Division. Impact. Before the. Pensions

|

|

|

- Shawn Little

- 8 years ago

- Views:

Transcription

1 Oregon Insurance Division Statement of Teresa Miller, Administrator Oregon Insurance Division Department of Consumer and Business Services ON Impact Affordable Care Act: on Health Insura ance Rate Review Before the Senate Committee on Health, Education, Labor & United States Senate Pensions Aug. 2, 2011

2 Introduction Good morning Chairman Harkin, Ranking Member Enzi, and distinguished members of the committee. My name is Teresa Miller, and I am the administrator of the Oregon Insurance Division of the Department of Consumer and Business Services. I am honored to be here today and appreciate the opportunity to explain how federal grants are improving our health insurance rate review process in Oregon. Over the past four years, Oregon has transformed its review of rate requests, making it more transparent, rigorous, and inclusive. Our process is as open as any in the country and it is backed by a strong rate review statute. As we strengthened our state law and opened our process, federal grants available through the Affordable Care Act provided additional staff to conduct more in-depth reviews of rate increases and funds to solicit meaningful public comment. In addition to giving the Oregon Insurance Division the ability to prevent excessive rate increases, Oregon s rate review allows us to engage consumers and educate them about the factors that lead to rising health insurance costs. I would like to give you some background on rate review in Oregon and the improvements we have made and plan to make with grants available under the Affordable Care Act. Rate review in Oregon Oregon, unlike many states, has a competitive health insurance market. Seven Oregon-based insurers actively compete in the small group and individual markets that we regulate. Insurers in these markets must submit rates and have them approved by the state before they take effect. The Oregon Insurance Division reviews rates to ensure they are reasonable in relation to the benefits provided. During our review, we look at the cost of medical care and prescription drugs, the company s past history of rate changes, the financial strength of the company, actual and projected claims costs, enrollment trends, premiums, administrative costs, and profit. Oregon s own health reform law passed in 2009 expanded the factors we can consider in evaluating a rate request. It gives us, for example, explicit authority to consider factors such as an insurer s investment income, surplus, and efforts to control costs and improve quality. Perhaps most significantly, we may also consider an insurer s overall profitability rather than just the profitability of a particular line of insurance. Finally, insurers must separately report and justify changes in administrative expenses by line of business and must provide more detail about what they spend on salaries, commissions, marketing, advertising, and other administrative expenses. In addition to strengthening our authority, we also have taken many steps in recent years to make our process more transparent. For example, we have added the following elements: We post rate filings for individual, portability, and small-employer plans on the Insurance Division website once they are deemed complete. All information is public. A required feature of the filing by the insurer is a plain-language summary highlighting the insurer s request along with a five-year history of rate increases for that line of insurance. The posting of the filing triggers a 30-day public comment period. We send an to policyholders who sign up for notification when their company files a rate request. Any comments consumers make are posted to the website.

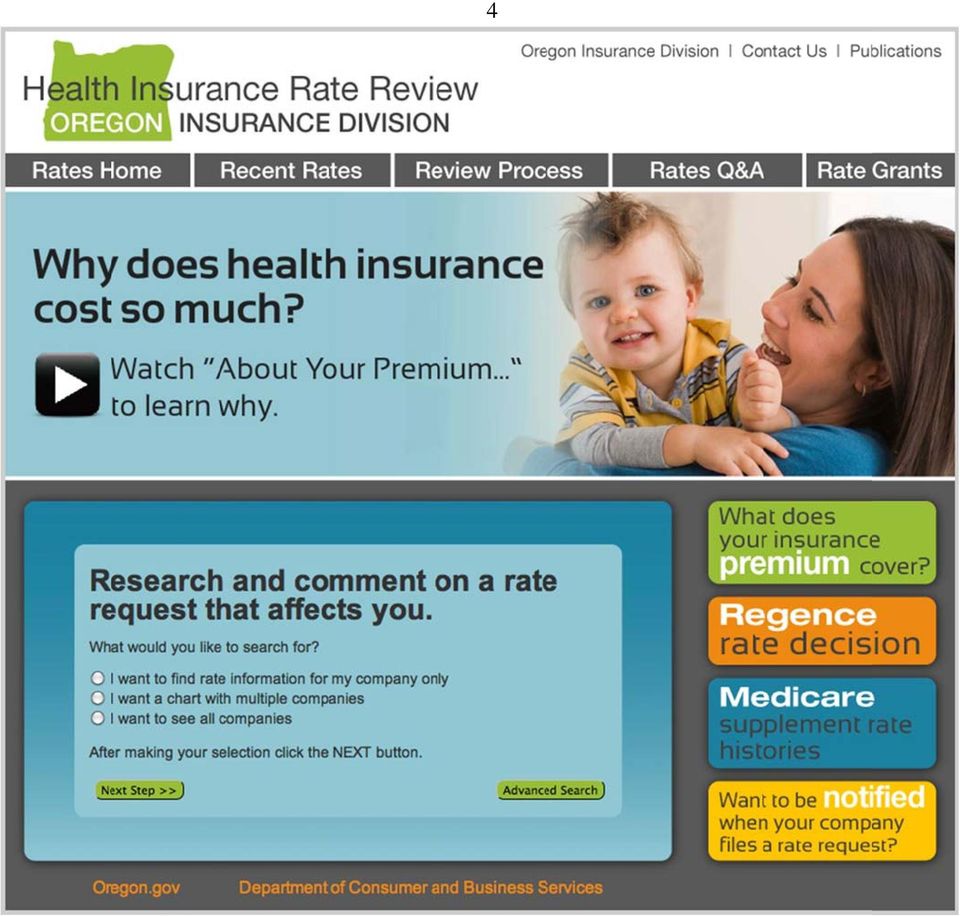

3 1 We contract with a consumer group, using federal grant money, to comment on key rate requests on behalf of consumers. We must issue a decision within 10 days of the close of the public comment period meaning we have 40 days to complete most of the work. Because every rate change is based on a unique set of facts, we file a plain-language summary on the website listing key factors underlying each rate filing decision. Finally, we send policyholders an with a link to the decision. Let me explain how this process works in the context of a rate filing. This past spring, Regence BlueCross BlueShield of Oregon, the largest carrier in the markets we regulate, requested a 22.1 percent rate increase. This affected about 59,000 people with individual health plans, the state s single-largest group of individual health plan policyholders. Once our intake coordinator (hired with new federal grant funding) verified the filing was complete, we posted all the company s documents on our website, notified consumers that Regence had filed for a rate increase, and launched the 30-day public comment period. At the same time, a consumer watchdog group that we contract with using federal grant funds began its analysis of the request. In addition to reviewing the filing with its own actuary, this group generated an additional 800 public comments as part of its outreach. Finally, because of the size of the proposed increase and number of policyholders affected, I scheduled the division s first public hearing in at least 20 years. We used federal grant funds to help pay the hearing costs. At the hearing, which was attended by more than 150 people, the company outlined its request, the division posed questions to the insurer, and the consumer group outlined its concerns. In this case, our actuaries questioned the company s assumptions about future medical costs and the costs of new benefits required by federal reform. Our authority to take into account an insurer s surplus and overall profitability were also key factors. Of course, we analyzed the company s medical loss ratio that is how much of the premium dollar goes to health care costs as opposed to administration and profit. In Oregon s competitive market, most or all of our large health insurers already meet the new federal requirement to spend at least 80 percent of premium dollars on medical costs. The division ultimately approved a 12.8 percent rate increase instead of the 22.1 percent requested. The division s decision to significantly reduce the rate increase was based on a desire to stem a recent history of enrollment losses in these particular plans and to spur greater stability in rates going forward. And, it was done with the knowledge that Regence is financially sound with substantial surplus, which could help offset any losses incurred from these plans. Once the decision was made, our grant-funded project coordinator drafted a brief, plain-language explanation of our decision as well as a detailed response to the consumer group s comments. We posted these online and sent an link to consumers. ACA grants to improve rate review Federal grants have proved essential for us to conduct these detailed reviews and to solicit meaningful public comments. Here are some examples of how we have spent federal grant dollars to date. Public input: When we instituted a 30-day public comment period, we initially attracted few public comments. After all, the bulk of rate filing materials remain highly technical. Those who did comment generally said they could not afford rising premiums but did not address the factors we must consider by

4 2 law in weighing rate requests. That is why we used $100,000 of our cycle 1 grant to contract with a consumer advocacy group to weigh in on behalf of consumers. This group s detailed analyses have been extremely helpful. Oregon State Public Interest Research Group (OSPIRG) keeps us on our toes and reminds us of the questions consumers want answered. In-depth review: Because Oregon has a competitive health insurance market, we review approximately 50 rate requests a year. The first round of federal grants enabled us to add an actuary to our staff, and we propose to add another one in the next grant cycle. This would double the number of our health actuaries, from two to four. This enables us to do a more in-depth analysis, to pursue any issues raised by the consumer group, and to hold more public hearings so that those who want to watch or participate can see the scrutiny we give these requests. Additionally, the grant funds pay for a market analyst who tracks insurers administrative costs by line of business and for staff to process filings, manage the grants and write the explanations of our rate decisions. These additional staff members are key to making decisions within the required 40 days from the time a filing is deemed complete. Meeting this deadline became increasingly difficult as we added steps to open up our process and as we required more information from insurers through our strengthened rate review law. Our strengthened law and additional staff have resulted in cost savings for consumers. In the year that followed the strengthening of our state s rate review law, we lowered insurance company rate requests 50 percent of the time. The size of the reduction averaged 4 percentage points for example a company would request a 16 percent rate increase and we would grant a 12 percent increase. That saves consumers just under $10 a month. Of course, that does not solve the problem of affordability, but every percentage point of a rate request matters to us. At the same time, we understand we must control health care costs to stabilize insurance rates. Communications: Although insurance company rate request documents have been public for several years, they have been difficult for consumers to find on our website. With the federal grant, we were able to create a new web page devoted to health insurance rates featuring a search engine that allows consumers to more easily find a rate filing, a seven-minute animated video explaining why health insurance costs so much, and other information about how we review health insurance rates. I have attached a screenshot of this page. On the day we issued the Regence decision, we had 500 hits on this page. We also used some money to conduct the Regence public hearing, which was instructive for a variety of reasons. The Oregonians who attended appreciated the opportunity to have their voice heard as well as watching us question the company about the request. Study on how rate review could help lower medical costs: Ultimately, the key to stabilizing health insurance costs is controlling medical costs. In Oregon, considering all insurance markets, an average of 89 cents of every premium dollar goes to pay for health care. To explore how we might be able to affect health care costs in rate review, we used $150,000 of our first-year federal grant to contract with an actuarial firm to conduct a study. The study results are due this fall, and may result in legislation. One idea we are exploring is to deny rate requests if the insurer reimburses providers for specified medical errors that should never happen. With Oregon s competitive insurance market, providers in more rural parts of the state often have an upper hand in contract negotiations. One of the goals of this study is to identify ways of leveling the playing field between insurers and providers by, for example, requiring all insurers to include certain provisions aimed at controlling costs in their contracts with providers.

5 Future grant proposals In conducting the recent public hearing in Oregon, it became clear that even with one of the most open processes in the country, consumers are unaware of the scrutiny we apply to rate requests. I m proud of our work and want Oregonians to see the rigor of our reviews, so we plan to apply for additional federal grant money to incorporate public hearings into most individual and small group rate requests. We anticipate approximately 20 public hearings a year and would expand funding to the consumer group so it could provide comments and participate. During the proposed hearings, our actuaries and a contracted consumer advocacy group would pose questions to insurance company actuaries covering issues that we might otherwise call or about. At the conclusion, we would open the meeting to public comment. We are including money in the grant for technology that would allow people to watch the hearings from their computers live or later at their convenience. By fall, we also hope to begin posting all the actuarial correspondence between the division and insurers. While this correspondence is public record, it currently is not readily accessible to the public. In addition to the public hearings, we will propose using grant money to hire another health actuary to scrutinize rate requests and participate in public hearings and a health insurance rate liaison to explain our process and to provide rate information to consumers. We also will propose a health reform/exchange coordinator to assist with federal and state reform efforts that impact our rate review process. In Oregon, the Health Insurance Exchange is governed by a public corporation, and much of the planning rests with this corporation and a separate state agency charged with coordinating and implementing state health care reform. We work closely with the Exchange and this agency and will continue to do so as the Exchange in Oregon becomes operational. For example, we will review health plans offered through the Exchange to ensure that they meet the standards established by the state Exchange and the Affordable Care Act. Finally, we will continue improvements to our web and print publications designed to better educate consumers about rate review, including the key factors that drive health insurance rates. Conclusion Federal grants to improve states review of health insurance rates are essential to educating the public and preventing excessive rates. In Oregon, the next step in rate review is finding ways to help lower medical costs so that we can truly make health insurance affordable to consumers. Thank you for this opportunity to share Oregon s experience and for the funding that enables us to strive for continued improvement. I m happy to answer your questions. 3 References Oregon s rate review web page: Example of a decision summary: Insurance Division response to OSPIRG analysis: Grant page: Oregon s administrative rules on rate review ( ):

6 4

7 5

Oregon Health Insurance Rates

Kate Brown, Secretary of State Gary Blackmer, Director, Audits Division Oregon Secretary of State 1 Oregon Health Insurance Rates Introduction We conducted preliminary work on the Oregon Insurance Division

Kate Brown, Secretary of State Gary Blackmer, Director, Audits Division Oregon Secretary of State 1 Oregon Health Insurance Rates Introduction We conducted preliminary work on the Oregon Insurance Division

Frequently Asked Questions on Rate Filing, Rate Reviews and Approval of Health Insurance Rates in Colorado

Page 1 of 5 Frequently Asked Questions on Rate Filing, Rate Reviews and Approval of Health Insurance Rates in Colorado As the cost of health care continues to rise, many insurance companies are raising

Page 1 of 5 Frequently Asked Questions on Rate Filing, Rate Reviews and Approval of Health Insurance Rates in Colorado As the cost of health care continues to rise, many insurance companies are raising

2016 Individual Health Benefit Plans - Factors Affecting The Cost

Health Insurance Rate Decisions for 2016 Individual Company Average Rate Request Requested Portland Silver 40 year old rate Rate Decision Portland Silver 40 year old rate ATRIO Health Plans 18.4% 292 18.4%

Health Insurance Rate Decisions for 2016 Individual Company Average Rate Request Requested Portland Silver 40 year old rate Rate Decision Portland Silver 40 year old rate ATRIO Health Plans 18.4% 292 18.4%

Frequently Asked Questions on Rate Filing, Rate Reviews and Approval of Health Insurance Rates in Connecticut

Frequently Asked Questions on Rate Filing, Rate Reviews and Approval of Health Insurance Rates in Connecticut As the cost of health care continues to rise, many insurance companies and health maintenance

Frequently Asked Questions on Rate Filing, Rate Reviews and Approval of Health Insurance Rates in Connecticut As the cost of health care continues to rise, many insurance companies and health maintenance

Health insurance rates are something consumers care

RESEARCH BRIEF NO. 6 June 2015 Health Insurance Rate Review: A Powerful Tool for Addressing Consumer Health Costs SUMMARY Rate review is the process by which insurance regulators review health carriers

RESEARCH BRIEF NO. 6 June 2015 Health Insurance Rate Review: A Powerful Tool for Addressing Consumer Health Costs SUMMARY Rate review is the process by which insurance regulators review health carriers

OHIO CONSUMERS FOR HEALTH COVERAGE POLICY PRIORITIES FY 2012-13. Medicaid Make Improvements to Improve Care and Lower Costs

OHIO CONSUMERS FOR HEALTH COVERAGE POLICY PRIORITIES FY 2012-13 Ohio Consumers for Health Coverage supports robust implementation of the Patient Protection and Affordable Care Act (ACA) in Ohio, making

OHIO CONSUMERS FOR HEALTH COVERAGE POLICY PRIORITIES FY 2012-13 Ohio Consumers for Health Coverage supports robust implementation of the Patient Protection and Affordable Care Act (ACA) in Ohio, making

SEPTEMBER 2012. Presented by the Illinois Department of Insurance Andrew Boron, Director

SEPTEMBER 2012 Presented by the Illinois Department of Insurance Andrew Boron, Director This Guide Will Explain How: 2 Let s Get Started the basics Before we can discuss the rate review process, it will

SEPTEMBER 2012 Presented by the Illinois Department of Insurance Andrew Boron, Director This Guide Will Explain How: 2 Let s Get Started the basics Before we can discuss the rate review process, it will

Authors Jonathan Fox, California Public Interest Research Group Education Fund Laura Etherton, U.S. Public Interest Research Group

30 November, 2012 Comments on the Aetna Life Insurance Company Proposal to Increase Aetna Managed Choice (MC) & Aetna Preferred Provider Organization (PPO) Rates, Effective 1 January 2013. State Tracking

30 November, 2012 Comments on the Aetna Life Insurance Company Proposal to Increase Aetna Managed Choice (MC) & Aetna Preferred Provider Organization (PPO) Rates, Effective 1 January 2013. State Tracking

ANNUAL REPORT Per SCR 111 of 2007

ANNUAL REPORT Per SCR 111 of 2007 BY LOUISIANA PATIENT S COMPENSATION FUND October 1, 2008 A BRIEF HISTORY OF THE LOUISIANA PATIENT S COMPENSATION FUND In the early 1970 s, a problem of crisis proportions

ANNUAL REPORT Per SCR 111 of 2007 BY LOUISIANA PATIENT S COMPENSATION FUND October 1, 2008 A BRIEF HISTORY OF THE LOUISIANA PATIENT S COMPENSATION FUND In the early 1970 s, a problem of crisis proportions

PENN TREATY NETWORK AMERICA INSURANCE COMPANY AMERICAN NETWORK INSURANCE COMPANY FREQUENTLY ASKED QUESTIONS

Revised 1/8/10 STATUS OF PTNA AND ANIC PENN TREATY NETWORK AMERICA INSURANCE COMPANY AMERICAN NETWORK INSURANCE COMPANY FREQUENTLY ASKED QUESTIONS 1. Are Penn Treaty Network America Insurance Company (PTNA)

Revised 1/8/10 STATUS OF PTNA AND ANIC PENN TREATY NETWORK AMERICA INSURANCE COMPANY AMERICAN NETWORK INSURANCE COMPANY FREQUENTLY ASKED QUESTIONS 1. Are Penn Treaty Network America Insurance Company (PTNA)

Before the House Ways and Means Committee Subcommittee on Oversight. June 24, 2015 10:00 AM

Testimony of Washington State Insurance Commissioner, Mike Kreidler Before the House Ways and Means Committee Subcommittee on Oversight June 24, 2015 10:00 AM Good morning Chairman Roskam, Ranking Member

Testimony of Washington State Insurance Commissioner, Mike Kreidler Before the House Ways and Means Committee Subcommittee on Oversight June 24, 2015 10:00 AM Good morning Chairman Roskam, Ranking Member

For The U.S. House of Representatives Committee on Energy and Commerce Subcommittee on Oversight and Investigations Hearing September 29, 2015

Written Statement For The U.S. House of Representatives Committee on Energy and Commerce Subcommittee on Oversight and Investigations Hearing September 29, 2015 By Patrick Allen, Director Department of

Written Statement For The U.S. House of Representatives Committee on Energy and Commerce Subcommittee on Oversight and Investigations Hearing September 29, 2015 By Patrick Allen, Director Department of

Act 171 Consumer Protection Report. Robin Lunge, Director of Health Care Reform Devon Green, Policy Analyst

Act 171 Consumer Protection Report Robin Lunge, Director of Health Care Reform Devon Green, Policy Analyst 1 Consumer Protection Models Connecticut-- government agency public advocacy Addresses private

Act 171 Consumer Protection Report Robin Lunge, Director of Health Care Reform Devon Green, Policy Analyst 1 Consumer Protection Models Connecticut-- government agency public advocacy Addresses private

Frequently Asked Questions about Health Insurance Rates and the Maryland Insurance Administration s Rate Review Process

MARTIN O MALLEY Governor ANTHONY G. BROWN Lt. Governor THERESE M. GOLDSMITH Commissioner KAREN STAKEM HORNIG Deputy Commissioner JOY HATCHETTE Associate Commissioner Consumer Education and Advocacy 200

MARTIN O MALLEY Governor ANTHONY G. BROWN Lt. Governor THERESE M. GOLDSMITH Commissioner KAREN STAKEM HORNIG Deputy Commissioner JOY HATCHETTE Associate Commissioner Consumer Education and Advocacy 200

PRIVATE HEALTH INSURANCE. Early Effects of Medical Loss Ratio Requirements and Rebates on Insurers and Enrollees

United States Government Accountability Office Report to the Chairman, Committee on Commerce, Science, and Transportation, U.S. Senate July 2014 PRIVATE HEALTH INSURANCE Early Effects of Medical Loss Ratio

United States Government Accountability Office Report to the Chairman, Committee on Commerce, Science, and Transportation, U.S. Senate July 2014 PRIVATE HEALTH INSURANCE Early Effects of Medical Loss Ratio

ATTACHMENT A - STATEMENT OF WORK REQUEST FOR PROPOSALS FOR INDEPENDENT BENEFIT CONSULTING, ACTUARIAL AND AUDITING SERVICES DMS-13/14-018

4050 Esplanade Way Tallahassee, Florida 32399-0950 Tel: 850.488.2786 Fax: 850. 922.6149 Rick Scott, Governor Craig J. Nichols, Agency Secretary ATTACHMENT A - STATEMENT OF WORK REQUEST FOR PROPOSALS FOR

4050 Esplanade Way Tallahassee, Florida 32399-0950 Tel: 850.488.2786 Fax: 850. 922.6149 Rick Scott, Governor Craig J. Nichols, Agency Secretary ATTACHMENT A - STATEMENT OF WORK REQUEST FOR PROPOSALS FOR

NM Health Insurance Rate Review Project Narrative

RATE REVIEW CYCLE II PHASE I A. Current Health Insurance Rate Review Capacity and Process 1. General Health Insurance Rate Regulation Information Health Insurance Products All comprehensive health insurance

RATE REVIEW CYCLE II PHASE I A. Current Health Insurance Rate Review Capacity and Process 1. General Health Insurance Rate Regulation Information Health Insurance Products All comprehensive health insurance

Report on Health Insurance Rate Review Process and Information Provided to Consumers

Report on Health Insurance Rate Review Process and Information Provided to Consumers August 17, 2011 EXECUTIVE SUMMARY Last year, pursuant to Section 1003 of the Patient Protection and Affordable Care

Report on Health Insurance Rate Review Process and Information Provided to Consumers August 17, 2011 EXECUTIVE SUMMARY Last year, pursuant to Section 1003 of the Patient Protection and Affordable Care

Section-by-Section Summary: House Small Business Health Care Bill

Section-by-Section Summary: House Small Business Health Care Bill Section 1: Studying Mandated Benefits Requires the Division of Health Care Finance and Policy (DHCFP) to periodically review all mandated

Section-by-Section Summary: House Small Business Health Care Bill Section 1: Studying Mandated Benefits Requires the Division of Health Care Finance and Policy (DHCFP) to periodically review all mandated

A Glimpse into Arizona s Health Insurance Rate Review Program July 1, 2013

A Glimpse into Arizona s Health Insurance Rate Review Program July 1, 2013 Executive Summary The purpose of A Glimpse into Arizona s Health Insurance Rate Review Program is to provide an initial analysis

A Glimpse into Arizona s Health Insurance Rate Review Program July 1, 2013 Executive Summary The purpose of A Glimpse into Arizona s Health Insurance Rate Review Program is to provide an initial analysis

HEALTH BENEFIT PLAN FILING & REVIEW COMPONENTS

Agenda Health benefit plan filing and review components Forms Plans Rates Ratemaking and rate review Company ratemaking considerations History and context of Oregon s rate review process Rate review process

Agenda Health benefit plan filing and review components Forms Plans Rates Ratemaking and rate review Company ratemaking considerations History and context of Oregon s rate review process Rate review process

GAO PRIVATE HEALTH INSURANCE. State Oversight of Premium Rates. Report to Congressional Requesters. United States Government Accountability Office

GAO United States Government Accountability Office Report to Congressional Requesters July 2011 PRIVATE HEALTH INSURANCE State Oversight of Premium Rates GAO-11-701 July 2011 PRIVATE HEALTH INSURANCE State

GAO United States Government Accountability Office Report to Congressional Requesters July 2011 PRIVATE HEALTH INSURANCE State Oversight of Premium Rates GAO-11-701 July 2011 PRIVATE HEALTH INSURANCE State

Health Insurance Rate Review: A Critical Part of Health Care Reform in Vermont. Lila Richardson Staff Attorney

Health Insurance Rate Review: A Critical Part of Health Care Reform in Vermont Lila Richardson Staff Attorney Vermont Legal Aid Office of the Health Care Advocate July 2014 Table of Contents Introduction...

Health Insurance Rate Review: A Critical Part of Health Care Reform in Vermont Lila Richardson Staff Attorney Vermont Legal Aid Office of the Health Care Advocate July 2014 Table of Contents Introduction...

August 26, 2014. Dear Chairman Harkin:

August 26, 2014 Senator Tom Harkin Chairman Committee on Health, Education, Labor and Pensions United States Senate 428 Senate Dirksen Office Building Washington, D.C. 20510 Dear Chairman Harkin: On behalf

August 26, 2014 Senator Tom Harkin Chairman Committee on Health, Education, Labor and Pensions United States Senate 428 Senate Dirksen Office Building Washington, D.C. 20510 Dear Chairman Harkin: On behalf

FOR IMMEDIATE RELEASE No. 16-004

FOR IMMEDIATE RELEASE No. 16-004 Contact: Lori Wing-Heier Director, Division of Insurance (907) 269-7900 lori.wing-heier@alaska.gov Division of Insurance and Moda Negotiate Consent Agreement February 8,

FOR IMMEDIATE RELEASE No. 16-004 Contact: Lori Wing-Heier Director, Division of Insurance (907) 269-7900 lori.wing-heier@alaska.gov Division of Insurance and Moda Negotiate Consent Agreement February 8,

PROJECT NARRATIVE. The Pennsylvania Insurance Department (PID) reviews all rate filings for individual products.

reviews all rate filings for individual products.") PROJECT NARRATIVE a) Current health insurance rate review capacity and process General health insurance rate regulation information Which health insurance products (HMO, PPO etc) are licensed and regulated

PROJECT NARRATIVE a) Current health insurance rate review capacity and process General health insurance rate regulation information Which health insurance products (HMO, PPO etc) are licensed and regulated

State Review of Insurance Rate Increases In the Individual Health Insurance Market

State Review of Insurance Rate Increases In the Individual Health Insurance Market Before and After the Affordable Care Act Rose C. Chu DHHS/ASPE/Office of Health Policy June 26, 2012 1 Individual Health

State Review of Insurance Rate Increases In the Individual Health Insurance Market Before and After the Affordable Care Act Rose C. Chu DHHS/ASPE/Office of Health Policy June 26, 2012 1 Individual Health

Table of Contents. Introduction... 1. Definition of Loss Ratio... 2. Notes on Using the Results...2. How Rates are Regulated... 4

Report of 2013 Loss Ratio Experience in the Individual and Small Employer Markets for: Insurance Companies Nonprofit Health Service Plan Corporations and Health Maintenance Organizations June, 2014 Table

Report of 2013 Loss Ratio Experience in the Individual and Small Employer Markets for: Insurance Companies Nonprofit Health Service Plan Corporations and Health Maintenance Organizations June, 2014 Table

Simple answers to health reform s complex issues facing every employer, and what you can do now to protect your business and your future.

Simple answers to health reform s complex issues facing every employer, and what you can do now to protect your business and your future. If you have any questions, please contact: Health Reform: A Guide

Simple answers to health reform s complex issues facing every employer, and what you can do now to protect your business and your future. If you have any questions, please contact: Health Reform: A Guide

Health Insurance Premiums What are you paying for? May 2013

Health Insurance Premiums What are you paying for? May 2013 Health insurance companies have been making headlines because of the skyrocketing prices consumers are paying for coverage. The national organization

Health Insurance Premiums What are you paying for? May 2013 Health insurance companies have been making headlines because of the skyrocketing prices consumers are paying for coverage. The national organization

Medicare versus Private Health Insurance: The Cost of Administration. Presented by: Mark E. Litow, FSA Consulting Actuary.

Medicare versus Private Health Insurance: The Cost of Administration Presented by: Mark E. Litow, FSA Consulting Actuary January 6, 2006 Medicare versus Private Health Insurance: The Cost of Administration

Medicare versus Private Health Insurance: The Cost of Administration Presented by: Mark E. Litow, FSA Consulting Actuary January 6, 2006 Medicare versus Private Health Insurance: The Cost of Administration

North Carolina Department of Insurance

North Carolina Department of Insurance North Carolina Actuarial Memorandum Requirements for Rate Submissions Effective 1/1/2016 and Later Small Group Market Non grandfathered Business These actuarial memorandum

North Carolina Department of Insurance North Carolina Actuarial Memorandum Requirements for Rate Submissions Effective 1/1/2016 and Later Small Group Market Non grandfathered Business These actuarial memorandum

STATEMENT BY MARGARET L. BAPTISTE PRESIDENT NATIONAL ACTIVE AND RETIRED FEDERAL EMPLOYEES ASSOCIATION

STATEMENT BY MARGARET L. BAPTISTE PRESIDENT NATIONAL ACTIVE AND RETIRED FEDERAL EMPLOYEES ASSOCIATION TO THE SPECIAL COMMITTEE ON AGING AND THE SUBCOMMITTEE ON OVERSIGHT OF GOVERNMENT MANAGEMENT, THE FEDERAL

STATEMENT BY MARGARET L. BAPTISTE PRESIDENT NATIONAL ACTIVE AND RETIRED FEDERAL EMPLOYEES ASSOCIATION TO THE SPECIAL COMMITTEE ON AGING AND THE SUBCOMMITTEE ON OVERSIGHT OF GOVERNMENT MANAGEMENT, THE FEDERAL

Monday, May 13, 2013 11:00 AM Room 123, John A. Wilson Building. Mila Kofman, J.D. Executive Director Health Benefit Exchange Authority

STATEMENT OF MILA KOFMAN, J.D. EXECUTIVE DIRECTOR OF THE HEALTH BENEFIT EXCHANGE AUTHORITY COUNCIL OF THE DISTRICT OF COLUMBIA COMMITTEE ON HEALTH COUNCILMEMBER YVETTE ALEXANDER, CHAIRPERSON PUBLIC OVERSIGHT

STATEMENT OF MILA KOFMAN, J.D. EXECUTIVE DIRECTOR OF THE HEALTH BENEFIT EXCHANGE AUTHORITY COUNCIL OF THE DISTRICT OF COLUMBIA COMMITTEE ON HEALTH COUNCILMEMBER YVETTE ALEXANDER, CHAIRPERSON PUBLIC OVERSIGHT

UNITED STATES OFFICE OF PERSONNEL MANAGEMENT

UNITED STATES OFFICE OF PERSONNEL MANAGEMENT STATEMENT OF JONATHAN FOLEY DIRECTOR, PLANNING AND POLICY ANALYSIS U.S. OFFICE OF PERSONNEL MANAGEMENT before the SUBCOMMITTEE ON FEDERAL WORKFORCE, U.S. POSTAL

UNITED STATES OFFICE OF PERSONNEL MANAGEMENT STATEMENT OF JONATHAN FOLEY DIRECTOR, PLANNING AND POLICY ANALYSIS U.S. OFFICE OF PERSONNEL MANAGEMENT before the SUBCOMMITTEE ON FEDERAL WORKFORCE, U.S. POSTAL

HHealth HEALTH INSURANCE EXCHANGE FAQs

HHealth HEALTH INSURANCE EXCHANGE FAQs Page 1 TABLE OF CONTENTS Introduction... 3 Background... 3 Health Insurance Exchange FAQs... 4 What is the Patient Protection and Affordable Care Act (PPACA)?...

HHealth HEALTH INSURANCE EXCHANGE FAQs Page 1 TABLE OF CONTENTS Introduction... 3 Background... 3 Health Insurance Exchange FAQs... 4 What is the Patient Protection and Affordable Care Act (PPACA)?...

STATE OF CONNECTICUT

STATE OF CONNECTICUT INSURANCE DEPARTMENT ConnectiCare Inc. HMO Individual Off Exchange 2016 Finding of Facts 1. The starting rates for this Individual Direct product have been developed as follows. The

STATE OF CONNECTICUT INSURANCE DEPARTMENT ConnectiCare Inc. HMO Individual Off Exchange 2016 Finding of Facts 1. The starting rates for this Individual Direct product have been developed as follows. The

TESTIMONY ON HOUSE BILL 1409 DELINQUENT PROPERTY TAX COLLECTION/SALES PRESENTED TO THE HOUSE URBAN AFFAIRS COMMITTEE

TESTIMONY ON HOUSE BILL 1409 DELINQUENT PROPERTY TAX COLLECTION/SALES PRESENTED TO THE HOUSE URBAN AFFAIRS COMMITTEE BY LISA SCHAEFER GOVERNMENT RELATIONS MANAGER November 12, 2013 Harrisburg, PA On behalf

TESTIMONY ON HOUSE BILL 1409 DELINQUENT PROPERTY TAX COLLECTION/SALES PRESENTED TO THE HOUSE URBAN AFFAIRS COMMITTEE BY LISA SCHAEFER GOVERNMENT RELATIONS MANAGER November 12, 2013 Harrisburg, PA On behalf

Alabama Department of Insurance Narrative for the Department of Health and Human Services Grants to States for Health Insurance Premium Review Cycle I

Alabama Department of Insurance Project, Page 1 Alabama Department of Insurance Narrative for the Department of Health and Human Services Grants to States for Health Insurance Premium Review Cycle I PROJECT

Alabama Department of Insurance Project, Page 1 Alabama Department of Insurance Narrative for the Department of Health and Human Services Grants to States for Health Insurance Premium Review Cycle I PROJECT

407-767-8554 Fax 407-767-9121

Florida Consumers Notice of Rights Health Insurance, F.S.C.A.I, F.S.C.A.I., FL 32832, FL 32703 Introduction The Office of the Insurance Consumer Advocate has created this guide to inform consumers of some

Florida Consumers Notice of Rights Health Insurance, F.S.C.A.I, F.S.C.A.I., FL 32832, FL 32703 Introduction The Office of the Insurance Consumer Advocate has created this guide to inform consumers of some

The New Municipal Health Insurance Law: Final FY12 Budget Proposal (H. 3535 w/ Gov s Amendments in H. 3581)

") The New Municipal Health Insurance Law: Final FY12 Budget Proposal (H. 3535 w/ Gov s Amendments in H. 3581) Section Language Effect New Definitions SECTION 51 Chapter 32B of the General Laws is hereby

The New Municipal Health Insurance Law: Final FY12 Budget Proposal (H. 3535 w/ Gov s Amendments in H. 3581) Section Language Effect New Definitions SECTION 51 Chapter 32B of the General Laws is hereby

Frequently asked questions. FP7 Financial Guide

Frequently asked questions FP7 Financial Guide Budgetary matters Eligible costs of a project What are the criteria for determining whether the costs of a project are eligible? First of all, costs must

Frequently asked questions FP7 Financial Guide Budgetary matters Eligible costs of a project What are the criteria for determining whether the costs of a project are eligible? First of all, costs must

COBRA Frequently Asked Questions (for employers)

") COBRA Frequently Asked Questions (for employers) What is COBRA? COBRA stands for the Consolidated Omnibus Budget Reconciliation Act (COBRA). COBRA is a federal statute that requires employers to provide

COBRA Frequently Asked Questions (for employers) What is COBRA? COBRA stands for the Consolidated Omnibus Budget Reconciliation Act (COBRA). COBRA is a federal statute that requires employers to provide

RESOLUTION OF THE BOARD OF TRUSTEES APPROVING SCOPES OF ASSISTANCE FOR PROCUREMENT OF STUDIES MANDATED IN MARYLAND HEALTH BENEFIT EXCHANGE ACT OF 2011

RESOLUTION OF THE BOARD OF TRUSTEES APPROVING SCOPES OF ASSISTANCE FOR PROCUREMENT OF STUDIES MANDATED IN MARYLAND HEALTH BENEFIT EXCHANGE ACT OF 2011 WHEREAS, the Maryland Health Benefit Exchange Act

RESOLUTION OF THE BOARD OF TRUSTEES APPROVING SCOPES OF ASSISTANCE FOR PROCUREMENT OF STUDIES MANDATED IN MARYLAND HEALTH BENEFIT EXCHANGE ACT OF 2011 WHEREAS, the Maryland Health Benefit Exchange Act

HEALTH INSURANCE RATES AND THE REVIEW PROCESS

FREQUENTLY ASKED QUESTIONS: HEALTH INSURANCE RATES AND THE REVIEW PROCESS Insurance Administration TABLE OF CONTENTS Who We Are...1 How We Help Consumers...1 Frequently Asked Questions and Answers: Health

FREQUENTLY ASKED QUESTIONS: HEALTH INSURANCE RATES AND THE REVIEW PROCESS Insurance Administration TABLE OF CONTENTS Who We Are...1 How We Help Consumers...1 Frequently Asked Questions and Answers: Health

Go Your Own Way: Your Guide to Choosing and Enrolling in the Aon Retiree Health Exchange

Go Your Own Way: Your Guide to Choosing and Enrolling in the Aon Retiree Health Exchange What s Changing In order to provide Medicare-eligible retirees and their Medicare-eligible dependents with better

Go Your Own Way: Your Guide to Choosing and Enrolling in the Aon Retiree Health Exchange What s Changing In order to provide Medicare-eligible retirees and their Medicare-eligible dependents with better

Governor S Proposal - Proposed Retiree Health Benefits and Taxpayers

The 2015-16 Budget: Health Benefits for Retired State Employees MAC TAYLOR LEGISLATIVE ANALYST MARCH 16, 2015 2 Legislative Analyst s Office www.lao.ca.gov 2015-16 BUDGET EXECUTIVE SUMMARY The Governor

The 2015-16 Budget: Health Benefits for Retired State Employees MAC TAYLOR LEGISLATIVE ANALYST MARCH 16, 2015 2 Legislative Analyst s Office www.lao.ca.gov 2015-16 BUDGET EXECUTIVE SUMMARY The Governor

Page 1 of 12. Subject As passed by Senate As passed by House Legislative intent; findings; purpose

Page 1 of 12 Side-by-side comparison of S.252, An act relating to financing for Green Mountain Care, as passed by House and Senate Prepared by Jennifer Carbee, Legislative Counsel, Office of Legislative

Page 1 of 12 Side-by-side comparison of S.252, An act relating to financing for Green Mountain Care, as passed by House and Senate Prepared by Jennifer Carbee, Legislative Counsel, Office of Legislative

Affordable Care Act: What The Health Care Law Means for Small Businesses

Affordable Care Act: What The Health Care Law Means for Small Businesses August 2013 Indian Country Business Summit These materials are provided for informational purposes only and are not intended as

Affordable Care Act: What The Health Care Law Means for Small Businesses August 2013 Indian Country Business Summit These materials are provided for informational purposes only and are not intended as

Health Reform s Value for Your Dollar Rule: Early Impact in Arizona

HEALTH DATA REPORT MAY 2012 Health Reform s Value for Your Dollar Rule: Early Impact in Arizona SUMMARY Beginning in 2011, the Affordable Care Act required insurers covering individuals and small businesses

HEALTH DATA REPORT MAY 2012 Health Reform s Value for Your Dollar Rule: Early Impact in Arizona SUMMARY Beginning in 2011, the Affordable Care Act required insurers covering individuals and small businesses

County of Santa Barbara Office of the Auditor-Controller County Retirement Costs: White Paper by Robert W. Geis, CPA (Through June, 30, 2006)

") County of Santa Barbara Office of the Auditor-Controller County Retirement Costs: White Paper by Robert W. Geis, CPA (Through June, 30, 2006) The County Retirement plan and underlying systems can be difficult

County of Santa Barbara Office of the Auditor-Controller County Retirement Costs: White Paper by Robert W. Geis, CPA (Through June, 30, 2006) The County Retirement plan and underlying systems can be difficult

HEALTH CARE SYSTEMS ELECTION 2012 ISSUE PAPER NO. 3 SEPTEMBER 2012. Where Are We Now?

ELECTION 2012 HEALTH CARE SYSTEMS ISSUE PAPER NO. 3 SEPTEMBER 2012 Vermont League of Cities and Towns 89 Main Street, Suite 4, Montpelier, VT 05602 (802) 229-9111 or (800) 649-7915 info@vlct.org Where

ELECTION 2012 HEALTH CARE SYSTEMS ISSUE PAPER NO. 3 SEPTEMBER 2012 Vermont League of Cities and Towns 89 Main Street, Suite 4, Montpelier, VT 05602 (802) 229-9111 or (800) 649-7915 info@vlct.org Where

Fast Forward. 2015 Employer Mandate: Pay or Play?

Fast Forward 2015 Employer Mandate: Pay or Play? Employer Mandate Beginning Jan. 1, 2015, the Affordable Care Act (ACA) will impose an employer mandate that states that grandfathered and non-grandfathered

Fast Forward 2015 Employer Mandate: Pay or Play? Employer Mandate Beginning Jan. 1, 2015, the Affordable Care Act (ACA) will impose an employer mandate that states that grandfathered and non-grandfathered

Affordable Care Act 101: What The Health Care Law Means for Small Businesses

Affordable Care Act 101: What The Health Care Law Means for Small Businesses December 2013 These materials are provided for informational purposes only and are not intended as legal or tax advice. Readers

Affordable Care Act 101: What The Health Care Law Means for Small Businesses December 2013 These materials are provided for informational purposes only and are not intended as legal or tax advice. Readers

Proposed Readoption: N.J.A.C. 11:21-11, 13, 15, 20 and 21; and 11:21 Appendix Exhibit BB, Parts 3, 4 and 5.

INSURANCE DEPARTMENT OF BANKING AND INSURANCE DIVISION OF INSURANCE Small Employer Health Benefits Program Proposed Readoption: N.J.A.C. 11:21-11, 13, 15, 20 and 21; and 11:21 Appendix Exhibit BB, Parts

INSURANCE DEPARTMENT OF BANKING AND INSURANCE DIVISION OF INSURANCE Small Employer Health Benefits Program Proposed Readoption: N.J.A.C. 11:21-11, 13, 15, 20 and 21; and 11:21 Appendix Exhibit BB, Parts

August 29, 2014. Via email to HEAA2014@help.senate.gov

Closing the gaps in opportunity and achievement, pre-k through college. August 29, 2014 Via email to HEAA2014@help.senate.gov The Honorable Tom Harkin Chairman Health, Education, Labor and Pensions Committee

Closing the gaps in opportunity and achievement, pre-k through college. August 29, 2014 Via email to HEAA2014@help.senate.gov The Honorable Tom Harkin Chairman Health, Education, Labor and Pensions Committee

DEPT: EMPLOYEE FRINGE BENEFITS UNIT NO. 1950 FUND: General - 0001

BUDGET SUMMARY 2010 Actual 2011 Budget 2012 Budget 2011/2012 Change Health Benefit Expenditures $ 132,619,138 $ 138,642,087 $ 120,566,786 $ (18,075,301) Pension Related Expenditures 67,972,949 66,872,988

BUDGET SUMMARY 2010 Actual 2011 Budget 2012 Budget 2011/2012 Change Health Benefit Expenditures $ 132,619,138 $ 138,642,087 $ 120,566,786 $ (18,075,301) Pension Related Expenditures 67,972,949 66,872,988

want this Subcommittee to know that I am always interested in challenging myself, my staff, and our partners to do even better.

Testimony of David I. Maurstad Acting Director and Federal Insurance Administrator Mitigation Division Federal Emergency Management Agency Emergency Preparedness and Response Directorate Department of

Testimony of David I. Maurstad Acting Director and Federal Insurance Administrator Mitigation Division Federal Emergency Management Agency Emergency Preparedness and Response Directorate Department of

The health insurance marketplaces, or exchanges, created

Employee Benefits Report 2121 N Glenville Drive Richardson, TX 75082 866.881.2255 www.mgmbenefits.com Health Insurance November 2013 Volume 11 Number 11 Private Exchanges: An Option Worth Exploring An

Employee Benefits Report 2121 N Glenville Drive Richardson, TX 75082 866.881.2255 www.mgmbenefits.com Health Insurance November 2013 Volume 11 Number 11 Private Exchanges: An Option Worth Exploring An

Health insurance coverage for individuals and families

Health insurance coverage for individuals and families Health care reform is here. If it seems like information is coming at you from all directions, it probably is. But just because it s a hot topic of

Health insurance coverage for individuals and families Health care reform is here. If it seems like information is coming at you from all directions, it probably is. But just because it s a hot topic of

MASSACHUSETTS UNDER THE AFFORDABLE CARE ACT: EMPLOYER-RELATED ISSUES AND POLICY OPTIONS

MASSACHUSETTS UNDER THE AFFORDABLE CARE ACT: EMPLOYER-RELATED ISSUES AND POLICY OPTIONS JULY 2012 Fredric Blavin, Linda J. Blumberg, Matthew Buettgens, and Jeremy Roth of the Urban Institute ABOUT THE

MASSACHUSETTS UNDER THE AFFORDABLE CARE ACT: EMPLOYER-RELATED ISSUES AND POLICY OPTIONS JULY 2012 Fredric Blavin, Linda J. Blumberg, Matthew Buettgens, and Jeremy Roth of the Urban Institute ABOUT THE

STATE OF RHODE ISLAND AND PROVIDENCE PLANTATIONS HealthSource RI Rhode Island Health Benefits Exchange Phone# 401-415-8100

Governor Chafee: (HSRI), which was created by Executive Order and without an underlying, specific statute, is in a unique situation as it develops its budget for FY2016. In this letter of transmittal I

Governor Chafee: (HSRI), which was created by Executive Order and without an underlying, specific statute, is in a unique situation as it develops its budget for FY2016. In this letter of transmittal I

Things New Yorkers Should Know About. Public Retirement Benefits in New York State

Things New Yorkers Should Know About Public Retirement Benefits in New York State October 2010 INTRODUCTION Citizens Budget Commission One Penn Plaza, Suite 640 New York, NY 10119 411 State Street Albany,

Things New Yorkers Should Know About Public Retirement Benefits in New York State October 2010 INTRODUCTION Citizens Budget Commission One Penn Plaza, Suite 640 New York, NY 10119 411 State Street Albany,

Enhancements to the Massachusetts Health Insurance Rate Review Practice: Promoting Transparency and Protecting Massachusetts Consumers

Page 1 of 9 Enhancements to the Massachusetts Health Insurance Rate Review Practice: Promoting Transparency and Protecting Massachusetts Consumers a) Current Health Insurance Rate Review Capacity and Process

Page 1 of 9 Enhancements to the Massachusetts Health Insurance Rate Review Practice: Promoting Transparency and Protecting Massachusetts Consumers a) Current Health Insurance Rate Review Capacity and Process

The Story of Non-admitted Insurance in California

The Surplus Line Association Of California CA The Story of Non-admitted Insurance in California The Story of Non-Admitted Insurance in California It is vital an innovative and imaginative insurance marketplace

The Surplus Line Association Of California CA The Story of Non-admitted Insurance in California The Story of Non-Admitted Insurance in California It is vital an innovative and imaginative insurance marketplace

WORKERS COMPENSATION GLOSSARY

WORKERS COMPENSATION GLOSSARY ACCIDENT An unplanned and unexpected event which occurs suddenly and at a definite place resulting in injury and/or damage. ACCIDENT FREQUENCY The rate of the occurrence of

WORKERS COMPENSATION GLOSSARY ACCIDENT An unplanned and unexpected event which occurs suddenly and at a definite place resulting in injury and/or damage. ACCIDENT FREQUENCY The rate of the occurrence of

LOS ANGELES COUNTY EMPLOYEES RETIREMENT ASSOCIATION REQUEST FOR PROPOSAL JULY 10, 2014

LOS ANGELES COUNTY EMPLOYEES RETIREMENT ASSOCIATION REQUEST FOR PROPOSAL JULY 10, 2014 SEEKING: EXECUTIVE SEARCH SERVICES FOR PRINCIPAL INVESTMENT OFFICER POSITION Contact Person: John Nogales Director

LOS ANGELES COUNTY EMPLOYEES RETIREMENT ASSOCIATION REQUEST FOR PROPOSAL JULY 10, 2014 SEEKING: EXECUTIVE SEARCH SERVICES FOR PRINCIPAL INVESTMENT OFFICER POSITION Contact Person: John Nogales Director

pcodr Performance Metrics Report

pcodr Performance Metrics Report April 2015 TABLE OF CONTENTS EXECUTIVE SUMMARY...ii Operations...ii Transparency...ii Stakeholder Engagement... iii Looking Ahead... iii 1. INTRODUCTION... 1 2. PERFORMANCE

pcodr Performance Metrics Report April 2015 TABLE OF CONTENTS EXECUTIVE SUMMARY...ii Operations...ii Transparency...ii Stakeholder Engagement... iii Looking Ahead... iii 1. INTRODUCTION... 1 2. PERFORMANCE

ASO. BlueCross BlueShield of Oregon HOW AN ADMINISTRATIVE SERVICES ONLY (ASO) PLAN CAN WORK FOR YOU AN INTRODUCTION FOR GROUPS OF 51-99 MT HOOD

PLAN CAN WORK FOR YOU AN INTRODUCTION FOR GROUPS OF 51-99 MT HOOD") BlueCross BlueShield of Oregon ASO HOW AN ADMINISTRATIVE SERVICES ONLY (ASO) PLAN CAN WORK FOR YOU AN INTRODUCTION FOR GROUPS OF 51-99 Regence BlueCross BlueShield of Oregon is an Independent Licensee

BlueCross BlueShield of Oregon ASO HOW AN ADMINISTRATIVE SERVICES ONLY (ASO) PLAN CAN WORK FOR YOU AN INTRODUCTION FOR GROUPS OF 51-99 Regence BlueCross BlueShield of Oregon is an Independent Licensee

PATIENT PROTECTION AND AFFORDABLE CARE ACT. Status of Federal and State Efforts to Establish Health Insurance Exchanges for Small Businesses

United States Government Accountability Office Report to the Chairman, Committee on Small Business, House of Representatives June 2013 PATIENT PROTECTION AND AFFORDABLE CARE ACT Status of Federal and State

United States Government Accountability Office Report to the Chairman, Committee on Small Business, House of Representatives June 2013 PATIENT PROTECTION AND AFFORDABLE CARE ACT Status of Federal and State

Employer s guide to health care reform requirements

Employer s guide to health care reform requirements June 2015 edition As the Affordable Care Act (ACA) continues to be implemented, you ll need to remain aware of the policies and provisions that affect

Employer s guide to health care reform requirements June 2015 edition As the Affordable Care Act (ACA) continues to be implemented, you ll need to remain aware of the policies and provisions that affect

The Honorable Kathleen Sebelius Department of Health and Human Services 200 Independence Avenue, S.W. Washington, D.C. 20201.

The Honorable Kathleen Sebelius Department of Health and Human Services 200 Independence Avenue, S.W. Washington, D.C. 20201 October 12, 2011 Submitted Via Electronic Mail: MLRAdjustments@hhs.gov Indiana

The Honorable Kathleen Sebelius Department of Health and Human Services 200 Independence Avenue, S.W. Washington, D.C. 20201 October 12, 2011 Submitted Via Electronic Mail: MLRAdjustments@hhs.gov Indiana

Health care reform for large businesses

FOR PRODUCERS AND EMPLOYERS Health care reform for large businesses A guide to what you need to know now DECEMBER 2013 CONTENTS 2 Introduction Since 2010 when the Affordable Care Act (ACA) was signed into

FOR PRODUCERS AND EMPLOYERS Health care reform for large businesses A guide to what you need to know now DECEMBER 2013 CONTENTS 2 Introduction Since 2010 when the Affordable Care Act (ACA) was signed into

Public Act No. 14-10

Public Act No. 14-10 AN ACT CONCERNING LONG-TERM CARE INSURANCE PREMIUM RATE INCREASES. Be it enacted by the Senate and House of Representatives in General Assembly convened: Section 1. Subsections (a)

Public Act No. 14-10 AN ACT CONCERNING LONG-TERM CARE INSURANCE PREMIUM RATE INCREASES. Be it enacted by the Senate and House of Representatives in General Assembly convened: Section 1. Subsections (a)

Health Reform s Value for Your Dollar Rule: Early Impact in Florida

HEALTH DATA REPORT MAY 2012 Health Reform s Value for Your Dollar Rule: Early Impact in Florida SUMMARY Beginning in 2011, the Affordable Care Act required insurers covering small businesses and individuals

HEALTH DATA REPORT MAY 2012 Health Reform s Value for Your Dollar Rule: Early Impact in Florida SUMMARY Beginning in 2011, the Affordable Care Act required insurers covering small businesses and individuals

Employer s Guide To Health Care Reform

Employer s Guide To Health Care Reform A nonprofit independent licensee of the Blue Cross Blue Shield Association National strength. Local focus. Individual care. SM As part of our commitment to being

Employer s Guide To Health Care Reform A nonprofit independent licensee of the Blue Cross Blue Shield Association National strength. Local focus. Individual care. SM As part of our commitment to being

BARACK OBAMA S PLAN FOR A HEALTHY AMERICA:

BARACK OBAMA S PLAN FOR A HEALTHY AMERICA: Lowering health care costs and ensuring affordable, high-quality health care for all The U.S. spends $2 trillion on health care every year, and offers the best

BARACK OBAMA S PLAN FOR A HEALTHY AMERICA: Lowering health care costs and ensuring affordable, high-quality health care for all The U.S. spends $2 trillion on health care every year, and offers the best

Supreme Court upholds the Affordable Care Act in its entirety:

Supreme Court upholds the Affordable Care Act in its entirety: What does this mean for Seniors? The Supreme Court s decision to uphold the Affordable Care Act (ACA) in its entirety is a huge victory for

Supreme Court upholds the Affordable Care Act in its entirety: What does this mean for Seniors? The Supreme Court s decision to uphold the Affordable Care Act (ACA) in its entirety is a huge victory for

City of Boston PEC Meeting February 18, 2015

City of Boston PEC Meeting February 18, 2015 Medical/Rx Rates Effective July 1, 2015 Standard HMO Plan Harvard Pilgrim Health Care (HPHC) PPO Plan Blue Cross Blue Shield of Massachusetts (BCBSMA) Value

City of Boston PEC Meeting February 18, 2015 Medical/Rx Rates Effective July 1, 2015 Standard HMO Plan Harvard Pilgrim Health Care (HPHC) PPO Plan Blue Cross Blue Shield of Massachusetts (BCBSMA) Value

It s the month for shamrocks and a glimpse of spring. We continue to stay busy as you ll see in this latest news from VIM.

THE VIM BULLETIN News from the Clinic MARCH, 2014 It s the month for shamrocks and a glimpse of spring. We continue to stay busy as you ll see in this latest news from VIM. UPDATE ON ACA ENROLLMENT PROGRESS

THE VIM BULLETIN News from the Clinic MARCH, 2014 It s the month for shamrocks and a glimpse of spring. We continue to stay busy as you ll see in this latest news from VIM. UPDATE ON ACA ENROLLMENT PROGRESS

May 4, 2006. Good morning. Chairman Herger, Ranking Member McDermott and

TESTIMONY OF MASON BISHOP DEPUTY ASSISTANT SECRETARY EMPLOYMENT AND TRAINING ADMINISTRATION U.S. DEPARTMENT OF LABOR BEFORE THE HOUSE COMMITTEE ON WAYS AND MEANS SUBCOMMITTEE ON HUMAN RESOURCES May 4,

TESTIMONY OF MASON BISHOP DEPUTY ASSISTANT SECRETARY EMPLOYMENT AND TRAINING ADMINISTRATION U.S. DEPARTMENT OF LABOR BEFORE THE HOUSE COMMITTEE ON WAYS AND MEANS SUBCOMMITTEE ON HUMAN RESOURCES May 4,

Request for Qualifications (RFQ) Insurance Broker/Consultation Services City of Shenandoah Employee Benefits Plan

Insurance Broker/Consultation Services City of Shenandoah Employee Benefits Plan") Request for Qualifications (RFQ) Insurance Broker/Consultation Services City of Shenandoah Employee Benefits Plan I. GENERAL INFORMATION/PUBLISHING The City of Shenandoah, Texas (CITY) is accepting Qualification

Request for Qualifications (RFQ) Insurance Broker/Consultation Services City of Shenandoah Employee Benefits Plan I. GENERAL INFORMATION/PUBLISHING The City of Shenandoah, Texas (CITY) is accepting Qualification

Pharmaceutical Distribution Supply Chain Pilot Projects; Request for Information Docket No. FDA-2016-N-1114

May 16, 2016 [Submitted electronically to http://www.regulations.gov] Division of Dockets Management (HFA-305) Food and Drug Administration 5630 Fishers Lane, Rm. 1061 Rockville MD, 20852 RE: Pharmaceutical

May 16, 2016 [Submitted electronically to http://www.regulations.gov] Division of Dockets Management (HFA-305) Food and Drug Administration 5630 Fishers Lane, Rm. 1061 Rockville MD, 20852 RE: Pharmaceutical

June 23, 2014 BY CERTIFIED MAIL. Dr. Wilma Mishoe, Interim President Wilberforce University 1055 North Bickett Road Wilberforce, OH 45384-1001

June 23, 2014 BY CERTIFIED MAIL Dr. Wilma Mishoe, Interim President Wilberforce University 1055 North Bickett Road Wilberforce, OH 45384-1001 Dear President Mishoe: This letter is formal notification of

June 23, 2014 BY CERTIFIED MAIL Dr. Wilma Mishoe, Interim President Wilberforce University 1055 North Bickett Road Wilberforce, OH 45384-1001 Dear President Mishoe: This letter is formal notification of

Protect your ministry with GuideStone s self-funded health plans

Protect your ministry with GuideStone s self-funded health plans Ministries are searching for ways to comply with health care reform and provide quality health coverage to their staff without breaking

Protect your ministry with GuideStone s self-funded health plans Ministries are searching for ways to comply with health care reform and provide quality health coverage to their staff without breaking

COMPLIANCE AUDIT. Lansdowne Borough Police Pension Plan Delaware County, Pennsylvania For the Period January 1, 2012 to December 31, 2014

COMPLIANCE AUDIT Lansdowne Borough Police Pension Plan Delaware County, Pennsylvania For the Period January 1, 2012 to December 31, 2014 July 2015 The Honorable Mayor and Borough Council Lansdowne Borough

COMPLIANCE AUDIT Lansdowne Borough Police Pension Plan Delaware County, Pennsylvania For the Period January 1, 2012 to December 31, 2014 July 2015 The Honorable Mayor and Borough Council Lansdowne Borough

MEMORANDUM. Members of the Senate Commerce Committee

Philip Kirschner President Melanie Willoughby Senior Vice President Frank Robinson First Vice President Grassroots & Government Affairs To: From: MEMORANDUM Members of the Senate Commerce Committee Christine

Philip Kirschner President Melanie Willoughby Senior Vice President Frank Robinson First Vice President Grassroots & Government Affairs To: From: MEMORANDUM Members of the Senate Commerce Committee Christine

ITN for Group Term Life Insurance ITN No.: DMS 14/15-025 Response to Vendor Questions

1 1.6 7 Timeline of Events- Why does contract start date say 3/20/15 in the timeline and not 1/1/16? 2 1.6 7 Timeline of Events- Can an extension be provided due to the amount of missing information and

1 1.6 7 Timeline of Events- Why does contract start date say 3/20/15 in the timeline and not 1/1/16? 2 1.6 7 Timeline of Events- Can an extension be provided due to the amount of missing information and

GAO HEALTH INSURANCE. Report to the Committee on Health, Education, Labor, and Pensions, U.S. Senate. United States Government Accountability Office

GAO United States Government Accountability Office Report to the Committee on Health, Education, Labor, and Pensions, U.S. Senate March 2008 HEALTH INSURANCE Most College Students Are Covered through Employer-Sponsored

GAO United States Government Accountability Office Report to the Committee on Health, Education, Labor, and Pensions, U.S. Senate March 2008 HEALTH INSURANCE Most College Students Are Covered through Employer-Sponsored

July 2, 2009. Honorable Edward M. Kennedy Chairman Committee on Health, Education, Labor, and Pensions United States Senate Washington, DC 20510

CONGRESSIONAL BUDGET OFFICE U.S. Congress Washington, DC 20515 Douglas W. Elmendorf, Director July 2, 2009 Honorable Edward M. Kennedy Chairman Committee on Health, Education, Labor, and Pensions United

CONGRESSIONAL BUDGET OFFICE U.S. Congress Washington, DC 20515 Douglas W. Elmendorf, Director July 2, 2009 Honorable Edward M. Kennedy Chairman Committee on Health, Education, Labor, and Pensions United

Affordable Care Act 101: What The Health Care Law Means for Small Businesses

Affordable Care Act 101: What The Health Care Law Means for Small Businesses December 2013 These materials are provided for informational purposes only and are not intended as legal or tax advice. Readers

Affordable Care Act 101: What The Health Care Law Means for Small Businesses December 2013 These materials are provided for informational purposes only and are not intended as legal or tax advice. Readers

Analysis Item 65: Department of Revenue Property Valuation System

Analysis Item 65: Department of Revenue Property Valuation System Analysts: John Borden and Sean McSpaden Request: Allocate $1.5 million from the Emergency Fund for an increase to the Property Valuation

Analysis Item 65: Department of Revenue Property Valuation System Analysts: John Borden and Sean McSpaden Request: Allocate $1.5 million from the Emergency Fund for an increase to the Property Valuation

An Employer s Guide to Group Health Continuation Coverage Under COBRA

An Employer s Guide to Group Health Continuation Coverage Under COBRA The Consolidated Omnibus Budget Reconciliation Act U.S. Department of Labor Employee Benefits Security Administration This publication

An Employer s Guide to Group Health Continuation Coverage Under COBRA The Consolidated Omnibus Budget Reconciliation Act U.S. Department of Labor Employee Benefits Security Administration This publication

Statement of Colleen M. Kelley National President National Treasury Employees Union H.R. 4735

Statement of Colleen M. Kelley National President National Treasury Employees Union On H.R. 4735 Presented to House Committee on Oversight and Government Reform Subcommittee on Federal Workforce, Postal

Statement of Colleen M. Kelley National President National Treasury Employees Union On H.R. 4735 Presented to House Committee on Oversight and Government Reform Subcommittee on Federal Workforce, Postal

Structured Settlement Program

Structured Settlement Program 2014 Annual Report to the Legislature January 2015 Document number: LR 14-01 Available online at: Lni.wa.gov/LegReports Table of Contents Executive Summary... 1 Introduction...

Structured Settlement Program 2014 Annual Report to the Legislature January 2015 Document number: LR 14-01 Available online at: Lni.wa.gov/LegReports Table of Contents Executive Summary... 1 Introduction...

The Impact on Business

The Impact on Business Affordable Care Act Reform addresses access to coverage not healthcare cost or population health ACA passed in 2010. The Supreme Court upheld ACA in 2012 and President Obama was

The Impact on Business Affordable Care Act Reform addresses access to coverage not healthcare cost or population health ACA passed in 2010. The Supreme Court upheld ACA in 2012 and President Obama was

Health Insurance Marketplace. vhealth insurance exchanges. What to expect in 2014. What to expect in 2014

vhealth insurance exchanges Health Insurance Marketplace What to expect in 2014 What to expect in 2014 The basics of exchanges As part of the Affordable Care Act (ACA or health care reform law), starting

vhealth insurance exchanges Health Insurance Marketplace What to expect in 2014 What to expect in 2014 The basics of exchanges As part of the Affordable Care Act (ACA or health care reform law), starting

52ND LEGISLATURE - STATE OF NEW MEXICO - FIRST SESSION, 2015

SENATE JUDICIARY COMMITTEE SUBSTITUTE FOR SENATE BILL ND LEGISLATURE - STATE OF NEW MEXICO - FIRST SESSION, AN ACT RELATING TO MANAGED HEALTH CARE; AMENDING AND ENACTING SECTIONS OF THE NEW MEXICO INSURANCE

SENATE JUDICIARY COMMITTEE SUBSTITUTE FOR SENATE BILL ND LEGISLATURE - STATE OF NEW MEXICO - FIRST SESSION, AN ACT RELATING TO MANAGED HEALTH CARE; AMENDING AND ENACTING SECTIONS OF THE NEW MEXICO INSURANCE

MISSION OF THE FARM CREDIT ADMINISTRATION

Testimony of the Honorable Kenneth A. Spearman Chairman and Chief Executive Officer Farm Credit Administration Before the Subcommittee on Agriculture, Rural Development, Food and Drug Administration, and

Testimony of the Honorable Kenneth A. Spearman Chairman and Chief Executive Officer Farm Credit Administration Before the Subcommittee on Agriculture, Rural Development, Food and Drug Administration, and

ARTICLE 20:06 INSURANCE. 20:06:06 Credit life, health, and unemployment insurance.

ARTICLE 20:06 INSURANCE Chapter 20:06:01 Administration. 20:06:02 Individual risk premium, Repealed. 20:06:03 Domestic stock insurers. 20:06:04 Insider trading of equity securities. 20:06:05 Voting proxies

ARTICLE 20:06 INSURANCE Chapter 20:06:01 Administration. 20:06:02 Individual risk premium, Repealed. 20:06:03 Domestic stock insurers. 20:06:04 Insider trading of equity securities. 20:06:05 Voting proxies