GOVERNMENT DEBT MANAGEMENT AT THE ZERO LOWER BOUND

|

|

|

- Annabelle Oliver

- 8 years ago

- Views:

Transcription

1 GOVERNMENT DEBT MANAGEMENT AT THE ZERO LOWER BOUND ROBIN GREENWOOD SAMUEL G. HANSON JOSHUA S. RUDOLPH LAWRENCE H. SUMMERS

2 OUR PAPER I. Quantify Fed vs. Treasury conflict in QE era II. Fed vs. Treasury in historical perspective III. A modern framework for debt management Will develop and extend logic from Greenwood, Hanson, Stein (2015) Logic applied to consolidated government balance sheet IV. Ways to resolve Fed vs. Treasury conflict

3 10 YEAR EQUIVALENTS QE QE = SOMA 0.95*Currency QE x Duration / Duration(10 yr) = QE (10 year equivalents) Treasury Maturity Extension

Treasury Maturity")

4 10 YEAR EQUIVALENTS (TABLE 2)

5 PULLING IN OPPOSITE DIRECTIONS 10-year duration equivalents, Change since Dec. 31, 2007 (% of GDP) 20% 15% 10% The Fed s Quantitative Easing (QE) policies have reduced the net supply of long-term securities. 5% 0% -5% -10% Fed QE: Treasuries, Agencies and MBS 15.6% -15% QE1 QE2 Twist QE3-20%

6 PULLING IN OPPOSITE DIRECTIONS 10-year duration equivalents, Change since Dec. 31, 2007 (% of GDP) 20% 15% 10% 5% 0% Meanwhile the Treasury was doing the opposite, extending the average maturity of its borrowings. Treasury: Maturity Extension 5.6% -5% -10% Fed QE: Treasuries, Agencies and MBS -15% QE1 QE2 Twist QE3-20%

7 PULLING IN OPPOSITE DIRECTIONS 10-year duration equivalents, Change since Dec. 31, 2007 (% of GDP) 20% 15% 10% 5% 0% -5% -10% Treasury: Maturity Extension Fed QE: Treasuries, Agencies and MBS Net Impact: 10.1% -15% QE1 QE2 Twist QE3-20%

8 PULLING IN OPPOSITE DIRECTIONS 10-year duration equivalents, Change since Dec. 31, 2007 (% of GDP) 30% 24.9% 20% 10-year equivalents, % of GDP 10% 0% -10% Treasury: Rising Debt Stock Maturity Extension Fed QE 5.5% 15.6% -20%

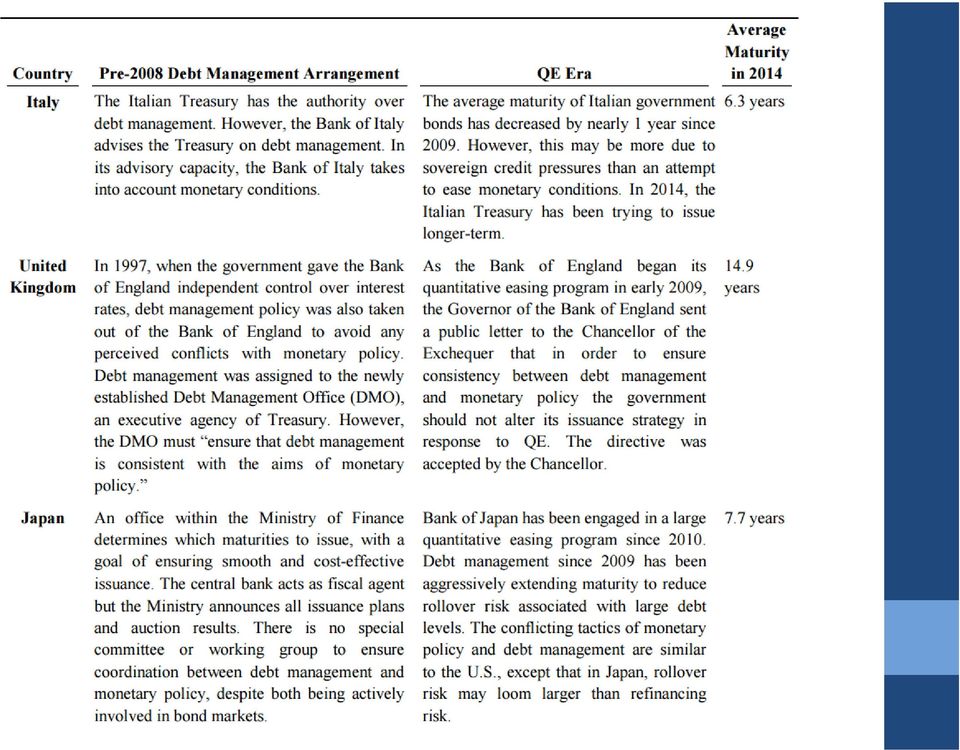

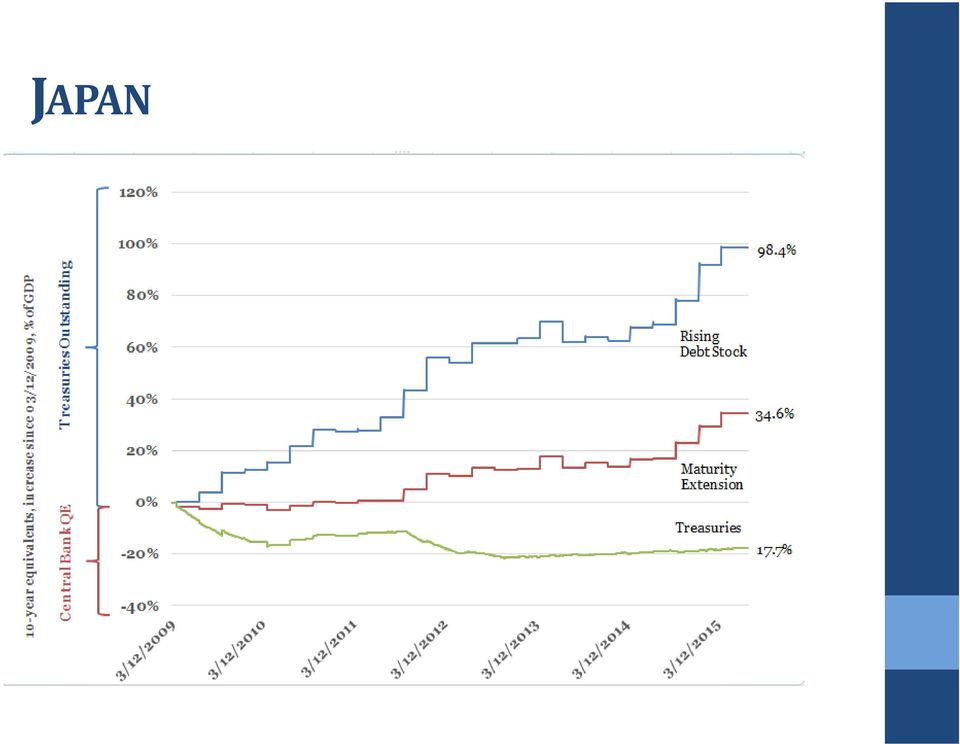

9 OTHER COUNTRIES We have done this analysis for the UK and Japan (and attempted for the Eurozone!) Similar issues in Japan In UK, agreement between BoE and Exchequer mitigates this effect

Similar issues in Japan In UK, agreement")

10 MARKET IMPACT Relying on prior studies, we estimate that the Fed s QE policies have lowered the yield on 10-year Treasuries by a cumulative 1.37 percentage points. Thus, Treasury s maturity extension may have offset as much as one-third of QE s market impact.

11 FED VS. TREASURY HISTORICALLY Before 2008, the Fed s balance sheet was far smaller. As a result, the Fed had little impact on the maturity structure of the government s consolidated debts. 100% 75% % of GDP 50% > 5y 25% 1-5y < 1y 0% <1y > 5y 1-5y -25% Treasury Fed

12 INTERNATIONAL PRECEDENTS FOR COOPERATION

13

14 JAPAN

15 TRADITIONAL DEBT MANAGEMENT Treasury s traditional approach to determining the appropriate maturity of the debt traded off a desire to achieve low cost financing against the desire to limit fiscal risk. Low cost financing Limit fiscal risk Shorter-term Longer-term

16 ELEMENTS OF MODEL Analytical framework from Greenwood, Hanson, Stein (2015) Government: Raises taxes and issues debt to finance a one time expenditure (or an accumulated deficit) Standard tax smoothing motive due to convex distortionary costs New twist: households derive greater monetary / liquidity services from short term debt Absent money demand, govt. opts for longer term debt Eliminates refinancing risk (i.e., govt. needs to raise taxes when short rates rise) which enables govt. to perfectly smooth taxes With money demand, optimally tilts towards short term debt and incurs some refinancing risk Central trade off: Govt. tries to satisfy money demand for short term debt, but is limited by tax smoothing costs of uncertain refinancing Trade offs appear to be reflected in U.S. government maturity choices over time

17 TRADITIONAL DEBT MANAGEMENT Issuing short-term is cheaper because it allows Treasury to capture the liquidity premium on T-bills and to conserve on the term premium investors demand to hold long bonds. Liquidity premium on short-term T-bills, Basis points month OIS 1 month Tbill bps 100 GHS have another measure

18 TRADITIONAL DEBT MANAGEMENT Term Premium on 10-Year Zero-Coupon Treasuries (1990 to 2014) QE1 QE2 Twist QE %

19 TRADITIONAL DEBT MANAGEMENT What is fiscal risk? Refinancing risk If the government issues short-term, it is exposed to increases in interest rates If the government issues long-term, it locks in the cost of capital Rollover risk Failed auction Self-fulfilling bank run

20 TRADITIONAL DEBT MANAGEMENT The desire to limit fiscal risk looms larger when the overall debt burden rises. Low cost financing Limit fiscal risk Shorter-term Longer-term

21 IMPLICATIONS Thus, Treasury has historically tended to extend the average maturity of the debt when debt-to-gdp rises. Much like the Treasury is doing today. 120% 100% 80% 60% 40% 20% 0% Long-term share Treasury Debt/GDP

22 HOW BIG IS FISCAL RISK EMPIRICALLY?

23 QUANTIFYING FISCAL RISK: A COUNTERFACTUAL We argue that the fiscal risk generated by issuing short-term debt is less important than traditionally thought.

24 QUANTIFYING FISCAL RISK: A COUNTERFACTUAL We argue that the fiscal risk generated by issuing short-term debt is less important than traditionally thought.

25 QUANTIFYING FISCAL RISK: A COUNTERFACTUAL We argue that the fiscal risk generated by issuing short-term debt is less important than traditionally thought.

26 FISCAL RISK Driven by changes in short term interest rates But, in practice, rates are high when there are primary surpluses: both rates and surpluses are driven in part by the business cycle Theoretically, the effective weight the social planner places on fiscal risks depends on the covariance between primary surpluses and changes in short term rates

27 TRADITIONAL DEBT MANAGEMENT Low cost financing Limit fiscal risk Shorter-term Longer-term

28 MODERN DEBT MANAGEMENT Modern debt management recognizes that the maturity of government debt may also be a valuable tool for managing aggregate demand and promoting financial stability. Limit fiscal risk Financial stability Aggregate demand Low cost Shorter-term Longer-term

29 FINANCIAL STABILITY Private sector banks who can also engage in money creation Banks want to issue short term, safe debt because it is cheap Caballero & Krishnamurthy 08: Responding to a global shortage, US financial sector tried to manufacture riskless assets precrisis Gorton 10, Gorton & Metrick 09: Money creation by unregulated shadow banking system Banking sector response to cheapness may be socially excessive Stein 12: Excessive private money creation makes the system too vulnerable to crises Short term debt leads to costly fire sales in bad states, since banks must liquidate assets to repay Private banks issue too much short term debt because they do not fully internalize these fire sale costs

30 DEBT MANAGEMENT CONFLICTS Objectives of modern debt management have been assigned to Treasury and Fed, which exercise different policy weights Fed Fed Treasury Financial stability Aggregate demand Low cost Limit fiscal risk Treasury Shorter-term Longer-term

31 OTHER CONSIDERATIONS Inflation protected securities Liquid Benchmark Curve Treasury places value on having a liquid benchmark curve for market participants

32 DEBT MANAGEMENT CONFLICTS Expansionary monetary policy at ZLB Extend average duration to mitigate fiscal risk (Treasury) Shorten average duration to bolster aggregate demand (Fed) Fed and Treasury in direct conflict over objectives Contractionary monetary policy Rise in premium on money-like assets Increases incentive to issue short In this case, Treasury-led debt management is expansionary

33 SOLVING THE CONFLICTS Outside of the zero-lower-bound, Fed sterilization of Treasury debt management is imperfect workaround Fed gets last word using short rate But sterilization no longer possible at the ZLB Better solution: Treasury and Fed release annual joint statement on combined public debt management strategy Forces each agency to internalize other s objectives Fed charged with routine tactical adjustments because of its expertise in open-market operations

34 ADDITIONAL THOUGHTS In an era of low real and nominal interest rates, cooperation between fiscal and monetary authorities becomes more important Even outside of the issues we have presented here, working model of a fully independent central bank is going to come into question

GOVERNMENT DEBT MANAGEMENT AT

Working Paper #5 September 30, 2014 GOVERNMENT DEBT MANAGEMENT AT THE ZERO LOWER BOUND Robin Greenwood, George Gund Professor of Finance and Banking, Harvard Business School Samuel G. Hanson, Assistant

Working Paper #5 September 30, 2014 GOVERNMENT DEBT MANAGEMENT AT THE ZERO LOWER BOUND Robin Greenwood, George Gund Professor of Finance and Banking, Harvard Business School Samuel G. Hanson, Assistant

The Collateral Damage of Today s Monetary Policies: Funding Long-Term Liabilities

The Collateral Damage of Today s Monetary Policies: Funding Long-Term Liabilities Craig Turnbull, Harry Hibbert, Adam Koursaris October 2011 www.barrhibb.com Page Change in Spot Rate (Q3 2008 to Q3 2011)

The Collateral Damage of Today s Monetary Policies: Funding Long-Term Liabilities Craig Turnbull, Harry Hibbert, Adam Koursaris October 2011 www.barrhibb.com Page Change in Spot Rate (Q3 2008 to Q3 2011)

The central task of debt management is to decide which debt instruments THE OPTIMAL MATURITY OF GOVERNMENT DEBT

1 THE OPTIMAL MATURITY OF GOVERNMENT DEBT Robin Greenwood, Samuel G. Hanson, Joshua S. Rudolph, and Lawrence H. Summers The central task of debt management is to decide which debt instruments the government

1 THE OPTIMAL MATURITY OF GOVERNMENT DEBT Robin Greenwood, Samuel G. Hanson, Joshua S. Rudolph, and Lawrence H. Summers The central task of debt management is to decide which debt instruments the government

Why Treasury Yields Are Projected to Remain Low in 2015 March 2015

Why Treasury Yields Are Projected to Remain Low in 5 March 5 PERSPECTIVES Key Insights Monica Defend Head of Global Asset Allocation Research Gabriele Oriolo Analyst Global Asset Allocation Research While

Why Treasury Yields Are Projected to Remain Low in 5 March 5 PERSPECTIVES Key Insights Monica Defend Head of Global Asset Allocation Research Gabriele Oriolo Analyst Global Asset Allocation Research While

Self-fulfilling debt crises: Can monetary policy really help? By P. Bacchetta, E. Van Wincoop and E. Perazzi

Self-fulfilling debt crises: Can monetary policy really help? By P. Bacchetta, E. Van Wincoop and E. Perazzi Discussion by Luca Dedola (ECB) Nonlinearities in Macroeconomics and Finance in Light of the

Self-fulfilling debt crises: Can monetary policy really help? By P. Bacchetta, E. Van Wincoop and E. Perazzi Discussion by Luca Dedola (ECB) Nonlinearities in Macroeconomics and Finance in Light of the

Principles and Trade-Offs when Making Issuance Choices in the UK

Please cite this paper as: OECD (2011), Principles and Trade-Offs when Making Issuance Choices in the UK, OECD Working Papers on Sovereign Borrowing and Public Debt Management, No. 2, OECD Publishing.

Please cite this paper as: OECD (2011), Principles and Trade-Offs when Making Issuance Choices in the UK, OECD Working Papers on Sovereign Borrowing and Public Debt Management, No. 2, OECD Publishing.

11/6/2013. Chapter 16: Government Debt. The U.S. experience in recent years. The troubling long-term fiscal outlook

Chapter 1: Government Debt Indebtedness of the world s governments Country Gov Debt (% of GDP) Country Gov Debt (% of GDP) Japan 17 U.K. 9 Italy 11 Netherlands Greece 11 Norway Belgium 9 Sweden U.S.A.

Chapter 1: Government Debt Indebtedness of the world s governments Country Gov Debt (% of GDP) Country Gov Debt (% of GDP) Japan 17 U.K. 9 Italy 11 Netherlands Greece 11 Norway Belgium 9 Sweden U.S.A.

2.5 Monetary policy: Interest rates

2.5 Monetary policy: Interest rates Learning Outcomes Describe the role of central banks as regulators of commercial banks and bankers to governments. Explain that central banks are usually made responsible

2.5 Monetary policy: Interest rates Learning Outcomes Describe the role of central banks as regulators of commercial banks and bankers to governments. Explain that central banks are usually made responsible

Economics 152 Solution to Sample Midterm 2

Economics 152 Solution to Sample Midterm 2 N. Das PART 1 (84 POINTS): Answer the following 28 multiple choice questions on the scan sheet. Each question is worth 3 points. 1. If Congress passes legislation

Economics 152 Solution to Sample Midterm 2 N. Das PART 1 (84 POINTS): Answer the following 28 multiple choice questions on the scan sheet. Each question is worth 3 points. 1. If Congress passes legislation

Monetary Policy as a Carry Trade

Monetary Policy as a Carry Trade Marvin Goodfriend Carnegie Mellon University 90 th International Business Cycle Conference World Economic Outlook: New Directions for Economic Policy Kiel Institute for

Monetary Policy as a Carry Trade Marvin Goodfriend Carnegie Mellon University 90 th International Business Cycle Conference World Economic Outlook: New Directions for Economic Policy Kiel Institute for

Office of Debt Management. Treasury Debt Management Strategy

Office of Debt Management Treasury Debt Management Strategy Overview Treasury may borrow on the credit of the United States Government amounts necessary for expenditures authorized by law and may issue

Office of Debt Management Treasury Debt Management Strategy Overview Treasury may borrow on the credit of the United States Government amounts necessary for expenditures authorized by law and may issue

International Money and Banking: 12. The Term Structure of Interest Rates

International Money and Banking: 12. The Term Structure of Interest Rates Karl Whelan School of Economics, UCD Spring 2015 Karl Whelan (UCD) Term Structure of Interest Rates Spring 2015 1 / 35 Beyond Interbank

International Money and Banking: 12. The Term Structure of Interest Rates Karl Whelan School of Economics, UCD Spring 2015 Karl Whelan (UCD) Term Structure of Interest Rates Spring 2015 1 / 35 Beyond Interbank

GUIDELINES FOR CENTRAL GOVERNMENT DEBT MANAGEMENT 2015

GUIDELINES FOR CENTRAL GOVERNMENT DEBT MANAGEMENT 2015 Decision taken at the Cabinet meeting November 13 2014 2015 LONG-TERM PERSPECTIVES COST MINIMISATION FLEXIBILITY Guidelines for the mana g ement of

GUIDELINES FOR CENTRAL GOVERNMENT DEBT MANAGEMENT 2015 Decision taken at the Cabinet meeting November 13 2014 2015 LONG-TERM PERSPECTIVES COST MINIMISATION FLEXIBILITY Guidelines for the mana g ement of

Mishkin ch.14: The Money Supply Process

Mishkin ch.14: The Money Supply Process Objective: Show how the Fed controls stocks of money; focus on M1. - Macro theory simply assumes that the Fed can set M via open market operations. - Point here:

Mishkin ch.14: The Money Supply Process Objective: Show how the Fed controls stocks of money; focus on M1. - Macro theory simply assumes that the Fed can set M via open market operations. - Point here:

Markets, Investments, and Financial Management FIFTEENTH EDITION

INTRODUCTION TO FINANCE Markets, Investments, and Financial Management FIFTEENTH EDITION Ronald W. Melicher Professor of Finance University of Colorado at Boulder Edgar A. Norton Professor of Finance Illinois

INTRODUCTION TO FINANCE Markets, Investments, and Financial Management FIFTEENTH EDITION Ronald W. Melicher Professor of Finance University of Colorado at Boulder Edgar A. Norton Professor of Finance Illinois

FISCAL POLICY: HAS BRAZIL GRADUATED FROM PRO- CYCLICAL POLICIES? Marcio Holland Secretary of Economic Policy Ministry of Finance, Brazil

FISCAL POLICY: HAS BRAZIL GRADUATED FROM PRO- CYCLICAL POLICIES? Marcio Holland Secretary of Economic Policy Ministry of Finance, Brazil XXXIX Meeting of the Network of Central Banks and Finance Ministries

FISCAL POLICY: HAS BRAZIL GRADUATED FROM PRO- CYCLICAL POLICIES? Marcio Holland Secretary of Economic Policy Ministry of Finance, Brazil XXXIX Meeting of the Network of Central Banks and Finance Ministries

Highlights from the OECD Sovereign Borrowing Outlook N 4 *

Highlights from the OECD Sovereign Borrowing Outlook N 4 * by Hans J. Blommestein, Ahmet Keskinler and Perla Ibarlucea Flores ** Abstract OECD governments are facing unprecedented challenges in the markets

Highlights from the OECD Sovereign Borrowing Outlook N 4 * by Hans J. Blommestein, Ahmet Keskinler and Perla Ibarlucea Flores ** Abstract OECD governments are facing unprecedented challenges in the markets

Inside and outside liquidity provision

Inside and outside liquidity provision James McAndrews, FRBNY, ECB Workshop on Excess Liquidity and Money Market Functioning, 19/20 November, 2012 The views expressed in this presentation are those of

Inside and outside liquidity provision James McAndrews, FRBNY, ECB Workshop on Excess Liquidity and Money Market Functioning, 19/20 November, 2012 The views expressed in this presentation are those of

Fiscal sustainability, long-term interest rates and debt management

Fiscal sustainability, long-term interest rates and debt management Fabrizio Zampolli Bank for International Settlements Basel A presentation at the Dubrovnik Economic Conference 13-14 June 2013 The opinions

Fiscal sustainability, long-term interest rates and debt management Fabrizio Zampolli Bank for International Settlements Basel A presentation at the Dubrovnik Economic Conference 13-14 June 2013 The opinions

2013 global economic outlook: Are promising growth trends sustainable? Timothy Hopper, Ph.D., Chief Economist, TIAA-CREF January 24, 2013

2013 global economic outlook: Are promising growth trends sustainable? Timothy Hopper, Ph.D., Chief Economist, TIAA-CREF January 24, 2013 U.S. stock market performance in 2012 * +12.59% total return +6.35%

2013 global economic outlook: Are promising growth trends sustainable? Timothy Hopper, Ph.D., Chief Economist, TIAA-CREF January 24, 2013 U.S. stock market performance in 2012 * +12.59% total return +6.35%

Chapter 17. Fixed Exchange Rates and Foreign Exchange Intervention. Copyright 2003 Pearson Education, Inc.

Chapter 17 Fixed Exchange Rates and Foreign Exchange Intervention Slide 17-1 Chapter 17 Learning Goals How a central bank must manage monetary policy so as to fix its currency's value in the foreign exchange

Chapter 17 Fixed Exchange Rates and Foreign Exchange Intervention Slide 17-1 Chapter 17 Learning Goals How a central bank must manage monetary policy so as to fix its currency's value in the foreign exchange

LEBANON'S DEBT MANAGEMENT FRAMEWORK

LEBANON'S DEBT MANAGEMENT FRAMEWORK FOR 2010-2015 MARCH 2010 For further information, please contact: 1 DEBT MANAGEMENT FRAMEWORK FOR 2010-2015 CONTENTS I. Purpose of the report... 5 II. Regulatory framework...

LEBANON'S DEBT MANAGEMENT FRAMEWORK FOR 2010-2015 MARCH 2010 For further information, please contact: 1 DEBT MANAGEMENT FRAMEWORK FOR 2010-2015 CONTENTS I. Purpose of the report... 5 II. Regulatory framework...

Bond Investing in a Rising Rate Environment

September 3 W H I T E PA P E R Bond Investing in a Rising Rate Environment Contents Yields Past, Present and Future Allocation and Mandate Revisited Benchmark Comparisons Investment Options to Consider

September 3 W H I T E PA P E R Bond Investing in a Rising Rate Environment Contents Yields Past, Present and Future Allocation and Mandate Revisited Benchmark Comparisons Investment Options to Consider

Conducting Monetary Policy with Large Public Debts. Gita Gopinath Harvard University

Conducting Monetary Policy with Large Public Debts Gita Gopinath Harvard University 1 Large Public Debts Net Government debt to GDP Greece 155 Japan 134 Portugal 111 Italy 103 Ireland 102 United States

Conducting Monetary Policy with Large Public Debts Gita Gopinath Harvard University 1 Large Public Debts Net Government debt to GDP Greece 155 Japan 134 Portugal 111 Italy 103 Ireland 102 United States

Econ 330 Exam 1 Name ID Section Number

Econ 330 Exam 1 Name ID Section Number MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) If during the past decade the average rate of monetary growth

Econ 330 Exam 1 Name ID Section Number MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) If during the past decade the average rate of monetary growth

A Comparative-Advantage Approach to Government Debt Maturity

A Comparative-Advantage Approach to Government Debt Maturity Robin Greenwood Samuel G. Hanson Jeremy C. Stein Working aper 11-035 Copyright 010 by Robin Greenwood, Samuel G. Hanson, and Jeremy C. Stein

A Comparative-Advantage Approach to Government Debt Maturity Robin Greenwood Samuel G. Hanson Jeremy C. Stein Working aper 11-035 Copyright 010 by Robin Greenwood, Samuel G. Hanson, and Jeremy C. Stein

How To Write A Medium Term Debt Strategy

Medium-Term Debt Strategy Based on Client Presentation May 2010 1 Outline Developing a Medium-Term Debt Strategy Risk Indicators and Sensitivity Analysis Cost-Risk Analysis Implementation Performance Measurement

Medium-Term Debt Strategy Based on Client Presentation May 2010 1 Outline Developing a Medium-Term Debt Strategy Risk Indicators and Sensitivity Analysis Cost-Risk Analysis Implementation Performance Measurement

Research. What Impact Will Ballooning Government Debt Levels Have on Government Bond Yields?

Research What Impact Will Ballooning Government Debt Levels Have on Government Bond Yields? The global economy appears to be on the road to recovery and the risk of a double dip recession is receding.

Research What Impact Will Ballooning Government Debt Levels Have on Government Bond Yields? The global economy appears to be on the road to recovery and the risk of a double dip recession is receding.

Risk of loss: Should investors shift from bonds because of the prospect of rising rates?

Risk of loss: Should investors shift from bonds because of the prospect of rising rates? Vanguard research July 2010 Executive summary. Many investors, whether individual or institutional, hold a diversified

Risk of loss: Should investors shift from bonds because of the prospect of rising rates? Vanguard research July 2010 Executive summary. Many investors, whether individual or institutional, hold a diversified

Debt, consolidation and growth

Debt, consolidation and growth Robert Chote Annual meeting of OECD PBO and IFI officials Paris, 23 February 2012 Outline Very interesting paper. Will focus on UK approach to these issues rather than detailed

Debt, consolidation and growth Robert Chote Annual meeting of OECD PBO and IFI officials Paris, 23 February 2012 Outline Very interesting paper. Will focus on UK approach to these issues rather than detailed

Chapter 17. Preview. Introduction. Fixed Exchange Rates and Foreign Exchange Intervention

Chapter 17 Fixed Exchange Rates and Foreign Exchange Intervention Slides prepared by Thomas Bishop Copyright 2009 Pearson Addison-Wesley. All rights reserved. Preview Balance sheets of central banks Intervention

Chapter 17 Fixed Exchange Rates and Foreign Exchange Intervention Slides prepared by Thomas Bishop Copyright 2009 Pearson Addison-Wesley. All rights reserved. Preview Balance sheets of central banks Intervention

U.S. Treasury Securities

U.S. Treasury Securities U.S. Treasury Securities 4.6 Nonmarketable To help finance its operations, the U.S. government from time to time borrows money by selling investors a variety of debt securities

U.S. Treasury Securities U.S. Treasury Securities 4.6 Nonmarketable To help finance its operations, the U.S. government from time to time borrows money by selling investors a variety of debt securities

Back to Basics Investment Portfolio Risk Management

Back to Basics Investment Portfolio Risk Management By Tom Slefinger, Senior Vice President, Director of Institutional Fixed Income Sales at Balance Sheet Solutions, LLC. Tom can be reached at tom.slefinger@balancesheetsolutions.org.

Back to Basics Investment Portfolio Risk Management By Tom Slefinger, Senior Vice President, Director of Institutional Fixed Income Sales at Balance Sheet Solutions, LLC. Tom can be reached at tom.slefinger@balancesheetsolutions.org.

The Case for Monetary Finance An Essentially Political Issue

16TH JACQUES POLAK ANNUAL RESEARCH CONFERENCE NOVEMBER 5 6, 2015 The Case for Monetary Finance An Essentially Political Issue Adair Turner Institute for New Economic Thinking Paper presented at the 16th

16TH JACQUES POLAK ANNUAL RESEARCH CONFERENCE NOVEMBER 5 6, 2015 The Case for Monetary Finance An Essentially Political Issue Adair Turner Institute for New Economic Thinking Paper presented at the 16th

11.2 Monetary Policy and the Term Structure of Interest Rates

518 Chapter 11 INFLATION AND MONETARY POLICY Thus, the monetary policy that is consistent with a permanent drop in inflation is a sudden upward jump in the money supply, followed by low growth. And, in

518 Chapter 11 INFLATION AND MONETARY POLICY Thus, the monetary policy that is consistent with a permanent drop in inflation is a sudden upward jump in the money supply, followed by low growth. And, in

The Fix Fixed income flashback: is history going to repeat?

December 2014 For professional investors only The Fix Fixed income flashback: is history going to repeat? Kellie Wood, Portfolio Manager, Fixed Income Traditional financial theory portends that bond prices

December 2014 For professional investors only The Fix Fixed income flashback: is history going to repeat? Kellie Wood, Portfolio Manager, Fixed Income Traditional financial theory portends that bond prices

High-Yield Spread U.S. 10-Year Treasury Yield Investment Grade Spread

WisdomTree ETFs BOFA MERRILL LYNCH HIGH YIELD BOND ZERO DURATION FUND HYZD The U.S. high-yield bond market has been one of the best-performing subsets of the fixed income investable universe over the past

WisdomTree ETFs BOFA MERRILL LYNCH HIGH YIELD BOND ZERO DURATION FUND HYZD The U.S. high-yield bond market has been one of the best-performing subsets of the fixed income investable universe over the past

State budget borrowing requirements financing plan and its background May 2013

Public Debt Department State budget borrowing requirements financing plan and its background May 2013 THE MOST IMPORTANT INFORMATION Monthly issuance calendar... 2 Record high level of foreign investors'

Public Debt Department State budget borrowing requirements financing plan and its background May 2013 THE MOST IMPORTANT INFORMATION Monthly issuance calendar... 2 Record high level of foreign investors'

Chapter 12. Page 1. Bonds: Analysis and Strategy. Learning Objectives. INVESTMENTS: Analysis and Management Second Canadian Edition

INVESTMENTS: Analysis and Management Second Canadian Edition W. Sean Cleary Charles P. Jones Chapter 12 Bonds: Analysis and Strategy Learning Objectives Explain why investors buy bonds. Discuss major considerations

INVESTMENTS: Analysis and Management Second Canadian Edition W. Sean Cleary Charles P. Jones Chapter 12 Bonds: Analysis and Strategy Learning Objectives Explain why investors buy bonds. Discuss major considerations

Investment strategy insights

CIO WM Research 9 January 2015 Investment strategy insights Balance sheet optimization Michael Crook, strategist, UBS FS michael.crook@ubs.com, +1 212 649 8153 In our view, households should focus on balance

CIO WM Research 9 January 2015 Investment strategy insights Balance sheet optimization Michael Crook, strategist, UBS FS michael.crook@ubs.com, +1 212 649 8153 In our view, households should focus on balance

Weekly Relative Value

Back to Basics Identifying Value in Fixed Income Markets As managers of fixed income portfolios, one of our key responsibilities is to identify cheap sectors and securities for purchase while avoiding

Back to Basics Identifying Value in Fixed Income Markets As managers of fixed income portfolios, one of our key responsibilities is to identify cheap sectors and securities for purchase while avoiding

The Institutional and Legal Base for Effective Debt Management

December 2001 The Institutional and Legal Base for Effective Debt Management Tomas Magnusson Paper prepared for the Third Inter-regional Debt Management Conference in Geneva 3-5 December 2001, arranged

December 2001 The Institutional and Legal Base for Effective Debt Management Tomas Magnusson Paper prepared for the Third Inter-regional Debt Management Conference in Geneva 3-5 December 2001, arranged

PRESENT DISCOUNTED VALUE

THE BOND MARKET Bond a fixed (nominal) income asset which has a: -face value (stated value of the bond) - coupon interest rate (stated interest rate) - maturity date (length of time for fixed income payments)

THE BOND MARKET Bond a fixed (nominal) income asset which has a: -face value (stated value of the bond) - coupon interest rate (stated interest rate) - maturity date (length of time for fixed income payments)

Monetary policy, fiscal policy and public debt management

Monetary policy, fiscal policy and public debt management People s Bank of China Abstract This paper touches on the interaction between monetary policy, fiscal policy and public debt management. The first

Monetary policy, fiscal policy and public debt management People s Bank of China Abstract This paper touches on the interaction between monetary policy, fiscal policy and public debt management. The first

FINANCIAL DOMINANCE MARKUS K. BRUNNERMEIER & YULIY SANNIKOV

Based on: The I Theory of Money - Redistributive Monetary Policy CFS Symposium: Banking, Liquidity, and Monetary Policy 26 September 2013, Frankfurt am Main 2013 FINANCIAL DOMINANCE MARKUS K. BRUNNERMEIER

Based on: The I Theory of Money - Redistributive Monetary Policy CFS Symposium: Banking, Liquidity, and Monetary Policy 26 September 2013, Frankfurt am Main 2013 FINANCIAL DOMINANCE MARKUS K. BRUNNERMEIER

Chapter 3 Fixed Income Securities

Chapter 3 Fixed Income Securities Road Map Part A Introduction to finance. Part B Valuation of assets, given discount rates. Fixed-income securities. Stocks. Real assets (capital budgeting). Part C Determination

Chapter 3 Fixed Income Securities Road Map Part A Introduction to finance. Part B Valuation of assets, given discount rates. Fixed-income securities. Stocks. Real assets (capital budgeting). Part C Determination

2.If actual investment is greater than planned investment, inventories increase more than planned. TRUE.

Macro final exam study guide True/False questions - Solutions Case, Fair, Oster Chapter 8 Aggregate Expenditure and Equilibrium Output 1.Firms react to unplanned inventory investment by reducing output.

Macro final exam study guide True/False questions - Solutions Case, Fair, Oster Chapter 8 Aggregate Expenditure and Equilibrium Output 1.Firms react to unplanned inventory investment by reducing output.

Managing the Fragility of the Eurozone. Paul De Grauwe University of Leuven

Managing the Fragility of the Eurozone Paul De Grauwe University of Leuven Paradox Gross government debt (% of GDP) 100 90 80 70 UK Spain 60 50 40 30 20 10 0 2000 2001 2002 2003 2004 2005 2006 2007 2008

Managing the Fragility of the Eurozone Paul De Grauwe University of Leuven Paradox Gross government debt (% of GDP) 100 90 80 70 UK Spain 60 50 40 30 20 10 0 2000 2001 2002 2003 2004 2005 2006 2007 2008

The Risk of Fixed Income Indexing vs. Active Multi-Sector Management

Pioneer Perspectives TM May 2012 The Risk of Fixed Income Indexing vs. Active Multi-Sector Management A Different Future for Fixed Income Investors? Tepid economic growth coupled with volatile equity markets

Pioneer Perspectives TM May 2012 The Risk of Fixed Income Indexing vs. Active Multi-Sector Management A Different Future for Fixed Income Investors? Tepid economic growth coupled with volatile equity markets

The Response of Interest Rates to U.S. and U.K. Quantitative Easing

The Response of Interest Rates to U.S. and U.K. Quantitative Easing Jens H.E. Christensen & Glenn D. Rudebusch Federal Reserve Bank of San Francisco Term Structure Modeling and the Lower Bound Problem

The Response of Interest Rates to U.S. and U.K. Quantitative Easing Jens H.E. Christensen & Glenn D. Rudebusch Federal Reserve Bank of San Francisco Term Structure Modeling and the Lower Bound Problem

What Investors Should Know about Money Market Reforms

What Investors Should Know about Money Market Reforms What Investors Should Know about Money Market Reforms Executive Summary Ò New SEC regulations for the $2.7 trillion money market industry may present

What Investors Should Know about Money Market Reforms What Investors Should Know about Money Market Reforms Executive Summary Ò New SEC regulations for the $2.7 trillion money market industry may present

NOTES ON OPTIMAL DEBT MANAGEMENT

Journal of Applied Economics, Vol. II, No. 2 (Nov 1999), 281-289 NOTES ON OPTIMAL DEBT MANAGEMENT 281 NOTES ON OPTIMAL DEBT MANAGEMENT ROBERT J. BARRO Harvard University Consider the finance of an exogenous

Journal of Applied Economics, Vol. II, No. 2 (Nov 1999), 281-289 NOTES ON OPTIMAL DEBT MANAGEMENT 281 NOTES ON OPTIMAL DEBT MANAGEMENT ROBERT J. BARRO Harvard University Consider the finance of an exogenous

Convertibles: An investment solution for Insurance portfolios in challenging times

Convertibles: An investment solution for Insurance portfolios in challenging times By: Ravi Malik, CFA April 2013 Introduction In recent years the Federal Reserve has implemented unprecedented monetary

Convertibles: An investment solution for Insurance portfolios in challenging times By: Ravi Malik, CFA April 2013 Introduction In recent years the Federal Reserve has implemented unprecedented monetary

FRBSF ECONOMIC LETTER

FRBSF ECONOMIC LETTER 2010-03 February 1, 2010 Mortgage Choice and the Pricing of Fixed-Rate and Adjustable-Rate Mortgages BY JOHN KRAINER In the United States throughout 2009, the share of adjustable-rate

FRBSF ECONOMIC LETTER 2010-03 February 1, 2010 Mortgage Choice and the Pricing of Fixed-Rate and Adjustable-Rate Mortgages BY JOHN KRAINER In the United States throughout 2009, the share of adjustable-rate

Chapter 11 Money and Monetary Policy Macroeconomics In Context (Goodwin, et al.)

") Chapter 11 Money and Monetary Policy Macroeconomics In Context (Goodwin, et al.) Chapter Overview In this chapter, you will be introduced to a standard treatment of the banking system and monetary policy.

Chapter 11 Money and Monetary Policy Macroeconomics In Context (Goodwin, et al.) Chapter Overview In this chapter, you will be introduced to a standard treatment of the banking system and monetary policy.

GOVERNMENT OF SAINT LUCIA DEBT MANAGEMENT STRATEGY

Page 1 of 5 Introduction GOVERNMENT OF SAINT LUCIA DEBT MANAGEMENT STRATEGY Debt management is the process of establishing and executing a strategy for managing the government s debt in order to raise

Page 1 of 5 Introduction GOVERNMENT OF SAINT LUCIA DEBT MANAGEMENT STRATEGY Debt management is the process of establishing and executing a strategy for managing the government s debt in order to raise

Republic of Italy Borrowing Strategy 30-yr Syndicated BTP. Public Debt Department Italian Treasury

Republic of Italy Borrowing Strategy 30-yr Syndicated BTP Public Debt Department Italian Treasury September 2003 2 Introduction Strengthened Public Finance Framework The Republic of Italy has focused on

Republic of Italy Borrowing Strategy 30-yr Syndicated BTP Public Debt Department Italian Treasury September 2003 2 Introduction Strengthened Public Finance Framework The Republic of Italy has focused on

CHAPTER 7: FIXED-INCOME SECURITIES: PRICING AND TRADING

CHAPTER 7: FIXED-INCOME SECURITIES: PRICING AND TRADING Topic One: Bond Pricing Principles 1. Present Value. A. The present-value calculation is used to estimate how much an investor should pay for a bond;

CHAPTER 7: FIXED-INCOME SECURITIES: PRICING AND TRADING Topic One: Bond Pricing Principles 1. Present Value. A. The present-value calculation is used to estimate how much an investor should pay for a bond;

Development of Money Markets

Development of Money Markets Mats Filipsson International Monetary Fund Monetary and Exchange Affairs Department Workshop on Developing Government Bond Markets in APEC Economies Shanghai, November 12 15,

Development of Money Markets Mats Filipsson International Monetary Fund Monetary and Exchange Affairs Department Workshop on Developing Government Bond Markets in APEC Economies Shanghai, November 12 15,

Moving Forward With the Normalization of Yields

Moving Forward With the Normalization of Yields April 8, 2014 by Scott Mather, Michael Story of PIMCO One response to yield normalization is to consider retaining core bonds and diversifying the specific

Moving Forward With the Normalization of Yields April 8, 2014 by Scott Mather, Michael Story of PIMCO One response to yield normalization is to consider retaining core bonds and diversifying the specific

6. Budget Deficits and Fiscal Policy

Prof. Dr. Thomas Steger Advanced Macroeconomics II Lecture SS 2012 6. Budget Deficits and Fiscal Policy Introduction Ricardian equivalence Distorting taxes Debt crises Introduction (1) Ricardian equivalence

Prof. Dr. Thomas Steger Advanced Macroeconomics II Lecture SS 2012 6. Budget Deficits and Fiscal Policy Introduction Ricardian equivalence Distorting taxes Debt crises Introduction (1) Ricardian equivalence

The Empirical Approach to Interest Rate and Credit Risk in a Fixed Income Portfolio

www.empirical.net Seattle Portland Eugene Tacoma Anchorage March 27, 2013 The Empirical Approach to Interest Rate and Credit Risk in a Fixed Income Portfolio By Erik Lehr In recent weeks, market news about

www.empirical.net Seattle Portland Eugene Tacoma Anchorage March 27, 2013 The Empirical Approach to Interest Rate and Credit Risk in a Fixed Income Portfolio By Erik Lehr In recent weeks, market news about

The Liquidity Trap and U.S. Interest Rates in the 1930s

The Liquidity Trap and U.S. Interest Rates in the 1930s SHORT SUMMARY Christopher Hanes Department of Economics School of Business University of Mississippi University, MS 38677 (662) 915-5829 chanes@bus.olemiss.edu

The Liquidity Trap and U.S. Interest Rates in the 1930s SHORT SUMMARY Christopher Hanes Department of Economics School of Business University of Mississippi University, MS 38677 (662) 915-5829 chanes@bus.olemiss.edu

Bonds and Yield to Maturity

Bonds and Yield to Maturity Bonds A bond is a debt instrument requiring the issuer to repay to the lender/investor the amount borrowed (par or face value) plus interest over a specified period of time.

Bonds and Yield to Maturity Bonds A bond is a debt instrument requiring the issuer to repay to the lender/investor the amount borrowed (par or face value) plus interest over a specified period of time.

The Public Finance Sector DEBT MANAGEMENT STRATEGY. In the years 2006-2008

The Public Finance Sector DEBT MANAGEMENT STRATEGY In the years 2006-2008 Ministry of Finance Warsaw, September 2005 The Public Finance Sector DEBT MANAGEMENT STRATEGY in the years 2006-08 I. INTRODUCTION

The Public Finance Sector DEBT MANAGEMENT STRATEGY In the years 2006-2008 Ministry of Finance Warsaw, September 2005 The Public Finance Sector DEBT MANAGEMENT STRATEGY in the years 2006-08 I. INTRODUCTION

Futures Price d,f $ 0.65 = (1.05) (1.04)

(1.04)") 24 e. Currency Futures In a currency futures contract, you enter into a contract to buy a foreign currency at a price fixed today. To see how spot and futures currency prices are related, note that holding

24 e. Currency Futures In a currency futures contract, you enter into a contract to buy a foreign currency at a price fixed today. To see how spot and futures currency prices are related, note that holding

4 Further details of the responses received are presented below.

REPORT ON BOND EXCHANGES AND DEBT BUY-BACKS A SURVEY OF PRACTICE BY EC DEBT MANAGERS In June 2001 a questionnaire covering the practices followed by debt managers implementing bond exchange or buy-back

REPORT ON BOND EXCHANGES AND DEBT BUY-BACKS A SURVEY OF PRACTICE BY EC DEBT MANAGERS In June 2001 a questionnaire covering the practices followed by debt managers implementing bond exchange or buy-back

NPH Fixed Income Research Update. Bob Downing, CFA. NPH Senior Investment & Due Diligence Analyst

White Paper: NPH Fixed Income Research Update Authored By: Bob Downing, CFA NPH Senior Investment & Due Diligence Analyst National Planning Holdings, Inc. Due Diligence Department National Planning Holdings,

White Paper: NPH Fixed Income Research Update Authored By: Bob Downing, CFA NPH Senior Investment & Due Diligence Analyst National Planning Holdings, Inc. Due Diligence Department National Planning Holdings,

Eighth UNCTAD Debt Management Conference

Eighth UNCTAD Debt Management Conference Geneva, 14-16 November 2011 Debt Resolution Mechanisms: Should there be a Statutory Mechanism for Resolving Debt Crises? by Mr. Hakan Tokaç Deputy Director General

Eighth UNCTAD Debt Management Conference Geneva, 14-16 November 2011 Debt Resolution Mechanisms: Should there be a Statutory Mechanism for Resolving Debt Crises? by Mr. Hakan Tokaç Deputy Director General

State budget borrowing requirements financing plan and its background

Public Debt Department State budget borrowing requirements financing plan and its background September 2014 THE MOST IMPORTANT INFORMATION Monthly issuance calendar... 2 MoF comment... 8 Rating agencies

Public Debt Department State budget borrowing requirements financing plan and its background September 2014 THE MOST IMPORTANT INFORMATION Monthly issuance calendar... 2 MoF comment... 8 Rating agencies

Global bond investing

Global bond investing Todd Schlanger, CFA Investment Strategy Group Vanguard Asset Management, Limited This document is directed at professional investors and should not be distributed to, or relied upon

Global bond investing Todd Schlanger, CFA Investment Strategy Group Vanguard Asset Management, Limited This document is directed at professional investors and should not be distributed to, or relied upon

Danish mortgage bonds provide attractive yields and low risk

JANUARY 2015 Danish mortgage bonds provide attractive yields and low risk New European Union legislation favours Danish mortgage bonds KEY CONCEPTS New legislation favours Danish mortgage bonds Attractive

JANUARY 2015 Danish mortgage bonds provide attractive yields and low risk New European Union legislation favours Danish mortgage bonds KEY CONCEPTS New legislation favours Danish mortgage bonds Attractive

Governments Debt and Asset Management and Financial Crises: Sellers Beware. By Michael P. Dooley. Revised February 1997

Governments Debt and Asset Management and Financial Crises: Sellers Beware By Michael P. Dooley Revised February 1997 I Introduction A great deal of attention has recently been devoted to the question

Governments Debt and Asset Management and Financial Crises: Sellers Beware By Michael P. Dooley Revised February 1997 I Introduction A great deal of attention has recently been devoted to the question

Behavior of Interest Rates

Behavior of Interest Rates Notes on Mishkin Chapter 5 (pages 91-108) Prof. Leigh Tesfatsion (Iowa State U) Last Revised: 21 February 2011 Mishkin Chapter 5: Selected Key In-Class Discussion Questions and

Behavior of Interest Rates Notes on Mishkin Chapter 5 (pages 91-108) Prof. Leigh Tesfatsion (Iowa State U) Last Revised: 21 February 2011 Mishkin Chapter 5: Selected Key In-Class Discussion Questions and

Guidelines for central government debt management 2015

12 March 2015 Guidelines for central government debt management 2015 The debt management is regulated by the Budget Act (2011:203), Ordinance (2007:1447) containing Instructions for the National Debt Office

12 March 2015 Guidelines for central government debt management 2015 The debt management is regulated by the Budget Act (2011:203), Ordinance (2007:1447) containing Instructions for the National Debt Office

Investment Solutions for Federal Funds - Retirement Plans

LGIP QUARTERLY MEETING & CONFERENCE CALL 7.26.2012 OFFICE OF THE ARIZONA STATE TREASURER AGENDA LGIP Performance Endowment Performance Endowment Distribution Formula State Cash Flow Guest Presentation:

LGIP QUARTERLY MEETING & CONFERENCE CALL 7.26.2012 OFFICE OF THE ARIZONA STATE TREASURER AGENDA LGIP Performance Endowment Performance Endowment Distribution Formula State Cash Flow Guest Presentation:

U.S. ECONOMIC ACTIVITY. http://www.dallasfed.org

U.S. ECONOMIC ACTIVITY 1-month % change 1.5 Nominal Personal Consumption Expenditures 1.0 0.5 0.0-0.5-1.0-1.5 Aug-29-release, Jul = 0.33 Source: Bureau of Economic Analysis 1-month % change 1.0 Real Personal

U.S. ECONOMIC ACTIVITY 1-month % change 1.5 Nominal Personal Consumption Expenditures 1.0 0.5 0.0-0.5-1.0-1.5 Aug-29-release, Jul = 0.33 Source: Bureau of Economic Analysis 1-month % change 1.0 Real Personal

U.S. ECONOMIC ACTIVITY. http://www.dallasfed.org

U.S. ECONOMIC ACTIVITY Index of Leading Economic Indicators 140 Index 130 120 110 100 90 80 70 1998 1999 2000 2001 2002 2003 2004 2005 2006 Recession Leading Index (Aug-18-release, Jul = 124.3) Source:

U.S. ECONOMIC ACTIVITY Index of Leading Economic Indicators 140 Index 130 120 110 100 90 80 70 1998 1999 2000 2001 2002 2003 2004 2005 2006 Recession Leading Index (Aug-18-release, Jul = 124.3) Source:

FUNDS TM. G10 Currencies: White Paper. A Monetary Policy Analysis FUNDS. The Authority on Currencies

FUNDS White Paper The Authority on Currencies Merk Investments LLC Research MAY 2012 G10 Currencies: A Monetary Policy Analysis Merk Monetary Score favors currencies of, and Canada; disfavors currencies

FUNDS White Paper The Authority on Currencies Merk Investments LLC Research MAY 2012 G10 Currencies: A Monetary Policy Analysis Merk Monetary Score favors currencies of, and Canada; disfavors currencies

Bond Markets in Emerging Asia: Progress, Challenges, and ADB Work Plan to Support Bond Market Development. Asian Development Bank

Bond Markets in Emerging Asia: Progress, Challenges, and ADB Work Plan to Support Bond Market Development Asian Development Bank November 2009 A. Noy Siackhachanh Advisor Office of Regional Economic Integration

Bond Markets in Emerging Asia: Progress, Challenges, and ADB Work Plan to Support Bond Market Development Asian Development Bank November 2009 A. Noy Siackhachanh Advisor Office of Regional Economic Integration

SACRS Fall Conference 2013

SACRS Fall Conference 2013 Bank Loans November 14, 2013 Allan Martin, Partner What Are Floating Rate Bank Loans? Senior secured floating rate debt: Current Typical Terms: Spread: LIBOR + 5.00%-6.00% LIBOR

SACRS Fall Conference 2013 Bank Loans November 14, 2013 Allan Martin, Partner What Are Floating Rate Bank Loans? Senior secured floating rate debt: Current Typical Terms: Spread: LIBOR + 5.00%-6.00% LIBOR

Project LINK Meeting New York, 20-22 October 2010. Country Report: Australia

Project LINK Meeting New York, - October 1 Country Report: Australia Prepared by Peter Brain: National Institute of Economic and Industry Research, and Duncan Ironmonger: Department of Economics, University

Project LINK Meeting New York, - October 1 Country Report: Australia Prepared by Peter Brain: National Institute of Economic and Industry Research, and Duncan Ironmonger: Department of Economics, University

The table below shows Capita Asset Services forecast of the expected movement in medium term interest rates:

Annex A Forecast of interest rates as at September 2015 The table below shows Capita Asset Services forecast of the expected movement in medium term interest rates: NOW Sep-15 Dec-15 Mar-16 Jun-16 Sep-16

Annex A Forecast of interest rates as at September 2015 The table below shows Capita Asset Services forecast of the expected movement in medium term interest rates: NOW Sep-15 Dec-15 Mar-16 Jun-16 Sep-16

Cash Flow Forecasting and Cash Balance Management DPI 10

Cash Flow Forecasting and Cash Balance Management DPI 10 Cash forecasting and cash management - Background 1 What is cash management? The strategy and associated processes for managing cost-effective the

Cash Flow Forecasting and Cash Balance Management DPI 10 Cash forecasting and cash management - Background 1 What is cash management? The strategy and associated processes for managing cost-effective the

Bond Fund Investing in a Rising Rate Environment

MUTUAL FUND RESEARCH Danette Szakaly Ext. 71937 Date Issued: 1/14/11 Fund Investing in a Rising Rate Environment The recent rise in U.S. Treasury bond yields has some investors wondering how to manage

MUTUAL FUND RESEARCH Danette Szakaly Ext. 71937 Date Issued: 1/14/11 Fund Investing in a Rising Rate Environment The recent rise in U.S. Treasury bond yields has some investors wondering how to manage

UK Government s Public Finance Plans and Fiscal Targets

UK Government s Public Finance Plans and Fiscal Targets Scottish Government June 2015 Overview This paper analyses the scope to make different choices about the UK s public finances, within the fiscal

UK Government s Public Finance Plans and Fiscal Targets Scottish Government June 2015 Overview This paper analyses the scope to make different choices about the UK s public finances, within the fiscal

Guidelines for public debt management

2016 Guidelines for public debt management 2016 Public Debt Management Guidelines Contents FOREWORD... 3 2016 ISSUANCE PROGRAMME AND DEBT MANAGEMENT... 4 Preliminary considerations... 4 ISSUANCE PROGRAMME

2016 Guidelines for public debt management 2016 Public Debt Management Guidelines Contents FOREWORD... 3 2016 ISSUANCE PROGRAMME AND DEBT MANAGEMENT... 4 Preliminary considerations... 4 ISSUANCE PROGRAMME

Pre-Test Chapter 11 ed17

Pre-Test Chapter 11 ed17 Multiple Choice Questions 1. Built-in stability means that: A. an annually balanced budget will offset the procyclical tendencies created by state and local finance and thereby

Pre-Test Chapter 11 ed17 Multiple Choice Questions 1. Built-in stability means that: A. an annually balanced budget will offset the procyclical tendencies created by state and local finance and thereby

Supplemental Unit 5: Fiscal Policy and Budget Deficits

1 Supplemental Unit 5: Fiscal Policy and Budget Deficits Fiscal and monetary policies are the two major tools available to policy makers to alter total demand, output, and employment. This feature will

1 Supplemental Unit 5: Fiscal Policy and Budget Deficits Fiscal and monetary policies are the two major tools available to policy makers to alter total demand, output, and employment. This feature will

What three main functions do they have? Reducing transaction costs, reducing financial risk, providing liquidity

Unit 4 Test Review KEY Savings, Investment and the Financial System 1. What is a financial intermediary? Explain how each of the following fulfills that role: Financial Intermediary: Transforms funds into

Unit 4 Test Review KEY Savings, Investment and the Financial System 1. What is a financial intermediary? Explain how each of the following fulfills that role: Financial Intermediary: Transforms funds into

If Some Dare Call It Treason, Was Milton Friedman a Traitor?

N O R T H E R N T R U S T G L O B A L E C O N O M I C R E S E A R C H If Some Dare Call It Treason, Was Milton Friedman a Traitor? September 211 Paul L. Kasriel, Chief Economist PH: 312.444.4145 4 4 plk1@ntrs.com

N O R T H E R N T R U S T G L O B A L E C O N O M I C R E S E A R C H If Some Dare Call It Treason, Was Milton Friedman a Traitor? September 211 Paul L. Kasriel, Chief Economist PH: 312.444.4145 4 4 plk1@ntrs.com

Politics, Surpluses, Deficits, and Debt

Defining Surpluses and Debt Politics, Surpluses,, and Debt Chapter 11 A surplus is an excess of revenues over payments. A deficit is a shortfall of revenues relative to payments. 2 Introduction After having

Defining Surpluses and Debt Politics, Surpluses,, and Debt Chapter 11 A surplus is an excess of revenues over payments. A deficit is a shortfall of revenues relative to payments. 2 Introduction After having

Development of the government bond market and public debt management in Singapore

Development of the government bond market and public debt management in Singapore Monetary Authority of Singapore Abstract This paper describes the growth of the Singapore Government Securities (SGS) market.

Development of the government bond market and public debt management in Singapore Monetary Authority of Singapore Abstract This paper describes the growth of the Singapore Government Securities (SGS) market.

THE CDS AND THE GOVERNMENT BONDS MARKETS AFTER THE LAST FINANCIAL CRISIS. The CDS and the Government Bonds Markets after the Last Financial Crisis

THE CDS AND THE GOVERNMENT BONDS MARKETS AFTER THE LAST FINANCIAL CRISIS The CDS and the Government Bonds Markets after the Last Financial Crisis Abstract In the 1990s, the financial market had developed

THE CDS AND THE GOVERNMENT BONDS MARKETS AFTER THE LAST FINANCIAL CRISIS The CDS and the Government Bonds Markets after the Last Financial Crisis Abstract In the 1990s, the financial market had developed

U.S. ECONOMIC ACTIVITY. http://www.dallasfed.org

U.S. ECONOMIC ACTIVITY Purchasing Managers Index Index 65 60 55 50 45 40 35 30 Aug-01-release, Jul = 52.6 Source: Institute for Supply Management Real Value of the Dollar March 1973 = 100 120 110 100 90

U.S. ECONOMIC ACTIVITY Purchasing Managers Index Index 65 60 55 50 45 40 35 30 Aug-01-release, Jul = 52.6 Source: Institute for Supply Management Real Value of the Dollar March 1973 = 100 120 110 100 90

The Interest Rate Conundrum: Interest Rates Are Too Low

The Interest Rate Conundrum: Interest Rates Are Too Low By Brian Fabbri (February 2013) The present aggressive and unconventional monetary policy carried out by the US Federal Reserve, the ECB, and the

The Interest Rate Conundrum: Interest Rates Are Too Low By Brian Fabbri (February 2013) The present aggressive and unconventional monetary policy carried out by the US Federal Reserve, the ECB, and the

Fixed Income in a Rising Rate Environment

Fixed Income in a Rising Rate Environment Market Commentary May 2016 SINCE THE FIRST FEDERAL FUNDS RATE INCREASE IN DECEMBER 2015, interest rates have generally declined. This counterintuitive result underscores

Fixed Income in a Rising Rate Environment Market Commentary May 2016 SINCE THE FIRST FEDERAL FUNDS RATE INCREASE IN DECEMBER 2015, interest rates have generally declined. This counterintuitive result underscores

Chapter 1. Why Study Money, Banking, and Financial Markets?

Chapter 1 Why Study Money, Banking, and Financial Markets? Why Study Money, Banking, and Financial Markets To examine how financial markets such as bond, stock and foreign exchange markets work To examine

Chapter 1 Why Study Money, Banking, and Financial Markets? Why Study Money, Banking, and Financial Markets To examine how financial markets such as bond, stock and foreign exchange markets work To examine

Bonds - Strategic S fixed Income Portfolio Management

OPTIMIZING YOUR BOND PORTFOLIO THROUGH RISK FACTOR MODELING FIXED INCOME INVESTMENTS SPAN A BROAD RANGE OF SENSITIVITIES TO CHANGES IN YIELDS AND CREDIT SPREADS. Understanding how different types of fixed

OPTIMIZING YOUR BOND PORTFOLIO THROUGH RISK FACTOR MODELING FIXED INCOME INVESTMENTS SPAN A BROAD RANGE OF SENSITIVITIES TO CHANGES IN YIELDS AND CREDIT SPREADS. Understanding how different types of fixed

The Yield Curve, Stocks, and Interest Rates

The Yield Curve, Stocks, and Interest Rates The Yield Curve as of 6/26/09 (from Bloomberg.com): Bonds with identical risk, liquidity, and tax characteristics have different interest rates based on time

The Yield Curve, Stocks, and Interest Rates The Yield Curve as of 6/26/09 (from Bloomberg.com): Bonds with identical risk, liquidity, and tax characteristics have different interest rates based on time