GENERAL CONDITIONS OF USE

|

|

|

- Eustace Johnston

- 8 years ago

- Views:

Transcription

1 Tools for life

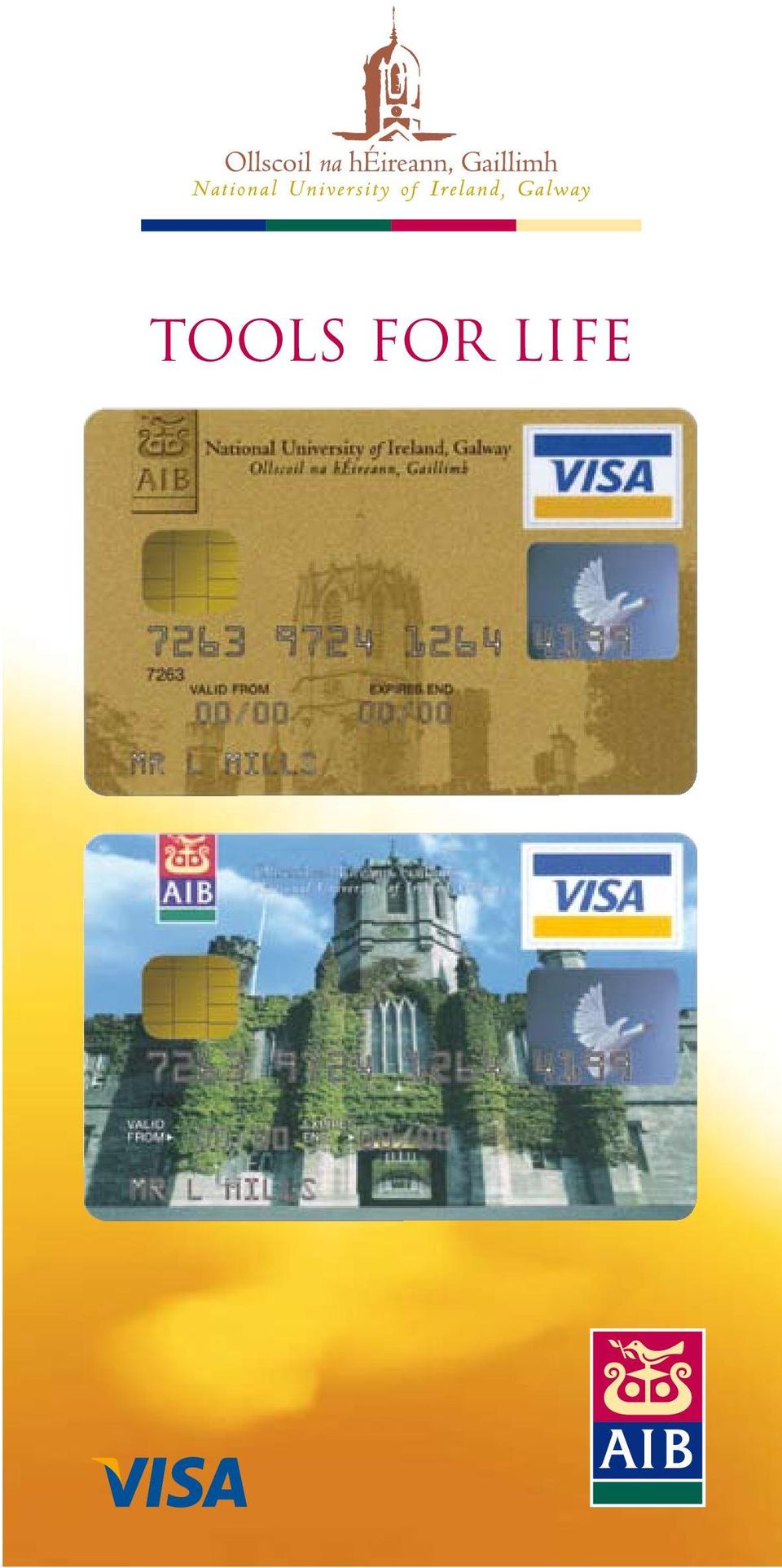

2 Notes National University of Ireland, Galway has joined with AIB to offer you a special Affinity Credit Card, issued exclusively to National University of Ireland, Galway graduates, staff, students and friends of the University. The features and benefits of the NUI, Galway Standard and Gold Visa Cards are detailed inside this pack and include the following: Preferential APR on purchases No Annual Fee 1 Balance Transfer for 6.9% for 12 months from the date the credit card account is opened Free Personal Accident Travel Insurance 2 Up to 56 days Interest Free Credit Statement carry updates on events and happenings in NUI, Galway. To apply, please complete the enclosed application form. For further information, please contact AIB Card Services on Freefone Thank you for your support. 1 Government stamp duty of 40 is charged annually per Credit Card account. 2 Please note this insurance does not substitute fully comprehensive Travel Insurance. Terms and Conditions apply. 3 Fees and Charges apply. 4 Terms and Conditions apply. Why choose an NUI, Galway Standard Credit Card? The NUI, Galway Visa Card is a very tangible way of keeping in touch and supporting your University. The attractive card depicting a clock tower is a visible sign of your ties with the University and every time a card is issued or used, much needed funds are generated to support a range of University priority projects. If you are someone who leads a really busy life then this card is for you. It simplifies shopping, travelling and entertainment while providing you with a detailed record of expenditure. The NUI, Galway Standard Visa Card is ideal if you need to borrow occasionally or intend paying your outstanding balance in full every month. What are the extra benefits of an NUI, Galway Gold Visa Card? If you require a higher credit limit, and you earn at least 25,000 annually, then this card can offer you a higher credit limit, starting from 3,200. Preferential Rate of Interest Your NUI, Galway Credit Card offers you an attractive APR. No Annual Fee There is no annual fee on the NUI, Galway Credit Card % Balance Transfer Rate As a new cardholder, an APR of 6.9% will be applied on all balances transferred from store or non-aib cards. This APR is fixed for 12 months from the date the account is opened. After 12 months the balance transfer APR reverts to the standard APR applicable at that time. Free Personal Accident Travel Insurance You will receive free Personal Travel Accident Insurance 2 when you use your NUI, Galway Credit Card to pay for your travel tickets. Up to 56 days Interest Free Credit 3 To avoid paying interest simply clear your balance by the due date each month. Cash conveniently at hand At home or abroad, you can rely on your NUI, Galway Credit Card along with your PIN (Personal Identification Number) to obtain cash. Simply visit any ATM or bank where you see the Visa logo. 3 At your service around the clock We provide an extensive service for cardholders which means we are available to you by phone, 24 hours a day, 7 days a week. Share the benefits with a second card You can nominate a family member, your partner or a close friend as an additional cardholder on your NUI, Galway Credit Card account for free. You ll have all the convenience of two cards with the peace of mind of a single bill. Emergency Service Should your NUI, Galway Credit Card be lost or stolen while abroad, you can have access to up to US$5,000 in emergency cash (subject to available card limit). Optional Payment Protection Plan 4 Nobody can be certain of what lies ahead. This is why AIB Insurance recommends that all customers consider taking out payment protection insurance. A service designed to give you peace of mind and protection in the event of disability (as a result of accident and/or sickness) involuntary unemployment, critical illness or loss of life. For a cost of just 60c per every 100 outstanding on your NUI, Galway Credit Card account each month, a monthly benefit will be paid equivalent to 10% of your total outstanding balance (as at your last statement), for up to 12 months per eligible claim. Pinnacle Card Protection Cover 4 What would you do if you lost your NUI, Galway Credit Card or other important personal items while abroad? With our Card Protection Service, help is just a Freefone call away from anywhere in the world. Help includes a confidential record of all your Credit Cards, instant Card loss notification, and emergency travel tickets. Annual premium is 16. Optional Travel Insurance In addition to the free Personal Travel Accident Insurance cover on this card, you can also upgrade to full Travel Insurance cover for an additional premium. We also have other Travel Insurance products to meet your individual needs. Check out our website at

3 AIB VISA CREDIT CARD APPLICATION Please ensure that the application is completed in full. Non AIB account holders must provide original Photographic Identification (Passport / Driver s License) and proof of Address (one household bill) to any AIB branch. Please complete in BLOCK CAPITALS and tick ( ) boxes as required. Please issue my NUI, Galway Credit Card as a: Standard Visa Gold Visa If you do not clearly select one of the above options, on approval of your application you will be issued with an NUI, Galway Standard Credit Card. Please state your affinity with the University: Graduate Student Staff Friend of NUIG NUIG Student No. Personal Details Mr Mrs Miss Ms Other title (please state) Surname First names Please spell out your name as you wish it to appear on the card using no more than 26 letters or spaces. Address Home telephone number Area code Mobile number Place of birth Date of birth D D M M Y Y Local number Graduation Year Existing AIB Credit Card holders, please fill in your existing AIB Credit Card number here. (16 digits) You may continue to use your existing AIB Credit Card (as detailed above). Following despatch of your new NUI, Galway Credit Card, the Credit Card account entered above will be closed and all balances transferred to your new account. If you do not wish us to close your existing account please tick ( ) here. Number of dependants Marital status Single Married Widowed Separated/Divorced Are you A home Living with owner parents Tenant Time at current address Years Months If tenant or at current address for less than 3 years, please give previous home address Employment Details Employee Self-employed Retired Homemaker Student Unemployed Other Occupation/Profession Financial Manufacturing Construction services Distribution Other Employer s name and address (if self-employed, please give business name and address) Business telephone number Area code Local number Time employed Years Months Gross Total household Annual income income Method of Payment Cash Cheque Credit Transfer Other Frequency of Payment Weekly Fortnightly Monthly Irregularly Financial Details Banker s name and address Bank sorting code number Type of accounts held Current Deposit Loan Other Mortgage/Rent Loans H.P. Other Monthly commitments If house is mortgaged give: Balance Name of lender Valuation outstanding Other cards held Mother s maiden name (for security purposes) Address Account number Time with bank Years Months Visa MasterCard Diners Club American Express Store Card Optional Annual Travel Insurance I wish to avail of the increased Travel Insurance cover and have indicated so by signing the box below. I authorise you until further notice in writing to debit my AIB NUIG Credit Card Account with the amount due (one year s cover, currently ). Signature of Principal Cardholder AIB Bank Payment Protection Plan Applicant must complete option 1 OR Option 2. Statement of reasons as to why this product is suitable for you AIB Insurance recommends that all customers consider taking out payment protection insurance. AIB Insurance Services offers payment protection insurance through a combination of CLAC (Combined Life Assurance Company Limited) and LGI (London General Insurance Company) exclusively. AIB Insurance Services Ltd. offers only one credit card payment protection insurance product and considers this product to be suitable for customers credit card payment protection insurance needs. You may already have existing insurance to cover some of the benefits offered under the optional payment protection product. This offer of cover relates only to protecting this specific agreement and does not suggest or imply any advice in relation to existing covers. OPTION 1: I wish to avail of the Payment Protection Plan. I hereby declare that I am: (i) over the age of 18 and under the age of 65 and (ii) that I am ordinarily resident in the Republic of Ireland, Northern Ireland or Great Britain including Channel Island and Isle of Man. (iii) I also hereby declare that I am in gainful employment (including selfemployment or fixed term contracts) of not less than 16 hours per week on an annualised average basis and that I am actively at work and unaware of impending unemployment. I hereby authorise and request you to charge the related premiums to the facility, if granted. I accept that the Bank shall have no liability for any loss or damage caused by any failure to collect these premiums. Signature of Principal Cardholder if accepting Payment Protection Plan OPTION 2: I do NOT wish to accept the offer of Payment Protection Plan. Signature of Principal Cardholder if declining Payment Protection Plan Consent to Communicate* I consent to AIB contacting me at any time (including outside normal business hours) in connection with my Card and Card Account by personal visit and/or telephone, including at my place of employment, or business or elsewhere. *if you do not wish to give this consent please tick this box Terms and Conditions apply. Credit facilities are subject to repayment capacity and financial status and are not available to persons under 18 years of age. Government stamp duty of 40 is charged annually per Credit Card account. AIB Insurance Services Ltd. is a wholly owned subsidiary of Allied Irish Banks, p.l.c. AIB Insurance Services Ltd. is a Multi Agency Intermediary regulated by the Financial Regulator. Allied Irish Banks, p.l.c. is regulated by the Financial Regulator.

4 Data Protection Notice Use of Information This Notice explains how AIB Group will use information provided by you. References to "AIB Group" means Allied Irish Banks, p.l.c., its Irish subsidiaries and associated companies from time to time. 1. The information that you provide will be held by AIB Group on a computer database and/or in any other way. AIB Group will use this information to administer the products and services we supply to you and any future agreements we may have with you. You have the right of access to the personal data held about you by AIB Group by sending a written request to your local AIB branch or to the Data Protection Unit, Allied Irish Banks, p.l.c., Bankcentre, Ballsbridge, Dublin 4, and on payment of a fee of You also have the right to require AIB Group to correct any inaccuracies in the information we hold about you. 2. When considering a request, proposal, application or administering your agreement(s), managing your account(s) or making decisions regarding credit, including whether to make credit available or to continue or to extend existing credit, AIB Group may carry out searches (for the purpose of verifying your identity) and/or a credit search with one or more licensed credit reference agencies. AIB Group may use credit scoring and other automated decision making systems. To prevent or detect fraud, we may make searches of the AIB Group records. We may also pass information to financial and other organisations involved in fraud prevention to protect ourselves and our customers from theft and fraud. If you give us false or inaccurate information and we suspect fraud, we will record this. Where you borrow or enter into a financial obligation, or may do so, AIB Group may give details of your agreement(s)/account(s) and how you conduct your agreement(s)/account(s), to licensed credit reference agencies on a regular basis. Licensed credit reference agencies will record details of each type of search AIB Group makes whether or not your application proceeds. You have the right of access to the personal data held about you by licensed credit reference agencies. Please write to the Data Protection Unit, Allied Irish Banks, p.l.c., Bankcentre, Ballsbridge, Dublin 4, if you would like to know the names of the agencies used by AIB Group. If you decide to proceed with this application or have any other communication with AIB Group through or in relation to its products and services you accept the use by AIB Group of your personal data as indicated above. Product Information In future we, AIB Group, would like to use your personal data for the purpose of offering you other products and services, including those available from other companies in AIB Group and carefully selected third parties, which AIB Group thinks may be of interest to you. In this connection, and occasionally for market research and statistical purposes, the services of a reputable external agency may be used. Are you happy to receive this information by the following? Mail Y N Phone Y N Y N Pinnacle Card Protection Service I wish to avail of Pinnacle Card Protection Service. I authorise you until further notice in writing to debit my NUI, Galway Credit Card with the premium due (1 years protection currently 16). Signature of Principal Cardholder if accepting Pinnacle Card Protection Service Request for Additional Card for an Authorised User You can have one additional cardholder on your NUI, Galway Credit Card. Existing AIB Credit Cardholders: Any existing Authorised User on your account will automatically be transferred over to your new account. If you do not wish to transfer your existing Authorised User then please tick the box opposite. If you wish to amend or add an Authorised User then complete the area below. Please issue an NUI, Galway Credit Card and related Personal Identification Number (PIN) to me. I have read and agree to be bound by the Conditions of Use (as set out overleaf) and join in the consents and understandings set forth in the request for Card facilities above in so far as they relate to me. Mr Mrs Miss Ms Other title (please state) Surname First names Please spell out your name as you wish it to appear on the card using no more than 26 letters or spaces. Relationship Signature of Authorised User Request for Card Facilities Date of Birth Signature of Principal Cardholder X D D M M Y Y Please issue an NUI, Galway Credit Card and confidential Personal Identification Number (PIN) to me and open an AIB Account in my name. I confirm that I am over 18 years of age and that the information given herein is true and complete. To enable you to meet your obligations (in regard to the prevention of money laundering) under the Criminal Justice Act 1994, I agree to furnish you with suitable evidence of identity and permanent residence and consent to you making such other enquiries in connection with this application as you deem appropriate. In the interest of combating crime arising from the use of credit cards, I consent to the information herein supplied being held on and being accessed through a centralised data bank. I have read and agreed to be bound by the Conditions of Use overleaf. I consent to the above conditions governing Use of Information as contained in the Data Protection Notice. If my application is accepted, I authorise you (if so requested) to issue an additional NUI, Galway Credit Card and confidential PIN to the person named above as an Authorised User on my AIB Account. I authorise AIB to disclose my choice of fund, student number, graduation year, affinity with the University, name, addresses (home and business), telephone number(s) and date of birth to the Alumni Office in NUIG. However, no other information regarding my personal data is to be disclosed to NUIG. Date For branch use only I confirm that this application complies with the Criminal Justice Act, 1994 BRANCH BRAND Compliance with CJA'94 Yes No Type of Document Issued By/At Ref. No Customer ID Provided Permanent Add. Verified CJA Folio No. Recommended I.D. Credit Limit number Authorised Signature CL LC SC LID SID Direct Debit Instructions If you wish to pay your Credit Card bill by direct debit, please complete this form and return to the postal address below. Credit Card number Name and address Bank sort code Banker s name and address Account number Instructions to bank I authorise you until further notice in writing to debit my account with the amount due from AIB Credit Card Services. The amounts are variable and may be debited on various dates. I will inform the bank in writing if I wish to cancel this instruction. I understand that if any direct debit is paid which breaks the terms of this instruction, the bank will make a refund. Please tick ( ) the box below indicating the direct debit option you require. 5% 10% 20% (min of 6.35) 25% 50% 100% If the mandate is completed and no box is filled, the 5% option will apply. Signature of Principal Cardholder X Date Some banks may decline to pay Direct Debits from certain types of accounts. This is a guarantee provided by your bank as a member of the Direct Debit Scheme, in which Banks and Originators of Direct Debits participate. If you authorise payment by Direct Debit, then - Your Direct Debit Originator will notify you in advance of the amounts to be debited to your account. - Your Bank will accept and pay such debits, provided that your account has sufficient available funds. If it is established that an unauthorised Direct Debit was charged to your account, you are guaranteed a prompt refund by your Bank of the amount so charged. You can cancel the Direct Debit Instruction by writing in good time to your Bank. Postal Information For Office Use only OIN OIN OIN If you are posting your application to us, please place it in an envelope addressed as follows: AIB Card Services, PO Box 708, Donnybrook House, Donnybrook, Dublin 4. POT DD Processing NSC

5 GENERAL CONDITIONS OF USE The use of your credit card is governed by these general terms and conditions. DEFINITIONS Account means the card account kept by us in the name of the Cardholder in which debits and credits in respect of Transactions are recorded; Agreement means this agreement (and Conditions) between the Cardholder and the Bank for the opening of an Account and the issue of a Card and incorporates the application form and each card carrier (a confidential mailing slip or cover containing instructions regarding authentication and security and the current Credit Limit); Available Credit means at any time the unutilised amount of the Credit Limit; Balance Transfer means the transfer to the Account, with our consent, of an amount owed on a credit card or store card to another financial institution (but excludes transfers of debt from existing AIB Cards). Bank; we ; us ; and our means Allied Irish Banks, p.l.c., its successors, subusidiaries, assigns and associated companies; Card means a credit card issued to the Cardholder or any Authorised User for the purpose of effecting Transactions on the Account pursuant to the terms of the Agreement and incorporates all elements of that card, including, without limitation, the Chip; Cardholder means only the person in whose name the Account is maintained and does not include Authorised Users; Cardholder Not Present Transaction means a Transaction that is carried out where you are not present at the location of the machine used to effect the Transaction. These include transactions carried out by post, phone, internet, fax or other electronic means as may be authorised from time to time; Cash Machine means an electronic machine used for dispensing cash and, in some cases, performing other functions; Chip means an integrated circuit embedded in a Card; Conditions means these terms and conditions as amended, extended, supplemented or replaced from time to time; Credit Limit means the maximum debit balance that you are allowed to have outstanding on the Account at any time; Ireland means the Republic of Ireland; Merchant means any person who accepts payment made with a Card; PIN means the secret personal identification number that is used with a Card as allotted by us and/or subsequently chosen by you; Statement means a paper statement issued by us, in respect of the Account. The Bank and the Principal Cardholder may agree from time to time to vary the format of a Statement to include statements of account issued by electronic means; Transaction means a transaction in which a Card is used to obtain goods, services or cash on credit (includes all debits and credits made to the Account pursuant to this Agreement); you and your refers to the Cardholder and, unless the context otherwise requires, any Authorised User. Looking after your Card and PIN 1. The Card and PIN must be used in accordance with these Conditions. Each Card is and remains our property and may be cancelled, suspended, recalled or retained by us in accordance with the provisions of the Agreement. 2. You must: sign your Card as soon as you receive it using a ball point pen; keep your PIN secret and keep your Card secure; only use your Card (a) within the Credit Limit, (b) within the period for which it is stated to be valid and (c) strictly in accordance with the Agreement; and tell us immediately if there is a change of name, bankers, business or home telephone numbers, or the address to which Statements are sent in accordance with clause You must not: let anybody else use your Card or your PIN; disclose your Card number to anyone, except when carrying out a transaction or to report it lost, stolen or likely to be misused; disclose, write or record your PIN or any other code allocated to you; Credit Limit 4. We will set a Credit Limit on the Account. We may, subject to applicable law or regulation, vary the Credit Limit from time to time at our discretion or at your request. We will notify you of any such variation. You will be given not less than 10 days notice of any proposed decrease in the Credit Limit on the Account, except where such decrease is requested by you. If your Card is used for a transaction which would bring the outstanding debit balance ( Outstanding Balance ) in excess of the Credit Limit, we reserve the right to authorise or decline such transactions. If we authorise a Transaction in excess of the Credit Limit currently applying to the Account, this will not affect the Credit Limit and subsequent transactions bringing the Outstanding Balance in excess of the Credit Limit or where the Credit Limit has been exceeded may be declined. 5. Where you provide your Card number to a Merchant in relation to any transaction, your Available Credit may be reduced by the amount or an estimate of the amount of the transaction before the transaction is completed. 6. In some cases a Merchant may obtain specific authorisation in advance from us or our agents to honour a Card for a particular transaction. This may affect the Available Credit. Restrictions 7. A Card must not be used: if the Agreement is ended; after a Card has expired or been reported lost, copied or stolen or has been cancelled or suspended; at any Cash Machine abroad in violation of local regulations; or for any illegal purchase or purpose whatsoever. 8. A request for a Balance Transfer will only be considered where the other financial institution is within the euro zone and clearance of the amount owed can be effected by us by electronic means. Balance Transfers will only be made in euro. Transfers of amounts owed on existing AIB Cards will be regarded as normal outstanding balances and not Balance Transfers. Cash Withdrawals 9. Your Card may be used in conjunction with your PIN to avail of certain services at Cash Machines that display the appropriate credit card symbol. The use of your Card to withdraw cash from a Cash Machine is subject to both transaction and daily limits. The transaction limit can vary between financial institutions and from time to time. The cash advance limit will be determined by us and may vary from time to time. Details of the cash advance limit are available from us. We will not be obliged to provide Cash Machine facilities at any particular time and may withdraw or terminate such facilities without notice. We will not be liable for any loss or damage resulting from failure to provide any service, or failure or malfunction of a Cash Machine. 10. A Card may be used outside Ireland subject to any limits or regulations that may be imposed by the appropriate regulatory authorities from time to time. 11. Where the Card is used outside the Eurozone to obtain Euros, the local bank may convert the amount of Euros into the local currency and may charge a foreign exchange margin. This may result in an amount debited from the Account that is different to the amount you withdrew. Authorised Users 12. From time to time, we may permit the issue of an additional Card, together with a separate PIN, for use by a person nominated by you (an Authorised User ). However, there is no obligation on us to do so. You may enquire from your local branch whether this facility is available. If we consent to the issue of additional Cards, they will be issued subject to these Conditions. Each Authorised User will be furnished with a copy of these Conditions and will be bound to observe these Conditions to the extent that they apply or are relevant. You will, however, be primarily responsible for all transactions for which the additional Card is used, including those charged to the Account after the additional Card has been returned to us. 13. We will cancel any additional Card at any time if the Cardholder requests this in writing, in which case the additional Card, cut in two (through the signature box, magnetic strip and Chip) for security reasons, must be returned to us at address below. 14. By entering into this Agreement, the Cardholder gives us the authority to pass on information about the Account or transactions to any Authorised User by electronic or other means. However, no amendments to the Account details or variation of the Credit Limit will be accepted from an Authorised User. 15. The Cardholder is liable for the payment of all Transactions carried out by an Authorised User regardless of the ability of that Authorised User or whether they are a minor or not, as if the Transactions had been personally carried out by the Cardholder. Loss or misuse of a Card 16. You will take all reasonable steps to ensure the safety of the Card. If you think someone else knows your PIN, or if your Card is lost, copied, mislaid, stolen, used, or likely to be used, for a fraudulent or improper purpose, you must tell us immediately by telephoning (24 hours a day) (or from abroad). We may request that you confirm the same in writing to us, but without affecting the validity of any action taken by us in response to your telephone call. 17. Notification of loss or theft of a Card will be accepted by us from card protection service organisations. 18. By reporting a Card as lost, copied, mislaid or stolen or as being used, or likely to be used, for a fraudulent or improper purpose, you will be deemed to have thereby authorised us to cancel that Card. It cannot be used again. If found, it must be cut in two (through the signature box, magnetic strip and Chip) for security reasons and returned to us immediately at the address below. 19. You will be responsible for any loss sustained, up to the time of notification to us in accordance with clause 16 or 17. Your liability will be limited to an overall limit of 63.49, except: if you acted, knowingly, fraudulently or with gross negligence; or if any Transactions were effected as a result of the breach of clause 3; or if any Card is used by any other person outside the terms of this Agreement and who has possession of it with your consent; or if you do not notify us in accordance with clause 16 that a Card has been lost, mislaid or stolen or used, or likely to be used, for a fraudulent or improper purpose. 20. In the event of notification by you in accordance with clause 16 above you will co-operate with us and the relevant police authority in any investigation and give us and the police all information relating to such loss, theft or disclosure and all reasonable assistance to lead to the recovery of the Card. You authorise us to inform any appropriate third party of the loss, mislaying, theft or possible misuse of the Card and to give them such other information as may be required. 21. If we suspect that a Card is being used improperly, fraudulently or in breach of this agreement we may decline to authorise any further transactions on the Account until we have contacted you. We will endeavour to contact you before we take this decision but this may not be possible. You hereby agree and authorise us to take such actions as we deem necessary including suspending the Account in such circumstances. You agree that any contact by us is for the purposes of combating wrongdoing and is not connected to this Agreement. The Account 22. The amount of all Transactions will be debited to the Account reducing the Available Credit. In the event of a query or dispute you must notify us as soon as practicable and, in any event, within 60 days of the date of the Transaction being debited to the Account. Payment for goods or services 23. The Cardholder will be liable to pay all sums that are charged to the Account in respect of or resulting from all Transactions including where such transactions are effected by telephone, mail order or internet or in breach of these Conditions. 24. You accept that electronic communications via the internet or SMS-based telecommunications media may not be secure and may be intercepted by unauthorised persons or delivered incorrectly. Any such communications shall be at your risk. Where a Transaction is conducted through a Secure System (a system approved by us to enable the secure use of your Card over the Internet) in accordance with all instructions and in compliance with all security requirements issued by us you will no longer be liable for the risk of interception by unauthorised persons or incorrect delivery. Use of any Secure System by you is subject to the terms and conditions of the Secure System. 25. When authorising a Transaction using your PIN you must confirm the amount with the Merchant at time of authorisation. The entries relating to a Transaction recorded in the Account are conclusive evidence that the Transaction occurred as so recorded. The use of the PIN will be regarded as conclusive evidence that the Transaction was authorised by the Cardholder or, as the case may be, the Authorised User. 26. The amount of any Transaction effected outside of the euro zone will be converted to euro at the rate of exchange applicable on the date the Transaction is debited to the Account in accordance with the procedures of Visa or MasterCard. We have no control over the applicable exchange rate. You will also be charged a transaction fee as set by Visa or MasterCard. These transaction fees may vary depending on the country where a Transaction is effected (as per the Schedule of Fees and Charges). In addition, we will charge commission on the total amount at the rate notified in the schedule of fees and charges relevant to your Account type for the time being in force. Exchange rates may fluctuate between the date of a Transaction and the date on which the transaction amount is debited to the Account. Monthly statement payment arrangements 27. We will normally issue a Statement monthly to the Cardholder, on a date which we may decide, containing (a) details of all Transactions debited and credited to the Account since the previous Statement (or, in the case of the first statement, since the opening of the Account), and (b) the Outstanding Balance (if any) at the Statement date. 28. If a Statement is not received for any month, or if it cannot be produced or issued for any reason your responsibilities under this Agreement continue. You will be required to obtain details of the Outstanding Balance and make the appropriate minimum payment by using our online or telephone banking facilities or by contacting us. 29. The initial monthly payment will fall due within the period chosen on the application form following the first use of the Card. Each month the Cardholder must make the minimum payment to the Account as stipulated in the statement for that month. The Cardholder may select as the minimum payment percentage any of the following percentages: 3% (only available with direct debit) 5%, 10%, 20%, 25%, 50% (subject to a minimum payment of 6.35 if greater) or 100%. Other than when paying by direct debit, the Cardholder must ensure that the payment is made or sent so as to reach us at the specified address for payment credited to the Account not later than the payment due date (this is specified in your statement). Any payment made will take effect when correctly received by us and credited to the Account. When making a payment you should allow at least 4 working days for the payment to be processed by us. 30. If the minimum payment is not paid by the due date, we may decline to authorise transactions. 31. We may grant, at our discretion, a Payment Holiday (a period when we may allow you to defer a payment or payments). Interest will continue to be charged under clauses 36 to 43 and the period referred to in clause 40 will not be extended. 32. The Cardholder must pay on demand, and in any case, on receiving the statement:- any outstanding excess over the Credit Limit; any arrears; the amount of any Transaction made in breach of these Conditions. 33. Should a payment be received more than 3 working days prior to the payment due date, the amount calculated for payment by direct debit will be reduced by this amount. Payments received within 3 days of the payment due date will not reduce the amount collected by direct debit. The Cardholder must ensure that funds are available to meet all payments due on the Account. 34. We reserve the right to debit the Account by the amount of any unpaid item or any other amount which we are obliged to refund to a third party for any justifiable reason. 35. Without affecting any other right of set off which we may have, if you have a credit balance on any other account with us (whether due or not and in any currency), we may use this credit balance to satisfy any sum due on the Account. We may or may not give prior notification to you where this is done.

; Available Credit means at any time the unutilised amount of the Credit Limit; Balance Transfer means the")

6 Annual Percentage Rate of Charge 36. The annual percentage rate of charge (APR) applied to the Account is designed to measure the total cost of credit to the consumer and will be advised to the Cardholder on the opening of the Account. We may vary the APR at any time. A variation will normally be caused by market conditions, changes in the cost of providing the service, including variations in the prevailing ECB and market rates, changes in legal or other requirements affecting us, promotional reasons or any other good reason. Any variation in the interest rate will result in a change in the APR. If we vary the interest rate (an consequently the APR) we will notify (in accordance with clause 59 & 60) the Cardholder of the variation and also of the corresponding change in the APR. On receiving such notification, the Cardholder may end the Agreement and cancel the Card(s) in accordance with clause 45. Fees, Charges & Interest 37. All fees, charges and interest payable in connection with the Account will be the Cardholder s liability and will be debited to the Account in accordance with the following arrangements: all fees payable on the account are outlined in the schedule of fees and charges relevant to your Account type for the time being in force; and all stamp duties and government levies payable in respect of the Card are your liability and will be collected by us by debit of the Account. Should you close your account before the date of collection the amount will be debited at closure and payable by you. 38. Where a Card is used to obtain a cash advance, a cash advance fee will apply as notified to you from time to time in the schedule of fees and charges relevant to your Account type for the time being in force. In all cases, the cash advance fee will be debited to the Account on the date of the cash advance and will appear in the next statement. 39. Separate charges may be incurred and debited to the Account and will be advised to you from time to time. These can be in respect of late payments, returned payments or operating in excess of your Credit Limit. These charges will be advised to you in writing on the opening of the Account and will be published in the schedule of fees and charges relevant to your Account type for the time being in force. We will ensure that the charges conform to any scale or amounts that may be set under any law, regulation or other order. Interest 40. Interest will not be charged on any amount debited to your Account in respect of purchases or advances if the whole of the Outstanding Balance on a Statement is paid in full and credited to the Account by the payment due date specified on the statement upon which the amount first appears, except in the case of Low Interest MasterCard and Budget MasterCard where no interest free credit days apply. The interest rate for purchases and cash advances being applied to an Account will be notified to the Cardholder on the Statement. 41. If the full balance is not repaid by the payment due date specified on the Statement upon which the amount first appears, then the interest free period as set out in clause 40 is forfeit and interest is charged on the full balance from the transaction date of each purchase or cash advance, as shown on your Statement, until full repayment is credited to the Account. Interest on Balance Transfer transactions will be charged from the date the transaction was debited to the Account until full repayment is made. 42. Subject to clause 40 above, interest will be payable on all amounts owing to us on the Account. Interest will accrue (as well after judgement or demand as before) on a daily basis at the current (variable) rate advised to you. Interest will be charged to the Account monthly. In respect of Transactions, interest will accrue and be charged on from the date of the Transaction until the date a payment is received and credited to the Account. Where a part payment is made, interest will continue to accrue and be charged on the remaining balance up to and including the date of the next statement, when the interest for the period will be debited to the Account. 43. Payments received will be deducted from the opening balances on the Account in the following order based on the portion of the balance representing: interest; fees from previous statement; cash advances (including cash from a Cash Machine) from previous statement; and purchases from previous statement. The remainder (if any) will be applied to Transactions on the current statement in the following order: fees; cash advances; purchases and Balance Transfers; and, any other promotional offers. Issue of new cards 44. New Cards may be issued by us to you from time to time at our discretion without the need for further application. If a Card is reported lost, copied or stolen, the Bank can refuse to issue a new Card if:- the Cardholder has requested in writing, not less than 30 days before the renewal date on the current Card, that we do not issue any new Card(s); or we have decided (in accordance with clause 46 or 47) not to issue a renewal or replacement Card. Ending the agreement 45. The Cardholder may at any time end the Agreement by giving notice in writing to us and returning all Card(s) cancelled by being cut in two (through the signature box, magnetic strip and Chip) to us. 46. If: you become bankrupt or enter into a voluntary arrangement with your creditors; you are no longer, in our opinion, able to manage your financial affairs; you die; or it becomes unlawful for you to continue to have a Card, we can immediately suspend any Card, end the Agreement, cancel all Card(s) and/or refuse to issue, renew or replace any Card by giving written notice to the Cardholder whereupon you must cut all Card(s) in two (through the signature box, magnetic strip and Chip) and return them to us. 47. If: any representation, warranty or statement made by you in connection with the Agreement is breached or is or becomes, in our opinion, untrue in any material respect; or you breach this Agreement or any other agreement with us, we (having served on the Cardholder any notice required in accordance with the Consumer Credit Act, 1995) may suspend any Card, end the Agreement, cancel all Card(s) and/or refuse to issue, renew or replace any Card whereupon you must cut all Card(s) in two (through the signature box, magnetic strip and Chip) and return them to us. 48. We may publish the suspension or cancellation of any Card. 49. If you make a notification under clause 16 or 17 or if the Agreement is ended we may request a retailer or other person to retain any Card or cancel any Card by cutting it in two (through the signature box, magnetic strip and Chip) and return them to us. 50. If this Agreement is ended (by the Cardholder or by us) the Cardholder will remain liable for all transactions and must pay in full the Outstanding Balance on the date the Agreement is ended as well as: all outstanding Transactions, fees and charges, all stamp duties and government levies and any accrued but unpaid interest. The terms of this Agreement will remain in full force until all money owed is paid. For the avoidance of doubt, there will be no other costs incurred by the Cardholder in respect of termination of this Agreement. 51. On the death or legal disability of the Cardholder, the Outstanding Balance on the Account will become a liability of the estate of the Cardholder and all Cards must be returned to us cut in two (through the signature box, magnetic strip and Chip). Assignment 52. We may assign or otherwise transfer all or any of our rights, benefits and/or obligations under the Agreement to any natural or legal person. Refunds 53. If a Merchant initiates a refund we will only credit the Account with the amount due upon receipt of the refund amount from the Merchant and, unless so credited (but subject to any rights conferred on you by law), the Account will be payable in full. Refunds are not treated as payments made to the Account and therefore will not be reflected in the current amount due for settlement as required under Clause 27. The amount due must be settled in the normal manner and any refund received will be recognised and taken into account in the following Statement. General 54. We shall neither be in breach of our obligations under the Agreement nor liable for any loss or damage suffered by you if there is any total or partial failure of performance of our duties and obligations occasioned by any act of God, fire, act of government or state, war, civil commotion, insurrection, embargo, inability to communicate with third parties for whatever reason, failure of any computer or settlement system, failure of or delay in the transmission of messages via any mobile phone network, prevention from or hindrance in obtaining any energy or other supplies, labour disputes of whatever nature, late or mistaken payment by an agent or any other reason (whether or not similar in kind to any of the above) beyond our control or that of our agents or sub-contractors. 55. The documents and records kept by us or on our behalf, whether on paper, microfilm, by electronic recording or otherwise, will, in the absence of manifest error, constitute conclusive evidence of any facts or events relied upon by us in connection with any matter or dealing in relation to the Account. 56. We are not obliged to grant or continue any additional facility or benefit made available to you which is not specified in the Agreement. Accordingly, any such facility or benefit may be varied or withdrawn by us without notice. 57. Save to the extent we are unable under applicable law to disclaim such liability, we shall not be liable for any loss or damage suffered by you as a result of the failure of third party providers of additional facilities and benefits to perform their duties and obligations. 58. We may record or monitor phone calls between you and us so that we can check instructions and make sure that we are meeting our service standards and to ensure the security of our business, and that of our customers and staff. Variation of the Agreement 59. We may alter the terms of the Agreement from time to time. Alterations will normally be caused by market conditions, changes in the cost of providing the service, changes in legal or other requirements affecting us, promotional reasons or any other good reason. Any such alteration will be notified to the Cardholder in accordance with applicable law or regulation 60. Notification of any such alteration (and notifications of alterations in the interest rate, the Credit Limit or the fees and charges) may be given by advertisement published in a national daily newspaper or by post or by being enclosed with the Statement or the Card or by being prominently displayed at our branches in a notice addressed to All AIB Bank Card Holders, or by any other means required by law. On receiving such notification, the Cardholder may end the Agreement and cancel the Card(s) in accordance with clause 45. Notwithstanding any such termination, the Cardholder shall remain liable for all Transactions. Waiver 61. If we do not enforce any condition of this Agreement, or we delay in enforcing it, this will not prevent us from enforcing the condition retrospectively at a later date and will not constitute a waiver of that condition. No liability for refusal or for goods or services 62. We shall not be liable for any loss arising as a result of the refusal or delayed acceptance of any Card by a Merchant or other third party, or for any loss or damage you may suffer as a result of the way in which any such refusal or delay is communicated to you or is otherwise published. 63. Save to the extent that we are unable under applicable law to disclaim such liability, we are not responsible for the delivery or condition of any goods and/or services paid for by a Card. We accept no liability for any loss or damage suffered in connection with any goods and/or services paid for by a Card. Severance 64. If at any time any provision of the Agreement is or becomes invalid, illegal or unenforceable in any jurisdiction in any respect, the validity, legality and enforceability of the remaining provisions thereof shall not in any way be affected or impaired thereby. 65. No provision in these Conditions shall affect your statutory rights under the Consumer Credit Act, 1995 or any regulations made thereunder. In the event of any conflict between these Conditions and such rights, your statutory rights shall prevail. Governing Law & Jurisdiction 66. The Agreement is governed by the laws of Ireland and is subject to the exclusive jurisdiction of the courts of Ireland. 67. The Agreement will be treated as having been executed within the Dublin Metropolitan area at AIB Card Services, Donnybrook House, Donnybrook, Dublin 4. Larger Version 68. Should you wish to have a copy of these Conditions in a larger print, they will be made available on request. What to do if you have a complaint 69. In the event that you wish to make a complaint you may do so by writing to us, at the address below. If you are still not satisfied you may be entitled to take your complaint to the Financial Services Ombudsman at 3rd Floor, Lincoln House, Lincoln Place, Dublin 2. Contacting us AIB Card Services, Donnybrook, Dublin 4. Telephone: Allied Irish Bank, plc is regulated by the Financial Regulator. Allied Irish Banks, p.l.c. Registered in Ireland No Registered Office: Bankcentre, Ballsbridge, Dublin 4. If you are posting your application to us please place it in an envelope addressed as follows: AIB Card Services, PO Box 708, Donnybrook House, Donnybrook, Dublin 4.

7 COLLEGE AFFINITY Credit Card INFORMATION Information about your Distance Contract Effective from 1 st October 2006 European Communities (Distance Marketing of Consumer Financial Services) Regulations About Us We are Allied Irish Banks, p.l.c. whose principal business is the provision of financial services. Our registered office is at Bankcentre, Ballsbridge, Dublin 4. We are registered at the Companies Registration Office, Dublin. Our registered number is Our VAT number is IE 8E86432H. We are regulated by the Financial Regulator, PO Box 9138, College Green, Dublin 2. About Our Credit Cards We issue credit cards. These cards allow you to make payments for goods and services by use of the card without having to pay cash. Cards can also be used at automated teller facilities (ATMs) to obtain cash. We keep a card account for you and bill you for all card transactions. Our credit cards are subject to terms and conditions which will be notified to you in full with your credit card application. This will constitute our agreement with you in relation to the credit card (the Agreement ). Pricing The total price for the card service is made up of government stamp duty, interest, cash advance fees, currency conversion fees and the other charges outlined below. 1. Government Stamp Duty Government stamp duty of 40 is charged annually per Credit Card account. 2. Interest Card Type APR- Purchases 1 Standard APR - Purchases APR- Cash APR Balance Transfers 2 Standard College Affinity 6.9% 13.9% (variable) 18.65% (variable) 6.9% Visa Credit Card Gold College Affinity 6.9% 10.9% (variable) 15.96% (variable) 6.9% Visa Credit Card 1 Special introductory rate of 6.9% APR on purchases only, will apply to the accounts of new AIB credit cardholders only, for the first 12 months from the date the account is opened. At the end of those 12 months the APR reverts back to the standard rate applicable to the product at that time. 2 Special introductory rate of 6.9% APR on Balance Transfers only, will apply to the accounts of new AIB credit cardholders only, for the first 12 months from the date the account is opened. At the end of those 12 months the APR reverts back to the standard rate applicable to the product at that time. 3. Cash Advance Fee 1.90 or 1.5% of the transaction value whichever is greater. 4. Currency Conversion Fees AIB Visa AIB FX Transactions Visa Europe Region 1.75% FX Transactions Visa Rest of World 2.75% Note: No currency conversion fees apply on Euro transactions.

8 5. Late Payment Charge Should payment not be made in accordance with the Agreement, an administration charge of 3.81 will be debited to the card account. 6. Over Limit Charge If on your statement date you are exceeding the agreed limit on your Credit Card account you will be liable for a fee of Returned Payment Charge Should any payment either by cheque or direct debit be returned unpaid, an administration charge of 4.44 will be debited to the account. 8. Miscellaneous Charges Supplying copy sales voucher on request 3.81 Supplying copy statement on request 2.54 These rates may change. The above information is valid as of 1st October Arrangements for Payment You can pay your credit card bill by direct debit, standing order, AIB Internet Banking or by credit transfer from your bank. Your Right to Cancel You will not be bound by your credit card application or the Agreement unless and until you or we, debit your card for the first time. If your credit card has not being debited, you have the right to cancel your Agreement with us within 14 days of your receiving the Agreement or a copy of it. By sending a written note of cancellation to The Manager, Card Issuing, Donnybrook House, Dublin 4, quoting details of the Agreement. If you avail of this right, your account will not be charged Government Stamp Duty. Your Agreement with us is not subject to a minimum duration and if you do not exercise your right of cancellation the terms of the agreement will continue to apply for an unspecified period. In addition to your right to cancel within the 14 day period, you have the right to terminate the Agreement at any time by cutting your card in two and returning it to The Manager, Card Issuing, Donnybrook House, Dublin 4. We can terminate the agreement by giving you written notice requiring you to cut your card in two and return it to us. If you cancel your Agreement you will be liable to repay the outstanding balance on the card on that date and all outstanding card transactions, fees, charges, stamp duties, government levies and all accrued but unpaid interest. The Agreement will be governed by the laws of Ireland and the Courts of Ireland will have exclusive jurisdiction to resolve any disputes. This will include any negotiations or discussions prior to you entering into the Agreement. The Agreement and all information and communication with you will be in English. What to do if you have a complaint In the event that you wish to make a complaint you may do so by writing to our Service Quality Unit, Card Issuing, Donnybrook House, Donnybrook, Dublin 4. If you are still not satisfied you are entitled to take your complaint to the Financial Services Ombudsman, 3rd Floor, Lincoln House, Lincoln Place, Dublin 2.

9 Supplier College affinity CREDIT CARD : TRAVEL INSURANCE Information about your Distance Contract Effective from 1 st October The AIB Credit Card Travel Insurance (the Policy) is provided by ACE European Group Limited (ACE), through AIB Insurance Services Limited. ACE is an insurance provider, and is regulated by the Financial Regulator ( Registered in Ireland, Number Address: ACE European Group Limited, Guild House, Guild Street, I.F.S.C., Dublin 1 2. The insurance mediation service is provided by AIB Insurance Services Limited and involves the introduction of ACE to you and arrangement of the Policy. AIB Insurance Services is a wholly owned subsidiary of Allied Irish Banks, p.l.c. AIB Insurance Services Limited is a Multi Agency Intermediary regulated by the Financial Regulator ( Registered in Ireland, Number Address: AIB Insurance Services Limited, Bankcentre, Ballsbridge, Dublin 4. About AIB Credit Card Travel Insurance The policy provides annual cover to i) The Cardholder; and ii) his / her Partner and accompanying Children under 18 or under 23 if in full-time education; and iii) Authorised user (if applicable). Provided at least 50% of the fares have been charged to the card. Maximum period for any one trip is 45 days. Age limit is 75 years. The Policy provides annual cover for (as defined in the full Policy terms and conditions): Cancellation and curtailment, Travel Delay, Personal Liability, Legal Advice and Expenses, Personal Accident, Medical Expenses, Hospital Benefit, Additional Travel Expenses, Loss of Personal Property and Baggage, Personal Property Delay, Loss of Passport and other specified documents, ACE Rescue/Repatriation, Hijack. The Policy will cost 125 per annum (if the cover is not already included as part of your annual card fee) and this will be debited to your credit card account with Allied Irish Bank plc. AIB Insurance Services Limited will not charge you directly for its introduction and arrangement service. Please also note that other taxes or charges may exist that neither ACE or AIB Insurance Services Limited pay or impose themselves. You have a legal right to cancel the Policy within 14 days of receiving full Policy terms and conditions. You will receive a full refund provided you have not taken or booked a trip abroad during the 14 day period, by writing to AIB Credit Card Centre, PO Box 708, Donnybrook House, Donnybrook, Dublin 4. If you do not exercise your right to cancel, your Policy will continue for one year and be renewable annually. ACE may cancel the policy by giving you 30 days notice in writing. The negotiations and discussions prior to, and the Policy itself, will be governed by the laws of Ireland and the Courts of Ireland will have exclusive jurisdiction to resolve any dispute. The Policy and all information and communications prior to entering into the Policy with you will be in English. In the event that you wish to make a complaint under the Policy or for any service provided by AIB Insurance Services Limited, you should contact the Manager, AIB Insurance Services Limited, Bank Centre, Ballsbridge, Dublin 4 in the first instance. If you are still not satisfied you are entitled to take your complaint to the Financial Services Ombudsman at 3rd Floor, Lincoln House, Lincoln Place, Dublin 2 or contact the Financial Regulator on the consumer helpline at The above information is valid as at the Effective From date listed above. AIB Insurance Services Limited has no interest in the share capital of ACE. Neither ACE nor any parent of ACE has an interest in the share capital of AIB Insurance Services Limited. AIB Insurance Services Limited offers travel insurance through ACE exclusively. This is only one of the insurance products offered through AIB Insurance Services Limited. If you have any questions as to the suitability of this product for you, please contact the AIB Service Quality Unit on for further information. The above should be read in conjunction with the full copy of the Evidence of Cover This information is provided pursuant to the European Communities (Distance Marketing of Consumer Financial Services) Regulations 2004 and the European Communities (Insurance Mediation) Regulations 2005.

10 Supplier COLLEGE AFFINITY CREDIT CARD: Card Protection Information about your Distance Contract Effective from 1 st October The Card Protection service (the Policy) is provided by Pinnacle Insurance plc (Pinnacle), through AIB Insurance Services Limited. Pinnacle is authorised and regulated by the United Kingdom Financial Services Authority ( Registered in the United Kingdom, Number Address: Pinnacle House, A1 Barnet Way, Borehamwood, Hertfordshire, WD6 2XX, United Kingdom. 2. The insurance mediation service is provided by AIB Insurance Services Limited and involves the introduction of Pinnacle to you and arranging the policy. AIB Insurance Services is a wholly owned subsidiary of Allied Irish Banks, p.l.c. AIB Insurance Services Limited is a Multi Agency Intermediary regulated by the Financial Regulator ( Registered in Ireland, Number Address: AIB Insurance Services Limited, Bankcentre, Ballsbridge, Dublin 4. About Pinnacle Card Protection In the event your credit card (or other cards registered with Pinnacle) is lost or stolen, Pinnacle will cancel the relevant card(s) and request replacement(s), can provide you with up to 1000 emergency cash advance facility, and provide assistance in obtaining emergency travel documentation and ticket replacement, if necessary. Pinnacle will charge you 16 per annum and this will be debited to your credit card account with Allied Irish Bank plc. Pinnacle will not pay for losses arising from fraud, if a cardholder makes a dishonest claim under the policy, all rights to the benefits under the policy will be lost. If anything that is covered by the policy is lost or stolen, the cardholder must report it to the Police and Pinnacle within 24 hours of discovering the loss. The cardholder must obtain a full report from the Police confirming the loss. A full Police reference number, address and telephone number of the police station where the report was made will be required. You will not be charged by AIB Insurance Services Limited for its introduction and arrangement service. Please note that other taxes or charges may exist that neither Pinnacle or AIB Insurance Services Limited pay or impose themselves. You have a legal right to cancel the Policy within 14 days of your receiving the full Policy terms and conditions, however, in addition to this right, Pinnacle give you the right to cancel the Policy in the first 90 days. In either case you will receive a full refund, provided no claims have been made. After the 90 day period has expired, you may cancel the Policy by giving 7 days notice in writing; no refund will be available in these circumstances. To cancel, write to Pinnacle at the above address or phone Pinnacle Insurance plc may cancel the policy by giving you 30 days notice in writing. The Insurance is automatically cancelled if: The premium is not paid You submit a claim knowing it to be false, fraudulent or a misrepresentation. Either you or Pinnacle cancels the cover. The negotiations and discussions prior to, and the Policy itself, will be governed by the laws of Ireland and the Courts of Ireland will have exclusive jurisdiction to resolve any disputes. The Policy and all information and communications prior to entering into the Policy with you will be in English. In the event that you wish to make a complaint under the Policy or for any service provided by AIB Insurance Services Limited, you should contact either Pinnacle or AIB Insurance Services Limited at the addresses shown above in the first instance. If you are still not satisfied you are entitled to take your complaint to the Financial Services Ombudsman at 3rd Floor, Lincoln House, Lincoln Place, Dublin 2 or contact the Financial Regulator on the consumer helpline at The above information is valid as at the Effective From date listed above. AIB Insurance Services Limited has no interest in the share capital of Pinnacle. Neither Pinnacle nor any parent of Pinnacle has an interest in the share capital of AIB Insurance Services Limited. AIB Insurance Services Ltd. recommends that all customers assess their Card Protection Insurance needs. AIB Insurance Services Ltd. offer only one Card Protection Insurance product which is underwritten by Pinnacle Insurance p.l.c. AIB Insurance Services Ltd. deem this product suitable for customer's Card Protection Insurance needs. The Policy provides insurance cover in the event your AIB credit card (or other cards registered with Pinnacle) is lost or stolen. This is the only insurance product of this particular type offered through AIB Insurance Services Limited and the Plan provides suitable cover for the AIB credit cards through which it is provided. If you have any questions as to the suitability of this product for you, please contact AIB Card Protection Services Centre on for further information. Financial Services Compensation Scheme Pinnacle are covered by the Financial Services Compensation Scheme (the "Scheme"). You may be entitled to compensation from the Scheme if they cannot meet their obligations. The amount of compensation depends on the type of business. Further information about compensation arrangements is available from the Financial Services Compensation Scheme, telephone number The above should be read in conjunction with the full copy of the Evidence of Cover The above information is subject to the provision of appropriate evidence of cover This information is provided pursuant to the European Communities (Distance Marketing of Consumer Financial Services) Regulations 2004 and the European Communities (Insurance Mediation) Regulations 2005.

11 You are eligible if you are: COLLEGE AFFINITY CREDIT CARD: PAYMENT PROTECTION PLAN Over 18 years old and under 65 at the start date, and Information about your Distance Contract Effective from 1 st October 2006 in gainful employment in the Republic of Ireland, Northern Ireland, or Great Britain (including Channel Islands and Isle of Man) for at least 16 hours per week (or the equivalent of 70 hours per month) and have been for the previous 6 months*, and Actively at work and not absent due to accident or sickness**, and ordinarily resident in the Republic of Ireland, Northern Ireland, or Great Britain (including Channel Islands and Isle of Man). * if you have not been in work for 6 months your cover for disability and involuntary unemployment will start when you have worked the necessary 6 months. ** if you are unable to work due to accident or sickness your cover for disability will start when you resume work. Supplier The Payment Protection Plan (the Plan) is provided by Combined Life Assurance Company Limited (CLAC) and London General Insurance Company Limited, (LGI) through AIB Insurance Services Limited. 1. The life benefit service forming part of the Plan is provided by CLAC through AIB Insurance Services Limited. CLAC is registered in Ireland with company number E CLAC is authorised and regulated by the Financial Regulator ( Address: PO Box No.9138, College Green, Dublin 2 (Ireland). 2. The critical illness, disability or involuntary unemployment benefit service forming part of the plan is provided by LGI through AIB Insurance Services Limited. LGI is registered in Ireland with registered number E LGI is authorised and regulated by the Financial Regulator (www. financialregulator.ie). Address: PO Box No.9138, College Green, Dublin 2 (Ireland). 3. The insurance mediation service is provided by AIB Insurance Services Limited and involves the introduction of CLAC and LGI to you and arranging the plan. AIB Insurance Services is a wholly owned subsidiary of Allied Irish Banks, p.l.c. AIB Insurance Services Limited is a Multi Agency Intermediary regulated by the Financial Regulator ( Address: AIB Insurance Services Limited, Bankcentre, Ballsbridge, Dublin 4. Our registered number is How much does it cost? The cover provided by the Plan will cost 60 cent per 100 of your variable outstanding balance and this will be debited to your credit card account with Allied Irish Bank p.l.c. on a monthly basis. AIB Insurance Services Limited will not charge you directly for its introduction and arrangement service. Please also note that other taxes or charges may exist other than those which AIB Insurance Services Limited, CLAC or LGI pay or impose themselves. How do you apply for a Payment Protection Plan and how long does it last? The Plan is only available when applying for a new Credit Card. Cover is provided on a monthly basis providing the relevant premium is paid. There is no minimum duration for cover under the Plan. How does the cover work? Disability (Accident /Sickness) If you can t work because of an accident or sickness, a payment equivalent to 10% of your outstanding balance* will be made for every 30 complete consecutive days you are out of work, for a maximum of 12 months. Involuntary Unemployment. If you become involuntarily unemployed due to redundancy or you are dismissed for reasons other than wilful misconduct, dishonesty or fraud, or your business ceases to trade, a payment equivalent to 10% of your outstanding balance* will be made for every 30 complete consecutive days you are unemployed for up to 12 months per claim. Critical illness. If you suffer any one of the 7 specified critical illnesses (coronary artery bypass surgery/cancer/heart attack/major organ transplant/stroke/severe kidney failure/loss of limb or sight) your outstanding balance, at the date of diagnosis (less any arrears), will be paid in full to a maximum of 15,500. Loss of life. If you die during the term of your policy your outstanding balance (less any arrears at the date of death) will be paid in full to a maximum of 15,500. * the outstanding balance at the date of your last statement prior to the commencement of your disability or involuntary unemployment.

.")

12 What isn t covered Main Exclusions Life Exclusions There are no general & specific exclusions applicable to the loss of life benefit General Exclusions No benefit will be payable for critical illness, disability or involuntary unemployment in relation to HIV and/or any HIV related illness including AIDS, war, civil commotion, radioactive contamination or the use of alcohol or drugs. Critical Illness Exclusions If your critical illness is diagnosed within 30 days of the starting date and if at any time it results directly or indirectly from a pre-existing medical condition as defined in the terms. Disability Exclusions For disability benefit if your disability results directly or indirectly from: a pre-existing medical condition as defined in the policy terms; any psychiatric, mental or nervous disorders, unless it is due to organic mental disease or psychosis; backache, unless a doctor provides medical evidence showing definite symptoms of restriction of movement. Involuntary Unemployment Exclusions unless your involuntary unemployment is immediately preceded by 6 months continuous employment or self-employment; if it starts within 90 days of the starting date; if at the starting date you knew you were to become unemployed or it is reasonable for us to conclude that you knew that it was likely to happen; if it is brought about by the expiry of a fixed-term contract, unless certain conditions are met. Customer Care In the event that you wish to make a complaint under the Plan or for any service provided by AIB Insurance Services Limited, you should contact the Manager, AIB Insurance Services Limited, Bankcentre, Ballsbridge, Dublin 4 in the first instance. If you are still not satisfied you are entitled to take your complaint to the Financial Services Ombudsman at 3rd Floor, Lincoln House, Lincoln Place, Dublin 2 or contact the Financial Regulator on the consumer helpline at You have a legal right to cancel the Plan within 30 days of your receiving the full Plan terms and conditions. If you decide to cancel the Plan within 30 days, you will receive a full refund of the premium paid although if a claim has been paid the insurer may recover any costs incurred. To cancel, write to AIB Insurance Services Limited at the address shown above. The Plan can be cancelled at any time after the expiry of the 30 day period by notifying AIB Insurance Services Limited at the address shown above in writing. No refund will be available in these circumstances. CLAC and LGI may cancel the Plan at any time by giving you 30 days notice in writing. The Plan is automatically cancelled if: The monthly premium for the Plan is not paid; Your credit card agreement with Allied Irish Bank plc (to which the Plan relates) is terminated You or CLAC or LGI cancels the cover. The negotiations and discussions prior to, and the Plan itself, will be governed by the laws of Ireland and the Courts of Ireland will have exclusive jurisdiction to resolve any dispute. The Plan and all information and communications prior to entering into the Plan with you will be in English The above information is valid as at the Effective From date listed above. AIB Insurance Services Limited holds no interest in the share capital of CLAC or LGI. Neither CLAC or LGI nor any parent of CLAC or LGI holds any interest in the share capital of AIB Insurance Services Limited. AIB Insurance Services Limited offers payment protection insurance through a combination of CLAC and LGI exclusively. The Plan provides insurance cover in certain instances of disability, involuntary unemployment, critical illness and loss of life. AIB Insurance recommends that all customers consider taking out payment protection insurance. AIB Insurance Services offers payment protection insurance through a combination of CLAC (Combined Life Assurance Limited) and LGI (London General Insurance Company) exclusively. AIB Insurance Services Ltd. offers only one credit card payment protection insurance product and considers this product to be suitable for customers' credit card payment protection insurance needs. If you have any questions as to the suitability of this product for you, please contact the AIB Payment Protection Call Centre on for further information. The above should be read in conjunction with the full copy of the Evidence of Cover This information is provided pursuant to the European Communities (Distance Marketing of Consumer Financial Services) Regulations 2004 and the European Communities (Insurance Mediation) Regulations AIBPICOLLAFF 10/06

Debit Card Terms and Conditions of Use. This document contains important information. Please read carefully and retain for future reference.

Debit Card Terms and Conditions of Use This document contains important information. Please read carefully and retain for future reference. Effective from 2nd April 2015 Contents Definitions page 2 Looking

Debit Card Terms and Conditions of Use This document contains important information. Please read carefully and retain for future reference. Effective from 2nd April 2015 Contents Definitions page 2 Looking

APPLICATION FORM FOR THE BROWN THOMAS MASTERCARD AND ENCORE REWARDS PROGRAMME EXPERIENCE THE EXTRAORDINARY ENCORE REWARDS

APPLICATION FORM FOR THE BROWN THOMAS MASTERCARD AND ENCORE REWARDS PROGRAMME EXPERIENCE THE EXTRAORDINARY ENCORE REWARDS 1 The Brown Thomas MasterCard Infinitely Rewarding As a Brown Thomas MasterCard

APPLICATION FORM FOR THE BROWN THOMAS MASTERCARD AND ENCORE REWARDS PROGRAMME EXPERIENCE THE EXTRAORDINARY ENCORE REWARDS 1 The Brown Thomas MasterCard Infinitely Rewarding As a Brown Thomas MasterCard

ATM/Debit Terms and conditions

ATM/Debit Terms and conditions www.bankofireland.com Bank of Ireland is regulated by the Central Bank of Ireland. 37-1108R (11/11) Terms and Conditions ATM Card and Visa Debit Card 1.0 Definitions of Terms

ATM/Debit Terms and conditions www.bankofireland.com Bank of Ireland is regulated by the Central Bank of Ireland. 37-1108R (11/11) Terms and Conditions ATM Card and Visa Debit Card 1.0 Definitions of Terms

CUSTOMER COPY Credit Agreement

CUSTOMER COPY Credit Agreement IMPORTANT INFORMATION 1. Amount of credit limit: Credit limit is notified to you from time to time. 2. Duration of agreement: No fixed period, see Condition 8 of the Terms

CUSTOMER COPY Credit Agreement IMPORTANT INFORMATION 1. Amount of credit limit: Credit limit is notified to you from time to time. 2. Duration of agreement: No fixed period, see Condition 8 of the Terms

AIB Visa Corporate and Business Cards. Additional Cardholder Form AIB/WEBVF1 06/11 AIB046C00007BRA5

AIB Visa Corporate and Business Cards Additional Cardholder Form The AIB Visa Corporate & Business Card Suite * This is not a substitute for fully comprehensive Travel Insurance CLASSIC PREMIER EXECUTIVE

AIB Visa Corporate and Business Cards Additional Cardholder Form The AIB Visa Corporate & Business Card Suite * This is not a substitute for fully comprehensive Travel Insurance CLASSIC PREMIER EXECUTIVE

Terms and Conditions for the Online Notice Deposit 7 & 21 Accounts

Terms and Conditions for the Online Notice Deposit 7 & 21 Accounts This document contains important information. Please read carefully and retain for future reference. July 2014 Terms and Conditions These

Terms and Conditions for the Online Notice Deposit 7 & 21 Accounts This document contains important information. Please read carefully and retain for future reference. July 2014 Terms and Conditions These

AIB Visa Corporate and Business Cards. Additional Cardholder Form

AIB Visa Corporate and Business Cards Additional Cardholder Form The AIB Visa Corporate & Business Card Suite. Classic This card is ideal for SMEs or for larger companies looking for an easy payment tool

AIB Visa Corporate and Business Cards Additional Cardholder Form The AIB Visa Corporate & Business Card Suite. Classic This card is ideal for SMEs or for larger companies looking for an easy payment tool

Bacstel-IP. Customer Agreement for the Bacstel-IP Direct Service

Bacstel-IP Customer Agreement for the Bacstel-IP Direct Service Customer Agreement for the Bacstel-IP Direct Service 1. INTRODUCTION This agreement relates to the provision of the Bacstel-IP Service (

Bacstel-IP Customer Agreement for the Bacstel-IP Direct Service Customer Agreement for the Bacstel-IP Direct Service 1. INTRODUCTION This agreement relates to the provision of the Bacstel-IP Service (

First Trust Bank Visa Card / First Trust Bank MasterCard INTO Visa Card / ICAI Gold MasterCard Terms & Conditions of use

First Trust Bank Visa Card / First Trust Bank MasterCard INTO Visa Card / ICAI Gold MasterCard Terms & Conditions of use Effective date 30 June 2015 These conditions apply to the Agreement (referred to

First Trust Bank Visa Card / First Trust Bank MasterCard INTO Visa Card / ICAI Gold MasterCard Terms & Conditions of use Effective date 30 June 2015 These conditions apply to the Agreement (referred to

Diners Club Corporate Travel System Terms and Conditions

Diners Club Corporate Travel System Terms and Conditions Contents 1 Definitions 4 2 Accepting these Terms and Conditions 7 3 Authorised Users and Authorised Cardholders 7 4 Authorised Travel Agents 7

Diners Club Corporate Travel System Terms and Conditions Contents 1 Definitions 4 2 Accepting these Terms and Conditions 7 3 Authorised Users and Authorised Cardholders 7 4 Authorised Travel Agents 7

365 Phone, Online and Mobile Banking Terms and Conditions - Republic of Ireland Effective from 25 th November 2013

365 Phone, Online and Mobile Banking Terms and Conditions - Republic of Ireland Effective from 25 th November 2013 1.0 Definitions of Terms used in this Document 2.0 Accounts 3.0 Mandates 4.0 SEPA Transfers

365 Phone, Online and Mobile Banking Terms and Conditions - Republic of Ireland Effective from 25 th November 2013 1.0 Definitions of Terms used in this Document 2.0 Accounts 3.0 Mandates 4.0 SEPA Transfers

Basic cash account. This document can be made available in Braille, large print or audio upon request. Please ask any member of staff for details.

Basic cash account www.bankofireland.co.uk This document can be made available in Braille, large print or audio upon request. Please ask any member of staff for details. Bank of Ireland UK is a trading

Basic cash account www.bankofireland.co.uk This document can be made available in Braille, large print or audio upon request. Please ask any member of staff for details. Bank of Ireland UK is a trading

Rothschild Visa Card Terms and Conditions

Rothschild Visa Card Terms and Conditions These Rothschild Visa Card Terms and Conditions (June 2010 edition) are in addition to and supplemental to the Bank s standard Terms and Conditions (October 2007

Rothschild Visa Card Terms and Conditions These Rothschild Visa Card Terms and Conditions (June 2010 edition) are in addition to and supplemental to the Bank s standard Terms and Conditions (October 2007

Business Debit Card Application form

Business Debit Card Application form 1 Contents Applying for the AIB Business Debit Card... 3 Section A - Business Details... 4 Section B - Authorised Users section... 5 Section C - Resolution... 6 Section

Business Debit Card Application form 1 Contents Applying for the AIB Business Debit Card... 3 Section A - Business Details... 4 Section B - Authorised Users section... 5 Section C - Resolution... 6 Section

first direct credit card terms