ACCOUNTING FOR MERCHANDISING OPERATIONS

|

|

|

- Harry Clement Elliott

- 10 years ago

- Views:

Transcription

1 Chapter 5 ACCOUNTING FOR MERCHANDISING OPERATIONS PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CPA, CIA Cynthia J. Rooney, Ph.D., CPA Winston Kwok, Ph.D., CPA McGraw-Hill/Irwin Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved.

2 5-2 C 1 SERVICE COMPANIES Service organizations sell time to earn revenue. Examples: Accounting firms, law firms and plumbing services

3 5-3 C 1 MERCHANDISER Merchandising Companies Manufacturer Wholesaler Retailer Consumers

4 C 1 REPORTING INCOME FOR A MERCHANDISER 5-4 Merchandising companies sell products to earn revenue. Examples: sporting goods, clothing, and auto parts stores

5 C 2 OPERATING CYCLE FOR A MERCHANDISER Begins with the purchase of merchandise and ends with the collection of cash from the sale of merchandise. 5-5

6 5-6 C 2 INVENTORY SYSTEMS

7 5-7 C 2 INVENTORY SYSTEMS Perpetual systems continually update accounting records for merchandising transactions Periodic systems accounting records relating to merchandise transactions are updated only at the end of the accounting period

8 5-8 P1 MERCHANDISE PURCHASES On November 2, Z-Mart purchased $1,200 of merchandise inventory for cash.

9 5-9 P1 TRADE DISCOUNTS Used by manufacturers and wholesalers to offer better prices for greater quantities purchased. Example Z-Mart offers a 30% trade discount for orders of 1,000 units or more on its popular product Racer. Each Racer has a list price of $5.25. Quantity sold 1,000 Price per unit $ 5.25 Total 5,250 Less 30% discount (1,575) Invoice price $ 3,675

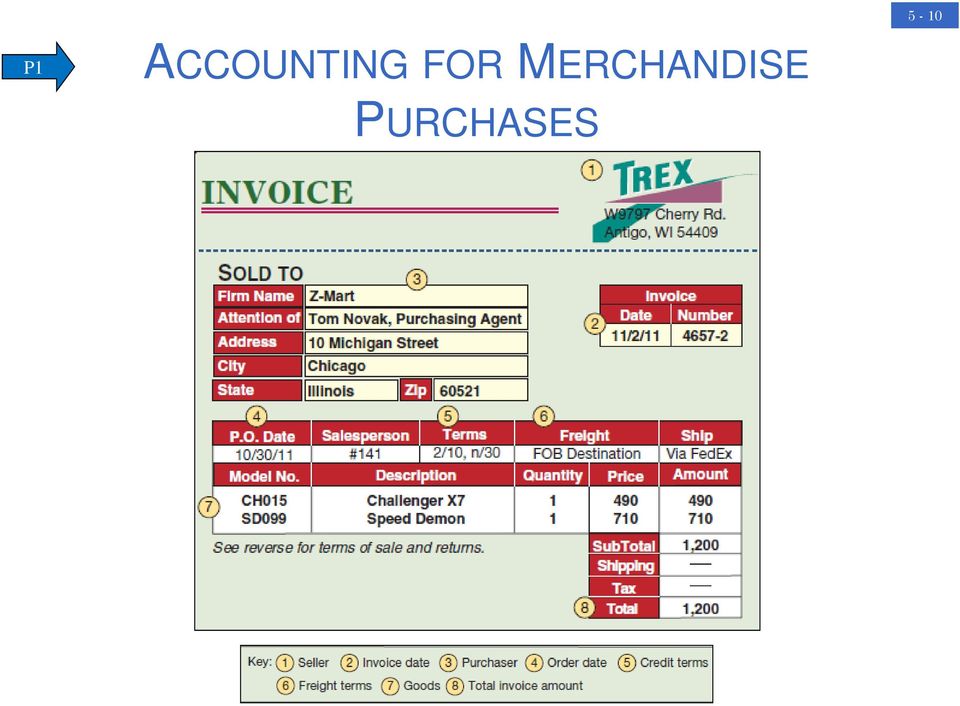

10 5-10 P1 ACCOUNTING FOR MERCHANDISE PURCHASES

11 5-11 P1 PURCHASE DISCOUNTS A deduction from the invoice price granted to induce early payment of the amount due.

12 5-12 P1 PURCHASE DISCOUNTS 2/10,n/30 Discount Percent Number of Days Discount Is Available Otherwise, Net (or All) Is Due in 30 Days Credit Period

Is Due in 30 Days Credit")

13 5-13 P1 PURCHASE DISCOUNTS On November 2, Z-Mart purchased $1,200 of merchandise inventory on account, credit terms are 2/10, n/30.

14 5-14 P1 PURCHASE DISCOUNTS On November 12, Z-Mart paid the amount due on the purchase of November 2.

15 5-15 P1 PURCHASE DISCOUNTS After we post these entries, the accounts involved look like these:

16 5-16 P1 PURCHASE RETURNS AND ALLOWANCES Purchase Return... Merchandise returned by the purchaser to the supplier. Purchase Allowance... A reduction in the cost of defective or unacceptable merchandise received by a purchaser from a supplier.

17 5-17 P1 PURCHASE RETURNS AND ALLOWANCES On November 15, Z-Mart (buyer) issues a $300 debit memorandum for an allowance from Trex for defective merchandise.

18 5-18 P1 PURCHASE RETURNS AND ALLOWANCES Z-Mart purchases $1,000 of merchandise on June 1 with terms 2/10, n/60. Two days later, Z-Mart returns $100 of goods before paying the invoice. When Z-Mart later pays on June 11, it takes the 2% discount only on the $900 remaining balance.

19 P1 TRANSPORTATION COSTS AND OWNERSHIP TRANSFER 5-19

20 5-20 P1 TRANSPORTATION COSTS Z-Mart purchased merchandise on terms of FOB shipping point. The transportation charge is $75.

21 5-21 P1 ACCOUNTING FOR MERCHANDISE

22 P2 ACCOUNTING FOR MERCHANDISE SALES 5-22

23 5-23 P2 SALES OF MERCHANDISE Each sales transaction for a seller of merchandise involves two parts: Revenue received in the form of an asset from a customer. Recognition of the cost of merchandise sold to a customer.

24 5-24 P2 SALES OF MERCHANDISE On November 3, Z-Mart sold $2,400 of merchandise on credit. The merchandise has a cost basis to Z-Mart of $1,600.

25 5-25 P2 SALES DISCOUNTS Sales discounts on credit sales can benefit a seller by decreasing the delay in receiving cash and reducing future collection efforts.

26 5-26 P2 SALES DISCOUNTS Z-Mart completes a $1,000 credit sale with terms of 2/10, n/60. The account was paid in full within the 60-day period. The account was paid in full within the 10-day discount period.

27 5-27 P2 SALES RETURNS AND ALLOWANCES Sales returns and allowances usually involve dissatisfied customers and the possibility of lost future sales. Sales returns refer to merchandise that customers return to the seller after a sale. Sales allowances refer to reductions in the selling price of merchandise sold to customers.

28 5-28 P2 SALES RETURNS AND ALLOWANCES Recall Z-Mart s sale for $2,400 that had a cost of $1,600. Assume the customer returns part of the merchandise. The returned items sell for $800 and cost $600.

29 5-29 P2 SALES ALLOWANCES Assume that $800 of the merchandise Z-Mart sold on November 3 is defective but the buyer decides to keep it because Z-Mart offers a $100 price reduction.

30 5-30 P2 MERCHANDISING COST FLOW IN THE ACCOUNTING CYCLE Beginning inventory Net purchases Period 1 Merchandise available for sale Ending inventory Beginning inventory Cost of goods sold Net purchases To Income Statement To Balance Sheet Period 2 Merchandise available for sale Ending inventory Cost of goods sold To Income Statement To Balance Sheet

31 P3 ADJUSTING ENTRIES FOR MERCHANDISERS 5-31 A merchandiser using a perpetual inventory system is usually required to make an adjustment to update the Merchandise Inventory account to reflect any loss of merchandise, including theft and deterioration. Z-Mart s Merchandise Inventory account at the end of year 2011 has a balance of $21,250, but a physical count reveals that only $21,000 of inventory exists.

32 P3 CLOSING ENTRIES FOR MERCHANDISERS 5-32

33 5-33 P4 INCOME STATEMENT An income statement format shows net sales and other costs and expenses.

34 5-34 P4 CLASSIFIED BALANCE SHEET Highly Liquid Less Liquid

35 5-35 A1 ACID-TEST RATIO Acid-Test Ratio = Quick Assets Current Liabilities Acid-Test Ratio = Cash + S-T Investments + Receivables Current Liabilities A common rule of thumb is the acid-test ratio should have a value of at least 1.0 to conclude a company is unlikely to face liquidity problems in the near future.

36 5-36 A2 GROSS MARGIN RATIO Gross Margin Ratio = Net Sales - Cost of Goods Sold Net Sales Percentage of dollar sales available to cover expenses and provide a profit.

37 5-37 A1/A2 Nestlé

38 P5 APPENDIX 5A: PERIODIC INVENTORY SYSTEM 5-38 (a) (b) (c) (d) (e) (f) (g) A periodic inventory system requires updating the inventory account only at the end of a period to reflect the quantity and cost of both the goods available and the goods sold.

39 5-39 P5 APPENDIX 5A: PERIODIC INVENTORY SYSTEM

40 5-40 P5 APPENDIX 5B: WORKSHEET PERPETUAL SYSTEM

41 END OF CHAPTER

Chapter 04 - Accounting for Merchandising Operations. Chapter Outline

I. Merchandising Activities Products that a company acquires to resell to customers are referred to as merchandise (also called goods). A merchandiser earns net income by buying and selling merchandise.

I. Merchandising Activities Products that a company acquires to resell to customers are referred to as merchandise (also called goods). A merchandiser earns net income by buying and selling merchandise.

2. A service company earns net income by buying and selling merchandise. Ans: False

Chapter 6: Accounting For Merchandising Activities True/False 1. Merchandise consists of products that a company acquires for the purpose of reselling them to customers. 2. A service company earns net

Chapter 6: Accounting For Merchandising Activities True/False 1. Merchandise consists of products that a company acquires for the purpose of reselling them to customers. 2. A service company earns net

Chapter 5. Accounting for merchandising operations. Appendix 5A: Periodic inventory system

1 Chapter 5 Accounting for merchandising operations Appendix 5A: Periodic inventory system 2 Learning objectives 1. Record purchase and sales transactions under the periodic inventory system 2. Prepare

1 Chapter 5 Accounting for merchandising operations Appendix 5A: Periodic inventory system 2 Learning objectives 1. Record purchase and sales transactions under the periodic inventory system 2. Prepare

Accounting Notes. Purchasing Merchandise under the Perpetual Inventory system:

Systems: Perpetual VS Periodic " Keeps running record of all goods " Does not keep a running record bought and sold " is counted once a year " is counted at least once a year " Used for all types of goods

Systems: Perpetual VS Periodic " Keeps running record of all goods " Does not keep a running record bought and sold " is counted once a year " is counted at least once a year " Used for all types of goods

Merchandise Accounts. Chapter 7 - Unit 14

Merchandise Accounts Chapter 7 - Unit 14 Merchandising... Merchandising... There are many types of companies out there Merchandising... There are many types of companies out there Service company - sells

Merchandise Accounts Chapter 7 - Unit 14 Merchandising... Merchandising... There are many types of companies out there Merchandising... There are many types of companies out there Service company - sells

CHAPTER5 Accounting for Merchandising Operations 5-1

CHAPTER5 Accounting for Merchandising Operations 5-1 5-2 PreviewofCHAPTER5 Merchandising Operations Merchandising Companies Buy and Sell Goods Wholesaler Retailer Consumer The primary source of revenues

CHAPTER5 Accounting for Merchandising Operations 5-1 5-2 PreviewofCHAPTER5 Merchandising Operations Merchandising Companies Buy and Sell Goods Wholesaler Retailer Consumer The primary source of revenues

CHAPTER 5 ACCOUNTING FOR MERCHANDISING OPERATIONS

CHAPTER 5 ACCOUNTING FOR MERCHANDISING OPERATIONS LEARNING OBJECTIVES 1. IDENTIFY THE DIFFERENCES BETWEEN SERVICE AND MERCHANDISING COMPANIES. 2. EXPLAIN THE RECORDING OF PURCHASES UNDER A PERPETUAL INVENTORY

CHAPTER 5 ACCOUNTING FOR MERCHANDISING OPERATIONS LEARNING OBJECTIVES 1. IDENTIFY THE DIFFERENCES BETWEEN SERVICE AND MERCHANDISING COMPANIES. 2. EXPLAIN THE RECORDING OF PURCHASES UNDER A PERPETUAL INVENTORY

CHAPTER 5 Merchandising Operations. Study Objectives

CHAPTER 5 Merchandising Operations Study Objectives Identify the differences between a service enterprise and a merchandising company. Explain the recording of purchases under a perpetual inventory system.

CHAPTER 5 Merchandising Operations Study Objectives Identify the differences between a service enterprise and a merchandising company. Explain the recording of purchases under a perpetual inventory system.

SOLUTIONS. Learning Goal 22 LG 22-1. LG 22-2.

S1 Learning Goal 22 Multiple Choice 1. b 2. d A purchase discount is recorded when payment is made. 3. a The payment is within the discount period, so $5,000.02 = $100. 4. b The discount is ($1,000/.98)

S1 Learning Goal 22 Multiple Choice 1. b 2. d A purchase discount is recorded when payment is made. 3. a The payment is within the discount period, so $5,000.02 = $100. 4. b The discount is ($1,000/.98)

Income Statements. Accounting for Merchandising Operations

Accounting Principles, 7 th Edition Weygandt Kieso Kimmel Income Statements Accounting for Merchandising Operations Prepared by Naomi Karolinski Monroe Community College and Marianne Bradford Bryant College

Accounting Principles, 7 th Edition Weygandt Kieso Kimmel Income Statements Accounting for Merchandising Operations Prepared by Naomi Karolinski Monroe Community College and Marianne Bradford Bryant College

2 Under a perpetual inventory system merchandise is purchased for cash. Which is the correct journal entry to record this purchase?

KRUG PRACTICE TEST ACCTG 1 - CHAP 5,6 PRACTICE TEST -- The following is a practice test for Accounting 1, Chapters 5 and 6 It is only a representation of wha the test could be like. It is not a guarantee

KRUG PRACTICE TEST ACCTG 1 - CHAP 5,6 PRACTICE TEST -- The following is a practice test for Accounting 1, Chapters 5 and 6 It is only a representation of wha the test could be like. It is not a guarantee

Module 4 - Audio File Legend

Module 4 - Audio File Legend Part 1 2 3 4 5 Content Learning Objectives and Basics of merchandising operations Recording merchandise purchases and sales Problem: Purchase and sale journal entries Income

Module 4 - Audio File Legend Part 1 2 3 4 5 Content Learning Objectives and Basics of merchandising operations Recording merchandise purchases and sales Problem: Purchase and sale journal entries Income

Accounting for Merchandising Operations

Instructor: masum 5-1 Bangladesh University of Textiles 5 Accounting for Merchandising Operations Learning Objectives After studying this chapter, you should be able to: [1] Identify the differences between

Instructor: masum 5-1 Bangladesh University of Textiles 5 Accounting for Merchandising Operations Learning Objectives After studying this chapter, you should be able to: [1] Identify the differences between

INVENTORY. Merchandising Firms COST OF GOODS SOLD. Traditional bookkeeping uses separate accounts for different types of transactions

Merchandising Firms Principles of Accounting Created 2005 By Michael Worthington Elizabeth City State University INVENTORY Traditional bookkeeping uses separate accounts for different types of transactions

Merchandising Firms Principles of Accounting Created 2005 By Michael Worthington Elizabeth City State University INVENTORY Traditional bookkeeping uses separate accounts for different types of transactions

The Measurement of the Business Income. 1 by recording revenues when earned and expenses when incurred. 2 by adjusting accounts

Recap from Week 3 The Measurement of the Business Income The primary objective of accounting is measuring the net income of the businesses according to the generally accepted accounting principles. Net

Recap from Week 3 The Measurement of the Business Income The primary objective of accounting is measuring the net income of the businesses according to the generally accepted accounting principles. Net

Investments Advance to subsidiary company 81,000

EXERCISE 7-3 (10 15 minutes) Current assets Accounts receivable Customers Accounts (of which accounts in the amount of $40,000 have been pledged as security for a bank loan) $79,000 Installment accounts

EXERCISE 7-3 (10 15 minutes) Current assets Accounts receivable Customers Accounts (of which accounts in the amount of $40,000 have been pledged as security for a bank loan) $79,000 Installment accounts

Short-term investments (also known as marketable securities) are easily convertible to cash that a company plans to hold for a year or less.

are easily convertible to cash that a company plans to hold for a year or less.") Accounting Fundamentals Lesson 5 5.0 Receivables & Investments Short-term investments (also known as marketable securities) are easily convertible to cash that a company plans to hold for a year or less.

Accounting Fundamentals Lesson 5 5.0 Receivables & Investments Short-term investments (also known as marketable securities) are easily convertible to cash that a company plans to hold for a year or less.

IMPERIAL OIL LIMITED (in millions) December 31 1994 1993

December 31 1994 1993") C H A P T E R 5 Accounting for Merchandising Activities Many companies earn profits by buying merchandise and selling it to customers. Accounting helps managers to determine the amount of income earned

C H A P T E R 5 Accounting for Merchandising Activities Many companies earn profits by buying merchandise and selling it to customers. Accounting helps managers to determine the amount of income earned

Financial Accounting. John J. Wild. Sixth Edition. McGraw-Hill/Irwin. Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved.

Financial Accounting John J. Wild Sixth Edition McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Chapter 05 Reporting and Analyzing Inventories Conceptual Chapter

Financial Accounting John J. Wild Sixth Edition McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Chapter 05 Reporting and Analyzing Inventories Conceptual Chapter

Chapter 5 Merchandising Operations

Chapter 5 Merchandising Operations Financial Statements of a Service Company and a Merchandiser: - Service Companies: Revenues earned through performance of services. Examples: Dentists, Accounting Firms,

Chapter 5 Merchandising Operations Financial Statements of a Service Company and a Merchandiser: - Service Companies: Revenues earned through performance of services. Examples: Dentists, Accounting Firms,

Chapter 6. An advantage of the periodic method is that it is a easy system to maintain.

Chapter 6 Periodic and Perpetual Inventory Systems There are two methods of handling inventories: the periodic inventory system, and the perpetual inventory system With the periodic inventory system, the

Chapter 6 Periodic and Perpetual Inventory Systems There are two methods of handling inventories: the periodic inventory system, and the perpetual inventory system With the periodic inventory system, the

Accounting for Merchandising Companies: Journal Entries

PrinciplesofAccounting HelpLesson #4 Accounting for Merchandising Companies: Journal Entries By Laurie L. Swanson Merchandising Company A merchandising business is one that buys and sells goods in order

PrinciplesofAccounting HelpLesson #4 Accounting for Merchandising Companies: Journal Entries By Laurie L. Swanson Merchandising Company A merchandising business is one that buys and sells goods in order

Chapter 6. Inventories

1 Chapter 6 Inventories 2 Learning objectives 1. Define and identify the items included in inventory at the reporting date 2. Determine the s to be included in the value of inventory 3. Describe the four

1 Chapter 6 Inventories 2 Learning objectives 1. Define and identify the items included in inventory at the reporting date 2. Determine the s to be included in the value of inventory 3. Describe the four

Chapter 5. Merchandising Operations

Merchandising Operations Chapter 5 When a service business earns fees they record revenue from the services rendered. In the case of the merchandising business you still have the revenue transaction, but

Merchandising Operations Chapter 5 When a service business earns fees they record revenue from the services rendered. In the case of the merchandising business you still have the revenue transaction, but

5-1. Prepared by Coby Harmon University of California, Santa Barbara Westmont College

5-1 Prepared by Coby Harmon University of California, Santa Barbara Westmont College 5 Accounting for Merchandising Operations Learning Objectives After studying this chapter, you should be able to: [1]

5-1 Prepared by Coby Harmon University of California, Santa Barbara Westmont College 5 Accounting for Merchandising Operations Learning Objectives After studying this chapter, you should be able to: [1]

Accounting for Merchandising Operations

Prepared by Coby Harmon University of California, Santa Barbara Westmont College 5-1 5 Accounting for Merchandising Operations Learning Objectives After studying this chapter, you should be able to: [1]

Prepared by Coby Harmon University of California, Santa Barbara Westmont College 5-1 5 Accounting for Merchandising Operations Learning Objectives After studying this chapter, you should be able to: [1]

Dutchess Community College ACC 104 Financial Accounting Quiz Prep Chapter 5

Dutchess Community College ACC 104 Financial Accounting Quiz Prep Chapter 5 Merchandising Operations Peter Rivera October 2009 Disclaimer This Quiz Prep is provided as an outline of the key concepts from

Dutchess Community College ACC 104 Financial Accounting Quiz Prep Chapter 5 Merchandising Operations Peter Rivera October 2009 Disclaimer This Quiz Prep is provided as an outline of the key concepts from

CHAPTER 6. Accounting for retailing CONTENTS

CHAPTER 6 Accounting for retailing CONTENTS 6.1 Journal entries periodic inventory system 6.2 Journal entries involving discounts, closing entries and statements of financial performance both perpetual

CHAPTER 6 Accounting for retailing CONTENTS 6.1 Journal entries periodic inventory system 6.2 Journal entries involving discounts, closing entries and statements of financial performance both perpetual

Purchase Requisition. Sporting Goods Department Purchasing Department. Request purchase of the following item(s):

:") Extend Your Knowledge 9-2: Voucher System of Control A voucher system is a set of procedures and approvals designed to control cash disbursements and acceptance of obligations. The voucher system of control

Extend Your Knowledge 9-2: Voucher System of Control A voucher system is a set of procedures and approvals designed to control cash disbursements and acceptance of obligations. The voucher system of control

Purchasing/Human Resources/Payment Process: Recording and Evaluating Expenditure Process Activities

Chapter 8 Purchasing/Human Resources/Payment Process: Recording and Evaluating Expenditure Process Activities McGraw-Hill/Irwin Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved. What

Chapter 8 Purchasing/Human Resources/Payment Process: Recording and Evaluating Expenditure Process Activities McGraw-Hill/Irwin Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved. What

Dutchess Community College ACC 104 Financial Accounting Chapter 6 Quiz Prep

Dutchess Community College ACC 104 Financial Accounting Chapter 6 Quiz Prep Reporting & Analyzing Peter Rivera March 2007 Revised March 26, 2007 Disclaimer This Quiz Prep is provided as an outline of the

Dutchess Community College ACC 104 Financial Accounting Chapter 6 Quiz Prep Reporting & Analyzing Peter Rivera March 2007 Revised March 26, 2007 Disclaimer This Quiz Prep is provided as an outline of the

of Goods Sold and Inventory

Date: 10th July 2008 Time: 12:03 User ID: narayanansa 6 Cost of Goods Sold and Inventory After studying Chapter 6, you should be able to: ä 1 ä 2 ä 3 ä 4 ä 5 ä 6 ä 7 ä 8 ä 9 Describe the types of inventories

Date: 10th July 2008 Time: 12:03 User ID: narayanansa 6 Cost of Goods Sold and Inventory After studying Chapter 6, you should be able to: ä 1 ä 2 ä 3 ä 4 ä 5 ä 6 ä 7 ä 8 ä 9 Describe the types of inventories

Study Guide Chapter 5 Financial

Study Guide Chapter 5 Financial 53. Merchandising companies that sell to retailers are known as a. brokers. b. corporations. c. wholesalers. d. service firms. 57. Gross profit equals the difference between

Study Guide Chapter 5 Financial 53. Merchandising companies that sell to retailers are known as a. brokers. b. corporations. c. wholesalers. d. service firms. 57. Gross profit equals the difference between

CHAPTER 5 ACCOUNTING FOR MERCHANDISING OPERATIONS SUMMARY OF QUESTIONS BY STUDY OBJECTIVES AND BLOOM S TAXONOMY. True-False Statements

sg st a CHAPTER 5 ACCOUNTING FOR MERCHANDISING OPERATIONS SUMMARY OF QUESTIONS BY STUDY OBJECTIVES AND BLOOM S TAXONOMY Item SO BT Item SO BT Item SO BT Item SO BT Item SO BT True-False Statements 1. 1

sg st a CHAPTER 5 ACCOUNTING FOR MERCHANDISING OPERATIONS SUMMARY OF QUESTIONS BY STUDY OBJECTIVES AND BLOOM S TAXONOMY Item SO BT Item SO BT Item SO BT Item SO BT Item SO BT True-False Statements 1. 1

Accounting 303 Exam 3, Chapters 7-9

Accounting 303 Exam 3, Chapters 7-9 Spring 2012 Name Row I. Multiple Choice Questions. (2 points each, 30 points in total) Read each question carefully and indicate your answer by circling the letter preceding

Accounting 303 Exam 3, Chapters 7-9 Spring 2012 Name Row I. Multiple Choice Questions. (2 points each, 30 points in total) Read each question carefully and indicate your answer by circling the letter preceding

Inventory - A current asset whose ending balance should report the cost of a merchandiser's products waiting to be sold.

Accounting Fundamentals Lesson 6 6.0 Inventory & Cost of Sales Inventory - A current asset whose ending balance should report the cost of a merchandiser's products waiting to be sold. The inventory of

Accounting Fundamentals Lesson 6 6.0 Inventory & Cost of Sales Inventory - A current asset whose ending balance should report the cost of a merchandiser's products waiting to be sold. The inventory of

1. Merchandising company VS Service company V.S Manufacturing company

Chapter 6 Mechandising Activities 1. Merchandising company VS Service company V.S Manufacturing company Manufacturing companies use raw materials to make the inventory they sell. Their operating cycles

Chapter 6 Mechandising Activities 1. Merchandising company VS Service company V.S Manufacturing company Manufacturing companies use raw materials to make the inventory they sell. Their operating cycles

RAPID REVIEW Chapter Content

RAPID REVIEW BASIC ACCOUNTING EQUATION (Chapter 2) INVENTORY (Chapters 5 and 6) Basic Equation Assets Owner s Equity Expanded Owner s Owner s Assets Equation = Liabilities Capital Drawing Revenues Debit

RAPID REVIEW BASIC ACCOUNTING EQUATION (Chapter 2) INVENTORY (Chapters 5 and 6) Basic Equation Assets Owner s Equity Expanded Owner s Owner s Assets Equation = Liabilities Capital Drawing Revenues Debit

Merchandising Operations

5 Merchandising Operations WHAT YOU PROBABLY ALREADY KNOW You want to order a pair of pants from a mail-order catalog. The price listed in the catalog is $50. There is a 10% off coupon in the catalog for

5 Merchandising Operations WHAT YOU PROBABLY ALREADY KNOW You want to order a pair of pants from a mail-order catalog. The price listed in the catalog is $50. There is a 10% off coupon in the catalog for

How To Factoring

THE BASICS OF FACTORING A Guide to Understanding Accounts Receivable Financing The Basics of Factoring Table of Contents What is Factoring?.. 1 Benefits of Factoring 4 What Types of Businesses Utilize

THE BASICS OF FACTORING A Guide to Understanding Accounts Receivable Financing The Basics of Factoring Table of Contents What is Factoring?.. 1 Benefits of Factoring 4 What Types of Businesses Utilize

CHAPTER 8 Valuation of Inventories: A Cost Basis Approach

CHAPTER 8 Valuation of Inventories: A Cost Basis Approach 8-1 LECTURE OUTLINE This chapter can be covered in three to four class sessions. Students should have had previous exposure to inventory accounting

CHAPTER 8 Valuation of Inventories: A Cost Basis Approach 8-1 LECTURE OUTLINE This chapter can be covered in three to four class sessions. Students should have had previous exposure to inventory accounting

Inventories: Measurement

RECORDING AND MEASURING INVENTORY TYPES OF INVENTORY There are two types of inventories depending on the kind of business operation. Merchandise Inventory A merchandising concern buys and resells inventory

RECORDING AND MEASURING INVENTORY TYPES OF INVENTORY There are two types of inventories depending on the kind of business operation. Merchandise Inventory A merchandising concern buys and resells inventory

ANSWERS TO QUESTIONS FOR GROUP LEARNING

Accounting for a 5 Merchandising Business ANSWERS TO QUESTIONS FOR GROUP LEARNING Q5-1 A merchandising business has a major revenue reduction called cost of goods sold. The computation of cost of goods

Accounting for a 5 Merchandising Business ANSWERS TO QUESTIONS FOR GROUP LEARNING Q5-1 A merchandising business has a major revenue reduction called cost of goods sold. The computation of cost of goods

Module 4: Accounting for merchandising activities

Course Schedule Course Modules Review and Practice Exam Preparation Resources Module 4: Accounting for merchandising activities Overview In the first three modules, you studied how to determine income

Course Schedule Course Modules Review and Practice Exam Preparation Resources Module 4: Accounting for merchandising activities Overview In the first three modules, you studied how to determine income

Chapter 24 Stock Handling and Inventory Control. Section 24.1 The Stock Handling Process Section 24.2 Inventory Control

Chapter 24 Stock Handling and Inventory Control Section 24.1 The Stock Handling Process Section 24.2 Inventory Control The Stock Handling Process Key Terms receiving record blind check method direct check

Chapter 24 Stock Handling and Inventory Control Section 24.1 The Stock Handling Process Section 24.2 Inventory Control The Stock Handling Process Key Terms receiving record blind check method direct check

Accounting Building Business Skills. Learning Objectives. Learning Objectives. Paul D. Kimmel. Chapter Four: Inventories

Accounting Building Business Skills Paul D. Kimmel Chapter Four: Inventories PowerPoint presentation by Christine Langridge Swinburne University of Technology, Lilydale 2003 John Wiley & Sons Australia,

Accounting Building Business Skills Paul D. Kimmel Chapter Four: Inventories PowerPoint presentation by Christine Langridge Swinburne University of Technology, Lilydale 2003 John Wiley & Sons Australia,

Self-test Comprehensive Problems II 综 合 自 测 题 II

Self-test Comprehensive Problems II 综 合 自 测 题 II Part One (30%) 1. Give the Chinese/English of the following terms: (5%) subsidiary ledger 统 制 账 户 purchase requisition 现 金 溢 缺 petty cash fund 永 续 盘 存 制

Self-test Comprehensive Problems II 综 合 自 测 题 II Part One (30%) 1. Give the Chinese/English of the following terms: (5%) subsidiary ledger 统 制 账 户 purchase requisition 现 金 溢 缺 petty cash fund 永 续 盘 存 制

1. A set of procedures for controlling cash payments by preparing and approving vouchers before payments are made is known as a voucher system.

Accounting II True/False Indicate whether the sentence or statement is true or false. 1. A set of procedures for controlling cash payments by preparing and approving vouchers before payments are made is

Accounting II True/False Indicate whether the sentence or statement is true or false. 1. A set of procedures for controlling cash payments by preparing and approving vouchers before payments are made is

Chapter 5 Accounting for Merchandising Operations

Chapter 5 Accounting for Merchandising Operations Purchase Transactions Purchaser records goods at cost. When goods are returned, purchaser reduces Inventory. On September 5, De La Hoya Company buys merchandise

Chapter 5 Accounting for Merchandising Operations Purchase Transactions Purchaser records goods at cost. When goods are returned, purchaser reduces Inventory. On September 5, De La Hoya Company buys merchandise

INVENTORY VALUATION THE SIGNIFICANCE OF INVENTORY

THE SIGNIFICANCE OF INVENTORY INVENTORY VALUATION In the balance sheet inventory is frequently the most significant current asset. In the income statement, inventory is vital in determining the results

THE SIGNIFICANCE OF INVENTORY INVENTORY VALUATION In the balance sheet inventory is frequently the most significant current asset. In the income statement, inventory is vital in determining the results

Accounts Receivable 7200 Sales 7200 (No entry )

") INVENTORY. Inventory: It is defined as tangible personal property: 1. Held for sale in the ordinary course of business. 2. In the process of production for such sale. 3. To be used currently in the production

INVENTORY. Inventory: It is defined as tangible personal property: 1. Held for sale in the ordinary course of business. 2. In the process of production for such sale. 3. To be used currently in the production

Inventories: Cost Measurement and Flow Assumptions

CHAPTER 8 O BJECTIVES After reading this chapter, you will be able to: 1 Describe how inventory accounts are classified. 2 Explain the uses of the perpetual and periodic inventory systems. 3 Identify how

CHAPTER 8 O BJECTIVES After reading this chapter, you will be able to: 1 Describe how inventory accounts are classified. 2 Explain the uses of the perpetual and periodic inventory systems. 3 Identify how

中 原 大 學 95 學 年 度 轉 學 考 招 生 入 學 考 試

中 原 大 學 95 學 年 度 轉 學 考 招 生 入 學 考 試 7 月 12 日 14:00~15:30 商 學 群 組 二 年 級 科 目 : 會 計 學 ( 共 七 頁 第 一 頁 ) 可 使 用 計 算 機, 惟 僅 限 不 具 可 程 式 及 多 重 記 憶 者 一 MULTIPLE CHOICE QUESTIONS: (50%) 誠 實 是 我 們 珍 視 的 美 德, 我 們 喜

中 原 大 學 95 學 年 度 轉 學 考 招 生 入 學 考 試 7 月 12 日 14:00~15:30 商 學 群 組 二 年 級 科 目 : 會 計 學 ( 共 七 頁 第 一 頁 ) 可 使 用 計 算 機, 惟 僅 限 不 具 可 程 式 及 多 重 記 憶 者 一 MULTIPLE CHOICE QUESTIONS: (50%) 誠 實 是 我 們 珍 視 的 美 德, 我 們 喜

Accounting 201 Comprehensive Practice Exam 2C Page 1

Accounting 201 Comprehensive Practice Exam 2C Page 1 1. A business organized as a corporation a. is not a separate legal entity in most states. b. requires that stockholders be personally liable for the

Accounting 201 Comprehensive Practice Exam 2C Page 1 1. A business organized as a corporation a. is not a separate legal entity in most states. b. requires that stockholders be personally liable for the

Chapter 8 Inventories: Measurement

Chapter 8 Inventories: Measurement AACSB assurance of learning standards in accounting and business education require documentation of outcomes assessment. Although schools, departments, and faculty may

Chapter 8 Inventories: Measurement AACSB assurance of learning standards in accounting and business education require documentation of outcomes assessment. Although schools, departments, and faculty may

CHAPTER 9 WHAT IS REPORTED AS INVENTORY? WHAT IS INVENTORY? COST OF GOODS SOLD AND INVENTORY

CHAPTER 9 COST OF GOODS AND INVENTORY 1 WHAT IS REPORTED AS INVENTORY? Inventory represents goods that are either manufactured or purchased for resale in the normal course of business Inventory is classified

CHAPTER 9 COST OF GOODS AND INVENTORY 1 WHAT IS REPORTED AS INVENTORY? Inventory represents goods that are either manufactured or purchased for resale in the normal course of business Inventory is classified

... points " General Journal Debit Credit. 10 out of 10.00

1. award: 10.00... points " Apr. 2 Purchased merchandise from Lyon Company under the following terms: S4,000 price, invoice dated April 2, credit terms of 2115, n/60, and FOB shipping point. 3 Paid S224

1. award: 10.00... points " Apr. 2 Purchased merchandise from Lyon Company under the following terms: S4,000 price, invoice dated April 2, credit terms of 2115, n/60, and FOB shipping point. 3 Paid S224

MERCHANDISING BUSINESS

MERCHANDISING BUSINESS Business that buys finished goods and resells them. Business which deals in inventory. Business that sells physical goods or products to its customers. Revenue activities of merchandising

MERCHANDISING BUSINESS Business that buys finished goods and resells them. Business which deals in inventory. Business that sells physical goods or products to its customers. Revenue activities of merchandising

1. $45000 2. $108000 3. $63000 4. $135000

For the last several years Monte Cristo Corp. has operated with a gross profit rate of 30%. On January 1 of the current year, the company had on hand inventory with a cost of $150,000. Purchases of merchandise

For the last several years Monte Cristo Corp. has operated with a gross profit rate of 30%. On January 1 of the current year, the company had on hand inventory with a cost of $150,000. Purchases of merchandise

Principles of Financial Accounting ACC-101-TE. TECEP Test Description

Principles of Financial Accounting ACC-101-TE TECEP Test Description This TECEP is an introduction to the field of financial accounting. It covers the accounting cycle, merchandising concerns, and financial

Principles of Financial Accounting ACC-101-TE TECEP Test Description This TECEP is an introduction to the field of financial accounting. It covers the accounting cycle, merchandising concerns, and financial

4/10/2012. Inventories and Cost of Goods Sold. Learning Objectives (LO) Learning Objectives (LO) LO 1 Gross Profit and Cost of Goods Sold

Learning Objectives (LO) LO 1 Gross Profit and Cost of Goods Sold") Learning Objectives (LO) Inventories and Cost of Goods Sold CHAPTER 7 After studying this chapter, you should be able to 1. Link inventory valuation to gross profit 2. Use both perpetual and periodic inventory

Learning Objectives (LO) Inventories and Cost of Goods Sold CHAPTER 7 After studying this chapter, you should be able to 1. Link inventory valuation to gross profit 2. Use both perpetual and periodic inventory

Chapter Review Problems

Chapter Review Problems Unit 17.1 Income statements 1. When revenues exceed expenses, is the result (a) net income or (b) net loss? (a) net income 2. Do income statements reflect profits of a business

Chapter Review Problems Unit 17.1 Income statements 1. When revenues exceed expenses, is the result (a) net income or (b) net loss? (a) net income 2. Do income statements reflect profits of a business

Page 1 of 6 Ehab Abdou (97672930)

") Inventory Issues: 1- Recording inventory There are two systems (methods) used in recording Inventory Perpetual Inventory system نظام الجرد المستمر 1- Beginning Inventory 100 Units at $6 per unit No Entry

Inventory Issues: 1- Recording inventory There are two systems (methods) used in recording Inventory Perpetual Inventory system نظام الجرد المستمر 1- Beginning Inventory 100 Units at $6 per unit No Entry

When you are low on cash but need to pick up party

C H A P T E R 6 Accounting for Merchandising Businesses Susan Van Etten D O L L A R T R E E S T O R E S, I N C. When you are low on cash but need to pick up party supplies, housewares, or other consumer

C H A P T E R 6 Accounting for Merchandising Businesses Susan Van Etten D O L L A R T R E E S T O R E S, I N C. When you are low on cash but need to pick up party supplies, housewares, or other consumer

Accounting 303 Exam 3, Chapters 7-9 Fall 2013 Section Row

Accounting 303 Name Exam 3, Chapters 7-9 Fall 2013 Section Row I. Multiple Choice Questions. (2 points each, 28 points in total) Read each question carefully and indicate your answer by circling the letter

Accounting 303 Name Exam 3, Chapters 7-9 Fall 2013 Section Row I. Multiple Choice Questions. (2 points each, 28 points in total) Read each question carefully and indicate your answer by circling the letter

Perpetual vs. Periodic Inventory Accounting

Chapter 6 INVENTORY In the balance sheet of merchandising and manufacturing companies, inventory is frequently the most significant current asset. In the income statement, inventory is vital in determining

Chapter 6 INVENTORY In the balance sheet of merchandising and manufacturing companies, inventory is frequently the most significant current asset. In the income statement, inventory is vital in determining

Accounting 303 Exam 3, Chapters 7-9 Fall 2012 Section Row

Accounting 303 Name Exam 3, Chapters 7-9 Fall 2012 Section Row I. Multiple Choice Questions. (2 points each, 34 points in total) Read each question carefully and indicate your answer by circling the letter

Accounting 303 Name Exam 3, Chapters 7-9 Fall 2012 Section Row I. Multiple Choice Questions. (2 points each, 34 points in total) Read each question carefully and indicate your answer by circling the letter

Engineering Economics 2013/2014 MISE

Problem: JS, Inc. shows the following accounting records for 2011: Sales commissions 15000 Beginning merchandise inventory 16000 Ending merchandise inventory 9000 Sales 185000 Advertising 10000 Purchases

Problem: JS, Inc. shows the following accounting records for 2011: Sales commissions 15000 Beginning merchandise inventory 16000 Ending merchandise inventory 9000 Sales 185000 Advertising 10000 Purchases

Chapter 8. Inventory Chapters. Learning Objectives. Learning Objectives. Inventory. Inventory. Valuation of Inventories: A Cost-Basis Approach

Chapter 8 Valuation of Inventories: A Cost-Basis Approach Chapters Topic of chapters 8 and 9 : Asset on balance sheet Cost of goods sold: Expense on I/S See Safeway, Dr. Pepper, Campbell, Grainger, Amazon,

Chapter 8 Valuation of Inventories: A Cost-Basis Approach Chapters Topic of chapters 8 and 9 : Asset on balance sheet Cost of goods sold: Expense on I/S See Safeway, Dr. Pepper, Campbell, Grainger, Amazon,

Chapter 8. Reporting and Analyzing Receivables

Chapter 8 Reporting and Analyzing Receivables Study Objective 1 - Identify the Different Types of Receivables The term receivables refers to amounts due from individuals and companies. Receivables are

Chapter 8 Reporting and Analyzing Receivables Study Objective 1 - Identify the Different Types of Receivables The term receivables refers to amounts due from individuals and companies. Receivables are

Granite Bay Jet Ski, Incorporated

Granite Bay Jet Ski, Incorporated Level II 5 th Edition Transactions For June 24-30 Page 1 June 24 Issued the following checks as payment in full for miscellaneous billings: Check 31230 to Edwards Auto

Granite Bay Jet Ski, Incorporated Level II 5 th Edition Transactions For June 24-30 Page 1 June 24 Issued the following checks as payment in full for miscellaneous billings: Check 31230 to Edwards Auto

Intermediate Accounting

Intermediate Accounting Thomas H. Beechy Schulich School of Business, York University Joan E. D. Conrod Faculty of Management, Dalhousie University PowerPoint slides by: Bruce W. MacLean, Faculty of Management,

Intermediate Accounting Thomas H. Beechy Schulich School of Business, York University Joan E. D. Conrod Faculty of Management, Dalhousie University PowerPoint slides by: Bruce W. MacLean, Faculty of Management,

Financial Statements and Ratios: Notes

Financial Statements and Ratios: Notes 1. Uses of the income statement for evaluation Investors use the income statement to help judge their return on investment and creditors (lenders) use it to help

Financial Statements and Ratios: Notes 1. Uses of the income statement for evaluation Investors use the income statement to help judge their return on investment and creditors (lenders) use it to help

Module 3 - Inventory Definitions

Module 3 - Inventory Definitions Inventory goods held for resale COGS expenses incurred to purchase or manufacture the merchandise sold for a period Raw material Work-In-Process Finished Goods Inventory

Module 3 - Inventory Definitions Inventory goods held for resale COGS expenses incurred to purchase or manufacture the merchandise sold for a period Raw material Work-In-Process Finished Goods Inventory

For more course tutorials visit www.uoptutorial.com

ACC 290 Final Exam Guide (New) Click Here to Buy the Tutorial http://www.uoptutorial.com/index.php?route=product/ product&path=737&product_id=11101 For more course tutorials visit www.uoptutorial.com ACC

ACC 290 Final Exam Guide (New) Click Here to Buy the Tutorial http://www.uoptutorial.com/index.php?route=product/ product&path=737&product_id=11101 For more course tutorials visit www.uoptutorial.com ACC

Jackson Company recorded the following cash transactions for the year:

ACC 290 Final Exam Guide (New) Click Here to Buy the Tutorial http://www.uoptutorial.com/index.php?route=product/product&path=7 37&product_id=11101 For more course tutorials visit www.uoptutorial.com ACC

ACC 290 Final Exam Guide (New) Click Here to Buy the Tutorial http://www.uoptutorial.com/index.php?route=product/product&path=7 37&product_id=11101 For more course tutorials visit www.uoptutorial.com ACC

Accounting for a Merchandising Business

CHAPTER 10 Accounting for a Merchandising Business SECTION 10.1 REVIEW QUESTIONS (page 401) 1. A service business sells a service to the general public but does not deal in merchandise. For example, a

CHAPTER 10 Accounting for a Merchandising Business SECTION 10.1 REVIEW QUESTIONS (page 401) 1. A service business sells a service to the general public but does not deal in merchandise. For example, a

1. Analyze the following T-account in the ledger of Moxy Pool Supply Company

Name: Date: 1. Analyze the following T-account in the ledger of Moxy Pool Supply Company Mdse. Inventory 5,000 400 If $5,000 in the Inventory account represents merchandise purchased from a supplier, we

Name: Date: 1. Analyze the following T-account in the ledger of Moxy Pool Supply Company Mdse. Inventory 5,000 400 If $5,000 in the Inventory account represents merchandise purchased from a supplier, we

Study Guide - Final Exam Accounting I

Study Guide - Final Exam Accounting I True/False Indicate whether the sentence or statement is true or false. 1. Entries in a sales journal affect account balances in both the accounts receivable ledger

Study Guide - Final Exam Accounting I True/False Indicate whether the sentence or statement is true or false. 1. Entries in a sales journal affect account balances in both the accounts receivable ledger

Chapter 5 In-Class Exercise Merchandising

Chapter 5 In-Class Exercise Merchandising 1. The following events pertain to Downtown Toy Shop for October 2016. The company uses the perpetual inventory method. Record the following transactions in general

Chapter 5 In-Class Exercise Merchandising 1. The following events pertain to Downtown Toy Shop for October 2016. The company uses the perpetual inventory method. Record the following transactions in general

Chapter 27 Pricing Math. Section 27.1 Calculating Prices Section 27.2 Calculating Discounts

Chapter 27 Pricing Math Section 27.1 Calculating Prices Section 27.2 Calculating Discounts Calculating Prices Key Terms gross profit maintained markup Objectives Explain how a firm s profit is related

Chapter 27 Pricing Math Section 27.1 Calculating Prices Section 27.2 Calculating Discounts Calculating Prices Key Terms gross profit maintained markup Objectives Explain how a firm s profit is related

Chapter 8 Topic 1. Chapter 8: Topic 1 Valuation of Inventories The Basics. Student Learning Outcomes. Inventories: Financial Analysis

Chapter 8: Topic 1 Valuation of Inventories The Basics Dr. Chula King ACG 3101 Student Learning Outcomes Perpetual versus periodic inventory system Effects of inventory errors Items to include in inventory

Chapter 8: Topic 1 Valuation of Inventories The Basics Dr. Chula King ACG 3101 Student Learning Outcomes Perpetual versus periodic inventory system Effects of inventory errors Items to include in inventory

Accounting for a Merchandising Business

Chapter 11 Accounting for a Merchandising Business ANSWERS TO SECTION 11.1 REVIEW QUESTIONS (text p. 428) The Merchandising Business 1. 2. 3. 4. 5. 6. 7. 8. 9. 10. 11. 12. 13. 1. 2. 3. 4. 14. 15. Copyright

Chapter 11 Accounting for a Merchandising Business ANSWERS TO SECTION 11.1 REVIEW QUESTIONS (text p. 428) The Merchandising Business 1. 2. 3. 4. 5. 6. 7. 8. 9. 10. 11. 12. 13. 1. 2. 3. 4. 14. 15. Copyright

Financial/Accounting Analysis Ratios Excel Calculator

User Guide Financial/Accounting Analysis Ratios Excel Calculator Dec 2008 Version 2 copyright 2008 Business Tools Templates Financial/Accounting Analysis Ratios Excel Calculator Financial Analysis Ratios

User Guide Financial/Accounting Analysis Ratios Excel Calculator Dec 2008 Version 2 copyright 2008 Business Tools Templates Financial/Accounting Analysis Ratios Excel Calculator Financial Analysis Ratios

Inventories: Cost Measurement and Flow Assumptions

CHAPTER Inventories: Cost Measurement and Flow Assumptions OBJECTIVES After careful study of this chapter, you will be able to: 1. Describe how inventory accounts are classified. 2. Explain the uses of

CHAPTER Inventories: Cost Measurement and Flow Assumptions OBJECTIVES After careful study of this chapter, you will be able to: 1. Describe how inventory accounts are classified. 2. Explain the uses of

Dr. M.D. Chase Accounting Principles Examination 2J Page 1

Accounting Principles Examination 2J Page 1 Code 1 1. The term "net sales" refers to gross sales revenue reduced by sales discounts and transportation-in. 2. The cost of goods available for sale in a given

Accounting Principles Examination 2J Page 1 Code 1 1. The term "net sales" refers to gross sales revenue reduced by sales discounts and transportation-in. 2. The cost of goods available for sale in a given

Tutoring Monk. Exam 3 Notes Chapter 6

Tutoring Monk Have No Fear, The Monks Are Here Exam 3 Notes Chapter 6 To supplement these notes, please watch the videos FIRST. Video Access: http://www.accounting1.tutoringmonk.com Chapter 6 Please refer

Tutoring Monk Have No Fear, The Monks Are Here Exam 3 Notes Chapter 6 To supplement these notes, please watch the videos FIRST. Video Access: http://www.accounting1.tutoringmonk.com Chapter 6 Please refer

Learning Objectives: Quick answer key: Question # Multiple Choice True/False. 14.1 Describe the important of accounting and financial information.

0 Learning Objectives: 14.1 Describe the important of accounting and financial information. 14.2 Differentiate between managerial and financial accounting. 14.3 Identify the six steps of the accounting

0 Learning Objectives: 14.1 Describe the important of accounting and financial information. 14.2 Differentiate between managerial and financial accounting. 14.3 Identify the six steps of the accounting

In the event of a tie, the score on the last ten questions will be used as a tie-breaker.

NEW YORK STATE ASSOCIATION FUTURE BUSINESS LEADERS OF AMERICA SPRING DISTRICT MEETING ACCOUNTING I 2010 TEST DIRECTIONS 1. Complete the information requested on the answer sheet. PRINT your name on the

NEW YORK STATE ASSOCIATION FUTURE BUSINESS LEADERS OF AMERICA SPRING DISTRICT MEETING ACCOUNTING I 2010 TEST DIRECTIONS 1. Complete the information requested on the answer sheet. PRINT your name on the

Course- Financial Management.

Course- Financial Management. PHAR 4233 Semester/Year: Spring 2015 Lecture Objective Template Lecture #1/2 Date/time: 10:00 AM 1/6-7/2015 Lecture/Name Topic: Introduction to Financial Management and Accounting

Course- Financial Management. PHAR 4233 Semester/Year: Spring 2015 Lecture Objective Template Lecture #1/2 Date/time: 10:00 AM 1/6-7/2015 Lecture/Name Topic: Introduction to Financial Management and Accounting

CHAPTER 9 INVENTORIES: ADDITIONAL VALUATION ISSUES. MULTIPLE CHOICE Conceptual

CHAPTER 9 INVENTORIES: ADDITIONAL VALUATION ISSUES Answer No. Description MULTIPLE CHOICE Conceptual d 1. Knowledge of lower of cost or market valuations. d 2. Appropriate use of LCM valuation. c 3. Definition

CHAPTER 9 INVENTORIES: ADDITIONAL VALUATION ISSUES Answer No. Description MULTIPLE CHOICE Conceptual d 1. Knowledge of lower of cost or market valuations. d 2. Appropriate use of LCM valuation. c 3. Definition

CHAPTER 6 INVENTORIES SUMMARY OF QUESTIONS BY STUDY OBJECTIVES AND BLOOM S TAXONOMY. True-False Statements. Multiple Choice Questions

CHAPTER 6 INVENTORIES SUMMARY OF QUESTIONS BY STUDY OBJECTIVES AND BLOOM S TAXONOMY Item SO BT Item SO BT Item SO BT Item SO BT Item SO BT True-False Statements 1. 1 C 8. 2 C 15. 3 K 2. 1 C 9. 2 C 16.

CHAPTER 6 INVENTORIES SUMMARY OF QUESTIONS BY STUDY OBJECTIVES AND BLOOM S TAXONOMY Item SO BT Item SO BT Item SO BT Item SO BT Item SO BT True-False Statements 1. 1 C 8. 2 C 15. 3 K 2. 1 C 9. 2 C 16.

Bookkeeping Proficiency

Bookkeeping Proficiency (Exam) Your AccountingCoach PRO membership includes lifetime access to all of our materials. Take a quick tour by visiting www.accountingcoach.com/quicktour. Table of Contents (click

Bookkeeping Proficiency (Exam) Your AccountingCoach PRO membership includes lifetime access to all of our materials. Take a quick tour by visiting www.accountingcoach.com/quicktour. Table of Contents (click

PROFESSOR S NAME ACC 255 FALL 2011 COVER SHEET FOR COMPREHENSIVE PROBLEM 2 (CHAPTERS 2, 5-8)

") COMPREHENSIVE PROBLEM 2 (CHAPTERS 2, 5-8) Page 137 NAME ANSWER KEY PROFESSOR S NAME SECTION SCORE ACC 255 FALL 2011 COVER SHEET FOR COMPREHENSIVE PROBLEM 2 (CHAPTERS 2, 5-8) INSTRUCTIONS: COMPLETE ALL

COMPREHENSIVE PROBLEM 2 (CHAPTERS 2, 5-8) Page 137 NAME ANSWER KEY PROFESSOR S NAME SECTION SCORE ACC 255 FALL 2011 COVER SHEET FOR COMPREHENSIVE PROBLEM 2 (CHAPTERS 2, 5-8) INSTRUCTIONS: COMPLETE ALL

Chapter 2: Debits and Credits. 2012 Educating Bookkeepers for Business, Inc.

Chapter 2: Debits and Credits Think through and record transactions (write sentences) using T-accounts and journal entries. Debits and Credits Every transaction (sentence in the story of what happened

Chapter 2: Debits and Credits Think through and record transactions (write sentences) using T-accounts and journal entries. Debits and Credits Every transaction (sentence in the story of what happened

Income Measurement and Profitability Analysis

PROFITABILITY ANALYSIS The following financial statements for Spencer Company will be used to demonstrate the calculation of the various ratios in profitability analysis. Spencer Company Comparative Balance

PROFITABILITY ANALYSIS The following financial statements for Spencer Company will be used to demonstrate the calculation of the various ratios in profitability analysis. Spencer Company Comparative Balance

Ch6. Student: 2. Cost of goods sold is an asset reported in the balance sheet and inventory is an expense reported in the income statement.

Ch6 Student: 1. Inventory is usually reported as a long-term asset in the balance sheet. 2. Cost of goods sold is an asset reported in the balance sheet and inventory is an expense reported in the income

Ch6 Student: 1. Inventory is usually reported as a long-term asset in the balance sheet. 2. Cost of goods sold is an asset reported in the balance sheet and inventory is an expense reported in the income