Member Business Lending October 14, 2015

|

|

|

- Claire Lawrence

- 8 years ago

- Views:

Transcription

1 Member Business Lending October 14, 2015 Presented by BKD, LLP John Bourquard, Principal Ryan Swope, Director

2 Topics We ll Cover Current Trends Case studies Credit Administration

3 Charge-Offs

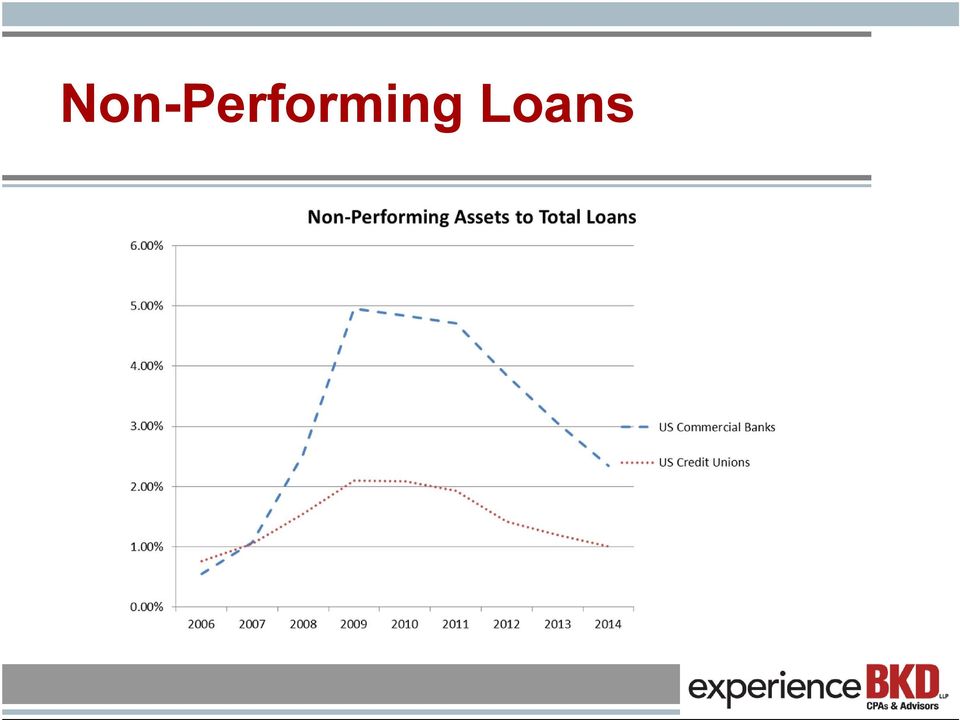

4 Non-Performing Loans

5 Bank Failures

6 Credit Union Failures YTD

7 Problem Banks

8 Troubled Credit Unions At the end of 2014, assets in CAMEL code 3, 4 and 5 rated credit unions dropped to $109.6 billion, compared to $122.4 billion at the end of The number of troubled credit unions also declined to 276 at the end of 2014, down 10.1 percent for the year.

9 CAMEL Ratings In all, 4.4 percent of all federally insured credit unions were troubled in 2014, compared to 4.7 percent in At the end of 2014, troubled credit unions held just 1 percent of the system s assets.

10 BKD s Median Observations on Classified Assets to Capital

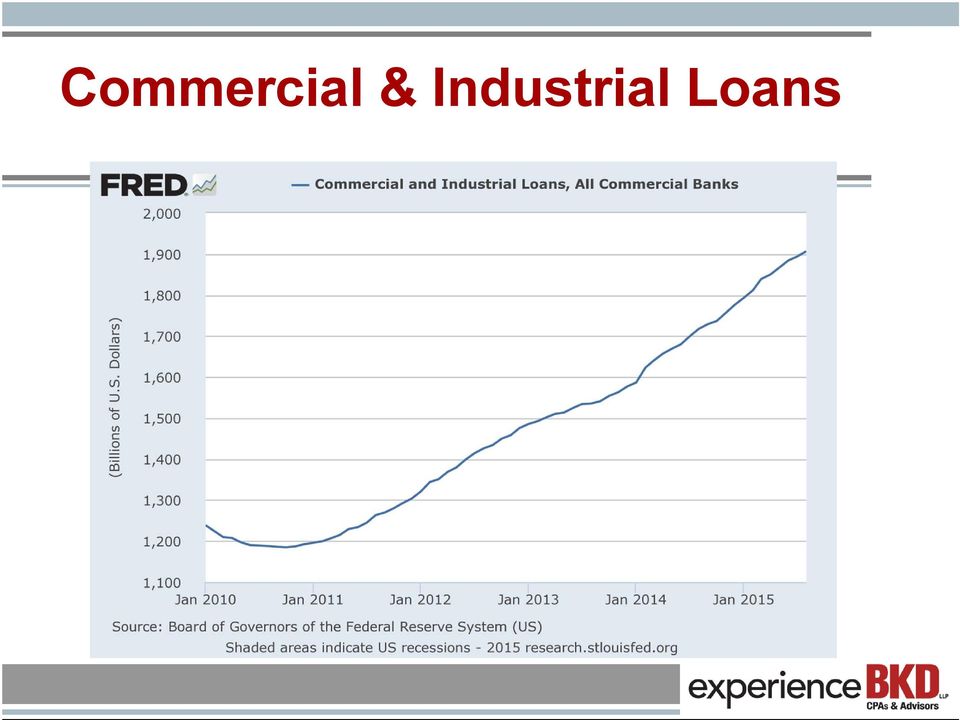

11 Commercial & Industrial Loans

12 Loan Growth Loan growth has been modest 10% at credit unions 6% at banks Led by institutions showing large growth rates Many are still struggling to find growth

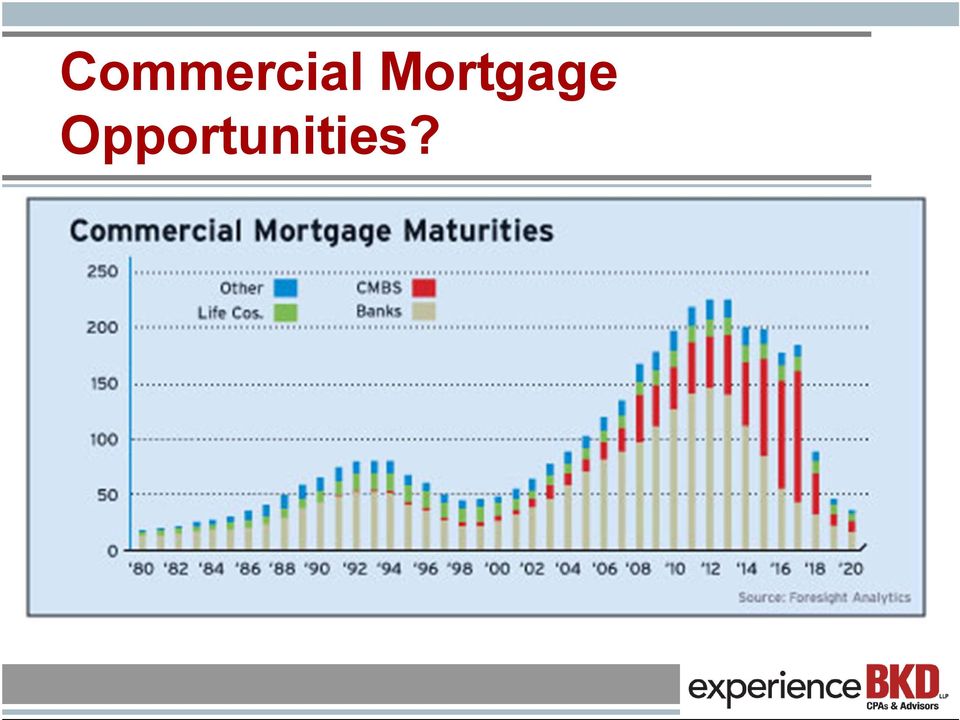

13 Commercial Mortgage Opportunities?

14 Current Risks Growth and earnings pressures Changing credit risk tolerances Intense competition Easing of underwriting standards More policy exceptions, often multiple exceptions

15 Current Risks Growth and earnings pressures continued Doing more with less Underwriting Monitoring Reaching for yield while increasing credit risk New loan types requiring specialists Sacrificing loan quality in favor of growth

16 Current Risks Growth and earnings pressures continued In general, high level of strategic risk as banks and credit unions adapt to sluggish growth and low rates

17 Easing Credit Standards Erosion of underwriting standards Leveraged lending Indirect lending 60% of auto loans in 4 th qtr had terms of 72 months or more (OCC) Average advance in 4 th quarter 2014 was 137% (and 150% for subprime). Construction and development lending

.")

18 Easing Credit Standards Risk layering Increased collateral advance rates Not requiring/ lowering guarantees Extended interest only payments and longer amortization Increasing policy exceptions Loosening financial covenants

19 Growth and Delinquency Year 1 Year 2 Year 3 Loans $10MM $20MM $40MM Delinquent $60M $400M $1,200M Percent 0.60% 2.0% 3.0%

20 Growth and Delinquency Year 1 Year 2 Year 3 Loans $10MM $20MM $40MM Delinquent $60M $400M $1,200M Percent of prior Year Loans 4.0% 6.0% Delinquency is a lagging indicator of credit quality

21 CASE STUDY #1 Real estate investor lower priced rental homes Rapid Growth Weakening cash flow

22 CASE STUDY # Available for DS (NOI) $861M $862M $596M (Global) Estimated DS $674M $1,019M $1,050M Excess/Shortfall $187M ($157M) ($454M) Debt Coverage Ratio

23 CASE STUDY #1 Guarantor s PFS Cash Real Estate Total Assets $ 800M $22,261M $27,305M Mortgage Debt $17,382M Net Worth $ 9,910M

24 CASE STUDY #1 The Bank s Perspective: Bank analyzed each loan based on projections which showed positive results. It performed a global cash flow analysis, but discounted the negative results. He doesn t report all of his income. Bank was comforted by the $800M of cash on the PFS and the $9.9MM net worth. He always paid as agreed!

25 CASE STUDY #1 Consider however: How much NOI should $22MM of real estate produce? $1.1MM to $1.5MM. How short is the cash flow on covering just interest on $17MM of debt? $350M. What value might an NOI of $596M support? Maybe $12MM or so.

26 CASE STUDY #1 Result: Fraud by the borrower Loss of over 50% of the bank s loans A loss they could have easily avoided

27 Drivers of Credit Risk Economy Credit administration Concentrations Structural weakness in loans

28 Drivers of Credit Risk Credit Administration Number one driver of risk Shaping how your bank will look in the next economic downturn Policy Underwriting Monitoring Collecting

29 Drivers of Credit Risk Concentrations Concentrations can be dangerous Always view in terms of capital Limit? Percent that might migrate to problem status if economy turns? Percent of loan that might be lost?

30 Drivers of Credit Risk Structural Weakness Indefinite or speculative loan purpose Overly liberal repayment program Nonexistent, weak or waived covenants Inadequate debt-service coverage Repayment or coverage based on speculative values

31 Drivers of Credit Risk Structural Weakness continued Inadequate financial analysis Inadequate collateral Lack of guarantor

32 Case Study #2 Contractor commercial roofing Bank customer 1.5 years Bank had renewed and increased the line three months earlier using the 2014 numbers.

33 Case Study # Sales $3,002 $3,582 $3,231 $2,313 Net Profit ($48) ($143) $202 $25 Traditional cash flow measures for 2013 and 2014 were satisfactory.

34 Case Study # AR $1,187 $1,528 $1,127 $1,330 AP $ 357 $ 671 $ 330 $ 319 Line $ 711 $1,000 $ 788 $ 963 AR Turn Debt/Worth Cash flow after ($192) ($166) ($3) ($259) debt service (UCA) Loan officer indicated in loan presentation that the 210 day AR turn was a timing issue and not management issue.

35 Case Study #2 12/31/14 Borrowing Base Accts Receivable $1,330M Less over 90 days (25) Net Eligible $1,305M x 80% = $1,044M Line Excess Availability $ 963M $ 81M

36 Case Study #2 +Traditional cash flow is positive. +Leverage is high, but they have positive equity and appear to be able to weather some ups and downs. -The receivable turn is increasing. -The Bank increased the line. -Borrowing base appears to have errors -UCA cash flow is negative.

37 Case Study #2 Result: Fraud borrower made up a lot of receivables and/or did not properly age them. Bank lost about $400M.

38 Credit Risk Identification: What we hear Their family has banked here for years I drive by the business/project all the time It is a timing issue They have a great backlog This is the premier manufacturer of widgets in the county They are well respected in the community

39 Credit Risk Identification: What we hear They can live on $10,000 per year If they don t pay, their parents will We have plenty of collateral We have a strong guarantor The examiners didn t downgrade it They have always paid as agreed!

40 Risk Identification Why is early identification critical? Knowledge is power First in line It has an impact on your institution s capital Early recognition reflects well on you Not recognizing the issues often makes the outcome worse

41 Early Warning Signs of Problems Decline in sales Weakness in traditional cash flow Strain on working capital Line usage Accounts receivable turnover High leverage Credit scores

42 Cash flow is short how is the loan being paid? Working capital management Unpaid real estate or payroll taxes Collecting receivables faster Stretching payments to the trade Increasing your line usage Decreasing cash / Overdrafts Equity or other source of cash injection

43 Early Warning Signs Working Capital Shortfall after Debt Service $0 ($100) ($175)

44 Early Warning Signs Working Capital Shortfall after Debt Service $0 ($100) ($175) Working Capital $220 $125 ($175)

45 Early Warning Signs Working Capital Shortfall after Debt Service $0 ($100) ($175) Receivables $1,000 $800 $600 Inventory $700 $750 $500 Current Assets $1,700 $1,550 $1,100 ====== ====== ====== Bank Line $1,130 $1,100 $975 Payables $350 $325 $300 Current Liabilities $1,480 $1,425 $1,275 ====== ====== ====== Working Capital $220 $125 ($175)

46 Early Warning Signs Working Capital Shortfall after Debt Service $0 ($100) ($175) Receivables $1,000 $800 $600 Inventory $700 $750 $500 Current Assets $1,700 $1,550 $1,100 ====== ====== ====== Bank Line $1,130 $1,100 $975 Payables $350 $325 $300 Current Liabilities $1,480 $1,425 $1,275 ====== ====== ====== Working Capital $220 $125 ($175) Cash Freed Up $95 $300

47 Early Warning Signs Working Capital Shortfall after Debt Service $0 ($100) ($175) Receivables $1,000 $800 $600 Inventory $700 $750 $500 Current Assets $1,700 $1,550 $1,100 ====== ====== ====== Bank Line $1,130 $1,100 $975 Payables $350 $325 $300 Current Liabilities $1,480 $1,425 $1,275 ====== ====== ====== Working Capital $220 $125 ($175) Cash Freed Up $95 $300 Bank Debt/(AR + Inventory) 66.5% 71.0% 88.6%

48 Case Study #3 Existing bank customer with $550,000 of exposure, graded OAEM. Payments are always timely 12/31/11 12/31/12 Net profit $52M $54M Debt coverage ratio Net Worth ($201M) ($174M) 4 Working capital ($200M) ($379M) AR + Inventory total $690M $670M Bank line, overdraft and accounts payable total $890M $1,049

49 Case Study #3 How did they make payments? Reduced AR & inventory by $20M while increasing associated debt to bank & trade by $159M This created funds of $179M to borrower In July 2013, borrower requested a short term $150M increase in their line to be repaid in October Bank granted this request using 12/31/12 financial statement After the loan was granted, Bank obtained 6 month July 2013 financial statement showing a $200M loss 4 This is a contractor & receivables offer little value at liquidation Bank lost $250M

50 Credit Administration Operational Risk Financial statement exceptions and monitoring Loan operations Loans booked as approved Non-accrual tracking Collateral documents

51 Credit Administration Operational Risk Construction loan disbursements Equity in the project Equity up front Lending against stored or ordered materials Quality of fixtures, trim, etc. on homes being completed today Landscaping All funds advanced with work still to be completed

52 Credit Administration Operational Risk Borrowing bases Floor plan lending

53 Example: Food Processor/Distributor FYE 1 FYE 2 FYE 3 FY 4-8 mos Sales $8,950 $7,200 $6,500 $2,700 Profit $ 101 $ 4 ($ 346) ($ 525) Equity $ 903 $ 922 $ 542 $ 17 Debt/Equity Working Capital $ 270 ($ 240) ($1,105) ($1,280) Cash Freed Up $ 510 $ 865 $ (Change in WC)

54 Example: Food Processor/Distributor FYE 1 FYE 2 FYE 3 FY 4-8 mos Bank Line $1,175 $1,497 $2,230 $2,260 Bank Line/ (AR + Inv.) 55% 73% 110% 121% (Line + AP)/ (AR + Inv.) 75% 105% 153% 156% 54

55 Summary Growth creates risk and the current environment is causing a shift in many institutions approach to growth Look closely at some of the new loan growth and the risk. The actions you take today are the foundation of how your institution will fare in the next economic downturn Importance of objectively looking at your practices and the risks created

56 PRESENTERS Please call anytime with questions. John Bourquard Ryan Swope Principal Director BKD, LLP BKD, LLP Loan Review Services Loan Review Services

Director s Guide to Credit

Federal Reserve Bank of Atlanta Director s Guide to Credit This guide was created by the Supervision and Regulation Division of the Federal Reserve Bank of Atlanta, 1000 Peachtree Street NE, Atlanta,

Federal Reserve Bank of Atlanta Director s Guide to Credit This guide was created by the Supervision and Regulation Division of the Federal Reserve Bank of Atlanta, 1000 Peachtree Street NE, Atlanta,

Federal Reserve Bank of Atlanta. Components of a Sound Credit Risk Management Program

Federal Reserve Bank of Atlanta Components of a Sound Credit Risk Management Program LOAN POLICY The loan policy is the foundation for maintaining sound asset quality because it outlines the organization

Federal Reserve Bank of Atlanta Components of a Sound Credit Risk Management Program LOAN POLICY The loan policy is the foundation for maintaining sound asset quality because it outlines the organization

Analyzing Cash Flows. April 2013

Analyzing Cash Flows April 2013 Overview Introductions Importance of cash flow in underwriting decisions Key attributes to calculating cash flow Where to obtain information to calculate cash flows Considerations

Analyzing Cash Flows April 2013 Overview Introductions Importance of cash flow in underwriting decisions Key attributes to calculating cash flow Where to obtain information to calculate cash flows Considerations

3. Seasonal or cyclical working capital to finance the temporary cash shortfalls due to the nature of the firm s normal business cycle.

11.437 Financing Community Economic Development Class 5: Working Capital Financing I. Three different meanings of term working capital 1. Excess of current assets over current liabilities 2. Firm's investment

11.437 Financing Community Economic Development Class 5: Working Capital Financing I. Three different meanings of term working capital 1. Excess of current assets over current liabilities 2. Firm's investment

Tabletop Exercises: Allowance for Loan and Lease Losses and Troubled Debt Restructurings

Tabletop Exercises: Allowance for Loan and Lease Losses and Troubled Debt Restructurings Index Measuring Impairment Example 1: Present Value of Expected Future Cash Flows Method (Unsecured Loan)... - 1

Tabletop Exercises: Allowance for Loan and Lease Losses and Troubled Debt Restructurings Index Measuring Impairment Example 1: Present Value of Expected Future Cash Flows Method (Unsecured Loan)... - 1

5 Ways of Financing Your Growth

5 Ways of Financing Your Growth Kwesi Rogers President & CEO Federal National Commercial Credit In this whitepaper, you will learn five ways of financing your growth. It will show the opportunity and challenges

5 Ways of Financing Your Growth Kwesi Rogers President & CEO Federal National Commercial Credit In this whitepaper, you will learn five ways of financing your growth. It will show the opportunity and challenges

NOTE ON LOAN CAPITAL MARKETS

The structure and use of loan products Most businesses use one or more loan products. A company may have a syndicated loan, backstop, line of credit, standby letter of credit, bridge loan, mortgage, or

The structure and use of loan products Most businesses use one or more loan products. A company may have a syndicated loan, backstop, line of credit, standby letter of credit, bridge loan, mortgage, or

SAMPLE AUDIT REPORT. Sample Credit Union. Report on Operations. As of Audit Date

Sample Credit Union Report on Operations As of Audit Date GENERAL OVERVIEW Overall, the Credit Union appeared to be well managed and continuing to maintain its financial stability. During the twelve months

Sample Credit Union Report on Operations As of Audit Date GENERAL OVERVIEW Overall, the Credit Union appeared to be well managed and continuing to maintain its financial stability. During the twelve months

2013 Survey of Credit Underwriting Practices

2013 Survey of Credit Underwriting Practices Office of the Comptroller of the Currency Washington, D.C. January 2014 Contents Introduction... 1 Part I: Overall Results... 3 Primary Findings... 3 Commentary

2013 Survey of Credit Underwriting Practices Office of the Comptroller of the Currency Washington, D.C. January 2014 Contents Introduction... 1 Part I: Overall Results... 3 Primary Findings... 3 Commentary

Commercial and Industrial Lending

Commercial and Industrial Lending A CPA Perspective April 2014 Overview Introductions and Goals of Presentation Commercial and Industrial Lending: Brief Background Covenants, Advance Rates, and Borrowing

Commercial and Industrial Lending A CPA Perspective April 2014 Overview Introductions and Goals of Presentation Commercial and Industrial Lending: Brief Background Covenants, Advance Rates, and Borrowing

Credit Risk Management. Debunking Myths and Misinformation

Credit Risk Management Debunking Myths and Misinformation Key Topics Impairment vs. Nonaccrual Collateral Dependent Loans Troubled Debt Restructures Concession Criteria Classification, Nonaccrual Quick

Credit Risk Management Debunking Myths and Misinformation Key Topics Impairment vs. Nonaccrual Collateral Dependent Loans Troubled Debt Restructures Concession Criteria Classification, Nonaccrual Quick

2014 Survey of Credit Underwriting Practices

2014 Survey of Credit Underwriting Practices Office of the Comptroller of the Currency Washington, D.C. December 2014 Contents Introduction... 1 Part I: Overall Results... 3 Primary Findings... 3 Commentary

2014 Survey of Credit Underwriting Practices Office of the Comptroller of the Currency Washington, D.C. December 2014 Contents Introduction... 1 Part I: Overall Results... 3 Primary Findings... 3 Commentary

Commercial Loan Pricing Variables for Consideration

Commercial Loan Pricing Variables for Consideration OFN Small Business Finance Forum June 18, 2012 HOPE Colorado Enterprise Fund Commercial Loan Pricing Variables for Consideration HOPE The Primary Driver

Commercial Loan Pricing Variables for Consideration OFN Small Business Finance Forum June 18, 2012 HOPE Colorado Enterprise Fund Commercial Loan Pricing Variables for Consideration HOPE The Primary Driver

SUPERVISION GUIDELINE

SUPERVISION GUIDELINE G6: GUIDELINES FOR LOAN CLASSIFICATION AND PROVISIONING FOR IMPAIRED ASSETS Issued To All Licensed Financial Institutions AUTHORITY Section 316 (4) of the International Business Corporations

SUPERVISION GUIDELINE G6: GUIDELINES FOR LOAN CLASSIFICATION AND PROVISIONING FOR IMPAIRED ASSETS Issued To All Licensed Financial Institutions AUTHORITY Section 316 (4) of the International Business Corporations

Table 2. 2.56 spreads=eased) Premiums charged on riskier loans 2.35 Loan covenants 2.72 Collateralization requirements 2.89 Other 2.

Premiums charged on riskier loans 2.35 Loan covenants 2.72 Collateralization requirements 2.89 Other 2.") Table 2 SENIOR LOAN OFFICER OPINION SURVEY ON BANK LENDING PRACTICES AT SELECTED BRANCHES AND AGENCIES OF FOREIGN BANKS IN THE UNITED STATES 1 (Status of policy as of April 2003) Questions 1-5 ask about

Table 2 SENIOR LOAN OFFICER OPINION SURVEY ON BANK LENDING PRACTICES AT SELECTED BRANCHES AND AGENCIES OF FOREIGN BANKS IN THE UNITED STATES 1 (Status of policy as of April 2003) Questions 1-5 ask about

Guide to Financial Ratios Analysis A Step by Step Guide to Balance Sheet and Profit and Loss Statement Analysis

Guide to Financial Ratios Analysis A Step by Step Guide to Balance Sheet and Profit and Loss Statement Analysis By BizMove Management Training Institute Other free books by BizMove that may interest you:

Guide to Financial Ratios Analysis A Step by Step Guide to Balance Sheet and Profit and Loss Statement Analysis By BizMove Management Training Institute Other free books by BizMove that may interest you:

MEMBER BUSINESS LOAN GUIDANCE

MEMBER BUSINESS LOAN GUIDANCE The following guidance was drafted based on information in NCUA s Member Business Loans Regulation as detailed in Part 723, and other applicable laws and regulations. It is

MEMBER BUSINESS LOAN GUIDANCE The following guidance was drafted based on information in NCUA s Member Business Loans Regulation as detailed in Part 723, and other applicable laws and regulations. It is

2015 Survey of Credit Underwriting Practices

2015 Survey of Credit Underwriting Practices Office of the Comptroller of the Currency Washington, D.C. December 2015 Contents Introduction... 1 Part I: Overall Results... 3 Primary Findings... 3 Commentary

2015 Survey of Credit Underwriting Practices Office of the Comptroller of the Currency Washington, D.C. December 2015 Contents Introduction... 1 Part I: Overall Results... 3 Primary Findings... 3 Commentary

The State of the Corporate Banking Industry 2008 2009 Banking Industry Crisis Andrew Cardimen, Senior Vice President Middle Market Corporate Banking Harris Bank, N.A. 1 The 2008 2009 Credit Crisis 2 ~8,300

The State of the Corporate Banking Industry 2008 2009 Banking Industry Crisis Andrew Cardimen, Senior Vice President Middle Market Corporate Banking Harris Bank, N.A. 1 The 2008 2009 Credit Crisis 2 ~8,300

Federal Reserve Bank of Atlanta. A Guide for Specialized Credit Activities

Federal Reserve Bank of Atlanta A Guide for Specialized Credit Activities CONSUMER LENDING According to the Federal Reserve Board of Governors, seasonally adjusted consumer credit outstanding including

Federal Reserve Bank of Atlanta A Guide for Specialized Credit Activities CONSUMER LENDING According to the Federal Reserve Board of Governors, seasonally adjusted consumer credit outstanding including

SMALL BUSINESS DEVELOPMENT CENTER RM. 032

SMALL BUSINESS DEVELOPMENT CENTER RM. 032 FINANCING THROUGH COMMERCIAL BANKS Revised January, 2013 Adapted from: National Federation of Independent Business report Steps to Small Business Financing Jeffrey

SMALL BUSINESS DEVELOPMENT CENTER RM. 032 FINANCING THROUGH COMMERCIAL BANKS Revised January, 2013 Adapted from: National Federation of Independent Business report Steps to Small Business Financing Jeffrey

Financial Ratio Analysis A GUIDE TO USEFUL RATIOS FOR UNDERSTANDING YOUR SOCIAL ENTERPRISE S FINANCIAL PERFORMANCE

Financial Ratio Analysis A GUIDE TO USEFUL RATIOS FOR UNDERSTANDING YOUR SOCIAL ENTERPRISE S FINANCIAL PERFORMANCE December 2013 Acknowledgments This guide and supporting tools were developed by Julie

Financial Ratio Analysis A GUIDE TO USEFUL RATIOS FOR UNDERSTANDING YOUR SOCIAL ENTERPRISE S FINANCIAL PERFORMANCE December 2013 Acknowledgments This guide and supporting tools were developed by Julie

A. Eligibility Requirements for a Loan Modification & Troubled Debt Restructure (TDRs)

") POLICY: L127 This policy governs any changes in original terms, on consumer and business loans including but not limited to real estate loans, that were agreed to at loan approval. Loan modifications and

POLICY: L127 This policy governs any changes in original terms, on consumer and business loans including but not limited to real estate loans, that were agreed to at loan approval. Loan modifications and

So You Want to Borrow Money to Start a Business?

So You Want to Borrow Money to Start a Business? M any small business owners cannot understand why a lending institution would refuse to lend them money. Others have no trouble getting money, but they

So You Want to Borrow Money to Start a Business? M any small business owners cannot understand why a lending institution would refuse to lend them money. Others have no trouble getting money, but they

TEXTRON FINANCIAL CORPORATION

TEXTRON FINANCIAL CORPORATION Quarterly Financial Statements (Unaudited) For the fiscal quarter ended Textron Financial Corporation is a wholly-owned subsidiary of Textron Inc. Beginning with the quarter

TEXTRON FINANCIAL CORPORATION Quarterly Financial Statements (Unaudited) For the fiscal quarter ended Textron Financial Corporation is a wholly-owned subsidiary of Textron Inc. Beginning with the quarter

STANDARDS OF SOUND BUSINESS AND FINANCIAL PRACTICES

STANDARDS OF SOUND BUSINESS AND FINANCIAL PRACTICES DICO BY-LAW No. 5 Assessment Workbook Module: Commercial Lending February 2005 3. Credit Risk Management: Commercial Lending It is a sound business and

STANDARDS OF SOUND BUSINESS AND FINANCIAL PRACTICES DICO BY-LAW No. 5 Assessment Workbook Module: Commercial Lending February 2005 3. Credit Risk Management: Commercial Lending It is a sound business and

Key Points to Borrowing Money

Key Points to Borrowing Money Borrowing money is one of the most common sources of funding for a small business, but obtaining a loan isn't always easy. Before you approach your banker for a loan, it is

Key Points to Borrowing Money Borrowing money is one of the most common sources of funding for a small business, but obtaining a loan isn't always easy. Before you approach your banker for a loan, it is

Assessing Credit Risk

Assessing Credit Risk Objectives Discuss the following: Inherent Risk Quality of Risk Management Residual or Composite Risk Risk Trend 2 Inherent Risk Define the risk Identify sources of risk Quantify

Assessing Credit Risk Objectives Discuss the following: Inherent Risk Quality of Risk Management Residual or Composite Risk Risk Trend 2 Inherent Risk Define the risk Identify sources of risk Quantify

MBL 2700 Business Loan Collection

MBL 2700 Business Loan Collection Effective: September 2011 Departments Impacted List areas of the Credit Union (departments/branches) affected by the procedure. Introduction The Introduction section contains

MBL 2700 Business Loan Collection Effective: September 2011 Departments Impacted List areas of the Credit Union (departments/branches) affected by the procedure. Introduction The Introduction section contains

Policy Statement on Prudent Commercial Real Estate Loan Workouts (October 30, 2009)

") Policy Statement on Prudent Commercial Real Estate Loan Workouts (October 30, 2009) The financial regulators 1 recognize that financial institutions face significant challenges when working with commercial

Policy Statement on Prudent Commercial Real Estate Loan Workouts (October 30, 2009) The financial regulators 1 recognize that financial institutions face significant challenges when working with commercial

Policy Statement on Prudent Commercial Real Estate Loan Workouts

Policy Statement on Prudent Commercial Real Estate Loan Workouts The financial regulators 1 recognize that financial institutions face significant challenges when working with commercial real estate (CRE)

Policy Statement on Prudent Commercial Real Estate Loan Workouts The financial regulators 1 recognize that financial institutions face significant challenges when working with commercial real estate (CRE)

Financial Statement Ratio Analysis

Management Accounting 319 Financial Statement Ratio Analysis Financial statements as prepared by the accountant are documents containing much valuable information. Some of the information requires little

Management Accounting 319 Financial Statement Ratio Analysis Financial statements as prepared by the accountant are documents containing much valuable information. Some of the information requires little

United Federal Credit Union. Consolidated Financial Report with Additional Information December 31, 2014

Consolidated Financial Report with Additional Information December 31, 2014 Contents Report Letter 1-2 Consolidated Financial Statements Statement of Financial Condition 3 Statement of Income 4 Statement

Consolidated Financial Report with Additional Information December 31, 2014 Contents Report Letter 1-2 Consolidated Financial Statements Statement of Financial Condition 3 Statement of Income 4 Statement

How Bankers Think. Build a sound financial base to support your company for future growth

How Bankers Think Build a sound financial base to support your company for future growth Presented by: Lisa Chapman Business Planning, Social Media Marketing & SEO 615-477-8412 Questions to Consider First

How Bankers Think Build a sound financial base to support your company for future growth Presented by: Lisa Chapman Business Planning, Social Media Marketing & SEO 615-477-8412 Questions to Consider First

Partners for the Common Good Financial Statements December 31, 2014 and 2013

Partners for the Common Good Financial Statements December 31, 2014 and 2013 TABLE OF CONTENTS Page Independent Auditors' Report 1-2 Financial Statements: Statements of Financial Position 3 Statements

Partners for the Common Good Financial Statements December 31, 2014 and 2013 TABLE OF CONTENTS Page Independent Auditors' Report 1-2 Financial Statements: Statements of Financial Position 3 Statements

Vincent H. Vieten, MBL PO Office of Examination and Insurance MBL. CUNA Lending Council Conference Fort Lauderdale, FL November 9, 2015

Vincent H. Vieten, MBL PO Office of Examination and Insurance MBL CUNA Lending Council Conference Fort Lauderdale, FL November 9, 2015 Credit unions continue to post strong loan growth in first half of

Vincent H. Vieten, MBL PO Office of Examination and Insurance MBL CUNA Lending Council Conference Fort Lauderdale, FL November 9, 2015 Credit unions continue to post strong loan growth in first half of

How Do I Qualify for a loan?

How Do I Qualify for a loan? Borrowing money is one of the most common sources of funding for a small business, but obtaining a loan isn't always easy. Before you approach your banker for a loan, it is

How Do I Qualify for a loan? Borrowing money is one of the most common sources of funding for a small business, but obtaining a loan isn't always easy. Before you approach your banker for a loan, it is

SMALL BUSINESS QUARTERLY PULSE CHECK

SMALL BUSINESS QUARTERLY PULSE CHECK To make your business #CPAPOWERED, call today and let s get started. 16733-312_CPAPowered_Quarterly Pulse_Check Checklist_final.indd 1 Sound planning is one of the

SMALL BUSINESS QUARTERLY PULSE CHECK To make your business #CPAPOWERED, call today and let s get started. 16733-312_CPAPowered_Quarterly Pulse_Check Checklist_final.indd 1 Sound planning is one of the

CR CREDIT RISK. 58 April 2013 The RMA Journal Copyright 2013 by RMA

CR CREDIT RISK Let Us Count the Ways 58 April 2013 The RMA Journal Copyright 2013 by RMA ONLY CASH PAYS LOANS ys to Measure Cash Flow This first article in a two-part series discusses the four most widely

CR CREDIT RISK Let Us Count the Ways 58 April 2013 The RMA Journal Copyright 2013 by RMA ONLY CASH PAYS LOANS ys to Measure Cash Flow This first article in a two-part series discusses the four most widely

Risk Rating Systems for Small Business Community Development Financial Institutions (CDFIs)

") Risk Rating Systems for Small Business Community Development Financial Institutions (CDFIs) By Donna Nails May 2012 Donna Nails and Opportunity Finance Network wish to thank Clint Gwin of Pathway Lending,

Risk Rating Systems for Small Business Community Development Financial Institutions (CDFIs) By Donna Nails May 2012 Donna Nails and Opportunity Finance Network wish to thank Clint Gwin of Pathway Lending,

Business Lending: Lessons Learned and Effective Risk Management

Presenting Business Lending: Lessons Learned and Effective Risk Management Ryan Sturgis, Senior Manager Moss Adams LLP 503.478.2280 ryan.sturgis@mossadams.com Moss Adams Financial Institutions Practice

Presenting Business Lending: Lessons Learned and Effective Risk Management Ryan Sturgis, Senior Manager Moss Adams LLP 503.478.2280 ryan.sturgis@mossadams.com Moss Adams Financial Institutions Practice

2012 Survey of Credit Underwriting Practices

2012 Survey of Credit Underwriting Practices Office of the Comptroller of the Currency Washington, D.C. June 2012 Contents Introduction... 1 Part I: Overall Results... 3 Primary Findings... 3 Commentary

2012 Survey of Credit Underwriting Practices Office of the Comptroller of the Currency Washington, D.C. June 2012 Contents Introduction... 1 Part I: Overall Results... 3 Primary Findings... 3 Commentary

HOME BUYING101. 701.255.0042 www.capcu.org i

HOME BUYING101 701.255.0042 www.capcu.org i This book is intended as a general guide to the topics discussed, and it does not deliver accounting, personal finance, or legal advice. It is not intended,

HOME BUYING101 701.255.0042 www.capcu.org i This book is intended as a general guide to the topics discussed, and it does not deliver accounting, personal finance, or legal advice. It is not intended,

Use this section to learn more about business loans and specific financial products that might be right for your company.

Types of Financing Use this section to learn more about business loans and specific financial products that might be right for your company. Revolving Line Of Credit Revolving lines of credit are the most

Types of Financing Use this section to learn more about business loans and specific financial products that might be right for your company. Revolving Line Of Credit Revolving lines of credit are the most

Policy Statement on Prudent Commercial Real Estate Loan Workouts I. Purpose

Policy Statement on Prudent Commercial Real Estate Loan Workouts (October 30, 2009) The financial regulators 1 [Footnote 1. The financial regulators consist of the Board of Governors of the Federal Reserve

Policy Statement on Prudent Commercial Real Estate Loan Workouts (October 30, 2009) The financial regulators 1 [Footnote 1. The financial regulators consist of the Board of Governors of the Federal Reserve

Cooperative Housing/ Share Loan Financing. Larry Mathe Chris Goettke National Cooperative Bank

Cooperative Housing/ Share Loan Financing Larry Mathe Chris Goettke National Cooperative Bank The NCB Story NCB delivers banking and financial services to cooperative organizations complemented by a special

Cooperative Housing/ Share Loan Financing Larry Mathe Chris Goettke National Cooperative Bank The NCB Story NCB delivers banking and financial services to cooperative organizations complemented by a special

NORTH ISLAND CREDIT UNION

NORTH ISLAND CREDIT UNION Policy Section: Business Services Policy Name: Member Business Lending Policy No: 500-05-01 Board Review & Approval: July 21, 2014 Effective Date: July 22, 2014 POLICY STATEMENT

NORTH ISLAND CREDIT UNION Policy Section: Business Services Policy Name: Member Business Lending Policy No: 500-05-01 Board Review & Approval: July 21, 2014 Effective Date: July 22, 2014 POLICY STATEMENT

Commercial Paper Conduritization Program

VII COMMERCIAL PAPER BACKED BY CREDIT CARD RECEIVABLES INTRODUCTION Asset-backed commercial paper (ABCP) conduits issue short-term notes backed by trade receivables, credit card receivables, or medium-term

VII COMMERCIAL PAPER BACKED BY CREDIT CARD RECEIVABLES INTRODUCTION Asset-backed commercial paper (ABCP) conduits issue short-term notes backed by trade receivables, credit card receivables, or medium-term

Share Loan and Underlying Mortgage Financing. Jeremy Morgan, NCB Larry Mathe, NCB

Share Loan and Underlying Mortgage Financing Jeremy Morgan, NCB Larry Mathe, NCB About NCB NCB is the premier lender to housing cooperatives nationwide. NCB has financed over $6 Billion to housing cooperatives

Share Loan and Underlying Mortgage Financing Jeremy Morgan, NCB Larry Mathe, NCB About NCB NCB is the premier lender to housing cooperatives nationwide. NCB has financed over $6 Billion to housing cooperatives

Riverside County s Credit Union LOAN POLICY Revised 11/22//99 ==================================================================== INTRODUCTION

INTRODUCTION Riverside County s Credit Union (RCCU) considers the making of loans to members to be the most important element of our operation. In order to protect the credit union s asset quality, emphasis

INTRODUCTION Riverside County s Credit Union (RCCU) considers the making of loans to members to be the most important element of our operation. In order to protect the credit union s asset quality, emphasis

Understanding Financial Statements. For Your Business

Understanding Financial Statements For Your Business Disclaimer The information provided is for informational purposes only, does not constitute legal advice or create an attorney-client relationship,

Understanding Financial Statements For Your Business Disclaimer The information provided is for informational purposes only, does not constitute legal advice or create an attorney-client relationship,

BY RICHARD FARLEY & URSULA MACKEY. I. Background. 2014 Supplement

November 2014 Follow @Paul_Hastings Interagency Guidance on Leveraged Lending (March 2013) A Summary of the 2014 Interagency Shared National Credit Review and Answers to the Most Frequently Asked Questions

November 2014 Follow @Paul_Hastings Interagency Guidance on Leveraged Lending (March 2013) A Summary of the 2014 Interagency Shared National Credit Review and Answers to the Most Frequently Asked Questions

Appraisal A written analysis prepared by a qualified appraiser and estimating the value of a property

REAL ESTATE BASICS Affordability Analysis An analysis of a buyer s ability to afford the purchase of a home, reviews income, liabilities, and available funds, and considers the type of mortgage a buyer

REAL ESTATE BASICS Affordability Analysis An analysis of a buyer s ability to afford the purchase of a home, reviews income, liabilities, and available funds, and considers the type of mortgage a buyer

Calculating financial position and cash flow indicators

Calculating financial position and cash flow indicators Introduction When a business is deciding whether to grant credit to a potential customer, or whether to continue to grant credit terms to an existing

Calculating financial position and cash flow indicators Introduction When a business is deciding whether to grant credit to a potential customer, or whether to continue to grant credit terms to an existing

DEPARTMENT OF LABOR, LICENSING AND REGULATION SUBTITLE 03 - Commissioner of Financial Regulation. Chapter: 09.03.

DEPARTMENT OF LABOR, LICENSING AND REGULATION SUBTITLE 03 - Commissioner of Financial Regulation Chapter: 09.03.01 - Credit Unions Authority: Financial Institutions Article, 2-105.1, Annotated Code of

DEPARTMENT OF LABOR, LICENSING AND REGULATION SUBTITLE 03 - Commissioner of Financial Regulation Chapter: 09.03.01 - Credit Unions Authority: Financial Institutions Article, 2-105.1, Annotated Code of

Overview of Financial Solutions

Overview of Financial Solutions The Etra Advisory Group provides solutions to businesses for growth, expansion, cash flow, refinance and acquisition. We cover the world of business financing that banks

Overview of Financial Solutions The Etra Advisory Group provides solutions to businesses for growth, expansion, cash flow, refinance and acquisition. We cover the world of business financing that banks

Senior Executive Vice President and Chief Financial Officer 973-305-4003

News Release FOR IMMEDIATE RELEASE Contact: Alan D. Eskow Senior Executive Vice President and Chief Financial Officer 973-305-4003 VALLEY NATIONAL BANCORP REPORTS FIRST QUARTER EARNINGS, SOLID ASSET QUALITY

News Release FOR IMMEDIATE RELEASE Contact: Alan D. Eskow Senior Executive Vice President and Chief Financial Officer 973-305-4003 VALLEY NATIONAL BANCORP REPORTS FIRST QUARTER EARNINGS, SOLID ASSET QUALITY

Module 6 Understanding Lending Decisions Module Outline

Module 6 Understanding Lending Decisions Module Outline Introduction The Five C s of Credit Roadside Chat #1 1. Character Adapting to Change Management Ability Commitment to Loan Repayment Sound Production

Module 6 Understanding Lending Decisions Module Outline Introduction The Five C s of Credit Roadside Chat #1 1. Character Adapting to Change Management Ability Commitment to Loan Repayment Sound Production

FDIC Atlanta Region Regulatory Conference Call Commercial & Industrial Lending April 12, 2012

FDIC Atlanta Region Regulatory Conference Call Commercial & Industrial Lending April 12, 2012 1 Commercial & Industrial (C&I) Lending In the wake of the real estate market collapse, many banks are looking

FDIC Atlanta Region Regulatory Conference Call Commercial & Industrial Lending April 12, 2012 1 Commercial & Industrial (C&I) Lending In the wake of the real estate market collapse, many banks are looking

Graduate School of Colorado SBA lending Presentation

Graduate School of Colorado SBA lending Presentation SBA lending course summary The course will provide an overview and comparison of SBA 7a, SBA 504 and USDA Business & Industry (B&I) loan programs. SBA

Graduate School of Colorado SBA lending Presentation SBA lending course summary The course will provide an overview and comparison of SBA 7a, SBA 504 and USDA Business & Industry (B&I) loan programs. SBA

From PLI s Course Handbook Private Equity Acquisition Financing Summit 2006 #10725. Get 40% off this title right now by clicking here.

From PLI s Course Handbook Private Equity Acquisition Financing Summit 2006 #10725 Get 40% off this title right now by clicking here. 2 ASSET-BASED FINANCINGS FOR ACQUISITIONS COUNTING ON YOUR ASSETS Seth

From PLI s Course Handbook Private Equity Acquisition Financing Summit 2006 #10725 Get 40% off this title right now by clicking here. 2 ASSET-BASED FINANCINGS FOR ACQUISITIONS COUNTING ON YOUR ASSETS Seth

THE ABC S OF BORROWING

THE ABC S OF BORROWING All businesses, no matter what size, need to raise money at some time. Small business owners may be able to dip into their personal savings or borrow money from friends. More likely,

THE ABC S OF BORROWING All businesses, no matter what size, need to raise money at some time. Small business owners may be able to dip into their personal savings or borrow money from friends. More likely,

Proposed Definitions of Higher-Risk Consumer and C&I Loans and Securities under FDIC Large Bank Pricing

Proposed Definitions of Higher-Risk Consumer and C&I Loans and Securities under FDIC Large Bank Pricing On March 20, the FDIC Board proposed for public comment revised definitions of subprime consumer

Proposed Definitions of Higher-Risk Consumer and C&I Loans and Securities under FDIC Large Bank Pricing On March 20, the FDIC Board proposed for public comment revised definitions of subprime consumer

HOME BUYING101 TM %*'9 [[[ EPXEREJGY SVK i

HOME BUYING101 TM i This book is intended as a general guide to the topics discussed, and it does not deliver accounting, personal finance, or legal advice. It is not intended, and should not be used,

HOME BUYING101 TM i This book is intended as a general guide to the topics discussed, and it does not deliver accounting, personal finance, or legal advice. It is not intended, and should not be used,

Module 1: Corporate Finance and the Role of Venture Capital Financing TABLE OF CONTENTS

1.0 ALTERNATIVE SOURCES OF FINANCE Module 1: Corporate Finance and the Role of Venture Capital Financing Alternative Sources of Finance TABLE OF CONTENTS 1.1 Short-Term Debt (Short-Term Loans, Line of

1.0 ALTERNATIVE SOURCES OF FINANCE Module 1: Corporate Finance and the Role of Venture Capital Financing Alternative Sources of Finance TABLE OF CONTENTS 1.1 Short-Term Debt (Short-Term Loans, Line of

W i n t r u s t B a n k

W i n t r u s t B a n k 1 WHO ARE WE Wintrust Financial is a financial services holding company We provide traditional community banking services, commercial banking, wealth management, commercial insurance

W i n t r u s t B a n k 1 WHO ARE WE Wintrust Financial is a financial services holding company We provide traditional community banking services, commercial banking, wealth management, commercial insurance

UNIVERSITY OF WISCONSIN CREDIT UNION. CONSOLIDATED FINANCIAL STATEMENTS December 31, 2014 and 2013

CONSOLIDATED FINANCIAL STATEMENTS Madison, Wisconsin CONSOLIDATED FINANCIAL STATEMENTS CONTENTS INDEPENDENT AUDITOR S REPORT... 1 CONSOLIDATED FINANCIAL STATEMENTS CONSOLIDATED STATEMENTS OF FINANCIAL

CONSOLIDATED FINANCIAL STATEMENTS Madison, Wisconsin CONSOLIDATED FINANCIAL STATEMENTS CONTENTS INDEPENDENT AUDITOR S REPORT... 1 CONSOLIDATED FINANCIAL STATEMENTS CONSOLIDATED STATEMENTS OF FINANCIAL

Responses to Online Questions from the Web and Telephone Seminar

Small Business Administration (SBA) Lending Programs and the American Recovery and Reinvestment Act of 2009 A Web and Telephone Seminar (Hosted by the Office of the Comptroller of the Currency (OCC)) September

Small Business Administration (SBA) Lending Programs and the American Recovery and Reinvestment Act of 2009 A Web and Telephone Seminar (Hosted by the Office of the Comptroller of the Currency (OCC)) September

Sample Risk Rating Model

Commercial Loan Best Practices Risk Rating Sample Risk Rating Model Spring 2005 Sample Risk Rating Model Introduction Risk rating involves the categorization of individual credit facilities based on credit

Commercial Loan Best Practices Risk Rating Sample Risk Rating Model Spring 2005 Sample Risk Rating Model Introduction Risk rating involves the categorization of individual credit facilities based on credit

The Accessing Capital Workshop

The Accessing Capital Workshop Small Business Capital Access Strategies Toll-free: (800) 381-0073 Online: www.ar2credit.com 2009 Covenant Capital Corporation. All Rights Reserved. NET30 Advisors Who We

The Accessing Capital Workshop Small Business Capital Access Strategies Toll-free: (800) 381-0073 Online: www.ar2credit.com 2009 Covenant Capital Corporation. All Rights Reserved. NET30 Advisors Who We

GrowFL and SunTrust Bank Present: Business Acquisitions and Partner Buyouts How SBA Loans can be leveraged to help

GrowFL and SunTrust Bank Present: Business Acquisitions and Partner Buyouts How SBA Loans can be leveraged to help GrowFL Webinar Series Date: September 4, 2012 Presented by: Hetal Engineer, SunTrust VP

GrowFL and SunTrust Bank Present: Business Acquisitions and Partner Buyouts How SBA Loans can be leveraged to help GrowFL Webinar Series Date: September 4, 2012 Presented by: Hetal Engineer, SunTrust VP

FEDERAL HOUSING FINANCE AGENCY

FEDERAL HOUSING FINANCE AGENCY ADVISORY BULLETIN AB 2012-02 FRAMEWORK FOR ADVERSELY CLASSIFYING LOANS, OTHER REAL ESTATE OWNED, AND OTHER ASSETS AND LISTING ASSETS FOR SPECIAL MENTION Introduction This

FEDERAL HOUSING FINANCE AGENCY ADVISORY BULLETIN AB 2012-02 FRAMEWORK FOR ADVERSELY CLASSIFYING LOANS, OTHER REAL ESTATE OWNED, AND OTHER ASSETS AND LISTING ASSETS FOR SPECIAL MENTION Introduction This

How To Get A Working Capital Loan From The Ex-Im Bank

How to Finance Export Receivables By Michael D. Farstad Export Finance Lender Table of Contents New Products Working Capital Supply Chain Finance Guarantee Program Global Credit Express Loan Guarantee

How to Finance Export Receivables By Michael D. Farstad Export Finance Lender Table of Contents New Products Working Capital Supply Chain Finance Guarantee Program Global Credit Express Loan Guarantee

ALASKA USA FEDERAL CREDIT UNION AND SUBSIDIARIES Anchorage, Alaska. CONSOLIDATED FINANCIAL STATEMENTS December 31, 2014 and 2013

ALASKA USA FEDERAL CREDIT UNION AND SUBSIDIARIES Anchorage, Alaska CONSOLIDATED FINANCIAL STATEMENTS Anchorage, Alaska CONSOLIDATED FINANCIAL STATEMENTS CONTENTS INDEPENDENT AUDITOR S REPORT... 1 CONSOLIDATED

ALASKA USA FEDERAL CREDIT UNION AND SUBSIDIARIES Anchorage, Alaska CONSOLIDATED FINANCIAL STATEMENTS Anchorage, Alaska CONSOLIDATED FINANCIAL STATEMENTS CONTENTS INDEPENDENT AUDITOR S REPORT... 1 CONSOLIDATED

TOWN OF HAMDEN, CONNECTICUT Economic & Community Development Department 2750 Dixwell Avenue Hamden, Connecticut 06518

TOWN OF HAMDEN, CONNECTICUT Economic & Community Development Department 2750 Dixwell Avenue Hamden, Connecticut 06518 Dale Kroop, Director TO ALL INTERESTED LOAN APPLICANTS NOTICE OF AVAILABLE FUNDS SMALL

TOWN OF HAMDEN, CONNECTICUT Economic & Community Development Department 2750 Dixwell Avenue Hamden, Connecticut 06518 Dale Kroop, Director TO ALL INTERESTED LOAN APPLICANTS NOTICE OF AVAILABLE FUNDS SMALL

Chapter 12 Special Industries: Banks, Utilities, Oil and Gas, Transportation, Insurance, Real Estate Companies

Chapter 12 Special Industries: Banks, Utilities, Oil and Gas, Transportation, Insurance, Real Estate Companies TO THE NET 1. a. Item 1 Business Market Area Competition The bank contends with considerable

Chapter 12 Special Industries: Banks, Utilities, Oil and Gas, Transportation, Insurance, Real Estate Companies TO THE NET 1. a. Item 1 Business Market Area Competition The bank contends with considerable

RMA Commercial & Business Banking

RMA Commercial & Business Banking The Commercial Real Estate Lending Decision Process The Commercial Real Estate Lending Decision Process, authored by The Risk Management Association and brought to you

RMA Commercial & Business Banking The Commercial Real Estate Lending Decision Process The Commercial Real Estate Lending Decision Process, authored by The Risk Management Association and brought to you

Exhibit 7.9 Sample Loan Operations Risk Based Audit Program

Sample Loan Operations Risk Based Program Inquire about and review written procedures followed during the process of opening and setting up new loans on the system, and procedures on loan approval and

Sample Loan Operations Risk Based Program Inquire about and review written procedures followed during the process of opening and setting up new loans on the system, and procedures on loan approval and

FEDERAL DEPOSIT INSURANCE CORPORATION Washington, D.C. 20429 FORM 10 Q

FEDERAL DEPOSIT INSURANCE CORPORATION Washington, D.C. 20429 FORM 10 Q [ X ] QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the quarterly period ended June

FEDERAL DEPOSIT INSURANCE CORPORATION Washington, D.C. 20429 FORM 10 Q [ X ] QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the quarterly period ended June

How to Assess Your Financial Planning and Loan Proposals By BizMove Management Training Institute

How to Assess Your Financial Planning and Loan Proposals By BizMove Management Training Institute Other free books by BizMove that may interest you: Free starting a business books Free management skills

How to Assess Your Financial Planning and Loan Proposals By BizMove Management Training Institute Other free books by BizMove that may interest you: Free starting a business books Free management skills

Borrowing Money for Your Business

Borrowing Money for Your Business After you have developed a cash flow analysis and determined when your business will make profit, you may decide you need additional funding. Borrowing money is one of

Borrowing Money for Your Business After you have developed a cash flow analysis and determined when your business will make profit, you may decide you need additional funding. Borrowing money is one of

Understanding the NEW DISCLOSURES FOR THE ALLOWANCE FOR CREDIT LOSSES

Understanding the NEW DISCLOSURES FOR THE ALLOWANCE FOR CREDIT LOSSES Executive Summary & Recommendations This document refers to the recent changes in disclosure requirements for financing receivables

Understanding the NEW DISCLOSURES FOR THE ALLOWANCE FOR CREDIT LOSSES Executive Summary & Recommendations This document refers to the recent changes in disclosure requirements for financing receivables

11.437 Financing Community Economic Development Class 6: Fixed Asset Financing

11.437 Financing Community Economic Development Class 6: Fixed Asset Financing I. Purpose of asset financing Fixed asset financing refers to the financing for real estate and equipment needs of a business.

11.437 Financing Community Economic Development Class 6: Fixed Asset Financing I. Purpose of asset financing Fixed asset financing refers to the financing for real estate and equipment needs of a business.

F INANCIAL S TATEMENTS. Brazos Student Finance Corporation Year Ended June 30, 2014 With Independent Auditors Report

F INANCIAL S TATEMENTS Brazos Student Finance Corporation Year Ended June 30, 2014 With Independent Auditors Report Financial Statements Year Ended June 30, 2014 Contents Independent Auditors Report...1

F INANCIAL S TATEMENTS Brazos Student Finance Corporation Year Ended June 30, 2014 With Independent Auditors Report Financial Statements Year Ended June 30, 2014 Contents Independent Auditors Report...1

Shared National Credits Program 2014 Leveraged Loan Supplement

Shared National Credits Program 2014 Leveraged Loan Supplement Board of Governors of the Federal Reserve System Federal Deposit Insurance Corporation Office of the Comptroller of the Currency Washington,

Shared National Credits Program 2014 Leveraged Loan Supplement Board of Governors of the Federal Reserve System Federal Deposit Insurance Corporation Office of the Comptroller of the Currency Washington,

How To Apply For A Small Business Loan Guarantee Program

VIRGINIA SMALL BUSINESS FINANCING AUTHORITY LOAN GUARANTY PROGRAM Application Instructions GENERAL INFORMATION: The Virginia Small Business Financing Authority's (VSBFA) Loan Guaranty Program is designed

VIRGINIA SMALL BUSINESS FINANCING AUTHORITY LOAN GUARANTY PROGRAM Application Instructions GENERAL INFORMATION: The Virginia Small Business Financing Authority's (VSBFA) Loan Guaranty Program is designed

Performance Review for Electricity Now

Performance Review for Electricity Now For the period ending 03/31/2008 Provided By Mark Dashkewytch 780-963-5783 Report prepared for: Electricity Now Industry: 23821 - Electrical Contractors Revenue:

Performance Review for Electricity Now For the period ending 03/31/2008 Provided By Mark Dashkewytch 780-963-5783 Report prepared for: Electricity Now Industry: 23821 - Electrical Contractors Revenue:

SBA 504 Loan Program Lender s Guide

Eligible Use of Proceeds: Land acquisition and improvements New construction Purchase of existing building(s) Renovations to existing building(s) Purchase of Machinery and Equipment (minimum of 10 years

Eligible Use of Proceeds: Land acquisition and improvements New construction Purchase of existing building(s) Renovations to existing building(s) Purchase of Machinery and Equipment (minimum of 10 years

UNDERSTANDING WHERE YOU STAND. A Simple Guide to Your Company s Financial Statements

UNDERSTANDING WHERE YOU STAND A Simple Guide to Your Company s Financial Statements Contents INTRODUCTION One statement cannot diagnose your company s financial health. Put several statements together

UNDERSTANDING WHERE YOU STAND A Simple Guide to Your Company s Financial Statements Contents INTRODUCTION One statement cannot diagnose your company s financial health. Put several statements together

Q4. How should institutions determine if they may exclude asset-based loans (ABL) from their definition of leveraged loans?

from their definition of leveraged loans?") Board of Governors of the Federal Reserve System Federal Deposit Insurance Corporation Office of the Comptroller of the Currency Frequently Asked Questions (FAQ) for Implementing March 2013 Interagency

Board of Governors of the Federal Reserve System Federal Deposit Insurance Corporation Office of the Comptroller of the Currency Frequently Asked Questions (FAQ) for Implementing March 2013 Interagency

Supervisory Letter. Evaluating Credit Union Requests for Waivers of Provisions in NCUA Rules and Regulations Part 723, Member Business Loans (MBLs)

") Supervisory Letter Evaluating Credit Union Requests for Waivers of Provisions in NCUA Rules and Regulations Part 723, Member Business Loans (MBLs) I. Introduction. NCUA provides flexibility in applying

Supervisory Letter Evaluating Credit Union Requests for Waivers of Provisions in NCUA Rules and Regulations Part 723, Member Business Loans (MBLs) I. Introduction. NCUA provides flexibility in applying

Working Capital and Contract Caplines Program. Caplines 2.0: New and Improved

Working Capital and Contract Caplines Program Caplines 2.0: New and Improved Topics for Today s Discussion Structural Changes Key Features for Working Capital Caplines Key Features for Contract Caplines

Working Capital and Contract Caplines Program Caplines 2.0: New and Improved Topics for Today s Discussion Structural Changes Key Features for Working Capital Caplines Key Features for Contract Caplines

BANK ONE CORPORATION and Subsidiaries Average Balance Sheets, Yields, & Rates - Reported Basis

2002 AVERAGE BALANCE SHEET Short-term investments $MM $ 9,484 $ 10,300 $ 12,560 $ 14,442 $ 12,704 Trading assets (1) 6,426 6,941 6,239 6,487 6,982 U.S. government and federal agency 30,331 26,655 25,883

2002 AVERAGE BALANCE SHEET Short-term investments $MM $ 9,484 $ 10,300 $ 12,560 $ 14,442 $ 12,704 Trading assets (1) 6,426 6,941 6,239 6,487 6,982 U.S. government and federal agency 30,331 26,655 25,883

C&I LOAN EVALUATION UNDERWRITING GUIDELINES. A Whitepaper

C&I LOAN EVALUATION & UNDERWRITING A Whitepaper C&I Lending Commercial and Industrial, or C&I Lending, has long been a cornerstone product for many successful banking institutions. Also known as working

C&I LOAN EVALUATION & UNDERWRITING A Whitepaper C&I Lending Commercial and Industrial, or C&I Lending, has long been a cornerstone product for many successful banking institutions. Also known as working

Loan Participation Enrollment Form

Loan Participation Enrollment Form Emerging Entrepreneur s Fund Program Business Information 1. Name and Address of Business: 2. NAICS Code: 3. DUNS No.: 4. Number of Employees Employed by Business at

Loan Participation Enrollment Form Emerging Entrepreneur s Fund Program Business Information 1. Name and Address of Business: 2. NAICS Code: 3. DUNS No.: 4. Number of Employees Employed by Business at

St. Vincent and the Grenadines International Financial Services Authority Statement of Guidance No. 3

St. Vincent and the Grenadines International Financial Services Authority Statement of Guidance No. 3 Loan Classification Criteria Provisioning Guidelines Treatment of Interest on Loans Write off Procedures

St. Vincent and the Grenadines International Financial Services Authority Statement of Guidance No. 3 Loan Classification Criteria Provisioning Guidelines Treatment of Interest on Loans Write off Procedures

QUAINT OAK BANCORP, INC. ANNOUNCES SECOND QUARTER EARNINGS

FOR RELEASE: Tuesday, July 28, 2015 at 4:30 PM (Eastern) QUAINT OAK BANCORP, INC. ANNOUNCES SECOND QUARTER EARNINGS Southampton, PA Quaint Oak Bancorp, Inc. (the Company ) (OTCQX: QNTO), the holding company

FOR RELEASE: Tuesday, July 28, 2015 at 4:30 PM (Eastern) QUAINT OAK BANCORP, INC. ANNOUNCES SECOND QUARTER EARNINGS Southampton, PA Quaint Oak Bancorp, Inc. (the Company ) (OTCQX: QNTO), the holding company

Borrowing 101. Resources. Are you ready to Borrow?

Borrowing 101 The BDC wants your business to succeed and in turn pay the BDC back. Our programs are revolving loan funds that require loans to be repaid so that we can lend our dollars to other businesses

Borrowing 101 The BDC wants your business to succeed and in turn pay the BDC back. Our programs are revolving loan funds that require loans to be repaid so that we can lend our dollars to other businesses

The transfer between levels of hierarchy (i.e., from Level 2 to Level 1) in 2010 was due to the listing of the SMC shares in December 2010.

in 2010 was due to the listing of the SMC shares in December 2010.") 24 In accordance with this amendment, financial assets and liabilities measured at fair value in the statement of financial position are categorized in accordance with the fair value hierarchy. This hierarchy

24 In accordance with this amendment, financial assets and liabilities measured at fair value in the statement of financial position are categorized in accordance with the fair value hierarchy. This hierarchy

STATEMENT OF CASH FLOWS AND WORKING CAPITAL ANALYSIS

C H A P T E R 1 0 STATEMENT OF CASH FLOWS AND WORKING CAPITAL ANALYSIS I N T R O D U C T I O N Historically, profit-oriented businesses have used the accrual basis of accounting in which the income statement,

C H A P T E R 1 0 STATEMENT OF CASH FLOWS AND WORKING CAPITAL ANALYSIS I N T R O D U C T I O N Historically, profit-oriented businesses have used the accrual basis of accounting in which the income statement,