NEW YORK STATE DEPARTMENT OF FINANCIAL SERVICES REPORT ON MARKET CONDUCT EXAMINATION OF THE HSBC INSURANCE AGENCY (USA) INC. AND

|

|

|

- Gwendolyn Brooks

- 8 years ago

- Views:

Transcription

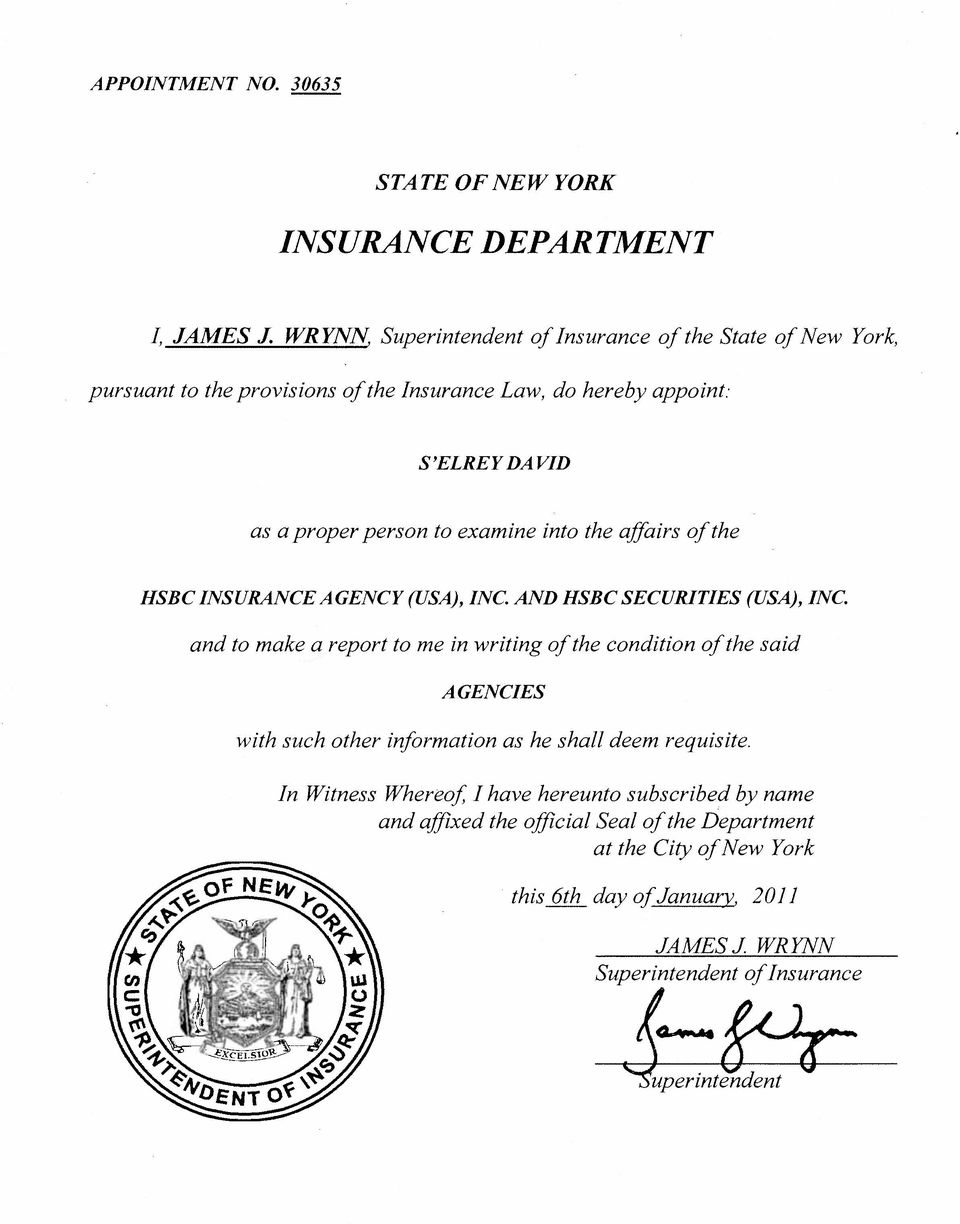

1 NEW YORK STATE DEPARTMENT OF FINANCIAL SERVICES REPORT ON MARKET CONDUCT EXAMINATION OF THE HSBC INSURANCE AGENCY (USA) INC. AND HSBC SECURITIES (USA) INC. CONDITION: DECEMBER 31, 2010 DATE OF REPORT: JUNE 30, 2011

INC.")

2 NEW YORK STATE DEPARTMENT OF FINANCIAL SERVICES REPORT ON MARKET CONDUCT EXAMINATION OF THE HSBC INSURANCE AGENCY (USA) INC. AND HSBC SECURITIES (USA) INC. AS OF DECEMBER 31, 2010 DATE OF REPORT: JUNE 30, 2011 EXAMINER: S EL REY N. DAVID

3 TABLE OF CONTENTS ITEM PAGE NO. 1. Executive summary 2 2. Scope of examination 3 3. Description of Agency 4 4. Market conduct activities 5 A. Complaints 5 B. New Business and Surrenders 7 C. Replacements Summary and conclusions 12

4

5 2 1. EXECUTIVE SUMMARY The recommendations contained in this report are summarized below. The examiner recommends that the Agencies, (1) prepare a list of all New York consumer complaints pertaining to the sale of life insurance policies or annuity contracts that the Agencies received, whether written or oral, during the period January 1, 2005 to December 31, 2010, (2) advise the insurer that issued the product of each such complaint and provide the insurer with a summary of the complaint and the manner in which it was resolved by the Agencies. (See Section 4A1) The examiner also recommends that all current and future complaints and their disposition be reported to the insurance carriers. (See Section 4A1)

6 3 2. SCOPE OF EXAMINATION The examiner conducted a target examination of the Agencies policies and procedures with respect to the handling of complaints and the solicitation of life and annuity contracts, including replacements, during the period from January 1, 2005 through December 31, The examination comprised a review of market conduct activities and utilized the National Association of Insurance Commissioners Market Regulations Handbook or such other examination procedures, as deemed appropriate, in such review. The objective of the examination was to determine whether the Agencies satisfied and complied with applicable New York Insurance Law and Department regulations and circular letters, the rules and guidelines set forth in sales and servicing agreements with licensed insurers, the operating rules and guidelines of the Agencies, and internal control standards. In connection with the examination of the Agencies, information was also requested from the licensed insurers who had appointed the Agencies to solicit their products. This report on examination is confined to comments on those matters which involve departure from laws, regulations or rules, or which require explanation or description.

7 4 3. DESCRIPTION OF AGENCIES HSBC Securities (USA) Inc. ( HSI ) is a Delaware corporation headquartered in New York City and is a wholly-owned subsidiary of HSBC Markets USA Inc. ( HMUS ). HSBC Insurance Agency (USA) Inc. ( HIA ) is a New York domiciled insurance agency and is a wholly-owned subsidiary of HSBC Bank USA, N.A. ( HBUS ). Both entities are wholly-owned indirect subsidiaries of HSBC North American Holdings Inc. ( HNAH ), which is a wholly owned indirect subsidiary of HSBC Holdings plc, the ultimate holding company in the HSBC group of companies. HSI is registered as a broker-dealer with the Securities and Exchange Commission and is a member of the Financial Industry Regulatory Authority ( FINRA ). HSI is registered as an Agency for distribution of annuity and insurance products and currently has 481 retail registered branch offices throughout the US, the majority of which are in New York. HSI operates under a Networking Agreement, conducting business on the premises of HBUS. HIA has 1,262 licensed agents, primarily located in New York, and offers a broad range of insurance products Term, Whole Life, Universal and Variable Life, as well as Long Term Care Insurance, Disability Insurance, and Property & Casualty Products, through third party carriers to customers of HBUS. HSI and HIA were appointed to sell annuities and life insurance products by 23 and 55 New York licensed life insurers, respectively. HSI averages annual sales of approximately 10,000 contracts, with fixed annuities accounting for 70% of them. Whole life policies represent the greatest percentage of HIA s business. As a standard business practice, HSI signs off on all variable life contract sales. The two entities share in most respects agents and branch locations, and are supported by their respective legal, compliance, and sales infrastructure personnel.

, which is a wholly owned indirect subsidiary of HSBC Holdings plc, the ultimate holding company in the HSBC group of companies.")

8 5 4. MARKET CONDUCT ACTIVITIES The examiner reviewed various elements of the Agencies market conduct activities affecting policyholders, applicants and complainants to determine compliance with applicable statutes and regulations and the operating rules of the Agencies. A. Complaints The examiner reviewed various elements of the Agencies complaint handling processes to determine compliance with applicable statutes and regulations, the rules and guidelines set forth in sales and servicing agreements with licensed insurers, the operating rules and guidelines of the Agencies, and internal control standards. HIA defines a complaint as, an expressing by or on behalf of a client of dissatisfaction with a service provided. A complaint may be oral or written, delivered by telephone or in person. A written record is required to be made of all oral complaints. All complaints received by an Agent are time stamped and logged by the Agent. The responsibility for reviewing and providing a prompt response to all complaints has been delegated to the Insurance Compliance Department ( ICD ). Regardless of how a complaint is received, the type of complaint, or the source of the complaint, client, regulator, attorney, etc, ICD sends an Acknowledgment Letter to the client before forwarding the complaint to the proper party for resolution. In the case of an oral complaint, the specific nature of the complaint will be recorded in the Acknowledgment Letter. Once the complaint has been fully investigated and a determination made, a letter is sent to the client detailing the reason for denial or the nature of the settlement. HSI defines a customer complaint as, any grievance, verbal or written, regarding HSI or a HSI Registered Representative, whether initiated by a customer or someone acting on behalf of the customer. All complaints must be reported to the Compliance Department ( Compliance ) to ensure accurate and timely reporting and tracking by the Agency. When a written complaint is received, a copy is forwarded immediately to Compliance for follow-up. Verbal complaints are handled by the Regional Sales Manager or their qualified designee unless deemed otherwise and reported to Compliance via the Lotus Notes based Verbal Customer Complaint System. All customer complaints that are subject to FINRA reporting requirements must be acknowledged within 15 business days of receipt. The acknowledgment may be by letter or in the same format

9 6 that the complaint was received in. Responses to customers regarding the resolution of a complaint are sent promptly, based on the nature of the complaint and the time necessary to investigate the issues raised in the complaint. The Agencies provided a data file of 314 complaints, 45 insurance policy related complaints and 269 annuity contract related complaints, received during the period under examination. Of the complaints reviewed, 13 were received from the Department s Consumer Services Bureau. The examiner selected a sample of 78 complaint files, 14 of which were received by HIA and 64 by HSI. The sample was selected with an emphasis on complaints regarding misrepresentation or suitability. 1. Complaint Reporting The sales and services agreements between the Agencies and the licensed insurers call for the Agencies, to promptly notify the insurers of any complaint, oral or written, or to notify the insurers of written complaints only. In 29 of the 78 complaint files reviewed, the complaint was forwarded to the Agencies by the insurance carrier. In the 49 complaint files where the complaint was received directly by the Agencies, the examiner s review revealed 42 instances that should have been reported to the insurance carriers in accordance with the selling agreement. In 39 (92.9%) of the 42 instances, the examiner found no evidence in the complaint file that the Agencies notified the insurance carrier of the complaint. The Agencies failed to comply with its selling agreement with the insurance carriers. The examiner recommends that the Agencies, (1) prepare a list of all New York consumer complaints pertaining to the sale of life insurance policies or annuity contracts that the Agencies received, whether written or oral, during the period January 1, 2005 to December 31, 2010, (2) advise the insurer that issued the product of each such complaint and provide the insurer with a summary of the complaint and the manner in which it was resolved by the Agencies. The examiner also recommends that all current and future complaints and their disposition be reported to the insurance carriers.

10 7 In response to the examiner s finding, the Agencies agreed that it will promptly report all customer complaints to all insurance carriers, whether required in the selling agreements or not. The Agencies also stated that all customer complaints received in 2011 have been reported to the relevant insurance carrier(s). 2. Complaint Handling Following are summaries of the complaints reviewed where the examiner noted the Agencies lack of adequate procedures along with the examiner s recommendations: In 3 instances the clients complained that they did not understand the products sold to them due to difficulty understanding the English language. The examiner s review revealed that the Agencies do not have a procedure in place to ensure that clients for whom English is not a primary language, have an understanding of both the product and the documents that are presented to them. The examiner recommends that the Agencies implement a procedure to ensure that clients for whom English is not the primary language, have an understanding of the product proposed to them, prior to completing the transaction. In one instance a sub-agent of the Agencies was fined by the Department for not providing Department Regulation No. 60 disclosures on a replacement policy. The examiner s review revealed that the Agencies failed to notify the insurance carrier that issued the life insurance policy, of the disciplinary action involving the sub-agent. The examiner recommends that the Agencies report Department disciplinary actions/fines to the issuing insurance carrier(s). B. New Business and Surrenders The examiner reviewed various elements of the Agencies new business files and surrender files to determine compliance with applicable statutes and regulations, compliance with the operating rules and guidelines of the Agencies, and compliance with internal control standards. The Agencies provided a data file of 9,208 life insurance (including universal life and variable life) policies, 39,580 fixed annuities and 13,281 variable annuities. 1. New Life Policy Business Files

11 8 The examiner reviewed a sample of 47 new life business files processed by HIA and HSI. Based upon the sample reviewed, no significant findings were noted. 2. New Annuity Contract Business Files The Agencies utilize a structure and system of supervision on new business sales to ensure that it is in compliance with Agencies policies and procedures. The Regional Sales Managers are responsible for overseeing the Registered Representatives/Agents and others under their supervision; as well as enforcing policies and procedures in their respective regions. The Middle Office Group in Buffalo, which is responsible for reviewing insurance and annuity submissions, provides an independent review of all applications and ensures that any required pre-sale approvals are documented. The Middle Office also validates the reviews and approvals made by the Regional Sales Managers and ensures that all customer information is provided and is compliant with the Agencies suitability guidelines. Trades identified as Not in Good Order are rejected by the Middle Office and returned to the Registered Representative/Agent for correction. The examiner reviewed a sample of 65 new business files, 48 fixed annuities and 17 variable annuities, processed by HSI. HSI procedures require supervisory pre-sale approval for certain transactions. A Registered Representative is required to obtain pre-approval from their Regional Sales Manager or their qualified designee, or their Sales Director for transactions such as sales involving new fixed or variable annuity contract into a tax qualified plan, sales of variable/fixed annuity or a variable life insurance policy to a customer over 65 years old, sales where the ratio of scheduled/target premium to income exceeds 60%, etc. The examiner s review of HSI s new business files revealed instances where HSI failed to adhere to its procedures regarding supervisory approval and/or documentation. In 10 out of 65 (15.4%) new business files reviewed, HSI failed to provide evidence that all required supervisory pre-sale approvals and/or waivers were obtained. The examiner recommends that HSI enhance its training and supervisory activities to ensure that all required supervisory pre-sale approvals and waivers are obtained prior to documentation being forwarded to the insurance carrier, in accordance with its policies and procedures.

12 9 HSI ensures compliance with its policies and procedures by maintaining standardized forms such as annuity disclosure and investment acknowledgement forms, switch authorization forms, supervisory trade approval forms, etc. The Registered Representatives/Agents are required to use the standardized forms in all transactions, and therefore have limited ability to make sales over prescribed limits. The client s financial information, investment objective, time horizon and risk tolerance are recorded on multiple forms and form the basis for the analysis of the product s suitability. The examiner s review revealed inconsistencies in the information recorded in the standardized forms. In addition, documents were sometimes not dated correctly or changes therein were not evidenced by the applicant s initial. In 20 out of 65 (30.8%) new business files reviewed, the HSI s internal documentation was incomplete or inconsistent and was not returned as Not in Good Order by the Middle Office. The examiner recommends that HSI enhance its training and supervisory activities to ensure that all required internal documentation are completed fully and correctly, and that all internal documentation and documents forwarded to the insurance carrier are consistent. In particular the examiner recommends that: all documents required to be signed by the client are fully completed at the time of signature all documents are dated to accurately reflect when the client s signature was obtained all changes to documentation are initialed by the client the amounts entered on to the Account Application for Estimated Net Worth and Liquid Assets, are stated at the amount available before deducting the amount necessary to purchase the policy or contract 3. Cancelled and Surrendered Files The examiner selected a sample of 50 contracts issued to clients 65 years and above, and cancelled or surrendered during the examination period, from an inventory of 2,191 cancelled or surrendered contracts provided by the Agencies top eight insurance carriers, based on number of contracts sold by the Agencies. Included in the 50, were 8 single premium universal life policies, 24 fixed annuity contracts, and 18 variable annuity contracts. The sample was selected

13 10 to verify that seniors were not being targeted by agents and sold products that were not appropriate for their investment objectives. Of the 50 files reviewed, 25 (50.0%) were surrendered within one year of issue and 40 (80.0%) were surrendered within the surrender charge period. In 2008, the Group Financial Services and European Audit issued a report on HSBC Insurance North America, encompassing the work of HBUS. The report focused on ensuring that the key risks arising from the activities of the entity were being managed in an appropriate manner and in accordance with expected Group standards. In the Section on Insurance Distribution, under Sales Compliance Monitoring, the report contained the following relating to the Insurance Compliance Function: " do not monitor risk factors such as early cancellations or whether any branches/agents are unusually successful in order to enable them to assess where there are increased risks of compliance failures nor have they revisited any branches that have previously failed a review although they do ask management to certify that any issues have been addressed." The examiner s review revealed that the Agencies have no procedure in place to monitor early cancelations for evidence of compliance failures, including potential suitability issues. The examiner recommends that the Agencies review all contracts surrendered or otherwise terminated within one year of the issue date for compliance failures, as well as potential suitability issues. The examiner s review also noted the following: 19 (38.0%) of the cancelled and surrendered files reviewed did not contain the required supervisory approval, and/or documentation at the time of issue. 5 (10.0%) of the cancelled and surrendered files reviewed did not contain evidence that all required supervisory pre-approvals were obtained. 17 (34.0%) of the cancelled and surrendered files reviewed contain documentation that was incomplete or inconsistent. C. Replacements The examiner reviewed the Agencies replacement handling process to determine compliance with Department Regulation No. 60 and the operating rules and guidelines of the Agencies.

14 11 In response to the examiner s request for an inventory of policies and contracts replaced by the Agencies during the period under examination, the Agencies provided data files of 422 life policies, 6,809 fixed annuities and 2,367 variable annuities. The examiner reviewed a sample of 50 replacement files, 16 processed by HIA and 34 processed by HSI. The examiner s review revealed that, although the Agencies made reasonable attempts to comply with Department Regulation No. 60, there were deviations from technical aspects of the regulation. For example, the agent failed to answer the question regarding the use of sales materials on the Disclosure Statement, or the agent failed to provide evidence that a copy of any proposal, including the sales material used in the sale of the proposed life insurance policy or annuity contract was provided to the insurer. In response to the examiners findings, the Agencies stated that it has distributed Department Regulation No. 60 Compliance Procedures to all its agents. In addition, the Agencies stated that it has incorporated this training into its Financial Advisor New Hire Training program, which became effective in June The Agencies anticipate that this training, in addition to enhanced diligence by the Agencies Middle Office to the proper completion of documentation, will address the Department Regulation No. 60 issues noted by the examiners during the audit.

15 12 5. SUMMARY AND CONCLUSIONS Following are the recommendations contained in this report: Item Description Page No(s). A The examiner recommends that the Agencies, (1) prepare a list of all New York consumer complaints pertaining to the sale of life insurance policies or annuity contracts that the Agencies received, whether written or oral, during the period January 1, 2005 to December 31, 2010, (2) advise the insurer that issued the product of each such complaint and provide the insurer with a summary of the complaint and the manner in which it was resolved by the Agencies. 6 B The examiner also recommends that all current and future complaints and their disposition be reported to the insurance carriers. 6 C The examiner recommends that the Agencies implement a procedure to ensure that clients for whom English is not the primary language, have an understanding of the product proposed to them, prior to completing the transaction. 7 D The examiner recommends that the Agencies report Department disciplinary actions/fines to the issuing insurance carrier(s). 7 E The examiner recommends that HSI enhance its training and supervisory activities to ensure that all required supervisory pre-sale approvals and waivers are obtained prior to documentation being forwarded to the insurance carrier, in accordance with its policies and procedures. 8 F The examiner recommends that HSI enhance its training and supervisory activities to ensure that all required internal documentation are completed fully and correctly, and that all internal documentation and documents forwarded to the insurance carrier are consistent. 9 G The examiner recommends that the Agencies review all contracts surrendered or otherwise terminated within one year of the issue date for compliance failures, as well as potential suitability issues. 10

16

17

NEW YORK STATE DEPARTMENT OF FINANCIAL SERVICES REPORT ON MARKET CONDUCT EXAMINATION OF THE CHASE INSURANCE AGENCY AND

NEW YORK STATE DEPARTMENT OF FINANCIAL SERVICES REPORT ON MARKET CONDUCT EXAMINATION OF THE CHASE INSURANCE AGENCY AND CHASE INVESTMENT SERVICES CORPORATION CONDITION: DECEMBER 31, 2010 DATE OF REPORT:

NEW YORK STATE DEPARTMENT OF FINANCIAL SERVICES REPORT ON MARKET CONDUCT EXAMINATION OF THE CHASE INSURANCE AGENCY AND CHASE INVESTMENT SERVICES CORPORATION CONDITION: DECEMBER 31, 2010 DATE OF REPORT:

MEGA Life and Health Insurance Company Office of the President 9151 Grapevine Highway North Richland Hills, Texas 76180

TO: MEGA Life and Health Insurance Company Office of the President 9151 Grapevine Highway North Richland Hills, Texas 76180 RE: Delaware Market Conduct Examination #04-709 CONSENT DECREE WHEREAS, the MEGA

TO: MEGA Life and Health Insurance Company Office of the President 9151 Grapevine Highway North Richland Hills, Texas 76180 RE: Delaware Market Conduct Examination #04-709 CONSENT DECREE WHEREAS, the MEGA

02 DEPARTMENT OF PROFESSIONAL AND FINANCIAL REGULATION

02 DEPARTMENT OF PROFESSIONAL AND FINANCIAL REGULATION 031 BUREAU OF INSURANCE Chapter 917: SUITABILITY IN ANNUITY TRANSACTIONS Table of Contents Section 1. Section 2. Section 3. Section 4. Section 5.

02 DEPARTMENT OF PROFESSIONAL AND FINANCIAL REGULATION 031 BUREAU OF INSURANCE Chapter 917: SUITABILITY IN ANNUITY TRANSACTIONS Table of Contents Section 1. Section 2. Section 3. Section 4. Section 5.

MARKET CONDUCT EXAMINATION NUMBER 2012C-0026 BROOKE LIFE INSURANCE COMPANY

STATE OF MICHIGAN DEPARTMENT OF LICENSING AND REGULATORY AFFAIRS MARKET CONDUCT EXAMINATION NUMBER 2012C-0026 TARGETED MARKET CONDUCT EXAMINATION REPORT OF BROOKE LIFE INSURANCE COMPANY LANSING, MICHIGAN

STATE OF MICHIGAN DEPARTMENT OF LICENSING AND REGULATORY AFFAIRS MARKET CONDUCT EXAMINATION NUMBER 2012C-0026 TARGETED MARKET CONDUCT EXAMINATION REPORT OF BROOKE LIFE INSURANCE COMPANY LANSING, MICHIGAN

IX 2.1. IX. Retail Sales Insurance. Retail Insurance Sales. Introduction. Regulatory and Policy Requirements. Examination Procedures

IX. Retail Sales Insurance Retail Insurance Sales Introduction The following supervisory information and examination procedures apply to retail sales, solicitation, advertising, or offers of any insurance

IX. Retail Sales Insurance Retail Insurance Sales Introduction The following supervisory information and examination procedures apply to retail sales, solicitation, advertising, or offers of any insurance

REVISED. SUITABILITY IN ANNUITY TRANSACTIONS MODEL REGULATION Executive Summary

REVISED SUITABILITY IN ANNUITY TRANSACTIONS MODEL REGULATION Executive Summary Commissioners Thomas R. Sullivan (CT) and Adam Hamm (ND) chair and vice chair of the Life Insurance and Annuities (A) Committee,

REVISED SUITABILITY IN ANNUITY TRANSACTIONS MODEL REGULATION Executive Summary Commissioners Thomas R. Sullivan (CT) and Adam Hamm (ND) chair and vice chair of the Life Insurance and Annuities (A) Committee,

MARKET CONDUCT EXAMINATION NUMBER 2015C-0082 EQUITRUST LIFE INSURANCE COMPANY

STATE OF MICHIGAN DEPARTMENT OF INSURANCE AND FINANCIAL SERVICES MARKET CONDUCT EXAMINATION NUMBER 2015C-0082 TARGETED MARKET CONDUCT EXAMINATION REPORT OF EQUITRUST LIFE INSURANCE COMPANY CHICAGO, ILLINOIS

STATE OF MICHIGAN DEPARTMENT OF INSURANCE AND FINANCIAL SERVICES MARKET CONDUCT EXAMINATION NUMBER 2015C-0082 TARGETED MARKET CONDUCT EXAMINATION REPORT OF EQUITRUST LIFE INSURANCE COMPANY CHICAGO, ILLINOIS

SUITABILITY IN ANNUITY TRANSACTIONS MODEL REGULATION

Model Regulation Service April 2010 SUITABILITY IN ANNUITY TRANSACTIONS MODEL REGULATION Table of Contents Section 1. Section 2. Section 3. Section 4. Section 5. Section 6. Section 7. Section 8. Section

Model Regulation Service April 2010 SUITABILITY IN ANNUITY TRANSACTIONS MODEL REGULATION Table of Contents Section 1. Section 2. Section 3. Section 4. Section 5. Section 6. Section 7. Section 8. Section

MARKET CONDUCT EXAMINATION REPORT OF PACIFIC LIFE INSURANCE COMPANY 700 NEWPORT CENTER DRIVE NEWPORT BEACH, CALIFORNIA 92660

MARKET CONDUCT EXAMINATION REPORT OF PACIFIC LIFE INSURANCE COMPANY 700 NEWPORT CENTER DRIVE NEWPORT BEACH, CALIFORNIA 92660 January 1, 1992 through December 31, 1996 BY THE OFFICE OF THE INSURANCE COMMISSIONER

MARKET CONDUCT EXAMINATION REPORT OF PACIFIC LIFE INSURANCE COMPANY 700 NEWPORT CENTER DRIVE NEWPORT BEACH, CALIFORNIA 92660 January 1, 1992 through December 31, 1996 BY THE OFFICE OF THE INSURANCE COMMISSIONER

CHAPTER 26.1-34.2 ANNUITY TRANSACTION PRACTICES

CHAPTER 26.1-34.2 ANNUITY TRANSACTION PRACTICES 26.1-34.2-01. Exemptions. Unless otherwise specifically included, this chapter does not apply to recommendations involving: 1. Direct response solicitations

CHAPTER 26.1-34.2 ANNUITY TRANSACTION PRACTICES 26.1-34.2-01. Exemptions. Unless otherwise specifically included, this chapter does not apply to recommendations involving: 1. Direct response solicitations

THE COMMONWEALTH OF MASSACHUSETTS

THE COMMONWEALTH OF MASSACHUSETTS OFFICE OF CONSUMER AFFAIRS AND BUSINESS REGULATION DIVISION OF INSURANCE Report on the Comprehensive Market Conduct Examination of The Paul Revere Variable Annuity Insurance

THE COMMONWEALTH OF MASSACHUSETTS OFFICE OF CONSUMER AFFAIRS AND BUSINESS REGULATION DIVISION OF INSURANCE Report on the Comprehensive Market Conduct Examination of The Paul Revere Variable Annuity Insurance

Chapter 89. Regulation 70 Replacement of Life Insurance and Annuities INSURANCE

INSURANCE I am a member of the American Academy of Actuaries (or if not, state other qualifications to sign annual statement actuarial opinions). I have examined the interest-indexed universal life insurance

INSURANCE I am a member of the American Academy of Actuaries (or if not, state other qualifications to sign annual statement actuarial opinions). I have examined the interest-indexed universal life insurance

Requirement 8368 Sales Procedure Update - Suitability of Annuity Transactions (MN H.B. 791)

") Effective: June 1, 2013 Requirement 8368 Sales Procedure Update - Suitability of Annuity Transactions (MN H.B. 791) In recommending to a consumer the purchase of an annuity or the exchange of an annuity

Effective: June 1, 2013 Requirement 8368 Sales Procedure Update - Suitability of Annuity Transactions (MN H.B. 791) In recommending to a consumer the purchase of an annuity or the exchange of an annuity

REPORT ON LIMITED LINES INSURANCE JANUARY 15, 2014. MSAR No. 9844

REPORT ON LIMITED LINES INSURANCE JANUARY 15, 2014 MSAR No. 9844 For more information concerning this document, please contact: Nancy J. Egan Assistant Director of Government Relations Maryland Insurance

REPORT ON LIMITED LINES INSURANCE JANUARY 15, 2014 MSAR No. 9844 For more information concerning this document, please contact: Nancy J. Egan Assistant Director of Government Relations Maryland Insurance

TARGETED MARKET CONDUCT EXAMINATION OF

A TARGETED MARKET CONDUCT EXAMINATION OF NATIONAL WESTERN LIFE INSURANCE COMPANY NAIC #66850 As Of December 31, 2009 John R. Kasich, Governor Mary Taylor, Lt. Governor/ Director 50 West Town Street Third

A TARGETED MARKET CONDUCT EXAMINATION OF NATIONAL WESTERN LIFE INSURANCE COMPANY NAIC #66850 As Of December 31, 2009 John R. Kasich, Governor Mary Taylor, Lt. Governor/ Director 50 West Town Street Third

Market Conduct Examination

Market Conduct Examination American General Life Insurance Company Houston, Texas STATE OF NEW JERSEY DEPARTMENT OF BANKING AND INSURANCE Division of Enforcement and Consumer Protection Market Conduct

Market Conduct Examination American General Life Insurance Company Houston, Texas STATE OF NEW JERSEY DEPARTMENT OF BANKING AND INSURANCE Division of Enforcement and Consumer Protection Market Conduct

GENERAL AGENT AGREEMENT

Complete Wellness Solutions, Inc. 6338 Constitution Drive Fort Wayne, Indiana 46804 GENERAL AGENT AGREEMENT This Agreement is made by and between Complete Wellness Solutions, Inc. (the Company ) and (the

Complete Wellness Solutions, Inc. 6338 Constitution Drive Fort Wayne, Indiana 46804 GENERAL AGENT AGREEMENT This Agreement is made by and between Complete Wellness Solutions, Inc. (the Company ) and (the

THE COMMONWEALTH OF MASSACHUSETTS. Division of Insurance. Arbella Indemnity Insurance Company, Inc.

THE COMMONWEALTH OF MASSACHUSETTS OFFICE OF CONSUMER AFFAIRS AND BUSINESS REGULATION Division of Insurance Report on the Comprehensive Market Conduct Examination of Arbella Indemnity Insurance Company,

THE COMMONWEALTH OF MASSACHUSETTS OFFICE OF CONSUMER AFFAIRS AND BUSINESS REGULATION Division of Insurance Report on the Comprehensive Market Conduct Examination of Arbella Indemnity Insurance Company,

FINANCIAL INSTITUTION AGREEMENT

Banner Life Insurance Company 3275 Bennett Creek Avenue Frederick, Maryland 21704 (800) 638-8428 FINANCIAL INSTITUTION AGREEMENT 1. Subject to the terms and conditions of this Agreement, the undersigned

Banner Life Insurance Company 3275 Bennett Creek Avenue Frederick, Maryland 21704 (800) 638-8428 FINANCIAL INSTITUTION AGREEMENT 1. Subject to the terms and conditions of this Agreement, the undersigned

CHAPTER 64 REGULATION GOVERNING SUITABILITY IN ANNUITY TRANSACTIONS

CHAPTER 64 REGULATION GOVERNING SUITABILITY IN ANNUITY TRANSACTIONS Section 1. Authority These rules and regulations governing the suitability in annuity transactions in the State of Wyoming supplement

CHAPTER 64 REGULATION GOVERNING SUITABILITY IN ANNUITY TRANSACTIONS Section 1. Authority These rules and regulations governing the suitability in annuity transactions in the State of Wyoming supplement

Consumer Affairs Laws Section 1380 and Regulations

Insurance Consumer Protection The Gramm-Leach-Bliley Financial Services Modernization Act (the Act) was enacted on November 12, 1999. Section 305 of the Act required the federal banking agencies (the Agencies)

Insurance Consumer Protection The Gramm-Leach-Bliley Financial Services Modernization Act (the Act) was enacted on November 12, 1999. Section 305 of the Act required the federal banking agencies (the Agencies)

MARKET CONDUCT EXAMINATION REPORT HARTFORD UNDERWRITERS INSURANCE COMPANY NAIC # 30104. One Hartford Plaza Hartford, Connecticut 06155-0001

MARKET CONDUCT EXAMINATION REPORT ON HARTFORD UNDERWRITERS INSURANCE COMPANY NAIC # 30104 One Hartford Plaza Hartford, Connecticut 06155-0001 EXAMINATION NUMBER 09.701 March 31, 2009 TABLE OF CONTENTS

MARKET CONDUCT EXAMINATION REPORT ON HARTFORD UNDERWRITERS INSURANCE COMPANY NAIC # 30104 One Hartford Plaza Hartford, Connecticut 06155-0001 EXAMINATION NUMBER 09.701 March 31, 2009 TABLE OF CONTENTS

State of Rhode Island and Providence Plantations DEPARTMENT OF BUSINESS REGULATION Division of Insurance 1511 Pontiac Avenue Cranston, RI 02920

State of Rhode Island and Providence Plantations DEPARTMENT OF BUSINESS REGULATION Division of Insurance 1511 Pontiac Avenue Cranston, RI 02920 INSURANCE REGULATION 12 SUITABILITY IN ANNUITY TRANSACTIONS

State of Rhode Island and Providence Plantations DEPARTMENT OF BUSINESS REGULATION Division of Insurance 1511 Pontiac Avenue Cranston, RI 02920 INSURANCE REGULATION 12 SUITABILITY IN ANNUITY TRANSACTIONS

WRAP FEE PROGRAM BROCHURE for the Guided Portfolio Services Program and Guided Portfolio Advantage Program (Part 2A Appendix 1 of Form ADV)

") Item 1 - Cover Page WRAP FEE PROGRAM BROCHURE for the Guided Portfolio Services Program and Guided Portfolio Advantage Program (Part 2A Appendix 1 of Form ADV) VALIC Financial Advisors, Inc. 2929 Allen

Item 1 - Cover Page WRAP FEE PROGRAM BROCHURE for the Guided Portfolio Services Program and Guided Portfolio Advantage Program (Part 2A Appendix 1 of Form ADV) VALIC Financial Advisors, Inc. 2929 Allen

REPORT OF MARKET CONDUCT EXAMINATION OF

REPORT OF MARKET CONDUCT EXAMINATION OF UNITED INSURANCE COMPANY OF AMERICA St. Louis, MI AS OF December 10, 2010 COMMONWEALTH OF PENNSYLVANIA INSURANCE DEPARTMENT MARKET CONDUCT DIVISION Issued: January

REPORT OF MARKET CONDUCT EXAMINATION OF UNITED INSURANCE COMPANY OF AMERICA St. Louis, MI AS OF December 10, 2010 COMMONWEALTH OF PENNSYLVANIA INSURANCE DEPARTMENT MARKET CONDUCT DIVISION Issued: January

004. Scope. This rule shall apply to all title insurers authorized to do business in Nebraska and all title insurance agents licensed in Nebraska.

Title 210 - NEBRASKA DEPARTMENT OF INSURANCE Chapter 34 - TITLE INSURANCE 001. Authority. This rule is adopted and promulgated by the Director of Insurance of the State of Nebraska pursuant to the Title

Title 210 - NEBRASKA DEPARTMENT OF INSURANCE Chapter 34 - TITLE INSURANCE 001. Authority. This rule is adopted and promulgated by the Director of Insurance of the State of Nebraska pursuant to the Title

DELAWARE DEPARTMENT OF INSURANCE MARKET CONDUCT EXAMINATION REPORT. PHL Variable Insurance Company NAIC #93548 One American Row Hartford, CT 06115

DELAWARE DEPARTMENT OF INSURANCE MARKET CONDUCT EXAMINATION REPORT NAIC #93548 One American Row Hartford, CT 06115 As of June 30, 2010 Table of Contents EXECUTIVE SUMMARY... 2 SCOPE OF EXAMINATION...

DELAWARE DEPARTMENT OF INSURANCE MARKET CONDUCT EXAMINATION REPORT NAIC #93548 One American Row Hartford, CT 06115 As of June 30, 2010 Table of Contents EXECUTIVE SUMMARY... 2 SCOPE OF EXAMINATION...

NASD Notice to Members 00-44. Executive Summary

INFORMATIONAL Variable Contracts The NASD Reminds Members Of Their Responsibilities Regarding The Sale Of Variable Life Insurance SUGGESTED ROUTING The Suggested Routing function is meant to aid the reader

INFORMATIONAL Variable Contracts The NASD Reminds Members Of Their Responsibilities Regarding The Sale Of Variable Life Insurance SUGGESTED ROUTING The Suggested Routing function is meant to aid the reader

MARKET CONDUCT EXAMINATION ST. PAUL FIRE AND MARINE INSURANCE COMPANY AND AFFILIATES 385 WASHINGTON STREET ST. PAUL, MINNESOTA 55102

MARKET CONDUCT EXAMINATION ST. PAUL FIRE AND MARINE INSURANCE COMPANY AND AFFILIATES 385 WASHINGTON STREET ST. PAUL, MINNESOTA 55102 MARCH 1, 2002 FEBRUARY 28, 2003 TABLE OF CONTENTS Section Page Table

MARKET CONDUCT EXAMINATION ST. PAUL FIRE AND MARINE INSURANCE COMPANY AND AFFILIATES 385 WASHINGTON STREET ST. PAUL, MINNESOTA 55102 MARCH 1, 2002 FEBRUARY 28, 2003 TABLE OF CONTENTS Section Page Table

GOLDEN RULE INSURANCE COMPANY

GOLDEN RULE INSURANCE COMPANY LIMITED SCOPE MARKET CONDUCT EXAMINATION REPORT NAIC COMPANY CODE: 62286 MICHIGAN OFFICE OF FINANCIAL AND INSURANCE REGULATION MARKET CONDUCT DEPARTMENT By Tracy Post, J.D.

GOLDEN RULE INSURANCE COMPANY LIMITED SCOPE MARKET CONDUCT EXAMINATION REPORT NAIC COMPANY CODE: 62286 MICHIGAN OFFICE OF FINANCIAL AND INSURANCE REGULATION MARKET CONDUCT DEPARTMENT By Tracy Post, J.D.

CODE OF CONDUCT MADE UNDER THE BERMUDA STOCK EXCHANGE TRADING MEMBERSHIP REGULATIONS

MADE UNDER THE BERMUDA STOCK EXCHANGE TRADING MEMBERSHIP REGULATIONS The Bermuda Stock Exchange All rights reserved CODE OF CONDUCT FOR TRADING MEMBERS 1 CITATION 1.1 This Code of Conduct shall be known

MADE UNDER THE BERMUDA STOCK EXCHANGE TRADING MEMBERSHIP REGULATIONS The Bermuda Stock Exchange All rights reserved CODE OF CONDUCT FOR TRADING MEMBERS 1 CITATION 1.1 This Code of Conduct shall be known

POLICY MANUAL. Responsibility: Approved by: Last Approval Date:

Page: 1 of 6 Section: SECTION F - Mandates Name: ATCO Audit & Risk Committee Responsibility: Approved by: Last Approval Date: Chair ATCO Audit & Risk ATCO Audit & Risk Committee February 23, Committee

Page: 1 of 6 Section: SECTION F - Mandates Name: ATCO Audit & Risk Committee Responsibility: Approved by: Last Approval Date: Chair ATCO Audit & Risk ATCO Audit & Risk Committee February 23, Committee

REPORT OF MARKET CONDUCT EXAMINATION OF

REPORT OF MARKET CONDUCT EXAMINATION OF CONSECO LIFE INSURANCE COMPANY Carmel, IN AS OF December 23, 2010 COMMONWEALTH OF PENNSYLVANIA INSURANCE DEPARTMENT MARKET CONDUCT DIVISION Issued: January 27, 2011

REPORT OF MARKET CONDUCT EXAMINATION OF CONSECO LIFE INSURANCE COMPANY Carmel, IN AS OF December 23, 2010 COMMONWEALTH OF PENNSYLVANIA INSURANCE DEPARTMENT MARKET CONDUCT DIVISION Issued: January 27, 2011

NASAA Recordkeeping Requirements For Investment Advisers Model Rule 203(a)-2 Adopted 9/3/87, amended 5/3/99, 4/18/04, 9/11/05; Amended 9/11/2011

-2 Adopted 9/3/87, amended 5/3/99, 4/18/04, 9/11/05; Amended 9/11/2011") NASAA Recordkeeping Requirements For Investment Advisers Model Rule 203(a)-2 Adopted 9/3/87, amended 5/3/99, 4/18/04, 9/11/05; Amended 9/11/2011 NOTE: Italicized information is explanatory and not intended

NASAA Recordkeeping Requirements For Investment Advisers Model Rule 203(a)-2 Adopted 9/3/87, amended 5/3/99, 4/18/04, 9/11/05; Amended 9/11/2011 NOTE: Italicized information is explanatory and not intended

Insurance Sales Management System Manual

System Manual A proper insurance underwriting management system must be established, under which directors, etc. recognize the importance of compliance and compliance-oriented corporate culture is cultivated,

System Manual A proper insurance underwriting management system must be established, under which directors, etc. recognize the importance of compliance and compliance-oriented corporate culture is cultivated,

THE COMMONWEALTH OF MASSACHUSETTS

THE COMMONWEALTH OF MASSACHUSETTS OFFICE OF CONSUMER AFFAIRS AND BUSINESS REGULATION DIVISION OF INSURANCE Report on the Comprehensive Market Conduct Examination of The Paul Revere Life Insurance Company

THE COMMONWEALTH OF MASSACHUSETTS OFFICE OF CONSUMER AFFAIRS AND BUSINESS REGULATION DIVISION OF INSURANCE Report on the Comprehensive Market Conduct Examination of The Paul Revere Life Insurance Company

CHAPTER 26.1-31.1 REINSURANCE INTERMEDIARIES

CHAPTER 26.1-31.1 REINSURANCE INTERMEDIARIES 26.1-31.1-01. Definitions. As used in this chapter: 1. "Actuary" means a person who is a member in good standing of the American academy of actuaries. 2. "Controlling

CHAPTER 26.1-31.1 REINSURANCE INTERMEDIARIES 26.1-31.1-01. Definitions. As used in this chapter: 1. "Actuary" means a person who is a member in good standing of the American academy of actuaries. 2. "Controlling

CHAPTER 2013-163. Committee Substitute for Committee Substitute for Senate Bill No. 166

CHAPTER 2013-163 Committee Substitute for Committee Substitute for Senate Bill No. 166 An act relating to annuities; amending s. 627.4554, F.S.; providing that recommendations relating to annuities made

CHAPTER 2013-163 Committee Substitute for Committee Substitute for Senate Bill No. 166 An act relating to annuities; amending s. 627.4554, F.S.; providing that recommendations relating to annuities made

Grievance Redressal Policy Max Life Insurance Company Limited

Grievance Redressal Policy Max Life Insurance Company Limited Distribution: Max Life website, Max Life customer portal, Agent portal, Maxters, Customer lounge in general offices Version: 2 Effective date:

Grievance Redressal Policy Max Life Insurance Company Limited Distribution: Max Life website, Max Life customer portal, Agent portal, Maxters, Customer lounge in general offices Version: 2 Effective date:

APPLICATION PACKAGE FOR INTERMEDIARY INSURANCE LICENSING (AGENT, BROKER AND SOLICITOR)

") APPLICATION PACKAGE FOR INTERMEDIARY INSURANCE LICENSING (AGENT, BROKER AND SOLICITOR) INSURANCE BOARD/COMMISSION FEDERATED STATES OF MICRONESIA TownPlaza building, Suite 12 P.O. Box K-2980 Kolonia Pohnpei,

APPLICATION PACKAGE FOR INTERMEDIARY INSURANCE LICENSING (AGENT, BROKER AND SOLICITOR) INSURANCE BOARD/COMMISSION FEDERATED STATES OF MICRONESIA TownPlaza building, Suite 12 P.O. Box K-2980 Kolonia Pohnpei,

The Direction of Annuity Suitability Regulation

The Direction of Annuity Suitability Regulation The future of annuity regulation is uncertain. Amidst suggestions that the state regulatory framework is not sufficient to protect consumers in annuity transactions,

The Direction of Annuity Suitability Regulation The future of annuity regulation is uncertain. Amidst suggestions that the state regulatory framework is not sufficient to protect consumers in annuity transactions,

INSURANCE AGENTS AND BROKERS ERRORS AND OMISSIONS APPLICATION

RETURN TO: ANGELA SCHRODER ANGELA@USEO.COM FAX: 281-480-1585 BROKERS INSURANCE AGENTS AND BROKERS ERRORS AND OMISSIONS APPLICATION Please Print or Type and complete all questions. Section I 1. Legal Entity

RETURN TO: ANGELA SCHRODER ANGELA@USEO.COM FAX: 281-480-1585 BROKERS INSURANCE AGENTS AND BROKERS ERRORS AND OMISSIONS APPLICATION Please Print or Type and complete all questions. Section I 1. Legal Entity

SPIN MASTER CORP. CHARTER OF THE AUDIT COMMITTEE

SPIN MASTER CORP. CHARTER OF THE AUDIT COMMITTEE 1. Introduction This charter (the Charter ) sets forth the purpose, composition, duties and responsibilities of the Audit Committee (the Committee ) of

SPIN MASTER CORP. CHARTER OF THE AUDIT COMMITTEE 1. Introduction This charter (the Charter ) sets forth the purpose, composition, duties and responsibilities of the Audit Committee (the Committee ) of

114CSR8 LEGISLATIVE RULES INSURANCE COMMISSIONER SERIES 8 REPLACEMENT OF LIFE INSURANCE POLICIES AND ANNUITY CONTRACTS

114CSR8 LEGISLATIVE RULES INSURANCE COMMISSIONER SERIES 8 REPLACEMENT OF LIFE INSURANCE POLICIES AND ANNUITY CONTRACTS Section 114-8-1. General. 114-8-2. Definitions. 114-8-3. Exemptions. 114-8-4. Duties

114CSR8 LEGISLATIVE RULES INSURANCE COMMISSIONER SERIES 8 REPLACEMENT OF LIFE INSURANCE POLICIES AND ANNUITY CONTRACTS Section 114-8-1. General. 114-8-2. Definitions. 114-8-3. Exemptions. 114-8-4. Duties

CHAPTER 88. AN ACT concerning certain annuity products, and supplementing chapter 25 of Title 17B of the New Jersey Statutes.

CHAPTER 88 AN ACT concerning certain annuity products, and supplementing chapter 25 of Title 17B of the New Jersey Statutes. BE IT ENACTED by the Senate and General Assembly of the State of New Jersey:

CHAPTER 88 AN ACT concerning certain annuity products, and supplementing chapter 25 of Title 17B of the New Jersey Statutes. BE IT ENACTED by the Senate and General Assembly of the State of New Jersey:

Anti-Money Laundering Program and Suspicious Activity Reporting Requirements For Insurance Companies. Frequently Asked Questions

Anti-Money Laundering Program and Suspicious Activity Reporting Requirements For Insurance Companies Frequently Asked Questions We are providing the following Frequently Asked Questions to assist insurance

Anti-Money Laundering Program and Suspicious Activity Reporting Requirements For Insurance Companies Frequently Asked Questions We are providing the following Frequently Asked Questions to assist insurance

DAIRYLAND INSURANCE COMPANY MARKET CONDUCT EXAMINATION OCTOBER 31, 1996- OCTOBER 31, 1997

DAIRYLAND INSURANCE COMPANY MARKET CONDUCT EXAMINATION OCTOBER 31, 1996- OCTOBER 31, 1997 Seattle Washington Deborah Senn Insurance Commissioner Olympia, Washington 98504 Pursuant to your instructions

DAIRYLAND INSURANCE COMPANY MARKET CONDUCT EXAMINATION OCTOBER 31, 1996- OCTOBER 31, 1997 Seattle Washington Deborah Senn Insurance Commissioner Olympia, Washington 98504 Pursuant to your instructions

September 2008. Claims Guideline

September 2008 Claims Guideline CLAIMS GUIDELINE Table of Contents 1 INTRODUCTION... 1 2 PURPOSE OF THE GUIDELINE... 1 3 DEFINITIONS... 2 MARKET CONDUCT 4 GENERAL REQUIREMENTS... 3 5 CLAIMS NOTIFICATION...

September 2008 Claims Guideline CLAIMS GUIDELINE Table of Contents 1 INTRODUCTION... 1 2 PURPOSE OF THE GUIDELINE... 1 3 DEFINITIONS... 2 MARKET CONDUCT 4 GENERAL REQUIREMENTS... 3 5 CLAIMS NOTIFICATION...

CHAPTER 12 REGULATION GOVERNING REPLACEMENT OF LIFE INSURANCE POLICIES AND ANNUITIES

CHAPTER 12 REGULATION GOVERNING REPLACEMENT OF LIFE INSURANCE POLICIES AND ANNUITIES Section 1. Authority These rules and regulations governing the replacement of life insurance policies and annuities

CHAPTER 12 REGULATION GOVERNING REPLACEMENT OF LIFE INSURANCE POLICIES AND ANNUITIES Section 1. Authority These rules and regulations governing the replacement of life insurance policies and annuities

Chapter 21 - UNFAIR TRADE PRACTICE COMPLAINT REGISTER

Title 210 - NEBRASKA DEPARTMENT OF INSURANCE Chapter 21 - UNFAIR TRADE PRACTICE COMPLAINT REGISTER 001. Authority. This Regulation is promulgated pursuant to the authority granted by Neb.Rev.Stat. 44-1525

Title 210 - NEBRASKA DEPARTMENT OF INSURANCE Chapter 21 - UNFAIR TRADE PRACTICE COMPLAINT REGISTER 001. Authority. This Regulation is promulgated pursuant to the authority granted by Neb.Rev.Stat. 44-1525

LICENSING PROCEDURES FOR MANAGING GENERAL AGENTS TO OBTAIN AUTHORITY IN VIRGINIA

LICENSING PROCEDURES FOR MANAGING GENERAL AGENTS TO OBTAIN AUTHORITY IN VIRGINIA October 2005 GENERAL INFORMATION The 1992 Virginia General Assembly passed legislation requiring the licensing of managing

LICENSING PROCEDURES FOR MANAGING GENERAL AGENTS TO OBTAIN AUTHORITY IN VIRGINIA October 2005 GENERAL INFORMATION The 1992 Virginia General Assembly passed legislation requiring the licensing of managing

RULE 97 LIFE INSURANCE AND ANNUITIES REPLACEMENT

Table of Contents RULE 97 LIFE INSURANCE AND ANNUITIES REPLACEMENT Section 1. Purpose and Scope Section 2. Authority Section 3. Definitions Section 4. Duties of Producers Section 5. Duties of Insurers

Table of Contents RULE 97 LIFE INSURANCE AND ANNUITIES REPLACEMENT Section 1. Purpose and Scope Section 2. Authority Section 3. Definitions Section 4. Duties of Producers Section 5. Duties of Insurers

LAUREATE ANTI-CORRUPTION POLICY

LAUREATE ANTI-CORRUPTION POLICY Laureate Anti-Corruption Policy 1.0 PURPOSE AND BACKGROUND This Anti-Corruption Policy establishes basic standards and a framework for the prevention and detection of bribery

LAUREATE ANTI-CORRUPTION POLICY Laureate Anti-Corruption Policy 1.0 PURPOSE AND BACKGROUND This Anti-Corruption Policy establishes basic standards and a framework for the prevention and detection of bribery

MFDA POLICY NO. 2 MINIMUM STANDARDS FOR ACCOUNT SUPERVISION

13.1.2 MFDA Policy No. 2 Minimum Standards for Account Supervision Introduction MFDA POLICY NO. 2 MINIMUM STANDARDS FOR ACCOUNT SUPERVISION This Policy establishes minimum industry standards for account

13.1.2 MFDA Policy No. 2 Minimum Standards for Account Supervision Introduction MFDA POLICY NO. 2 MINIMUM STANDARDS FOR ACCOUNT SUPERVISION This Policy establishes minimum industry standards for account

DELAWARE DEPARTMENT OF INSURANCE MARKET CONDUCT EXAMINATION REPORT

DELAWARE DEPARTMENT OF INSURANCE MARKET CONDUCT EXAMINATION REPORT NAIC #63312 301 East Fourth Street Cincinnati, OH 45202 As of June 30, 2011 Contents EXECUTIVE SUMMARY... 2 SCOPE OF EXAMINATION...

DELAWARE DEPARTMENT OF INSURANCE MARKET CONDUCT EXAMINATION REPORT NAIC #63312 301 East Fourth Street Cincinnati, OH 45202 As of June 30, 2011 Contents EXECUTIVE SUMMARY... 2 SCOPE OF EXAMINATION...

Procedure Update Suitability of Annuity Transactions (NE L.B. 887)

") Procedure Update Suitability of Annuity Transactions (NE L.B. 887) Effective Date: The rules stated in this Update apply to solicitations occurring on and after January 1, 2013. The company must establish

Procedure Update Suitability of Annuity Transactions (NE L.B. 887) Effective Date: The rules stated in this Update apply to solicitations occurring on and after January 1, 2013. The company must establish

State of Rhode Island and Providence Plantations DEPARTMENT OF BUSINESS REGULATION Division of Insurance 1511 Pontiac Avenue Cranston, RI 02920

Table of Contents State of Rhode Island and Providence Plantations DEPARTMENT OF BUSINESS REGULATION Division of Insurance 1511 Pontiac Avenue Cranston, RI 02920 INSURANCE REGULATION 29 LIFE INSURANCE

Table of Contents State of Rhode Island and Providence Plantations DEPARTMENT OF BUSINESS REGULATION Division of Insurance 1511 Pontiac Avenue Cranston, RI 02920 INSURANCE REGULATION 29 LIFE INSURANCE

TARGETED MARKET CONDUCT EXAMINATION OF

A TARGETED MARKET CONDUCT EXAMINATION OF JACKSON NATIONAL LIFE INSURANCE COMPANY NAIC #65056 As Of December 31, 2009 John R. Kasich, Governor Mary Taylor, Lt. Governor/Director 50 West Town Street Third

A TARGETED MARKET CONDUCT EXAMINATION OF JACKSON NATIONAL LIFE INSURANCE COMPANY NAIC #65056 As Of December 31, 2009 John R. Kasich, Governor Mary Taylor, Lt. Governor/Director 50 West Town Street Third

Managing General Agents (MGAs) Guideline

Guideline") Managing General Agents (MGAs) Guideline JUNE 2013 DRAFT FOR COMMENT BC AUTHORIZED LIFE INSURERS www.fic.gov.bc.ca PURPOSE This draft guideline outlines best practices that the Financial Institutions Commission

Managing General Agents (MGAs) Guideline JUNE 2013 DRAFT FOR COMMENT BC AUTHORIZED LIFE INSURERS www.fic.gov.bc.ca PURPOSE This draft guideline outlines best practices that the Financial Institutions Commission

GRIEVANCE REDRESSAL PROCESS

GRIEVANCE REDRESSAL PROCESS PREFFACE Complaints are an opportunity for an organization to understand or identify gaps in any process, product or communication, work towards process improvements as well

GRIEVANCE REDRESSAL PROCESS PREFFACE Complaints are an opportunity for an organization to understand or identify gaps in any process, product or communication, work towards process improvements as well

STATE OF OREGON DEPARTMENT OF CONSUMER AND BUSINESS SERVICES INSURANCE DIVISION

0 1 STATE OF OREGON DEPARTMENT OF CONSUMER AND BUSINESS SERVICES INSURANCE DIVISION In the Matter of Bankers Life and ) STIPULATION and Casualty Company ) FINAL ORDER ) Case No. INS 0--00 STIPULATION The

0 1 STATE OF OREGON DEPARTMENT OF CONSUMER AND BUSINESS SERVICES INSURANCE DIVISION In the Matter of Bankers Life and ) STIPULATION and Casualty Company ) FINAL ORDER ) Case No. INS 0--00 STIPULATION The

Chapter 91. Regulation 68 Patient Rights under Health Insurance Coverage in Louisiana

D. A copy of the certification form shall be maintained by the insurer and by the producing agent or broker in the policyholder's record for a period of five years from the date of issuance of the insurance

D. A copy of the certification form shall be maintained by the insurer and by the producing agent or broker in the policyholder's record for a period of five years from the date of issuance of the insurance

NEW YORK STATE INSURANCE DEPARTMENT REGULATION NO. 60 11 NYCRR 51 REPLACEMENT OF LIFE INSURANCE POLICIES AND ANNUITY CONTRACTS

NEW YORK STATE INSURANCE DEPARTMENT REGULATION NO. 60 11 NYCRR 51 REPLACEMENT OF LIFE INSURANCE POLICIES AND ANNUITY CONTRACTS I, Neil D. Levin, Superintendent of Insurance of the State of New York, pursuant

NEW YORK STATE INSURANCE DEPARTMENT REGULATION NO. 60 11 NYCRR 51 REPLACEMENT OF LIFE INSURANCE POLICIES AND ANNUITY CONTRACTS I, Neil D. Levin, Superintendent of Insurance of the State of New York, pursuant

represent to both. It does is primarily this Policy Members supervisory Page 1 of 15

September 12, 2013 MFDA POLICY NO. 2 MINIMUM STANDARDS FOR ACCOUNT SUPERVISION Introduction This Policy establishes minimumm industry standards for account supervision. These standards represent the minimum

September 12, 2013 MFDA POLICY NO. 2 MINIMUM STANDARDS FOR ACCOUNT SUPERVISION Introduction This Policy establishes minimumm industry standards for account supervision. These standards represent the minimum

STATE OF FLORIDA OFFICE OF FINANCIAL REGULATION

STATE OF FLORIDA OFFICE OF FINANCIAL REGULATION Registration of Crowdfunding Intermediary Application (Form FL-INT) Pursuant to Section 517.12, Florida Statutes GENERAL INSTRUCTIONS An intermediary of

STATE OF FLORIDA OFFICE OF FINANCIAL REGULATION Registration of Crowdfunding Intermediary Application (Form FL-INT) Pursuant to Section 517.12, Florida Statutes GENERAL INSTRUCTIONS An intermediary of

DIVISION OF SECURITIES INVESTMENT ADVISOR SELF-INSPECTION CHECKLIST

DIVISION OF SECURITIES INVESTMENT ADVISOR SELF-INSPECTION CHECKLIST July 2013 0 Investment Advisor Self-Inspection Checklist Registration Is the investment advisor properly registered in the IARD System?

DIVISION OF SECURITIES INVESTMENT ADVISOR SELF-INSPECTION CHECKLIST July 2013 0 Investment Advisor Self-Inspection Checklist Registration Is the investment advisor properly registered in the IARD System?

LIFE SETTLEMENT PROVIDER BEST PRACTICES

LIFE SETTLEMENT PROVIDER BEST PRACTICES The standardization of life settlement origination practices is critical to promote the growth of life settlements as an asset class. Standardized origination practices

LIFE SETTLEMENT PROVIDER BEST PRACTICES The standardization of life settlement origination practices is critical to promote the growth of life settlements as an asset class. Standardized origination practices

NO. 17-11 DATE: June 27, 2011

NO. 17-11 DATE: June 27, 2011 TO: FROM: SUBJECT: All Producers Licensed in New Jersey James P. Payne, Compliance Officer Suitability in Annuity Transactions The purpose of this Compliance Bulletin is to

NO. 17-11 DATE: June 27, 2011 TO: FROM: SUBJECT: All Producers Licensed in New Jersey James P. Payne, Compliance Officer Suitability in Annuity Transactions The purpose of this Compliance Bulletin is to

STATE OF NEW YORK INSURANCE DEPARTMENT REPORT ON EXAMINATION OF THE PRUCO LIFE INSURANCE COMPANY OF NEW JERSEY AS OF DECEMBER 31, 2001

STATE OF NEW YORK INSURANCE DEPARTMENT REPORT ON EXAMINATION OF THE PRUCO LIFE INSURANCE COMPANY OF NEW JERSEY AS OF DECEMBER 31, 2001 DATE OF REPORT: JANUARY 15, 2003 EXAMINER: WILLIAM M. TARDOGNO TABLE

STATE OF NEW YORK INSURANCE DEPARTMENT REPORT ON EXAMINATION OF THE PRUCO LIFE INSURANCE COMPANY OF NEW JERSEY AS OF DECEMBER 31, 2001 DATE OF REPORT: JANUARY 15, 2003 EXAMINER: WILLIAM M. TARDOGNO TABLE

Broker-Dealer and Investment Adviser Compliance Programs

Lori A. Richards Principal, PricewaterhouseCoopers Financial Services Regulatory Practice Broker-Dealer and Investment Adviser Compliance Programs Regulatory Requirements, Common Minimum Elements, Other

Lori A. Richards Principal, PricewaterhouseCoopers Financial Services Regulatory Practice Broker-Dealer and Investment Adviser Compliance Programs Regulatory Requirements, Common Minimum Elements, Other

LIVINGSTON COUNTY CREDIT CARD PROCEDURES

LIVINGSTON COUNTY CREDIT CARD PROCEDURES INTRODUCTION Livingston County is introducing an alternative approach to purchasing products and services through the use of credit cards. A credit card purchase

LIVINGSTON COUNTY CREDIT CARD PROCEDURES INTRODUCTION Livingston County is introducing an alternative approach to purchasing products and services through the use of credit cards. A credit card purchase

ALTERNATIVE ELECTRIC SUPPLIER APPLICATION FOR THE MICHIGAN PUBLIC SERVICE COMMISSION RETAIL ACCESS PARTICIPATION AGREEMENT

ALTERNATIVE ELECTRIC SUPPLIER APPLICATION FOR THE MICHIGAN PUBLIC SERVICE COMMISSION RETAIL ACCESS PARTICIPATION AGREEMENT Michigan law, PA 286 of 2008, Section 10a(1)(a), provides that the Michigan Public

ALTERNATIVE ELECTRIC SUPPLIER APPLICATION FOR THE MICHIGAN PUBLIC SERVICE COMMISSION RETAIL ACCESS PARTICIPATION AGREEMENT Michigan law, PA 286 of 2008, Section 10a(1)(a), provides that the Michigan Public

211 CMR: DIVISION OF INSURANCE 211 CMR 142.00: INSURANCE SALES BY BANKS AND CREDIT UNIONS

211 CMR 142.00: INSURANCE SALES BY BANKS AND CREDIT UNIONS Section 142.01: Scope and Purpose 142.02: Applicability 142.03: Definitions 142.04: Licensing 142.05: Consumer Protection Terms and Conditions

211 CMR 142.00: INSURANCE SALES BY BANKS AND CREDIT UNIONS Section 142.01: Scope and Purpose 142.02: Applicability 142.03: Definitions 142.04: Licensing 142.05: Consumer Protection Terms and Conditions

Proposed New Rules: N.J.A.C. 11:4-34.29 and 34.30, and 11:4-34 Appendices J and K. Steven M. Goldman, Commissioner, Department of Banking and

INSURANCE DEPARTMENT OF BANKING AND INSURANCE OFFICE OF LIFE AND HEALTH Long-Term Care Insurance Training Requirements; Partnership Policies General Requirements Proposed New Rules: N.J.A.C. 11:4-34.29

INSURANCE DEPARTMENT OF BANKING AND INSURANCE OFFICE OF LIFE AND HEALTH Long-Term Care Insurance Training Requirements; Partnership Policies General Requirements Proposed New Rules: N.J.A.C. 11:4-34.29

IAC 11/18/09 Insurance[191] Ch 58, p.1 CHAPTER 58 THIRD-PARTY ADMINISTRATORS

![IAC 11/18/09 Insurance[191] Ch 58, p.1 CHAPTER 58 THIRD-PARTY ADMINISTRATORS](/thumbs/32/15644477.jpg "IAC 11/18/09 Insurance[191] Ch 58, p.1 CHAPTER 58 THIRD-PARTY ADMINISTRATORS") IAC 11/18/09 Insurance[191] Ch 58, p.1 CHAPTER 58 THIRD-PARTY ADMINISTRATORS 191 58.1(510) Purpose. The purpose of this chapter is to administer the provisions of Iowa Code chapter 510 relating to the

IAC 11/18/09 Insurance[191] Ch 58, p.1 CHAPTER 58 THIRD-PARTY ADMINISTRATORS 191 58.1(510) Purpose. The purpose of this chapter is to administer the provisions of Iowa Code chapter 510 relating to the

NEBRASKA DEPARTMENT OF INSURANCE P.O. BOX 82089 LINCOLN, NE 68501-2089. Requirements For Transacting Business as a Managing General Agent

NEBRASKA DEPARTMENT OF INSURANCE P.O. BOX 82089 LINCOLN, NE 68501-2089 Requirements For Transacting Business as a Managing General Agent Article 49 Managing General Agents Section 44-4901 Act, how cited.

NEBRASKA DEPARTMENT OF INSURANCE P.O. BOX 82089 LINCOLN, NE 68501-2089 Requirements For Transacting Business as a Managing General Agent Article 49 Managing General Agents Section 44-4901 Act, how cited.

Franklin County Treasurer Broker/Dealer Request for Information

Franklin County Treasurer Broker/Dealer Request for Information Section I: Statement of Position and General Requirements The Treasurer of Franklin County, Ohio (hereinafter referred to as the Treasurer

Franklin County Treasurer Broker/Dealer Request for Information Section I: Statement of Position and General Requirements The Treasurer of Franklin County, Ohio (hereinafter referred to as the Treasurer

American National Insurance Company. Annuity Suitability. AMERICAN NATIONAL INSURANCE COMPANY One Moody Plaza, Galveston, Texas 77550-7999

American National Insurance Company Annuity Suitability STANDARD & Guidelines AMERICAN NATIONAL INSURANCE COMPANY One Moody Plaza, Galveston, Texas 77550-7999 American National Insurance Company Annuity

American National Insurance Company Annuity Suitability STANDARD & Guidelines AMERICAN NATIONAL INSURANCE COMPANY One Moody Plaza, Galveston, Texas 77550-7999 American National Insurance Company Annuity

MFDA Bulletin. Policy. For Distribution to Relevant Parties within your Firm

Contact: Paige Ward General Counsel & Vice-President, Policy Phone: 416-943-5838 E-mail: pward@mfda.ca MFDA Bulletin Policy BULLETIN #0560 P February 22, 2013 For Distribution to Relevant Parties within

Contact: Paige Ward General Counsel & Vice-President, Policy Phone: 416-943-5838 E-mail: pward@mfda.ca MFDA Bulletin Policy BULLETIN #0560 P February 22, 2013 For Distribution to Relevant Parties within

STATE OF MISSOURI DEPARTMENT OF INSURANCE, FINANCIAL INSTITUTIONS AND PROFESSIONAL REGISTRATION

STATE OF MISSOURI DEPARTMENT OF INSURANCE, FINANCIAL INSTITUTIONS AND PROFESSIONAL REGISTRATION FINAL MARKET CONDUCT EXAMINATION REPORT Of the Property and Casualty Business of Direct General Insurance

STATE OF MISSOURI DEPARTMENT OF INSURANCE, FINANCIAL INSTITUTIONS AND PROFESSIONAL REGISTRATION FINAL MARKET CONDUCT EXAMINATION REPORT Of the Property and Casualty Business of Direct General Insurance

DELAWARE DEPARTMENT OF INSURANCE MARKET CONDUCT EXAMINATION REPORT

DELAWARE DEPARTMENT OF INSURANCE MARKET CONDUCT EXAMINATION REPORT NAIC # 66281 4333 Edgewood Road NE Cedar Rapids, IA 52499 As of December 31, 2010 Table of Contents EXECUTIVE SUMMARY... 2 SCOPE OF

DELAWARE DEPARTMENT OF INSURANCE MARKET CONDUCT EXAMINATION REPORT NAIC # 66281 4333 Edgewood Road NE Cedar Rapids, IA 52499 As of December 31, 2010 Table of Contents EXECUTIVE SUMMARY... 2 SCOPE OF

Reinsurance Intermediary Broker Reinsurance Intermediary Manager Licensing Instructions

STATE OF WEST VIRGINIA Offices of the Insurance Commissioner Financial Conditions Division Mailing Address: Financial Conditions PO Box 50540 Charleston WV 25305-0540 Telephone: (304) 558-2100 Facsimile:

STATE OF WEST VIRGINIA Offices of the Insurance Commissioner Financial Conditions Division Mailing Address: Financial Conditions PO Box 50540 Charleston WV 25305-0540 Telephone: (304) 558-2100 Facsimile:

TARGETED MARKET CONDUCT EXAMINATION OF

A TARGETED MARKET CONDUCT EXAMINATION OF LIFE INSURANCE COMPANY OF THE SOUTHWEST NAIC #65528 As Of December 31, 2009 John R. Kasich, Governor Mary Taylor, Lt. Governor/Director 50 West Town Street Third

A TARGETED MARKET CONDUCT EXAMINATION OF LIFE INSURANCE COMPANY OF THE SOUTHWEST NAIC #65528 As Of December 31, 2009 John R. Kasich, Governor Mary Taylor, Lt. Governor/Director 50 West Town Street Third

PRIVATE HEALTH INSURANCE INTERMEDIARIES. DOCUMENT 1: Self-Audit Guide for All Members of PHIIA JUNE 2015 VERSION 2

PRIVATE HEALTH INSURANCE INTERMEDIARIES DOCUMENT 1: Self-Audit Guide for All Members of PHIIA JUNE 2015 VERSION 2 9 For All Members of PHIIA Code Compliance Committee Private Health Insurance Intermediaries

PRIVATE HEALTH INSURANCE INTERMEDIARIES DOCUMENT 1: Self-Audit Guide for All Members of PHIIA JUNE 2015 VERSION 2 9 For All Members of PHIIA Code Compliance Committee Private Health Insurance Intermediaries

CLAIMS HANDLING GUIDELINES. for CTP Insurers

CLAIMS HANDLING GUIDELINES for CTP Insurers Initially issued 2000 Reissued: 1 July 2004; 18 September 2006; 1 July 2008; 1 October 2008, 1 May 2014 INTRODUCTION The MAA Claims Handling Guidelines (the

CLAIMS HANDLING GUIDELINES for CTP Insurers Initially issued 2000 Reissued: 1 July 2004; 18 September 2006; 1 July 2008; 1 October 2008, 1 May 2014 INTRODUCTION The MAA Claims Handling Guidelines (the

THE CLAIMS MANAGEMENT CODE ( the Code )

") THE CLAIMS MANAGEMENT CODE ( the Code ) CONTENTS 1 Introduction 2 Principles 3 Publishing the Code 4 Training and Competence 5 Advertising, Marketing and Promotional Activities 6 Charges 7 Information

THE CLAIMS MANAGEMENT CODE ( the Code ) CONTENTS 1 Introduction 2 Principles 3 Publishing the Code 4 Training and Competence 5 Advertising, Marketing and Promotional Activities 6 Charges 7 Information

STATE OF MAINE DEPARTMENT OF PROFESSIONAL AND FINANCIAL REGULATION BUREAU OF INSURANCE ) )

)") STATE OF MAINE DEPARTMENT OF PROFESSIONAL AND FINANCIAL REGULATION BUREAU OF INSURANCE IN RE: BANKERS LIFE AND CASUALTY COMPANY and GARY R. SMITH DOCKET NO. INS-04-228 IN RE: BANKERS LIFE AND CASUALTY

STATE OF MAINE DEPARTMENT OF PROFESSIONAL AND FINANCIAL REGULATION BUREAU OF INSURANCE IN RE: BANKERS LIFE AND CASUALTY COMPANY and GARY R. SMITH DOCKET NO. INS-04-228 IN RE: BANKERS LIFE AND CASUALTY

Public Act No. 15-162

Public Act No. 15-162 AN ACT CONCERNING A STUDENT LOAN BILL OF RIGHTS. Be it enacted by the Senate and House of Representatives in General Assembly convened: Section 1. (NEW) (Effective October 1, 2015)

Public Act No. 15-162 AN ACT CONCERNING A STUDENT LOAN BILL OF RIGHTS. Be it enacted by the Senate and House of Representatives in General Assembly convened: Section 1. (NEW) (Effective October 1, 2015)

OFFICE OF FINANCIAL REGULATION COLLECTION AGENCY REGISTRATIONS MORTGAGE-RELATED AND CONSUMER COLLECTION AGENCY COMPLAINTS PRIOR AUDIT FOLLOW-UP

REPORT NO. 2013-031 OCTOBER 2012 OFFICE OF FINANCIAL REGULATION COLLECTION AGENCY REGISTRATIONS MORTGAGE-RELATED AND CONSUMER COLLECTION AGENCY COMPLAINTS PRIOR AUDIT FOLLOW-UP Operational Audit COMMISSIONER

REPORT NO. 2013-031 OCTOBER 2012 OFFICE OF FINANCIAL REGULATION COLLECTION AGENCY REGISTRATIONS MORTGAGE-RELATED AND CONSUMER COLLECTION AGENCY COMPLAINTS PRIOR AUDIT FOLLOW-UP Operational Audit COMMISSIONER

211 CMR: DIVISION OF INSURANCE

211 CMR 34.00: THE REPLACEMENT OF LIFE INSURANCE AND ANNUITIES Section 34.01: Purpose 34.02: Definitions 34.03: Exemptions 34.04: Duties of Agents and Brokers 34.05: Duties of All Insurers 34.06: Duties

211 CMR 34.00: THE REPLACEMENT OF LIFE INSURANCE AND ANNUITIES Section 34.01: Purpose 34.02: Definitions 34.03: Exemptions 34.04: Duties of Agents and Brokers 34.05: Duties of All Insurers 34.06: Duties

Title 24-A: MAINE INSURANCE CODE

Title 24-A: MAINE INSURANCE CODE Chapter 72-A: MAINE LIABILITY RISK RETENTION ACT HEADING: PL 1987, c. 769, Pt. A, 100 (rpr) Table of Contents Section 6091. SHORT TITLE... 3 Section 6092. PURPOSE... 3

Title 24-A: MAINE INSURANCE CODE Chapter 72-A: MAINE LIABILITY RISK RETENTION ACT HEADING: PL 1987, c. 769, Pt. A, 100 (rpr) Table of Contents Section 6091. SHORT TITLE... 3 Section 6092. PURPOSE... 3

NEBRASKA MORTGAGE BANKER FREQUENTLY ASKED QUESTIONS

NEBRASKA MORTGAGE BANKER FREQUENTLY ASKED QUESTIONS Loan Originator Licensing Q. What are the requirements to obtain a mortgage loan originator license in Nebraska? A. In accordance with the requirements

NEBRASKA MORTGAGE BANKER FREQUENTLY ASKED QUESTIONS Loan Originator Licensing Q. What are the requirements to obtain a mortgage loan originator license in Nebraska? A. In accordance with the requirements

JAZZ PHARMACEUTICALS PLC CHARTER OF THE AUDIT COMMITTEE OF THE BOARD OF DIRECTORS

JAZZ PHARMACEUTICALS PLC CHARTER OF THE AUDIT COMMITTEE OF THE BOARD OF DIRECTORS PURPOSE AND POLICY The purpose of the Audit Committee (the Committee ) shall be to act on behalf of the Board of Directors

JAZZ PHARMACEUTICALS PLC CHARTER OF THE AUDIT COMMITTEE OF THE BOARD OF DIRECTORS PURPOSE AND POLICY The purpose of the Audit Committee (the Committee ) shall be to act on behalf of the Board of Directors

004. Scope. This rule shall apply to all title insurers authorized to do business in Nebraska and all title insurance agents licensed in Nebraska.

Title 210 - NEBRASKA DEPARTMENT OF INSURANCE Chapter 34 - TITLE INSURANCE 001. Authority. This rule is adopted and promulgated by the Director of Insurance of the State of Nebraska pursuant to the Title

Title 210 - NEBRASKA DEPARTMENT OF INSURANCE Chapter 34 - TITLE INSURANCE 001. Authority. This rule is adopted and promulgated by the Director of Insurance of the State of Nebraska pursuant to the Title

WEST VIRGINIA OFFICES OF THE INSURANCE COMMISSIONER Medical Malpractice Insurance Review Standards Checklist

Medical Malpractice REVIEW REQUIREMENTS REFERENCE COMMENTS FORMS Applications REFERENCE COMMENTS Fee, filing 33-6-34 The Filing Fee is $50.00 per Form filing and applies on a per company basis. WVIL All

Medical Malpractice REVIEW REQUIREMENTS REFERENCE COMMENTS FORMS Applications REFERENCE COMMENTS Fee, filing 33-6-34 The Filing Fee is $50.00 per Form filing and applies on a per company basis. WVIL All

Key Rules for General Insurance Brokers

Key Rules for General Insurance Brokers Contents 1. Introduction 3 2. Principles for businesses 6 3. Conduct of business rules 7 Financial promotion 7 Initial disclosure 9 Arranging and suitable advice

Key Rules for General Insurance Brokers Contents 1. Introduction 3 2. Principles for businesses 6 3. Conduct of business rules 7 Financial promotion 7 Initial disclosure 9 Arranging and suitable advice

STATE OF NEW YORK INSURANCE DEPARTMENT MARKET CONDUCT REPORT ON EXAMINATION OF THE RIVERSOURCE LIFE INSURANCE CO. OF NEW YORK

STATE OF NEW YORK INSURANCE DEPARTMENT MARKET CONDUCT REPORT ON EXAMINATION OF THE RIVERSOURCE LIFE INSURANCE CO. OF NEW YORK CONDITION: DECEMBER 31, 2006 DATE OF REPORT: OCTOBER 12, 2007 STATE OF NEW

STATE OF NEW YORK INSURANCE DEPARTMENT MARKET CONDUCT REPORT ON EXAMINATION OF THE RIVERSOURCE LIFE INSURANCE CO. OF NEW YORK CONDITION: DECEMBER 31, 2006 DATE OF REPORT: OCTOBER 12, 2007 STATE OF NEW

THE COMMONWEALTH OF MASSACHUSETTS. Division of Insurance. Boston Mutual Life Insurance Company

THE COMMONWEALTH OF MASSACHUSETTS OFFICE OF CONSUMER AFFAIRS AND BUSINESS REGULATION Division of Insurance Report on the Limited Scope Multi-State Market Conduct Examination of Boston Mutual Life Insurance

THE COMMONWEALTH OF MASSACHUSETTS OFFICE OF CONSUMER AFFAIRS AND BUSINESS REGULATION Division of Insurance Report on the Limited Scope Multi-State Market Conduct Examination of Boston Mutual Life Insurance

MARKET CONDUCT EXAMINATION

MARKET CONDUCT EXAMINATION A COLLABORATIVE EXAMINATION CONDUCTED BY WASHINGTON, IDAHO, AND ARIZONA OF: WESTERN UNITED LIFE ASSURANCE COMPANY OLD STANDARD LIFE INSURANCE COMPANY OLD WEST LIFE & ANNUITY

MARKET CONDUCT EXAMINATION A COLLABORATIVE EXAMINATION CONDUCTED BY WASHINGTON, IDAHO, AND ARIZONA OF: WESTERN UNITED LIFE ASSURANCE COMPANY OLD STANDARD LIFE INSURANCE COMPANY OLD WEST LIFE & ANNUITY