There is a handout with the highlights of this talk and it will be posted on the San Angelo website.

|

|

|

- Gabriella Campbell

- 8 years ago

- Views:

Transcription

1 Pasture Range & Forage Insurance is a very good product because of the subsidies provided by USDA Risk Management Agency. These subsidies should offset any of the complaints that I have heard about the problems with NOAA s rain gauges, i.e., your ranch did not get a rain but the grid index was above average. However, the insurance is very complicated and it takes a great deal of effort to understand it and to use it as an effective financial and range management tool. There is not time today to discuss all of the intricacies or show how all of the numbers were derived. Rather than to understand this presentation in detail try to grasp general concepts and trends. There is a handout with the highlights of this talk and it will be posted on the San Angelo website. 1

2 Your acreage can be distributed in multiple ways among the different intervals as long as each interval has a minimum of 10% and no more than 50% of the enrolled acreage. At 10 percentage unit increments that creates over 300 more choices, which multiplied by the 92,700 results in over 27 million choices. If you make 4 mouse clicks every second, 24 hours a day between now (Sept. 6) and the November 15, 2012 deadline for signing up for PRF insurance in 2013 you just might get through all 27,000,000 calculations 2

3 3

4 4

5 Do you have life insurance? Clearly, if you have life insurance, and if you are reading this, you don t mind paying a premium even though you have not received an indemnity. In fact you never will receive an indemnity for your life insurance. Do you have homeowner s insurance? Did you make a claim against it last year? But you still pay the premiums. One of the biggest mistakes that has recently been made with PRF insurance is that in 2010 people who took out PRF paid big premiums so they did not take it out in Do you plan to die or have your home destroyed in the next 5 years? Do you expect there will be a drought in the next 5 years? Do you expect there could be more than 1 drought in the next 5 years? That is the big difference between PRF and other types of insurance that you are familiar with. With other types of insurance you don t expect to use them but with PRF you expect to have a drought and to collect an indemnity, which in part is why when you have to pay a premium it ishigh. 5

6 6

7 If for a given month during a 10 year period it rained 1 inch every year except 1 year when it rained 11 inches how much would you expect it to rain? 2 inches which is the average for the 10 year period or 1 inch which is the most common amount of rainfall? 7

8 May has had as much as over 11 inches of rain in the past 30 years and the average is about 2.7 inches but the median is 2 inches. The median for the year is 81% of the average a number that I will show the relevance to the PRF decisions latter. 8

9 9

10 10

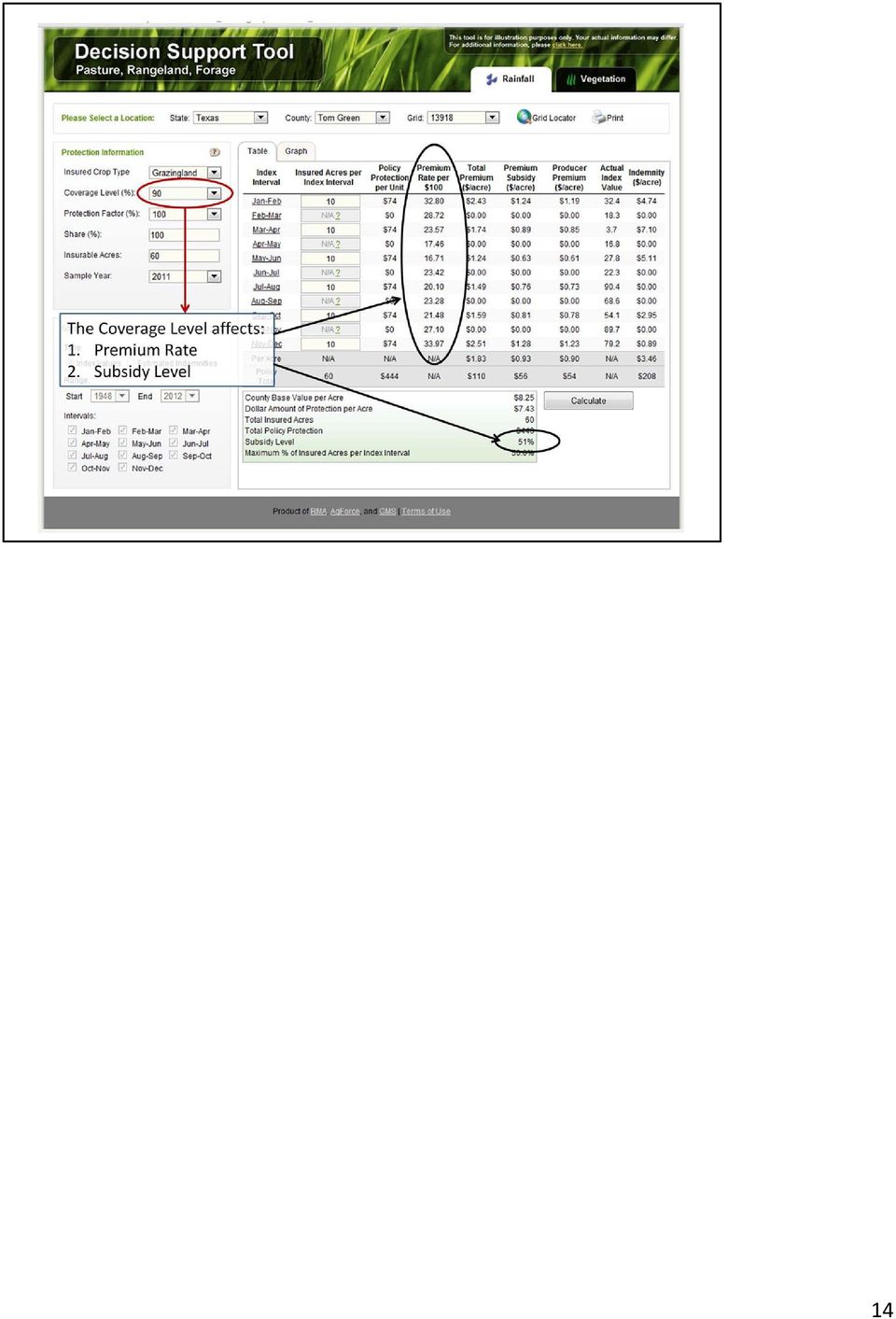

11 This is the website to access the Decision Support Tool to evaluate different PRF insurance options for your property. 11

12 Current Extension budgets for this area assume a lease rate of 13.50/Animal Unit Month. The county based average of $8.25/acres is the equivalent of a stocking rate of 20 ac/ AU. If you think the rental price for pasturing a cow should be different than $13.50 per month you can calculate the effect of that rental price on the equivalent stocking rate of the county base value using the following formula: Equivalent Stocking Rate (ac/cow) = monthly rate x 12 count base value x = 19.6 ac/cow 10 x = 14.5 ac/cow If you believe that your carrying capacity is different from stocking rate based on the county base value it can be adjusted using the Protection Factor. For instance, if you think the actual carrying capacity for your ranch is 30 ac/cow the Protection Factor adjustment would be x 100 = 66%. 12

13 Coverage Level is like the deductible on a home owners insurance how much of the loss will you cover? When deciding what coverage level you want recall that for San Angelo the Median Rainfall of 16.6 inches is 81% of the Average Rainfall Protection Factor is like the valuation of the home. 13

14 14

15 There are several thing to note on this chart 1. Premiums decrease as the amount of coverage declines, which is the equivalent of lowering your premiums by increasing your deductible. 2. The cost of coverage is quite high. Homeowner s insurance for this area is generally less than $1/$100 of coverage. PRF insurance averaged across all intervals and Coverage Levels is $22 / $100, i.e., 22 times as high, which reflects the fact that we expect to be in a drought. 3. The cost of coverage varies for the different periods. 15

16 The Protection Factor affects both the Premium Rate per $100 and the subsidy level. The higher the Protection Factor the higher the Premium Rate, because you will be indemnified more often. 16

17 The subsidy for Producer Premium does not change between 70 & 75% or 80 & 85% Coverage Levels. Producer Premiums for the highest cost interval is nearly twice a great as for the lowest cost interval. Because the median rainfall which is really the most reasonable amount of rain to expect is 81% of the average rainfall and because the subsidy is the same for the 80 or 85% coverage level this is a very reasonable coverage level to consider. 17

18 Net returns presented in this chart is the average net return averaged across 64 years and all 11 intervals within a year. Net returns are highest at the higher coverage levels and higher Protection Factors because you are using more of RMA s funds on an actual dollar basis. At the 70% Coverage Level and 60% Protection Factor the total premium is $3.47/ac and RMA contributes $2.04. At the 90% Coverage Level and 150% Protection Factor the total premium is $11.14/ac and RMA contributes $5.68. Even though at the 90% Coverage Level the percentage subsidy is lower (51% compared to 59% for 70% Coverage Level) the amount of dollars leveraged is greater resulting in a higher net return. BUT! In a wet year the premiums will also be much higher $5.46/ac compared to 1.43/ac. You must be certain that you can afford the premiums. 18

19 On average and over the long haul the number of intervals insured does not affect average net return per acre. However, next year is not a long term average it is a single year and by taking only 2 intervals you could pay a high premium because of a large rainfall event in one of the intervals that you selected even though you are in the middle of a drought, but by continuing the program every year this will not happen. 19

20 20

21 El Niño AKA El Niño Southern Oscillation (ENSO) or Oceanic Niño Index (ONI) affects rainfall. In years when a La Niña occurs, there tends to be warmer and drier conditions in many areas, including Texas. State climatologist John Nielsen Gammon says. In general terms, a La Niña period means drier weather patterns for Texas. There are numerous studies on how El Niño and La Niña affect weather patterns, specifically hurricanes and their intensity. Some research indicates that the type of hurricanes that affect Texas are more common during La Niña periods than during a neutral or El Niño year. 21

22 The Net Returns in this chart are the average net return across all years for a given ONI condition and all 11 intervals. I defined El Niño years as having an average surface temperature +0.5 above normal and to be above +0.5 during at least a 6 months during the year. La Niña years were just the opposite. By this criteria during the past 64 years there have been 14 El Niño years, 14 La Niña years and 34 neutral years. As discussed in the previous slide, La Niña tends to produce drought conditions. Witness 2011, thus the La Niña years had net returns nearly 3 times as great as El Niño or Neutral years. And surprisingly, even though El Niño is supposed to result in above average rainfall there was no difference between El Niño and Neutral years. Finally over the long term all ONI conditions produced a positive result, this reflects the subsidy on producer premiums. 22

23 This chart shows how net returns were distributed across the 11 intervals for grid It is different for each of the ONI conditions and you should consider distributing your insurance according to the historic variation in returns. 23

24 PRF would be the perfect insurance product if you could decide what intervals to insure at the end of the year instead of 2 months before the beginning of the year. Knowing that the ONI affects amounts and patterns of rainfall you have to use predictions of the ONI that come out in the middle of each month. 24

25 This slide is important because it shows that short term trend may not track long term trends. In this case averaged across all intervals PRF insurance under performed during the last 9 years for El Niño and Neutral conditions but did better for the La Niña condition. 25

26 These recommendations are rather intuitive, but are based on: 1. The fact that number of intervals insured did not appear to affect net return. 2. Adjustments for intervals that will result in above average returns should not exceed about 10 percentage units of an equal distribution of all acres. 29

27 30

28 31

29 32

30 The 9 year average means very little if in say 2004 you could not pay the premium and when bankrupt. A couple of things to notice on this slide. 1. The only difference between the profit maximizer and the risk minimizer scenario 1 is the size of the indemnities received and premiums paid. The profit maximizer all ways received larger indemnities and paid larger premiums because he used more of RMA s money. But the pattern between the 2 is the same because they both distributed their acreage the same for the different scenarios. 2. Spreading his risk across all intervals never paid off for the risk minimizer in scenario By distributing their acreage according to the suggested distribution for a predicted El Niño condition the net return in the years when indemnities were received was nearly as high in the non La Niña years and in the La Niña years 33

31 34

32 35

33 36

34 There will be other predictions in mid September and mid October before the November 15 deadline. 37

35 These recommendations are rather intuitive, but are based on: 1. The fact that number of intervals insured did not appear to affect net return. 2. Adjustments for intervals that will result in above average returns should not exceed about 10 percentage units of an equal distribution of all acres. 38

36 39

Pasture, Rangeland, and Forage Insurance: A Risk Management Tool for Hay and Livestock Producers

October 2012 Pasture, Rangeland, and Forage Insurance: A Risk Management Tool for Hay and Livestock Producers Monte Vandeveer, Otoe County Extension Educator University of Nebraska-Lincoln Institute of

October 2012 Pasture, Rangeland, and Forage Insurance: A Risk Management Tool for Hay and Livestock Producers Monte Vandeveer, Otoe County Extension Educator University of Nebraska-Lincoln Institute of

Annual Forage (AF) Pilot Program

Pilot Program") Oklahoma Cooperative Extension Service AGEC-626 Annual Forage (AF) Pilot Program Jody Campiche Assistant Professor & Extension Economist JJ Jones Southeast Area Extension Agriculture Economist The Rainfall

Oklahoma Cooperative Extension Service AGEC-626 Annual Forage (AF) Pilot Program Jody Campiche Assistant Professor & Extension Economist JJ Jones Southeast Area Extension Agriculture Economist The Rainfall

Federal Crop Insurance: The Basics

Federal Crop Insurance: The Basics Presented by Shawn Wade Director of Communications Plains Cotton Growers, Inc. 4517 West Loop 289 Lubbock, TX 79414 WWW.PLAINSCOTTON.ORG Why Federal Crop Insurance? Every

Federal Crop Insurance: The Basics Presented by Shawn Wade Director of Communications Plains Cotton Growers, Inc. 4517 West Loop 289 Lubbock, TX 79414 WWW.PLAINSCOTTON.ORG Why Federal Crop Insurance? Every

SCHEDULE C FORAGE PRODUCTION PLAN

SCHEDULE C FORAGE PRODUCTION PLAN This Schedule C, Forage Production Plan forms an integral part of the PRODUCTION INSURANCE AGREEMENT and as such contains supplementary information specific to insurance

SCHEDULE C FORAGE PRODUCTION PLAN This Schedule C, Forage Production Plan forms an integral part of the PRODUCTION INSURANCE AGREEMENT and as such contains supplementary information specific to insurance

Multiple Peril Crop Insurance

Multiple Peril Crop Insurance Multiple Peril Crop Insurance (MPCI) is a broadbased crop insurance program regulated by the U.S. Department of Agriculture and subsidized by the Federal Crop Insurance Corporation

Multiple Peril Crop Insurance Multiple Peril Crop Insurance (MPCI) is a broadbased crop insurance program regulated by the U.S. Department of Agriculture and subsidized by the Federal Crop Insurance Corporation

Crop Insurance For Those Who Choose To Manage Risk

2008 INSIDE: Crop Insurance For Those Who Choose To Manage Risk n Price And Weather Volatility Increase Risks n It Doesn t Cost To Ask n How To Evaluate Crop-Hail Insurance n Risk Management Checklist

2008 INSIDE: Crop Insurance For Those Who Choose To Manage Risk n Price And Weather Volatility Increase Risks n It Doesn t Cost To Ask n How To Evaluate Crop-Hail Insurance n Risk Management Checklist

CROP INSURANCE FOR NEW YORK VEGETABLE CROPS

CROP INSURANCE FOR NEW YORK VEGETABLE CROPS Multi-peril crop insurance is a valuable risk management tool that allows growers to insure against losses due to adverse weather conditions, price fluctuations,

CROP INSURANCE FOR NEW YORK VEGETABLE CROPS Multi-peril crop insurance is a valuable risk management tool that allows growers to insure against losses due to adverse weather conditions, price fluctuations,

Good planning is good farming

Production Insurance Plan Overview New Forage Seeding Good planning is good farming Connecting producers with programs What you need to know about protecting your new forage seeding under Production Insurance.

Production Insurance Plan Overview New Forage Seeding Good planning is good farming Connecting producers with programs What you need to know about protecting your new forage seeding under Production Insurance.

Crop Insurance for Cotton Producers: Key Concepts and Terminology

Crop Insurance for Cotton Producers: Key Concepts and Terminology With large investments in land, equipment, and technology, cotton producers typically have more capital at risk than producers of other

Crop Insurance for Cotton Producers: Key Concepts and Terminology With large investments in land, equipment, and technology, cotton producers typically have more capital at risk than producers of other

Comparing LRP to a Put Option

Comparing LRP to a Put Option Dr. G. A. Art Barnaby, Jr Kansas State University Phone: (785) 532-1515 Email: abarnaby@agecon.ksu.edu Check out our WEB at: AgManager.info 1 Livestock Risk Protection (LRP)

Comparing LRP to a Put Option Dr. G. A. Art Barnaby, Jr Kansas State University Phone: (785) 532-1515 Email: abarnaby@agecon.ksu.edu Check out our WEB at: AgManager.info 1 Livestock Risk Protection (LRP)

Price, Yield and Enterprise Revenue Risk Management Analysis Using Combo Insurance Plans, Futures and/or Options Markets

Price, Yield and Enterprise Revenue Risk Management Analysis Using Combo Insurance Plans, Futures and/or Options Markets Authors: Duane Griffith, Montana State University, Extension Farm Management Specialist

Price, Yield and Enterprise Revenue Risk Management Analysis Using Combo Insurance Plans, Futures and/or Options Markets Authors: Duane Griffith, Montana State University, Extension Farm Management Specialist

Group Risk Income Protection Plan and Group Risk Plans added in New Kansas Counties for 2005 1 Updated 3/12/05

Disclaimer: This web page is designed to aid farmers with their marketing and risk management decisions. The risk of loss in trading futures, options, forward contracts, and hedge-to-arrive can be substantial

Disclaimer: This web page is designed to aid farmers with their marketing and risk management decisions. The risk of loss in trading futures, options, forward contracts, and hedge-to-arrive can be substantial

CROP REVENUE COVERAGE INSURANCE PROVIDES ADDITIONAL RISK MANAGEMENT WHEAT ALTERNATIVES 1

Presented at the 1997 Missouri Commercial Agriculture Crop Institute CROP REVENUE COVERAGE INSURANCE PROVIDES ADDITIONAL RISK MANAGEMENT WHEAT ALTERNATIVES 1 Presented by: Art Barnaby Managing Risk With

Presented at the 1997 Missouri Commercial Agriculture Crop Institute CROP REVENUE COVERAGE INSURANCE PROVIDES ADDITIONAL RISK MANAGEMENT WHEAT ALTERNATIVES 1 Presented by: Art Barnaby Managing Risk With

U.S. crop program fiscal costs: Revised estimates with updated participation information

U.S. crop program fiscal costs: Revised estimates with updated participation information June 2015 FAPRI MU Report #02 15 Providing objective analysis for 30 years www.fapri.missouri.edu Published by the

U.S. crop program fiscal costs: Revised estimates with updated participation information June 2015 FAPRI MU Report #02 15 Providing objective analysis for 30 years www.fapri.missouri.edu Published by the

Will ARC Allow Farmers to Cancel Their 2014 Crop Insurance (Updated)? 1

? 1") Disclaimer: This web page is designed to aid farmers with their marketing and risk management decisions. The risk of loss in trading futures, options, forward contracts, and hedge-to-arrive can be substantial

Disclaimer: This web page is designed to aid farmers with their marketing and risk management decisions. The risk of loss in trading futures, options, forward contracts, and hedge-to-arrive can be substantial

Group Risk Income Protection Plan added in Kansas for 2006 Wheat (Updated) 1

1") Disclaimer: This web page is designed to aid farmers with their marketing and risk management decisions. The risk of loss in trading futures, options, forward contracts, and hedge-to-arrive can be substantial

Disclaimer: This web page is designed to aid farmers with their marketing and risk management decisions. The risk of loss in trading futures, options, forward contracts, and hedge-to-arrive can be substantial

Rain on Planting Protection. Help Guide

Rain on Planting Protection Help Guide overview Rain on Planting Protection allows growers to protect themselves from losses if rain prevents planting from being completed on schedule. Coverage is highly

Rain on Planting Protection Help Guide overview Rain on Planting Protection allows growers to protect themselves from losses if rain prevents planting from being completed on schedule. Coverage is highly

The Supplementary Insurance Coverage Option: A New Risk Management Tool for Wyoming Producers

The Supplementary Insurance Coverage Option: A New Risk Management Tool for Wyoming Producers Agricultural Marketing Policy Center Linfield Hall P.O. Box 172920 Montana State University Bozeman, MT 59717-2920

The Supplementary Insurance Coverage Option: A New Risk Management Tool for Wyoming Producers Agricultural Marketing Policy Center Linfield Hall P.O. Box 172920 Montana State University Bozeman, MT 59717-2920

Details of the Proposed Stacked Income Protection Plan (STAX) Program for Cotton Producers and Potential Strategies for Extension Education

Program for Cotton Producers and Potential Strategies for Extension Education") Journal of Agricultural and Applied Economics, 45,3(August 2013):569 575 Ó 2013 Southern Agricultural Economics Association Details of the Proposed Stacked Income Protection Plan (STAX) Program for Cotton

Journal of Agricultural and Applied Economics, 45,3(August 2013):569 575 Ó 2013 Southern Agricultural Economics Association Details of the Proposed Stacked Income Protection Plan (STAX) Program for Cotton

Federal Crop Insurance: Background

Dennis A. Shields Specialist in Agricultural Policy August 13, 2015 Congressional Research Service 7-5700 www.crs.gov R40532 Summary The federal crop insurance program began in 1938 when Congress authorized

Dennis A. Shields Specialist in Agricultural Policy August 13, 2015 Congressional Research Service 7-5700 www.crs.gov R40532 Summary The federal crop insurance program began in 1938 when Congress authorized

Title I Programs of the 2014 Farm Bill

Frequently Asked Questions: Title I Programs of the 2014 Farm Bill November 2014 Robin Reid G.A. Art Barnaby Mykel Taylor Extension Associate Extension Specialist Assistant Professor Kansas State University

Frequently Asked Questions: Title I Programs of the 2014 Farm Bill November 2014 Robin Reid G.A. Art Barnaby Mykel Taylor Extension Associate Extension Specialist Assistant Professor Kansas State University

Health Care Primer: What Do You Really Need to Know? Christianna L. Finnern

Health Care Primer: What Do You Really Need to Know? Christianna L. Finnern Obligations Under the Health Care Law Employers should be aware of their short and long term obligations under the Patient Protection

Health Care Primer: What Do You Really Need to Know? Christianna L. Finnern Obligations Under the Health Care Law Employers should be aware of their short and long term obligations under the Patient Protection

Means Testing is Good Politics, But Economic Sense? 1

Disclaimer: This web page is designed to aid farmers with their marketing and risk management decisions. The risk of loss in trading futures, options, forward contracts, and hedge-to-arrive can be substantial

Disclaimer: This web page is designed to aid farmers with their marketing and risk management decisions. The risk of loss in trading futures, options, forward contracts, and hedge-to-arrive can be substantial

AgriInsurance in Canada

AgriInsurance in Canada Brad Klak, President and Managing Director Merle Jacobson, COO, Operations Division Agriculture Financial Services Corporation Alberta, Canada Agriculture in Canada Total Cash Receipts

AgriInsurance in Canada Brad Klak, President and Managing Director Merle Jacobson, COO, Operations Division Agriculture Financial Services Corporation Alberta, Canada Agriculture in Canada Total Cash Receipts

Crop Insurance Reserving

Carl X. Ashenbrenner Abstract: The crop insurance industry is a private-public partnership, whereby the private companies issue policies and handle claims for multi-peril crop insurance policies, which

Carl X. Ashenbrenner Abstract: The crop insurance industry is a private-public partnership, whereby the private companies issue policies and handle claims for multi-peril crop insurance policies, which

Managing Risk With Revenue Insurance

Managing Risk With Revenue Insurance VOLUME 4 ISSUE 5 22 Robert Dismukes, dismukes@ers.usda.gov Keith H. Coble, coble@agecon.msstate.edu Comstock 10 Crop revenue insurance offers farmers a way to manage

Managing Risk With Revenue Insurance VOLUME 4 ISSUE 5 22 Robert Dismukes, dismukes@ers.usda.gov Keith H. Coble, coble@agecon.msstate.edu Comstock 10 Crop revenue insurance offers farmers a way to manage

Minnetonka Independent School District 276 Levy Adoption Taxes Payable in 2012

Minnetonka Independent School District 276 Levy Adoption Taxes Payable in 2012 Public Schools Established by Minnesota Constitution ARTICLE XIII MISCELLANEOUS SUBJECTS Section 1. UNIFORM SYSTEM OF PUBLIC

Minnetonka Independent School District 276 Levy Adoption Taxes Payable in 2012 Public Schools Established by Minnesota Constitution ARTICLE XIII MISCELLANEOUS SUBJECTS Section 1. UNIFORM SYSTEM OF PUBLIC

From Catastrophic to Shallow Loss Coverage: An Economist's Perspective of U.S. Crop Insurance Program and Implications for Developing Countries

From Catastrophic to Shallow Loss Coverage: An Economist's Perspective of U.S. Crop Insurance Program and Implications for Developing Countries Robert Dismukes Agricultural Economist Insurance coverage:

From Catastrophic to Shallow Loss Coverage: An Economist's Perspective of U.S. Crop Insurance Program and Implications for Developing Countries Robert Dismukes Agricultural Economist Insurance coverage:

Crop Insurance as a Tool

Crop Insurance as a Tool By: Chris Bastian University of Wyoming There are several approaches to address income variability associated with production risk. One approach is to produce more than one product

Crop Insurance as a Tool By: Chris Bastian University of Wyoming There are several approaches to address income variability associated with production risk. One approach is to produce more than one product

Analysis of the STAX and SCO Programs for Cotton Producers

Analysis of the STAX and SCO Programs for Cotton Producers Jody L. Campiche Department of Agricultural Economics Oklahoma State University Selected Paper prepared for presentation at the Agricultural &

Analysis of the STAX and SCO Programs for Cotton Producers Jody L. Campiche Department of Agricultural Economics Oklahoma State University Selected Paper prepared for presentation at the Agricultural &

U.S. Farm Policy: Overview and Farm Bill Update. Jason Hafemeister 12 June 2014. Office of the Chief Economist. Trade Bureau

U.S. Farm Policy: Office of the Chief Economist Trade Bureau Overview and Farm Bill Update Jason Hafemeister 12 June 2014 Agenda Background on U.S. Agriculture area, output, inputs, income Key Elements

U.S. Farm Policy: Office of the Chief Economist Trade Bureau Overview and Farm Bill Update Jason Hafemeister 12 June 2014 Agenda Background on U.S. Agriculture area, output, inputs, income Key Elements

Insured Information Security Policy 1 Introduction to Rain and Hail... 1 Company Directory... 2

Table of Contents i Table of Contents 2016 Pasture, Rangeland, Forage and Apiculture Rainfall/Vegetation Index Training Manual PUBL_1306_06_09_15 For the electronic version of this manual, please visit:

Table of Contents i Table of Contents 2016 Pasture, Rangeland, Forage and Apiculture Rainfall/Vegetation Index Training Manual PUBL_1306_06_09_15 For the electronic version of this manual, please visit:

Crop Insurance: Background Statistics on Participation and Results

September 2010 Crop Insurance: Background Statistics on Participation and Results FAPRI MU Report #10 10 Providing objective analysis for more than 25 years www.fapri.missouri.edu This report was prepared

September 2010 Crop Insurance: Background Statistics on Participation and Results FAPRI MU Report #10 10 Providing objective analysis for more than 25 years www.fapri.missouri.edu This report was prepared

What Percent Level and Type of Crop Insurance Should Winter Wheat Growers Select? 1

Disclaimer: This web page is designed to aid farmers with their marketing and risk management decisions. The risk of loss in trading futures, options, forward contracts, and hedge-to-arrive can be substantial

Disclaimer: This web page is designed to aid farmers with their marketing and risk management decisions. The risk of loss in trading futures, options, forward contracts, and hedge-to-arrive can be substantial

Lower Rates Mean Lower Crop Insurance Cost 1

Disclaimer: This web page is designed to aid farmers with their marketing and risk management decisions. The risk of loss in trading futures, options, forward contracts, and hedge-to-arrive can be substantial

Disclaimer: This web page is designed to aid farmers with their marketing and risk management decisions. The risk of loss in trading futures, options, forward contracts, and hedge-to-arrive can be substantial

IGAD CLIMATE PREDICTION AND APPLICATION CENTRE

IGAD CLIMATE PREDICTION AND APPLICATION CENTRE CLIMATE WATCH REF: ICPAC/CW/No.32 May 2016 EL NIÑO STATUS OVER EASTERN EQUATORIAL OCEAN REGION AND POTENTIAL IMPACTS OVER THE GREATER HORN OF FRICA DURING

IGAD CLIMATE PREDICTION AND APPLICATION CENTRE CLIMATE WATCH REF: ICPAC/CW/No.32 May 2016 EL NIÑO STATUS OVER EASTERN EQUATORIAL OCEAN REGION AND POTENTIAL IMPACTS OVER THE GREATER HORN OF FRICA DURING

Communicating the Positive Messages of Crop Insurance

Who is NCIS? Communicating the Positive Messages of Crop Insurance Trade Association Provide support and service to crop insurance companies for both Federal and private crop insurance All AIPs are members

Who is NCIS? Communicating the Positive Messages of Crop Insurance Trade Association Provide support and service to crop insurance companies for both Federal and private crop insurance All AIPs are members

Implications of Crop Insurance as Social Policy

Implications of Crop Insurance as Social Policy Bruce Babcock Iowa State University Presented at the Minnesota Crop Insurance Conference Sept 10, 2014 Mankato, MN Summary of talk 2014 farm bill irrevocably

Implications of Crop Insurance as Social Policy Bruce Babcock Iowa State University Presented at the Minnesota Crop Insurance Conference Sept 10, 2014 Mankato, MN Summary of talk 2014 farm bill irrevocably

Both the House and Senate farm bills include two new supplemental crop insurance programs:

Background Both the House and Senate farm bills include two new supplemental crop insurance programs: Supplemental Coverage Option (SCO) Stacked Income Protection Plan (STAX) for upland cotton Similar

Background Both the House and Senate farm bills include two new supplemental crop insurance programs: Supplemental Coverage Option (SCO) Stacked Income Protection Plan (STAX) for upland cotton Similar

DROUGHT ASSISTANCE PROGRAMS AND TAX IMPLICATIONS OF DROUGHT INDUCED LIVESTOCK SALES

DROUGHT ASSISTANCE PROGRAMS AND TAX IMPLICATIONS OF DROUGHT INDUCED LIVESTOCK SALES Russell Tronstad 1 Government payment assistance during or after a drought is a very real possibility. Drought assistance

DROUGHT ASSISTANCE PROGRAMS AND TAX IMPLICATIONS OF DROUGHT INDUCED LIVESTOCK SALES Russell Tronstad 1 Government payment assistance during or after a drought is a very real possibility. Drought assistance

Temporal variation in snow cover over sea ice in Antarctica using AMSR-E data product

Temporal variation in snow cover over sea ice in Antarctica using AMSR-E data product Michael J. Lewis Ph.D. Student, Department of Earth and Environmental Science University of Texas at San Antonio ABSTRACT

Temporal variation in snow cover over sea ice in Antarctica using AMSR-E data product Michael J. Lewis Ph.D. Student, Department of Earth and Environmental Science University of Texas at San Antonio ABSTRACT

The Noninsured Crop Disaster Assistance Program (NAP) and Whole Farm Revenue Protection Program (WFRP)

and Whole Farm Revenue Protection Program (WFRP)") The Noninsured Crop Disaster Assistance Program (NAP) and Whole Farm Revenue Protection Program (WFRP) 1 1 NAP: WHAT IS THE PREMIUM? Example: Rye grown in Cass County, MN Access the NAP tool at: http://fsa.usapas.com/nap.aspx

The Noninsured Crop Disaster Assistance Program (NAP) and Whole Farm Revenue Protection Program (WFRP) 1 1 NAP: WHAT IS THE PREMIUM? Example: Rye grown in Cass County, MN Access the NAP tool at: http://fsa.usapas.com/nap.aspx

RentersPLUS Move In Special

$500.00 $658.00 $125.00 Security Deposit Insurance is for $500.00 of coverage and is a non refundable premium. Move In Savings of $375.00 by Choosing Security Deposit Insurance. $288.00 $750.00 $908.00

$500.00 $658.00 $125.00 Security Deposit Insurance is for $500.00 of coverage and is a non refundable premium. Move In Savings of $375.00 by Choosing Security Deposit Insurance. $288.00 $750.00 $908.00

El Niño-Southern Oscillation (ENSO): Review of possible impact on agricultural production in 2014/15 following the increased probability of occurrence

: Review of possible impact on agricultural production in 2014/15 following the increased probability of occurrence") El Niño-Southern Oscillation (ENSO): Review of possible impact on agricultural production in 2014/15 following the increased probability of occurrence EL NIÑO Definition and historical episodes El Niño

El Niño-Southern Oscillation (ENSO): Review of possible impact on agricultural production in 2014/15 following the increased probability of occurrence EL NIÑO Definition and historical episodes El Niño

PUTTING FORAGES TOGETHER FOR YEAR ROUND GRAZING

PUTTING FORAGES TOGETHER FOR YEAR ROUND GRAZING Jimmy C. Henning A good rotational grazing system begins with a forage system that allows the maximum number of grazing days per year with forages that are

PUTTING FORAGES TOGETHER FOR YEAR ROUND GRAZING Jimmy C. Henning A good rotational grazing system begins with a forage system that allows the maximum number of grazing days per year with forages that are

Using Crop Models and Climate Forecasts to Aid in Peanut Crop Insurance Decisions 1

CIR1468 Using Crop Models and Climate Forecasts to Aid in Peanut Crop Insurance Decisions 1 C. W. Fraisse, J. L. Novak, A. Garcia y Garcia, J. W. Jones, C. Brown, and G. Hoogenboom 2 Introduction Crop

CIR1468 Using Crop Models and Climate Forecasts to Aid in Peanut Crop Insurance Decisions 1 C. W. Fraisse, J. L. Novak, A. Garcia y Garcia, J. W. Jones, C. Brown, and G. Hoogenboom 2 Introduction Crop

How To Calculate Teacher Compensation In The Sreb States

Beyond Salaries: Gale F. Gaines Employee Benefits for Teachers in the SREB States Southern Regional Education Board 592 10th St. N.W. Atlanta, GA 30318 (404) 875-9211 www.sreb.org Contact Gale F. Gaines

Beyond Salaries: Gale F. Gaines Employee Benefits for Teachers in the SREB States Southern Regional Education Board 592 10th St. N.W. Atlanta, GA 30318 (404) 875-9211 www.sreb.org Contact Gale F. Gaines

Group Risk Income Protection

Group Risk Income Protection James B. Johnson and John Hewlett* Objective Analysis for Informed Agricultural Marketing Policy Paper No. 13 July 2006 Decision Making * University of Wyoming, Extension Educator

Group Risk Income Protection James B. Johnson and John Hewlett* Objective Analysis for Informed Agricultural Marketing Policy Paper No. 13 July 2006 Decision Making * University of Wyoming, Extension Educator

And Changes under Healthcare Reform affecting businesses

And Changes under Healthcare Reform affecting businesses 1 Individual Mandate 2 First there were two choices Under the Affordable Care Act every individual must have Minimum Essential Healthcare Coverage

And Changes under Healthcare Reform affecting businesses 1 Individual Mandate 2 First there were two choices Under the Affordable Care Act every individual must have Minimum Essential Healthcare Coverage

(Over)reacting to bad luck: low yields increase crop insurance participation. Howard Chong Jennifer Ifft

reacting to bad luck: low yields increase crop insurance participation. Howard Chong Jennifer Ifft") (Over)reacting to bad luck: low yields increase crop insurance participation Howard Chong Jennifer Ifft Motivation Over the last 3 decades, U.S. farms have steadily increased participation in the Federal

(Over)reacting to bad luck: low yields increase crop insurance participation Howard Chong Jennifer Ifft Motivation Over the last 3 decades, U.S. farms have steadily increased participation in the Federal

OptionTrader. Amazingly Accurate New Mechanical Options Strategies! Plus: The NEW Visual Volatility Tool. NEW Harnessing the Power of Options Course

Nirvana s OptionTrader Amazingly Accurate New Mechanical Options Strategies! Plus: The NEW Visual Volatility Tool NEW Harnessing the Power of Options Course Ed Downs Will Teach You How To: Maximize Profits:

Nirvana s OptionTrader Amazingly Accurate New Mechanical Options Strategies! Plus: The NEW Visual Volatility Tool NEW Harnessing the Power of Options Course Ed Downs Will Teach You How To: Maximize Profits:

San Jacinto County Appraisal District PO Box 1170 Coldspring, Texas 77331 936-653-1450 936-653-5271 (Fax)

") San Jacinto County Appraisal District PO Box 1170 Coldspring, Texas 77331 936-653-1450 936-653-5271 (Fax) (Referenced) Property Tax Code Section 23.51 Guidelines to Qualify for 1-d-1 Open Space Land Appraisal

San Jacinto County Appraisal District PO Box 1170 Coldspring, Texas 77331 936-653-1450 936-653-5271 (Fax) (Referenced) Property Tax Code Section 23.51 Guidelines to Qualify for 1-d-1 Open Space Land Appraisal

GAO CROP INSURANCE. Savings Would Result from Program Changes and Greater Use of Data Mining

GAO March 2012 United States Government Accountability Office Report to the Ranking Member, Permanent Subcommittee on Investigations, Committee on Homeland Security and Governmental Affairs, U.S. Senate

GAO March 2012 United States Government Accountability Office Report to the Ranking Member, Permanent Subcommittee on Investigations, Committee on Homeland Security and Governmental Affairs, U.S. Senate

Livestock Risk Protection (LRP) Insurance for Feeder Cattle

Insurance for Feeder Cattle") Livestock Risk Protection (LRP) Insurance for Feeder Cattle Department of Agricultural MF-2705 Livestock Marketing Economics Risk management strategies and tools that cattle producers can use to protect

Livestock Risk Protection (LRP) Insurance for Feeder Cattle Department of Agricultural MF-2705 Livestock Marketing Economics Risk management strategies and tools that cattle producers can use to protect

Paying for Health Care in Retirement

Paying for Health Care in Retirement One of the complications in retirement planning is the need to make predictions what will our future living expenses be, and what about inflation rates? A big mistake

Paying for Health Care in Retirement One of the complications in retirement planning is the need to make predictions what will our future living expenses be, and what about inflation rates? A big mistake

Crop Tariff Models For Farmers Insurance

Rationality of Choices in Subsidized Crop Insurance Markets HONGLI FENG, IOWA STATE UNIVERSITY XIAODONG (SHELDON) DU, UNIVERSITY OF WISCONSIN-MADISON DAVID HENNESSY, IOWA STATE UNIVERSITY Plan of talk

Rationality of Choices in Subsidized Crop Insurance Markets HONGLI FENG, IOWA STATE UNIVERSITY XIAODONG (SHELDON) DU, UNIVERSITY OF WISCONSIN-MADISON DAVID HENNESSY, IOWA STATE UNIVERSITY Plan of talk

AN OVERVIEW OF FEDERAL CROP INSURANCE IN WISCONSIN

Learning for life AN OVERVIEW OF FEDERAL CROP INSURANCE IN WISCONSIN PAUL D. MITCHELL AGRICULTURAL AND APPLIED ECONOMICS UNIVERSITY OF WISCONSIN-MADISON UNIVERSITY OF WISCONSIN-EXTENSION Author Contact

Learning for life AN OVERVIEW OF FEDERAL CROP INSURANCE IN WISCONSIN PAUL D. MITCHELL AGRICULTURAL AND APPLIED ECONOMICS UNIVERSITY OF WISCONSIN-MADISON UNIVERSITY OF WISCONSIN-EXTENSION Author Contact

Temperature and Humidity

Temperature and Humidity Overview Water vapor is a very important gas in the atmosphere and can influence many things like condensation and the formation of clouds and rain, as well as how hot or cold

Temperature and Humidity Overview Water vapor is a very important gas in the atmosphere and can influence many things like condensation and the formation of clouds and rain, as well as how hot or cold

Climate, Drought, and Change Michael Anderson State Climatologist. Managing Drought Public Policy Institute of California January 12, 2015

Climate, Drought, and Change Michael Anderson State Climatologist Managing Drought Public Policy Institute of California January 12, 2015 Oroville Reservoir January 2009 Presentation Overview The Rules

Climate, Drought, and Change Michael Anderson State Climatologist Managing Drought Public Policy Institute of California January 12, 2015 Oroville Reservoir January 2009 Presentation Overview The Rules

Life Insurance Buyer's Guide Prepared by the National Association of Insurance Commissioners

Life Insurance Buyer's Guide Prepared by the National Association of Insurance Commissioners Buying Life Insurance How much do you need? What is the Right Kind? Finding a Low Cost Policy Things to Remember

Life Insurance Buyer's Guide Prepared by the National Association of Insurance Commissioners Buying Life Insurance How much do you need? What is the Right Kind? Finding a Low Cost Policy Things to Remember

AFBF Comparison of Senate and House Committee passed Farm Bills May 16, 2013

CURRENT LAW SENATE AG COMMITTEE (S. 954) HOUSE AG COMMITTEE (HR 1947) Reported out of Committee 15 5 Reported out of Committee 36 10 Cost $979.7 billion over the 10 years before sequester reductions of

CURRENT LAW SENATE AG COMMITTEE (S. 954) HOUSE AG COMMITTEE (HR 1947) Reported out of Committee 15 5 Reported out of Committee 36 10 Cost $979.7 billion over the 10 years before sequester reductions of

Evaluating Taking Prevented Planting Payments for Corn

May 30, 2013 Evaluating Taking Prevented Planting Payments for Corn Permalink URL http://farmdocdaily.illinois.edu/2013/05/evaluating-prevented-planting-corn.html Due to continuing wet weather, some farmers

May 30, 2013 Evaluating Taking Prevented Planting Payments for Corn Permalink URL http://farmdocdaily.illinois.edu/2013/05/evaluating-prevented-planting-corn.html Due to continuing wet weather, some farmers

Livestock Risk Protection

E-335 RM4-12.0 10-08 Risk Management Livestock Risk Protection Livestock Risk Protection (LRP) insurance is a single-peril insurance program offered by the Risk Management Agency (RMA) of USDA through

E-335 RM4-12.0 10-08 Risk Management Livestock Risk Protection Livestock Risk Protection (LRP) insurance is a single-peril insurance program offered by the Risk Management Agency (RMA) of USDA through

Pennsylvania s Medicaid program (Medical Assistance) has dozens of eligibility groups and programs, each with its own qualifying criteria.

has dozens of eligibility groups and programs, each with its own qualifying criteria.") 1 Pennsylvania s Medicaid program (Medical Assistance) has dozens of eligibility groups and programs, each with its own qualifying criteria. Non Financial Factors include: Age; Disability (temporary, permanent

1 Pennsylvania s Medicaid program (Medical Assistance) has dozens of eligibility groups and programs, each with its own qualifying criteria. Non Financial Factors include: Age; Disability (temporary, permanent

DRAFT. Final Report. Wisconsin Department of Health Services Division of Health Care Access and Accountability

Final Report Wisconsin Department of Health Services Division of Health Care Access and Accountability Wisconsin s Small Group Insurance Market March 2009 Table of Contents 1 INTRODUCTION... 3 2 EMPLOYER-BASED

Final Report Wisconsin Department of Health Services Division of Health Care Access and Accountability Wisconsin s Small Group Insurance Market March 2009 Table of Contents 1 INTRODUCTION... 3 2 EMPLOYER-BASED

Currency Trading and Forex 100 Success Secrets 100 Most Asked Questions on becoming a Successful Currency Trader

Currency Trading and Forex 100 Success Secrets 100 Most Asked Questions on becoming a Successful Currency Trader Copyright 2008 Currency Trading and Forex 100 Success Secrets Notice of rights All rights

Currency Trading and Forex 100 Success Secrets 100 Most Asked Questions on becoming a Successful Currency Trader Copyright 2008 Currency Trading and Forex 100 Success Secrets Notice of rights All rights

climate science A SHORT GUIDE TO This is a short summary of a detailed discussion of climate change science.

A SHORT GUIDE TO climate science This is a short summary of a detailed discussion of climate change science. For more information and to view the full report, visit royalsociety.org/policy/climate-change

A SHORT GUIDE TO climate science This is a short summary of a detailed discussion of climate change science. For more information and to view the full report, visit royalsociety.org/policy/climate-change

2013 Crop Insurance Decisions March 4, 2013. Roger Betz Senior District Extension Farm Management Agent

2013 Crop Insurance Decisions March 4, 2013 Roger Betz Senior District Extension Farm Management Agent 1. Crop Insurance Basics Review 2. Corn & Soybean Price Outlook 3. Re-Evaluate ACRE Todays Topics

2013 Crop Insurance Decisions March 4, 2013 Roger Betz Senior District Extension Farm Management Agent 1. Crop Insurance Basics Review 2. Corn & Soybean Price Outlook 3. Re-Evaluate ACRE Todays Topics

Estimating Cash Rental Rates for Farmland

Estimating Cash Rental Rates for Farmland Tenant operators farm more than half of the crop land in Iowa. Moreover, nearly 70 percent of the rented crop land is operated under a cash lease. Cash leases

Estimating Cash Rental Rates for Farmland Tenant operators farm more than half of the crop land in Iowa. Moreover, nearly 70 percent of the rented crop land is operated under a cash lease. Cash leases

TexasET Network Water My Yard Program

TexasET Network Water My Yard Program What is the Water My Yard Program? The WaterMyYard Program (http://watermyyard.org) is a new program and website that solves two of the biggest problems in getting

TexasET Network Water My Yard Program What is the Water My Yard Program? The WaterMyYard Program (http://watermyyard.org) is a new program and website that solves two of the biggest problems in getting

Managing Feed and Milk Price Risk: Futures Markets and Insurance Alternatives

Managing Feed and Milk Price Risk: Futures Markets and Insurance Alternatives Dillon M. Feuz Department of Applied Economics Utah State University 3530 Old Main Hill Logan, UT 84322-3530 435-797-2296 dillon.feuz@usu.edu

Managing Feed and Milk Price Risk: Futures Markets and Insurance Alternatives Dillon M. Feuz Department of Applied Economics Utah State University 3530 Old Main Hill Logan, UT 84322-3530 435-797-2296 dillon.feuz@usu.edu

Section 2.5 Average Rate of Change

Section.5 Average Rate of Change Suppose that the revenue realized on the sale of a company s product can be modeled by the function R( x) 600x 0.3x, where x is the number of units sold and R( x ) is given

Section.5 Average Rate of Change Suppose that the revenue realized on the sale of a company s product can be modeled by the function R( x) 600x 0.3x, where x is the number of units sold and R( x ) is given

The Health Insurance Marketplace. A Consumer Perspective. HFMA Tampa, May 19, 2015

The Health Insurance Marketplace A Consumer Perspective HFMA Tampa, May 19, 2015 The Role of Navigators Provide information on eligibility and how to use insurance Help to choose a plan Provide referrals

The Health Insurance Marketplace A Consumer Perspective HFMA Tampa, May 19, 2015 The Role of Navigators Provide information on eligibility and how to use insurance Help to choose a plan Provide referrals

CLIMATE, WATER & LIVING PATTERNS THINGS

CLIMATE, WATER & LIVING PATTERNS NAME THE SIX MAJOR CLIMATE REGIONS DESCRIBE EACH CLIMATE REGION TELL THE FIVE FACTORS THAT AFFECT CLIMATE EXPLAIN HOW THOSE FACTORS AFFECT CLIMATE DESCRIBE HOW CLIMATES

CLIMATE, WATER & LIVING PATTERNS NAME THE SIX MAJOR CLIMATE REGIONS DESCRIBE EACH CLIMATE REGION TELL THE FIVE FACTORS THAT AFFECT CLIMATE EXPLAIN HOW THOSE FACTORS AFFECT CLIMATE DESCRIBE HOW CLIMATES

The 2014 Farm Bill left the farm-level COM-

Current Crop Ag Decision Maker Insurance Policies File A1-48 The 2014 Farm Bill left the farm-level COM- BO products introduced by the Risk Management Agency in 2011 unchanged, but released the Area Risk

Current Crop Ag Decision Maker Insurance Policies File A1-48 The 2014 Farm Bill left the farm-level COM- BO products introduced by the Risk Management Agency in 2011 unchanged, but released the Area Risk

Pair Trading with Options

Pair Trading with Options Jeff Donaldson, Ph.D., CFA University of Tampa Donald Flagg, Ph.D. University of Tampa Ashley Northrup University of Tampa Student Type of Research: Pedagogy Disciplines of Interest:

Pair Trading with Options Jeff Donaldson, Ph.D., CFA University of Tampa Donald Flagg, Ph.D. University of Tampa Ashley Northrup University of Tampa Student Type of Research: Pedagogy Disciplines of Interest:

Crop Insurance Rates and the Laws of Probability

Crop Insurance Rates and the Laws of Probability Bruce A. Babcock, Chad E. Hart, and Dermot J. Hayes Working Paper 02-WP 298 April 2002 Center for Agricultural and Rural Development Iowa State University

Crop Insurance Rates and the Laws of Probability Bruce A. Babcock, Chad E. Hart, and Dermot J. Hayes Working Paper 02-WP 298 April 2002 Center for Agricultural and Rural Development Iowa State University

With a combination of soaking rain, flying debris, high winds, and tidal surges, Hurricanes and tropical storms can pack a powerful punch.

With a combination of soaking rain, flying debris, high winds, and tidal surges, Hurricanes and tropical storms can pack a powerful punch. Besides causing extensive damage in coastal areas, hurricanes

With a combination of soaking rain, flying debris, high winds, and tidal surges, Hurricanes and tropical storms can pack a powerful punch. Besides causing extensive damage in coastal areas, hurricanes

BREAK-EVEN COSTS FOR COW/CALF PRODUCERS

L-5220 9/98 BREAK-EVEN COSTS FOR COW/CALF PRODUCERS L.R. Sprott* CALCULATING BREAK-EVEN COSTS of production can help cow/calf producers make better management decisions for the current year or for the

L-5220 9/98 BREAK-EVEN COSTS FOR COW/CALF PRODUCERS L.R. Sprott* CALCULATING BREAK-EVEN COSTS of production can help cow/calf producers make better management decisions for the current year or for the

FIX-RIGHT USER S GUIDE

FIX-RIGHT FLAT RATE REPAIR PRICE BOOK FIX-RIGHT USER S GUIDE HELPING CONTRACTORS ACHIEVE SUCCESS AND PROFITABILITY! Since we began using flat rate pricing, no technician who worked with it wanted to go

FIX-RIGHT FLAT RATE REPAIR PRICE BOOK FIX-RIGHT USER S GUIDE HELPING CONTRACTORS ACHIEVE SUCCESS AND PROFITABILITY! Since we began using flat rate pricing, no technician who worked with it wanted to go

Covered California s 2014 Sliding Scale Plans Single Person

Covered California s 2014 Sliding Scale Plans Single Person Annual Income $11,490 - $17,235 $17,235 - $22,980 $22,980 - $28,725 $28,725 - $45,960 $19 - $57 $57 - $121 $121 - $193 $193 - $364 Covered California

Covered California s 2014 Sliding Scale Plans Single Person Annual Income $11,490 - $17,235 $17,235 - $22,980 $22,980 - $28,725 $28,725 - $45,960 $19 - $57 $57 - $121 $121 - $193 $193 - $364 Covered California

City of San Diego Water Demand Forecast

Presentation to Scripps Institute of Oceanography City of San Diego Water Demand Forecast Public Utilities Department Engineering Program Management Division Feryal Moshavegh, Associate Engineer Michael

Presentation to Scripps Institute of Oceanography City of San Diego Water Demand Forecast Public Utilities Department Engineering Program Management Division Feryal Moshavegh, Associate Engineer Michael

Characterization of the Beef Cow-calf Enterprise of the Northern Great Plains

Characterization of the Beef Cow-calf Enterprise of the Northern Great Plains Barry Dunn 1, Edward Hamilton 1, and Dick Pruitt 1 Departments of Animal and Range Sciences and Veterinary Science BEEF 2003

Characterization of the Beef Cow-calf Enterprise of the Northern Great Plains Barry Dunn 1, Edward Hamilton 1, and Dick Pruitt 1 Departments of Animal and Range Sciences and Veterinary Science BEEF 2003

Livestock Risk Protection Insurance: How Does It Work

Livestock Risk Protection Insurance: How Does It Work James Mintert, Ph.D. Professor & Extension State Leader Department of Agricultural Economics Kansas State University www.agmanager.info/livestock/marketing

Livestock Risk Protection Insurance: How Does It Work James Mintert, Ph.D. Professor & Extension State Leader Department of Agricultural Economics Kansas State University www.agmanager.info/livestock/marketing

Covered California s 2014 Sliding Scale Plans Single Person

Covered California s 2014 Sliding Scale Plans Single Person Annual Income $11,490 - $17,235 $17,235 - $22,980 $22,980 - $28,725 $28,725 - $45,960 $19 - $57 $57 - $121 $121 - $193 $193 - $364 DRUG DEDUCTIBLE,

Covered California s 2014 Sliding Scale Plans Single Person Annual Income $11,490 - $17,235 $17,235 - $22,980 $22,980 - $28,725 $28,725 - $45,960 $19 - $57 $57 - $121 $121 - $193 $193 - $364 DRUG DEDUCTIBLE,

Office of the Actuary

DEPARTMENT OF HEALTH & HUMAN SERVICES Centers for Medicare & Medicaid Services 7500 Security Boulevard, Mail Stop N3-01-21 Baltimore, Maryland 21244-1850 Office of the Actuary DATE: March 25, 2008 FROM:

DEPARTMENT OF HEALTH & HUMAN SERVICES Centers for Medicare & Medicaid Services 7500 Security Boulevard, Mail Stop N3-01-21 Baltimore, Maryland 21244-1850 Office of the Actuary DATE: March 25, 2008 FROM:

Market will worry about demand later Weekly Corn Review for May 11, 2016 By Bryce Knorr

Market will worry about demand later Weekly Corn Review for May 11, 2016 By Bryce Knorr USDA didn t do much to help the corn market in its May 10 reports other than give soybeans a big lift. That could

Market will worry about demand later Weekly Corn Review for May 11, 2016 By Bryce Knorr USDA didn t do much to help the corn market in its May 10 reports other than give soybeans a big lift. That could

Flood Insurance 101 WHY YOUR CLIENTS NEED MORE THAN A HOMEOWNERS POLICY

Flood Insurance 101 WHY YOUR CLIENTS NEED MORE THAN A HOMEOWNERS POLICY Table of Contents Introduction... 3 Who Is at Risk? Answer: Everyone... 5 Helping Customers Understand Their Flood Risk... 7 How

Flood Insurance 101 WHY YOUR CLIENTS NEED MORE THAN A HOMEOWNERS POLICY Table of Contents Introduction... 3 Who Is at Risk? Answer: Everyone... 5 Helping Customers Understand Their Flood Risk... 7 How

Influence of the Premium Subsidy on Farmers Crop Insurance Coverage Decisions

Influence of the Premium Subsidy on Farmers Crop Insurance Coverage Decisions Bruce A. Babcock and Chad E. Hart Working Paper 05-WP 393 April 2005 Center for Agricultural and Rural Development Iowa State

Influence of the Premium Subsidy on Farmers Crop Insurance Coverage Decisions Bruce A. Babcock and Chad E. Hart Working Paper 05-WP 393 April 2005 Center for Agricultural and Rural Development Iowa State

Annuity Owner Mistakes

Annuity Owner Mistakes Tips and Ideas That Could Save You Thousands Provided to you by: William E. Watson III, RFC Registered Financial Consultant Annuity Owner Mistakes Written by Javelin Marketing, Inc.

Annuity Owner Mistakes Tips and Ideas That Could Save You Thousands Provided to you by: William E. Watson III, RFC Registered Financial Consultant Annuity Owner Mistakes Written by Javelin Marketing, Inc.

Health Reform Employer Impact Analysis. Sample Employer. Prepared for. Date

Health Reform Employer Impact Analysis Prepared for Sample Employer Date 2 Health Reform Employer Impact Analysis Overview Beginning in 2014, an applicable large employer becomes subject to what are referred

Health Reform Employer Impact Analysis Prepared for Sample Employer Date 2 Health Reform Employer Impact Analysis Overview Beginning in 2014, an applicable large employer becomes subject to what are referred

Volume Title: The Intended and Unintended Effects of U.S. Agricultural and Biotechnology Policies

This PDF is a selection from a published volume from the National Bureau of Economic Research Volume Title: The Intended and Unintended Effects of U.S. Agricultural and Biotechnology Policies Volume Author/Editor:

This PDF is a selection from a published volume from the National Bureau of Economic Research Volume Title: The Intended and Unintended Effects of U.S. Agricultural and Biotechnology Policies Volume Author/Editor:

Voluntary benefits can be part of a winning game plan in a post-health care world. But communicating value is key.

Guardian in sync Future Opportunities Benefits and Behavior s Voluntary benefits can be part of a winning game plan in a post-health care world. But communicating value is key. Both employers and employees

Guardian in sync Future Opportunities Benefits and Behavior s Voluntary benefits can be part of a winning game plan in a post-health care world. But communicating value is key. Both employers and employees

Capital Market Theory: An Overview. Return Measures

Capital Market Theory: An Overview (Text reference: Chapter 9) Topics return measures measuring index returns (not in text) holding period returns return statistics risk statistics AFM 271 - Capital Market

Capital Market Theory: An Overview (Text reference: Chapter 9) Topics return measures measuring index returns (not in text) holding period returns return statistics risk statistics AFM 271 - Capital Market

Craig Thomas MSU-Extension Educator Dairy Farm Business Management and Milk Marketing

Livestock Gross Margin Insurance for Dairy Craig Thomas MSU-Extension Educator Dairy Farm Business Management and Milk Marketing Livestock Gross Margin Insurance for Dairy (LGM-Dairy) is a subsidized insurance

Livestock Gross Margin Insurance for Dairy Craig Thomas MSU-Extension Educator Dairy Farm Business Management and Milk Marketing Livestock Gross Margin Insurance for Dairy (LGM-Dairy) is a subsidized insurance

State Teachers Retirement System of Ohio Pension Reform Summary

Welcome to the STRS Ohio webinar. During this webinar we will explain changes to pension plan components resulting from the 2012 passage of pension reform legislation. This legislation was enacted to preserve

Welcome to the STRS Ohio webinar. During this webinar we will explain changes to pension plan components resulting from the 2012 passage of pension reform legislation. This legislation was enacted to preserve

How To Choose Life Insurance

Life Insurance - An Introduction to the Term or Permanent Question Written by: Gary T. Bottoms, CLU, ChFC gbottoms@thebottomsgroup.com The Question Once a need is established for cash created in the event

Life Insurance - An Introduction to the Term or Permanent Question Written by: Gary T. Bottoms, CLU, ChFC gbottoms@thebottomsgroup.com The Question Once a need is established for cash created in the event

5 Biggest Mistakes When Choosing a Mover

5 Biggest Mistakes When Choosing a Mover Mistake # 1 Getting Moving Quotes Online or Over the Phone The first step towards a quality move is an in-home inspection of the goods to be moved. Virtually anyone

5 Biggest Mistakes When Choosing a Mover Mistake # 1 Getting Moving Quotes Online or Over the Phone The first step towards a quality move is an in-home inspection of the goods to be moved. Virtually anyone

Climate Extremes Research: Recent Findings and New Direc8ons

Climate Extremes Research: Recent Findings and New Direc8ons Kenneth Kunkel NOAA Cooperative Institute for Climate and Satellites North Carolina State University and National Climatic Data Center h#p://assessment.globalchange.gov

Climate Extremes Research: Recent Findings and New Direc8ons Kenneth Kunkel NOAA Cooperative Institute for Climate and Satellites North Carolina State University and National Climatic Data Center h#p://assessment.globalchange.gov

Federal Crop Insurance RISK MANAGEMENT. Chris Eddy Dell s Insurance Agency

Federal Crop Insurance RISK MANAGEMENT Chris Eddy Dell s Insurance Agency Multiperil Coverage Crop: Barley Practice: Irrigated Level: 75% Actual Price: $2.05 per bu. Average Yield: 130 bu/acre Guarantee

Federal Crop Insurance RISK MANAGEMENT Chris Eddy Dell s Insurance Agency Multiperil Coverage Crop: Barley Practice: Irrigated Level: 75% Actual Price: $2.05 per bu. Average Yield: 130 bu/acre Guarantee