SPECIAL TAX ISSUES FOR EXPATRIATE AMERICANS

|

|

|

- Tracey Phelps

- 8 years ago

- Views:

Transcription

1 SPECIAL TAX ISSUES FOR EXPATRIATE AMERICANS Anthony Malik Point Square Consulting P: (770) F: (770) E: Presented: July, 2015 Atlanta Chapter, Georgia Association of Enrolled Agents

2 Objective Discussion regarding special international tax issues that effect Americans living abroad and immigrants to the U.S. The focus of this course will be on foreign retirement arrangements (i.e., pensions, non-u.s. social security, annuities etc.) and financial instruments.

3 Obligatory Items All Section ( ) references are to the U.S. Internal Revenue Code of 1986, as amended, and the U.S. Department of the Treasury regulations promulgated thereunder unless stated otherwise. Unless stated otherwise, the term tax means income tax. Disclaimer: Information contained herein is provided solely for educational benefits. No information contained herein is to be construed as the rendering of tax, legal or other professional advice by Point Square Consulting, Inc.

4 Agenda Overview of two broad areas that every tax practitioner with an expat client needs to be aware of: Foreign pension, retirement and social security type plans Foreign mutual funds, stocks, money market accounts and similar financial accounts

5 Foreign Retirement, Pension and Social Security Type Schemes ( Such Schemes ) American taxpayer moves to a foreign country to work for a foreign employer. American taxpayer is given the option to enroll in an employer provided non-u.s. retirement plan. American taxpayer is in for a nasty surprise

6 Tax Treatment of Such Schemes Tax treatment depends on the specifics of any given retirement arrangement Default rule: Three levels of taxation Treaty modifications (e.g., Canada and the U.K.) Form 8833 to elect treaty-based return positions $1,000 penalty for failing to disclose

Form 8833 to elect treaty-based return positions $1,000 penalty for")

7 Foreign Trust Reporting for Such Schemes Generally foreign trusts under U.S. law (Reg (a)) Trust reporting via Forms 3520/3520-A (PLRs , ) Applicable treaty articles do not prevent trust reporting $10,000 penalty per year per scheme ( 6677) Exception for foreign trust reporting provided only through specific administrative rulings (e.g., Canada)

8 Foreign Mutual Funds, Index Funds, Stocks and Similar Financial Accounts ( Such Financial Accounts ) It is the IRS s position that the onerous Passive Foreign Investment Company ( PFIC ) regime applies to such financial accounts (CCA ) PFIC classification ( 1297) Income test: 75% or more of the income is passive Asset test: 50% or more of the assets produce passive income

9 Tax Return Reporting Three alternative methods for PFIC income reporting via Form Deferred interest charge default method ( 1291) Qualified electing fund ( QEF ) election method ( 1295) Mark-to-market ( MTM ) election method ( 1296)

election method ( 1295)")

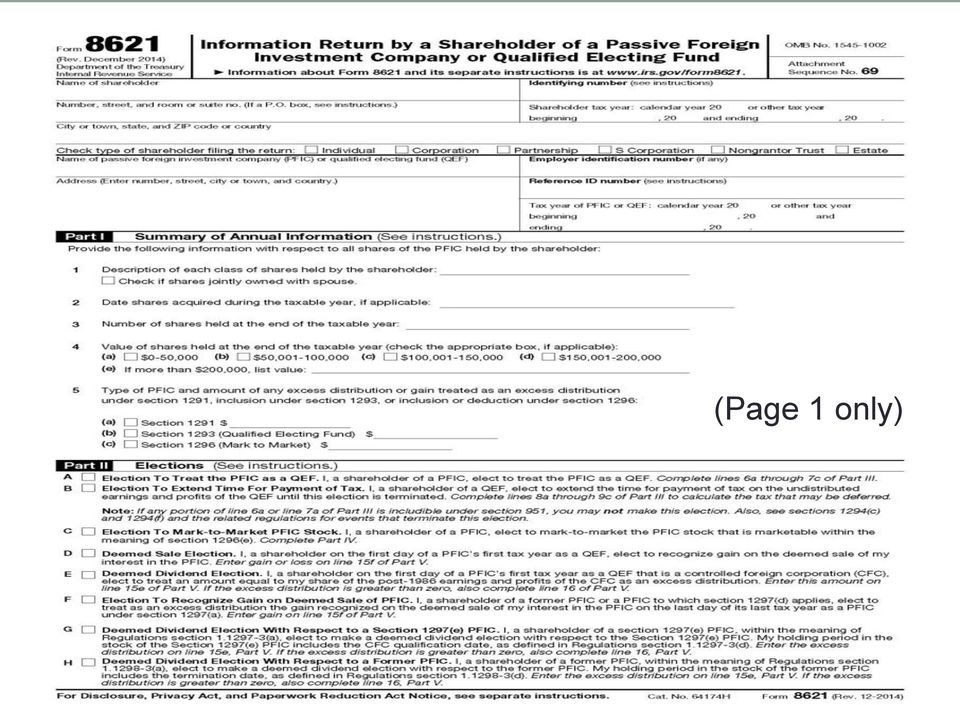

10 8621 (Page 1 only)

11 Taxation of 1291 Funds: A Very Simplified Illustration (Loosely Based on a Very Complex Actual Case) Nicholas ( Nick ) K., a U.S. citizen, invests in a single foreign mutual fund during The mutual fund pays dividends of $200 each during 2012 and Nick reports the dividends as ordinary dividends on his 2012 and 2013 Forms Nick sells the mutual fund at a gain in 2014 and reports the gain as a long-term gain. So far, so good, right?

12 Taxation of 1291 Funds: International Tax Horror Absolutely not! He s subject to, at the very minimum, a $10,000 penalty for FATCA and 1298(f) noncompliance. He s separately also subject to accuracy related penalties and interest.

noncompliance.")

13 Taxation of 1291 Funds: Methodology Correct dividend reporting Incorrect gain reporting The deferred interest charge method applies to the gain (Form 8621) Financial math (Basic idea): Spread the gain over the entire period of PFIC ownership Tax calculation based on the highest applicable rates for the year Interest calculation (using variable interest rates) Current day roll-forward

Current day")

14 Electing QEF Taxation Election to include a pro rata share of the fund s ordinary income and capital gains (dividends are never qualified) into the owner s taxable income Think partnership taxation Greatly reduces compliance costs but only available to shareholders provided with a PFIC Annual Information Statement (Reg (g))

15 (Presenter s comments and observations)

16 Late QEF Elections The election generally must be made during the year of fund acquisition (concept of pedigreed fund ) A QEF election for an unpedigreed fund also requires a deemed-sale election ( purging election ) to cleanse the PFIC taint ( 1291(d)(2)(A)) * Proceed with caution * Gain on PFIC sale = BOY FMV adjusted basis Taxpayer must recognize gain (taxed under 1291) ; losses are disallowed Thereafter file Form 8621 in every subsequent year for all QEFs

; losses are disallowed Thereafter file Form 8621 in every subsequent year for")

17 Electing MTM Taxation The MTM election is available only for marketable funds The MTM election allows recognition of realized gains Gain computation: EOY FMV BOY adjusted basis Income taxed at ordinary rates (2014 Form 1040, line 21) Losses are only allowed to the extent of unreversed inclusions ( 1296(d))

Losses are only allowed to the extent of unreversed")

18 Late MTM Elections Similar (not identical) to making a late QEF election Painful taxation in the year of untimely election because of the deemed-sale attributed to the EOY (versus BOY in the case of a late QEF election) The details are complicated. Basic idea: MTM treatment is inapplicable until the year following the late election whereas the default rules of 1291 fully apply in the year of late election (Reg (i)(2)) Dilemma: Instructions for Form 8621 are incorrect in a late MTM election scenario, i.e., the guidance conflicts with federal law.

(2)) Dilemma: Instructions for Form 8621 are incorrect in a late MTM election scenario, i.e., the guidance conflicts with federal law.")

19 PFIC Attribution Through Foreign Trusts Remember that most all foreign pension/retirement arrangements are trusts for U.S. tax purposes PFIC stock ownership through a trust is attributed to its beneficiaries ( 1298(a)(3)) Indirect ownership permits the IRS to directly tax the U.S. beneficiaries of the foreign trust (TAM ) Introduces considerable complexity as the income effectively becomes subject to two separate tax regimes, i.e., the PFIC regime and Subchapter J (fiduciaries)

20 Coordination of Election and Attribution Rules Presenter s Comments & Observations

21 Employee Trusts: The Opaque Doctrine PFIC attribution suspended for employee trusts (Reg (a)-0) Resultantly, U.S. beneficiaries not considered owners of the underlying assets thereby relieving them from filing Forms 8621, 8938, FBARs etc. This leads us to the question: What is an employee trust? (Which in turn necessitates discussing what are grantor, nongrantor and hybrid trusts.) Credit: Andrew Mitchell, Esq. Andrew Mitchell, LLC

22 Trusts in the Foreign Pension Context Most foreign pensions are classified as trusts under U.S. law Specific classification will depend on a given pension s unique financial and legal terms Grantor trusts: Donor is the beneficiary (fiscally transparent entity) Nongrantor trusts: Degree of separation is the determining factor Employee trusts: The law refers to employee trusts but provides no definition of such. Nongrantor trust in which the employer maintains a high degree of control.

23 Employee Trusts Employee trusts are conceptualized by reference to 402(b). Likely an employee trust if/when the trust is: Created by the employer for the benefit of the employee Administered by the employer on behalf of the employee Over 50% funded by the employer for the benefit of the employee Hybrid employee trusts Bifurcation requirement in the event that the employee s contributions exceed those of the employer (Reg (b)- 1(b)(6)). Opaque doctrine inapplicable to the portion of the trust treated as a grantor trust.

24 Role of Income Tax Treaties As previously discussed, treaties can modify the default taxation of foreign retirement arrangements In similar fashion, Reg T(b)(3)(ii) provides an exception to the PFIC reporting requirements when PFIC ownership is attributed through a foreign pension where a treaty allows deferral.

25 IRS Voluntary Disclosure Programs to Redress Prior-Year Noncompliance Offshore Voluntary Disclosure Program Streamlined Domestic Offshore Procedure Streamlined Foreign Offshore Procedure Delinquent International Information Return Submission Procedure Delinquent FBAR Submission Procedure Quiet disclosure (Not an IRS program per se)

26 Quick Recap Foreign retirement/pension schemes Default U.S. tax rule: No enjoyment of tax deferral unless specified by an applicable international tax treaty Trusts for U.S. tax purposes necessitating special tax reporting via Forms 3520 and 3520-A Passive Foreign Investment Companies ( PFICs ) The HIRE Act in 2010 imposed the onerous PFIC reporting requirements on certain forms of foreign financial instruments namely mutual funds, index funds, money market accounts etc. Three alternative methods of reporting PFIC income (i.e., default, QEF, MTM) via Form The default rules are punitive. PFIC ownership through trusts is attributable to the beneficiaries.

27 Suggested Further Reading Passive Foreign Investment Company Reporting: It s No Longer Just a Concern of the High-Net-Worth Investor, EA Journal, National Association of Enrolled Agents, September/October (Accessible to NAEA members at Discussion valid-to-date) Indirect Ownership of CFC and PFIC Shares by U.S. Beneficiaries of Foreign Trusts, Journal of Taxation, Thomson Reuters, February (Google-accessible Read for conceptual grounding only)

28 Questions?

Non-US Collective Investment Vehicles: Suitable Investments for US Taxpayers? Michael J. Legamaro

Non-US Collective Investment Vehicles: Suitable Investments for US Taxpayers? Michael J. Legamaro 480401032 Structure of Most CIVs Most non-us collective investment vehicles (i.e., funds) are organized

Non-US Collective Investment Vehicles: Suitable Investments for US Taxpayers? Michael J. Legamaro 480401032 Structure of Most CIVs Most non-us collective investment vehicles (i.e., funds) are organized

Tax Implications for US Citizens/Residents Moving to & Living in Canada

Tax Implications for US Citizens/Residents Moving to & Living in Canada TAX Julia Klann & Domeny Wu March 20, 2014 Topics to Discuss Moving to Canada & Overview of Canadian & US Tax Systems US Filing Requirements

Tax Implications for US Citizens/Residents Moving to & Living in Canada TAX Julia Klann & Domeny Wu March 20, 2014 Topics to Discuss Moving to Canada & Overview of Canadian & US Tax Systems US Filing Requirements

TAX CONSEQUENCES FOR U.S. CITIZENS AND OTHER U.S. PERSONS LIVING IN CANADA

March 2015 CONTENTS U.S. income tax filing requirements Non-filers U.S. foreign reporting requirements Foreign trusts Foreign corporations Foreign partnerships U.S. Social Security U.S. estate tax U.S.

March 2015 CONTENTS U.S. income tax filing requirements Non-filers U.S. foreign reporting requirements Foreign trusts Foreign corporations Foreign partnerships U.S. Social Security U.S. estate tax U.S.

international tax issues and reporting requirements

international tax issues and reporting requirements Foreign income exclusions and foreign tax credits can significantly reduce the taxes you pay on foreign sourced income and help you avoid double taxation.

international tax issues and reporting requirements Foreign income exclusions and foreign tax credits can significantly reduce the taxes you pay on foreign sourced income and help you avoid double taxation.

Presentation by Jennifer Coates for the American Immigration Lawyers Association

Tax Issues for Non- Citizens What Immigration Lawyers Need to Know Presentation by Jennifer Coates for the American Immigration Lawyers Association Principal, Jenny Coates Law, PLLC Seattle and Bainbridge,

Tax Issues for Non- Citizens What Immigration Lawyers Need to Know Presentation by Jennifer Coates for the American Immigration Lawyers Association Principal, Jenny Coates Law, PLLC Seattle and Bainbridge,

INTERNATIONAL TIDBIT: Reporting Foreign Investments New Requirements for the 2013 Tax Year

INTERNATIONAL TIDBIT: Reporting Foreign Investments New Requirements for the 2013 Tax Year The last few years have seen increased emphasis on individuals reporting about their foreign investments and penalizing

INTERNATIONAL TIDBIT: Reporting Foreign Investments New Requirements for the 2013 Tax Year The last few years have seen increased emphasis on individuals reporting about their foreign investments and penalizing

Top 10 Tax Considerations for U.S. Citizens Living in Canada

Top 10 Tax Considerations for U.S. Citizens Living in Canada Recent Canadian media reports have estimated that there are approximately one million U.S. citizens living in Canada and that a relatively low

Top 10 Tax Considerations for U.S. Citizens Living in Canada Recent Canadian media reports have estimated that there are approximately one million U.S. citizens living in Canada and that a relatively low

57 th UIA CONGRESS Macau / China October 31 November 4, 2013 IMMIGRATION AND NATIONALITY LAW GLOBAL TRENDS ON CITIZENSHIP AND NATIONALITY

57 th UIA CONGRESS Macau / China October 31 November 4, 2013 IMMIGRATION AND NATIONALITY LAW Saturday, November 2, 2013 GLOBAL TRENDS ON CITIZENSHIP AND NATIONALITY UIA 2013 THE TAX ISSUES PROMOTING, AND

57 th UIA CONGRESS Macau / China October 31 November 4, 2013 IMMIGRATION AND NATIONALITY LAW Saturday, November 2, 2013 GLOBAL TRENDS ON CITIZENSHIP AND NATIONALITY UIA 2013 THE TAX ISSUES PROMOTING, AND

US Citizens Living in Canada

US Citizens Living in Canada Income Tax Considerations 1) I am a US citizen living in Canada. What are my income tax filing and reporting requirements? US Income Tax Returns A US citizen residing in Canada

US Citizens Living in Canada Income Tax Considerations 1) I am a US citizen living in Canada. What are my income tax filing and reporting requirements? US Income Tax Returns A US citizen residing in Canada

REPORT OFFERING PROPOSED GUIDANCE REGARDING THE PASSIVE FOREIGN INVESTMENT COMPANY RULES

REPORT OFFERING PROPOSED GUIDANCE REGARDING THE PASSIVE FOREIGN INVESTMENT COMPANY RULES The Committee on Taxation of Business Entities September 21, 2009 Table of Contents Page I. INTRODUCTION...- 1 -

REPORT OFFERING PROPOSED GUIDANCE REGARDING THE PASSIVE FOREIGN INVESTMENT COMPANY RULES The Committee on Taxation of Business Entities September 21, 2009 Table of Contents Page I. INTRODUCTION...- 1 -

U.S. / ISRAELI INCOME TAX UPDATE FOR YEAR 2015 (2014 Tax Year)

") 02-999-2104, 03-527-3254, 09-746-0623 Cellular: 052-274-9999 Fax: 02-991-0195 Email: alan@ardcpa.com Website: www.ardcpa.com U.S. / ISRAELI INCOME TAX UPDATE FOR YEAR 2015 (2014 Tax Year) The 2014 U.S.

02-999-2104, 03-527-3254, 09-746-0623 Cellular: 052-274-9999 Fax: 02-991-0195 Email: alan@ardcpa.com Website: www.ardcpa.com U.S. / ISRAELI INCOME TAX UPDATE FOR YEAR 2015 (2014 Tax Year) The 2014 U.S.

New Year brings new US Reporting requirement introducing Form 8938 Statement of Specified Foreign Financial Assets

New Year brings new US Reporting requirement introducing Form 8938 Statement of Specified Foreign Financial Assets Arthur J. Dichter Cantor & Webb P.A., Miami FL The following article gives an overview

New Year brings new US Reporting requirement introducing Form 8938 Statement of Specified Foreign Financial Assets Arthur J. Dichter Cantor & Webb P.A., Miami FL The following article gives an overview

TOP TEN INVESTMENT MISTAKES MADE BY AMERICANS ABROAD

TOP TEN INVESTMENT MISTAKES MADE BY AMERICANS ABROAD January 2015 1) Buying foreign mutual funds. Foreign mutual funds may seem attractive to an American living abroad. However, in the view of the IRS,

TOP TEN INVESTMENT MISTAKES MADE BY AMERICANS ABROAD January 2015 1) Buying foreign mutual funds. Foreign mutual funds may seem attractive to an American living abroad. However, in the view of the IRS,

U.S. Taxation and information reporting for foreign trusts and their U.S. owners and U.S. beneficiaries

Private Company Services U.S. Taxation and information reporting for foreign trusts and their U.S. owners and U.S. beneficiaries United States (U.S.) owners and beneficiaries of foreign trusts (i.e., non-u.s.

Private Company Services U.S. Taxation and information reporting for foreign trusts and their U.S. owners and U.S. beneficiaries United States (U.S.) owners and beneficiaries of foreign trusts (i.e., non-u.s.

Corrective U.S. Tax Compliance for Dual Status and Foreign Taxpayers Andrew Bernknopf, Esq., Member:

Corrective U.S. Tax Compliance for Dual Status and Foreign Taxpayers Andrew Bernknopf, Esq., Member: This article provides an overview of corrective United States tax compliance measures for individuals

Corrective U.S. Tax Compliance for Dual Status and Foreign Taxpayers Andrew Bernknopf, Esq., Member: This article provides an overview of corrective United States tax compliance measures for individuals

Taxing Decisions. Gary S. Wolfe and Allen Walburn

Taxing Decisions U.S.-Based Hedge Funds And Offshore Reinsurance Gary S. Wolfe and Allen Walburn U.S.-Based Hedge Funds And Offshore Reinsurance Gary S. Wolfe and Allen Walburn U.S.-based hedge funds are

Taxing Decisions U.S.-Based Hedge Funds And Offshore Reinsurance Gary S. Wolfe and Allen Walburn U.S.-Based Hedge Funds And Offshore Reinsurance Gary S. Wolfe and Allen Walburn U.S.-based hedge funds are

USA Taxation. 3.1 Taxation of funds. Taxation of regulated investment companies: income tax

USA Taxation FUNDS AND FUND MANAGEMENT 2010 3.1 Taxation of funds Taxation of regulated investment companies: income tax Investment companies in the United States (US) are structured either as openend

USA Taxation FUNDS AND FUND MANAGEMENT 2010 3.1 Taxation of funds Taxation of regulated investment companies: income tax Investment companies in the United States (US) are structured either as openend

Representing U.S.-Swiss Dual Passport Holders in IRS Voluntary Disclosure Cases

Volume 55, Number 9 August 31, 2009 Representing U.S.-Swiss Dual Passport Holders in IRS Voluntary Disclosure Cases by William M. Sharp Sr. and Natalie Peter Reprinted from Tax Notes Int l, August 31,

Volume 55, Number 9 August 31, 2009 Representing U.S.-Swiss Dual Passport Holders in IRS Voluntary Disclosure Cases by William M. Sharp Sr. and Natalie Peter Reprinted from Tax Notes Int l, August 31,

CALIFORNIA STATE BAR TAXATION SECTION TAX PROCEDURE AND LITIGATION COMMITTEE AND INTERNATIONAL TAX COMMITTEE

CALIFORNIA STATE BAR TAXATION SECTION TAX PROCEDURE AND LITIGATION COMMITTEE AND INTERNATIONAL TAX COMMITTEE A SIMPLIFIED PROCEDURE TO ALLOW LATE FILED FORMS 8891 FOR INDIVIDUALS WITH CANADIAN RETIREMENT

CALIFORNIA STATE BAR TAXATION SECTION TAX PROCEDURE AND LITIGATION COMMITTEE AND INTERNATIONAL TAX COMMITTEE A SIMPLIFIED PROCEDURE TO ALLOW LATE FILED FORMS 8891 FOR INDIVIDUALS WITH CANADIAN RETIREMENT

Radio X June 19 Broadcast Foreign Asset Reporting Questions & Answers

Radio X June 19 Broadcast Foreign Asset Reporting Questions & Answers 1. What is the FBAR filing? FBAR is the acronym for the Foreign Bank Account Report that must be filed annually with the IRS to report

Radio X June 19 Broadcast Foreign Asset Reporting Questions & Answers 1. What is the FBAR filing? FBAR is the acronym for the Foreign Bank Account Report that must be filed annually with the IRS to report

Pre-Immigration Tax Planning and Post-Immigration Tax Compliance for EB-5 Investors

Pre-Immigration Tax Planning and Post-Immigration Tax Compliance for EB-5 Investors Alan Winston Granwell DLA Piper Steve Trow Trow & Rahal, PC This presentation is offered for informational purposes only

Pre-Immigration Tax Planning and Post-Immigration Tax Compliance for EB-5 Investors Alan Winston Granwell DLA Piper Steve Trow Trow & Rahal, PC This presentation is offered for informational purposes only

May 7, 2012 California Bar Suggests Guidance, Safe Harbor to Aid Foreign Pension Beneficiaries

May 7, 2012 California Bar Suggests Guidance, Safe Harbor to Aid Foreign Pension Beneficiaries Philip D.W. Hodgen and Steven L. Walker of the California State Bar Taxation Section proposed that the IRS

May 7, 2012 California Bar Suggests Guidance, Safe Harbor to Aid Foreign Pension Beneficiaries Philip D.W. Hodgen and Steven L. Walker of the California State Bar Taxation Section proposed that the IRS

Foreign Financial Account & Asset Reporting: FinCen (FBAR) v. FATCA

v. FATCA") Foreign Financial Account & Asset Reporting: FinCen (FBAR) v. FATCA Presented by David J Lewis, Attorney, of Krugliak, Wilkins, Griffiths & Dougherty Co. LPA and Patricia L Gibbs, CPA, of CBIZ MHM September

Foreign Financial Account & Asset Reporting: FinCen (FBAR) v. FATCA Presented by David J Lewis, Attorney, of Krugliak, Wilkins, Griffiths & Dougherty Co. LPA and Patricia L Gibbs, CPA, of CBIZ MHM September

Pre-Immigration Planning

Estate Planners Day 2013 Estate Planning Council Pre-Immigration Planning Kathryn von Matthiessen Cantor & Webb, P.A. May 8, 2013 Resident/Nonresident Domiciliary/Nondomiciliary RESIDENT DOMICILIARY NONRESIDENT

Estate Planners Day 2013 Estate Planning Council Pre-Immigration Planning Kathryn von Matthiessen Cantor & Webb, P.A. May 8, 2013 Resident/Nonresident Domiciliary/Nondomiciliary RESIDENT DOMICILIARY NONRESIDENT

[LOGO] ROGERS COMMUNICATIONS INC. DIVIDEND REINVESTMENT PLAN. November 1, 2010

![[LOGO] ROGERS COMMUNICATIONS INC. DIVIDEND REINVESTMENT PLAN. November 1, 2010](/thumbs/30/14484201.jpg "[LOGO] ROGERS COMMUNICATIONS INC. DIVIDEND REINVESTMENT PLAN. November 1, 2010") [LOGO] ROGERS COMMUNICATIONS INC. DIVIDEND REINVESTMENT PLAN November 1, 2010 Rogers Communications Inc. Dividend Reinvestment Plan Table of Contents SUMMARY... 3 DEFINITIONS... 4 ELIGIBILITY... 6 ENROLLMENT...

[LOGO] ROGERS COMMUNICATIONS INC. DIVIDEND REINVESTMENT PLAN November 1, 2010 Rogers Communications Inc. Dividend Reinvestment Plan Table of Contents SUMMARY... 3 DEFINITIONS... 4 ELIGIBILITY... 6 ENROLLMENT...

International Tax Developments Inbound Update. By Robert A. Chaves, Esq. Gutter Chaves Josepher Rubin Forman Fleisher P.A.

International Tax Developments Inbound Update By Robert A. Chaves, Esq. Gutter Chaves Josepher Rubin Forman Fleisher P.A. I. Legislative/Statutory Updates A. Suspension of Three Year Assessment Limitation

International Tax Developments Inbound Update By Robert A. Chaves, Esq. Gutter Chaves Josepher Rubin Forman Fleisher P.A. I. Legislative/Statutory Updates A. Suspension of Three Year Assessment Limitation

Ellen Harrison. Philadelphia Estate Planning Council ( PEPC ) October 21, 2014

October 21, 2014") Ellen Harrison Philadelphia Estate Planning Council ( PEPC ) October 21, 2014 Topics to be covered Who and what is foreign under the Code and treaties US taxation of citizens regardless of residency Limited

Ellen Harrison Philadelphia Estate Planning Council ( PEPC ) October 21, 2014 Topics to be covered Who and what is foreign under the Code and treaties US taxation of citizens regardless of residency Limited

United States Tax Alert

International Tax United States Tax Alert Contacts Jeff O Donnell jodonnell@deloitte.com Paul Crispino pcrispino@deloitte.com Jason Robertson jarobertson@deloitte.com April 6, 2016 Anti-Inversion Guidance:

International Tax United States Tax Alert Contacts Jeff O Donnell jodonnell@deloitte.com Paul Crispino pcrispino@deloitte.com Jason Robertson jarobertson@deloitte.com April 6, 2016 Anti-Inversion Guidance:

Tax Management International Journal

Tax Management International Journal Reproduced with permission from Tax Management International Journal, 44 TMIJ 220, 04/10/2015. Copyright 2015 by The Bureau of National Affairs, Inc. (800-372- 1033)

Tax Management International Journal Reproduced with permission from Tax Management International Journal, 44 TMIJ 220, 04/10/2015. Copyright 2015 by The Bureau of National Affairs, Inc. (800-372- 1033)

Instructions for Form 8938 (Rev. December 2014)

") Instructions for Form 8938 (Rev. December 2014) Statement of Specified Foreign Financial Assets Department of the Treasury Internal Revenue Service Section references are to the Internal Revenue Code unless

Instructions for Form 8938 (Rev. December 2014) Statement of Specified Foreign Financial Assets Department of the Treasury Internal Revenue Service Section references are to the Internal Revenue Code unless

Instructions for Form 8960

2014 Instructions for Form 8960 Net Investment Income Tax Individuals, Estates, and Trusts Department of the Treasury Internal Revenue Service Section references are to the Internal Revenue Code unless

2014 Instructions for Form 8960 Net Investment Income Tax Individuals, Estates, and Trusts Department of the Treasury Internal Revenue Service Section references are to the Internal Revenue Code unless

Your Taxes: IRS grants 3-week extension for its tax-amnesty program

Your Taxes: IRS grants 3-week extension for its tax-amnesty program Sep. 22, 2009 KEVIN E. PACKMAN and LEON HARRIS, THE JERUSALEM POST This article is an urgent update for US taxpayers... and it comes

Your Taxes: IRS grants 3-week extension for its tax-amnesty program Sep. 22, 2009 KEVIN E. PACKMAN and LEON HARRIS, THE JERUSALEM POST This article is an urgent update for US taxpayers... and it comes

United States. A-Z of U.S. Estate Planning Concepts

United States A-Z of U.S. Estate Planning Concepts This glossary is directed mainly at the solicitor whose clients are American, have assets in America, or U.S. family members who are beneficiaries of

United States A-Z of U.S. Estate Planning Concepts This glossary is directed mainly at the solicitor whose clients are American, have assets in America, or U.S. family members who are beneficiaries of

MOODYS LLP TAX ADVISORS 21-MARCH-2011 CALGARY

MOODYS LLP TAX ADVISORS 21-MARCH-2011 CALGARY CANADA/U.S. TAX AND ESTATE PLANNING CROSS-BORDER ISSUES Presented by Edward C. Northwood, Esq. Of Counsel THE RUCHELMAN LAW FIRM Toronto-Dominion Centre, Royal

MOODYS LLP TAX ADVISORS 21-MARCH-2011 CALGARY CANADA/U.S. TAX AND ESTATE PLANNING CROSS-BORDER ISSUES Presented by Edward C. Northwood, Esq. Of Counsel THE RUCHELMAN LAW FIRM Toronto-Dominion Centre, Royal

PATH Act Provides Favorable New Rules for Foreign Real Estate Investment Through REITs

Tax Practice Group December 23, 2015 PATH Act Provides Favorable New Rules for Foreign Real Estate Investment Through REITs For more information, contact: Kathryn M. Furman +1 404 572 3599 kfurman@kslaw.com

Tax Practice Group December 23, 2015 PATH Act Provides Favorable New Rules for Foreign Real Estate Investment Through REITs For more information, contact: Kathryn M. Furman +1 404 572 3599 kfurman@kslaw.com

Instructions for Form 8938

2015 Instructions for Form 8938 Statement of Specified Foreign Financial Assets Department of the Treasury Internal Revenue Service Section references are to the Internal Revenue Code unless otherwise

2015 Instructions for Form 8938 Statement of Specified Foreign Financial Assets Department of the Treasury Internal Revenue Service Section references are to the Internal Revenue Code unless otherwise

Dispelling Fear! What are your fears?! - Criminal implications! - Cost of penalties! - Cost of getting compliant with advisors!

Dispelling Fear! What are your fears?! - Criminal implications! - Cost of penalties! - Cost of getting compliant with advisors! Do not fear the consequences, get the facts:! Each Individual is unique!

Dispelling Fear! What are your fears?! - Criminal implications! - Cost of penalties! - Cost of getting compliant with advisors! Do not fear the consequences, get the facts:! Each Individual is unique!

Americans in the UK Need to Avoid this Catch-22 Investment Trap

Americans in the UK Need to Avoid this Catch-22 Investment Trap By David Kuenzi, Thun Financial Advisors, Copyright 2015 2015 Summary The U.S. Passive Foreign Investment Company (PFIC) tax regime raises

Americans in the UK Need to Avoid this Catch-22 Investment Trap By David Kuenzi, Thun Financial Advisors, Copyright 2015 2015 Summary The U.S. Passive Foreign Investment Company (PFIC) tax regime raises

US Taxpayers Participating in Non US Retirement Plans: When is There an FBAR or FATCA Reporting Obligation?

February 29, 2012 Authors: Anubhav Gogna and David W. Powell If you have questions, please contact your regular Groom attorney or any of the attorneys listed below: Anubhav Gogna agogna@groom.com (202)

February 29, 2012 Authors: Anubhav Gogna and David W. Powell If you have questions, please contact your regular Groom attorney or any of the attorneys listed below: Anubhav Gogna agogna@groom.com (202)

Canadian RRSPs, RRIFs and Other Foreign Funded Retirement Plans: Tax Planning and Reporting for 402(b) Funded Plans

Funded Plans") FOR LIVE PROGRAM ONLY Canadian RRSPs, RRIFs and Other Foreign Funded Retirement Plans: Tax Planning and Reporting for 402(b) Funded Plans TUESDAY, JUNE 7, 2016, 1:00-2:50 pm Eastern IMPORTANT INFORMATION

FOR LIVE PROGRAM ONLY Canadian RRSPs, RRIFs and Other Foreign Funded Retirement Plans: Tax Planning and Reporting for 402(b) Funded Plans TUESDAY, JUNE 7, 2016, 1:00-2:50 pm Eastern IMPORTANT INFORMATION

Delivering U.S. International Tax Advice to U.S. Clients Doing Business Abroad

Delivering U.S. International Tax Advice to U.S. Clients Doing Business Abroad OGLE INTERNATIONAL TAX ADVISORS www.ogleintltax.com OUR INTERNATIONAL TAX PRACTICE INCLUDES BOTH CPAS AND ATTORNEYS WITH BIG

Delivering U.S. International Tax Advice to U.S. Clients Doing Business Abroad OGLE INTERNATIONAL TAX ADVISORS www.ogleintltax.com OUR INTERNATIONAL TAX PRACTICE INCLUDES BOTH CPAS AND ATTORNEYS WITH BIG

Nonqualified Deferred Compensation Plans Why Administration Matters

Nonqualified Deferred Compensation Plans Why Administration Matters By: Howard D. Stern, FSA Vice President & Actuary The Pangburn Company HOWARD D. STERN, FSA is Vice President and Actuary with the Pangburn

Nonqualified Deferred Compensation Plans Why Administration Matters By: Howard D. Stern, FSA Vice President & Actuary The Pangburn Company HOWARD D. STERN, FSA is Vice President and Actuary with the Pangburn

US Tax Issues for Canadian Residents

US Tax Issues for Canadian Residents SPECIAL REPORT US Tax Issues for Canadian Residents The IRS has recently declared new catch up filing procedures for non-resident US taxpayers who are considered innocent

US Tax Issues for Canadian Residents SPECIAL REPORT US Tax Issues for Canadian Residents The IRS has recently declared new catch up filing procedures for non-resident US taxpayers who are considered innocent

DEPARTMENT OF THE TREASURY TECHNICAL EXPLANATION OF THE PROTOCOL BETWEEN THE UNITED STATES OF AMERICA AND

DEPARTMENT OF THE TREASURY TECHNICAL EXPLANATION OF THE PROTOCOL BETWEEN THE UNITED STATES OF AMERICA AND THE FRENCH REPUBLIC SIGNED AT WASHINGTON ON DECEMBER 8, 2004 AMENDING THE CONVENTION BETWEEN THE

DEPARTMENT OF THE TREASURY TECHNICAL EXPLANATION OF THE PROTOCOL BETWEEN THE UNITED STATES OF AMERICA AND THE FRENCH REPUBLIC SIGNED AT WASHINGTON ON DECEMBER 8, 2004 AMENDING THE CONVENTION BETWEEN THE

FATCA (Foreign Account Tax Compliance Act): What American Investors Need to Know Now

: What American Investors Need to Know Now") FATCA (Foreign Account Tax Compliance Act): What American Investors Need to Know Now Article Summary This article examines the new FATCA law (Foreign Account Tax Compliance Act) and explains the significant

FATCA (Foreign Account Tax Compliance Act): What American Investors Need to Know Now Article Summary This article examines the new FATCA law (Foreign Account Tax Compliance Act) and explains the significant

THE INCOME TAXATION OF ESTATES & TRUSTS

The income taxation of estates and trusts can be complex because, as with partnerships, estates and trusts are a hybrid entity for income tax purposes. Trusts and estates are treated as an entity for certain

The income taxation of estates and trusts can be complex because, as with partnerships, estates and trusts are a hybrid entity for income tax purposes. Trusts and estates are treated as an entity for certain

IRS Issues Final and New Proposed Regulations Implementing the 3.8% Tax on Investment Income

IRS Issues Final and New Proposed Regulations Implementing the 3.8% Tax on Investment Income Final Regulations and New Proposed Regulations Implement the 3.8% Tax on Net Investment Income of Individuals,

IRS Issues Final and New Proposed Regulations Implementing the 3.8% Tax on Investment Income Final Regulations and New Proposed Regulations Implement the 3.8% Tax on Net Investment Income of Individuals,

FBAR Foreign Bank Account Reporting

FBAR Foreign Bank Account Reporting ------------------------------------------------------------------------------------------------------------ Form TD F 90-22.1 is required when a U.S. Person has a financial

FBAR Foreign Bank Account Reporting ------------------------------------------------------------------------------------------------------------ Form TD F 90-22.1 is required when a U.S. Person has a financial

IRS Issues Reliance Proposed Regulations On Some Net Investment Income Tax Issues. Background

/////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////// Special Report Series on Section 1411

/////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////// Special Report Series on Section 1411

Tax Considerations Of Foreign

FIRPTA requires that a buyer withhold 10% of the gross sales price, subject to certain exceptions, and send it to the Internal Revenue Service if the seller is a foreign person. U.S. Taxes Foreign investors

FIRPTA requires that a buyer withhold 10% of the gross sales price, subject to certain exceptions, and send it to the Internal Revenue Service if the seller is a foreign person. U.S. Taxes Foreign investors

TAX PLANNING FOR INDIVIDUALS. Selected Tax Issues

CANADA-U.S. US TAX PLANNING FOR INDIVIDUALS Selected Tax Issues [May 2015] By: Michael Cadesky and Edward Northwood C A D E S K Y A N D A S S O C I A T E S LLP CANADIAN, U.S. AND INTERNATIONAL TAX SPECIALISTS

CANADA-U.S. US TAX PLANNING FOR INDIVIDUALS Selected Tax Issues [May 2015] By: Michael Cadesky and Edward Northwood C A D E S K Y A N D A S S O C I A T E S LLP CANADIAN, U.S. AND INTERNATIONAL TAX SPECIALISTS

How To Disclose Your Foreign Bank Accounts And Avoid Criminal Prosecution! FIVE STONE. tax advisers

How To Disclose Your Foreign Bank Accounts And Avoid Criminal Prosecution! Do you have or think you may have a foreign bank account that should be disclosed to the United States Government? Have you received

How To Disclose Your Foreign Bank Accounts And Avoid Criminal Prosecution! Do you have or think you may have a foreign bank account that should be disclosed to the United States Government? Have you received

October 23, 2015. Ann Marie Regal, CFP Wealth Manager +65 9146 1862 amregal@globaleye.sg

October 23, 2015 Ann Marie Regal, CFP Wealth Manager +65 9146 1862 amregal@globaleye.sg Aron Lanie Wealth Manager +84 (0) 938531784 alanie@globaleye.com Disclaimer The information presented herein is for

October 23, 2015 Ann Marie Regal, CFP Wealth Manager +65 9146 1862 amregal@globaleye.sg Aron Lanie Wealth Manager +84 (0) 938531784 alanie@globaleye.com Disclaimer The information presented herein is for

INTERNATIONAL TAX CONTROVERSY

INTERNATIONAL TAX CONTROVERSY BY MISHKIN SANTA PETER MITCHELL About Us Who we are What we do Why we re here Part I: International Tax Controversy Voluntary Disclosure Attorney-client privilege IRM 9.5.11.9

INTERNATIONAL TAX CONTROVERSY BY MISHKIN SANTA PETER MITCHELL About Us Who we are What we do Why we re here Part I: International Tax Controversy Voluntary Disclosure Attorney-client privilege IRM 9.5.11.9

Article 1. Paragraph 3 of Article IV Dual resident companies

DEPARTMENT OF THE TREASURY TECHNICAL EXPLANATION OF THE PROTOCOL DONE AT CHELSEA ON SEPTEMBER 21, 2007 AMENDING THE CONVENTION BETWEEN THE UNITED STATES OF AMERICA AND CANADA WITH RESPECT TO TAXES ON INCOME

DEPARTMENT OF THE TREASURY TECHNICAL EXPLANATION OF THE PROTOCOL DONE AT CHELSEA ON SEPTEMBER 21, 2007 AMENDING THE CONVENTION BETWEEN THE UNITED STATES OF AMERICA AND CANADA WITH RESPECT TO TAXES ON INCOME

Hedge Funds: Tax Advantages and Liabilities

Presenting a live 110-minute teleconference with interactive Q&A Hedge Funds: Tax Advantages and Liabilities for Investors and Fund Managers Leveraging Qualified Dividend Income, Net Investment Tax, Management

Presenting a live 110-minute teleconference with interactive Q&A Hedge Funds: Tax Advantages and Liabilities for Investors and Fund Managers Leveraging Qualified Dividend Income, Net Investment Tax, Management

IRS regulations The Foreign Account Tax Compliance Act (FATCA) and its impact on the US foreign withholding tax and reporting system

and its impact on the US foreign withholding tax and reporting system") IRS regulations The Foreign Account Tax Compliance Act (FATCA) and its impact on the US foreign withholding tax and reporting system What is FATCA? The Foreign Account Tax Compliance Act (FATCA) is a new

IRS regulations The Foreign Account Tax Compliance Act (FATCA) and its impact on the US foreign withholding tax and reporting system What is FATCA? The Foreign Account Tax Compliance Act (FATCA) is a new

Simplified Instructions for Completing a Form W-8BEN-E

Simplified Instructions for Completing a Form W-8BEN-E For Non-Financial Institutions Only Updated April 2015 Circular 230 Disclaimer: Any tax advice contained in this communication is not intended or

Simplified Instructions for Completing a Form W-8BEN-E For Non-Financial Institutions Only Updated April 2015 Circular 230 Disclaimer: Any tax advice contained in this communication is not intended or

Professional Tax Preparation and Consulting Engagement Agreement American Expat Tax Services Pte Ltd (Singapore Reg. No.

DISCLAIMER: and (SPOUSE/if filing Jointly) the undersigned taxpayer (s) hereby engage the services of American Expat Tax Services, Pte Limited (referred to hereinafter as AETS) as a U.S. tax preparation

DISCLAIMER: and (SPOUSE/if filing Jointly) the undersigned taxpayer (s) hereby engage the services of American Expat Tax Services, Pte Limited (referred to hereinafter as AETS) as a U.S. tax preparation

Tax Consequences for Canadians Doing Business in the U.S.

April 2012 CONTENTS U.S. basis of taxation The benefits of the Canada-U.S. tax treaty U.S. filing requirements U.S. taxpayer identification U.S. withholding Tax U.S. state taxation Other considerations

April 2012 CONTENTS U.S. basis of taxation The benefits of the Canada-U.S. tax treaty U.S. filing requirements U.S. taxpayer identification U.S. withholding Tax U.S. state taxation Other considerations

Spin-Off of Time Warner Cable Inc. Tax Information Statement As of March 19, 2009

Spin-Off of Time Warner Cable Inc. Tax Information Statement As of March 19, 2009 On March 12, 2009, Time Warner Inc. ( Time Warner ) completed the spin-off (the Spin-Off ) of Time Warner s ownership interest

Spin-Off of Time Warner Cable Inc. Tax Information Statement As of March 19, 2009 On March 12, 2009, Time Warner Inc. ( Time Warner ) completed the spin-off (the Spin-Off ) of Time Warner s ownership interest

SPECIAL REPORT state tax notes

Spring Cleaning for the Massachusetts Legislature and the DOR by Matthew A. Morris Matthew A. Morris Matthew A. Morris is a partner at Kerstein, Coren & Lichtenstein LLP, Wellesley, Massachusetts. His

Spring Cleaning for the Massachusetts Legislature and the DOR by Matthew A. Morris Matthew A. Morris Matthew A. Morris is a partner at Kerstein, Coren & Lichtenstein LLP, Wellesley, Massachusetts. His

FOREIGN INCOME, ASSETS, AND IRS AMNESTY PROGRAMS

FOREIGN INCOME, ASSETS, AND IRS AMNESTY PROGRAMS Ahuja & Clark, PLLC By: Madhu Ahuja, CPA, CVA, CFE Ravi Modi, CPA www.ahujaclark.com WHO IS SUBJECT TO TAX FILING REQUIREMENTS? U.S. Citizen and Green Card

FOREIGN INCOME, ASSETS, AND IRS AMNESTY PROGRAMS Ahuja & Clark, PLLC By: Madhu Ahuja, CPA, CVA, CFE Ravi Modi, CPA www.ahujaclark.com WHO IS SUBJECT TO TAX FILING REQUIREMENTS? U.S. Citizen and Green Card

Foreign Account Tax Compliance Act ( FATCA ) How Does It Affect NFFEs and Individuals

How Does It Affect NFFEs and Individuals") Foreign Account Tax Compliance Act ( FATCA ) How Does It Affect NFFEs and Individuals May, 2012 2008 Venable LLP 1 agenda Overview FATCA and NFFEs FATCA and Individuals US Information Reporting for US

Foreign Account Tax Compliance Act ( FATCA ) How Does It Affect NFFEs and Individuals May, 2012 2008 Venable LLP 1 agenda Overview FATCA and NFFEs FATCA and Individuals US Information Reporting for US

Income Tax and Social Insurance

The Global Employer: Focus on Global Immigration & Mobility Income Tax and Social Insurance An employee who works abroad is always concerned about the possibility of increased income taxation and social

The Global Employer: Focus on Global Immigration & Mobility Income Tax and Social Insurance An employee who works abroad is always concerned about the possibility of increased income taxation and social

Expatriation - A Comparison of Tax Issues in the US & UK in an Increasingly Mobile World

Expatriation - A Comparison of Tax Issues in the US & UK in an Increasingly Mobile World Henry Christensen III Jay E. Rivlin www.mwe.com Boston Brussels Chicago Düsseldorf Frankfurt Houston London Los

Expatriation - A Comparison of Tax Issues in the US & UK in an Increasingly Mobile World Henry Christensen III Jay E. Rivlin www.mwe.com Boston Brussels Chicago Düsseldorf Frankfurt Houston London Los

Incentive Stock Options

JPH Advisory Group Curtis Hearn, CFP 600 Galleria Pkwy Ste 1600 Atlanta, GA 30339 770-859-0076 curtis@jphadvisory.com www.jphadvisory.com Incentive Stock Options Page 1 of 6, see disclaimer on final page

JPH Advisory Group Curtis Hearn, CFP 600 Galleria Pkwy Ste 1600 Atlanta, GA 30339 770-859-0076 curtis@jphadvisory.com www.jphadvisory.com Incentive Stock Options Page 1 of 6, see disclaimer on final page

Estate Planning and Income Tax Issues for Nonresident Aliens Owning US Real Estate

Estate Planning and Income Tax Issues for Nonresident Aliens Owning US Real Estate 1. Introductory Matters. Presented by Paul McCawley Greenberg Traurig, P.A. mccawleyp@gtlaw.com 954.768.8269 October 24,

Estate Planning and Income Tax Issues for Nonresident Aliens Owning US Real Estate 1. Introductory Matters. Presented by Paul McCawley Greenberg Traurig, P.A. mccawleyp@gtlaw.com 954.768.8269 October 24,

S Corporations: 2013 Tax Update and M&A Issues & Considerations. November 15, 2013

S Corporations: 2013 Tax Update and M&A Issues & Considerations November 15, 2013 48th Annual Bank & Capital Markets Tax Institute S Corporations: 2013 Tax Update and M&A Issues & Considerations November

S Corporations: 2013 Tax Update and M&A Issues & Considerations November 15, 2013 48th Annual Bank & Capital Markets Tax Institute S Corporations: 2013 Tax Update and M&A Issues & Considerations November

What s News in Tax Analysis That Matters from Washington National Tax

What s News in Tax Analysis That Matters from Washington National Tax Have Undisclosed Foreign Assets? IRS Offers Options There is good news for individuals who inadvertently failed to fulfill tax and

What s News in Tax Analysis That Matters from Washington National Tax Have Undisclosed Foreign Assets? IRS Offers Options There is good news for individuals who inadvertently failed to fulfill tax and

American Bar Association Section of Family Law 2014 Spring CLE Conference PLENARY:

American Bar Association Section of Family Law 2014 Spring CLE Conference PLENARY: How to Find Your Spouse s Secret Offshore Bank Account: Using U.S. Tax Reporting Requirements as a Discovery Tool for

American Bar Association Section of Family Law 2014 Spring CLE Conference PLENARY: How to Find Your Spouse s Secret Offshore Bank Account: Using U.S. Tax Reporting Requirements as a Discovery Tool for

Guidance for companies, trusts and partnerships on completing a self-certification form

Guidance for companies, trusts and partnerships on completing a self-certification form In order to combat tax evasion by both individuals and businesses, the UK and many other countries have entered into

Guidance for companies, trusts and partnerships on completing a self-certification form In order to combat tax evasion by both individuals and businesses, the UK and many other countries have entered into

Are You Ready For New Form 8938 to Report Specified Foreign Financial Assets?

Are You Ready For New Form 8938 to Report Specified Foreign Financial Assets? The Hiring Incentives to Restore Employment ( HIRE ) Act, signed into law in 2010, included modified provisions of the previously

Are You Ready For New Form 8938 to Report Specified Foreign Financial Assets? The Hiring Incentives to Restore Employment ( HIRE ) Act, signed into law in 2010, included modified provisions of the previously

FBAR s: 2011 Final (BSA) Regulations and How they apply to Protectors, Directors and other Powerholders

Regulations and How they apply to Protectors, Directors and other Powerholders") FBAR s: 2011 Final (BSA) Regulations and How they apply to Protectors, Directors and other Powerholders STEP Miami Branch One Day Conference Friday, June 10, 2011 Conrad Hotel, Miami, FL Stewart L. Kasner

FBAR s: 2011 Final (BSA) Regulations and How they apply to Protectors, Directors and other Powerholders STEP Miami Branch One Day Conference Friday, June 10, 2011 Conrad Hotel, Miami, FL Stewart L. Kasner

Expanding internationally. What small and mid-sized businesses need to know.

Expanding internationally. What small and mid-sized businesses need to know. a TABLE OF CONTENTS U.S. Compliance 2 Expatriate and Inpatriate Taxation 6 Cross-Border Issues 8 Accounting Related Issues Structuring

Expanding internationally. What small and mid-sized businesses need to know. a TABLE OF CONTENTS U.S. Compliance 2 Expatriate and Inpatriate Taxation 6 Cross-Border Issues 8 Accounting Related Issues Structuring

IN THIS ISSUE: July, 2011 j Income Tax Planning Concepts in Estate Planning

IN THIS ISSUE: Goals of Income Tax Planning Basic Estate Planning Has No Income Tax Impact Advanced Estate Planning Can Have Income Tax Implications Taxation of Corporations, LLCs, Partnerships and Non-

IN THIS ISSUE: Goals of Income Tax Planning Basic Estate Planning Has No Income Tax Impact Advanced Estate Planning Can Have Income Tax Implications Taxation of Corporations, LLCs, Partnerships and Non-

Human Resource Services Webcast

Human Resource Services Webcast Foreign reporting requirements in Canada and the US: What s new and why you need to comply Administrative information 60 minute webcast Audio with slides For a better viewing

Human Resource Services Webcast Foreign reporting requirements in Canada and the US: What s new and why you need to comply Administrative information 60 minute webcast Audio with slides For a better viewing

Nuts & Bolts of Cross Border Tax Issues

Nuts & Bolts of Cross Border Tax Issues Central Arizona Estate Planning Council November 2, 2015 Presented by: Certified Public Accountant Attorney at Law 1 Overview What is an International Tax Practice?

Nuts & Bolts of Cross Border Tax Issues Central Arizona Estate Planning Council November 2, 2015 Presented by: Certified Public Accountant Attorney at Law 1 Overview What is an International Tax Practice?

Tax Update. New Cost Basis Reporting Rules (Form 1099-B) Effective For 2011. April 2011

Effective For 2011. April 2011") Tax Update April 2011 New Cost Basis Reporting Rules (Form 1099-B) Effective For 2011 by Ron Kramer, Director of Strategic Tax Planning If your memory is as bad as mine, you have probably forgotten that

Tax Update April 2011 New Cost Basis Reporting Rules (Form 1099-B) Effective For 2011 by Ron Kramer, Director of Strategic Tax Planning If your memory is as bad as mine, you have probably forgotten that

ELECTRONIC COMMUNICATION:

TAX FILING YEAR 2015 DISCLAIMER: and (SPOUSE/if filing Jointly) the undersigned taxpayer (s) hereby engage the services of American Expat Tax Services, Pte Limited (referred to hereinafter as AETS) as

TAX FILING YEAR 2015 DISCLAIMER: and (SPOUSE/if filing Jointly) the undersigned taxpayer (s) hereby engage the services of American Expat Tax Services, Pte Limited (referred to hereinafter as AETS) as

Tax Aspects of Consulting The Exit Tax Roth IRA Conversions Other. Foreign Bank Account Reporting Update Social Security

The Wolf Group, PC Tax Aspects of Consulting The Exit Tax Roth IRA Conversions Other Foreign Bank Account Reporting Update Social Security U.S. citizen Green card holder G-4 visa holder Based on common

The Wolf Group, PC Tax Aspects of Consulting The Exit Tax Roth IRA Conversions Other Foreign Bank Account Reporting Update Social Security U.S. citizen Green card holder G-4 visa holder Based on common

Estate Planning for the International Client

Estate Planning for the International Client Brenda Jackson-Cooper Doug Andre March 24, 2015 I. Rules and Definitions Agenda II. Estate Planning Case Studies III. Questions 2 Effects of U.S. transfer tax

Estate Planning for the International Client Brenda Jackson-Cooper Doug Andre March 24, 2015 I. Rules and Definitions Agenda II. Estate Planning Case Studies III. Questions 2 Effects of U.S. transfer tax

The IRS Is Looking For Non-Compliant Taxpayers With Foreign Interests: Is Your Taxpayer One Of Them?

The IRS Is Looking For Non-Compliant Taxpayers With Foreign Interests: Is Your Taxpayer One Of Them? Josh O. Ungerman and Anthony P. Daddino Each year, in the United States alone, offshore tax evasion

The IRS Is Looking For Non-Compliant Taxpayers With Foreign Interests: Is Your Taxpayer One Of Them? Josh O. Ungerman and Anthony P. Daddino Each year, in the United States alone, offshore tax evasion

TABLE OF CONTENTS PAGE GENERAL INFORMATION B-3 CERTAIN FEDERAL INCOME TAX CONSEQUENCES B-3 PUBLISHED RATINGS B-7 ADMINISTRATION B-7

STATEMENT OF ADDITIONAL INFORMATION INDIVIDUAL VARIABLE ANNUITY ISSUED BY JEFFERSON NATIONAL LIFE INSURANCE COMPANY AND JEFFERSON NATIONAL LIFE ANNUITY ACCOUNT G ADMINISTRATIVE OFFICE: P.O. BOX 36840,

STATEMENT OF ADDITIONAL INFORMATION INDIVIDUAL VARIABLE ANNUITY ISSUED BY JEFFERSON NATIONAL LIFE INSURANCE COMPANY AND JEFFERSON NATIONAL LIFE ANNUITY ACCOUNT G ADMINISTRATIVE OFFICE: P.O. BOX 36840,

ACTION: Notice of proposed rulemaking and notice of public. SUMMARY: This document contains proposed rules for the treatment

[4830-01-U] DEPARTMENT OF THE TREASURY Internal Revenue Service 26 CFR Part 1 [REG-106031-98] RIN 1545-AW13 Trading Safe Harbors. AGENCY: Internal Revenue Service (IRS), Treasury. ACTION: Notice of proposed

[4830-01-U] DEPARTMENT OF THE TREASURY Internal Revenue Service 26 CFR Part 1 [REG-106031-98] RIN 1545-AW13 Trading Safe Harbors. AGENCY: Internal Revenue Service (IRS), Treasury. ACTION: Notice of proposed

International Tax. Las Vegas, Nevada December 4-5, 2012

International Tax 4 th Annual Southwest Tax Conference Las Vegas, Nevada December 4-5, 2012 Brian Phillip Lau Cindy Hsieh br@rowbotham.com plau@rowbotham.com chsieh@rowbotham.com 101 2 nd Street, Suite

International Tax 4 th Annual Southwest Tax Conference Las Vegas, Nevada December 4-5, 2012 Brian Phillip Lau Cindy Hsieh br@rowbotham.com plau@rowbotham.com chsieh@rowbotham.com 101 2 nd Street, Suite

Limited Liability Company (LLC)

") Vertex Wealth Management LLC Michael Aluotto President Private Wealth Manager 1325 Franklin Ave., Ste. 335 Garden City, NY 11530 516-294-8200 mjaluotto@1stallied.com Limited Liability Company (LLC) Page

Vertex Wealth Management LLC Michael Aluotto President Private Wealth Manager 1325 Franklin Ave., Ste. 335 Garden City, NY 11530 516-294-8200 mjaluotto@1stallied.com Limited Liability Company (LLC) Page

Compensating Owners and Key Employees of Partnerships and LLC's

College of William & Mary Law School William & Mary Law School Scholarship Repository William & Mary Annual Tax Conference Conferences, Events, and Lectures 2013 Compensating Owners and Key Employees of

College of William & Mary Law School William & Mary Law School Scholarship Repository William & Mary Annual Tax Conference Conferences, Events, and Lectures 2013 Compensating Owners and Key Employees of

Your Target Market. Taking Your Company Global. International Tax & Accounting Services

Your Target Market Taking Your Company Global & Company www.rowbotham.com (415) 433-1177 consulting@rowbotham.com San Francisco Silicon Valley Associated Firms Worldwide International Tax & Accounting

Your Target Market Taking Your Company Global & Company www.rowbotham.com (415) 433-1177 consulting@rowbotham.com San Francisco Silicon Valley Associated Firms Worldwide International Tax & Accounting

Vertex Wealth Management LLC

Vertex Wealth Management LLC Michael Aluotto President Private Wealth Manager 1325 Franklin Ave., Ste. 335 Garden City, NY 11530 516-294-8200 mjaluotto@1stallied.com S Corporation Page 1 of 7, see disclaimer

Vertex Wealth Management LLC Michael Aluotto President Private Wealth Manager 1325 Franklin Ave., Ste. 335 Garden City, NY 11530 516-294-8200 mjaluotto@1stallied.com S Corporation Page 1 of 7, see disclaimer

International Issues. Affecting. Domestic Planners

International Issues Affecting Domestic Planners Robert D. Colvin (Houston, Texas, USA) Houston Business & Estate Planning Council October 22, 2009 Overview of Presentation Offshore Voluntary Disclosure

International Issues Affecting Domestic Planners Robert D. Colvin (Houston, Texas, USA) Houston Business & Estate Planning Council October 22, 2009 Overview of Presentation Offshore Voluntary Disclosure

management fee documentation

Issue 2010-02 www.bdo.ca the tax factor e-communications from the cra READ MORE p4 management fee documentation READ MORE p6 relief on US FBAR requirements READ MORE p8 Changes to the Tax Deferral on Publicly

Issue 2010-02 www.bdo.ca the tax factor e-communications from the cra READ MORE p4 management fee documentation READ MORE p6 relief on US FBAR requirements READ MORE p8 Changes to the Tax Deferral on Publicly

FAQs on Cost-Basis Reporting for Brokers

FAQs on Cost-Basis Reporting for Brokers The IRS published a list of Frequently Asked Questions on the new expanded tax reporting requirement for brokers which include reporting their customer s tax basis

FAQs on Cost-Basis Reporting for Brokers The IRS published a list of Frequently Asked Questions on the new expanded tax reporting requirement for brokers which include reporting their customer s tax basis

Year End Gifts and Investments

Wealth Planning Year End Tax Tips The end of every year poses a critical deadline for utilizing certain tax benefits. The following covers various items to address in your annual tax, estate, retirement

Wealth Planning Year End Tax Tips The end of every year poses a critical deadline for utilizing certain tax benefits. The following covers various items to address in your annual tax, estate, retirement

Tax Considerations In Structuring US-Based Private Equity Funds

As appeared in the Private Equity and Venture Capital 2002 edition of the International Financial Law Review. Tax Considerations In Structuring US-Based Private Equity Funds By Patrick Fenn and David Goldstein

As appeared in the Private Equity and Venture Capital 2002 edition of the International Financial Law Review. Tax Considerations In Structuring US-Based Private Equity Funds By Patrick Fenn and David Goldstein

Offshore Tax Evasion: US Initiatives

Scott D. Michel, Caplin & Drysdale This Article discusses the US reporting rules for US taxpayers with foreign accounts and assets (including FBAR and FATCA), the civil penalties for non-compliance with

Scott D. Michel, Caplin & Drysdale This Article discusses the US reporting rules for US taxpayers with foreign accounts and assets (including FBAR and FATCA), the civil penalties for non-compliance with

I. WHY LIMITED LIABILITY COMPANIES? A. History and Types of LLC s:

I. WHY LIMITED LIABILITY COMPANIES? A. History and Types of LLC s: The concept of the limited liability company did not begin to develop until the 1970 s. In 1977 the state of Wyoming enacted the first

I. WHY LIMITED LIABILITY COMPANIES? A. History and Types of LLC s: The concept of the limited liability company did not begin to develop until the 1970 s. In 1977 the state of Wyoming enacted the first

FATCA AND NEW ZEALAND LAW FIRMS

This Practice Briefing does not constitute legal advice INTRODUCTION The FATCA agreement between New Zealand and United States is directed at reducing tax evasion by US taxpayers. New Zealand law firms

This Practice Briefing does not constitute legal advice INTRODUCTION The FATCA agreement between New Zealand and United States is directed at reducing tax evasion by US taxpayers. New Zealand law firms

Foreign Account Tax Compliance Act ("FATCA")

") Required Form Who Must File? Does the United States include U.S. territories? Reporting Threshold (Total Value of Assets) When do you have an interest in an account or asset? Foreign Account Tax Compliance

Required Form Who Must File? Does the United States include U.S. territories? Reporting Threshold (Total Value of Assets) When do you have an interest in an account or asset? Foreign Account Tax Compliance