BUSINESS PLAN ABC TAXI SERVICE INC.

|

|

|

- Aleesha Nichols

- 8 years ago

- Views:

Transcription

1 BUSINESS PLAN ABC TAXI SERVICE INC.

2 Confidentiality Agreement The undersigned reader acknowledges that the information provided by in this business plan is confidential; therefore, reader agrees not to disclose it without the express written permission of. It is acknowledged by reader that information to be furnished in this business plan is in all respects confidential in nature, other than information which is in the public domain through other means and that any disclosure or use of same by reader, may cause serious harm or damage to. Upon request, this document is to be immediately returned to. Signature Name (typed or printed) Date This is a business plan. It does not imply an offering of securities.

3 Table of Contents 1.0 Executive Summary Mission...1 Chart: Highlights Objectives Company Summary Company Ownership Start-up Summary...3 Table: Start-up...3 Table: Start-up Funding...4 Chart: Start-up Services Market Analysis Summary Market Segmentation...5 Table: Market Analysis...6 Chart: Market Analysis (Pie) Target Market Segment Strategy Competition and Buying Patterns Strategy and Implementation Summary Sales Strategy Sales Forecast...8 Chart: Sales Monthly...9 Chart: Sales by Year...9 Table: Sales Forecast Competitive Edge Milestones...10 Table: Milestones Management Summary Personnel Plan...11 Table: Personnel Financial Plan Important Assumptions...11 Table: General Assumptions Break-even Analysis...12 Chart: Break-even Analysis...12 Table: Break-even Analysis Projected Profit and Loss...13 Table: Profit and Loss Projected Balance Sheet...14 Table: Balance Sheet Projected Cash Flow...15 Table: Cash Flow...15 Chart: Cash Business Ratios...16 Table: Ratios...17 Table: Sales Forecast...1 Table: Personnel...2 Table: General Assumptions...3 Page 1

4 Table of Contents Table: Profit and Loss...4 Table: Cash Flow...5 Table: Balance Sheet...6 Page 2

5 1.0 Executive Summary ABC Taxi Service Inc is a Toronto-based taxi service. ABCTSI provides limousine like service without the typical high limousine price. Although ABCTSI cars are not true stretch limousines, they are late model high-end luxury vehicles. ABCTSI is lead by Mohammed Hakim Zadah, a transportation industry veteran. ABCTSI has forecasted sales of $611,890 by year three PLUS MEMBERSHIPS AND DISPATCH FEES The Market and Services Offered The market is a large one with over 1.5 million potential customers The Competitive Edge ABCTSI recognizes that their key to success will be providing unmatched customer service. ABCTSI has infused the importance of customer service into the drivers' jobs by offering financial incentives to the drivers for superior service. This will ensure that the best customer service will be offered at every level and interaction with the company. Management Team ABCTSI was founded and is run by Mohammed Hakim Zadah. Mohammed began his transportation career as a taxi driver. Mohammed's logistics and customer service experience will be essential to the success of ABCTSI. The logistics experience will provide ABCTSI with hyper-efficient operations and the customer service experience will support their competitive edge. 1.1 Mission The Mission of ABC Taxi Servive Inc (ABCTSI) is to provide the customer the finest transportation service available. We exist to attract and maintain customers. When we adhere to this maxim, everything else will fall in to place. Our services will exceed the expectations of our customers. ABCTSI mission is to establish a universal licensing plan to be held only by owner operators. To have all or most of the taxi drivers under one main umbrella whereby they pay an annual membership fee and monthly dispatch fee to one orginazation. The drivers will by a mutal agreement between the management of ABCTSI and all the members, share in the profits of the corporation. Page 1

6 1.2 Objectives The objectives for the first three years of operation include: 1. To create a service-based company whose primary goal is to exceed customer's expectations. 2. To increase customers by 20% per year through superior performance and word-ofmouth referrals. 3. To develop a sustainable Taxi company serving the GTA 4. To establish the only company in which it's members share in the profits 5. To establish with the help of the Toronto government a Universal License for owner operators 2.0 Company Summary ABCTSI offers a general taxi service for the GTA. ABCTSI will offer their service 24 hours a day to most neighborhoods in the GTA. ABCTSI will be priced less than a limousine service but more than a group shuttle service. Mohammed Hakim Zadah will be working full time as the Manager and have four other employees. 2.1 Company Ownership ABCTSI is an Ontario corporation founded and owned by Mohammed Hakim Zadah. Page 2

7 2.2 Start-up Summary Table: Start-up Start-up Requirements Start-up Expenses Legal $0 Stationery etc. $0 Insurance $0 Rent $0 Computer $0 Other $0 Total Start-up Expenses $0 Start-up Assets Cash Required $0 Other Current Assets $0 Long-term Assets $0 Total Assets $0 Total Requirements $0 Page 3

8 Table: Start-up Funding Start-up Funding Start-up Expenses to Fund $0 Start-up Assets to Fund $0 Total Funding Required $0 Assets Non-cash Assets from Start-up $0 Cash Requirements from Start-up $0 Additional Cash Raised $35,000 Cash Balance on Starting Date $35,000 Total Assets $35,000 Liabilities and Capital Liabilities Current Borrowing $0 Long-term Liabilities $0 Accounts Payable (Outstanding Bills) $0 Other Current Liabilities (interest-free) $0 Total Liabilities $0 Capital Planned Investment Investor 1 $35,000 Other $0 Additional Investment Requirement $0 Total Planned Investment $35,000 Loss at Start-up (Start-up Expenses) $0 Total Capital $35,000 Total Capital and Liabilities $35,000 Total Funding $35,000 Page 4

$0 Total Capital $35,000 Total Capital and Liabilities $35,000 Total")

9 3.0 Services ABCTSI provides a general Taxi and Airport transportation solution for the GTA. ABCTSI can provide airport travel on short notice if cars are available, but they generally work with a reservation system. A customer would call up in advance and provide ABCTSI with flight information. ABCTSI would schedule the pick up time and then call and send an to confirm the pickup. For pick up at the airport, ABCTSI would meet the customer outside of baggage claim after the customer has picked up their luggage and would drive them home. 4.0 Market Analysis Summary ABCTSI will be focusing on families as well as business travelers. Both groups will likely demand our services. The families will utilize our service because it is convenient and less expensive than if they drove themselves and paid for long-term parking of their car. Business travelers will use our service because it offers a limousine-like service (other than the fact that ABCTSI does not use limousines) where the traveler has a ride waiting for them when their planes comes in, but the service is less expensive than normal limousine services. Since the service is fairly comparable to a louisine service, companies will encourage their workers to utilize ABCTSI as a cost saving measure, particularly in this economic downturn. 4.1 Market Segmentation Our customers can be divided into two groups: families/individuals on pleasure trips, and business travelers. Page 5

10 The first group is taking a trip for pleasure and will either be an individual or a family. Their choices are to either drive and park in long term parking, take a taxi, or use a limousine service. This group does not typically mind paying a bit more for a solution that takes care of their transportation to and from the airport. Since they are are on vacation, they appreciate having a service that gets them to the airport in a seamless way so they do not have to worry about anything. All they have to do is make the reservation and show up at the arranged pickup point. The second group is the business traveler. In the past a company would typically hire a limousine service to pick up their worker. The company would always pay for the service. With ABCTSI as an alternative, there is a transportation service that functions like a limousine (you can preschedule pickup dates and be taken directly home or to the airport) but without the overly fancy car and the associated high price. As companies are always looking at ways to cut costs, ABCTSI offers a very reasonable solution in terms of comfort and cost. The business traveler will not notice anything different with ABCTSI versus a limo service other than the vehicle they are traveling won't be a limo, but will still be a sufficiently large and comfortable car. Table: Market Analysis Market Analysis Potential Customers Growth CAGR Individual/families 9% 578, , , , , % Business travelers 8% 425, , , , , % Total 8.58% 1,003,000 1,089,020 1,182,442 1,283,905 1,394, % 4.2 Target Market Segment Strategy ABCTSI will be targeting these two groups because they consistently travel, and ABCTSI solution makes traveling easy for them. While a slow economy has some effect on travel. In general north Americans tend to travel more each year, this trend beginning in the early 1980s. These Page 6

11 groups are particularly attractive to ABCTSI because they will always need to get to the airport and they are willing to pay a bit extra for the luxury of having someone take them there instead of being required to get themselves there. Please note, however, ABCTSI is only slightly more expensive for trips under four days; over four days it is more cost effective to use ABCTSI. Compared to driving a personal vehicle and paying for long-term parking. In regard to the business customers, it is generally accepted practice for the company to provide the transportation for their employees. For trips over four days, there is no question that ABCTSI is more cost effective. Under four days ABCTSI service is slightly more expensive than driving oneself and parking, however, companies are more than willing to pay a bit extra as their employee is giving up a decent amount of their free time to go on the trip for work and the business recognizes and appreciates this. Of course for the companies already willing to pay limousine prices, ABCTSI will appear as a way of reducing travel costs with no appreciable loss in service quality. 4.3 Competition and Buying Patterns Currently in Toronto there are several competing Taxi and airport transportation systems: 1. Public transportation: TTC provides rapid transit service to the airport. While this is an inexpensive alternative there are several disadvantages. The service does not run all hours of the night. 2. Taxi service: Taxis do provide service to and from the airport, however, travelers cannot book the trip in advance, forcing them to call right before they want to travel. The level of service is inconsistent from taxi service to taxi service as well as from occasion to occasion. Taxis can also be quite expensive if city dwellers are going out to the suburbs. 3. Airport parking: Airport parking can be cost effective if it is for fewer than four days. Driving oneself has the advantage of not having to deal with anyone else, the flip side to this however is they must do everything for themselves. Lastly, there is always the risk of damage to their car when it is parked and all airport parking facilities have drivers sign a waiver absolving the lot from responsibility if anything happens to the car. 4. Shuttle service: This option packs a few different people into a van and takes them to the airport. This is a less expensive option, however, it takes longer to make the commute due to the other customers that are traveling Additionally, travelers lose out on the personalized service relative to ABCTSI or a limousine service. The buying patterns of these services vary based on the length of the trip, who is paying for it, and if it is a last minute or planned in advance trip. The longer the trip, the more economical a transportation option is relative to airport parking. A large percentage of business travelers use an upscale airport transportation solution like ABCTSI or a limousine service for their employees. People who are just scraping by to go on vacation are likely to choose the least costly option, public transportation. Lastly, if the trip is planned at the last minute, taxi service might be the only option however, ABCTSI will offer last minute rides if cars are available. 5.0 Strategy and Implementation Summary ABCTSI's marketing/sales strategy will be two pronged, one to address each of our two segmented targeted groups: 1. Families/individuals: In addition to some advertising, we will be working with associations such as CAA and other community groups to try to build up a network of users.abctsi believes that working with these groups will provide us with steady flow of Page 7

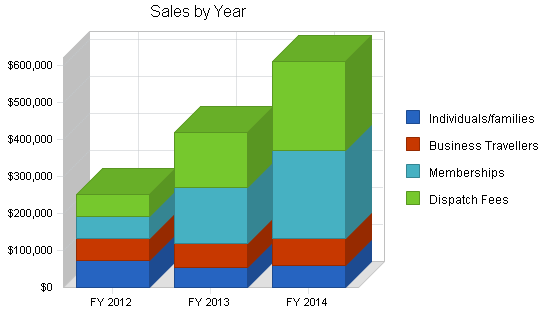

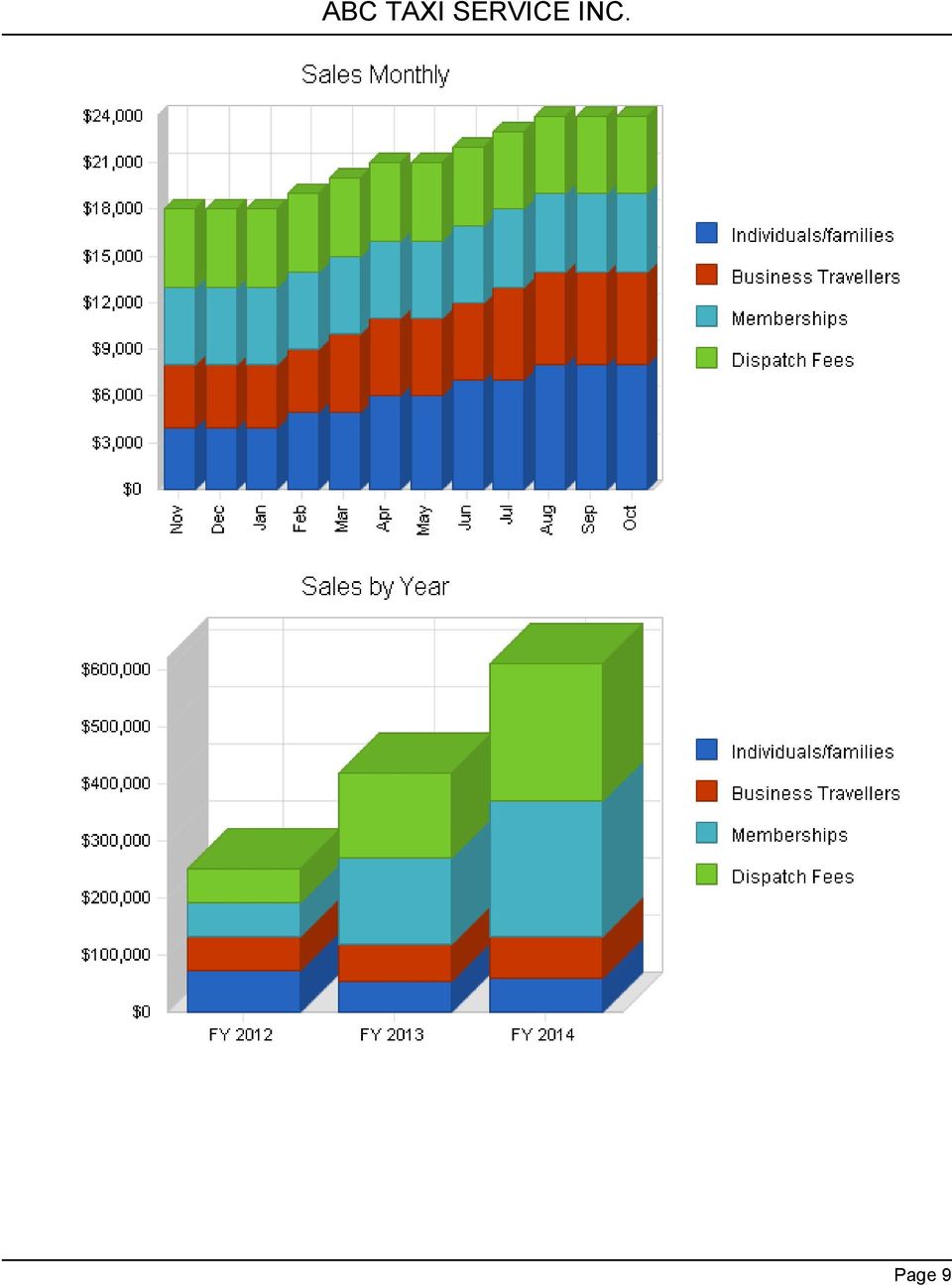

12 customers. Additionally, since a lot of these groups have close knit among member referrals will be quite powerful when they are coming from a member who already has established a trust bond with other organizational members. 2. Business travelers: ABCTSI will be contacting the travel department of many of the different companies in Toronto that have a lot of employees traveling and informing them about our service and offering them an introductory discount. This will be an important segment to win over as companies routinely have employees traveling throughout the year. Businesses are also valuable because once the initial contact is made, the relationship can be turned into a steady stream of business. 5.1 Sales Strategy As stated earlier, we will be going after both families/individuals as well as business travelers. ABCTSI will have a different strategy for each group. For the individuals, ABCTSI will use contacts through membership associations and clubs to build customers. Customers that are a part of an association tend to put more trust in a service provider when the service provider is aligned with the association. ABCTSI will offer a discount for the association members to try to build up a following. Our selling spiel will be total convenience at a cost that is competitive with the price that they currently pay when they leave their car in the parking lot. Offering the ability to schedule in advance pick up from home and then pick up from airport should be a big selling point. People like convenience, and people are willing to pay for conveniences. One phone call to arrange all of your transport needs to the airport is quite a convenience. Our strategy of wooing the business travelers will be a campaign to introduce ABCTSI to the different travel departments of the larger companies in the area. The initial contact will be a letter/brochure describing our services along with a pricing guide. ABCTSI will then follow that up with a phone call to try to receive a commitment from the company. By including the pricing information within the brochure, ABCTSI believes that this will catch the eyes of the companies' travel departments as they are acutely aware of the costs that they are paying now and ABCTSI believes that they can convert the lead into a customer by offering essentially the same service of a limo company at a reduced rate Sales Forecast The first month will be spent setting up the business. It is unlikely that everything will be ready to go so that we could begin to take fares. By month two the business office will be in order, brochures will have been sent out and ABCTSI will have been working with associations to create visibility for the company. ABCTSI will have two drivers and will be paying a base monthly wage on the assumption that ABCTSI wants to have the drivers ready when fares come up but there is not likely to be enough fares to support the wages of the two drivers. Page 8

13 Page 9

14 Table: Sales Forecast Sales Forecast FY 2012 FY 2013 FY 2014 Sales Individuals/families $72,000 $53,900 $59,290 Business Travellers $60,000 $66,000 $72,600 Memberships $60,000 $150,000 $240,000 Dispatch Fees $60,000 $150,000 $240,000 Total Sales $252,000 $419,900 $611,890 Direct Cost of Sales FY 2012 FY 2013 FY 2014 Individuals/families $22,050 $24,255 $26,681 Business travelers $27,000 $29,700 $32,670 Subtotal Direct Cost of Sales $49,050 $53,955 $59, Competitive Edge ABCTSI competitive advantage will be based on an incentive system that rewards the drivers/ members economically when they achieve good service, develop repeat customers and act in a team fashion instead of competing against other company drivers. This incentive system will reward drivers when: 1. The company receives positive feedback about the driver (a feedback system will be set up). 2. The customer is turned into a repeat customer. 3. The driver develops new customers. 4. The driver acts in manners that are team based instead of for individual gain. Through this complicated but purposeful system, ABCTSI is incentivizing behavior that they believe will help the company succeed, while not rewarding behavior that is destructive to the company. 5.3 Milestones ABCTSI will have several milestones to aim for: 1. Business plan completion. This will be done as a road map for the organization. While we do not need a business plan to raise capital, it will be an indispensable tool for the ongoing performance and improvement of the company. 2. Set up office. 3. Profitability. 4. Bringing on board the fourth driver. 5. Establish the universal license 6. Attract 300 members in the first year and 800 by year three Page 10

15 Table: Milestones Milestones Milestone Start Date End Date Budget Manager Department Business plan completion 31/10/ /11/2011 $0 ABC Department Set up office 31/10/ /11/2011 $0 ABC Department Profitability 31/10/ /11/2011 $0 ABC Department Fourth drive hired 31/10/ /11/2011 $0 ABC Department Totals $0 6.0 Management Summary ABC Taxi Service Inc. is owned and operated by Mohammed Hakim Zadah. He has over 15 years experiance in the taxi service industry. 6.1 Personnel Plan The staff will consist of Mohammed working full time in the back office. Mohammed will be responsible for setting up the appointments as well as the marketing to develop customers. By month two, Mohammed will be bringing on board a part-time employee to help him out in answering the phones and setting up appointments for fares. Month two will also bring two drivers to ABCTSI. The head count will remain the same until month five when a third driver will be brought on board. Lastly, month 11 will see a fourth driver brought on board. Table: Personnel Personnel Plan FY 2012 FY 2013 FY 2014 Mohammed $36,000 $36,000 $36,000 Part-time employee $8,800 $16,500 $16,500 Driver $20,600 $21,600 $21,600 Total People Total Payroll $65,400 $74,100 $74, Financial Plan The following sections will detail important financial information. 7.1 Important Assumptions The following table highlights some of the important financial assumptions for ABCTSI. Page 11

16 Table: General Assumptions ABC TAXI SERVICE INC. General Assumptions FY 2012 FY 2013 FY 2014 Plan Month Current Interest Rate 8.00% 8.00% 8.00% Long-term Interest Rate 8.00% 8.00% 8.00% Tax Rate 18.00% 18.00% 18.00% Other Break-even Analysis The Break-even Analysis indicates that ABCTSI must have $15,016 in revenue to break even. Table: Break-even Analysis Break-even Analysis Monthly Revenue Break-even $16,101 Assumptions: Average Percent Variable Cost 19% Estimated Monthly Fixed Cost $12,967 Page 12

17 7.3 Projected Profit and Loss The following table will indicate projected profit and loss. Table: Profit and Loss Pro Forma Profit and Loss FY 2012 FY 2013 FY 2014 Sales $252,000 $419,900 $611,890 Direct Cost of Sales $49,050 $53,955 $59,351 Other $0 $0 $0 Total Cost of Sales $49,050 $53,955 $59,351 Gross Margin $202,950 $365,945 $552,539 Gross Margin % 80.54% 87.15% 90.30% Expenses Payroll $65,400 $74,100 $74,100 Sales and Marketing and Other Expenses $3,100 $3,600 $3,600 Depreciation $28,500 $51,300 $41,040 Web site maintenance $600 $600 $600 Utilities $1,200 $1,200 $1,200 Insurance $5,400 $5,400 $5,400 Rent $6,000 $6,000 $6,000 Payroll Taxes $5,400 $5,800 $6,000 Members profit allocation $40,000 $100,000 $160,000 Total Operating Expenses $155,600 $248,000 $297,940 Profit Before Interest and Taxes $47,350 $117,945 $254,599 EBITDA $75,850 $169,245 $295,639 Interest Expense $21,920 $20,080 $18,160 Taxes Incurred $4,577 $17,616 $42,559 Net Profit $20,853 $80,249 $193,880 Net Profit/Sales 8.27% 19.11% 31.69% Page 13

18 7.4 Projected Balance Sheet The following table will indicate the projected balance sheet. Table: Balance Sheet Pro Forma Balance Sheet Assets FY 2012 FY 2013 FY 2014 Current Assets Cash $143,628 $227,512 $445,715 Other Current Assets $0 $0 $0 Total Current Assets $143,628 $227,512 $445,715 Long-term Assets Long-term Assets $285,000 $285,000 $285,000 Accumulated Depreciation $28,500 $79,800 $120,840 Total Long-term Assets $256,500 $205,200 $164,160 Total Assets $400,128 $432,712 $609,875 Liabilities and Capital FY 2012 FY 2013 FY 2014 Current Liabilities Accounts Payable $41,275 $17,610 $24,893 Current Borrowing $263,000 $239,000 $215,000 Other Current Liabilities $40,000 $40,000 $40,000 Subtotal Current Liabilities $344,275 $296,610 $279,893 Long-term Liabilities $0 $0 $0 Total Liabilities $344,275 $296,610 $279,893 Paid-in Capital $35,000 $35,000 $35,000 Retained Earnings $0 $20,853 $101,102 Earnings $20,853 $80,249 $193,880 Total Capital $55,853 $136,102 $329,982 Total Liabilities and Capital $400,128 $432,712 $609,875 Net Worth $55,853 $136,102 $329,982 Page 14

19 7.5 Projected Cash Flow The following chart and table will indicate projected cash flow. Table: Cash Flow Pro Forma Cash Flow Cash Received FY 2012 FY 2013 FY 2014 Cash from Operations Cash Sales $252,000 $419,900 $611,890 Subtotal Cash from Operations $252,000 $419,900 $611,890 Additional Cash Received Sales Tax, VAT, HST/GST Received $0 $0 $0 New Current Borrowing $285,000 $0 $0 New Other Liabilities (interest-free) $40,000 $0 $0 New Long-term Liabilities $0 $0 $0 Sales of Other Current Assets $0 $0 $0 Sales of Long-term Assets $0 $0 $0 New Investment Received $0 $0 $0 Subtotal Cash Received $577,000 $419,900 $611,890 Expenditures FY 2012 FY 2013 FY 2014 Expenditures from Operations Cash Spending $65,400 $74,100 $74,100 Bill Payments $95,972 $237,916 $295,586 Subtotal Spent on Operations $161,372 $312,016 $369,686 Additional Cash Spent Sales Tax, VAT, HST/GST Paid Out $0 $0 $0 Principal Repayment of Current Borrowing $22,000 $24,000 $24,000 Other Liabilities Principal Repayment $0 $0 $0 Long-term Liabilities Principal Repayment $0 $0 $0 Purchase Other Current Assets $0 $0 $0 Purchase Long-term Assets $285,000 $0 $0 Dividends $0 $0 $0 Subtotal Cash Spent $468,372 $336,016 $393,686 Net Cash Flow $108,628 $83,884 $218,204 Cash Balance $143,628 $227,512 $445,715 Page 15

4111, Local and Suburban Transit, are shown for")

20 7.6 Business Ratios The business ratios table below is generated by the planning software using the interconnected tables. Standard industry ratios, based upon Standard Industrial Classification Code (SIC) 4111, Local and Suburban Transit, are shown for comparison. Page 16

4111, Local and Suburban Transit, are")

21 Table: Ratios Ratio Analysis FY 2012 FY 2013 FY 2014 Industry Profile Sales Growth n.a % 45.72% 3.70% Percent of Total Assets Other Current Assets 0.00% 0.00% 0.00% 45.30% Total Current Assets 35.90% 52.58% 73.08% 64.40% Long-term Assets 64.10% 47.42% 26.92% 35.60% Total Assets % % % % Current Liabilities 86.04% 68.55% 45.89% 31.20% Long-term Liabilities 0.00% 0.00% 0.00% 25.20% Total Liabilities 86.04% 68.55% 45.89% 56.40% Net Worth 13.96% 31.45% 54.11% 43.60% Percent of Sales Sales % % % % Gross Margin 80.54% 87.15% 90.30% 66.70% Selling, General & Administrative Expenses 86.04% 65.37% 60.12% 46.50% Advertising Expenses 0.36% 0.21% 0.19% 0.50% Profit Before Interest and Taxes 18.79% 28.09% 41.61% 2.90% Main Ratios Current Quick Total Debt to Total Assets 86.04% 68.55% 45.89% 56.40% Pre-tax Return on Net Worth 45.53% 71.91% 71.65% 4.60% Pre-tax Return on Assets 6.36% 22.62% 38.77% 10.50% Additional Ratios FY 2012 FY 2013 FY 2014 Net Profit Margin 8.27% 19.11% 31.69% n.a Return on Equity 37.34% 58.96% 58.75% n.a Activity Ratios Accounts Payable Turnover n.a Payment Days n.a Total Asset Turnover n.a Debt Ratios Debt to Net Worth n.a Current Liab. to Liab n.a Liquidity Ratios Net Working Capital ($200,647) ($69,098) $165,822 n.a Interest Coverage n.a Additional Ratios Assets to Sales n.a Current Debt/Total Assets 86% 69% 46% n.a Acid Test n.a Sales/Net Worth n.a Dividend Payout n.a Page 17

22 Appendix Table: Sales Forecast Sales Forecast Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct Sales Individuals/families $4,000 $4,000 $4,000 $5,000 $5,000 $6,000 $6,000 $7,000 $7,000 $8,000 $8,000 $8,000 Business Travellers $4,000 $4,000 $4,000 $4,000 $5,000 $5,000 $5,000 $5,000 $6,000 $6,000 $6,000 $6,000 Memberships $5,000 $5,000 $5,000 $5,000 $5,000 $5,000 $5,000 $5,000 $5,000 $5,000 $5,000 $5,000 Dispatch Fees $5,000 $5,000 $5,000 $5,000 $5,000 $5,000 $5,000 $5,000 $5,000 $5,000 $5,000 $5,000 Total Sales $18,000 $18,000 $18,000 $19,000 $20,000 $21,000 $21,000 $22,000 $23,000 $24,000 $24,000 $24,000 Direct Cost of Sales Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct Individuals/families $1,350 $1,350 $1,350 $1,800 $1,800 $1,800 $1,800 $1,800 $2,250 $2,250 $2,250 $2,250 Business travelers $1,800 $1,800 $1,800 $1,800 $2,250 $2,250 $2,250 $2,250 $2,700 $2,700 $2,700 $2,700 Subtotal Direct Cost of Sales $3,150 $3,150 $3,150 $3,600 $4,050 $4,050 $4,050 $4,050 $4,950 $4,950 $4,950 $4,950 Page 1

23 Appendix Table: Personnel Personnel Plan Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct Mohammed 0% $3,000 $3,000 $3,000 $3,000 $3,000 $3,000 $3,000 $3,000 $3,000 $3,000 $3,000 $3,000 Part-time employee 0% $0 $800 $800 $800 $800 $800 $800 $800 $800 $800 $800 $800 Driver 0% $0 $2,200 $2,200 $1,800 $1,800 $1,800 $1,800 $1,800 $1,800 $1,800 $1,800 $1,800 Total People Total Payroll $3,000 $6,000 $6,000 $5,600 $5,600 $5,600 $5,600 $5,600 $5,600 $5,600 $5,600 $5,600 Page 2

24 Appendix Table: General Assumptions General Assumptions Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct Plan Month Current Interest Rate 8.00% 8.00% 8.00% 8.00% 8.00% 8.00% 8.00% 8.00% 8.00% 8.00% 8.00% 8.00% Long-term Interest Rate 8.00% 8.00% 8.00% 8.00% 8.00% 8.00% 8.00% 8.00% 8.00% 8.00% 8.00% 8.00% Tax Rate 18.00% 18.00% 18.00% 18.00% 18.00% 18.00% 18.00% 18.00% 18.00% 18.00% 18.00% 18.00% Other Page 3

25 Appendix Table: Profit and Loss Pro Forma Profit and Loss Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct Sales $18,000 $18,000 $18,000 $19,000 $20,000 $21,000 $21,000 $22,000 $23,000 $24,000 $24,000 $24,000 Direct Cost of Sales $3,150 $3,150 $3,150 $3,600 $4,050 $4,050 $4,050 $4,050 $4,950 $4,950 $4,950 $4,950 Other $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 Total Cost of Sales $3,150 $3,150 $3,150 $3,600 $4,050 $4,050 $4,050 $4,050 $4,950 $4,950 $4,950 $4,950 Gross Margin $14,850 $14,850 $14,850 $15,400 $15,950 $16,950 $16,950 $17,950 $18,050 $19,050 $19,050 $19,050 Gross Margin % 82.50% 82.50% 82.50% 81.05% 79.75% 80.71% 80.71% 81.59% 78.48% 79.38% 79.38% 79.38% Expenses Payroll $3,000 $6,000 $6,000 $5,600 $5,600 $5,600 $5,600 $5,600 $5,600 $5,600 $5,600 $5,600 Sales and Marketing and Other $150 $175 $200 $225 $250 $300 $300 $300 $300 $300 $300 $300 Expenses Depreciation $2,375 $2,375 $2,375 $2,375 $2,375 $2,375 $2,375 $2,375 $2,375 $2,375 $2,375 $2,375 Web site maintenance $50 $50 $50 $50 $50 $50 $50 $50 $50 $50 $50 $50 Utilities $100 $100 $100 $100 $100 $100 $100 $100 $100 $100 $100 $100 Insurance $450 $450 $450 $450 $450 $450 $450 $450 $450 $450 $450 $450 Rent $500 $500 $500 $500 $500 $500 $500 $500 $500 $500 $500 $500 Payroll Taxes 15% $450 $450 $450 $450 $450 $450 $450 $450 $450 $450 $450 $450 Members profit allocation $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 $40,000 Total Operating Expenses $7,075 $10,100 $10,125 $9,750 $9,775 $9,825 $9,825 $9,825 $9,825 $9,825 $9,825 $49,825 Profit Before Interest and Taxes $7,775 $4,750 $4,725 $5,650 $6,175 $7,125 $7,125 $8,125 $8,225 $9,225 $9,225 ($30,775) EBITDA $10,150 $7,125 $7,100 $8,025 $8,550 $9,500 $9,500 $10,500 $10,600 $11,600 $11,600 ($28,400) Interest Expense $1,900 $1,887 $1,873 $1,860 $1,847 $1,833 $1,820 $1,807 $1,793 $1,780 $1,767 $1,753 Taxes Incurred $1,058 $515 $513 $682 $779 $953 $955 $1,137 $1,158 $1,340 $1,343 ($5,855) Net Profit $4,818 $2,348 $2,338 $3,108 $3,549 $4,339 $4,350 $5,181 $5,274 $6,105 $6,116 ($26,673) Net Profit/Sales 26.76% 13.04% 12.99% 16.36% 17.75% 20.66% 20.71% 23.55% 22.93% 25.44% 25.48% % Page 4

26 Appendix Table: Cash Flow Pro Forma Cash Flow Cash Received Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct Cash from Operations Cash Sales $18,000 $18,000 $18,000 $19,000 $20,000 $21,000 $21,000 $22,000 $23,000 $24,000 $24,000 $24,000 Subtotal Cash from Operations $18,000 $18,000 $18,000 $19,000 $20,000 $21,000 $21,000 $22,000 $23,000 $24,000 $24,000 $24,000 Additional Cash Received Sales Tax, VAT, HST/GST Received 0.00% $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 New Current Borrowing $285,000 $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 New Other Liabilities (interest-free) $40,000 $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 New Long-term Liabilities $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 Sales of Other Current Assets $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 Sales of Long-term Assets $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 New Investment Received $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 Subtotal Cash Received $343,000 $18,000 $18,000 $19,000 $20,000 $21,000 $21,000 $22,000 $23,000 $24,000 $24,000 $24,000 Expenditures Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct Expenditures from Operations Cash Spending $3,000 $6,000 $6,000 $5,600 $5,600 $5,600 $5,600 $5,600 $5,600 $5,600 $5,600 $5,600 Bill Payments $260 $7,790 $7,277 $7,308 $7,936 $8,483 $8,685 $8,681 $8,874 $9,757 $9,920 $11,002 Subtotal Spent on Operations $3,260 $13,790 $13,277 $12,908 $13,536 $14,083 $14,285 $14,281 $14,474 $15,357 $15,520 $16,602 Additional Cash Spent Sales Tax, VAT, HST/GST Paid Out $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 Principal Repayment of Current Borrowing $0 $2,000 $2,000 $2,000 $2,000 $2,000 $2,000 $2,000 $2,000 $2,000 $2,000 $2,000 Other Liabilities Principal Repayment $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 Long-term Liabilities Principal Repayment $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 Purchase Other Current Assets $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 Purchase Long-term Assets $285,000 $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 Dividends $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 Subtotal Cash Spent $288,260 $15,790 $15,277 $14,908 $15,536 $16,083 $16,285 $16,281 $16,474 $17,357 $17,520 $18,602 Net Cash Flow $54,740 $2,210 $2,723 $4,092 $4,464 $4,917 $4,715 $5,719 $6,526 $6,643 $6,480 $5,398 Cash Balance $89,740 $91,950 $94,673 $98,765 $103,229 $108,146 $112,861 $118,580 $125,106 $131,749 $138,230 $143,628 Page 5

27 Appendix Table: Balance Sheet Pro Forma Balance Sheet Assets Starting Balances Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct Current Assets Cash $35,000 $89,740 $91,950 $94,673 $98,765 $103,229 $108,146 $112,861 $118,580 $125,106 $131,749 $138,230 $143,628 Other Current Assets $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 Total Current Assets $35,000 $89,740 $91,950 $94,673 $98,765 $103,229 $108,146 $112,861 $118,580 $125,106 $131,749 $138,230 $143,628 Long-term Assets Long-term Assets $0 $285,000 $285,000 $285,000 $285,000 $285,000 $285,000 $285,000 $285,000 $285,000 $285,000 $285,000 $285,000 Accumulated Depreciation $0 $2,375 $4,750 $7,125 $9,500 $11,875 $14,250 $16,625 $19,000 $21,375 $23,750 $26,125 $28,500 Total Long-term Assets $0 $282,625 $280,250 $277,875 $275,500 $273,125 $270,750 $268,375 $266,000 $263,625 $261,250 $258,875 $256,500 Total Assets $35,000 $372,365 $372,200 $372,548 $374,265 $376,354 $378,896 $381,236 $384,580 $388,731 $392,999 $397,105 $400,128 Liabilities and Capital Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct Current Liabilities Accounts Payable $0 $7,547 $7,034 $7,044 $7,653 $8,193 $8,396 $8,386 $8,549 $9,426 $9,589 $9,579 $41,275 Current Borrowing $0 $285,000 $283,000 $281,000 $279,000 $277,000 $275,000 $273,000 $271,000 $269,000 $267,000 $265,000 $263,000 Other Current Liabilities $0 $40,000 $40,000 $40,000 $40,000 $40,000 $40,000 $40,000 $40,000 $40,000 $40,000 $40,000 $40,000 Subtotal Current Liabilities $0 $332,547 $330,034 $328,044 $326,653 $325,193 $323,396 $321,386 $319,549 $318,426 $316,589 $314,579 $344,275 Long-term Liabilities $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 Total Liabilities $0 $332,547 $330,034 $328,044 $326,653 $325,193 $323,396 $321,386 $319,549 $318,426 $316,589 $314,579 $344,275 Paid-in Capital $35,000 $35,000 $35,000 $35,000 $35,000 $35,000 $35,000 $35,000 $35,000 $35,000 $35,000 $35,000 $35,000 Retained Earnings $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 Earnings $0 $4,818 $7,165 $9,504 $12,612 $16,161 $20,500 $24,850 $30,031 $35,305 $41,410 $47,526 $20,853 Total Capital $35,000 $39,818 $42,165 $44,504 $47,612 $51,161 $55,500 $59,850 $65,031 $70,305 $76,410 $82,526 $55,853 Total Liabilities and Capital $35,000 $372,365 $372,200 $372,548 $374,265 $376,354 $378,896 $381,236 $384,580 $388,731 $392,999 $397,105 $400,128 Net Worth $35,000 $39,818 $42,165 $44,504 $47,612 $51,161 $55,500 $59,850 $65,031 $70,305 $76,410 $82,526 $55,853 Page 6

Business Plan Planning Service Financial Analyses and Projections

Business Plan Planning Service Financial Analyses and Projections Financials Included With Every Ceo Resource Plan These are the financial analyses and projections that are included with all plans developed

Business Plan Planning Service Financial Analyses and Projections Financials Included With Every Ceo Resource Plan These are the financial analyses and projections that are included with all plans developed

BUSINESS PLAN SAMPLE Wedding Consultants source business plan pro, Palo Alto Software, Inc.

BUSINESS PLAN SAMPLE Wedding Consultants source business plan pro, Palo Alto Software, Inc. 1.0 Executive Summary TLC Wedding Consultants is a full service company that provides complete consulting services

BUSINESS PLAN SAMPLE Wedding Consultants source business plan pro, Palo Alto Software, Inc. 1.0 Executive Summary TLC Wedding Consultants is a full service company that provides complete consulting services

Business Plan Template

Business Plan Template This simple business plan template was created from Business Plan Pro 11.0, the best-selling business planning software published by Palo Alto Software, Inc. To learn more about

Business Plan Template This simple business plan template was created from Business Plan Pro 11.0, the best-selling business planning software published by Palo Alto Software, Inc. To learn more about

CBC- A complete test of red blood cell count, white blood count, and a platelet count. Each of these three can be ordered individually if needed.

Laboratory Business Plan Fargo Medical Laboratories Executive Summary Fargo Medical Laboratories (FML) is a start-up company committed to providing the most convenient, friendliest blood testing service

Laboratory Business Plan Fargo Medical Laboratories Executive Summary Fargo Medical Laboratories (FML) is a start-up company committed to providing the most convenient, friendliest blood testing service

Youth Sports Nonprofit Business Plan

Youth Sports Nonprofit Business Plan YouthSports Executive Summary Twenty-five percent of Richmond Metro youth participated in organized sports last year, compared with 85 to 90 percent in the suburbs,

Youth Sports Nonprofit Business Plan YouthSports Executive Summary Twenty-five percent of Richmond Metro youth participated in organized sports last year, compared with 85 to 90 percent in the suburbs,

FREIGHT BROKER SAMPLE BUSINESS PLAN. Executive Summary. 1.1 Objectives

FREIGHT BROKER SAMPLE BUSINESS PLAN Executive Summary Silicon Freight Brokers (SFB) is a specialized freight broker service located in Hood River, OR. The company has been set up as an Oregon C Corporation

FREIGHT BROKER SAMPLE BUSINESS PLAN Executive Summary Silicon Freight Brokers (SFB) is a specialized freight broker service located in Hood River, OR. The company has been set up as an Oregon C Corporation

Neo Consulting. Neo Consulting 123 Business Street Orlando, FL 32805 123-456-7890 info@neoconsulting.com

Neo Consulting 123 Business Street Orlando, FL 32805 123-456-7890 info@neoconsulting.com This sample marketing plan has been made available to clients of BizCentral USA for reference only. All information

Neo Consulting 123 Business Street Orlando, FL 32805 123-456-7890 info@neoconsulting.com This sample marketing plan has been made available to clients of BizCentral USA for reference only. All information

Car Wash Business Plan Soapy Rides Car Wash

Car Wash Business Plan Soapy Rides Car Wash Executive Summary Soapy Rides is a prominent hand car wash serving the East Meadow, Long Island, NY community. Soapy Rides will be run by Mark Deshpande, of

Car Wash Business Plan Soapy Rides Car Wash Executive Summary Soapy Rides is a prominent hand car wash serving the East Meadow, Long Island, NY community. Soapy Rides will be run by Mark Deshpande, of

Personal Event Planning Business Plan Occasions, The Event Planning Specialists

Personal Event Planning Business Plan Occasions, The Event Planning Specialists 1.0 Executive Summary Welcome to the future of event planning! Occasions, The Event Planning Specialists, brings to the community

Personal Event Planning Business Plan Occasions, The Event Planning Specialists 1.0 Executive Summary Welcome to the future of event planning! Occasions, The Event Planning Specialists, brings to the community

Real Estate Management Business Plan

Real Estate Management Business Plan MSN Real Estate Executive Summary MSN Real Estate (MSN) is an Oregon-based real estate company that will offer benchmarked rental units for the Eugene, Oregon community.

Real Estate Management Business Plan MSN Real Estate Executive Summary MSN Real Estate (MSN) is an Oregon-based real estate company that will offer benchmarked rental units for the Eugene, Oregon community.

Business Plan. Your Business Name

Business Plan Your Business Name Owners Address City, ST ZIP Code Telephone Fax E-Mail Date: Page 2 II. Executive Summary Write this section last. We suggest that you make it one page long; two pages max.

Business Plan Your Business Name Owners Address City, ST ZIP Code Telephone Fax E-Mail Date: Page 2 II. Executive Summary Write this section last. We suggest that you make it one page long; two pages max.

UNDERSTANDING WHERE YOU STAND. A Simple Guide to Your Company s Financial Statements

UNDERSTANDING WHERE YOU STAND A Simple Guide to Your Company s Financial Statements Contents INTRODUCTION One statement cannot diagnose your company s financial health. Put several statements together

UNDERSTANDING WHERE YOU STAND A Simple Guide to Your Company s Financial Statements Contents INTRODUCTION One statement cannot diagnose your company s financial health. Put several statements together

Sample Business Plan: Weddings With Panache

Sample Business Plan: Weddings With Panache Table of Contents 1.0 Executive Summary 1.1 Objectives 1.2 Mission 1.3 Keys to Success 2.0 Company Summary 2.1 Company Ownership 2.2 Start-up Summary 2.3 Company

Sample Business Plan: Weddings With Panache Table of Contents 1.0 Executive Summary 1.1 Objectives 1.2 Mission 1.3 Keys to Success 2.0 Company Summary 2.1 Company Ownership 2.2 Start-up Summary 2.3 Company

BUSINESS PLAN TEMPLATE

iplanner.net Small Business Plans Online BUSINESS PLAN TEMPLATE For a start-up company 18/01/2012 12:33:19(GMT) Executive Summary... 3 Business Overview... 3 Products and Services... 3 Sales Forecast...

iplanner.net Small Business Plans Online BUSINESS PLAN TEMPLATE For a start-up company 18/01/2012 12:33:19(GMT) Executive Summary... 3 Business Overview... 3 Products and Services... 3 Sales Forecast...

Financial Statement Consolidation

Financial Statement Consolidation We will consolidate the previously completed worksheets in this financial plan. In order to complete this section of the plan, you must have already completed all of the

Financial Statement Consolidation We will consolidate the previously completed worksheets in this financial plan. In order to complete this section of the plan, you must have already completed all of the

Ashland Entrepreneur Center EXAMPLE Business Plan

Ashland Entrepreneur Center EXAMPLE Business Plan Questions regarding this plan should be directed to: Larry Ferguson, E-Center Director (606) 326-2232 Or Kim Boggs, E-Center Coordinator (606) 326-2164

Ashland Entrepreneur Center EXAMPLE Business Plan Questions regarding this plan should be directed to: Larry Ferguson, E-Center Director (606) 326-2232 Or Kim Boggs, E-Center Coordinator (606) 326-2164

Need to know finance

Need to know finance You can t hide from it Every decision has financial implications Estimating sales and cost of sales (aka direct costs) Gross Profit and Gross Profit Margin (GPM) Sales cost of sales

Need to know finance You can t hide from it Every decision has financial implications Estimating sales and cost of sales (aka direct costs) Gross Profit and Gross Profit Margin (GPM) Sales cost of sales

Tranquility Day Spa. A Comprehensive Business Plan. Jane Smith. 100 Any Place Road. Any Town, FL. 32837. Phone: 407-999-8888

A Comprehensive Business Plan Jane Smith 100 Any Place Road Any Town, FL. 32837 Phone: 407-999-8888 Email: info@tranquilityds.com Confidentiality Agreement The undersigned reader acknowledges that the

A Comprehensive Business Plan Jane Smith 100 Any Place Road Any Town, FL. 32837 Phone: 407-999-8888 Email: info@tranquilityds.com Confidentiality Agreement The undersigned reader acknowledges that the

OPERATING FUND. PRELIMINARY & UNAUDITED FINANCIAL HIGHLIGHTS September 30, 2015 RENDELL L. JONES CHIEF FINANCIAL OFFICER

PRELIMINARY & UNAUDITED FINANCIAL HIGHLIGHTS September 30, 2015 RENDELL L. JONES CHIEF FINANCIAL OFFICER MANAGEMENT OVERVIEW September 30, 2015 Balance Sheet Cash and cash equivalents had a month-end balance

PRELIMINARY & UNAUDITED FINANCIAL HIGHLIGHTS September 30, 2015 RENDELL L. JONES CHIEF FINANCIAL OFFICER MANAGEMENT OVERVIEW September 30, 2015 Balance Sheet Cash and cash equivalents had a month-end balance

Training Manual: The Basics of Financing Agriculture

Training Manual: The Basics of Financing Agriculture Acknowledgement The Agriculture Finance Training Manual is part of AgriFin s Agriculture Finance Training Tools. The Manual was developed by IPC - Internationale

Training Manual: The Basics of Financing Agriculture Acknowledgement The Agriculture Finance Training Manual is part of AgriFin s Agriculture Finance Training Tools. The Manual was developed by IPC - Internationale

What is a business plan?

What is a business plan? A business plan is the presentation of an idea for a new business. When a person (or group) is planning to open a business, there is a great deal of research that must be done

What is a business plan? A business plan is the presentation of an idea for a new business. When a person (or group) is planning to open a business, there is a great deal of research that must be done

MANAGING YOUR BUSINESS S CASH FLOW. Managing Your Business s Cash Flow. David Oetken, MBA CPM

MANAGING YOUR BUSINESS S CASH FLOW Managing Your Business s Cash Flow David Oetken, MBA CPM 1 2 Being a successful entrepreneur takes a unique mix of skills and practices. You need to generate exciting

MANAGING YOUR BUSINESS S CASH FLOW Managing Your Business s Cash Flow David Oetken, MBA CPM 1 2 Being a successful entrepreneur takes a unique mix of skills and practices. You need to generate exciting

Financial Planning. Presented by Emma's Garden

+ Financial Planning Presented by Emma's Garden Financial Planning A comprehensive financial plan helps you to forecast and set your financial goals and milestones. Your financial forecasts are an essential

+ Financial Planning Presented by Emma's Garden Financial Planning A comprehensive financial plan helps you to forecast and set your financial goals and milestones. Your financial forecasts are an essential

Learning Objectives: Quick answer key: Question # Multiple Choice True/False. 14.1 Describe the important of accounting and financial information.

0 Learning Objectives: 14.1 Describe the important of accounting and financial information. 14.2 Differentiate between managerial and financial accounting. 14.3 Identify the six steps of the accounting

0 Learning Objectives: 14.1 Describe the important of accounting and financial information. 14.2 Differentiate between managerial and financial accounting. 14.3 Identify the six steps of the accounting

6.3 PROFIT AND LOSS AND BALANCE SHEETS. Simple Financial Calculations. Analysing Performance - The Balance Sheet. Analysing Performance

63 COSTS AND COSTING 6 PROFIT AND LOSS AND BALANCE SHEETS Simple Financial Calculations Analysing Performance - The Balance Sheet Analysing Performance Analysing Financial Performance Profit And Loss Forecast

63 COSTS AND COSTING 6 PROFIT AND LOSS AND BALANCE SHEETS Simple Financial Calculations Analysing Performance - The Balance Sheet Analysing Performance Analysing Financial Performance Profit And Loss Forecast

Components Of A Business Plan

1 Components Of A Business Plan Cover Page Table of Contents Statement of Purpose Description of the Business Competition Market Strategy Location Management Personnel Application and Expected Effect of

1 Components Of A Business Plan Cover Page Table of Contents Statement of Purpose Description of the Business Competition Market Strategy Location Management Personnel Application and Expected Effect of

AT&T Global Network Client for Windows Product Support Matrix January 29, 2015

AT&T Global Network Client for Windows Product Support Matrix January 29, 2015 Product Support Matrix Following is the Product Support Matrix for the AT&T Global Network Client. See the AT&T Global Network

AT&T Global Network Client for Windows Product Support Matrix January 29, 2015 Product Support Matrix Following is the Product Support Matrix for the AT&T Global Network Client. See the AT&T Global Network

HELPING HAND. Alleviating Hunger in Johnson County

DISCLAIMER This business plan is sample plan only. It will provide you an example of a comprehensive plan. Information presented in this business plan is considered private information and may not be distributed

DISCLAIMER This business plan is sample plan only. It will provide you an example of a comprehensive plan. Information presented in this business plan is considered private information and may not be distributed

PLANNING FOR SUCCESS P a g e 0

PLANNING FOR SUCCESS P a g e 0 PLANNING FOR SUCCESS P a g e 1 Planning for Success: Your Guide to Preparing a Business and Marketing Plan This guide is designed to help you put together a comprehensive,

PLANNING FOR SUCCESS P a g e 0 PLANNING FOR SUCCESS P a g e 1 Planning for Success: Your Guide to Preparing a Business and Marketing Plan This guide is designed to help you put together a comprehensive,

Understanding Financial Statements. For Your Business

Understanding Financial Statements For Your Business Disclaimer The information provided is for informational purposes only, does not constitute legal advice or create an attorney-client relationship,

Understanding Financial Statements For Your Business Disclaimer The information provided is for informational purposes only, does not constitute legal advice or create an attorney-client relationship,

Developing Financial Statements

New York StartUP! Business Plan Competition Developing Financial Statements Presented by Paisley Demby, CEO PBN Consulting, LLC www.pbnconsulting.com 1 Invitation to Tweet #2015NYStartUp PaisleyDemby Contents

New York StartUP! Business Plan Competition Developing Financial Statements Presented by Paisley Demby, CEO PBN Consulting, LLC www.pbnconsulting.com 1 Invitation to Tweet #2015NYStartUp PaisleyDemby Contents

FINANCIAL MANAGEMENT

100 Arbor Drive, Suite 108 Christiansburg, VA 24073 Voice: 540-381-9333 FAX: 540-381-8319 www.becpas.com Providing Professional Business Advisory & Consulting Services Douglas L. Johnston, II djohnston@becpas.com

100 Arbor Drive, Suite 108 Christiansburg, VA 24073 Voice: 540-381-9333 FAX: 540-381-8319 www.becpas.com Providing Professional Business Advisory & Consulting Services Douglas L. Johnston, II djohnston@becpas.com

STATEMENT OF CASH FLOWS AND WORKING CAPITAL ANALYSIS

C H A P T E R 1 0 STATEMENT OF CASH FLOWS AND WORKING CAPITAL ANALYSIS I N T R O D U C T I O N Historically, profit-oriented businesses have used the accrual basis of accounting in which the income statement,

C H A P T E R 1 0 STATEMENT OF CASH FLOWS AND WORKING CAPITAL ANALYSIS I N T R O D U C T I O N Historically, profit-oriented businesses have used the accrual basis of accounting in which the income statement,

IGCSE Business Studies revision notes Finance Neil.elrick@tes.tp.edu.tw

IGCSE FINANCE REVISION NOTES Table of contents Table of contents... 2 SOURCES OF FINANCE... 3 CASH FLOW... 5 HOW TO CALCULATE THE CASH BALANCE... 5 HOW TO WORK OUT THE CASH AVAILABLE TO THE BUSINESS...

IGCSE FINANCE REVISION NOTES Table of contents Table of contents... 2 SOURCES OF FINANCE... 3 CASH FLOW... 5 HOW TO CALCULATE THE CASH BALANCE... 5 HOW TO WORK OUT THE CASH AVAILABLE TO THE BUSINESS...

Financial Plan. A) Estimated One-Time Financial Requirements. Part One

Estimated One-Time Financial Requirements. Part One") Financial Plan The Financial Plan is perhaps one of the most important components of your Business Plan (see Business Plan Handout). Not only is it essential if you are seeking external financing it is

Financial Plan The Financial Plan is perhaps one of the most important components of your Business Plan (see Business Plan Handout). Not only is it essential if you are seeking external financing it is

CREDIT VALUES CREDIT LIMIT 2,900 CREDIT RATING 2,400

Business report generated at 16/09/2015 11:56:43 12345678 : SAMPLE LIMITED OVERALL CREDIT SCORE 56 Below Average Risk CREDIT VALUES CREDIT LIMIT 2,900 CREDIT RATING 2,400 KEY SCORE FACTORS 2 POSITIVE 2

Business report generated at 16/09/2015 11:56:43 12345678 : SAMPLE LIMITED OVERALL CREDIT SCORE 56 Below Average Risk CREDIT VALUES CREDIT LIMIT 2,900 CREDIT RATING 2,400 KEY SCORE FACTORS 2 POSITIVE 2

Instructor Comments:

Instructor Comments: The sample business plan is taken from a website selling business plan software and is not the product of a student assignment. However, it does give some examples of components of

Instructor Comments: The sample business plan is taken from a website selling business plan software and is not the product of a student assignment. However, it does give some examples of components of

Knowledge is Power The Business Mindset The nitty gritty of understanding your cash flow CCIQ Webinar 28 October 2015

Knowledge is Power The Business Mindset The nitty gritty of understanding your cash flow CCIQ Webinar 28 October 2015 Webinar Presenter Jason Krenske Partner at Ulton Jason has worked with many businesses

Knowledge is Power The Business Mindset The nitty gritty of understanding your cash flow CCIQ Webinar 28 October 2015 Webinar Presenter Jason Krenske Partner at Ulton Jason has worked with many businesses

ebrief for freelancers and contractors Contractors guide to investing surplus cash

ebrief for freelancers and contractors Contractors guide to investing surplus cash Making the most of your Surplus Cash Intouch Accounting, the personal online accountant, looks at this all important question

ebrief for freelancers and contractors Contractors guide to investing surplus cash Making the most of your Surplus Cash Intouch Accounting, the personal online accountant, looks at this all important question

COMPARISON OF FIXED & VARIABLE RATES (25 YEARS) CHARTERED BANK ADMINISTERED INTEREST RATES - PRIME BUSINESS*

CHARTERED BANK ADMINISTERED INTEREST RATES - PRIME BUSINESS*") COMPARISON OF FIXED & VARIABLE RATES (25 YEARS) 2 Fixed Rates Variable Rates FIXED RATES OF THE PAST 25 YEARS AVERAGE RESIDENTIAL MORTGAGE LENDING RATE - 5 YEAR* (Per cent) Year Jan Feb Mar Apr May Jun

COMPARISON OF FIXED & VARIABLE RATES (25 YEARS) 2 Fixed Rates Variable Rates FIXED RATES OF THE PAST 25 YEARS AVERAGE RESIDENTIAL MORTGAGE LENDING RATE - 5 YEAR* (Per cent) Year Jan Feb Mar Apr May Jun

COMPARISON OF FIXED & VARIABLE RATES (25 YEARS) CHARTERED BANK ADMINISTERED INTEREST RATES - PRIME BUSINESS*

CHARTERED BANK ADMINISTERED INTEREST RATES - PRIME BUSINESS*") COMPARISON OF FIXED & VARIABLE RATES (25 YEARS) 2 Fixed Rates Variable Rates FIXED RATES OF THE PAST 25 YEARS AVERAGE RESIDENTIAL MORTGAGE LENDING RATE - 5 YEAR* (Per cent) Year Jan Feb Mar Apr May Jun

COMPARISON OF FIXED & VARIABLE RATES (25 YEARS) 2 Fixed Rates Variable Rates FIXED RATES OF THE PAST 25 YEARS AVERAGE RESIDENTIAL MORTGAGE LENDING RATE - 5 YEAR* (Per cent) Year Jan Feb Mar Apr May Jun

Module 2: Preparing for Capital Venture Financing Building Pro-Forma Financial Statements

Module 2: Preparing for Capital Venture Financing Building Pro-Forma Financial Statements Module 2: Preparing for Capital Venture Financing Building Pro-Forma Financial Statements TABLE OF CONTENTS 1.0

Module 2: Preparing for Capital Venture Financing Building Pro-Forma Financial Statements Module 2: Preparing for Capital Venture Financing Building Pro-Forma Financial Statements TABLE OF CONTENTS 1.0

Smithfield Motors: A case in lending, strategy, and value

ABSTRACT Smithfield Motors: A case in lending, strategy, and value Steve A. Nenninger Sam Houston State University The primary subject matter of this case is financial statement analysis. Issues examined

ABSTRACT Smithfield Motors: A case in lending, strategy, and value Steve A. Nenninger Sam Houston State University The primary subject matter of this case is financial statement analysis. Issues examined

Mohave Community College Small Business Development Center Financial Statement Spreadsheet Program

Mohave Community College Small Business Development Center Financial Statement Spreadsheet Program Copyright (c) 1998 NPC SBDC Table of Contents 1.0 Overview 2.0 Basic Structure of the program 3.0 Why

Mohave Community College Small Business Development Center Financial Statement Spreadsheet Program Copyright (c) 1998 NPC SBDC Table of Contents 1.0 Overview 2.0 Basic Structure of the program 3.0 Why

Steak House 1.0 EXECUTIVE SUMMARY 2.0 COMPANY AND FINANCING SUMMARY 4.0 STRATEGIC AND MARKET ANALYSIS. 4.2 Industry Analysis 5.

Business Plans Handbooks "Steak House." Business Plans Handbook. Ed. Lynn M. Pearce. Vol. 20. Detroit: Gale, 2011. 133-147. Business Plans Handbooks. Web. 31 May 2012. Document URL http://go.galegroup.com/ps/i.do?id=gale%7ccx1999800022&v=2.1&u=chipl&it=r&p=gvrl.plans1&sw

Business Plans Handbooks "Steak House." Business Plans Handbook. Ed. Lynn M. Pearce. Vol. 20. Detroit: Gale, 2011. 133-147. Business Plans Handbooks. Web. 31 May 2012. Document URL http://go.galegroup.com/ps/i.do?id=gale%7ccx1999800022&v=2.1&u=chipl&it=r&p=gvrl.plans1&sw

Case 2:08-cv-02463-ABC-E Document 1-4 Filed 04/15/2008 Page 1 of 138. Exhibit 8

Case 2:08-cv-02463-ABC-E Document 1-4 Filed 04/15/2008 Page 1 of 138 Exhibit 8 Case 2:08-cv-02463-ABC-E Document 1-4 Filed 04/15/2008 Page 2 of 138 Domain Name: CELLULARVERISON.COM Updated Date: 12-dec-2007

Case 2:08-cv-02463-ABC-E Document 1-4 Filed 04/15/2008 Page 1 of 138 Exhibit 8 Case 2:08-cv-02463-ABC-E Document 1-4 Filed 04/15/2008 Page 2 of 138 Domain Name: CELLULARVERISON.COM Updated Date: 12-dec-2007

Basic Business Plan Outline

Basic Business Plan Outline A business plan needs to be a well thought out, honest, appraisal of the business and opportunity. This outline is meant to be used for your road map. It should be a living

Basic Business Plan Outline A business plan needs to be a well thought out, honest, appraisal of the business and opportunity. This outline is meant to be used for your road map. It should be a living

Understanding Financial Information for Bankruptcy Lawyers Understanding Financial Statements

Understanding Financial Information for Bankruptcy Lawyers Understanding Financial Statements In the United States, businesses generally present financial information in the form of financial statements

Understanding Financial Information for Bankruptcy Lawyers Understanding Financial Statements In the United States, businesses generally present financial information in the form of financial statements

Total shares at the end of ten years is 100*(1+5%) 10 =162.9.

10 =162.9.") FCS5510 Sample Homework Problems Unit04 CHAPTER 8 STOCK PROBLEMS 1. An investor buys 100 shares if a $40 stock that pays a annual cash dividend of $2 a share (a 5% dividend yield) and signs up for the

FCS5510 Sample Homework Problems Unit04 CHAPTER 8 STOCK PROBLEMS 1. An investor buys 100 shares if a $40 stock that pays a annual cash dividend of $2 a share (a 5% dividend yield) and signs up for the

How to Write a Business Plan

How to Write a Business Plan Small Business Development Center (SBDC) A well-written comprehensive business plan forms the basis for the success of any business venture. The business plan is a written

How to Write a Business Plan Small Business Development Center (SBDC) A well-written comprehensive business plan forms the basis for the success of any business venture. The business plan is a written

Start Your. Business Business Plan

Start Your Waste Recycling Business A TECHNICAL STEP-BY-STEP-GUIDE OF HOW TO START A COMMUNITY-BASED WASTE RECYCLING BUSINESS Start Your Waste Recycling Business Business Plan INTERNATIONAL LABOUR OFFICE

Start Your Waste Recycling Business A TECHNICAL STEP-BY-STEP-GUIDE OF HOW TO START A COMMUNITY-BASED WASTE RECYCLING BUSINESS Start Your Waste Recycling Business Business Plan INTERNATIONAL LABOUR OFFICE

Business Planning Worksheets

Business Planning Worksheets Copyright 2003-2010 Lamar University SBDC Table of Contents Introductory Section... 1 Cover Sheet... 1 Executive Summary... 1 Narrative Section... 2 Description of the Business...

Business Planning Worksheets Copyright 2003-2010 Lamar University SBDC Table of Contents Introductory Section... 1 Cover Sheet... 1 Executive Summary... 1 Narrative Section... 2 Description of the Business...

Trxade Group, Inc. (TCQB: TRXD): Record Revenues in Q3

: Record Revenues in Q3") Siddharth Rajeev, B.Tech, MBA, CFA Analyst November 5, 2015 Trxade Group, Inc. (TCQB: TRXD): Record Revenues in Q3 Sector/Industry: E-commerce Market Data (as of November 5, 2015) Current Price $1.15 Fair

Siddharth Rajeev, B.Tech, MBA, CFA Analyst November 5, 2015 Trxade Group, Inc. (TCQB: TRXD): Record Revenues in Q3 Sector/Industry: E-commerce Market Data (as of November 5, 2015) Current Price $1.15 Fair

Financial Projections. Making sense of the money

Financial Projections Making sense of the money The Burning Questions What are your capital needs? Projections How will you get that capital? Structure: Equity or debt? Ownership structure Up-front or

Financial Projections Making sense of the money The Burning Questions What are your capital needs? Projections How will you get that capital? Structure: Equity or debt? Ownership structure Up-front or

Financial Ratio Cheatsheet MyAccountingCourse.com PDF

Financial Ratio Cheatsheet MyAccountingCourse.com PDF Table of contents Liquidity Ratios Solvency Ratios Efficiency Ratios Profitability Ratios Market Prospect Ratios Coverage Ratios CPA Exam Ratios to

Financial Ratio Cheatsheet MyAccountingCourse.com PDF Table of contents Liquidity Ratios Solvency Ratios Efficiency Ratios Profitability Ratios Market Prospect Ratios Coverage Ratios CPA Exam Ratios to

BRILLIANT CLEANING SERVICE

SAMPLE SERVICE BUSINESS PLAN Created by Northeast Entrepreneur Fund, Inc. The contents of this Business Plan are fictional. No intent is made to resemble a business in existence. BRILLIANT CLEANING SERVICE

SAMPLE SERVICE BUSINESS PLAN Created by Northeast Entrepreneur Fund, Inc. The contents of this Business Plan are fictional. No intent is made to resemble a business in existence. BRILLIANT CLEANING SERVICE

how to finance the business

A DV I C E B O O K L E T how to finance the business HOW TO FINANCE THE BUSINESS Getting enough of the right funding is one of the more difficult tasks that you will face as a new entrepreneur. Typically,

A DV I C E B O O K L E T how to finance the business HOW TO FINANCE THE BUSINESS Getting enough of the right funding is one of the more difficult tasks that you will face as a new entrepreneur. Typically,

Chapter 9 E-Commerce: Digital Markets, Digital Goods

1 Chapter 9 E-Commerce: Digital Markets, Digital Goods LEARNING TRACK #: 2: BUILD BUSINESS PLAN There are lots of different ways to lay out a business plan. The sample

1 Chapter 9 E-Commerce: Digital Markets, Digital Goods LEARNING TRACK #: 2: BUILD BUSINESS PLAN There are lots of different ways to lay out a business plan. The sample

CHAPTER 11 Solutions STOCKHOLDERS EQUITY

CHAPTER 11 Solutions STOCKHOLDERS EQUITY Chapter 11, SE 1. 1. c 4. 2. a 5. 3. b 6. d e a Chapter 11, SE 2. 1. Advantage 4. 2. Disadvantage 5. 3. Advantage 6. Advantage Disadvantage Advantage Chapter 11,

CHAPTER 11 Solutions STOCKHOLDERS EQUITY Chapter 11, SE 1. 1. c 4. 2. a 5. 3. b 6. d e a Chapter 11, SE 2. 1. Advantage 4. 2. Disadvantage 5. 3. Advantage 6. Advantage Disadvantage Advantage Chapter 11,

Tax Return Questionnaire - 2014 Tax Year

Print this form out, take some time to fill it out, and bring it with you when you come to the office. This will save you time and money, and help us help you more effectively. Tax Return Questionnaire

Print this form out, take some time to fill it out, and bring it with you when you come to the office. This will save you time and money, and help us help you more effectively. Tax Return Questionnaire

Understanding A Firm s Financial Statements

CHAPTER OUTLINE Spotlight: J&S Construction Company (http://www.jsconstruction.com) 1 The Lemonade Kids Financial statement (accounting statements) reports of a firm s financial performance and resources,

CHAPTER OUTLINE Spotlight: J&S Construction Company (http://www.jsconstruction.com) 1 The Lemonade Kids Financial statement (accounting statements) reports of a firm s financial performance and resources,

Preparing a Successful Financial Plan

Topic 9 Preparing a Successful Financial Plan LEARNING OUTCOMES By the end of this topic, you should be able to: 1. Describe the overview of accounting methods; 2. Prepare the three major financial statements

Topic 9 Preparing a Successful Financial Plan LEARNING OUTCOMES By the end of this topic, you should be able to: 1. Describe the overview of accounting methods; 2. Prepare the three major financial statements

BUSINESS PLAN GUIDE. Send completed business plans to:

BUSINESS PLAN GUIDE Send completed business plans to: Waubetek Business Development Corporation 6 Rainbow Ridge Road P.O. Box 209 Birch Island, ON P0P 1A0 1-800-665-2248 toll-free (705) 285-4275 phone

BUSINESS PLAN GUIDE Send completed business plans to: Waubetek Business Development Corporation 6 Rainbow Ridge Road P.O. Box 209 Birch Island, ON P0P 1A0 1-800-665-2248 toll-free (705) 285-4275 phone

Financial Forecasting (Pro Forma Financial Statements)

") Financial Modeling Templates Financial Forecasting (Pro Forma Financial Statements) http://spreadsheetml.com/finance/financialplanningforecasting_proformafinancialstatements.shtml Copyright (c) 2009, ConnectCode

Financial Modeling Templates Financial Forecasting (Pro Forma Financial Statements) http://spreadsheetml.com/finance/financialplanningforecasting_proformafinancialstatements.shtml Copyright (c) 2009, ConnectCode

PREPARING FINAL ACCOUNTS. part

15_1312MH_CH09 27/1/05 8:38 am Page 87 PREPARING part 3 FINAL ACCOUNTS 9 The final accounts of sole traders 10 Accounting principles, concepts and policies 11 Depreciation and fixed assets 12 Bad debts

15_1312MH_CH09 27/1/05 8:38 am Page 87 PREPARING part 3 FINAL ACCOUNTS 9 The final accounts of sole traders 10 Accounting principles, concepts and policies 11 Depreciation and fixed assets 12 Bad debts

ebrief for freelancers and contractors Claiming business travel expenses: a guide for contractors and freelancers

ebrief for freelancers and contractors Claiming business travel expenses: a guide for contractors and freelancers Could you be missing out on claiming all your business travel expenses? We all like to

ebrief for freelancers and contractors Claiming business travel expenses: a guide for contractors and freelancers Could you be missing out on claiming all your business travel expenses? We all like to

Tom Serwatka, Business Advisor MV Small Business Development Center SUNY Institute of Technology serwatt@sunyit.edu 315-792-7557

Tom Serwatka, Business Advisor MV Small Business Development Center SUNY Institute of Technology serwatt@sunyit.edu 315-792-7557 1 Objectives of Presentation To walk you through the steps needed to create

Tom Serwatka, Business Advisor MV Small Business Development Center SUNY Institute of Technology serwatt@sunyit.edu 315-792-7557 1 Objectives of Presentation To walk you through the steps needed to create

How to Prepare a Cash Flow Forecast

The Orangeville & Area Small Business Enterprise Centre (SBEC) 87 Broadway, Orangeville ON L9W 1K1 519-941-0440 Ext. 2286 or 2291 sbec@orangeville.ca www.orangevillebusiness.ca Supported by its Partners:

The Orangeville & Area Small Business Enterprise Centre (SBEC) 87 Broadway, Orangeville ON L9W 1K1 519-941-0440 Ext. 2286 or 2291 sbec@orangeville.ca www.orangevillebusiness.ca Supported by its Partners:

Report Description. Business Counts. Top 10 States (by Business Counts) Page 1 of 16

Page 1 of 16") 5-Year County-Level Financial Profile Industry Report Architectural Services (SIC Code: 8712) in Prince George County, Maryland Sales Range: $500,000 - $999,999 Date: 11/07/08 Report Description This 5-Year

5-Year County-Level Financial Profile Industry Report Architectural Services (SIC Code: 8712) in Prince George County, Maryland Sales Range: $500,000 - $999,999 Date: 11/07/08 Report Description This 5-Year

The Merchant Securities FTSE 100. Hindsight II Note PRIVATE CLIENT ADVISORY

The Merchant Securities FTSE 100 Hindsight II Note Our first FTSE-100 Hindsight Note is now fully subscribed; however, as a result of exceptional investor demand we are launching the FTSE- 100 Hindsight

The Merchant Securities FTSE 100 Hindsight II Note Our first FTSE-100 Hindsight Note is now fully subscribed; however, as a result of exceptional investor demand we are launching the FTSE- 100 Hindsight

REC 3033 Commercial Recreation and Tourism. Class Week 12. The Dollars and Sense of Your Business. Preparation of Proforma Statements

REC 3033 Commercial Recreation and Tourism Class Week 12 The Dollars and Sense of Your Business Tourism operators not making large sums of money Tourism Canada Study (1995) average adventure travel operator

REC 3033 Commercial Recreation and Tourism Class Week 12 The Dollars and Sense of Your Business Tourism operators not making large sums of money Tourism Canada Study (1995) average adventure travel operator

Author: Theresa Klein Submitted to Sink or Swim Business Plan Competition 2010 The Seasteading Institute

Boundless Talent Consulting Services Facilitating immigration of high tech talent Author: Theresa Klein Submitted to Sink or Swim Business Plan Competition 2010 The Seasteading Institute This work is licensed

Boundless Talent Consulting Services Facilitating immigration of high tech talent Author: Theresa Klein Submitted to Sink or Swim Business Plan Competition 2010 The Seasteading Institute This work is licensed

Building a Financing Plan For the Entrepreneur For the Investor

Building a Financing Plan For the Entrepreneur For the Investor Founded by: Sections B asics Entrepreneur vs. Investor Fund Raising Environment Sources of information Questions Where do you start? You

Building a Financing Plan For the Entrepreneur For the Investor Founded by: Sections B asics Entrepreneur vs. Investor Fund Raising Environment Sources of information Questions Where do you start? You

ebrief for freelancers and contractors Borrowing company money

ebrief for freelancers and contractors Borrowing company money The facts behind the Directors Loan Account Taking money from the business for personal use when trading as a partnership or sole trader is

ebrief for freelancers and contractors Borrowing company money The facts behind the Directors Loan Account Taking money from the business for personal use when trading as a partnership or sole trader is

Business Planner. Your small business planning guide

Business Planner Your small business planning guide What s Inside the TD Canada Trust Business Planner Glossary...4 Your Business Profile What your business does or intends to do and your competitive advantage

Business Planner Your small business planning guide What s Inside the TD Canada Trust Business Planner Glossary...4 Your Business Profile What your business does or intends to do and your competitive advantage

ebrief for freelancers and contractors Car & motorcycle expenses for contractors

ebrief for freelancers and contractors Car & motorcycle expenses for contractors Personally owned cars and motorbikes: Are you really claiming all the travel and subsistence expenses you are entitled to?

ebrief for freelancers and contractors Car & motorcycle expenses for contractors Personally owned cars and motorbikes: Are you really claiming all the travel and subsistence expenses you are entitled to?

FINANCIAL RESULTS Q1 2012. 16 May 2012

FINANCIAL RESULTS Q1 2012 16 May 2012 Highlights Q1 2012 Satisfactory Q1 financials underlying EBITDA and profit before tax on a par with Q1 2011 - Lower power prices partly offset by increased power generation

FINANCIAL RESULTS Q1 2012 16 May 2012 Highlights Q1 2012 Satisfactory Q1 financials underlying EBITDA and profit before tax on a par with Q1 2011 - Lower power prices partly offset by increased power generation

1. A set of procedures for controlling cash payments by preparing and approving vouchers before payments are made is known as a voucher system.

Accounting II True/False Indicate whether the sentence or statement is true or false. 1. A set of procedures for controlling cash payments by preparing and approving vouchers before payments are made is

Accounting II True/False Indicate whether the sentence or statement is true or false. 1. A set of procedures for controlling cash payments by preparing and approving vouchers before payments are made is

Speed Grill Business Plan

Speed Grill Business Plan Prepared as a Sample Business Plan by Franchise Direct Franchisee Name Address Phone Number Email Copyright 2012 by Franchise Direct. All rights reserved. This material may not

Speed Grill Business Plan Prepared as a Sample Business Plan by Franchise Direct Franchisee Name Address Phone Number Email Copyright 2012 by Franchise Direct. All rights reserved. This material may not

Merchandising Operations

5 Merchandising Operations WHAT YOU PROBABLY ALREADY KNOW You want to order a pair of pants from a mail-order catalog. The price listed in the catalog is $50. There is a 10% off coupon in the catalog for

5 Merchandising Operations WHAT YOU PROBABLY ALREADY KNOW You want to order a pair of pants from a mail-order catalog. The price listed in the catalog is $50. There is a 10% off coupon in the catalog for

In this chapter, we build on the basic knowledge of how businesses

03-Seidman.qxd 5/15/04 11:52 AM Page 41 3 An Introduction to Business Financial Statements In this chapter, we build on the basic knowledge of how businesses are financed by looking at how firms organize

03-Seidman.qxd 5/15/04 11:52 AM Page 41 3 An Introduction to Business Financial Statements In this chapter, we build on the basic knowledge of how businesses are financed by looking at how firms organize

Performance Review. Sample Company

Performance Review Sample Company For the period ended 12/31/2017 Provided By Page 1 / 18 This report is designed to assist you in your business' development. Below you will find your overall ranking,

Performance Review Sample Company For the period ended 12/31/2017 Provided By Page 1 / 18 This report is designed to assist you in your business' development. Below you will find your overall ranking,

Chapter 1 The Scope of Corporate Finance

Chapter 1 The Scope of Corporate Finance MULTIPLE CHOICE 1. One of the tasks for financial managers when identifying projects that increase firm value is to identify those projects where a. marginal benefits

Chapter 1 The Scope of Corporate Finance MULTIPLE CHOICE 1. One of the tasks for financial managers when identifying projects that increase firm value is to identify those projects where a. marginal benefits

===============================

Business Plan Pages: 09 Work Al. Izzi / 131 Ellison Street / Paterson / 973-754-8695 / Correo Electronico izzaji@aol.com =============================== Cover Sheet Business Plan Begin the Plan with a

Business Plan Pages: 09 Work Al. Izzi / 131 Ellison Street / Paterson / 973-754-8695 / Correo Electronico izzaji@aol.com =============================== Cover Sheet Business Plan Begin the Plan with a

Financial Statement Preparation Webinar. Presented by Nick Chapman VEI Program Coordinator New York City

Financial Statement Preparation Webinar Presented by Nick Chapman VEI Program Coordinator New York City 122 Amsterdam Ave. New York, NY 10023 Phone: 212-769-2710 www.veinternational.org Objectives: Review

Financial Statement Preparation Webinar Presented by Nick Chapman VEI Program Coordinator New York City 122 Amsterdam Ave. New York, NY 10023 Phone: 212-769-2710 www.veinternational.org Objectives: Review

CHAPTER 2 ACCOUNTING STATEMENTS, TAXES, AND CASH FLOW

CHAPTER 2 ACCOUNTING STATEMENTS, TAXES, AND CASH FLOW Answers to Concepts Review and Critical Thinking Questions 1. True. Every asset can be converted to cash at some price. However, when we are referring

CHAPTER 2 ACCOUNTING STATEMENTS, TAXES, AND CASH FLOW Answers to Concepts Review and Critical Thinking Questions 1. True. Every asset can be converted to cash at some price. However, when we are referring

BUSINESS PLAN: SHANNON LOWERY ERIN FAIGHT CHRISTINA RULLO ALEC ROBERTSON

BUSINESS PLAN: SHANNON LOWERY ERIN FAIGHT CHRISTINA RULLO ALEC ROBERTSON LEGAL NAME: Groceries-R-Us BUSINESS DESCRIPTION: Our company will offer the service of delivering groceries to people who are unable

BUSINESS PLAN: SHANNON LOWERY ERIN FAIGHT CHRISTINA RULLO ALEC ROBERTSON LEGAL NAME: Groceries-R-Us BUSINESS DESCRIPTION: Our company will offer the service of delivering groceries to people who are unable

Performance Review for Electricity Now

Performance Review for Electricity Now For the period ending 03/31/2008 Provided By Mark Dashkewytch 780-963-5783 Report prepared for: Electricity Now Industry: 23821 - Electrical Contractors Revenue:

Performance Review for Electricity Now For the period ending 03/31/2008 Provided By Mark Dashkewytch 780-963-5783 Report prepared for: Electricity Now Industry: 23821 - Electrical Contractors Revenue:

BUSINESS LOAN APPLICATION

BUSINESS LOAN APPLICATION Superior National Bank & Trust Company 235 Quincy Street, P.O. Box 450 Hancock, MI 49930 phone 906.482.0404 toll-free 1.866.482.0404 1 INTRODUCTION Thank you for considering Superior

BUSINESS LOAN APPLICATION Superior National Bank & Trust Company 235 Quincy Street, P.O. Box 450 Hancock, MI 49930 phone 906.482.0404 toll-free 1.866.482.0404 1 INTRODUCTION Thank you for considering Superior

Institute of Certified Bookkeepers. Business Plan Template

Institute of Certified Bookkeepers Business Plan Template 2014 Executive Summary... 2 The Objective... 2 Keys to success... 3 The Mission... 3 Business Summary... 3 Start up phase... 4 Business Location

Institute of Certified Bookkeepers Business Plan Template 2014 Executive Summary... 2 The Objective... 2 Keys to success... 3 The Mission... 3 Business Summary... 3 Start up phase... 4 Business Location

Assuming office supplies are charged to the Office Supplies inventory account when purchased:

Adjusting Entries Prepaid Expenses Second Bullet Example - Assuming office supplies are charged to the Office Supplies inventory account when purchased: Office supplies expense 7,800 Office supplies 7,800

Adjusting Entries Prepaid Expenses Second Bullet Example - Assuming office supplies are charged to the Office Supplies inventory account when purchased: Office supplies expense 7,800 Office supplies 7,800

Financial Ratio Operating Statistics SURVEY

2013 Financial Ratio Operating Statistics SURVEY Compare your own numbers to the national norms, and find out where you need to focus to increase your profits. Balance Sheet Prior Year Assets Current Assets

2013 Financial Ratio Operating Statistics SURVEY Compare your own numbers to the national norms, and find out where you need to focus to increase your profits. Balance Sheet Prior Year Assets Current Assets

Please NOTE This example report is for a manufacturing company; however, we can address a similar report for any industry sector.

Please NOTE This example report is for a manufacturing company; however, we can address a similar report for any industry sector. Performance Review For the period ended 12/31/2013 Provided By Holbrook

Please NOTE This example report is for a manufacturing company; however, we can address a similar report for any industry sector. Performance Review For the period ended 12/31/2013 Provided By Holbrook

Business Example Car Wash Business Plan Soapy Rides Car Wash

Business Example Car Wash Business Plan Soapy Rides Car Wash http://www.bplans.com/car_wash_business_plan/company_summary_fc.php#.uciee6dwplu Read more: http://www.bplans.com/car_wash_business_plan/executive_summary_fc.php#ixzz22wl39guk