Lecture 5: Review Investment decisions and break even analysis

|

|

|

- Morgan Black

- 10 years ago

- Views:

Transcription

1 Lecture 5: Review Investment decisions and break even analysis

2 2 Summary Investments imply willingness to trade dollars in the present for dollars in the future. Wealth-creating transactions occur when individuals with low discount rates (rate at which they value future vs current dollars) lend to those with high discount rates. Companies, like individuals, have different discount rates, determined by their cost of capital. They invest only in projects that earn a return higher than the cost of capital. The NPV rule states that if the present value of the net cash flow of a project is larger than zero, the project earns economic profit (i.e., the investment earns more than the cost of capital). Although NPV is the correct way to analyze investments, not all companies use it. Instead, they use break-even analysis because it is easier and more intuitive. Break-even quantity is equal to fixed cost divided by the contribution margin. If you expect to sell more than the break-even quantity, then your investment is profitable.

.")

3 3 Shutdown decisions Shutdown decisions are difficult psychologically, but economically, the rule of thumb is straightforward Avoidable costs are costs that can be recovered from shutting down. Shutdown if the marginal benefits associated with recouping avoidable costs exceeds marginal costs, in this case, the foregone revenue from shutting down. If you incur sunk costs specific to a trade relationship, you are subject to the hold-up problem. Anticipate hold-up and choose organizational or contractual forms to give each party both the incentive to make relationship-specific investments and to trade after these investments are made.

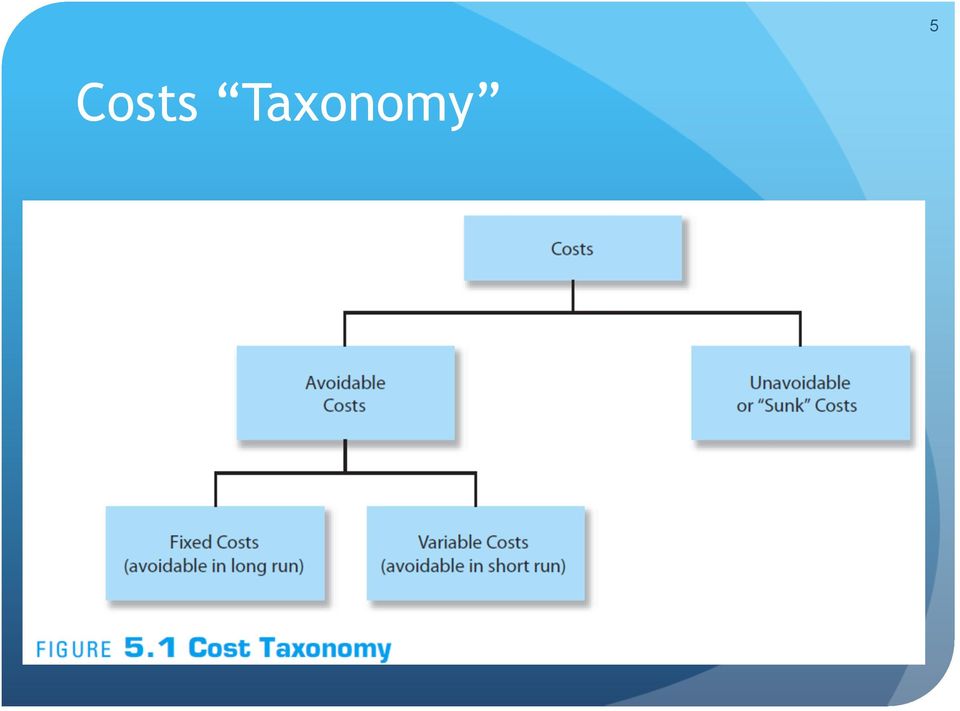

4 4 Should we shut down? Shut-down decisions are made using break-even prices rather than quantities. The break-even price is the average avoidable cost per unit Profit = Rev-Cost= (P-AC)(Q) If you shut down, you lose your revenue, but you get back your avoidable cost. If average avoidable cost is less than price, shut down. Determining avoidable costs can be difficult. To identify avoidable costs firms use Cost Taxonomy

5 Costs Taxonomy 5

6 6 KEY POINT #3 Difficult decisions to shutdown often involve psychological costs. A firm should shut down when average avoidable cost is less than the price. Example: Consider a firm that produces 500,000 units per year. The firm s fixed costs are $100,000, marginal costs are $250 and the price per unit is $400. In the short-run, how low can price go before it is profitable to shut down?

7 7 Uh Oh! It s a hold up! National Geographic can reduce shipping costs by printing with regional printers. To print a high quality magazine, the printer must buy a $12 million printing press. Each magazine has a MC of $1 and the printer would print 12 million copies over two years. The break-even cost/average cost is $7 = ($12M / 2M copies) + $1/copy BUT once the press is purchased, the cost is sunk and the break-even price changes. Because of this the magazine can hold up the printer by renogiating the terms of the deal because the price of the press is unavoidable, and sunk, the break-even price falls to $1, the marginal cost.

+ $1/copy BUT once the press is purchased, the cost is sunk and the break-even price changes.")

8 Sunk costs and post-investment hold up 8 Always remember the business maxim look ahead and reason back. This can help you avoid potential hold up. Before making a sunk cost investment, ask what you will do if you are held up. What would you do to address hold up? One possible solution to post-investment hold-up is vertical integration. Another, is the so called exchange of hostages.

9 9 Solutions and a final example Example: Bauxite mine and alumina refinery Refineries are tailored to specific qualities of ore Building refineries near mines reduces costs for the refiner, but, the building of the refinery becomes a sunk cost The transaction options are: Long-term contracts Vertical integration Vertical integration refers to the common ownership of two firms in separate stages of the vertical supply chain that connects raw materials to finished goods We can make it expensive to hold up. Incentives should be introduced that cause both parties to adhere to original agreements. Contractual view of marriage What is the hold-up problem?

10 10 Lecture 5 TOPIC #1: Simple Pricing and demand

11 Summary of main points Aggregate demand or market demand is the total number of units that will be purchased by a group of consumers at a given price. Pricing is an extent decision. Reduce price (increase quantity) if MR > MC. Increase price (reduce quantity) if MR < MC. The optimal price is where MR = MC. Price elasticity of demand, e = (% change in quantity demanded) (% change in price) If e > 1, demand is elastic; if e < 1, demand is inelastic. %ΔRevenue %ΔPrice + %ΔQuantity Elastic Demand ( e > 1): Quantity changes more than price. Inelastic Demand ( e < 1): Quantity changes less than price.

(% change in price) If e > 1, demand is elastic; if e < 1, demand is inelastic.")

12 Summary (cont.) MR > MC implies that (P - MC)/P > 1/ e ; in words, if the actual markup is bigger than the desired markup, reduce price Equivalently, sell more Four factors make demand more elastic: Products with close substitutes (or distant complements) have more elastic demand. Demand for brands is more elastic than industry demand. In the long run, demand becomes more elastic. As price increases, demand becomes more elastic. Income elasticity, cross-price elasticity, and advertising elasticity are measures of how changes in these other factors affect demand. It is possible to use elasticity to forecast changes in demand: %ΔQuantity (factor elasticity)*(%δfactor). Stay-even analysis can be used to determine the volume required to offset a change in costs or prices.

13 Introductory anecdote: Mattel Mattel: introduced Hot Wheels in 1968, kept price below $1.00 for 40 years, even as production costs rose Finally tested a price increase, experienced profits increase of 20% Why? Profit=(P-TC)xQ Businesses tend to focus on TC and Q, neglect P

14 14 Roger Brinner, Parthenon Group In many instances, companies can make money by simply raising prices. Pricing is the grossly neglected orphan of profit management. Most companies leave list prices unchanged year after year or simply modestly increase list prices in an unchallenged annual ritual. Other companies perform strategic analyses, producing the facts and generating the confidence to change prices aggressively and to raise profits dramatically.

15 Background: consumer surplus and demand curves First Law of Demand - consumers demand (purchase) more as price falls, assuming other factors are held constant. Consumers make consumption decisions using marginal analysis, consume more if marginal value > price But, the marginal value of consuming each subsequent unit diminishes the more you consume. Consumer surplus = value to consumer - price paid Definition: Demand curves are functions that relate the price of a product to the quantity demanded by consumers

16 16 KEY POINT #1 INDIVIDUAL DEMAND CURVES SLOPE DOWN. THE LAW OF DEMAND! As we raise price, consumers will respond by purchasing less.

17 Background: consumer surplus and demand curves (cont.) Hot dog consumer Values first dog at $5, next at $4... fifth at $1 Note that if hot dogs price is $3, consumer will purchase 3 hot dogs

18 Background: aggregate demand Aggregate Demand: the buying behavior of a group of consumers; a total of all the individual demand curves. To construct demand, sort by value. Discussion: Why do aggregate demand curves slope downward?

19 19 Pricing trade-off Pricing is an extent decision Profit= Total Revenue Total Cost Demand curves turn pricing decisions into quantity decisions: what price should I charge? is equivalent to how much should I sell? Fundamental tradeoff: Lower price sell more, but earn less on each unit sold Higher price sell less, but earn more on each unit sold Tradeoff created by downward sloping demand

20 20 Pricing Marginal analysis finds the profit increasing solution to the pricing tradeoff. It tells you only whether to raise or lower price, not by how much. Definition: marginal revenue (MR) is change in total revenue from selling extra unit. If MR>0, then total revenue will increase if you sell one more. Highest level of MR doesn t mean profits are maximized as we saw on our quiz. If MR>MC, then total profits will increase if you sell one more. We already know: Profits are maximized when MR = MC

21 21 KEY POINT #2 MARGINAL ANALYSIS TELLS US THAT WHEN MR>MC. PRODUCE AND SELL MORE!!! HOW???? DECREASE PRICE WHEN MR<MC. WE ARE PRODUCING AND SELLING TOO MUCH. SELL LESS!!! HOW??? INCREASE PRICE

22 Start from the top FILL IT IN: FIXED COST =$5 22 PRICE Q Demand Revnue MR MC Profit $7 1 $1.50 $6 2 $1.50 $5 3 $1.50 $4 4 $1.50 $3 5 $1.50 $2 6 $1.50 $1 7 $1.50

23 23 Let s tell the truth Having worked as an economic consultant, I can tell you, you will never see a complete demand curve. Even still, the analysis we have just seen can give invaluable intuition into understanding pricing decisions. In particular, what we have just seen is that MR and MC are what we need to know. We can use this information and market information about elasticities to form the proper decisions.

24 24 Elasticity of demand Price elasticity is a factor in calculating MR. Definition: price elasticity of demand (e) (%Δ in Q d ) (%Δ in price) If e is less than one, demand is said to be inelastic. If e is greater than one, demand is said to be elastic.

25 Price change between month 1 and month 2 25 Definition: Elasticity= [(q 2 -q 1 )/(q 1 +q 2 )] [(p 2 -p 1 )/(p 1 +p 2 )]. Note, by the law of demand, elasticity of price change should be negative. Example: On a promotion week for Vlasic, the price of Vlasic pickles dropped by 25% and quantity increased by 300%. Is the price elasticity of demand -12? HINT: could something other than price be changing?

26 26 KEY POINT #3 WHEN DEMAND IS ELASTIC, RAISING THE PRICE WILL REDUCE REVENUE. WHEN DEMAND IS INELASTIC, RAISING THE PRICE WILL RAISE REVENUE!! Note: Remember revenue is only one side of the coin. We would need to know something about costs to determine if profit are maximized.

27 Example: Grocery Store (MidSouth in 1999) Liter Coke Promotion (Instituted to meet Wal- Mart promotion) Compute price elasticity of 3 liter coke; cross price elasticity of 2 liter coke with respect to 3 liter price;

28 28 Revenue: Demand for 3-liters was very elastic. Please calculate the revenue that resulted from the price decrease. Did revenue increase or decrease? Should increase as we already discussed. We can show the %change in revenue is equal to the %change in price + % change in quantity. Since prices and quantities move in opposite directions, total revenue changes will determined by which changes by more (in absolute value).

29 If you want, I ll show you the math 29 Proposition: MR = Avg(P)(1-1/ e ) If e >1, MR>0. If e <1, MR<0. Discussion: If demand for Nike sneakers is inelastic, should Nike raise or lower price? Discussion: If demand for Nike sneakers is elastic, should Nike raise or lower price?

30 30 Example MR>MC => avg(p)[1-1/ e ]>MC =>avg(p)-avg(p)/ e >MC =>avg(p)-mc>avg(p)/ e =>[avg(p)-mc]/avg(p)>1/ e The firm s actual mark-up exceeds the desired markup! It should lower price!

31 31 Example Suppose you have the following data: Elasticity= 2 Average Price =$10 Marginal Cost= $8 Should we raise the price? How do you know?

11 PERFECT COMPETITION. Chapter. Competition

Chapter 11 PERFECT COMPETITION Competition Topic: Perfect Competition 1) Perfect competition is an industry with A) a few firms producing identical goods B) a few firms producing goods that differ somewhat

Chapter 11 PERFECT COMPETITION Competition Topic: Perfect Competition 1) Perfect competition is an industry with A) a few firms producing identical goods B) a few firms producing goods that differ somewhat

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

MBA 640 Survey of Microeconomics Fall 2006, Quiz 6 Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) A monopoly is best defined as a firm that

MBA 640 Survey of Microeconomics Fall 2006, Quiz 6 Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) A monopoly is best defined as a firm that

Profit Maximization. 2. product homogeneity

Perfectly Competitive Markets It is essentially a market in which there is enough competition that it doesn t make sense to identify your rivals. There are so many competitors that you cannot single out

Perfectly Competitive Markets It is essentially a market in which there is enough competition that it doesn t make sense to identify your rivals. There are so many competitors that you cannot single out

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

Practice for Perfect Competition Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) Which of the following is a defining characteristic of a

Practice for Perfect Competition Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) Which of the following is a defining characteristic of a

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question on the accompanying scantron.

Principles of Microeconomics, Quiz #5 Fall 2007 Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question on the accompanying scantron. 1) Perfect competition

Principles of Microeconomics, Quiz #5 Fall 2007 Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question on the accompanying scantron. 1) Perfect competition

Practice Questions Week 8 Day 1

Practice Questions Week 8 Day 1 Multiple Choice Identify the choice that best completes the statement or answers the question. 1. The characteristics of a market that influence the behavior of market participants

Practice Questions Week 8 Day 1 Multiple Choice Identify the choice that best completes the statement or answers the question. 1. The characteristics of a market that influence the behavior of market participants

11.3 BREAK-EVEN ANALYSIS. Fixed and Variable Costs

385 356 PART FOUR Capital Budgeting a large number of NPV estimates that we summarize by calculating the average value and some measure of how spread out the different possibilities are. For example, it

385 356 PART FOUR Capital Budgeting a large number of NPV estimates that we summarize by calculating the average value and some measure of how spread out the different possibilities are. For example, it

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

Chapter 11 Perfect Competition - Sample Questions MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) Perfect competition is an industry with A) a

Chapter 11 Perfect Competition - Sample Questions MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) Perfect competition is an industry with A) a

2011 Pearson Education. Elasticities of Demand and Supply: Today add elasticity and slope, cross elasticities

2011 Pearson Education Elasticities of Demand and Supply: Today add elasticity and slope, cross elasticities What Determines Elasticity? Influences on the price elasticity of demand fall into two categories:

2011 Pearson Education Elasticities of Demand and Supply: Today add elasticity and slope, cross elasticities What Determines Elasticity? Influences on the price elasticity of demand fall into two categories:

1 Monopoly Why Monopolies Arise? Monopoly is a rm that is the sole seller of a product without close substitutes. The fundamental cause of monopoly is barriers to entry: A monopoly remains the only seller

1 Monopoly Why Monopolies Arise? Monopoly is a rm that is the sole seller of a product without close substitutes. The fundamental cause of monopoly is barriers to entry: A monopoly remains the only seller

Learning Objectives. Chapter 6. Market Structures. Market Structures (cont.) The Two Extremes: Perfect Competition and Pure Monopoly

The Two Extremes: Perfect Competition and Pure Monopoly") Chapter 6 The Two Extremes: Perfect Competition and Pure Monopoly Learning Objectives List the four characteristics of a perfectly competitive market. Describe how a perfect competitor makes the decision

Chapter 6 The Two Extremes: Perfect Competition and Pure Monopoly Learning Objectives List the four characteristics of a perfectly competitive market. Describe how a perfect competitor makes the decision

Learning Objectives. After reading Chapter 11 and working the problems for Chapter 11 in the textbook and in this Workbook, you should be able to:

Learning Objectives After reading Chapter 11 and working the problems for Chapter 11 in the textbook and in this Workbook, you should be able to: Discuss three characteristics of perfectly competitive

Learning Objectives After reading Chapter 11 and working the problems for Chapter 11 in the textbook and in this Workbook, you should be able to: Discuss three characteristics of perfectly competitive

The Cost of Production

The Cost of Production 1. Opportunity Costs 2. Economic Costs versus Accounting Costs 3. All Sorts of Different Kinds of Costs 4. Cost in the Short Run 5. Cost in the Long Run 6. Cost Minimization 7. The

The Cost of Production 1. Opportunity Costs 2. Economic Costs versus Accounting Costs 3. All Sorts of Different Kinds of Costs 4. Cost in the Short Run 5. Cost in the Long Run 6. Cost Minimization 7. The

COST THEORY. I What costs matter? A Opportunity Costs

COST THEORY Cost theory is related to production theory, they are often used together. However, the question is how much to produce, as opposed to which inputs to use. That is, assume that we use production

COST THEORY Cost theory is related to production theory, they are often used together. However, the question is how much to produce, as opposed to which inputs to use. That is, assume that we use production

Chapter 5 Estimating Demand Functions

Chapter 5 Estimating Demand Functions 1 Why do you need statistics and regression analysis? Ability to read market research papers Analyze your own data in a simple way Assist you in pricing and marketing

Chapter 5 Estimating Demand Functions 1 Why do you need statistics and regression analysis? Ability to read market research papers Analyze your own data in a simple way Assist you in pricing and marketing

Chapter 6 Competitive Markets

Chapter 6 Competitive Markets After reading Chapter 6, COMPETITIVE MARKETS, you should be able to: List and explain the characteristics of Perfect Competition and Monopolistic Competition Explain why a

Chapter 6 Competitive Markets After reading Chapter 6, COMPETITIVE MARKETS, you should be able to: List and explain the characteristics of Perfect Competition and Monopolistic Competition Explain why a

Managerial Economics & Business Strategy Chapter 8. Managing in Competitive, Monopolistic, and Monopolistically Competitive Markets

Managerial Economics & Business Strategy Chapter 8 Managing in Competitive, Monopolistic, and Monopolistically Competitive Markets I. Perfect Competition Overview Characteristics and profit outlook. Effect

Managerial Economics & Business Strategy Chapter 8 Managing in Competitive, Monopolistic, and Monopolistically Competitive Markets I. Perfect Competition Overview Characteristics and profit outlook. Effect

Homework 3, Solutions Managerial Economics: Eco 685

Homework 3, Solutions Managerial Economics: Eco 685 Question 1 a. Second degree since we have a quantity discount. For 2 GB the cost is $15 per GB, for 5 GB the cost is $10 per GB, and for 10 GB the cost

Homework 3, Solutions Managerial Economics: Eco 685 Question 1 a. Second degree since we have a quantity discount. For 2 GB the cost is $15 per GB, for 5 GB the cost is $10 per GB, and for 10 GB the cost

Market Structure: Perfect Competition and Monopoly

WSG8 7/7/03 4:34 PM Page 113 8 Market Structure: Perfect Competition and Monopoly OVERVIEW One of the most important decisions made by a manager is how to price the firm s product. If the firm is a profit

WSG8 7/7/03 4:34 PM Page 113 8 Market Structure: Perfect Competition and Monopoly OVERVIEW One of the most important decisions made by a manager is how to price the firm s product. If the firm is a profit

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

Economics 103 Spring 2012: Multiple choice review questions for final exam. Exam will cover chapters on perfect competition, monopoly, monopolistic competition and oligopoly up to the Nash equilibrium

Economics 103 Spring 2012: Multiple choice review questions for final exam. Exam will cover chapters on perfect competition, monopoly, monopolistic competition and oligopoly up to the Nash equilibrium

Practice Questions Week 6 Day 1

Practice Questions Week 6 Day 1 Multiple Choice Identify the choice that best completes the statement or answers the question. 1. Economists assume that the goal of the firm is to a. maximize total revenue

Practice Questions Week 6 Day 1 Multiple Choice Identify the choice that best completes the statement or answers the question. 1. Economists assume that the goal of the firm is to a. maximize total revenue

Figure 1, A Monopolistically Competitive Firm

The Digital Economist Lecture 9 Pricing Power and Price Discrimination Many firms have the ability to charge prices for their products consistent with their best interests even thought they may not be

The Digital Economist Lecture 9 Pricing Power and Price Discrimination Many firms have the ability to charge prices for their products consistent with their best interests even thought they may not be

Elasticity. Definition of the Price Elasticity of Demand: Formula for Elasticity: Types of Elasticity:

Elasticity efinition of the Elasticity of emand: The law of demand states that the quantity demanded of a good will vary inversely with the price of the good during a given time period, but it does not

Elasticity efinition of the Elasticity of emand: The law of demand states that the quantity demanded of a good will vary inversely with the price of the good during a given time period, but it does not

Review of Production and Cost Concepts

Sloan School of Management 15.010/15.011 Massachusetts Institute of Technology RECITATION NOTES #3 Review of Production and Cost Concepts Thursday - September 23, 2004 OUTLINE OF TODAY S RECITATION 1.

Sloan School of Management 15.010/15.011 Massachusetts Institute of Technology RECITATION NOTES #3 Review of Production and Cost Concepts Thursday - September 23, 2004 OUTLINE OF TODAY S RECITATION 1.

KEELE UNIVERSITY MID-TERM TEST, 2007 BA BUSINESS ECONOMICS BA FINANCE AND ECONOMICS BA MANAGEMENT SCIENCE ECO 20015 MANAGERIAL ECONOMICS II

KEELE UNIVERSITY MID-TERM TEST, 2007 Thursday 22nd NOVEMBER, 12.05-12.55 BA BUSINESS ECONOMICS BA FINANCE AND ECONOMICS BA MANAGEMENT SCIENCE ECO 20015 MANAGERIAL ECONOMICS II Candidates should attempt

KEELE UNIVERSITY MID-TERM TEST, 2007 Thursday 22nd NOVEMBER, 12.05-12.55 BA BUSINESS ECONOMICS BA FINANCE AND ECONOMICS BA MANAGEMENT SCIENCE ECO 20015 MANAGERIAL ECONOMICS II Candidates should attempt

Principles of Economics: Micro: Exam #2: Chapters 1-10 Page 1 of 9

Principles of Economics: Micro: Exam #2: Chapters 1-10 Page 1 of 9 print name on the line above as your signature INSTRUCTIONS: 1. This Exam #2 must be completed within the allocated time (i.e., between

Principles of Economics: Micro: Exam #2: Chapters 1-10 Page 1 of 9 print name on the line above as your signature INSTRUCTIONS: 1. This Exam #2 must be completed within the allocated time (i.e., between

Theoretical Tools of Public Economics. Part-2

Theoretical Tools of Public Economics Part-2 Previous Lecture Definitions and Properties Utility functions Marginal utility: positive (negative) if x is a good ( bad ) Diminishing marginal utility Indifferences

Theoretical Tools of Public Economics Part-2 Previous Lecture Definitions and Properties Utility functions Marginal utility: positive (negative) if x is a good ( bad ) Diminishing marginal utility Indifferences

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

Chapter 11 Monopoly practice Davidson spring2007 MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) A monopoly industry is characterized by 1) A)

Chapter 11 Monopoly practice Davidson spring2007 MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) A monopoly industry is characterized by 1) A)

17. If a good is normal, then the Engel curve A. Slopes upward B. Slopes downward C. Is vertical D. Is horizontal

Sample Exam 1 1. Suppose that when the price of hot dogs is $2 per package, there is a demand for 10,000 bags of hot dog buns. When the price of hot dogs is $3 per package, the demand for hot dog buns

Sample Exam 1 1. Suppose that when the price of hot dogs is $2 per package, there is a demand for 10,000 bags of hot dog buns. When the price of hot dogs is $3 per package, the demand for hot dog buns

Problems: Table 1: Quilt Dress Quilts Dresses Helen 50 10 1.8 9 Carolyn 90 45 1 2

Problems: Table 1: Labor Hours needed to make one Amount produced in 90 hours: Quilt Dress Quilts Dresses Helen 50 10 1.8 9 Carolyn 90 45 1 2 1. Refer to Table 1. For Carolyn, the opportunity cost of 1

Problems: Table 1: Labor Hours needed to make one Amount produced in 90 hours: Quilt Dress Quilts Dresses Helen 50 10 1.8 9 Carolyn 90 45 1 2 1. Refer to Table 1. For Carolyn, the opportunity cost of 1

CE2451 Engineering Economics & Cost Analysis. Objectives of this course

CE2451 Engineering Economics & Cost Analysis Dr. M. Selvakumar Associate Professor Department of Civil Engineering Sri Venkateswara College of Engineering Objectives of this course The main objective of

CE2451 Engineering Economics & Cost Analysis Dr. M. Selvakumar Associate Professor Department of Civil Engineering Sri Venkateswara College of Engineering Objectives of this course The main objective of

2.4 Multiproduct Monopoly. 2.4 Multiproduct Monopoly

.4 Multiproduct Monopoly Matilde Machado Slides available from: http://www.eco.uc3m.es/oi-i-mei/.4 Multiproduct Monopoly The firm is a monopoly in all markets where it operates i=,.n goods sold by the

.4 Multiproduct Monopoly Matilde Machado Slides available from: http://www.eco.uc3m.es/oi-i-mei/.4 Multiproduct Monopoly The firm is a monopoly in all markets where it operates i=,.n goods sold by the

DUKE UNIVERSITY Fuqua School of Business. FINANCE 351 - CORPORATE FINANCE Problem Set #1 Prof. Simon Gervais Fall 2011 Term 2.

DUKE UNIVERSITY Fuqua School of Business FINANCE 351 - CORPORATE FINANCE Problem Set #1 Prof. Simon Gervais Fall 2011 Term 2 Questions 1. Two years ago, you put $20,000 dollars in a savings account earning

DUKE UNIVERSITY Fuqua School of Business FINANCE 351 - CORPORATE FINANCE Problem Set #1 Prof. Simon Gervais Fall 2011 Term 2 Questions 1. Two years ago, you put $20,000 dollars in a savings account earning

Pre-Test Chapter 21 ed17

Pre-Test Chapter 21 ed17 Multiple Choice Questions 1. Which of the following is not a basic characteristic of pure competition? A. considerable nonprice competition B. no barriers to the entry or exodus

Pre-Test Chapter 21 ed17 Multiple Choice Questions 1. Which of the following is not a basic characteristic of pure competition? A. considerable nonprice competition B. no barriers to the entry or exodus

Chapter. Perfect Competition CHAPTER IN PERSPECTIVE

Perfect Competition Chapter 10 CHAPTER IN PERSPECTIVE In Chapter 10 we study perfect competition, the market that arises when the demand for a product is large relative to the output of a single producer.

Perfect Competition Chapter 10 CHAPTER IN PERSPECTIVE In Chapter 10 we study perfect competition, the market that arises when the demand for a product is large relative to the output of a single producer.

c. Given your answer in part (b), what do you anticipate will happen in this market in the long-run?

, what do you anticipate will happen in this market in the long-run?") Perfect Competition Questions Question 1 Suppose there is a perfectly competitive industry where all the firms are identical with identical cost curves. Furthermore, suppose that a representative firm

Perfect Competition Questions Question 1 Suppose there is a perfectly competitive industry where all the firms are identical with identical cost curves. Furthermore, suppose that a representative firm

Pricing and Output Decisions: i Perfect. Managerial Economics: Economic Tools for Today s Decision Makers, 4/e By Paul Keat and Philip Young

Chapter 9 Pricing and Output Decisions: i Perfect Competition and Monopoly M i l E i E i Managerial Economics: Economic Tools for Today s Decision Makers, 4/e By Paul Keat and Philip Young Pricing and

Chapter 9 Pricing and Output Decisions: i Perfect Competition and Monopoly M i l E i E i Managerial Economics: Economic Tools for Today s Decision Makers, 4/e By Paul Keat and Philip Young Pricing and

Managerial Economics

Managerial Economics Unit 1: Demand Theory Rudolf Winter-Ebmer Johannes Kepler University Linz Winter Term 2012/13 Winter-Ebmer, Managerial Economics: Unit 1 - Demand Theory 1 / 54 OBJECTIVES Explain the

Managerial Economics Unit 1: Demand Theory Rudolf Winter-Ebmer Johannes Kepler University Linz Winter Term 2012/13 Winter-Ebmer, Managerial Economics: Unit 1 - Demand Theory 1 / 54 OBJECTIVES Explain the

Chapter 8. Competitive Firms and Markets

Chapter 8. Competitive Firms and Markets We have learned the production function and cost function, the question now is: how much to produce such that firm can maximize his profit? To solve this question,

Chapter 8. Competitive Firms and Markets We have learned the production function and cost function, the question now is: how much to produce such that firm can maximize his profit? To solve this question,

CEVAPLAR. Solution: a. Given the competitive nature of the industry, Conigan should equate P to MC.

1 I S L 8 0 5 U Y G U L A M A L I İ K T İ S A T _ U Y G U L A M A ( 4 ) _ 9 K a s ı m 2 0 1 2 CEVAPLAR 1. Conigan Box Company produces cardboard boxes that are sold in bundles of 1000 boxes. The market

1 I S L 8 0 5 U Y G U L A M A L I İ K T İ S A T _ U Y G U L A M A ( 4 ) _ 9 K a s ı m 2 0 1 2 CEVAPLAR 1. Conigan Box Company produces cardboard boxes that are sold in bundles of 1000 boxes. The market

N. Gregory Mankiw Principles of Economics. Chapter 15. MONOPOLY

N. Gregory Mankiw Principles of Economics Chapter 15. MONOPOLY Solutions to Problems and Applications 1. The following table shows revenue, costs, and profits, where quantities are in thousands, and total

N. Gregory Mankiw Principles of Economics Chapter 15. MONOPOLY Solutions to Problems and Applications 1. The following table shows revenue, costs, and profits, where quantities are in thousands, and total

Pricing with Perfect Competition. Business Economics Advanced Pricing Strategies. Pricing with Market Power. Markup Pricing

Business Economics Advanced Pricing Strategies Thomas & Maurice, Chapter 12 Herbert Stocker [email protected] Institute of International Studies University of Ramkhamhaeng & Department of Economics

Business Economics Advanced Pricing Strategies Thomas & Maurice, Chapter 12 Herbert Stocker [email protected] Institute of International Studies University of Ramkhamhaeng & Department of Economics

OVERVIEW. 2. If demand is vertical, demand is perfectly inelastic. Every change in price brings no change in quantity.

7 PRICE ELASTICITY OVERVIEW 1. The elasticity of demand measures the responsiveness of 1 the buyer to a change in price. The coefficient of price elasticity is the percentage change in quantity divided

7 PRICE ELASTICITY OVERVIEW 1. The elasticity of demand measures the responsiveness of 1 the buyer to a change in price. The coefficient of price elasticity is the percentage change in quantity divided

Practice Multiple Choice Questions Answers are bolded. Explanations to come soon!!

Practice Multiple Choice Questions Answers are bolded. Explanations to come soon!! For more, please visit: http://courses.missouristate.edu/reedolsen/courses/eco165/qeq.htm Market Equilibrium and Applications

Practice Multiple Choice Questions Answers are bolded. Explanations to come soon!! For more, please visit: http://courses.missouristate.edu/reedolsen/courses/eco165/qeq.htm Market Equilibrium and Applications

Chapter 6. Elasticity: The Responsiveness of Demand and Supply

Chapter 6. Elasticity: The Responsiveness of Demand and Supply Instructor: JINKOOK LEE Department of Economics / Texas A&M University ECON 202 504 Principles of Microeconomics Elasticity Demand curve:

Chapter 6. Elasticity: The Responsiveness of Demand and Supply Instructor: JINKOOK LEE Department of Economics / Texas A&M University ECON 202 504 Principles of Microeconomics Elasticity Demand curve:

12 Monopolistic Competition and Oligopoly

12 Monopolistic Competition and Oligopoly Read Pindyck and Rubinfeld (2012), Chapter 12 09/04/2015 CHAPTER 12 OUTLINE 12.1 Monopolistic Competition 12.2 Oligopoly 12.3 Price Competition 12.4 Competition

12 Monopolistic Competition and Oligopoly Read Pindyck and Rubinfeld (2012), Chapter 12 09/04/2015 CHAPTER 12 OUTLINE 12.1 Monopolistic Competition 12.2 Oligopoly 12.3 Price Competition 12.4 Competition

Figure 4-1 Price Quantity Quantity Per Pair Demanded Supplied $ 2 18 3 $ 4 14 4 $ 6 10 5 $ 8 6 6 $10 2 8

Econ 101 Summer 2005 In-class Assignment 2 & HW3 MULTIPLE CHOICE 1. A government-imposed price ceiling set below the market's equilibrium price for a good will produce an excess supply of the good. a.

Econ 101 Summer 2005 In-class Assignment 2 & HW3 MULTIPLE CHOICE 1. A government-imposed price ceiling set below the market's equilibrium price for a good will produce an excess supply of the good. a.

Marginal cost. Average cost. Marginal revenue 10 20 40

Economics 101 Fall 2011 Homework #6 Due: 12/13/2010 in lecture Directions: The homework will be collected in a box before the lecture. Please place your name, TA name and section number on top of the homework

Economics 101 Fall 2011 Homework #6 Due: 12/13/2010 in lecture Directions: The homework will be collected in a box before the lecture. Please place your name, TA name and section number on top of the homework

A. a change in demand. B. a change in quantity demanded. C. a change in quantity supplied. D. unit elasticity. E. a change in average variable cost.

1. The supply of gasoline changes, causing the price of gasoline to change. The resulting movement from one point to another along the demand curve for gasoline is called A. a change in demand. B. a change

1. The supply of gasoline changes, causing the price of gasoline to change. The resulting movement from one point to another along the demand curve for gasoline is called A. a change in demand. B. a change

or, put slightly differently, the profit maximizing condition is for marginal revenue to equal marginal cost:

Chapter 9 Lecture Notes 1 Economics 35: Intermediate Microeconomics Notes and Sample Questions Chapter 9: Profit Maximization Profit Maximization The basic assumption here is that firms are profit maximizing.

Chapter 9 Lecture Notes 1 Economics 35: Intermediate Microeconomics Notes and Sample Questions Chapter 9: Profit Maximization Profit Maximization The basic assumption here is that firms are profit maximizing.

AP Microeconomics Chapter 12 Outline

I. Learning Objectives In this chapter students will learn: A. The significance of resource pricing. B. How the marginal revenue productivity of a resource relates to a firm s demand for that resource.

I. Learning Objectives In this chapter students will learn: A. The significance of resource pricing. B. How the marginal revenue productivity of a resource relates to a firm s demand for that resource.

Chapter 8 Production Technology and Costs 8.1 Economic Costs and Economic Profit

Chapter 8 Production Technology and Costs 8.1 Economic Costs and Economic Profit 1) Accountants include costs as part of a firm's costs, while economists include costs. A) explicit; no explicit B) implicit;

Chapter 8 Production Technology and Costs 8.1 Economic Costs and Economic Profit 1) Accountants include costs as part of a firm's costs, while economists include costs. A) explicit; no explicit B) implicit;

CHAPTER 17 DIVISIONAL PERFORMANCE EVALUATION

CHAPTER 17 DIVISIONAL PERFORMANCE EVALUATION CHAPTER SUMMARY This chapter is the second of two chapters on performance evaluation. It focuses on the measurement of divisional performance. It begins by

CHAPTER 17 DIVISIONAL PERFORMANCE EVALUATION CHAPTER SUMMARY This chapter is the second of two chapters on performance evaluation. It focuses on the measurement of divisional performance. It begins by

Lecture 2. Marginal Functions, Average Functions, Elasticity, the Marginal Principle, and Constrained Optimization

Lecture 2. Marginal Functions, Average Functions, Elasticity, the Marginal Principle, and Constrained Optimization 2.1. Introduction Suppose that an economic relationship can be described by a real-valued

Lecture 2. Marginal Functions, Average Functions, Elasticity, the Marginal Principle, and Constrained Optimization 2.1. Introduction Suppose that an economic relationship can be described by a real-valued

We will study the extreme case of perfect competition, where firms are price takers.

Perfectly Competitive Markets A firm s decision about how much to produce or what price to charge depends on how competitive the market structure is. If the Cincinnati Bengals raise their ticket prices

Perfectly Competitive Markets A firm s decision about how much to produce or what price to charge depends on how competitive the market structure is. If the Cincinnati Bengals raise their ticket prices

Pure Competition urely competitive markets are used as the benchmark to evaluate market

R. Larry Reynolds Pure Competition urely competitive markets are used as the benchmark to evaluate market P performance. It is generally believed that market structure influences the behavior and performance

R. Larry Reynolds Pure Competition urely competitive markets are used as the benchmark to evaluate market P performance. It is generally believed that market structure influences the behavior and performance

Key Concepts and Skills. Credit and Receivables. Components of Credit Policy

Key Concepts and Skills Understand the key issues related to credit management Understand the impact of cash discounts Be able to evaluate a proposed credit policy Understand the components of credit analysis

Key Concepts and Skills Understand the key issues related to credit management Understand the impact of cash discounts Be able to evaluate a proposed credit policy Understand the components of credit analysis

At the end of Chapter 18, you should be able to answer the following:

1 How to Study for Chapter 18 Pure Monopoly Chapter 18 considers the opposite of perfect competition --- pure monopoly. 1. Begin by looking over the Objectives listed below. This will tell you the main

1 How to Study for Chapter 18 Pure Monopoly Chapter 18 considers the opposite of perfect competition --- pure monopoly. 1. Begin by looking over the Objectives listed below. This will tell you the main

MPP 801 Monopoly Kevin Wainwright Study Questions

MPP 801 Monopoly Kevin Wainwright Study Questions MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) The marginal revenue facing a monopolist A) is

MPP 801 Monopoly Kevin Wainwright Study Questions MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) The marginal revenue facing a monopolist A) is

Thus MR(Q) = P (Q) Q P (Q 1) (Q 1) < P (Q) Q P (Q) (Q 1) = P (Q), since P (Q 1) > P (Q).

= P (Q) Q P (Q 1) (Q 1) < P (Q) Q P (Q) (Q 1) = P (Q), since P (Q 1) > P (Q).") A monopolist s marginal revenue is always less than or equal to the price of the good. Marginal revenue is the amount of revenue the firm receives for each additional unit of output. It is the difference

A monopolist s marginal revenue is always less than or equal to the price of the good. Marginal revenue is the amount of revenue the firm receives for each additional unit of output. It is the difference

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question on the accompanying scantron.

Principles of Microeconomics Fall 2007, Quiz #6 Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question on the accompanying scantron. 1) A monopoly is

Principles of Microeconomics Fall 2007, Quiz #6 Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question on the accompanying scantron. 1) A monopoly is

Elasticities of Demand

rice Elasticity of Demand 4.0 rinciples of Microeconomics, Fall 007 Chia-Hui Chen September 0, 007 Lecture 3 Elasticities of Demand Elasticity. Elasticity measures how one variable responds to a change

rice Elasticity of Demand 4.0 rinciples of Microeconomics, Fall 007 Chia-Hui Chen September 0, 007 Lecture 3 Elasticities of Demand Elasticity. Elasticity measures how one variable responds to a change

Demand, Supply and Elasticity

Demand, Supply and Elasticity CHAPTER 2 OUTLINE 2.1 Demand and Supply Definitions, Determinants and Disturbances 2.2 The Market Mechanism 2.3 Changes in Market Equilibrium 2.4 Elasticities of Supply and

Demand, Supply and Elasticity CHAPTER 2 OUTLINE 2.1 Demand and Supply Definitions, Determinants and Disturbances 2.2 The Market Mechanism 2.3 Changes in Market Equilibrium 2.4 Elasticities of Supply and

http://ezto.mhecloud.mcgraw-hill.com/hm.tpx

Page 1 of 17 1. Assume the price elasticity of demand for U.S. Frisbee Co. Frisbees is 0.5. If the company increases the price of each Frisbee from $12 to $16, the number of Frisbees demanded will Decrease

Page 1 of 17 1. Assume the price elasticity of demand for U.S. Frisbee Co. Frisbees is 0.5. If the company increases the price of each Frisbee from $12 to $16, the number of Frisbees demanded will Decrease

Chapter 9: Perfect Competition

Chapter 9: Perfect Competition Perfect Competition Law of One Price Short-Run Equilibrium Long-Run Equilibrium Maximize Profit Market Equilibrium Constant- Cost Industry Increasing- Cost Industry Decreasing-

Chapter 9: Perfect Competition Perfect Competition Law of One Price Short-Run Equilibrium Long-Run Equilibrium Maximize Profit Market Equilibrium Constant- Cost Industry Increasing- Cost Industry Decreasing-

CHAPTER 10 MARKET POWER: MONOPOLY AND MONOPSONY

CHAPTER 10 MARKET POWER: MONOPOLY AND MONOPSONY EXERCISES 3. A monopolist firm faces a demand with constant elasticity of -.0. It has a constant marginal cost of $0 per unit and sets a price to maximize

CHAPTER 10 MARKET POWER: MONOPOLY AND MONOPSONY EXERCISES 3. A monopolist firm faces a demand with constant elasticity of -.0. It has a constant marginal cost of $0 per unit and sets a price to maximize

Why is Insurance Good? An Example Jon Bakija, Williams College (Revised October 2013)

") Why is Insurance Good? An Example Jon Bakija, Williams College (Revised October 2013) Introduction The United States government is, to a rough approximation, an insurance company with an army. 1 That is

Why is Insurance Good? An Example Jon Bakija, Williams College (Revised October 2013) Introduction The United States government is, to a rough approximation, an insurance company with an army. 1 That is

Figure: Computing Monopoly Profit

Name: Date: 1. Most electric, gas, and water companies are examples of: A) unregulated monopolies. B) natural monopolies. C) restricted-input monopolies. D) sunk-cost monopolies. Use the following to answer

Name: Date: 1. Most electric, gas, and water companies are examples of: A) unregulated monopolies. B) natural monopolies. C) restricted-input monopolies. D) sunk-cost monopolies. Use the following to answer

Elasticity. I. What is Elasticity?

Elasticity I. What is Elasticity? The purpose of this section is to develop some general rules about elasticity, which may them be applied to the four different specific types of elasticity discussed in

Elasticity I. What is Elasticity? The purpose of this section is to develop some general rules about elasticity, which may them be applied to the four different specific types of elasticity discussed in

4. Market Structures. Learning Objectives 4-63. Market Structures

1. Supply and Demand: Introduction 3 2. Supply and Demand: Consumer Demand 33 3. Supply and Demand: Company Analysis 43 4. Market Structures 63 5. Key Formulas 81 2014 Allen Resources, Inc. All rights

1. Supply and Demand: Introduction 3 2. Supply and Demand: Consumer Demand 33 3. Supply and Demand: Company Analysis 43 4. Market Structures 63 5. Key Formulas 81 2014 Allen Resources, Inc. All rights

Elasticities of Demand and Supply

1 CHAPTER CHECKLIST Elasticities of Demand and Supply Chapter 5 1. Define, explain the factors that influence, and calculate the price elasticity of demand. 2. Define, explain the factors that influence,

1 CHAPTER CHECKLIST Elasticities of Demand and Supply Chapter 5 1. Define, explain the factors that influence, and calculate the price elasticity of demand. 2. Define, explain the factors that influence,

A Detailed Price Discrimination Example

A Detailed Price Discrimination Example Suppose that there are two different types of customers for a monopolist s product. Customers of type 1 have demand curves as follows. These demand curves include

A Detailed Price Discrimination Example Suppose that there are two different types of customers for a monopolist s product. Customers of type 1 have demand curves as follows. These demand curves include

CHAPTER 11 DECISION MAKING AND RELEVANT INFORMATION

CHAPTER 11 DECISION MAKING AND RELEVANT INFORMATION 11-28 Equipment upgrade versus replacement. 1. Based on the analysis in the table below, TechGuide will be better off by $337,500 over three years if

CHAPTER 11 DECISION MAKING AND RELEVANT INFORMATION 11-28 Equipment upgrade versus replacement. 1. Based on the analysis in the table below, TechGuide will be better off by $337,500 over three years if

CHAPTER 11 PRICE AND OUTPUT IN MONOPOLY, MONOPOLISTIC COMPETITION, AND PERFECT COMPETITION

CHAPTER 11 PRICE AND OUTPUT IN MONOPOLY, MONOPOLISTIC COMPETITION, AND PERFECT COMPETITION Chapter in a Nutshell Now that we understand the characteristics of different market structures, we ask the question

CHAPTER 11 PRICE AND OUTPUT IN MONOPOLY, MONOPOLISTIC COMPETITION, AND PERFECT COMPETITION Chapter in a Nutshell Now that we understand the characteristics of different market structures, we ask the question

Profit maximization in different market structures

Profit maximization in different market structures In the cappuccino problem as well in your team project, demand is clearly downward sloping if the store wants to sell more drink, it has to lower the

Profit maximization in different market structures In the cappuccino problem as well in your team project, demand is clearly downward sloping if the store wants to sell more drink, it has to lower the

CHAPTER 8 PROFIT MAXIMIZATION AND COMPETITIVE SUPPLY

CHAPTER 8 PROFIT MAXIMIZATION AND COMPETITIVE SUPPLY TEACHING NOTES This chapter begins by explaining what we mean by a competitive market and why it makes sense to assume that firms try to maximize profit.

CHAPTER 8 PROFIT MAXIMIZATION AND COMPETITIVE SUPPLY TEACHING NOTES This chapter begins by explaining what we mean by a competitive market and why it makes sense to assume that firms try to maximize profit.

CPD Spotlight Quiz September 2012. Working Capital

CPD Spotlight Quiz September 2012 Working Capital 1 What is working capital? This is a topic that has been the subject of debate for many years and will, no doubt, continue to be so. One response to the

CPD Spotlight Quiz September 2012 Working Capital 1 What is working capital? This is a topic that has been the subject of debate for many years and will, no doubt, continue to be so. One response to the

Aggressive Advertisement. Normal Advertisement Aggressive Advertisement. Normal Advertisement

Professor Scholz Posted: 11/10/2009 Economics 101, Problem Set #9, brief answers Due: 11/17/2009 Oligopoly and Monopolistic Competition Please SHOW your work and, if you have room, do the assignment on

Professor Scholz Posted: 11/10/2009 Economics 101, Problem Set #9, brief answers Due: 11/17/2009 Oligopoly and Monopolistic Competition Please SHOW your work and, if you have room, do the assignment on

Health Economics. University of Linz & Demand and supply of health insurance. Gerald J. Pruckner. Lecture Notes, Summer Term 2010

Health Economics Demand and supply of health insurance University of Linz & Gerald J. Pruckner Lecture Notes, Summer Term 2010 Gerald J. Pruckner Health insurance 1 / 25 Introduction Insurance plays a

Health Economics Demand and supply of health insurance University of Linz & Gerald J. Pruckner Lecture Notes, Summer Term 2010 Gerald J. Pruckner Health insurance 1 / 25 Introduction Insurance plays a

Chapter 3 Quantitative Demand Analysis

Managerial Economics & Business Strategy Chapter 3 uantitative Demand Analysis McGraw-Hill/Irwin Copyright 2010 by the McGraw-Hill Companies, Inc. All rights reserved. Overview I. The Elasticity Concept

Managerial Economics & Business Strategy Chapter 3 uantitative Demand Analysis McGraw-Hill/Irwin Copyright 2010 by the McGraw-Hill Companies, Inc. All rights reserved. Overview I. The Elasticity Concept

Final Exam (Version 1) Answers

Answers") Final Exam Economics 101 Fall 2003 Wallace Final Exam (Version 1) Answers 1. The marginal revenue product equals A) total revenue divided by total product (output). B) marginal revenue divided by marginal

Final Exam Economics 101 Fall 2003 Wallace Final Exam (Version 1) Answers 1. The marginal revenue product equals A) total revenue divided by total product (output). B) marginal revenue divided by marginal

QE1: Economics Notes 1

QE1: Economics Notes 1 Box 1: The Household and Consumer Welfare The final basket of goods that is chosen are determined by three factors: a. Income b. Price c. Preferences Substitution Effect: change

QE1: Economics Notes 1 Box 1: The Household and Consumer Welfare The final basket of goods that is chosen are determined by three factors: a. Income b. Price c. Preferences Substitution Effect: change

SECOND-DEGREE PRICE DISCRIMINATION

SECOND-DEGREE PRICE DISCRIMINATION FIRST Degree: The firm knows that it faces different individuals with different demand functions and furthermore the firm can tell who is who. In this case the firm extracts

SECOND-DEGREE PRICE DISCRIMINATION FIRST Degree: The firm knows that it faces different individuals with different demand functions and furthermore the firm can tell who is who. In this case the firm extracts

Employment and Pricing of Inputs

Employment and Pricing of Inputs Previously we studied the factors that determine the output and price of goods. In chapters 16 and 17, we will focus on the factors that determine the employment level

Employment and Pricing of Inputs Previously we studied the factors that determine the output and price of goods. In chapters 16 and 17, we will focus on the factors that determine the employment level

D) Marginal revenue is the rate at which total revenue changes with respect to changes in output.

Marginal revenue is the rate at which total revenue changes with respect to changes in output.") Ch. 9 1. Which of the following is not an assumption of a perfectly competitive market? A) Fragmented industry B) Differentiated product C) Perfect information D) Equal access to resources 2. Which of

Ch. 9 1. Which of the following is not an assumption of a perfectly competitive market? A) Fragmented industry B) Differentiated product C) Perfect information D) Equal access to resources 2. Which of

2.5 Monetary policy: Interest rates

2.5 Monetary policy: Interest rates Learning Outcomes Describe the role of central banks as regulators of commercial banks and bankers to governments. Explain that central banks are usually made responsible

2.5 Monetary policy: Interest rates Learning Outcomes Describe the role of central banks as regulators of commercial banks and bankers to governments. Explain that central banks are usually made responsible

Pricing Products and Services

Pricing Products and Services Pricing products and services is a challenging process f most new home-based business owners. Often entrepreneurs will underestimate the value of their time and expertise

Pricing Products and Services Pricing products and services is a challenging process f most new home-based business owners. Often entrepreneurs will underestimate the value of their time and expertise

Chapter 7 Monopoly, Oligopoly and Strategy

Chapter 7 Monopoly, Oligopoly and Strategy After reading Chapter 7, MONOPOLY, OLIGOPOLY AND STRATEGY, you should be able to: Define the characteristics of Monopoly and Oligopoly, and explain why the are

Chapter 7 Monopoly, Oligopoly and Strategy After reading Chapter 7, MONOPOLY, OLIGOPOLY AND STRATEGY, you should be able to: Define the characteristics of Monopoly and Oligopoly, and explain why the are

17. In class Edward discussed one way to reduce health-care costs is to increases the supply of doctors. A) True B) False

True B) False") Economics 2010 Sec 300 Second Midterm Fall 2009 Version B There are 58 questions on Version B The test bank questions and the questions we created are mixed together. Name: Date: 1. Lot of people exercise

Economics 2010 Sec 300 Second Midterm Fall 2009 Version B There are 58 questions on Version B The test bank questions and the questions we created are mixed together. Name: Date: 1. Lot of people exercise

An increase in the number of students attending college. shifts to the left. An increase in the wage rate of refinery workers.

1. Which of the following would shift the demand curve for new textbooks to the right? a. A fall in the price of paper used in publishing texts. b. A fall in the price of equivalent used text books. c.

1. Which of the following would shift the demand curve for new textbooks to the right? a. A fall in the price of paper used in publishing texts. b. A fall in the price of equivalent used text books. c.

Chapter 04 Firm Production, Cost, and Revenue

Chapter 04 Firm Production, Cost, and Revenue Multiple Choice Questions 1. A key assumption about the way firms behave is that they a. Minimize costs B. Maximize profit c. Maximize market share d. Maximize

Chapter 04 Firm Production, Cost, and Revenue Multiple Choice Questions 1. A key assumption about the way firms behave is that they a. Minimize costs B. Maximize profit c. Maximize market share d. Maximize

Chapter 4: Elasticity

Chapter : Elasticity Elasticity of eman: It measures the responsiveness of quantity emane (or eman) with respect to changes in its own price (or income or the price of some other commoity). Why is Elasticity

Chapter : Elasticity Elasticity of eman: It measures the responsiveness of quantity emane (or eman) with respect to changes in its own price (or income or the price of some other commoity). Why is Elasticity

INTRODUCTORY MICROECONOMICS

INTRODUCTORY MICROECONOMICS UNIT-I PRODUCTION POSSIBILITIES CURVE The production possibilities (PP) curve is a graphical medium of highlighting the central problem of 'what to produce'. To decide what

INTRODUCTORY MICROECONOMICS UNIT-I PRODUCTION POSSIBILITIES CURVE The production possibilities (PP) curve is a graphical medium of highlighting the central problem of 'what to produce'. To decide what

Name Eco200: Practice Test 2 Covering Chapters 10 through 15

Name Eco200: Practice Test 2 Covering Chapters 10 through 15 1. Four roommates are planning to spend the weekend in their dorm room watching old movies, and they are debating how many to watch. Here is

Name Eco200: Practice Test 2 Covering Chapters 10 through 15 1. Four roommates are planning to spend the weekend in their dorm room watching old movies, and they are debating how many to watch. Here is

Long Run Supply and the Analysis of Competitive Markets. 1 Long Run Competitive Equilibrium

Long Run Competitive Equilibrium. rinciples of Microeconomics, Fall 7 Chia-Hui Chen October 9, 7 Lecture 6 Long Run Supply and the Analysis of Competitive Markets Outline. Chap 8: Long Run Equilibrium.

Long Run Competitive Equilibrium. rinciples of Microeconomics, Fall 7 Chia-Hui Chen October 9, 7 Lecture 6 Long Run Supply and the Analysis of Competitive Markets Outline. Chap 8: Long Run Equilibrium.

Profit Maximization. PowerPoint Slides prepared by: Andreea CHIRITESCU Eastern Illinois University

Profit Maximization PowerPoint Slides prepared by: Andreea CHIRITESCU Eastern Illinois University 1 The Nature and Behavior of Firms A firm An association of individuals Firms Who have organized themselves

Profit Maximization PowerPoint Slides prepared by: Andreea CHIRITESCU Eastern Illinois University 1 The Nature and Behavior of Firms A firm An association of individuals Firms Who have organized themselves

Monopoly and Monopsony Labor Market Behavior

Monopoly and Monopsony abor Market Behavior 1 Introduction For the purposes of this handout, let s assume that firms operate in just two markets: the market for their product where they are a seller) and

Monopoly and Monopsony abor Market Behavior 1 Introduction For the purposes of this handout, let s assume that firms operate in just two markets: the market for their product where they are a seller) and