describing what IRA investors typically do, & comparing it to two simple but powerful ideas

IRA Tax Fundamentals and Strategies Today s Objectives Today I ll demonstrate how you can improve your legacy by describing what IRA investors typically do, & comparing it to two simple but powerful ideas

The Charitable Remainder Trust & Charitable Lead Trust. Presented by: Jeffery T. Peetz Woods & Aitken LLP

The Charitable Remainder Trust & Charitable Lead Trust Presented by: Jeffery T. Peetz Woods & Aitken LLP The Charitable Remainder Trust The charitable remainder trust is a popular and time-tested method

The Charitable Remainder Trust & Charitable Lead Trust Presented by: Jeffery T. Peetz Woods & Aitken LLP The Charitable Remainder Trust The charitable remainder trust is a popular and time-tested method

Wealth Transfer Planning

Wealth Transfer Planning For Business Owners ESTATE PLANNING SERVICES Merrill Lynch does not provide tax, accounting or legal advice. Any information presented about tax considerations affecting client

Wealth Transfer Planning For Business Owners ESTATE PLANNING SERVICES Merrill Lynch does not provide tax, accounting or legal advice. Any information presented about tax considerations affecting client

Estate Tax Concepts. for Edward and Tina Collins

Estate Tax Concepts for Edward and Tina Collins Joseph Davis, CLU, ChFC 215 Broad Street Charlotte, North Carolina 26292 Phone: 704-927-5555 Mobile Phone: 704-549-5555 Fax: 704-549-6666 Email: joseph.davis@aol.com

Estate Tax Concepts for Edward and Tina Collins Joseph Davis, CLU, ChFC 215 Broad Street Charlotte, North Carolina 26292 Phone: 704-927-5555 Mobile Phone: 704-549-5555 Fax: 704-549-6666 Email: joseph.davis@aol.com

A New Use for Your. a donor s guide. The Stelter Company

A New Use for Your R E T I R E M E N T P L A N A S S E T S a donor s guide The Stelter Company APPRECIATED PROPERTY Learn how to uncover the value of your appreciated assets. Like many Americans, you are

A New Use for Your R E T I R E M E N T P L A N A S S E T S a donor s guide The Stelter Company APPRECIATED PROPERTY Learn how to uncover the value of your appreciated assets. Like many Americans, you are

Charitable {Giving Guide

Charitable {Giving Guide Ways to Give There are many ways to make a charitable contribution. This summary highlights some of the most popular charitable giving options, including gifts of stock, bequests,

Charitable {Giving Guide Ways to Give There are many ways to make a charitable contribution. This summary highlights some of the most popular charitable giving options, including gifts of stock, bequests,

EXPLORING CHARITABLE GIFT ANNUITIES. Enjoy an immediate partial tax deduction and a lifetime of annuity income.

EXPLORING CHARITABLE GIFT ANNUITIES Enjoy an immediate partial tax deduction and a lifetime of annuity income. The Raymond James Charitable Endowment Fund does not issue gift annuities in AL, AR, CA, HI,

EXPLORING CHARITABLE GIFT ANNUITIES Enjoy an immediate partial tax deduction and a lifetime of annuity income. The Raymond James Charitable Endowment Fund does not issue gift annuities in AL, AR, CA, HI,

IRA Maximization. Wealth transfer strategies to enhance your legacy CLC.1124 (05.14)

") Maximization Wealth transfer strategies to enhance your legacy CLC.1124 (05.14) Congratulations! For many years you ve put in the hard work planning, saving and investing for retirement. With all of that

Maximization Wealth transfer strategies to enhance your legacy CLC.1124 (05.14) Congratulations! For many years you ve put in the hard work planning, saving and investing for retirement. With all of that

Understanding Annuities

Annuities, 06 5/4/05 12:43 PM Page 1 Important Information about Variable Annuities Variable annuities are offered by prospectus, which you can obtain from your financial professional or the insurance

Annuities, 06 5/4/05 12:43 PM Page 1 Important Information about Variable Annuities Variable annuities are offered by prospectus, which you can obtain from your financial professional or the insurance

Retirement: Time to Enjoy Your Rewards

Retirement: Time to Enjoy Your Rewards New York Life Guaranteed Lifetime Income Annuity The Company You Keep Some people generate retirement income by withdrawing money from their savings as they need

Retirement: Time to Enjoy Your Rewards New York Life Guaranteed Lifetime Income Annuity The Company You Keep Some people generate retirement income by withdrawing money from their savings as they need

Zero Estate Tax Strategy

Zero Estate Tax Strategy AN PLANNING STRATEGY USING LIFE INSURANCE, A FOUNDATION, AND WEALTH REPLACEMENT TRUST The Prudential Insurance Company of America 0257697 0257697-00003-00 Ed. 07/2015 Exp. 01/20/2017

Zero Estate Tax Strategy AN PLANNING STRATEGY USING LIFE INSURANCE, A FOUNDATION, AND WEALTH REPLACEMENT TRUST The Prudential Insurance Company of America 0257697 0257697-00003-00 Ed. 07/2015 Exp. 01/20/2017

Using Life Insurance and Private Foundations

Zero Estate Tax Strategy Using Life Insurance and Private Foundations Presented by: Joe Sample, [Designations per field stationery guidelines] [Company Approved Title][or][DBA Title][or][Brokerage Title]

Zero Estate Tax Strategy Using Life Insurance and Private Foundations Presented by: Joe Sample, [Designations per field stationery guidelines] [Company Approved Title][or][DBA Title][or][Brokerage Title]

Guide to Individual Retirement Accounts. Make a secure retirement yours

Guide to Individual Retirement Accounts Make a secure retirement yours Retirement means something different to everyone. Some dream of stopping employment completely and some want to continue working.

Guide to Individual Retirement Accounts Make a secure retirement yours Retirement means something different to everyone. Some dream of stopping employment completely and some want to continue working.

How To Save An Annuity From Being Lost At The Hands Of The Taxman

Annuity Rescue Strategy An estate planning technique for individuals who own deferred annuities with sizable growth. Transamerica Occidental Life Insurance Company Despite the advantage of tax-deferred

Annuity Rescue Strategy An estate planning technique for individuals who own deferred annuities with sizable growth. Transamerica Occidental Life Insurance Company Despite the advantage of tax-deferred

Converting to a Roth IRA Eliminating the Pain by using Life Insurance. Lanny D. Levin, CLU, ChFC, President LANNY D. LEVIN AGENCY, INC.

Converting to a Roth IRA Eliminating the Pain by using Life Insurance Lanny D. Levin, CLU, ChFC, President LANNY D. LEVIN AGENCY, INC. The Roth Advantage as an estate tool Traditional IRAs are great for

Converting to a Roth IRA Eliminating the Pain by using Life Insurance Lanny D. Levin, CLU, ChFC, President LANNY D. LEVIN AGENCY, INC. The Roth Advantage as an estate tool Traditional IRAs are great for

The New Era of Wealth Transfer Planning #1. American Taxpayer Relief Act Boosts Life Insurance. For agent use only. Not for public distribution.

The New Era of Wealth Transfer Planning #1 American Taxpayer Relief Act Boosts Life Insurance For agent use only. Not for public distribution. In January 2013 Congress stepped back from the fiscal cliff

The New Era of Wealth Transfer Planning #1 American Taxpayer Relief Act Boosts Life Insurance For agent use only. Not for public distribution. In January 2013 Congress stepped back from the fiscal cliff

Understanding Annuities: A Lesson in Variable Annuities

Understanding Annuities: A Lesson in Variable Annuities Did you know that an annuity can be used to systematically accumulate money for retirement purposes, as well as to guarantee a retirement income

Understanding Annuities: A Lesson in Variable Annuities Did you know that an annuity can be used to systematically accumulate money for retirement purposes, as well as to guarantee a retirement income

Estate Planning for Retirement Benefits

Estate Planning for Retirement Benefits April Caudill, J.D., CLU, ChFC, AEP Senior Advanced Planning Attorney Advanced Financial Security Planning Northwestern Mutual The Northwestern Mutual Life Insurance

Estate Planning for Retirement Benefits April Caudill, J.D., CLU, ChFC, AEP Senior Advanced Planning Attorney Advanced Financial Security Planning Northwestern Mutual The Northwestern Mutual Life Insurance

IRA. Mistakes and Opportunities. Dru Donatelli, JD-MBA, ChFC, CLU. AVP, Field Director, and Advanced Planning Attorney Special Markets

IRA Mistakes and Opportunities Dru Donatelli, JD-MBA, ChFC, CLU AVP, Field Director, and Advanced Planning Attorney Special Markets Wood Logan Academy We give financial professionals a lot of credit Not

IRA Mistakes and Opportunities Dru Donatelli, JD-MBA, ChFC, CLU AVP, Field Director, and Advanced Planning Attorney Special Markets Wood Logan Academy We give financial professionals a lot of credit Not

Gifts of Life Insurance

Gifts of Life Insurance Effective Ways to Make Them If you have a desire to make a major contribution to support our good works, life insurance can be an excellent tool for helping you accomplish your

Gifts of Life Insurance Effective Ways to Make Them If you have a desire to make a major contribution to support our good works, life insurance can be an excellent tool for helping you accomplish your

Wealth Transfer Planning in a Low Interest Rate Environment

Wealth Transfer Planning in a Low Interest Rate Environment MLINY0508088997 1 of 44 Did You Know 1/3 of affluent households over the age of 50 do not have an estate plan in place 31% of households with

Wealth Transfer Planning in a Low Interest Rate Environment MLINY0508088997 1 of 44 Did You Know 1/3 of affluent households over the age of 50 do not have an estate plan in place 31% of households with

NEWS. Seven Financial Gifting Tips for Year-End

NEWS Contact: David Kaiser, ChFC, AIF 4101 East Wesley Avenue, Suite 1 Denver, CO 80222 Phone: (303) 758-2002 (800) 781-6114 Email: dlkaiser@pinnacorfinancial.com Web site: http://www.pinnacorfinancial.com

NEWS Contact: David Kaiser, ChFC, AIF 4101 East Wesley Avenue, Suite 1 Denver, CO 80222 Phone: (303) 758-2002 (800) 781-6114 Email: dlkaiser@pinnacorfinancial.com Web site: http://www.pinnacorfinancial.com

The Effective Use of Life Insurance in Wealth Transfer Planning

INDIVIDUAL LIFE INSURANCE A Consumer Resource The Effective Use of Life Insurance in Wealth Transfer Planning A Guide for Professionals and Consumers Table of Contents INTRODUCTION What is Wealth Transfer

INDIVIDUAL LIFE INSURANCE A Consumer Resource The Effective Use of Life Insurance in Wealth Transfer Planning A Guide for Professionals and Consumers Table of Contents INTRODUCTION What is Wealth Transfer

An Asset Repositioning Strategy Repositioning Retirement Assets to Preserve a Legacy using Life Insurance

An Asset Repositioning Strategy Repositioning Retirement Assets to Preserve a Legacy using Life Insurance Chana Beene, CLU Beene Wealth Management 400 Austin Avenue, Suite 200 Waco, TX 76701 Phone 254-755-6575

An Asset Repositioning Strategy Repositioning Retirement Assets to Preserve a Legacy using Life Insurance Chana Beene, CLU Beene Wealth Management 400 Austin Avenue, Suite 200 Waco, TX 76701 Phone 254-755-6575

Guaranteeing an Income for Life: An Immediate Income Annuity Review

Guaranteeing an Income for Life: An Immediate Income Annuity Review The biggest financial risk that anyone faces during retirement is the risk that savings will be depleted...the risk that income will

Guaranteeing an Income for Life: An Immediate Income Annuity Review The biggest financial risk that anyone faces during retirement is the risk that savings will be depleted...the risk that income will

G U A R A N T E E D I N C O M E S O L U T I O N S NEW YORK LIFE LIFETIME INCOME ANNUITY

G U A R A N T E E D I N C O M E S O L U T I O N S NEW YORK LIFE LIFETIME INCOME ANNUITY NEW YORK LIFE: BUILT FOR TIMES LIKE THESE New York Life Insurance Company, the parent company of New York Life Insurance

G U A R A N T E E D I N C O M E S O L U T I O N S NEW YORK LIFE LIFETIME INCOME ANNUITY NEW YORK LIFE: BUILT FOR TIMES LIKE THESE New York Life Insurance Company, the parent company of New York Life Insurance

Turning Savings Into Retirement Income

Turning Savings Into Retirement Income Inside: Determining Your Income Needs Funding Your Goals Monitoring Your Retirement Income Plan For more information on BlackRock retirement income solutions, contact

Turning Savings Into Retirement Income Inside: Determining Your Income Needs Funding Your Goals Monitoring Your Retirement Income Plan For more information on BlackRock retirement income solutions, contact

IRAS TAXES AND MOODY STEWARDSHIP. A Ministry of Moody Bible Institute

MOODY STEWARDSHIP A Ministry of Moody Bible Institute IRAS AND TAXES IRAs and Other Qualified Retirement Plans IRAs, pensions, and estate planning are all excellent resources for preparing an enjoyable,

MOODY STEWARDSHIP A Ministry of Moody Bible Institute IRAS AND TAXES IRAs and Other Qualified Retirement Plans IRAs, pensions, and estate planning are all excellent resources for preparing an enjoyable,

LIQUIDATING RETIREMENT ASSETS

LIQUIDATING RETIREMENT ASSETS IN A TAX-EFFICIENT MANNER By William A. Raabe and Richard B. Toolson When you enter retirement, you retire from work, not from decision-making. Among the more important decisions

LIQUIDATING RETIREMENT ASSETS IN A TAX-EFFICIENT MANNER By William A. Raabe and Richard B. Toolson When you enter retirement, you retire from work, not from decision-making. Among the more important decisions

Planning Retirement in a Rising Tax Environment

Planning Retirement in a Rising Tax Environment (Based on the published article written in the 2014 semi-annual edition of Wealth Channel Magazine) By Francis J. Lojewski, MSFS, ChFC, CLU, LUTCF, AEP One-sentence

Planning Retirement in a Rising Tax Environment (Based on the published article written in the 2014 semi-annual edition of Wealth Channel Magazine) By Francis J. Lojewski, MSFS, ChFC, CLU, LUTCF, AEP One-sentence

Distributions and Rollovers from

Page 1 of 6 Frequently Asked Questions about Distributions and Rollovers from Retirement Accounts Choosing what to do with your retirement savings is an important decision. Tax implications are just one

Page 1 of 6 Frequently Asked Questions about Distributions and Rollovers from Retirement Accounts Choosing what to do with your retirement savings is an important decision. Tax implications are just one

Estate Planning Fact Finder

Estate Planning Fact Finder Advanced Markets Estate Planning Fact Finder Date: Personal Information Note: If you want to do a basic estate planning analysis, please complete pages 2 5. If you want a more

Estate Planning Fact Finder Advanced Markets Estate Planning Fact Finder Date: Personal Information Note: If you want to do a basic estate planning analysis, please complete pages 2 5. If you want a more

YOUR PRACTICE AND POSITIONING FOR STRATEGIC ADVANTAGE LEADERS PARTNERS, INC. 100 S. WYNSTONE PARK DRIVE NORTH BARRINGTON, IL 60010 847.304.

YOUR PRACTICE AND LEADERS PARTNERS POSITIONING FOR STRATEGIC ADVANTAGE ASSET LEVERAGE STRATEGIES INTRINSIC STOCK VALUE LOCK IN STRATEGY We all have our favorite stocks which most likely have taken a hit

YOUR PRACTICE AND LEADERS PARTNERS POSITIONING FOR STRATEGIC ADVANTAGE ASSET LEVERAGE STRATEGIES INTRINSIC STOCK VALUE LOCK IN STRATEGY We all have our favorite stocks which most likely have taken a hit

Understanding IRA distributions

Understanding IRA distributions A retirement distribution guide Allianz Life Insurance Company of New York Allianz Life Insurance Company of North America AMK-019-N Page 1 of 12 It s important to know

Understanding IRA distributions A retirement distribution guide Allianz Life Insurance Company of New York Allianz Life Insurance Company of North America AMK-019-N Page 1 of 12 It s important to know

Preserving value for the next generation. Lincoln LifeLINC Advisor Guide. For agent or broker use only. Not for use with the public.

Preserving value for the next generation Lincoln LifeLINC Advisor Guide For agent or broker use only. Not for use with the public. Contents Wealth transfer planning 2 Connect your clients to the Lincoln

Preserving value for the next generation Lincoln LifeLINC Advisor Guide For agent or broker use only. Not for use with the public. Contents Wealth transfer planning 2 Connect your clients to the Lincoln

FINDING LEVERAGE IN ESTATE AND CHARITABLE PLANNING. Howard County Estate Planning Council May 14, 2015

FINDING LEVERAGE IN ESTATE AND CHARITABLE PLANNING Howard County Estate Planning Council May 14, 2015 Presented By Kim Olson Managing Director BKA Private Wealth Management Group ESTATE PLANNING SOLUTIONS

FINDING LEVERAGE IN ESTATE AND CHARITABLE PLANNING Howard County Estate Planning Council May 14, 2015 Presented By Kim Olson Managing Director BKA Private Wealth Management Group ESTATE PLANNING SOLUTIONS

MassMutual Single Premium Immediate Annuity

ANNUITIES MassMutual Single Premium Immediate Annuity Retirement Can Be An Exciting Journey INVEST INSURE RETIRE Peter and Gail Doherty will celebrate their 40th wedding anniversary later this year. When

ANNUITIES MassMutual Single Premium Immediate Annuity Retirement Can Be An Exciting Journey INVEST INSURE RETIRE Peter and Gail Doherty will celebrate their 40th wedding anniversary later this year. When

the t. rowe price Guide for IRA and 403(b) Account Beneficiaries

Account Beneficiaries") the t. rowe price Guide for IRA and 403(b) Account Beneficiaries who should use this guide T. Rowe Price retirement specialists have designed this guide for: 1 : Individuals who are beneficiaries of the

the t. rowe price Guide for IRA and 403(b) Account Beneficiaries who should use this guide T. Rowe Price retirement specialists have designed this guide for: 1 : Individuals who are beneficiaries of the

Maximize Retirement Income and Preserve Accumulated Wealth

Maximize Retirement Income and Preserve Accumulated Wealth Welcome! Steven M. Dalton, CFP 40 South River Road, Unit 15 Bedford, NH 03110 603-668-2303 Securities offered through Comprehensive Asset Management

Maximize Retirement Income and Preserve Accumulated Wealth Welcome! Steven M. Dalton, CFP 40 South River Road, Unit 15 Bedford, NH 03110 603-668-2303 Securities offered through Comprehensive Asset Management

Common mistakes in estate planning

Common mistakes in estate planning Disclaimers The Lyon Group is not in the business of providing tax, legal or accounting advice, and none is intended nor should be inferred from the foregoing comments

Common mistakes in estate planning Disclaimers The Lyon Group is not in the business of providing tax, legal or accounting advice, and none is intended nor should be inferred from the foregoing comments

Understanding the Estate Planning and Financial Planning Issues of the Non-Citizen Spouse

Understanding the Estate Planning and Financial Planning Issues of the Non-Citizen Spouse For the family that meets the description US citizen married to a US citizen the estate tax rules are fairly straight-forward.

Understanding the Estate Planning and Financial Planning Issues of the Non-Citizen Spouse For the family that meets the description US citizen married to a US citizen the estate tax rules are fairly straight-forward.

Frequently asked questions

Page 1 of 6 Frequently asked questions Distributions and rollovers from retirement accounts Choosing what to do with your retirement savings is an important decision. Tax implications are just one of several

Page 1 of 6 Frequently asked questions Distributions and rollovers from retirement accounts Choosing what to do with your retirement savings is an important decision. Tax implications are just one of several

Estate planning strategies using life insurance in a trust Options for handling distributions, rollovers and conversions

Estate planning strategies using life insurance in a trust Options for handling distributions, rollovers and conversions Life s better when we re connected Table of contents Find your questions review

Estate planning strategies using life insurance in a trust Options for handling distributions, rollovers and conversions Life s better when we re connected Table of contents Find your questions review

Presented By: Tim Voorhees, JD, MBA

Zero Tax and Asset Protection Planning Zero Tax Planning Presented By: Tim Voorhees, JD, MBA 695 Town Center Drive 7th Floor Costa Mesa, CA 92626 Tel: 800.447.7090 Fax: 866.447.7090 info@vfos.com www.vfos.com

Zero Tax and Asset Protection Planning Zero Tax Planning Presented By: Tim Voorhees, JD, MBA 695 Town Center Drive 7th Floor Costa Mesa, CA 92626 Tel: 800.447.7090 Fax: 866.447.7090 info@vfos.com www.vfos.com

U.S. Taxes for Canadians with U.S. assets

U.S. Taxes for Canadians with U.S. assets December 2014 U.S. Gift, Estate and Generation Skipping Transfer Tax can affect Canadians who don t even live in the United States. This article examines how these

U.S. Taxes for Canadians with U.S. assets December 2014 U.S. Gift, Estate and Generation Skipping Transfer Tax can affect Canadians who don t even live in the United States. This article examines how these

The 3.8 Percent Medicare Surtax in Retirement Income Planning

Reprinted with permission from the Society of FSP. Reproduction prohibited without publisher's written permission. The 3.8 Percent Medicare Surtax in by Lynn A. Nolan, CLU, ChFC, CASL, RICP Abstract: In

Reprinted with permission from the Society of FSP. Reproduction prohibited without publisher's written permission. The 3.8 Percent Medicare Surtax in by Lynn A. Nolan, CLU, ChFC, CASL, RICP Abstract: In

Igor A. Zey, MSFS, CFP, CLU, ChFC, CAP, AEP

Igor A. Zey, MSFS, CFP, CLU, ChFC, CAP, AEP White, Zuckerman, Warsavsky, Luna & Hunt Advisors, LLC Professional Financial Resources, Inc. 15490 Ventura Blvd., #220 Sherman Oaks, California 91403 Office

Igor A. Zey, MSFS, CFP, CLU, ChFC, CAP, AEP White, Zuckerman, Warsavsky, Luna & Hunt Advisors, LLC Professional Financial Resources, Inc. 15490 Ventura Blvd., #220 Sherman Oaks, California 91403 Office

The Basics of Annuities: Planning for Income Needs

March 2013 The Basics of Annuities: Planning for Income Needs summary the facts of retirement Earning income once your paychecks stop that is, after your retirement requires preparing for what s to come

March 2013 The Basics of Annuities: Planning for Income Needs summary the facts of retirement Earning income once your paychecks stop that is, after your retirement requires preparing for what s to come

The Basics of Annuities: Income Beyond the Paycheck

The Basics of Annuities: PLANNING FOR INCOME NEEDS TABLE OF CONTENTS Income Beyond the Paycheck...1 The Facts of Retirement...2 What Is an Annuity?...2 What Type of Annuity Is Right for Me?...2 Payment

The Basics of Annuities: PLANNING FOR INCOME NEEDS TABLE OF CONTENTS Income Beyond the Paycheck...1 The Facts of Retirement...2 What Is an Annuity?...2 What Type of Annuity Is Right for Me?...2 Payment

KURT D. PANOUSES, P.A. ATTORNEYS AND COUNSELORS AT LAW 310 Fifth Avenue Indialantic, FL 32903 (321) 729-9455 FAX: (321) 768-2655

729-9455 FAX: (321) 768-2655") KURT D. PANOUSES, P.A. ATTORNEYS AND COUNSELORS AT LAW 310 Fifth Avenue Indialantic, FL 32903 (321) 729-9455 FAX: (321) 768-2655 Kurt D. Panouses is Board Certified by the Florida Bar as a Specialist in

KURT D. PANOUSES, P.A. ATTORNEYS AND COUNSELORS AT LAW 310 Fifth Avenue Indialantic, FL 32903 (321) 729-9455 FAX: (321) 768-2655 Kurt D. Panouses is Board Certified by the Florida Bar as a Specialist in

CLIENT GUIDE. Advanced Markets. Estate Planning Client Guide

CLIENT GUIDE Advanced Markets Estate Planning Client Guide TABLE OF CONTENTS Why Create an Estate Plan?........................ 1 Basic Estate Planning Tools......................... 2 Funding an Irrevocable

CLIENT GUIDE Advanced Markets Estate Planning Client Guide TABLE OF CONTENTS Why Create an Estate Plan?........................ 1 Basic Estate Planning Tools......................... 2 Funding an Irrevocable

Creating future lifetime income with Deferred Income Annuities

Creating future lifetime income with Deferred Income Annuities Fixed annuities available at Fidelity are issued by third-party insurance companies, which are not affiliated with any Fidelity Investments

Creating future lifetime income with Deferred Income Annuities Fixed annuities available at Fidelity are issued by third-party insurance companies, which are not affiliated with any Fidelity Investments

A PROFESSIONAL S GUIDE TO INCOME OPPORTUNITIES USING ANNUITIES

A PROFESSIONAL S GUIDE TO INCOME OPPORTUNITIES USING ANNUITIES CPAs Attorneys Enrolled Agents Tax Professionals Professional Education Network TM www.edwardjones.com/teamwork CONTENTS 1 Introduction 2

A PROFESSIONAL S GUIDE TO INCOME OPPORTUNITIES USING ANNUITIES CPAs Attorneys Enrolled Agents Tax Professionals Professional Education Network TM www.edwardjones.com/teamwork CONTENTS 1 Introduction 2

Annuity Owner Mistakes Tips and Ideas That Could Save You Thousands

Annuity Owner Mistakes Tips and Ideas That Could Save You Thousands Provided to you by: Victoria Woods & Damon King 405-348-0909 Annuity Owner Mistakes Written by Financial Educators Provided to you by

Annuity Owner Mistakes Tips and Ideas That Could Save You Thousands Provided to you by: Victoria Woods & Damon King 405-348-0909 Annuity Owner Mistakes Written by Financial Educators Provided to you by

An IRA can put you in control of your retirement, whether you

IRAs: Powering Your Retirement One of the most effective ways to build and manage funds to help you meet your financial goals is through an Individual Retirement Account (IRA). An IRA can put you in control

IRAs: Powering Your Retirement One of the most effective ways to build and manage funds to help you meet your financial goals is through an Individual Retirement Account (IRA). An IRA can put you in control

Guaranteed Lifetime Income Annuity II 1

Just the facts about the New York Life... Guaranteed Lifetime Income Annuity II 1 Issuing company Product type Issue ages 2 Single premium payment Income payment modes New York Life Insurance and Annuity

Just the facts about the New York Life... Guaranteed Lifetime Income Annuity II 1 Issuing company Product type Issue ages 2 Single premium payment Income payment modes New York Life Insurance and Annuity

Charitable Trusts. Charitable Trusts

Charitable Trusts Charitable Trusts Gifts to charitable trusts can be during lifetime or at the time of death. Charitable trusts provide an income interest to a person, persons, or charities for a period

Charitable Trusts Charitable Trusts Gifts to charitable trusts can be during lifetime or at the time of death. Charitable trusts provide an income interest to a person, persons, or charities for a period

Planning Concepts For Non-Qualified Money

Planning Concepts For Non-Qualified Money 1. Make CD's Your Ally, Instead of Your Enemy. When your prospect has a lot of money in CD's of varying durations, it is typically because they want to be sure

Planning Concepts For Non-Qualified Money 1. Make CD's Your Ally, Instead of Your Enemy. When your prospect has a lot of money in CD's of varying durations, it is typically because they want to be sure

Giving Today to Guarantee Tomorrow: Charitable Gifts of Life Insurance

Giving Today to Guarantee Tomorrow: Charitable Gifts of Life Insurance A gift of life insurance can represent a substantial future gift to a favorite charity at relatively little cost to you. Table of

Giving Today to Guarantee Tomorrow: Charitable Gifts of Life Insurance A gift of life insurance can represent a substantial future gift to a favorite charity at relatively little cost to you. Table of

CASE District IV Conference Fort Worth, Texas. March 25, 2013. What true assets does your family possess?

HOW TO INITIATE GIFT PLANNING DISCUSSIONS WITH DONORS The Charitable Planning Process CASE District IV Conference Fort Worth, Texas March 25, 2013 Laura Hansen Dean, J.D. Attorney at Law (Texas, Indiana)

HOW TO INITIATE GIFT PLANNING DISCUSSIONS WITH DONORS The Charitable Planning Process CASE District IV Conference Fort Worth, Texas March 25, 2013 Laura Hansen Dean, J.D. Attorney at Law (Texas, Indiana)

The Insured Annuity Strategy. What would you do in retirement if you knew your income was guaranteed for life?

The Insured Annuity Strategy What would you do in retirement if you knew your income was guaranteed for life? Enjoy the retirement you want to live. You re working hard to save for your retirement. Yet

The Insured Annuity Strategy What would you do in retirement if you knew your income was guaranteed for life? Enjoy the retirement you want to live. You re working hard to save for your retirement. Yet

Palladium Single Premium Immediate Annuity With

Palladium Single Premium Immediate Annuity With Cost Of Living Adjustment Income For Now... Guaranteed Income For Life! A Single Premium Immediate Annuity Issued By Income for Your Needs Now and in the

Palladium Single Premium Immediate Annuity With Cost Of Living Adjustment Income For Now... Guaranteed Income For Life! A Single Premium Immediate Annuity Issued By Income for Your Needs Now and in the

Annuity Maximization. Annuities are designed for retirement income What if you do not need the income? Using Life Insurance AD-OC-851A

Annuity Maximization Annuities are designed for retirement income What if you do not need the income? AD-OC-851A Annuity Maximization The Situation Deferred annuities have traditionally been a vehicle

Annuity Maximization Annuities are designed for retirement income What if you do not need the income? AD-OC-851A Annuity Maximization The Situation Deferred annuities have traditionally been a vehicle

Creating lifetime income with Immediate Fixed Income Annuities

Creating lifetime income with Immediate Fixed Income Annuities Fixed annuities available at Fidelity are issued by third-party insurance companies, which are not affiliated with any Fidelity Investments

Creating lifetime income with Immediate Fixed Income Annuities Fixed annuities available at Fidelity are issued by third-party insurance companies, which are not affiliated with any Fidelity Investments

ANNUITIES: WHAT ARE THEY AND HOW ARE THEY USED

ANNUITIES: WHAT ARE THEY AND HOW ARE THEY USED (FORC Journal: Vol. 18 Edition 1 - Spring 2007) 1 An annuity is a contract under which the owner of the contract pays money or transfers assets to the obligor

ANNUITIES: WHAT ARE THEY AND HOW ARE THEY USED (FORC Journal: Vol. 18 Edition 1 - Spring 2007) 1 An annuity is a contract under which the owner of the contract pays money or transfers assets to the obligor

Program outlines: Retirement Planning

Program outlines: Retirement Planning 1. Casey County Kentucky Retirement & Estate Planning Program 1997 Session 1. Saving For Your Retirement Assessing present financial status-net worth, investments,

Program outlines: Retirement Planning 1. Casey County Kentucky Retirement & Estate Planning Program 1997 Session 1. Saving For Your Retirement Assessing present financial status-net worth, investments,

Mission: Our Vision: United Way Services of Geauga County unites people and resources to improve lives.

Create your legacy. Mission: United Way Services of Geauga County unites people and resources to improve lives. Our Vision: United Way Services of Geauga County is the organization recognized for collaborating

Create your legacy. Mission: United Way Services of Geauga County unites people and resources to improve lives. Our Vision: United Way Services of Geauga County is the organization recognized for collaborating

Pacific. Income Provider. A Single-Premium, Immediate Fixed Annuity for a Confident Retirement. Client Guide 9/15 80002-15A

Pacific Income Provider A Single-Premium, Immediate Fixed Annuity for a Confident Retirement 9/15 80002-15A Client Guide Why Pacific Life Pacific Life has more than 145 years of experience, and we remain

Pacific Income Provider A Single-Premium, Immediate Fixed Annuity for a Confident Retirement 9/15 80002-15A Client Guide Why Pacific Life Pacific Life has more than 145 years of experience, and we remain

10 common IRA mistakes

10 common mistakes Help protect your valuable retirement assets Not FDIC Insured May Lose Value No Bank Guarantee Not Insured by Any Government Agency You ve worked hard to build your retirement assets......

10 common mistakes Help protect your valuable retirement assets Not FDIC Insured May Lose Value No Bank Guarantee Not Insured by Any Government Agency You ve worked hard to build your retirement assets......

Basic Features of the Charitable Lead Trust 1

W E A L T H C A R E C A P I T A L M A N A G E M E N T : A D V I S O R E M A I L For the latest in Financeware news and Wealthcare resources, please see the last page of this document. A PRIMER ON THE CHARITABLE

W E A L T H C A R E C A P I T A L M A N A G E M E N T : A D V I S O R E M A I L For the latest in Financeware news and Wealthcare resources, please see the last page of this document. A PRIMER ON THE CHARITABLE

Estate Planning. Some common tools used to help meet those particular needs include:

Estate Planning The Importance of Having an Estate Plan Having an estate plan is one of the most important things you can do for your family. It's not just about planning for estate taxes; it's about developing

Estate Planning The Importance of Having an Estate Plan Having an estate plan is one of the most important things you can do for your family. It's not just about planning for estate taxes; it's about developing

Using Life Insurance for Pension Maximization

Using Life Insurance for Pension Maximization Help your clients capitalize on their pension plans Agent Guide For agent use only. Not to be used for consumer solicitation purposes. Help Your Clients Obtain

Using Life Insurance for Pension Maximization Help your clients capitalize on their pension plans Agent Guide For agent use only. Not to be used for consumer solicitation purposes. Help Your Clients Obtain

Annuity Owner Mistakes

Annuity Owner Mistakes Tips and Ideas That Could Save You Thousands Provided to you by: William E. Watson III, RFC Registered Financial Consultant Annuity Owner Mistakes Written by Javelin Marketing, Inc.

Annuity Owner Mistakes Tips and Ideas That Could Save You Thousands Provided to you by: William E. Watson III, RFC Registered Financial Consultant Annuity Owner Mistakes Written by Javelin Marketing, Inc.

Valued Client Owner Age: 60 State of Issue: Michigan. Death Benefit: Maximum Daily Value II

ForeRetirement TM III B-Share Prepared for: Valued Client Owner Age: 60 State of Issue: Michigan Prepared on: April 30, 2015 Prepared by: Guest User Firm Name: Guest Input Summary: Initial Investment:

ForeRetirement TM III B-Share Prepared for: Valued Client Owner Age: 60 State of Issue: Michigan Prepared on: April 30, 2015 Prepared by: Guest User Firm Name: Guest Input Summary: Initial Investment:

Advanced Wealth Transfer Strategies

Family Limited Partnerships (FLPS) Advanced Wealth Transfer Strategies The American Taxpayer Relief Act of 2012 established a permanent gift and estate tax exemption of $5 million, which is adjusted annually

Family Limited Partnerships (FLPS) Advanced Wealth Transfer Strategies The American Taxpayer Relief Act of 2012 established a permanent gift and estate tax exemption of $5 million, which is adjusted annually

Charitable remainder trusts

Charitable remainder trusts An estate planning strategy for charitably inclined investors This strategy may be a good fit when: You want to make a significant gift to charity You have assets that you want

Charitable remainder trusts An estate planning strategy for charitably inclined investors This strategy may be a good fit when: You want to make a significant gift to charity You have assets that you want

Understanding annuities

ab Wealth Management Americas Understanding annuities Rethinking the role they play in retirement income planning Protecting your retirement income security from life s uncertainties. The retirement landscape

ab Wealth Management Americas Understanding annuities Rethinking the role they play in retirement income planning Protecting your retirement income security from life s uncertainties. The retirement landscape

Traditional and Roth IRAs

october 2012 Understanding Traditional and Roth IRAs summary An Individual Retirement Account (IRA) is a powerful savings vehicle that can help you meet your financial goals. As shown in the chart on page

october 2012 Understanding Traditional and Roth IRAs summary An Individual Retirement Account (IRA) is a powerful savings vehicle that can help you meet your financial goals. As shown in the chart on page

A New Look at Cash Value as an Asset

A New Look at Cash Value as an Asset Brought to you by: Pinney Insurance Center, Inc. 2266 Lava Ridge Court Roseville, CA 95661 www.pinneyinsurance.com Cash Value Life Insurance Advantages of cash value

A New Look at Cash Value as an Asset Brought to you by: Pinney Insurance Center, Inc. 2266 Lava Ridge Court Roseville, CA 95661 www.pinneyinsurance.com Cash Value Life Insurance Advantages of cash value

The Power of the Charitable Remainder Trust

The Power of the Charitable Remainder Trust As people become better educated about the power and fl exibility of the Charitable Remainder Trust (CRT), they are incorporating it more and more as an effective

The Power of the Charitable Remainder Trust As people become better educated about the power and fl exibility of the Charitable Remainder Trust (CRT), they are incorporating it more and more as an effective

Gifts of Life Insurance

Gifts of Life Insurance Effective Ways to Make Them If you have a desire to make a major contribution to support our good works, life insurance can be an excellent tool for helping you accomplish your

Gifts of Life Insurance Effective Ways to Make Them If you have a desire to make a major contribution to support our good works, life insurance can be an excellent tool for helping you accomplish your

SAMPLE. Steven and Heather Reynolds. ANALYSIS OF CURRENT SITUATION November 18, 2014. PREPARED BY: Matthew Schulte, CLU, ChFC, CFP

Steven and Heather Reynolds ANALYSIS OF CURRENT SITUATION November 18, 2014 PREPARED BY: Matthew Schulte, CLU, ChFC, CFP SAMPLE Table of Contents Table of Contents... 2 Financial Statements Analysis...

Steven and Heather Reynolds ANALYSIS OF CURRENT SITUATION November 18, 2014 PREPARED BY: Matthew Schulte, CLU, ChFC, CFP SAMPLE Table of Contents Table of Contents... 2 Financial Statements Analysis...

Taxes and Transitions

Taxes and Transitions THE NEW FRONTIER FOR RETIREMENT PLANNING Wealthy individuals have been hit with their first major tax increase in more than 20 years, with tax hikes on ordinary income, dividends

Taxes and Transitions THE NEW FRONTIER FOR RETIREMENT PLANNING Wealthy individuals have been hit with their first major tax increase in more than 20 years, with tax hikes on ordinary income, dividends

Exploring the Roth 401(k)

") Exploring the Roth 401(k) Our Purpose Today What is the Roth 401(k)? How does it differ from traditional 401(k)s? How does it differ from Roth IRAs? Other points to consider Is the Roth 401(k) right for

Exploring the Roth 401(k) Our Purpose Today What is the Roth 401(k)? How does it differ from traditional 401(k)s? How does it differ from Roth IRAs? Other points to consider Is the Roth 401(k) right for