FOR IMMEDIATE RELEASE March 30, 2011

|

|

|

- Julian Gilmore

- 8 years ago

- Views:

Transcription

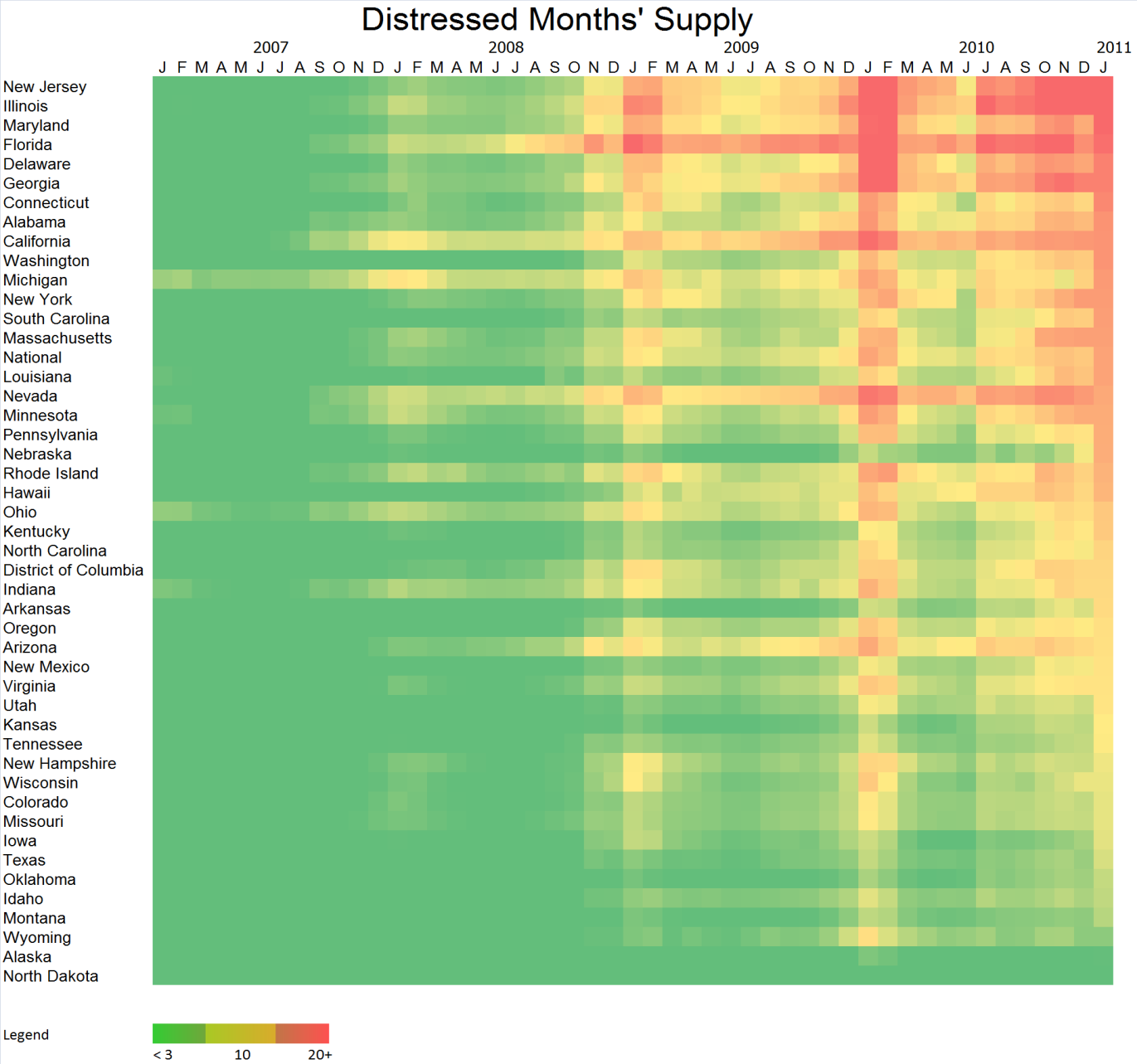

1 Contact Information Below CoreLogic Reports Shadow Inventory Declines Slightly, However, Nine Months Worth of Supply Remains Accelerated Loan Modifications and Short Sales Could Reduce Inventory SANTA ANA, Calif., CoreLogic (NYSE: CLGX), a leading provider of consumer, financial and property information and business services, reported today that the current residential shadow inventory as of January 2011 declined to 1.8 million units, representing a nine months supply. This is down slightly from 2.0 million units, also a nine months supply, from a year ago. CoreLogic research indicates that although a material portion of the shadow inventory can be optimally treated via modification or short sale, only a small share can be effectively remediated from the shadow supply. CoreLogic estimates current shadow inventory, also known as pending supply, by calculating the number of distressed properties not currently listed on multiple listing services (MLS) that are seriously delinquent (90 days or more), in foreclosure and real estate owned (REO) by lenders. Transition rates of delinquency to foreclosure and foreclosure to REO are used to identify the currently distressed non-listed properties most likely to become REO properties. Properties that are not yet delinquent but may become delinquent in the future are not included in the estimate of the current shadow inventory. Shadow inventory is typically not included in the official metrics of unsold inventory. Data Highlights: The shadow inventory of residential properties as of January 2011 fell to 1.8 million units, or nine months worth of supply, down from 2.0 million, also nine months supply from a year ago. Of the 1.8-million unit current shadow inventory supply, 870,000 units are seriously delinquent (4.2 months supply), 445,000 are in some stage of foreclosure (2.1 months supply) and 470,000 are already in REO (2.2 months supply).

2 For the first time, CoreLogic has examined how loan modifications and short sales could reduce shadow inventory levels. The analysis took into account optimal treatment methods, based on net present value calculations, as well as expected severity and redefault rates for loan modifications and short sales. Based on these factors, loan modifications and short sales could potentially reduce shadow supply by one-half, but low borrower response rates to lender outreach and high modification re-default rates would render the optimal treatment s impact to be small. In addition to the current shadow inventory supply, there are nearly 2 million current negative equity loans that are more than 50 percent upside down that will likely become shadow supply in the near future. The highest levels of distressed months supply, which is the ratio of the number of properties that are 90 days or more delinquent to the number of home sales, are in New Jersey, Illinois and Maryland. The driving force behind these states with the highest distressed supply is a combination of higher than average 90+ day delinquencies and lower sales activity. The states with the lowest distressed months supply are where the boom/bust did not occur and include North Dakota, Alaska and Wyoming. The largest state with the lowest level of distressed months supply was Texas. Mark Fleming, chief economist for CoreLogic commented, While the trend of the shadow inventory is improving somewhat, the current level and distressed months supply remain very high. The short-term weakness in prices and longer-term weakness in the drivers that affect the housing market imply that excess supply will remain high for an extended period of time.

3

4 Methodology: CoreLogic utilized its LoanPerformance Servicing and Securities databases to size the number of 90+ day delinquencies, foreclosures and REOs. Roll rates, which measure the proportion of loans that were in one stage of default that rolled to the next stage of default over a period of time, were applied to the number of loans in default by each stage of default. This calculation allowed for estimating the number of loans that were proceeding from earlier to later stages of default. Then we calculated the share of loans in default that are currently listed on MLS by matching public record properties in default to MLS active listings. We applied the percentage of defaulted loans that are being listed to our estimate of outstanding loans that will proceed to further stages of default to calculate the pending supply inventory by stage of default and added that to the visible inventory that is reported for existing homes and new homes by the National Association of Realtors and the Bureau of the Census, respectively. To determine months supply for visible and shadow inventories, we utilized the number of non-seasonally adjusted home sales according to CoreLogic. About CoreLogic CoreLogic is a leading provider of consumer, financial and property information, analytics and services to business and government. The company combines public, contributory and proprietary data to develop predictive decision analytics and provide business services that bring dynamic insight and transparency to the markets it serves. CoreLogic has built the

5 largest and most comprehensive U.S. real estate, mortgage application, fraud, and loan performance databases and is a recognized leading provider of mortgage and automotive credit reporting, property tax, valuation, flood determination, and geospatial analytics and services. More than one million users rely on CoreLogic to assess risk, support underwriting, investment and marketing decisions, prevent fraud, and improve business performance in their daily operations. Formerly, the information solutions group of The First American Corporation, CoreLogic began trading under the ticker CLGX on the NYSE on June 2, The company, headquartered in Santa Ana, Calif., has more than 10,000 employees globally with 2010 revenues of $1.6 billion. For more information visit CoreLogic is a registered trademark of CoreLogic. Media Contact: Investor Contact: Alyson Austin Dan Smith Corporate Communications Investor Relations newsmedia@corelogic.com investor@corelogic.com ###

FOR IMMEDIATE RELEASE June 12, 2013

Media Contacts Below CORELOGIC REPORTS 850,000 MORE RESIDENTIAL PROPERTIES RETURN TO POSITIVE EQUITY IN FIRST QUARTER OF 2013 9.7 Million Residential Properties with a Mortgage Still in Negative Equity

Media Contacts Below CORELOGIC REPORTS 850,000 MORE RESIDENTIAL PROPERTIES RETURN TO POSITIVE EQUITY IN FIRST QUARTER OF 2013 9.7 Million Residential Properties with a Mortgage Still in Negative Equity

Suite. Market - Leading Data, Analytics & Scoring

Suite Market - Leading Data, Analytics & Scoring We have the tools that enable you to avoid risk. Market-Leading Data, Analytics & Scoring Suite As residential mortgage fraud continues to evolve and escalate,

Suite Market - Leading Data, Analytics & Scoring We have the tools that enable you to avoid risk. Market-Leading Data, Analytics & Scoring Suite As residential mortgage fraud continues to evolve and escalate,

CoreLogic National Foreclosure Report

CoreLogic National Foreclosure Report JUNE 2014 3.9% In June, the foreclosure inventory was down 3.9 percent from May 2014, representing 32 months of consecutive year-over-year declines. While 32 straight

CoreLogic National Foreclosure Report JUNE 2014 3.9% In June, the foreclosure inventory was down 3.9 percent from May 2014, representing 32 months of consecutive year-over-year declines. While 32 straight

The Obama Administration s Efforts To Stabilize the Housing Market and Help American Homeowners

The Obama Administration s Efforts To Stabilize the Housing Market and Help American Homeowners February 2015 U.S. Department of Housing and Urban Development Office of Policy Development and Research

The Obama Administration s Efforts To Stabilize the Housing Market and Help American Homeowners February 2015 U.S. Department of Housing and Urban Development Office of Policy Development and Research

Redefault Rates Improve for Recent Loan Modifications

Redefault Rates Improve for Recent Loan Modifications State Foreclosure Prevention Working Group Memorandum on Loan Modification Performance August 2010 Introduction and Summary of Key Findings For over

Redefault Rates Improve for Recent Loan Modifications State Foreclosure Prevention Working Group Memorandum on Loan Modification Performance August 2010 Introduction and Summary of Key Findings For over

The Obama Administration s Efforts To Stabilize The Housing Market and Help American Homeowners

The Obama Administration s Efforts To Stabilize The Housing Market and Help American Homeowners July 2013 U.S. Department of Housing and Urban Development Office of Policy Development Research U.S Department

The Obama Administration s Efforts To Stabilize The Housing Market and Help American Homeowners July 2013 U.S. Department of Housing and Urban Development Office of Policy Development Research U.S Department

National Foreclosure Report

National Foreclosure Report JANUARY 2015 2.7% In January, the foreclosure inventory was down 2.7 percent from December 20, representing 39 months of consecutive year-overyear declines. Job growth and homevalue

National Foreclosure Report JANUARY 2015 2.7% In January, the foreclosure inventory was down 2.7 percent from December 20, representing 39 months of consecutive year-overyear declines. Job growth and homevalue

The Obama Administration s Efforts To Stabilize The Housing Market and Help American Homeowners

The Obama Administration s Efforts To Stabilize The Housing Market and Help American Homeowners July 2014 U.S. Department of Housing and Urban Development Office of Policy Development and Research U.S

The Obama Administration s Efforts To Stabilize The Housing Market and Help American Homeowners July 2014 U.S. Department of Housing and Urban Development Office of Policy Development and Research U.S

The Obama Administration s Efforts To Stabilize The Housing Market and Help American Homeowners

The Obama Administration s Efforts To Stabilize The Housing Market and Help American Homeowners April 2014 U.S. Department U.S Department of Housing of Housing and Urban and Urban Development Development

The Obama Administration s Efforts To Stabilize The Housing Market and Help American Homeowners April 2014 U.S. Department U.S Department of Housing of Housing and Urban and Urban Development Development

The Obama Administration s Efforts To Stabilize the Housing Market and Help American Homeowners

The Obama Administration s Efforts To Stabilize the Housing Market and Help American Homeowners March 2015 U.S. Department of Housing and Urban Development Office of Policy Development and Research U.S

The Obama Administration s Efforts To Stabilize the Housing Market and Help American Homeowners March 2015 U.S. Department of Housing and Urban Development Office of Policy Development and Research U.S

The Obama Administration s Efforts To Stabilize The Housing Market and Help American Homeowners

The Obama Administration s Efforts To Stabilize The Housing Market and Help American Homeowners August 2013 U.S. Department of Housing and Urban Development Office of Policy Development Research U.S Department

The Obama Administration s Efforts To Stabilize The Housing Market and Help American Homeowners August 2013 U.S. Department of Housing and Urban Development Office of Policy Development Research U.S Department

The Distressed Property Market and Shadow Inventory in Florida: Estimates and Analysis

The Distressed Property Market and Shadow Inventory in Florida: Estimates and Analysis Introduction Florida was one of the states hardest hit by the real estate downturn. Delinquencies, foreclosures and

The Distressed Property Market and Shadow Inventory in Florida: Estimates and Analysis Introduction Florida was one of the states hardest hit by the real estate downturn. Delinquencies, foreclosures and

Report on Nevada s Housing Market

July Report on Nevada s Housing Market This series of reports on Nevada s Housing Market is co-presented by the Lied Institute for Real Estate Studies at the University of Nevada, Las Vegas and the State

July Report on Nevada s Housing Market This series of reports on Nevada s Housing Market is co-presented by the Lied Institute for Real Estate Studies at the University of Nevada, Las Vegas and the State

Black Knight Mortgage Monitor

Black Knight Mortgage Monitor Mortgage Market Performance Observations Data as of February, 2014 Month-end Focus Points Focus 1: Loan originations, property sales and underwriting criteria Focus 2: Modification

Black Knight Mortgage Monitor Mortgage Market Performance Observations Data as of February, 2014 Month-end Focus Points Focus 1: Loan originations, property sales and underwriting criteria Focus 2: Modification

The Obama Administration s Efforts To Stabilize The Housing Market and Help American Homeowners

The Obama Administration s Efforts To Stabilize The Housing Market and Help American Homeowners June 2013 U.S. Department of Housing and Urban Development Office of Policy Development Research U.S Department

The Obama Administration s Efforts To Stabilize The Housing Market and Help American Homeowners June 2013 U.S. Department of Housing and Urban Development Office of Policy Development Research U.S Department

Understanding Credit & Credit Risk Scores. Plus, Helping Consumers Get The Most From Their Credit Rating

Understanding Credit & Credit Risk Scores Plus, Helping Consumers Get The Most From Their Credit Rating This document contains actual excerpts from Fair Isaac, TransUnion, Equifax and Experian. CoreLogic

Understanding Credit & Credit Risk Scores Plus, Helping Consumers Get The Most From Their Credit Rating This document contains actual excerpts from Fair Isaac, TransUnion, Equifax and Experian. CoreLogic

Equity Report FOURTH QUARTER 2014

Equity Report FOURTH QUARTER 2014 Negative equity continued to be a serious issue for the housing market and the U.S. economy at the end of 2014 with 5.4 million homeowners still underwater. We expect

Equity Report FOURTH QUARTER 2014 Negative equity continued to be a serious issue for the housing market and the U.S. economy at the end of 2014 with 5.4 million homeowners still underwater. We expect

Minneapolis St. Paul Residential Real Estate Index

University of St. Thomas Minneapolis St. Paul Residential Real Estate Index Welcome to the latest edition of the UST Minneapolis St. Paul Residential Real Estate Index. The University of St Thomas Residential

University of St. Thomas Minneapolis St. Paul Residential Real Estate Index Welcome to the latest edition of the UST Minneapolis St. Paul Residential Real Estate Index. The University of St Thomas Residential

MORTGAGE PAYMENT RESET The Issue and the Impact

May 30, 2007 MORTGAGE PAYMENT RESET The Issue and the Impact Christopher L. Cagan, Ph.D. Director of Research and Analytics First American CoreLogic 4 First American Way Santa Ana, CA 92707 (714) 250.6177

May 30, 2007 MORTGAGE PAYMENT RESET The Issue and the Impact Christopher L. Cagan, Ph.D. Director of Research and Analytics First American CoreLogic 4 First American Way Santa Ana, CA 92707 (714) 250.6177

How The $25 Billion Foreclosure Settlement Will Really Affect The Housing Market

How The $25 Billion Foreclosure Settlement Will Really Affect The Housing Market Well, struggling homeowners, that long-anticipated mortgage relief plan President Obama has been alluding to has finally

How The $25 Billion Foreclosure Settlement Will Really Affect The Housing Market Well, struggling homeowners, that long-anticipated mortgage relief plan President Obama has been alluding to has finally

U.S. and Regional Housing Markets

U.S. and Regional Housing Markets House Prices Boom, Bust and Rebound Index, 1991: Q1=1* 3 CoreLogic house price index Real FHFA house price index 25 2 15 1 5 1991 199 1997 2 23 26 29 212 215 *Seasonally

U.S. and Regional Housing Markets House Prices Boom, Bust and Rebound Index, 1991: Q1=1* 3 CoreLogic house price index Real FHFA house price index 25 2 15 1 5 1991 199 1997 2 23 26 29 212 215 *Seasonally

HOME AFFORDABLE MODIFICATION PROGRAM BASE NET PRESENT VALUE (NPV) MODEL SPECIFICATIONS

MODEL SPECIFICATIONS") Overview HOME AFFORDABLE MODIFICATION PROGRAM BASE NET PRESENT VALUE (NPV) MODEL SPECIFICATIONS As a part of the Making Home Affordable Program, we are providing standardized guidance and a base net present

Overview HOME AFFORDABLE MODIFICATION PROGRAM BASE NET PRESENT VALUE (NPV) MODEL SPECIFICATIONS As a part of the Making Home Affordable Program, we are providing standardized guidance and a base net present

Obama Administration Efforts to Stabilize the Housing Market and Help American Homeowners

The Obama Administration s Efforts To Stabilize The Housing Market and Help American Homeowners March 21 U.S. Department of Housing and Urban Development Office of Policy Development Research U.S Department

The Obama Administration s Efforts To Stabilize The Housing Market and Help American Homeowners March 21 U.S. Department of Housing and Urban Development Office of Policy Development Research U.S Department

NATIONAL DELINQUENCY SURVEY: FACTS

NATIONAL DELINQUENCY SURVEY: FACTS The NDS is a voluntary survey of over 120 mortgage lenders, including mortgage banks, commercial banks, thrifts, savings and loan associations, subservicers and life

NATIONAL DELINQUENCY SURVEY: FACTS The NDS is a voluntary survey of over 120 mortgage lenders, including mortgage banks, commercial banks, thrifts, savings and loan associations, subservicers and life

Report on Nevada s Housing Market

June Report on Nevada s Housing Market This is the first of a series of reports on Nevada s Housing Market co-presented by the Lied Institute for Real Estate Studies at the University of Nevada, Las Vegas

June Report on Nevada s Housing Market This is the first of a series of reports on Nevada s Housing Market co-presented by the Lied Institute for Real Estate Studies at the University of Nevada, Las Vegas

Property Management Software

Property Management Software Jenark property management software by CoreLogic drives operational efficiencies to meet the needs of any property management company. Multifamily Management Community Association

Property Management Software Jenark property management software by CoreLogic drives operational efficiencies to meet the needs of any property management company. Multifamily Management Community Association

Complaints from consumers, real estate

CasCade of Changes New systems and practices manage the flow of loss mitigation options. Complaints from consumers, real estate professionals and public officials are rampant it takes too long to get an

CasCade of Changes New systems and practices manage the flow of loss mitigation options. Complaints from consumers, real estate professionals and public officials are rampant it takes too long to get an

Homeownership Preservation Policy for Residential Mortgage Assets. Section 110 of the Emergency Economic Stabilization Act (EESA)

") Homeownership Preservation Policy for Residential Mortgage Assets Section 110 of the Emergency Economic Stabilization Act (EESA) requires that each Federal property manager that holds, owns, or controls

Homeownership Preservation Policy for Residential Mortgage Assets Section 110 of the Emergency Economic Stabilization Act (EESA) requires that each Federal property manager that holds, owns, or controls

Virginia Housing Market and Foreclosure Status

Virginia Housing Market and Foreclosure Status Virginia Foreclosure Task Force September 17, 2013 Virginia Housing Development Authority Overview 1. Looking back: Market conditions and foreclosure trends

Virginia Housing Market and Foreclosure Status Virginia Foreclosure Task Force September 17, 2013 Virginia Housing Development Authority Overview 1. Looking back: Market conditions and foreclosure trends

Durango Real Estate: Look West to Cal-i-forn-i-a by Luke T Miller

Durango Real Estate: Look West to Cal-i-forn-i-a by Luke T Miller As a finance professor, I often get asked my opinion of the housing market. Many times I respond with the most recent housing numbers.

Durango Real Estate: Look West to Cal-i-forn-i-a by Luke T Miller As a finance professor, I often get asked my opinion of the housing market. Many times I respond with the most recent housing numbers.

The GSEs Are Helping to Stabilize an Unstable Mortgage Market

Update on the Single-Family Credit Guarantee Business Rick Padilla Director, Corporate Relations & Housing Outreach The Changing Economy: The New Community Lending Environment June 1, 29 The GSEs Are Helping

Update on the Single-Family Credit Guarantee Business Rick Padilla Director, Corporate Relations & Housing Outreach The Changing Economy: The New Community Lending Environment June 1, 29 The GSEs Are Helping

Professor Chris Mayer (Columbia Business School; NBER; Visiting Scholar, Federal Reserve Bank of New York)

") Professor Chris Mayer (Columbia Business School; NBER; Visiting Scholar, Federal Reserve Bank of New York) Lessons Learned from the Crisis: Housing, Subprime Mortgages, and Securitization THE PAUL MILSTEIN

Professor Chris Mayer (Columbia Business School; NBER; Visiting Scholar, Federal Reserve Bank of New York) Lessons Learned from the Crisis: Housing, Subprime Mortgages, and Securitization THE PAUL MILSTEIN

Chapter URL: http://www.nber.org/chapters/c1737

This PDF is a selection from an out-of-print volume from the National Bureau of Economic Research Volume Title: Commercial Bank Activities in Urban Mortgage Financing Volume Author/Editor: Carl F Behrens

This PDF is a selection from an out-of-print volume from the National Bureau of Economic Research Volume Title: Commercial Bank Activities in Urban Mortgage Financing Volume Author/Editor: Carl F Behrens

U.S. Residential Mortgage Delinquency Rates Seasonally Adjusted Data, 1998Q2 to 2011Q1 Source: Mortgage Bankers Association / Haver Analytics

U.S. Residential Mortgage Delinquency Rates Seasonally Adjusted Data, 1998Q2 to 211Q1 3 2 2 1 1 Delinquency Rate (%) U.S. Residential Mortgage Foreclosure Rates Seasonally Adjusted Data, 1998Q2 to 211Q1

U.S. Residential Mortgage Delinquency Rates Seasonally Adjusted Data, 1998Q2 to 211Q1 3 2 2 1 1 Delinquency Rate (%) U.S. Residential Mortgage Foreclosure Rates Seasonally Adjusted Data, 1998Q2 to 211Q1

Appendix A: Description of the Data

Appendix A: Description of the Data This data release presents information by year of origination on the dollar amounts, loan counts, and delinquency experience through year-end 2009 of single-family mortgages

Appendix A: Description of the Data This data release presents information by year of origination on the dollar amounts, loan counts, and delinquency experience through year-end 2009 of single-family mortgages

Florida: An Overview of Foreclosures

Florida: An Overview of Foreclosures February 4, 2015 Presented by: The Florida Legislature Office of Economic and Demographic Research 850.487.1402 http://edr.state.fl.us Foreclosure Timeline... The housing

Florida: An Overview of Foreclosures February 4, 2015 Presented by: The Florida Legislature Office of Economic and Demographic Research 850.487.1402 http://edr.state.fl.us Foreclosure Timeline... The housing

Federal Reserve Bank of Kansas City: Consumer Credit Report

Federal Reserve Bank of Kansas City: Consumer Credit Report Tenth District Consumer Credit Report May 29, 2015 By Kelly Edmiston, Senior Economist and Mwai Malindi, Research Associate FIRST QUARTER 2015

Federal Reserve Bank of Kansas City: Consumer Credit Report Tenth District Consumer Credit Report May 29, 2015 By Kelly Edmiston, Senior Economist and Mwai Malindi, Research Associate FIRST QUARTER 2015

Housing Market and Mortgage Performance in the Fifth District

QUARTERLY UPDATE Housing Market and Mortgage Performance in the Fifth District 1 st Quarter, 2015 Jamie Feik Lisa Hearl Joseph Mengedoth 400 375 350 325 300 Index, 1995:Q1=100 United States District of

QUARTERLY UPDATE Housing Market and Mortgage Performance in the Fifth District 1 st Quarter, 2015 Jamie Feik Lisa Hearl Joseph Mengedoth 400 375 350 325 300 Index, 1995:Q1=100 United States District of

FEDERAL HOUSING FINANCE AGENCY

FEDERAL HOUSING FINANCE AGENCY ADVISORY BULLETIN AB 2012-02 FRAMEWORK FOR ADVERSELY CLASSIFYING LOANS, OTHER REAL ESTATE OWNED, AND OTHER ASSETS AND LISTING ASSETS FOR SPECIAL MENTION Introduction This

FEDERAL HOUSING FINANCE AGENCY ADVISORY BULLETIN AB 2012-02 FRAMEWORK FOR ADVERSELY CLASSIFYING LOANS, OTHER REAL ESTATE OWNED, AND OTHER ASSETS AND LISTING ASSETS FOR SPECIAL MENTION Introduction This

COMPREHENSIVE LOAN MODIFICATION PROGRAM

I. Definitions. COMPREHENSIVE LOAN MODIFICATION PROGRAM a) Residential mortgage loan shall mean any loan primarily for personal, family, or household use that is secured by a mortgage, deed of trust, or

I. Definitions. COMPREHENSIVE LOAN MODIFICATION PROGRAM a) Residential mortgage loan shall mean any loan primarily for personal, family, or household use that is secured by a mortgage, deed of trust, or

Investment Symposium March 14-15, 2013 New York, NY. Session E5, U.S. Economic Conditions and the Housing/Mortgage Market

Investment Symposium March 1-15, 213 New York, NY Session E5, U.S. Economic Conditions and the Housing/Mortgage Market Moderator: Jonathan Glowacki Presenter: David Berson Housing & Mortgage Market Outlook

Investment Symposium March 1-15, 213 New York, NY Session E5, U.S. Economic Conditions and the Housing/Mortgage Market Moderator: Jonathan Glowacki Presenter: David Berson Housing & Mortgage Market Outlook

Mortgage Arrears in Ireland: Introducing the Enhanced Quarterly Statistics

8 Mortgage Arrears in Ireland: Introducing the Jean Goggin * Abstract This article introduces the recently expanded Residential Mortgage Arrears and Repossessions Statistics published by the Central Bank

8 Mortgage Arrears in Ireland: Introducing the Jean Goggin * Abstract This article introduces the recently expanded Residential Mortgage Arrears and Repossessions Statistics published by the Central Bank

REALTORS Guide to FORECLOSURE RESOURCES

REALTORS Guide to FORECLOSURE RESOURCES Federal & State Programs That May Help Those Facing Foreclosure Making Home Affordable Program Designed to assist families who may face foreclosure, the federal

REALTORS Guide to FORECLOSURE RESOURCES Federal & State Programs That May Help Those Facing Foreclosure Making Home Affordable Program Designed to assist families who may face foreclosure, the federal

Trends in Homeownership and Mortgage Debt among Older Americans Office for Older Americans

June 24, 2015 Trends in Homeownership and Mortgage Debt among Older Americans Office for Older Americans Presentation for MHA Trusted Advisors Note: This document was used in support of a live discussion.

June 24, 2015 Trends in Homeownership and Mortgage Debt among Older Americans Office for Older Americans Presentation for MHA Trusted Advisors Note: This document was used in support of a live discussion.

Mortgage Insurance Basics. Ken Dailey, FCAS, MAAA Casualty Loss Reserve Seminar September 15, 2009

Mortgage Insurance Basics Ken Dailey, FCAS, MAAA Casualty Loss Reserve Seminar September 15, 2009 What is Mortgage Insurance 1 (MI)? Mortgage Insurance (MI) is a type of credit insurance where a mortgage

Mortgage Insurance Basics Ken Dailey, FCAS, MAAA Casualty Loss Reserve Seminar September 15, 2009 What is Mortgage Insurance 1 (MI)? Mortgage Insurance (MI) is a type of credit insurance where a mortgage

The Law of First Impressions A Practical Guide to Mortgage Applicants

The Law of First Impressions A Practical Guide to Mortgage Applicants Increased Importance of Borrower Financial Statements For Commercial Real Estate Financing Robert T. Gibney Real estate investors prepare

The Law of First Impressions A Practical Guide to Mortgage Applicants Increased Importance of Borrower Financial Statements For Commercial Real Estate Financing Robert T. Gibney Real estate investors prepare

Mortgage Lending Analytics

Mortgage Lending Analytics Operational Practices December 2, 2014 Leslie Deich Today s Agenda The basics of mortgage lending from both the borrower and lender s perspective Overview of the operational

Mortgage Lending Analytics Operational Practices December 2, 2014 Leslie Deich Today s Agenda The basics of mortgage lending from both the borrower and lender s perspective Overview of the operational

How to Sell Your House Fast

How to Sell Your House Fast If you are reading this report then you are interested in selling your house as fast as you possibly can. Usually this is because you are in foreclosure, are behind on payments

How to Sell Your House Fast If you are reading this report then you are interested in selling your house as fast as you possibly can. Usually this is because you are in foreclosure, are behind on payments

HOUSING MARKETS HOUSING CONSTRUCTION TRENDS JOINT CENTER FOR HOUSING STUDIES OF HARVARD UNIVERSITY

2 HOUSING MARKETS Although the news was mixed in 214, housing markets made some advances that set the stage for moderate growth. Singlefamily construction continued to languish, but multifamily construction

2 HOUSING MARKETS Although the news was mixed in 214, housing markets made some advances that set the stage for moderate growth. Singlefamily construction continued to languish, but multifamily construction

CoreLogic Equity Report

CoreLogic Equity Report REPORT NATIONAL OVERVIEW Rising Home Prices Led to Improvements In Home Equity, with 312,000 Residential Properties Regaining Equity In Q1 2014 6.3 Million Homes with a Mortgage

CoreLogic Equity Report REPORT NATIONAL OVERVIEW Rising Home Prices Led to Improvements In Home Equity, with 312,000 Residential Properties Regaining Equity In Q1 2014 6.3 Million Homes with a Mortgage

Joint Federal-State Mortgage Servicing Settlement EXECUTIVE SUMMARY

Joint Federal-State Mortgage Servicing Settlement EXECUTIVE SUMMARY The settlement between the state attorneys general and the five leading bank mortgage servicers will result in approximately $25 billion

Joint Federal-State Mortgage Servicing Settlement EXECUTIVE SUMMARY The settlement between the state attorneys general and the five leading bank mortgage servicers will result in approximately $25 billion

Request for Information Regarding an Initiative to Promote Student Loan Affordability

This Request for Information is scheduled to be published to the Federal Register in late February. In the meantime, please send comments via email to studentloanaffordability@cfpb.gov Billing Code: 4810-AM-P

This Request for Information is scheduled to be published to the Federal Register in late February. In the meantime, please send comments via email to studentloanaffordability@cfpb.gov Billing Code: 4810-AM-P

TRENDS IN DELINQUENCIES AND FORECLOSURES IN UTAH

TRENDS IN DELINQUENCIES AND FORECLOSURES IN UTAH April 2009 Jan Bontrager, Community Development Department, Federal Reserve Bank of San Francisco Outline of Presentation National Trends Rising foreclosures

TRENDS IN DELINQUENCIES AND FORECLOSURES IN UTAH April 2009 Jan Bontrager, Community Development Department, Federal Reserve Bank of San Francisco Outline of Presentation National Trends Rising foreclosures

Home Equity Lending Landscape. WHITE PAPER February 2016

Home Equity Lending Landscape WHITE PAPER February 2016 Confidential The recipient of this document agrees that at all times and notwithstanding any other agreement or understanding, it will hold in strict

Home Equity Lending Landscape WHITE PAPER February 2016 Confidential The recipient of this document agrees that at all times and notwithstanding any other agreement or understanding, it will hold in strict

Why home values may take decades to recover. by Dennis Cauchon, USA TODAY

Why home values may take decades to recover by Dennis Cauchon, USA TODAY 200 180 160 140 120 100 80 The history of housing as an investment 1950 1952 1954 1956 1958 1960 1962 1964 1966 1968 1970 1972 1974

Why home values may take decades to recover by Dennis Cauchon, USA TODAY 200 180 160 140 120 100 80 The history of housing as an investment 1950 1952 1954 1956 1958 1960 1962 1964 1966 1968 1970 1972 1974

Automated Valuation Testing. Whitepaper4 July 2011

Automated Valuation Testing Whitepaper4 July 2011 Confidential The recipient of this document agrees that at all times and notwithstanding any other agreement or understanding, it will hold in strict confidence

Automated Valuation Testing Whitepaper4 July 2011 Confidential The recipient of this document agrees that at all times and notwithstanding any other agreement or understanding, it will hold in strict confidence

HOW TO INFLUENCE THE SHORT SALE BPO

HOW TO INFLUENCE THE SHORT SALE BPO Working With the Lender s BPO Agent to Get a Fair and Accurate As Is Market Value Understanding what a Broker Price Opinion is and what it is used for is a key component

HOW TO INFLUENCE THE SHORT SALE BPO Working With the Lender s BPO Agent to Get a Fair and Accurate As Is Market Value Understanding what a Broker Price Opinion is and what it is used for is a key component

Legacy Asset Servicing. Terry Laughlin Legacy Asset Servicing Executive

Legacy Asset Servicing i Terry Laughlin Legacy Asset Servicing Executive Key Takeaways Split of Legacy Asset Servicing from Bank of America Home Loans to accomplish two goals: Enable greater focus on the

Legacy Asset Servicing i Terry Laughlin Legacy Asset Servicing Executive Key Takeaways Split of Legacy Asset Servicing from Bank of America Home Loans to accomplish two goals: Enable greater focus on the

Update on Market Challenges

Update on Market Challenges Charlottesville Area Association of Realtors August 6, 2009 Virginia Housing Development Authority Four inter-related factors continue to hold back recovery in the Charlottesville

Update on Market Challenges Charlottesville Area Association of Realtors August 6, 2009 Virginia Housing Development Authority Four inter-related factors continue to hold back recovery in the Charlottesville

Should Investors Unload Their Mortgage REITs?

Should Investors Unload Their Mortgage REITs? May 5, 2015 by Keith Jurow For the past several years, I have written extensively about the Fed s dangerous efforts to drive interest rates low enough to stimulate

Should Investors Unload Their Mortgage REITs? May 5, 2015 by Keith Jurow For the past several years, I have written extensively about the Fed s dangerous efforts to drive interest rates low enough to stimulate

HUD PD&R Housing Market Profiles

Houston-Sugar Land-Baytown, Texas Quick Facts About Houston-Sugar LandBaytown By Robert Stephens Current sales market conditions: slightly tight. Current apartment market conditions: balanced. The inventory

Houston-Sugar Land-Baytown, Texas Quick Facts About Houston-Sugar LandBaytown By Robert Stephens Current sales market conditions: slightly tight. Current apartment market conditions: balanced. The inventory

HOPE NOW: Loan Mods & Short Sales for Homeowners Total 108,000 in January

March 13, 2013 Media Contact: Brad Dwin (410) 303-6391 brad@hopenow.com HOPE NOW: Loan Mods & Short Sales for Homeowners Total 108,000 in January Foreclosure Sales & Starts Show Declines from Same Time

March 13, 2013 Media Contact: Brad Dwin (410) 303-6391 brad@hopenow.com HOPE NOW: Loan Mods & Short Sales for Homeowners Total 108,000 in January Foreclosure Sales & Starts Show Declines from Same Time

HOME EQUITY CREDIT ACCOUNT DISCLOSURES

HOME EQUITY CREDIT ACCOUNT DISCLOSURES This disclosure contains important information about your Home Equity Credit Account. You should read it carefully and keep a copy for your records. 1. Availability

HOME EQUITY CREDIT ACCOUNT DISCLOSURES This disclosure contains important information about your Home Equity Credit Account. You should read it carefully and keep a copy for your records. 1. Availability

Homeowners with Jumbos Pose Greatest Risk of Strategic Default

Homeowners with Jumbos Pose Greatest Risk of A new national telephone interview study indicates who mortgage lenders need to worry about the most: Prime jumbo borrowers with good FICO scores are now the

Homeowners with Jumbos Pose Greatest Risk of A new national telephone interview study indicates who mortgage lenders need to worry about the most: Prime jumbo borrowers with good FICO scores are now the

Durango Real Estate: Revisiting California and Price-to-Rent by Luke T Miller, PhD

Durango Real Estate: Revisiting California and Price-to-Rent by Luke T Miller, PhD About one year ago, I compared Durango real estate to southern California and also conducted a price-to-rent ratio analysis

Durango Real Estate: Revisiting California and Price-to-Rent by Luke T Miller, PhD About one year ago, I compared Durango real estate to southern California and also conducted a price-to-rent ratio analysis

Snapshot of older consumers and mortgage debt. Office for Older Americans

Snapshot of older consumers and mortgage debt Office for Older Americans May 2014 Table of contents Table of contents... 2 1. Introduction... 3 2. Rising mortgage debt threatens retirement security for

Snapshot of older consumers and mortgage debt Office for Older Americans May 2014 Table of contents Table of contents... 2 1. Introduction... 3 2. Rising mortgage debt threatens retirement security for

Statistical Release 10 March 2016

Statistical Release 10 March 2016 Decer 2015 Residential Mortgage Arrears and Repossessions Statistics: Q4 2015 Summary The number of mortgage accounts for principal dwelling houses (PDH) in arrears continued

Statistical Release 10 March 2016 Decer 2015 Residential Mortgage Arrears and Repossessions Statistics: Q4 2015 Summary The number of mortgage accounts for principal dwelling houses (PDH) in arrears continued

2015 Mortgage Fraud Report

2015 Mortgage Fraud Report October 2015 Fraud Report National Overview The top 10 states with the highest risk for mortgage fraud have remained stable the past year with notable changes being District

2015 Mortgage Fraud Report October 2015 Fraud Report National Overview The top 10 states with the highest risk for mortgage fraud have remained stable the past year with notable changes being District

National Mortgage Settlement

National Mortgage Settlement Housing and Land Use Policy Program University of Iowa Public Policy Center Sally Scott, Ph.D. and Jerry Anthony, Ph.D. October 2012 Overview On February 9 of 2012, a bipartisan

National Mortgage Settlement Housing and Land Use Policy Program University of Iowa Public Policy Center Sally Scott, Ph.D. and Jerry Anthony, Ph.D. October 2012 Overview On February 9 of 2012, a bipartisan

Historically, employment in financial

Employment in financial activities: double billed by housing and financial crises The housing market crash, followed by the financial crisis of the 2007-09 recession, helped depress financial activities

Employment in financial activities: double billed by housing and financial crises The housing market crash, followed by the financial crisis of the 2007-09 recession, helped depress financial activities

Subject: Characteristics and Performance of Nonprime Mortgages

United States Government Accountability Office Washington, DC 20548 July 28, 2009 The Honorable Carolyn B. Maloney Chair Joint Economic Committee House of Representatives The Honorable Charles E. Schumer

United States Government Accountability Office Washington, DC 20548 July 28, 2009 The Honorable Carolyn B. Maloney Chair Joint Economic Committee House of Representatives The Honorable Charles E. Schumer

Statement of Edward L. Golding Senior Vice President Economics and Policy Freddie Mac

Statement of Edward L. Golding Senior Vice President Economics and Policy Freddie Mac Hearing of the Philadelphia, PA Chair Warren and members of the, thank you for inviting me to speak today. I am Edward

Statement of Edward L. Golding Senior Vice President Economics and Policy Freddie Mac Hearing of the Philadelphia, PA Chair Warren and members of the, thank you for inviting me to speak today. I am Edward

Zillow Negative Equity Report

Overview The housing market is finally showing signs of life, with many metropolitan areas having hit the elusive bottom and seeing home value appreciation, however negative equity remains a drag on the

Overview The housing market is finally showing signs of life, with many metropolitan areas having hit the elusive bottom and seeing home value appreciation, however negative equity remains a drag on the

CREDIT UNION TRENDS REPORT

CREDIT UNION TRENDS REPORT CUNA Mutual Group Economics July 2 (May 2 data) Highlights First quarter data revisions were modest. The number of credit unions was revised down by and assets and loans were

CREDIT UNION TRENDS REPORT CUNA Mutual Group Economics July 2 (May 2 data) Highlights First quarter data revisions were modest. The number of credit unions was revised down by and assets and loans were

2002 in the Mortgage Industry, an Industry Retrospective 1

2002 in the Mortgage Industry, an Industry Retrospective 1 Jeff Lebowitz; MORTECH, LLC The year 2002 was year with an economic recession that followed immediately upon the heels of the stock market crash

2002 in the Mortgage Industry, an Industry Retrospective 1 Jeff Lebowitz; MORTECH, LLC The year 2002 was year with an economic recession that followed immediately upon the heels of the stock market crash

Net Income by Quarter

Farmers Capital Bank Corporation 202 West Main Street l Post Office Box 309 Frankfort, Kentucky 40602-0309 phone: 502.227.1668 l Fax: 502.227.1692 www.farmerscapital.com NEWS RELEASE October 22, 2014 Farmers

Farmers Capital Bank Corporation 202 West Main Street l Post Office Box 309 Frankfort, Kentucky 40602-0309 phone: 502.227.1668 l Fax: 502.227.1692 www.farmerscapital.com NEWS RELEASE October 22, 2014 Farmers

Quarterly Banking Profile

INSURED INSTITUTION PERFORMANCE Net Income of $37.2 Billion Is $3.1 Billion Below Year-Ago Level Reduced Mortgage Activity Contributes to Decline in Revenue 54 Percent of Banks Report Year-Over-Year Improvement

INSURED INSTITUTION PERFORMANCE Net Income of $37.2 Billion Is $3.1 Billion Below Year-Ago Level Reduced Mortgage Activity Contributes to Decline in Revenue 54 Percent of Banks Report Year-Over-Year Improvement

Historically, housing Leads us into the recession and historically, housing leads us out of the recession.

Institute for Economic Development & Real Estate Research 214 Economic Outlook & Real Estate Forecast Information provided by the LATTER & BLUM Research Division Historically, housing Leads us into the

Institute for Economic Development & Real Estate Research 214 Economic Outlook & Real Estate Forecast Information provided by the LATTER & BLUM Research Division Historically, housing Leads us into the

The Current Crisis in the Subprime Mortgage Market. Jason Vinar GMAC ResCap

The Current Crisis in the Subprime Mortgage Market Jason Vinar GMAC ResCap Overview Merrill s Market Economist, August 2006 Morgan Stanley s Mortgage Finance, March 2007 Citigroup s Housing Monitor, March

The Current Crisis in the Subprime Mortgage Market Jason Vinar GMAC ResCap Overview Merrill s Market Economist, August 2006 Morgan Stanley s Mortgage Finance, March 2007 Citigroup s Housing Monitor, March

Mortgage Defaults. Shane M. Sherlund. Board of Governors of the Federal Reserve System. March 8, 2010

Mortgage Defaults Shane M. Sherlund Board of Governors of the Federal Reserve System March 8, 2010 The analysis and conclusions contained herein reflect those of the author and do not necessarily reflect

Mortgage Defaults Shane M. Sherlund Board of Governors of the Federal Reserve System March 8, 2010 The analysis and conclusions contained herein reflect those of the author and do not necessarily reflect

HUD PD&R Housing Market Profiles

Philadelphia, Pennsylvania Quick Facts About Philadelphia By Timothy D. McNally Current sales market conditions: slightly soft. Current apartment market conditions: balanced. Of the top 10 employers in

Philadelphia, Pennsylvania Quick Facts About Philadelphia By Timothy D. McNally Current sales market conditions: slightly soft. Current apartment market conditions: balanced. Of the top 10 employers in

Guidelines for Pilot PACE Financing Programs

Guidelines for Pilot PACE Financing Programs May 7, 2010 This document provides best practice guidelines to help implement the Policy Framework for PACE Financing Programs announced on October 18, 2009.

Guidelines for Pilot PACE Financing Programs May 7, 2010 This document provides best practice guidelines to help implement the Policy Framework for PACE Financing Programs announced on October 18, 2009.

SBA 504 Expanded Refinancing Eligibility

SBA 504 Expanded Refinancing Eligibility When is a commercial mortgage considered eligible for refinancing under the new rules? 1. The loan must have funded at least 2 years ago 2. 85% of the loan proceeds

SBA 504 Expanded Refinancing Eligibility When is a commercial mortgage considered eligible for refinancing under the new rules? 1. The loan must have funded at least 2 years ago 2. 85% of the loan proceeds

NORTH ISLAND CREDIT UNION

NORTH ISLAND CREDIT UNION Policy Section: Business Services Policy Name: Member Business Lending Policy No: 500-05-01 Board Review & Approval: July 21, 2014 Effective Date: July 22, 2014 POLICY STATEMENT

NORTH ISLAND CREDIT UNION Policy Section: Business Services Policy Name: Member Business Lending Policy No: 500-05-01 Board Review & Approval: July 21, 2014 Effective Date: July 22, 2014 POLICY STATEMENT

Gulf Coast Florida Association of Mortgage Professionals Pinellas REALTOR Organization (PRO)

") Presented By: Pam Marron Sponsored By: Gulf Coast Florida Association of Mortgage Professionals Pinellas REALTOR Organization (PRO) Pam Marron Innovative Mortgage Services, Inc., NMLS#246438 GulfCoast

Presented By: Pam Marron Sponsored By: Gulf Coast Florida Association of Mortgage Professionals Pinellas REALTOR Organization (PRO) Pam Marron Innovative Mortgage Services, Inc., NMLS#246438 GulfCoast

Consumer Credit Report

Page 1 of 5 Consumer Credit Report Tenth District Consumer Credit Report December 2, 2015 By Kelly Edmiston, Senior Economist Average debt for Tenth District consumers, defined for this report as all outstanding

Page 1 of 5 Consumer Credit Report Tenth District Consumer Credit Report December 2, 2015 By Kelly Edmiston, Senior Economist Average debt for Tenth District consumers, defined for this report as all outstanding

Citi U.S. Consumer Mortgage Lending Data and Servicing Foreclosure Prevention Efforts

Citi U.S. Consumer Mortgage Lending Data and Servicing Foreclosure Prevention Efforts Second Quarter 29 EXECUTIVE SUMMARY In February 28, we published our initial data report on Citi s U.S. mortgage lending

Citi U.S. Consumer Mortgage Lending Data and Servicing Foreclosure Prevention Efforts Second Quarter 29 EXECUTIVE SUMMARY In February 28, we published our initial data report on Citi s U.S. mortgage lending

SOUTHEAST EUROPE MORTGAGE FINANCE WORKING GROUP Sofia February 23, 2005

SOUTHEAST EUROPE MORTGAGE FINANCE WORKING GROUP Sofia February 23, 2005 Who We Are Presentation Topics Credit Life Insurance Mortgaged Property Insurance Mortgage Insurance Who We Are The leading international

SOUTHEAST EUROPE MORTGAGE FINANCE WORKING GROUP Sofia February 23, 2005 Who We Are Presentation Topics Credit Life Insurance Mortgaged Property Insurance Mortgage Insurance Who We Are The leading international

Summary. Abbas P. Grammy 1 Professor of Economics California State University, Bakersfield

The State of the Economy: Kern County, California Summary Abbas P. Grammy 1 Professor of Economics California State University, Bakersfield Kern County households follow national trends. They turned less

The State of the Economy: Kern County, California Summary Abbas P. Grammy 1 Professor of Economics California State University, Bakersfield Kern County households follow national trends. They turned less

Servicing s Pain Points

C o v e r R e p o r t : Te c h n o l o g y Servicing s Pain Points BY J O H N G U Z Z O Historic changes are occurring in the servicing business. Not least among the many changes that have occurred in

C o v e r R e p o r t : Te c h n o l o g y Servicing s Pain Points BY J O H N G U Z Z O Historic changes are occurring in the servicing business. Not least among the many changes that have occurred in

Hilltop Advisors, LLC. Loan Review Services. Presented by: Hilltop Advisors, LLC (an accounting advisory and consulting firm)

") Loan Review Services Presented by: (an accounting advisory and consulting firm) For further information about our proposal or the company, please contact: Geoffrey A. Oliver CPA, CFF, CMB CEO & Managing

Loan Review Services Presented by: (an accounting advisory and consulting firm) For further information about our proposal or the company, please contact: Geoffrey A. Oliver CPA, CFF, CMB CEO & Managing

Stress Testing Modeling Symposium

Stress Testing Modeling Symposium Residential Mortgage Modeling Issues Paul S. Calem Division of Supervision, Regulation, and Credit Federal Reserve Bank of Philadelphia Views are my own and not those

Stress Testing Modeling Symposium Residential Mortgage Modeling Issues Paul S. Calem Division of Supervision, Regulation, and Credit Federal Reserve Bank of Philadelphia Views are my own and not those

FOR IMMEDIATE RELEASE November 7, 2013 MEDIA CONTACT: Lisa Gagnon 703-903-3385 INVESTOR CONTACT: Robin Phillips 571-382-4732

FOR IMMEDIATE RELEASE MEDIA CONTACT: Lisa Gagnon 703-903-3385 INVESTOR CONTACT: Robin Phillips 571-382-4732 FREDDIE MAC REPORTS PRE-TAX INCOME OF $6.5 BILLION FOR THIRD QUARTER 2013 Release of Valuation

FOR IMMEDIATE RELEASE MEDIA CONTACT: Lisa Gagnon 703-903-3385 INVESTOR CONTACT: Robin Phillips 571-382-4732 FREDDIE MAC REPORTS PRE-TAX INCOME OF $6.5 BILLION FOR THIRD QUARTER 2013 Release of Valuation

Automated valuation models: Changes in the housing market require additional risk management considerations

Automated valuation models: Changes in the housing market require additional risk management considerations Overview From 2003 to 2006, the US residential real estate market experienced an unprecedented

Automated valuation models: Changes in the housing market require additional risk management considerations Overview From 2003 to 2006, the US residential real estate market experienced an unprecedented

Spotlight on the Housing Market in the Orlando-Kissimmee-Sanford, FL MSA

Spotlight on in Orlando-Kissimmee-Sanford, FL MSA The Orlando-Kissimmee-Sanford, FL Metropolitan Statistical Area (Orlando MSA) is located in central Florida and includes four counties: Lake, Orange, Osceola,

Spotlight on in Orlando-Kissimmee-Sanford, FL MSA The Orlando-Kissimmee-Sanford, FL Metropolitan Statistical Area (Orlando MSA) is located in central Florida and includes four counties: Lake, Orange, Osceola,

Nine Things to Consider When Evaluating Trust Deed Investment Sources for Your Clients. A White Paper for Financial Advisers

Nine Things to Consider When Evaluating Trust Deed Investment Sources for Your Clients A White Paper for Financial Advisers Presented by Sterling Pacific Financial (www.sterlpac.com) Nine Things to Consider

Nine Things to Consider When Evaluating Trust Deed Investment Sources for Your Clients A White Paper for Financial Advisers Presented by Sterling Pacific Financial (www.sterlpac.com) Nine Things to Consider

Announcement 08-16 June 25, 2008

Announcement 08-16 June 25, 2008 Amends these Guides: Selling Bankruptcy, Foreclosure, and Conversion of Principal Residence Policy Changes; and Revised Property Value Representation and Warranty Requirements

Announcement 08-16 June 25, 2008 Amends these Guides: Selling Bankruptcy, Foreclosure, and Conversion of Principal Residence Policy Changes; and Revised Property Value Representation and Warranty Requirements

NEWS RELEASE GREAT AMERICAN BANCORP, INC. UNAUDITED RESULTS FOR FOURTH QUARTER 2008 NET INCOME FOR FISCAL 2008 - $1,110,000

NEWS RELEASE FOR IMMEDIATE RELEASE January 13, 2009 Contact: Ms. Jane F. Adams Chief Financial Officer and Investor Relations (217) 356-2265 GREAT AMERICAN BANCORP, INC. UNAUDITED RESULTS FOR FOURTH QUARTER

NEWS RELEASE FOR IMMEDIATE RELEASE January 13, 2009 Contact: Ms. Jane F. Adams Chief Financial Officer and Investor Relations (217) 356-2265 GREAT AMERICAN BANCORP, INC. UNAUDITED RESULTS FOR FOURTH QUARTER

Mortgage Meltdown Is Every State Impacted?

Mortgage Meltdown Is Every State Impacted? Good morning and thank you for taking your valuable time to learn more about the current status of the mortgage lending industry. I am glad to have the opportunity

Mortgage Meltdown Is Every State Impacted? Good morning and thank you for taking your valuable time to learn more about the current status of the mortgage lending industry. I am glad to have the opportunity

2012 Foreclosure Trends Report

2012 2012 Foreclosure Trends Report Division of Banks Commonwealth of Massachusetts 12/20/2013 Background In November of 2007, to address rising foreclosures in the Commonwealth, Governor Deval Patrick

2012 2012 Foreclosure Trends Report Division of Banks Commonwealth of Massachusetts 12/20/2013 Background In November of 2007, to address rising foreclosures in the Commonwealth, Governor Deval Patrick