VILLAGE OF CHASE BYLAW NO A Bylaw to Adopt the Village of Chase Financial Plan

|

|

|

- Justina Rich

- 8 years ago

- Views:

Transcription

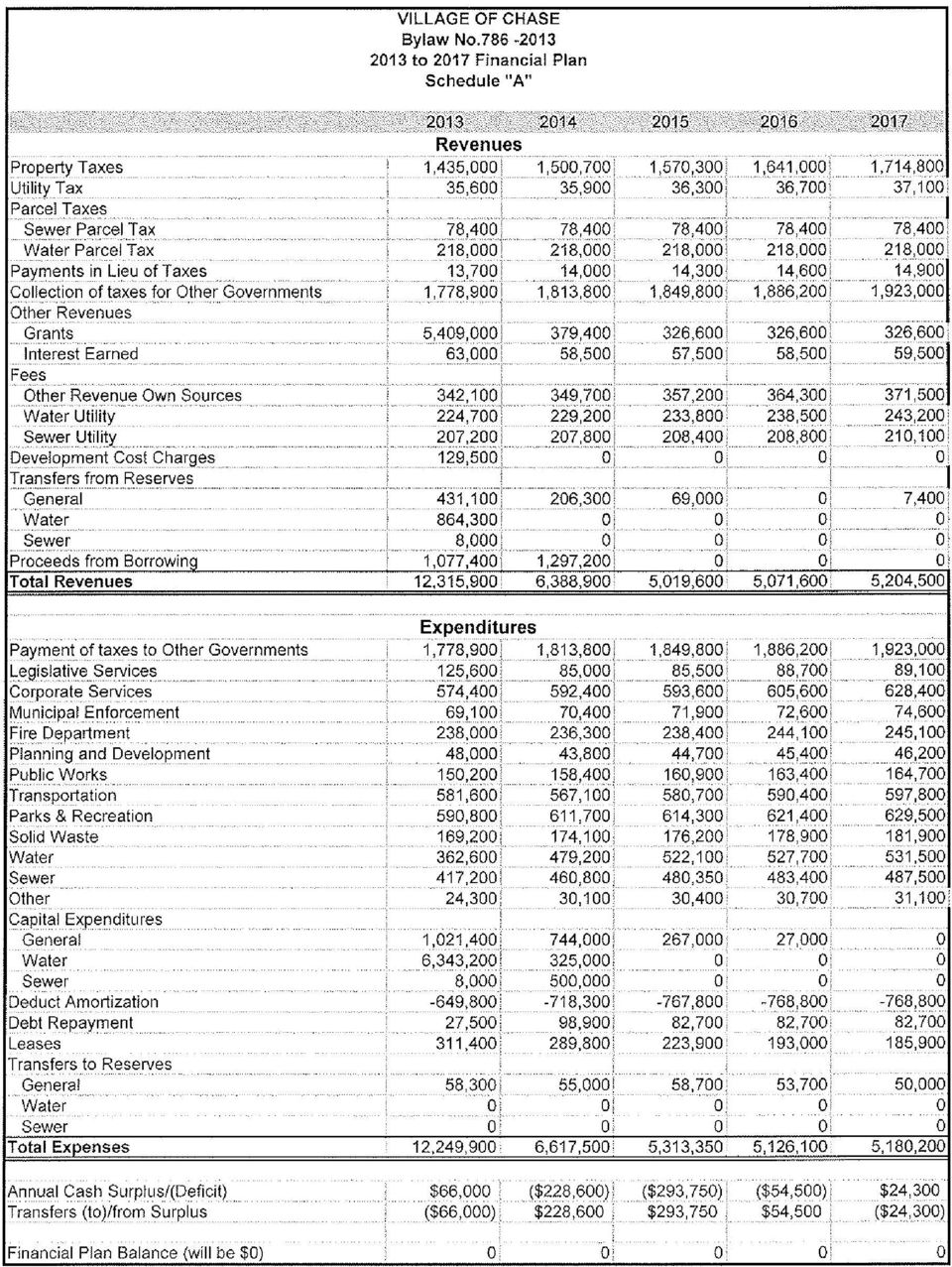

1 VILLAGE OF CHASE BYLAW NO A Bylaw to Adopt the Village of Chase Financial Plan WHEREAS the Community Charter requires that municipalities must establish a five year financial plan that is adopted annually by bylaw; NOW THEREFORE the Council of the Village of Chase, in the Province of British Columbia, in an open meeting assembled enacts as follows: 1. Schedule A, Village of Chase 2013 to 2017 Financial Plan and Schedule B, Statement of s and Policies, attached hereto, shall form part of this Bylaw and are hereby adopted as the Five Year Financial Plan for the Village of Chase for the years 2013 to 2017 inclusive 2. This Bylaw may be cited as Village of Chase 2013 to 2017 Five Year Financial Plan Bylaw No READ A FIRST TIME THIS 7 th DAY OF MAY, 2013 READ A SECOND TIME THIS 7 th DAY OF MAY, 2013 READ A THIRD TIME THIS 7 th DAY OF MAY, 2013 ADOPTED THIS 14 th DAY OF MAY, 2013 X Mayor, R. Anderson X Corporate Officer, L. Randle

2

3 Village of Chase Bylaw No to 2017 Financial Plan Schedule B Statement of s and Policies In accordance with Section 165(3.1) of the Community Charter, the Five Year Financial Plan must include objectives and policies regarding each of the following: 1. The proportion of total revenue that comes from the following funding sources described in Section 165(7) of the Community Charter: (a) revenue from property value taxes; (b) revenue from parcel taxes; (c) revenue from fees; (d) revenue from other sources; (e) proceeds from borrowing. 2. The distribution of property taxes among the property classes, and 3. The use of permissive tax exemptions. FUNDING SOURCES Table 1 shows the proportion of total revenue proposed to be raised from each funding source in In 2013, grants, included in the Other Sources line in Table 1, form the greatest proportion of revenue for the Village. Chase has been very fortunate to secure over 4.5 million dollars from the Canada British Columbia Building Canada Fund which will pay for two-thirds of the new Water Treatment Plant. Construction of the plant was delayed from 2012 and is proceeding in Property taxation, the second largest revenue source, offers a stable and reliable source of revenue for services that are difficult or undesirable to fund on a user-pay basis. These include services such as maintenance of streets, sidewalks, and parks, general administration, fire protection, bylaw enforcement, and snow removal. Borrowing forms the third largest portion of planned source of funds. Borrowing has been necessary to fund part of the Village s one-third share in the cost of the new Water Treatment Plant. Two million dollars will be borrowed, to be paid back over the next 25 years. With a life expectancy of forty to fifty years for the water treatment plant, funding in this manner is justifiable. Other borrowings will be for five year leases for equipment. Over the next five years, the Village will increase the proportion of revenue that is received from user fees and charges until the fees and charges more closely meet the costs incurred to provide the services.

revenue from fees; (d) revenue from other sources; (e) proceeds from borrowing. 2. The distribution of property taxes among the property classes, and 3.")

4 Policies Where possible, the Village will supplement revenues from user fees and charges, rather than taxation, to lessen the burden on its limited, primarily residential, property tax base. Based on the above statement, the Village will be reviewing and revising user fees to ensure that they are adequately meeting both the capital and operating costs of the services for which they are collected. A billing process for metered water usage is planned for implementation in early At this time, sample bills with anticipated metered rates will be included with the normal utility bills as soon as the bugs have been worked out of the system. It is anticipated that actual metered billings will be implemented in early Sewer fees will be reviewed and adjusted. Table Revenue Sources Revenue Source Amount Percentage of Total Property Taxes 1,435, Parcel Taxes 296,400 4 Fees 774,000 7 Other Sources 5,650, Borrowing 1,077, Total 9,233, DISTRIBUTION OF PROPERTY TAX RATES Table 2 outlines the distribution of property tax rates among the property classes. The residential property class provides the largest proportion of property tax revenue. This is appropriate as this class forms the largest proportion of the assessment base and consumes the majority of Village services. Our only Major Industry class, Adams Lake Lumber, is exempted from any Village of Chase property tax rate increases, as the Letters Patent by which their property was incorporated into the Village of Chase requires that the tax rate to be used is set by the provincial Taxation (Rural Area) Act Regulation. The Utility class is also determined by the province under that same regulation and we are already using the maximum tax rate allowed and therefore it cannot change. The amount of taxes to be collected from the Residential, Business and Other, Recreation/Non-Profit and Farm classes will increase by about 4% per year. This will be reviewed as user fees are implemented to offset property taxes. Policies The Village will supplement its revenues from user fees and charges to keep property tax increases to a minimum. The Village will continue to maintain and encourage economic development initiatives designed to attract more retail and commercial businesses to invest in the community and create new jobs. The Village will regularly review the tax rates and revenues relative to the expenses incurred within each property class.

5 Table 2 - Distribution of Property Taxes Property Classification % of Total Property Taxation Value Residential (1) 73.68% 1,039,214 Utilities (2) 2.02% 28,422 Major Industry (4) 9.08% 128,065 Business and Other (6) 15.08% 212,738 Recreation / Non-Profit (8) 0.06% 908 Farm (9) 0.08% 1074 Total All Sources % 1,410,421 PERMISSIVE TAX EXEMPTIONS The Village has established past practice to guide decision making for permissive tax exemptions, but has no specific policy. Council considers the following criteria before granting permissive tax exemptions: The tax exemption must demonstrate benefit to the community and residents of the Village by enhancing the quality of life economically, socially and/or culturally. The goals, policies and principles of the organization receiving the exemption must be consistent with those of the Village. The organization receiving the exemption must be a registered non-profit organization or government institution. Permissive tax exemptions will be considered in conjunction with: (a) Other assistance being provided by the Village; (b) The potential demand for Village services or infrastructure arising from the property; and (c) The amount of revenue that the Village will lose if the exemption is granted. The Village will continue to provide permissive tax exemptions to non-profit societies, agencies and government institutions providing services to the community. The Village will consider additional permissive tax exemptions as allowed under the Community Charter. Policies Consider the development of a tax exemption policy detailing the procedures to be used for all permissive tax exemptions.

CITY OF TERRACE BYLAW NO. 2047 2014

CITY OF TERRACE BYLAW NO. 2047 2014 "A BYLAW TO ADOPT THE 2014-2018 FINANCIAL PLAN." WHEREAS pursuant to Section 165 of the Community Charter, being Chapter 26 of the Statutes of British Columbia, 2003,

CITY OF TERRACE BYLAW NO. 2047 2014 "A BYLAW TO ADOPT THE 2014-2018 FINANCIAL PLAN." WHEREAS pursuant to Section 165 of the Community Charter, being Chapter 26 of the Statutes of British Columbia, 2003,

TOWN OF VIEW ROYAL BYLAW NO. 862

TOWN OF VIEW ROYAL BYLAW NO. 862 A BYLAW TO AUTHORIZE THE FINANCIAL PLAN FOR THE YEARS 20132017 The Council of the Town of View Royal, in open meeting assembled, enacts as follows: 1. This Bylaw may be

TOWN OF VIEW ROYAL BYLAW NO. 862 A BYLAW TO AUTHORIZE THE FINANCIAL PLAN FOR THE YEARS 20132017 The Council of the Town of View Royal, in open meeting assembled, enacts as follows: 1. This Bylaw may be

TOWN OF LAKE COWICHAN. A Bylaw respecting the Financial Plan for the Town of Lake Cowichan

TOWN OF LAKE COWICHAN Bylaw No. 943-2014 A Bylaw respecting the Financial Plan for the Town of Lake Cowichan WHEREAS Section 165 of the Community Charter requires a Municipality to prepare and adopt, a

TOWN OF LAKE COWICHAN Bylaw No. 943-2014 A Bylaw respecting the Financial Plan for the Town of Lake Cowichan WHEREAS Section 165 of the Community Charter requires a Municipality to prepare and adopt, a

CITY OF SURREY BY-LAW NO. 16828. A by-law to provide for the adoption of the Surrey 2009 2013 Consolidated Financial Plan.

CITY OF SURREY BY-LAW NO. 16828 A by-law to provide for the adoption of the Surrey 2009 2013 Consolidated Financial Plan. WHEREAS pursuant to Section 165 of the Community Charter being Chapter 26 of the

CITY OF SURREY BY-LAW NO. 16828 A by-law to provide for the adoption of the Surrey 2009 2013 Consolidated Financial Plan. WHEREAS pursuant to Section 165 of the Community Charter being Chapter 26 of the

FIVE YEAR FINANCIAL PLAN BYLAW, 2015 BYLAW NO. 15-025

FIVE YEAR FINANCIAL PLAN BYLAW, 2015 BYLAW NO. 15-025 This consolidation is a copy of a bylaw consolidated under the authority of section 139 of the Community Charter. (Consolidated on September 1, 2015

FIVE YEAR FINANCIAL PLAN BYLAW, 2015 BYLAW NO. 15-025 This consolidation is a copy of a bylaw consolidated under the authority of section 139 of the Community Charter. (Consolidated on September 1, 2015

5 YEAR FINANCIAL PLAN (2013-2017)

") CITY OF RICHMOND 5 YEAR FINANCIAL PLAN (2013-2017) BYLAW NO. 8990 EFFECTIVE DATE February 25, 2013 - 2 - Bylaw 8990 5 Year Financial Plan (2013-2017) The Council of the City of Richmond enacts as follows:

CITY OF RICHMOND 5 YEAR FINANCIAL PLAN (2013-2017) BYLAW NO. 8990 EFFECTIVE DATE February 25, 2013 - 2 - Bylaw 8990 5 Year Financial Plan (2013-2017) The Council of the City of Richmond enacts as follows:

CITY OF PRINCE RUPERT 2014 FIVE YEAR FINANCIAL PLAN BYLAW NO. 3345, 2014

CITY OF PRINCE RUPERT 2014 FIVE YEAR FINANCIAL PLAN BYLAW NO. 3345, 2014 A BYLAW FOR THE CITY OF PRINCE RUPERT RESPECTING THE FIVE YEAR FINANCIAL PLAN FOR THE PERIOD 2014-2018 The Council of the City of

CITY OF PRINCE RUPERT 2014 FIVE YEAR FINANCIAL PLAN BYLAW NO. 3345, 2014 A BYLAW FOR THE CITY OF PRINCE RUPERT RESPECTING THE FIVE YEAR FINANCIAL PLAN FOR THE PERIOD 2014-2018 The Council of the City of

5 YEAR FINANCIAL PLAN (2015-2019)

") BYLAW NO. 9220 EFFECTIVE DATE April 13, 2015 CONSOLIDATED FOR CONVENIENCE ONLY This is a consolidation of the bylaws listed below. The amendment bylaws have been combined with the original bylaw for convenience

BYLAW NO. 9220 EFFECTIVE DATE April 13, 2015 CONSOLIDATED FOR CONVENIENCE ONLY This is a consolidation of the bylaws listed below. The amendment bylaws have been combined with the original bylaw for convenience

DISTRICT OF KITIMAT 2012 FINANCIAL PLAN, BYLAW NO. 1799 Appendix A, Financial Plan for the Five-Year Period 2012-2016

DISTRICT OF KITIMAT 2012 FINANCIAL PLAN, BYLAW NO. 1799 Appendix A, Financial Plan for the Five-Year Period 2012-2016 2012 2013 2014 2015 2016 Revenues Taxation and Grants in Lieu -20 615 983-21 543 702-22

DISTRICT OF KITIMAT 2012 FINANCIAL PLAN, BYLAW NO. 1799 Appendix A, Financial Plan for the Five-Year Period 2012-2016 2012 2013 2014 2015 2016 Revenues Taxation and Grants in Lieu -20 615 983-21 543 702-22

THE CORPORATION OF THE CITY OF PORT COQUITLAM BYLAW NO. 3899

THE CORPORATION OF THE CITY OF PORT COQUITLAM BYLAW NO. A Bylaw to adopt the 2015 to 2019 Financial Plan Whereas the Community Charter, Section 165, directs that a Five Year Financial Plan may be amended

THE CORPORATION OF THE CITY OF PORT COQUITLAM BYLAW NO. A Bylaw to adopt the 2015 to 2019 Financial Plan Whereas the Community Charter, Section 165, directs that a Five Year Financial Plan may be amended

Council will attempt to increase the proportion of Town revenue that is derived from sources other than property taxes.

The Community Charter requires certain information to be presented as part of the Five Year Financial Plan. The following Section citations reference the Community Charter: 1) Portion of Funding from Revenue

The Community Charter requires certain information to be presented as part of the Five Year Financial Plan. The following Section citations reference the Community Charter: 1) Portion of Funding from Revenue

CITY OF KELOWNA BYLAW NO. 10515

SUMMARY: The Development Cost Charge Bylaw sets out the charges imposed for roads, water, sanitary sewer, drainage and public park when subdividing or constructing, altering or extending a building, pursuant

SUMMARY: The Development Cost Charge Bylaw sets out the charges imposed for roads, water, sanitary sewer, drainage and public park when subdividing or constructing, altering or extending a building, pursuant

Contributed by the Municipal Finance Authority of British Columbia

Capital Financing Contributed by the Municipal Finance Authority of British Columbia Responsibility The Municipal Finance Authority of British Columbia (MFA) was established in 1970 by the Municipal Finance

Capital Financing Contributed by the Municipal Finance Authority of British Columbia Responsibility The Municipal Finance Authority of British Columbia (MFA) was established in 1970 by the Municipal Finance

Vicken municipality - $1.2 Billion Dollar Tax Rebate

Village of Fruitvale 5 Year Financial Plan What is a Financial Plan Required under the Community Charter Future planning for works and services Maintaining current service levels Consider future service

Village of Fruitvale 5 Year Financial Plan What is a Financial Plan Required under the Community Charter Future planning for works and services Maintaining current service levels Consider future service

2011-2015 Five-Year Financial Plan Public Consultation and Information Package

2011-2015 Five-Year Financial Plan Public Consultation and Information Package Community Charter s.166: A council must undertake a process of public consultation regarding the proposed financial plan before

2011-2015 Five-Year Financial Plan Public Consultation and Information Package Community Charter s.166: A council must undertake a process of public consultation regarding the proposed financial plan before

PUBLIC NOTICE OF INTENT. Bylaw No. 7-2015 A BYLAW FOR ESTABLISHING A DEVELOPMENT LEVY FOR LANDS THAT ARE TO BE DEVELOPED OR REDEVELOPED WITHIN THE

PUBLIC NOTICE OF INTENT Bylaw No. 7-2015 A BYLAW FOR ESTABLISHING A DEVELOPMENT LEVY FOR LANDS THAT ARE TO BE DEVELOPED OR REDEVELOPED WITHIN THE DISTRICT OF LAKELAND No. 521 Public notice is hereby given

PUBLIC NOTICE OF INTENT Bylaw No. 7-2015 A BYLAW FOR ESTABLISHING A DEVELOPMENT LEVY FOR LANDS THAT ARE TO BE DEVELOPED OR REDEVELOPED WITHIN THE DISTRICT OF LAKELAND No. 521 Public notice is hereby given

2. Downtown Revitalization Tax Exemption Program Summary

SUMMARY Downtown Revitalization Tax Exemption Program 1. Revitalization Tax Exemptions Under the provisions of section 226 of the Community Charter a revitalization tax exemption program may be established

SUMMARY Downtown Revitalization Tax Exemption Program 1. Revitalization Tax Exemptions Under the provisions of section 226 of the Community Charter a revitalization tax exemption program may be established

THE CORPORATION OF THE COUNTY OF SIMCOE. A By-law to Provide for a Tax Rebate Program for Eligible Charities and Similar Organizations.

BY-LAW NO. 6104 OF THE CORPORATION OF THE COUNTY OF SIMCOE A By-law to Provide for a Tax Rebate Program for Eligible Charities and Similar Organizations. WHEREAS the Municipal Act, SO. 2001, c.25, Section

BY-LAW NO. 6104 OF THE CORPORATION OF THE COUNTY OF SIMCOE A By-law to Provide for a Tax Rebate Program for Eligible Charities and Similar Organizations. WHEREAS the Municipal Act, SO. 2001, c.25, Section

BYLAW 3526 Revitalization Tax Exemption Bylaw

Contents BYLAW 3526 Revitalization Tax Exemption Bylaw Section 1 Definitions 2 Rationale 3 Program establishment 4 Eligible property 5 Extent of tax exemption 6 Amount of tax exemption 7 Term of tax exemption

Contents BYLAW 3526 Revitalization Tax Exemption Bylaw Section 1 Definitions 2 Rationale 3 Program establishment 4 Eligible property 5 Extent of tax exemption 6 Amount of tax exemption 7 Term of tax exemption

Municipal Revenue Sources Review An Analysis of Tax Policy Objectives

Municipal Revenue Sources Review An Analysis of Policy Objectives August, 2012 Introduction This paper reviews the financial plan bylaws of select communities across the Province of British Columbia (Province).

Municipal Revenue Sources Review An Analysis of Policy Objectives August, 2012 Introduction This paper reviews the financial plan bylaws of select communities across the Province of British Columbia (Province).

City of Chilliwack. Bylaw No. 3747. A bylaw to regulate the use of security and fire alarm systems

City of Chilliwack Bylaw No. 3747 A bylaw to regulate the use of security and fire alarm systems WHEREAS Section 196(1) of the Community Charter, S.B.C. 2003, c. 26 (the Community Charter ) provides that

City of Chilliwack Bylaw No. 3747 A bylaw to regulate the use of security and fire alarm systems WHEREAS Section 196(1) of the Community Charter, S.B.C. 2003, c. 26 (the Community Charter ) provides that

THE CORPORATION OF THE VILLAGE OF WARFIELD BYLAW #643

THE CORPORATION OF THE VILLAGE OF WARFIELD A BYLAW TO REGULATE AND LICENSE BUSINESS WHEREAS Part 20 of the LOCAL GOVERNMENT ACT (RS Chapter 323) authorizes the Council of the Village of Warfield to regulate

THE CORPORATION OF THE VILLAGE OF WARFIELD A BYLAW TO REGULATE AND LICENSE BUSINESS WHEREAS Part 20 of the LOCAL GOVERNMENT ACT (RS Chapter 323) authorizes the Council of the Village of Warfield to regulate

REPORT FOR CONSIDERATION

Main Office: 155 George Street, Prince George, BC V2L 1P8 Telephone: (250) 960-4400 / Fax: (250) 563-7520 Toll Free: 1-800-667-1959 / http://www.rdffg.bc.ca REPORT FOR CONSIDERATION TO: Chairman and Directors

Main Office: 155 George Street, Prince George, BC V2L 1P8 Telephone: (250) 960-4400 / Fax: (250) 563-7520 Toll Free: 1-800-667-1959 / http://www.rdffg.bc.ca REPORT FOR CONSIDERATION TO: Chairman and Directors

BYLAW 187-03 OF ALBERTA BEACH IN THE PROVINCE OF ALBERTA

OF ALBERTA BEACH IN THE PROVINCE OF ALBERTA BEING A BYLAW OF ALBERTA BEACH, IN THE PROVINCE OF ALBERTA, TO REGULATE AND CONTROL THE OPERATION OF ALL OFF-HIGHWAY VEHICLES WITHIN THE BOUNDARIES OF ALBERTA

OF ALBERTA BEACH IN THE PROVINCE OF ALBERTA BEING A BYLAW OF ALBERTA BEACH, IN THE PROVINCE OF ALBERTA, TO REGULATE AND CONTROL THE OPERATION OF ALL OFF-HIGHWAY VEHICLES WITHIN THE BOUNDARIES OF ALBERTA

THE CORPORATION OF THE MUNICIPALITY OF POWASSAN BY-LAW NO. 2006-05

THE CORPORATION OF THE MUNICIPALITY OF POWASSAN BY-LAW NO. 2006-05 BEING A BY-LAW TO ESTABLISH A TAX REBATE PROGRAM FOR THE PURPOSES OF PROVIDING RELIEF FROM TAXES OR AMOUNTS PAID ON ACCOUNT OF TAXES ON

THE CORPORATION OF THE MUNICIPALITY OF POWASSAN BY-LAW NO. 2006-05 BEING A BY-LAW TO ESTABLISH A TAX REBATE PROGRAM FOR THE PURPOSES OF PROVIDING RELIEF FROM TAXES OR AMOUNTS PAID ON ACCOUNT OF TAXES ON

How To Write An Annual Budget For Town Of Golden

2013 Proposed Annual Budget (2013-2017 Five-Year Financial Plan) Public Consultation and Information Package We Want Your Opinion! Building the Annual Budget A Summary How we Build the Annual Budget (Financial

2013 Proposed Annual Budget (2013-2017 Five-Year Financial Plan) Public Consultation and Information Package We Want Your Opinion! Building the Annual Budget A Summary How we Build the Annual Budget (Financial

The Corporation of the Municipality of West Grey By-law Number 50-2015

The Corporation of the Municipality of West Grey By-law Number 50-2015 Being, A by-law to approve and authorize the execution of an Agreement between the Municipality of West Grey and Gemini Canada Ltd.,

The Corporation of the Municipality of West Grey By-law Number 50-2015 Being, A by-law to approve and authorize the execution of an Agreement between the Municipality of West Grey and Gemini Canada Ltd.,

BYLAW NO. 3650 Being a bylaw to exempt from taxation certain lands and improvements for the years 2008, 2009 and 2010

CITY OF SALMON ARM BYLAW NO. 3650 Being a bylaw to exempt from taxation certain lands and improvements for the years 2008, 2009 and 2010 WHEREAS it is provided by Section 224 of the Community Charter,

CITY OF SALMON ARM BYLAW NO. 3650 Being a bylaw to exempt from taxation certain lands and improvements for the years 2008, 2009 and 2010 WHEREAS it is provided by Section 224 of the Community Charter,

City of Vernon REVITALIZATION TAX EXEMPTION BYLAW (CITY CENTRE DISTRICT) BYLAW #5362

BYLAW #5362") City of Vernon REVITALIZATION TAX EXEMPTION BYLAW (CITY CENTRE DISTRICT) BYLAW #5362 THE CORPORATION OF THE CITY OF VERNON BYLAW NUMBER 5363 AMENDMENTS BYLAW NO. ADOPTION AMENDMENT 5515 September 8, 2014

City of Vernon REVITALIZATION TAX EXEMPTION BYLAW (CITY CENTRE DISTRICT) BYLAW #5362 THE CORPORATION OF THE CITY OF VERNON BYLAW NUMBER 5363 AMENDMENTS BYLAW NO. ADOPTION AMENDMENT 5515 September 8, 2014

Financial Statement Guide. A Guide to Local Government Financial Statements

Financial Statement Guide A Guide to Local Government Financial Statements January, 2012 Ministry of Community, Sport and 1 Financial Statement Guide Table of Contents Introduction Legislative Requirements

Financial Statement Guide A Guide to Local Government Financial Statements January, 2012 Ministry of Community, Sport and 1 Financial Statement Guide Table of Contents Introduction Legislative Requirements

Property Tax Collection By-law

Property Tax Collection By-law A-8 Consolidated November 10, 2015 In Force and Effect January 1, 2016 This by-law is printed under and by authority of the Council of the City of London, Ontario, Canada

Property Tax Collection By-law A-8 Consolidated November 10, 2015 In Force and Effect January 1, 2016 This by-law is printed under and by authority of the Council of the City of London, Ontario, Canada

THE CORPORATION OF THE CITY OF PORT COQUITLAM BYLAW NO. 3889

THE CORPORATION OF THE CITY OF PORT COQUITLAM BYLAW NO. A Bylaw to establish rates and charges for the use of the City of Port Coquitlam Sanitary Sewerage System The Municipal Council of The Corporation

THE CORPORATION OF THE CITY OF PORT COQUITLAM BYLAW NO. A Bylaw to establish rates and charges for the use of the City of Port Coquitlam Sanitary Sewerage System The Municipal Council of The Corporation

FLOOD PLAIN DESIGNATION AND PROTECTION

CITY OF RICHMOND FLOOD PLAIN DESIGNATION AND PROTECTION BYLAW NO. 8204 EFFECTIVE DATE - SEPTEMBER 8, 2008 CONSOLIDATED FOR CONVENIENCE ONLY This is a consolidation of the bylaws listed below. The amendment

CITY OF RICHMOND FLOOD PLAIN DESIGNATION AND PROTECTION BYLAW NO. 8204 EFFECTIVE DATE - SEPTEMBER 8, 2008 CONSOLIDATED FOR CONVENIENCE ONLY This is a consolidation of the bylaws listed below. The amendment

THE CORPORATION OF THE CITY OF MISSISSAUGA BY-LAW 121-15

THE CORPORATION OF THE CITY OF MISSISSAUGA BY-LAW 121-15 Establish Tax Ratios to Levy Residential, Commercial, Industrial, Multi-Residential, Pipeline, Farmland, Managed Forests, Public Hospitals, Universities

THE CORPORATION OF THE CITY OF MISSISSAUGA BY-LAW 121-15 Establish Tax Ratios to Levy Residential, Commercial, Industrial, Multi-Residential, Pipeline, Farmland, Managed Forests, Public Hospitals, Universities

FINANCIAL PLAN 2014-2018

City of Kamloops FINANCIAL PLAN 2014-2018 Financial Planning Process at a Glance The following schedule provides the dates for the Financial Plan process. July-September 2013 Budget preparation guidelines

City of Kamloops FINANCIAL PLAN 2014-2018 Financial Planning Process at a Glance The following schedule provides the dates for the Financial Plan process. July-September 2013 Budget preparation guidelines

Sewer System Charges By-law

Sewer System Charges By-law WM-15 Consolidated October 09, 2012 This by-law is printed under and by authority of the Council of the City of London, Ontario, Canada Disclaimer: The following consolidation

Sewer System Charges By-law WM-15 Consolidated October 09, 2012 This by-law is printed under and by authority of the Council of the City of London, Ontario, Canada Disclaimer: The following consolidation

THE TOWN OF LAKE COWICHAN BYLAW NO. 934-2013

THE TOWN OF LAKE COWICHAN BYLAW NO. 934-2013 A BYLAW TO ESTABLISH A SCHEME FOR INTER-COMMUNITY LICENCING AND REGULATING OF TRADES, OCCUPATIONS AND BUSINESSES. WHEREAS Council may, pursuant to Section 8(6)

THE TOWN OF LAKE COWICHAN BYLAW NO. 934-2013 A BYLAW TO ESTABLISH A SCHEME FOR INTER-COMMUNITY LICENCING AND REGULATING OF TRADES, OCCUPATIONS AND BUSINESSES. WHEREAS Council may, pursuant to Section 8(6)

CITY OF KINGSTON. Ontario

CITY OF KINGSTON Ontario BY-LAW NO. 2010-17 A BY-LAW TO IMPOSE GAS RATES (1425445 Ontario Limited operating as Utilities Kingston) PASSED: December 15, 2009 UPDATED TO: February 4, 2015 As Amended By:

CITY OF KINGSTON Ontario BY-LAW NO. 2010-17 A BY-LAW TO IMPOSE GAS RATES (1425445 Ontario Limited operating as Utilities Kingston) PASSED: December 15, 2009 UPDATED TO: February 4, 2015 As Amended By:

The Corporation of the City of Nelson

The Corporation of the City of Nelson Agenda 1. Introduction 2. Council Priorities & Strategic Direction 3. 2012 2016 Financial Plan Process 4. Proposed 2012 2016 Financial Plan Presentation 5. City Assets/Reserves/Debt

The Corporation of the City of Nelson Agenda 1. Introduction 2. Council Priorities & Strategic Direction 3. 2012 2016 Financial Plan Process 4. Proposed 2012 2016 Financial Plan Presentation 5. City Assets/Reserves/Debt

TOWN OF COMOX BYLAW NO. 1721 A BYLAW TO REGULATE THE DISCHARGE OF FIREWORKS IN THE TOWN OF COMOX

TOWN OF COMOX BYLAW NO. 1721 A BYLAW TO REGULATE THE DISCHARGE OF FIREWORKS IN THE TOWN OF COMOX In open meeting assembled the Council of the Town of Comox enacts as follows: 1. Title This Bylaw may be

TOWN OF COMOX BYLAW NO. 1721 A BYLAW TO REGULATE THE DISCHARGE OF FIREWORKS IN THE TOWN OF COMOX In open meeting assembled the Council of the Town of Comox enacts as follows: 1. Title This Bylaw may be

Consolidated for Convenience Only

CITY OF KAMLOOPS Consolidated for Convenience Only This is a consolidation of "City of Kamloops Tree Protection By-law No. 24-35, 1998". The amendment by-law listed below has been combined with the original

CITY OF KAMLOOPS Consolidated for Convenience Only This is a consolidation of "City of Kamloops Tree Protection By-law No. 24-35, 1998". The amendment by-law listed below has been combined with the original

BILL 5 THE CORPORATION OF THE TOWNSHIP OF ADJALA-TOSORONTIO BY-LAW NO. 15-

BILL 5 THE CORPORATION OF THE TOWNSHIP OF ADJALA-TOSORONTIO BY-LAW NO. 15- A BY-LAW TO ESTABLISH MUNICIPAL RATES AND TAX RATIOS FOR THE YEAR 2015 AND TO PROVIDE FOR THE COLLECTION OF INTEREST 2015 Final

BILL 5 THE CORPORATION OF THE TOWNSHIP OF ADJALA-TOSORONTIO BY-LAW NO. 15- A BY-LAW TO ESTABLISH MUNICIPAL RATES AND TAX RATIOS FOR THE YEAR 2015 AND TO PROVIDE FOR THE COLLECTION OF INTEREST 2015 Final

BYLAW 11-10 BEING A BYLAW OF THE TOWN OF OKOTOKS IN THE PROVINCE OF ALBERTA FOR THE PURPOSE OF REDUCING FALSE ALARMS

BYLAW 11-10 BEING A BYLAW OF THE TOWN OF OKOTOKS IN THE PROVINCE OF ALBERTA FOR THE PURPOSE OF REDUCING FALSE ALARMS WHEREAS the Municipal Government Act RSA 2000, M -26 and regulations as amended, provides

BYLAW 11-10 BEING A BYLAW OF THE TOWN OF OKOTOKS IN THE PROVINCE OF ALBERTA FOR THE PURPOSE OF REDUCING FALSE ALARMS WHEREAS the Municipal Government Act RSA 2000, M -26 and regulations as amended, provides

THE CITY OF YELLOWKNIFE

THE CITY OF YELLOWKNIFE NORTHWEST TERRITORIES CONSOLIDATION OF TAX ADMINISTRATION BY-LAW NO. 4207 Adopted June 24, 2002 AS AMENDED BY By-law No. 4246 - February 10, 2003 By-law No. 4303 March 22, 2004

THE CITY OF YELLOWKNIFE NORTHWEST TERRITORIES CONSOLIDATION OF TAX ADMINISTRATION BY-LAW NO. 4207 Adopted June 24, 2002 AS AMENDED BY By-law No. 4246 - February 10, 2003 By-law No. 4303 March 22, 2004

Financing Mechanisms and Financial Incentives

2 Best Practices for Sustainable Wind Energy Development in the Great Lakes Region Great Lakes Wind Collaborative Best Practice #2 High energy prices can act as a driver for creating and enhancing wind

2 Best Practices for Sustainable Wind Energy Development in the Great Lakes Region Great Lakes Wind Collaborative Best Practice #2 High energy prices can act as a driver for creating and enhancing wind

Presentation of DISTRICT OF HOUSTON. 2010 TO 2014 Financial Plan

Presentation of DISTRICT OF HOUSTON 2010 TO 2014 Financial Plan What is a Financial Plan? Why? 1) Prudent Planning! 2) Legal Requirement, Community Charter (s165 & s166) First year of the plan is the budget

Presentation of DISTRICT OF HOUSTON 2010 TO 2014 Financial Plan What is a Financial Plan? Why? 1) Prudent Planning! 2) Legal Requirement, Community Charter (s165 & s166) First year of the plan is the budget

Municipal Affairs. Property Tax: Adding Amounts to the Tax Roll

Municipal Affairs Property Tax: Adding Amounts to the Tax Roll Revised May 2013 Introduction This summary has been prepared by Alberta Municipal Affairs as a reference document. It outlines the various

Municipal Affairs Property Tax: Adding Amounts to the Tax Roll Revised May 2013 Introduction This summary has been prepared by Alberta Municipal Affairs as a reference document. It outlines the various

Corporate. Report COUNCIL DATE: Nov. 30, 1998 NO: R1706 REGULAR COUNCIL. TO: Mayor & Council DATE: November 12, 1998

R1706 : Industrial & Commercial Utility Rates Corporate NO: R1706 Report COUNCIL DATE: Nov. 30, 1998 REGULAR COUNCIL TO: Mayor & Council DATE: November 12, 1998 FROM: Acting General Manager, Engineering

R1706 : Industrial & Commercial Utility Rates Corporate NO: R1706 Report COUNCIL DATE: Nov. 30, 1998 REGULAR COUNCIL TO: Mayor & Council DATE: November 12, 1998 FROM: Acting General Manager, Engineering

Bylaw No. 6673. A bylaw of The City of Saskatoon to provide for the payment of taxes and the application of discounts and penalties thereto.

Bylaw No. 6673 A bylaw of The City of Saskatoon to provide for the payment of taxes and the application of discounts and penalties thereto. Codified to Bylaw No. 9046 (August 15, 2012) BYLAW NO. 6673 A

Bylaw No. 6673 A bylaw of The City of Saskatoon to provide for the payment of taxes and the application of discounts and penalties thereto. Codified to Bylaw No. 9046 (August 15, 2012) BYLAW NO. 6673 A

Finance and Budget Department

Finance and Budget Department SUBJECT: Resolution authorizing the city to enter into a lease purchase agreement with Chase Equipment Leasing Inc., for the purchase of two fire trucks. MEETING DATE: December

Finance and Budget Department SUBJECT: Resolution authorizing the city to enter into a lease purchase agreement with Chase Equipment Leasing Inc., for the purchase of two fire trucks. MEETING DATE: December

Revitalization Tax Exemptions. A Primer on the Provisions in the Community Charter

Revitalization Tax Exemptions A Primer on the Provisions in the Community Charter January 2008 REVITALIZATION TAX EXEMPTIONS Legislation Section 226 of the Community Charter provides authority to exempt

Revitalization Tax Exemptions A Primer on the Provisions in the Community Charter January 2008 REVITALIZATION TAX EXEMPTIONS Legislation Section 226 of the Community Charter provides authority to exempt

City of Salmon Arm. Controlled Substance - Safe Premises Bylaw No. 3601

City of Salmon Arm Controlled Substance - Safe Premises Bylaw No. 3601 : City of Salmon Arm Controlled Substance - Safe Premises Bylaw No. 3601 Table of Contents Page # Part 1 Citation... 1 Part 2 Severability...

City of Salmon Arm Controlled Substance - Safe Premises Bylaw No. 3601 : City of Salmon Arm Controlled Substance - Safe Premises Bylaw No. 3601 Table of Contents Page # Part 1 Citation... 1 Part 2 Severability...

REQUEST FOR TAX REBATE FOR REGISTERED CHARITABLE ORGANIZATIONS

County of Brant 519-449-2451 Fax: 519-449-2454 1-888-250-2297 www.brant.ca Taxation Division 26 Park Ave P.O. Box 160 Burford ON, N0E 1A0 REQUEST FOR TAX REBATE FOR REGISTERED CHARITABLE ORGANIZATIONS

County of Brant 519-449-2451 Fax: 519-449-2454 1-888-250-2297 www.brant.ca Taxation Division 26 Park Ave P.O. Box 160 Burford ON, N0E 1A0 REQUEST FOR TAX REBATE FOR REGISTERED CHARITABLE ORGANIZATIONS

Town of Creston. Bylaw No. 1813

Town of Creston Bylaw No. 1813 A Bylaw relating to the care and maintenance of private property and adjoining public places within the Town of Creston. WHEREAS Sections 62 and 64 of the Community Charter

Town of Creston Bylaw No. 1813 A Bylaw relating to the care and maintenance of private property and adjoining public places within the Town of Creston. WHEREAS Sections 62 and 64 of the Community Charter

CITY OF SURREY BY-LAW NO. 6569

CITY OF SURREY BY-LAW NO. 6569 As amended by By-laws No. 7026, 02/01/82; 9960, 03/13/90; 10368, 01/22/90; 10797, 01/28/91; 12268, 04/25/94; 12384, 07/02/94; 12828, 05/13/96; 13171, 07/29/97; 13220, 09/22/97;

CITY OF SURREY BY-LAW NO. 6569 As amended by By-laws No. 7026, 02/01/82; 9960, 03/13/90; 10368, 01/22/90; 10797, 01/28/91; 12268, 04/25/94; 12384, 07/02/94; 12828, 05/13/96; 13171, 07/29/97; 13220, 09/22/97;

REGIONAL DISTRICT OF CENTRAL KOOTENAY BYLAW NO. 1851

REGIONAL DISTRICT OF CENTRAL KOOTENAY BYLAW NO. 1851 As Amended by Bylaw No. 1905, 2007 As Amended by Bylaw No. 1956, 2008 As Amended by Bylaw No. 2212, 2011 As Amended by Bylaw No. 2294, 2012 As Amended

REGIONAL DISTRICT OF CENTRAL KOOTENAY BYLAW NO. 1851 As Amended by Bylaw No. 1905, 2007 As Amended by Bylaw No. 1956, 2008 As Amended by Bylaw No. 2212, 2011 As Amended by Bylaw No. 2294, 2012 As Amended

*Local Law Filing New York State Department of State 41 State Street, Albany, NY 12231 (Use this form to file a local law with the Secretary of State.) Text of law should be given as amended. Do not include

*Local Law Filing New York State Department of State 41 State Street, Albany, NY 12231 (Use this form to file a local law with the Secretary of State.) Text of law should be given as amended. Do not include

Last Consolidated: September, 2011

Last Consolidated: September, 2011 Security Alarm System Bylaw Bylaw No. 6358, 1995 CITY OF PRINCE GEORGE BYLAW NO. 6358 A Bylaw to establish fees for services provided in response to a false alarm of

Last Consolidated: September, 2011 Security Alarm System Bylaw Bylaw No. 6358, 1995 CITY OF PRINCE GEORGE BYLAW NO. 6358 A Bylaw to establish fees for services provided in response to a false alarm of

1. That the following principles be adopted in establishing mill rate factors for 2013:

CR13-16 February 19, 2013 To: Re: His Worship the Mayor and Members of City Council 2013 Reassessment Tax Policy RECOMMENDATION OF THE EXECUTIVE COMMITTEE - FEBRUARY 13, 2013 1. That the following principles

CR13-16 February 19, 2013 To: Re: His Worship the Mayor and Members of City Council 2013 Reassessment Tax Policy RECOMMENDATION OF THE EXECUTIVE COMMITTEE - FEBRUARY 13, 2013 1. That the following principles

Cultus Lake Park Board Bylaw No. 1056, 2014 BOATING BYLAW. A Bylaw to regulate boating and boat moorage within the Cultus Lake Park foreshore.

Cultus Lake Park Board Bylaw No. 1056, 2014 BOATING BYLAW Adopted 04/23/2014/ A Bylaw to regulate boating and boat moorage within the Cultus Lake Park foreshore. WHEREAS Section 12 of the Cultus Lake Park

Cultus Lake Park Board Bylaw No. 1056, 2014 BOATING BYLAW Adopted 04/23/2014/ A Bylaw to regulate boating and boat moorage within the Cultus Lake Park foreshore. WHEREAS Section 12 of the Cultus Lake Park

Tuesday, June 14, 2016 2:00 PM

Agenda Arlington City Council Special Meeting Council Briefing Room 101 W. Abram St., 3rd Floor Tuesday, June 14, 2016 2:00 PM I. CALL TO ORDER II. WORK SESSION A. City Council Committees B. Economic Development

Agenda Arlington City Council Special Meeting Council Briefing Room 101 W. Abram St., 3rd Floor Tuesday, June 14, 2016 2:00 PM I. CALL TO ORDER II. WORK SESSION A. City Council Committees B. Economic Development

THE CORPORATION OF THE CITY OF PETERBOROUGH BY-LAW NUMBER 05-004

THE CORPORATION OF THE CITY OF PETERBOROUGH BY-LAW NUMBER 05-004 BEING A BY-LAW TO AUTHORIZE AN AGREEMENT WITH THE GOVERNING COUNCIL OF THE SALVATON ARMY IN CANADA ON BEHALF OF THE SALVATION ARMY COMMUNITY

THE CORPORATION OF THE CITY OF PETERBOROUGH BY-LAW NUMBER 05-004 BEING A BY-LAW TO AUTHORIZE AN AGREEMENT WITH THE GOVERNING COUNCIL OF THE SALVATON ARMY IN CANADA ON BEHALF OF THE SALVATION ARMY COMMUNITY

NO: R176 COUNCIL DATE: July 26, 2010. First Responder Consent and Indemnity Agreement with the Emergency Health Services Commission (EHSC)

") NO: R176 COUNCIL DATE: July 26, 2010 REGULAR COUNCIL TO: Mayor & Council DATE: July 26, 2010 FROM: Fire Chief FILE: 2240-20 SUBJECT: First Responder Consent and Indemnity Agreement with the Emergency Health

NO: R176 COUNCIL DATE: July 26, 2010 REGULAR COUNCIL TO: Mayor & Council DATE: July 26, 2010 FROM: Fire Chief FILE: 2240-20 SUBJECT: First Responder Consent and Indemnity Agreement with the Emergency Health

1. The City accept credit card payments for online property tax and online utility payments as a pilot project effective August 1, 2016.

City of Richmond Report to Committee To: From: General Purposes Committee Jerry Chong Director, Finance Re: Credit Card Payment Service Fee Bylaw No. 9536 Date: March 30, 2016 File: 03-0900-01/2015-Vol

City of Richmond Report to Committee To: From: General Purposes Committee Jerry Chong Director, Finance Re: Credit Card Payment Service Fee Bylaw No. 9536 Date: March 30, 2016 File: 03-0900-01/2015-Vol

The Corporation of the TOWN OF MILTON

Report to: From: Mayor G.A. Krantz and Members of Council Linda Leeds, Director, Corporate Services & Treasurer Date: October 05, 2010 Report No. CORS-079-10 Subject: 2011 Interim by-law for the Monthly

Report to: From: Mayor G.A. Krantz and Members of Council Linda Leeds, Director, Corporate Services & Treasurer Date: October 05, 2010 Report No. CORS-079-10 Subject: 2011 Interim by-law for the Monthly

Glossary. Accounting for expenses and revenues as they are incurred, not when funds are actually disbursed or received (see Cash Basis).

.") Glossary Accrual Basis Accounting for expenses and revenues as they are incurred, not when funds are actually disbursed or received (see Cash Basis). Amalgamation Costs The costs directly associated with

Glossary Accrual Basis Accounting for expenses and revenues as they are incurred, not when funds are actually disbursed or received (see Cash Basis). Amalgamation Costs The costs directly associated with

REPORT TO PLANNING, TRANSPORTATION AND PROTECTIVE SERVICES COMMITTEE MEETING OF WEDNESDAY, MARCH 27, 2013

PPS/HFP 2013-04 REPORT TO PLANNING, TRANSPORTATION AND PROTECTIVE SERVICES COMMITTEE MEETING OF WEDNESDAY, MARCH 27, 2013 SUBJECT 2013 Minor Capital Projects Capital Borrowing Bylaw 158, 2013 ISSUE To

PPS/HFP 2013-04 REPORT TO PLANNING, TRANSPORTATION AND PROTECTIVE SERVICES COMMITTEE MEETING OF WEDNESDAY, MARCH 27, 2013 SUBJECT 2013 Minor Capital Projects Capital Borrowing Bylaw 158, 2013 ISSUE To

162 Washington Avenue, Albany, NY 12231

Local Law Filing New York State Department of State 162 Washington Avenue, Albany, NY 12231 County of Tioga Local Law No. 5 of the Year 1997. A Local Law increasing the rate of taxes on sales and uses

Local Law Filing New York State Department of State 162 Washington Avenue, Albany, NY 12231 County of Tioga Local Law No. 5 of the Year 1997. A Local Law increasing the rate of taxes on sales and uses

THE CORPORATION OF THE CITY OF COURTENAY BYLAW NO. 2182. A bylaw to amend Storm Sewer Bylaw No. 1402, 1986

THE CORPORATION OF THE CITY OF COURTENAY BYLAW NO. 2182 A bylaw to amend Storm Sewer Bylaw No. 1402, 1986 The Council of the Corporation of the City of Courtenay in open meeting assembled enacts as follows:

THE CORPORATION OF THE CITY OF COURTENAY BYLAW NO. 2182 A bylaw to amend Storm Sewer Bylaw No. 1402, 1986 The Council of the Corporation of the City of Courtenay in open meeting assembled enacts as follows:

Quarterly Budget Report

City of Chicago Quarterly Report 3rd Quarter Mayor Rahm Emanuel Quarterly Report-3 rd Quarter Content and Purpose This quarterly report presents an overview of the City s operating revenues and expenditures

City of Chicago Quarterly Report 3rd Quarter Mayor Rahm Emanuel Quarterly Report-3 rd Quarter Content and Purpose This quarterly report presents an overview of the City s operating revenues and expenditures

Glossary of Assessment Terms:

Glossary of Assessment Terms: Abatement A reduction or elimination of a tax or charge imposed by a governmental unit, applicable to property tax bills, motor vehicle excise taxes, fees, charges, and special

Glossary of Assessment Terms: Abatement A reduction or elimination of a tax or charge imposed by a governmental unit, applicable to property tax bills, motor vehicle excise taxes, fees, charges, and special

VILLAGE OF RADIUM HOT SPRINGS Telephone 250-347-6455 Box 340 Facsimile 250-347-9068

VILLAGE OF RADIUM HOT SPRINGS Telephone 250-347-6455 Box 340 Facsimile 250-347-9068 Radium Hot Springs, BC www.radiumhotsprings.ca V0A 1M0 Dear Applicant, RE: Building Permit Applications Pursuant to the

VILLAGE OF RADIUM HOT SPRINGS Telephone 250-347-6455 Box 340 Facsimile 250-347-9068 Radium Hot Springs, BC www.radiumhotsprings.ca V0A 1M0 Dear Applicant, RE: Building Permit Applications Pursuant to the

Property Taxes and Competitiveness in British Columbia

Property Taxes and Competitiveness in British Columbia A report prepared by Harry Kitchen and Enid Slack for the BC Expert Panel on Business Tax Competitiveness May, 22 Table of Contents. Introduction...

Property Taxes and Competitiveness in British Columbia A report prepared by Harry Kitchen and Enid Slack for the BC Expert Panel on Business Tax Competitiveness May, 22 Table of Contents. Introduction...

DISTRICT OF NORTH VANCOUVER GUIDE TO FINANCIAL STATEMENTS

DISTRICT OF NORTH VANCOUVER GUIDE TO FINANCIAL STATEMENTS DISTRICT OF NORTH VANCOUVER Our goal at North Vancouver District is to make information sharing and reporting convenient, accessible and relevant

DISTRICT OF NORTH VANCOUVER GUIDE TO FINANCIAL STATEMENTS DISTRICT OF NORTH VANCOUVER Our goal at North Vancouver District is to make information sharing and reporting convenient, accessible and relevant

Department of Finance Policies and Procedures Reserve Funds Policy # Authorized by: City Council Date of issue: September 30, 2004

Department of Finance Policies and Procedures Reserve Funds Policy # Authorized by: City Council Date of issue: September 30, 2004 Revised: April 2011 Purpose The purpose of the Reserve Fund Policy is

Department of Finance Policies and Procedures Reserve Funds Policy # Authorized by: City Council Date of issue: September 30, 2004 Revised: April 2011 Purpose The purpose of the Reserve Fund Policy is

BYLAW NO. B-22/2010 OF THE CITY OF AIRDRIE IN THE PROVINCE OF ALBERTA

BYLAW NO. B-22/2010 OF THE CITY OF AIRDRIE IN THE PROVINCE OF ALBERTA Being a bylaw to reduce the number of false security alarms responded to by the City of Airdrie s Police Service WHEREAS the Municipal

BYLAW NO. B-22/2010 OF THE CITY OF AIRDRIE IN THE PROVINCE OF ALBERTA Being a bylaw to reduce the number of false security alarms responded to by the City of Airdrie s Police Service WHEREAS the Municipal

Capital Project Development - definitions, Values and Funding

Definitions and Descriptions Capital Expenditure - A capital expenditure is any significant expenditure incurred to acquire or improve land, buildings, engineering structures, machinery and equipment.

Definitions and Descriptions Capital Expenditure - A capital expenditure is any significant expenditure incurred to acquire or improve land, buildings, engineering structures, machinery and equipment.

CORPORATION OF THE COUNTY OF PETERBOROUGH BY-LAW NO. 2007 49

CORPORATION OF THE COUNTY OF PETERBOROUGH BY-LAW NO. 2007 49 A BY-LAW TO ALLOW FOR RELIEF OF A RESIDENTIAL TAX INCREASE IN 2007 OR 2008 OR 2009 FOR LOW INCOME SENIORS AND LOW INCOME PERSONS WITH DISABILITIES.

CORPORATION OF THE COUNTY OF PETERBOROUGH BY-LAW NO. 2007 49 A BY-LAW TO ALLOW FOR RELIEF OF A RESIDENTIAL TAX INCREASE IN 2007 OR 2008 OR 2009 FOR LOW INCOME SENIORS AND LOW INCOME PERSONS WITH DISABILITIES.

TREATY SETTLEMENT LAND: THE FISCAL IMPACTS ON LOCAL GOVERNMENT

TREATY SETTLEMENT LAND: THE FISCAL IMPACTS ON LOCAL GOVERNMENT PREPARED BY: Peter Adams Victoria Consulting Network Ltd PREPARED FOR: The Union of British Columbia Municipalities, The Ministry of Aboriginal

TREATY SETTLEMENT LAND: THE FISCAL IMPACTS ON LOCAL GOVERNMENT PREPARED BY: Peter Adams Victoria Consulting Network Ltd PREPARED FOR: The Union of British Columbia Municipalities, The Ministry of Aboriginal

PLAINFIELD CHARTER TOWNSHIP KENT COUNTY, MICHIGAN ORDINANCE NO. RESOLUTION NO.

PLAINFIELD CHARTER TOWNSHIP KENT COUNTY, MICHIGAN ORDINANCE NO. RESOLUTION NO. AN ORDINANCE TO AMEND PLAINFIELD CHARTER TOWNSHIP ORDINANCE NO. 612, TO PROVIDE FOR A SERVICE CHARGE IN LIEU OF TAXES FOR

PLAINFIELD CHARTER TOWNSHIP KENT COUNTY, MICHIGAN ORDINANCE NO. RESOLUTION NO. AN ORDINANCE TO AMEND PLAINFIELD CHARTER TOWNSHIP ORDINANCE NO. 612, TO PROVIDE FOR A SERVICE CHARGE IN LIEU OF TAXES FOR

Government of the District of Columbia Office of the Chief Financial Officer

Government of the District of Columbia Office of the Chief Financial Officer Natwar M. Gandhi Chief Financial Officer TAX ABATEMENT FINANCIAL ANALYSIS TO: The Honorable Vincent C. Gray Mayor, District

Government of the District of Columbia Office of the Chief Financial Officer Natwar M. Gandhi Chief Financial Officer TAX ABATEMENT FINANCIAL ANALYSIS TO: The Honorable Vincent C. Gray Mayor, District

Fall 2014 UPDATE ON QUÉBEC S ECONOMIC AND FINANCIAL SITUATION

Fall 2014 UPDATE ON QUÉBEC S ECONOMIC AND FINANCIAL SITUATION Fall 2014 UPDATE ON QUÉBEC S ECONOMIC AND FINANCIAL SITUATION Update on Québec's economic and financial situation Fall 2014 Legal deposit December

Fall 2014 UPDATE ON QUÉBEC S ECONOMIC AND FINANCIAL SITUATION Fall 2014 UPDATE ON QUÉBEC S ECONOMIC AND FINANCIAL SITUATION Update on Québec's economic and financial situation Fall 2014 Legal deposit December

INDEPENDENT FISCAL OFFICE Matthew Knittel, Director Testimony Before the Senate Finance Committee June 10, 2015

INDEPENDENT FISCAL OFFICE Matthew Knittel, Director Testimony Before the Senate Finance Committee June 10, 2015 Chairmen Eichelberger and Blake, members of the committee, thank you for the opportunity

INDEPENDENT FISCAL OFFICE Matthew Knittel, Director Testimony Before the Senate Finance Committee June 10, 2015 Chairmen Eichelberger and Blake, members of the committee, thank you for the opportunity

PUBLIC LAW 104 184 AUG. 6, 1996 DISTRICT OF COLUMBIA WATER AND SEWER AUTHORITY ACT OF 1996

DISTRICT OF COLUMBIA WATER AND SEWER AUTHORITY ACT OF 1996 110 STAT. 1696 PUBLIC LAW 104 184 AUG. 6, 1996 Aug. 6, 1996 [H.R. 3663] District of Columbia Water and Sewer Authority Act of 1996. Public Law

DISTRICT OF COLUMBIA WATER AND SEWER AUTHORITY ACT OF 1996 110 STAT. 1696 PUBLIC LAW 104 184 AUG. 6, 1996 Aug. 6, 1996 [H.R. 3663] District of Columbia Water and Sewer Authority Act of 1996. Public Law

Municipality of the District of West Hants

Municipality of the District of West Hants STAFF REPORT TO: FROM: West Hants Planning Advisory Committee Jeanne Bourque, Planner DATE: July 21, 2011 SUBJECT: Richard Pineo - Application to Amend the West

Municipality of the District of West Hants STAFF REPORT TO: FROM: West Hants Planning Advisory Committee Jeanne Bourque, Planner DATE: July 21, 2011 SUBJECT: Richard Pineo - Application to Amend the West

Land Title and Survey Authority of British Columbia

Land Title and Survey Authority of British Columbia Management s Discussion and Analysis For the three months ended June 30, 2012 The following is a discussion and analysis of the financial condition and

Land Title and Survey Authority of British Columbia Management s Discussion and Analysis For the three months ended June 30, 2012 The following is a discussion and analysis of the financial condition and

MEMORANDUM BACKGROUND

MEMORANDUM TO: Randy Alexander DATE: May 30, 2013 General Manager, Regional & Community Services FROM: Mike Donnelly FILE: 5620-20 ERWS Manager of Water and Utility Services SUBJECT: French Creek Bulk

MEMORANDUM TO: Randy Alexander DATE: May 30, 2013 General Manager, Regional & Community Services FROM: Mike Donnelly FILE: 5620-20 ERWS Manager of Water and Utility Services SUBJECT: French Creek Bulk

City of Kamloops FINANCIAL PLAN - DRAFT 2016-2020

City of Kamloops FINANCIAL PLAN - DRAFT 2016-2020 Financial Planning Process at a Glance The following schedule provides the dates for the Financial Plan process. July-September 2015 Budget preparation

City of Kamloops FINANCIAL PLAN - DRAFT 2016-2020 Financial Planning Process at a Glance The following schedule provides the dates for the Financial Plan process. July-September 2015 Budget preparation

MEMORANDUM. Lee Ledesma Utilities Operations Manager. Randy Ready Assistant City Manager. Amend Electric Large Commercial Rates

ne MEMORANDUM TO Mayor and City Council FROM THRU Lee Ledesma Utilities Operations Manager David Hornbacher Director of Utilities and Environmental Initiatives Randy Ready Assistant City Manager DATE OF

ne MEMORANDUM TO Mayor and City Council FROM THRU Lee Ledesma Utilities Operations Manager David Hornbacher Director of Utilities and Environmental Initiatives Randy Ready Assistant City Manager DATE OF

Report to: General Committee Report Date: May 26 th, 2015. PREPARED BY: Shane Manson - Senior Manager, Revenue & Property Tax

Report to: General Committee Report Date: May 26 th, 2015 SUBJECT: 2015 Tax Rates and Levy By-law PREPARED BY: Shane Manson - Senior Manager, Revenue & Property Tax RECOMMENDATIONS: 1. THAT the report

Report to: General Committee Report Date: May 26 th, 2015 SUBJECT: 2015 Tax Rates and Levy By-law PREPARED BY: Shane Manson - Senior Manager, Revenue & Property Tax RECOMMENDATIONS: 1. THAT the report

Dental Health Services in Canada

Dental Health Services in Canada Facts and Figures 2010 Canadian Dental Association Number of Dentists In January 2010, there were 19,563 licensed dentists in Canada. Approximately 89% were in general

Dental Health Services in Canada Facts and Figures 2010 Canadian Dental Association Number of Dentists In January 2010, there were 19,563 licensed dentists in Canada. Approximately 89% were in general

Catering Contract Agreement

Catering Contract Agreement This Agreement is made on the 25 th day of February 2014 Between: And; Kevin Michael Topping Operating as Topping Expectations of 4102 34 A Street in the City of Vernon in the

Catering Contract Agreement This Agreement is made on the 25 th day of February 2014 Between: And; Kevin Michael Topping Operating as Topping Expectations of 4102 34 A Street in the City of Vernon in the

THIS PRINT COVERS CALENDAR ITEM NO. : 10.5 SAN FRANCISCO MUNICIPAL TRANSPORTATION AGENCY. DIVISION: Finance and Information Technology

THIS PRINT COVERS CALENDAR ITEM NO. : 10.5 SAN FRANCISCO MUNICIPAL TRANSPORTATION AGENCY DIVISION: Finance and Information Technology BRIEF DESCRIPTION: Amend Division II of the Transportation Code to

THIS PRINT COVERS CALENDAR ITEM NO. : 10.5 SAN FRANCISCO MUNICIPAL TRANSPORTATION AGENCY DIVISION: Finance and Information Technology BRIEF DESCRIPTION: Amend Division II of the Transportation Code to

Proposed 2015 2019 Five Year Financial Plan

Proposed 2015 2019 Five Year Financial Plan Received by Committee of the Whole on March 2, 2015 Table of Contents Executive Summary -----------------------------------------------------------------------------

Proposed 2015 2019 Five Year Financial Plan Received by Committee of the Whole on March 2, 2015 Table of Contents Executive Summary -----------------------------------------------------------------------------

BUILDING A FENCE? THE CITY OF CAMBRIDGE REQUIRES THAT ALL FENCES WITHIN THE CITY CONFORM TO THE REGULATIONS OF FENCE BY-LAW

BUILDING A FENCE? THE CITY OF CAMBRIDGE REQUIRES THAT ALL FENCES WITHIN THE CITY CONFORM TO THE REGULATIONS OF FENCE BY-LAW FENCING FOR SWIMMING POOLS/HOT TUBS SPECIAL INFORMATION Your attention is drawn

BUILDING A FENCE? THE CITY OF CAMBRIDGE REQUIRES THAT ALL FENCES WITHIN THE CITY CONFORM TO THE REGULATIONS OF FENCE BY-LAW FENCING FOR SWIMMING POOLS/HOT TUBS SPECIAL INFORMATION Your attention is drawn

SHARED REVENUE AND TAX RELIEF

455 SHARED REVENUE AND TAX RELIEF GOVERNOR S BUDGET RECOMMENDATIONS Source FY01 FY02 % Change FY03 % Change of Funds Adjusted Base Recommended Over FY01 Recommended Over FY02 GPR 1,717,508,900 1,715,169,400-0.1

455 SHARED REVENUE AND TAX RELIEF GOVERNOR S BUDGET RECOMMENDATIONS Source FY01 FY02 % Change FY03 % Change of Funds Adjusted Base Recommended Over FY01 Recommended Over FY02 GPR 1,717,508,900 1,715,169,400-0.1

Growth Management in the City of Brampton

Growth Management in the City of Brampton Brampton introduced its Growth Management Program in 2003 to respond to the opportunities and challenges arising from rapid population and employment growth in

Growth Management in the City of Brampton Brampton introduced its Growth Management Program in 2003 to respond to the opportunities and challenges arising from rapid population and employment growth in

2012 CEEI Floor Area Methodology - Residential, Commercial, and Industrial Buildings

2012 CEEI Methodology - Residential, Commercial, and Buildings 1.1. Protocol and Guiding Principles In order to improve understanding of the building characteristics at a neighbourhood level, the BC Assessment

2012 CEEI Methodology - Residential, Commercial, and Buildings 1.1. Protocol and Guiding Principles In order to improve understanding of the building characteristics at a neighbourhood level, the BC Assessment

f) That expenditures associated with employee insurance & benefits be increased by $319,000;

That expenditures associated with employee insurance & benefits be increased by $319,000;") 2014 BUSINESS PLAN with GC amendments included 1. That the 2014 tax-supported base operating budget for municipal operations, with total gross expenditures of $179.2 million and a net property tax levy

2014 BUSINESS PLAN with GC amendments included 1. That the 2014 tax-supported base operating budget for municipal operations, with total gross expenditures of $179.2 million and a net property tax levy

Fire Commissioner Office of the Fire Commissioner Emergency Management BC Ministry of Justice Victoria

Fire Commissioner Office of the Fire Commissioner Emergency Management BC Ministry of Justice Victoria The Office of the Fire Commissioner is mandated to minimize the loss of life and property from fire

Fire Commissioner Office of the Fire Commissioner Emergency Management BC Ministry of Justice Victoria The Office of the Fire Commissioner is mandated to minimize the loss of life and property from fire