REPORT OF MARKET CONDUCT EXAMINATION CENTRAL RESERVE LIFE INSURANCE CO ROYALTON RD STRONGSVILLE, OH AS OF MARCH 31,2003

|

|

|

- Nathaniel Tyler

- 8 years ago

- Views:

Transcription

1 REPORT OF MARKET CONDUCT EXAMINATION CENTRAL RESERVE LIFE INSURANCE CO ROYALTON RD STRONGSVILLE, OH AS OF MARCH 31,2003 BY KANSAS INSURANCE DEPARTMENT 1

2 TABLE OF CONTENTS SUBJECT PAGE NO. SALUTATION 3 EXECUTIVE SUMMARY 4 SCOPE OF REVIEW 5 SUMMARY OF REVIEW 5 DESK EXAMINATION/ON SITE EXAMINATION 6 COMPANY OVERVIEW 6 COMPLAINT HANDLING 7 CLAIM HANDLING 12 GENERAL COMMENTS 15 CONCLUSION 16 TABLE I TABLE 2 APPENDIX I 2

3 Honorable Sandy Praeger January 9, 2004 Insurance Commissioner Kansas Insurance Department 420 SW Ninth Street Topeka, KS Dear Commissioner Praeger: In accordance with your respective authorization, and pursuant to K.S.A , a market conduct examination has been conducted on the business affairs of: Central Reserve Life Insurance Co Royalton Rd Strongsville, OH hereafter referred to as CRL or the Company, and the following report as such examination is respectfully submitted, Lyle Behrens, CPCU, CIE, ARM Market Conduct Supervisor Examiner in Charge 3

4 EXECUTIVE SUMMARY The Kansas Insurance Department performed a market conduct examination of the Central Reserve Life Insurance Co. (CRL). The examiners reviewed the company underwriting, claims, and rating manuals. The exam team reviewed claim, and complaint files in company s Administrative office in Strongsville, OH. A series of meetings were held with the CRL staff that focused on their current operations. To supplement and verify the understanding of how the company does business, a series of samples were selected for review to verify their procedures and practices in complaint and claim handling. The company passed most tests; and in terms of delivering good service to its insured customers, the examiners were impressed with the overall positive and very professional performance by the CRL staff and management to their policyholders. The exam team has made recommendations on several issues. LIST OF RECOMMENDATIONS Complaint Handling 1. While the response times were within KID s tolerances, the exam team feels that the company should review their complaint handling procedures so everyone is aware of the response times required for the different levels of complaints. General 1. The new business rejection letter listed the former third party administrator as the contact for anyone interested in obtaining health insurance through the Kansas Health Insurance Assoc. When advised of this error, the company corrected the form per K.S.A (f). Claims 1. CRL needs to review their claim procedures to insure that claims are being processed in a timely fashion per K.S.A (a)(1) and (a)(2). 2. CRL needs to review their claim procedures to insure that claims that are not processed with in the time lines specified in the Prompt Pay Act, K.S.A , have interest paid according to K.S.A (b). 4

5 SCOPE OF REVIEW A targeted market conduct examination of CRL s, claims and complaints was completed to determine compliance with applicable statutes, regulations and bulletins of the state of Kansas. The examination was conducted according to the guidelines and procedures recommended in the NAIC Market Conduct Examiners Handbook. The examination included, but was not limited to the following: COMPANY OVERVIEW Certificates of Authority COMPLAINT HANDLING Record Keeping Timely Response CLAIMS Claim Processing Use of Outside Pricing Entities Timeliness and Accuracy of Claim Payment Proper Maintenance of Claim Files SUMMARY OF REVIEW The market conduct examination focused on CRL. The testing and file review consisted of sampling from the Company s complaints and settled claim files in Strongsville, Oh. The examination included a review of the Company s complaints and settled claim files from January 1, 2001 to March 31, General topics were covered in Interrogatories submitted to the Companies for their written response. Subjects covered were Complaints, and Claims. The response received adequately addressed the issues presented. 5

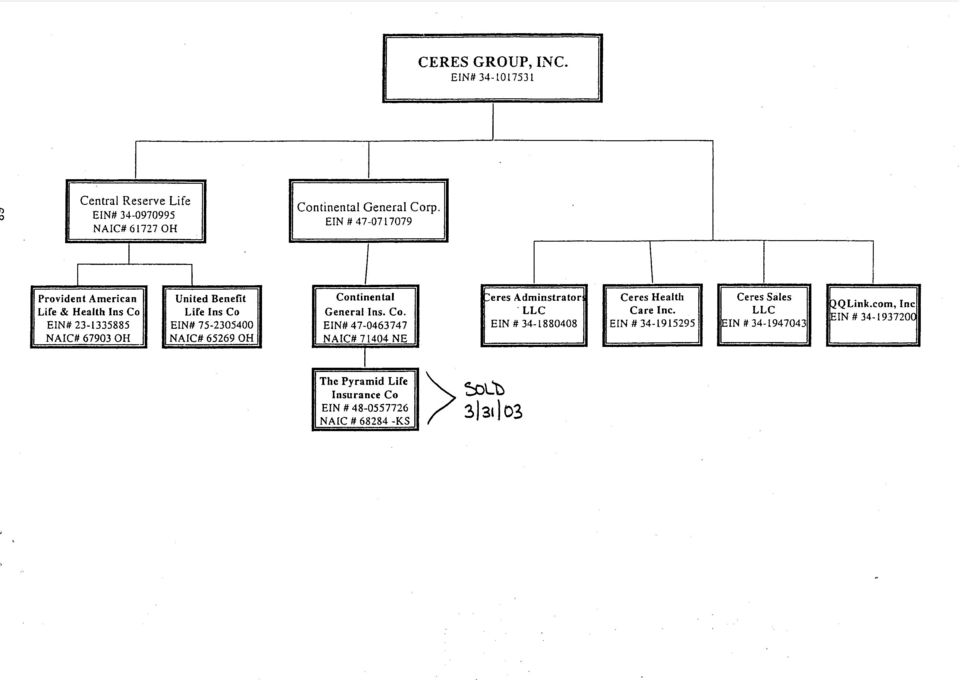

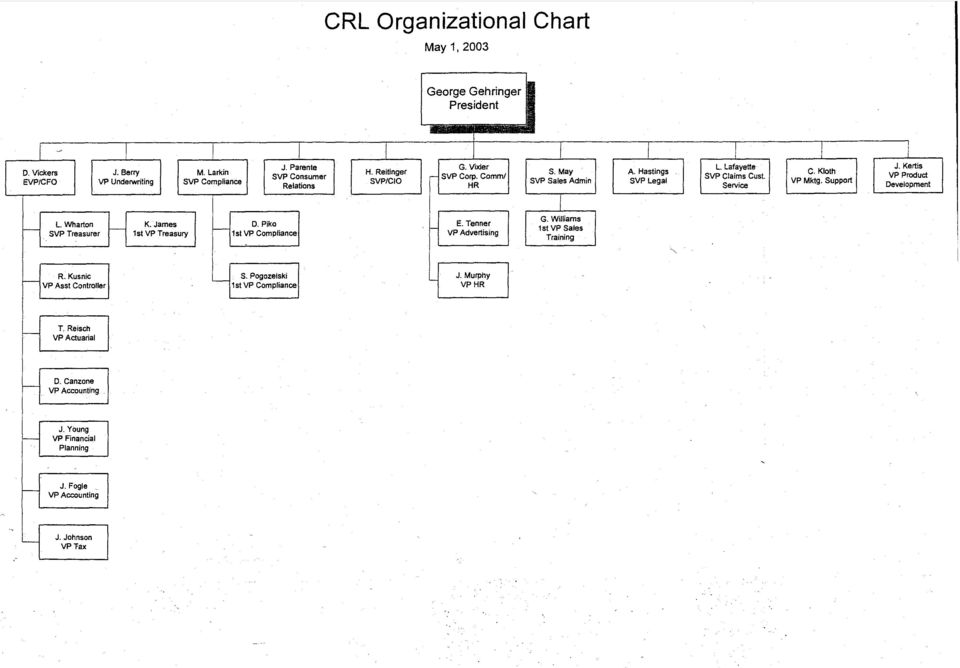

6 COMPANY OVERVIEW History & Organization DESK EXAMINATION/ON-SITE EXAMINATION CRL was originally incorporated in 1963 under the name American Central Reserve Life Insurance Company. In 1967 the name was changed to Central Reserve Life of North America Insurance Company. In 1967 the company was reorganized as Central Reserve Life Insurance Corporation (CRLC), with CRL as its principal operating subsidiary. In December of 1998 CRLC changed its name to Ceres Group, Inc. (Ceres). Ceres is a public company that has traded on NASDAQ since CRL is an Ohio domiciled corporation that is authorized to transact business in 35 states. CRL offers small group, large group, association group and individual major medical insurance. Association group business is issued through Eagle Consumer Association, the situs of which is Illinois. Employer group business is issued through the International Professional Trust, this situs of which is Ohio. CRL's products are marketed through a network of Managing General Agents and General Agents who work with more than 14,000 independent insurance agents. Table 1 shows the organization of the Ceres group and its subsidiary Companies. Table 2 shows the organization of the different departments within CRL Tests for Company Operations/Management Standard 7 Records are adequate, accessible, consistent and orderly and comply with state record retention requirements. K.S.A (a), (b), (c) and (g). The company provided the exam team with the necessary records and documents in a timely fashion. Standard 8 The company is licensed for the lines of business that are being written. K.S.A The Certificate of Authority was reviewed and found to be in order, and the company was complying with it. Standard 9 The company cooperates on a timely basis with examiners performing the examinations. K.S.A (c) and (g). 6

. Ceres is a public company that has traded on NASDAQ since 1980. CRL is an Ohio domiciled corporation that is authorized to transact business in 35 states.")

7 The company was very cooperative and provided the exam team with the items requested within the time frames established for this exam. COMPLAINTS Company Complaint/Grievance Procedures CRL s complaint/grievance procedures are explained in their Kansas Appeal Procedure Coverage Rider which is described below: Regular Appeal 1 st Level Appeal Process 2 nd Level Appeal Process Utilization Review (UR) Appear Adverse decision If expedited follow 1 st Level Appeal Process If Standard Follow 2 nd Level Appeal Process External Review ADVERSE DECISION APPEAL PROCESS Levels of Review The Insured Person may ask CRL to review its decisions involving his requests for service or request to have his claims paid within sixty (60) days of CRL's response to the Insured Person. In general, the following three levels of review will be available to the Insured Person: Level 1 - Expedited Appeal Level 2 - Standard Appeal Level 3 - External Review (1) Expedited Appeal (Level 1) (a) Eligibility: i. The Insured Person may request Expedited Appeal only when a denial of Certification is made before or during an ongoing service, and the attending health care provider or other ordering provider believes that the determination warrants immediate Appeal. The attending health care provider or other ordering provider may request Expedited Appeal by telephone [ ] or via facsimile [ ]. 7

")

8 ii. The Insured Person may not request Expedited Appeal of a denied request for a service that has already been provided. Instead, he may start the review process by seeking Standard Appeal. (b) Decision: i. CRL shall review the supporting documentation and provide immediate access to a Peer Clinical Reviewer, including the documentation used in the original determination. After reviewing the supporting documentation, CRL shall notify the Insured Person and the treating or ordering physician immediately by telephone of its decision. Written notification shall be sent within one (1) working day. ii. If the Expedited Appeal does not resolve a difference of opinion, the Insured Person or the provider acting on behalf of the Insured Person may request further review through the Standard Appeal process. (2) Standard Appeal (Level 2) (a) Eligibility: i. The Insured Person may request Standard Appeal as a formal request to reconsider a denial of the Certification of an admission, extension of stay, or other health care service. He may also request Standard Appeal for further review of your Expedited Appeal. The Insured Person may request Standard Appeal either in writing or by telephone to the following: Standard Appeal Central Reserve Life Insurance Company Royalton Road Cleveland, Ohio (b) Decision i. CRL or its authorized Utilization Review Organization shall request copies of part or all of the clinical records or a written statement from the attending health care provider or other ordering provider as deemed necessary in order to review the Appeal. Prior to upholding any denial, the Appeal will be referred to a Peer Clinical Reviewer who was not involved in the original denial for review. ii. In the absence of any contractual agreement, CRL shall notify the Insured Person, attending health care provider or other ordering provider, in writing, of its determination on the Appeal as soon as practical, but in no event later than thirty (30) days, after receiving all required documentation. 8

working day. ii.")

9 iii. If the Standard Appeal does not resolve a difference of opinion, the Insured Person or the provider acting on behalf of the Insured Person may request further review through the External Review process. iv. CRL shall notify the Insured Person, attending health care provider or other ordering provider of their right to file External Review. (3) External Review (Level 3) (a) Eligibility: If dissatisfied with the Standard Appeal, the Insured Person, treating physician, health care provider acting on behalf of the Insured Person (with written authorization), or a legally authorized designee of the Insured Person, may request External Review within ninety (90) days after the date of receipt of notice of the Standard Appeal Adverse Decision. The Insured Person may also request External Review if CRL agrees to waive the Standard Appeal process or if CRL has failed to respond to his Standard Appeal within sixty (60) days (except to the extent that the delay was requested by the Insured Person). In the case of an Emergency Medical Condition, your External Review shall be considered on an expedited basis. Requests for External Review should be sent to: Kansas Department of Insurance Commissioner of Insurance 420 S.W. 9th Street Topeka, Kansas (b) Decision i. The External Review shall be assigned by the Commissioner to an approved External Review Organization to conduct the External Review. ii. The Insured Person is required to provide the Commissioner of Insurance with an Appeal form and a fully executed release for the Commissioner and the External Review Organization authorizing them to obtain any medical records deemed necessary for the determination of benefits. iii. Within seven (7) business days CRL or its authorized Utilization Review Organization shall provide the Commissioner of Insurance with documents and information they wish the External Review Organization to consider in making its decision. The Commissioner will conduct a preliminary review and, if the case qualifies for External Review, it will be assigned to an External Review Organization. In addition to such documents, the External Review Organization shall consider the following documents in making its determination: 9

, or a legally authorized designee of the Insured Person, may request External Review within ninety (90) days after the date of receipt of notice of the Standard Appeal Adverse")

10 [a] The Insured Person's pertinent medical records; [b] The attending health care professional's recommendation; [c] Consulting reports from appropriate health care professionals; [d] The terms of coverage under the insurance plan; [e] The most appropriate practice guidelines, including generally accepted practice guidelines, evidence-based practice guidelines, or any other practice guidelines developed by the federal government and national or professional medical societies, boards, and associations; and [f] Any applicable clinical review criteria developed and used by CRL or its authorized Utilization Review Organization. iv. Within thirty (30) business days of receipt of the request for External Review, the External Review Organization shall provide notice to the Insured Person or their authorized representative, CRL, and the Commissioner of its decision to uphold or reverse the Adverse Decision. Notification shall include: [a] A general description of the reason for the request for External Review; [b] The date the External Review was conducted; [c] The date of the External Review Organization's decision; [d] The rationale for the External Review Organization's decision; and [e] References, as needed, to the evidence or documentation, including the practice guidelines that the External Review Organization considered in reaching its decision. v. In the case of an expedited External Review, the External Review Organization shall within seven (7) business days after the date of receipt of the request for External Review, make a decision to uphold or reverse the Adverse Decision. Notification of the decision shall be sent to the Insured Person, their authorized representative, CRL and the Commissioner. If the initial notification is not in writing, within two (2) days of its decision the External Review Organization shall provide written confirmation of its decision. vi. CRL must provide benefits as determined by the External Review Organization, subject to the terms, limitations, and conditions of the certificate. Tests for Complaint/Grievance Handling 10

![developed by the federal government and national or professional medical societies, boards, and associations; and [f] Any applicable clinical review criteria developed and used by CRL or its](/docs-images/44/12981734/images/page_10.jpg "authorized Utilization Review Organization. iv.")

11 Standard 1 All complaints are recorded in the required format on the company complaint register. K.S.A (10). The complaint register was up to date and complete with the required columns from the Kansas statutes and CRL complaint/grievance procedures. Standard 2 The company has adequate complaint handling procedures in place and communicates such procedures to policyholders. K.A.R (5)(a) & (6). The procedures written into company policy are adequate and provide control of the complaint/grievance timelines by one department and one assigned person. Generally, these procedures work quite well. Standard 3 The company takes adequate steps to finalize and dispose of the complaint in accordance with applicable statutes, rules and regulations, and contract language. K.A.R (6). The company met this standard. See Standard 4. Standard 4 The time frame within which the company responds to complaints is in accordance with applicable statutes, rules and regulations. KAR (6) & (8a&c) Complaints/Grievance Type Sample Errors %Pass DOI complaints % 1 st Level complaints % 2 nd Level complaints % 2002 Complaints/Grievance Type Sample Errors %Pass DOI complaints % 1 st Level complaints % 2 nd Level complaints % Total Complaints Reviewed % 117 complaints were reviewed at CRL s headquarters. Timelines required by Kansas Regulations were met for the most part. One response to the Kansas Insurance Department took 23 working days instead of the required 15 working days. This is in violation of KAR Sec 6. There were 3 complaints where the company exceeded 30 days at 2 nd level of complaint. CRL shall notify the Insured Person, attending health care provider or other ordering provider, in writing, of its determination on the Appeal as soon as practical, but in no 11

12 event later than thirty (30) days, after receiving all required documentation. This is in violation of the company s insurance policy and K.A.R , Sec 7, Sec 8(a) & 8(c). Recommendations: 1. While the response times were within KID s tolerances, the exam team feels that the company should review their complaint handling procedures so everyone is aware of the response times required for the different levels of complaints. CLAIMS Company claim processing procedures: Tests for Claims (See Appendix I for the wording of the appropriate statute or regulation) Standard 1 The initial contact by the company with the claimant is within the required time frame. K.A.R , Sec 6(a) & (d); K.S.A (a)(1), (a)(2) and (b). Type Sample Errors %Pass Un-Paid % Paid % The Company passed Standard 1. Standard 2 Investigations are conducted in a timely manner. K.A.R , Sec. 7 & Sec. 8(c); K.S.A (a)(1), (a)(2) and (b). Type Sample Errors %Pass Un-Paid % Paid % The Company failed Standard 2. For un-paid claims. There were 12 files that were not adjudicated and paid within 30 days per K.A.R , Sec 7 and K.S.A (a). From the sample, 10 cases were from 2001, and 1 was from For paid claims. There were 11 files that were not adjudicated and paid with in 30 days per K.A.R , Sec 7 and K.S.A (a). Out of the sample of errors, 4 claims were from 2002 and the remainders were from prior years. Standard 3 Claims are resolved in a timely manner. K.A.R Sec. 8(a) & 8(c); K.S.A (a)(1), (a)(2) and (b). 12

Standard 1 The initial contact by the company with the claimant")

13 Type Sample Errors %Pass Un-Paid % Paid % The Company failed Standard 3. See the comments under Standard 2. Standard 4 The company responds to claim correspondence in a timely manner. K.A.R , Sec. 6(a) and 6(d); K.S.A (a)(1), (a)(2) and (b). Type Sample Errors %Pass Un-Paid % Paid % The Company failed Standard 4. See the comments under Standard 2. Standard 5 Claim files are adequately documented. K.A.R Sec.4, Sec. 6(a) & Sec. 8(b). Type Sample Errors %Pass Un-Paid % Paid % The Company passed Standard 5. Standard 6 Claims are properly handled in accordance with policy provisions HIPAA and state law. K.A.R , Sec. 5(a), Sec. 8, &K.S.A (a) (1), (a)(2) and (b). Type Sample Errors %Pass Un-Paid % Paid % The Company passed Standard 6. For un-paid claims - There were 2 coding errors per a. On a portion of 2 claims where there was a payment made late, the interest was not calculated per K.S.A (b). For paid claims - There were 3 claims where there was a payment made late, the interest was not calculated per K.S.A (b). Standard 7 Company claim forms are appropriate for the type of product. Type Sample Errors %Pass 13

, Sec. 8, &K.S.A. 40-2442(a) (1), (a)(2) and (b).")

14 Un-Paid % Paid % The Company passed Standard 9. Standard 8 Claim files are reserved in accordance with the company s established procedures. The exam team did not specifically test for this standard. Standard 9 Denied and closed-without-payment claims are handled in accordance with policy provisions, HIPPA and state law. K.A.R , Sec. 8(a) & 8(c). Type Sample Errors %Pass Un-Paid % The Company passed Standard 9. Standard 10 Canceled benefit checks and drafts reflect appropriate claim handling practices. KAR (f). Type Sample Errors %Pass Un-Paid % The Company passed Standard 10. Standard 11 Claim handling practices do not compel claimants to institute litigation, in cases of clear liability and coverage, to recover amounts due under policies by offering substantially less than is due under the policy. K.S.A (f) and (9)(g) Standard 12 Type Sample Errors %Pass Un-Paid % Paid % The Company passed Standard 11. The company complies with the requirements of The NewBorns' and Mothers' Health Protection Act of K.S.A. 40-2,102 14

. Type Sample Errors %Pass Un-Paid 99 0 100% The Company passed Standard 10.")

15 This standard was not specifically tested for. In the normal review of the 100 un-paid and 99 paid claims, any maternity claims would have been reviewed and the examiner would have noted it. There were no issues with the files that were reviewed. Standard 13 The group health plan complies with the requirements of the Mental Health Parity Act of 1996 (MHPA). K.S.A. 40-2,105(a) Separate from the exam but observed by the exam team in several of the sample files, the company had additional language in their contracts that had been filed and approved and was interpreting it inconsistent with how KID viewed K.S.A. 40-2,105 (a) - Mental Health Party Act. The company and KID came to an agreement on the policy language, and the company has re-filed their policies to correct the contracts on a going forward basis for claims incurred beginning 7/1/03. Recommendations: 1. CRL needs to review their claim procedures to insure that claims are being processed in a timely fashion per K.S.A (a)(1)and (a)(2). 2. CRL needs to review their claim procedures to insure that claims that are not processed with in the time lines specified in the Prompt Pay Act, K.S.A , have interest paid according to K.S.A (b). GENERAL COMMENTS Complaint Handling 1. While the response times were within KID s tolerances, the exam team feels that the company should review their complaint handling procedures so everyone is aware of the response times required for the different levels of complaints. General 1. The new business rejection letter listed the old third party administrator as the contact for anyone interested in obtaining health insurance through the Kansas Health Insurance Assoc. When advised of this error, the company corrected the form per K.S.A (f). Claims 1. CRL needs to review their claim procedures to insure that claims are being processed in a timely fashion per K.S.A (a)(1) and (a)(2). 15

16 2. CRL needs to review their claim procedures to insure that claims that are not processed with in the time lines specified in the prompt Pay Act, KSA , have interested paid according to K.S.A (b) CONCLUSION I would like to acknowledge the cooperation and courtesy extended to the examination team by the Ms. Sandra Pogozelski and the staff of CERES Insurance Group. The following examiners of the Office of the Commissioner of Insurance in the State of Kansas participated in the review: Market Conduct Division Lyle Behrens Michael Grover Mary Lou Maritt Supervisor Market Conduct Examiner Market Conduct Examiner Respectfully submitted, Lyle Behrens, CPCU, CIE, ARM 16

17

18

19 APPENDIX I A. K.A.R Unfair claims practices provides for the following guidelines to be met in the processing and investigation and settlement/denial of a claim: -Definitions, Sec. 3 -File and Record Documentation, Sec. 4 -Misrepresentation of Policy Provisions, Sec. 5 -Failure to Acknowledge to Pertinent communication, Sec. 6 -Standards for Prompt Investigation of Claims, Sec. 7 -Standards for Prompt, Fair and Equitable Settlements Applicable to all Insurers, Sec. 8 -Standards for Fair and Equitable Settlements Applicable To Auto Insurance, Sec. 9 -Kansas Automobile Injury Reparations Act (Payment of Benefits). K.S.A Unfair methods of competition or unfair and deceptive acts or practices. KSA Interest Due On Insurance Settlements. KSA 40-2, K.A.R Sec. 3. Definitions The definitions of "person" and of "insurance policy or insurance contract" contained in section 2 of the Unfair Trade Practice Act shall apply to this regulation and, in addition, where used in this regulation: (a) "Agent" means any individual, corporation, association, partnership or other legal entity authorized to represent an insure with respect to a claim; (b) "Claimant" means either a first party claimant, a third party claimant, or both and includes such claimant's designated legal representative and includes a member of the claimant's immediate family designated by the claimant; (c) "First party claimant" means an individual, corporation, association, or partnership or other legal entity asserting a right to payment under an insurance policy or insurance contract arising out of the occurrence of the contingency or loss covered by such policy or contract; (d) "Insurer" means a person licensed to issue or who issues any insurance policy or insurance contract in this State. (e) "Investigation" means all activities of an insurer directly or indirectly related to the determination of liabilities under coverages afforded by an insurance policy or insurance contract. (f) "Notification of claim" mean any notification, whether in writing or other means acceptable under the terms of an insurance policy or insurance contract, to an insurer or its agent, by a claimant, which reasonably apprises the insurer of the facts pertinent to a claim;

. K.S.A. 40-3110 -Unfair methods of competition or unfair and deceptive acts or practices.")

20 (g) "Third party claimant" means any individual, corporation, association, partnership or other legal entity asserting a claim against any individual, corporation, association, partnership or other legal entity insured under an insurance policy or insurance contract of an insurer; and (h) "Worker's Compensation" includes, but is not limited to, Longshoremen's and Harbor Worker's Compensation. 2. K.A.R Sec. 4 - File and Record Documentation The insurer's claim files shall be subject to examination by the (Commissioner) or by his/her duly appointed designees. Such files shall contain all notes and work papers pertaining to the claim in such detail that pertinent events and the dates of such events can be reconstructed. 3. K.A.R Sec. 5. Misrepresentation of Policy Provisions (a) No insurer shall fail to fully disclose to first party claimants all pertinent benefits, coverages or other provisions of an insurance policy or insurance contract under which a claim is presented. (b) No agent shall conceal from first party claimants benefits, coverages or other provisions of any insurance policy or insurance contract when such benefits, coverages or other provisions are pertinent to a claim. (c) No insurer shall deny a claim for failure to exhibit the property without proof of demand and unfounded refusal by a claimant to do so. (d) No insurer shall, except where there is a time limit specified in the policy, make statements, written or otherwise, requiring a claimant to give written notice of loss or proof of loss within a specified time limit and which seek to relieve the company of its obligations if such a time limit is not complied with unless the failure to comply with such time limit prejudices the insurer's rights. (e) No insurer shall request a first party claimant to sin a release that extends beyond the subject matter that gave rise to the claim payment. (f) No insurer shall issue checks or drafts in partial settlement of a loss or claim under a specific coverage which contain language which release the insurer or its insured from its total liability. 4. K.A.R Sec. 6 - Failure to Acknowledge Pertinent Communications: (a) Every insurer, upon receiving notification of a claim shall, within ten working days, acknowledge the receipt of such notice unless payment is made within such period of time. If an acknowledgement is made by means other than writing, an appropriate notation of such acknowledgement shall be made in the claim file of the insurer and dated. Notification given to an agent of an insurer shall be notification to the insurer.

21 (b) Every insurer, upon receipt of any inquiry from the insurance department respecting a claim shall, within fifteen working days of receipt of such inquiry, furnish the department with an adequate response to the inquiry. (c) An appropriate reply shall be made within ten working days on all other pertinent communications from a claimant which reasonably suggest that a response is expected. (d) Every insurer, upon receiving notification of claim, shall promptly provide necessary claim forms, instructions, and reasonable assistance so that first party claimants can comply with the policy conditions and the insurer's reasonable requirements. Compliance with this paragraph within ten working days of notification of a claim shall constitute compliance with subsection (a) of this section. 5. K.A.R Sec. 7 - Failure to Acknowledge Pertinent Communications Every insurer shall complete investigation of a claim within thirty days after notification of claim, unless such investigation cannot reasonably be completed within such time. 6. K.A.R Sec. 8 - Standards for Prompt, Fair and Equitable Settlements Applicable to All Insurers (a) Within 15 working days after receipt by the insurer of properly executed proofs of loss, the first party claimant shall be advised of the acceptance or denial of the claim by the insurer. No insurer shall deny a claim on the grounds of a specific policy provision, condition, or exclusion unless reference to such provision, condition, or exclusion is included in the denial. The denial must be given to the claimant in writing and the claim file of the insurer shall contain a copy of the denial. (b) If a claim is denied for reasons other than those described in paragraph (a) and is made by any other means than writing, an appropriate notation shall be made in the claim file of the insurer. (c) If the insurer needs more time to determine whether a first party claim should be accepted or denied, it shall so notify the first party claimant within fifteen working days after receipt of the proofs of loss, giving the reasons more time is needed. If the investigation remains incomplete, the insurer shall, forty-five days from the date of the initial notification and every forty-five days thereafter, send to such claimant a letter setting forth the reasons additional time is needed for investigation. (d) Insurers shall not fail to settle first party claims on the basis that responsibility for payment should be assumed by others except as may otherwise be provided by policy provisions. (e) Insurers shall not continue negotiations for settlement of a claim directly with a claimant who is neither an attorney nor represented by an attorney until the claimant's rights may be affected by a statute of limitations or a policy or contract time limit, without

22 giving the claimant written notice that the time limit may be expiring and may affect the claimant's rights. Such notice shall be given to first party claimants thirty days and to third party claimants sixty days before the date on which such time limit may expire. (f) No insurer shall make statements which indicate that the rights of a third party claimant may be impaired if a form or release is not completed within a given period of time unless the statement is given for the purpose of notifying the third party claimant of the provision of a statute of limitations. (g) An insurer shall not attempt to settle a loss with a first party claimant on the basis of a cash settlement which is less than the amount the insurer would pay if repairs were made, other than in total loss situations, unless such amount is agreed to by the insured. B. KSA Unfair methods of competition or unfair and deceptive acts or practices; disclosure of nonpublic personal information; rules and regulations. The following are hereby defined as unfair methods of competition and unfair or deceptive acts or practices in the business of insurance: (9) Unfair claim settlement practices. It is an unfair claim settlement practice if any of the following or any rules and regulations pertaining thereto are: (A) Committed flagrantly and in conscious disregard of such provisions, or (B) committed with such frequency as to indicate a general business practice. (a) Misrepresenting pertinent facts or insurance policy provisions relating to coverages at issue; (b) failing to acknowledge and act reasonably promptly upon communications with respect to claims arising under insurance policies; (c) failing to adopt and implement reasonable standards for the prompt investigation of claims arising under insurance policies; (d) refusing to pay claims without conducting a reasonable investigation based upon all available information; (e) failing to affirm or deny coverage of claims within a reasonable time after proof of loss statements have been completed; (f) not attempting in good faith to effectuate prompt, fair and equitable settlements of claims in which liability has become reasonably clear; (g) compelling insureds to institute litigation to recover amounts due under an insurance policy by offering substantially less than the amounts ultimately recovered in actions brought by such insureds;

23 (h) attempting to settle a claim for less than the amount to which a reasonable person would have believed that such person was entitled by reference to written or printed advertising material accompanying or made part of an application; (i) attempting to settle claims on the basis of an application which was altered without notice to, or knowledge or consent of the insured; (j) making claims payments to insureds or beneficiaries not accompanied by a statement setting forth the coverage under which payments are being made; (k) making known to insureds or claimants a policy of appealing from arbitration awards in favor of insureds or claimants for the purpose of compelling them to accept settlements or compromises less than the amount awarded in arbitration; (l) delaying the investigation or payment of claims by requiring an insured, claimant or the physician of either to submit a preliminary claim report and then requiring the subsequent submission of formal proof of loss forms, both of which submissions contain substantially the same information; (m) failing to promptly settle claims, where liability has become reasonably clear, under one portion of the insurance policy coverage in order to influence settlements under other portions of the insurance policy coverage; or (n) failing to promptly provide a reasonable explanation of the basis in the insurance policy in relation to the facts or applicable law for denial of a claim or for the offer of a compromise settlement. C. KSA Same; claims; procedures; rules and regulations. (a) Within 30 days after receipt of any claim, and amendments thereto, any insurer issuing a policy of accident and sickness insurance shall pay a clean claim for reimbursement in accordance with this section or send a written or electronic notice acknowledging receipt of and the status of the claim. Such notice shall include the date such claim was received by the insurer and state that: (1) The insurer refuses to reimburse all or part of the claim and specify each reason for denial; or (2) additional information is necessary to determine if all or any part of the claim will be reimbursed and what specific additional information is necessary. (b) If any insurer issuing a policy of accident and sickness insurance fails to comply with subsection (a), such insurer shall pay interest at the rate of 1% per month on the amount of the claim that remains unpaid 30 days after the receipt of the claim. The interest paid pursuant to this subsection shall be included in any late reimbursement without requiring the person who filed the original claim to make any additional claim for such interest

24 D. KSA 40-2,126. Interest Due On Insurance Settlements, Except as otherwise provided by K.S.A , and a, and amendments thereto, each insurance company, fraternal benefit society and any reciprocal or interinsurance exchange licensed to transact the business of insurance in this state which fails or refuses to pay any amount due under any contract of insurance within the time prescribed herein shall pay interest on the amount due. If payment is to be made to the claimant and the same is not paid within 30 calendar days after the amount of the payment is agreed to between the claimant and the insurer, interest at the rate of 18% per annum shall be payable from the date of such agreement. If payment is to be made to any other person for providing repair or other services to the claimant and the same is not paid within 30 calendar days following the date of completion of such services and receipt of the billing statement, interest at the rate of 18% per annum shall be payable on the amount agreed to between the claimant and the insurer from the date of receipt of the billing statement. CAD/MC 7/02

Rule and Regulation 43 UNFAIR CLAIMS SETTLEMENT PRACTICES

Rule and Regulation 43 UNFAIR CLAIMS SETTLEMENT PRACTICES Section 1. Purpose. 2. Authority. 3. Applicability and scope. 4. Effective Date. 5. Definitions. 6. File and record documentation. 7. Failure to

Rule and Regulation 43 UNFAIR CLAIMS SETTLEMENT PRACTICES Section 1. Purpose. 2. Authority. 3. Applicability and scope. 4. Effective Date. 5. Definitions. 6. File and record documentation. 7. Failure to

REPORT OF MARKET CONDUCT EXAMINATION TRADERS INSURANCE COMPANY 8916 TROOST AVE. KANSAS CITY, MO 64131 KANSAS INSURANCE DEPARTMENT AS OF MARCH 31, 2002

REPORT OF MARKET CONDUCT EXAMINATION TRADERS INSURANCE COMPANY 8916 TROOST AVE. KANSAS CITY, MO 64131 BY KANSAS INSURANCE DEPARTMENT AS OF MARCH 31, 2002 1 TABLE OF CONTENTS SUBJECT EXECUTIVE SUMMARY PAGE

REPORT OF MARKET CONDUCT EXAMINATION TRADERS INSURANCE COMPANY 8916 TROOST AVE. KANSAS CITY, MO 64131 BY KANSAS INSURANCE DEPARTMENT AS OF MARCH 31, 2002 1 TABLE OF CONTENTS SUBJECT EXECUTIVE SUMMARY PAGE

MARKET CONDUCT EXAMINATION REPORT

MARKET CONDUCT EXAMINATION REPORT KEY INSURANCE COMPANY NAIC # 12966 8595 College Blvd, Suite 200 Overland Park, KS 66210 ETS # KS057-M11 As of December 31, 2011 KANSAS INSURANCE DEPARTMENT TABLE OF CONTENTS

MARKET CONDUCT EXAMINATION REPORT KEY INSURANCE COMPANY NAIC # 12966 8595 College Blvd, Suite 200 Overland Park, KS 66210 ETS # KS057-M11 As of December 31, 2011 KANSAS INSURANCE DEPARTMENT TABLE OF CONTENTS

Department of Banking, Insurance, Securities & Health Care Administration Vermont Insurance Division

Department of Banking, Insurance, Securities & Health Care Administration Vermont Insurance Division REGULATION 79-2 Fair Claims Practices (Agents, Adjusters, etc.) Sept. 1, 1979 S 1 Authority 8 V.S.A.,

Department of Banking, Insurance, Securities & Health Care Administration Vermont Insurance Division REGULATION 79-2 Fair Claims Practices (Agents, Adjusters, etc.) Sept. 1, 1979 S 1 Authority 8 V.S.A.,

MARYLAND CLAIM SETTLEMENT LAWS AND REGULATIONS

MARYLAND CLAIM SETTLEMENT LAWS AND REGULATIONS LAWS: SUBTITLE 3. UNFAIR CLAIM SETTLEMENT PRACTICES 27-301. Intent and effect of subtitle. (a) Intent of subtitle.- The intent of this subtitle is to provide

MARYLAND CLAIM SETTLEMENT LAWS AND REGULATIONS LAWS: SUBTITLE 3. UNFAIR CLAIM SETTLEMENT PRACTICES 27-301. Intent and effect of subtitle. (a) Intent of subtitle.- The intent of this subtitle is to provide

REPORT OF MARKET CONDUCT EXAMINATION

REPORT OF MARKET CONDUCT EXAMINATION GUIDEONE AMERICA INSURANCE COMPANY GUIDEONE ELITE INSURANCE COMPANY GUIDEONE MUTUAL INSURANCE COMPANY GUIDEONE SPECIALTY MUTUAL INSURANCE COMPANY 1111 ASHWORTH ROAD

REPORT OF MARKET CONDUCT EXAMINATION GUIDEONE AMERICA INSURANCE COMPANY GUIDEONE ELITE INSURANCE COMPANY GUIDEONE MUTUAL INSURANCE COMPANY GUIDEONE SPECIALTY MUTUAL INSURANCE COMPANY 1111 ASHWORTH ROAD

BEFORE THE COMMISSIONER OF INSURANCE OF THE STATE OF KANSAS. ) GUARANTEE TRUST LIFE INSURANCE COMPANY ) Docket No. 4273-MC NAIC # 64211 ) ) ORDER

GUARANTEE TRUST LIFE INSURANCE COMPANY ) Docket No. 4273-MC NAIC # 64211 ) ) ORDER") BEFORE THE COMMISSIONER OF INSURANCE OF THE STATE OF KANSAS FINAL ORDER Effective: 8-19-11 In the Matter of ) GUARANTEE TRUST LIFE INSURANCE COMPANY ) Docket No. NAIC # 64211 ) ) ORDER Pursuant to the

BEFORE THE COMMISSIONER OF INSURANCE OF THE STATE OF KANSAS FINAL ORDER Effective: 8-19-11 In the Matter of ) GUARANTEE TRUST LIFE INSURANCE COMPANY ) Docket No. NAIC # 64211 ) ) ORDER Pursuant to the

114CSR14 WEST VIRGINIA LEGISLATIVE RULE INSURANCE COMMISSIONER SERIES 14 UNFAIR TRADE PRACTICES

114CSR14 WEST VIRGINIA LEGISLATIVE RULE INSURANCE COMMISSIONER SERIES 14 UNFAIR TRADE PRACTICES Section. 114-14-1. General. 114-14-2. Definitions. 114-14-3. File and Record Documentation. 114-14-4. Representation

114CSR14 WEST VIRGINIA LEGISLATIVE RULE INSURANCE COMMISSIONER SERIES 14 UNFAIR TRADE PRACTICES Section. 114-14-1. General. 114-14-2. Definitions. 114-14-3. File and Record Documentation. 114-14-4. Representation

Chapter 60 - UNFAIR PROPERTY AND CASUALTY SETTLEMENT PRACTICES RULE

Title 210 NEBRASKA DEPARTMENT OF INSURANCE Chapter 60 - UNFAIR PROPERTY AND CASUALTY SETTLEMENT PRACTICES RULE 001. Authority. This rule is adopted under the authority of the Unfair Insurance Claims Settlement

Title 210 NEBRASKA DEPARTMENT OF INSURANCE Chapter 60 - UNFAIR PROPERTY AND CASUALTY SETTLEMENT PRACTICES RULE 001. Authority. This rule is adopted under the authority of the Unfair Insurance Claims Settlement

20 CSR 100-1.040 Standards for Prompt Investigation of Claims (Rescinded July 30, 2008)...4

...4") Rules of Department of Insurance, Financial Institutions and Professional Registration Chapter 1 Improper or Unfair Claims Settlement Practices Title Page 20 CSR 100-1.010 Definitions...3 20 CSR 100-1.020

Rules of Department of Insurance, Financial Institutions and Professional Registration Chapter 1 Improper or Unfair Claims Settlement Practices Title Page 20 CSR 100-1.010 Definitions...3 20 CSR 100-1.020

"Catastrophe" means a calamity or other disastrous event that causes widespread losses resulting in excessive claims volume.

NEW JERSEY ADMINISTRATIVE CODE TITLE 11. DEPARTMENT OF BANKING AND INSURANCE DIVISION OF INSURANCE CHAPTER 2. INSURANCE GROUP SUBCHAPTER 17. UNFAIR CLAIMS SETTLEMENT PRACTICES 11:2-17.1 Purpose N.J.S.A.

NEW JERSEY ADMINISTRATIVE CODE TITLE 11. DEPARTMENT OF BANKING AND INSURANCE DIVISION OF INSURANCE CHAPTER 2. INSURANCE GROUP SUBCHAPTER 17. UNFAIR CLAIMS SETTLEMENT PRACTICES 11:2-17.1 Purpose N.J.S.A.

WEST VIRGINIA OFFICES OF THE INSURANCE COMMISSIONER Medical Malpractice Insurance Review Standards Checklist

Medical Malpractice REVIEW REQUIREMENTS REFERENCE COMMENTS FORMS Applications REFERENCE COMMENTS Fee, filing 33-6-34 The Filing Fee is $50.00 per Form filing and applies on a per company basis. WVIL All

Medical Malpractice REVIEW REQUIREMENTS REFERENCE COMMENTS FORMS Applications REFERENCE COMMENTS Fee, filing 33-6-34 The Filing Fee is $50.00 per Form filing and applies on a per company basis. WVIL All

State of Rhode Island and Providence Plantations DEPARTMENT OF BUSINESS REGULATION Division of Insurance 233 Richmond Street Providence, RI 02903

State of Rhode Island and Providence Plantations DEPARTMENT OF BUSINESS REGULATION Division of Insurance 233 Richmond Street Providence, RI 02903 INSURANCE REGULATION 73 UNFAIR PROPERTY/CASUALTY CLAIMS

State of Rhode Island and Providence Plantations DEPARTMENT OF BUSINESS REGULATION Division of Insurance 233 Richmond Street Providence, RI 02903 INSURANCE REGULATION 73 UNFAIR PROPERTY/CASUALTY CLAIMS

How To Enforce The Insurance Regulation 13.1.1

State of Rhode Island and Providence Plantations DEPARTMENT OF BUSINESS REGULATION Division of Insurance 1511 Pontiac Avenue Cranston, RI 02920 INSURANCE REGULATION 13 UNFAIR LIFE, ACCIDENT AND HEALTH

State of Rhode Island and Providence Plantations DEPARTMENT OF BUSINESS REGULATION Division of Insurance 1511 Pontiac Avenue Cranston, RI 02920 INSURANCE REGULATION 13 UNFAIR LIFE, ACCIDENT AND HEALTH

FINAL ORDER EFFECTIVE: 11-18-13

BEFORE THE COMMISSIONER OF INSURANCE OF THE STATE OF KANSAS In the Matter of ) ) FARMERS INSURANCE COMPANY, INC. ) Docket No. 4613-MC NAIC #21628 ) SUMMARY ORDER Pursuant to the authority conferred upon

BEFORE THE COMMISSIONER OF INSURANCE OF THE STATE OF KANSAS In the Matter of ) ) FARMERS INSURANCE COMPANY, INC. ) Docket No. 4613-MC NAIC #21628 ) SUMMARY ORDER Pursuant to the authority conferred upon

Product Liability Property Damage Tort Defense. 50 State Survey

Product Liability Property Damage Tort Defense 50 State Survey John J. Soltys, Esq. 206-224-1276 jsoltys@cozen.com 1201 Third Avenue Suite 5200 Seattle, WA 98101-3071 Tel: 206.340.1000 Fax: 206.621.8783

Product Liability Property Damage Tort Defense 50 State Survey John J. Soltys, Esq. 206-224-1276 jsoltys@cozen.com 1201 Third Avenue Suite 5200 Seattle, WA 98101-3071 Tel: 206.340.1000 Fax: 206.621.8783

HILTON HARRISBURG & TOWERS

UNFAIR CLAIMS SETTLEMENT PRACTICES (REGULATIONS) AND PRIVACY OF CONSUMER FINANCIAL INFORMATION (REGULATIONS) THEIR POTENTIAL IMPACT UPON BAD FAITH ACTIONS Presented By: Jay Barry Harris, Esquire Krista

UNFAIR CLAIMS SETTLEMENT PRACTICES (REGULATIONS) AND PRIVACY OF CONSUMER FINANCIAL INFORMATION (REGULATIONS) THEIR POTENTIAL IMPACT UPON BAD FAITH ACTIONS Presented By: Jay Barry Harris, Esquire Krista

NEBRASKA PROPERTY AND LIABILITY INSURANCE GUARANTY ASSOCIATION ACT

NEBRASKA PROPERTY AND LIABILITY INSURANCE GUARANTY ASSOCIATION ACT Section. 44-2401. Purpose of sections. 44-2402. Kinds of insurance covered. 44-2403. Terms, defined. 44-2404. Nebraska Property and Liability

NEBRASKA PROPERTY AND LIABILITY INSURANCE GUARANTY ASSOCIATION ACT Section. 44-2401. Purpose of sections. 44-2402. Kinds of insurance covered. 44-2403. Terms, defined. 44-2404. Nebraska Property and Liability

ILLINOIS UNFAIR CLAIMS LAW & REGULATIONS

Statutes: ILLINOIS UNFAIR CLAIMS LAW & REGULATIONS (215 ILCS 5/154.5) (from Ch. 73, par. 766.5) Sec. 154.5. Improper Claims Practices) It is an improper claims practice for any domestic, foreign or alien

Statutes: ILLINOIS UNFAIR CLAIMS LAW & REGULATIONS (215 ILCS 5/154.5) (from Ch. 73, par. 766.5) Sec. 154.5. Improper Claims Practices) It is an improper claims practice for any domestic, foreign or alien

State of Rhode Island and Providence Plantations DEPARTMENT OF BUSINESS REGULATION Division of Insurance 1511 Pontiac Avenue Cranston, RI 02920

State of Rhode Island and Providence Plantations DEPARTMENT OF BUSINESS REGULATION Division of Insurance 1511 Pontiac Avenue Cranston, RI 02920 INSURANCE REGULATION 73 UNFAIR PROPERTY/CASUALTY CLAIMS SETTLEMENT

State of Rhode Island and Providence Plantations DEPARTMENT OF BUSINESS REGULATION Division of Insurance 1511 Pontiac Avenue Cranston, RI 02920 INSURANCE REGULATION 73 UNFAIR PROPERTY/CASUALTY CLAIMS SETTLEMENT

2016 -- H 7412 SUBSTITUTE A ======== LC004346/SUB A ======== S T A T E O F R H O D E I S L A N D

01 -- H 1 SUBSTITUTE A LC00/SUB A S T A T E O F R H O D E I S L A N D IN GENERAL ASSEMBLY JANUARY SESSION, A.D. 01 A N A C T RELATING TO INSURANCE - UNFAIR CLAIMS SETTLEMENT PRACTICES ACT Introduced By:

01 -- H 1 SUBSTITUTE A LC00/SUB A S T A T E O F R H O D E I S L A N D IN GENERAL ASSEMBLY JANUARY SESSION, A.D. 01 A N A C T RELATING TO INSURANCE - UNFAIR CLAIMS SETTLEMENT PRACTICES ACT Introduced By:

An Act. SECTION 1. AMENDATORY 36 O.S. 2011, Section 1250.5, is amended to read as follows:

An Act ENROLLED HOUSE BILL NO. 1968 By: Mulready of the House and Brown of the Senate An Act relating to insurance; amending 36 O.S. 2011, Section 1250.5, which relates to unfair claims settlement practices;

An Act ENROLLED HOUSE BILL NO. 1968 By: Mulready of the House and Brown of the Senate An Act relating to insurance; amending 36 O.S. 2011, Section 1250.5, which relates to unfair claims settlement practices;

WASHINGTON INSURANCE GUARANTY ASSOCIATION ACT

WASHINGTON INSURANCE GUARANTY ASSOCIATION ACT Section 48.32.010. Purpose 48.32.020. Scope 48.32.030. Definitions 48.32.040. Creation of the association-required accounts 48.32.050. Board of directors 48.32.060.

WASHINGTON INSURANCE GUARANTY ASSOCIATION ACT Section 48.32.010. Purpose 48.32.020. Scope 48.32.030. Definitions 48.32.040. Creation of the association-required accounts 48.32.050. Board of directors 48.32.060.

Homeowner's insurance usually covers the following when they are due to accident or specific

Insurance TYPES OF POLICIES There are as many types of insurance policies as there are risks. During a disaster people may draw upon health, property and casualty and life insurance. These types of policies

Insurance TYPES OF POLICIES There are as many types of insurance policies as there are risks. During a disaster people may draw upon health, property and casualty and life insurance. These types of policies

MARKET CONDUCT EXAMINATION

MARKET CONDUCT EXAMINATION A COLLABORATIVE EXAMINATION CONDUCTED BY WASHINGTON, IDAHO, AND ARIZONA OF: WESTERN UNITED LIFE ASSURANCE COMPANY OLD STANDARD LIFE INSURANCE COMPANY OLD WEST LIFE & ANNUITY

MARKET CONDUCT EXAMINATION A COLLABORATIVE EXAMINATION CONDUCTED BY WASHINGTON, IDAHO, AND ARIZONA OF: WESTERN UNITED LIFE ASSURANCE COMPANY OLD STANDARD LIFE INSURANCE COMPANY OLD WEST LIFE & ANNUITY

days. Reply to claimant Life: Affirm or deny coverage every 45 days If settlement period specified, If settlement period specified,

The date following each state indicates the last time information for the state was reviewed/changed. AL 27-1-17 Health 45 days for paper claims; 30 days for electronic claims. 1 ½% per month. If claim

The date following each state indicates the last time information for the state was reviewed/changed. AL 27-1-17 Health 45 days for paper claims; 30 days for electronic claims. 1 ½% per month. If claim

HAWAI`I REVISED STATUTES CHAPTER 672B DESIGN CLAIM CONCILIATION PANEL. Act 207, 2007 Session Laws of Hawai`i

HAWAI`I REVISED STATUTES CHAPTER 672B DESIGN CLAIM CONCILIATION PANEL Act 207, 2007 Session Laws of Hawai`i Section 672B-1 Definitions 672B-2 Administration of chapter 672B-3 Design claim conciliation

HAWAI`I REVISED STATUTES CHAPTER 672B DESIGN CLAIM CONCILIATION PANEL Act 207, 2007 Session Laws of Hawai`i Section 672B-1 Definitions 672B-2 Administration of chapter 672B-3 Design claim conciliation

REPORT OF MARKET CONDUCT EXAMINATION OF

REPORT OF MARKET CONDUCT EXAMINATION OF UNITED INSURANCE COMPANY OF AMERICA St. Louis, MI AS OF December 10, 2010 COMMONWEALTH OF PENNSYLVANIA INSURANCE DEPARTMENT MARKET CONDUCT DIVISION Issued: January

REPORT OF MARKET CONDUCT EXAMINATION OF UNITED INSURANCE COMPANY OF AMERICA St. Louis, MI AS OF December 10, 2010 COMMONWEALTH OF PENNSYLVANIA INSURANCE DEPARTMENT MARKET CONDUCT DIVISION Issued: January

FINAL ORDER EFFECTIVE: 6-30-14

FINAL ORDER EFFECTIVE: 6-30-14 BEFORE THE COMMISSIONER OF INSURANCE OF THE STATE OF KANSAS In the Matter of ) ) PROTECTIVE LIFE INSURANCE COMPANY ) Docket No. 4662-MC NAIC #68136 ) SUMMARY ORDER Pursuant

FINAL ORDER EFFECTIVE: 6-30-14 BEFORE THE COMMISSIONER OF INSURANCE OF THE STATE OF KANSAS In the Matter of ) ) PROTECTIVE LIFE INSURANCE COMPANY ) Docket No. 4662-MC NAIC #68136 ) SUMMARY ORDER Pursuant

MARKET CONDUCT EXAMINATION ATLANTA CASUALTY COMPANY ATLANTA SPECIALTY COMPANY 3169 HOLCOMB BRIDGE ROAD NORCROSS, GEORGIA 30348

Page 1 of 14 MARKET CONDUCT EXAMINATION OF ATLANTA CASUALTY COMPANY ATLANTA SPECIALTY COMPANY 3169 HOLCOMB BRIDGE ROAD NORCROSS, GEORGIA 30348 JANUARY 1, 1999 DECEMBER 31, 1999 Seattle Washington June

Page 1 of 14 MARKET CONDUCT EXAMINATION OF ATLANTA CASUALTY COMPANY ATLANTA SPECIALTY COMPANY 3169 HOLCOMB BRIDGE ROAD NORCROSS, GEORGIA 30348 JANUARY 1, 1999 DECEMBER 31, 1999 Seattle Washington June

TEXAS UNFAIR CLAIMS STATUTES AND REGULATIONS

TEXAS UNFAIR CLAIMS STATUTES AND REGULATIONS 541.060. UNFAIR SETTLEMENT PRACTICES. (a) It is an unfair method of competition or an unfair or deceptive act or practice in the business of insurance to engage

TEXAS UNFAIR CLAIMS STATUTES AND REGULATIONS 541.060. UNFAIR SETTLEMENT PRACTICES. (a) It is an unfair method of competition or an unfair or deceptive act or practice in the business of insurance to engage

Findings of Fact. 1. The Commissioner of Insurance has jurisdiction over this matter pursuant

BEFORE THE COMMISSIONER OF INSURANCE -12 OF THE STATE OF KANSAS FINAL ORDER EFFECTIVE: 12-26-12 In the Matter of the Proposed Adoption ) of the Financial Condition Examination ) Report as of December 31,

BEFORE THE COMMISSIONER OF INSURANCE -12 OF THE STATE OF KANSAS FINAL ORDER EFFECTIVE: 12-26-12 In the Matter of the Proposed Adoption ) of the Financial Condition Examination ) Report as of December 31,

LONG TERM DISABILITY INSURANCE CERTIFICATE BOOKLET

LONG TERM DISABILITY INSURANCE CERTIFICATE BOOKLET GROUP INSURANCE FOR SOUTH LYON COMMUNITY SCHOOL NUMBER 143 TEACHERS The benefits for which you are insured are set forth in the pages of this booklet.

LONG TERM DISABILITY INSURANCE CERTIFICATE BOOKLET GROUP INSURANCE FOR SOUTH LYON COMMUNITY SCHOOL NUMBER 143 TEACHERS The benefits for which you are insured are set forth in the pages of this booklet.

REPORT OF MARKET CONDUCT EXAMINATION OF

REPORT OF MARKET CONDUCT EXAMINATION OF CONSECO LIFE INSURANCE COMPANY Carmel, IN AS OF December 23, 2010 COMMONWEALTH OF PENNSYLVANIA INSURANCE DEPARTMENT MARKET CONDUCT DIVISION Issued: January 27, 2011

REPORT OF MARKET CONDUCT EXAMINATION OF CONSECO LIFE INSURANCE COMPANY Carmel, IN AS OF December 23, 2010 COMMONWEALTH OF PENNSYLVANIA INSURANCE DEPARTMENT MARKET CONDUCT DIVISION Issued: January 27, 2011

LONG TERM DISABILITY INSURANCE CERTIFICATE BOOKLET

LONG TERM DISABILITY INSURANCE CERTIFICATE BOOKLET GROUP INSURANCE FOR WAYNE WESTLAND COMMUNITY SCHOOLS SCHOOL NUMBER 944 TEACHERS The benefits for which you are insured are set forth in the pages of this

LONG TERM DISABILITY INSURANCE CERTIFICATE BOOKLET GROUP INSURANCE FOR WAYNE WESTLAND COMMUNITY SCHOOLS SCHOOL NUMBER 944 TEACHERS The benefits for which you are insured are set forth in the pages of this

BAD FAITH IN WASHINGTON

BAD FAITH IN WASHINGTON By Steve Jensen,, and An insurer s bad faith can give rise to two related causes of action under Washington law: 1) a cause of action for bad faith sounding in tort, and 2) a cause

BAD FAITH IN WASHINGTON By Steve Jensen,, and An insurer s bad faith can give rise to two related causes of action under Washington law: 1) a cause of action for bad faith sounding in tort, and 2) a cause

FINAL ORDER EFFECTIVE: 8-11-14

BEFORE THE COMMISSIONER OF INSURANCE OF THE STATE OF KANSAS In the Matter of ) ALLIANZ LIFE INSURANCE COMPANY OF NORTH ) Docket No. 4680-MC AMERICA ) NAIC #90611 ) SUMMARY ORDER Pursuant to the authority

BEFORE THE COMMISSIONER OF INSURANCE OF THE STATE OF KANSAS In the Matter of ) ALLIANZ LIFE INSURANCE COMPANY OF NORTH ) Docket No. 4680-MC AMERICA ) NAIC #90611 ) SUMMARY ORDER Pursuant to the authority

BEFORE THE COMMISSIONER OF INSURANCE OF THE STATE OF KANSAS CONSENT ORDER

BEFORE THE COMMISSIONER OF INSURANCE OF THE STATE OF KANSAS In the Matter of ) FIRSTCOMP INSURANCE ) Docket No. 3946-CO COMPANY ) CONSENT ORDER The Kansas Insurance Department ( KID ) and FirstComp Insurance

BEFORE THE COMMISSIONER OF INSURANCE OF THE STATE OF KANSAS In the Matter of ) FIRSTCOMP INSURANCE ) Docket No. 3946-CO COMPANY ) CONSENT ORDER The Kansas Insurance Department ( KID ) and FirstComp Insurance

MARKET CONDUCT EXAMINATION NUMBER 2012C-0026 BROOKE LIFE INSURANCE COMPANY

STATE OF MICHIGAN DEPARTMENT OF LICENSING AND REGULATORY AFFAIRS MARKET CONDUCT EXAMINATION NUMBER 2012C-0026 TARGETED MARKET CONDUCT EXAMINATION REPORT OF BROOKE LIFE INSURANCE COMPANY LANSING, MICHIGAN

STATE OF MICHIGAN DEPARTMENT OF LICENSING AND REGULATORY AFFAIRS MARKET CONDUCT EXAMINATION NUMBER 2012C-0026 TARGETED MARKET CONDUCT EXAMINATION REPORT OF BROOKE LIFE INSURANCE COMPANY LANSING, MICHIGAN

PENNSYLVANIA UNFAIR CLAIMS STATUTES & REGULATIONS

PENNSYLVANIA UNFAIR CLAIMS STATUTES & REGULATIONS STATUTES: T. 40 P.S., Ch. 4, Prec. 1171.1, Refs & Annos T. 40 P.S., Ch. 4, Prec. 1171.1, Refs & Annos Purdon's Pennsylvania Statutes and Consolidated Statutes

PENNSYLVANIA UNFAIR CLAIMS STATUTES & REGULATIONS STATUTES: T. 40 P.S., Ch. 4, Prec. 1171.1, Refs & Annos T. 40 P.S., Ch. 4, Prec. 1171.1, Refs & Annos Purdon's Pennsylvania Statutes and Consolidated Statutes

MARKET CONDUCT EXAMINATION NUMBER 2013C-0059 TARGETED MARKET CONDUCT EXAMINATION REPORT ALLSTATE PROPERTY AND CASUALTY INSURANCE COMPANY

STATE OF MICHIGAN DEPARTMENT OF INSURANCE AND FINANCIAL SERVICES MARKET CONDUCT EXAMINATION NUMBER 2013C-0059 TARGETED MARKET CONDUCT EXAMINATION REPORT OF ALLSTATE PROPERTY AND CASUALTY INSURANCE COMPANY

STATE OF MICHIGAN DEPARTMENT OF INSURANCE AND FINANCIAL SERVICES MARKET CONDUCT EXAMINATION NUMBER 2013C-0059 TARGETED MARKET CONDUCT EXAMINATION REPORT OF ALLSTATE PROPERTY AND CASUALTY INSURANCE COMPANY

FINAL ORDER Effective: 11-27-07

BEFORE THE COMMISSIONER OF INSURANCE OF THE STATE OF KANSAS ) SunAmerica Life ) Insurance Company ) SUMMARY ORDER Pursuant to the authority granted to the Commissioner of Insurance ( Commissioner ) by

BEFORE THE COMMISSIONER OF INSURANCE OF THE STATE OF KANSAS ) SunAmerica Life ) Insurance Company ) SUMMARY ORDER Pursuant to the authority granted to the Commissioner of Insurance ( Commissioner ) by

LONG TERM DISABILITY INSURANCE CERTIFICATE BOOKLET

LONG TERM DISABILITY INSURANCE CERTIFICATE BOOKLET GROUP INSURANCE FOR MONROE CO COMMUNITY COLLEGE SCHOOL NUMBER 704 TEACHERS The benefits for which you are insured are set forth in the pages of this booklet.

LONG TERM DISABILITY INSURANCE CERTIFICATE BOOKLET GROUP INSURANCE FOR MONROE CO COMMUNITY COLLEGE SCHOOL NUMBER 704 TEACHERS The benefits for which you are insured are set forth in the pages of this booklet.

NEW YORK CITY FALSE CLAIMS ACT Administrative Code 7-801 through 7-810 *

NEW YORK CITY FALSE CLAIMS ACT Administrative Code 7-801 through 7-810 * 7-801. Short title. This chapter shall be known as the "New York city false claims act." 7-802. Definitions. For purposes of this

NEW YORK CITY FALSE CLAIMS ACT Administrative Code 7-801 through 7-810 * 7-801. Short title. This chapter shall be known as the "New York city false claims act." 7-802. Definitions. For purposes of this

RLI Insurance Company Peoria, Illinois 61615 A Stock Insurance Company. Personal Umbrella Liability Policy SPECIMEN

Policy Number: RLI Insurance Company Peoria, Illinois 61615 A Stock Insurance Company Personal Umbrella Liability Policy STATE OF NEW YORK AMENDATORY ENDORSEMENT In accordance with the laws and regulations

Policy Number: RLI Insurance Company Peoria, Illinois 61615 A Stock Insurance Company Personal Umbrella Liability Policy STATE OF NEW YORK AMENDATORY ENDORSEMENT In accordance with the laws and regulations

MARKET CONDUCT EXAMINATION ST. PAUL FIRE AND MARINE INSURANCE COMPANY AND AFFILIATES 385 WASHINGTON STREET ST. PAUL, MINNESOTA 55102

MARKET CONDUCT EXAMINATION ST. PAUL FIRE AND MARINE INSURANCE COMPANY AND AFFILIATES 385 WASHINGTON STREET ST. PAUL, MINNESOTA 55102 MARCH 1, 2002 FEBRUARY 28, 2003 TABLE OF CONTENTS Section Page Table

MARKET CONDUCT EXAMINATION ST. PAUL FIRE AND MARINE INSURANCE COMPANY AND AFFILIATES 385 WASHINGTON STREET ST. PAUL, MINNESOTA 55102 MARCH 1, 2002 FEBRUARY 28, 2003 TABLE OF CONTENTS Section Page Table

UNIFORM HEALTH CARRIER EXTERNAL REVIEW MODEL ACT

Model Regulation Service April 2010 UNIFORM HEALTH CARRIER EXTERNAL REVIEW MODEL ACT Table of Contents Section 1. Title Section 2. Purpose and Intent Section 3. Definitions Section 4. Applicability and

Model Regulation Service April 2010 UNIFORM HEALTH CARRIER EXTERNAL REVIEW MODEL ACT Table of Contents Section 1. Title Section 2. Purpose and Intent Section 3. Definitions Section 4. Applicability and

COMMONWEALTH OF PENNSYLVANIA INSURANCE DEPARTMENT MARKET CONDUCT EXAMINATION REPORT HIGHMARK INC. CAMP HILL, PA

COMMONWEALTH OF PENNSYLVANIA INSURANCE DEPARTMENT MARKET CONDUCT EXAMINATION REPORT OF HIGHMARK INC. CAMP HILL, PA As of: March 8, 2013 Issued: May 3, 2013 MARKET ACTIONS BUREAU LIFE AND HEALTH DIVISION

COMMONWEALTH OF PENNSYLVANIA INSURANCE DEPARTMENT MARKET CONDUCT EXAMINATION REPORT OF HIGHMARK INC. CAMP HILL, PA As of: March 8, 2013 Issued: May 3, 2013 MARKET ACTIONS BUREAU LIFE AND HEALTH DIVISION

STATE OF MISSOURI DEPARTMENT OF INSURANCE, FINANCIAL INSTITUTIONS AND PROFESSIONAL REGISTRATION

STATE OF MISSOURI DEPARTMENT OF INSURANCE, FINANCIAL INSTITUTIONS AND PROFESSIONAL REGISTRATION FINAL MARKET CONDUCT EXAMINATION REPORT Of the Property and Casualty Business of Direct General Insurance

STATE OF MISSOURI DEPARTMENT OF INSURANCE, FINANCIAL INSTITUTIONS AND PROFESSIONAL REGISTRATION FINAL MARKET CONDUCT EXAMINATION REPORT Of the Property and Casualty Business of Direct General Insurance

Sample Disability Income Salary Continuation Plan Resolution And Agreement

Sample Disability Income Salary Continuation Plan Resolution And Agreement The sample agreement has been prepared as guides to assist attorneys. This sample agreement cannot be used as a final draft. Clients

Sample Disability Income Salary Continuation Plan Resolution And Agreement The sample agreement has been prepared as guides to assist attorneys. This sample agreement cannot be used as a final draft. Clients

CALIFORNIA CODE OF REGULATIONS, TITLE 10, CHAPTER 5. SUBCHAPTER 7.5 Unfair or Deceptive Acts or Practices in the Business of Insurance

CALIFORNIA CODE OF REGULATIONS, TITLE 10, CHAPTER 5 SUBCHAPTER 7.5 Unfair or Deceptive Acts or Practices in the Business of Insurance Article 1. Fair Claims Settlement Practices Section 2695.1. Preamble.

CALIFORNIA CODE OF REGULATIONS, TITLE 10, CHAPTER 5 SUBCHAPTER 7.5 Unfair or Deceptive Acts or Practices in the Business of Insurance Article 1. Fair Claims Settlement Practices Section 2695.1. Preamble.

NATIONAL TEACHERS ASSOCIATES LIFE INSURANCE COMPANY NAIC # 87963 CDI # 4418-0

[IN ACCORDANCE WITH CALIFORNIA INSURANCE CODE (CIC) SECTION 12938, THIS REPORT WILL BE MADE PUBLIC AND PUBLISHED ON THE CALIFORNIA DEPARTMENT OF INSURANCE (CDI) WEBSITE] WEBSITE PUBLISHED REPORT OF THE

[IN ACCORDANCE WITH CALIFORNIA INSURANCE CODE (CIC) SECTION 12938, THIS REPORT WILL BE MADE PUBLIC AND PUBLISHED ON THE CALIFORNIA DEPARTMENT OF INSURANCE (CDI) WEBSITE] WEBSITE PUBLISHED REPORT OF THE

DAIRYLAND INSURANCE COMPANY MARKET CONDUCT EXAMINATION OCTOBER 31, 1996- OCTOBER 31, 1997

DAIRYLAND INSURANCE COMPANY MARKET CONDUCT EXAMINATION OCTOBER 31, 1996- OCTOBER 31, 1997 Seattle Washington Deborah Senn Insurance Commissioner Olympia, Washington 98504 Pursuant to your instructions

DAIRYLAND INSURANCE COMPANY MARKET CONDUCT EXAMINATION OCTOBER 31, 1996- OCTOBER 31, 1997 Seattle Washington Deborah Senn Insurance Commissioner Olympia, Washington 98504 Pursuant to your instructions

MEGA Life and Health Insurance Company Office of the President 9151 Grapevine Highway North Richland Hills, Texas 76180

TO: MEGA Life and Health Insurance Company Office of the President 9151 Grapevine Highway North Richland Hills, Texas 76180 RE: Delaware Market Conduct Examination #04-709 CONSENT DECREE WHEREAS, the MEGA

TO: MEGA Life and Health Insurance Company Office of the President 9151 Grapevine Highway North Richland Hills, Texas 76180 RE: Delaware Market Conduct Examination #04-709 CONSENT DECREE WHEREAS, the MEGA

The Commonwealth of Massachusetts

SENATE, NO. 2476 [Senate, June 17, 2010 - New draft of Senate, No. 462 and House, No. 979 reported from the committee on Financial Services.] The Commonwealth of Massachusetts IN THE YEAR OF TWO THOUSAND

SENATE, NO. 2476 [Senate, June 17, 2010 - New draft of Senate, No. 462 and House, No. 979 reported from the committee on Financial Services.] The Commonwealth of Massachusetts IN THE YEAR OF TWO THOUSAND

MARKET CONDUCT EXAMINATION REPORT TITAN INDEMNITY INSURANCE COMPANY NAIC #13242. June 30, 2009

MARKET CONDUCT EXAMINATION REPORT TITAN INDEMNITY INSURANCE COMPANY NAIC #13242 June 30, 2009 TABLE OF CONTENTS SALUTATION... 1 EXECUTIVE SUMMARY... 2 SCOPE OF EXAMINATION... 3 HISTORY AND PROFILE...

MARKET CONDUCT EXAMINATION REPORT TITAN INDEMNITY INSURANCE COMPANY NAIC #13242 June 30, 2009 TABLE OF CONTENTS SALUTATION... 1 EXECUTIVE SUMMARY... 2 SCOPE OF EXAMINATION... 3 HISTORY AND PROFILE...

This subchapter applies to claims arising under motor vehicle collision and comprehensive coverages.

NEW JERSEY ADMINISTRATIVE CODE TITLE 11. DEPARTMENT OF BANKING AND INSURANCE DIVISION OF INSURANCE CHAPTER 3. AUTOMOBILE INSURANCE SUBCHAPTER 10. AUTO PHYSICAL DAMAGE CLAIMS 11:3-10.1 Scope This subchapter

NEW JERSEY ADMINISTRATIVE CODE TITLE 11. DEPARTMENT OF BANKING AND INSURANCE DIVISION OF INSURANCE CHAPTER 3. AUTOMOBILE INSURANCE SUBCHAPTER 10. AUTO PHYSICAL DAMAGE CLAIMS 11:3-10.1 Scope This subchapter

Indiana Department of Insurance Filing Company Checklist INDIVIDUAL MEDICARE SUPPLEMENT Review Standards (Checklist must be submitted with filing.

Indiana Department of Insurance Filing Company Checklist INDIVIDUAL MEDICARE SUPPLEMENT Review Standards (Checklist must be submitted with filing.) Company Name NAIC # Form number(s) Filing date Statute/Regulation

Indiana Department of Insurance Filing Company Checklist INDIVIDUAL MEDICARE SUPPLEMENT Review Standards (Checklist must be submitted with filing.) Company Name NAIC # Form number(s) Filing date Statute/Regulation

28 Texas Administrative Code

28 Texas Administrative Code Chapter 127 - Designated Doctor Procedures and Requirements Link to the Secretary of State for 28 TAC Chapter 127 (HTML): http://info.sos.state.tx.us/pls/pub/readtac$ext.viewtac?tac_view=4&ti=28&pt=2&ch=127.

28 Texas Administrative Code Chapter 127 - Designated Doctor Procedures and Requirements Link to the Secretary of State for 28 TAC Chapter 127 (HTML): http://info.sos.state.tx.us/pls/pub/readtac$ext.viewtac?tac_view=4&ti=28&pt=2&ch=127.

ILLINOIS LAW MANUAL CHAPTER XIII BAD FAITH AND EXTRA CONTRACTUAL LIABILITY. An insured or an assignee may recover extra-contractual damages from an

If you have questions or would like further information regarding Excess Judgments in Third Party Claims, please contact: Kevin Caplis 312-540-7630 kcaplis@querrey.com Result Oriented. Success Driven.

If you have questions or would like further information regarding Excess Judgments in Third Party Claims, please contact: Kevin Caplis 312-540-7630 kcaplis@querrey.com Result Oriented. Success Driven.

MARKET CONDUCT REPORT ON EXAMINATION MVP HEALTH PLAN, INC. MVP HEALTH INSURANCE COMPANY MVP HEALTH SERVICES CORP. PREFERRED ASSURANCE COMPANY, INC.

MARKET CONDUCT REPORT ON EXAMINATION OF MVP HEALTH PLAN, INC. MVP HEALTH INSURANCE COMPANY MVP HEALTH SERVICES CORP. PREFERRED ASSURANCE COMPANY, INC. AS OF DECEMBER 31, 2010 DATE OF REPORT MAY 24, 2013

MARKET CONDUCT REPORT ON EXAMINATION OF MVP HEALTH PLAN, INC. MVP HEALTH INSURANCE COMPANY MVP HEALTH SERVICES CORP. PREFERRED ASSURANCE COMPANY, INC. AS OF DECEMBER 31, 2010 DATE OF REPORT MAY 24, 2013

WEST VIRGINIA OFFICES OF THE INSURANCE COMMISSIONER Homeowners Insurance Review Standards Checklist

Homeowners REVIEW REFERENCE COMMENTS REQUIREMENTS FORMS Applications REFERENCE COMMENTS Fee, filing 33-6-34 The Filing Fee is $50.00 per Form filing and applies on a per company basis. Submission, filing

Homeowners REVIEW REFERENCE COMMENTS REQUIREMENTS FORMS Applications REFERENCE COMMENTS Fee, filing 33-6-34 The Filing Fee is $50.00 per Form filing and applies on a per company basis. Submission, filing

NC WORKERS COMPENSATION: BASIC INFORMATION FOR MEDICAL PROVIDERS

NC WORKERS COMPENSATION: BASIC INFORMATION FOR MEDICAL PROVIDERS CURRENT AS OF APRIL 1, 2010 I. INFORMATION SOURCES Where is information available for medical providers treating patients with injuries/conditions

NC WORKERS COMPENSATION: BASIC INFORMATION FOR MEDICAL PROVIDERS CURRENT AS OF APRIL 1, 2010 I. INFORMATION SOURCES Where is information available for medical providers treating patients with injuries/conditions

MARKET CONDUCT EXAMINATION REPORT NATIONWIDE PROPERTY AND CASUALTY INSURANCE COMPANY NAIC #37877

MARKET CONDUCT EXAMINATION REPORT NATIONWIDE PROPERTY AND CASUALTY INSURANCE COMPANY NAIC #37877 June 30, 2009 Contents SALUTATION... 1 EXECUTIVE SUMMARY... 2 SCOPE OF EXAMINATION... 3 HISTORY AND PROFILE...

MARKET CONDUCT EXAMINATION REPORT NATIONWIDE PROPERTY AND CASUALTY INSURANCE COMPANY NAIC #37877 June 30, 2009 Contents SALUTATION... 1 EXECUTIVE SUMMARY... 2 SCOPE OF EXAMINATION... 3 HISTORY AND PROFILE...

FINAL ORDER EFFECTIVE: 2-10-14

BEFORE THE COMMISSIONER OF INSURANCE OF THE STATE OF KANSAS In the Matter of ) AMERICAN EQUITY INVESTMENT LIFE ) INSURANCE COMPANY ) Docket No. 4628-MC NAIC #92738 SUMMARY ORDER Pursuant to the authority

BEFORE THE COMMISSIONER OF INSURANCE OF THE STATE OF KANSAS In the Matter of ) AMERICAN EQUITY INVESTMENT LIFE ) INSURANCE COMPANY ) Docket No. 4628-MC NAIC #92738 SUMMARY ORDER Pursuant to the authority

GENERAL AGENT AGREEMENT

Complete Wellness Solutions, Inc. 6338 Constitution Drive Fort Wayne, Indiana 46804 GENERAL AGENT AGREEMENT This Agreement is made by and between Complete Wellness Solutions, Inc. (the Company ) and (the

Complete Wellness Solutions, Inc. 6338 Constitution Drive Fort Wayne, Indiana 46804 GENERAL AGENT AGREEMENT This Agreement is made by and between Complete Wellness Solutions, Inc. (the Company ) and (the

211 CMR 123.00: DIRECT PAYMENT OF MOTOR VEHICLE COLLISION AND COMPREHENSIVE COVERAGE CLAIMS AND REFERRAL REPAIR SHOP PROGRAMS

211 CMR 123.00: DIRECT PAYMENT OF MOTOR VEHICLE COLLISION AND COMPREHENSIVE COVERAGE CLAIMS AND REFERRAL REPAIR SHOP PROGRAMS Section 123.01: Authority 123.02: Purpose and Scope 123.03: Definitions 123.04:

211 CMR 123.00: DIRECT PAYMENT OF MOTOR VEHICLE COLLISION AND COMPREHENSIVE COVERAGE CLAIMS AND REFERRAL REPAIR SHOP PROGRAMS Section 123.01: Authority 123.02: Purpose and Scope 123.03: Definitions 123.04:

MARKET CONDUCT EXAMINATION REPORT PROMPT PAY. BCBSD, Inc. as of. June 30, 2006

MARKET CONDUCT EXAMINATION REPORT PROMPT PAY of BCBSD, Inc. as of June 30, 2006 TABLE OF CONTENTS SALUTATION.... 1 EXECUTIVE SUMMARY..2 SCOPE OF EXAMINATION...3 HISTORY AND PROFILE...4 METHODOLOGY...4

MARKET CONDUCT EXAMINATION REPORT PROMPT PAY of BCBSD, Inc. as of June 30, 2006 TABLE OF CONTENTS SALUTATION.... 1 EXECUTIVE SUMMARY..2 SCOPE OF EXAMINATION...3 HISTORY AND PROFILE...4 METHODOLOGY...4

3420. Liability insurance; standard provisions; right of injured person

3420. Liability insurance; standard provisions; right of injured person (a) No policy or contract insuring against liability for injury to person, except as provided in subsection (g) of this section,

3420. Liability insurance; standard provisions; right of injured person (a) No policy or contract insuring against liability for injury to person, except as provided in subsection (g) of this section,

CREDIT REPAIR ORGANIZATIONS ACT 15 U.S.C. 1679 et. seq.

CREDIT REPAIR ORGANIZATIONS ACT 15 U.S.C. 1679 et. seq. Please note that the information contained herein should not be construed as legal advice and is intended for informational purposes only. In addition,

CREDIT REPAIR ORGANIZATIONS ACT 15 U.S.C. 1679 et. seq. Please note that the information contained herein should not be construed as legal advice and is intended for informational purposes only. In addition,

DISCOVERY IN A COVERAGE CASE

DISCOVERY IN A COVERAGE CASE Michael J. Mohlman Smith Coonrod Mohlman, LLC 7001 W. 79th Street Overland Park, KS 66204 Telephone: (913) 495-9965; Facsimile: (913) 894-1686 mike@smithcoonrod.com www.smithcoonrod.com

DISCOVERY IN A COVERAGE CASE Michael J. Mohlman Smith Coonrod Mohlman, LLC 7001 W. 79th Street Overland Park, KS 66204 Telephone: (913) 495-9965; Facsimile: (913) 894-1686 mike@smithcoonrod.com www.smithcoonrod.com

How To Defend A Policy In Nevada

Insurance for In-House Counsel April 2014 Kevin Stolworthy, Esq. / Conor Flynn, Esq. / Matthew Stafford, Esq. Commercial General Liability Insurance ( CGL insurance ) Purpose of CGL Insurance CGL insurance

Insurance for In-House Counsel April 2014 Kevin Stolworthy, Esq. / Conor Flynn, Esq. / Matthew Stafford, Esq. Commercial General Liability Insurance ( CGL insurance ) Purpose of CGL Insurance CGL insurance

BULLETIN 96-7 FREQUENT PROBLEMS FOUND IN FILINGS

1 of 8 6/25/2008 3:39 PM BULLETIN 96-7 FREQUENT PROBLEMS FOUND IN FILINGS Property and Casualty Lines Over the years we have found that insurance companies consistently fail to make their forms and filings

1 of 8 6/25/2008 3:39 PM BULLETIN 96-7 FREQUENT PROBLEMS FOUND IN FILINGS Property and Casualty Lines Over the years we have found that insurance companies consistently fail to make their forms and filings

RIVERSOURCE LIFE INSURANCE COMPANY

RIVERSOURCE LIFE INSURANCE COMPANY MARKET CONDUCT EXAMINATION REPORT DATE OF EXAMINATION: August 26, 2013 through November 8, 2013 EXAMINATION OF: LOCATION: RiverSource Life Insurance Company NAIC Number:

RIVERSOURCE LIFE INSURANCE COMPANY MARKET CONDUCT EXAMINATION REPORT DATE OF EXAMINATION: August 26, 2013 through November 8, 2013 EXAMINATION OF: LOCATION: RiverSource Life Insurance Company NAIC Number:

FINAL ORDER EFFECTIVE: 11-5-12

BEFORE THE COMMISSIONER OF INSURANCE -12 OF THE STATE OF KANSAS FINAL ORDER EFFECTIVE: 11-5-12 In the Matter of ) 5 STAR LIFE INSURANCE CO. ) Docket No. NAIC#77879 ) ) CONSENT AGREEMENT AND FINAL ORDER

BEFORE THE COMMISSIONER OF INSURANCE -12 OF THE STATE OF KANSAS FINAL ORDER EFFECTIVE: 11-5-12 In the Matter of ) 5 STAR LIFE INSURANCE CO. ) Docket No. NAIC#77879 ) ) CONSENT AGREEMENT AND FINAL ORDER

BEFORE THE COMMISSIONER OF INSURANCE OF THE STATE OF KANSAS. In the Matter of NAL Insurance ) Docket No. 3975-SO Agency )

Docket No. 3975-SO Agency )") BEFORE THE COMMISSIONER OF INSURANCE OF THE STATE OF KANSAS In the Matter of NAL Insurance ) Docket No. 3975-SO Agency ) And In the Matter of Fred Styka ) Docket No. 3974 -SO FINAL ORDER NOW on this 2nd

BEFORE THE COMMISSIONER OF INSURANCE OF THE STATE OF KANSAS In the Matter of NAL Insurance ) Docket No. 3975-SO Agency ) And In the Matter of Fred Styka ) Docket No. 3974 -SO FINAL ORDER NOW on this 2nd

Chapter 120-2-14 GEORGIA AUTOMOBILE INSURANCE PLAN

Chapter 120-2-14 GEORGIA AUTOMOBILE INSURANCE PLAN Section 120-2-14-.01 Authority. 120-2-14-.02 Purpose. 120-2-14-.03 Definitions. 120-2-14-.04 Administration of the plan. 120-2-14-.05 Duties of governing

Chapter 120-2-14 GEORGIA AUTOMOBILE INSURANCE PLAN Section 120-2-14-.01 Authority. 120-2-14-.02 Purpose. 120-2-14-.03 Definitions. 120-2-14-.04 Administration of the plan. 120-2-14-.05 Duties of governing

BEFORE THE COMMISSIONER OF INSURANCE OF THE STATE OF KANSAS

BEFORE THE COMMISSIONER OF INSURANCE OF THE STATE OF KANSAS FINAL ORDER Effective: 10-3-11 In the Matter of the Proposed Adoption ) of the Financial Condition Examination ) Report as of As of March 31,

BEFORE THE COMMISSIONER OF INSURANCE OF THE STATE OF KANSAS FINAL ORDER Effective: 10-3-11 In the Matter of the Proposed Adoption ) of the Financial Condition Examination ) Report as of As of March 31,

SURA/JEFFERSON SCIENCE ASSOCIATES, LLC COMPREHENSIVE HEALTH AND WELFARE BENEFIT PLAN. Amended and Restated

SURA/JEFFERSON SCIENCE ASSOCIATES, LLC COMPREHENSIVE HEALTH AND WELFARE BENEFIT PLAN Amended and Restated Effective June 1, 2006 SURA/JEFFERSON SCIENCE ASSOCIATES, LLC COMPREHENSIVE HEALTH AND WELFARE

SURA/JEFFERSON SCIENCE ASSOCIATES, LLC COMPREHENSIVE HEALTH AND WELFARE BENEFIT PLAN Amended and Restated Effective June 1, 2006 SURA/JEFFERSON SCIENCE ASSOCIATES, LLC COMPREHENSIVE HEALTH AND WELFARE

COMMONWEALTH OF PENNSYLVANIA INSURANCE DEPARTMENT MARKET CONDUCT EXAMINATION REPORT HUMANA INSURANCE COMPANY DE PERE, WI

COMMONWEALTH OF PENNSYLVANIA INSURANCE DEPARTMENT MARKET CONDUCT EXAMINATION REPORT OF HUMANA INSURANCE COMPANY DE PERE, WI As of: June 28, 2012 Issued: August 23, 2012 BUREAU OF MARKET ACTIONS LIFE AND

COMMONWEALTH OF PENNSYLVANIA INSURANCE DEPARTMENT MARKET CONDUCT EXAMINATION REPORT OF HUMANA INSURANCE COMPANY DE PERE, WI As of: June 28, 2012 Issued: August 23, 2012 BUREAU OF MARKET ACTIONS LIFE AND

CHAPTER 267. BE IT ENACTED by the Senate and General Assembly of the State of New Jersey:

CHAPTER 267 AN ACT concerning third party administrators of health benefits plans and third party billing services and supplementing Title 17B of the New Jersey Statutes. BE IT ENACTED by the Senate and

CHAPTER 267 AN ACT concerning third party administrators of health benefits plans and third party billing services and supplementing Title 17B of the New Jersey Statutes. BE IT ENACTED by the Senate and

FINAL ORDER EFFECTIVE: 10-24-12

BEFORE THE COMMISSIONER OF INSURANCE -12 OF THE STATE OF KANSAS FINAL ORDER EFFECTIVE: 10-24-12 In the Matter of ) LINCOLN HERITAGE LIFE INSURANCE COMPANY ) Docket No. NAIC#65927 ) ) CONSENT AGREEMENT

BEFORE THE COMMISSIONER OF INSURANCE -12 OF THE STATE OF KANSAS FINAL ORDER EFFECTIVE: 10-24-12 In the Matter of ) LINCOLN HERITAGE LIFE INSURANCE COMPANY ) Docket No. NAIC#65927 ) ) CONSENT AGREEMENT

FAIR CLAIMS SETTLEMENT PRACTICES REGULATIONS CALIFORNIA CODE OF REGULATIONS, TITLE 10, CHAPTER 5 AMEND SUBCHAPTER 7.5 TO READ:

FAIR CLAIMS SETTLEMENT PRACTICES REGULATIONS CALIFORNIA CODE OF REGULATIONS, TITLE 10, CHAPTER 5 AMEND SUBCHAPTER 7.5 TO READ: TABLE OF CONTENTS SUBCHAPTER 7.5 FAIR CLAIMS SETTLEMENT PRACTICES REGULATIONS

FAIR CLAIMS SETTLEMENT PRACTICES REGULATIONS CALIFORNIA CODE OF REGULATIONS, TITLE 10, CHAPTER 5 AMEND SUBCHAPTER 7.5 TO READ: TABLE OF CONTENTS SUBCHAPTER 7.5 FAIR CLAIMS SETTLEMENT PRACTICES REGULATIONS

Molina Healthcare of Ohio, Inc. PO Box 22712 Long Beach, CA 90801

Section 9. Claims As a contracted provider, it is important to understand how the claims process works to avoid delays in processing your claims. The following items are covered in this section for your

Section 9. Claims As a contracted provider, it is important to understand how the claims process works to avoid delays in processing your claims. The following items are covered in this section for your

BUSINESS ASSOCIATE AGREEMENT

BUSINESS ASSOCIATE AGREEMENT THIS BUSINESS ASSOCIATE AGREEMENT ( Agreement ) is entered into by and between (the Covered Entity ), and Iowa State Association of Counties (the Business Associate ). RECITALS

BUSINESS ASSOCIATE AGREEMENT THIS BUSINESS ASSOCIATE AGREEMENT ( Agreement ) is entered into by and between (the Covered Entity ), and Iowa State Association of Counties (the Business Associate ). RECITALS

SUBCHAPTER 11. VIATICAL SETTLEMENTS REGULATION

TITLE 365. CHAPTER 25. LICENSURE OF AGENTS, BAIL BONDSMEN, COMPANIES, PREPAID FUNERAL BENEFITS, AND VIATICAL SETTLEMENTS PROVIDERS AND BROKERS SUBCHAPTER 11. VIATICAL SETTLEMENTS REGULATION 365:25-11-1.